UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant þ Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| þ | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to § 240.14a-12 |

CH ENERGY GROUP, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than Registrant)

Payment of Filing Fee (Check the appropriate box):

| þ | No fee required. |

| ¨ | Fee computed below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11 and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Shareholder Presentation Overview of Fortis Transaction Thursday, May 31, 2012 |

2 Forward-Looking Statements Additional Information about the Proposed Fortis Transaction and Where to Find It This communication is being made in respect of the proposed merger transaction involving CH Energy Group and Fortis and may be deemed to be soliciting material relating to the proposed transaction. In connection with the proposed acquisition of CH Energy Group by Fortis, CH Energy Group filed a proxy statement with the SEC on May 9, 2012, and may file other relevant materials with the SEC as well. The proposed transaction will be submitted to CH Energy Group's shareholders for their consideration. Before making any voting or investment decision, investors and shareholders of CH Energy Group are urged to read the proxy statement, and other relevant materials filed with the SEC when they become available, because they contain or will contain important information about the proposed acquisition and related matters. The proxy statement has been mailed to CH Energy Group shareholders. Investors and shareholders may obtain a free copy of the proxy statement and other documents filed by CH Energy Group at the SEC's Web site, www.sec.gov. These documents (when they are available) can also be obtained by investors and shareholders free of charge from CH Energy Group at CH Energy Group’s website at www.chenergygroup.com, or by contacting CH Energy Group's Shareholder Relations Department at (845) 486-5204. Participants in the Solicitation of Proxies Statements included in this presentation which are not historical in nature are intended to be, and are hereby identified as, “forward-looking statements” for purposes of the safe harbor provided by Section 21E of the Exchange Act. Forward-looking statements may be identified by words including “anticipates,” “intends,” “estimates,” “believes,” “projects,” “expects,” “plans,” “assumes,” “seeks,” and similar expressions. Forward-looking statements including, without limitation, those relating to CH Energy Group, Inc.’s and Central Hudson Gas & Electric Company’s future business prospects, revenues, proceeds, working capital, investment valuations, liquidity, income, and margins, as well as statements relating to CH Energy Group, Inc.'s proposed acquisition by a subsidiary of Fortis, Inc. and the expected terms and timing of the transaction, are subject to certain risks and uncertainties that could cause actual results to differ materially from those indicated in the forward-looking statements, due to several important factors, including those identified from time-to-time in the forward-looking statements. Those factors include, but are not limited to: the possibility that various conditions precedent to the consummation of the proposed Fortis transaction will not be satisfied or waived; the ability to obtain shareholder and regulatory approvals of the proposed Fortis transaction on the timing and terms thereof; deviations from normal seasonal weather and storm activity; fuel prices; energy supply and demand; potential future acquisitions; legislative, regulatory, and competitive developments; interest rates; access to capital; market risks; electric and natural gas industry restructuring and cost recovery; the ability to obtain adequate and timely rate relief; changes in fuel supply or costs including future market prices for energy, capacity, and ancillary services; the success of strategies to satisfy electricity, natural gas, fuel oil, and propane requirements; the outcome of pending litigation and certain environmental matters, particularly the status of inactive hazardous waste disposal sites and waste site remediation requirements; and certain presently unknown or unforeseen factors, including, but not limited to, acts of terrorism and other factors described in, or incorporated by reference in, but are not limited to, CH Energy Group Inc.'s proxy statement filed with the SEC. CH Energy Group and Central Hudson undertake no obligation to update publicly any forward-looking statements, whether as a result of new information, future events, or otherwise. Given these uncertainties, undue reliance should not be placed on the forward-looking statements. CH Energy Group, Fortis and certain of their respective directors and executive officers, under SEC rules, may be deemed to be participants in the solicitation of proxies from shareholders of CH Energy Group in connection with the proposed acquisition. Information about CH Energy's directors and executive officers may be found in its 2011 Annual Report on Form 10-K filed with the SEC on February 16, 2012, and definitive proxy statement relating to its 2012 Annual Meeting of Shareholders filed with the SEC on March 21, 2012. Information about Fortis directors and executive officers may be found in its Management Information Circular available on its website at www.fortisinc.com. Additional information regarding the interests of such potential participants in the solicitation of proxies in connection with the proposed merger is included in the proxy statement filed with the SEC on May 9, 2012 and may be included in other relevant materials filed with the SEC when they become available. |

FORTIS TRANSACTION On February 21, 2012, CH Energy announced an agreement with Fortis for a sale of CH Energy at a price of $65.00 per share in cash 100% cash consideration Locks in premium value at a time of cyclically high industry valuations Fortis purchase price represents a 21.9x P/E multiple on 2011A EPS—at the high end of these multiple ranges for comparable utility industry transactions Transaction terms do not preclude other interested parties from making a topping offer prior to shareholder approval The Fortis federation business model will allow CH Energy to largely operate as an independent entity, with little change in its day-to-day services and operations Will have improved access to growth capital as a Fortis affiliate 3 $65 per share IN CASH Compelling value for shareholders |

4 FORTIS TRANSACTION Key transaction terms ACQUIROR Fortis Inc., the largest investor-owned distribution utility in Canada, with assets of approximately $14 billion CONSIDERATION $65.00 per share in cash FUTURE DIVIDENDS CH Energy expects to pay its regular quarterly common stock dividends (currently $0.555/share) in the ordinary course through closing, subject to the discretion of its Board of Directors KEY CLOSING CONDITIONS No material adverse effect on CH Energy CH Energy shareholder approval Regulatory approvals No financing condition for Fortis BREAK-UP FEE Approximately $19.7 million; 2% of implied equity value OTHER Customary non-solicit provision with fiduciary out for Board 12-month drop-dead date (with 6 month extension for regulatory approvals, if necessary) |

In May 2011, CH Energy was approached by a representative of Fortis to ascertain CH Energy’s interest in pursuing a potential transaction with Fortis Fortis had very recently agreed to pay an attractive multiple of earnings for Central Vermont Public Service Fortis, however, expressed unwillingness to participate in an auction process Fortis had a publicly stated strategic objective of growing in the U.S. through utility acquisitions The Board conducted a strategic review and valuation of its standalone plan in the summer of 2011 Concluded that it would be worth engaging with Fortis on a confidential basis to determine what price/value they would see in CH Energy Offer represented multiple of 20.4x 2011E EPS and a 19.7% premium over the closing price of CH Energy common stock on the last trading day prior to the offer 5 FORTIS TRANSACTION On November 28, 2011, Fortis, at the request of CH Energy, provided its initial indicative offer of $62.70 in cash per share of CH Energy common stock How did our Board maximize shareholder value? |

CH Energy’s Board determined CH Energy should seek a higher price from Fortis and provide further access to confidential information to encourage Fortis to find additional value, but not to approach other potential transaction partners The Board considered several factors regarding process, including the limited universe of potential transaction partners, Fortis unwillingness to participate in an auction, risks of leaks and further diversion of management and employees, and the ability to seek merger agreement terms that would not preclude alternative proposals post-signing and prior to shareholder approval After additional due diligence, CH Energy instructed Fortis to provide its “best and final” offer On February 13, 2012 Fortis submitted an offer of $64.20 in cash per share Agreed to a 2% break-up fee after extensive negotiation CH Energy’s Board continued to seek an additional increase in price to at least $65.00 per share Fortis agreed to a $65.00 per share all-cash price, and the parties entered into the merger agreement on February 20, 2012 To date, no other party has approached CH Energy regarding an alternative transaction 6 FORTIS TRANSACTION How did our Board maximize shareholder value? |

Secures premium for CH Energy shareholders, on top of CH Energy’s already above-peer and historically high trading value and trading multiples Cash consideration Locks in value at a time of cyclically high valuations for the industry Eliminates downside from potential industry dynamics, including rate/regulatory risks Eliminates downside from potential macroeconomic changes, including increases in interest rates and dividend tax rates, which could adversely affect CH Energy’s stock price Significant value premium vs. standalone prospects Eliminates risks to value/stock price associated with potential inability to achieve long- term strategic plans 7 FORTIS TRANSACTION Benefits of the transaction |

Full and fair value Offer evaluated by experienced financial advisor (Lazard) to be fair, from a financial point of view, to CH Energy shareholders Continuation of quarterly common stock dividends pre-merger close Limited alternatives (particularly M&A) available Low break-up fee (2% of equity deal value) if a superior offer arises Fortis is a large, high quality company who has a demonstrated history of growing successfully through prior acquisitions Benefits to customers and commitment to charitable contributions enhance probability of closing 8 FORTIS TRANSACTION Benefits of the transaction Fortis price is at the top end of financial advisor’s private market valuation range Process involved significant negotiation with Fortis over time, including two increases in their offer price |

9 COMPLETION OF STRATEGIC SHIFT In 2011, CH Energy completed its “strategic shift” Further shareholder upside is limited given: More moderate EPS growth (rate) going forward (beyond 2012) Trading at healthy premium to peers Historically low interest rate environment Potential increase in taxation of dividends Insufficient scale to pursue significant value-enhancing growth projects Ongoing regulatory risk Limited universe of alternate acquirors Divested renewable energy portfolio Use proceeds to repurchase stock, retire debt Focus on energy delivery: Invest in Central Hudson’s delivery system Grow Griffith’s customer base Improve service quality and customer satisfaction Strategic shift reduced business risk; CH Energy share price reacted favorably to refocus on the core business |

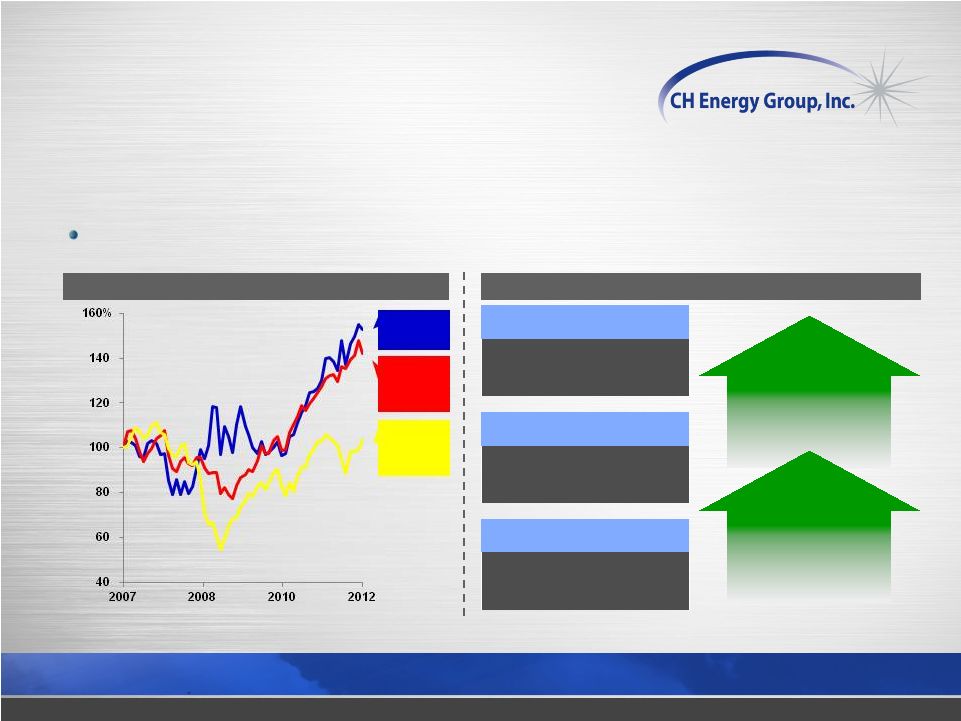

10 COMPLETION OF STRATEGIC SHIFT 2011 EPS $2.97 2010 EPS $2.44 5-YEAR SHAREHOLDER RETURN STRONG INCREASE IN EPS Source: FactSet. Note: Trading data as of February 17, 2012 (last trading day prior to transaction announcement). 1 Here and throughout this presentation, CH Energy peers are Consolidated Edison, Northeast Utilities, NorthWestern, NSTAR, Pepco, UIL and WGL. 2 Based on Management estimates provided to Fortis (and included in proxy filings). Management has created significant shareholder value over the past several years 2012E EPS $3.47 17% INCREASE 22% INCREASE CHG 52.6% CHG Peers 1 41.9% S&P 500 3.7% Significant growth in EPS from 2010 – 2012E; this growth rate is unsustainable going forward 2 |

11 TRADING PERFORMANCE CH Energy was trading near its all-time high CH ENERGY 10-YEAR HISTORICAL TRADING PRICE Fortis Price: $65.00 9.5% Premium Transaction Represents 9.5% Premium to All- Time High Source: FactSet. Note: Trading data as of February 17, 2012 (last trading day prior to transaction announcement). 1 All-time high closing price of $59.37 occurred on December 29, 2011. 1 1 |

12 TRADING PERFORMANCE NTM P/E PERFORMANCE—LAST 20 YEARS CH Energy trading at a forward P/E premium Source: FactSet. Note: Trading data as of February 17, 2012 (last trading day prior to transaction announcement). 10-YEAR TREASURY YIELD—LAST 20 YEARS High absolute P/E and relative to both utility peers and vs. S&P Interest rates, which are at historic lows, typically exhibit a strong negative correlation with utility market valuations |

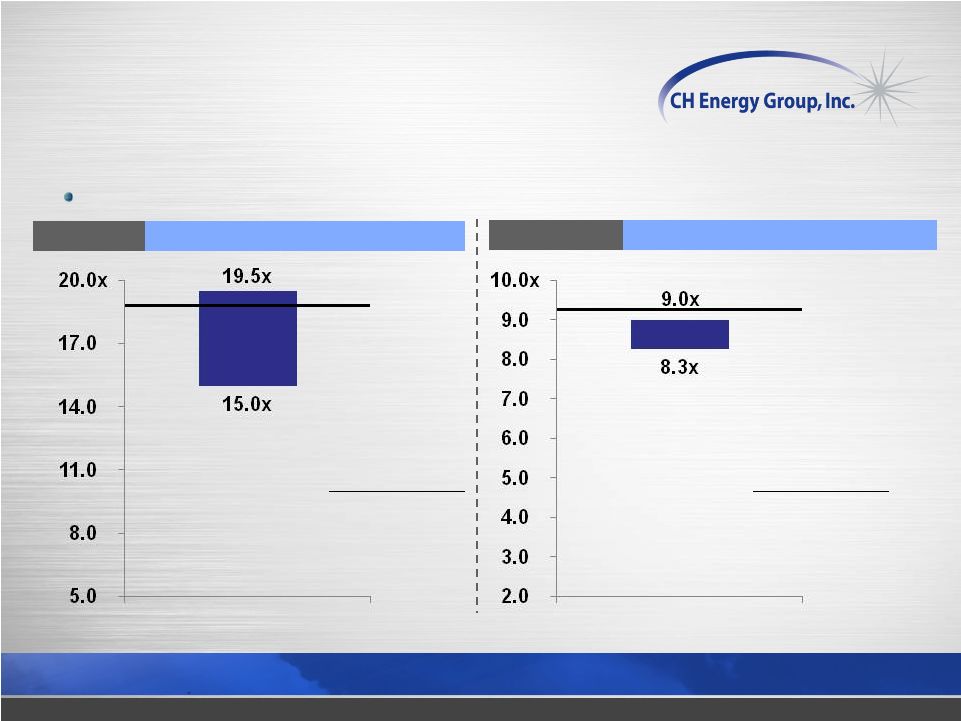

13 Fortis Price: 18.7x Fortis Price: 9.2x ATTRACTIVE VALUE PROPOSITION Proposed price is at attractive valuation 2012E EPS PRECEDENT RANGE 1 : 15.0x – 19.5x 2012E EBITDA PRECEDENT RANGE 1 : 8.3x – 9.0x Recent Transactions Gaz Métro–CVPS: 19.6x AGL–Nicor: 18.1x AES–DPL: 12.4x Exelon– Constellation: 11.9x Recent Transactions Gaz Métro–CVPS: NA AGL–Nicor: 7.7x AES–DPL: NA Exelon– Constellation: 5.9x Note: Based on Management estimates; see proxy filing for additional detail. 1 Reflects transaction multiples based on Lazard’s analysis of the relevant metrics, after adjusting for certain outliers. 2 Multiples reflect 1-year forward multiples as of respective transaction announcement dates. Does not represent comprehensive list of precedent transactions reviewed. Fortis purchase price is near the top of the range of selected comparable transactions 2 2 |

14 ATTRACTIVE VALUE PROPOSITION Proposed price is at attractive valuation 2013E EPS PEER TRADING RANGE: 13.5x – 16.4x 2012E EPS PEER TRADING RANGE: 14.4x – 16.8x Fortis Price: 18.7x CHG Pre- Announce: 16.6x Fortis Price: 19.1x CHG Pre- Announce: 16.9x Note: Based on Management estimates; see proxy filing for additional detail. 20% premium to midpoint of peer range 28% premium to midpoint of peer range Fortis purchase price is well above the range of peer P/E trading multiples CH Energy had been trading at a P/E multiple premium to its peers prior to the transaction announcement 14.4x 16.8x 5.0 8.0 11.0 14.0 17.0 20.0x 13.5x 16.4x 5.0 8.0 11.0 14.0 17.0 20.0x |

15 ATTRACTIVE VALUE PROPOSITION 2013E EBITDA PEER TRADING RANGE: 7.4x – 8.6x 2012E EBITDA PEER TRADING RANGE: 7.8x – 8.8x Proposed price is at attractive valuation Fortis Price: 9.2x Fortis Price: 9.1x CHG Pre- Announce: 8.5x CHG Pre- Announce: 8.4x 11% premium to midpoint of peer range 14% premium to midpoint of peer range Note: Based on Management estimates; see proxy filing for additional detail. 10.0x 9.0 8.0 7.0 6.0 5.0 4.0 3.0 2.0 8.8x 7.8x 10.0x 9.0 8.0 7.0 6.0 5.0 4.0 3.0 2.0 8.6x 7.4x Fortis purchase price is well above the range of peer EV/EBITDA trading multiples |

16 ATTRACTIVE VALUE PROPOSITION Our Board reviewed a variety of methodologies used by Lazard to evaluate the transaction Note: See proxy filing for additional detail. Fortis Price: $65.00 $47.44 $49.50 $48.25 $50.75 $47.75 $52.25 $59.74 $57.00 $56.00 $58.00 $55.75 $62.75 40.00 50.00 60.00 $70.00 52-Week High/Low Comparable Company Multiples— Consolidated Comparable Company Multiples— Sum-of- the-Parts Discounted Cash Flow— Consolidated Discounted Cash Flow— Sum-of- the-Parts Selected Precedent Transactions The Fortis purchase price exceeds the value expected to be derived from the standalone plan and eliminates many risks associated with executing on such plan |

Transfers regulatory, operational, interest rate, and general market/utility valuation risk away from shareholders Fixed price, cash transaction avoids “equity valuation risk” (both market and company specific) present in stock-for-stock deals Low break-up fee “leaves the door open” for competing bidders prior to shareholder approval (however, prospect unlikely given high valuation and limited potential buyer universe) Transaction terms give CH Energy operational flexibility during closing process (including ability to declare and pay regular quarterly common dividends in the ordinary course) 17 FORTIS TRANSACTION Merger terms minimize risk to shareholders Break-up fee as a % of purchase price well below peer utility industry transaction average |

The Board concluded that the Fortis offer represents a significant premium over CH Energy’s standalone value and other strategic alternatives Low break-up fee does not preclude other interested parties from making a topping offer prior to shareholder approval The Board recommends that shareholders vote for the transaction 18 SUMMARY RECOMMENDATION |

Proxy Statement Mailed: May 14 Special Meeting of Shareholders: June 19 FERC FTC/DOJ—Hart-Scott-Rodino Act Committee on Foreign Investment in the U.S. NY PSC 19 TRANSACTION TIMETABLE Next steps Shareholder approval schedule Pursue required regulatory approvals BEST ESTIMATE OF CLOSING DATE 1 ST QUARTER OF 2013* *Could change Closing can occur once all approvals are received |