Fomento Económico Mexicano, S.A.B. de C.V. (FMX)

Filed: 26 Feb 09, 12:00am

| FOMENTO ECONÓMICO MEXICANO, S.A. DE C.V. | |||

| By: | /s/ Javier Astaburuaga | ||

| Javier Astaburuaga | |||

| Chief Financial Officer | |||

| FEMSA Delivers Double-Digit Growth in 4Q08 and 2008 |

| Operating Income increased 15.0% in 4Q08 and 14.9% in 2008 | |

Monterrey, Mexico, February 26, 2009 — Fomento Económico Mexicano, S.A.B. de C.V. (“FEMSA”) announced today its operational and financial results for the fourth quarter and full year 2008. | |

Fourth Quarter 2008 Highlights: | |

· Consolidated total revenues grew 15.4% and income from operations grew 15.0%. In spite of the increasingly challenging economic environment and a more cautious consumer, FEMSA delivered robust growth in operating income driven by strong results at Coca-Cola FEMSA and FEMSA Comercio that more than offset the mixed results at FEMSA Cerveza. | |

· Coca-Cola FEMSA total revenues and income from operations increased 23.9% and 25.7%, respectively. Driven by double-digit income from operations growth in Mercosur and Latincentro and robust growth in Mexico. | |

· FEMSA Cerveza total revenues increased 8.6%. In an environment of healthy pricing and lapping solid 6.0% volume growth in 4Q07, sales volume decreased 0.7% in Mexico. In Brazil, volumes declined 3.5% having grown 9.3% in 4Q07, and as a result of unfavorable weather conditions. Export sales volume grew a robust 12.3%, despite the decline in the overall US import category. Continued raw material pressures and sustained marketing investments behind our brands across our operations resulted in a 9.3% decrease in income from operations. | |

· FEMSA Comercio continued its pace of strong growth and margin expansion. Income from operations increased over 27.0% for the 8th consecutive quarter, resulting in an operating margin expansion of 110 basis points to reach 9.3%. | |

2008 Full Year Highlights: | |

· Consolidated total revenues increased 13.9%. All operating units contributed to this top-line growth. | |

· Consolidated income from operations increased 14.9%, driven by double-digit growth at Coca-Cola FEMSA and FEMSA Comercio. | |

· Coca-Cola FEMSA total revenue and income from operations increased 19.8% and 19.2%, respectively. Strong growth in Mercosur, supported by the integration of Remil, and by Latincentro, as well as more tempered growth in Mexico drove these results. | |

· FEMSA Cerveza total revenues increased 7.1%, mainly as a result of increases in average price per hectoliter across our main operations in local currencies. Income from operations decreased 1.9%, reflecting continued pressure on raw materials and sustained investment in our brands. | |

· FEMSA Comercio income from operations increased 32.6%, reaching an all-time-high operating margin of 6.5% and resulting in a 100 basis point expansion. For the 7th consecutive year, income from operations increased over 25%, driven by the opening of 811 new stores during the year as well as by stable same store sales. |

| 1 | FEMSA Units consist of FEMSA BD Units and FEMSA B Units. Each FEMSA BD Unit is comprised of one Series B Share, two Series D-B Shares and two Series D-L Shares. Each FEMSA B Unit is comprised of five Series B Shares. The number of FEMSA Units outstanding as of December 31, 2008 was 3,578,226,270 equivalent to the total number of FEMSA Shares outstanding as of the same date, divided by 5. |

| 2 | As used herein, Net debt/EBITDA is calculated by dividing net debt at the end of the quarter by the EBITDA for year, as reported in Mexican pesos and converted to US dollars with the period-end exchange rate. |

CONFERENCE CALL INFORMATION: Our Fourth Quarter 2008 Conference Call will be held on: Thursday February 26, 2009, 11:00 AM Eastern Time (10:00 AM Mexico City Time). To participate in the conference call, please dial: Domestic US: (1-888) 505-4328, International: (1-719) 325-2388. The conference call will be webcast live through streaming audio. For details please visit www.femsa.com/investor. If you are unable to participate live, the conference call replay will be available through March 6, 2009; dialing Domestic US: (1-888) 203-1112, International: (1-719) 457-0820 using passcode: 4465369. Additionally, the conference call audio will be available on http://ir.femsa.com/results.cfm |

| Consolidated Income Statement |

| Millions of Pesos |

| For the fourth quarter of: | For the twelve months of: | |||||||||||||||||||||||||||||||||||||||

2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | 2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | |||||||||||||||||||||||||||||||

| Total revenues | 44,816 | 100.0 | 38,832 | 100.0 | 15.4 | 168,022 | 100.0 | 147,556 | 100.0 | 13.9 | ||||||||||||||||||||||||||||||

| Cost of sales | 23,871 | 53.3 | 20,588 | 53.0 | 15.9 | 90,399 | 53.8 | 79,739 | 54.0 | 13.4 | ||||||||||||||||||||||||||||||

| Gross profit | 20,945 | 46.7 | 18,244 | 47.0 | 14.8 | 77,623 | 46.2 | 67,817 | 46.0 | 14.5 | ||||||||||||||||||||||||||||||

| Administrative expenses | 2,444 | 5.5 | 2,317 | 6.0 | 5.5 | 9,531 | 5.7 | 9,121 | 6.2 | 4.5 | ||||||||||||||||||||||||||||||

| Selling expenses | 11,789 | 26.2 | 10,093 | 26.0 | 16.8 | 45,408 | 27.0 | 38,960 | 26.4 | 16.6 | ||||||||||||||||||||||||||||||

| Operating expenses | 14,233 | 31.7 | 12,410 | 32.0 | 14.7 | 54,939 | 32.7 | 48,081 | 32.6 | 14.3 | ||||||||||||||||||||||||||||||

| Income from operations | 6,712 | 15.0 | 5,834 | 15.0 | 15.0 | 22,684 | 13.5 | 19,736 | 13.4 | 14.9 | ||||||||||||||||||||||||||||||

| Other expenses | (792 | ) | (543 | ) | 45.9 | (2,374 | ) | (1,297 | ) | 83.0 | ||||||||||||||||||||||||||||||

| Interest expense | (1,276 | ) | (1,152 | ) | 10.8 | (4,930 | ) | (4,722 | ) | 4.4 | ||||||||||||||||||||||||||||||

| Interest income | 95 | 194 | (51.0 | ) | 598 | 769 | (22.2 | ) | ||||||||||||||||||||||||||||||||

| Interest expense, net | (1,181 | ) | (958 | ) | 23.3 | (4,332 | ) | (3,953 | ) | 9.6 | ||||||||||||||||||||||||||||||

| Foreign exchange (loss) gain | (1,898 | ) | 209 | N.S. | (1,694 | ) | 691 | N.S. | ||||||||||||||||||||||||||||||||

| (Loss) gain on monetary position | (35 | ) | 656 | N.S. | 657 | 1,640 | (59.9 | ) | ||||||||||||||||||||||||||||||||

Gain (Loss) on financial instruments (C) | (1,331 | ) | 70 | N.S. | (1,456 | ) | 69 | N.S. | ||||||||||||||||||||||||||||||||

| Integral result of financing | (4,445 | ) | (23 | ) | N.S. | (6,825 | ) | (1,553 | ) | N.S. | ||||||||||||||||||||||||||||||

| Income before income tax | 1,475 | 5,268 | (72.0 | ) | 13,485 | 16,886 | (20.1 | ) | ||||||||||||||||||||||||||||||||

| Income tax | (607 | ) | (1,661 | ) | (63.5 | ) | (4,207 | ) | (4,950 | ) | (15.0 | ) | ||||||||||||||||||||||||||||

| Net income | 868 | 3,607 | (75.9 | ) | 9,278 | 11,936 | (22.3 | ) | ||||||||||||||||||||||||||||||||

| Net majority income | 586 | 2,640 | (77.8 | ) | 6,708 | 8,511 | (21.2 | ) | ||||||||||||||||||||||||||||||||

| Net minority income | 282 | 967 | (70.8 | ) | 2,570 | 3,425 | (25.0 | ) | ||||||||||||||||||||||||||||||||

(A) Average Mexican Pesos of 2008. | ||||||||||||

(B) Constant Mexican Pesos as of Decmber 31, 2007 | ||||||||||||

(C) Includes solely derivative instruments that do not meet hedging criteria for accounting purposes |

| EBITDA & CAPEX | ||||||||||||||||||||||||||||||||||||||||

| Income from operations | 6,712 | 15.0 | 5,834 | 15.0 | 15.0 | 22,684 | 13.5 | 19,736 | 13.4 | 14.9 | ||||||||||||||||||||||||||||||

| Depreciation | 1,386 | 3.1 | 1,104 | 2.8 | 25.5 | 4,967 | 3.0 | 4,359 | 3.0 | 13.9 | ||||||||||||||||||||||||||||||

Amortization & other(5) | 933 | 2.1 | 853 | 2.3 | 9.4 | 4,031 | 2.4 | 3,708 | 2.4 | 8.7 | ||||||||||||||||||||||||||||||

| EBITDA | 9,031 | 20.2 | 7,791 | 20.1 | 15.9 | 31,682 | 18.9 | 27,803 | 18.8 | 14.0 | ||||||||||||||||||||||||||||||

| CAPEX | 5,409 | 3,915 | 38.2 | 14,234 | 11,257 | 26.4 | ||||||||||||||||||||||||||||||||||

| FINANCIAL RATIOS | 2008 | 2007 | Var. p.p. | |||||||||

Liquidity(1) | 0.89 | 1.00 | (0.11 | ) | ||||||||

Interest coverage(2) | 7.65 | 8.13 | (0.49 | ) | ||||||||

Leverage(3) | 0.91 | 0.85 | 0.06 | |||||||||

Capitalization(4) | 33.49 | % | 33.27 | % | 0.22 | |||||||

(1) Total current assets / total current liabilities. |

(2) Income from operations + depreciation + amortization & other / interest expense, net. |

(3) Total liabilities / total stockholders' equity. |

(4) Total debt / long-term debt + stockholders' equity. |

| Total debt = short-term bank loans + current maturities long-term debt + long-term bank loans |

| and notes payable. |

(5) Includes returnable bottle breakage expense. |

| FEMSA | ||||||||||||

| Consolidated Balance Sheet | ||||||||||||

| As of December 31: | ||||||||||||

| ASSETS | 2008 (A) | 2007 (B) | % Increase | |||||||||

| Cash and cash equivalents | 9,110 | 10,456 | (12.9 | ) | ||||||||

| Accounts receivable | 10,759 | 9,329 | 15.3 | |||||||||

| Inventories | 13,065 | 10,037 | 30.2 | |||||||||

| Prepaid expenses and other | 6,083 | 3,663 | 66.1 | |||||||||

| Total current assets | 39,017 | 33,485 | 16.5 | |||||||||

| Property, plant and equipment, net | 61,425 | 54,707 | 12.3 | |||||||||

Intangible assets(1) | 65,299 | 60,234 | 8.4 | |||||||||

| Other assets | 19,299 | 17,369 | 11.1 | |||||||||

| TOTAL ASSETS | 185,040 | 165,795 | 11.6 | |||||||||

| LIABILITIES & STOCKHOLDERS´ EQUITY | ||||||||||||

| Bank loans | 5,799 | 3,447 | 68.2 | |||||||||

| Current maturities long-term debt | 5,849 | 5,917 | (1.2 | ) | ||||||||

| Interest payable | 376 | 475 | (20.8 | ) | ||||||||

| Operating liabilities | 31,728 | 23,565 | 34.6 | |||||||||

| Total current liabilities | 43,752 | 33,404 | 31.0 | |||||||||

Long-term debt (2) | 31,275 | 30,664 | 2.0 | |||||||||

| Labor liabilities | 2,886 | 3,718 | (22.4 | ) | ||||||||

| Other liabilities | 10,232 | 8,356 | 22.5 | |||||||||

| Total liabilities | 88,145 | 76,142 | 15.8 | |||||||||

| Total stockholders’ equity | 96,895 | 89,653 | 8.1 | |||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | 185,040 | 165,795 | 11.6 | |||||||||

(1) Includes mainly the intangible assets generated by acquisitions. |

(A) Mexican Pesos for the end of 2008. |

(B) Constant Mexican Pesos as of Decmber 31, 2007 |

(2) Includes the effect of assigned and non assigned derivative financial instruments on long-term debt, for accountig propuses |

| December 31, 2008 | ||||||||||||

| DEBT MIX | Ps. | % Integration | Average Rate | |||||||||

| Denominated in: | ||||||||||||

| Mexican pesos | 30,377 | 70.8 | % | 9.5 | % | |||||||

| Dollars | 9,681 | 22.6 | % | 5.4 | % | |||||||

| Colombian pesos | 1,648 | 3.8 | % | 15.2 | % | |||||||

| Argentinan pesos | 789 | 1.8 | % | 19.6 | % | |||||||

| Venezuelan bolivars | 354 | 0.8 | % | 22.2 | % | |||||||

| Brazilian Reals | 74 | 0.2 | % | 14.3 | % | |||||||

| Total debt | 42,923 | 100.0 | % | 9.4 | % | |||||||

Fixed rate(1) | 23,613 | 55.0 | % | |||||||||

Variable rate(1) | 19,310 | 45.0 | % | |||||||||

| % of Total Debt | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | + | ||||||||||||||||||||

| DEBT MATURITY PROFILE | 27.0 | % | 9.1 | % | 10.3 | % | 19.6 | % | 18.3 | % | 3.2 | % | 12.5 | % | ||||||||||||||

(1) Includes the effect of interest rate swaps. |

| Coca-Cola FEMSA | ||||||||||||||||||||||||||||||||||||||||

| Results of Operations | ||||||||||||||||||||||||||||||||||||||||

| Millions of Pesos | ||||||||||||||||||||||||||||||||||||||||

| For the fourth quarter of: | For the twelve months of: | |||||||||||||||||||||||||||||||||||||||

2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | 2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | |||||||||||||||||||||||||||||||

| Total revenues | 22,752 | 100.0 | 18,361 | 100.0 | 23.9 | 82,976 | 100.0 | 69,251 | 100.0 | 19.8 | ||||||||||||||||||||||||||||||

| Cost of sales | 12,292 | 54.0 | 9,350 | 50.9 | 31.5 | 43,895 | 52.9 | 35,876 | 51.8 | 22.4 | ||||||||||||||||||||||||||||||

| Gross profit | 10,460 | 46.0 | 9,011 | 49.1 | 16.1 | 39,081 | 47.1 | 33,375 | 48.2 | 17.1 | ||||||||||||||||||||||||||||||

| Administrative expenses | 1,007 | 4.4 | 998 | 5.4 | 0.9 | 4,094 | 4.9 | 3,728 | 5.4 | 9.8 | ||||||||||||||||||||||||||||||

| Selling expenses | 5,400 | 23.8 | 4,789 | 26.1 | 12.8 | 21,292 | 25.7 | 18,161 | 26.2 | 17.2 | ||||||||||||||||||||||||||||||

| Operating expenses | 6,407 | 28.2 | 5,787 | 31.5 | 10.7 | 25,386 | 30.6 | 21,889 | 31.6 | 16.0 | ||||||||||||||||||||||||||||||

| Income from operations | 4,053 | 17.8 | 3,224 | 17.6 | 25.7 | 13,695 | 16.5 | 11,486 | 16.6 | 19.2 | ||||||||||||||||||||||||||||||

| Depreciation | 640 | 2.8 | 509 | 2.8 | 25.7 | 2,528 | 3.0 | 2,050 | 3.0 | 23.3 | ||||||||||||||||||||||||||||||

| Amortization & other | 260 | 1.1 | 190 | 1.0 | 36.8 | 893 | 1.1 | 898 | 1.2 | (0.6 | ) | |||||||||||||||||||||||||||||

| EBITDA | 4,953 | 21.7 | 3,923 | 21.4 | 26.3 | 17,116 | 20.6 | 14,434 | 20.8 | 18.6 | ||||||||||||||||||||||||||||||

| Capital expenditures | 1,938 | 0.0 | 1,297 | 0.0 | 49.4 | 4,802 | 0.0 | 3,682 | 0.0 | 30.4 | ||||||||||||||||||||||||||||||

(A) Average Mexican Pesos of 2008. |

(B) Constant Mexican Pesos as of Decmber 31, 2007 |

| Sales volumes | ||||||||||||||||||||||||||||||||||||||||

| (Millions of unit cases) | ||||||||||||||||||||||||||||||||||||||||

| Mexico | 282.9 | 47.2 | 272.2 | 48.8 | 3.9 | 1,149.0 | 51.2 | 1,110.4 | 52.4 | 3.5 | ||||||||||||||||||||||||||||||

| Latincentro | 139.9 | 23.3 | 143.6 | 25.7 | (2.6 | ) | 537.2 | 24.0 | 534.9 | 25.2 | 0.4 | |||||||||||||||||||||||||||||

| Mercosur | 177.0 | 29.5 | 142.6 | 25.5 | 24.1 | 556.6 | 24.8 | 475.5 | 22.4 | 17.1 | ||||||||||||||||||||||||||||||

| Total | 599.8 | 100.0 | 558.4 | 100.0 | 7.4 | 2,242.8 | 100.0 | 2,120.8 | 100.0 | 5.8 | ||||||||||||||||||||||||||||||

| FEMSA Cerveza | ||||||||||||||||||||||||||||||||||||||||

| Results of Operations | ||||||||||||||||||||||||||||||||||||||||

| Millions of Pesos | ||||||||||||||||||||||||||||||||||||||||

| For the fourth quarter of: | For the twelve months of: | |||||||||||||||||||||||||||||||||||||||

2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | 2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | |||||||||||||||||||||||||||||||

| Sales: | ||||||||||||||||||||||||||||||||||||||||

| Mexico | 7,808 | 67.9 | 7,147 | 67.6 | 9.2 | 29,224 | 68.9 | 27,215 | 68.8 | 7.4 | ||||||||||||||||||||||||||||||

| Brazil | 1,835 | 16.0 | 1,933 | 18.3 | (5.1 | ) | 6,182 | 14.6 | 5,903 | 14.9 | 4.7 | |||||||||||||||||||||||||||||

| Export | 942 | 8.2 | 719 | 6.7 | 31.0 | 3,608 | 8.5 | 3,339 | 8.4 | 8.1 | ||||||||||||||||||||||||||||||

| Beer sales | 10,585 | 92.1 | 9,799 | 92.6 | 8.0 | 39,014 | 92.0 | 36,457 | 92.1 | 7.0 | ||||||||||||||||||||||||||||||

| Other revenues | 907 | 7.9 | 779 | 7.4 | 16.4 | 3,371 | 8.0 | 3,109 | 7.9 | 8.4 | ||||||||||||||||||||||||||||||

| Total revenues | 11,492 | 100.0 | 10,578 | 100.0 | 8.6 | 42,385 | 100.0 | 39,566 | 100.0 | 7.1 | ||||||||||||||||||||||||||||||

| Cost of sales | 5,425 | 47.2 | 4,778 | 45.2 | 13.5 | 19,540 | 46.1 | 17,833 | 45.1 | 9.6 | ||||||||||||||||||||||||||||||

| Gross profit | 6,067 | 52.8 | 5,800 | 54.8 | 4.6 | 22,845 | 53.9 | 21,733 | 54.9 | 5.1 | ||||||||||||||||||||||||||||||

| Administrative expenses | 1,041 | 9.1 | 1,111 | 10.5 | (6.3 | ) | 4,093 | 9.7 | 4,295 | 10.9 | (4.7 | ) | ||||||||||||||||||||||||||||

| Selling expenses | 3,565 | 31.0 | 3,079 | 29.1 | 15.8 | 13,358 | 31.5 | 11,941 | 30.1 | 11.9 | ||||||||||||||||||||||||||||||

| Operating expenses | 4,606 | 40.1 | 4,190 | 39.6 | 9.9 | 17,451 | 41.2 | 16,236 | 41.0 | 7.5 | ||||||||||||||||||||||||||||||

| Income from operations | 1,461 | 12.7 | 1,610 | 15.2 | (9.3 | ) | 5,394 | 12.7 | 5,497 | 13.9 | (1.9 | ) | ||||||||||||||||||||||||||||

| Depreciation | 448 | 3.9 | 377 | 3.6 | 18.8 | 1,714 | 4.0 | 1,614 | 4.1 | 6.2 | ||||||||||||||||||||||||||||||

| Amortization & other | 635 | 5.5 | 526 | 5.0 | 20.7 | 2,539 | 6.1 | 2,320 | 5.8 | 9.4 | ||||||||||||||||||||||||||||||

| EBITDA | 2,544 | 22.1 | 2,513 | 23.8 | 1.2 | 9,647 | 22.8 | 9,431 | 23.8 | 2.3 | ||||||||||||||||||||||||||||||

| Capital expenditures | 2,168 | 1,966 | 10.3 | 6,418 | 5,373 | 19.4 | ||||||||||||||||||||||||||||||||||

(A) Average Mexican Pesos of 2008. | ||||||||||||

(B) Constant Mexican Pesos as of Decmber 31, 2007 |

| Sales volumes | ||||||||||||||||||||||||||||||||||||||||

| (Thousand hectoliters) | ||||||||||||||||||||||||||||||||||||||||

| Mexico | 7,118.1 | 64.6 | 7,169.4 | 64.6 | (0.7 | ) | 27,392.9 | 66.7 | 26,961.8 | 67.5 | 1.6 | |||||||||||||||||||||||||||||

| Brazil | 3,145.9 | 28.6 | 3,259.1 | 29.4 | (3.5 | ) | 10,180.8 | 24.8 | 9,794.8 | 24.5 | 3.9 | |||||||||||||||||||||||||||||

| Exports | 752.4 | 6.8 | 670.3 | 6.0 | 12.3 | 3,479.4 | 8.5 | 3,183.2 | 8.0 | 9.3 | ||||||||||||||||||||||||||||||

| Total | 11,016.4 | 100.0 | 11,098.8 | 100.0 | (0.7 | ) | 41,053.1 | 100.0 | 39,939.8 | 100.0 | 2.8 | |||||||||||||||||||||||||||||

| Price per hectoliter | ||||||||||||||||||||||||||||||||||||||||

| Mexico | 1,096.9 | 996.9 | 10.0 | 1,066.8 | 1,009.4 | 5.7 | ||||||||||||||||||||||||||||||||||

| Brazil | 583.3 | 593.1 | (1.7 | ) | 607.2 | 602.7 | 0.8 | |||||||||||||||||||||||||||||||||

| Exports | 1,251.9 | 1,072.7 | 16.7 | 1,037.0 | 1,048.9 | (1.1 | ) | |||||||||||||||||||||||||||||||||

| Total | 960.8 | 882.9 | 8.8 | 950.3 | 912.8 | 4.1 | ||||||||||||||||||||||||||||||||||

| Price per hectoliter (Local currency) | ||||||||||||||||||||||||||||||||||||||||

| Brazil (Real) | 102.4 | 96.8 | 5.8 | 100.2 | 98.2 | 2.0 | ||||||||||||||||||||||||||||||||||

| Exports (USD) | 96.5 | 98.3 | (1.8 | ) | 94.0 | 93.8 | 0.2 | |||||||||||||||||||||||||||||||||

| Results of Operations |

| Millions of Pesos |

| For the fourth quarter of: | For the twelve months of: | |||||||||||||||||||||||||||||||||||||||

2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | 2008 (A) | % of rev. | 2007 (B) | % of rev. | % Increase | |||||||||||||||||||||||||||||||

| Total revenues | 12,206 | 100.0 | 10,982 | 100.0 | 11.1 | 47,146 | 100.0 | 42,103 | 100.0 | 12.0 | ||||||||||||||||||||||||||||||

| Cost of sales | 8,007 | 65.6 | 7,649 | 69.7 | 4.7 | 32,565 | 69.1 | 30,301 | 72.0 | 7.5 | ||||||||||||||||||||||||||||||

| Gross profit | 4,199 | 34.4 | 3,333 | 30.3 | 26.0 | 14,581 | 30.9 | 11,802 | 28.0 | 23.5 | ||||||||||||||||||||||||||||||

| Administrative expenses | 216 | 1.8 | 196 | 1.8 | 10.2 | 833 | 1.8 | 751 | 1.8 | 10.9 | ||||||||||||||||||||||||||||||

| Selling expenses | 2,844 | 23.3 | 2,240 | 20.3 | 27.0 | 10,671 | 22.6 | 8,731 | 20.7 | 22.2 | ||||||||||||||||||||||||||||||

| Operating expenses | 3,060 | 25.1 | 2,436 | 22.1 | 25.6 | 11,504 | 24.4 | 9,482 | 22.5 | 21.3 | ||||||||||||||||||||||||||||||

| Income from operations | 1,139 | 9.3 | 897 | 8.2 | 27.0 | 3,077 | 6.5 | 2,320 | 5.5 | 32.6 | ||||||||||||||||||||||||||||||

| Depreciation | 176 | 1.4 | 145 | 1.3 | 21.4 | 663 | 1.4 | 543 | 1.3 | 22.1 | ||||||||||||||||||||||||||||||

| Amortization & other | 133 | 1.2 | 106 | 1.0 | 25.5 | 468 | 1.0 | 422 | 1.0 | 10.9 | ||||||||||||||||||||||||||||||

| EBITDA | 1,448 | 11.9 | 1,148 | 10.5 | 26.1 | 4,208 | 8.9 | 3,285 | 7.8 | 28.1 | ||||||||||||||||||||||||||||||

| Capital expenditures | 957 | 725 | 32.0 | 2,720 | 2,112 | 28.8 | ||||||||||||||||||||||||||||||||||

(A) Average Mexican Pesos of 2008. | ||||||||||||

(B) Constant Mexican Pesos as of Decmber 31, 2007 |

| Information of Convenience Stores | ||||||||||||||||||||||||

| Total stores | 6,374 | 5,563 | 14.6 | |||||||||||||||||||||

| Net new stores | 286 | 326 | (12.3 | ) | 811 | 716 | 13.3 | |||||||||||||||||

Same store data: (1) | ||||||||||||||||||||||||

| Sales (thousands of pesos) | 627.6 | 626.8 | 0.1 | 637.1 | 634.3 | 0.4 | ||||||||||||||||||

| Traffic | 24.1 | 21.5 | 12.1 | 24.4 | 21.6 | 13.0 | ||||||||||||||||||

| Ticket | 26.0 | 29.1 | (10.7 | ) | 26.1 | 29.4 | (11.2 | ) | ||||||||||||||||

(1) Monthly average information per store, considering same stores with at least 13 months of operations. |

| Macroeconomic Information | ||||||

| Exchange Rate | ||||||||||||||||||||||||

| Inflation | as of December 31, 2008 | as of December 31, 2007 | ||||||||||||||||||||||

| December 07 - | ||||||||||||||||||||||||

| 4Q 2008 | December 08 | Per USD | Per Mx. Peso | Per USD | Per Mx. Peso | |||||||||||||||||||

| Mexico | 2.53 | % | 6.52 | % | 13.54 | 1.0000 | 10.87 | 1.0000 | ||||||||||||||||

| Colombia | 1.07 | % | 7.67 | % | 2,243.59 | 0.0060 | 2,014.76 | 0.0054 | ||||||||||||||||

| Venezuela | 7.48 | % | 30.90 | % | 2.15 | 6.2969 | 2,150.00 | 0.0051 | ||||||||||||||||

| Brazil | 1.17 | % | 6.48 | % | 2.34 | 5.7929 | 1.77 | 6.1355 | ||||||||||||||||

| Argentina | 1.11 | % | 7.24 | % | 3.45 | 3.9207 | 3.15 | 3.4506 | ||||||||||||||||

| Fourth Quarter | YTD | |||||||||||||||||||||||

| 2008 | 2007 | Δ% | 2008 | 2007 | Δ% | |||||||||||||||||||

| Total Revenues | 22,752 | 18,361 | 23.9 | % | 82,976 | 69,251 | 19.8 | % | ||||||||||||||||

| Gross Profit | 10,460 | 9,011 | 16.1 | % | 39,081 | 33,375 | 17.1 | % | ||||||||||||||||

| Operating Income | 4,053 | 3,224 | 25.7 | % | 13,695 | 11,486 | 19.2 | % | ||||||||||||||||

| Majority Net Income | 585 | 1,932 | -69.7 | % | 5,598 | 6,908 | -19.0 | % | ||||||||||||||||

EBITDA(1) | 4,953 | 3,923 | 26.3 | % | 17,116 | 14,434 | 18.6 | % | ||||||||||||||||

Net Debt (2) | 12,382 | 11,374 | 8.9 | % | ||||||||||||||||||||

(3) EBITDA/ Interest Expense, net | 9.65 | 9.22 | ||||||||||||||||||||||

(3) EBITDA/ Interest Expense | 7.76 | 6.63 | ||||||||||||||||||||||

| Earnings per Share | 0.32 | 1.05 | 3.03 | 3.74 | ||||||||||||||||||||

Capitalization(4) | 26.5 | % | 29.2 | % | ||||||||||||||||||||

| Expressed in million of Mexican pesos. Figures of 2007 are expresed with purchasing power as of December 31, 2007 (1) EBITDA = Operating income + Depreciation + Amortization & Other operative Non-cash Charges. See reconciliation table on page 10 except for Earnings per Share (2) Net Debt = Total Debt - Cash (3) LTM figures (4) Total debt / (long-term debt + stockholders' equity) · Total revenues reached Ps. 22,752 million in the fourth quarter of 2008, an increase of 23.9% compared to the fourth quarter of 2007; the acquisition of Refrigerantes Minas Gerais (“Remil”) contributed approximately 35% of this growth. · Consolidated operating income grew 25.7% to Ps. 4,053 million for the fourth quarter of 2008 mainly driven by double-digit operating income growth recorded in our Mercosur and Latincentro divisions. Our operating margin reached 17.8% for the fourth quarter of 2008. · Consolidated majority net income decreased 69.7% to Ps. 585 million in the fourth quarter of 2008, mainly reflecting the devaluation of the Mexican peso as applied to our U.S. dollar-denominated debt, resulting in earnings per share of Ps. 0.32 in the fourth quarter of 2008. Mexico City (February 25, 2009), Coca-Cola FEMSA, S.A.B. de C.V. (BMV: KOFL, NYSE: KOF) (“Coca-Cola FEMSA” or the “Company”), the largest Coca-Cola bottler in Latin America and the second-largest Coca-Cola bottler in the world in terms of sales volume, announces results for the fourth quarter of 2008. "Despite of facing a challenging economic environment and pressures in our U.S. dollar-denominated raw material cost, our company delivered solid volume, revenue, and EBITDA growth for the quarter. Revenue-management and multi-segmentation strategies across our territories, combined with the acquisitions we made during the year, drove our operations’ top-and bottom-line growth. The successful integration of the Remil franchise territory in Brazil, the acquisition of the Agua de los Angeles jug water business in the Valley of Mexico and the consolidation of the Jugos del Valle line of business, specially in Mexico and Colombia, provided new avenues of growth for the company. This year, turbulent market and economic conditions present our company with the challenge of continuing to work relentlessly-without losing our focus-to achieve our goals. Our business is in a significantly better position to capture the opportunities that lie ahead in the beverage industry." said Carlos Salazar Lomelin, Chief Executive Officer of the Company. | |

| February 25, 2009 |  | Page 13 |

| February 25, 2009 | | Page 14 |

| Currency | % Total Debt(1) | % Interest Rate Floating(1)(2) | ||||||

| Mexican pesos | 34.6 | % | 79.8 | % | ||||

| U.S. dollars | 50.3 | % | 64.6 | % | ||||

| Colombian pesos | 8.9 | % | 100.0 | % | ||||

| Venezuelan bolivars | 1.9 | % | 0.0 | % | ||||

| Argentine pesos | 4.3 | % | 47.5 | % | ||||

| (1) | After giving effect to cross-currency swaps and interest rate swaps. |

| (2) | Calculated by weighting each year’s outstanding debt balance mix. |

| Maturity Date | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 + |

| % of Total Debt | 32.8% | 10.3% | 0.0% | 21.3% | 12.8/% | 22.8% |

| February 25, 2009 | | Page 15 |

| February 25, 2009 | | Page 16 |

| February 25, 2009 | | Page 17 |

| February 25, 2009 | | Page 18 |

| February 25, 2009 | | Page 19 |

| · | On January 29, 2009, Coca-Cola FEMSA successfully issued Ps. 2,000 million in 1.1 year “Certificados Bursátiles” at a yield of 28-day TIIE plus 80 basis points. The proceeds from this issuance were used to bolster existing cash reserves and complement expected free cash flow. |

| · | On February 6, 2009 – Coca-Cola FEMSA and The Coca-Cola Company received an approval from the Colombian anti-trust authorities to jointly acquire the Brisa bottled water business (including the Brisa brand and production assets) from Bavaria, a subsidiary of SABMiller. This transaction, which we expect to close soon, will enable us to increase our presence in the water business and complement our portfolio. Brisa sold 47 million unit cases in 2008 in Colombia. |

| February 25, 2009 | | Page 20 |

| Consolidated Income Statement |

Expressed in million of Mexican pesos(1), figures of 2007 are expresed with purchasing power as of December 31, 2007 |

| 4Q 08 | % Rev | 4Q 07 | % Rev | Δ% | YTD 08 | % Rev | YTD 07 | % Rev | Δ% | |||||||||||||||||||||||||||||||

Volume (million unit cases) (2) | 599.8 | 558.4 | 7.4 | % | 2,242.8 | 2,120.8 | 5.8 | % | ||||||||||||||||||||||||||||||||

Average price per unit case (2) | 36.59 | 31.94 | 14.6 | % | 35.93 | 31.95 | 12.5 | % | ||||||||||||||||||||||||||||||||

| Net revenues | 22,597 | 18,263 | 23.7 | % | 82,468 | 68,969 | 19.6 | % | ||||||||||||||||||||||||||||||||

Other operating revenues (5) | 155 | 98 | 58.2 | % | 508 | 282 | 80.1 | % | ||||||||||||||||||||||||||||||||

| Total revenues | 22,752 | 100 | % | 18,361 | 100 | % | 23.9 | % | 82,976 | 100 | % | 69,251 | 100 | % | 19.8 | % | ||||||||||||||||||||||||

| Cost of sales | 12,292 | 54.0 | % | 9,350 | 50.9 | % | 31.5 | % | 43,895 | 52.9 | % | 35,876 | 51.8 | % | 22.4 | % | ||||||||||||||||||||||||

| Gross profit | 10,460 | 46.0 | % | 9,011 | 49.1 | % | 16.1 | % | 39,081 | 47.1 | % | 33,375 | 48.2 | % | 17.1 | % | ||||||||||||||||||||||||

| Operating expenses | 6,407 | 28.2 | % | 5,787 | 31.5 | % | 10.7 | % | 25,386 | 30.6 | % | 21,889 | 31.6 | % | 16.0 | % | ||||||||||||||||||||||||

| Operating income | 4,053 | 17.8 | % | 3,224 | 17.6 | % | 25.7 | % | 13,695 | 16.5 | % | 11,486 | 16.6 | % | 19.2 | % | ||||||||||||||||||||||||

| Other expenses, net | 426 | 178 | 139.3 | % | 1,831 | 701 | 161.2 | % | ||||||||||||||||||||||||||||||||

| Interest expense | 515 | 485 | 6.2 | % | 2,207 | 2,178 | 1.3 | % | ||||||||||||||||||||||||||||||||

| Interest income | 65 | 152 | -57.2 | % | 433 | 613 | -29.4 | % | ||||||||||||||||||||||||||||||||

| Interest expense, net | 450 | 333 | 35.1 | % | 1,774 | 1,565 | 13.4 | % | ||||||||||||||||||||||||||||||||

| Foreign exchange loss (gain) | 1,501 | (27 | ) | -5659.3 | % | 1,477 | (99 | ) | -1591.9 | % | ||||||||||||||||||||||||||||||

| (Gain) on monetary position in Inflationary subsidiries | 36 | (423 | ) | -108.5 | % | (658 | ) | (1,006 | ) | -34.6 | % | |||||||||||||||||||||||||||||

| Market value loss (gain) on inefective derivative instruments | 836 | (45 | ) | -1957.8 | % | 959 | (114 | ) | -941.2 | % | ||||||||||||||||||||||||||||||

| Integral result of financing | 2,823 | (162 | ) | -1842.6 | % | 3,552 | 346 | 926.6 | % | |||||||||||||||||||||||||||||||

| Income before taxes | 804 | 3,208 | -74.9 | % | 8,312 | 10,439 | -20.4 | % | ||||||||||||||||||||||||||||||||

| Taxes | 143 | 1,228 | -88.4 | % | 2,486 | 3,336 | -25.5 | % | ||||||||||||||||||||||||||||||||

| Consolidated net income | 661 | 1,980 | -66.6 | % | 5,826 | 7,103 | -18.0 | % | ||||||||||||||||||||||||||||||||

| Majority net income | 585 | 2.6 | % | 1,932 | 10.5 | % | -69.7 | % | 5,598 | 6.7 | % | 6,908 | 10.0 | % | -19.0 | % | ||||||||||||||||||||||||

| Minority net income | 76 | 48 | 58.3 | % | 228 | 195 | 16.9 | % | ||||||||||||||||||||||||||||||||

| Operating income | 4,053 | 17.8 | % | 3,224 | 17.6 | % | 25.7 | % | 13,695 | 16.5 | % | 11,486 | 16.6 | % | 19.2 | % | ||||||||||||||||||||||||

| Depreciation | 640 | 509 | 25.7 | % | 2,528 | 2,050 | 23.3 | % | ||||||||||||||||||||||||||||||||

Amortization and other operative non-cash charges (3) | 260 | 190 | 36.8 | % | 893 | 898 | -0.6 | % | ||||||||||||||||||||||||||||||||

EBITDA (4) | 4,953 | 21.8 | % | 3,923 | 21.4 | % | 26.3 | % | 17,116 | 20.6 | % | 14,434 | 20.8 | % | 18.6 | % | ||||||||||||||||||||||||

(1) Except volume and average price per unit case figures. |

(2) Sales volume and average price per unit case exclude beer results |

(3) Includes returnable bottle breakage expense. |

(4) EBITDA = Operating Income + depreciation, amortization & other operative non-cash charges. |

(5) Since november 2007, we integrated Complejo Industrial CAN, S.A. (CICAN) a can bottling facility in Argentina. |

| Since June 2008, we integrated Minas Gerais (Remil) in Brazil. |

| February 25, 2009 | | Page 21 |

| Consolidated Balance Sheet | ||||

| Expressed in million of Mexican pesos, figures of 2007 are expresed with purchasing power as of December 31, 2007 | ||||

| Assets | Dec 08 | Dec 07 | ||||||||

| Current Assets | ||||||||||

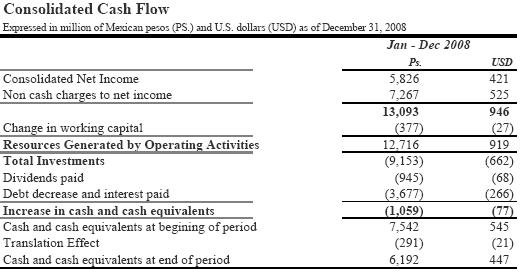

| Cash and cash equivalents | Ps. | 6,192 | Ps. | 7,542 | ||||||

| Total accounts receivable | 5,240 | 4,706 | ||||||||

| Inventories | 4,313 | 3,418 | ||||||||

| Prepaid expenses and other | 2,239 | 1,792 | ||||||||

| Total current assets | 17,984 | 17,458 | ||||||||

| Property, plant and equipment | ||||||||||

| Bottles and cases | 1,622 | 1,175 | ||||||||

| Property, plant and equipment | 50,925 | 44,140 | ||||||||

| Accumulated depreciation | (24,388 | ) | (21,682 | ) | ||||||

| Total property, plant and equipment, net | 28,159 | 23,633 | ||||||||

| Investment in shares | 1,797 | 1,476 | ||||||||

| Deferred charges, net | 1,246 | 1,255 | ||||||||

| Intangibles assets and other assets | 48,772 | 43,356 | ||||||||

| Total Assets | Ps. | 97,958 | Ps. | 87,178 | ||||||

| Liabilities and Stockholders' Equity | Dec 08 | Dec 07 | ||||||||

| Current Liabilities | ||||||||||

| Short-term bank loans and notes | Ps. | 6,119 | Ps. | 4,814 | ||||||

| Interest payable | 267 | 274 | ||||||||

| Suppliers | 7,790 | 6,100 | ||||||||

| Other current liabilities | 7,018 | 5,009 | ||||||||

| Total Current Liabilities | 21,194 | 16,197 | ||||||||

| Long-term bank loans | 12,455 | 14,102 | ||||||||

| Pension plan and seniority premium | 936 | 993 | ||||||||

| Other liabilities | 5,757 | 5,105 | ||||||||

| Total Liabilities | 40,342 | 36,397 | ||||||||

| Stockholders' Equity | ||||||||||

| Minority interest | 1,703 | 1,641 | ||||||||

| Majority interest: | ||||||||||

| Capital stock | 3,116 | 3,116 | ||||||||

| Additional paid in capital | 13,220 | 13,333 | ||||||||

| Retained earnings of prior years | 34,346 | 27,930 | ||||||||

| Net income for the period | 5,598 | 6,908 | ||||||||

| Cumulative results of holding non-monetary assets | (367 | ) | (2,147 | ) | ||||||

| Total majority interest | 55,913 | 49,140 | ||||||||

| Total stockholders' equity | 57,616 | 50,781 | ||||||||

| Total Liabilities and Equity | Ps. | 97,958 | Ps. | 87,178 | ||||||

| February 25, 2009 | | Page 22 |

| Mexico Division |

Expressed in million of Mexican pesos(1), figures of 2007 are expresed with purchasing power as of December 31, 2007 |

| 4Q 08 | % Rev | 4Q 07 | % Rev | Δ% | YTD 08 | % Rev | YTD 07 | % Rev | Δ% | |||||||||||||||||||||||||||||||

| Volume (million unit cases) | 282.9 | 272.2 | 3.9 | % | 1,149.0 | 1,110.4 | 3.5 | % | ||||||||||||||||||||||||||||||||

| Average price per unit case | 29.73 | 29.57 | 0.5 | % | 29.30 | 29.18 | 0.4 | % | ||||||||||||||||||||||||||||||||

| Net revenues | 8,411 | 8,048 | 4.5 | % | 33,665 | 32,399 | 3.9 | % | ||||||||||||||||||||||||||||||||

| Other operating revenues | 39 | 41 | -4.9 | % | 134 | 154 | -13.0 | % | ||||||||||||||||||||||||||||||||

| Total revenues | 8,450 | 100.0 | % | 8,089 | 100.0 | % | 4.5 | % | 33,799 | 100.0 | % | 32,553 | 100.0 | % | 3.8 | % | ||||||||||||||||||||||||

| Cost of sales | 4,163 | 49.3 | % | 3,734 | 46.2 | % | 11.5 | % | 16,484 | 48.8 | % | 15,547 | 47.8 | % | 6.0 | % | ||||||||||||||||||||||||

| Gross profit | 4,287 | 50.7 | % | 4,355 | 53.8 | % | -1.6 | % | 17,315 | 51.2 | % | 17,006 | 52.2 | % | 1.8 | % | ||||||||||||||||||||||||

| Operating expenses | 2,447 | 29.0 | % | 2,636 | 32.6 | % | -7.2 | % | 10,600 | 31.4 | % | 10,567 | 32.5 | % | 0.3 | % | ||||||||||||||||||||||||

| Operating income | 1,840 | 21.8 | % | 1,719 | 21.3 | % | 7.0 | % | 6,715 | 19.9 | % | 6,439 | 19.8 | % | 4.3 | % | ||||||||||||||||||||||||

Depreciation, amortization & other operative non-cash charges (2) | 446 | 5.3 | % | 358 | 4.4 | % | 24.6 | % | 1,671 | 4.9 | % | 1,621 | 5.0 | % | 3.1 | % | ||||||||||||||||||||||||

EBITDA (3) | 2,286 | 27.1 | % | 2,077 | 25.7 | % | 10.1 | % | 8,386 | 24.8 | % | 8,060 | 24.8 | % | 4.0 | % | ||||||||||||||||||||||||

(1) Except volume and average price per unit case figures. |

(2) Includes returnable bottle breakage expense. |

(3) EBITDA = Operating Income + Depreciation, amortization & other operative non-cash charges. |

| Latincentro Division |

Expressed in million of Mexican pesos(1) figures of 2007 are expresed with purchasing power as of December 31, 2007 |

| 4Q 08 | % Rev | 4Q 07 | % Rev | Δ% | YTD 08 | % Rev | YTD 07 | % Rev | Δ% | |||||||||||||||||||||||||||||||

| Volume (million unit cases) | 139.9 | 143.6 | -2.6 | % | 537.2 | 534.9 | 0.4 | % | ||||||||||||||||||||||||||||||||

| Average price per unit Case | 53.99 | 39.21 | 37.7 | % | 52.00 | 40.18 | 29.4 | % | ||||||||||||||||||||||||||||||||

| Net revenues | 7,552 | 5,631 | 34.1 | % | 27,933 | 21,491 | 30.0 | % | ||||||||||||||||||||||||||||||||

| Other operating revenues | 5 | 5 | 0.0 | % | 40 | 32 | 25.0 | % | ||||||||||||||||||||||||||||||||

| Total revenues | 7,557 | 100.0 | % | 5,636 | 100.0 | % | 34.1 | % | 27,973 | 100.0 | % | 21,523 | 100.0 | % | 30.0 | % | ||||||||||||||||||||||||

| Cost of sales | 4,437 | 58.7 | % | 3,104 | 55.1 | % | 42.9 | % | 15,622 | 55.8 | % | 11,843 | 55.0 | % | 31.9 | % | ||||||||||||||||||||||||

| Gross profit | 3,120 | 41.3 | % | 2,532 | 44.9 | % | 23.2 | % | 12,351 | 44.2 | % | 9,680 | 45.0 | % | 27.6 | % | ||||||||||||||||||||||||

| Operating expenses | 2,137 | 28.3 | % | 1,845 | 32.7 | % | 15.8 | % | 8,692 | 31.1 | % | 6,978 | 32.4 | % | 24.6 | % | ||||||||||||||||||||||||

| Operating income | 983 | 13.0 | % | 687 | 12.2 | % | 43.1 | % | 3,659 | 13.1 | % | 2,702 | 12.6 | % | 35.4 | % | ||||||||||||||||||||||||

Depreciation, amortization & other operative non-cash charges (2) | 304 | 4.0 | % | 226 | 4.0 | % | 34.5 | % | 1,092 | 3.9 | % | 886 | 4.1 | % | 23.3 | % | ||||||||||||||||||||||||

EBITDA (3) | 1,287 | 17.0 | % | 913 | 16.2 | % | 41.0 | % | 4,751 | 17.0 | % | 3,588 | 16.7 | % | 32.4 | % | ||||||||||||||||||||||||

(1) Except volume and average price per unit case figures. |

(2) Includes returnable bottle breakage expense. |

(3) EBITDA = Operating Income + Depreciation, amortization & other operative non-cash charges. |

| February 25, 2009 | | Page 23 |

| Mercosur Division | |

Expressed in million of Mexican pesos(1), figures of 2007 are expresed with purchasing power as of December 31, 2007 | |

| Financial figures include beer results | |

| 4Q 08 | % Rev | 4Q 07 | % Rev | Δ% | YTD 08 | % Rev | YTD 07 | % Rev | Δ% | |||||||||||||||||||||||||||||||

Volume (million unit cases) (2) | 177.0 | 142.6 | 24.1 | % | 556.6 | 475.5 | 17.1 | % | ||||||||||||||||||||||||||||||||

Average price per unit case (2) | 33.82 | 29.13 | 16.1 | % | 34.11 | 29.16 | 17.0 | % | ||||||||||||||||||||||||||||||||

| Net revenues | 6,634 | 4,584 | 44.7 | % | 20,870 | 15,079 | 38.4 | % | ||||||||||||||||||||||||||||||||

Other operating revenues (5) | 111 | 52 | 113.5 | % | 334 | 96 | 247.9 | % | ||||||||||||||||||||||||||||||||

| Total revenues | 6,745 | 100.0 | % | 4,636 | 100.0 | % | 45.5 | % | 21,204 | 100.0 | % | 15,175 | 100.0 | % | 39.7 | % | ||||||||||||||||||||||||

| Cost of sales | 3,692 | 54.7 | % | 2,512 | 54.2 | % | 47.0 | % | 11,789 | 55.6 | % | 8,486 | 55.9 | % | 38.9 | % | ||||||||||||||||||||||||

| Gross profit | 3,053 | 45.3 | % | 2,124 | 45.8 | % | 43.7 | % | 9,415 | 44.4 | % | 6,689 | 44.1 | % | 40.8 | % | ||||||||||||||||||||||||

| Operating expenses | 1,823 | 27.0 | % | 1,306 | 28.2 | % | 39.6 | % | 6,094 | 28.7 | % | 4,344 | 28.6 | % | 40.3 | % | ||||||||||||||||||||||||

| Operating income | 1,230 | 18.2 | % | 818 | 17.6 | % | 50.4 | % | 3,321 | 15.7 | % | 2,345 | 15.5 | % | 41.6 | % | ||||||||||||||||||||||||

Depreciation, Amortization & Other operative non-cash charges (3) | 150 | 2.2 | % | 115 | 2.5 | % | 30.4 | % | 658 | 3.1 | % | 441 | 2.9 | % | 49.2 | % | ||||||||||||||||||||||||

EBITDA (4) | 1,380 | 20.5 | % | 933 | 20.1 | % | 47.9 | % | 3,979 | 18.8 | % | 2,786 | 18.4 | % | 42.8 | % | ||||||||||||||||||||||||

(1) Except volume and average price per unit case figures. |

(2) Sales volume and average price per unit case exclude beer results |

(3) Includes returnable bottle breakage expense. |

(4) EBITDA = Operating Income + Depreciation, amortization & other operative non-cash charges. |

(5) Since november 2007, we integrated Complejo Industrial CAN, S.A. (CICAN) a can bottling facility in Argentina. |

| Since June 2008, we integrated Minas Gerais (Remil) in Brazil. |

| February 25, 2009 | | Page 24 |

| SELECTED INFORMATION |

| For the three months ended December 31, 2008 and 2007 |

| Expressed in million of Mexican pesos. Figures of 2007 are expresed with purchasing power as of December 31, 2007 |

| 4Q 08 | 4Q 07 | |||||||||||||||||||||||||||||||||||||||

| Capex | 1,937.6 | Capex | 1,297.2 | |||||||||||||||||||||||||||||||||||||

| Depreciation | 640.0 | Depreciation | 509.0 | |||||||||||||||||||||||||||||||||||||

| Amortization & Other non-cash charges | 260.0 | Amortization & Other non-cash charges | 190.0 | |||||||||||||||||||||||||||||||||||||

| VOLUME | ||||||||||||||||||||||||||||||||||||||||

| Expressed in million unit cases | ||||||||||||||||||||||||||||||||||||||||

| 4Q 08 | 4Q 07 | |||||||||||||||||||||||||||||||||||||||

| Sparkling | Water (1) | Bulk Water (2) | Still (3) | Total | Sparkling | Water (1) | Bulk Water (2) | Still (3) | Total | |||||||||||||||||||||||||||||||

| Mexico | 212.8 | 9.9 | 48.1 | 12.1 | 282.9 | 216.2 | 10.4 | 43.0 | 2.6 | 272.2 | ||||||||||||||||||||||||||||||

| Central America | 30.4 | 1.4 | - | 2.4 | 34.2 | 30.6 | 1.4 | - | 1.9 | 33.9 | ||||||||||||||||||||||||||||||

| Colombia | 47.2 | 2.4 | 2.4 | 2.6 | 54.6 | 46.4 | 2.9 | 2.6 | 0.8 | 52.7 | ||||||||||||||||||||||||||||||

| Venezuela | 46.5 | 3.0 | - | 1.6 | 51.1 | 51.8 | 3.2 | - | 2.0 | 57.0 | ||||||||||||||||||||||||||||||

| Latincentro | 124.1 | 6.7 | 2.4 | 6.6 | 139.9 | 128.8 | 7.5 | 2.6 | 4.7 | 143.6 | ||||||||||||||||||||||||||||||

| Brazil | 111.8 | 6.5 | - | 3.1 | 121.4 | 80.8 | 5.6 | - | 1.3 | 87.7 | ||||||||||||||||||||||||||||||

| Argentina | 52.5 | 0.6 | - | 2.5 | 55.6 | 52.6 | 0.7 | - | 1.6 | 54.9 | ||||||||||||||||||||||||||||||

| Mercosur | 164.3 | 7.2 | - | 5.6 | 177.0 | 133.4 | 6.3 | - | 2.9 | 142.6 | ||||||||||||||||||||||||||||||

| Total | 501.2 | 23.8 | 50.5 | 24.3 | 599.8 | 478.4 | 24.2 | 45.6 | 10.2 | 558.4 | ||||||||||||||||||||||||||||||

(1) Excludes water presentations larger than 5.0 Lt |

(2) Bulk Water = Still bottled water in 5.0, 19.0 and 20.0 - liter packaging presentations |

(3) Still Beverages include flavored water |

| · | Volume of Brazil, Mercosur division, and Consolidated for quarterly results includes tree months of Remil’s operation, accounting for 31.3 million unit cases. |

| SELECTED INFORMATION |

| For the twelve months ended December 31, 2008 and 2007 |

| Expressed in million of Mexican pesos. Figures of 2007 are expresed with purchasing power as of December 31, 2007 |

| YTD 08 | YTD 07 | |||||||||||||||||||||||||||||||||||||||

| Capex | 4,802.1 | Capex | 3,682.1 | |||||||||||||||||||||||||||||||||||||

| Depreciation | 2,528.0 | Depreciation | 2,050.0 | |||||||||||||||||||||||||||||||||||||

| Amortization & Other non-cash charges | 893.0 | Amortization & Other non-cash charges | 898.0 | |||||||||||||||||||||||||||||||||||||

| VOLUME | ||||||||||||||||||||||||||||||||||||||||

| Expressed in million unit cases | ||||||||||||||||||||||||||||||||||||||||

| YTD 08 | YTD 07 | |||||||||||||||||||||||||||||||||||||||

| CSD | Water | Jug Water | Other | Total | CSD | Water (1) | Jug Water | Other | Total | |||||||||||||||||||||||||||||||

| Mexico | 866.7 | 53.1 | 195.2 | 34.0 | 1,149.0 | 869.5 | 47.0 | 182.4 | 11.5 | 1,110.4 | ||||||||||||||||||||||||||||||

| Central America | 117.8 | 5.6 | - | 9.2 | 132.6 | 115.0 | 5.5 | - | 7.6 | 128.1 | ||||||||||||||||||||||||||||||

| Colombia | 172.4 | 9.9 | 9.8 | 5.8 | 197.9 | 173.3 | 11.0 | 10.8 | 2.7 | 197.8 | ||||||||||||||||||||||||||||||

| Venezuela | 188.7 | 11.9 | - | 6.1 | 206.7 | 189.0 | 11.8 | - | 8.2 | 209.0 | ||||||||||||||||||||||||||||||

| Latincentro | 478.9 | 27.4 | 9.8 | 21.1 | 537.2 | 477.3 | 28.3 | 10.8 | 18.5 | 534.9 | ||||||||||||||||||||||||||||||

| Brazil | 341.1 | 21.2 | - | 8.3 | 370.6 | 271.6 | 19.9 | - | 4.6 | 296.1 | ||||||||||||||||||||||||||||||

| Argentina | 176.7 | 2.4 | - | 6.9 | 186.0 | 172.6 | 1.7 | - | 5.1 | 179.4 | ||||||||||||||||||||||||||||||

| Mercosur | 517.8 | 23.6 | - | 15.2 | 556.6 | 444.2 | 21.6 | - | 9.7 | 475.5 | ||||||||||||||||||||||||||||||

| Total | 1,863.4 | 108.1 | 201.0 | 70.3 | 2,242.8 | 1,791.0 | 96.9 | 193.2 | 39.7 | 2,120.8 | ||||||||||||||||||||||||||||||

(1) Excludes water presentations larger than 5.0 Lt |

(2) Bulk Water = Still bottled water in 5.0, 19.0 and 20.0 - liter packaging presentations |

(3) Still Beverages include flavored water |

| · | Volume of Brazil, Mercosur division, and Consolidated for the twelve months results includes seven months of Remil’s operation, accounting for 66.1 million unit cases. |

| February 25, 2009 | | Page 25 |

| December 2008 |

| Macroeconomic Information |

Inflation (1) | Foreign Exchange Rate (local currency per US Dollar) (2) | |||||||||||||||

| LTM | 4Q 2008 | Dec 08 | Dec 07 | |||||||||||||

| Mexico | 6.52 | % | 2.53 | % | 13.5383 | 10.8662 | ||||||||||

| Colombia | 7.67 | % | 1.07 | % | 2,243.59 | 2,014.76 | ||||||||||

Venezuela (3) | 30.90 | % | 7.48 | % | 2.1500 | 2,150 | ||||||||||

| Brazil | 6.48 | % | 1.17 | % | 2.3370 | 1.7713 | ||||||||||

| Argentina | 7.24 | % | 1.11 | % | 3.4530 | 3.1490 | ||||||||||

(1) Source: Mexican inflation is published by Banco de México (Mexican Central Bank). |

(2) Exchange rates at the end of period are the official exchange rates published by the Central Bank of each country. |

(3) In Venezuela since January 1, 2008, the local currency is 'Bolivar Fuerte', 'Bolivar' the former currency, was divided by one thousand. |

| February 25, 2009 | | Page 26 |