Exhibit 99.1

CGI Group Inc.

2012 Annual Report

CGI’s 2012 Annual Report is comprised

of two separate volumes:

Volume 1:Experience the commitment

&

Volume 2:Numbers

Volume 1 of the Annual Report

follows this page.

(this page does not form part of the Annual Report)

2012 annual report

Experience the commitment®

The CGI Constitution

Our dream

To create an environment in which we enjoy working together and, as owners, contribute to building a company we can be proud of.

Our mission

To help our clients with professional services of outstanding quality, competence and objectivity, delivering the best solutions to fully satisfy client objectives in information technology, business processes and management. In all we do, we foster a culture of partnership, intrapreneurship, teamwork and integrity, building a world class IT and business process services company.

Our vision

To be a world class IT and business process services leader helping our clients succeed.

Our values

Partnership and quality

For us, partnership and quality are both a philosophy and a way of life. We develop and follow the best management practices and we entrench these approaches into client relationships and service delivery frameworks in order to foster long-term and strong partnerships with our clients. We listen to our clients and we are committed to their total satisfaction in everything we do.

Objectivity and integrity

We exercise the highest degree of independent thinking in selecting the products, services and solutions we recommend to clients. In doing so, we adhere to the highest values of quality, objectivity and integrity. Consequently, strict rules of business and professional conduct are applied. We do not accept any remuneration from suppliers.

Intrapreneurship and sharing

Our success is based on the competence, commitment and enthusiasm of our members. Therefore, we promote a climate of innovation and initiative where we are empowered with a sense of ownership in supporting clients, thus ensuring the firm’s profitable growth. Through teamwork, sharing our know-how and expertise, we bring the best of CGI to our clients. As members, we share in the value we create through equity ownership and profit participation.

Respect

As a global company, we recognize the richness that diversity brings to the company and welcome this diversity while embracing the overall CGI culture. In all we do, we are respectful of our fellow members, clients, business partners and competitors.

Financial strength

We strive to deliver strong, consistent financial performance, which sustains long-term growth and rewards our members and shareholders. Financial strength enables us to continuously invest and improve services and business solutions to the benefit of our clients. To this end, we manage our business to generate industry superior returns.

Corporate social responsibility

Our business model is designed to ensure that we are close to our clients and communities. As members, we embrace our social responsibilities and contribute to the continuous development of the communities in which we live and work.

Visit our online annual report to access the complete financial report and learn how our committed approach achieves results for our clients.

cgi.com/2012-ar

For 36 years, CGI has been a reliable and trusted partner committed to our clients’ success, providing flexibility, accountability and quality through our client proximity business model and the application of our Management Foundation.

Historically, CGI has profitably doubled its size every three to five years. With the combination of CGI and Logica, we now have the scale to offer our clients greater presence, service capabilities and expertise around the world. We are also better positioned to provide our professionals, or members as we refer to them, with opportunities to build rewarding careers and to deliver shareholders superior results and industry-leading returns for the long term.

CGI: Experience the commitment®

CGI: Built to grow and last.

Experience has taught us that clients, employees and shareholders want to be associated with the best—the best partner, the best employer and the best investment. We are passionate about building and operating a sound, stable and growing business for the benefit of all stakeholders.

Clients:

Fostering long-term relationships with 10,000 global clients

For CGI, global growth is not an option; it is a necessity. As markets globalize, so does a significant portion of our client base. In fact, 60% of our largest clients have a presence in both North America and in Europe, while approximately a third are in North America, Europe and Asia. We are dedicated to growing and expanding our capabilities to serve all of our clients wherever they are.

In line with this commitment and consistent with our profitable growth strategy, 2012 will be remembered as a milestone year for CGI. On August 20, 2012 we enthusiastically welcomed 41,000 new colleagues into the CGI family as we merged with UK-based Logica. We did so, not with an eye on becoming the biggest, but to become the best. We strive to deliver performance that sustains long-term growth, increases client loyalty and rewards our members and shareholders.

In addition, we now have access to the European IT market, which we consider very attractive as it represents approximately 30% of the global IT spend. Perhaps more acutely than ever, Europe’s ongoing economic and social challenges will require IT investments to increase efficiency and achieve the cost curtailment required to remain competitive.

We are now stronger than ever, significantly expanding our reach and bringing critical mass to both local and global clients. As we expand alongside them, both at home and abroad, we understand that our success as a business is measured by our clients’ success and directly linked to their trust and confidence in CGI. Our track record of profitable and rapid growth, including more than 70 successful integrations, provide us the necessary execution experience and confidence to ensure synergies are delivered and efficiencies are gained quickly and seamlessly.

Together, as a team of 72,000 members across a network of 400 local offices in 40 countries, our model is designed to empower local decision making and accountability. With strong market positions in North America, Europe and Asia Pacific, CGI is now the fifth largest independent IT services provider worldwide, generating more than $10 billion in combined annual revenue and providing a balanced blend of onshore, nearshore and offshore delivery options that bring our vast experience and expertise to clients’ front doors.

We pride ourselves on the long-term and deep relationships we’ve developed with our clients, which have been the guiding force behind many of our innovations and service offerings. By aligning our future strategies to clients’ critical business imperatives, we have become a leader in such technologies as cloud computing and health information exchanges and are at the forefront of cybersecurity and biometrics.

This culture of innovation has helped us prepare not only for today’s needs, but also for the opportunities and challenges that tomorrow will bring. It is through innovative thinking and a consultative approach to doing business with our clients that we have booked $5.2 billion in new business during fiscal 2012, increasing our backlog to $17.6 billion.

In fiscal 2012, we continued our tradition of high client satisfaction, scoring an average of 9.1 out of 10 based on signed client assessments CGI rigorously conducts with its clients. As important, we received a 9.4 rating for client loyalty, denoting our clients’ intent to continue to use and recommend CGI’s services to others. Client loyalty is important in any business, but in a services business like ours, it is vital. That is why we are prioritizing the roll out of our client assessment program across the Logica client base in fiscal 2013.

Members:

Building a company we can be proud of

As members, we are encouraged to be owners, enjoy our work and benefit from the success that comes from building a company that best satisfies the needs of all our stakeholders. This is why the motivation of our members differentiates us. At CGI, we are easier to do business with because we are driven, individually and collectively, to satisfy our clients and grow our company.

While most companies have a vision and mission, CGI goes a step beyond. We have a company dream:

“To create an environment in which we enjoy working together and, as owners, contribute to building a company we can be proud of.”

A key aspect of our management approach is ownership, because it is empowering, fosters engagement and instills accountability among our members.

As a result, we have one of the lowest attrition rates in the industry. Our ability to attract and retain top talent provides clients with the best experts and long-term partners to drive the innovation, cost reductions and improved operations critical to their success. In fact, our clients’ satisfaction is the top driver of our members’ satisfaction based on our annual member consultation.

Shareholders:

Creating sustainable value for the long term

At CGI, we’ve always understood that to be a strong global company we need to be strong financially. Our financial strength is a cornerstone of our commitment to be the best. It has enabled us to continuously invest in and improve services, to innovate and to profitably grow CGI for the benefit of all stakeholders.

This consistent and disciplined approach has provided the necessary fuel to successfully execute our “Build and Buy” profitable growth strategy, delivering both strong organic growth and accretive acquisitions throughout our history.

During fiscal 2012, CGI’s share price increased by approximately 35%, adding $3 billion to the market value of CGI. Consistent with our acquisition history, we expect the Logica transaction to create additional shareholder value and be accretive to our earnings per share by 25-30% before acquisition related and integration costs in fiscal 2013 and continue accelerating throughout the three-year integration period.

Our ability to generate consistent results with industry leading margins is proof that adhering to the fundamentals of operational and delivery excellence is key to running a sound and stable business.

We greatly appreciate the trust our shareholders have placed in us. We are committed to creating long-term value, while maintaining the flexibility to capitalize on new opportunities as they arise.

Committed to being the best

In all we do, we strive to be the best—continuously expanding our capabilities so that we can meet our commitments, earn new business and, ultimately, exceed expectations. Going forward, this continues to be our goal and our passion.

We want to thank you for your continued interest and commitment to CGI. Together, we will remain a strong, stable company anchored in profitable growth—today and in the years to come.

Serge Godin

Founder and

Executive Chairman of the Board

Michael E. Roach

President and

Chief Executive Officer

Revenue growth

13%

Recurring revenue of

64%

Market cap up 58% to

$8.1 billion

Annual revenue to exceed

$10 billion

Satisfying clients is our business

Through a consistent, disciplined and accountable delivery approach, CGI has achieved an industry-leading track record of on-time, on-budget projects, helping clients leverage current investments while adopting new technology. As a result of this approach, our average client satisfaction score for the past 10 years has measured consistently higher than 9 out of 10.

CGI’s geographical reach covers 85% of global IT spending. With this global presence, CGI is well positioned to help our clients win and grow. In addition, our high level of recurring revenue enables us to maintain long-term relationships and invest in the future for the benefit of our clients.

Business highlights*

(based on fiscal 2012 revenue)

Contract types

64%

Management of IT and business functions (outsourcing)

46%

IT services

18%

Business process services

36%

Systems integration and consulting

Geographic markets (based on client domicile)

47%

United States

36%

Canada

17%

Rest of world

Targeted verticals

40%

Government

22%

Financial services

14%

Telecommunications and utilities

14%

Manufacturing, retail and distribution

10%

Health

Backlog of long-term signed contracts

$17.6 billion

New contract bookings

$5.2 billion

| * | Includes Logica revenue from August 20, 2012. |

cgi.com/2012-ar/at-a-glance

Global rank 5th among independent IT and BPS firms

Proven performance 95% on-time, on-budget

Client loyalty 9.4 out of 10 based on signed clients assessments

Our approach

Clients tell us the way we deliver services is a primary reason they select CGI. These are the key characteristics that distinguish our approach.

People—Our members are motivated, as owners, to build our company and best satisfy client needs.

Proximity—Our members across 400 local offices are empowered with local decision making while bringing global capabilities.

Quality—Consistent processes across our operations enable consistent outcomes which are measured and continuously improved.

Services—Industry and technology expertise, end to end services and rich IP-based solutions deliver performance.

Creativity—We drive innovation together with our clients to better support their business strategies.

Financial strength—36 years of disciplined performance and sustained growth facilitate long-term relationships and large-scaleengagements.

Our services

CGI offers a full spectrum of services, solutions and industry know-how to accelerate clients’ business transformation.

High-end business and IT consulting—Vast array of services, including business and IT strategy, enterprise architecture, process redesign, change management and performance measurement.

Systems integration—System architecture, system development and implementation of business and technology solutions.

Application development and management—Design, development, implementation, maintenance and improvement of business applications.

Infrastructure services—Comprehensive infrastructure management capabilities that adapt to business requirements and service priorities.

Business process services—Management of back-office business processes to streamline operations.

IP-based solutions—Deep portfolio of 100+ mission-critical solutions.

Our industries

CGI offers its end-to-end services to a selected set of economic sectors covering 90% of global IT spend.

Financial services—Helping financial institutions, including most major banks and top insurers, reduce cost, increase efficiency and improve customer service.

Government—Supporting over 2,000 government organizations in reducing costs and improving the efficiency, quality and accountability of public services, all while increasing citizen engagement.

Health—Helping more than 1,000 healthcare facilities, hospitals and departments of health implement solutions for better care, better business and better outcomes.

Telecommunications and utilities—Helping 6 of the top 10 global telecom providers and 9 of the top 10 European utilities deliver new revenue streams and improve productivity and service.

Manufacturing, retail and distribution—Enabling business transformation for more than 2,000 clients by improving efficiency and loyalty, lowering costs and boosting sustainable growth.

Oil and gas—Helping our clients, including 3 of the top 6 oil companies, extract more value from every aspect of their supply chains.

Creating significant shareholder value over time

The strength of our profitability, cash flow and recurrent revenue streams reflect the discipline that allowed us to build a sound and stable enterprise for the long term. Our successful “Build and Buy” profitable growth strategy balances strong organic growth and the successful integration of more than 70 acquisitions. We are committed to creating additional value for our shareholders over time as we continue to adhere to the same fundamentals that have guided us throughout our 36-year history.

Revenue

In billions of dollars

Contract backlog

In billions of dollars

New contract bookings

In billions of dollars

Cash provided by operating activities

In millions of dollars

Number of members at year end

CGI’s 2012 and 2011 financial results are reported under IFRS and the 2010 results are reported under Canadian GAAP.

Corporate social responsibility

Promoting a caring culture

As one of our core values, CSR represents a key aspect of our business model, which is designed to bring us closer to our members, clients, shareholders and communities. We’ve always believed that balancing this equilibrium between our stakeholders is key to our long term sustainability. Last year, we linked all our best practices to a new global policy formalizing our approach and identifying the following commitments:

Provide our professionals with training, health, wellness and ownership programs that positively influence their well-being and satisfaction

Partner with our clients to deliver energy and environmental sustainability solutions and to collectively support charitable causes

Support our communities through causes that improve their social, economic and environmental well-being

Improve the environment through environmentally-friendly operating practices, community service activities and green IT offerings

Continue operating with the highest level of integrity through a strong code of ethics and good corporate governance

Extend our CSR commitments to our supply chain

As a further step, we published a roadmap, which has brought our policy to life by defining objectives and measures to support our commitments. This coming year, we will publish our first global CSR report to present quantitative and qualitative results, identify achievements and list key indicators on which we aim to set our objectives going forward. We look forward to sharing our progress with you, and continuing our journey as a responsible and caring partner.

cgi.com/csr

Creativity to transform and add value

Driving innovation, reducing costs and improving operations are strategic business imperatives. CGI members work alongside our clients locally, while bringing the depth and breadth of our global resources to solve these complex challenges—and more.

CGI offers innovative solutions to gain operating efficiencies, reduce costs and improve competitive advantage. Technology is usually at the heart of every solution—this is where CGI adds value. We believe in finding practical answers not always found in the R&D lab. We operate under an open, collaborative approach that encompasses the entire business process. CGI gathers the best ideas from markets, clients, partners, academia and our members and tests them against real world scenarios to find the right solution. Best of all, we are smart about finding creative ways to make the most of our clients’ current assets—combining them with new technologies and business innovations that make the most business sense.

With a track record of 95% of projects delivered on time and within budget, we align our teams in lockstep with our clients’ business strategies to achieve significant top-to-bottom line results.

These are some representative wins from our $5.2 billion in fiscal 2012 bookings.

Visit cgi.com/newsroom for the full announcements.

CGI awarded US$143 million contract to deliver intelligence support to the U.S. Army Training and Doctrine Command

The UK Department of Health chooses Logica, now part of CGI, for delivery of payroll for its Arms Length Bodies

CGI’s U.S. public sector tax and revenue clients collect more than $2 billion in additional revenues

CGI launches fraud detection service for the insurance industry, solution powered by SAS

CGI’s ERP program honored as “Best Fit Integrator” for 5th year by the Center for Digital Government

ISS and CGI strike Nordic partnership deal

CGI secures IT partnership agreement with Countrywide

RSA renews IT services agreement with CGI for 6 years

Rio Tinto and CGI renew and expand their IT outsourcing contract

CGI selected to build U.S.-wide competitive health insurance exchange

The City of Västerås signs £27 million deal with Logica, now part of CGI, to manage its IT operations

CGI to transition the Nuclear Regulatory Commission’s financial systems to the Momentum Community Cloud

CGI partners with the Centers for Medicare & Medicaid Services to deliver Medicare.gov multi-platform experience for 47 million users

CGI signs new, expanded three-year partnership agreement with Société Générale Corporate & Investment Banking

CGI signs multi-million dollar managed collections agreement with World Omni Financial Corp.

National Bank of Canada and CGI sign new five-year agreement worth $350M

John Hancock selects CGI for data center consolidation and the provision of highly secure on-demand Cloud services

cgi.com/2012-ar/clients

A strong local presence in 400 communities around the world

AMERICAS

ARGENTINA

BRAZIL

CANADA

CHILE

COLOMBIA

PERU

UNITED STATES

VENEZUELA

EUROPE, MIDDLE EAST AND AFRICA

BELGIUM

CZECH REPUBLIC

DENMARK

EGYPT

ESTONIA

FINLAND

FRANCE

GERMANY

HUNGARY

IRELAND

ITALY

LUXEMBOURG

MOROCCO

NETHERLANDS

NORWAY

POLAND

PORTUGAL

SAUDI ARABIA

SLOVAKIA

SPAIN

SWEDEN

SWITZERLAND

UNITED ARAB EMIRATES

UNITED KINGDOM

ASIA PACIFIC

AUSTRALIA

INDIA

MALAYSIA

PHILIPPINES

SINGAPORE

| * | Indicates local CGI office(s) |

Board of directors

Claude Boivin (a)

Director since 1993

Director of Companies

Bernard Bourigeaud (b)

Director since 2008

Director of Companies

Jean Brassard (a)

Director since 1978

Director of Companies

Robert Chevrier (b)

Director since 2003

Chair of the Human Resources Committee, CGI

President, Roche Management Co. Inc.

Dominic D’Alessandro (b)

Director since 2010

Director of Companies

Thomas P. d’Aquino (c)

Director since 2006

Lead Director, CGI

Chief Executive, Intercounsel Ltd

Paule Doré (c)

Director since 1995

Director of Companies

Richard B. Evans (a)

Director since 2009

Director of Companies

Chairman of the Board, Resolute Forest Products

Serge Godin

Director since 1976

Founder and Executive Chairman of the Board, CGI

André Imbeau

Director since 1976

Founder, Executive Vice-Chairman of the Board and Corporate Secretary, CGI

Gilles Labbé (a)

Director since 2010

Chair of the Audit and Risk Management Committee, CGI

President and Chief Executive Officer, Héroux-Devtek Inc.

Eileen A. Mercier (c)

Director since 1996

Chair of the Corporate Governance Committee, CGI

Director of Companies

Donna Morea

Director since 2012

Director of Companies

Michael E. Roach

Director since 2006

President and

Chief Executive Officer, CGI

| (a) | Member of the Audit and Risk Management Committee |

| (b) | Member of the Human Resources Committee |

| (c) | Member of the Corporate Governance Committee |

Leadership team: Corporate Services

Serge Godin

Founder and Executive Chairman of the Board

André Imbeau

Founder, Executive Vice-Chairman of the Board and Corporate Secretary

Michael E. Roach

President and Chief Executive Officer

R. David Anderson

Executive VP and Chief Financial Officer

Jame Cofran

Senior VP and Chief Marketing Officer

Benoit Dubé

Executive VP and Chief Legal Officer

Julie Godin

Executive VP, Human Resources and Strategic Planning

Lorne Gorber

Senior VP, Global Communications and Investor Relations

Eva Maglis

Executive VP,

Global Chief Information Officer

Luc Pinard

Executive VP, Corporate

Performance and Knowledge Management

Daniel Rocheleau

Executive VP and Chief Business Engineering Officer

Claude Séguin

Senior VP, Corporate Development and Strategic Investments

Leadership team: Global Operations

United States

George Schindler

President

Pete Ihrig

US Enterprise Markets

Mark Boyajian

US Mid-Atlantic

Dave Delgado

US West

Robert Farrell

Global Infrastructure Services

Dave Henderson

US Central-South

Christopher James

IP Solutions

Gregg Mossburg

US Northeast

Donna Ryan

President, CGI Federal

Amy Bleken

Defense Agency Programs

Cheryl Campbell

Health & Compliance Programs

Barbara Fast

Army & Defense Intelligence Programs

Tim Hurlebaus

National Security Programs

Tom Kirk

Government Secure Solutions

Toni Townes-Whitley

Civilian Agency Programs

Asia Pacific & Middle East

Colin Holgate

President

S. Chandramouli

India

Michael Shepherd

Australia

Hervé Vincent

Southeast Asia

Canada

Douglas McCuaig

President

Claude Marcoux

Chief Operating Officer

Réjean Bernard

Global Infrastructure Services

Shawn Derby

Western Canada

Michael Godin

National Capital Region

Jamie Holland

IP Solutions

Roy Hudson

Communication Services Business

Bernard Labelle

Québec City

Marie MacDonald

Greater Toronto

Jay MacIsaac

Atlantic Canada

Guy Vigeant

Greater Montreal

Central & Eastern Europe

Serge Dubrana

President

Ron de Mos

Netherlands

Dariusz Gorzen

Poland

Torsten Strass

Germany & Switzerland

Stefan Szabó

Czech Republic & Slovakia

Hans Vets

Belgium

France

Jean-Marc Lazzari

President

Jean-Michel Baticle

Regions

Philippe Bouron

Paris

Mohamed Lakhlifi

Morocco

José Lopez

Business Consulting

Patrick Navarro

I2B

United Kingdom

Timothy Gregory

President

David Fitzpatrick

Global Infrastructure Services

Melba Foggo

Business Consulting

Andrew Marsh

Business Processing Services

Paula Sussex

Public Sector

Steve Thorn

Application Services

Mike Whitchurch

Commercial Sector

Nordics, Southern Europe & South America

João Baptista

President

Gisle Eckhoff

Norway

José Carlos Gonçalves

Southern Europe & Latin America

Björn Ivroth

Sweden

Edson Leite

Brazil

Heikki Nikku

Finland & Estonia

Martin Petersen

Denmark

Shareholder information

Shareholder information listing

IPO: 1986

Toronto Stock Exchange, April 1992: GIB.A

New York Stock Exchange, October 1998: GIB

Number of shares outstanding as of September 30, 2012:

273,771,106 Class A subordinate shares

33,608,159 Class B shares

High/low of share price from October 1, 2011 to September 30, 2012:

TSX (CDN$) NYSE (U.S.$)

High: 27.00 27.71

Low: 17.88 17.01

The certifications by CGI’s Chief Executive Officer and Chief Financial Officer concerning the quality of the Company’s public disclosure pursuant to Canadian regulatory requirements are filed in Canada on SEDAR (sedar.com). Similar certifications pursuant to Rule 13a-14 of the U.S. Securities Exchange Act of 1934 and Section 302 of the Sarbanes-Oxley Act of 2002 are exhibits to our Form 40-F filed on EDGAR (sec.gov). The Company has also filed with the New York Stock Exchange the certification required by Section 303A.12 of the exchange’s Listed Company Manual.

CGI’s corporate governance practices do not differ in any significant way from those required of domestic companies under New York Stock Exchange listing standards and they are set out in the CGI Management Proxy Circular, which is filed with Canadian and U.S. securities authorities and is therefore available on SEDAR and EDGAR, respectively, as well as on CGI’s website (cgi.com).

Auditors

Ernst & Young LLP

Transfer agent

Computershare Trust Company of Canada

100 University Avenue, 9th Floor

Toronto, Ontario M5J 2Y1

Telephone: 1 800 564-6253

www.investorcentre.com/service

Investor relations

For further information about the Company, additional copies of this report or other financial information, please contact:

CGI Group Inc.

Investor relations

Email: ir@cgi.com

Twitter: CGI_IR

Web: cgi.com/investors

1350 René-Lévesque Blvd West

Montréal, Québec H3G 1T4

Canada

Tel.: (514) 841-3200

Annual general meeting of shareholders

Wednesday, January 30, 2013 at 11:00 a.m.

Omni Mont-Royal Hotel

Saisons A & B

1050 Sherbrooke West

Montréal, Québec H3A 2R6

A live webcast of the Annual General Meeting will be available via cgi.com/investors. Complete instructions for viewing the webcast will be available on CGI’s website. To vote by phone or by using the Internet, please refer to the instructions provided in the CGI Management Proxy Circular.

The online version of CGI’s annual report is available at cgi.com/2012-ar

Le rapport annuel 2012 de CGI est aussi publié en français et disponible sur cgi.com/2012-ra.

Our aspiration: To be the best

At CGI, we are connected through a common culture, a disciplined management approach and a network of vast capabilities and expertise. These connections deliver results.

For our clients

A track record of 95% on-time, on-budget delivery fuels high client satisfaction, which has measured consistently greater than 9 out of 10 for the past 10 years.

For our members

With a majority of our members as owners, we foster a performance-based culture that allows members to benefit from their company’s success.

For our shareholders

CGI has a track record of industry-leading margins that demonstrates our ability to run a sound and stable business for the long term, and an average annual return of more than 30% over the last 15 years.

As a global leader, CGI will continue to strive to be the best to satisfy the needs of our clients, offer rewarding careers for our members and provide a superior return over time for our shareholders.

cgi.com

CGI Group Inc.

2012 Annual Report

CGI’s 2012 Annual Report is comprised

of two separate volumes:

Volume 1:Experience the commitment

&

Volume 2:Numbers

Volume 2 of the Annual Report

follows this page.

(this page does not form part of the Annual Report)

2012 annual report

Numbers

MANAGEMENT’S DISCUSSIONAND ANALYSIS

FISCAL YEAR 2012

November 28, 2012

Basis of Presentation

This Management’s Discussion and Analysis of the Financial Position and Results of Operations (“MD&A”) is the responsibility of management and has been reviewed and approved by the Board of Directors. This MD&A has been prepared in accordance with the requirements of the Canadian Securities Administrators. The Board of Directors is ultimately responsible for reviewing and approving the MD&A. The Board of Directors carries out its responsibility mainly through its Audit and Risk Management Committee, which is appointed by the Board of Directors and is comprised entirely of independent and financially literate directors.

Throughout this document, CGI Group Inc. is referred to as “CGI”, “we”, “our” or “Company”. This MD&A provides information management believes is relevant to an assessment and understanding of the consolidated results of operations and financial condition of the Company. This document should be read in conjunction with the audited consolidated financial statements and the notes thereto for the years ended September 30, 2012 and 2011. CGI’s accounting policies are in accordance with International Financials Reporting Standards (“IFRS”) of the International Accounting Standards Board (“IASB”). All dollar amounts are in Canadian dollars unless otherwise indicated.

First Year Reporting under IFRS

The year’s audited consolidated financial statements and this MD&A represent our first fiscal year reporting under IFRS. Under the rules and regulations of the U.S. Securities and Exchange Commission, CGI is classified as a foreign private issuer and is therefore permitted to use IFRS. CGI transitioned from Canadian Generally Accepted Accounting Principles (“Canadian GAAP”) to IFRS on October 1, 2010 and adjusted the financial results of fiscal 2011 to reflect the adoption of IFRS. Note 33 to the audited consolidated financial statements for the year ended September 30, 2012 contains a detailed description of our conversion to IFRS, including a reconciliation of key items from Canadian GAAP to IFRS. Periods prior to October 1, 2010 presented in this MD&A have not been adjusted and are in accordance with Canadian GAAP.

Although the adoption of IFRS resulted in adjustments to our consolidated financial statements, it did not materially impact the underlying cash flows or profitability trends of our operating performance, debt covenants or compensation arrangements.

Materiality of Disclosures

This MD&A includes information we believe is material to investors. We consider something to be material if it results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares, or if it is likely that a reasonable investor would consider the information to be important in making an investment decision.

Forward-Looking Statements

All statements in this MD&A that do not directly and exclusively relate to historical facts constitute “forward-looking statements” within the meaning of that term in Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended, and are “forward-looking information” within the meaning of Canadian securities laws. These statements and this information represent CGI’s intentions, plans, expectations and beliefs, and are subject to risks, uncertainties and other factors, of which many are beyond the control of the Company. These factors could cause actual results to differ materially from such forward-looking statements or forward-looking information. These factors include but are not restricted to: the timing and size of new contracts; acquisitions and other corporate developments; the ability to attract and retain qualified members; market competition in the rapidly evolving information technology industry; general economic and business conditions; foreign exchange and other risks identified in the MD&A, in CGI’s Annual Report on Form 40-F filed with the U.S. Securities and Exchange Commission (filed on EDGAR atwww.sec.gov), the Company’s Annual Information Form filed with the Canadian securities authorities (filed on SEDAR atwww.sedar.com), as well as

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 2 of 48 |

assumptions regarding the foregoing. The words “believe,” “estimate,” “expect,” “intend,” “anticipate,” “foresee,” “plan,” and similar expressions and variations thereof, identify certain of such forward-looking statements or forward-looking information, which speak only as of the date on which they are made. In particular, statements relating to future performance are forward-looking statements and forward-looking information. CGI disclaims any intention or obligation to publicly update or revise any forward-looking statements or forward-looking information, whether as a result of new information, future events or otherwise, except as required by applicable law. Readers are cautioned not to place undue reliance on these forward-looking statements or on this forward-looking information. You will find more information about the risks that could cause our actual results to differ significantly from our current expectations in Section 10 – Risk Environment.

Non-GAAP Measures

The reader should note that the Company reports its financial results in accordance with IFRS. However, in this MD&A, certain non-GAAP financial measures are used:

| 1. | Earnings before acquisition-related and integration costs, finance costs, finance income, other income, share of profit on joint venture, and income tax expense (“adjusted EBIT”); |

| 2. | Constant currency growth; |

| 3. | Days Sales Outstanding (“DSO”); |

| 4. | Return on Invested Capital (“ROIC”); |

| 5. | Return on Equity (“ROE”); and |

| 6. | Net Debt to Capitalization ratio. |

Management believes that these non-GAAP measures provide useful information to investors regarding the Company’s financial condition and results of operations as they provide additional measures of its performance. These non-GAAP measures do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other issuers. These measures should be considered as supplemental in nature and not as a substitute for the related financial information prepared in accordance with IFRS.

A reconciliation of adjusted EBIT to its closest IFRS measure can be found on page 20. Definitions of constant currency growth, DSO, ROIC, ROE, and net debt to capitalization are provided on pages 9 and 10. A discussion of DSO, ROIC, ROE and net debt to capitalization can be found on page 27.

Change in Reporting Segments

In 2012, we modified our basis of reporting such that the growth and profitability of the India activities were reallocated from our previously combined U.S. and India segment to each reporting segment, namely: Global Infrastructure Services (“GIS”), Canada, U.S., and Europe & Asia Pacific. This view reflects each segment’s utilization of our delivery centres in India; the segmented results for the year and three months ended September 30, 2011 were therefore retrospectively revised. In Q4 2012, our acquisition of Logica plc (“Logica”) became effective six weeks before our fiscal year-end. As at September 30, 2012, the operations of Logica were managed and reviewed as one component and is therefore being presented as its own operating segment. As a result of changes in the management reporting structure effective October 1, 2012, the Company will change its operating segments beginning in the first quarter of 2013 as follows: Canada; United States of America; Nordics, Southern Europe and South America; Central and Eastern Europe (including Netherlands, Germany and Belgium); United Kingdom; Asia Pacific (including Australia, India, Philippines and the Middle East); and France (including Luxembourg and Morocco). For more details on how our operations are managed, please refer to Note 27 of the audited consolidated financial statements.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 3 of 48 |

MD&A Objectives and Contents

| • | Provide a narrative explanation of the audited consolidated financial statements through the eyes of management; |

| • | Provide the context within which the audited consolidated financial statements should be analyzed, by giving enhanced disclosure about the dynamics and trends of the Company’s business; and |

| • | Provide information to assist the reader in ascertaining the likelihood that past performance is indicative of future performance. |

In order to achieve these objectives, this MD&A is presented in the following main sections:

Section | Contents | Pages | ||||||||

| 1. | Corporate Overview | This includes a description of our business and how we generate revenue as well as the markets in which we operate.

| ||||||||

| 1.1. | About CGI | 6 | ||||||||

| 1.2. | Vision and Strategy | 7 | ||||||||

| 1.3. | Competitive Environment | 7 | ||||||||

| 2. | Highlights and Key Performance Measures | A summary of key achievements during the quarter, the past three years’ key performance measures, and CGI’s share performance.

| ||||||||

| 2.1. | Fiscal 2012 Highlights | 8 | ||||||||

| 2.2. | Key Performance Measures Defined | 9 | ||||||||

| 2.3. | Selected Yearly Information & Key Performance Measures | 10 | ||||||||

| 2.4. | Stock Performance | 11 | ||||||||

| 3. | Financial Review | A discussion of year-over-year changes to operating results for the years ended September 30, 2012 and 2011, describing the factors affecting revenue and earnings on a consolidated and reportable segment basis, and also by describing the factors affecting changes in the major expense categories. Also discussed are bookings broken down by geography, vertical market, contract and service type. | ||||||||

| 3.1. | Bookings and Book-to-Bill Ratio | 12 | ||||||||

| 3.2. | Foreign Exchange | 13 | ||||||||

| 3.3. | Revenue Distribution | 14 | ||||||||

| 3.4. | Revenue Variation and Revenue by Segment | 15 | ||||||||

| 3.5. | Operating Expenses | 17 | ||||||||

| 3.6. | Adjusted EBIT by Segment | 18 | ||||||||

| 3.7. | Earnings before Income Taxes | 20 | ||||||||

| 3.8. | Net Earnings and Earnings Per Share (“EPS”) | 21 | ||||||||

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 4 of 48 |

Section | Contents | Pages | ||||||||

| 4. | Liquidity | This includes a discussion of changes in cash flows from operating, investing and financing activities. This section also describes the Company’s available capital resources, financial instruments, and off-balance sheet financing and guarantees. Measures of liquidity (days sales outstanding) and capital structure (return on equity, net debt to capitalization, and return on invested capital) are analyzed on a year-over- year basis. | ||||||||

| 4.1. | Consolidated Statements of Cash Flows | 23 | ||||||||

| 4.2. | Capital Resources | 24 | ||||||||

| 4.3. | Contractual Obligations | 25 | ||||||||

| 4.4. | Financial Instruments and Hedging Transactions | 25 | ||||||||

| 4.5. | Selected Measures of Liquidity and Capital Resources | 27 | ||||||||

| 4.6. | Off-Balance Sheet Financing and Guarantees | 27 | ||||||||

| 4.7. | Capability to Deliver Results | 28 | ||||||||

| 5. | Fourth Quarter Results | A discussion of year-over-year changes to operating results for the three months ended September 30, 2012 and 2011, describing the factors affecting revenue and earnings on a consolidated and reportable segment basis.

| ||||||||

| 5.1 | Revenue Variation and Revenue by Segment | 29 | ||||||||

| 5.2 | Adjusted EBIT by Segment | 32 | ||||||||

| 5.3 | Net Earnings and Earnings per Share | 33 | ||||||||

| 6. | Eight Quarter Summary | A summary of the past eight quarters’ key performance measures and a discussion of the factors that could impact our quarterly results. | 35 | |||||||

| 7. | Changes in Accounting Policies | A summary of current accounting standards in effect and future accounting standards to be adopted.

| ||||||||

| 7.1 | Adoption of IFRS | 36 | ||||||||

| 7.2 | Future Accounting Standard Changes | 36 | ||||||||

| 8. | Critical Accounting Estimates | A discussion of the estimates and judgements made in the preparation of the consolidated financial statements. | 37 | |||||||

| 9. | Integrity of Disclosure | A discussion of the existence of appropriate information systems, procedures and controls to ensure that information used internally and disclosed externally is complete and reliable. | 40 | |||||||

| 10. | Risk Environment | A discussion of the risks affecting our business activities and what may be the impact if these risks are realized.

| ||||||||

| 10.1 | Risks and Uncertainties | 41 | ||||||||

| 10.2 | Legal Proceedings | 48 | ||||||||

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 5 of 48 |

| 1. | Corporate Overview |

| 1.1. | ABOUT CGI |

Founded in 1976 and headquartered in Montreal, Canada, CGI is one of the largest independent providers of end-to-end information technology services (“IT services”) and business process services (“BPS”) to clients worldwide. CGI has approximately 72,000 members across the globe. The Company’s proximity model provides for work to be delivered onsite at clients’ premises, on-shore, near-shore or through one of its global offshore delivery centres. We also have a number of leading business solutions that support long-term client relationships. Our services are broken down as:

| • | Consulting – CGI provides a full range of IT and management consulting services, including business transformation, IT strategic planning, business process engineering and systems architecture. |

| • | Systems integration – CGI integrates and customizes leading technologies and software applications to create IT systems that respond to clients’ strategic needs. |

| • | Management of IT and business functions (“outsourcing”) – Clients delegate entire or partial responsibility for their IT or business functions to CGI to achieve significant savings and access the best suited technology, while retaining control over strategic IT and business functions. As part of such agreements, we implement our quality processes and practices to improve the efficiency of the clients’ operations. We also integrate clients’ operations into our technology network. Finally, we may take on specialized professionals from our clients, enabling our clients to focus on key operations. Services provided as part of an outsourcing contract may include development and integration of new projects and applications; applications maintenance and support; technology infrastructure management (enterprise and end-user computing and network services); transaction and business processing such as payroll, insurance processing, and document management services. Outsourcing contracts typically have terms from five to ten years. |

CGI offers its end-to-end services to a focused set of industry vertical markets where we have developed extensive and deep subject matter expertise. This allows us to fully understand our clients’ business realities and to have the knowledge and solutions needed to advance their business goals. Our targeted vertical markets include government, financial services, manufacturing, retail & distribution (“MRD”), telecommunications & utilities, and health.

CGI has a wide range of proprietary business solutions which help shape opportunities and drive value for our clients and shareholders. Examples of these include Enterprise Resource Planning solutions, energy management, credit and debt collections, tax management, claims auditing and fraud detection.

We take great pride in delivering high quality services to our clients. To do so consistently, we have implemented and continue to maintain the International Organization for Standardization (“ISO”) quality program. By designing and implementing rigorous service delivery and quality standards, followed by monitoring and measurement, we are better able to satisfy our clients’ needs. As a measure of the scope of our ISO 9001 program, all of the legacy CGI’s business units continue to be certified and we will initiate the work on improving Logica’s processes and applying for the same certification.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 6 of 48 |

| 1.2. | VISION AND STRATEGY |

At CGI, we derive our business vision from our dream which is to create an environment in which members enjoy working together and, as owners, contribute to building a company we can be proud of. That dream led to CGI’s vision of being a world-class IT and BPS leader, helping its clients win and grow. Our build and buy strategy is refined through a four-pillar growth strategy that combines organic growth and acquisitions.

The first two pillars of our strategy focus on organic growth. The first pillar focuses on smaller contract wins, renewals and extensions. The second involves the pursuit of new large, long-term outsourcing contracts, leveraging our end-to-end services, global delivery model and critical mass.

The third pillar of our growth strategy focuses on the acquisition of smaller firms or niche players. We identify niche acquisitions through a strategic mapping program that systematically searches for targets that will strengthen our vertical market knowledge or increase the richness of our service offerings.

The fourth pillar involves the pursuit of transformational acquisitions focused on expanding our geographic presence and critical mass. This approach further enables us to strengthen our qualifications to compete for large outsourcing contracts. CGI continues to be a consolidator in the IT services industry.

Throughout its history, CGI has been highly disciplined in following this four-pillar growth strategy, with an emphasis on earnings accretion and maximizing shareholder value.

| 1.3. | COMPETITIVE ENVIRONMENT |

As a global provider of end-to-end information technology and business process services, CGI operates in a highly competitive and rapidly evolving global industry. Our competition comprises a variety of global players, from niche companies providing specialized services to other end-to-end service providers, mainly in the U.S., Europe and India, all of whom are competing to deliver some or all of the services we provide.

Recent mergers and acquisition activity has resulted in CGI being positioned as one of the few remaining IT services firms that operates independently of any hardware or software vendor. This independence allows CGI to deliver the best-suited technology available globally to our clients.

CGI offers its end-to-end services to a select set of targeted vertical markets in which we have deep business and technical expertise covering 90% of global IT spend. To compete effectively, CGI focuses on high-end systems integration, consulting and outsourcing where vertical market industry knowledge and expertise are required.

Our client proximity metro markets business model combined with our global delivery model results in highly responsive and cost competitive delivery. CGI’s global delivery model provides clients with a unique blend of onshore, nearshore and offshore delivery options that caters to their strategic and cost requirements. CGI also has a number of leading business solutions that support long-term client relationships. Moreover, all of CGI’s business operations are executed based on the same management foundation, ensuring consistency and cohesion across the Company.

There are many factors involved in winning and retaining IT and BPS contracts, including the following: total cost of services; ability to deliver; track record; vertical market expertise; investment in business solutions; local presence; global delivery capability; and the strength of client relationships. CGI compares favourably with its competition with respect to all of these factors.

In summary, CGI’s competitive value proposition encompasses the following: end-to-end IT and BPS capability; expertise and proprietary business solutions in five vertical markets covering the majority of global IT spending; a unique global delivery model, which includes industry leading delivery capabilities; a disciplined management foundation; and our focus on client satisfaction which is supported by our client proximity business model. Based on this value proposition and CGI’s growing critical mass in our target markets which collectively cover approximately 84% of global IT spending – we are in a position to compete effectively on an international scale and win large contracts.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 7 of 48 |

| 2. | Highlights and Key Performance Measures |

| 2.1. | FISCAL 2012 HIGHLIGHTS |

| • | Revenue of $4.8 billion, increase of 12.1% year-over-year on a constant currency basis; |

| • | Bookings of $5.2 billion resulting in a book-to-bill ratio of 109%; |

| • | Backlog of $17.6 billion; |

| • | Strong underlying profitability delivered across legacy CGI operations; |

| • | Accelerating profitable growth and bookings in U.S. operations; and |

| • | Cash from operations of $613.3 million, or $2.24 per share. |

| 2.1.1. | Acquisition of Logica plc |

On August 20, 2012, CGI completed its acquisition of Logica for $1.63 (105 pence) per ordinary share equivalent to a total purchase price of $2.7 billion plus the assumption of Logica’s net debt of $0.9 billion. The cash acquisition of all the outstanding ordinary shares of Logica was effected by means of a Court-sanctioned scheme of arrangement in the United Kingdom. Our results for the year incorporate the operations of Logica subsequent to August 20, 2012.

Logica is a business and technology services company, employing 41,000 people. It provides business consulting, systems integration and outsourcing services to clients around the world, including many of Europe’s largest businesses.

The acquisition was funded through a combination of:

| • | The issuance of 46.7 million Class A shares in CGI for a consideration of $1.0 billion from the Caisse de dépôt et placement du Québec (“CDPQ”); |

| • | Additional debt funding through a term loan of $1.9 billion from a syndicate of international financial institutions; and |

| • | The remaining financing requirements of $0.8 billion were drawn from CGI’s existing credit facility and cash. |

Based on the impact of the issuance of the new debt and equity and the realization of some of the planned synergies, the transaction is expected to be accretive in the range of 25% to 30% in the first 12 months to CGI’s earnings per share excluding acquisition-related and integration costs. As the Company continues to realize an approximate amount of $300 million of annual business synergies over the next three years at an approximate cost of $400 million, we expect the accretion level of EPS to increase.

The combined company has approximately 72,000 members in more than 40 countries and pro-forma revenue of $10.4 billion, offering clients across the world the best mix of business and technology expertise as well as an unmatched combination of local and global delivery options. In addition to operational breadth and depth, the combined business has critical mass and blue chip client relationships. CGI incurred $0.3 billion in acquisition-related and integration costs over the last half of fiscal 2012.

| 2.1.2. | Credit Facility and Debt Private Placement |

On December 7, 2011, the Company renewed its unsecured revolving credit facility of $1.5 billion for an additional five years, through December 2016. The facility, which can be extended annually, includes an accordion feature providing for an additional $750.0 million, bringing the facility’s potential capacity to $2.25 billion. In addition, during the first quarter of fiscal 2012, the Company received the proceeds of the US$475.0 million debt private placement financing with U.S. institutional investors.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 8 of 48 |

| 2.2. | KEY PERFORMANCE MEASURES DEFINED |

We use a combination of financial measures, ratios, and non-GAAP measures to assess our Company’s performance. The table below summarizes our most relevant key performance measures. The calculated results and the discussion of each indicator follow in the subsequent sections.

| Profitability | • | Adjusted EBIT – is a measure of earnings before items not directly related to the cost of operations, such as financing costs, acquisition-related and integration costs and income taxes (see definition on page 3). Management believes this best reflects the profitability of our operations. | ||

| • | Diluted earnings per share – is a measure of earnings generated for shareholders on a per share basis, assuming all dilutive elements are exercised. | |||

| Liquidity | • | Cash provided by operating activities – is a measure of cash generated from managing our day-to-day business operations. We believe strong operating cash flow is indicative of financial flexibility, allowing us to execute our corporate strategy. | ||

| • | Days sales outstanding – is the average number of days to convert our trade receivables and work in progress into cash. Management tracks this metric closely to ensure timely collection, healthy liquidity, and is committed to a DSO target of 45 days. | |||

| Growth | • | Constant currency growth – is a measure of revenue growth before foreign currency impacts. This growth is calculated by translating current period results in local currency using the conversion rates in the equivalent period from the prior year. We believe that it is helpful to adjust revenue to exclude the impact of currency fluctuations to facilitate period-to-period comparisons of business performance. | ||

| • | Backlog – represents management’s best estimate of revenue to be realized in the future based on the terms of respective client agreements in effect at a point in time. | |||

| • | Book-to-Bill ratio – is a measure of the proportion of the value of our contract wins to our revenue in the period. This metric allows management to monitor the Company’s business development efforts to ensure we grow our backlog and our business over time. Management remains committed to maintaining a target ratio greater than 100% over a 12-month period. Management believes that the longer period is a more effective measure as the size and timing of bookings could cause this measurement to fluctuate significantly if taken for only a three-month period. | |||

| Capital Structure | • | Net Debt to Capitalization ratio – is a measure of our level of financial leverage net of our cash and cash equivalents, short-term investments and marketable long-term investments. Management uses this metric to monitor the proportion of debt versus capital used to finance our operations and it provides insight into our financial strength. | ||

| • | Return on Equity – is a measure of the rate of return on the ownership interest of our shareholders. Management looks at ROE to measure its efficiency at generating profits for the Company’s shareholders and how well the Company uses the invested funds to generate earnings growth. | |||

| • | Return on Invested Capital – is a measure of the Company’s efficiency at allocating the capital under its control to profitable investments. Management examines this ratio to assess how well it is using its money to generate returns. | |||

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 9 of 48 |

| 2.3. | SELECTED YEARLY INFORMATION & KEY PERFORMANCE MEASURES |

| As at and for the years ended September 30, | 2012 | 2011 | Change | 2010 | ||||||||||||

(in thousands of dollars unless otherwise noted) | IFRS | IFRS | 2012 / 2011 | CDN GAAP | ||||||||||||

Growth | ||||||||||||||||

Backlog(in millions of dollars)1 | 17,647 | 13,398 | 4,249 | 13,320 | ||||||||||||

Bookings(in millions of dollars) | 5,180 | 4,875 | 305 | 4,643 | ||||||||||||

Book-to-bill ratio | 109 | % | 115 | % | (6 | %) | 124 | % | ||||||||

Revenue | 4,772,454 | 4,223,942 | 548,512 | 3,732,117 | ||||||||||||

Year-over-year growth2 | 13.0 | % | 15.8 | % | (2.8 | %) | (2.4 | %) | ||||||||

Constant currency growth2 | 12.1 | % | 18.9 | % | (6.8 | %) | 3.4 | % | ||||||||

Profitability | ||||||||||||||||

Adjusted EBIT3 | 546,729 | 536,347 | 10,382 | 511,902 | ||||||||||||

Adjusted EBIT margin | 11.5 | % | 12.7 | % | (1.2 | %) | 13.7 | % | ||||||||

Net earnings | 131,529 | 438,139 | (306,610 | ) | 362,766 | |||||||||||

Net earnings margin | 2.8 | % | 10.4 | % | (7.6 | %) | 9.7 | % | ||||||||

Basic EPS(in dollars) | 0.50 | 1.65 | (1.15 | ) | 1.27 | |||||||||||

Diluted EPS(in dollars) | 0.48 | 1.59 | (1.11 | ) | 1.24 | |||||||||||

Liquidity | ||||||||||||||||

Cash provided by operating activities | 613,262 | 570,002 | 43,260 | 552,367 | ||||||||||||

As a percentage of revenue | 12.9 | % | 13.5 | % | (0.6 | %) | 14.8 | % | ||||||||

Days sales outstanding4 | 70 | 53 | 17 | 47 | ||||||||||||

Capital structure | ||||||||||||||||

Net debt to capitalization ratio5 | 46.6 | % | 27.4 | % | 19.2 | % | 30.6 | % | ||||||||

Net debt | 3,105,313 | 918,968 | 2,186,345 | 1,010,816 | ||||||||||||

Return on equity6 | 5.0 | % | 19.6 | % | (14.6 | %) | 16.4 | % | ||||||||

Return on invested capital7 | 11.4 | % | 13.7 | % | (2.3 | %) | 16.3 | % | ||||||||

Balance sheet | ||||||||||||||||

Cash and cash equivalents, bank overdraft and short-term investments | 127,562 | 70,839 | 56,723 | 141,020 | ||||||||||||

Total assets | 10,453,442 | 4,657,354 | 5,796,088 | 4,607,191 | ||||||||||||

Long-term financial liabilities8 | 4,124,342 | 238,151 | 3,886,191 | 1,159,198 | ||||||||||||

| 1 | Backlog includes new contract wins, extensions and renewals (“bookings”), partially offset by the backlog consumed during the quarter as a result of client work performed and adjustments related to the volume, cancellation and/or the impact of foreign currencies to our existing contracts. Backlog incorporates estimates from management that are subject to change. Fiscal 2012 backlog includes the backlog from Logica. The bookings and book-to-bill ratio include the results of Logica for the period from August 20, 2012. |

| 2 | Constant currency growth is adjusted to remove the impact of foreign currency exchange rate fluctuations. Please refer to page 15 for details. The reader should note that both the year-over-year and constant currency growth rates for fiscal 2011 have not been restated as fiscal 2010 numbers under IFRS are not available. |

| 3 | Adjusted EBIT is a non-GAAP measure for which we provide the reconciliation to its closest IFRS measure on page 20. |

| 4 | Days sales outstanding are obtained by subtracting deferred revenue from trade accounts receivable and work in progress; the result is divided by the quarter’s revenue over 90 days. |

| 5 | The net debt to capitalization ratio represents the proportion of debt net of cash and cash equivalents, short-term and marketable long-term investments (“net debt”) over the sum of shareholders’ equity and debt. Net debt and capitalization are both net of the fair value of forward contracts. |

| 6 | The return on equity ratio is calculated as the proportion of earnings for the last 12 months over the last four quarters’ average equity. |

| 7 | The return on invested capital ratio represents the proportion of the after-tax adjusted EBIT for the last 12 months, over the last four quarters’ average invested capital, which is defined as the sum of equity and debt, less cash and cash equivalents, short-term and marketable long-term investments, net of the impact of the fair value of forward contracts. |

| 8 | Long-term financial liabilities include the long-term portion of debt, long-term provisions, retirement benefits obligations and other long-term liabilities. |

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 10 of 48 |

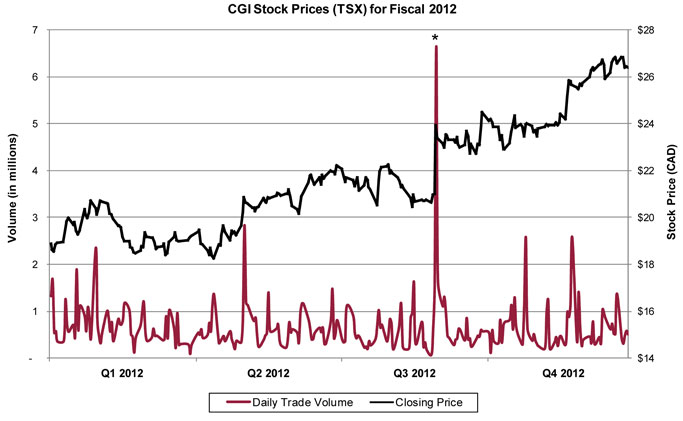

| 2.4. | STOCK PERFORMANCE |

| * | May 31, 2012 – Logica acquisition announcement date; 6.7 million shares were traded on the TSX. |

| 2.4.1. | Fiscal 2012 Trading Summary |

CGI’s shares are listed on the Toronto Stock Exchange (“TSX”) (stock quote – GIB.A) and the New York Stock Exchange (“NYSE”) (stock quote – GIB) and are included in the S&P/TSX Composite Index, the S&P/TSX Capped Information Technology and Midcap Indices, and the Dow Jones Sustainability Index.

| TSX | (CDN$) | |||

Open: | 19.50 | |||

High: | 27.00 | |||

Low: | 17.88 | |||

Close: | 26.40 | |||

CDN average daily trading volumes: | 1,013,111 | |||

Includes the average daily volumes of both the TSX and alternative trading systems.

| NYSE | (US$) | |||

Open: | 18.56 | |||

High: | 27.71 | |||

Low: | 17.01 | |||

Close: | 26.86 | |||

U.S. average daily trading volumes: | 186,414 | |||

| 2.4.2. | Share Repurchase Program |

On February 1, 2012, the Company’s Board of Directors authorized and subsequently received the approval from the TSX for the renewal of the Normal Course Issuer Bid (“NCIB”) to purchase up to 10% of the public float of the Company’s Class A subordinate shares over the next 12 months. The NCIB enables CGI to purchase, on the open market, up to 22,064,163 Class A subordinate shares for cancellation. The Class A subordinate shares may be purchased under the NCIB commencing February 9, 2012 and ending on the earlier of February 8, 2013, or the date on which the Company has either acquired the maximum number of Class A subordinate shares allowable under the NCIB, or elects to terminate the NCIB.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 11 of 48 |

During fiscal 2012, the Company repurchased 5,368,000 of its Class A subordinate shares for $102.8 million at an average price of $19.16 under the previous and current programs. As at September 30, 2012, the Company may purchase up to an additional 21.0 million shares under the current NCIB.

| 2.4.3. | Capital Stock and Options Outstanding (as at November 23, 2012) |

273,976,033 Class A subordinate shares

33,608,159 Class B shares

18,578,393 options to purchase Class A subordinate shares

| 3. | Financial Review |

| 3.1. | BOOKINGS AND BOOK-TO-BILL RATIO |

The Company achieved a book-to-bill ratio of 109% for the year, while bookings for the fiscal year were $5.2 billion. The breakdown of the $5.2 billion in bookings signed during the year is as follows:

Information regarding our bookings is a key indicator of the volume of our business over time. However, due to the timing and transition period associated with outsourcing contracts, the realization of revenue related to these bookings may fluctuate from period to period. The values initially booked may change over time due to their variable attributes, including demand-driven usage, modifications in the scope of work to be performed caused by changes in client requirements as

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 12 of 48 |

well as termination clauses at the option of the client. As such, information regarding our bookings is not comparable to, nor should it be substituted for an analysis of our revenue; it is instead a key indicator of our future revenue used by the Company’s management to measure growth.

| 3.2. | FOREIGN EXCHANGE |

The Company operates globally and is exposed to changes in foreign currency rates. We report all dollar amounts in Canadian dollars. Accordingly, we value assets, liabilities and transactions that are measured in foreign currencies using various exchange rates as prescribed by IFRS.

Closing foreign exchange rates

As at September 30, | 2012 | 2011 | Change | |||||||||

U.S. dollar | 0.9837 | 1.0389 | (5.3 | %) | ||||||||

Euro | 1.2646 | 1.3971 | (9.5 | %) | ||||||||

Indian rupee | 0.0186 | 0.0212 | (12.3 | %) | ||||||||

British pound | 1.5869 | 1.6231 | (2.2 | %) | ||||||||

Average foreign exchange rates

For the years ended September 30, | 2012 | 2011 | Change | |||||||||

U.S. dollar | 1.0074 | 0.9866 | 2.1 | % | ||||||||

Euro | 1.3077 | 1.3759 | (5.0 | %) | ||||||||

Indian rupee | 0.0192 | 0.0219 | (12.3 | %) | ||||||||

British pound | 1.5878 | 1.5845 | 0.2 | % | ||||||||

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 13 of 48 |

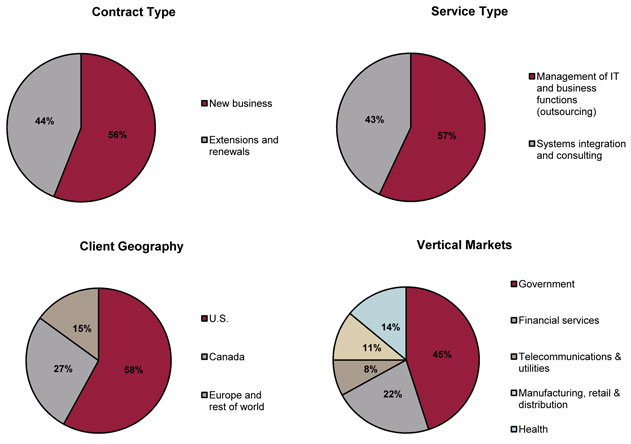

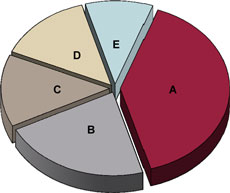

| 3.3. | REVENUE DISTRIBUTION |

The following charts provide additional information regarding our revenue mix for the year:

| Service Type

A. ��Management of IT and business functions (outsourcing) – 64%

1. IT services – 46%

2. Business process services – 18%

B. Systems integration and consulting – 36% | |

|

Client Geography

Based on client’s domicile

A. U.S. – 47%

B. Canada – 36%

C. Europe and rest of the world – 17% | |

|

Vertical Markets

A. Government – 40%

B. Financial services – 22%

C. Telecommunications and utilities – 14%

D. Manufacturing, retail and distribution – 14%

E. Health – 10% |

| 3.3.1. | Client Concentration |

IFRS guidance on Segment Disclosures defines a single customer as a group of entities that are known to the reporting enterprise to be under common control. The Company considers the federal government, the provincial or territorial government, the local government, or a foreign government each to be a single customer. Our work for the U.S. federal government including its various agencies represented 28.0% of our revenue for fiscal 2012 as compared to 29.2% in fiscal 2011.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 14 of 48 |

| 3.4. | REVENUE VARIATION AND REVENUE BY SEGMENT |

Our operations are managed in four operating segments based on our delivery model incorporating domestic activities as well as services from utilizing our unique global delivery model. The GIS segment incorporates all services we provide to our clients globally for the management of their technology infrastructure. The other segments are based on our geographic delivery model: United States (“U.S.”), Europe & Asia Pacific (“Europe”), and Canada which include their respective utilization of our delivery centres in India. For the year ended September 30, 2012, we added another segment – Logica, which incorporates the results of the acquired company as of August 20, 2012.

The following table provides a summary of our revenue variation, in total and by segment, separately showing the impacts of foreign currency exchange rate variations between the fiscal 2012 and 2011 periods. The fiscal 2011 revenue by segment was recorded reflecting the actual foreign exchange rates for that period. The foreign exchange impact is the difference between the current period’s actual results and the current period’s results converted with the prior year’s foreign exchange rates.

For the years ended September 30, (in thousands of dollars except for percentage) | 2012 | 2011 | Change | |||||||||

Total CGI revenue | 4,772,454 | 4,223,942 | 13.0 | % | ||||||||

Variation prior to foreign currency impact | 12.1 | % | ||||||||||

Foreign currency impact | 0.9 | % | ||||||||||

Variation over previous period | 13.0 | % | ||||||||||

U.S. | ||||||||||||

Revenue prior to foreign currency impact | 2,044,878 | 1,896,002 | 7.9 | % | ||||||||

Foreign currency impact | 46,234 | |||||||||||

U.S. revenue | 2,091,112 | 1,896,002 | 10.3 | % | ||||||||

Canada | ||||||||||||

Revenue prior to foreign currency impact | 1,212,791 | 1,287,056 | (5.8 | %) | ||||||||

Foreign currency impact | (176 | ) | ||||||||||

Canada revenue | 1,212,615 | 1,287,056 | (5.8 | %) | ||||||||

Global Infrastructure Services | ||||||||||||

Revenue prior to foreign currency impact | 683,018 | 816,663 | (16.4 | %) | ||||||||

Foreign currency impact | 1,852 | |||||||||||

Global Infrastructure Services revenue | 684,870 | 816,663 | (16.1 | %) | ||||||||

Europe | ||||||||||||

Revenue prior to foreign currency impact | 224,080 | 224,221 | (0.1 | %) | ||||||||

Foreign currency impact | (8,098 | ) | ||||||||||

Europe revenue | 215,982 | 224,221 | (3.7 | %) | ||||||||

Logica | ||||||||||||

Revenue prior to foreign currency impact | 567,875 | — | N/A | |||||||||

Foreign currency impact | N/A | |||||||||||

Logica revenue | 567,875 | — | N/A | |||||||||

We ended fiscal 2012 with revenue of $4,772.5 million, an increase of $548.5 million or 13.0% over fiscal 2011. On a constant currency basis, revenue increased by 12.1%, while foreign currency rate fluctuations favourably impacted our revenue by $39.8 million or 0.9%. On a constant currency basis, our MRD vertical grew the most at 32.3%, followed by our healthcare vertical at 24.2% and telecommunications & utilities at 21.5%.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 15 of 48 |

Our U.S. segment posted the strongest growth year-over-year, representing 7.9% on a constant currency basis, coming primarily from the health and government vertical markets. This strong U.S. performance was partly offset by the expiry of an outsourcing contract in the financial services vertical within GIS, the non-renewal of a low margin contract in the government vertical market within the Canadian segment, and the sale of Conseillers en informatique d’affaires CIA Inc. (“CIA”), also within Canada. Excluding these items, our revenue would have grown by 18.2% or 17.2% on a constant currency basis.

Fiscal 2012 was notably marked by the acquisition of Logica completed on August 20, 2012. Separated into a standalone segment for reporting purposes, Logica’s results subsequent to the acquisition date represented $567.9 million, representing 13.4% to the total Company growth.

| 3.4.1. | U.S. |

Revenue in our U.S. segment was $2,091.1 million in fiscal 2012, an increase of $195.1 million or 10.3% from $1,896.0 million in fiscal 2011. When removing the favourable foreign exchange impact of $46.2 million, revenue grew $148.9 million or 7.9% year-over-year. The increase in revenue was primarily due to additional work from new contracts as well as due to the extended scope of existing engagements in the government and health vertical markets.

| 3.4.2. | Canada |

Revenue in our Canada segment for fiscal 2012 was $1,212.6 million, a decrease of $74.4 million or 5.8% compared to fiscal 2011. The decrease was mainly due to the run off of client projects as they were delivered, primarily in the health and government vertical markets. We also encountered delays in contract awards and the ramping up of new projects. In addition, the actions taken effective the third quarter of last year with the expiration of a government contract not meeting our profitability standards and the disposal of our interest in Conseillers en informatique d’affaires CIA Inc. (“CIA”), as previously disclosed, also contributed to the year-over-year revenue decline. These last two items alone had a year-over-year impact of $44.4 million. Excluding these two items, the revenue would have decreased by 2.4% on a constant currency basis.

| 3.4.3. | Global Infrastructure Services |

Revenue in our Global Infrastructure Services segment was $684.9 million, a decrease of $131.8 million or 16.1% compared to fiscal 2011. Foreign currency fluctuations had an insignificant impact for the year. As disclosed earlier in fiscal 2012, the expiry of a large outsourcing contract in the financial services vertical market, representing $140.9 million of the year-over-year variation, was the primary cause of the decrease. When excluding this impact, revenue would have increased by 1.1% on a constant currency basis.

| 3.4.4. | Europe |

Revenue in the Europe segment was $216.0 million for fiscal 2012. On a constant currency basis, revenue remained stable. Taking into account the effect of foreign currency, revenue decreased $8.2 million or 3.7% from the $224.2 million reported in prior year. Lower consulting and project work in the telecommunications and utilities vertical, primarily resulting from cautious investing behaviours in the European market, was offset by the ramp-up of work volumes with new and existing clients across all other vertical markets.

| CGI Group Inc. – Management’s Discussion and Analysis for the year ended September 30, 2012 | Page 16 of 48 |

| 3.4.5. | Logica |

The acquisition of Logica occurred during the peak vacation period in Europe where a significant number of the members as well as their clients were on leave. As a significant portion of Logica’s revenue is recognized on a time and material basis, the resulting revenue for this period was not reflective of business-as-usual.

Revenue generated by Logica operations for the six-week period subsequent to the acquisition date represented $567.9 million or 11.9% of total Company revenue for the year. During this period, Logica’s revenue consisted of 14.1% from financial services, 29.4% from government, 2.8% from healthcare, 29.9% from MRD, and 23.8% from telecommunications & utilities.

| 3.5. | OPERATING EXPENSES |

| % of | % of | Change | ||||||||||||||||||||||

(in thousands of dollars except for percentage) | 2012 | Revenue | 2011 | Revenue | $ | % | ||||||||||||||||||

Costs of services, selling and administrative | 4,226,859 | 88.6 | % | 3,690,960 | 87.4 | % | 535,899 | 14.5 | % | |||||||||||||||

Foreign exchange gain | (1,134 | ) | (0.0 | %) | (3,365 | ) | (0.1 | %) | 2,231 | (66.3 | %) | |||||||||||||

| 3.5.1. | Costs of Services, Selling and Administrative |