Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Statement Nos. 333-163504 and

333-163504-01 through 333-163504-09

PROSPECTUS

Solo Cup Company

Solo Cup Operating Corporation

OFFER TO EXCHANGE

$300,000,000 aggregate principal amount of 10.5% Senior Secured Notes due 2013 (CUSIP No. 83427B AB2)

that have been registered under the Securities Act of 1933

for

$300,000,000 aggregate principal amount of outstanding

10.5% Senior Secured Notes due 2013 (CUSIP Nos. 83427B AA4 and U83440 AA2)

The exchange offer will expire at 5:00 p.m., Eastern time, on January 27, 2010, unless we extend the exchange offer.

We refer to the registered notes offered in the exchange offer as the exchange notes and to the outstanding 10.5% senior secured notes due 2013, which were issued on July 2, 2009, as the original notes. We refer to the original notes and the exchange notes collectively as the notes. We refer to Solo Cup Company and Solo Cup Operating Corporation, the issuers of the notes, as the issuers.

The issuers will exchange a like aggregate principal amount of the exchange notes for all outstanding original notes that are validly tendered pursuant to the exchange offer and not properly withdrawn prior to the expiration of the exchange offer. You may withdraw tenders of original notes at any time prior to the expiration of the exchange offer.

The terms of the exchange notes are substantially identical to the terms of the original notes, except that the exchange notes will have been registered under the Securities Act of 1933, the exchange notes will not bear restrictive legends restricting their transfer under the Securities Act of 1933 and holders of exchange notes will not be entitled to registration rights and special interest provisions that apply to the original notes under the registration rights agreement entered into in connection with the issuance of the original notes.

The obligations of the issuers under the original notes are, and their obligations under the exchange notes will be, fully and unconditionally guaranteed, jointly and severally, on a senior secured basis by Solo Cup Company’s domestic subsidiaries other than Solo Cup Operating Corporation (a co-issuer of the notes), an inactive receivables subsidiary and specified immaterial subsidiaries.

The exchange of the original notes for exchange notes will not be a taxable transaction for United States federal income tax purposes, but you should see the discussion under the heading “Material U.S. Federal Income Tax Considerations” for more information.

We will not receive any cash proceeds from the exchange offer.

The issuers issued the original notes in a transaction not requiring registration under the Securities Act of 1933 and, as a result, transfer of the original notes is restricted. We are making the exchange offer to satisfy your registration rights as a holder of original notes.

The exchange notes are not listed on any national securities exchange.

See “Risk Factors” beginning on page 14 to read about risks you should consider prior to tendering your original notes for exchange.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act of 1933 in connection with any resale of such exchange notes. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for original notes where such original notes were acquired as a result of market-making activities or other trading activities.

The date of this prospectus is December 23, 2009.

Table of Contents

| Page | ||

| 1 | ||

| 14 | ||

| 30 | ||

| 31 | ||

| 31 | ||

| 32 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 35 | |

| 57 | ||

| 63 | ||

| 66 | ||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 74 | |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | 76 | |

| 79 | ||

| 83 | ||

| 92 | ||

| 170 | ||

| 171 | ||

| 172 | ||

| 172 | ||

| 172 | ||

| F-1 |

You should rely only upon the information provided in this prospectus. We have not authorized anyone to provide you with different information. The information contained in this prospectus is current only as of its date. The distribution of this prospectus and the offer and sale of the exchange notes and related guarantees may be restricted by law in certain jurisdictions. Persons who come into possession of this prospectus or any of the exchange notes must inform themselves about and observe any such restrictions. You must comply with all applicable laws and regulations in force in any jurisdiction in which you purchase, offer or sell the exchange notes or possess or distribute this prospectus and, in connection with any purchase, offer or sale by you of the exchange notes, must obtain any consent, approval or permission required under the laws and regulations in force in any jurisdiction to which you are subject or in which you make such purchase, offer or sale.

i

Table of Contents

The following summary is qualified in its entirety by the more detailed information, including the risk factors described under “Risk Factors” and the financial statements and related notes, included elsewhere in this prospectus. Because this is a summary, it may not contain all the information that may be important to you. You should read the entire prospectus, including our consolidated financial statements and related notes, before tendering your original notes for exchange. In this prospectus, unless the context otherwise requires:

| • | “Solo” refers only to Solo Cup Company, a Delaware corporation, and not to any of its subsidiaries; |

| • | “SCOC” refers to Solo Cup Operating Corporation and not to any of its subsidiaries; |

| • | “issuers” refers to Solo and SCOC, the issuers of the notes; and |

| • | “we,” “us” and “our” refer to Solo and all of its subsidiaries, including SCOC. |

Our Company

We are a leading producer and marketer of single-use products used to serve food and beverages in quick service restaurants, or QSRs, other foodservice settings and homes. We distribute our products globally and have served our industry for more than 70 years. We manufacture and supply a broad portfolio of single-use products, including cups, lids, food containers, plates, bowls, portion cups, cutlery and straws, with products available in plastic, paper, foam, post-consumer recycled content and renewable resources.

We currently operate 15 manufacturing facilities and 13 distribution centers, some of which are combined in one location, in North America, the United Kingdom and Panama. For Fiscal Year 2008, we generated approximately $1.8 billion of net sales and a loss from continuing operations of approximately $12.2 million. Sales in the United States accounted for approximately 82% of our net sales for Fiscal Year 2008.

We serve two primary customer groups: (1) foodservice distributors and operators, referred to collectively in this prospectus as foodservice customers, and (2) retailers of consumer products, referred to in this prospectus as consumer customers. Approximately 83% of our net sales for Fiscal Year 2008 were to foodservice customers. Sales to consumer customers accounted for approximately 17% of our net sales for Fiscal Year 2008.

Refinancing Transactions

On July 2, 2009, we undertook a series of transactions to refinance some of our then-existing debt. These transactions, which we refer to collectively as the refinancing transactions, consisted of

| • | the offer and sale of the original notes; |

| • | the entry into a loan agreement, dated July 2, 2009, providing for revolving credit of up to $200.0 million, subject to borrowing base limitations and other specified terms and conditions, which we refer to as our asset-based revolving credit facility; and |

| • | the use of the approximately $293.8 million of gross proceeds from the sale of the original notes, together with approximately $28.3 million of borrowings under our asset-based revolving credit facility, to repay all amounts outstanding, consisting of $300.9 million of borrowings and accrued interest, under our credit agreement, dated February 27, 2004, as amended, which we refer to as the first lien credit agreement; to pay $17.3 million of fees, expenses and other costs relating to the offer and sale of the original notes, the entry into our asset-based revolving credit facility and the repayment of all amounts outstanding under the first lien credit agreement; and to provide $3.9 million for operating needs. |

1

Table of Contents

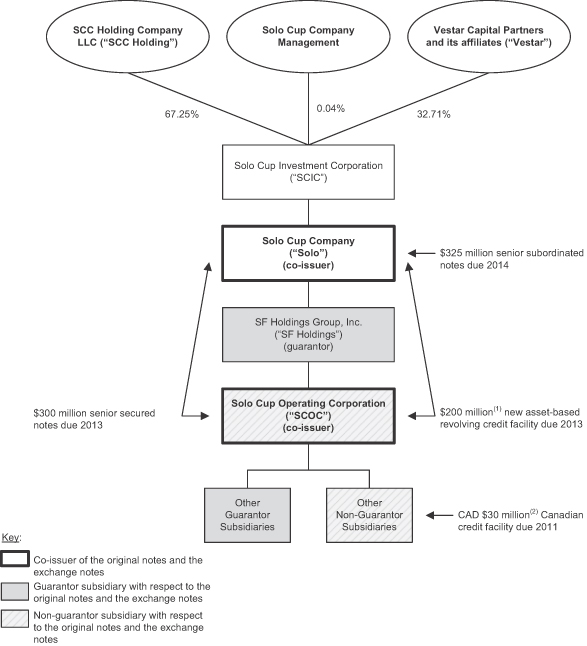

Our Structure

The following chart illustrates our corporate structure and certain of our indebtedness as of September 27, 2009:

| (1) | Our asset-based revolving credit facility provides for up to $200.0 million of borrowings, subject to borrowing base limitations and other specified terms and conditions. See “Description of Certain Other Indebtedness — Asset-Based Revolving Credit Facility.” As of September 27, 2009, we had $12.4 million of outstanding letters of credit and approximately $109.9 million available for borrowing under our asset-based revolving credit facility, after giving effect to borrowing base limitations. |

2

Table of Contents

| (2) | The commitment amount for the Canadian revolving credit facility at September 27, 2009 was CAD $16.5 million (approximately $15.1 million; however, unused capacity was CAD $11.9 million (approximately $11.0 million) due to borrowing base limitations. See “Description of Certain Other Indebtedness — Canadian Credit Facility.” |

Directors appointed by Vestar Capital Partners IV, L.P. and its affiliates, or Vestar, constitute a majority of the board of directors of each of Solo and Solo Cup Investment Corporation, or SCIC, the 100% owner of Solo. Robert L. Hulseman, Chairman Emeritus of Solo’s board of directors, holds 50% of the voting membership interests of SCC Holding Company LLC, or SCC Holding. His brother, John F. Hulseman, holds the other 50% of the voting membership interests of SCC Holding. See “Risk Factors — Risks Related to Our Business — We are controlled by the stockholders of SCIC, the interests of which may conflict with the interests of holders of the notes” and “Certain Relationships and Related Transactions and Director Independence.”

Vestar Capital Partners

Vestar is a leading international private equity firm that specializes in management buyouts, recapitalizations and growth capital investments. Headquartered in New York, Vestar has offices or affiliates in Denver, Boston, Paris, Milan and Munich. Vestar currently manages funds with committed capital totaling approximately $7 billion and has more than 90 employees.

Since the firm’s founding in 1988, Vestar has completed 65 investments in companies with a total value of over $30 billion. These companies have varied in size and span a broad range of industries. In addition, Vestar’s principals have had meaningful experience in the consumer products industries. Notable and recent investments include, in addition to Solo, AZ Electronic Materials, CCS Corporation, Cesare Fiorucci S.p.A., Consolidated Container Company LLC, MediMedia USA, National Mentor Holdings, Inc., PARIS RE Holdings Limited, Press Ganey Associates, Inc., Radiation Therapy Services, Inc., Seves S.p.A., St. John Knits, Inc. and The Sun Products Corporation.

For information with respect to our relationship with Vestar, see “— Our Structure,” “Security Ownership of Certain Beneficial Owners and Management” and “Certain Relationships and Related Transactions and Director Independence.”

Address and Telephone Number

Our principal executive offices are located at 150 S. Saunders Road, Suite 150, Lake Forest, Illinois 60045. Our telephone number is (847) 444-5000. Our website address is http://www.solocup.com. Information contained on our website, or on any other website referred to in this prospectus, does not constitute part of this prospectus and is not incorporated by reference in this prospectus.

3

Table of Contents

The Exchange Offer

On July 2, 2009, the issuers completed the private placement of $300,000,000 aggregate principal amount of 10.5% senior secured notes due 2013. As part of that offering, the issuers and the subsidiaries of Solo that guaranteed the original notes entered into a registration rights agreement with the initial purchasers of the original notes, dated as of July 2, 2009, in which they agreed to, among other things, deliver this prospectus to you and to conduct an exchange offer for the original notes. Below is a summary of the exchange offer.

Original Notes | 10.5% Senior Secured Notes due 2013, which the issuers issued on July 2, 2009. |

Exchange Notes | 10.5% Senior Secured Notes due 2013, which have been registered under the Securities Act of 1933, as amended, or the Securities Act. The terms of the exchange notes and those of the original notes are substantially identical, except that the exchange notes will have been registered under the Securities Act, the exchange notes will not bear restrictive legends restricting their transfer under the Securities Act and holders of exchange notes will not be entitled to registration rights and special interest provisions that apply to the original notes under the registration rights agreement. |

Exchange Offer | The issuers are offering to issue up to $300,000,000 aggregate principal amount of exchange notes in exchange for a like principal amount of original notes to satisfy their obligations under the registration rights agreement that the issuers and the guarantors entered into when the original notes were issued. |

Expiration Time | The exchange offer will expire at 5:00 p.m., Eastern time, on January 27, 2010, which is the twenty-first business day of the offering period, unless we extend the exchange offer. The term “expiration time” means 5:00 p.m., Eastern time, on January 27, 2010, except that, if we have extended the period of time for which the exchange offer is open, that term will mean the latest time and date to which we have extended the exchange offer. In the event of any material change in the exchange offer, we will extend the offering period if necessary so that at least five business days remain in the offering period following notice of the material change. |

Withdrawal Rights | Tenders of original notes may be withdrawn at any time at or prior to the expiration time. |

Procedures for Tendering Original Notes | A tendering holder must, at or prior to the expiration time: |

| • | transmit a properly completed and duly executed letter of transmittal, including all other documents required by the letter of transmittal, to the exchange agent at the address listed in this prospectus; or |

| • | if original notes are tendered in accordance with the book-entry procedures described in this prospectus, the tendering holder must |

4

Table of Contents

transmit an agent’s message to the exchange agent at the address listed in this prospectus. See “The Exchange Offer — Procedures for Tendering.” |

By tendering your original notes, you represent that:

| • | you are not an affiliate, as defined in Rule 405 under the Securities Act, of either of the issuers or any guarantor; |

| • | you are not engaged in, and do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes; |

| • | you are acquiring the exchange notes in your ordinary course of business; |

| • | if you are a broker-dealer that holds original notes that were acquired for your own account as a result of market-making activities or other trading activities (other than original notes acquired from the issuers or any of their affiliates), you will deliver a prospectus meeting the requirements of the Securities Act in connection with any resales of the exchange notes received by you in the exchange offer; |

| • | if you are a broker-dealer, that you did not purchase the original notes from either of the issuers or any of their affiliates; and |

| • | you are not acting on behalf of any person who could not truthfully and completely make the above representations. |

Special Procedures for Beneficial Owners | If you are a beneficial owner of original notes that are registered in the name of your broker, dealer, commercial bank, trust company or other nominee, and you wish to tender in the exchange offer, you should promptly contact the person in whose name your original notes are registered and instruct that person to tender on your behalf. See “The Exchange Offer — Procedures for Tendering.” |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions. If we materially change the terms of the exchange offer, we will extend the offering period if necessary so that at least five business days remain in the offering period following notice of any such material change. See “The Exchange Offer — Conditions to the Exchange Offer” for more information regarding conditions to the exchange offer. |

Accrued Interest on the Exchange Notes and Original Notes | The exchange notes will accrue interest from the most recent date to which interest has been paid on the original notes or, if no such interest has been paid, from July 2, 2009. If your original notes are accepted for exchange, you will receive interest on the exchange notes and not on the original notes. Any original notes not tendered will remain outstanding and continue to accrue interest according to their terms. |

5

Table of Contents

Material U.S. Federal Income Tax Considerations | Your exchange of original notes for exchange notes pursuant to the exchange offer generally will not be a taxable event for U.S. federal income tax purposes. See the discussion below under the caption “Material U.S. Federal Income Tax Considerations” for more information regarding the United States federal income tax consequences to you of the exchange offer. |

Appraisal or Dissenters’ Rights | You do not have any appraisal or dissenters’ rights in connection with the exchange offer. |

Regulatory Requirements | Following the effectiveness of the registration statement covering the exchange offer with the Securities and Exchange Commission, or the SEC, no other material federal regulatory requirement must be complied with in connection with the exchange offer. |

Exchange Agent | U.S. Bank National Association is serving as exchange agent in connection with the exchange offer. The address and telephone number of the exchange agent are listed under the heading “The Exchange Offer — Exchange Agent.” |

Use of Proceeds | We will not receive any cash proceeds from the exchange offer. |

Resales | Based on interpretations by the staff of the SEC in several no-action letters issued to third parties, we believe that the exchange notes issued in the exchange offer may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery requirements of the Securities Act as long as: |

| • | you are acquiring the exchange notes in the ordinary course of your business; |

| • | you are not engaged in, do not intend to engage in and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes; and |

| • | you are neither an affiliate of the issuers or the guarantors nor a broker-dealer tendering original notes acquired directly from the issuers for your own account; |

and provided that, if you are a broker-dealer that holds original notes that were acquired for your own account as a result of market-making or other trading activities, you must acknowledge that you will deliver a prospectus meeting the requirements of the Securities Act in connection with any resales of the exchange notes received by you in the exchange offer. See “Plan of Distribution.”

If you are an affiliate of the issuers or are engaged in or intend to engage in or have any arrangement or understanding with any person to participate in the distribution of the exchange notes:

| • | you cannot rely on the applicable interpretations of the staff of the SEC; |

6

Table of Contents

| • | you will not be able to tender your original notes in the exchange offer; and |

| • | you must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. |

Consequences of Not Exchanging Original Notes | If you do not exchange your original notes in the exchange offer, you will continue to be subject to the restrictions on transfer described in the legend on your original notes. In general, you may offer or sell your original notes only: |

| • | if they are registered under the Securities Act and applicable state securities laws; |

| • | if they are offered or sold under an exemption from registration under the Securities Act and applicable state securities laws; or |

| • | if they are offered or sold in a transaction not subject to the Securities Act and applicable state securities laws. |

We currently do not intend to register the original notes under the Securities Act. Under some circumstances, holders of the original notes, including holders who are not permitted to participate in the exchange offer or who may not freely sell exchange notes received in the exchange offer, may require us to file, and to cause to become effective, a shelf registration statement covering resales of the original notes by these holders. For more information regarding the consequences of not tendering your original notes and our obligations to file a shelf registration statement, see “The Exchange Offer — Consequences of Exchanging or Failing to Exchange the Original Notes” and “The Exchange Offer — Registration Rights Agreement.”

Summary Description of Exchange Notes

This “Summary Description of Exchange Notes” describes the principal terms of the exchange notes. The terms of the exchange notes and those of the outstanding original notes are substantially identical, except that the exchange notes will have been registered under the Securities Act, the exchange notes will not bear restrictive legends restricting their transfer under the Securities Act and holders of exchange notes will not be entitled to registration rights and special interest provisions that apply to the original notes under the registration rights agreement. We refer to the original notes and the exchange notes collectively as the notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. For a more complete understanding of the exchange notes, see “Description of Exchange Notes” in this prospectus.

Co-Issuers | Solo Cup Company and Solo Cup Operating Corporation. |

Exchange Notes Offered | $300.0 million in aggregate principal amount of 10.5% senior secured notes due 2013. |

Maturity | November 1, 2013. |

7

Table of Contents

Interest Rate | The exchange notes will bear interest at a rate of 10.5% per annum. Interest will be computed on the basis of a 360-day year composed of twelve 30-day months. |

Interest Payment Dates | Interest on the exchange notes will be payable semi-annually on May 1 and November 1 of each year, beginning on November 1, 2009. |

Guarantees | The obligations of the issuers under the original notes are, and their obligations under the exchange notes will be, fully and unconditionally guaranteed, jointly and severally, by all of Solo’s current and future domestic subsidiaries, other than SCOC (a co-issuer of the notes), an inactive receivables subsidiary and specified immaterial subsidiaries. See “Description of Exchange Notes.” |

The term “domestic subsidiaries,” when used in reference to the notes, our asset-based revolving credit facility or our existing senior subordinated notes, comprises, in addition to U.S. subsidiaries, non-U.S. subsidiaries (including Solo’s current subsidiaries located in the United Kingdom) other than controlled foreign corporations (as such term is defined under the Internal Revenue Code of 1986, as amended) and subsidiaries of controlled foreign corporations and other than any subsidiaries that have been designated as unrestricted subsidiaries in accordance with the indenture governing the notes (none of Solo’s subsidiaries has been so designated to date).

Not all of Solo’s subsidiaries will guarantee the notes. These non-guarantor subsidiaries, other than SCOC (a co-issuer of the notes), which currently comprise an inactive receivables subsidiary and Solo’s non-domestic subsidiaries, generated approximately 11.1% of our consolidated revenues in Fiscal Year 2008, and held approximately 9.8% of our consolidated assets as of September 27, 2009. The notes and the note guarantees will be structurally subordinated to indebtedness and other liabilities of Solo’s non-guarantor subsidiaries, other than SCOC.

Collateral | The exchange notes and the exchange note guarantees will be secured on a senior basis (subject to permitted prior liens), together with any other Priority Lien Obligations (as such term is defined in “Description of Exchange Notes — Certain Definitions”), equally and ratably by security interests granted to the collateral trustee in all Notes Collateral (as such term is defined in “Description of Exchange Notes — Certain Definitions”) from time to time owned by the issuers or the guarantors. |

The Notes Collateral will comprise substantially all of the issuers’ and the guarantors’ tangible and intangible assets, other than the ABL Collateral (as such term is defined in “Description of Exchange Notes — Certain Definitions”) and specified excluded assets. The collateral trustee will hold senior liens on the Notes Collateral in trust

8

Table of Contents

for the benefit of the noteholders and the holders of any other Priority Lien Obligations. See “Description of Exchange Notes — Security.” |

The exchange notes and the exchange note guarantees will also be secured on a junior basis (subject to permitted prior liens) by security interests granted to the collateral trustee in all ABL Collateral from time to time owned by the issuers or the guarantors.

The ABL Collateral comprises substantially all of the issuers’ and the guarantors’ accounts receivable, payment intangibles (other than those constituting identifiable proceeds of Notes Collateral), inventory, deposit accounts, commodity accounts, securities accounts, lock-boxes, instruments, chattel paper, cash and cash equivalents, general intangibles related to any of the foregoing, proceeds and products of the foregoing and certain assets related thereto, other than specified excluded assets. The collateral trustee will hold junior liens on the ABL Collateral in trust for the benefit of the noteholders and the holders of any other Priority Lien Obligations. See “Description of Exchange Notes — Security.”

Assets held by Solo’s non-guarantor subsidiaries will not be part of the collateral securing the notes or our asset-based revolving credit facility.

Ranking | The exchange notes will be the issuers’ general senior secured obligations, rankingpari passu in right of payment with all of the issuers’ existing and future indebtedness that is not subordinated and senior in right of payment to all of the issuers’ existing and future subordinated indebtedness, including our existing senior subordinated notes. |

The exchange notes will be effectively junior to our asset-based revolving credit facility to the extent of the value of the ABL Collateral, which secures that credit facility on a senior basis.

The exchange notes will be structurally subordinated to any existing and future indebtedness of any of Solo’s non-guarantor subsidiaries, other than SCOC. These non-guarantor subsidiaries had $0.7 million of indebtedness, including guarantees, as of September 27, 2009.

The exchange note guarantees will be general senior secured obligations of the guarantors, rankingpari passu in right of payment with all existing and future indebtedness that is not subordinated of each guarantor and senior in right of payment to any existing and future subordinated indebtedness of each guarantor, including such guarantor’s guarantee of our existing senior subordinated notes.

The exchange note guarantees will be effectively junior to our asset-based revolving credit facility to the extent of the value of the ABL Collateral, which secures that credit facility on a senior basis.

9

Table of Contents

Intercreditor Agreement | The collateral trustee has entered into an intercreditor agreement with the issuers, the guarantors and Bank of America, N.A., as administrative agent under our asset-based revolving credit facility, that will govern the relationship of noteholders and the lenders under our asset-based revolving credit facility with respect to collateral and certain other matters. See “Description of Exchange Notes — The Intercreditor Agreement.” |

Collateral Trust Agreement | The issuers have entered into a collateral trust agreement with the guarantors, the collateral trustee and the trustee under the indenture governing the notes. The collateral trust agreement sets forth the terms on which the collateral trustee will receive, hold, administer, maintain, enforce and distribute the proceeds of all of its liens upon the collateral. See “Description of Exchange Notes — The Collateral Trust Agreement.” |

Sharing of Liens and Collateral | The issuers and the guarantors may issue additional senior secured indebtedness under the indenture governing the notes. The liens securing the notes may also secure, together on an equal and ratable basis with the exchange notes, other Priority Lien Debt (as such term is defined in “Description of Exchange Notes — Certain Definitions”) permitted to be incurred by the issuers under the indenture governing the notes, including additional notes of the same class under the indenture governing the notes. The issuers and the guarantors may also grant additional liens on the collateral securing the notes on a junior basis to secure Subordinated Lien Debt (as such term is defined in “Description of Exchange Notes — Certain Definitions”) permitted to be incurred under the indenture governing the notes. |

Mandatory Redemption | None. |

Optional Redemption | On or after May 1, 2011, the issuers may redeem all or a part of the notes at the redemption prices set forth under “Description of Exchange Notes — Optional Redemption,” plus accrued and unpaid interest and special interest, if any, to the applicable redemption date. |

In addition, at any time prior to May 1, 2011, the issuers may, on one or more than one occasions, redeem some or all of the notes at any time at a redemption price equal to 100% of the principal amount of the notes redeemed, plus a “make-whole” premium as of, and accrued and unpaid interest and special interest, if any, to, the applicable redemption date. At any time prior to May 1, 2011, the issuers may also redeem up to 35% of the aggregate principal amount of the notes, using the proceeds of certain qualified equity offerings, at a redemption price of 110.500% of the principal amount thereof and may, not more than once in any 12-month period, redeem up to 10% of the original aggregate principal amount of the notes at a redemption price of 103%, in each case, plus accrued and unpaid interest and special interest, if any, to the applicable redemption date. See “Description of Exchange Notes — Optional Redemption.”

10

Table of Contents

Change of Control Offer | If Solo experiences certain change of control events, the issuers must offer to repurchase the notes at a repurchase price equal to 101% of the principal amount of the notes repurchased, plus accrued and unpaid interest and special interest, if any, to the applicable repurchase date. See “Description of Exchange Notes — Repurchase at the Option of Holders — Change of Control.” |

Asset Sale Offer | If we sell assets under certain circumstances, the issuers must offer to repurchase the notes at a repurchase price equal to 100% of the principal amount of the notes repurchased, plus accrued and unpaid interest and special interest, if any, to the applicable repurchase date. See “Description of Exchange Notes — Repurchase at the Option of Holders — Asset Sales.” |

Restrictive Covenants | The exchange notes will be issued under the same indenture as the indenture governing the original notes. That indenture contains covenants that, among other things, restrict Solo’s ability and the ability of Solo’s restricted subsidiaries to: |

| • | incur additional indebtedness or issue disqualified stock or preferred stock; |

| • | create liens; |

| • | pay dividends, make investments or make other restricted payments; |

| • | sell assets; |

| • | consolidate, merge, sell or otherwise dispose of all or substantially all of Solo’s or their assets; |

| • | enter into transactions with affiliates; and |

| • | designate subsidiaries as unrestricted. |

These covenants are subject to a number of important limitations and exceptions. See “Description of Exchange Notes — Certain Covenants.”

No Established Trading Market | There is no established trading market for the notes. The exchange notes will not be listed on any securities exchange or on any automated dealer quotation system. We cannot assure you that an active or liquid trading market for the exchange notes will develop. If an active or liquid trading market for the exchange notes does not develop, the market price and liquidity of the exchange notes may be adversely affected. |

Form and Denominations | The exchange notes will be issued in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. The exchange notes will be book-entry only and registered in the name of a nominee of DTC. |

11

Table of Contents

Risk Factors

You should carefully consider the information set forth under the caption “Risk Factors” on page 14 of this prospectus before tendering your original notes for exchange.

Ratio of Earnings to Fixed Charges

Earnings were insufficient to cover fixed charges by $38.4 million for the thirty-nine weeks ended September 27, 2009. Earnings were insufficient to cover fixed charges by $12.8 million, $27.2 million, $317.3 million, $41.3 million and $59.2 million for the years ended December 28, 2008, December 30, 2007, December 31, 2006, January 1, 2006 and December 31, 2004, respectively.

For purposes of the ratio of earnings to fixed charges, earnings means income (loss) from continuing operations before income taxes; fixed charges means gross interest expense including capitalized interest plus the amortization of deferred financing fees and the portion of rental expenses considered representative of the interest factor.

Industry Data

The data included in this prospectus regarding industry size and relative industry position are based on a variety of sources, including company research, third party studies and surveys, some of which we have commissioned, industry and general publications and estimates based on our knowledge and experience in the industry in which we operate. Our estimates have been based on information obtained from our customers, suppliers, trade and business organizations and other contacts in the industry, including Technomic, Inc., a consulting firm retained by us from time to time to perform industry studies and analyses, and The Nielsen Company. This information may prove to be inaccurate due to the method by which we obtained some of the data for our estimates or because this information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, you should be aware that industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable.

Presentation of Financial and Other Information

We report our financial statements in U.S. dollars and prepare our consolidated financial statements in accordance with generally accepted accounting principles in the United States, or GAAP. In this prospectus, except where otherwise indicated, all references to “$,” “dollars” or “U.S. dollars” are to the lawful currency of the United States and all references to “CAD$” or “Canadian dollars” are to the lawful currency of Canada.

Our fiscal year is the 52- or 53-week period ending on the last Sunday in December. In this prospectus, we refer to the fiscal year ended December 28, 2008 as “Fiscal Year 2008” or “2008,” the fiscal year ended December 30, 2007 as “Fiscal Year 2007” or “2007,” and the fiscal year ended December 31, 2006 as “Fiscal Year 2006” or “2006,” which are all 52-week periods. In a 52-week fiscal year, such as 2009, our fiscal year is divided into four 13-week fiscal periods, each of which is composed of two initial accounting periods of four weeks and a final five-week accounting period.

We own or have rights to various trademarks, copyrights and trade names used in our business, including: Solo®, Sweetheart®, BARETM, Jack Frost®, Trophy®, Jazz®, Galaxy®, Traveler®, Traveler Plus®, SoloGrips®, Go Cup®, Silent Service®, Guildware®, Simple Elegance®, SOLO SQUAREDTM, REVEALTM, DUO SHIELDTM

12

Table of Contents

and ULTRA CLEARTM. Sesame StreetTM is a trademark of Sesame Workshop that is used by us under license. This prospectus may contain additional trade names, trademarks and service marks belonging to us and to other companies. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

To track our inventory, we assign unique identifiers, known as SKUs, to products on a location-by-location basis. This means that a single product that is manufactured at a number of our facilities may have that number of separate and distinct SKUs assigned to it.

13

Table of Contents

You should carefully consider the risks described below as well as the other information included in this prospectus before tendering your original notes for exchange. If any of these risks have a material adverse effect on our business, financial condition, results of operations or cash flows, you may lose all or part of your investment in the notes.

Risks Related to Our Business

Our ability to meet our cash requirements and service our debt is impacted by many factors that are outside our control, including the current global recession and restricted credit markets.

Our future operating performance is dependent on many factors, some of which are beyond our control, including prevailing economic, financial and industry conditions. The sales of our products are primarily dependent on discretionary income of consumers. If global economic conditions continue to adversely impact consumer discretionary spending, our sales could continue to decline or become increasingly concentrated in lower-margin products, and our business, financial condition, results of operations or cash flows could be materially adversely affected.

The impact of the global recession and credit crisis on our suppliers and customers is also unpredictable, outside of our control and may create additional risks for us, both directly and indirectly. The inability of suppliers to access financing or the insolvency of one or more of our raw material suppliers could lead to disruptions in our supply chain, which could adversely impact our sales or increase our costs. Our suppliers may require us to pay cash in advance or obtain letters of credit for their benefit as a condition to selling us their products and services. A number of restaurant chains and consumer product retailers have sought bankruptcy protection. If more than one of our principal customers were to file for bankruptcy, our sales could be adversely impacted and our ability to collect outstanding accounts receivable from any such customer could be limited. Any of these risks and uncertainties could have a material adverse effect on our business, financial condition, results of operations or cash flows.

Our operating performance and ability to comply with covenants under our borrowing arrangements are dependent on our continued ability to access funds under our credit and loan agreements and from cash on hand, maintain sales volumes, drive profitable growth, realize cost savings and generate cash from operations. The financial institutions that fund our asset-based revolving credit facility are also being impacted by the volatility in the credit markets, and if one or more of them cannot fulfill our revolving credit requests then our operations may be adversely impacted. If our revolving credit is unavailable due to a lender not being able to fund requested amounts, or because we have not maintained compliance with our covenants, or we do not meet our costs, sales or growth initiatives within the time frame we expect, our cash flow could be materially adversely impacted. A material decrease in our cash flow could cause us to fail to meet covenants under our credit and loan agreements. A default under our credit or loan agreements could restrict or terminate our access to borrowings and materially impair our ability to meet our obligations as they come due. If we do not comply with any of our covenants and we do not obtain a waiver or amendment that otherwise addresses that non-compliance, our lenders may accelerate payment of all amounts outstanding under the affected borrowing arrangements, which would immediately become due and payable, together with accrued interest. Such an acceleration would cause a default under the indentures governing the notes and our senior subordinated notes and other agreements that provide us with access to funding and under our lease agreement with iStar SCC Financial Distribution Centers LLC covering six of our facilities. Any one or more defaults, or our inability to generate sufficient cash flow from our operations in the future to service our indebtedness and meet our other needs, may require us to refinance all or a portion of our existing indebtedness or obtain additional financing or reduce expenditures that we deem necessary to our business. We cannot assure you that any refinancing of this kind would be possible or that any additional financing could be obtained. The inability to obtain additional financing could have a material adverse

14

Table of Contents

effect on our financial condition and on our ability to meet our obligations to noteholders. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources.”

Our significant level of indebtedness could limit cash flow available for our operations, adversely affect our financial health and prevent the issuers from fulfilling their obligations under the notes and the guarantors from fulfilling their obligations under the note guarantees.

We have a significant amount of indebtedness. As of September 27, 2009, we had total indebtedness of $630.9 million, consisting of $294.0 million of the notes (reflecting $300.0 million in aggregate principal amount less $6.0 million of unamortized original issue discount), $325 million of our senior subordinated notes, $9.7 million of borrowings under our asset-based revolving credit facility, $0.7 million of borrowings under our Canadian credit facility and $1.5 million in capital lease obligations, and additional borrowing capacity under our new asset-based revolving credit facility of $177.9 million, subject to borrowing base limitations and other specified terms and conditions.

Our significant level of debt could have important consequences for our business and the holders of our debt securities, including the following:

| • | requiring that we use a large portion of our cash flow to pay principal and interest on the notes, our senior subordinated notes, our credit facilities and our other debt, which will reduce the availability of cash to fund working capital, capital expenditures, research and development and other business activities; |

| • | increasing our vulnerability to general adverse economic and industry conditions; |

| • | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| • | restricting us from making strategic acquisitions or exploiting business opportunities; |

| • | making it more difficult for us to satisfy our obligations with respect to the notes and our other debt; |

| • | placing us at a competitive disadvantage relative to competitors that have less debt; and |

| • | limiting our ability to borrow additional monies in the future to fund working capital, capital expenditures and other general corporate purposes. |

The instruments governing our outstanding indebtedness contain restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all or a portion of our outstanding indebtedness.

We may be able to incur substantial additional indebtedness that could further exacerbate the risks associated with our substantial leverage.

We may incur substantial additional indebtedness in the future. Although the indentures governing the notes and our senior subordinated notes and the loan agreement governing our asset-based revolving credit facility contain restrictions on our incurrence of additional debt, these restrictions are subject to a number of qualifications and exceptions, and we could incur substantial additional indebtedness, including additional senior indebtedness. As of September 27, 2009, our credit facilities (U.S. and Canadian) had unused capacity of $188.9 million, after taking into account outstanding letters of credit, subject to borrowing base limitations and other specified terms and conditions. If we incur additional debt, the risks described above under “Our significant level of indebtedness could limit cash flow available for our operations, adversely affect our financial health and prevent the issuers from fulfilling their obligations under the notes and the guarantors from fulfilling their obligations under the note guarantees” would intensify.

15

Table of Contents

Covenant restrictions under our indebtedness may limit our ability to operate our business.

The indentures governing the notes and our senior subordinated notes, the loan agreement governing our asset-based revolving credit facility and instruments governing our other existing indebtedness contain, and instruments governing our future indebtedness may contain, covenants that may restrict our ability to finance future operations or capital needs or to engage in other business activities, which restrictions include, among other things, limitations on Solo’s ability and the ability of Solo’s restricted subsidiaries to:

| • | incur additional indebtedness or issue disqualified stock or preferred stock; |

| • | create liens; |

| • | pay dividends, make investments or make other restricted payments; |

| • | sell assets; |

| • | consolidate, merge, sell or otherwise dispose of all or substantially all of Solo’s or their assets; |

| • | enter into transactions with affiliates; and |

| • | designate subsidiaries as unrestricted. |

Events beyond our control, including changes in general economic and business conditions, may affect our ability to comply with the covenants in the instruments governing our indebtedness. A breach of any of these covenants would result in a default under the loan agreement governing our asset-based revolving credit facility and the indentures governing the notes and our senior subordinated notes. If an event of default under the loan agreement governing our asset-based revolving credit facility occurs, the lenders thereunder could elect to declare all amounts outstanding under such credit facility, together with accrued interest, to be immediately due and payable. If the indebtedness under the loan agreement governing our asset-based revolving credit facility and the indentures governing the notes and our senior subordinated notes is accelerated, we cannot assure you that we would have sufficient assets to pay amounts due under our asset-based revolving credit facility, the notes, our senior subordinated notes or other indebtedness then outstanding. As a result, you may receive less than the full amount you would be otherwise entitled to receive on the notes. See “Description of Certain Other Indebtedness” and “Description of Exchange Notes — Certain Covenants.”

Failure to maintain our credit ratings could limit our access to the capital markets, adversely affect the cost and terms upon which we are able to obtain additional financing and negatively impact our business.

Although we believe existing cash, funds generated by operations and amounts available under our asset-based revolving credit facility will collectively provide adequate resources to fund our ongoing operating requirements, we may be required to seek additional financing to compete effectively in our market. In light of difficulties in the financial markets, there can be no assurance that we will be able to maintain our credit ratings. We have experienced downgrades in the past and may experience further downgrades. Failure to maintain these credit ratings could, among other things, limit our access to the capital markets and adversely affect the cost and terms upon which we are able to obtain additional financing, including any financing from our suppliers, which could negatively impact our business.

A credit rating is not a recommendation to buy, sell or hold any security and may be revised or withdrawn at any time by the issuing organization. Each credit rating should be evaluated independently of any other credit rating.

We could be adversely affected by raw material availability and pricing or a shortage of supply due to supplier financial difficulties, natural disasters or other causes.

Our principal raw materials include polystyrene, polypropylene, polyethylene terephthalate, or PET, emerging bio-resins such as polylactic acid, or PLA, coated and uncoated paper and renewable resources such as sugarcane. There are currently a limited number of polystyrene suppliers, and periods of short supply may occur

16

Table of Contents

if one or more suppliers’ operations are materially impacted due to financial difficulties, natural disasters or other causes. To the extent that our supply of raw materials becomes restricted and we cannot locate or substitute adequate alternative sources, our business, financial condition, results of operations or cash flows may be materially adversely affected.

In addition, prices for our raw materials fluctuate. When raw material prices decrease, we face increased pressure from our customers to reduce our selling prices for products containing such raw material. When raw material prices increase, our selling prices have historically also increased, although often with a time lag. The impact on us of raw material price changes is affected by a number of factors, including the underlying cause of price changes (e.g., natural disasters or general economic conditions), the level of our inventories at the time of price changes, the specific timing and frequency of price changes and the lead and lag time that generally accompanies the implementation of both raw material price changes and subsequent selling price changes. If raw material prices increase and we are unable to pass the price increases on to our customers or there is a significant time lag in any selling price increases we are able to implement, our profitability may be adversely affected, which could have a material adverse effect on our business, financial condition, results of operations or cash flows. We have not historically employed hedging strategies to limit our exposure to fluctuations in raw material prices on any meaningful level.

Our ability to successfully operate is dependent on the availability of energy and fuel at anticipated prices.

Sustained increases in global energy prices, particularly for crude oil and electricity, at prices greater than we have anticipated could have a material adverse impact on our operations if we are unable to pass through such increases to our customers in a timely manner. Increases in crude oil prices particularly impact our transportation and production costs and the price we pay for certain raw materials. Global energy prices are determined by many factors, which are beyond our control and are unpredictable. Consequently, we cannot predict whether global energy prices will remain at their current levels, and we cannot predict the impact that these prices will have on our business, financial condition, results of operations or cash flows.

We operate in a highly competitive environment and may not be able to compete successfully.

The single-use foodservice products industry is extremely competitive and highly fragmented. We compete for customers based on brand reputation, quality, cost, customer service, breadth of product offering, product differentiation, innovation, marketing programs and value. A few of our competitors are integrated in the manufacturing of single-use foodservice products and related raw materials, which reduces their costs for these materials and gives them greater access to these materials in periods of short supply. Our current or potential competitors may offer products at a lower price or products and services that are superior to ours. In addition, our competitors may be more effective and efficient in integrating new technologies or emerging raw materials to meet changing consumer demands. Our success depends upon successful research, development and engineering efforts to utilize emerging and legislatively mandated raw materials, our ability to expand or modify our manufacturing capacity, and the extent to which we are able to convince customers and consumers to accept our new products. If we fail to successfully innovate, introduce, market, manufacture and differentiate our products from those of our competitors, our ability to maintain or expand our net sales and to maintain or enhance our industry position or profit margins could be adversely affected. This, in turn, could materially adversely affect our business, financial condition, results of operations or cash flows.

Our products also compete with products that incorporate metal, glass, reusables and other packaging materials. If we are unable to react timely to changing consumer demands, legislative mandates and competitive conditions that favor those or other competing products, we may experience price reductions, reduced gross margins, decreased sales and reduced ability to attract and retain customers.

17

Table of Contents

Our operations and products are subject to environmental and governmental regulations that could adversely affect our business, financial condition, results of operations or cash flows.

Our operations are subject to comprehensive and frequently changing federal, state, foreign and local environmental and occupational health and safety laws and regulations. These laws and regulations include the Federal Food, Drug and Cosmetic Act, which regulates materials that have direct contact with food, and laws governing the use of certain raw materials in our products, emissions of air pollutants, discharges of waste and storm water, and the handling, use, treatment, storage and disposal of, or exposure to, hazardous substances. We are presently, and may in the future be, subject to liability for the investigation and remediation of environmental contamination, including contamination caused by other parties, at properties that we own or operate or that we formerly owned or operated and at other properties where we or our predecessors have arranged for the disposal of hazardous substances. As a result, we are involved from time to time in administrative and judicial proceedings and inquiries relating to environmental matters. Any present or future investigations, future clean up costs and remedial efforts relating to environmental matters could entail material costs or otherwise result in material liabilities. Under environmental laws applicable to our operations and our properties, we are required to obtain various environmental permits granted by federal, state, foreign and local authorities. There are various risks associated with noncompliance with these permits, including cessation of our operations at the noncompliant facilities and significant fines and penalties.

We cannot predict what environmental legislation or regulations will be enacted in the future, how existing or future laws or regulations will be administered or interpreted or affect the use of our products, or what environmental conditions may be found to exist at our facilities or at third party sites for which we are liable. Enactment of stricter laws or regulations, stricter interpretation of existing laws and regulations or the requirement to undertake the investigation or remediation of currently unknown environmental contamination at our own or third party sites may require us to make additional expenditures, some of which could be material.

The single-use foodservice products industry is subject to evolving federal, state, local and foreign legislation and regulations affecting the types of raw materials we may use in our products. The intent of such legislation is to reduce solid waste and litter by requiring, among other things, that manufacturers pay for the disposal of products they create and/or use raw materials that are recyclable, biodegradable or compostable. The legislation passed to date has not had a material adverse effect on our operations. However, if we are unable to procure or substitute raw materials that meet the requirements of future environmental legislation or regulations, our sales may decline in those localities where such laws and regulations have been adopted. Proposed legislation could increase our operating costs as a result of any fees imposed on manufacturers of foodservice products for the disposal of products that are not recyclable or compostable and could increase the cost of our products by prohibiting the use of traditional raw materials and requiring the use of emerging materials that are more expensive.

Our international operations expose us to risks related to conducting business in multiple jurisdictions outside the United States.

Our international operations consist of operating subsidiaries in four countries, as well as international export sales originating both in the United States and at our international facilities. The international scope of our operations may lead to volatile financial results and difficulties in managing our business. We generated approximately 18% of our net sales outside the United States during Fiscal Year 2008. International sales and operations are subject to a number of risks, including the following:

| • | exchange rate fluctuations and limitations on currency convertibility; |

| • | importation limitations and export control restrictions; |

| • | social and political turmoil, official corruption and civil unrest; |

| • | restrictive governmental actions, such as the imposition of trade quotas and restrictions on transfers of funds; |

18

Table of Contents

| • | changes in non-U.S. labor laws and regulations affecting our ability to hire, retain or dismiss employees; |

| • | violations of U.S. or local laws, including the U.S. Foreign Corrupt Practices Act; |

| • | compliance with multiple and potentially conflicting laws and regulations; |

| • | preference for locally branded products, and laws and business practices favoring local competition; |

| • | less effective protection of intellectual property; |

| • | difficulties and costs of staffing, managing and accounting for foreign operations; and |

| • | unfavorable business conditions or economic instability in any particular country or region. |

Our exposure to risks associated with currency exchange rate fluctuations results primarily from the translation exposure associated with the preparation of our consolidated financial statements, as well as from transaction exposure associated with generating revenues and incurring expenses in different currencies. While our consolidated financial statements are reported in U.S. dollars, the financial statements of our foreign subsidiaries are measured using the local currency as the functional currency and translated into U.S. dollars by applying an appropriate exchange rate. As a result, fluctuations in the exchange rate of the U.S. dollar relative to the local currencies in which our foreign subsidiaries report could cause significant fluctuations in our consolidated results. We record sales and expenses in a variety of currencies. While our expenses with respect to foreign operations are generally denominated in the same currency as the corresponding sales, we have transaction exposure to the extent our receipts and expenditures are not offsetting in any currency. Moreover, the costs of doing business abroad may increase as a result of adverse exchange rate fluctuations. In addition, we may lose customers if exchange rate fluctuations, currency devaluation or economic crises increase the local currency price of our products or reduce our customers’ ability to purchase our products. If we are unable to manage the operational challenges associated with our international activities, our business, financial condition, results of operations or cash flows could be materially and adversely affected.

In the event of a catastrophic loss of one of our key manufacturing facilities, our business would be adversely affected.

While we manufacture our products in a number of diversified facilities and maintain insurance covering our facilities, including business interruption insurance, a catastrophic loss of the use of all or a portion of one of our key manufacturing facilities due to accident, weather conditions, natural disaster or otherwise, whether short- or long-term, could have a material adverse effect on our business, financial condition, results of operations or cash flows.

We are controlled by the stockholders of SCIC, the interests of which may conflict with the interests of holders of the notes.

All of our outstanding capital stock is owned by our parent company, SCIC. Holders of SCC Holding’s voting interests control 100% of the outstanding common stock of SCIC, and affiliates of Vestar hold 99.9% of SCIC’s outstanding convertible participating preferred stock, or SCIC preferred stock, with the remaining balance of the SCIC preferred stock held by members of our management.

The SCIC preferred stock is currently convertible at any time, at the option of the holders, into 32.71% of the common stock of SCIC. The SCIC preferred stock is entitled to vote on all matters, voting together with the holders of common stock as a single class. Holders of a majority of the outstanding shares of SCIC preferred stock, voting as a separate class, are entitled to elect a majority of individuals to the board of directors of SCIC and Solo. In December 2006, Vestar became entitled to appoint a majority of the director positions of Solo pursuant to a stockholders’ agreement, referred to in this prospectus as the Stockholders’ Agreement, dated as of February 27, 2004, as amended, among Vestar, SCIC, SCC Holding, Solo and certain other parties. If Vestar

19

Table of Contents

receives a bona fide offer from a third party to purchase (whether by stock purchase, merger or otherwise) at least 80% of Solo’s common stock, SCC Holding has agreed at Vestar’s request to vote in favor of such offer.

The interests of SCC Holding and the holders of SCIC preferred stock, including Vestar, could conflict with the interests of holders of the notes. For example, if we encounter financial difficulties or are unable to pay our debts as they mature, the interests of these indirect equity holders might conflict with the interests of a note holder. SCIC’s stockholders may also have an interest in pursuing acquisitions, divestitures, financings or other transactions that, in their judgment, could enhance their equity investments, even though the transactions might involve risks to a holder of the notes. In addition, SCC Holding or its affiliates and Vestar or its affiliates may in the future own businesses that directly compete with ours. While we are subject to certain provisions of the Sarbanes-Oxley Act of 2002, these provisions do not require us to have independent directors.

The loss of one or more of our principal customers could have a material adverse effect on our business, financial condition, results of operations or cash flows.

We have a number of large customers that account for a significant portion of our net sales. For Fiscal Year 2008, our five largest customers represented approximately 32% of net sales, with no one customer accounting for more than 9.6% of net sales. The loss of one or more of our large customers could have a material adverse effect on our business, financial condition, results of operations or cash flows. In line with industry practice, we generally do not enter into long-term sales agreements with customers.

We may undertake acquisitions or divestitures and consequently face potential integration, management diversion and other risks.

We may make acquisitions or divestitures in the future. Any future acquisitions or divestitures could be of significant size and may involve domestic or international parties. To acquire and integrate a separate organization or significant new assets or to divest a portion of our business would divert management attention from other business activities. This diversion, together with other difficulties we may encounter in integrating an acquired business or selling a portion of our business, could have a material adverse effect on our business, financial condition, results of operations or cash flows. In connection with future acquisitions, we may also assume the liabilities of the businesses we acquire. These liabilities could materially adversely affect our business, financial condition, results of operations or cash flows.

We may not be able to adequately protect our intellectual property and other proprietary rights.

We rely on a combination of contractual provisions, confidentiality procedures and agreements, and patent, trademark, copyright, unfair competition, trade secret and other intellectual property laws to protect our intellectual property and other proprietary rights. Such measures may not provide adequate protection and may not prevent our competitors from gaining access to our intellectual property and proprietary information or independently developing technologies that are substantially equivalent or superior to our technology, which could harm our competitive position and could have a material adverse effect on our business, financial condition, results of operations or cash flows. Furthermore, no assurance can be given that any pending patent application or trademark application held by us will result in an issued patent or registered trademark, or that any issued or registered patents or trademarks will not be challenged, invalidated, circumvented or rendered unenforceable.

Litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties related to our intellectual property. Any litigation or claims brought by or against us, whether with or without merit, or whether successful or not, could result in substantial costs and diversion of our resources, which could have a material adverse effect on our business, financial condition, results of operations or cash flows. Any intellectual property litigation or claims against us could result in the loss or compromise of our intellectual property and proprietary rights, could subject us to

20

Table of Contents

significant liabilities, require us to seek licenses on unfavorable terms, if available at all, prevent us from manufacturing or selling products and require us to redesign, relabel or, in the case of trademark claims, rename our products, any of which could have a material adverse effect on our business, financial condition, results of operations or cash flows. We are currently a defendant in a case involving the patent marking statute as applied to certain patent markings on our products. This case was resolved in our favor on summary judgment, and it is currently on appeal at the U.S. Court of Appeals for the Federal Circuit. We believe that the plaintiff’s claims are without merit and we will continue to vigorously defend ourselves on appeal.

Financial market conditions have had a negative impact on the return of plan assets for our pension plans, which may require additional funding and negatively impact our cash flows.

Certain U.S., Canadian and European hourly and salaried employees are covered by our defined benefit pension plans. Between December 31, 1987 and March 31, 2001, the majority of the U.S. plans were frozen to new participants. Our pension expense and required contributions to our pension plan are directly affected by the value of plan assets, the projected rate of return on plan assets, the actual rate of return on plan assets and the actuarial assumptions we use to measure the defined benefit pension plan obligations. Due to the significant financial market downturn during 2008, the funded status of our pension plans has declined and actual asset returns were below the assumed rate of return used to determine pension expense. Our pension plans were underfunded by approximately $26.1 million and $4.0 million, as of December 28, 2008 and December 30, 2007, respectively. If plan assets continue to perform below expectations, future pension expense and funding obligations will increase, which could have a negative impact on our cash flows from operations, decrease borrowing capacity and increase interest expense. Moreover, under the Pension Protection Act of 2006, it is possible that continued losses to asset values may necessitate accelerated funding of U.S. pension plans in the future to meet minimum federal government requirements.

Risks Related to the Notes

The notes and the note guarantees are structurally subordinated to indebtedness and other liabilities of Solo’s non-guarantor subsidiaries.

Not all of Solo’s subsidiaries guarantee the notes. The notes and the note guarantees are structurally subordinated to the indebtedness and other liabilities of Solo’s non-guarantor subsidiaries, other than SCOC (a co-issuer of the notes), and noteholders do not have any claim as a creditor against any such non-guarantor subsidiary, other than SCOC. In addition, subject to certain limitations, the indentures governing the notes and our senior subordinated notes and the loan agreement governing our asset-based revolving credit facility permit Solo’s non-guarantor subsidiaries to incur additional indebtedness. Solo’s non-guarantor subsidiaries, other than SCOC, generated approximately 11.1% of our consolidated revenues in Fiscal Year 2008 and held approximately 9.8% of our consolidated assets as of September 27, 2009.

We will not have all title insurance policies delivered at closing.

In order to insure the priority of each of the mortgage liens, new title insurance policies insuring the priority of the liens will have to be obtained. These title insurance policies may not be delivered by the closing date and the liens may not be insured at the time of the issuance of the notes. In addition, if a title defect results in a loss, we cannot assure you that any insurance proceeds received by us will be sufficient to satisfy all the secured obligations, including the notes.

Security over certain collateral may not be in place by closing or may not be perfected by closing.

Certain security interests, including mortgages on certain of our real properties and liens on some of our intellectual property, will not be in place by the closing date of this offering or will not be perfected on the closing date of this offering. To the extent any security interest in the collateral securing the notes cannot be perfected on or prior to the closing date, we will be required to have all such security interests perfected, to the extent required by the indenture governing the notes and the security documents, promptly following closing date. To the extent a security interest in certain collateral is perfected following the closing date, that security

21

Table of Contents

interest would remain at risk of having been granted within 90 days of a bankruptcy filing (in which case it might be voided as a preferential transfer by a trustee in bankruptcy) even after the security interests perfected on the closing date were no longer subject to such risk.

The value of the collateral securing the notes may not be sufficient to satisfy our obligations under the notes.

No appraisal of the fair market value of the collateral securing the notes has been made, and the value of the collateral will depend on market and economic conditions, the availability of buyers and other factors. As a result, liquidating the collateral securing the notes may not produce proceeds in an amount sufficient to pay any amounts due on the notes. We cannot assure you of the value of the collateral or that the net proceeds received upon a sale of the collateral would be sufficient to repay all amounts due on the notes following a foreclosure upon the collateral (and any payments in respect of prior liens) or a liquidation of the issuers’ assets or the assets of the guarantors that grant these security interests.

In the event of a liquidation or foreclosure, the value of the collateral securing the notes is subject to fluctuations based on factors that include general economic conditions, the actual fair market value of the collateral at such time, the timing and the manner of the sale and the availability of buyers and similar factors. In addition, courts could limit recoverability with respect to the collateral if they apply laws of a jurisdiction other than the State of New York to a proceeding and deem a portion of the interest claim usurious in violation of applicable public policy. By its nature, some or all of the collateral may be illiquid and may have no readily ascertainable market value. Likewise, we cannot assure you that the collateral will be saleable or, if saleable, that there will not be substantial delays in its liquidation. To the extent that liens, rights and easements granted to third parties encumber assets located on property owned by the issuers or the guarantors or constitute senior,pari passu or subordinate liens on the collateral, those third parties have or may exercise rights and remedies with respect to the property subject to such encumbrances (including rights to require marshalling of assets) that could adversely affect the value of the collateral located at a particular site and the ability of the collateral trustee to realize or foreclose on the collateral at that site.

In the event that a bankruptcy case is commenced by or against us, if the value of the collateral is less than the amount of principal and accrued and unpaid interest on the notes and all other senior secured obligations, interest may cease to accrue on the notes from and after the date the bankruptcy petition is filed. In the event of a foreclosure, liquidation, bankruptcy or similar proceeding, we cannot assure you that the proceeds from any sale or liquidation of the collateral will be sufficient to pay the obligations due under the notes.

The lien ranking provisions in the intercreditor agreement limit the ability of noteholders to exercise rights and remedies with respect to the ABL Collateral.

The rights of the noteholders with respect to the ABL Collateral securing the notes on a junior basis are substantially limited by the terms of the lien ranking provisions in the intercreditor agreement. Under the terms of the intercreditor agreement, at any time that any obligations that have the benefit of senior liens on the ABL Collateral are outstanding, almost any action that may be taken in respect of the ABL Collateral, including the rights to exercise remedies with respect to, challenge the liens on, or object to actions taken by the administrative agent under our asset-based revolving credit facility with respect to, the ABL Collateral will be at the direction of the holders of the obligations secured by the senior liens on the ABL Collateral, and the collateral trustee, on behalf of noteholders with junior liens on the ABL Collateral, will not have the ability to control or direct such actions, even if the rights of noteholders are adversely affected.

In addition, the intercreditor agreement contains certain provisions benefiting holders of indebtedness under our asset-based revolving credit facility that prevent the collateral trustee from objecting to a number of important matters regarding the ABL Collateral following the filing of a bankruptcy petition. After such filing, the value of the ABL Collateral could materially deteriorate and noteholders would be unable to raise an objection. See “Description of Exchange Notes — The Intercreditor Agreement.”

22

Table of Contents