Use these links to rapidly review the document

TABLE OF CONTENTS

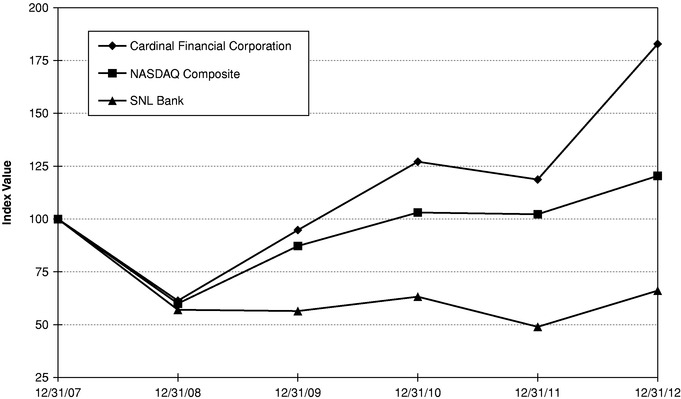

Item 8. Financial Statements and Supplementary Data

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | |

| (Mark One) | | |

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012 |

or |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

|

Commission file number: 0-24557

CARDINAL FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

| | |

Virginia

(State or other jurisdiction

of incorporation or organization) | | 54-1874630

(I.R.S. Employer

Identification No.) |

8270 Greensboro Drive, Suite 500 |

|

|

McLean, Virginia

(Address of principal executive offices) | | 22102

(Zip Code) |

Registrant's telephone number, including area code:(703) 584-3400

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered |

|---|

| Common Stock, par value $1.00 per share | | The Nasdaq Stock Market |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer o | | Accelerated filer ý | | Non-accelerated filer o

(Do not check if a

smaller reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of June 30, 2012: $353,538,977.

The number of shares outstanding of Common Stock, as of March 14, 2013, was 30,253,906.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement for the 2013 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K. With the exception of the portions of the Proxy Statement specifically incorporated herein by reference, the Proxy Statement is not deemed to be filed as part of this Form 10-K.

Table of Contents

TABLE OF CONTENTS

| | | | | | |

| |

| | Page | |

|---|

PART I | |

Item 1.

|

|

Business

|

|

|

3 |

|

Item 1A.

|

|

Risk Factors

|

|

|

23 |

|

Item 1B.

|

|

Unresolved Staff Comments

|

|

|

32 |

|

Item 2.

|

|

Properties

|

|

|

32 |

|

Item 3.

|

|

Legal Proceedings

|

|

|

33 |

|

Item 4.

|

|

Mine Safety Disclosures

|

|

|

33 |

|

PART II

|

|

Item 5.

|

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

|

|

33 |

|

Item 6.

|

|

Selected Financial Data

|

|

|

35 |

|

Item 7.

|

|

Management's Discussion and Analysis of Financial Condition and Results of Operations

|

|

|

36 |

|

Item 7A.

|

|

Quantitative and Qualitative Disclosures About Market Risk

|

|

|

77 |

|

Item 8.

|

|

Financial Statements and Supplementary Data

|

|

|

78 |

|

Item 9.

|

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

|

|

153 |

|

Item 9A.

|

|

Controls and Procedures

|

|

|

153 |

|

Item 9B.

|

|

Other Information

|

|

|

153 |

|

PART III

|

|

Item 10.

|

|

Directors, Executive Officers and Corporate Governance

|

|

|

154 |

|

Item 11.

|

|

Executive Compensation

|

|

|

154 |

|

Item 12.

|

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

|

|

154 |

|

Item 13.

|

|

Certain Relationships and Related Transactions, and Director Independence

|

|

|

154 |

|

Item 14.

|

|

Principal Accounting Fees and Services

|

|

|

155 |

|

Part IV

|

|

Item 15.

|

|

Exhibits, Financial Statement Schedules

|

|

|

155 |

|

This Annual Report on Form 10-K has not been reviewed, or confirmed for accuracy or relevance, by the Federal Deposit Insurance Corporation.

2

Table of Contents

PART I

Item 1. Business

Overview

Cardinal Financial Corporation, a financial holding company, was formed in late 1997 as a Virginia corporation, principally in response to opportunities resulting from the consolidation of several Virginia-based banks. These bank consolidations were typically accompanied by the dissolution of local boards of directors and relocation or termination of management and customer service professionals and a general deterioration of personalized customer service.

We own Cardinal Bank, (the "Bank"), a Virginia state-chartered community bank with 27 banking offices located in Northern Virginia, Maryland and the greater Washington, D.C. metropolitan area. The Bank offers a wide range of traditional bank loan and deposit products and services to both our commercial and retail customers. Our commercial relationship managers focus on attracting small and medium sized businesses as well as government contractors, commercial real estate developers and builders and professionals, such as physicians, accountants and attorneys.

Additionally, we complement our core banking operations by offering a wide range of services through our various subsidiaries, including mortgage banking through George Mason Mortgage, LLC ("George Mason") and Cardinal First Mortgage, LLC ("Cardinal First"), collectively the "mortgage banking segment," retail securities brokerage through Cardinal Wealth Services, Inc. ("CWS"), asset management through Wilson/Bennett Capital Management, Inc. ("Wilson/Bennett") and trust, estate, custody, investment management and retirement planning through the trust division of Cardinal Bank.

George Mason engages primarily in the origination and acquisition of residential mortgages for sale into the secondary market on a best efforts basis through 16 offices located throughout the metropolitan Washington, D.C. region. George Mason is one of the largest residential mortgage originators in the greater Washington metropolitan area, generating originations of approximately $6.6 billion in 2012 and $3.9 billion in 2011, excluding advances on construction loans and including loans purchased from other mortgage banking companies owned by local home builders but managed by George Mason. George Mason sells its mortgage loans to third party investors servicing released. The profitability of George Mason is cyclical as loan production levels are sensitive to changes in the level of interest rates and changes in local home buying activity, which may be seasonal or may be caused by tightening credit conditions or a deteriorating local economy.

Cardinal First offers a construction-to-permanent loan program. This program provides variable rate financing for customers to construct their residences. Once the home has been completed, the loan converts to fixed rate financing and is sold into the secondary market. These construction-to-permanent loans generate fee income as well as net interest income for Cardinal First and are classified as loans held for sale.

CWS provides brokerage and investment services through a contract with Raymond James Financial Services, Inc. Under this contract, CWS financial advisors can offer our customers an extensive range of financial products and services, including estate planning, qualified retirement plans, mutual funds, annuities, life insurance, fixed income and equity securities and equity research and recommendations. CWS's principal source of revenue is the net commissions it earns on the purchases and sales of investment products to its customers.

Wilson/Bennett provides professional investment management of financial assets with asset preservation as the primary goal. Clients include individuals, pension plans and medium sized corporations. Wilson/Bennett utilizes a value oriented investment approach and focuses on large capitalization stocks as well as cash management services. Wilson/Bennett earns fees based upon the market value of its clients' portfolios. During 2013, as part of our planned reorganization of our wealth

3

Table of Contents

management business segment, we will consolidate the Wilson/Bennett entity into CWS. A majority of Wilson/Bennett clients are expected to be serviced on the CWS platform beginning in the first half of 2013.

Cardinal Bank has a trust division that acts as trustee or custodian for client assets and earns fees primarily based upon balances under management. The trust division diversifies the Bank's sources of non-interest income and allows us to provide additional services to our customers. During 2013, we are exiting the third party institutional custody and trustee component of our trust services division due to our limited opportunity to leverage this platform. In addition, as a result of our current plans to reorganize our wealth management business segment, the majority of the remaining personal and commercial trust area of this business will consolidate into CWS.

Growth Strategy

We believe that the strong demographic characteristics of our market and the relative strength of the metropolitan Washington, D.C. area, particularly Northern Virginia, provide a significant opportunity to continue building a successful community-focused banking franchise. We intend to continue to expand our business through internal growth, as well as selective geographic expansion, while maintaining strong asset quality and achieving increasing profitability. The strategy for achieving these objectives includes the following:

Capitalize on the current market conditions. As the banking industry continues to restrict lending based on industry-wide asset quality limitations and capital constraints, we believe we are well positioned to take advantage of this void based on our strong balance sheet. We continue to see opportunities to grow our loan portfolio because the competition is distracted by current market conditions and their credit quality issues. We also continue to benefit from a move towards quality by well established business owners, including multi-generational businesses, seeking the safe and consistent reliable delivery of service that we are able to provide.

Penetrate our existing markets and further improve our branch positioning. We intend to continue to penetrate our existing markets with increased business development efforts through additional experienced bankers in communities that present attractive growth opportunities within Northern Virginia and other markets in the greater Washington, D.C. metropolitan area. We expect to continue to have opportunities to acquire or lease former branch sites from other financial institutions. As we have done in the past, we may acquire additional sites prior to planned branch openings when we believe the sites are attractive and are available on favorable terms. Because the opening of each new branch increases our operating expenses, we intend to stage future branch openings in an effort to minimize the impact of these expenses on our results of operations.

Capitalize on the continued bank consolidation in our market. We anticipate that bank mergers will result in further consolidation in our target market and we intend to capitalize on the dislocation of customers resulting from this consolidation. We believe this consolidation creates opportunities for expanding our branch network, as discussed above, as well as to increase our market share of bank deposits within our target market. We focus on building long term relationships with our clients and communities by providing personalized service from local management teams. We also will continue to explore the possibility of further growth through acquisition in Virginia, the metropolitan Washington, D.C. market, or other areas if we believe that such expansion will strengthen the Company by diversifying our customer base and sources of revenue and be accretive to earnings within a reasonable time frame.

Expand our lending activities. As of December 31, 2012, we have increased our legal lending limit to over $47.3 million as a result of retained earnings and our successful capital raise efforts during 2009. The increase in our legal lending limit allows us to further expand our commercial and real estate

4

Table of Contents

lending activities. It also improves our ability to seek business from larger government contractors, businesses who we believe are conservatively operated and well capitalized residential homebuilders. According to George Mason University's Center for Regional Analysis ("GMU-CRA"), federal procurement outlays in the greater Washington region declined 8.4% from 2010 to 2012. Federal procurement decreased from $80 billion in 2011 to $75.6 billion for 2012. As a result of the scheduled federal budget cuts this Spring 2013, we expect a significant impact to the economy in Greater Washington Metropolitan region. Economic impact could be in the form of a possible increase in unemployment in our region and restricted business development growth as companies adjust to the decreased levels of federal spending, all of which could decrease the growth in certain segments of our loan portfolio. It may also impact the credit quality of a portion of our loan portfolio that is dependent upon revenues from the federal government as a source of repayment. According to Dr. Stephen Fuller of GMU-CRA, procurement funds are expected to fall by about 2.3% to 17.4% in the greater Washington region's economy by 2015. Our goal is to aggressively grow our loan portfolio while maintaining superior asset quality through conservative underwriting practices as we operate in this challenging economic environment.

Continue to recruit experienced bankers. Historically, we have been successful in recruiting senior bankers with experience in, and knowledge of, our market. We believe current market conditions and consolidation will allow us to continue to find bankers who have been displaced or have grown dissatisfied as a result of consolidation. We intend to continue our efforts to recruit seasoned bankers, particularly experienced lenders, who we expect can immediately generate additional loan volume through their existing credit relationships.

Business Segment Operations

We operate in three business segments, commercial banking, mortgage banking and wealth management and trust services. The commercial banking segment includes both commercial and consumer lending and provides customers such products as commercial loans, real estate loans, and other business financing and consumer loans. In addition, this segment provides customers with several choices of deposit products, including demand deposit accounts, savings accounts and certificates of deposit. The mortgage banking segment engages primarily in the origination and acquisition of residential mortgages for sale into the secondary market on a best efforts basis. The wealth management and trust services segment provides investment and financial advisory services to businesses and individuals, including financial planning, retirement/estate planning, trust, estates, custody, investment management, escrows, and retirement plans.

For financial information about the reportable segments, see "Business Segment Operations" in Item 7 below and Note 21 of the notes to the consolidated financial statements in Item 8 below.

Market Area

We consider our primary target market to include the Virginia counties of Arlington, Fairfax, Loudoun, Prince William, and Stafford and the cities of Alexandria, Fairfax, Falls Church, Fredericksburg, Manassas and Manassas Park; Washington, D.C. and Montgomery County in Maryland. In addition to our primary market, we consider the Virginia counties of Spotsylvania, Culpeper and Fauquier and the Maryland county of Prince George's as secondary markets and the remaining Greater Washington Metropolitan area as a tertiary market. We will, however, consider expansion into other areas if we believe such expansion will strengthen the Company by diversifying its customer base and sources of revenue and be accretive to earnings within a reasonable time frame.

Based on estimates released by the U.S. Census Bureau, the population of the greater Washington metropolitan area was approximately 5.58 million people in 2010, the eighth largest statistical area in the country. The median annual household income for this area in 2010 was approximately $84,500,

5

Table of Contents

which makes it one of the wealthiest regions in the country. For 2012, based on estimates released by the Bureau of Labor Statistics of the U.S. Department of Labor, the unemployment rate for the greater Washington metropolitan area was approximately 5.0%, compared to a national unemployment rate of 7.8%. As of June 30, 2012, total deposits in this area were approximately $190 billion as reported by the Federal Deposit Insurance Corporation ("FDIC").

Our headquarters are located in the center of the business district of Fairfax County, Virginia. Fairfax County, with over one million people, is the most populous county in Virginia and the most populous jurisdiction in the Washington, D.C. area. According to the latest U.S. Census Bureau estimates, Fairfax County also has the second highest median household income of any county in the United States of $109,000, surpassed only by its neighbor, Loudoun County with $116,000.

We believe the diversity of our economy, including the stability provided by businesses serving the U.S. Government, provides us with the opportunities necessary to prudently grow our business.

Competition

The greater Washington region is dominated by branches of large regional or national banks headquartered outside of the region. Our market area is a highly competitive, highly branched, banking market. We compete as a financial intermediary with other commercial banks, savings and loan associations, savings banks, credit unions, mortgage banking firms, consumer finance companies, securities brokerage firms, insurance companies, mutual fund groups and other types of financial institutions. George Mason faces significant competition from both traditional financial institutions and other national and local mortgage banking operations.

The competition to acquire deposits and to generate loans, including mortgage loans, is intense, and pricing is important. Many of our competitors are larger and have substantially greater resources and lending limits than we do. In addition, many competitors offer more extensive branch and ATM networks than we currently have. Larger institutions operating in the greater Washington market have access to funding sources at lower costs than are available to us since they have larger and more diverse fund generating capabilities. However, we believe that we have and will continue to be successful in competing in this environment due to an emphasis on a high level of personalized customer service, localized and more responsive decision making, and community involvement.

Of the $190 billion in bank deposits in the greater Washington region at June 30, 2012, approximately 84% were held by banks that are either based outside of the greater Washington region or are operating wholesale banks that generate deposits nationally. Excluding institutions based outside our region, we have grown to the fifth largest financial institution headquartered in the greater Washington region as measured by total deposits. By providing competitive products and more personalized service and being actively involved in our local communities, we believe we can continue to increase our share of this deposit market.

Customers

We believe that the recent and ongoing bank consolidation within Northern Virginia and the greater Washington, D.C. region provides a significant opportunity to build a successful, locally-oriented banking franchise. We also believe that many of the larger financial institutions in our area do not emphasize the high level of personalized service to small and medium-sized commercial businesses, professionals or individual retail customers that we emphasize.

We expect to continue serving these business and professional markets with experienced commercial relationship managers, and we have increased our retail marketing efforts through the expansion of our branch network and development of additional retail products and services. We expanded our deposit market share through aggressive marketing of our First Choice Checking,

6

Table of Contents

President's Club, Chairman's Club, Simply Savings and Monster Money Market relationship products and our Simply Checking product.

Banking Products and Services

Our principal business is to accept deposits from the public and to make loans and other investments. The principal sources of funds for the Bank's loans and investments are demand, time, savings and other deposits, repayments of existing loans, and borrowings. Our principal source of income is interest collected on loans, investment securities and other investments. Non-interest income, which includes among other things deposit and loan fees and service charges, realized and unrealized gains on mortgage banking activities, investment fee income, and management fee income, is the next largest component of our revenues. Our principal expenses are interest expense on deposits and borrowings, employee compensation and benefits, occupancy-related expenses, and other overhead expenses.

The principal business of George Mason, the Bank's primary mortgage banking subsidiary, is to originate residential loans for sale into the secondary market on a best efforts basis. These loans are closed and serviced by George Mason on an interim basis pending their ultimate sale to a permanent investor. The mortgage subsidiary funds these loans through a line of credit from Cardinal Bank and cash available through its own operations. George Mason's income on these loans is generated from the fees it charges its customers, the gains it recognizes upon the sales of loans and the interest income it earns prior to the delivery of the loan to the investor. Costs associated with these loans are primarily comprised of salaries and commissions paid to loan originators and support personnel, interest expense incurred on funds borrowed to hold the loans pending sale and other expenses associated with the origination of the loans. In addition, George Mason generates management fee income by providing specific services to other mortgage banking companies owned by local home builders.

Cardinal First offers a construction-to-permanent loan program. This program provides variable rate financing for customers to construct their residences. Once the home has been completed, the loan converts to fixed rate financing and is sold into the secondary market. These construction-to-permanent loans generate fee income as well as net interest income and are classified as loans held for sale.

The mortgage banking segment's business is both cyclical and seasonal. The cyclical nature of its business is influenced by, among other things, the levels of and trends in mortgage interest rates, national and local economic conditions and consumer confidence in the economy. Historically, the mortgage banking segment has its lowest levels of quarterly loan closings during the first quarter of the year.

Both Cardinal Bank and George Mason are committed to providing high quality products and services to their customers, and have made a significant investment in their core information technology systems. These systems provide the technology that fully automates the branches, processes bank transactions, mortgage originations, other loans and electronic banking, conducts database and direct response marketing, provides cash management solutions, streamlined reporting and reconciliation support.

With this investment in technology, the Bank offers internet-based delivery of products for both individuals and commercial customers. Customers can open accounts, apply for loans, check balances, check account history, transfer funds, pay bills, download account transactions into Quicken™ and Microsoft Money™, and correspond via e-mail with the Bank over the internet. The internet provides an inexpensive way for the Bank to expand its geographic borders and branch activities while providing services offered by larger banks.

We offer a broad array of products and services to our customers. A description of our products and services is set forth below.

7

Table of Contents

Lending

We offer a full range of short to long-term commercial, real estate and consumer lending products and services, which are described in further detail below. We have established target percentage goals for each type of loan to insure adequate diversification of our loan portfolio. These goals, however, may change from time to time as a result of competition, market conditions, employee expertise, and other factors. Commercial and industrial loans, real estate-commercial loans, real estate-construction loans, real estate-residential loans, home equity loans, and consumer loans account for approximately 12%, 46%, 21%, 14%, 6% and 1%, respectively of our loan portfolio at December 31, 2012.

Commercial and Industrial Loans. We make commercial loans to qualified businesses in our market area. Our commercial lending portfolio consists primarily of commercial and industrial loans for the financing of accounts receivable, property, plant and equipment. Our government contract lending group provides secured lending to government contracting firms and businesses based primarily on receivables from the federal government. We also offer Small Business Administration (SBA) guaranteed loans and asset-based lending arrangements to our customers. We are certified as a preferred lender by the SBA, which provides us with much more flexibility in approving loans guaranteed under the SBA's various loan guaranty programs.

Historically, commercial and industrial loans generally have a higher degree of risk than residential mortgage loans. Residential mortgage loans generally are made on the basis of the borrower's ability to repay the loan from his or her salary and other income and are secured by residential real estate, the value of which generally is readily ascertainable. In contrast, commercial loans typically are made on the basis of the borrower's ability to repay the loan from the cash flow from its business and are secured by business assets, such as commercial real estate, accounts receivable, equipment and inventory, the values of which may fluctuate over time and generally cannot be appraised with as much precision as residential real estate. As a result, the availability of funds for the repayment of commercial loans may be substantially dependent upon the commercial success of the business itself.

To manage these risks, our policy is to secure the commercial loans we make with both the assets of the business, which are subject to the risks described above, and other additional collateral and guarantees that may be available. In addition, for larger relationships, we actively monitor certain attributes of the borrower and the credit facility, including advance rate, cash flow, collateral value and other credit factors that we consider appropriate.

Commercial Mortgage Loans. We originate commercial mortgage loans. These loans are primarily secured by various types of commercial real estate, including office, retail, warehouse, industrial and other non-residential types of properties and are made to the owners and/or occupiers of such property. These loans generally have maturities ranging from one to ten years.

Historically, commercial mortgage lending entails additional risk compared with traditional residential mortgage lending. Commercial mortgage loans typically involve larger loan balances concentrated with single borrowers or groups of related borrowers. Additionally, the repayment of loans secured by income-producing properties is typically dependent upon the successful operation of a business or real estate project and thus may be subject, to a greater extent than has historically been the case with residential mortgage loans, to adverse conditions in the commercial real estate market or in the general economy. Our commercial real estate loan underwriting criteria require an examination of debt service coverage ratios, the borrower's creditworthiness and prior credit history, and we generally require personal guarantees or endorsements with respect to these loans. In the loan underwriting process, we also carefully consider the location of the property that will be collateral for the loan.

Loan-to-value ratios for commercial mortgage loans generally do not exceed 80%. We permit loan-to-value ratios of up to 80% if the borrower has appropriate liquidity, net worth and cash flow.

8

Table of Contents

Residential Mortgage Loans. Residential mortgage loans are originated by Cardinal Bank, Cardinal First and George Mason. Our residential mortgage loans consist of residential first and second mortgage loans, residential construction loans and home equity lines of credit and term loans secured by the residences of borrowers. Second mortgage and home equity lines of credit are used for home improvements, education and other personal expenditures. We make mortgage loans with a variety of terms, including fixed, floating and variable interest rates, with maturities ranging from three months to thirty years.

Residential mortgage loans generally are made on the basis of the borrower's ability to repay the loan from his or her salary and other income and are secured by residential real estate, the value of which is generally readily ascertainable. These loans are made consistent with our appraisal and real estate lending policies, which detail maximum loan-to-value ratios and maturities. Residential mortgage loans and home equity lines of credit secured by owner-occupied property generally are made with a loan-to-value ratio of up to 80%. Loan-to-value ratios of up to 90% may be allowed on residential owner-occupied property if the borrower exhibits unusually strong creditworthiness. We generally do not make residential loans which, at the time of inception, have loan-to-value ratios in excess of 90%.

Construction Loans. Our construction loan portfolio consists of single-family residential properties, multi-family properties and commercial projects. Construction lending entails significant additional risks compared with residential mortgage lending. Construction loans often involve larger loan balances concentrated with single borrowers or groups of related borrowers. Construction loans also involve additional risks since funds are advanced while the property is under construction, which property has uncertain value prior to the completion of construction. Thus, it is more difficult to accurately evaluate the total loan funds required to complete a project and related loan-to-value ratios. To reduce the risks associated with construction lending, we limit loan-to-value ratios to 80% of when-completed appraised values for owner-occupied residential or commercial properties and for investor-owned residential or commercial properties. We expect that these loan-to-value ratios will provide sufficient protection against fluctuations in the real estate market to limit the risk of loss. Maturities for construction loans generally range from 12 to 24 months for non-complex residential, non-residential and multi-family properties. Construction loan agreements may include provisions which allow for the payment of contractual interest from an interest reserve. Amounts drawn from an interest reserve increase the amount of the outstanding balance of the construction loan. This is an industry standard practice.

Consumer Loans. Our consumer loans consist primarily of installment loans made to individuals for personal, family and household purposes. The specific types of consumer loans we make include home improvement loans, automobile loans, debt consolidation loans and other general consumer lending.

Consumer loans may entail greater risk than residential mortgage loans, particularly in the case of consumer loans that are unsecured, such as lines of credit, or secured by rapidly depreciable assets, such as automobiles. In such cases, any repossessed collateral for a defaulted consumer loan may not provide an adequate source of repayment of the outstanding loan balance as a result of the greater likelihood of damage, loss or depreciation. The remaining deficiency often does not warrant further substantial collection efforts against the borrower. In addition, consumer loan collections are dependent on the borrower's continuing financial stability, and thus are more likely to be adversely affected by job loss, divorce, illness or personal bankruptcy. Furthermore, the application of various federal and state laws, including federal and state bankruptcy and insolvency laws, may limit the amount that can be recovered on such loans. A loan may also give rise to claims and defenses by a consumer loan borrower against an assignee of such loan, such as the bank, and a borrower may be able to assert against such assignee claims and defenses that it has against the seller of the underlying collateral.

9

Table of Contents

Our policy for consumer loans is to accept moderate risk while minimizing losses, primarily through a careful credit and financial analysis of the borrower. In evaluating consumer loans, we require our lending officers to review the borrower's level and stability of income, past credit history, amount of debt currently outstanding and the impact of these factors on the ability of the borrower to repay the loan in a timely manner. In addition, we require our banking officers to maintain an appropriate differential between the loan amount and collateral value.

We also issue credit cards to certain of our customers. In determining to whom we will issue credit cards, we evaluate the borrower's level and stability of income, past credit history and other factors.

Finally, we make additional loans that are not classified in one of the above categories. In making such loans, we attempt to ensure that the borrower meets our loan underwriting standards.

Loan Participations

From time to time we purchase and sell commercial loan participations to or from other banks within our market area. All loan participations purchased have been underwritten using the Bank's standard and customary underwriting criteria and are in good standing.

Deposits

We offer a broad range of interest-bearing and non-interest-bearing deposit accounts, including commercial and retail checking accounts, money market accounts, individual retirement accounts, regular interest-bearing savings accounts and certificates of deposit with a range of maturity date options. The primary sources of deposits are small and medium-sized businesses and individuals within our target market. Senior management has the authority to set rates within specified parameters in order to remain competitive with other financial institutions in our market area. All deposits are insured by the FDIC up to the maximum amount permitted by law. We have a service charge fee schedule, which is generally competitive with other financial institutions in our market, covering such matters as maintenance fees and per item processing fees on checking accounts, returned check charges and other similar fees.

Courier Services

We offer courier services to our business customers. Courier services permit us to provide the convenience and personalized service that our customers require by scheduling pick-ups of deposits and other banking transactions.

Deposit on Demand

We provide our commercial banking customers electronic deposit capability through our Deposit on Demand product. Business customers who sign up for this service can scan their deposits and send electronic batches of their deposits to the Bank. This product reduces or eliminates the need for businesses with daily deposits and high check volume to visit the Bank and provides the benefit of viewing images of deposited checks.

Internet and Mobile Banking

We believe that there is a strong demand within our market for internet banking and to a much lesser extent telephone banking. These services allow both commercial and retail customers to access detailed account information and execute a wide variety of the banking transactions, including balance transfers and bill payment. We believe that these services are particularly attractive to our customers, as it enables them at any time to conduct their banking business and monitor their accounts. Internet

10

Table of Contents

banking assists us in attracting and retaining customers and encourages our existing customers to consider Cardinal for all of their banking and financial needs.

We offer Cardinal Mobile Banking to our customers. Customers who sign up for this service can access their accounts from any internet-enabled mobile device. Customers can check their balance, view account activity, transfer funds between deposit accounts, and may pay their bill online. Cardinal Mobile Banking is encrypted using the Wireless Transport Layer Security (WTLS) protocol, which provides the highest level of security available today. Additionally, all data that passes between the wireless gateway and Cardinal Bank's web servers is encrypted using Secure Socket Layer (SSL).

Automatic Teller Machines

We have an ATM at each of our branch offices and we make other financial institutions' ATMs available to our customers.

Other Products and Services

We offer other banking-related specialized products and services to our customers, such as travelers' checks, coin counters, wire services, and safe deposit box services. We issue letters of credit for some of our commercial customers, most of which are related to real estate construction loans. We have not engaged in any securitizations of loans.

Credit Policies

Our chief credit officer and senior lending officers are primarily responsible for maintaining both a quality loan portfolio and a strong credit culture throughout the organization. The chief credit officer is responsible for developing and updating our credit policies and procedures, which are approved by the board of directors. The chief credit officer and senior lending officers may make exceptions to these credit policies and procedures as appropriate, but any such exception must be documented and made for sound business reasons.

Credit quality is controlled by the chief credit officer through compliance with our credit policies and procedures. Our risk-decision process is actively managed in a disciplined fashion to maintain an acceptable risk profile characterized by soundness, diversity, quality, prudence, balance and accountability. Our credit approval process consists of specific authorities granted to the lending officers and combinations of lending officers. Loans exceeding a particular lending officer's level of authority, or the combined limit of several officers, are reviewed and considered for approval by an officers' loan committee and, when above a specified amount, by a committee of the Bank's board of directors. Generally, loans of $1,500,000 or more require committee approval. Our policy allows exceptions for very specific conditions, such as loans secured by deposits at our Bank. The chief credit officer works closely with each lending officer at the Bank level to ensure that the business being solicited is of the quality and structure that fits our desired risk profile.

Under our credit policies, we monitor our concentration of credit risk. We have established credit concentration guideline limits for commercial and industrial loans, real estate-commercial loans, real estate-residential loans and consumer purpose loans, which include home equity loans. Furthermore, the Bank has established limits on the total amount of the Bank's outstanding loans to one borrower, all of which are set below legal lending limits.

Loans closed by George Mason and Cardinal First are underwritten in accordance with guidelines established by the various secondary market investors to which George Mason sells its loans.

11

Table of Contents

Brokerage and Asset Management Services

CWS provides brokerage and investment services through an arrangement with Raymond James Financial Services, Inc. Under this arrangement, financial advisors can offer our customers an extensive range of investment products and services, including estate planning, qualified retirement plans, mutual funds, annuities, life insurance, fixed income and equity securities and equity research and recommendations. Through Wilson/Bennett, we also offer asset management services to customers using a value-oriented approach that focuses on large capitalization stocks.

The Bank has a trust division, and services provided by our trust division include trust, estates, custody, investment management, escrows, and retirement plans. The addition of trust services diversifies the Bank's sources of non-interest income and allows us to provide additional services to our customers.

During 2013, we expect to exit the third party institutional custody and trustee component of our trust services division due to our limited opportunity to leverage this platform. In addition, as a result of our current plans to reorganize our wealth management business segment, the majority of the remaining personal and commercial trust area of this business is expected to consolidate into CWS. As part of this wealth management reorganization, we plan to consolidate Wilson/Bennett clients into CWS and begin servicing these clients as part of CWS beginning in the first half of 2013.

Employees

At December 31, 2012, we had 706 full-time equivalent employees. None of our employees are represented by any collective bargaining unit. We believe our relations with our employees are good.

Government Supervision and Regulation

General

As a financial holding company, we are subject to regulation under the Bank Holding Company Act of 1956, as amended, and the examination and reporting requirements of the Board of Governors of the Federal Reserve System. Other federal and state laws govern the activities of our bank subsidiary, including the activities in which it may engage, the investments that it makes, the aggregate amount of loans that it may grant to one borrower, and the dividends it may declare and pay to us. Our bank subsidiary is also subject to various consumer and compliance laws. As a state-chartered bank, the Bank is primarily subject to regulation, supervision and examination by the Bureau of Financial Institutions of the Virginia State Corporation Commission. The Bank and its subsidiaries (George Mason and Cardinal First) also are subject to regulation, supervision and examination by the Federal Deposit Insurance Corporation.

The following description summarizes the more significant federal and state laws applicable to us. To the extent that statutory or regulatory provisions are described, the description is qualified in its entirety by reference to that particular statutory or regulatory provision.

The Bank Holding Company Act

Under the Bank Holding Company Act, we are subject to periodic examination by the Federal Reserve and required to file periodic reports regarding our operations and any additional information that the Federal Reserve may require. Our activities at the bank holding company level are limited to:

- •

- banking, managing or controlling banks;

- •

- furnishing services to or performing services for our subsidiaries; and

12

Table of Contents

- •

- engaging in other activities that the Federal Reserve has determined by regulation or order to be so closely related to banking as to be a proper incident to these activities.

Some of the activities that the Federal Reserve Board has determined by regulation to be closely related to the business of a bank holding company include making or servicing loans and specific types of leases, performing specific data processing services and acting in some circumstances as a fiduciary or investment or financial adviser.

With some limited exceptions, the Bank Holding Company Act requires every bank holding company to obtain the prior approval of the Federal Reserve before:

- •

- acquiring substantially all the assets of any bank; and

- •

- acquiring direct or indirect ownership or control of any voting shares of any bank if after such acquisition it would own or control more than 5% of the voting shares of such bank (unless it already owns or controls the majority of such shares), or merging or consolidating with another bank holding company.

In addition, and subject to some exceptions, the Bank Holding Company Act and the Change in Bank Control Act, together with their regulations, require Federal Reserve approval prior to any person or company acquiring 25% or more of any class of voting securities of the bank holding company. Prior notice to the Federal Reserve is required before a person acquires 10% or more, but less than 25%, of any class of voting securities and if the institution has registered securities under Section 12 of the Securities Exchange Act of 1934 or no other person owns a greater percentage of that class of voting securities immediately after the transaction.

In November 1999, Congress enacted the Gramm-Leach-Bliley Act ("GLBA"), which made substantial revisions to the statutory restrictions separating banking activities from other financial activities. Under the GLBA, bank holding companies that are well-capitalized and well-managed and meet other conditions can elect to become "financial holding companies." As financial holding companies, they and their subsidiaries are permitted to acquire or engage in previously impermissible activities, such as insurance underwriting and securities underwriting and distribution. In addition, financial holding companies may also acquire or engage in certain activities in which bank holding companies are not permitted to engage in, such as travel agency activities, insurance agency activities, merchant banking and other activities that the Federal Reserve determines to be financial in nature or complementary to these activities. Financial holding companies continue to be subject to the overall oversight and supervision of the Federal Reserve, but the GLBA applies the concept of functional regulation to the activities conducted by subsidiaries. For example, insurance activities would be subject to supervision and regulation by state insurance authorities. We became a financial holding company in 2004.

Payment of Dividends

Regulators have indicated that financial holding companies should generally pay dividends only if the organization's net income available to common shareholders is sufficient to fully fund the dividends, and the prospective rate of earnings retention appears consistent with the organization's capital needs, asset quality and overall financial condition.

We are a legal entity separate and distinct from Cardinal Bank, CWS, Wilson/Bennett, and Cardinal Statutory Trust I. Virtually all of our cash revenues will result from dividends paid to us by our bank subsidiary and interest earned on short term investments. Our bank subsidiary is subject to laws and regulations that limit the amount of dividends that it can pay. Under Virginia law, a bank may not declare a dividend in excess of its accumulated retained earnings. Additionally, our bank subsidiary may declare a dividend out of undivided earnings, but not if the total amount of all dividends, including the proposed dividend, declared by the bank in any calendar year exceeds the total of the bank's

13

Table of Contents

retained net income of that year to date, combined with its retained net income of the two preceding years, unless the dividend is approved by the FDIC. Our bank subsidiary may not declare or pay any dividend if, after making the dividend, the bank would be "undercapitalized," as defined in the banking regulations.

The FDIC and the state have the general authority to limit the dividends paid by insured banks if the payment is deemed an unsafe and unsound practice. Both the state and the FDIC have indicated that paying dividends that deplete a bank's capital base to an inadequate level would be an unsound and unsafe banking practice.

In addition, we are subject to certain regulatory requirements to maintain capital at or above regulatory minimums. These regulatory requirements regarding capital affect our dividend policies. Our regulators also may restrict our ability to repurchase securities.

Insurance of Accounts, Assessments and Regulation by the FDIC

The deposits of our bank subsidiary are insured by the FDIC up to the limits set forth under applicable law. The deposits of our bank subsidiary are subject to the deposit insurance assessments of the Deposit Insurance Fund, or "DIF", of the FDIC.

The FDIC has implemented a risk-based deposit insurance assessment system under which the assessment rate for an insured institution may vary according to regulatory capital levels of the institution and other factors, including supervisory evaluations. In addition to being influenced by the risk profile of the particular depository institution, FDIC premiums are also influenced by the size of the FDIC insurance fund in relation to total deposits in FDIC insured banks. The FDIC has authority to impose special assessments.

The FDIC is required to maintain a designated minimum ratio of the DIF to insured deposits in the United States. In July 2010, the Dodd Frank Wall Street Reform and Consumer Protection Act (the "Financial Reform Act") was signed into law. The Financial Reform Act requires the FDIC to achieve a DIF ratio of at least 1.35 percent by September 30, 2020. The FDIC has also adopted new regulations that establish a long-term target DIF ratio of greater than two percent. As a result of the ongoing instability in the economy and the failure of other U.S. depository institutions, the DIF ratio is currently below the required targets and the FDIC has adopted a restoration plan that will result in substantially higher deposit insurance assessments primarily for depository institutions with more than $10 billion in assets over the coming years. Deposit insurance assessment rates are subject to change by the FDIC and will be impacted by the overall economy and the stability of the banking industry as a whole.

Pursuant to the Financial Reform Act, FDIC insurance coverage limits were permanently increased to $250,000 per customer.

The Financial Reform Act also changed the methodology for calculating deposit insurance assessments by changing the assessment base from the amount of an insured depository institution's domestic deposits to its total assets minus tangible equity. The new regulation implementing revisions to the assessment system mandated by the Financial Reform Act was effective April 1, 2011 and was reflected in the June 30, 2011 FDIC fund balance and the invoices for assessments due September 30, 2011. As a result of the new regulations, our annual deposit insurance assessments are higher than before the financial crisis. While the burden on replenishing the DIF will be placed primarily on institutions with assets of greater than $10 billion, any future increases in required deposit insurance premiums or other bank industry fees could have a significant adverse impact on our financial condition and results of operations.

14

Table of Contents

The FDIC is authorized to prohibit any insured institution from engaging in any activity that the FDIC determines by regulation or order to pose a serious threat to the DIF. Also, the FDIC may initiate enforcement actions against banks, after first giving the institution's primary regulatory authority an opportunity to take such action. The FDIC may terminate the deposit insurance of any depository institution if it determines, after a hearing, that the institution has engaged or is engaging in unsafe or unsound practices, is in an unsafe or unsound condition to continue operations, or has violated any applicable law, regulation, order or any condition imposed in writing by the FDIC. It also may suspend deposit insurance temporarily during the hearing process for the permanent termination of insurance, if the institution has no tangible capital. If deposit insurance is terminated, the deposits at the institution at the time of termination, less subsequent withdrawals, shall continue to be insured for a period from six months to two years, as determined by the FDIC. We are unaware of any existing circumstances that could result in termination of any of our bank subsidiary's deposit insurance.

Consumer Financial Protection Bureau. The Financial Reform Act created a new, independent federal agency, the Consumer Financial Protection Bureau ("CFPB") having broad rulemaking, supervisory and enforcement powers under various federal consumer financial protection laws, including the Equal Credit Opportunity Act, Truth in Lending Act, Real Estate Settlement Procedures Act, Fair Credit Reporting Act, Fair Debt Collection Act, the Consumer Financial Privacy provisions of the Gramm-Leach-Bliley Act and certain other statutes. The CFPB has examination and primary enforcement authority with respect to depository institutions with $10 billion or more in assets. Smaller institutions, including the Bank, are subject to rules promulgated by the CFPB but continue to be examined and supervised by federal banking regulators for consumer compliance purposes. The CFPB has authority to prevent unfair, deceptive or abusive practices in connection with the offering of consumer financial products. The Financial Reform Act authorizes the CFPB to establish certain minimum standards for the origination of residential mortgages including a determination of the borrower's ability to repay. In addition, the Financial Reform Act will allow borrowers to raise certain defenses to foreclosure if they receive any loan other than a "qualified mortgage" as defined by the CFPB. The Financial Reform Act permits states to adopt consumer protection laws and standards that are more stringent than those adopted at the federal level and, in certain circumstances, permits state attorneys general to enforce compliance with both the state and federal laws and regulations.

Capital Requirements

Each of the FDIC and the Federal Reserve Board has issued risk-based and leverage capital guidelines applicable to banking organizations that it supervises. Under the risk-based capital requirements, we and our bank subsidiary are each generally required to maintain a minimum ratio of total capital to risk-weighted assets (including specific off-balance sheet activities, such as standby letters of credit) of 8%. At least half of the total capital must be composed of "Tier 1 Capital," which is defined as common equity, retained earnings, qualifying perpetual preferred stock and minority interests in common equity accounts of consolidated subsidiaries, less certain intangibles. The remainder may consist of "Tier 2 Capital", which is defined as specific subordinated debt, some hybrid capital instruments and other qualifying preferred stock and a limited amount of the loan loss allowance and pretax net unrealized holding gains on certain equity securities. In addition, each of the federal banking regulatory agencies has established minimum leverage capital requirements for banking organizations. Under these requirements, banking organizations must maintain a minimum ratio of Tier 1 capital to adjusted average quarterly assets equal to 3% to 5%, subject to federal bank regulatory evaluation of an organization's overall safety and soundness. In summary, the capital measures used by the federal banking regulators are:

- •

- Total Risk-Based Capital ratio, which is the total of Tier 1 Risk-Based Capital (which includes common shareholders' equity, trust preferred securities, minority interests and qualifying preferred stock, less goodwill and other adjustments) and Tier 2 Capital (which includes

15

Table of Contents

preferred stock not qualifying as Tier 1 capital, mandatory convertible debt, limited amounts of subordinated debt, other qualifying term debt and the allowance for loan losses up to 1.25 percent of risk-weighted assets and other adjustments) as a percentage of total risk-weighted assets

- •

- Tier 1 Risk-Based Capital ratio (Tier 1 capital divided by total risk-weighted assets), and

- •

- the Leverage ratio (Tier 1 capital divided by adjusted average total assets).

Under these regulations, a bank will be:

- •

- "well capitalized" if it has a Total Risk-Based Capital ratio of 10% or greater, a Tier 1 Risk-Based Capital ratio of 6% or greater, a Leverage ratio of 5% or greater, and is not subject to any written agreement, order, capital directive, or prompt corrective action directive by a federal bank regulatory agency to meet and maintain a specific capital level for any capital measure

- •

- "adequately capitalized" if it has a Total Risk-Based Capital ratio of 8% or greater, a Tier 1 Risk-Based Capital ratio of 4% or greater, and a Leverage ratio of 4% or greater (or 3% in certain circumstances) and is not well capitalized

- •

- "undercapitalized" if it has a Total Risk-Based Capital ratio of less than 8%, a Tier 1 Risk-Based Capital ratio of less than 4% (or 3% in certain circumstances), or a Leverage ratio of less than 4% (or 3% in certain circumstances)

- •

- "significantly undercapitalized" if it has a Total Risk-Based Capital ratio of less than 6%, a Tier 1 Risk-Based Capital ratio of less than 3%, or a Leverage ratio of less than 3%, or

- •

- "critically undercapitalized" if its tangible equity is equal to or less than 2% of tangible assets.

The risk-based capital standards of each of the FDIC and the Federal Reserve Board explicitly identify concentrations of credit risk and the risk arising from non-traditional activities, as well as an institution's ability to manage these risks, as important factors to be taken into account by the agency in assessing an institution's overall capital adequacy. The capital guidelines also provide that an institution's exposure to a decline in the economic value of its capital due to changes in interest rates be considered by the agency as a factor in evaluating a banking organization's capital adequacy.

The FDIC may take various corrective actions against any undercapitalized bank and any bank that fails to submit an acceptable capital restoration plan or fails to implement a plan acceptable to the FDIC. These powers include, but are not limited to, requiring the institution to be recapitalized, prohibiting asset growth, restricting interest rates paid, requiring prior approval of capital distributions by any financial holding company that controls the institution, requiring divestiture by the institution of its subsidiaries or by the holding company of the institution itself, requiring new election of directors, and requiring the dismissal of directors and officers. We are considered "well-capitalized" at December 31, 2012 and, in addition, our bank subsidiary maintained sufficient capital to remain in compliance with capital requirements and is considered "well-capitalized" at December 31, 2012.

The Financial Reform Act contains a number of provisions dealing with capital adequacy of insured depository institutions and their holding companies, which may result in more stringent capital requirements. Under the Collins Amendment to the Financial Reform Act, federal regulators have been directed to establish minimum leverage and risk-based capital requirements for, among other entities, bank holding companies on a consolidated basis. These minimum requirements cannot be less than the generally applicable leverage and risk-based capital requirements established for insured depository institutions nor quantitatively lower than the leverage and risk-based capital requirements established for insured depository institutions that were in effect as of July 21, 2010. These requirements in effect create capital level floors for bank holding companies similar to those in place

16

Table of Contents

currently for insured depository institutions. The Collins Amendment also excludes trust preferred securities issued after May 19, 2010 from being included in Tier 1 capital unless the issuing company is a bank holding company with less than $500 million in total assets. Trust preferred securities issued prior to that date will continue to count as Tier 1 capital for bank holding companies with less than $15 billion in total assets, and such securities will be phased out of Tier 1 capital treatment for bank holding companies with over $15 billion in total assets over a three-year period beginning in 2013. Accordingly, our trust preferred securities will continue to qualify as Tier 1 capital.

Proposed Changes in Capital Requirements. In June 2012, the Federal Reserve, the FDIC and the OCC jointly issued proposed rules that would revise the risk-based and leverage capital requirements and the method for calculating risk-weighted assets to be consistent with the agreements reached by the Basel Committee on Banking Supervision in "Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems" ("Basel III") and certain provisions of the Financial Reform Act. The proposed rules would apply to all depository institutions, top-tier bank holding companies with total consolidated assets of $500 million or more, and top-tier savings and loan holding companies ("banking organizations").

Among other things, the proposed rules establish a new common equity tier 1 ("CET1") minimum capital requirement, introduce a "capital conservation buffer" and raise minimum risk-based capital requirements. Basel III establishes the CET1 to risk-weighted assets to 4.5%, and a capital conservation buffer of an additional 2.5%, raising the target CET1 to risk-weighted assets ratio to 7%. It requires banks to maintain a minimum ratio of Tier 1 capital to risk weighted assets of at least 6.0%, plus the capital conservation buffer effectively resulting in Tier 1 capital ratio of 8.5%. Basel III increases the minimum total capital ratio to 8.0% plus the capital conservation buffer, increasing the minimum total capital ratio to 10.5%. Institutions that do not maintain the required capital buffer would be subject to progressively more stringent limitations on the percentage of earnings that can be paid out in dividends or used for stock repurchases and on the payment of discretionary bonuses to senior executive management. Basel III also introduces a non-risk adjusted tier 1 leverage ratio of 3%, based on a measure of total exposure rather than total assets, and new liquidity standards. Additionally, the U.S. implementation of Basel III contemplates that, for banking organizations with less than $15 billion in assets, the ability to treat trust preferred securities as tier 1 capital would be phased out over a ten-year period.

The proposed rules also introduce new methodologies for determining risk-weighted assets, including higher risk weightings (150%) to exposures that are more than 90 days past due or are on nonaccrual status and certain commercial real estate facilities that finance the acquisition, development or construction of real property. The proposed rules also require unrealized gains and losses on certain securities holdings to be included for purposes of calculating regulatory capital requirements. The proposed rules indicate that the final rule would become effective on January 1, 2013, and the changes set forth in the final rules will be phased in from January 1, 2013 through January 1, 2019. However, the regulatory agencies have recently indicated that, due to the volume of public comments received, the final rule would not be in effect on January 1, 2013 and implementation has been delayed indefinitely.

Other Safety and Soundness Regulations

There are significant obligations and restrictions imposed on financial holding companies and their depository institution subsidiaries by federal law and regulatory policy that are designed to reduce potential loss exposure to the depositors of such depository institutions and to the FDIC insurance fund in the event that the depository institution is insolvent or is in danger of becoming insolvent. These obligations and restrictions are not for the benefit of investors. Regulators may pursue an administrative action against any financial holding company or bank which violates the law, engages in an unsafe or unsound banking practice, or which is about to engage in an unsafe or unsound banking

17

Table of Contents

practice. The administrative action could take the form of a cease and desist proceeding, a removal action against the responsible individuals or, in the case of a violation of law or unsafe and unsound banking practice, a civil monetary penalty action. A cease and desist order, in addition to prohibiting certain action, could also require that certain actions be undertaken. Under the Financial Reform Act and longstanding policies of the Federal Reserve Board, we are required to serve as a source of financial strength to our subsidiary depository institution and to commit resources to support the Bank in circumstances where we might not do so otherwise.

The Bank Secrecy Act

Under the Bank Secrecy Act ("BSA"), a financial institution is required to have systems in place to detect certain transactions, based on the size and nature of the transaction. Financial institutions are generally required to report cash transactions involving more than $10,000 to the United States Treasury. In addition, financial institutions are required to file Suspicious Activity Reports for transactions that involve more than $5,000 and which the financial institution knows, suspects or has reason to suspect, involves illegal funds, is designed to evade the requirements of the BSA or has no lawful purpose. The USA PATRIOT Act of 2001, enacted in response to the September 11, 2001 terrorist attacks, requires bank regulators to consider a financial institution's compliance with the BSA when reviewing applications from a financial institution. As part of its BSA program, the USA PATRIOT Act of 2001 also requires a financial institution to follow customer identification procedures when opening accounts for new customers and to review U.S. government-maintained lists of individuals and entities that are prohibited from opening accounts at financial institutions.

Monetary Policy

The commercial banking business is affected not only by general economic conditions but also by the monetary policies of the Federal Reserve Board. The instruments of monetary policy employed by the Federal Reserve Board include open market operations in United States government securities, changes in the discount rate on member bank borrowings and changes in reserve requirements against deposits held by federally insured banks. The Federal Reserve Board's monetary policies have had a significant effect on the operating results of commercial banks in the past and are expected to continue to do so in the future. In view of changing conditions in the national and international economy and in the money markets, as well as the effect of actions by monetary and fiscal authorities, including the Federal Reserve System, no prediction can be made as to possible future changes in interest rates, deposit levels, loan demand or the business and earnings of our bank subsidiary, its subsidiary, or any of our other subsidiaries.

Federal Reserve System

In 1980, Congress enacted legislation that imposed reserve requirements on all depository institutions that maintain transaction accounts or non-personal time deposits. NOW accounts and demand deposit accounts that permit payments or transfers to third parties fall within the definition of transaction accounts and are subject to these reserve requirements. Effective January 1, 2013, the first $12.4 million of balances will be exempt from reserve requirements. A 3% reserve ratio will be assessed on net transaction account balances over $12.4 million to and including $79.5 million. A 10% reserve ratio will be applied to amounts in net transaction account balances in excess of $79.5 million. These percentages are subject to adjustment by the Federal Reserve Board. Because required reserves must be maintained in the form of vault cash or in a noninterest-bearing account at, or on behalf of, a Federal Reserve Bank, the effect of the reserve requirement is to reduce the amount of our interest-earning assets. Beginning October 2008, the Federal Reserve Banks pay financial institutions interest on their required reserve balances and excess funds deposited with the Federal Reserve. The interest rate paid is the targeted federal funds rate.

18

Table of Contents

Transactions with Affiliates

Transactions between banks and their affiliates are governed by Sections 23A and 23B of the Federal Reserve Act. An affiliate of a bank is any bank or entity that controls, is controlled by or is under common control with such bank. Generally, Sections 23A and 23B (i) limit the extent to which the bank or its subsidiaries may engage in "covered transactions" with any one affiliate to an amount equal to 10% of such institution's capital stock and surplus, and maintain an aggregate limit on all such transactions with affiliates to an amount equal to 20% of such capital stock and surplus, and (ii) require that all such transactions be on terms substantially the same as, or at least as favorable to those that, the bank has provided to a non-affiliate. Certain covered transactions also must be adequately secured by eligible collateral. The term "covered transaction" includes the making of loans, purchase of assets, issuance of a guarantee and similar other types of transactions. Section 23B applies to "covered transactions" as well as sales of assets and payments of money to an affiliate. These transactions must also be conducted on terms substantially the same as, or at least favorable to those that, the bank has provided to non-affiliates.

The Financial Reform Act also provides that banks may not "purchase an asset from, or sell an asset to" a bank insider (or their related interests) unless (i) the transaction is conducted on market terms between the parties, and (ii) if the proposed transaction represents more than 10 percent of the capital stock and surplus of the bank, it has been approved in advance by a majority of the bank's non-interested directors.

Loans to Insiders

The Federal Reserve Act and related regulations impose specific restrictions on loans to directors, executive officers and principal shareholders of banks. Under Section 22(h) of the Federal Reserve Act, loans to a director, an executive officer and to a principal shareholder of a bank, and to entities controlled by any of the foregoing, may not exceed, together with all other outstanding loans to such person and entities controlled by such person, the bank's loan-to-one borrower limit. Loans in the aggregate to insiders and their related interests as a class may not exceed two times the bank's unimpaired capital and unimpaired surplus until the bank's total assets equal or exceed $100,000,000, at which time the aggregate is limited to the bank's unimpaired capital and unimpaired surplus. Section 22(h) also prohibits loans above amounts prescribed by the appropriate federal banking agency to directors, executive officers and principal shareholders of a bank or bank holding company, and to entities controlled by such persons, unless such loan is approved in advance by a majority of the board of directors of the bank with any "interested" director not participating in the voting. The FDIC has prescribed the aggregate loan amount to such person for which prior board of director approval is required, as being the greater of $25,000 or 5% of capital and surplus (up to $500,000). Section 22(h) requires that loans to directors, executive officers and principal shareholders be made on terms and underwriting standards substantially the same as offered in comparable transactions to other persons.

Community Reinvestment Act

Under the Community Reinvestment Act and related regulations, depository institutions have an affirmative obligation to assist in meeting the credit needs of their market areas, including low and moderate-income areas, consistent with safe and sound banking practice. The Community Reinvestment Act requires the adoption by each institution of a Community Reinvestment Act statement for each of its market areas describing the depository institution's efforts to assist in its community's credit needs. Depository institutions are periodically examined for compliance with the Community Reinvestment Act and are periodically assigned ratings in this regard. Banking regulators consider a depository institution's Community Reinvestment Act rating when reviewing applications to establish new branches, undertake new lines of business, and/or acquire part or all of another depository institution.

19

Table of Contents

An unsatisfactory rating can significantly delay or even prohibit regulatory approval of a proposed transaction by a financial holding company or its depository institution subsidiaries.

GLBA and federal bank regulators have made various changes to the Community Reinvestment Act. Among other changes, Community Reinvestment Act agreements with private parties must be disclosed and annual reports must be made to a bank's primary federal regulator. A financial holding company or any of its subsidiaries will not be permitted to engage in new activities authorized under the GLBA if any bank subsidiary received less than a "satisfactory" rating in its latest Community Reinvestment Act examination.

Consumer Laws Regarding Fair Lending

In addition to the Community Reinvestment Act described above, other federal and state laws regulate various lending and consumer aspects of our business. Governmental agencies, including the Department of Housing and Urban Development, the Federal Trade Commission and the Department of Justice, have become concerned that prospective borrowers may experience discrimination in their efforts to obtain loans from depository and other lending institutions. These agencies have brought litigation against depository institutions alleging discrimination against borrowers. Many of these suits have been settled, in some cases for material sums of money, short of a full trial.

These governmental agencies have clarified what they consider to be lending discrimination and have specified various factors that they will use to determine the existence of lending discrimination under the Equal Credit Opportunity Act and the Fair Housing Act, including evidence that a lender discriminated on a prohibited basis, evidence that a lender treated applicants differently based on prohibited factors in the absence of evidence that the treatment was the result of prejudice or a conscious intention to discriminate, and evidence that a lender applied an otherwise neutral non-discriminatory policy uniformly to all applicants, but the practice had a discriminatory effect, unless the practice could be justified as a business necessity.