UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File No. 811-08777

CREDIT SUISSE HIGH YIELD BOND FUND

(Exact Name of Registrant as Specified in Charter)

Eleven Madison Avenue, New York, New York 10010

(Address of Principal Executive Offices) (Zip Code)

John G. Popp

Credit Suisse High Yield Bond Fund

Eleven Madison Avenue

New York, New York 10010

Registrant’s telephone number, including area code: (212) 325-2000

Date of fiscal year end: October 31st

Date of reporting period: November 1, 2021 to October 31, 2022

Item 1. Reports to Stockholders.

Credit Suisse High Yield Bond Fund

Eleven Madison Avenue

New York, NY 10010

Trustees

Steven N. Rappaport

Chairman of the Board

Laura A. DeFelice

Jeffrey E. Garten

Mahendra R. Gupta

John G. Popp

Officers

John G. Popp

Chief Executive Officer and President

Thomas J. Flannery

Chief Investment Officer

Rachael Hoffman

Chief Compliance Officer

Lou Anne McInnis

Chief Legal Officer

Omar Tariq

Chief Financial Officer and Treasurer

Karen Regan

Senior Vice President and Secretary

Investment Adviser

Credit Suisse Asset Management, LLC

Eleven Madison Avenue

New York, NY 10010

Administrator and Custodian

State Street Bank and Trust Co.

One Lincoln Street

Boston, MA 02111

Shareholder Servicing Agent

Computershare Trust Company, N.A.

P.O. Box 43006

Providence, RI 02940-3078

Legal Counsel

Willkie Farr & Gallagher LLP

787 7th Avenue

New York, NY 10019

Independent Registered Public Accounting Firm

PricewaterhouseCoopers LLP

300 Madison Avenue

New York, NY 10017

Credit Suisse

High Yield Bond Fund

ANNUAL REPORT

October 31, 2022

Credit Suisse High Yield Bond Fund

Annual Investment Adviser’s Report

October 31, 2022 (unaudited)

December 4, 2022

Dear Shareholder:

We are pleased to present this Annual Report covering the activities of the Credit Suisse High Yield Bond Fund (the “Fund”) for the 12-month period ended October 31, 2022.

Performance Summary

11/01/21 – 10/31/22

| | | | |

| Fund & Benchmark | | Performance | |

Total Return (based on net asset value (“NAV”))1 | | | (14.19 | %) |

Total Return (based on market value)1 | | | (22.10 | %) |

ICE BofA US High Yield Constrained Index2 | | | (11.44 | %) |

Market Review: Inflation and Uncertainty

The annual period ended October 31, 2022, was negative for the high yield market, as broad-based inflation led to a tightening of financial conditions across much of the developed world, pressuring the predominantly fixed-rate high yield asset class. The ICE BofA US High Yield Constrained Index (the “Index”), the Fund’s benchmark, lost 11.4% for the period.

While 2021 was a strong year for risk assets in general, 2022 started off poorly due in part to heightened expectations for central bank interest rate hikes. Throughout the year, economic conditions and investor sentiment soured as the Russian invasion of Ukraine intensified and knock-on effects of the COVID-19 pandemic continued to drive inflationary forces and disrupt global supply chains. Alongside a series of escalating federal funds rate hikes, the 10-year U.S. Treasury rate widened by 249 basis points over the period. Within this context, the floating nature of the bank loan asset class proved to be more resilient.

Overall, yields within the Index increased significantly to end the period at 8.97%—476 basis points wider than on October 31, 2021—while spreads widened to +471 basis points on October 31, 2022 versus +328 basis points on October 31, 2021.

For the period, CCC-rated bonds severely underperformed the Index, losing 15.5%. Conversely, B-rated and BB-rated bonds outperformed, although they still delivered negative absolute returns of -10.5% and -11.1%, respectively.

From an industry perspective, oil field equipment and services, oil refining and marketing, and multi-line insurance were the best performing sectors, returning 2.5%, 2.5% and -5.0%, respectively. In contrast, the worst performing sectors included discount stores, pharmaceuticals, and life insurance, returning -29.1%, -28.2% and -23.1%, respectively.

Default rates remained below long-term historical averages over the annual period, although there was a noticeable increase in distressed activity throughout 2022. According to JP Morgan Chase & Co., the trailing 12-month default rate, including distressed exchanges, ended the period at 1.59%—up 123 basis points since the beginning of 2022, but still well below its long-term average of 3.2%. We anticipate default activity to continue to increase in the near-term due to less favorable capital markets conditions.

After a very strong period of inflows in 2020—with mutual funds bringing in $44.9 billion—flows turned negative in 2021 and worsened in 2022. Year-to-date outflows totaled $51.1 billion as of October 31, 2022, compared to $12.4 billion of outflows in the comparable period of 2021, and $13.2 billion of outflows for all of 2021.

Capital markets activity has deteriorated in 2022 due to rising rates and declining risk appetites. Year-to-date, high yield issuance has totaled $95.1 billion, down approximately 78% compared to the same period in the prior year.

1

Credit Suisse High Yield Bond Fund

Annual Investment Adviser’s Report (continued)

October 31, 2022 (unaudited)

Strategic Review and Outlook: Cautiously optimistic

For the 12-month period ended October 31, 2022, the Fund underperformed the benchmark. For the period, the greatest contributor to relative returns from a ratings perspective came from B-rated investments. Additionally, portfolio returns benefitted from allocations to bank loans and collateralized loan obligations, while the allocation to high yield detracted from relative returns. From a sector perspective, positive selection in leisure, technology and retail were the greatest contributors to relative returns, while negative selection in services and allocations to information technology, healthcare, and media/telecommunications detracted from returns.

The high yield market has experienced significant pressure over the last year. The current inflationary environment has proven to be sticky, leading many central banks to accelerate interest rate hikes amidst an already challenging economic backdrop. In our view, the volatility to date has created unique opportunities, but with higher prices for goods and services as well as increasing borrowing costs expected to hamper corporate earnings growth, we remain cautious. Importantly, however, we see relatively healthy balance sheets and a manageable maturity schedule in the U.S. leveraged debt markets. We believe credit selection is paramount as certain industries and business models are more prone to demand and margin contractions.

| | |

Thomas J. Flannery Chief Investment Officer* | | John G. Popp Chief Executive Officer and President** |

High yield bonds are lower-quality bonds that are also known as “junk bonds.” Such bonds entail greater risks than those found in higher-rated securities.

The Fund is non-diversified, which means it may invest a greater proportion of its assets in securities of a smaller number of issuers than a diversified fund and may therefore be subject to greater volatility.

In addition to historical information, this report contains forward-looking statements, which may concern, among other things, domestic and foreign markets, industry and economic trends and developments and government regulation, and their potential impact on the Fund’s investments. These statements are subject to risks and uncertainties and actual trends, developments and regulations in the future, and their impact on the Fund, could be materially different from those projected, anticipated or implied. The Fund has no obligation to update or revise forward-looking statements.

The views of the Fund’s management are as of the date of this letter and the Fund holdings described in this document are as of October 31, 2022; these views and Fund holdings may have changed subsequent to these dates. Nothing in this document is a recommendation to purchase or sell securities.

2

Credit Suisse High Yield Bond Fund

Annual Investment Adviser’s Report (continued)

October 31, 2022 (unaudited)

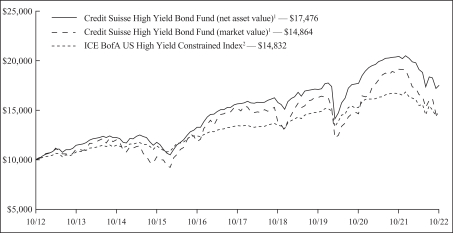

Comparison of Change in Value of $10,000 Investment in the

Credit Suisse High Yield Bond Fund1 and the

ICE BofA US High Yield Constrained Index2 For Ten Years

| 1 | Assuming reinvestment of distributions. |

| 2 | The ICE BofA US High Yield Constrained Index (the “Index”) is an unmanaged index that tracks the performance of below investment-grade U.S. dollar-denominated corporate bonds issued in the U.S. domestic market, where each issuer’s allocation is limited to 2% of the Index. The Index does not have transaction costs and investors cannot invest directly in the Index. |

| * | Thomas J. Flannery, Managing Director, is the Head of the Credit Suisse U.S. High Yield Management Team. Mr. Flannery joined Credit Suisse Asset Management, LLC (“Credit Suisse”) in June 2010. He is a portfolio manager for the Credit Investments Group (“CIG”) with responsibility for trading, directing investment decisions, originating and analyzing investment opportunities. Mr. Flannery is also a member of the CIG Credit Committee and is currently a high yield bond portfolio manager and trader for CIG. Mr. Flannery joined Credit Suisse AG in 2000 from First Dominion Capital, LLC where he was an Associate. Mr. Flannery holds a B.S. in Finance from Georgetown University. |

| ** | John G. Popp is a Managing Director of Credit Suisse and Group Head and Chief Investment Officer of CIG, with primary responsibility for making investment decisions and monitoring processes for CIG’s global investment strategies. Mr. Popp also serves as Trustee, Chief Executive Officer and President of the Credit Suisse Funds, as well as serving as Director, Chief Executive Officer and President for the Credit Suisse Asset Management Income Fund, Inc. and Trustee, Chief Executive Officer and President of the Credit Suisse High Yield Bond Fund. Mr. Popp has been associated with Credit Suisse since 1997. |

3

Credit Suisse High Yield Bond Fund

Annual Investment Adviser’s Report (continued)

October 31, 2022 (unaudited)

Average Annual Returns

October 31, 2022 (unaudited)

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 3 Years | | | 5 Years | | | 10 Years | |

Net Asset Value (NAV) | | | (14.19)% | | | | 0.78% | | | | 2.27% | | | | 5.74% | |

Market Value | | | (22.10)% | | | | (2.93)% | | | | (0.37)% | | | | 4.04% | |

Credit Suisse may waive fees and/or reimburse expenses, without which performance would be lower. Waivers and/or reimbursements are subject to change and may be discontinued at any time. Returns represent past performance and do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total investment return at NAV is based on the change in the NAV of Fund shares and assumes reinvestment of dividends, capital gains, and return of capital distributions, if any, at prices pursuant to the Fund’s dividend reinvestment program. Total investment return at market value is based on the change in the market price at which the Fund’s shares traded on the NYSE American during the period and assumes reinvestment of dividends, capital gains, and return of capital distributions, if any, at prices pursuant to the Fund’s dividend reinvestment program. Because the Fund’s shares trade in the stock market based on investor demand, the Fund may trade at a price higher or lower than its NAV. Therefore, returns are calculated based on NAV and share price. Past performance is no guarantee of future results. The current performance of the Fund may be lower or higher than the figures shown. The Fund’s yield, return, NAV and market price will fluctuate. Performance information current to the most recent month end is available by calling 1-800-293-1232.

The annualized gross and net expense ratios are 2.38% and 2.20%, respectively.

Credit Quality Breakdown*

(% of Total Investments as of October 31, 2022)

S&P Ratings**

| | | | |

BBB | | | 0.9 | % |

BB | | | 29.8 | |

B | | | 35.9 | |

CCC | | | 23.5 | |

CC | | | 0.1 | |

NR | | | 6.9 | |

| | | | |

Subtotal | | | 97.1 | |

Equity and Other | | | 2.9 | |

| | | | |

Total | | | 100.0 | % |

| | | | |

| * | Expressed as a percentage of total investments (excluding securities lending collateral, if applicable) and may vary over time. |

| ** | Credit Quality is based on ratings provided by the S&P Global Ratings Division of S&P Global Inc. (“S&P”). S&P is a main provider of ratings for credit assets classes and is widely used amongst industry participants. The NR category consists of securities that have not been rated by S&P. |

4

Credit Suisse High Yield Bond Fund

Schedule of Investments

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (104.8%) | | | | | | | | | | | | | | |

| | | | |

| | Aerospace & Defense (1.0%) | | | | | | | | | | | | | | |

| | | | | |

| $ | 965 | | | KBR, Inc., Rule 144A, Company Guaranteed Notes

(Callable 09/30/23 @ 102.38)(1) | | (BB-, Ba3) | | | 09/30/28 | | | | 4.750 | | | $ | 845,383 | |

| | | | | |

| | 1,250 | | | TransDigm, Inc., Global Company Guaranteed Notes

(Callable 12/01/22 @ 103.75) | | (B-, B3) | | | 03/15/27 | | | | 7.500 | | | | 1,236,250 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,081,633 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Auto Parts & Equipment (0.9%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,480 | | | Clarios U.S. Finance Co., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 104.25)(1),(2) | | (CCC+, Caa1) | | | 05/15/27 | | | | 8.500 | | | | 1,459,672 | |

| | | | | |

| | 350 | | | Tenneco, Inc., Rule 144A, Senior Secured Notes

(Callable 01/15/24 @ 103.94)(1) | | (B+, Ba3) | | | 01/15/29 | | | | 7.875 | | | | 347,335 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,807,007 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Automakers (0.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Thor Industries, Inc., Rule 144A, Company Guaranteed Notes

(Callable 10/15/24 @ 102.00)(1) | | (BB-, B1) | | | 10/15/29 | | | | 4.000 | | | | 243,009 | |

| | | | | |

| | 990 | | | Winnebago Industries, Inc., Rule 144A, Senior Secured Notes

(Callable 07/15/23 @ 103.13)(1) | | (BB+, Ba3) | | | 07/15/28 | | | | 6.250 | | | | 922,608 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,165,617 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Brokerage (0.9%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,920 | | | StoneX Group, Inc., Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 104.31)(1) | | (BB-, Ba3) | | | 06/15/25 | | | | 8.625 | | | | 1,893,581 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Building & Construction (1.4%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,010 | | | Adams Homes, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/16/22 @ 103.75)(1) | | (B+, B2) | | | 02/15/25 | | | | 7.500 | | | | 1,625,809 | |

| | | | | |

| | 970 | | | Installed Building Products, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 102.88)(1) | | (B+, B1) | | | 02/01/28 | | | | 5.750 | | | | 858,494 | |

| | | | | |

| | 525 | | | TopBuild Corp., Rule 144A, Company Guaranteed Notes

(Callable 03/15/24 @ 101.81)(1) | | (BB+, Ba2) | | | 03/15/29 | | | | 3.625 | | | | 417,923 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,902,226 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Building Materials (7.4%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,250 | | | Advanced Drainage System, Inc., Rule 144A, Company Guaranteed Notes

(Callable 07/15/25 @ 103.19)(1) | | (BB-, Ba2) | | | 06/15/30 | | | | 6.375 | | | | 2,177,640 | |

| | | | | |

| | 300 | | | Builders FirstSource, Inc., Rule 144A, Company Guaranteed Notes

(Callable 03/01/25 @ 102.50)(1) | | (BB-, Ba2) | | | 03/01/30 | | | | 5.000 | | | | 260,606 | |

| | | | | |

| | 2,100 | | | Builders FirstSource, Inc., Rule 144A, Company Guaranteed Notes

(Callable 06/15/27 @ 103.19)(1) | | (BB-, Ba2) | | | 06/15/32 | | | | 6.375 | | | | 1,937,082 | |

| | | | | |

| | 1,150 | | | Eco Material Technologies, Inc., Rule 144A, Senior Secured Notes

(Callable 01/31/24 @ 103.94)(1) | | (B, B2) | | | 01/31/27 | | | | 7.875 | | | | 1,076,435 | |

| | | | | |

| | 3,389 | | | Foundation Building Materials, Inc., Rule 144A, Company Guaranteed Notes (Callable 03/01/24 @ 103.00)(1) | | (CCC+, Caa1) | | | 03/01/29 | | | | 6.000 | | | | 2,346,318 | |

| | | | | |

| | 639 | | | LBM Acquisition LLC, Rule 144A, Company Guaranteed Notes

(Callable 01/15/24 @ 103.13)(1) | | (CCC, Caa1) | | | 01/15/29 | | | | 6.250 | | | | 448,520 | |

See Accompanying Notes to Financial Statements.

5

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Building Materials | | | | | | | | | | | | | | |

| | | | | |

| $ | 2,497 | | | MIWD Finance Corp., Rule 144A, Company Guaranteed Notes

(Callable 02/01/25 @ 102.75)(1) | | (B, B3) | | | 02/01/30 | | | | 5.500 | | | $ | 1,918,828 | |

| | | | | |

| | 1,750 | | | Oscar Finance, Inc., Rule 144A, Senior Unsecured Notes

(Callable 04/15/25 @ 104.75)(1) | | (CCC+, Caa1) | | | 04/15/30 | | | | 9.500 | | | | 1,487,462 | |

| | | | | |

| | 1,410 | | | Park River Holdings, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/24 @ 102.81)(1) | | (CCC, Caa1) | | | 02/01/29 | | | | 5.625 | | | | 897,534 | |

| | | | | |

| | 700 | | | Park River Holdings, Inc., Rule 144A, Senior Unsecured Notes

(Callable 08/01/24 @ 103.38)(1) | | (CCC, Caa1) | | | 08/01/29 | | | | 6.750 | | | | 461,909 | |

| | | | | |

| | 1,800 | | | PGT Innovations, Inc., Rule 144A, Company Guaranteed Notes

(Callable 10/01/24 @ 102.19)(1) | | (B+, B1) | | | 10/01/29 | | | | 4.375 | | | | 1,503,000 | |

| | | | | |

| | 1,050 | | | Standard Industries, Inc., Rule 144A, Senior Unsecured Notes

(Callable 07/15/25 @ 102.19)(1) | | (BB, B1) | | | 07/15/30 | | | | 4.375 | | | | 855,078 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 15,370,412 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Cable & Satellite TV (2.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,315 | | | CSC Holdings LLC, Global Senior Unsecured Notes | | (B, B3) | | | 06/01/24 | | | | 5.250 | | | | 1,276,937 | |

| | | | | |

| | 525 | | | CSC Holdings LLC, Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 102.75)(1) | | (BB, Ba3) | | | 04/15/27 | | | | 5.500 | | | | 493,445 | |

| | | | | |

| | 750 | | | CSC Holdings LLC, Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 102.69)(1) | | (BB-, Ba3) | | | 02/01/28 | | | | 5.375 | | | | 689,816 | |

| | | | | |

| | 900 | | | CSC Holdings LLC, Rule 144A, Company Guaranteed Notes

(Callable 11/15/26 @ 102.25)(1) | | (BB-, Ba3) | | | 11/15/31 | | | | 4.500 | | | | 704,831 | |

| | | | | |

| | 2,000 | | | Telenet Finance Luxembourg Notes Sarl, Rule 144A, Senior Secured Notes (Callable 12/01/22 @ 102.75)(1) | | (BB-, Ba3) | | | 03/01/28 | | | | 5.500 | | | | 1,757,200 | |

| | | | | |

| | 900 | | | UPC Broadband Finco B.V., Rule 144A, Senior Secured Notes

(Callable 07/15/26 @ 102.44)(1) | | (BB-, B1) | | | 07/15/31 | | | | 4.875 | | | | 748,503 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 5,670,732 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Chemicals (4.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Avient Corp., Rule 144A, Senior Unsecured Notes

(Callable 12/01/22 @ 102.88)(1) | | (BB-, Ba3) | | | 05/15/25 | | | | 5.750 | | | | 293,391 | |

| | | | | |

| | 715 | | | Avient Corp., Rule 144A, Senior Unsecured Notes

(Callable 08/01/25 @ 103.56)(1) | | (BB-, Ba3) | | | 08/01/30 | | | | 7.125 | | | | 684,680 | |

| | | | | |

| | 950 | | | Herens Holdco Sarl, Rule 144A, Senior Secured Notes

(Callable 05/15/24 @ 102.38)(1) | | (B, B2) | | | 05/15/28 | | | | 4.750 | | | | 779,654 | |

| | | | | |

| | 1,200 | | | Herens Midco Sarl, Rule 144A, Company Guaranteed Notes

(Callable 05/15/24 @ 102.63)(1),(3) | | (CCC+, Caa2) | | | 05/15/29 | | | | 5.250 | | | | 772,692 | |

| | | | | |

| | 1,200 | | | LSF11 A5 Holdings LLC, Rule 144A, Senior Unsecured Notes

(Callable 10/15/24 @ 103.31)(1),(2) | | (B-, Caa1) | | | 10/15/29 | | | | 6.625 | | | | 947,718 | |

| | | | | |

| | 525 | | | Olympus Water U.S. Holding Corp., Rule 144A, Senior Unsecured Notes

(Callable 10/01/24 @ 103.13)(1),(2) | | (CCC+, Caa2) | | | 10/01/29 | | | | 6.250 | | | | 365,366 | |

| | | | | |

| | 272 | | | Reichhold Industries, Inc., Rule 144A, Senior Secured Notes(1),(4),(5),(6),(7),(8),(9) | | (NR, WR) | | | 05/01/18 | | | | 0.000 | | | | 3,667 | |

| | | | | |

| | 1,800 | | | Schenectady International Group, Inc., Rule 144A, Senior Unsecured Notes (Callable 05/15/23 @ 103.38)(1) | | (CCC+, Caa2) | | | 05/15/26 | | | | 6.750 | | | | 866,466 | |

See Accompanying Notes to Financial Statements.

6

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Chemicals | | | | | | | | | | | | | | |

| | | | | |

| $ | 600 | | | Trinseo Materials Finance, Inc., Rule 144A, Company Guaranteed Notes

(Callable 04/01/24 @ 102.56)(1) | | (B, B2) | | | 04/01/29 | | | | 5.125 | | | $ | 341,370 | |

| | | | | |

| | 1,200 | | | Tronox, Inc., Rule 144A, Company Guaranteed Notes

(Callable 03/15/24 @ 102.31)(1) | | (BB-, B1) | | | 03/15/29 | | | | 4.625 | | | | 929,526 | |

| | | | | |

| | 1,800 | | | Valvoline, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/15/25 @ 102.13)(1) | | (BB-, Ba3) | | | 02/15/30 | | | | 4.250 | | | | 1,735,218 | |

| | | | | |

| | 3,335 | | | Vibrantz Technologies, Inc., Rule 144A, Senior Unsecured Notes

(Callable 02/15/25 @ 104.50)(1),(2) | | (CCC+, Caa2) | | | 02/15/30 | | | | 9.000 | | | | 2,205,177 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 9,924,925 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Consumer/Commercial/Lease Financing (1.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,900 | | | Cargo Aircraft Management, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 102.38)(1) | | (BB, Ba2) | | | 02/01/28 | | | | 4.750 | | | | 2,593,543 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Diversified Capital Goods (1.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,025 | | | Atkore, Inc., Rule 144A, Senior Unsecured Notes

(Callable 06/01/26 @ 102.13)(1) | | (BB, Ba2) | | | 06/01/31 | | | | 4.250 | | | | 1,648,492 | |

| | | | | |

| | 2,547 | | | GrafTech Finance, Inc., Rule 144A, Senior Secured Notes

(Callable 12/15/23 @ 102.31)(1) | | (BB, Ba3) | | | 12/15/28 | | | | 4.625 | | | | 2,067,794 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 3,716,286 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Electronics (0.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,800 | | | Synaptics, Inc., Rule 144A, Company Guaranteed Notes

(Callable 06/15/24 @ 102.00)(1) | | (B+, Ba3) | | | 06/15/29 | | | | 4.000 | | | | 1,489,440 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Energy - Exploration & Production (2.9%) | | | | | | | | | | | | | | |

| | | | | |

| | 62 | | | CNX Resources Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 105.44)(1) | | (BB, B1) | | | 03/14/27 | | | | 7.250 | | | | 61,629 | |

| | | | | |

| | 800 | | | CNX Resources Corp., Rule 144A, Company Guaranteed Notes

(Callable 01/15/24 @ 104.50)(1) | | (BB, B1) | | | 01/15/29 | | | | 6.000 | | | | 747,896 | |

| | | | | |

| | 2,095 | | | Northern Oil & Gas, Inc., Rule 144A, Senior Unsecured Notes

(Callable 03/01/24 @ 104.06)(1) | | (B+, B3) | | | 03/01/28 | | | | 8.125 | | | | 2,036,539 | |

| | | | | |

| | 2,100 | | | Rockcliff Energy II LLC, Rule 144A, Senior Unsecured Notes

(Callable 10/15/24 @ 102.75)(1) | | (B+, B3) | | | 10/15/29 | | | | 5.500 | | | | 1,875,542 | |

| | | | | |

| | 1,315 | | | W&T Offshore, Inc., Rule 144A, Secured Notes

(Callable 12/01/22 @ 100.00)(1) | | (B, Caa2) | | | 11/01/23 | | | | 9.750 | | | | 1,305,488 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 6,027,094 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Environmental (0.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 900 | | | Darling Ingredients, Inc., Rule 144A, Company Guaranteed Notes

(Callable 06/15/25 @ 103.00)(1) | | (BB+, Ba2) | | | 06/15/30 | | | | 6.000 | | | | 867,389 | |

| | | | | |

| | 300 | | | Stericycle, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/23 @ 101.94)(1) | | (BB-, NR) | | | 01/15/29 | | | | 3.875 | | | | 261,207 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,128,596 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Food - Wholesale (0.5%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,150 | | | U.S. Foods, Inc., Rule 144A, Company Guaranteed Notes

(Callable 06/01/25 @ 102.31)(1),(2) | | (B+, B3) | | | 06/01/30 | | | | 4.625 | | | | 999,074 | |

| | | | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements.

7

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Gaming (2.4%) | | | | | | | | | | | | | | |

| | | | | |

| $ | 500 | | | Boyd Gaming Corp., Rule 144A, Company Guaranteed Notes

(Callable 06/15/26 @ 102.38)(1) | | (BB-, B3) | | | 06/15/31 | | | | 4.750 | | | $ | 424,040 | |

| | | | | |

| | 1,200 | | | CDI Escrow Issuer, Inc., Rule 144A, Senior Unsecured Notes

(Callable 04/01/25 @ 102.88)(1) | | (B+, B1) | | | 04/01/30 | | | | 5.750 | | | | 1,084,800 | |

| | | | | |

| | 332 | | | Churchill Downs, Inc., Rule 144A, Company Guaranteed Notes

(Callable 01/15/23 @ 102.38)(1) | | (B+, B1) | | | 01/15/28 | | | | 4.750 | | | | 293,964 | |

| | | | | |

| | 618 | | | Fertitta Entertainment Finance Co., Inc, Rule 144A, Senior Secured Notes

(Callable 01/15/25 @ 102.31)(1) | | (B, B2) | | | 01/15/29 | | | | 4.625 | | | | 538,627 | |

| | | | | |

| | 1,600 | | | Jacobs Entertainment, Inc., Rule 144A, Senior Unsecured Notes

(Callable 02/15/25 @ 103.38)(1) | | (B, B2) | | | 02/15/29 | | | | 6.750 | | | | 1,413,336 | |

| | | | | |

| | 1,080 | | | Peninsula Pacific Entertainment Finance, Rule 144A, Senior Unsecured Notes (Callable 11/01/22 @ 107.47)(1) | | (B, B3) | | | 11/15/27 | | | | 8.500 | | | | 1,159,481 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 4,914,248 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Gas Distribution (5.9%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | CNX Midstream Partners LP, Rule 144A, Company Guaranteed Notes

(Callable 04/15/25 @ 102.38)(1) | | (BB, B1) | | | 04/15/30 | | | | 4.750 | | | | 988,728 | |

| | | | | |

| | 2,750 | | | Genesis Energy Finance Corp., Company Guaranteed Notes

(Callable 12/01/22 @ 100.00) | | (B, B2) | | | 06/15/24 | | | | 5.625 | | | | 2,691,452 | |

| | | | | |

| | 1,125 | | | Genesis Energy Finance Corp., Company Guaranteed Notes

(Callable 12/01/22 @ 103.13) | | (B, B2) | | | 05/15/26 | | | | 6.250 | | | | 1,045,027 | |

| | | | | |

| | 1,800 | | | Hess Midstream Operations LP, Rule 144A, Company Guaranteed Notes

(Callable 06/15/23 @ 102.56)(1) | | (BB+, Ba2) | | | 06/15/28 | | | | 5.125 | | | | 1,658,781 | |

| | | | | |

| | 600 | | | Hess Midstream Operations LP, Rule 144A, Company Guaranteed Notes

(Callable 10/15/25 @ 102.75)(1) | | (BB+, Ba2) | | | 10/15/30 | | | | 5.500 | | | | 542,142 | |

| | | | | |

| | 600 | | | Holly Energy Finance Corp., Rule 144A, Company Guaranteed Notes

(Callable 04/15/24 @ 103.19)(1) | | (BB+, Ba3) | | | 04/15/27 | | | | 6.375 | | | | 580,290 | |

| | | | | |

| | 1,450 | | | New Fortress Energy, Inc., Rule 144A, Senior Secured Notes

(Callable 03/31/23 @ 103.25)(1) | | (BB-, B1) | | | 09/30/26 | | | | 6.500 | | | | 1,407,218 | |

| | | | | |

| | 1,770 | | | Rockies Express Pipeline LLC, Rule 144A, Senior Unsecured Notes

(Callable 04/15/29 @ 100.00)(1) | | (BB+, Ba2) | | | 07/15/29 | | | | 4.950 | | | | 1,556,181 | |

| | | | | |

| | 915 | | | Rockies Express Pipeline LLC, Rule 144A, Senior Unsecured Notes

(Callable 02/15/30 @ 100.00)(1) | | (BB+, Ba2) | | | 05/15/30 | | | | 4.800 | | | | 774,451 | |

| | | | | |

| | 300 | | | Suburban Energy Finance Corp., Rule 144A, Senior Unsecured Notes

(Callable 06/01/26 @ 102.50)(1) | | (BB-, B1) | | | 06/01/31 | | | | 5.000 | | | | 252,897 | |

| | | | | |

| | 750 | | | Tallgrass Energy Finance Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 105.63)(1) | | (BB-, B1) | | | 10/01/25 | | | | 7.500 | | | | 759,173 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 12,256,340 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Health Facility (0.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Option Care Health, Inc., Rule 144A, Company Guaranteed Notes

(Callable 10/31/24 @ 102.19)(1) | | (B-, B3) | | | 10/31/29 | | | | 4.375 | | | | 258,209 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Health Services (3.4%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,560 | | | AMN Healthcare, Inc., Rule 144A, Company Guaranteed Notes

(Callable 04/15/24 @ 102.00)(1) | | (BB-, Ba3) | | | 04/15/29 | | | | 4.000 | | | | 1,348,596 | |

See Accompanying Notes to Financial Statements.

8

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Health Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 2,400 | | | Minerva Merger Sub, Inc., Rule 144A, Senior Unsecured Notes

(Callable 02/15/25 @ 103.25)(1),(2) | | (CCC, Caa2) | | | 02/15/30 | | | | 6.500 | | | $ | 1,873,248 | |

| | | | | |

| | 1,500 | | | Pediatrix Medical Group, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/15/25 @ 102.69)(1),(2) | | (BB-, Ba3) | | | 02/15/30 | | | | 5.375 | | | | 1,292,137 | |

| | | | | |

| | 3,650 | | | Radiology Partners, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 104.63)(1) | | (CCC, Caa2) | | | 02/01/28 | | | | 9.250 | | | | 1,939,792 | |

| | | | | |

| | 589 | | | Service Corp., International, Global Senior Unsecured Notes

(Callable 05/15/26 @ 102.00) | | (BB, Ba3) | | | 05/15/31 | | | | 4.000 | | | | 490,521 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 6,944,294 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Insurance Brokerage (3.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Acrisure Finance, Inc., Rule 144A, Senior Unsecured Notes

(Callable 12/01/22 @ 107.59)(1) | | (CCC+, Caa2) | | | 08/01/26 | | | | 10.125 | | | | 992,657 | |

| | | | | |

| | 893 | | | GTCR AP Finance, Inc., Rule 144A, Senior Unsecured Notes

(Callable 12/01/22 @ 104.00)(1) | | (CCC+, Caa2) | | | 05/15/27 | | | | 8.000 | | | | 851,667 | |

| | | | | |

| | 950 | | | NFP Corp., Rule 144A, Senior Secured Notes

(Callable 08/15/23 @ 102.44)(1) | | (B, B1) | | | 08/15/28 | | | | 4.875 | | | | 822,074 | |

| | | | | |

| | 600 | | | NFP Corp., Rule 144A, Senior Secured Notes

(Callable 10/01/25 @ 103.75)(1) | | (B, B1) | | | 10/01/30 | | | | 7.500 | | | | 572,342 | |

| | | | | |

| | 4,055 | | | NFP Corp., Rule 144A, Senior Unsecured Notes

(Callable 08/15/23 @ 103.44)(1) | | (CCC+, Caa2) | | | 08/15/28 | | | | 6.875 | | | | 3,459,413 | |

| | | | | |

| | 1,200 | | | Ryan Specialty Group LLC, Rule 144A, Senior Secured Notes

(Callable 02/01/25 @ 102.19)(1) | | (BB-, B1) | | | 02/01/30 | | | | 4.375 | | | | 1,027,500 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 7,725,653 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Investments & Misc. Financial Services (2.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,550 | | | Armor Holdco, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/24 @ 104.25)(1) | | (CCC+, Caa1) | | | 11/15/29 | | | | 8.500 | | | | 1,905,003 | |

| | | | | |

| | 2,050 | | | Compass Group Diversified Holdings LLC, Rule 144A, Company Guaranteed Notes (Callable 04/15/24 @ 102.63)(1) | | (B+, B1) | | | 04/15/29 | | | | 5.250 | | | | 1,768,197 | |

| | | | | |

| | 1,150 | | | Compass Group Diversified Holdings LLC, Rule 144A, Senior Unsecured Notes (Callable 01/15/27 @ 102.50)(1) | | (B+, B1) | | | 01/15/32 | | | | 5.000 | | | | 838,997 | |

| | | | | |

| | 1,560 | | | Home Point Capital, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 102.50)(1) | | (NR, Caa1) | | | 02/01/26 | | | | 5.000 | | | | 924,425 | |

| | | | | |

| | 300 | | | Paysafe Holdings U.S. Corp., Rule 144A, Senior Secured Notes

(Callable 06/15/24 @ 102.00)(1),(2) | | (B, B2) | | | 06/15/29 | | | | 4.000 | | | | 214,936 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 5,651,558 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Machinery (5.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,850 | | | Arcosa, Inc., Rule 144A, Company Guaranteed Notes

(Callable 04/15/24 @ 102.19)(1) | | (BB, Ba2) | | | 04/15/29 | | | | 4.375 | | | | 1,597,595 | |

| | | | | |

| | 2,495 | | | ATS Automation Tooling Systems, Inc., Rule 144A, Company Guaranteed Notes (Callable 12/15/23 @ 102.06)(1) | | (BB-, B2) | | | 12/15/28 | | | | 4.125 | | | | 2,136,606 | |

| | | | | |

| | 2,100 | | | Dornoch Debt Merger Sub, Inc., Rule 144A, Senior Unsecured Notes

(Callable 10/15/24 @ 103.31)(1) | | (CCC, Caa1) | | | 10/15/29 | | | | 6.625 | | | | 1,430,816 | |

| | | | | |

| | 2,850 | | | Granite U.S. Holdings Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 105.50)(1) | | (CCC+, Caa1) | | | 10/01/27 | | | | 11.000 | | | | 2,668,968 | |

See Accompanying Notes to Financial Statements.

9

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Machinery | | | | | | | | | | | | | | |

| | | | | |

| $ | 3,635 | | | Harsco Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 102.88)(1) | | (B, B3) | | | 07/31/27 | | | | 5.750 | | | $ | 2,584,721 | |

| | | | | |

| | 600 | | | Hillenbrand, Inc., Global Company Guaranteed Notes

(Callable 12/01/22 @ 102.88) | | (BB+, Ba1) | | | 06/15/25 | | | | 5.750 | | | | 596,274 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 11,014,980 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Managed Care (0.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 750 | | | HealthEquity, Inc., Rule 144A, Company Guaranteed Notes

(Callable 10/01/24 @ 102.25)(1) | | (B, B3) | | | 10/01/29 | | | | 4.500 | | | | 660,938 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Media - Diversified (0.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 300 | | | News Corp., Rule 144A, Company Guaranteed Notes

(Callable 02/15/27 @ 102.56)(1) | | (BB+, Ba1) | | | 02/15/32 | | | | 5.125 | | | | 268,230 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Media Content (0.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,507 | | | Diamond Sports Finance Co., Rule 144A, Company Guaranteed Notes

(Callable 11/16/22 @ 103.31)(1) | | (CCC-, Ca) | | | 08/15/27 | | | | 6.625 | | | | 79,118 | |

| | | | | |

| | 738 | | | Diamond Sports Finance Co., Rule 144A, Secured Notes

(Callable 11/16/22 @ 102.69)(1) | | (CCC+, Caa3) | | | 08/15/26 | | | | 5.375 | | | | 148,522 | |

| | | | | |

| | 300 | | | Sirius XM Radio, Inc., Rule 144A, Company Guaranteed Notes

(Callable 07/15/24 @ 102.00)(1) | | (BB, Ba3) | | | 07/15/28 | | | | 4.000 | | | | 258,352 | |

| | | | | |

| | 1,200 | | | Sirius XM Radio, Inc., Rule 144A, Company Guaranteed Notes

(Callable 07/01/24 @ 102.75)(1) | | (BB, Ba3) | | | 07/01/29 | | | | 5.500 | | | | 1,100,490 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,586,482 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Medical Products (1.2%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Embecta Corp., Rule 144A, Senior Secured Notes

(Callable 02/15/27 @ 101.25)(1) | | (B+, Ba3) | | | 02/15/30 | | | | 5.000 | | | | 858,630 | |

| | | | | |

| | 2,100 | | | Medline Borrower LP, Rule 144A, Senior Unsecured Notes

(Callable 10/01/24 @ 102.63)(1) | | (B-, Caa1) | | | 10/01/29 | | | | 5.250 | | | | 1,639,029 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,497,659 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Metals & Mining - Excluding Steel (4.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | Alcoa Nederland Holding B.V., Rule 144A, Company Guaranteed Notes

(Callable 06/15/23 @ 102.75)(1) | | (BB+, Baa3) | | | 12/15/27 | | | | 5.500 | | | | 1,119,334 | |

| | | | | |

| | 375 | | | Canpack U.S. LLC, Rule 144A, Company Guaranteed Notes

(Callable 11/15/24 @ 101.94)(1) | | (BB, NR) | | | 11/15/29 | | | | 3.875 | | | | 298,549 | |

| | | | | |

| | 2,700 | | | ERO Copper Corp., Rule 144A, Company Guaranteed Notes

(Callable 02/15/25 @ 103.25)(1) | | (B, B1) | | | 02/15/30 | | | | 6.500 | | | | 2,035,584 | |

| | | | | |

| | 2,150 | | | First Quantum Minerals Ltd., Rule 144A, Company Guaranteed Notes

(Callable 11/14/22 @ 103.44)(1) | | (B+, NR) | | | 03/01/26 | | | | 6.875 | | | | 2,022,978 | |

| | | | | |

| | 600 | | | Kaiser Aluminum Corp., Rule 144A, Company Guaranteed Notes

(Callable 03/01/23 @ 102.31)(1) | | (BB, B1) | | | 03/01/28 | | | | 4.625 | | | | 527,271 | |

| | | | | |

| | 600 | | | Kaiser Aluminum Corp., Rule 144A, Company Guaranteed Notes

(Callable 06/01/26 @ 102.25)(1) | | (BB, B1) | | | 06/01/31 | | | | 4.500 | | | | 482,136 | |

| | | | | |

| | 182 | | | Novelis Corp., Rule 144A, Company Guaranteed Notes

(Callable 01/30/25 @ 102.38)(1) | | (BB, Ba3) | | | 01/30/30 | | | | 4.750 | | | | 156,937 | |

See Accompanying Notes to Financial Statements.

10

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Metals & Mining - Excluding Steel | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,692 | | | SunCoke Energy, Inc., Rule 144A, Senior Secured Notes

(Callable 06/30/24 @ 102.44)(1) | | (BB, B1) | | | 06/30/29 | | | | 4.875 | | | $ | 1,389,995 | |

| | | | | |

| | 2,325 | | | Taseko Mines Ltd., Rule 144A, Senior Secured Notes

(Callable 02/15/23 @ 103.50)(1) | | (B-, B3) | | | 02/15/26 | | | | 7.000 | | | | 1,938,120 | |

| | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 9,970,904 | |

| | | | | | | | | | | | | | | | | | |

|

| | Oil Field Equipment & Services (0.1%) | |

| | | | | |

| | 300 | | | Enerflex Ltd., Rule 144A, Senior Secured Notes

(Callable 10/15/24 @ 106.75)(1) | | (BB-, B2) | | | 10/15/27 | | | | 9.000 | | | | 292,308 | |

| | | | | | | | | | | | | | | | | | |

|

| | Packaging (2.3%) | |

| | | | | |

| | 690 | | | Ardagh Metal Packaging Finance PLC, Rule 144A, Senior Unsecured Notes (Callable 05/15/24 @ 101.50)(1),(3) | | (B+, B3) | | | 09/01/29 | | | | 3.000 | | | | 489,683 | |

| | | | | |

| | 600 | | | Intelligent Packaging Ltd. Co-Issuer LLC, Rule 144A, Senior Secured Notes (Callable 12/01/22 @ 103.00)(1) | | (B-, B3) | | | 09/15/28 | | | | 6.000 | | | | 448,172 | |

| | | | | |

| | 800 | | | Pactiv Evergreen Group Issuer LLC, Rule 144A, Senior Secured Notes

(Callable 10/15/23 @ 102.00)(1) | | (B+, B1) | | | 10/15/27 | | | | 4.000 | | | | 716,080 | |

| | | | | |

| | 3,570 | | | TriMas Corp., Rule 144A, Company Guaranteed Notes

(Callable 04/15/24 @ 102.06)(1) | | (BB-, Ba3) | | | 04/15/29 | | | | 4.125 | | | | 3,084,301 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 4,738,236 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Personal & Household Products (1.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | Diamond BC B.V., Rule 144A, Company Guaranteed Notes

(Callable 10/01/24 @ 102.31)(1) | | (B, Caa1) | | | 10/01/29 | | | | 4.625 | | | | 883,308 | |

| | | | | |

| | 2,000 | | | High Ridge Brands Co., Rule 144A, Senior Unsecured Notes(1),(4),(6),(7),(9) | | (NR, NR) | | | 03/15/25 | | | | 0.000 | | | | 30,000 | |

| | | | | |

| | 2,400 | | | MajorDrive Holdings IV LLC, Rule 144A, Senior Unsecured Notes

(Callable 06/01/24 @ 103.19)(1) | | (CCC+, Caa2) | | | 06/01/29 | | | | 6.375 | | | | 1,694,856 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,608,164 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Pharmaceuticals (2.0%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,600 | | | Bausch Health Cos., Inc., Rule 144A, Company Guaranteed Notes

(Callable 05/30/24 @ 103.63)(1) | | (CCC, Ca) | | | 05/30/29 | | | | 7.250 | | | | 613,800 | |

| | | | | |

| | 325 | | | Bausch Health Cos., Inc., Rule 144A, Company Guaranteed Notes

(Callable 01/30/25 @ 102.63)(1) | | (CCC, Ca) | | | 01/30/30 | | | | 5.250 | | | | 126,711 | |

| | | | | |

| | 600 | | | Bausch Health Cos., Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/15/26 @ 102.63)(1) | | (CCC, Ca) | | | 02/15/31 | | | | 5.250 | | | | 236,913 | |

| | | | | |

| | 600 | | | Bausch Health Cos., Inc., Rule 144A, Senior Secured Notes

(Callable 06/01/24 @ 102.44)(1) | | (B-, Caa1) | | | 06/01/28 | | | | 4.875 | | | | 368,775 | |

| | | | | |

| | 1,064 | | | Emergent BioSolutions, Inc., Rule 144A, Company Guaranteed Notes

(Callable 08/15/23 @ 101.94)(1) | | (BB-, B3) | | | 08/15/28 | | | | 3.875 | | | | 638,787 | |

| | | | | |

| | 1,350 | | | Endo Finance LLC, Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 100.00)(1),(4) | | (NR, WR) | | | 10/15/24 | | | | 5.875 | | | | 1,073,506 | |

| | | | | |

| | 600 | | | Endo U.S., Inc., Rule 144A, Senior Secured Notes

(Callable 04/01/24 @ 104.59)(1),(4) | | (NR, WR) | | | 04/01/29 | | | | 6.125 | | | | 454,699 | |

| | | | | |

| | 800 | | | Grifols Escrow Issuer S.A., Rule 144A, Senior Unsecured Notes

(Callable 10/15/24 @ 102.38)(1) | | (B-, B3) | | | 10/15/28 | | | | 4.750 | | | | 626,060 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 4,139,251 | |

| | | | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements.

11

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Real Estate Development & Management (0.5%) | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,867 | | | WeWork Cos., Inc., Rule 144A, Company Guaranteed Notes(1) | | (CCC+, WR) | | | 05/01/25 | | | | 7.875 | | | $ | 1,022,173 | |

| | | | | | | | | | | | | | | | | | |

|

| | Real Estate Investment Trusts (2.5%) | |

| | | | | |

| | 1,906 | | | Global Net Lease Operating Partnership LP, Rule 144A, Company Guaranteed Notes (Callable 09/15/27 @ 100.00)(1) | | (BBB-, Ba3) | | | 12/15/27 | | | | 3.750 | | | | 1,541,164 | |

| | | | | |

| | 2,100 | | | iStar, Inc., Global Senior Unsecured Notes (Callable 12/01/22 @ 102.75) | | (BB, Ba2) | | | 02/15/26 | | | | 5.500 | | | | 2,096,829 | |

| | | | | |

| | 300 | | | iStar, Inc., Senior Unsecured Notes (Callable 07/01/24 @ 100.00) | | (BB, Ba2) | | | 10/01/24 | | | | 4.750 | | | | 296,834 | |

| | | | | |

| | 1,250 | | | VICI Note Co., Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/01/26 @ 100.00)(1) | | (BBB-, Ba1) | | | 02/01/27 | | | | 5.750 | | | | 1,183,856 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 5,118,683 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Recreation & Travel (5.5%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | Boyne U.S.A., Inc., Rule 144A, Senior Unsecured Notes

(Callable 05/15/24 @ 102.38)(1) | | (B, B1) | | | 05/15/29 | | | | 4.750 | | | | 1,052,658 | |

| | | | | |

| | 1,817 | | | Merlin Entertainments Ltd., Rule 144A, Secured Notes

(Callable 03/17/26 @ 100.00)(1) | | (B, B2) | | | 06/15/26 | | | | 5.750 | | | | 1,692,053 | |

| | | | | |

| | 3,475 | | | SeaWorld Parks & Entertainment, Inc., Rule 144A, Company Guaranteed Notes (Callable 08/15/24 @ 102.63)(1),(2) | | (B, B3) | | | 08/15/29 | | | | 5.250 | | | | 2,993,793 | |

| | | | | |

| | 450 | | | SeaWorld Parks & Entertainment, Inc., Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 104.38)(1) | | (BB, Ba3) | | | 05/01/25 | | | | 8.750 | | | | 461,536 | |

| | | | | |

| | 2,150 | | | Six Flags Entertainment Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 100.00)(1) | | (B-, B3) | | | 07/31/24 | | | | 4.875 | | | | 2,086,672 | |

| | | | | |

| | 3,435 | | | Speedway Funding II, Inc., Rule 144A, Senior Unsecured Notes

(Callable 12/01/22 @ 102.44)(1) | | (BB, B2) | | | 11/01/27 | | | | 4.875 | | | | 2,989,540 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 11,276,252 | |

| | | | | | | | | | | | | | | | | | |

|

| | Restaurants (0.8%) | |

| | | | | |

| | 1,825 | | | Yum! Brands, Inc., Global Senior Unsecured Notes

(Callable 04/01/27 @ 102.69) | | (BB, Ba3) | | | 04/01/32 | | | | 5.375 | | | | 1,635,173 | |

| | | | | | | | | | | | | | | | | | |

|

| | Software - Services (7.1%) | |

| | | | | |

| | 950 | | | CA Magnum Holdings, Rule 144A, Senior Secured Notes

(Callable 10/31/23 @ 102.69)(1) | | (NR, B1) | | | 10/31/26 | | | | 5.375 | | | | 798,074 | |

| | | | | |

| | 1,300 | | | Central Parent, Inc., Rule 144A, Senior Secured Notes

(Callable 06/15/25 @ 103.63)(1) | | (B+, B1) | | | 06/15/29 | | | | 7.250 | | | | 1,242,800 | |

| | | | | |

| | 946 | | | Coherent Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/14/24 @ 102.50)(1) | | (B+, B2) | | | 12/15/29 | | | | 5.000 | | | | 813,844 | |

| | | | | |

| | 3,150 | | | Elastic NV, Rule 144A, Senior Unsecured Notes

(Callable 07/15/24 @ 102.06)(1) | | (B+, B1) | | | 07/15/29 | | | | 4.125 | | | | 2,637,495 | |

| | | | | |

| | 2,675 | | | Endurance International Group Holdings, Inc., Rule 144A, Senior Unsecured Notes (Callable 02/15/24 @ 103.00)(1) | | (CCC+, Caa2) | | | 02/15/29 | | | | 6.000 | | | | 1,765,299 | |

| | | | | |

| | 945 | | | Open Text Corp., Rule 144A, Company Guaranteed Notes

(Callable 12/01/24 @ 101.94)(1) | | (BB, Ba2) | | | 12/01/29 | | | | 3.875 | | | | 754,625 | |

| | | | | |

| | 1,250 | | | Open Text Holdings, Inc., Rule 144A, Company Guaranteed Notes

(Callable 12/01/26 @ 102.06)(1) | | (BB, Ba2) | | | 12/01/31 | | | | 4.125 | | | | 952,038 | |

See Accompanying Notes to Financial Statements.

12

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Software - Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 2,512 | | | Presidio Holdings, Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/01/23 @ 104.13)(1) | | (CCC+, Caa1) | | | 02/01/28 | | | | 8.250 | | | $ | 2,241,307 | |

| | | | | |

| | 4,060 | | | Virtusa Corp., Rule 144A, Senior Unsecured Notes

(Callable 12/15/23 @ 103.56)(1) | | (CCC+, Caa2) | | | 12/15/28 | | | | 7.125 | | | | 2,918,437 | |

| | | | | |

| | 600 | | | ZoomInfo Finance Corp., Rule 144A, Company Guaranteed Notes

(Callable 02/01/24 @ 101.94)(1) | | (B+, B1) | | | 02/01/29 | | | | 3.875 | | | | 502,745 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 14,626,664 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Specialty Retail (4.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 61 | | | Asbury Automotive Group, Inc., Global Company Guaranteed Notes

(Callable 03/01/23 @ 102.25) | | (BB, B1) | | | 03/01/28 | | | | 4.500 | | | | 51,635 | |

| | | | | |

| | 733 | | | Asbury Automotive Group, Inc., Global Company Guaranteed Notes

(Callable 03/01/25 @ 102.38) | | (BB, B1) | | | 03/01/30 | | | | 4.750 | | | | 601,688 | |

| | | | | |

| | 300 | | | Asbury Automotive Group, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/24 @ 102.31)(1) | | (BB, B1) | | | 11/15/29 | | | | 4.625 | | | | 247,488 | |

| | | | | |

| | 300 | | | Asbury Automotive Group, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/26 @ 102.50)(1) | | (BB, B1) | | | 02/15/32 | | | | 5.000 | | | | 242,226 | |

| | | | | |

| | 102 | | | Eagle Intermediate Global Holdings BV(7),(9) | | (NR, NR) | | | 05/01/25 | | | | 0.000 | | | | 56,969 | |

| | | | | |

| | 77 | | | Eagle Intermediate Global Holdings BV, Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 103.75)(1),(7),(9) | | (NR, NR) | | | 05/01/25 | | | | 7.500 | | | | 57,277 | |

| | | | | |

| | 2,800 | | | Eagle Intermediate Global Holdings BV, Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 103.75)(1) | | (NR, Caa1) | | | 05/01/25 | | | | 7.500 | | | | 2,171,400 | |

| | | | | |

| | 1,425 | | | eG Global Finance PLC, Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 102.13)(1) | | (B-, B3) | | | 10/30/25 | | | | 8.500 | | | | 1,319,536 | |

| | | | | |

| | 600 | | | LCM Investments Holdings II LLC, Rule 144A, Senior Unsecured Notes

(Callable 05/01/24 @ 102.44)(1) | | (BB-, B2) | | | 05/01/29 | | | | 4.875 | | | | 507,681 | |

| | | | | |

| | 300 | | | Murphy Oil U.S.A., Inc., Rule 144A, Company Guaranteed Notes

(Callable 02/15/26 @ 101.88)(1) | | (BB+, Ba2) | | | 02/15/31 | | | | 3.750 | | | | 250,406 | |

| | | | | |

| | 600 | | | Penske Automotive Group, Inc., Company Guaranteed Notes

(Callable 06/15/24 @ 101.88) | | (BB-, Ba3) | | | 06/15/29 | | | | 3.750 | | | | 486,106 | |

| | | | | |

| | 900 | | | Sonic Automotive, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/24 @ 102.31)(1) | | (BB-, B1) | | | 11/15/29 | | | | 4.625 | | | | 707,251 | |

| | | | | |

| | 1,725 | | | Sonic Automotive, Inc., Rule 144A, Company Guaranteed Notes

(Callable 11/15/26 @ 102.44)(1),(2) | | (BB-, B1) | | | 11/15/31 | | | | 4.875 | | | | 1,314,407 | |

| | | | | |

| | 675 | | | Wolverine World Wide, Inc., Rule 144A, Company Guaranteed Notes

(Callable 08/15/24 @ 102.00)(1) | | (BB-, Ba3) | | | 08/15/29 | | | | 4.000 | | | | 534,242 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 8,548,312 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Support - Services (9.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 602 | | | Allied Universal Finance Corp., Rule 144A, Senior Secured Notes

(Callable 06/01/24 @ 102.31)(1) | | (B, B2) | | | 06/01/28 | | | | 4.625 | | | | 493,628 | |

| | | | | |

| | 1,821 | | | Allied Universal Finance Corp., Rule 144A, Senior Unsecured Notes

(Callable 12/01/22 @ 104.88)(1) | | (CCC+, Caa1) | | | 07/15/27 | | | | 9.750 | | | | 1,573,321 | |

| | | | | |

| | 1,950 | | | Allied Universal Finance Corp., Rule 144A, Senior Unsecured Notes

(Callable 06/01/24 @ 103.00)(1),(2) | | (CCC+, Caa1) | | | 06/01/29 | | | | 6.000 | | | | 1,358,432 | |

See Accompanying Notes to Financial Statements.

13

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Support - Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 710 | | | APi Group DE, Inc., Rule 144A, Company Guaranteed Notes

(Callable 07/15/24 @ 102.06)(1) | | (B, B1) | | | 07/15/29 | | | | 4.125 | | | $ | 570,339 | |

| | | | | |

| | 600 | | | APi Group DE, Inc., Rule 144A, Company Guaranteed Notes

(Callable 10/15/24 @ 102.38)(1) | | (B, B1) | | | 10/15/29 | | | | 4.750 | | | | 506,635 | |

| | | | | |

| | 600 | | | Clarivate Science Holdings Corp., Rule 144A, Company Guaranteed Notes

(Callable 06/30/24 @ 102.44)(1),(2) | | (CCC+, Caa1) | | | 07/01/29 | | | | 4.875 | | | | 502,188 | |

| | | | | |

| | 3,900 | | | CoreLogic, Inc., Rule 144A, Senior Secured Notes

(Callable 05/01/24 @ 102.25)(1) | | (B-, B2) | | | 05/01/28 | | | | 4.500 | | | | 2,631,281 | |

| | | | | |

| | 3,065 | | | GEMS Education Delaware LLC, Rule 144A, Senior Secured Notes

(Callable 12/05/22 @ 103.56)(1) | | (B-, B3) | | | 07/31/26 | | | | 7.125 | | | | 2,903,996 | |

| | | | | |

| | 3,000 | | | GYP Holdings III Corp., Rule 144A, Company Guaranteed Notes

(Callable 05/01/24 @ 102.31)(1) | | (B, B1) | | | 05/01/29 | | | | 4.625 | | | | 2,373,441 | |

| | | | | |

| | 1,200 | | | Pike Corp., Rule 144A, Company Guaranteed Notes

(Callable 09/01/23 @ 102.75)(1) | | (CCC+, B3) | | | 09/01/28 | | | | 5.500 | | | | 1,027,506 | |

| | | | | |

| | 1,795 | | | TMS International Corp., Rule 144A, Senior Unsecured Notes

(Callable 04/15/24 @ 103.13)(1) | | (B, Caa1) | | | 04/15/29 | | | | 6.250 | | | | 1,261,551 | |

| | | | | |

| | 750 | | | WESCO Distribution, Inc., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 103.56)(1) | | (BB, Ba3) | | | 06/15/25 | | | | 7.125 | | | | 758,430 | |

| | | | | |

| | 750 | | | WESCO Distribution, Inc., Rule 144A, Company Guaranteed Notes

(Callable 06/15/23 @ 103.63)(1) | | (BB, Ba3) | | | 06/15/28 | | | | 7.250 | | | | 761,929 | |

| | | | | |

| | 1,821 | | | White Cap Buyer LLC, Rule 144A, Senior Unsecured Notes

(Callable 10/15/23 @ 103.44)(1) | | (CCC+, Caa1) | | | 10/15/28 | | | | 6.875 | | | | 1,547,668 | |

| | | | | |

| | 865 | | | Williams Scotsman International, Inc., Rule 144A, Senior Secured Notes

(Callable 08/15/23 @ 102.31)(1) | | (B+, B2) | | | 08/15/28 | | | | 4.625 | | | | 782,570 | |

| | | | | |

| | 1,050 | | | ZipRecruiter, Inc., Rule 144A, Senior Unsecured Notes

(Callable 01/15/25 @ 102.50)(1) | | (BB-, B2) | | | 01/15/30 | | | | 5.000 | | | | 862,628 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 19,915,543 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Tech Hardware & Equipment (4.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,800 | | | Ciena Corp., Rule 144A, Company Guaranteed Notes

(Callable 01/31/25 @ 102.00)(1) | | (BB, Ba1) | | | 01/31/30 | | | | 4.000 | | | | 1,514,907 | |

| | | | | |

| | 1,690 | | | CommScope Technologies LLC, Rule 144A, Company Guaranteed Notes

(Callable 11/14/22 @ 101.00)(1) | | (CCC+, Caa1) | | | 06/15/25 | | | | 6.000 | | | | 1,579,913 | |

| | | | | |

| | 510 | | | CommScope Technologies LLC, Rule 144A, Company Guaranteed Notes

(Callable 11/14/22 @ 102.50)(1) | | (CCC+, Caa1) | | | 03/15/27 | | | | 5.000 | | | | 412,664 | |

| | | | | |

| | 2,000 | | | Entegris Escrow Corp., Rule 144A, Senior Secured Notes

(Callable 01/15/29 @ 100.00)(1) | | (BB+, Baa3) | | | 04/15/29 | | | | 4.750 | | | | 1,770,695 | |

| | | | | |

| | 2,400 | | | Imola Merger Corp., Rule 144A, Senior Secured Notes

(Callable 05/15/24 @ 102.38)(1) | | (BB-, B1) | | | 05/15/29 | | | | 4.750 | | | | 2,073,468 | |

| | | | | |

| | 1,380 | | | Vertiv Group Corp., Rule 144A, Senior Secured Notes

(Callable 11/15/24 @ 102.06)(1) | | (BB-, B1) | | | 11/15/28 | | | | 4.125 | | | | 1,203,781 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 8,555,428 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Telecom - Wireline Integrated & Services (2.9%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,485 | | | Altice France S.A., Rule 144A, Senior Secured Notes

(Callable 09/15/23 @ 102.56)(1) | | (B, B2) | | | 01/15/29 | | | | 5.125 | | | | 1,873,553 | |

See Accompanying Notes to Financial Statements.

14

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | CORPORATE BONDS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Telecom - Wireline Integrated & Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 300 | | | Altice France S.A., Rule 144A, Senior Secured Notes

(Callable 04/15/24 @ 102.56)(1) | | (B, B2) | | | 07/15/29 | | | | 5.125 | | | $ | 226,500 | |

| | | | | |

| | 300 | | | Altice France S.A., Rule 144A, Senior Secured Notes

(Callable 10/15/24 @ 102.75)(1) | | (B, B2) | | | 10/15/29 | | | | 5.500 | | | | 229,328 | |

| | | | | |

| | 4,000 | | | GTT Communications, Inc., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 101.97)(1),(4),(6) | | (NR, WR) | | | 12/31/24 | | | | 0.000 | | | | 280,000 | |

| | | | | |

| | 1,800 | | | LCPR Senior Secured Financing DAC, Rule 144A, Senior Secured Notes

(Callable 12/01/22 @ 103.38)(1) | | (B+, B1) | | | 10/15/27 | | | | 6.750 | | | | 1,680,804 | |

| | | | | |

| | 300 | | | LCPR Senior Secured Financing DAC, Rule 144A, Senior Secured Notes

(Callable 07/15/24 @ 102.56)(1) | | (B+, B1) | | | 07/15/29 | | | | 5.125 | | | | 253,479 | |

| | | | | |

| | 1,000 | | | Virgin Media Secured Finance PLC, Rule 144A, Senior Secured Notes

(Callable 11/10/22 @ 102.50)(1),(10) | | (BB-, Ba3) | | | 04/15/27 | | | | 5.000 | | | | 1,054,592 | |

| | | | | |

| | 600 | | | Vmed O2 UK Financing I PLC, Rule 144A, Senior Secured Notes

(Callable 01/31/26 @ 102.13)(1) | | (BB-, Ba3) | | | 01/31/31 | | | | 4.250 | | | | 478,628 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 6,076,884 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Theaters & Entertainment (2.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,374 | | | AMC Entertainment Holdings, Inc.,10.00% Cash, 12.00% PIK, Rule 144A, Secured Notes (Callable 06/15/23 @ 106.00)(1),(5) | | (CCC-, Caa3) | | | 06/15/26 | | | | 10.000 | | | | 1,262,792 | |

| | | | | |

| | 2,200 | | | Live Nation Entertainment, Inc., Rule 144A, Company Guaranteed Notes

(Callable 12/01/22 @ 100.00)(1) | | (B-, B3) | | | 11/01/24 | | | | 4.875 | | | | 2,141,458 | |

| | | | | |

| | 400 | | | Live Nation Entertainment, Inc., Rule 144A, Company Guaranteed Notes (Callable 12/01/22 @ 102.81)(1) | | (B, B3) | | | 03/15/26 | | | | 5.625 | | | | 382,544 | |

| | | | | |

| | 500 | | | Live Nation Entertainment, Inc., Rule 144A, Company Guaranteed Notes (Callable 12/01/22 @ 103.56)(1) | | (B, B3) | | | 10/15/27 | | | | 4.750 | | | | 445,605 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 4,232,399 | |

| | | | | | | | | | | | | | | | | | |

|

| | Transport Infrastructure/Services (0.9%) | |

| | | | | |

| | 1,800 | | | XPO Escrow Sub LLC, Rule 144A, Senior Unsecured Notes

(Callable 11/15/24 @ 103.75)(1) | | (BB+, Baa3) | | | 11/15/27 | | | | 7.500 | | | | 1,797,579 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Trucking & Delivery (0.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 600 | | | XO Management Holding, Inc., Rule 144A, Senior Unsecured Notes

(Callable 05/01/24 @ 103.94)(1) | | (B-, Caa1) | | | 05/01/27 | | | | 7.875 | | | | 544,326 | |

| | | | | |

| | 1,200 | | | XO Management Holdings, Inc., Rule 144A, Senior Unsecured Notes (Callable 02/01/25 @ 103.19)(1) | | (B-, Caa1) | | | 02/01/30 | | | | 6.375 | | | | 1,001,292 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,545,618 | |

| | | | | | | | | | | | | | | | | | |

| |

| | TOTAL CORPORATE BONDS (Cost $261,278,581) | | | | 216,648,328 | |

| | | | | | | | | | | | | | | | | | |

|

| | BANK LOANS (27.4%) | |

|

| | Aerospace & Defense (1.4%) | |

| | | | | |

| | 1,500 | | | Amentum Government Services Holdings LLC, LIBOR 6M + 8.750%(7),(11) | | (NR, NR) | | | 01/31/28 | | | | 12.920 | | | | 1,365,000 | |

| | | | | |

| | 399 | | | Amentum Government Services Holdings LLC, SOFR 3M + 4.000%(11) | | (B, B1) | | | 02/15/29 | | | | 7.206 - 7.558 | | | | 387,361 | |

| | | | | |

| | 1,214 | | | Peraton Corp., LIBOR 1M + 7.750%(11) | | (NR, NR) | | | 02/01/29 | | | | 11.162 | | | | 1,159,510 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,911,871 | |

| | | | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements.

15

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | BANK LOANS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Auto Parts & Equipment (0.4%) | | | | | | | | | | | | | | |

| | | | | |

| $ | 371 | | | Jason Group, Inc., LIBOR 1M + 1.000% Cash, 9.000% PIK(5),(11) | | (NR, NR) | | | 03/02/26 | | | | 13.754 | | | $ | 365,601 | |

| | | | | |

| | 493 | | | Jason Group, Inc., LIBOR 1M + 2.000% Cash, 4.000% PIK(5),(7),(11) | | (NR, NR) | | | 08/28/25 | | | | 9.754 | | | | 453,294 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 818,895 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Building Materials (0.4%) | | | | | | | | | | | | | | |

| | | | | |

| | 802 | | | Cornerstone Building Brands, Inc., SOFR 1M + 5.625%(11) | | (B, B2) | | | 08/01/28 | | | | 8.927 | | | | 725,560 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Chemicals (2.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,183 | | | Ascend Performance Materials Operations LLC, SOFR 6M + 4.750%(11) | | (BB-, Ba3) | | | 08/27/26 | | | | 8.831 | | | | 2,144,200 | |

| | | | | |

| | 1,268 | | | Polar U.S. Borrower LLC, LIBOR 1M + 4.750%, LIBOR 6M + 4.750%(11) | | (B-, B3) | | | 10/15/25 | | | | 8.096 - 9.021 | | | | 1,028,672 | |

| | | | | |

| | 2,000 | | | Vantage Specialty Chemicals, Inc., LIBOR 3M + 8.250%(7),(8),(11) | | (CCC, Caa2) | | | 10/27/25 | | | | 11.320 | | | | 1,805,000 | |

| | | | | |

| | 878 | | | Zep, Inc., LIBOR 3M + 4.000%(11) | | (CCC+, B2) | | | 08/12/24 | | | | 7.674 | | | | 768,017 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 5,745,889 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Diversified Capital Goods (0.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,503 | | | Electrical Components International, Inc., PRIME + 7.500%(7),(11) | | (B-, B2) | | | 06/26/25 | | | | 13.750 | | | | 1,398,238 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Electronics (1.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,392 | | | Idemia Group, LIBOR 3M + 4.500%(11) | | (B-, B3) | | | 01/09/26 | | | | 8.174 | | | | 2,298,958 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Energy - Exploration & Production (0.0%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,650 | | | PES Holdings LLC, 3.000% PIK(4),(5),(11) | | (NR, NR) | | | 12/31/22 | | | | 3.000 | | | | 83,660 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Food & Drug Retailers (0.7%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,500 | | | WOOF Holdings, Inc., LIBOR 3M + 7.250%(11) | | (CCC, Caa2) | | | 12/21/28 | | | | 10.815 | | | | 1,363,125 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Food - Wholesale (0.2%) | | | | | | | | | | | | | | |

| | | | | |

| | 503 | | | United Natural Foods, Inc., SOFR 1M + 3.250%(11) | | (BB-, B1) | | | 10/22/25 | | | | 7.093 | | | | 499,363 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Gas Distribution (1.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,075 | | | BCP Renaissance Parent LLC, SOFR 3M + 3.500%(11) | | (B+, B2) | | | 10/31/26 | | | | 7.053 | | | | 1,054,698 | |

| | | | | |

| | 1,628 | | | Traverse Midstream Partners LLC, SOFR 1M + 4.250%(11) | | (B+, B3) | | | 09/27/24 | | | | 7.977 | | | | 1,613,361 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 2,668,059 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Health Facility (0.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 811 | | | Carestream Health, Inc., SOFR 3M + 7.500%(11) | | (B-, B3) | | | 09/30/27 | | | | 11.019 - 11.153 | | | | 695,460 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Health Services (1.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,230 | | | MedAssets Software Intermediate Holdings, Inc.(12) | | (CCC, Caa2) | | | 12/17/29 | | | | 0.000 | | | | 1,063,335 | |

| | | | | |

| | 2,383 | | | U.S. Radiology Specialists, Inc., LIBOR 3M + 5.250%(11) | | (B-, B3) | | | 12/15/27 | | | | 8.924 | | | | 2,144,126 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 3,207,461 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Investments & Misc. Financial Services (1.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 2,329 | | | AqGen Ascensus, Inc., LIBOR 3M + 6.500%(11) | | (CCC, Caa2) | | | 08/02/29 | | | | 10.250 | | | | 2,084,848 | |

| | | | | |

| | 1,298 | | | Deerfield Dakota Holding LLC, LIBOR 1M + 6.750%(11) | | (CCC, Caa2) | | | 04/07/28 | | | | 10.504 | | | | 1,260,757 | |

See Accompanying Notes to Financial Statements.

16

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | BANK LOANS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Investments & Misc. Financial Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 130 | | | Ditech Holding Corp.(4),(6),(7) | | (NR, NR) | | | 06/30/22 | | | | 0.000 | | | $ | 16,264 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 3,361,869 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Life Insurance (0.5%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,281 | | | Vida Capital, Inc., LIBOR 1M + 6.000%(7),(11) | | (CCC+, B2) | | | 10/01/26 | | | | 9.754 | | | | 1,037,306 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Machinery (0.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,223 | | | LTI Holdings, Inc., LIBOR 1M + 6.750%(8),(11) | | (CCC+, Caa2) | | | 09/06/26 | | | | 10.504 | | | | 1,057,823 | |

| | | | | |

| | 582 | | | LTI Holdings, Inc., LIBOR 1M + 3.250%(11) | | (B-, B2) | | | 09/06/25 | | | | 7.004 | | | | 544,000 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,601,823 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Medical Products (0.8%) | | | | | | | | | | | | | | |

| | | | | |

| | 919 | | | Femur Buyer, Inc., LIBOR 3M + 5.500%(7),(11) | | (NR, NR) | | | 03/05/24 | | | | 9.174 | | | | 768,100 | |

| | | | | |

| | 982 | | | Viant Medical Holdings, Inc., LIBOR 1M + 6.250%(7),(11) | | (CCC+, B3) | | | 07/02/25 | | | | 10.004 | | | | 965,089 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 1,733,189 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Packaging (0.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 800 | | | Strategic Materials, Inc., LIBOR 3M + 7.750%(8),(11) | | (CC, C) | | | 10/31/25 | | | | 10.532 | | | | 288,000 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Personal & Household Products (1.6%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | ABG Intermediate Holdings 2 LLC, SOFR 1M + 6.000%(11) | | (CCC+, Caa1) | | | 12/20/29 | | | | 9.829 | | | | 1,117,500 | |

| | | | | |

| | 1,730 | | | Serta Simmons Bedding, LLC, First Out Term Loan, LIBOR 3M + 7.500%(11) | | (B-, B3) | | | 08/10/23 | | | | 10.793 | | | | 1,684,997 | |

| | | | | |

| | 1,048 | | | Serta Simmons Bedding, LLC, Second Out Term Loan, LIBOR 3M + 7.500%(11) | | (CCC+, Ca) | | | 08/10/23 | | | | 10.793 | | | | 526,040 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 3,328,537 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Pharmaceuticals (0.3%) | | | | | | | | | | | | | | |

| | | | | |

| | 583 | | | Akorn, Inc., LIBOR 3M + 7.500%(11) | | (CCC+, Caa3) | | | 10/01/25 | | | | 11.243 | | | | 552,836 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 552,836 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Recreation & Travel (2.0%) | | | | | | | | | | | | | | |

| | | | | |

| | 959 | | | Bulldog Purchaser, Inc., LIBOR 1M + 7.750%(11) | | (CCC-, Caa3) | | | 09/04/26 | | | | 11.579 | | | | 829,837 | |

| | | | | |

| | 1,820 | | | Bulldog Purchaser, Inc., LIBOR 1M + 3.750%(11) | | (B-, B3) | | | 09/05/25 | | | | 7.579 | | | | 1,594,715 | |

| | | | | |

| | 791 | | | Hornblower Sub LLC, LIBOR 3M + 4.500%(11) | | (CCC-, Caa2) | | | 04/27/25 | | | | 8.670 | | | | 586,576 | |

| | | | | |

| | 1,082 | | | Hornblower Sub LLC, LIBOR 3M + 8.125%(11) | | (NR, NR) | | | 11/10/25 | | | | 11.048 | | | | 1,093,299 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 4,104,427 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Restaurants (0.1%) | | | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Tacala LLC, LIBOR 1M + 7.500%(11) | | (CCC, Caa2) | | | 02/04/28 | | | | 11.254 | | | | 272,297 | |

| | | | | | | | | | | | | | | | | | |

| | | | |

| | Software - Services (5.0%) | | | | | | | | | | | | | | |

| | | | | |

| | 1,714 | | | Aston FinCo Sarl, LIBOR 1M + 4.250%(11) | | (B-, B2) | | | 10/09/26 | | | | 8.004 | | | | 1,610,801 | |

| | | | | |

| | 893 | | | Astra Acquisition Corp., LIBOR 1M + 5.250%(11) | | (B, B2) | | | 10/25/28 | | | | 9.004 | | | | 781,165 | |

| | | | | |

| | 900 | | | CommerceHub, Inc., LIBOR 1M + 7.000%(11) | | (CCC, Caa2) | | | 12/29/28 | | | | 10.674 | | | | 721,688 | |

| | | | | |

| | 1,810 | | | Epicor Software Corp., LIBOR 1M + 7.750%(11) | | (CCC, Caa2) | | | 07/31/28 | | | | 11.504 | | | | 1,781,999 | |

| | | | | |

| | 684 | | | Finastra U.S.A., Inc., LIBOR 3M + 3.500%(11) | | (CCC+, B2) | | | 06/13/24 | | | | 6.871 | | | | 621,130 | |

| | | | | |

| | 3,511 | | | Finastra U.S.A., Inc., LIBOR 1WK + 7.250%(11) | | (CCC-, Caa2) | | | 06/13/25 | | | | 10.621 | | | | 2,632,896 | |

| | | | | |

| | 1,200 | | | Project Alpha Intermediate Holding, Inc.(12) | | (B, B3) | | | 04/26/24 | | | | 0.000 | | | | 1,169,748 | |

See Accompanying Notes to Financial Statements.

17

Credit Suisse High Yield Bond Fund

Schedule of Investments (continued)

October 31, 2022

| | | | | | | | | | | | | | | | | | |

Par

(000) | | | | | Ratings†

(S&P/Moody’s) | | Maturity | | | Rate% | | | Value | |

| | | | |

| | BANK LOANS (continued) | | | | | | | | | | | | | | |

| | | | |

| | Software - Services | | | | | | | | | | | | | | |

| | | | | |

| $ | 748 | | | Quest Software U.S. Holdings, Inc., SOFR 3M + 4.250%(11) | | (B-, B2) | | | 02/01/29 | | | | 8.494 | | | $ | 556,930 | |

| | | | | |

| | 748 | | | Redstone Holdco 2 LP, LIBOR 3M + 4.750%(11) | | (B-, B3) | | | 04/27/28 | | | | 9.108 | | | | 541,045 | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | 10,417,402 | |

| | | | | | | | | | | | | | | | | | |

| | | | |