EXHIBIT 99.1

PRESENTATION

| Enterprise Products Partners L.P. Analyst Conference New York March 29, 2007 |

| Forward Looking Statements This presentation contains forward-looking statements and information that are based on Enterprise's beliefs and those of its general partner, as well as assumptions made by and information currently available to them. When used in this presentation, words such as anticipate, project, expect, plan, goal, forecast, intend, could, believe, may, and similar expressions and statements regarding the plans and objectives of Enterprise for future operations, are intended to identify forward-looking statements. Although Enterprise and its general partner believe that such expectations reflected in such forward looking statements are reasonable, neither it nor its general partner can give assurances that such expectations will prove to be correct. Such statements are subject to a variety of risks, uncertainties and assumptions. If one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect, actual results may vary materially from those Enterprise anticipated, estimated, projected or expected. Among the key risk factors that may have a direct bearing on Enterprise's results of operations and financial condition are: Fluctuations in oil, natural gas and NGL prices and production due to weather and other natural and economic forces; A reduction in demand for its products by the petrochemical, refining or heating industries; The effects of its debt level on its future financial and operating flexibility; A decline in the volumes of NGLs delivered by its facilities; The failure of its credit risk management efforts to adequately protect it against customer non-payment; Actual construction and development costs could exceed forecasted amounts; Operating cash flows from our capital projects may not be immediate; Terrorist attacks aimed at its facilities; and The failure to successfully integrate its operations with assets or companies, if any, that it may acquire in the future. Enterprise has no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. |

| Use of Non-GAAP Financial Measures This presentation utilizes the Non-GAAP financial measures of Gross Operating Margin, EBITDA, Distributable Cash Flow and Consolidated EBITDA. In general, we define Gross Operating Margin as operating income before (i) depreciation, amortization and accretion expense; (ii) operating lease expense for which we do not have the payment obligation; (iii) gains and losses on the sale of assets and (iv) general and administrative expenses. We define EBITDA as net income or loss before interest; provision for income taxes; and depreciation, amortization and accretion expense. In general, we define Distributable Cash Flow as net income or loss plus (i) depreciation, amortization and accretion expense; (ii) operating lease expense for which we do not have the payment obligation; (iii) cash distributions received from unconsolidated affiliates less equity in the earnings of such affiliates; (iv) the subtraction of sustaining capital expenditures; (v) gains and losses on the sale of assets; (vi) cash proceeds from the sale of assets or return of investment from unconsolidated affiliates; (vii) gains or losses on monetization of financial instruments recorded in Accumulated Other Comprehensive Income less related amortization of such amount to earnings; (viii) transition support payments received from El Paso related to the GTM Merger and (ix) the addition of losses or subtraction of gains related to other miscellaneous non-cash amounts affecting net income for the period. Distributable Cash Flow is a significant liquidity metric used by our senior management to compare basic cash flows generated by us to the cash distributions we expect to pay partners. Distributable Cash Flow is also an important Non-GAAP financial measure for our limited partners since it serves as an indicator of our success in providing a cash return on investment. Distributable Cash Flow is also a quantitative standard used by the investment community with respect to publicly traded partnerships such as ours because the value of a partnership unit is in part measured by its yield (which in turn is based on the amount of cash distributions a partnership pays to a unit holder). The GAAP measure most directly comparable to Distributable Cash Flow is net cash provided by operating activities. This presentation also includes references to credit leverage ratios that utilize Consolidated EBITDA, which is a term defined in the $1.25 billion revolving credit facility of Enterprise Products Operating L.P. (EPOLP), EPD's operating subsidiary. These credit ratios are used by certain of our lenders to evaluate our ability to support debt service. The GAAP measure most directly comparable to Consolidated EBITDA is net cash provided by operating activities. Please slides 134 through 138 for our calculations of these Non-GAAP financial measures along with the appropriate reconciliations. |

| Meeting Agenda Michael A. Creel - Introduction Robert G. Phillips - Business Introduction / Strategies James H. Lytal - Natural Gas Pipelines / Storage / Offshore A.J. Jim Teague - Gas Processing / NGLs / Gas Marketing James M. Collingsworth -NGL Pipelines Gil H. Radtke - Petrochemical Services Michael A. Creel - Financial Overview Reconciliations |

| Introduction / Overview Michael A. Creel |

| Overview Enterprise Products Partners L.P. (NYSE: EPD) is the primary partnership in the Enterprise family, which includes Enterprise GP Holdings L.P. (NYSE: EPE) and Duncan Energy Partners L.P. (NYSE: DEP) Combined family of partnerships has an equity market capitalization of approximately $18 billion and an enterprise value of more than $23 billion EPD is one of the largest publicly traded partnerships with an equity market capitalization of more than $13 billion, assets of $14 billion and an enterprise value of approximately $19 billion Ranks 183rd on the Fortune 500 Delivered record performance in 2006 EPD owns and operates one of North America's largest fully integrated midstream value chains with significant geographic and business diversity EPD focuses on long-term value creation for its investors by investing in a diversified portfolio of organic infrastructure projects and selected acquisitions to drive distribution growth |

| EPD Key Investment Considerations Strategically located assets serving the most prolific supply basins and largest consuming regions of natural gas, NGLs and crude oil in the United States Leading business positions across the midstream value chain Over 90% of gross operating margin from diversified fee-based assets Visible cash flow growth from approximately $2.5 billion of growth projects expected to be completed in 2007 EPD's lower long-term cost of equity capital results in more cash accretion from investments, which provides more cash to increase distributions and reinvest in growth Experienced management team with substantial ownership |

| Enterprise Family of Partnerships Formation of DEP DEP was created as a vehicle to facilitate the growth of EPD No GP incentive distribution rights (IDRs) and slower growth results in lower long-term cost of equity capital EPD benefits through drop downs to DEP and DEP's direct investment in competitive projects and acquisitions Initial $572 million transaction - highly successful IPO Gives EPD the ability to rationalize assets while retaining control of the assets and maintaining the integrity of EPD's value chain Value added for EPD's unitholders as it redeploys proceeds from drop downs to fund new EPD projects with higher expected returns on investment Diversifies EPD's sources of capital and effectively provides EPD with an alternative source of low cost equity capital Interests of Enterprise family of PTPs are aligned Growth at DEP with reinvestment at EPD is expected to drive higher distributable cash flow (DCF) per unit at EPD, which benefits EPE through its 25% IDR in EPD |

| No GP IDRs at DEP Results in Lower Cost of Equity Capital Unlike most partnerships, DEP's GP does not have IDRs DEP's GP distribution is always capped at 2% of total distributions Results in a lower cost of equity capital than most partnerships and corporations Makes DEP more competitive in pursuing acquisitions and organic projects Lower payments to GP enhances DEP's financial flexibility by providing cash for additional investment, debt reduction or increased cash distributions to limited partners |

| Three Partnerships, Three Total Return Profiles EPE (Higher Growth / Lower Yield) Highest potential distribution growth due to leverage provided by 25% GP IDRs in EPD distributions As EPD grows its distribution or issues new common units, EPE's cash flow increases In 2006, EPD increased its distribution rate by 7% and issued 42 million common units, which enabled EPE to increase its distribution rate by 25% EPD (Attractive Growth / Yield) Balanced total return proposition for investors with a long-term investment horizon Strong track record of distribution growth Largest ownership position by management Visible growth through large portfolio of organic growth projects DEP (Modest Growth / Higher Yield) For investors more focused on income versus capital appreciation Lowest cost of capital with no GP IDRs Supported by a strong sponsor and management team with a history of creating value for unitholders |

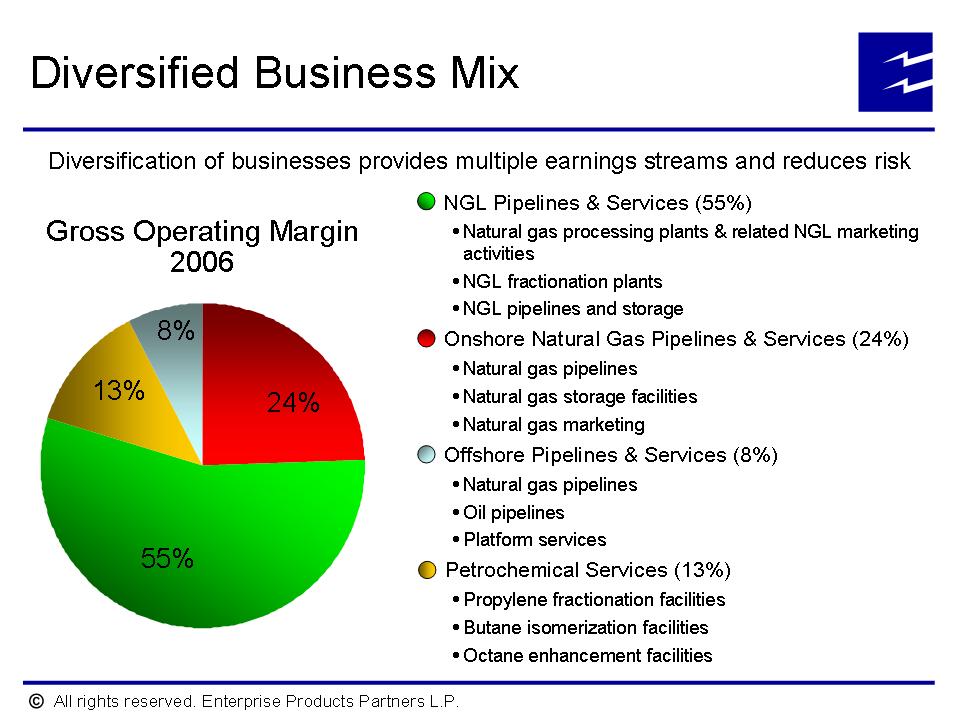

| Consistent Results from Diversified Businesses |

| Leadership in the Midstream Robert G. Phillips |

| Strategic Overview EPD owns one of the industry's leading midstream asset base Large geographic footprint touches 90% of natural gas production and 85% of reserves in lower 48 states Great market access for NGLs produced to 95% of ethylene capacity and 90% of motor gasoline refining capacity east of Rockies Unique integrated value chain concept promotes: Stronger earnings power Competitive positioning in corridors Linkage provides multiple service opportunities Benefit from affiliation with TEPPCO |

| Strategic Overview (continued) Organic growth investments designed to: Expand value chain Increase supply sources Improve market access Optimize capacity Maximize downstream economics New strategies focus on emerging trends / opportunities Unconventional natural gas plays - gathering Shift in NGL production from east to west - processing Shift in gas movements from west to east - transportation Increased volatility in gas pricing - storage Expansion of refining capacity - product distribution |

| Well Positioned for Growth |

| Access to High Growth Supply Regions |

| Multiple Value Chain Corridors |

| Western Value Chain |

| Offshore to Onshore Value Chain |

| Major Capital Projects in Service 2007 2007 is the culmination of several years of capital growth and development activities $2.5 billion new projects to be placed in-service in 2007 Generate significant incremental gross operating margin in 2007, primarily in 3rd and 4th quarters With the installation of Independence Hub / Trail, we have completed most of the major offshore projects initiated in 2003 - 2005 Commenced demand revenues this month ($44 million net to Enterprise annually for 5 years) Approximately $17 million per year in gross operating margin from volumetric fees for every 100 MMcf/d of average production |

| Shift in Focus to Rocky Mountain Region The Rocky Mountain Region has become EPD's next big regional growth strategy Approximately $1.9 billion in acquisitions completed and organic projects initiated since 2005 Attractive long-term fundamentals (long-lived reserves, low FD costs) Commitment by majors for exploration and production in Piceance Basin ExxonMobil recently announced that it will begin drilling 200 new wells next year to tap the estimated 35 Tcf of gas reserves in the Piceance Basin; will be their only land-based drilling operation planned in North America |

| New Projects and Emerging Strategies Barnett Shale / Gulf Crossing natural gas pipelines Unloads Texas Pipeline System; provides west to east bridge to access better markets Expands position in Barnett Shale region Expanded natural gas storage play Increased customer demand for seasonal storage Developing a Natural Gas Marketing organization to complement our successful NGL Marketing group Leverage existing expertise and significant portfolio of natural gas assets Provide customers with value-added solutions and flexibility while reducing Enterprise's operating costs |

| New Projects and Emerging Strategies Deepwater Trend miocene and lower tertiary crude oil developments Excess GOM oil pipeline capacity provides competitive advantage as production develops Increase services to expanding refinery sector Increased demand for blending products and offtake of co-products Increased demand for octane enhancement Continually link assets and optimize capacity utilization Leverage footprint Lower operating costs Maximize throughput |

| Natural Gas Pipelines / Storage and Offshore James H. Lytal |

| Gas Pipelines, Storage and Offshore Natural Gas Gathering and Transportation Provide best in class wellhead services Position for high growth developments Feed the value chain; maximize basis differentials Natural Gas Storage Economically expand existing facilities Link to existing infrastructure Benefit from increased demand / price volatility Offshore Pipelines and Platforms Implement final stages of Independence Project Ramp up oil volumes; develop miocene and lower tertiary play |

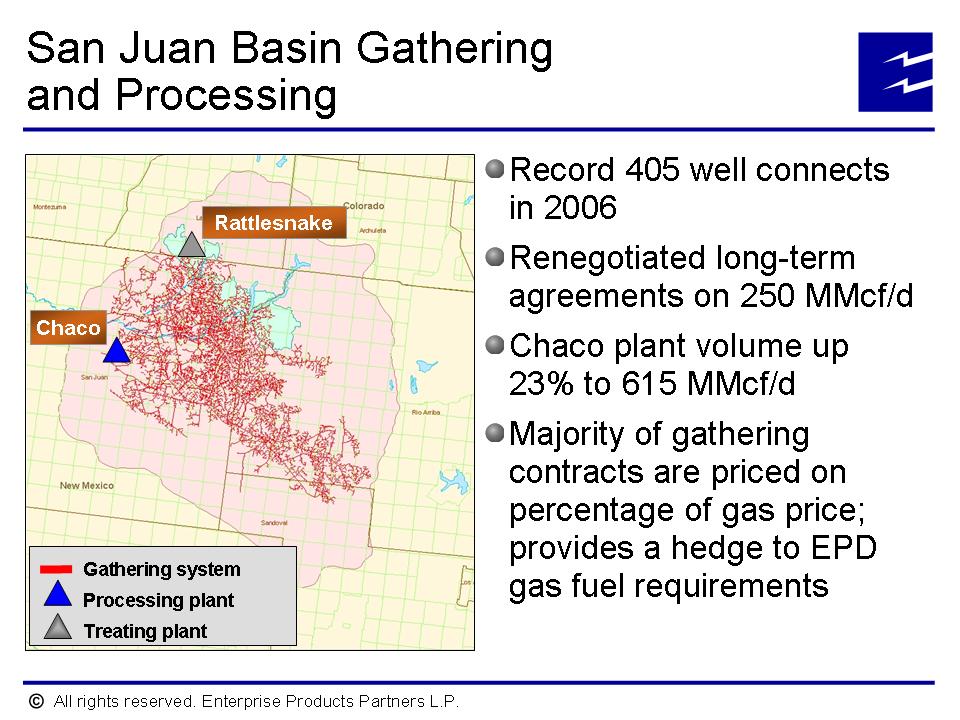

| San Juan Basin Gathering and Processing Record 405 well connects in 2006 Renegotiated long-term agreements on 250 MMcf/d Chaco plant volume up 23% to 615 MMcf/d Majority of gathering contracts are priced on percentage of gas price; provides a hedge to EPD gas fuel requirements |

| Texas Intrastate Pipeline System Over 8,000 miles of pipeline transporting 5 Bcf/d (gross) Connected to major cities and industrial complexes New long-term agreement with CenterPoint in Houston area Long-term extension of City of San Antonio contract Connected to all the major hubs Waha Hub Connected to 9 pipelines 1.6 Bcf/d of capacity Optionality provides for many supply sources Large basis between Waha and Houston Ship Channel |

| Significant Long-Term Gas Supply Multiple basins Low FD costs Largest processor in South Texas / Gulf Coast North Texas 36" provides bridge to eastern markets |

| LNG Supply New LNG facilities being built at Freeport and Beaumont / Port Arthur areas Freeport: 1.5 Bcf/d in 2008 Beaumont / Port Arthur: 2 Bcf/d in 2009 EPD well positioned with pipeline and gas storage assets to provide needed services |

| South Texas Gathering (Cerrito) Acquired in summer 2006 Fully integrated Improved run times and lower fuel and LAUF Approximately 200 Olmos wells planned in 2007 Large independents have acquired significant acreage to test shale play Potential for significant growth in rich gas volumes |

| Waha Gathering and Treating Morrow Gas Play Current production: 155 MMcf/d flowing to EPD Significant growth potential Major players: Anadarko, Forest, Chesapeake, Pogo West Texas Shale Play Early stages of development Thicker than the Fort Worth Shale Major players: Petro Hunt, Chesapeake, Encana, EOG Plan to expand system and integrate into the Texas Pipeline System |

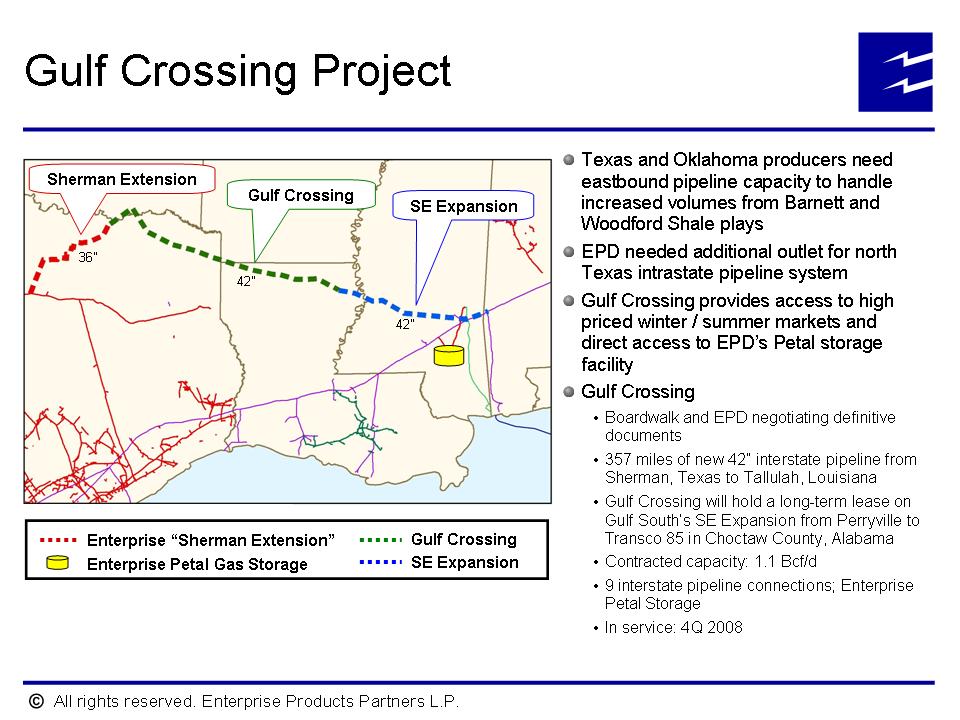

| Sherman Extension Project Barnett Shale Update New 1.1 Bcf/d, 178 mile pipeline extends EPD's Texas Intrastate System through growing Barnett Shale region Will connect with Boardwalk's Gulf Crossing project Long-term contracts with Devon Energy (largest Barnett Shale producer with volumes projected at over 1 Bcf/d by 2009 and 13.5 Tcf of reserve potential) Provides attractive export option for Waha (Permian) and Bossier (East Texas) producers In-service: 4Q 2008 |

| Gulf Crossing Project Texas and Oklahoma producers need eastbound pipeline capacity to handle increased volumes from Barnett and Woodford Shale plays EPD needed additional outlet for north Texas intrastate pipeline system Gulf Crossing provides access to high priced winter / summer markets and direct access to EPD's Petal storage facility Gulf Crossing Boardwalk and EPD negotiating definitive documents 357 miles of new 42" interstate pipeline from Sherman, Texas to Tallulah, Louisiana Gulf Crossing will hold a long-term lease on Gulf South's SE Expansion from Perryville to Transco 85 in Choctaw County, Alabama Contracted capacity: 1.1 Bcf/d 9 interstate pipeline connections; Enterprise Petal Storage In service: 4Q 2008 |

| Gas Storage Capacities Current and Projected (in Bcf) |

| Petal / Hattiesburg Gas Storage Converting 2 existing NGL caverns to natural gas Create 2.35 Bcf of capacity in 3Q 2007 Fully contracted 4.5 year payout Developing Petal #8 cavern Currently leaching new 5 Bcf cavern 2 Bcf subscribed long term Significant interest in remaining capacity New supply / market interconnects Gulf Crossing Southeast Supply Header (direct access to Florida markets) Interest in marketplace for additional 5 Bcf cavern |

| Wilson Gas Storage Developing Wilson #5 cavern Create 5.0 Bcf by 2Q 2009 55% contracted with CenterPoint deal (2.75 Bcf) New 30" pipeline Facility currently connected to EPD pipelines only Plan to build a new header pipeline to create storage hub New pipe connects provide for additional 5 Bcf expansion by late 2010 |

| Mont Belvieu Gas Storage Strong interest in Mont Belvieu gas storage generated by Open Season Low cost conversion of 4 caverns into 20 Bcf of natural gas storage Multiple interconnects provide a Hub service Located adjacent to EPD's Mont Belvieu NGL and petrochemical facilities Utilize to reduce corporate fuel costs Expect initial service in 2Q 2009 |

| Independence Project |

| World Class Achievements World deep-sea record setting Pipeline and riser (8,000 ft.) Platform (8,000 ft.) Subsea production (9,000 ft.) Record setting Largest GOM gas processing facility (1 Bcf/d) World's longest mooring lines (twelve lines, 2.4 miles each) Deepest water depth installation for suction pile World's largest monoethylene glycol (MEG) reclamation unit World's deepest pipeline inline future tie-in subsea structure World's largest single order for subsea umbilical |

| Installation and Final Steps for First Flow Towed to location at Mississippi Canyon 920 Installed mooring system Complete riser hang-offs Hydro test export line Pack linefill Complete umbilical connections Commission flow lines First flows expected in second half of 2007 |

| Positioned for Future Opportunities Producers tested numerous wells with over 50 MMcf/d Capacity anticipated to be filled early in 2008 Additional locations to be drilled when capacity is available Independence Hub is strategically located for future growth Lease Sale 181 comprises over 8 million acres and could yield significant resource potential |

| Benefits to Enterprise Expand our industry-leading deepwater infrastructure franchise Project to increase Gulf of Mexico natural gas production by 12% Opportunity to leverage our technical skills to provide industry solutions Experience from Marco Polo Major investment that should provide above average returns At full capacity, Independence could generate more than $200 million per year in gross operating margin Positions Enterprise for significant growth in the future |

| Deepwater Outlook - Miocene Trend Ownership in: Shelf-based oil pipelines with up to 1 MMBbls/d of capacity to Texas and Louisiana markets Over 600 MBPD of capacity in Deepwater oil gathering pipelines First flows from: Atlantis - late 2007 Neptune - early 2008 Shenzi - early 2009 9 additional discoveries that will most likely go to development |

| Deepwater Outlook - Lower Tertiary Well positioned for new Lower Tertiary (Wilcox) Trend 6 discoveries with an additional 7 active prospects Producer estimates are 3 - 15 billion Bbls of recoverable oil |

| NGL Services and Marketing and Natural Gas Services and Marketing A.J. Jim Teague |

| Strong NGL Industry Fundamentals 2006 was a strong year for NGLs characterized by record spreads in 2Q 2006 and 3Q 2006 Key factors are the economy and GDP growth, plant operating rates and gas-to-crude price ratio Ethane extraction increases as ethylene production increases History has shown that industry flexibility to switch off ethane cracking diminishes as ethylene production remains at 53 billion lbs/year or higher Gas-to-crude ratios and crack spreads are less of a factor as ethylene production rates remain at or greater than 53 billion lbs/year - currently at 54 billion lbs/year |

| NGL Services and Marketing EPD has created the industry's leading North American NGL value chain integrating gathering, processing, transportation, fractionation, storage and distribution assets Provides connectivity from major NGL supply sources to domestic petrochemical and refining markets and global LPG markets through our import / export facility NGL Services and Marketing leverages our NGL footprint to maintain throughput, increase profitability and create additional opportunities for growth along our value chain Benefits from long-term relationships and providing customers with multiple service options Disciplined approach to NGL Marketing requires compliance with flat book policy |

| Businesses Services: Gathering, processing, transportation, fractionation, storage, supply, etc. Marketing: Packaging of services that meet a customer's needs and brings value to both the customer and to Enterprise |

| Objectives (How?) Build long-term relationships To aggregate customers, both producers (supply) and consumers (demand); To create options around which we can optimize our system to create additional value; and To generate growth through expansion, extensions or joint ventures |

| NGL Footprint Facts Approximately 14,000 miles of NGL and petrochemical pipelines transporting 1.7 MMBbls/d in 2006 Approximately 9 Bcf/d net processing capacity in 25 facilities (including Pioneer and Meeker) 444 MMBbls/d of net fractionation capacity in 7 locations 162 MMBbls of storage in 10 states 20 MBbls/hour import capacity; 7 MBbls/hour export capability NGL Marketing and Services handles over 1,200 MBPD across all EPD and third-party assets |

| NGL System Defining Characteristics Mont Belvieu Hub Anchors NGL system Largest NGL fractionation complex Largest storage network Largest distribution system International reach Swing strength of footprint Storage in multiple locations Wheeling through supply source diversity Arbitrage through system reach Wealth of information Enterprise serves every NGL application and the largest producing basins |

| NGL System Defining Characteristics Unparalleled Supply System Green River Permian Western Canada Piceance Mid-Continent International Uintah South Texas Four Corners Gulf of Mexico Premier Market Connectivity Refinery Concentration National Footprint Petrochemical Access International Reach Heating Market |

| 2007 NGL System |

| U.S. Waterborne LPG Import Growth |

| 2006 U.S. LPG Imports by Terminal |

| NGL System Connectivity Gulf Coast Refinery Services |

| NGL System Connectivity Gulf Coast Petrochemical Services |

| 1998 at IPO |

| 2000 NGL System Tejas NGL acquisition from Shell included ownership in 10 gas processing facilities, 2 NGL fractionators, 20% interest in Dixie Pipeline and Louisiana Pipeline System Completed construction of a refrigerated export facility joint venture on the Houston Ship Channel |

| 2001 Lou-Tex NGL Pipeline Completed construction of Lou-Tex NGL Pipeline providing connectivity between the NGL markets in Texas and Louisiana |

| 2002 Diamond-Koch Storage Acquired 64 MMBbls of NGL storage in Mont Belvieu from Diamond-Koch that included 25 wells and associated distribution pipelines |

| 2002 Mid-America and Seminole Pipelines Acquired the Mid-America (MAPL) and Seminole Pipelines and northeastern terminals from Williams which connects the Rocky Mountains and Central United States with the Gulf Coast |

| 2004 GulfTerra Merger |

| 2005 Ferrellgas Storage and Dixie Pipeline Acquisitions Acquired 3 NGL storage facilities in Arizona, Utah and Kansas, and 4 terminals in Minnesota and North Carolina from Ferrellgas Acquired additional 46% interest in Dixie Pipeline and assumed operatorship |

| 2006 / 2007 Rockies Growth Constructing the 750 MMcf/d Pioneer gas processing facility in southwest Wyoming with completion in October 2007 Acquired interest in Jonah Gas Gathering System and currently expanding capacity to 2.3 Bcf/d with completion by late 2007 |

| 2006 / 2007 Rockies Growth Acquired Piceance Creek Gathering System from EnCana with 1.6 Bcf/d of capacity and extends through the heart of the Piceance Basin to the Meeker gas processing facility Constructing a 750 MMcf/d gas processing facility in Meeker, Colorado with Phase I completion in July 2007 and an additional 750 MMcf/d of Phase II capacity scheduled for July 2008 Constructing 200 MMcf/d treating and conditioning facilities for ExxonMobil with dedication |

| 2006 / 2007 Mid-Continent Growth Constructing new NGL fractionator in Hobbs, New Mexico with 75 MBPD capacity for Rocky Mountains growth and operational in September 2007 Constructing new 70-mile batch-service pipeline from Hobbs to Odessa to exclusively supply Huntsman / Flint Hills ethylene facility with ethane and propane; completion by May 2008 Expanding MAPL Central System to optimize north and south flexibility |

| 2006 / 2007 Texas Growth Acquired South Texas 16" Pipeline from ExxonMobil extending from Corpus Christi to South Houston Houston 8" NGL pipeline converted to ethane service January 1, 2006 with capacity of 31 MBPD |

| 2007 NGL System Connectivity to 95% of U.S. ethylene plants Connectivity to 90% of all refineries east of the Rockies |

| NGL Marketing Support of Asset Growth |

| Natural Gas Services and Marketing |

| Vision EPD has a unique opportunity to apply the same business concepts to create a leading North American natural gas services and marketing business Leverage an impressive set of natural gas assets that increasingly are linked through our value chain concept Create opportunities to increase throughput, enhance profitability and expand customer services Follows the same disciplined format as NGL Services and Marketing |

| Objectives (How?) Build long-term relationships To aggregate customers, both producers (supply) and consumers (demand); To create options around which we can optimize our system to create additional value; and To generate growth through expansion, extensions or joint ventures |

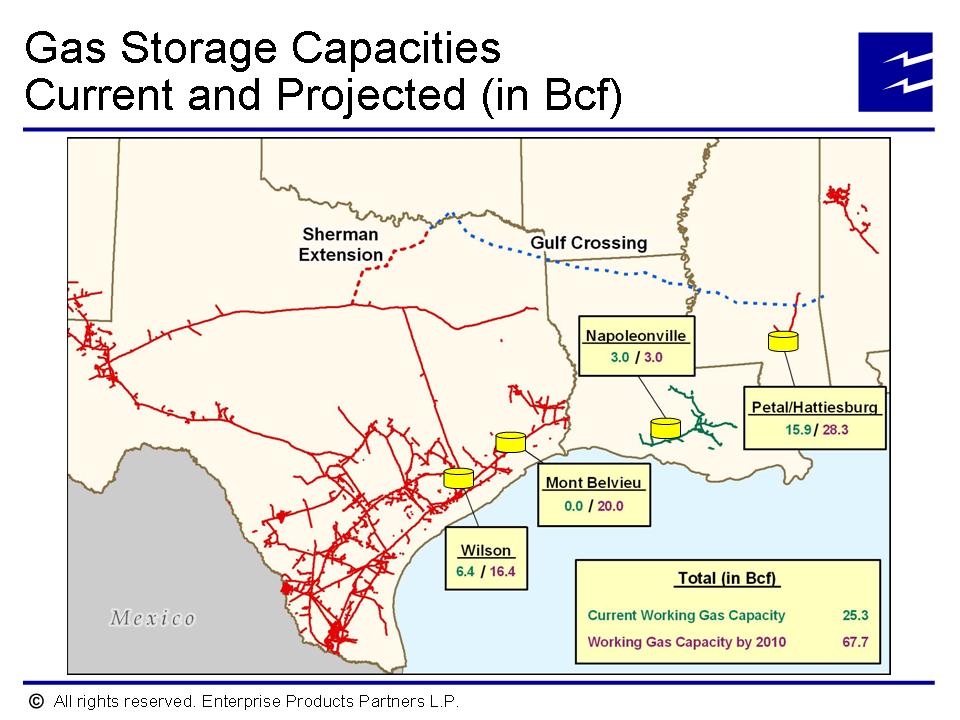

| Natural Gas Footprint Facts Over 20,400 miles of onshore and offshore natural gas pipelines (including Independence Trail) 25 Bcf of current storage capacity growing to approximately 68 Bcf by 2012 9 Bcf/d of equity processing capacity EPD's natural gas assets handle current total gross throughput of 10.5 Bcf/d (20% of current U.S. production) Current merchant activity on EPD assets is 600 MMcf/d (6% of total current gross volumes) Current system fuel and plant PTR requirements are approximately 350 MMcf/d (3.5% of total current gross volumes) |

| Defining Characteristics Strong supply system Excellent market connectivity Swing capability of footprint Wealth of information |

| Natural Gas System Strong Supply System |

| Rocky Mountain Market Connectivity |

| Louisiana / Mississippi / Gulf of Mexico Market Connectivity Pipeline Interconnects 14 interconnects with 8 interstate pipelines 8 interconnects with 4 intrastate pipelines Storage at Petal and Napoleonville Sherman / Gulf Crossing Project |

| Texas Pipeline System Market Connectivity Texas Pipeline System 51 interconnects with 14 interstate pipelines 53 interconnects with 8 intrastate pipelines Storage at Wilson and Mont Belvieu Sherman / Gulf Crossing Project Industrial users on Houston Ship Channel, Corpus Christi Ship Channel, Beaumont / Port Arthur / Orange Corridor Local distribution companies Power generators Independent power producers Mexico |

| Natural Gas System Swing strength of footprint Storage in key locations Wheeling through supply source diversity Arbitrage through system reach Wealth of information Enterprise serves every kind of application and the largest producing basins |

| Conclusion As EPD continues to expand its extensive footprint through organic projects and selected acquisitions our Marketing and Services groups will add value through optimization and optionality We will maintain a disciplined approach consistent with our asset based value chain concept Increased marketing capabilities in natural gas should lead to more growth opportunities through expansions, extensions and joint ventures |

| FERC Regulated NGL Pipelines James M. Collingsworth |

| MAPL, Seminole and Dixie Pipelines |

| Overview Regulated NGL Pipelines consists of 5 businesses Mid-America Pipelines Northern System Central System Rocky Mountain System Seminole Pipeline Company Dixie Pipeline Company Enterprise Terminaling and Storage Company Dixie Terminaling and Storage Company |

| Northern System 2,740 pipeline miles Terminals 15 ETS terminals 2 EPOLP terminals 9 third-party terminals Annual transport volumes E/P mix: 23 - 25 MMBbls Propane: 16 - 20 MMBbls Heavies: 6 - 8 MMBbls |

| Northern Propane System Growth Initiatives Potential increase in propane receipts in Cochin Expansion of the West Blue pipeline segment from Mankato to Pine Bend Increase Heavies capacity to Pine Bend area Potential for expansion in the Diluent market Increase in natural gasoline deliveries for the ethanol denaturant market |

| Northern System Rate Case Northern system has historically provided very competitive shipper rates resulting in under collection of costs and return (FERC 38) Filed new rates in June 2006 (FERC 41) to resolve rate issues and determine the FERC allowable Cost of Service General Commodity Rates (GCR) establishes room for future increases Seasonal Discount Rate (SDR), effectively an incentive rate, which is being charged shippers subject to refund Deferred revenue currently is $18 MM, increasing by $20 MM/year Shipper protests and lengthy settlement discussions lead to FERC hearing October 2007 Filed Cost of Service 28% above current SDR; 9% above GCR |

| Central System 190-mile expansion was completed in February ahead of schedule and within budget Increase MAPL's bi-directional capacity from Conway to Hobbs by 1.5 MBPM Having bi-directional flow capabilities from Conway to Hobbs allows Shippers to capture the arbitrage between the Conway and Mont Belvieu markets Additional new connections: ConocoPhillips Spearman Lovington Pipeline Loop Carrera Indian Creek Plant Penn Virginia Spearman Plant |

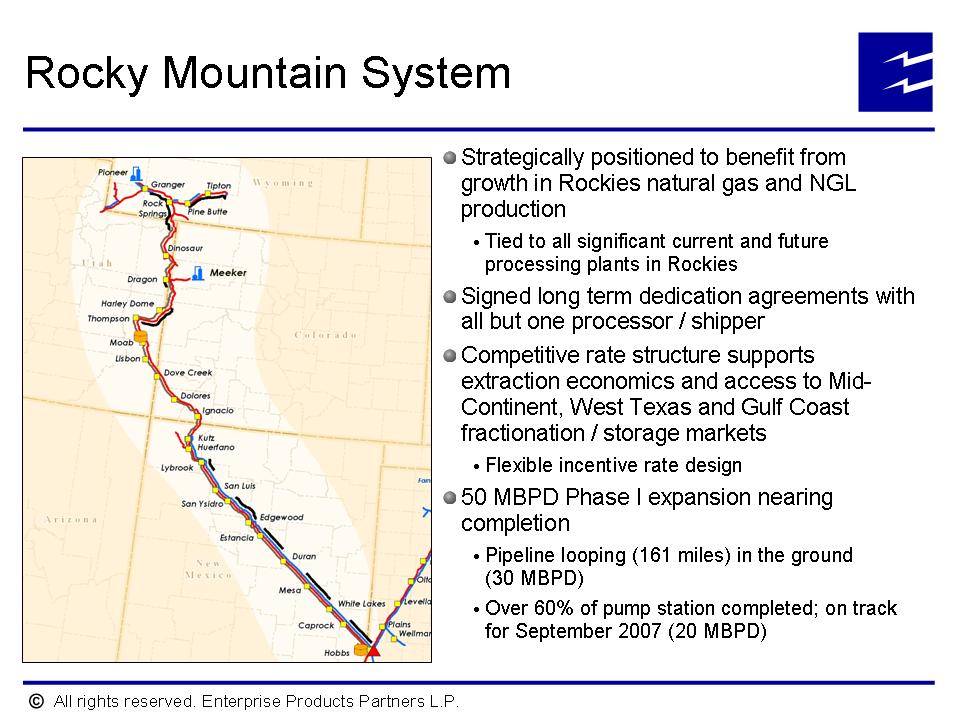

| Rocky Mountain System Strategically positioned to benefit from growth in Rockies natural gas and NGL production Tied to all significant current and future processing plants in Rockies Signed long term dedication agreements with all but one processor / shipper Competitive rate structure supports extraction economics and access to Mid-Continent, West Texas and Gulf Coast fractionation / storage markets Flexible incentive rate design 50 MBPD Phase I expansion nearing completion Pipeline looping (161 miles) in the ground (30 MBPD) Over 60% of pump station completed; on track for September 2007 (20 MBPD) |

| Competitive Analysis MAPL's 2007 scheduled volume growth Opal Expansion 1Q 15-20 MBPD Meeker 3Q 30 MBPD Chapita 3Q 4 MBPD Pioneer 4Q 17 MBPD Total 66-71 MBPD Competition with Overland Express (2Q 2008) - MAPL advantages Significant shipper dedications with PPI escalator Full EPD value chain to attract new supply sources Jonah / Pinedale, Piceance, San Juan Greater market access - Hobbs, Conway, Mont Belvieu Better flow assurance Multiple lines in right-of-way More Y-grade storage capacity MAPL's long-term forecast 260 MBPD by 2008 (Meeker I, Pioneer, Stage Coach, Kanda) 290 MBPD by 2009 (Meeker II, Piceance and Uintah growth) |

| Seminole Pipeline 90% owned by Enterprise / 10% owned by INEOS 540-mile Northern segment capable of transporting 180 MBPD of Y-grade into Mont Belvieu 635-mile Southern segment will evolve to a purities system moving 135 MBPD into Mont Belvieu Growth initiatives In April, Seminole will be capable of delivering 135 MBPD from West Texas and 120 MBPD from Mont Belvieu into INEOS' petrochemical complex at Stratton Ridge |

| Dixie Pipeline 1,370 mile pipeline from Mont Belvieu to Apex, North Carolina 220 MBPD of capacity with average daily flow rate of 102 MBPD Ownership 74% Enterprise 26% BP Growth initiatives Withdrew terminals and storage locations from FERC rate base and placed them in an unregulated company which positions them better to capitalize on market opportunities |

| Petrochemical Services Gil H. Radtke |

| 2007 Petrochemical Outlook Petrochemicals (billion pounds and growth) Ethylene US Global 06 Demand 55 3.1% 242 5.1% 07 Forecast 55 0.5% 251 3.8% Propylene 06 Demand 36 2.5% 159 5.5% 07 Forecast 37 2.3% 168 5.8% Big concentration of new ethylene crackers in Middle East. Far East and Europe expected to absorb this new production until 2009. Capital costs have doubled and tripled in some cases for some of these new facilities. |

| Petrochemical Services Overview Petrochemical segment consists of 5 businesses Butane isomerization (116 MBPD capacity) Propylene fractionation (currently 4.4 billion pounds or 65 MBPD, net capacity) Mont Belvieu hydrocarbon storage (104 MMbbls of usable capacity) Propylene and HP isobutane pipelines Octane enhancement (currently 12 MBPD capacity) |

| 2007 Mont Belvieu Growth Initiatives Pipelines Expanding propylene feedstock capability from Texas City Propylene feedstock from Port Arthur area South Texas NGL pipeline Storage Services Upgrading product handling facilities for increased volumes, new connections and new products Natural gas storage Refined product storage OTI and DIB expansions Propylene Fractionation Expanding capacity by 1.0 billion pounds (15 MBPD) Evaluating export expansion Octane Enhancement Convert existing Morgan's Point facility to produce isooctane |

| Butane Isomerization Service Isomerization is the process of converting normal butane to high purity isobutane EPD has a combined capacity of 116 MBPD 57 MBPD (49%) is committed under long-term third-party processing contracts with escalation provisions on the fees and 20 MBPD is used as feedstock for our octane enhancement facility Variations in volumes are typically caused by plant turnarounds and spot opportunities, but overall results are very steady |

| Isomerization Business Outlook Stable demand from long-term contracts base loads isomerization business EPD has available capacity to service future growth in isobutane demand and seasonal demand for gasoline without investing new capital Expect increase in demand for isobutane as premium gasoline components such as isooctane and alkylate will be required for blending into gasoline (isobutane is major component of isooctane and alkylate) |

| Propylene Fractionation Propylene splitters take refinery-grade propylene (RGP) and fractionate it into polymer-grade propylene (PGP) or chemical-grade propylene (CGP) and propane RGP is typically 60-75% propylene with the balance primarily propane RGP is referred to in barrels per day (BPD) of feed and PGP is referred to in millions of pounds (MMlbs) of production One barrel of propylene is equal to approximately 183 lbs. |

| Propylene Assets We own and operate 3 polymer-grade propylene fractionation (splitter) facilities with approximately 4.8 billion pounds per year (72 MBPD) of polymer-grade propylene production capacity (our share is 3.9 billion pounds) Basell owns approximately 45% of Splitter 1 and leases this capacity to us TOTAL Petrochemical owns 33% of Splitter 3 and takes its share of production to its polypropylene facility in LaPorte, Texas All 3 facilities are located at our Mont Belvieu site and are integrated into our other facilities including underground storage We own a 30% interest in a 1.5 billion pounds per year (22.5 MBPD) chemical-grade propylene splitter in Baton Rouge, Louisiana EPD designed, constructed and operates the facility ExxonMobil has 70% ownership, is the business manager, supplies the feedstock and is the major customer |

| Combined Propylene Systems |

| Propylene Outlook Propylene primarily sourced from refineries (to splitters) and as a co-product from steam crackers 2007 world demand expected to be 168 billion pounds 2007 North American demand expected to be 37 billion pounds World propylene demand expected to grow at roughly 5-6% per year and U.S. growth expected to be 2-3% per year (grows faster than ethylene) Future steam cracker investments insufficient to meet demand (mostly ethane based with low propylene yield) U.S. refinery expansions will help feed the demand growth |

| Propylene Expansion Includes the necessary improvements to pipelines, storage and measurement facilities Capacity: 1.0 billion pounds Expandable to 1.5 billion pounds Completion in 3Q 2007 Utilization ramping up to 60% in 2008, 80% in 2009 and 100% in 2010 forward Processing and sales margins of 3.1 cents per pound Incremental operating costs of 0.9 cents per pound |

| Mont Belvieu Storage Services Own and operate over 100 MMBbls of underground storage capacity at Mont Belvieu These storage facilities are interconnected by multiple pipelines to other producing and offtake facilities throughout the Gulf Coast, as well as connections to the Rocky Mountain and Midwest regions via the Seminole Pipeline and the TEPPCO mainline Focal point on the Gulf Coast for NGL and Olefins Very stable storage revenues from reservation fees (62%) and throughput fees (38%) |

| Mont Belvieu Storage Outlook Growth tied to petrochemical, refinery and NGL fractionation markets as well as imported NGL and our Western expansion Storage expansion tied to this growth, as well as new product storage opportunities for natural gas and refined products Well optimization plan will allow us to better utilize existing and future facilities Have filed request with the Texas RRC for a permit to allow for 6 existing NGL caverns and 5 future caverns to be used either for NGL / refined products or natural gas service |

| Octane Enhancement EPD owns a facility at Mont Belvieu that produces octane additives for motor gasoline Produced and sold isooctane in 2006 under contract at NYMEX RBOB plus pricing Allowed us to hedge our sales through 4Q 2006 We expect to execute the same hedge program in 2007 Also produce isobutylene mix for use as an additive for lube oil blending This contract priced at normal butane plus |

| Isooctane Only the second plant of its kind in the world; in place in advance of the phase out of MTBE Isooctane capacity: 12 MBPD Feedstock comes from our isomerization business Requires 2 gallons of high-purity isobutane to produce 1 gallon of isooctane Engineering work underway for the restart of sister facility at Morgan's Point with capacity to produce 9 MBPD of isooctane |

| Ethanol Drives Demand for Isooctane 2005 Energy Bill effectively removed MTBE from U.S. gasoline market Significant octane loss with 6.0 lbs. vapor pressure Corresponding Renewable Fuels Standard (RFS) mandated ethanol usage Blends to higher vapor pressure of 15.0 lbs. Forces removal of higher vapor pressure components from gasoline blending such as butanes and pentanes Refineries need new blending components that combine high octane and very low vapor pressure Isooctane combines 99.5 octane with 2.0 lbs. vapor pressure |

| 2007 Gasoline and Ethanol Outlook Gasoline (MMBPD and growth) 06 Demand 9.2 1.2% 07 Forecast 9.3 1.4% Ethanol (Billion Gallons) As more ethanol plants come on stream in 2007 and more ethanol is blended into gasoline, demand for alkylate and isooctane will increase. This benefits both the isooctane and the isom facilities. |

| Ethanol Capacity and Renewable Fuel Standard |

| Financial Overview Michael A. Creel |

| EPD Delivers Record 2006 Results Gross Operating Margin 2006 vs. 2005 NGL Pipelines and Services up 30% due in part to record pipeline volumes, improved processing and fractionation margins Onshore Natural Gas Pipelines and Services down 6% despite volume and margin increases at Texas intrastate which was more than offset by lower gathering fees in San Juan for percent of index gathering contracts and repair expenses at Wilson storage facility Offshore Pipelines and Services up 33% due to increased oil and gas volumes after 2005 hurricanes Petrochemical Services up 37% due to strong demand by petrochemical industry and refinery demand for motor gasoline additives 2006 gross operating margin includes approximately $64 million of recoveries under business interruption insurance |

| Major Organic Growth Projects Expected Start Dates and Cumulative Investment |

| History of Financial Discipline 56% of Growth Investment Funded with Equity |

| Realizing Benefits of Eliminating GP's 50% Splits Landmark action taken by EPD's GP in December 2002 to eliminate GP's 50% IDR for no consideration is beginning to provide significant benefits to debt and equity investors 4Q 2006 annualized savings of $87 million Cumulative savings of $108.6 million 36% of DCF retained in partnership since GTM merger is attributable to elimination of 50% IDR Enhances EPD's financial flexibility by retaining cash flow for debt retirement, fund growth and distribution increases Results in significantly lower long-term cost of capital and greater cash accretion from capital projects and acquisitions |

| History of Financial Discipline Managing Distributable Cash Flow |

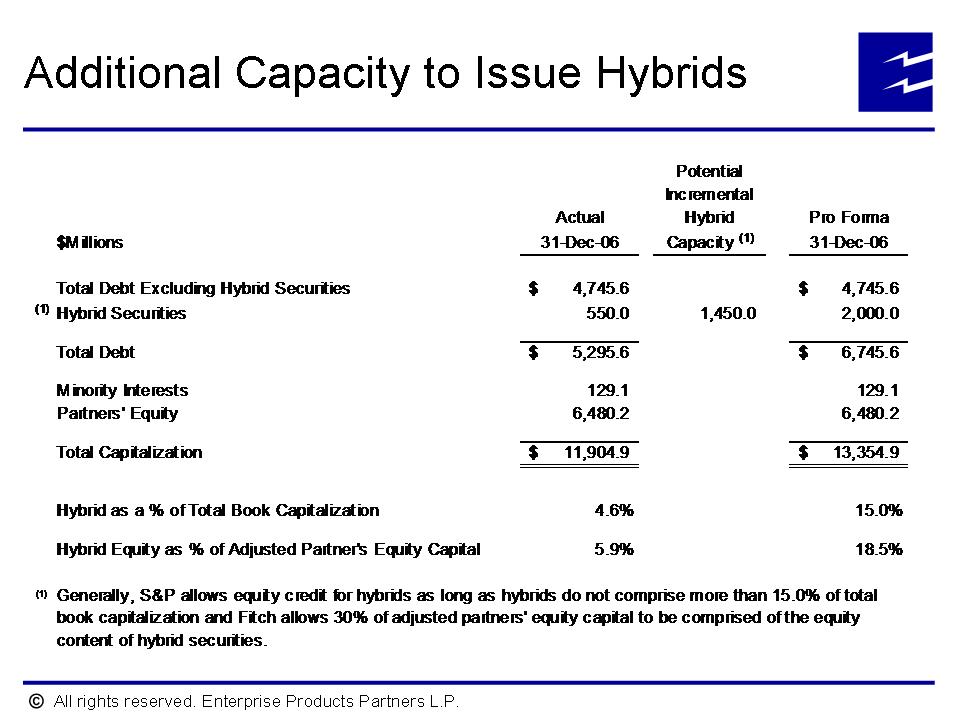

| Issuance of Hybrids Provides Additional Financial Flexibility Description $550 Million Principal Amount Long-Term Subordinated Notes (LoTSSM) - 60 Year Maturity; Fixed coupon 8.375% first 10 years Partial equity treatment by rating agencies 75% Fitch; 50% Moody's and SP Allow 10-15% of book capitalization in Hybrids EPD Rationale Provide financial flexibility by broadening and diversifying sources of debt and equity capital Partial equity treatment by rating agencies, allows for larger security issuances and reduces reliance on traditional equity markets Provide additional layer of protection for senior debt holders |

| Additional Capacity to Issue Hybrids |

| DEP Financial Objectives Facilitate growth objectives of the Enterprise family of partnerships Enable EPD to contribute assets to DEP for cash and / or units while maintaining control of assets, value chain benefits and redeploying proceeds into projects with higher returns Enhance the Enterprise position in pursuing acquisitions and projects in competitive environments Minimize the volatility of cash flow by managing the successful execution of Duncan Energy Partners' business strategy Invest in organic growth, pursue acquisitions of assets and businesses from related and third parties to generate additional cash flow Manage capital to provide financial flexibility for DEP while providing its investors with an attractive total return Maintain a strong balance sheet and conservative leverage ratios |

| Indicative Benefit to EPD from Initial Drop down to DEP |

| On Target to Fund Growth |

| Strong Financial Position at December 31, 2006 |

| EPD's Model for Sustained Growth Financial discipline and investment grade balance sheet Lower cost of capital than most of peer group due to 25% cap of GP IDRs at EPD and no GP IDRs at DEP Already funded more than 50% of 2006 and 2007 growth capital expenditures with 2006 equity offerings, hybrids, DRP, reinvested DCF and 2007 equity proceeds from DEP IPO Existing liquidity, hybrid capacity and DEP provide flexibility and are more than sufficient to fund remainder of 2007 growth capital plans |

| 2007 Outlook Another year of strong operating fundamentals $2.5 billion of new projects begin operations $44 million of annualized demand charges net to EPD at Independence Hub platform began mid-March 2007 First production to Independence and majority of other projects expected to commence in 2H 2007 and start to contribute cash flow late 2007 and 2008 Ramp up of new projects in 2007 are key for improving on record 2006 performance New opportunities to invest in organic growth projects that integrate with our large base of assets Increase distribution rate to partners at year end 2007 to $1.99/unit based on current expectations |

| 10 Largest Energy Partnerships Ranked by Enterprise Value(1) |

| 10 Largest Energy Partnerships Ranked by Average Daily Trading Volume(1) |

| Proven Growth, Superior Returns |

| Reconciliations |

| Non-GAAP Reconciliations |

| Non-GAAP Reconciliations |

| Non-GAAP Reconciliations |

| Non-GAAP Reconciliations |

| Non-GAAP Reconciliations |