UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______.

Commission File Number 000-30715

CoSine Communications, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 94-3280301 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification Number) |

| | |

560 South Winchester Blvd., Suite 500 San Jose, California | 95128 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number including area code:

(408) 236-7518

Securities Registered Pursuant to Section 12(b) of the Act:

None

Securities Registered Pursuant to Section 12(g) of the Act:

Common Stock, $.0001 Par Value

(Title of each class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer x

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes x No o

The aggregate market value of the voting and non voting common equity held by non-affiliates of the Registrant was $10,535,817 based on the number of shares held by non-affiliates as of March 1, 2007, and based on the reported last sale price of common stock on June 30, 2006, which is the last business day of the Registrant’s most recently completed second fiscal quarter. Shares of stock held by officers, directors and 5 percent or more stockholders have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 1, 2007, there were 10,090,635 shares of the Registrant’s Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for our 2007 Annual Meeting of Shareholders are incorporated into Part III of this

Form 10-K.

COSINE COMMUNICATIONS, INC.

FORM 10-K

Year Ended December 31, 2006

TABLE OF CONTENTS

| | | Page |

Part I |

| Item 1. | Business | 3 |

| Item 1A. | Risk Factors | 6 |

| Item 1B. | Unresolved Staff Comments | 10 |

| Item 2. | Properties | 10 |

| Item 3. | Legal Proceedings | 10 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 10 |

Part II |

| Item 5. | Market for Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities | 11 |

| Item 6. | Selected Financial Data | 14 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 15 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 26 |

| Item 8. | Financial Statements and Supplementary Data | 28 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 50 |

| Item 9A. | Controls and Procedures | 50 |

| Item 9B. | Other Information | 50 |

Part III |

| Item 10. | Directors, Executive Officers and Corporate Governance | 50 |

| Item 11. | Executive Compensation | 51 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 51 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 51 |

| Item 14. | Principal Accountant Fees and Services | 51 |

Part IV |

| Item 15. | Exhibits and Financial Statement Schedules | 51 |

| | Signatures | 53 |

| | Exhibit Index | 55 |

SAFE HARBOR STATEMENT UNDER

PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

This Annual Report on Form 10-K contains forward-looking statements. We use words such as "anticipate," "believe," "plan," "expect," "future," "intend" and similar expressions to identify forward-looking statements. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, failure to achieve revenue growth and profitability, our ability to identify and acquire new business operations, the time and costs required to identify and acquire new business operations, management and board interest in and distraction due to identifying and acquiring new business operations, and the reactions, either positive or negative, of investors and others to our strategic direction and to any specific business opportunity selected by us, all as are discussed in more detail in the section entitled "Risk Factors" on pages 6 to 9 of this report, as well as the other risk factors discussed in that section. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s opinions only as of the date hereof. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. Readers should carefully review the risk factors described in other documents that we file from time to time with the Securities and Exchange Commission, including the Quarterly Reports on Form 10-Q that we file in fiscal year 2007.

PART I

Overview

CoSine Communications, Inc. ("CoSine" or the "Company," which may be referred to as "we," "us" or "our") was incorporated in California on April 14, 1997 and in August 2000 was reincorporated in the State of Delaware. We were a provider of carrier network equipment products and services until the fourth quarter of fiscal year 2004 during which time we discontinued our product lines, took actions to lay-off most of our employees, terminated contract manufacturing arrangements, contractor and consulting arrangements and various facility leases, and sold, scrapped or wrote-off our inventory, property and equipment. From the fourth quarter of fiscal year 2004 through December 31, 2006, our business consisted primarily of a customer support capability for our discontinued products provided by a third party. In March 2006, we sold the rights to our patent portfolio, and in November 2006, we sold the remaining intellectual property rights to our carrier network equipment products and services. We terminated all customer service operations effective December 31, 2006 and do not intend to offer customer support services for our discontinued products in the future. We continue to execute our redeployment strategy, whereby we plan to identify and acquire one or more new business operations with existing or prospective taxable earnings that can be offset by use of our net operating loss carry-forwards (“NOLs”).

Business

On July 29, 2004, we announced that we were exploring various strategic alternatives and that we had hired an investment bank as our financial advisor, which had been first retained in May 2003.

Beginning in September 2004 and continuing through December 2004, we laid-off most of our employees, took actions to reduce our operating expenses and conserve our cash, notified our existing customers that our products had been formally discontinued and offered existing customers the opportunity to place “lifetime buy” orders to support their platform transition plans, negotiated transition support plans for our customers, terminated contract manufacturing arrangements, contractor and consulting arrangements, initiated liquidation procedures for certain of our foreign operations and facility leases and completed the sale, scrap or write-off of our inventory, property and equipment.

On January 7, 2005, we entered into an Agreement and Plan of Merger with Tut Systems, Inc. The merger was terminated on May 16, 2005.

On June 10, 2005, we reported in our Current Report on Form 8-K filed with the Securities and Exchange Commission that our stock would be de-listed from the Nasdaq National Market System pursuant to Nasdaq Marketplace Rules 4300 and 4330(a)(3). Our stock was de-listed on June 16, 2005 and now trades in the over the counter market and is quoted on the Pink Sheets Electronic Quotation Service under the symbol “COSN.PK.”

In July 2005, we completed a comprehensive review of strategic alternatives, including a sale of the Company, a sale or licensing of intellectual property, a redeployment of our assets into new business ventures, or a winding-up and liquidation of the business and a return of capital. The board of directors approved a plan to enhance stockholder value by redeploying our existing assets and resources to identify and acquire one or more new business operations, while continuing to support our existing customers and continuing to offer our intellectual property for license or sale. Our redeployment strategy involves the acquisition of one or more operating businesses with existing or prospective taxable earnings that can be offset by use of our net operating loss carry-forwards (“NOLs”). No candidate for acquisition has yet been identified, and no assurance can be given that we will find suitable candidates, and if we do, that we will be able to utilize our existing NOLs.

In implementing the redeployment strategy, on July 25, 2005 Jack L. Howard was elected to fill a vacancy created by the resignation of R. David Spreng, the managing general partner of Crescendo Ventures Management, LLC. Mr. Spreng resigned upon the sale of the shares of our common stock controlled by Crescendo Ventures Management, LLC to Steel Partners II, L.P. Mr. Howard holds representative positions with Steel Partners II, L.P. Steel Partners II, L.P., Mr. Howard and WHX CS Corp., a wholly owned subsidiary of WHX Corporation of which Steel Partners II, L.P. is a majority stockholder, currently own or control, in the aggregate, approximately 45% of our outstanding shares of common stock.

On September 1, 2005, we entered into a stockholders rights plan which provides for a dividend distribution of one preferred share purchase right for each outstanding share of our common stock which, when exercisable, would allow its holder to purchase from us one one-hundredth of a share of our Series A Junior Participating Preferred Stock, par value $0.0001, for a purchase price of $3.00. Each fractional share of this preferred stock would give the stockholder approximately the same dividend, voting and liquidation rights as does one share of our common stock. The purchase rights become exercisable after the acquisition or attempted acquisition of 5% or more of our outstanding common stock without the prior approval of our board of directors. The dividend was paid to our stockholders of record at the close of business on September 12, 2005. Our board of directors adopted the stockholders rights plan to protect stockholder value by protecting our stockholders from coercive takeover practices or takeover bids that are inconsistent with their best interests, and by protecting our ability to carry forward our NOLs.

At our 2005 Annual Meeting of Stockholders, the stockholders approved two amendments to our Second Amended and Restated Certificate of Incorporation. The first amendment restricts certain acquisitions of our securities in order to help assure the preservation of our NOLs. Although the transfer restrictions imposed on our securities is intended to reduce the likelihood of an impermissible ownership change, no assurance can be given that such restrictions would prevent all transfers that would result in an impermissible ownership change. This amendment generally restricts and requires prior approval of our board of directors of direct and indirect acquisitions of our equity securities if such an acquisition will affect the percentage of our capital stock that is treated as owned by a 5% stockholder. The restrictions will generally only affect persons trying to acquire a significant interest in our common stock. The second amendment to our Second Amended and Restated Certificate of Incorporation at our 2005 Annual Meeting de-classified our board of directors providing for an annual election of all our directors.

In March 2006, we sold the rights to our patent portfolio and, in November 2006, the rights to the intellectual property related to our carrier networking products and services. At December 31, 2006, we ceased all customer service operations.

We are continuing to seek to redeploy our existing resources to identify and acquire one or more new business operations with existing or prospective taxable earnings that can be offset by use of our NOLs.

Prior Business

Prior to and during the period ended September 30, 2004, we developed, marketed and sold a communications platform referred to as our IP Service Delivery Platform. Our product was designed to enable carrier network service providers to rapidly deliver a portfolio of communication services to business and consumer customers. We marketed our IP Service Delivery Platform through our direct sales force and through resellers to network service providers in Asia, Europe and North America.

During this period, the market for our IP Service Delivery Platform had been in the early stages of development, and the volume and timing of orders was difficult to predict. A customer’s decision to purchase our platform typically involved a significant commitment of its resources and a lengthy evaluation, testing and product qualification process. The long sales cycle and the timing of our customers’ rollout of services made possible by our platform, which affected repeat business, caused our revenue and operating results to vary significantly and unexpectedly from quarter to quarter and constrained our ability to secure new customers. We did not generate sufficient revenue to fund our communications platform product operations and were unable to increase our revenue in order to reduce our cash consumption and remain a viable and competitive supplier of communications platform products. We formally discontinued our communications platform products in fiscal year 2004 and ceased all our related customer support services as of December 31, 2006.

Products, Services and Technology

Prior to our announcement on September 8, 2004 that we were discontinuing sale of our products, we were a supplier of carrier network equipment which we referred to as our IP Service Delivery Platform. Our IP Service Delivery Platform consisted of hardware elements: a chassis, including our IPSX 9500 and IPSX 3500 Service Processing Switches, and sub-systems known as our IPSGs; and software components consisting of our InVision and InGage software. We formally discontinued our IP Service Delivery Platform in fiscal year 2004, sold the rights to our patent portfolio in March 2006, sold the remaining rights to our carrier network intellectual property in November 2006 and ceased all our related customer support services as of December 31, 2006.

Customers

During the year ended December 31, 2006, we recognized revenue from seven customers. Sprint, AT&T and Rogers Telecom accounted for 58%, 19% and 11% of our revenue, respectively. Geographically, our revenue was distributed as follows: North America 89% and Europe 11% (See Note 1 of the Notes to Consolidated Financial Statements). A small number of customers accounted for a substantial portion of our revenues, and the loss of any one customer would have a material impact on our results of operations. At December 31, 2006, we had no customers.

Sales and Marketing

We ceased all sales and marketing activities in September 2004. We had no sales and marketing employees at December 31, 2006.

Customer Service and Support

We provided transition support services to our existing customers through December 31, 2006, at which time we ceased providing customer support services. Our service and support operations were conducted by a third party contractor, and we had no employees in customer service and support at December 31, 2006.

Research and Development

We ceased all research and development activities in September 2004, other than to offer our existing customers transition support services, as provided by a third party contractor through December 31, 2006. At December 31, 2006, we had no employees in research and development.

Our research and development expenses, including non-cash charges related to equity issuances, totaled nil, $0.1 million and $15.1 million for the years ended December 31, 2006, 2005 and 2004, respectively.

Manufacturing

We ceased all manufacturing activities in December 2004 and had no employees in manufacturing at December 31, 2006.

Backlog

Historically, our backlog has included purchase orders from customers with approved credit status, representing products and services we planned to deliver within 12 months, plus our then current balance of deferred revenue. At December 31, 2006, 2005 and 2004, we had no backlog.

Competition

We provided transition support services for our discontinued products to our existing customers through December 31, 2006 at which time we terminated all such services. Due to the fact that our transition support services were limited to our own discontinued products and the limited period of availability for those transition support services, we did not foresee any material competition for our transition support services.

Intellectual Property

We have relied on copyright, patent, trade secret and trademark law to protect our intellectual property. In March 2006, we sold the rights to our patent portfolio for cash consideration of $180,000, retaining a royalty-free license allowing us to continue to use our former patent portfolio in support of our existing customers. In November 2006, we sold the remaining intellectual property rights related to our carrier networking products and services for consideration of $80,000, retaining rights to support our existing customers through December 31, 2006.

Employees

We had one employee, Terry R. Gibson, our President, Chief Executive Officer and Chief Financial Officer, at December 31, 2006.

Executive Officers of the Registrant

The name of our executive officer and his age, title and biography as of March 15, 2007 appears below.

Name | | Age | | Position |

| | | | | |

| Terry R. Gibson | | 53 | | President, Chief Executive Officer, Chief Financial Officer and Secretary |

Terry R. Gibson has served as our Chief Executive Officer since January 16, 2005 and as our Executive Vice President and Chief Financial Officer since joining us in January 2002. Prior to joining us, Mr. Gibson served as Chief Financial Officer of Calient Networks, Inc. from May 2000 through December 2001. He served as Chief Financial Officer of Ramp Networks, Inc. from March 1999 to May 2000 and as Chief Financial Officer of GaSonics, International from June 1996 through March 1999. He also served as Vice President and Corporate Controller of Lam Research Corporation from February 1991 through June 1996. Mr. Gibson holds a B.S. in Accounting from the University of Santa Clara.

Available Information

We file annual reports, quarterly reports, proxy statements and other documents with the Securities and Exchange Commission ("SEC") under the Securities Exchange Act of 1934 (the "Exchange Act").. The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 450 Fifth Street N.W., Washington, D.C. 20549. The public may obtain information on the operation of the public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers, including us, that file electronically with the SEC. The public can obtain any documents that we file with the SEC at http://www.sec.gov.

Item 1A. Risk Factors

Our future results and the market price for our stock are subject to numerous risks, many of which are driven by factors that we cannot control or predict. The following discussion, as well as other sections of this Annual Report on Form 10-K including Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations, describes certain risk factors related to our business. You should carefully consider the risk factors described below in conjunction of the other information is this document.

We have sold our operating assets, our patent portfolio and our intellectual property and are executing a redeployment strategy. There can be no assurance that the redeployment strategy will increase shareholder value, and we may decide to liquidate.

We have incurred losses since inception and expect that net losses and negative cash flow will continue for the foreseeable future. Between September 2004 and December 2004, we announced the termination of most of our employees and that our products had been formally discontinued to facilitate the strategic alternatives then in consideration and ceased all operations other than a customer service and support capability. In July 2005, we completed a comprehensive review of strategic alternatives and approved a plan to redeploy our existing resources to identify and acquire one or more new business operations, while continuing to support our existing customers and continuing to offer our intellectual property for license or sale. In March 2006, we sold the rights to our patent portfolio, and in November 2006, we sold the remaining intellectual property rights related to our carrier network equipment products and services. In December 2006, we discontinued our customer service business. If we are not successful in executing our redeployment strategy we will continue to incur operating losses and negative cash flow and may at some point decide to liquidate and return the net proceeds to our stockholders. In the case of a liquidation or bankruptcy, we would need to hold back or distribute assets to cover liabilities before paying stockholders, which may therefore reduce or delay the proceeds that stockholders may receive for their ownership in us. However, we believe we have adequate cash resources to continue to realize our assets and discharge our liabilities as a company through 2007.

Failure to execute our redeployment strategy could cause our stock price to decline.

Our stock price may decline due to any or all of the following potential occurrences:

| | · | we may not be able to find suitable acquisition candidates or may not be able to acquire suitable candidates with our limited financial resources; |

| | · | we may not be able to utilize our existing NOLs to offset future earnings; |

| | · | we may have difficulty retaining our key remaining employee; |

| | · | we may have difficulty retaining our board of directors or attracting suitable qualified candidates should a director resign. |

We will incur significant costs in connection with our evaluation of suitable acquisition candidates.

As part of our plan to redeploy our assets, our management is seeking, analyzing and evaluating potential acquisition and merger candidates. We will incur significant costs, such as due diligence and legal and other professional fees and expenses, as part of these redeployment efforts. Notwithstanding these efforts and expenditures, we cannot give any assurance that we will identify an appropriate acquisition opportunity in the near term, or at all.

We will likely have no operating history in our new line of business, which is yet to be determined, and therefore we will be subject to the risks inherent in establishing a new business.

We have not identified what our new line of business will be and, therefore, we cannot fully describe the specific risks presented by such business. It is likely that we will have had no operating history in the new line of business and it is possible that the target company may have a limited operating history in its business. Accordingly, there can be no assurance that our future operations will generate operating or net income, and as such our success will be subject to the risks, expenses, problems and delays inherent in establishing a new line of business for us. The ultimate success of such new business cannot be assured.

We may be unable to realize the benefits of our net operating loss carry-forwards ("NOLs").

NOLs may be carried forward to offset federal and state taxable income in future years and eliminate income taxes otherwise payable on such taxable income, subject to certain adjustments. Based on current federal corporate income tax rates, our NOLs and other carry-forwards could provide a benefit to us, if fully utilized, of significant future tax savings. However, our ability to use these tax benefits in future years will depend upon the amount of our otherwise taxable income. If we do not have sufficient taxable income in future years to use the tax benefits before they expire, we will lose the benefit of these NOLs permanently. Consequently, our ability to use the tax benefits associated with our substantial NOLs will depend significantly on our success in identifying suitable acquisition candidates, and once identified, successfully consummating an acquisition of these candidates.

Additionally, if we underwent an ownership change, the NOLs would be subject to an annual limit on the amount of the taxable income that may be offset by our NOLs generated prior to the ownership change. If an ownership change were to occur, we may be unable to use a significant portion of our NOLs to offset taxable income. In general, an ownership change occurs when, as of any testing date, the aggregate of the increase in percentage points is more than 50 percentage points of the total amount of a corporation's stock owned by "5-percent stockholders," within the meaning of the NOLs limitations, whose percentage ownership of the stock has increased as of such date over the lowest percentage of the stock owned by each such "5-percent stockholder" at any time during the three-year period preceding such date. In general, persons who own 5% or more of a corporation's stock are "5-percent stockholders," and all other persons who own less than 5% of a corporation's stock are treated, together, as a single, public group "5-percent stockholder," regardless of whether they own an aggregate of 5% of a corporation's stock.

The amount of NOLs that we have claimed has not been audited or otherwise validated by the U.S. Internal Revenue Service (“IRS”). The IRS could challenge our calculation of the amount of our NOLs or our determinations as to when a prior change in ownership occurred and other provisions of the Internal Revenue Code, may limit our ability to carry forward our NOLs to offset taxable income in future years. If the IRS was successful with respect to any such challenge, the potential tax benefit of the NOLs to us could be substantially reduced.

Certain transfer restrictions implemented by us to preserve our net operating loss carryforwards may not be effective or may have some unintended negative effects.

On November 15, 2005, at our 2005 Annual Meeting of Stockholders, our stockholders approved an amendment to our Amended and Restated Certificate of Incorporation to restrict certain acquisitions of our securities in order to help assure the preservation of our NOLs. The amendment generally restricts direct and indirect acquisitions of our equity securities if such acquisition will affect the percentage of our capital stock that is treated as owned by a "5-percent stockholder."

Although the transfer restrictions imposed on our capital stock is intended to reduce the likelihood of an impermissible ownership change, there is no guarantee that such restrictions would prevent all transfers that would result in an impermissible ownership change. The transfer restrictions also will require any person attempting to acquire a significant interest in us to seek the approval of our board of directors. This may have an "anti-takeover" effect because our board of directors may be able to prevent any future takeover. Similarly, any limits on the amount of capital stock that a stockholder may own could have the effect of making it more difficult for stockholders to replace current management. Additionally, because the transfer restrictions will have the effect of restricting a stockholder's ability to dispose of or acquire our common stock, the liquidity and market value of our common stock might suffer.

We could be required to register as an investment company under the Investment Company Act of 1940, which could significantly limit our ability to operate and acquire an established business.

The Investment Company Act of 1940 (the "Investment Company Act") requires registration, as an investment company, for companies that are engaged primarily in the business of investing, reinvesting, owning, holding or trading securities. We have sought to qualify for an exclusion from registration including the exclusion available to a company that does not own "investment securities" with a value exceeding 40% of the value of its total assets on an unconsolidated basis, excluding government securities and cash items. This exclusion, however, could be disadvantageous to us and/or our stockholders. If we were unable to rely on an exclusion under the Investment Company Act and were deemed to be an investment company under the Investment Company Act, we would be

forced to comply with substantive requirements of Investment Company Act, including: (i) limitations on our ability to borrow; (ii) limitations on our capital structure; (iii) restrictions on acquisitions of interests in associated companies; (iv) prohibitions on transactions with affiliates; (v) restrictions on specific investments; (vi) limitations on our ability to issue stock options; and (vii) compliance with reporting, record keeping, voting, proxy disclosure and other rules and regulations. Registration as an investment company would subject us to restrictions that would significantly impair our ability to pursue our fundamental business strategy of acquiring and operating an established business. In the event the SEC or a court took the position that we were an investment company, our failure to register as an investment company would not only raise the possibility of an enforcement action by the SEC or an adverse judgment by a court, but also could threaten the validity of corporate actions and contracts entered into by us during the period we were deemed to be an unregistered investment company. Moreover, the SEC could seek an enforcement action against us to the extent we were not in compliance with the Investment Company Act during any point in time.

We may issue a substantial amount of our common stock in the future which could cause dilution to new investors and otherwise adversely affect our stock price.

A key element of our growth strategy is to make acquisitions. As part of our acquisition strategy, we may issue additional shares of common stock as consideration for such acquisitions. These issuances could be significant. To the extent that we make acquisitions and issue our shares of common stock as consideration, your equity interest in us will be diluted. Any such issuance will also increase the number of outstanding shares of common stock that will be eligible for sale in the future. Persons receiving shares of our common stock in connection with these acquisitions may be more likely to sell off their common stock, which may influence the price of our common stock. In addition, the potential issuance of additional shares in connection with anticipated acquisitions could lessen demand for our common stock and result in a lower price than might otherwise be obtained. We may issue common stock in the future for other purposes as well, including in connection with financings, for compensation purposes, in connection with strategic transactions or for other purposes.

Our customers may sue us because we discontinued our products and may not meet all our contractual commitments.

Certain of our customer contracts contained provisions relating to the availability of products, spare parts and services for periods up to ten years. We have worked with our customers to aid in a smooth transition, but our customers may choose to sue us for breach of contract.

If our products contain defects, we may be subject to significant liability claims from customers, distribution partners and the end-users of our products and incur significant unexpected expenses and lost sales.

Our products are technically complex and can be adequately tested only when put to full use in large and diverse networks with high amounts of traffic. They have in the past contained, and may in the future contain, undetected or unresolved errors or defects. Despite extensive testing, errors, defects or failures may be found in our products. If this happens, we may experience product returns, increased service and warranty costs, any of which could have a material adverse effect on our business, financial condition and results of operations. Moreover, because our products are designed to provide critical communications services, we may receive significant liability claims. We attempted to include in our agreements with customers and distribution partners provisions intended to limit our exposure to liability claims. However, such provisions may not be effective in any or all cases or under any or all scenarios, and they may not preclude all potential claims resulting from a defect in one of our products or from a defect related to the installation or operation of one of its products. Although we maintain product liability and errors and omissions insurance covering certain damages arising from implementation and use of their products, our insurance may not cover all claims sought against us. Liability claims could require us to spend significant time and money in litigation or to pay significant damages. As a result, any such claims, whether or not successful, could seriously damage our business prospects.

If we became involved in an intellectual property dispute, we could be subject to significant liability, the time and attention of our management could be diverted from pursuing strategic alternatives.

We may become a party to litigation in the future because others may allege infringement of their intellectual property. These claims and any resulting lawsuits could subject us to significant liability for damages. These lawsuits, regardless of their merits, likely would be time-consuming and expensive to resolve and would divert management time and attention. Any potential intellectual property litigation alleging our infringement of a third-party’s intellectual property also could force us to:

| | · | obtain from the owner of the infringed intellectual property right a license to sell the relevant technology, which license may not be available on reasonable terms, or at all; or |

| | · | redesign those products or services that use the infringed technology. |

We have a history of losses that we expect will continue, and if we do not achieve profitability we may cease operations.

At December 31, 2006, we had an accumulated deficit of $517 million. We have incurred net losses since our incorporation. If we do not achieve profitability and are unable to obtain additional financing, we will run out of cash and cease operations.

If we cannot obtain director and officer liability insurance in acceptable amounts for acceptable rates, we may have difficulty recruiting and retaining qualified directors and officers.

Like most other public companies, we carry insurance protecting our officer and directors against claims relating to the conduct of our business. This insurance covers, among other things, the costs incurred by companies and their management to defend against and resolve claims relating to management conduct and results of operations, such as securities class action claims. These claims typically are expensive to defend against and resolve. We pay significant premiums to acquire and maintain this insurance, which is provided by third-party insurers, and we agree to underwrite a portion of such exposures under the terms of the insurance coverage. One consequence of the current economic downturn and decline in stock prices has been a substantial increase in the number of securities class actions and similar claims brought against public corporations and their management, including the company and certain of its current and former officers and directors. Consequently, insurers providing director and officer liability insurance have in recent periods sharply increased the premiums they charge for this insurance, raised retentions (that is, the amount of liability that a company is required to pay to defend and resolve a claim before any applicable insurance is provided), and limited the amount of insurance they will provide. Moreover, insurers typically provide only one-year policies. The insurance policies that may cover any current securities claims against us have a $500,000 retention. As a result, the costs we incur in defending such claims will not be reimbursed until they exceed $500,000. The policies that would cover any future claims may not provide any coverage to us and may cover the directors and officers only in the event we are unwilling or unable to cover their costs in defending against and resolving any future claims. As a result, our costs in defending any future claims could increase significantly. Particularly in the current economic environment, we cannot assure you that in the future we will be able to obtain sufficient director and officer liability insurance coverage at acceptable rates and with acceptable deductibles and other limitations. Failure to obtain such insurance could materially harm our financial condition in the event that we are required to defend against and resolve any future or existing securities class actions or other claims made against us or our management arising from the conduct of our operations. Further, the inability to obtain such insurance in adequate amounts may impair our future ability to retain and recruit qualified officers and directors.

Item 1B. Unresolved Staff Comments

None.

We lease approximately 300 square feet of office space in San Jose, California under a month-to-month operating lease.

On November 15, 2001, we, along with certain of our officers and directors, were named as defendants in a class action shareholder complaint filed in the United States District Court for the Southern District of New York, now captioned In re CoSine Communications, Inc. Initial Public Offering Securities Litigation, Case No. 01 CV 10105. The complaint generally alleges that various investment bank underwriters engaged in improper and undisclosed activities related to the allocation of shares in our initial public offering. The complaint brings claims for the violation of several provisions of the federal securities laws against those underwriters, and also against us and each of the directors and officers who signed the registration statement relating to the initial public offering. The plaintiffs seek unspecified monetary damages and other relief. Similar lawsuits concerning more than 300 other companies' initial public offerings were filed during 2001, and this lawsuit is being coordinated with those actions in the Southern District of New York before Judge Shira A. Scheindlin.

On or about July 1, 2002 an omnibus motion to dismiss was filed in the coordinated litigation on behalf of the issuer defendants, of which we and our named officer and directors are a part, on common pleading issues. In October 2002, pursuant to stipulation by the parties, the Court entered an order dismissing our named officers and directors from the action without prejudice. On February 19, 2003, the Court dismissed the Section 10(b) and Rule 10b-5 claims against us but did not dismiss the Section 11 claims against us.

In June 2004, a stipulation of settlement and release of claims against the issuer defendants, including us, was submitted to the court for approval. The terms of the settlement, if approved, would dismiss and release all claims against the participating defendants (including us). In exchange for this dismissal, D&O insurance carriers would agree to guarantee a recovery by the plaintiffs from the underwriter defendants of at least $1 billion, and the issuer defendants would agree to an assignment or surrender to the plaintiffs of certain claims the issuer defendants may have against the underwriters. On August 31, 2005, the court issued an order granting preliminary approval of the settlement. On April 24, 2006, the court held a fairness hearing in connection with the motion for final approval of the settlement but has yet to rule on this motion.

On December 5, 2006, the Court of Appeals for the Second Circuit reversed the court's October 2004 order certifying a class in six test cases that were selected by the underwriter defendants and plaintiffs in the coordinated proceedings. It is unclear what impact this will have on the case. The settlement is subject to a number of conditions, including final court approval, which cannot be assured. If the settlement is not consummated, we intend to defend the lawsuit vigorously. However, we cannot predict its outcome with certainty. If we are not successful in our defense of this lawsuit, we could be forced to make significant payments to the plaintiffs and their lawyers, and such payments could have a material adverse effect on our business, financial condition and results of operations if not covered by our insurance carrier. Even if these claims are not successful, the litigation could result in substantial costs and divert management's attention and resources, which could adversely affect our business, results of operations and financial position.

In the ordinary course of business, we are involved in legal proceedings involving contractual obligations, employment relationships and other matters. Except as described above, we do not believe there are any pending or threatened legal proceedings that will have a material impact on our financial position or results of operations.

| Item 4. | Submission of Matters to a Vote of Security Holders |

None.

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our common stock currently trades in the over the counter market and is quoted on the Pink Sheets Electronic Quotation Service under the symbol “COSN.PK.” Our common stock had been traded on the Nasdaq National Market under the symbol COSN from our initial public offering in September 2000 through June 15, 2005, when we were de-listed from the Nasdaq National Market System. There was no public market for our common stock prior to our September 2000 initial public offering.

The following table sets forth the high and low sales price of our common stock in the years ended December 2005 and 2006. Our common stock was de-listed from Nasdaq National Market System on June 15, 2005. For the remainder of fiscal year 2005 and for all of fiscal year 2006, our common stock is traded in the over-the-counter market. The following table sets forth the range of high and low bid information of our common stock. The high and low bid quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission, and may not represent actual transactions.

| | | High | | Low | |

2006 | | | | | | | |

| First quarter | | $ | 2.55 | | $ | 2.31 | |

| Second quarter | | $ | 2.70 | | $ | 2.35 | |

| Third quarter | | $ | 2.85 | | $ | 2.42 | |

| Fourth quarter | | $ | 3.40 | | $ | 2.58 | |

2005 | | | | | | | |

| First quarter | | $ | 2.54 | | $ | 1.94 | |

| Second quarter | | $ | 2.76 | | $ | 1.94 | |

| Third quarter | | $ | 3.15 | | $ | 1.85 | |

| Fourth quarter | | $ | 2.85 | | $ | 2.30 | |

Stockholders

According to the records of our transfer agent, at March 12, 2007 we had approximately 276 shareholders of record. The majority of our shares are held in approximately 4,100 customer accounts held by brokers and other institutions on behalf of stockholders.

Dividends

To date, we have not declared or paid any cash dividends on our common stock. Our current policy is to retain future earnings, if any, for use in the operations, and we do not anticipate paying any cash dividends in the foreseeable future.

Securities Authorized for Issuance under Equity Compensation Plans

The following table summarizes equity compensation plans approved by stockholders and equity compensation plans that were approved and not approved by the stockholders as of December 31, 2006:

EQUITY COMPENSATION PLAN INFORMATION

| | | Number of Securitiesto be Issued UponExercise of OutstandingOptions, Warrants and | | Weighted- AverageExercise Price of Outstanding Options, Warrants and | | Number of Securities Remaining Available forFuture Issuance UnderEquity Compensation | |

Plan category | | Rights | | Rights | | Plans (1) | |

| | | | | | | | |

| Equity compensation plans approved by stockholders | | | 147,000 (2 | ) | $ | 7.69 (2 | ) | | 1,940,455 (3 | ) |

| Equity compensation plans not approved by stockholders (4) | | | — | | | | | | 1,000,000 | |

| | | | | | | | | | | |

| Total | | | 147,000 | | $ | 7.69 | | | 2,940,455 | |

| (1) | These numbers exclude shares listed under the column heading "Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights." |

| | |

| (2) | Includes 5,000 shares subject to outstanding options under the 1997 Stock Plan, 112,000 shares subject to outstanding options under the 2000 Stock Plan, and 30,000 shares subject to outstanding options under the Director Plan. |

| | |

| (3) | Includes 1,924,455 shares available for future issuance under the 2000 Stock Plan, 16,000 shares available for future issuance under the Director Plan. |

| | |

| (4) | The only equity compensation plan not approved by stockholders is the 2002 Stock Plan (the "2002 Plan"). The board of directors adopted the 2002 Plan in January 2002 to make available for issuance certain shares of our common stock that have been (i) previously issued pursuant to the exercise of stock options granted under the 1997 Plan and (ii) subsequently reacquired by us pursuant to repurchase rights contained in restricted stock purchase agreements or pursuant to optionee defaults on promissory notes issued in connection with the exercise of such options ("Reacquired Shares"). Under the terms of the 1997 Plan and the 2000 Plan, these Reacquired Shares would not otherwise have been available for reissuance. No shares that were not previously issued under the 1997 Plan and subsequently reacquired by us have been or will be reserved for issuance under the 2002 Plan. A maximum of 1,000,000 shares may be reserved for issuance under the 2002 Plan. An aggregate of 335,791 shares were initially reserved for issuance under the 2002 Plan upon its adoption. These shares consisted of Reacquired Shares as of the date of adoption. Additional shares that become Reacquired Shares after the date of adoption of the 2002 Plan, up to a maximum of 664,209 additional shares, will also become available for issuance under the 2002 Plan. The provisions of the 2002 Plan are substantially similar to those of the 2000 Plan, except that the 2002 Plan does not permit the grant of awards to officers or directors and does not permit the grant of Incentive Stock Options. The 2002 Plan provides for the grant of nonstatutory stock options to employees (excluding officers) and consultants. Stock options granted under the 2002 Plan will be at prices not less than the fair value of the common stock at the date of grant. The term of each option, generally 10 years or less, will be determined by CoSine. |

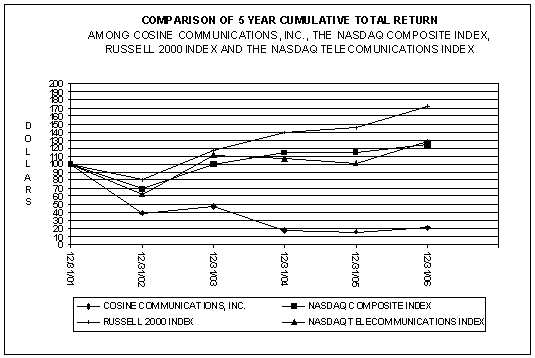

Performance Graph

Notwithstanding anything to the contrary set forth in any of our previous or future filings under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, the following Performance Graph, in whole or in part, shall not be incorporated by reference into any such filings and shall not otherwise be deemed to be "soliciting material" or " filed" under such acts.

The following graph demonstrates a comparison of cumulative total returns for our Common Stock, the Nasdaq Composite Index, the Russell 2000 Index and the Nasdaq Telecommunications Index for each of the last five fiscal years ended December 31, 2006. The graph assumes an investment of $100 on December 31, 2001 in each of our Common Stock, and the stocks comprising the Nasdaq Composite Index, the Russell 2000 Index and the Nasdaq Telecommunications Index. The Indices assume that all dividends were reinvested. On June 16, 2005, our Common Stock was de-listed from the Nasdaq National Market System and now trades in the over the counter market and is quoted on the Pink Sheets Electronic Quotation Service under the symbol “COSN.PK.” We were a provider of carrier network equipment products and services until the fourth quarter of fiscal year 2004 during which time we discontinued our product lines. We terminated all customer service operations effective December 31, 2006 and do not intend to offer customer support services for our discontinued products in the future. We are currently seeking to redeploy our existing resources to identify and acquire one or more new business operations with existing or prospective taxable earnings that can be offset by use of our NOLs. We have not identified any suitable acquisition candidates or what our new line of business will be and, therefore, cannot currently identify a group of comparable peer companies in an industry or line of business similar to our current business that we believe would provide our stockholders with a meaningful comparison.

| | | 12/31/01 | | 12/31/02 | | 12/31/03 | | 12/31/04 | | 12/31/05 | | 12/31/06 | |

| | | | | | | | | | | | | | |

| COSINE COMMUNICATIONS, INC. | | | 100.00 | | | 38.97 | | | 47.61 | | | 18.06 | | | 15.48 | | | 21.42 | |

| NASDAQ COMPOSITE INDEX | | | 100.00 | | | 69.66 | | | 99.71 | | | 113.79 | | | 114.47 | | | 124.20 | |

| RUSSELL 2000 INDEX | | | 100.00 | | | 79.52 | | | 117.09 | | | 138.55 | | | 144.86 | | | 171.47 | |

| NASDAQ TELECOMMUNICATIONS INDEX | | | 100.00 | | | 61.62 | | | 110.79 | | | 106.16 | | | 100.63 | | | 127.11 | |

The Stock Performance shown on the Graph above is not necessarily indicative of future performance. We will not make nor endorse any predictions as to future stock performance.

Use of Proceeds of Registered Securities

On September 25, 2000, in connection with our initial public offering, a Registration Statement on Form S-1 (File No. 333-35938) was declared effective by the Securities and Exchange Commission, pursuant to which 1,150,000 shares of our common stock were offered and sold for our account at a price of $230 per share, generating gross offering proceeds of $264.5 million. The managing underwriters were Goldman, Sachs & Co., Chase Securities Inc., Robertson Stephens, Inc. and JP Morgan Securities Inc. Our initial public offering closed on September 29, 2000. The net proceeds of the initial public offering were approximately $242.5 million after deducting approximately $18.5 million in underwriting discounts and approximately $3.5 million in other offering expenses.

We did not pay directly or indirectly any of the underwriting discounts or other related expenses of the initial public offering to any of our directors or officers, any person owning 10% or more of any class of our equity securities, or any of our affiliates.

We have used approximately $220 million of the funds from the initial public offering to fund our operations. We expect to use the remaining net proceeds for general corporate purposes, including funding our operations, our working capital needs and potential acquisitions pursuant to our redeployment strategy. Pending further use of the net proceeds, we have invested them in short-term, interest-bearing, investment-grade securities.

| Item 6. | Selected Financial Data |

The selected consolidated financial data below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes. The selected consolidated statements of operations data for the years ended December 31, 2006, 2005 and 2004 and the selected consolidated balance sheet data as of December 31, 2006 and 2005, are derived from, and are qualified by reference to, the audited consolidated financial statements included elsewhere in this Annual Report on Form 10-K. The selected consolidated statements of operations data for the fiscal years ended prior to December 31, 2004, and the selected consolidated balance sheet data prior to December 31, 2005, are derived from our audited consolidated financial statements that are not included in this Annual Report on Form 10-K. The historical results presented below are not necessarily indicative of future results.

| | | Year Ended December 31 | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (In thousands, except per share data) | |

Consolidated Statements of Operations Data: | | | | | | | | | | | |

| Revenue | | $ | 1,361 | | $ | 3,315 | | $ | 9,675 | | $ | 14,621 | | $ | 23,632 | |

| Cost of revenue | | | 1,663 | | | 2,049 | | | 7,086 | | | 6,765 | | | 13,807 | |

| Gross profit (loss) | | | (302 | ) | | 1,266 | | | 2,589 | | | 7,856 | | | 9,825 | |

| Operating expenses: | | | | | | | | | | | | | | | | |

| Research and development | | | — | | | 103 | | | 15,078 | | | 21,756 | | | 32,396 | |

| Sales and marketing | | | — | | | 105 | | | 10,052 | | | 13,808 | | | 28,271 | |

| General and administrative | | | 1,316 | | | 3,227 | | | 6,064 | | | 7,226 | | | 10,959 | |

| Restructuring and impairment charges | | | — | | | (91 | ) | | 8,909 | | | 336 | | | 34,538 | |

| Total operating expenses | | | 1,316 | | | 3,344 | | | 40,103 | | | 43,126 | | | 106,164 | |

| Loss from operations | | | (1,618 | ) | | (2,078 | ) | | (37,514 | ) | | (35,270 | ) | | (96,339 | ) |

| Other income (expense): | | | | | | | | | | | | | | | | |

| Interest income | | | 1,101 | | | 678 | | | 489 | | | 1,296 | | | 3,535 | |

| Interest expense | | | (4 | ) | | — | | | (3 | ) | | (224 | ) | | (966 | ) |

| Other | | | 918 | | | (46 | ) | | (276 | ) | | (447 | ) | | 313 | |

| Total other income | | | 2,015 | | | 632 | | | 210 | | | 625 | | | 2,882 | |

| Income (loss) before income tax provision (credit) | | | 397 | | | (1,446 | ) | | (37,304 | ) | | (34,645 | ) | | (93,457 | ) |

| Income tax provision (credit) | | | ( 52 | ) | | ( 228 | ) | | 33 | | | 287 | | | 509 | |

| Net income (loss) | | $ | 449 | | $ | (1,218 | ) | $ | (37,337 | ) | $ | (34,932 | ) | $ | (93,966 | ) |

| Basic net income (loss) per common share | | $ | 0.04 | | $ | (0.12 | ) | $ | (3.70 | ) | $ | (3.57 | ) | $ | (9.72 | ) |

| Diluted net income (loss) per common share | | $ | 0.04 | | $ | (0.12 | ) | $ | (3.70 | ) | $ | (3.57 | ) | $ | (9.72 | ) |

| Shares used in computing basic net income (loss) per common share | | | 10,091 | | | 10,094 | | | 10,082 | | | 9,791 | | | 9,670 | |

| Shares used in computing diluted net income (loss) per common share | | | 10,096 | | | 10,094 | | | 10,082 | | | 9,791 | | | 9,670 | |

| | | | | | | | | | | | | | | | | |

Consolidated Balance Sheets Data: | | | | | | | | | | | |

| Cash, cash equivalents and short-term investments | | $ | 22,857 | | $ | 23,166 | | $ | 24,913 | | $ | 57,752 | | $ | 101,467 | |

| Working capital | | | 22,477 | | | 22,353 | | | 23,214 | | | 59,705 | | | 91,868 | |

| Total assets | | | 23,036 | | | 23,840 | | | 27,823 | | | 73,426 | | | 119,561 | |

| Working capital loans | | | — | | | — | | | — | | | — | | | 131 | |

| Accrued rent | | | — | | | — | | | — | | | 2,078 | | | 2,069 | |

| Total stockholders’ equity | | | 22,477 | | | 22,603 | | | 23,364 | | | 61,174 | | | 93,481 | |

Quarterly financial information (unaudited):

| | | 2005 | | 2006 | |

| | | | 1st Quarter | | | 2nd Quarter | | | 3rd Quarter | | | 4th Quarter | | | 1st Quarter | | | 2nd Quarter | | | 3rd Quarter | | | 4th Quarter | |

| | | (In thousands, except per share data) | |

| Revenue | | $ | 897 | | $ | 699 | | $ | 785 | | $ | 934 | | $ | 579 | | $ | 520 | | $ | 134 | | $ | 128 | |

| Gross profit (loss) | | | 443 | | | 310 | | | 83 | | | 430 | | | 9 | | | (13 | ) | | (232 | ) | | (66 | ) |

| Net income (loss) | | | (878 | ) | | (633 | ) | | ( 31 | ) | | 324 | | | (126 | ) | | 205 | | | (225 | ) | | 595 | |

| Basic and diluted net income (loss) per share | | | (0.09 | ) | | (0.06 | ) | | (0.00 | ) | | 0.03 | | | (0.01 | ) | | 0.02 | | | (0.02 | ) | | 0.05 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

OVERVIEW

Our strategy is to enhance stockholder value by pursuing opportunities to redeploy our assets through an acquisition of one or more operating business with existing or prospective taxable earnings that can be offset by use of our net operating loss carry-forwards (“NOLs”). In 2006, we completed the wrap-up of our carrier services business, providing customer support services for our discontinued products through December 31, 2006, at which time we terminated all customer support offerings. We also sold the remaining assets of our carrier network products business with the sale of our patent portfolio in March 2006 and the sale of the rights to the related intellectual property in November 2006.

We were a provider of carrier network equipment products and services until the fourth quarter of fiscal year 2004 during which time we discontinued our product lines, took actions to lay-off most of our employees, terminated contract manufacturing arrangements, contractor and consulting arrangements and various facility leases, and sold, scrapped or wrote-off our inventory, property and equipment. In July 2005, we completed a comprehensive review of strategic alternatives, including a sale of the Company, a sale or licensing of intellectual property, a redeployment of our assets into new business ventures, or a winding-up and liquidation of the business and a return of capital. At that time, the board of directors approved the strategy of redeploying our existing resources to identify and acquire one or more new business operations, while continuing to support our existing customers and continuing to offer our intellectual property for license or sale.

Due to the adoption of our redeployment strategy, the information appearing below, which relates to prior periods, may not be indicative of the results that may be expected for any subsequent periods. The year ended December 31, 2006 primarily reflects, and future periods prior to a redeployment of our assets are expected to primarily reflect, general and administrative expenses and transaction expenses associated with the continuing administration of the Company and its efforts to redeploy its assets.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

General

Our discussion and analysis of our financial condition and results of operations are based on our consolidated financial statements, which have been prepared in accordance U.S. generally accepted accounting principles. The preparation of these consolidated financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenue and expenses, and related disclosures of contingent assets and liabilities. On an ongoing basis, we evaluate our estimates, including those related to revenue recognition, allowance for doubtful accounts, inventory valuation, long-lived assets, warranties and equity issuances. Additionally, the audit committee of our board of directors reviews these critical accounting estimates at least annually. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances. These estimates form the basis for certain judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates.

The following accounting policies are significantly affected by the judgments and estimates we use in the preparation of our consolidated financial statements.

Revenue Recognition

Historically, prior to discontinuing our products, most of our sales were generated from complex arrangements. Recognizing revenue in these arrangements required our making significant judgments, particularly in the areas of customer acceptance and collectibility.

Certain of our historic product sales arrangements required formal acceptance by our customers. In such cases, we did not recognize revenue until we received formal notification of acceptance. Although we worked closely with our customers to help them achieve satisfaction with our products prior to and after acceptance, the timing of customer acceptance could greatly affect the timing of the recognition of our revenue.

While the end user of our product was normally a large network service provider, we also sold products and services through small resellers and to small network service providers in Asia, Europe and North America. To recognize revenue before we receive payment, we were required to assess that collection from the customer was probable. If we could not satisfy ourselves that collection was probable, we deferred revenue recognition until we collected payment.

Through December 31, 2006, our business consisted primarily of customer service revenue. We record revenue as earned for customer service revenue, once we satisfy ourselves that collection from the customer is probable. If we cannot satisfy ourselves that collection is probable, we defer revenue recognition until we collect payment.

Allowance for Doubtful Accounts

We maintain allowances for doubtful accounts in connection with estimated losses resulting from the inability of our customers to pay our invoices. In order to estimate the appropriate level of this allowance, we analyze historical bad debts, customer concentrations, current customer credit-worthiness, current economic trends and changes in our customer payment patterns. In future periods, if the financial condition of our customers were to deteriorate and affect their ability to make payments, additional allowances may be required.

Inventory Valuation

Our inventory was either sold, scrapped or fully written-off at December 31, 2004, 2005 and 2006, respectively.

In assessing the value of our inventory, we are required to make judgments about future demand and then compare that demand with current inventory quantities and firm purchase commitments. If our inventories and firm purchase commitments are in excess of forecasted demand, we write down the value of our inventory. We generally used a 12-month forecast to assess future demand. Inventory write-downs are charged to cost of revenue. At September 30, 2004, in connection with our decision to discontinue our products, we recorded a charge of $3.5 million to cost of revenue to write our inventory down to its estimated net realizable value. During 2005, we sold $26,000 of previously written-down inventory. During 2004 we sold $0.7 million of previously written-down inventory.

Long-lived assets

At December 31, 2006, 2005 and 2004, respectively, all of our long-lived assets had been either sold, scrapped or fully written-off.

We evaluate the carrying value of long-lived assets, consisting primarily of property, plant and equipment, whenever certain events or changes in circumstances indicate that the carrying amount of these assets may not be recoverable. In assessing the recoverability of long-lived assets, we compare the carrying value of the assets to the undiscounted future cash flows the assets are expected to generate. If the total of the undiscounted future cash flows is less than the carrying amount of the assets, the assets will be written down to their estimated fair value. Fair value is generally determined by calculating the discounted future cash flows using a discount rate based on our weighted average cost of capital or specific appraisal, as appropriate. Significant judgments and assumptions are required in the forecast of future operating results used in the preparation of the estimated future cash flows, including long-term forecasts of overall market conditions and our participation in the market. Changes in these estimates could have a material adverse effect on the assessment of the long-lived assets such that we may be required to record further asset write-downs in the future. We had no impairment charges in 2006 or 2005. During 2004, we charged $2.3 million to operating expenses as a result of impairments. During 2004, we had a gain of $ 0.9 million with the sale of previously written-down long-lived assets.

Warranties

Prior to discontinuing our products, we provided a basic limited warranty, including repair or replacement of parts, and technical support for our products. The specific terms and conditions of those warranties varied depending on the customer or region in which we did business. We estimated the costs that could be incurred under our basic limited warranty and recorded a liability in the amount of such costs at the time product revenue was recognized. Our warranty obligation is affected by the number of installed units, product failure rates, materials usage and service delivery costs incurred in correcting product failures. Each quarter, we assess the adequacy of our recorded warranty liabilities and adjust the amounts as necessary. In future periods, if actual product failure rates, materials usage or service delivery costs differ from our estimates, adjustments to cost of revenue may result.

We no longer offer a warranty on product or service sales and all warranty obligations have expired prior to December 31, 2006.

Impact of Equity Issuances on Operating Results

Equity issuances have a material impact on our operating results. The equity issuances that have affected operating results to date include warrants granted to customers and suppliers, stock options granted to employees and consultants, stock issued in lieu of cash compensation to suppliers and re-priced stock options.

Our cost of revenue, operating expenses and interest expense were affected significantly by charges related to warrants and options issued for services. Furthermore, some of our employee stock option transactions have resulted in deferred compensation, which is presented as a reduction of stockholders’ equity on our consolidated balance sheet and was amortized over the vesting period of the applicable options using the graded vesting method.

The deferred compensation and amortization associated with shares and options relating to the following transactions are required to be re-measured at the end of each accounting period, based on the current stock price. The re-measurement at the end of each accounting period will result in unpredictable charges or credits in future periods, depending on future fluctuations in the market prices of our common stock:

| · | Non-recourse promissory notes receivable: During the fourth quarter of 2000, we converted full-recourse promissory notes received from employees upon the early exercise of unvested employee stock options to non-recourse obligations. Accordingly, we are required to re-measure the compensation associated with these shares until the earlier of repayment of the note or default. Deferred compensation expense, which is recorded at each re-measurement, is amortized over the remaining vesting period of the underlying options. |

| · | Re-priced stock options: In November 2002, we re-priced 1,091,453 outstanding employee stock options to purchase shares of our common stock with original exercise prices ranging from $5.45 per share to $159.38 per share. These options were re-priced to $5.00 per share, which was higher than the fair market value of the underlying shares on the re-pricing date. In July 2001, we re-priced 722,071 unexercised employee stock options to $15.50 per share, the fair market value of the underlying shares on the re-pricing date. These options had previously been granted at prices ranging from $40.00 to $400.00 per share. Compensation will be re-measured for these options until they are exercised, canceled, or expire. During the year ended December 31, 2006, no stock options re-priced in November 2002 were still outstanding. |

Some of the stock options granted to our employees prior to our IPO in September 2000 had resulted in deferred compensation as a result of stock options having an exercise price below their estimated fair value. Deferred compensation was presented as a reduction to stockholders’ equity on the consolidated balance sheet and is then amortized using an accelerated method over the vesting period of the applicable options. When an employee terminates, an expense credit is recorded for any amortization that has been previously recorded as an expense in excess of vesting.

In the first quarter of 2004, we began a program whereby we granted employees bonuses in shares of our common stock based on the achievement of certain Company objectives. At the end of each quarter, we determined whether objectives have been achieved and set the total value of the common stock grant. The number of shares to be issued is calculated the following quarter based on the fixed value of the common stock issued, as determined at quarter-end, divided by our stock price on the issuance date. Compensation expense is accrued in full in the quarter in which it is earned. No employee bonuses were earned in the second, third or fourth quarters of 2004 or in any quarter of 2005 or 2006 as the quarterly objectives were not met.

In the second quarter of 2004, we issued to a reseller a warrant to acquire 254,489 shares of our common stock at an exercise price of $4.65 per share. The warrant had a two-year term beginning May 28, 2004 and vested ratably over the term. If during the two-year term (1) any person or entity had acquired a greater than 50% interest in us or the ownership or control of more than 50% of our voting stock or (2) we had sold substantially all of our intellectual property assets, the warrant would have become exercisable. Even if the reseller did not immediately exercise the warrant upon the occurrence of such an event that made the warrant exercisable (a “trigger event”), the reseller would have been entitled to securities, cash and property to which it would have been entitled to upon the consummation of the trigger event, less the aggregate price applicable to the warrant. We calculated the fair value of the warrant to be approximately $487,000 using the Black-Scholes option pricing model, using a volatility factor of .97, a risk-free interest rate of 2.5%, and an expected life of two years. The fair value of the warrant was being amortized over the two-year expected life of the warrant. During the years ended December 31, 2006 and 2005, we amortized $100,000 and $339,000, respectively, to cost of revenue. During the year ended December 31, 2004, we amortized $6,000 to cost of revenue and $42,000 to general and administrative expenses.

RESULTS OF OPERATIONS

Revenue

In 2004, the majority of our revenue was recognized from the sale of our IP Service Delivery Platform and subsequent service support arrangements. In 2005 and 2006, our revenues were earned primarily from our customer service contracts. We recognize product revenue at the time of shipment or delivery (depending on shipping terms), assuming that persuasive evidence of an arrangement exists, the sales price is fixed or determinable and collection is probable, unless we have future obligations for installation or require customer acceptance, in which case revenue is deferred until these obligations are met. Our product incorporates software that is not incidental to the related hardware and, accordingly, we recognize revenue in accordance with the American Institute of Certified Public Accountants issued Statement of Position 97-2 “Software Revenue Recognition.” For arrangements that include the delivery of multiple elements, the revenue is allocated to the various products based on “vendor-specific objective evidence” (VSOE) of fair value. We establish VSOE based on either the price charged for the product when the same product is sold separately or for products not yet sold separately, based on the list prices of such products individually established by management with the relevant authority to do so.

Revenue from perpetual software licenses is recognized upon shipment or acceptance, if required. Revenue from one-year term licenses is recognized on a straight-line basis over the one-year license term. Post-delivery technical support, such as on-site service, phone support, parts and access to software upgrades, when and if available, is provided under separate support services agreements. In cases where the support services are sold as part of an arrangement including multiple elements, we allocate revenue to the support service based on the VSOE of the service and recognize it on a straight-line basis over the service period. Revenue from consulting and training services is recognized as the services are provided.

Amounts billed in excess of revenue recognized are included as deferred revenue in the accompanying consolidated balance sheets.

Revenue from customers by geographic region for the years ended December 31, 2006, 2005 and 2004 was as follows, in thousands:

| | 2006 | | % | | 2005 | | % | | 2004 | | % | |

| North America | | $ | 1,211 | | | 89 | % | $ | 1,901 | | | 57 | % | $ | 3,364 | | | 35 | % |

| Asia/Pacific | | | — | | | — | | | 617 | | | 19 | | | 3,258 | | | 34 | |

| Europe | | | 150 | | | 11 | % | | 797 | | | 24 | | | 3,053 | | | 31 | |

| Total revenue | | $ | 1,361 | | | 100 | % | $ | 3,315 | | | 100 | % | $ | 9,675 | | | 100 | % |

Hardware, software and service revenue for the years ended December 31, 2006, 2005 and 2004 was as follows, in thousands:

| | | 2006 | | % | | 2005 | | % | | 2004 | | % | |

| Hardware | | $ | — | | | — | | $ | 26 | | | 1 | % | $ | 6,316 | | | 65 | % |

| Software | | | — | | | — | | | 190 | | | 6 | | | 608 | | | 6 | |

| Services | | | 1,361 | | | 100 | % | | 3,099 | | | 93 | | | 2,751 | | | 29 | |

| | | | | | | | | | | | | | | | | | | | |

| Total revenue | | $ | 1,361 | | | 100 | % | $ | 3,315 | | | 100 | % | $ | 9,675 | | | 100 | % |

In 2006, all of our revenue was earned from our customer service contracts. The decline in revenue as compared to the prior year is due to the fact that our customers continued their transition from the discontinued CoSine products to other suppliers and, as a result, the demand for our services decreased during the year. At December 31, 2006, we discontinued our service offerings. See "Outlook" section on pages 25 to 26 and "Risk Factors" section on pages 6 to 9.

In 2005, our revenues were earned primarily from our customer service contracts. Hardware revenue consisted of a $26,000 sale of previously written-down equipment and software revenue consisted of $190,000 for sales of nonexclusive software licenses. Our customers purchased service contracts for their installed systems while they planned and executed their transition from our networking systems to other suppliers.

In 2004, product shipments declined compared to 2003. The decline was noted in all regions and was due to completion of expansion projects for certain customers in Japan and North America and no significant new customer wins or expansions by existing customers, partially offset by over $700,000 in “last time buy” sales in connection with our announced plans to discontinue our products. Service revenue remained relatively constant as existing customers continued to purchase service and support for their installed units. Software revenue increased over 2003 due to certain customers purchasing new software licenses for their existing installed base.

As of December 31, 2006, 2005 and 2004, we deferred nil, $0.1 million and $0.5 million, respectively, of revenue from contracts that we immediately invoiced but which provide for subsequent customer acceptance, consulting services and post-contract support services.

Non-Cash Charges and Credits Related to Equity Issuances

We amortized (benefited from) $140,000, $339,000 and ($780,000) of non-cash charges (credits) related to equity issuances to cost of revenue, operating expenses and interest expense, for the years ended December 31, 2006, 2005 and 2004, respectively.