MANAGEMENT’S

DISCUSSION AND ANALYSIS

FISCAL YEAR 2016

November 9, 2016

Basis of Presentation

This Management’s Discussion and Analysis of the Financial Position and Results of Operations (“MD&A”) is the responsibility of management and has been reviewed and approved by the Board of Directors. This MD&A has been prepared in accordance with the requirements of the Canadian Securities Administrators. The Board of Directors is ultimately responsible for reviewing and approving the MD&A. The Board of Directors carries out this responsibility mainly through its Audit and Risk Management Committee, which is appointed by the Board of Directors and is comprised entirely of independent and financially literate directors.

Throughout this document, CGI Group Inc. is referred to as “CGI”, “we”, “our” or “Company”. This MD&A provides information management believes is relevant to an assessment and understanding of the consolidated results of operations and financial condition of the Company. This document should be read in conjunction with the audited consolidated financial statements and the notes thereto for the years ended September 30, 2016 and 2015. CGI’s accounting policies are in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). All dollar amounts are in Canadian dollars unless otherwise indicated.

Materiality of Disclosures

This MD&A includes information we believe is material to investors. We consider something to be material if it results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares, or if it is likely that a reasonable investor would consider the information to be important in making an investment decision.

Forward-Looking Statements

All statements in this MD&A that do not directly and exclusively relate to historical facts constitute “forward-looking statements” within the meaning of that term in Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended, and are “forward-looking information” within the meaning of Canadian securities laws. These statements and this information represent CGI’s intentions, plans, expectations and beliefs, and are subject to risks, uncertainties and other factors, of which many are beyond the control of the Company. These factors could cause actual results to differ materially from such forward-looking statements or forward-looking information. These factors include but are not restricted to: the timing and size of new contracts; acquisitions and other corporate developments; the ability to attract and retain qualified employees; market competition in the rapidly evolving information technology industry; general economic and business conditions; foreign exchange and other risks identified in the MD&A and in other public disclosure documents filed with the Canadian securities authorities (filed on SEDAR at www.sedar.com) and the U.S. Securities and Exchange Commission (filed on EDGAR at www.sec.gov), as well as assumptions regarding the foregoing. The words “believe”, “estimate”, “expect”, “intend”, “anticipate”, “foresee”, “plan”, and similar expressions and variations thereof, identify certain of such forward-looking statements or forward-looking information, which speak only as of the date on which they are made. In particular, statements relating to future performance are forward-looking statements and forward-looking information. CGI disclaims any intention or obligation to publicly update or revise any forward-looking statements or forward-looking information, whether as a result of new information, future events or otherwise, except as required by applicable law. Readers are cautioned not to place undue reliance on these forward-looking statements or on this forward-looking information. You will find more information about the risks that could cause our actual results to differ significantly from our current expectations in section 10 – Risk Environment.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 1 |

Non-GAAP and Key Performance Measures

The reader should note that the Company reports its financial results in accordance with IFRS. However, we use a combination of financial measures, ratios, and non-GAAP measures to assess our Company’s performance. The non-GAAP measures used in this MD&A do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other issuers. These measures should be considered as supplemental in nature and not as a substitute for the related financial information prepared in accordance with IFRS.

The table below summarizes our non-GAAP measures and most relevant key performance measures:

| Profitability | • | Adjusted EBIT (non-GAAP) – is a measure of earnings excluding restructuring costs, net finance costs and income tax expense as these items are not directly related to the cost of operations. Management believes this measure is useful to investors as it best reflects the Company's operating profitability and allows for better comparability from period to period as well as to trend analysis in our operations. A reconciliation of the adjusted EBIT to its closest IFRS measure can be found in section 3.7 of the present document. |

| • | Net earnings – is a measure of earnings generated for shareholders. | |

| • | Diluted earnings per share – is a measure of earnings generated for shareholders on a per share basis, assuming all dilutive elements are exercised. | |

| • | Net earnings excluding specific items (non-GAAP) – is a measure of net earnings excluding certain items not considered by management to be part of the day to day operations. By excluding these items, it provides a better evaluation of operating performance using the same measures as management. Management believes that, as a result, the investors are afforded greater transparency in assessing the true operation performance of the Company also providing better comparability from period to period. A reconciliation of the net earnings excluding specific items to its closest IFRS measure can be found in section 3.8.3. of the present document. | |

| • | Basic and diluted earnings per share excluding specific items (non-GAAP) – is defined as the net earnings excluding specific items (non-GAAP) on a per share basis. Management believes that this measure is useful to investors as it best reflects the Company's operating profitability on a per share basis and allows for better comparability from period to period. The basic and diluted earnings per share reported in accordance with IFRS can be found in section 3.8 of the present document while the basic and diluted earnings per share excluding specific items can be found in section 3.8.3. | |

| Liquidity | • | Cash provided by operating activities – is a measure of cash generated from managing our day-to-day business operations. We believe strong operating cash flow is indicative of financial flexibility, allowing us to execute our Company's strategy. |

| • | Days sales outstanding ("DSO") (non-GAAP) – is the average number of days needed to convert our trade receivables and work in progress into cash. DSO is obtained by subtracting deferred revenue from trade accounts receivable and work in progress; the result is divided by the quarter’s revenue over 90 days. Deferred revenue is net of the fair value adjustments on revenue-generating contracts established upon a business combination. Management tracks this metric closely to ensure timely collection, healthy liquidity, and is committed to a DSO target of 45 days or less. We believe this measure is useful to investors as it demonstrates the Company's ability to timely convert its trade receivables and work in progress into cash. | |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 2 |

| Growth | • | Constant currency growth (non-GAAP) – is a measure of revenue growth before foreign currency impacts. This growth is calculated by translating current period results in local currency using the conversion rates in the equivalent period from the prior year. Management believes that it is helpful to adjust revenue to exclude the impact of currency fluctuations to facilitate period-to-period comparisons of business performance. We believe that this measure is useful to investors for the same reason. |

| • | Backlog (non-GAAP) – includes new contract wins, extensions and renewals (“bookings”(non-GAAP)), partially offset by the backlog consumed during the period as a result of client work performed and adjustments related to the volume, cancellation and the impact of foreign currencies to our existing contracts. Backlog incorporates estimates from management that are subject to change. Management tracks this measure as it is a key indicator of management's best estimate of revenue to be realized in the future and believes that this measure is useful to investors for the same reason. | |

| • | Book-to-bill ratio (non-GAAP) – is a measure of the proportion of the value of our bookings to our revenue in the period. This metric allows management to monitor the Company’s business development efforts to ensure we grow our backlog and our business over time and believes that this measure is useful to investors for the same reason. Management remains committed to maintaining a target ratio greater than 100% over a trailing 12-month period. Management believes that a longer period is a more representative measure as the services and contract type, size and timing of bookings could cause this measurement to fluctuate significantly if taken for only a three-month period. | |

| Capital Structure | • | Net debt (non-GAAP) – is obtained by subtracting from our debt our cash and cash equivalents, short-term investments, long-term investments and fair value of foreign currency derivative financial instruments related to debt. Management uses the net debt metric to monitor the Company's financial leverage. We believe that this metric is useful to investors as it provides insight into our financial strength. A reconciliation of net debt to its closest IFRS measure can be found in section 4.5 of the present document. |

| • | Net debt to capitalization ratio (non-GAAP) – is a measure of our level of financial leverage and is obtained by dividing the net debt by the sum of shareholder's equity and debt. Management uses the net debt to capitalization metric to monitor the proportion of debt versus capital used to finance our operations and to assess the Company's financial strength. We believe that this metric is useful to investors as it provides insight into our financial strength. | |

| • | Return on equity ("ROE") (non-GAAP) – is a measure of the rate of return on the ownership interest of our shareholders and is calculated as the proportion of earnings for the last 12 months over the last four quarters' average equity. Management looks at ROE to measure its efficiency at generating earnings for the Company’s shareholders and how well the Company uses the invested funds to generate earnings growth. We believe that this measure is useful to investors for the same reasons. | |

| • | Return on invested capital ("ROIC") (non-GAAP) – is a measure of the Company’s efficiency at allocating the capital under its control to profitable investments and is calculated as the proportion of the after-tax adjusted EBIT for the last 12 months, over the last four quarters' average invested capital, which is defined as the sum of equity and net debt. Management examines this ratio to assess how well it is using its funds to generate returns. We believe that this measure is useful to investors for the same reason. | |

Reporting segments

The Company's operations are managed through the following seven operating segments, referred to as our Strategic Business Units, namely: United States of America ("U.S."); Nordics; Canada; France (including Luxembourg and Morocco) ("France"); United Kingdom ("U.K."); Eastern, Central and Southern Europe (primarily Netherlands and Germany) ("ECS"); and Asia Pacific (including Australia, India and the Philippines) ("Asia Pacific"). Please refer to sections 3.4 and 3.6 of the present document and to note 27 of our audited consolidated financial statements for additional information on our segments.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 3 |

MD&A Objectives and Contents

| • | Provide a narrative explanation of audited consolidated financial statements through the eyes of management; |

| • | Provide the context within which audited consolidated financial statements should be analyzed, by giving enhanced disclosure about the dynamics and trends of the Company’s business; and |

| • | Provide information to assist the reader in ascertaining the likelihood that past performance is indicative of future performance. |

In order to achieve these objectives, this MD&A is presented in the following main sections:

| Section | Contents | Pages | |

| 1. Corporate Overview | A description of our business and how we generate revenue as well as the markets in which we operate. | ||

| 1.1. About CGI | |||

| 1.2. Vision and Strategy | |||

| 1.3. Competitive Environment | |||

| 2. Highlights and Key Performance Measures | A summary of key highlights during the year, the past three years' key performance measures, and CGI’s stock performance. | ||

| 2.1. Fiscal 2016 Year-Over-Year Highlights | |||

| 2.2. Selected Yearly Information & Key Performance Measures | |||

| 2.4. Investments in subsidiaries | |||

| 3. Financial Review | A discussion of year-over-year changes to financial results between the years ended September 30, 2016 and 2015, describing the factors affecting revenue and adjusted EBIT on a consolidated and reportable segment basis, and also by describing the factors affecting changes in the major expense categories. Also discussed are bookings broken down by contract type, service type, segment, and by vertical market. | ||

| 3.1. Bookings and Book-to-Bill Ratio | |||

| 3.2. Foreign Exchange | |||

| 3.3. Revenue Distribution | |||

| 3.4. Revenue Variation and Revenue by Segment | |||

| 3.5. Operating Expenses | |||

| 3.6. Adjusted EBIT by Segment | |||

| 3.7. Earnings Before Income Taxes | |||

| 3.8. Net Earnings and Earnings Per Share (“EPS”) | |||

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 4 |

| Section | Contents | Pages | |

| 4. Liquidity | A discussion of changes in cash flows from operating, investing and financing activities. This section also describes the Company’s available capital resources, financial instruments, and off-balance sheet financing and guarantees. Measures of capital structure (net debt to capitalization, ROE, and ROIC) and liquidity (DSO) are analyzed on a year-over-year basis. | ||

| 4.1. Consolidated Statements of Cash Flows | |||

| 4.2. Capital Resources | |||

| 4.3. Contractual Obligations | |||

| 4.4. Financial Instruments and Hedging Transactions | |||

| 4.5. Selected Measures of Liquidity and Capital Resources | |||

| 4.6. Off-Balance Sheet Financing and Guarantees | |||

| 4.7. Capability to Deliver Results | |||

| 5. Fourth Quarter Results | A discussion of year-over-year changes to operating results between the three months ended September 30, 2016 and 2015, describing the factors affecting revenue, adjusted EBIT earnings on a consolidated and reportable segment basis as well as cash from operating, investing and financing activities. | ||

| 5.1. Foreign Exchange | |||

| 5.2. Revenue Variation and Revenue by Segment | |||

| 5.3. Adjusted EBIT by Segment | |||

| 5.4. Net Earnings and EPS | |||

| 5.5. Consolidated Statements of Cash Flows | |||

| 6. Eight Quarter Summary | A summary of the past eight quarters’ key performance measures and a discussion of the factors that could impact our quarterly results. | ||

| 7. Changes in Accounting Policies | A summary of the future accounting standard changes. | ||

| 8. Critical Accounting Estimates | A discussion of the critical accounting estimates made in the preparation of the audited consolidated financial statements. | ||

| 9. Integrity of Disclosure | A discussion of the existence of appropriate information systems, procedures and controls to ensure that information used internally and disclosed externally is complete and reliable. | ||

| 10. Risk Environment | A discussion of the risks affecting our business activities and what may be the impact if these risks are realized. | ||

| 10.1. Risks and Uncertainties | |||

| 10.2. Legal Proceedings | |||

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 5 |

| 1. | Corporate Overview |

1.1. ABOUT CGI

Founded in 1976 and headquartered in Montréal, Canada, CGI is among the largest Information Technology ("IT") and business process service providers in the world, with approximately 68,000 professionals. Through high-end consulting, systems integration, transformational outsourcing and Intellectual Property ("IP") solutions, combined with in-depth industry expertise, CGI works with clients across the globe through a unique client proximity and best-fit global delivery model to accelerate their digital transformation and drive competitive advantage.

End-to-end services

CGI delivers end-to-end services that cover the full spectrum of delivery; from solution design and development, to implementation, integration and technology operations. Our portfolio encompasses:

| • | High-end consulting and system integration: CGI helps clients form their digital roadmap, adopting an agile, iterative approach that enables them to innovate, connect and rationalize legacy systems to deliver enterprise-wide change. |

| • | Transformational outsourcing: Our clients entrust us with full or partial responsibility for their IT and business functions. In return, we deliver significant efficiency improvements and cost savings. Typical services in an end-to-end engagement include: application development, integration and maintenance; technology infrastructure management; and business process services, such as collections and payroll management. Outsourcing contracts are long term in nature, with a typical duration of 5 to 10 or more years, allowing our clients to reinvest savings, further driving digital transformation. |

Deep industry expertise

CGI has long and focused practices in all of our core industries, providing clients with a partner that is not only expert in IT, but expert in their industries. This combination of business knowledge and digital technology expertise allows us to help our clients adapt as their industries change and, in the process, allows us to evolve the industries in which we operate.

Our targeted industries include: government, financial services, health, utilities, telecommunications, oil & gas, manufacturing, retail & consumer services, transportation and post & logistics. While these represent our go-to-market industry targets, we group these industries into the following: government; financial services; health; telecommunications & utilities; and manufacturing, retail & distribution ("MRD").

As the move toward digitalization continues to increase across industries, CGI partners with clients to support their strategic initiatives. We provide extensive industry expertise to guide them in becoming customer-centric digital organizations.

Digital IP solutions

CGI’s comprehensive portfolio of IP solutions support our clients’ mission-critical business functions and accelerate their digital transformation. We offer more than 150 IP-based solutions for the industries we serve, as well as cross-industry solutions. These solutions include digital-enabling software applications, reusable frameworks and innovative delivery methodologies - like Software as a Service.

Client-inspired innovation

CGI is a trusted partner with more than 40 years of experience in delivering innovative, client-inspired business services and solutions. Through innovation programs and investments, CGI supports clients with their most strategic initiatives. We help develop, innovate and protect the technology that enables clients to achieve their digital transformation goals faster with reduced risk and enduring results.

Quality processes

CGI clients expect consistency of service wherever and whenever they engage us. We have an outstanding track record of on-time, within-budget delivery as a result of our commitment to excellence and our robust governance model - the CGI Management Foundation. The CGI Management Foundation provides a common business language, frameworks and

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 6 |

practices for managing all operations consistently across the globe, driving a focus on continuous improvement. We also invest in rigorous quality and service delivery standards (including ISO and Capability Maturity Model Integration ("CMMI") certification programs), as well as a comprehensive Client Satisfaction Assessment Program, to ensure high client satisfaction on an ongoing basis.

1.2. VISION AND STRATEGY

CGI is unique compared to most companies. We not only have a vision, but also a dream: “To create an environment in which we enjoy working together and, as owners, contribute to building a company we can be proud of.” This dream has motivated us since our founding in 1976 and drives our vision: “To be a global, world-class information technology and business process services leader helping our clients succeed.”

In pursuing this dream and vision, CGI has been highly disciplined throughout its history in executing a Build and Buy profitable growth strategy comprised of four pillars that combine profitable organic growth (Build) and accretive acquisitions (Buy):

Pillar 1: Smaller contract wins, renewals and extensions

Pillar 2: Large, long-term transformational outsourcing contracts

Pillar 3: Small firm or niche player acquisitions

Pillar 4: Large, transformational acquisitions

The first two pillars relate to driving profitable organic growth through the pursuit of contracts - both large and small - with new and existing clients in our targeted industries.

The last two pillars focus on growth through niche and large acquisitions. We identify niche acquisitions through a strategic qualification process that systematically searches for targets to strengthen our local proximity in metro markets, our industry expertise and enhance our services and solutions. We also pursue large acquisitions to further expand our geographic presence and critical mass, which enables us to compete for large outsourcing contracts and broaden our client relationships. CGI will continue to be a consolidator in the IT services industry.

Since 1976, our professionals have been working toward the same dream and vision. Today, with a presence in hundreds of global locations and more than $10 billion in revenue, our aspiration is to double our size over a 5 to 7 year period.

Executing our strategy

CGI’s strategy is executed through a unique business model that combines client proximity with an extensive global delivery network to deliver the following benefits:

| • | Local responsiveness and accountability: We live and work near our clients to provide a high level of responsiveness. Our local CGI teams speak our clients' language, understand their business environment, and collaborate to meet their goals and advance their business. |

| • | Global reach: Our local presence is complemented by an expansive global delivery network that ensures our clients have 24/7 access to best-fit digital capabilities and resources to meet their end-to-end needs. |

| • | Committed experts: One of our key strategic goals is to be our clients’ expert of choice. To achieve this, we invest in recruiting professionals with extensive industry, business and technology expertise, particularly in high-demand areas, such as agile services, robotics process automation, cloud, mobile computing, cybersecurity, data analytics and the Internet of Things. In addition, a majority of CGI professionals are also shareholders, providing an added level of commitment to the success of our clients. |

| • | Comprehensive quality processes: CGI’s investment in quality frameworks and rigorous client satisfaction assessments has resulted in a consistent track record of on-time and within-budget project delivery. |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 7 |

1.3. COMPETITIVE ENVIRONMENT

In today’s digital era, there is a competitive urgency for organizations across industries to become digital in a sustainable way. The pressure is on to modernize legacy assets and connect them to digital business and operating models. Central to this massive transformation is the evolving role of technology. Traditionally viewed as an enabler, technology is now being recognized as a business driver. The promise of digital creates an enormous opportunity to transform organizations end-to-end, and CGI is well-positioned to serve as a digital partner and expert of choice. We’re working with clients across the globe to implement digital strategies, roadmaps and solutions that revolutionize the customer/citizen experience, drive the launch of new products and services, and deliver efficiencies and cost savings.

As the demand for digitalization increases, competition within the global IT industry is intensifying. CGI’s competition comprises a variety of players; from niche companies providing specialized services and software, to global, end-to-end IT service providers, to large consulting firms. All of these players are competing to deliver some or all of the services we provide. Many factors distinguish the industry leaders, including the following:

| • | Industry and technology expertise; |

| • | On-time, within-budget delivery; |

| • | Total cost of services; |

| • | Breadth of digital IP solutions; |

| • | Global delivery capabilities; and |

| • | Local presence and strength of client relationships. |

CGI compares very favourably with the competition with respect to all of these factors. We’re not only delivering all of the capabilities clients need to compete in a digital world, but the immediate results and long-term value they expect. We’re helping clients to better run, change and grow their businesses providing a competitive differentiator.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 8 |

2. | Highlights and Key Performance Measures |

2.1. FISCAL 2016 YEAR-OVER-YEAR HIGHLIGHTS

Key performance figures for the period include:

| • | Revenue of $10.7 billion, up 3.9%; |

| • | Bookings of $11.7 billion, or 110% of revenue; |

| • | Backlog of $20.9 billion; up $181.8 million; |

| • | Adjusted EBIT of $1,560.3 million, up 7.1%; |

| • | Adjusted EBIT margin of 14.6%, up 40 basis points; |

| • | Net earnings of $1,068.7 million, up 9.3%; |

| • | Net earnings margin of 10.0%, up 50 basis points; |

| • | Diluted EPS of $3.42, up 12.5%; |

| • | Cash provided by operating activities of $1,333.1 million, or 12.5% of revenue; |

| • | Net debt of $1.3 billion, down $446.3 million; and |

| • | Return on equity of 17.2%. |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 9 |

2.2. SELECTED YEARLY INFORMATION & KEY PERFORMANCE MEASURES

| As at and for the years ended September 30, | 2016 | 2015 | 2014 | Change 2016 / 2015 | Change 2015 / 2014 |

| In millions of CAD unless otherwise noted | |||||

| Growth | |||||

| Revenue | 10,683.3 | 10,287.1 | 10,499.7 | 396.2 | (212.6) |

| Year-over-year revenue growth | 3.9% | (2.0%) | 4.1% | 5.9% | (6.1%) |

Constant currency year-over-year revenue growth 1 | 0.2% | (4.0%) | (2.9%) | 4.2% | (1.1%) |

| Backlog | 20,893 | 20,711 | 18,237 | 182 | 2,474 |

| Bookings | 11,731 | 11,640 | 10,169 | 91 | 1,471 |

| Book-to-bill ratio | 109.8% | 113.2% | 96.8% | (3.4%) | 16.4% |

| Profitability | |||||

Adjusted EBIT 2 | 1,560.3 | 1,457.3 | 1,356.9 | 103.0 | 100.4 |

Adjusted EBIT margin 2 | 14.6% | 14.2% | 12.9% | 0.4% | 1.3% |

| Net earnings | 1,068.7 | 977.6 | 859.4 | 91.2 | 118.2 |

| Net earnings margin | 10.0% | 9.5% | 8.2% | 0.5% | 1.3% |

| Diluted EPS (in dollars) | 3.42 | 3.04 | 2.69 | 0.38 | 0.35 |

Net earnings excluding specific items3 | 1,081.5 | 1,005.1 | 893.5 | 76.4 | 111.6 |

Net earnings margin excluding specific items 3 | 10.1% | 9.8% | 8.5% | 0.3% | 1.3% |

Diluted EPS excluding specific items (in dollars) 3 | 3.46 | 3.13 | 2.80 | 0.33 | 0.33 |

| Liquidity | |||||

| Cash provided by operating activities | 1,333.1 | 1,289.3 | 1,174.8 | 43.8 | 114.5 |

| As a % of revenue | 12.5% | 12.5% | 11.2% | — | 1.3% |

Days sales outstanding 4 | 44 | 44 | 43 | — | 1 |

| Capital structure | |||||

Net debt 5 | 1,333.3 | 1,779.6 | 2,113.3 | (446.3) | (333.7) |

Net debt to capitalization ratio 6 | 15.8% | 21.7% | 27.6% | (5.9%) | (5.9%) |

Return on equity 7 | 17.2% | 17.7% | 18.8% | (0.5%) | (1.1%) |

Return on invested capital 8 | 14.5% | 14.5% | 14.5% | — | — |

| Balance sheet | |||||

| Cash and cash equivalents, and short-term investments | 596.5 | 305.3 | 535.7 | 291.2 | (230.4) |

| Total assets | 11,693.3 | 11,787.3 | 11,234.1 | (94.0) | 553.2 |

Long-term financial liabilities 9 | 1,765.4 | 1,896.4 | 2,748.4 | (131.0) | (852.0) |

1 | Constant currency growth is adjusted to remove the impact of foreign currency exchange rate fluctuations. Please refer to section 3.4 for details. |

2 | Adjusted EBIT is a measure for which we provide the reconciliation to its closest IFRS measure in section 3.7. For the year ended September 30, 2014, adjusted EBIT excludes integration-related costs related to the restructuring and transformation of the operations of Logica plc ("Logica") to the CGI model. |

3 | Net earnings excluding specific items is a measure for which we provide the reconciliation to its closest IFRS measure in section 3.8.3 for the years ended September 30, 2016 and 2015. For the year ended September 30, 2014 specific items includes integration-related costs and resolution of acquisition-related provisions net of taxes as well as tax adjustments. Resolution of acquisition-related provisions came from adjustments of provisions that were established as part of the purchase price allocation for the Logica acquisition. Subsequent to the finalization of the purchase price allocation, such adjustments flow through the statement of earnings. |

4 DSO is a measure which is discussed in section 4.5.

5 Net debt is a measure for which we provide the reconciliation to its closest IFRS measure in section 4.5.

6 | The net debt to capitalization ratio is a measure which is discussed in section 4.5. |

7 | ROE is a measure which is discussed in section 4.5. |

8 ROIC is a measure which is discussed in section 4.5.

9 | Long-term financial liabilities include the long-term portion of the debt and the long-term derivative financial instruments. |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 10 |

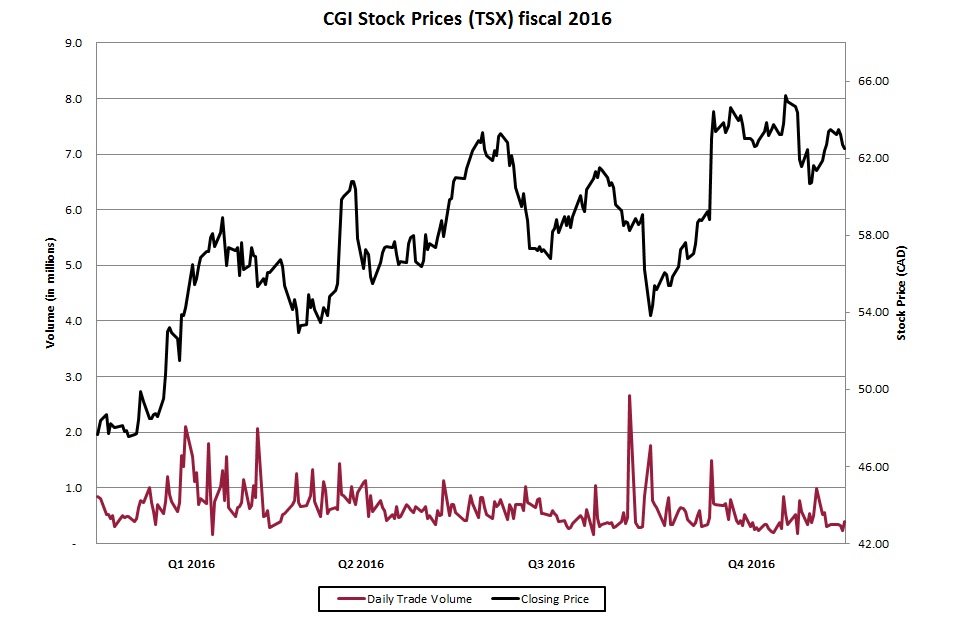

2.3. STOCK PERFORMANCE

2.3.1. Fiscal 2016 Trading Summary

CGI’s shares are listed on the Toronto Stock Exchange (“TSX”) (stock quote – GIB.A) and the New York Stock Exchange (“NYSE”) (stock quote – GIB) and are included in various indexes such as the S&P/TSX 60 Index.

| TSX | (CAD) | NYSE | (USD) | |||

| Open: | 48.35 | Open: | 36.34 | |||

| High: | 65.84 | High: | 50.58 | |||

| Low: | 46.91 | Low: | 35.38 | |||

| Close: | 62.49 | Close: | 47.63 | |||

CDN average daily trading volumes1: | 1,001,525 | NYSE average daily trading volumes: | 199,750 | |||

1 Includes the average daily volumes of both the TSX and alternative trading systems.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 11 |

2.3.2. Share Repurchase Program

On January 27, 2016, the Company’s Board of Directors authorized and subsequently received the approval from the TSX for the renewal of the Normal Course Issuer Bid (“NCIB”) to purchase up to 21,425,992 Class A subordinate voting shares for cancellation, representing 10% of the Company’s public float as of the close of business on January 22, 2016. The Class A subordinate voting shares may be purchased under the NCIB commencing February 11, 2016 and ending on the earlier of February 3, 2017 or the date on which the Company has either acquired the maximum number of Class A subordinate voting shares allowable under the NCIB, or elects to terminate the NCIB.

During fiscal 2016, the Company repurchased 9,319,875 Class A subordinate voting shares for approximately $517.8 million at an average price of $55.56 under the previous and current NCIB. The repurchased shares included 7,112,375 Class A subordinate voting shares repurchased from Caisse de dépôt et placement du Québec for cash consideration of $400.0 million. In accordance with the TSX rules, the repurchase is considered in the annual aggregate limit that the Company is entitled to repurchase under its current NCIB. As at September 30, 2016, the Company may repurchase up to 14,313,617 Class A subordinate voting shares under the current NCIB.

2.3.3. Capital Stock and Options Outstanding

The following table provides a summary of the Capital Stock and Options Outstanding as at November 4, 2016:

| Capital Stock and Options Outstanding | As at November 4, 2016 | |

| Class A subordinate voting shares | 272,103,193 | |

| Class B multiple voting shares | 32,852,748 | |

| Options to purchase Class A subordinate voting shares | 16,546,269 | |

2.4. INVESTMENTS IN SUBSIDIARIES

On November 4, 2016, the Company announced the closing of the acquisition of Collaborative Consulting, a system integration and consulting company headquartered in Boston, Massachusetts. With approximately 400 professionals and annualized revenues of approximately US$76.0M, Collaborative Consulting will enhance and accelerate CGI’s position as a provider of digital transformation services.

The cash acquisition of all unit holder positions of Collaborative Consulting was completed effective November 3, 2016.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 12 |

| 3. | Financial Review |

3.1. BOOKINGS AND BOOK-TO-BILL RATIO

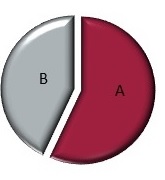

Bookings for the year were $11.7 billion representing a book-to-bill ratio of 109.8%. The breakdown of the new bookings signed during the year is as follows:

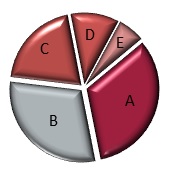

|  |  |  | |||||||||||||||

| Contract Type | Service Type | Segment | Vertical Market | |||||||||||||||

| A. | Extensions and | A. | Systems integration and | A. | U.S. | 25 | % | A. | Government | 33 | % | |||||||

| renewals | 57 | % | consulting | 53% | B. | Canada | 21 | % | B. | MRD | 30 | % | ||||||

| C. | Nordics | 15 | % | C. | Financial services | 20 | % | |||||||||||

| B. | New business | 43 | % | B. | Management of IT and | D. | France | 14 | % | D. | Telecommunications | |||||||

| business functions | 47% | E. | U.K. | 14 | % | & utilities | 11 | % | ||||||||||

| F. | ECS | 10 | % | E. | Health | 6 | % | |||||||||||

| G. | Asia Pacific | 1 | % | |||||||||||||||

Information regarding our bookings is a key indicator of the volume of our business over time. However, due to the timing and transition period associated with outsourcing contracts, the realization of revenue related to these bookings may fluctuate from period to period. The values initially booked may change over time due to their variable attributes, including demand-driven usage, modifications in the scope of work to be performed caused by changes in client requirements as well as termination clauses at the option of the client. As such, information regarding our bookings is not comparable to, nor should it be substituted for an analysis of our revenue; it is instead a key indicator of our future revenue used by the Company’s management to measure growth.

The following table provides a summary of the bookings and book-to-bill ratio by segment:

| In thousands of CAD except for percentages | Bookings for the year ended September 30, 2016 | Book-to-bill ratio for the year ended September 30, 2016 | ||||

| Total CGI | 11,730,713 | 109.8 | % | |||

| U.S. | 2,978,558 | 100.3 | % | |||

| Nordics | 1,736,860 | 100.6 | % | |||

| Canada | 2,495,550 | 151.4 | % | |||

| France | 1,584,578 | 107.6 | % | |||

| U.K. | 1,650,659 | 105.6 | % | |||

| ECS | 1,128,600 | 96.8 | % | |||

| Asia Pacific | 155,908 | 113.4 | % | |||

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 13 |

3.2. FOREIGN EXCHANGE

The Company operates globally and is exposed to changes in foreign currency rates. Accordingly, as prescribed by IFRS, we value assets, liabilities and transactions that are measured in foreign currencies using various exchange rates. We report all dollar amounts in Canadian dollars.

Closing foreign exchange rates

| As at September 30, | 2016 | 2015 | Change | |

| U.S. dollar | 1.3121 | 1.3399 | (2.1%) | |

| Euro | 1.4747 | 1.4958 | (1.4%) | |

| Indian rupee | 0.0197 | 0.0205 | (3.9%) | |

| British pound | 1.7076 | 2.0252 | (15.7%) | |

| Swedish krona | 0.1531 | 0.1596 | (4.1%) | |

| Australian dollar | 1.0061 | 0.9405 | 7.0% | |

Average foreign exchange rates

| For the years ended September 30, | 2016 | 2015 | Change | |

| U.S. dollar | 1.3255 | 1.2294 | 7.8% | |

| Euro | 1.4722 | 1.4081 | 4.6% | |

| Indian rupee | 0.0198 | 0.0195 | 1.5% | |

| British pound | 1.8876 | 1.8983 | (0.6%) | |

| Swedish krona | 0.1574 | 0.1506 | 4.5% | |

| Australian dollar | 0.9760 | 0.9634 | 1.3% | |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 14 |

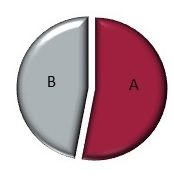

3.3. REVENUE DISTRIBUTION

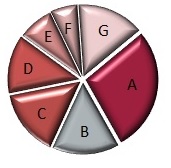

The following charts provide additional information regarding our revenue mix for the year:

|  |  | ||||||||||||

| Service Type | Client Geography | Vertical Market | ||||||||||||

| A. | Management of IT and business functions | 54% | A. | U.S. | 28 | % | A. | Government | 34 | % | ||||

| 1. | IT services | 44% | B. | Canada | 15 | % | B. | MRD | 23 | % | ||||

| 2. | Business process services | 10% | C. | U.K. | 15 | % | C. | Financial services | 21 | % | ||||

| D. | France | 13 | % | D. | Telecommunications & utilities | 15 | % | |||||||

| B. | Systems integration and consulting | 46% | E. | Sweden | 8 | % | E. | Health | 7 | % | ||||

| F. | Finland | 6 | % | |||||||||||

| G. | Rest of the world | 15 | % | |||||||||||

3.3.1. Client Concentration

IFRS guidance on segment disclosures defines a single customer as a group of entities that are known to the reporting entity to be under common control. As a consequence, our work for the U.S. federal government including its various agencies represented 13.2% of our revenue for fiscal 2016 as compared to 14.0% in fiscal 2015.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 15 |

3.4. REVENUE VARIATION AND REVENUE BY SEGMENT

Our seven segments are reported based on where the client's work is delivered from - our geographic delivery model.

The following table provides a summary of the year-over-year changes in our revenue, in total and by segment, separately showing the impacts of foreign currency exchange rate variations between fiscal 2016 and fiscal 2015. The fiscal 2015 revenue by segment was recorded reflecting the actual foreign exchange rates for that period. The foreign exchange impact is the difference between the current period’s actual results and the same period’s results converted with the prior year’s foreign exchange rate.

| For the years ended September 30, | 2016 | 2015 | Change | |||||

| $ | % | |||||||

| In thousands of CAD except for percentages | ||||||||

| Total CGI revenue | 10,683,264 | 10,287,096 | 396,168 | 3.9 | % | |||

| Variation prior to foreign currency impact | 0.2 | % | ||||||

| Foreign currency impact | 3.7 | % | ||||||

| Variation over previous period | 3.9 | % | ||||||

| U.S. | ||||||||

| Revenue prior to foreign currency impact | 2,673,658 | 2,813,127 | (139,469 | ) | (5.0 | %) | ||

| Foreign currency impact | 205,003 | |||||||

| U.S. revenue | 2,878,661 | 2,813,127 | 65,534 | 2.3 | % | |||

| Nordics | ||||||||

| Revenue prior to foreign currency impact | 1,583,199 | 1,638,985 | (55,786 | ) | (3.4 | %) | ||

| Foreign currency impact | 68,123 | |||||||

| Nordics revenue | 1,651,322 | 1,638,985 | 12,337 | 0.8 | % | |||

| Canada | ||||||||

| Revenue prior to foreign currency impact | 1,535,498 | 1,533,719 | 1,779 | 0.1 | % | |||

| Foreign currency impact | 833 | |||||||

| Canada revenue | 1,536,331 | 1,533,719 | 2,612 | 0.2 | % | |||

| France | ||||||||

| Revenue prior to foreign currency impact | 1,381,004 | 1,283,387 | 97,617 | 7.6 | % | |||

| Foreign currency impact | 63,962 | |||||||

| France revenue | 1,444,966 | 1,283,387 | 161,579 | 12.6 | % | |||

| U.K. | ||||||||

| Revenue prior to foreign currency impact | 1,445,329 | 1,331,287 | 114,042 | 8.6 | % | |||

| Foreign currency impact | (13,590 | ) | ||||||

| U.K. revenue | 1,431,739 | 1,331,287 | 100,452 | 7.5 | % | |||

| ECS | ||||||||

| Revenue prior to foreign currency impact | 1,152,070 | 1,211,228 | (59,158 | ) | (4.9 | %) | ||

| Foreign currency impact | 46,784 | |||||||

| ECS revenue | 1,198,854 | 1,211,228 | (12,374 | ) | (1.0 | %) | ||

| Asia Pacific | ||||||||

| Revenue prior to foreign currency impact | 533,059 | 475,363 | 57,696 | 12.1 | % | |||

| Foreign currency impact | 8,332 | |||||||

| Asia Pacific revenue | 541,391 | 475,363 | 66,028 | 13.9 | % | |||

For the year ended September 30, 2016 revenue was $10,683.3 million, an increase of $396.2 million, or 3.9% over the same period of fiscal 2015. On a constant currency basis, revenue increased by 0.2%. Foreign currency rate fluctuations favourably impacted our revenue by $379.4 million or 3.7%. The revenue growth in U.K., France and the increased use of our offshore global delivery centers in Asia Pacific compensated for the non-renewal of contracts in the U.S. federal defense market and lower work volumes in the Nordics and ECS segments.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 16 |

3.4.1. U.S.

For the year ended September 30, 2016 revenue in our U.S. segment was $2,878.7 million, an increase of $65.5 million or 2.3% over fiscal 2015. On a constant currency basis, revenue decreased by $139.5 million or 5.0%. The change in revenue was mainly driven by the non-renewal of contracts in the U.S. government market, mainly in the defense sector. This was partly offset by an increased volume of work within the U.S. federal civilian agencies.

For the year ended September 30, 2016, the top two U.S. vertical markets were government and financial services, which together accounted for approximately 77% of revenue.

3.4.2. Nordics

For the year ended September 30, 2016, revenue in our Nordics segment was $1,651.3 million, an increase of $12.3 million or 0.8% over the same period of fiscal 2015. On a constant currency basis, revenue decreased by $55.8 million or 3.4%. The change in revenue was mostly due to the expiration of certain infrastructure contracts, lower work volumes, and an increased usage of our offshore delivery centers in Asia Pacific. This was partly offset by an increased work volume in Denmark mainly in the MRD vertical market.

For the year ended September 30, 2016, Nordics' top two vertical markets were MRD and government, which together accounted for approximately 65% of revenue.

3.4.3. Canada

For the year ended September 30, 2016, revenue in our Canada segment was $1,536.3 million, an increase of $2.6 million or 0.2% compared to the same period last year. When considering the higher proportion of revenues delivered from our offshore delivery centers in Asia Pacific, our client revenue grew by 2.3%. This increase was mainly due to growth in the financial services market, including IP-based services and solutions revenue and new outsourcing contracts within the MRD vertical market. This was partly offset by expiration of certain infrastructure outsourcing contracts and the positive impact on revenue of a client arbitration award in Q3 2015.

For the year ended September 30, 2016, Canada’s top two vertical markets were financial services and telecommunications & utilities, which together accounted for approximately 62% of revenue.

3.4.4. France

For the year ended September 30, 2016, revenue in our France segment was $1,445.0 million, an increase of $161.6 million or 12.6% over the same period of fiscal 2015. On a constant currency basis, revenue increased by $97.6 million or 7.6%. The increase in revenue was mostly due to more work volume across the majority of their vertical markets and, to a lesser extent, to a recent business acquisition.

For the year ended September 30, 2016, France’s top two vertical markets were MRD and financial services, which together accounted for approximately 63% of revenue.

3.4.5. U.K.

For the year ended September 30, 2016, revenue in our U.K. segment was $1,431.7 million, an increase of $100.5 million or 7.5% over fiscal 2015. On a constant currency basis, revenue increased by $114.0 million or 8.6%. The increase in revenue was mainly due to new outsourcing contracts in the government market combined with higher work volume in the telecommunication & utilities and financial services vertical markets. This was partly offset by lower work volume with a client in the MRD vertical market.

For the year ended September 30, 2016, U.K.’s top two vertical markets were government and telecommunications & utilities, which together accounted for approximately 68% of revenue.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 17 |

3.4.6. ECS

For the year ended September 30, 2016, revenue in our ECS segment was $1,198.9 million, a decrease of $12.4 million or 1.0% over fiscal 2015. On a constant currency basis, revenue decreased by $59.2 million or 4.9%. The change in revenue was mostly due to lower work volume and projects completed in the Netherlands, lower work volume combined with the divesting of certain low margin contracts in Southern Europe and the wind-down of the majority of our operations in South America. This was partly offset by increased work volume in Germany mainly in the MRD and telecommunication & utilities vertical markets.

For the year ended September 30, 2016, ECS’ top two vertical markets were MRD and telecommunications & utilities, which together accounted for approximately 63% of revenue.

3.4.7. Asia Pacific

For the year ended September 30, 2016, revenue in our Asia Pacific segment was $541.4 million, an increase of $66.0 million or 13.9% over the same period of fiscal 2015. On a constant currency basis, revenue increased by $57.7 million or 12.1%. The increase in revenue was due the continued increased demand of our offshore delivery centers across our segments, as our clients continue taking advantage of our global delivery network. This was partly offset by lower work volumes in Australia.

For the year ended September 30, 2016, Asia Pacific’s top two vertical markets were telecommunications & utilities and MRD, which together accounted for approximately 72% of revenue.

3.5. OPERATING EXPENSES

| For the years ended September 30, | % of | % of | Change | |||||||||

| 2016 | Revenue | 2015 | Revenue | $ | % | |||||||

| In thousands of CAD except for percentages | ||||||||||||

| Costs of services, selling and administrative | 9,120,929 | 85.4 | % | 8,819,055 | 85.7 | % | 301,874 | 3.4 | % | |||

| Foreign exchange loss | 2,024 | 0.0 | % | 10,733 | 0.1 | % | (8,709 | ) | (81.1 | %) | ||

3.5.1. Costs of Services, Selling and Administrative

For the year ended September 30, 2016, costs of services, selling and administrative expenses amounted to $9,120.9 million, an increase of $301.9 million over the same period last year. As a percentage of revenue, cost of services, selling and administrative expenses improved to 85.4% from 85.7%. As a percentage of revenue, our costs of services improved compared to the same period last year mainly due to savings related to the recent restructuring program, improved utilization rates and the increased use of our global delivery network. Our selling and administrative expenses, as a percentage of revenue, remained stable.

During the year ended September 30, 2016 the translation of the results of our foreign operations from their local currencies to the Canadian dollar unfavourably impacted costs by $325.5 million substantially offsetting the favourable translation impact of $379.4 million on our revenue.

3.5.2. Foreign Exchange Loss

During the year ended September 30, 2016, CGI incurred $2.0 million of foreign exchange loss, mainly driven by the timing in payments combined with the volatility and fluctuation of foreign exchange rates. The Company, in addition to its natural hedges, has a strategy in place to manage its exposure, to the extent possible, to exchange rate fluctuations through the effective use of derivatives.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 18 |

3.6. ADJUSTED EBIT BY SEGMENT

| For the years ended September 30, | 2016 | 2015 | Change | |||||

| $ | % | |||||||

| In thousands of CAD except for percentages | ||||||||

| U.S. | 486,295 | 454,325 | 31,970 | 7.0 | % | |||

| As a percentage of U.S. revenue | 16.9 | % | 16.2 | % | ||||

| Nordics | 186,742 | 153,841 | 32,901 | 21.4 | % | |||

| As a percentage of Nordics revenue | 11.3 | % | 9.4 | % | ||||

| Canada | 345,483 | 343,692 | 1,791 | 0.5 | % | |||

| As a percentage of Canada revenue | 22.5 | % | 22.4 | % | ||||

| France | 174,685 | 146,615 | 28,070 | 19.1 | % | |||

| As a percentage of France revenue | 12.1 | % | 11.4 | % | ||||

| U.K. | 154,262 | 163,603 | (9,341 | ) | (5.7 | %) | ||

| As a percentage of U.K. revenue | 10.8 | % | 12.3 | % | ||||

| ECS | 114,256 | 118,141 | (3,885 | ) | (3.3 | %) | ||

| As a percentage of ECS revenue | 9.5 | % | 9.8 | % | ||||

| Asia Pacific | 98,588 | 77,091 | 21,497 | 27.9 | % | |||

| As a percentage of Asia Pacific revenue | 18.2 | % | 16.2 | % | ||||

| Adjusted EBIT | 1,560,311 | 1,457,308 | 103,003 | 7.1 | % | |||

| Adjusted EBIT margin | 14.6 | % | 14.2 | % | ||||

For the year ended September 30, 2016, adjusted EBIT margin increased to 14.6% from 14.2% for the same period last year. The favourable variance in adjusted EBIT margin was primarily due to productivity improvements, the savings driven by our restructuring program and a better mix of profitable revenue.

3.6.1. U.S.

For the year ended September 30, 2016, adjusted EBIT in the U.S. segment was $486.3 million, an increase of $32.0 million. Adjusted EBIT margin increased to 16.9% from 16.2% mostly due to additional research and development tax credits and the decrease in amortization of client relationships related to the acquisition of Stanley, Inc.

3.6.2. Nordics

For the year ended September 30, 2016, adjusted EBIT in the Nordics segment was $186.7 million, an increase of $32.9 million, while the adjusted EBIT margin improved to 11.3% from 9.4%. The increase in adjusted EBIT margin came mainly from the ongoing cost synergies within our infrastructure business, the improved delivery performance, and the savings generated from the restructuring program.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 19 |

3.6.3. Canada

For the year ended September 30, 2016, adjusted EBIT in the Canada segment was $345.5 million, an increase of $1.8 million compared to the same period last year, while the adjusted EBIT margin was stable when compared to fiscal 2015. When excluding the positive impact of a client arbitration award in Q3 2015, adjusted EBIT increased by 1.1% due to a better mix of profitable revenue, and growth in the financial services sector.

3.6.4. France

For the year ended September 30, 2016, adjusted EBIT in the France segment was $174.7 million, an increase of $28.1 million when compared to the same period last year. Adjusted EBIT margin improved to 12.1% from 11.4%. The increase in adjusted EBIT margin was mostly due to improved utilization rates on a year-over-year basis.

3.6.5. U.K.

For the year ended September 30, 2016, adjusted EBIT in the U.K. segment was $154.3 million, a decrease of $9.3 million when compared to fiscal 2015. Adjusted EBIT margin decreased to 10.8% from 12.3% mostly due to the positive impact of additional change orders on certain large contracts in fiscal 2015.

3.6.6. ECS

For the year ended September 30, 2016, adjusted EBIT was $114.3 million, a decrease of $3.9 million when compared to the same period last year. Adjusted EBIT margin was essentially stable with productivity improvements being offset by revenue impacts in the Netherlands as described in the revenue section.

3.6.7. Asia Pacific

For the year ended September 30, 2016, adjusted EBIT in the Asia Pacific segment was $98.6 million an increase of $21.5 million, while the margin improved to 18.2% from 16.2% compared to the same period last year mostly due to productivity improvements across their global delivery centers.

3.7. EARNINGS BEFORE INCOME TAXES

The following table provides a reconciliation between our adjusted EBIT and earnings before income taxes, which is reported in accordance with IFRS.

| For the years ended September 30, | 2016 | % of Revenue | 2015 | % of Revenue | Change | |||||||

| $ | % | |||||||||||

| In thousands of CAD except for percentage | ||||||||||||

| Adjusted EBIT | 1,560,311 | 14.6 | % | 1,457,308 | 14.2 | % | 103,003 | 7.1 | % | |||

| Minus the following items: | ||||||||||||

| Restructuring costs | 29,100 | 0.3 | % | 35,903 | 0.3 | % | (6,803 | ) | (18.9 | %) | ||

| Net finance costs | 78,426 | 0.7 | % | 92,857 | 0.9 | % | (14,431 | ) | (15.5 | %) | ||

| Earnings before income taxes | 1,452,785 | 13.6 | % | 1,328,548 | 12.9 | % | 124,237 | 9.4 | % | |||

3.7.1. Restructuring Costs

In Q1 2016, we completed the previously announced restructuring program for productivity improvement initiatives. For the year ended September 30, 2016, the Company incurred $29.1 million of restructuring costs for a total expense of $65.0 million over the entire program.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 20 |

3.7.2. Net Finance Costs

Net finance costs mainly include the interest on our long-term debt. The decrease in net finance costs for the year ended September 30, 2016 was mainly the result of the early repayments of the May 2016 maturing tranche of the unsecured committed term loan credit facility.

3.8. NET EARNINGS AND EARNINGS PER SHARE

The following table sets out the information supporting the earnings per share calculations:

| For the years ended September 30, | 2016 | 2015 | Change | |||||

| $ | % | |||||||

| In thousands of CAD except for percentage and shares data | ||||||||

| Earnings before income taxes | 1,452,785 | 1,328,548 | 124,237 | 9.4 | % | |||

| Income tax expense | 384,069 | 350,992 | 33,077 | 9.4 | % | |||

| Effective tax rate | 26.4 | % | 26.4 | % | ||||

| Net earnings | 1,068,716 | 977,556 | 91,160 | 9.3 | % | |||

| Net earnings margin | 10.0 | % | 9.5 | % | ||||

| Weighted average number of shares outstanding | ||||||||

| Class A subordinate voting shares and Class B multiple voting shares (basic) | 304,808,130 | 311,477,555 | (2.1 | %) | ||||

| Class A subordinate voting shares and Class B multiple voting shares (diluted) | 312,773,156 | 321,422,444 | (2.7 | %) | ||||

| Earnings per share (in dollars) | ||||||||

| Basic | 3.51 | 3.14 | 0.37 | 11.8 | % | |||

| Diluted | 3.42 | 3.04 | 0.38 | 12.5 | % | |||

3.8.1. Income Tax Expense

For the year ended September 30, 2016, the income tax expense was $384.1 million compared to $351.0 million over the same period last year, while our effective tax rate remained stable. The income tax expense was impacted by a favourable tax adjustment of $14.4 million in Q2 2016 attributable to the recognition of deferred tax assets following an agreement with the U.K. tax authority and an additional tax expense for an amount of $5.9 million in Q1 2016 resulting from the re-evaluation of our deferred tax assets following the U.K. corporate tax reduction enacted in November 18, 2015. When excluding these tax adjustments and the tax effects from restructuring costs incurred in both years, the income tax rate would have been 27.0% during fiscal 2016 compared to 26.3% in fiscal 2015. The increase in the income tax expense and the income tax rate was mainly attributable to the increased profitability of our U.S., India and France operations where enacted income tax rates are higher.

The table in section 3.8.3. shows the year-over-year comparison of the tax rate with the impact of specific items removed.

Based on the enacted rates at the end of fiscal 2016 and our current business mix, we expect our effective tax rate before any significant adjustments to be in the range of 27.0% to 29.0% in subsequent periods.

3.8.2. Weighted Average Number of Shares

For fiscal 2016, CGI’s basic and diluted weighted average number of shares decreased compared to fiscal 2015 due to the impact of the repurchase of Class A subordinate voting shares, partly offset by the grants and the exercise of stock options.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 21 |

3.8.3. Net Earnings and Earnings per Share Excluding Specific Items

Below is a table showing the year-over-year comparison excluding specific items namely, restructuring costs, and tax adjustments:

| For the years ended September 30, | 2016 | 2015 | Change | |||||

| $ | % | |||||||

| In thousands of CAD except for percentages and shares data | ||||||||

| Earnings before income taxes | 1,452,785 | 1,328,548 | 124,237 | 9.4 | % | |||

| Add back: | ||||||||

Restructuring costs1 | 29,100 | 35,903 | (6,803 | ) | (18.9 | %) | ||

| Earnings before income taxes excluding specific items | 1,481,885 | 1,364,451 | 117,434 | 8.6 | % | |||

| Income tax expense | 384,069 | 350,992 | 33,077 | 9.4 | % | |||

| Add back: | ||||||||

Tax adjustments2 | 8,500 | — | 8,500 | — | ||||

| Tax deduction on restructuring costs | 7,858 | 8,352 | (494 | ) | (5.9 | %) | ||

| Income tax expense excluding specific items | 400,427 | 359,344 | 41,083 | 11.4 | % | |||

| Effective tax rate excluding specific items | 27.0 | % | 26.3 | % | ||||

| Net earnings excluding specific items | 1,081,458 | 1,005,107 | 76,351 | 7.6 | % | |||

| Net earnings excluding specific items margin | 10.1 | % | 9.8 | % | ||||

| Weighted average number of shares outstanding | ||||||||

| Class A subordinate voting shares and Class B multiple voting shares (basic) | 304,808,130 | 311,477,555 | (2.1 | %) | ||||

| Class A subordinate voting shares and Class B multiple voting shares (diluted) | 312,773,156 | 321,422,444 | (2.7 | %) | ||||

| Earnings per share excluding specific items (in dollars) | ||||||||

| Basic | 3.55 | 3.23 | 0.32 | 9.9 | % | |||

| Diluted | 3.46 | 3.13 | 0.33 | 10.5 | % | |||

1 | Refer to section 3.7.1. |

2 | Refer to section 3.8.1. |

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 22 |

4. | Liquidity |

4.1. CONSOLIDATED STATEMENTS OF CASH FLOWS

CGI’s growth is financed through a combination of our cash flow from operations, borrowing under our existing credit facilities, the issuance of long-term debt, and the issuance of equity. One of our financial priorities is to maintain an optimal level of liquidity through the active management of our assets and liabilities as well as our cash flows.

As at September 30, 2016, cash and cash equivalents were $596.5 million. The following table provides a summary of the generation and use of cash for the years ended September 30, 2016 and 2015.

| For the years ended September 30, | 2016 | 2015 | Change | ||||

| In thousands of CAD | |||||||

| Cash provided by operating activities | 1,333,074 | 1,289,310 | 43,764 | ||||

| Cash used in investing activities | (382,731 | ) | (257,127 | ) | (125,604 | ) | |

| Cash used in financing activities | (666,304 | ) | (1,303,663 | ) | 637,359 | ||

| Effect of foreign exchange rate changes on cash and cash equivalents | 7,228 | 41,027 | (33,799 | ) | |||

| Net increase (decrease) in cash and cash equivalents | 291,267 | (230,453 | ) | 521,720 | |||

4.1.1. Cash Provided by Operating Activities

For the year ended September 30, 2016, cash provided by operating activities was $1,333.1 million or 12.5% of revenue as compared to $1,289.3 million or 12.5% from the prior year.

The following table provides a summary of the generation and use of cash from operating activities:

| For the years ended September 30, | 2016 | 2015 | Change | ||||

| In thousands of CAD | |||||||

| Net earnings | 1,068,716 | 977,556 | 91,160 | ||||

| Amortization and depreciation | 400,060 | 424,044 | (23,984 | ) | |||

Other adjustments 1 | 132,171 | 89,451 | 42,720 | ||||

| Cash flow from operating activities before net change in non-cash working capital items | 1,600,947 | 1,491,051 | 109,896 | ||||

| Net change in non-cash working capital items: | |||||||

| Accounts receivable, work in progress and deferred revenue | (134,632 | ) | (25,517 | ) | (109,115 | ) | |

| Accounts payable and accrued liabilities, accrued compensation, provisions and long-term liabilities | (115,853 | ) | (204,169 | ) | 88,316 | ||

Other 2 | (17,388 | ) | 27,945 | (45,333 | ) | ||

| Net change in non-cash working capital items | (267,873 | ) | (201,741 | ) | (66,132 | ) | |

| Cash provided by operating activities | 1,333,074 | 1,289,310 | 43,764 | ||||

1 | Comprised of deferred income taxes, foreign exchange gain and share-based payment costs. |

2 | Comprised of prepaid expenses and other assets, long-term financial assets related to operating activities, retirement benefits obligations, derivative financial instruments and income taxes. |

For the year ended September 30, 2016, the $267.9 million of net change in non-cash working capital items was mostly due to :

•The increase in other receivables comprised mainly of tax credits receivable; and,

| • | The decrease in accounts payable and accrued liabilities, accrued compensation, provisions and long-term liabilities mainly driven by the net decrease in provisions including the payments of the restructuring provision and the timing of payroll accruals. |

The timing of our working capital inflows and outflows will always have an impact on the cash flow from operations.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 23 |

4.1.2. Cash Used in Investing Activities

For the year ended September 30, 2016, $382.7 million were used in investing activities while $257.1 million were used in the prior year.

The following table provides a summary of the generation and use of cash from investing activities:

| For the years ended September 30, | 2016 | 2015 | Change | ||||

| In thousands of CAD | |||||||

| Business acquisitions | (38,442 | ) | — | (38,442 | ) | ||

| Proceeds from sale of capital assets | 10,254 | 15,255 | (5,001 | ) | |||

| Purchase of property, plant and equipment | (165,516 | ) | (122,492 | ) | (43,024 | ) | |

| Additions to contract costs | (103,156 | ) | (78,815 | ) | (24,341 | ) | |

| Additions to intangible assets | (100,963 | ) | (71,357 | ) | (29,606 | ) | |

| Net proceeds from sale (purchase) of long-term investments | 14,928 | (4,736 | ) | 19,664 | |||

| Payments received from long-term receivables | 164 | 5,018 | (4,854 | ) | |||

| Cash used in investing activities | (382,731 | ) | (257,127 | ) | (125,604 | ) | |

The increase of $125.6 million in cash used in investing activities during the year ended September 30, 2016 was mainly due to :

| • | The purchase of property, plant and equipment due to investments across our data center infrastructure operations and global delivery centers; |

•Cash used in business acquisitions;

| • | Investments in intangible assets for the purchase of software licenses used mainly in the delivery of client contracts as well as investment in internal-use software; and, |

| • | Cash used in contract costs for new clients. |

This was partially offset by the net proceeds from the sale of long-term investments.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 24 |

4.1.3. Cash Used in Financing Activities

For the year ended September 30, 2016, $666.3 million were used in financing activities while $1,303.7 million were used in the prior year.

The following table provides a summary of the generation and use of cash from financing activities:

| For the years ended September 30, | 2016 | 2015 | Change | ||||

| In thousands of CAD | |||||||

| Net change in long-term debt | (182,651 | ) | (901,566 | ) | 718,915 | ||

| Settlement of derivative financial instruments | (24,057 | ) | (121,615 | ) | 97,558 | ||

| Purchase of Class A subordinate voting shares held in trust | (21,795 | ) | (11,099 | ) | (10,696 | ) | |

| Repurchase of Class A subordinate voting shares | (527,286 | ) | (323,069 | ) | (204,217 | ) | |

| Issuance of Class A subordinate voting shares | 89,485 | 53,686 | 35,799 | ||||

| Cash used in financing activities | (666,304 | ) | (1,303,663 | ) | 637,359 | ||

For the year ended September 30, 2016, $182.7 million was used to reduce our outstanding long-term debt mainly driven by the $129.7 million repayment under the term loan credit facility, while we made net repayments of $901.6 million to reduce our long-term debt last year. During the years ended September 30, 2016 and 2015, the Company used $24.1 million and $121.6 million respectively to settle the cross-currency swaps related to the outstanding long-term debt repaid during these periods.

For the year ended September 30, 2016, an amount of $21.8 million was used to purchase CGI Class A subordinate voting shares in connection with the Company's Performance Share Unit Plan ("PSU Plan"), while for the comparable period last year, an amount of $11.1 million was used. More information concerning the PSU Plan can be found in note 19 of the audited consolidated financial statements.

For the year ended September 30, 2016, we used $517.8 million to repurchase 9,319,875 Class A subordinate voting shares under the previous and current NCIB. We also used $9.5 million to pay and subsequently cancel 200,000 Class A subordinate voting shares repurchased and held by the Company as at the end of fiscal 2015. For the year ended September 30, 2015, $323.1 million was used to repurchase 6,725,735 Class A subordinate voting shares under the annual aggregate limit of the NCIB then in effect.

Finally, for the year ended September 30, 2016, we received $89.5 million in proceeds from the exercise of stock options, compared to $53.7 million during the year ended September 30, 2015.

4.1.4. Effect of Foreign Exchange Rate Changes on Cash and Cash Equivalents

For the year ended September 30, 2016, the effect of foreign exchange rate changes on cash and cash equivalents was $7.2 million. This amount had no effect on net earnings as it was recorded in other comprehensive income.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 25 |

4.2. CAPITAL RESOURCES

| As at September 30, 2016 | Total | Available | Outstanding | |||

| In thousands of CAD | ||||||

| Cash and cash equivalents | — | 596,529 | — | |||

| Long-term investments | — | 27,246 | — | |||

Unsecured committed revolving facility a | 1,500,000 | 1,466,086 | 33,914 | |||

| Total | 1,500,000 | 2,089,861 | 33,914 | |||

a Consists of Letters of Credit for $33.9 million outstanding as at September 30, 2016.

Our cash position and bank lines are sufficient to support our growth strategy. At September 30, 2016, cash and cash equivalents and long-term investments represented $623.8 million.

Cash equivalents typically include term deposits, all with maturities of 90 days or less. Long-term investments include corporate and government bonds with maturities ranging from one to five years, rated "A" or higher.

The amount of capital available was $2,089.9 million. The long-term debt agreements contain covenants, which require us to maintain certain financial ratios. As at September 30, 2016, CGI was in compliance with these covenants.

Total debt decreased by $216.1 million to $1,911.0 million as at September 30, 2016, compared to $2,127.1 million as at September 30, 2015. The variation was mainly due to the $129.7 million repayment under the unsecured committed revolving credit facility combined with other repayments.

As at September 30, 2016, CGI was showing a positive working capital1 of $425.0 million. The Company also had $1,466.1 million available under its unsecured committed revolving facility and is generating a significant level of cash that will allow it to fund its operations while maintaining adequate levels of liquidity. On November 8, 2016, the unsecured committed revolving facility was extended by two years to December 2021 and can be further extended. There were no material changes in the terms and conditions including interest rates and banking covenants.

As at September 30, 2016, the cash and cash equivalents held by foreign subsidiaries were $557.8 million ($263.6 million as at September 30, 2015). The tax implications and impact related to its repatriation will not materially affect the Company's liquidity.

1 Working capital is defined as total current assets minus total current liabilities.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 26 |

4.3. CONTRACTUAL OBLIGATIONS

We are committed under the terms of contractual obligations which have various expiration dates, primarily for the rental of premises, computer equipment used in outsourcing contracts and long-term service agreements. For the year ended September 30, 2016, the Company decreased its commitments by $770.2 million mainly due to a decrease in rental office space commitments and repayments of long-term debt.

| Commitment type | Total | Less than 1 year | 2nd and 3rd years | 4th and 5th years | After 5 years | |||||

| In thousands of CAD | ||||||||||

| Long-term debt | 1,861,880 | 173,362 | 423,464 | 342,285 | 922,769 | |||||

| Estimated interest on long-term debt | 361,842 | 69,010 | 124,309 | 97,673 | 70,850 | |||||

| Finance lease obligations | 42,172 | 18,738 | 17,183 | 5,489 | 762 | |||||

| Estimated interest on finance lease obligations | 2,033 | 978 | 878 | 171 | 6 | |||||

| Operating leases | ||||||||||

| Rental of office space (excluding costs of services and taxes) | 573,957 | 154,247 | 209,521 | 117,861 | 92,328 | |||||

| Computer equipment | 15,562 | 7,941 | 6,350 | 976 | 295 | |||||

| Automobiles | 97,775 | 39,256 | 49,072 | 9,111 | 336 | |||||

| Long-term service agreements and other | 189,676 | 85,825 | 93,446 | 10,092 | 313 | |||||

| Total contractual obligations | 3,144,897 | 549,357 | 924,223 | 583,658 | 1,087,659 | |||||

Our required benefit plan contributions have not been included in this table as such contributions depend on periodic actuarial valuations for funding purposes. Our contributions to defined benefit plans are estimated at $19.2 million for fiscal 2017 as described in note 16 of the audited consolidated financial statements.

4.4. FINANCIAL INSTRUMENTS AND HEDGING TRANSACTIONS

We use various financial instruments to manage our exposure to fluctuations of foreign currency exchange rates and interest rates. Please refer to notes 3 and 30 of our audited consolidated financial statements for additional information on our financial instruments.

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 27 |

4.5. SELECTED MEASURES OF LIQUIDITY AND CAPITAL RESOURCES

| As at September 30, | 2016 | 2015 | |||

| In thousands of CAD except for percentages | |||||

| Reconciliation between net debt and long-term debt including the current portion: | |||||

| Net debt | 1,333,323 | 1,779,623 | |||

| Add back: | |||||

| Cash and cash equivalents | 596,529 | 305,262 | |||

| Long-term investments | 27,246 | 42,202 | |||

| Fair value of foreign currency derivative financial instruments related to debt | (46,123 | ) | — | ||

| Long-term debt including the current portion | 1,910,975 | 2,127,087 | |||

| Net debt to capitalization ratio | 15.8 | % | 21.7 | % | |

| Return on equity | 17.2 | % | 17.7 | % | |

| Return on invested capital | 14.5 | % | 14.5 | % | |

| Days sales outstanding | 44 | 44 | |||

We use the net debt to capitalization ratio as an indication of our financial leverage in order to pursue large outsourcing contracts, expand global delivery centers, or make acquisitions. The net debt to capitalization ratio decreased to 15.8% in 2016 from 21.7% in 2015. The change in the net debt to capitalization ratio was mostly due to our improved cash generation allowing us to reduce our net debt by $446.3 million.

ROE is a measure of the return we are generating for our shareholders. ROE decreased to 17.2% in fiscal 2016 from 17.7% in fiscal 2015. The change was mostly the result of an increase in average capital driven by accumulated earnings.

ROIC is a measure of the Company’s efficiency in allocating the capital under our control to profitable investments. The return on invested capital was stable when compared to fiscal 2015 at 14.5%.

DSO of 44 days was stable when compared to fiscal 2015. In calculating the DSO, we subtract the deferred revenue balance from trade accounts receivable and work in progress; for that reason, the timing of payments received from outsourcing clients in advance of the work to be performed and the timing of payments related to project milestones can affect the DSO fluctuations. We remain committed to manage our DSO within our 45 day target or less.

4.6. OFF-BALANCE SHEET FINANCING AND GUARANTEES

CGI engages in the practice of off-balance sheet financing in the normal course of operations for a variety of transactions such as operating leases for office space, computer equipment and vehicles as well as accounts receivable factoring. From time to time, we also enter into agreements to provide financial or performance assurances to third parties on the sale of assets, business divestitures and guarantees on government and commercial contracts.

In connection with sales of assets and business divestitures, we may be required to pay counterparties for costs and losses incurred as the result of breaches in our contractual obligations, representations and warranties, intellectual property right infringement and litigation against counterparties, among others. While some of the agreements specify a maximum potential exposure of approximately $10.8 million, others do not specify a maximum amount or limited period. It is not possible to reasonably estimate the maximum amount that may have to be paid under such guarantees. The amounts are dependent upon the outcome of future contingent events, the nature and likelihood of which cannot be determined at this time. The Company does not expect to incur any potential payment in connection with these guarantees that could have a materially adverse effect on its audited consolidated financial statements.

In the normal course of business, we may provide certain clients, principally governmental entities, with bid and performance bonds. In general, we would only be liable for the amount of the bid bonds if we refuse to perform the project once the bid is awarded. We would also be liable for the performance bonds in the event of default in the performance of our obligations. As at September 30, 2016, we had committed a total of $30.9 million for these bonds. To the best of our knowledge, we complied with our performance obligations under all service contracts for which there was a performance or bid bond, and the ultimate

| CGI Group Inc. - Management's Discussion and Analysis for the year ended September 30, 2016 | Page | 28 |