Exhibit 99.1

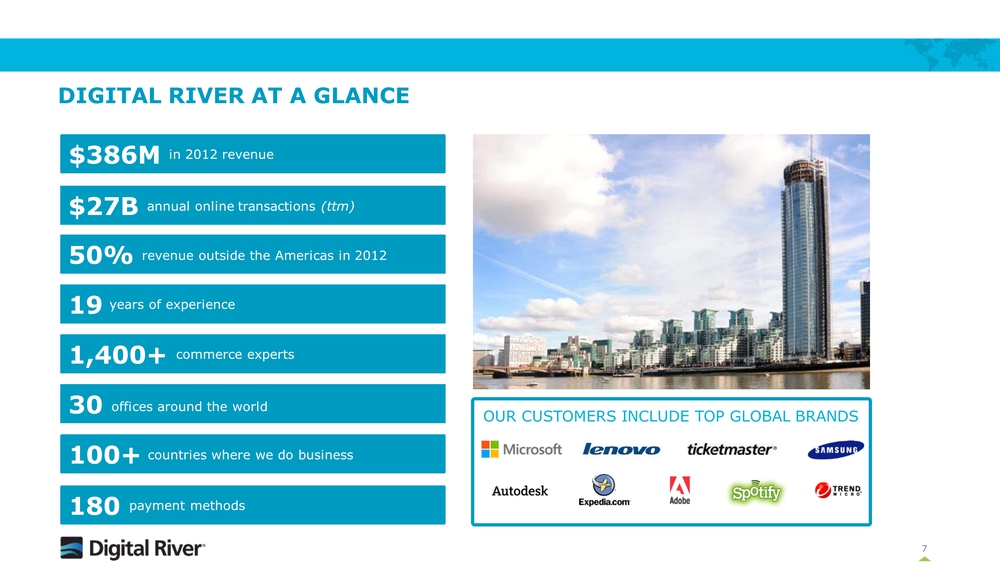

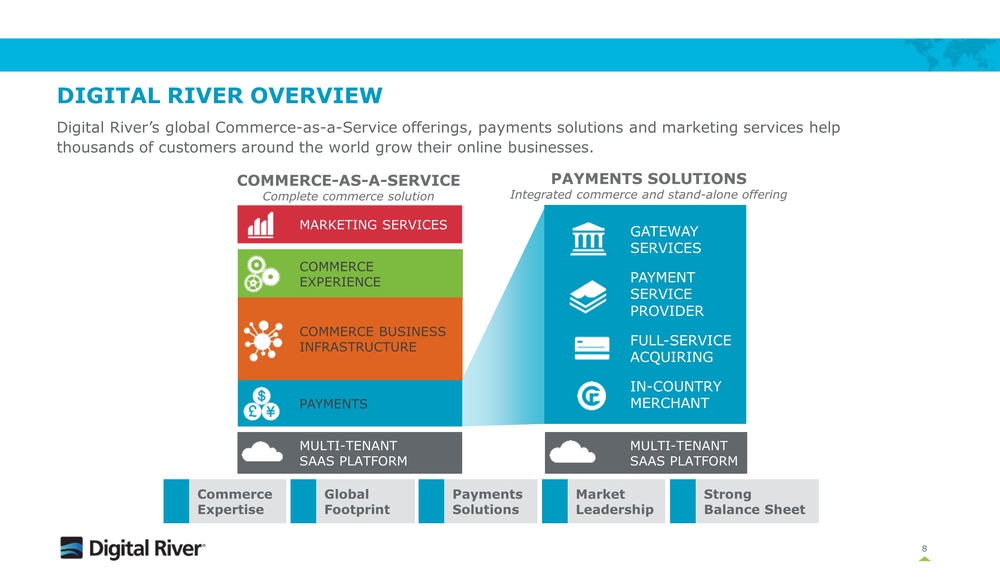

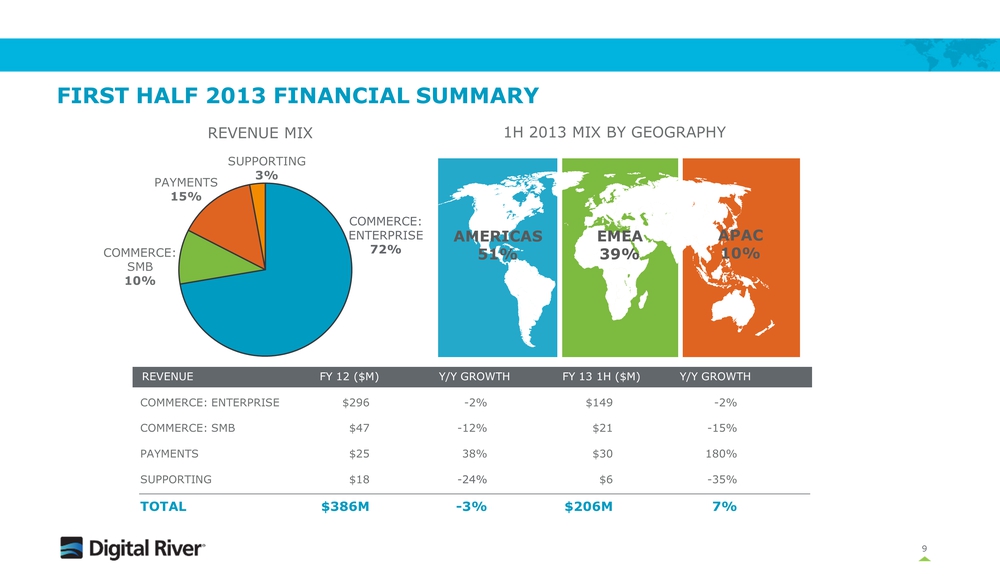

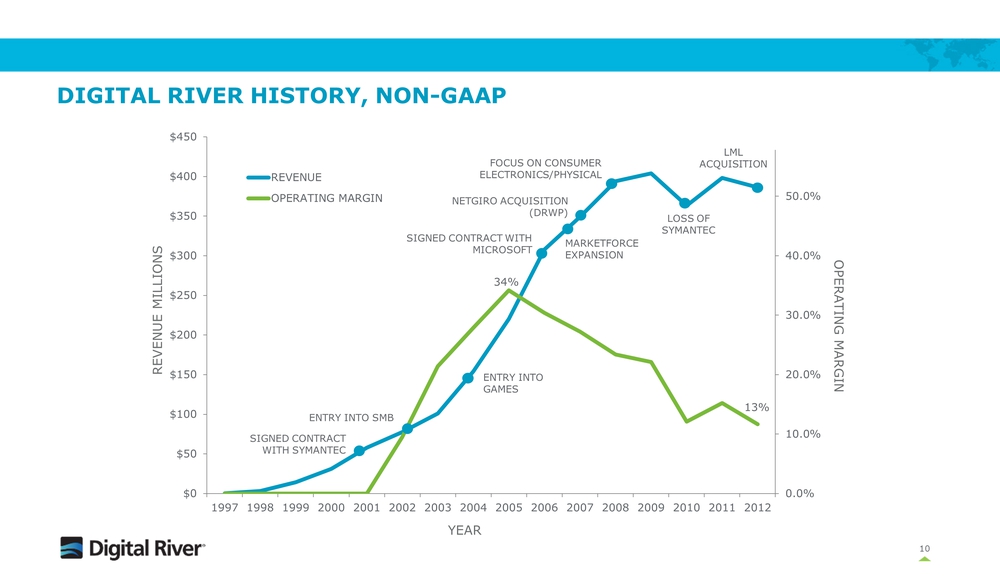

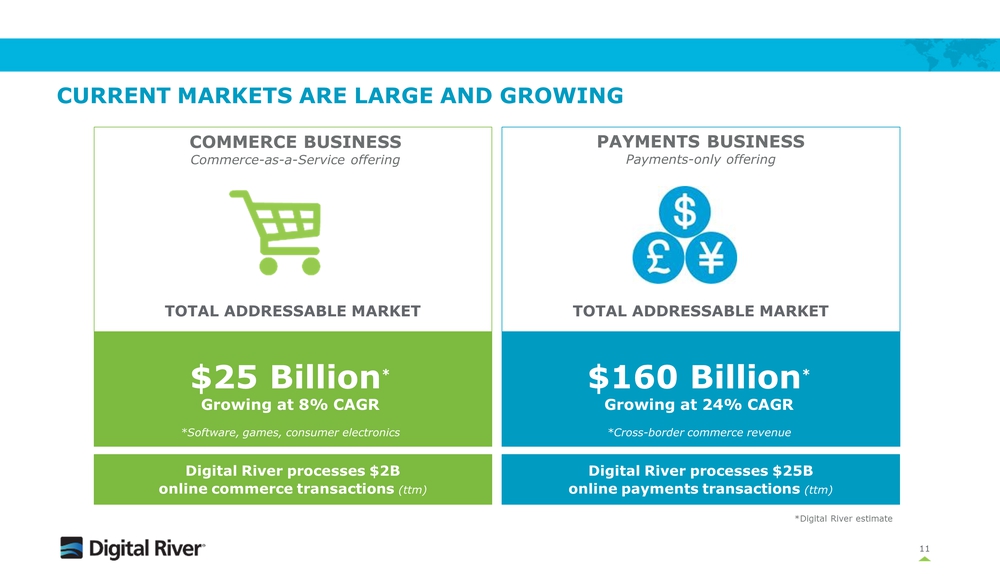

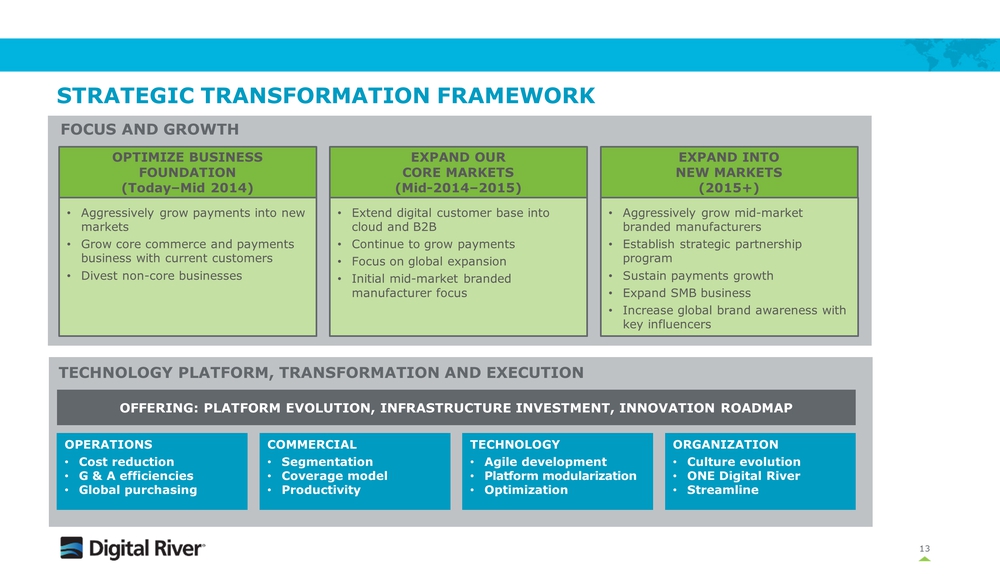

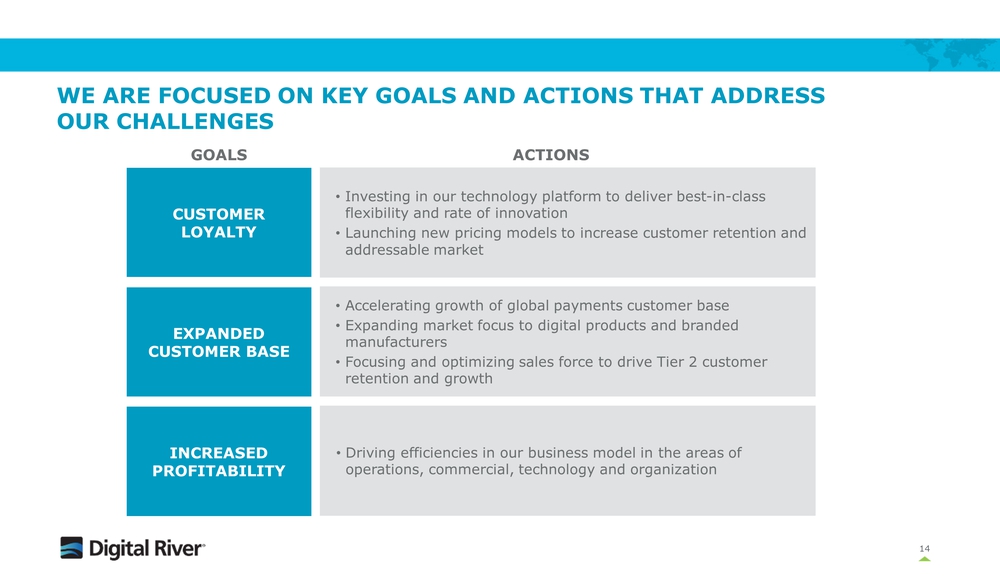

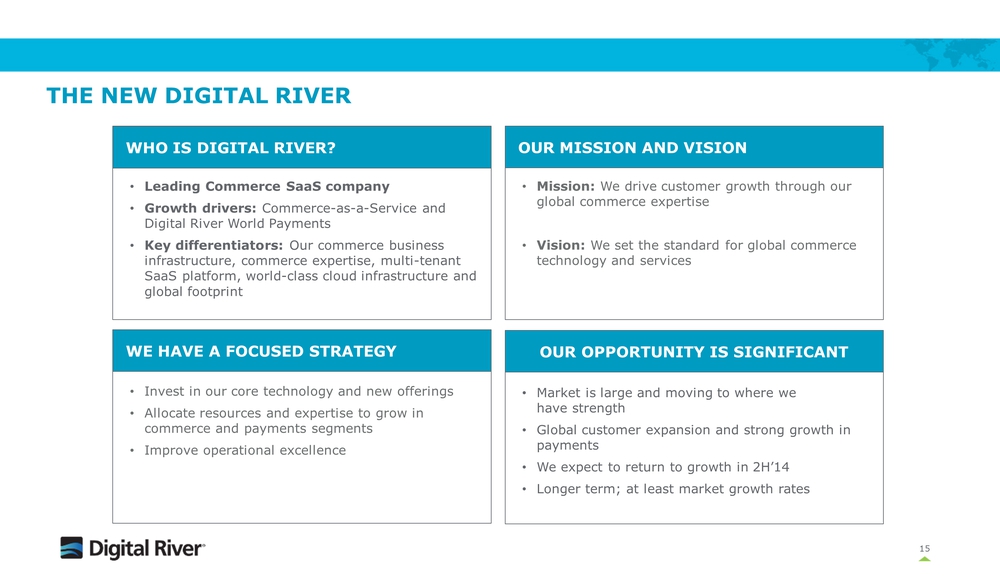

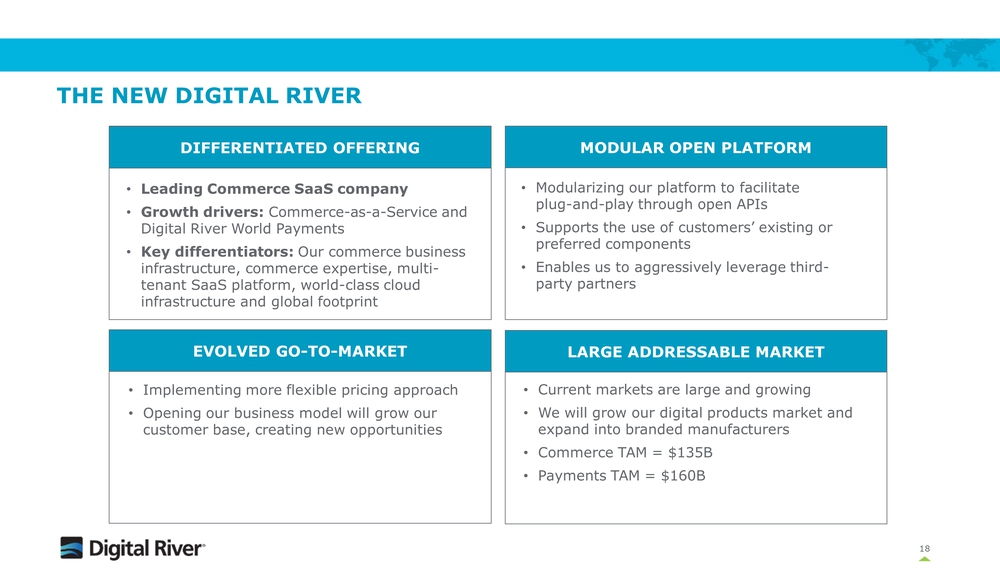

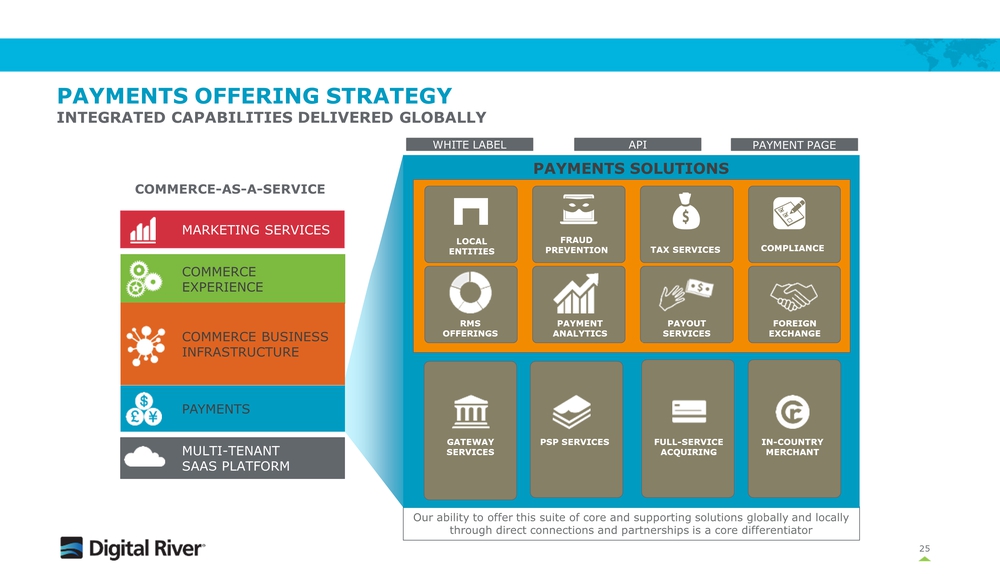

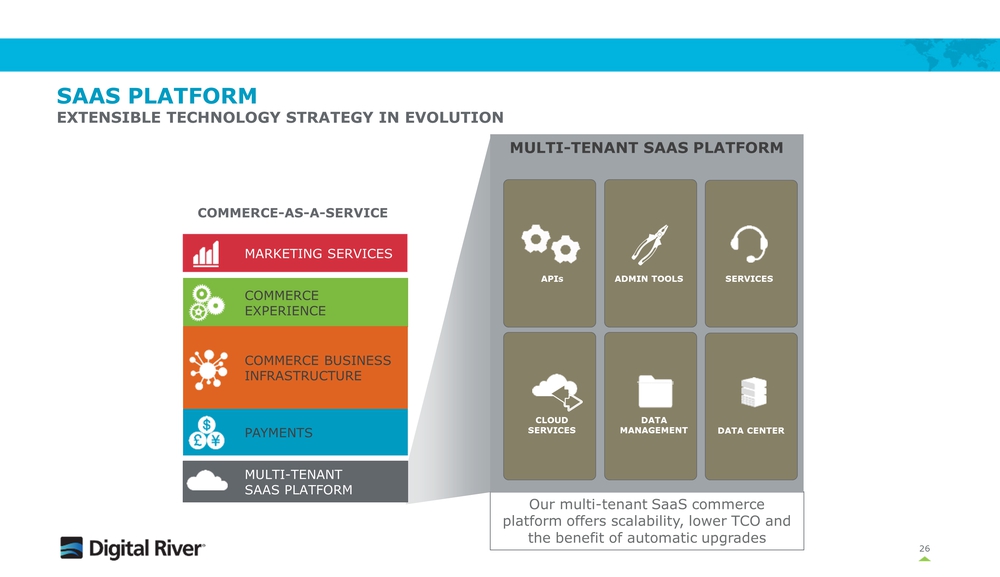

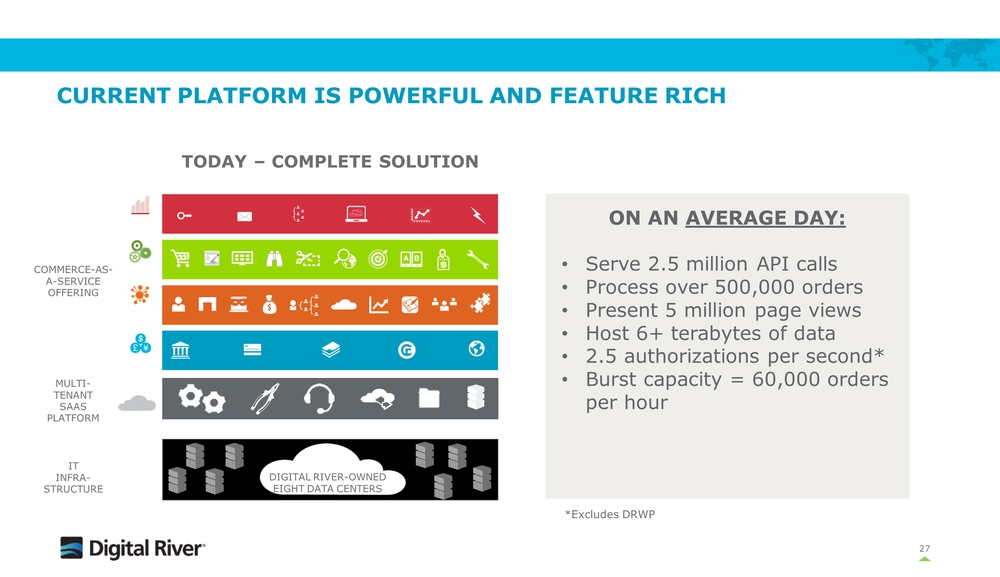

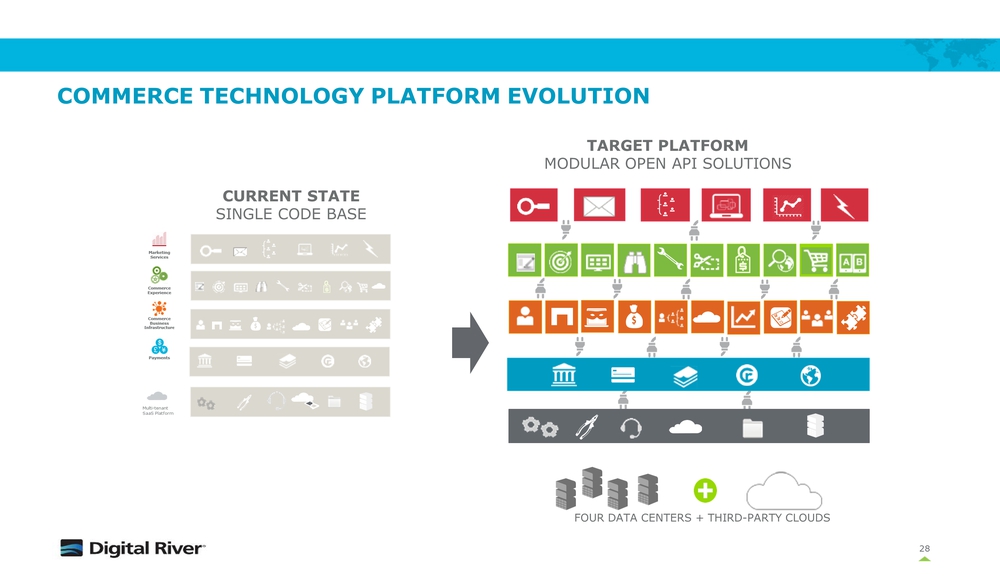

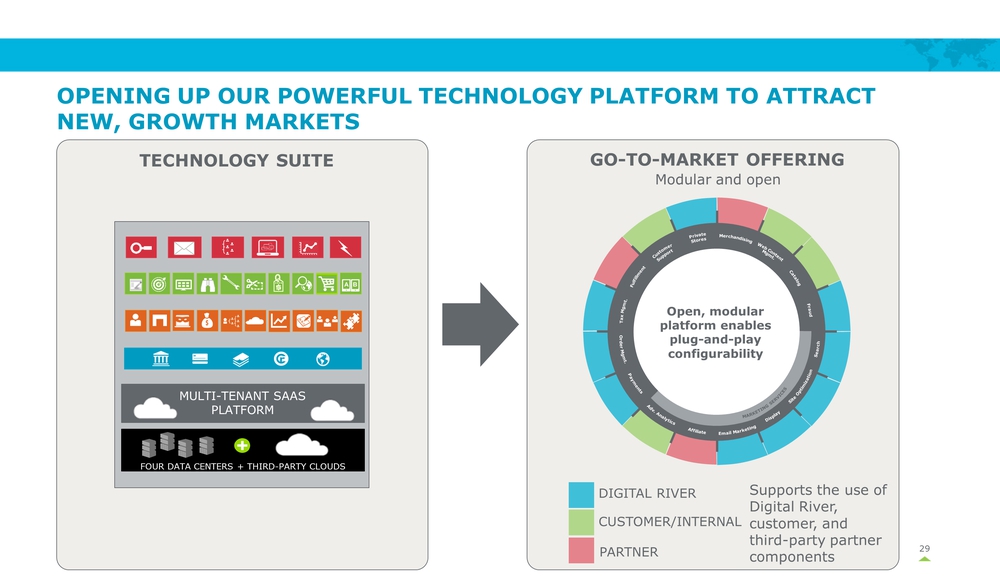

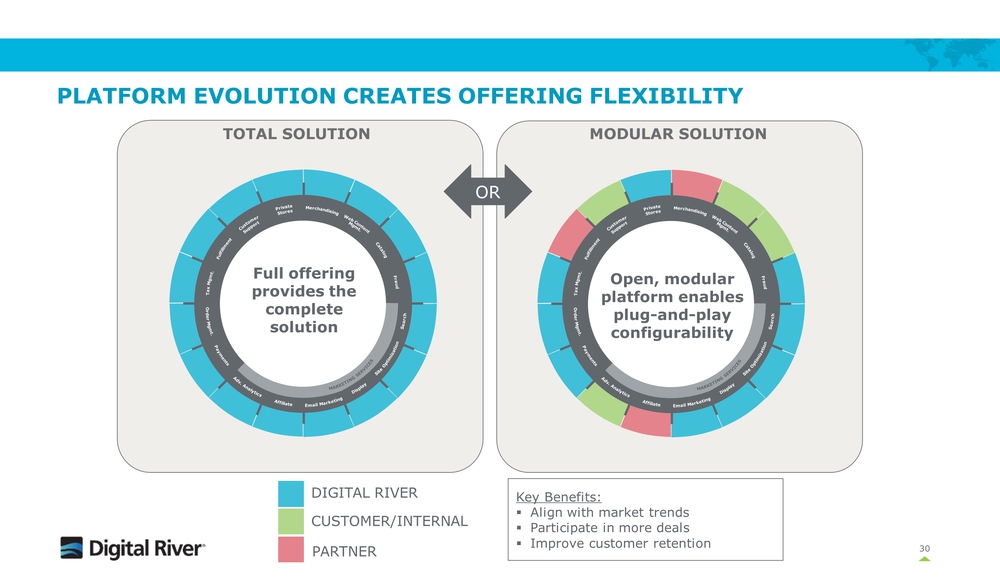

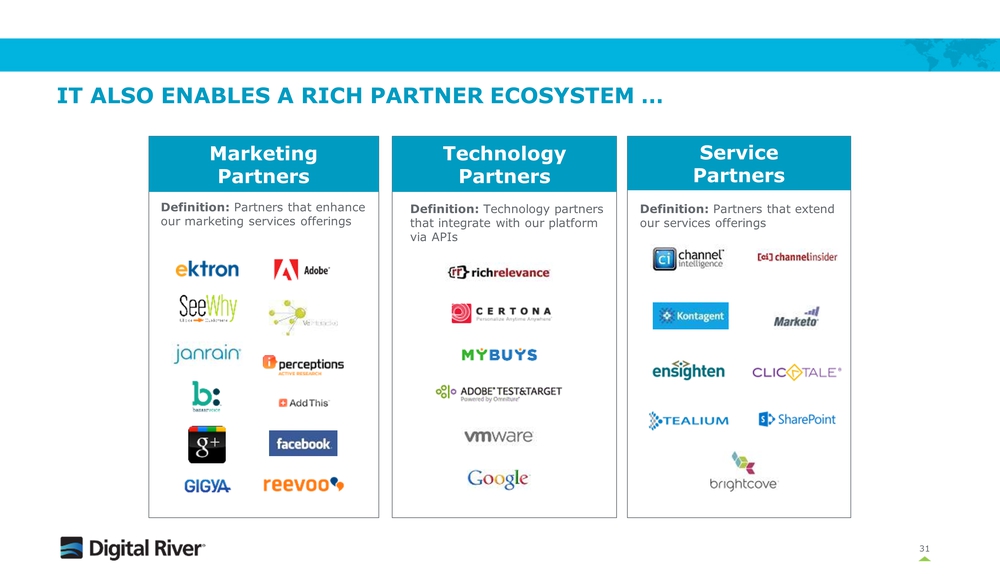

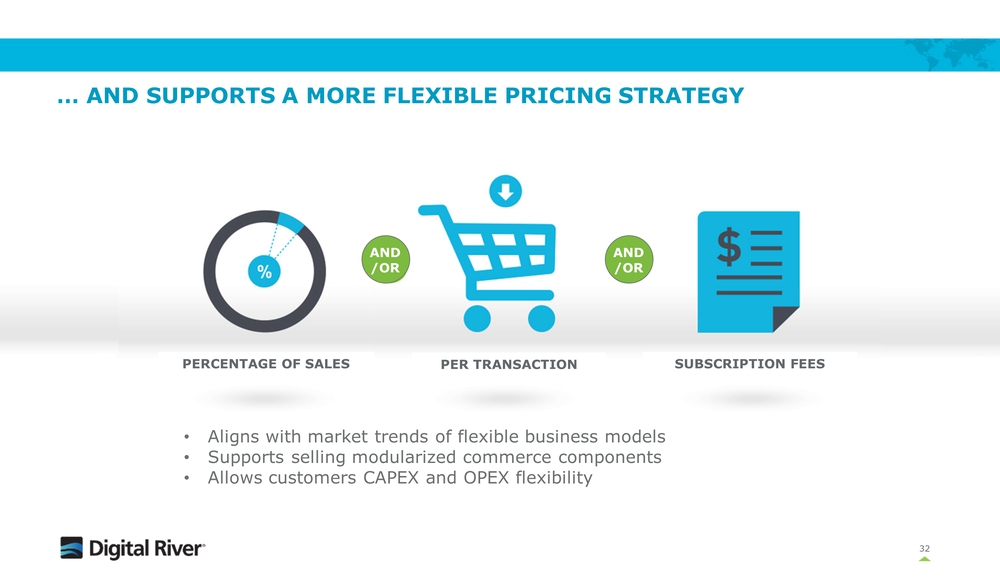

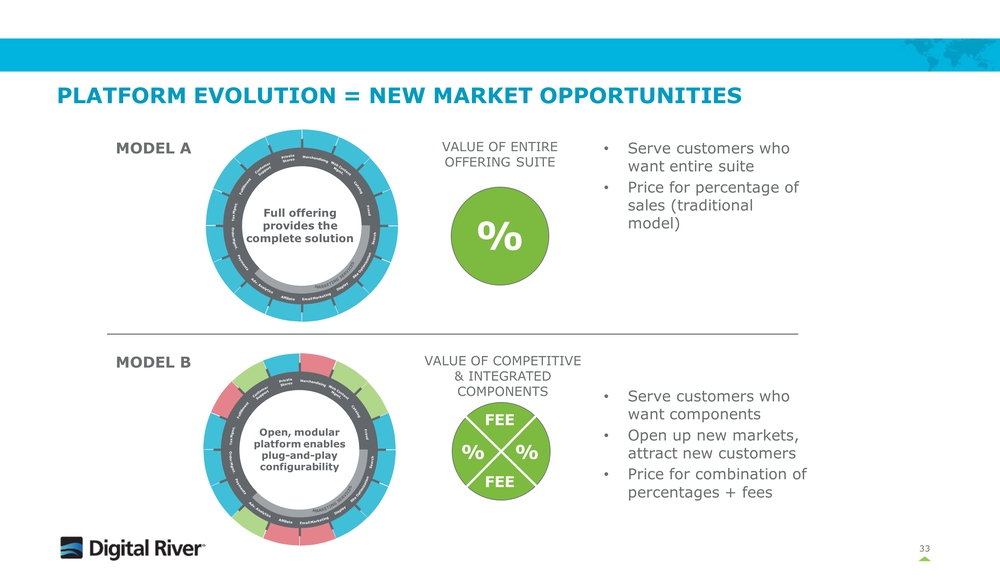

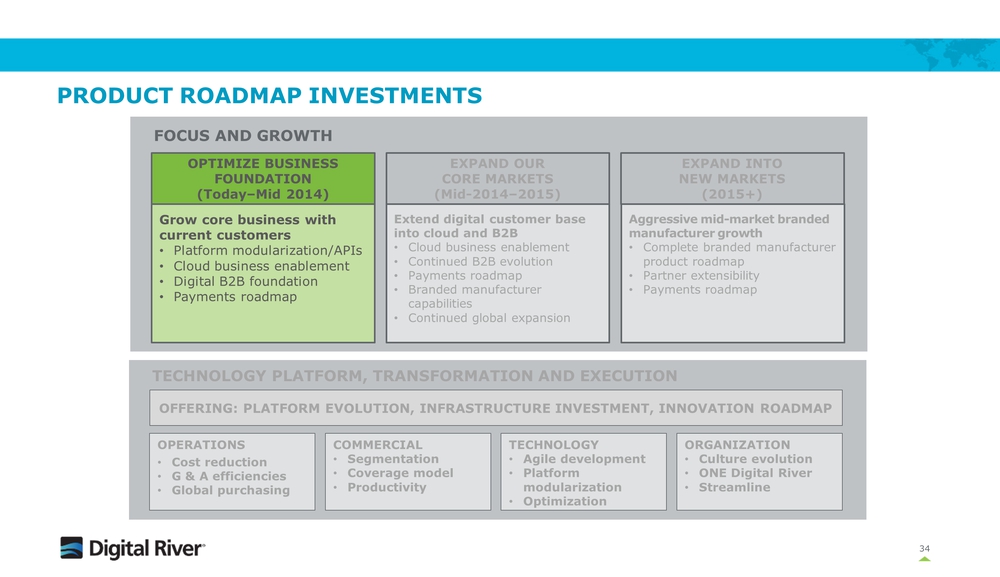

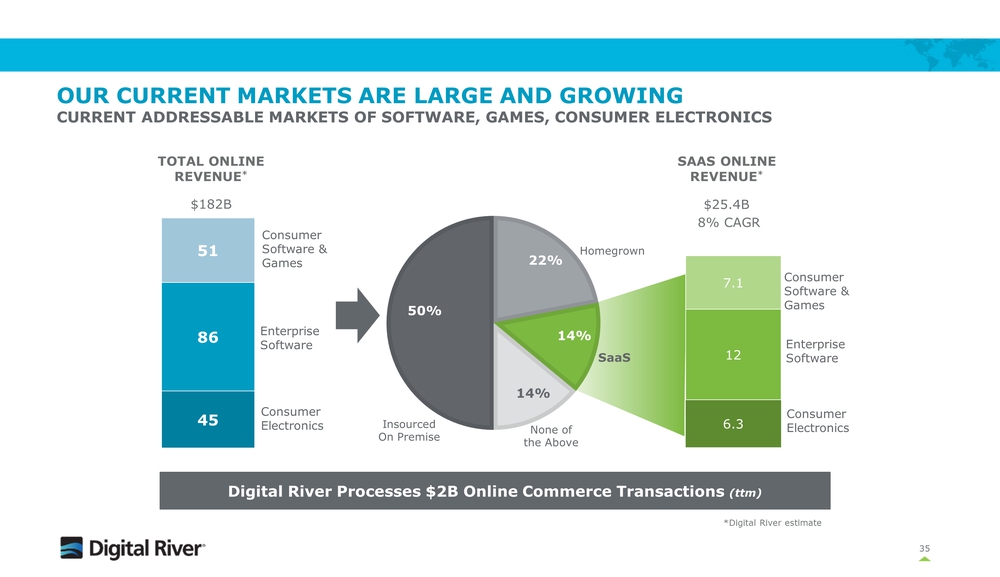

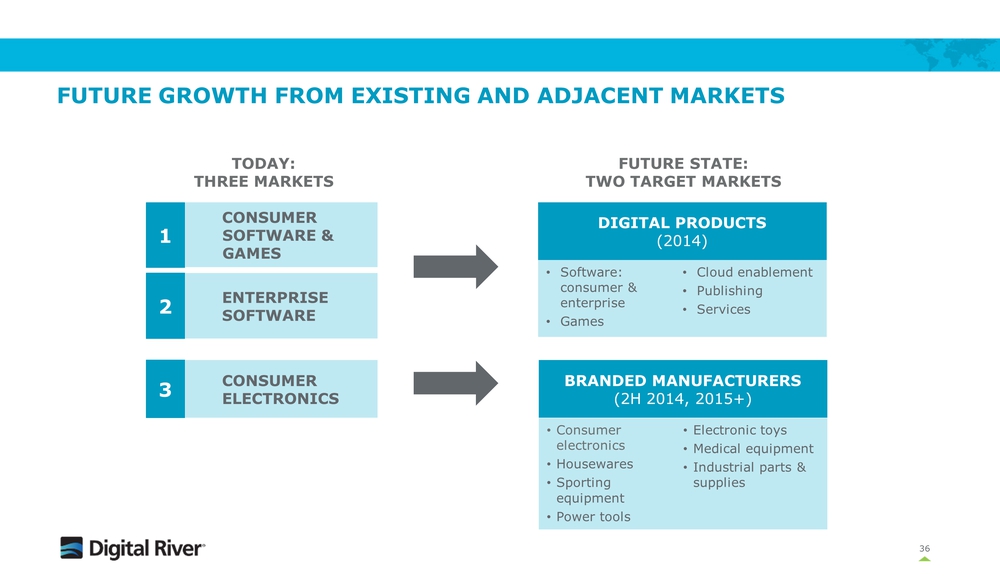

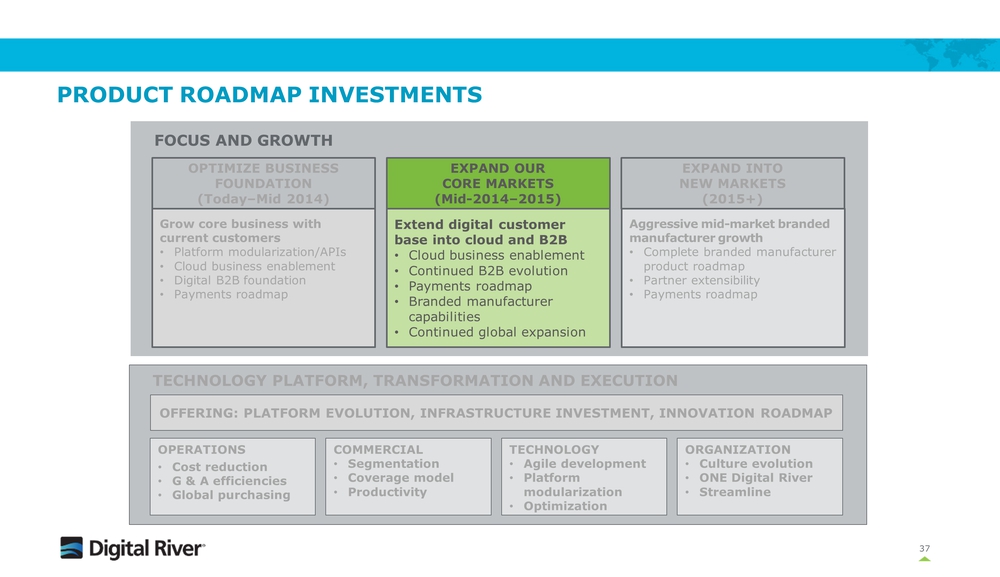

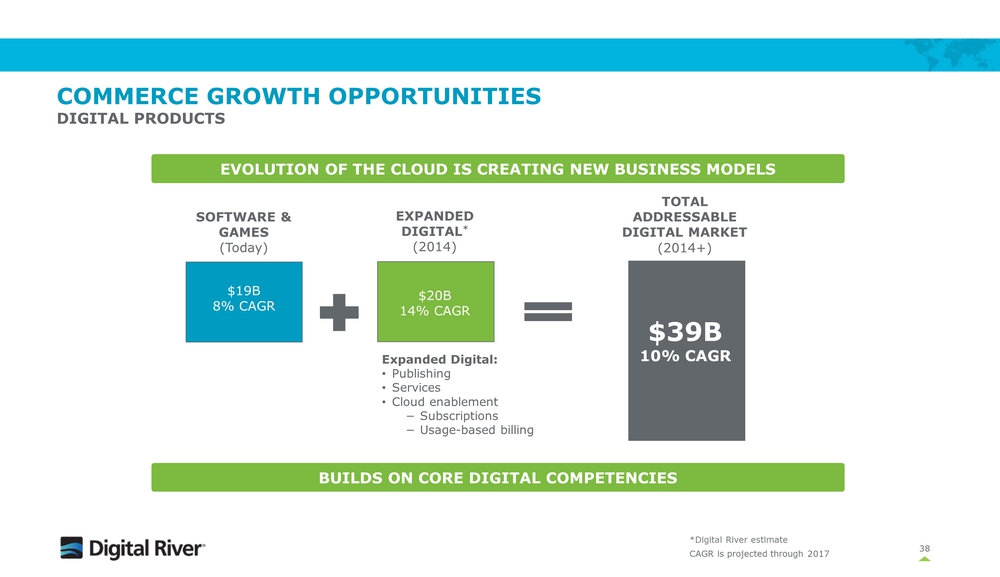

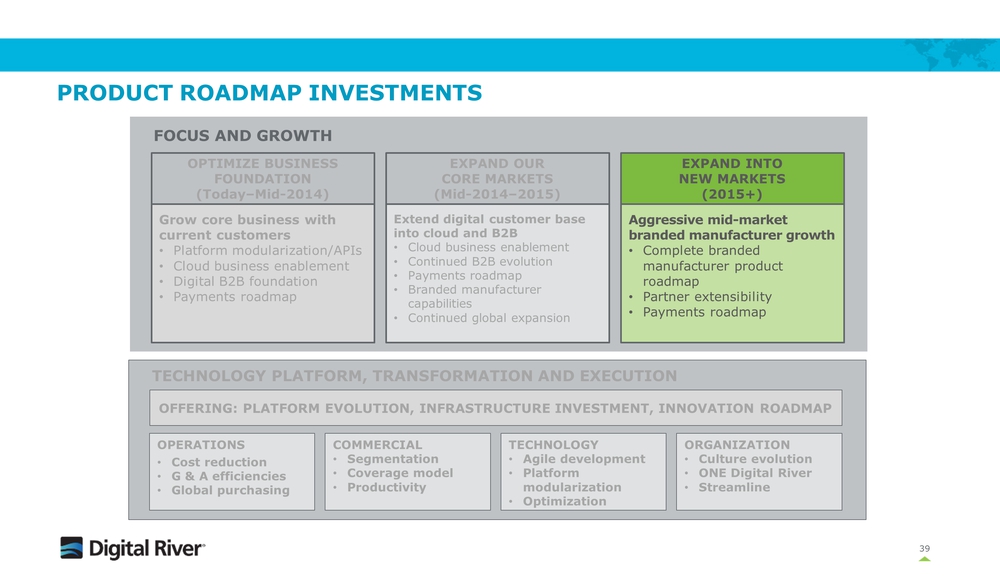

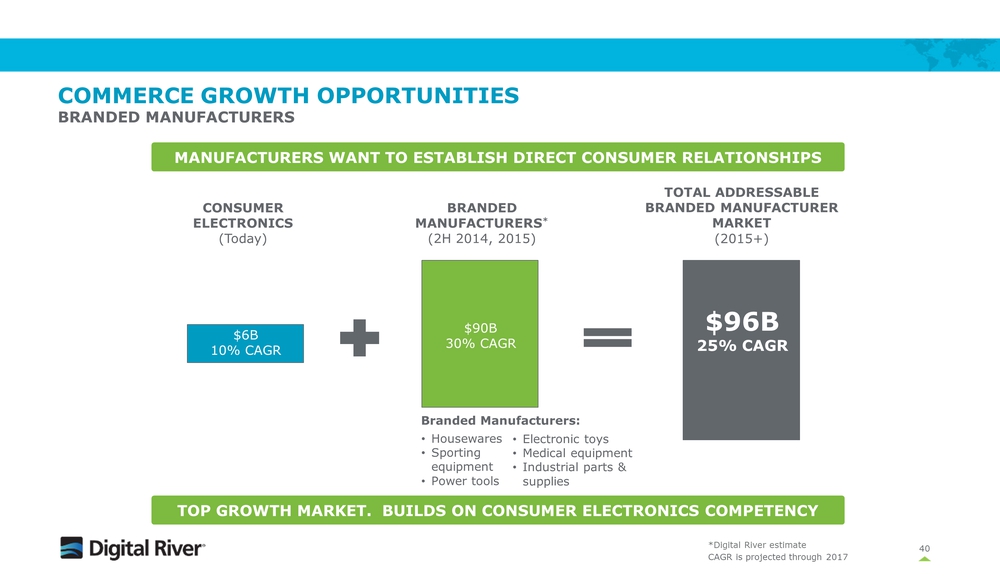

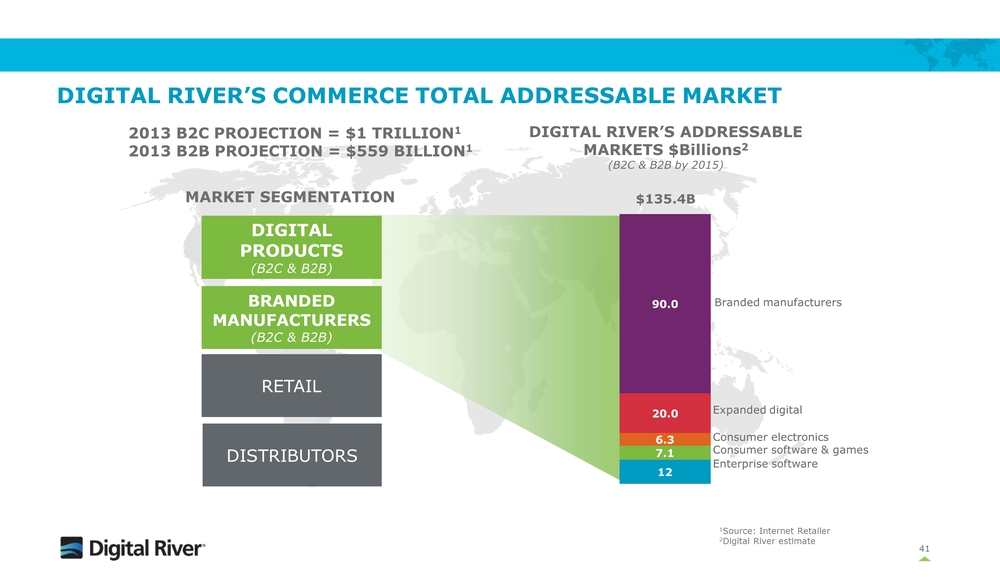

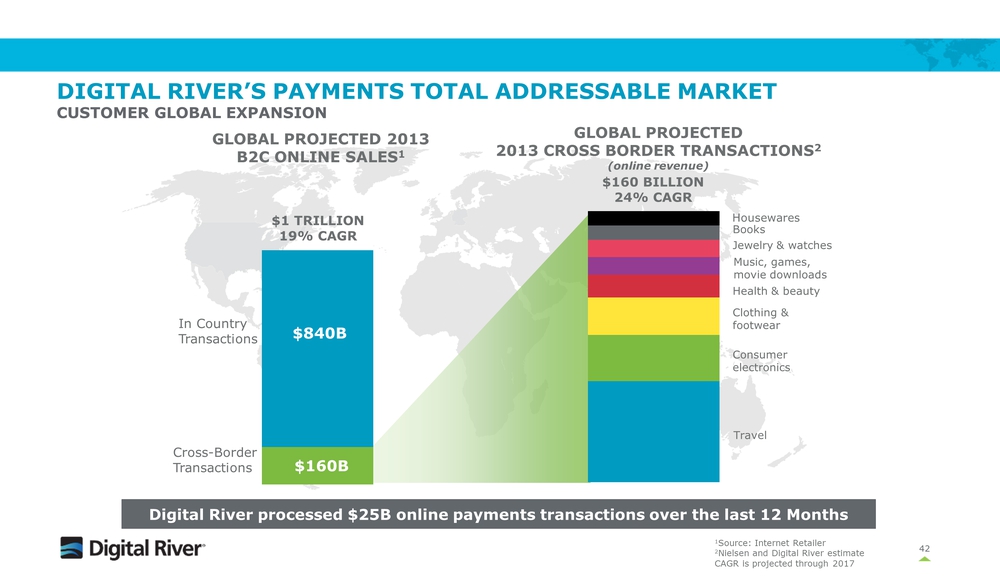

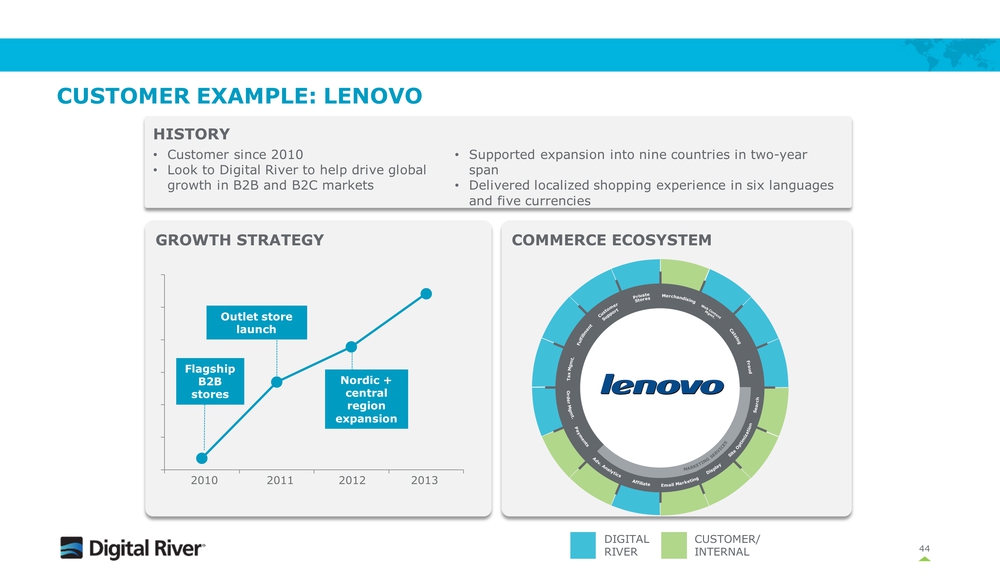

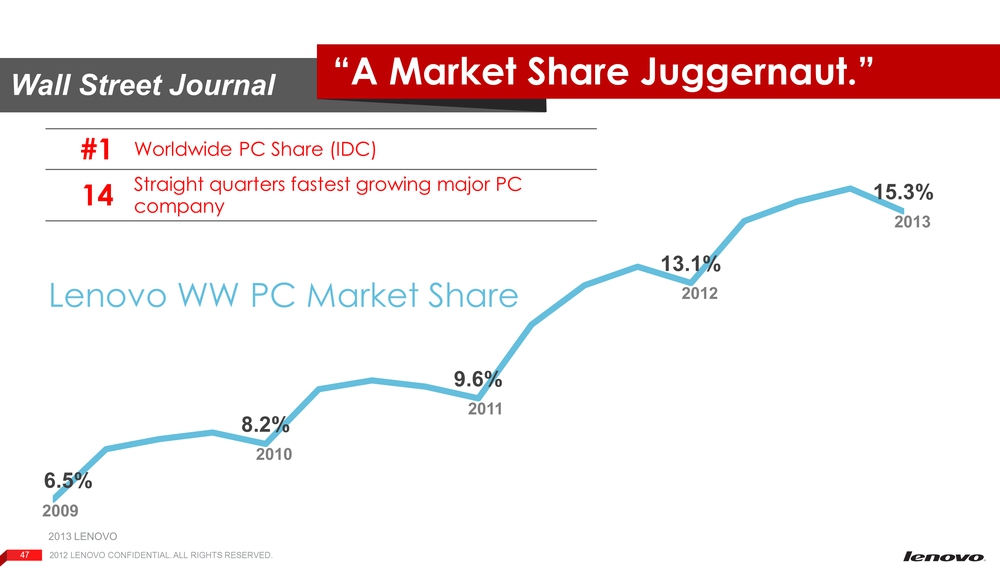

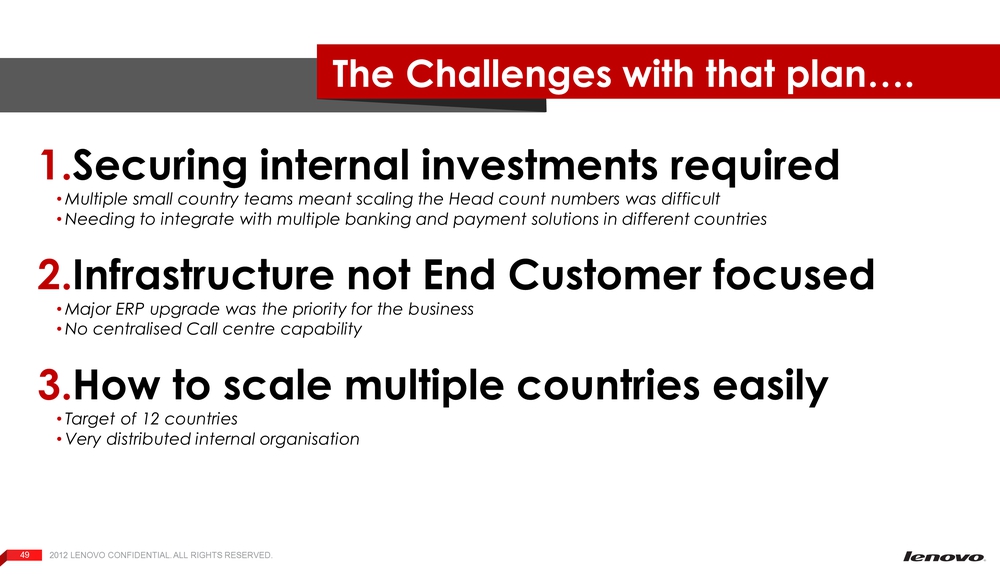

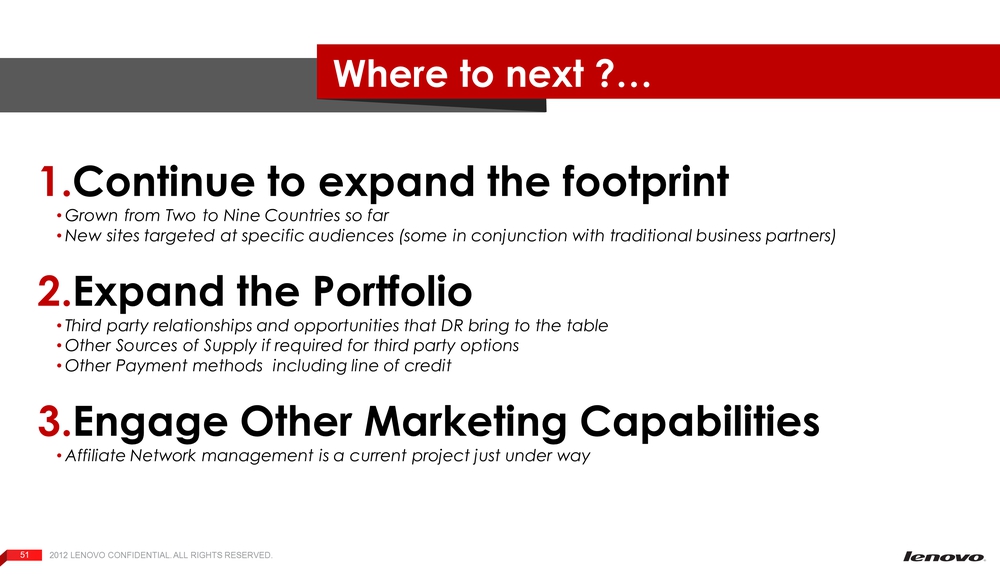

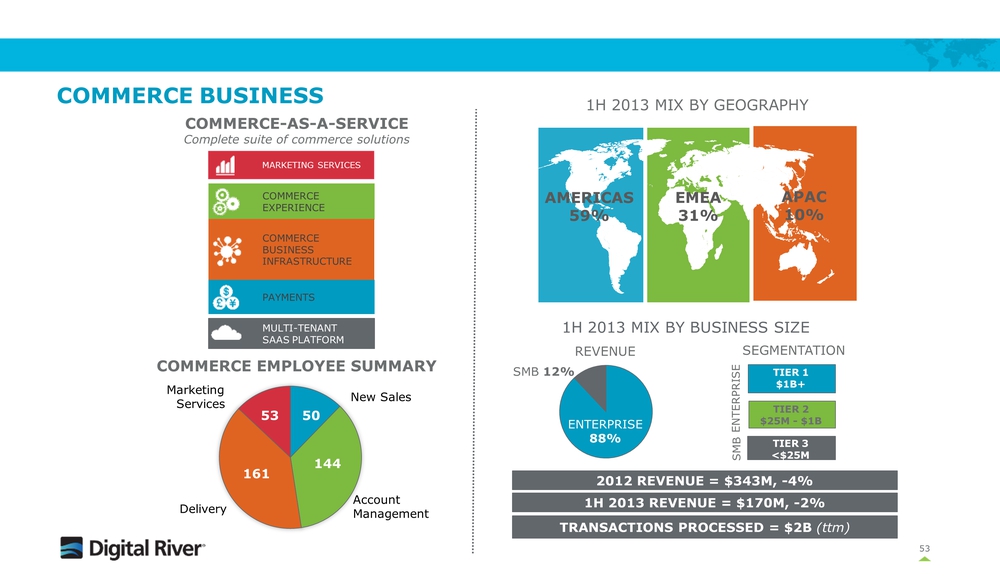

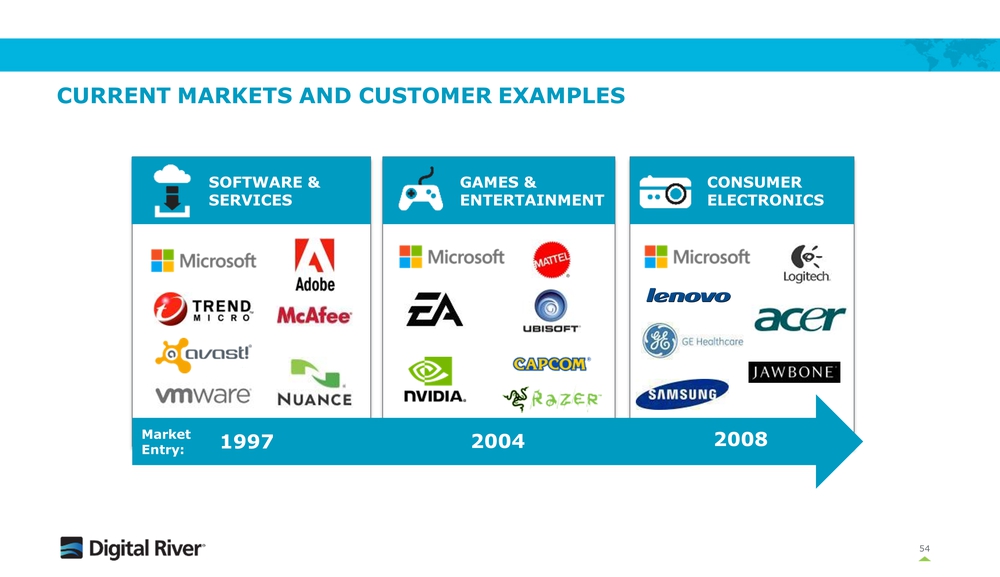

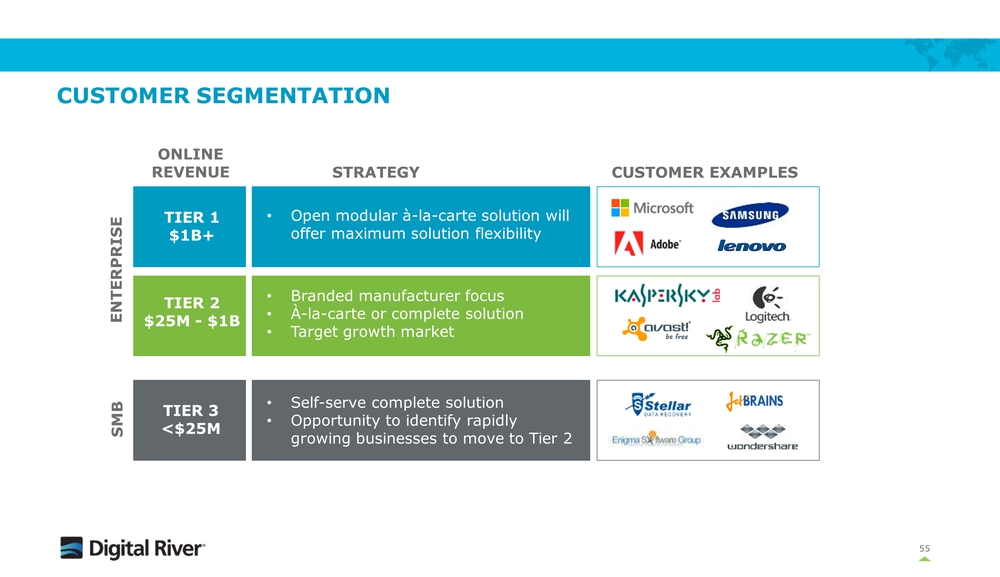

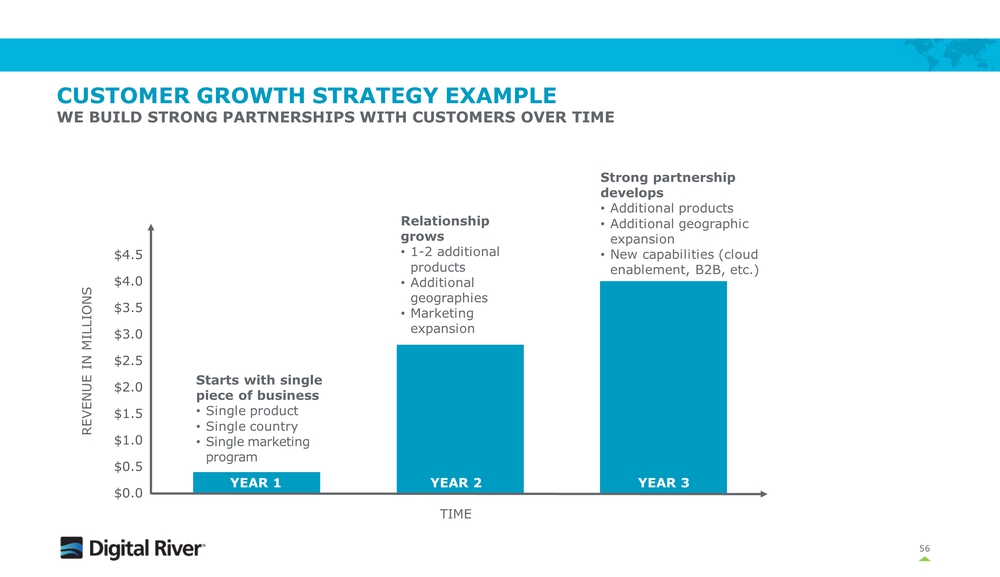

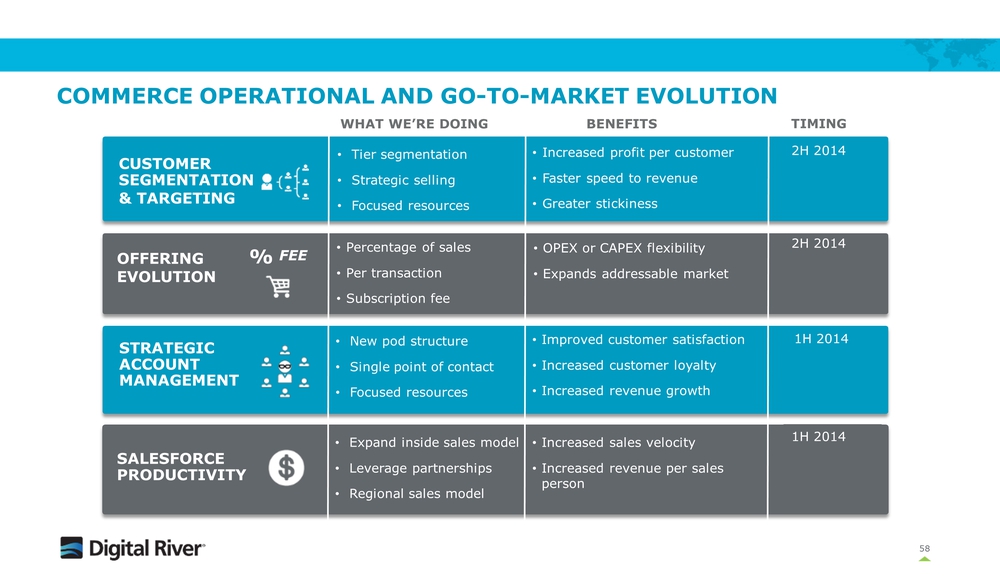

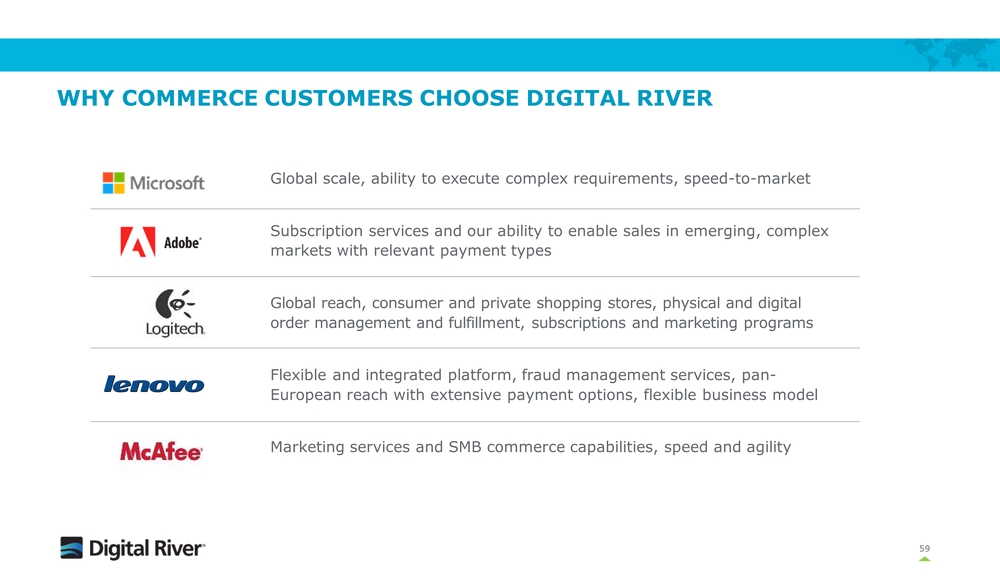

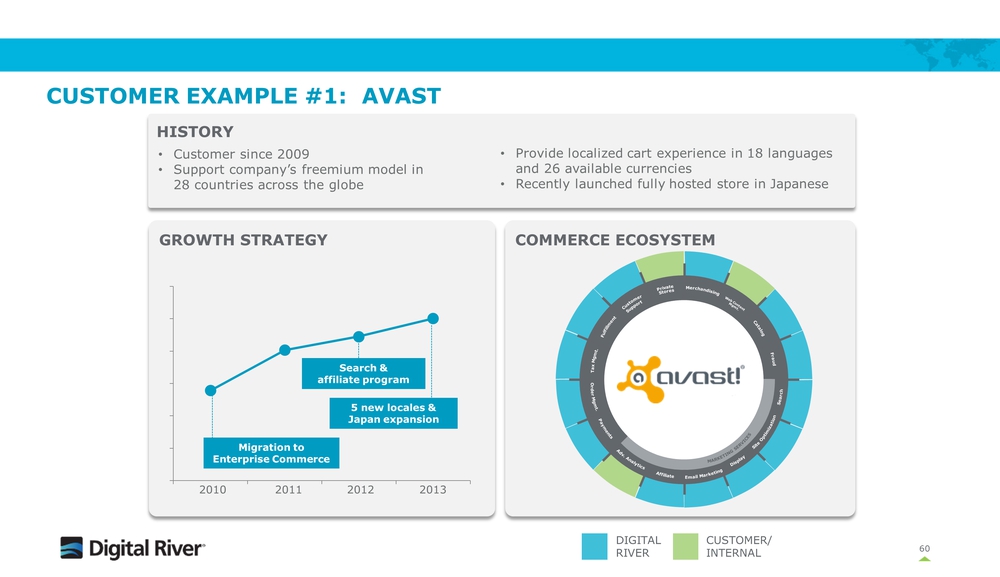

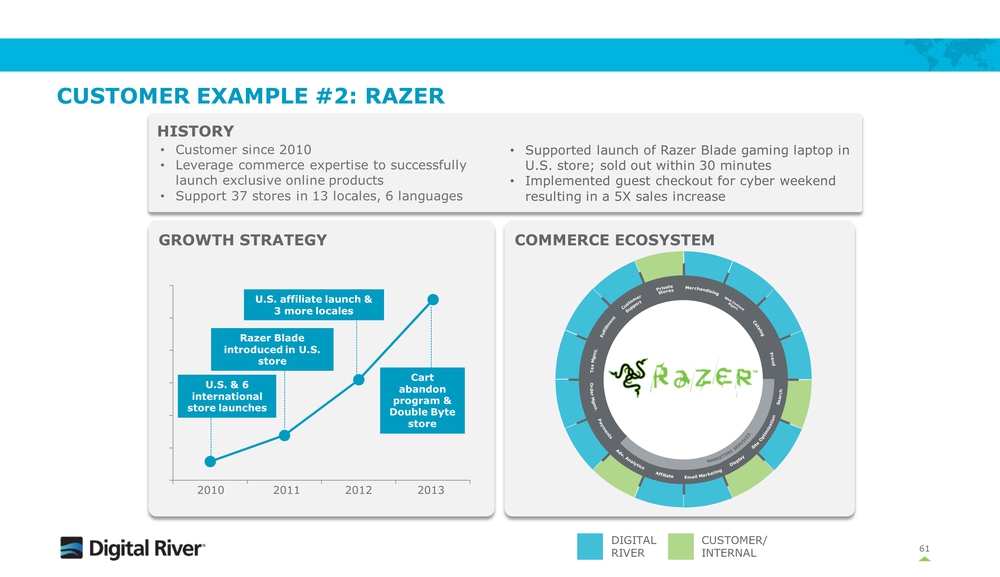

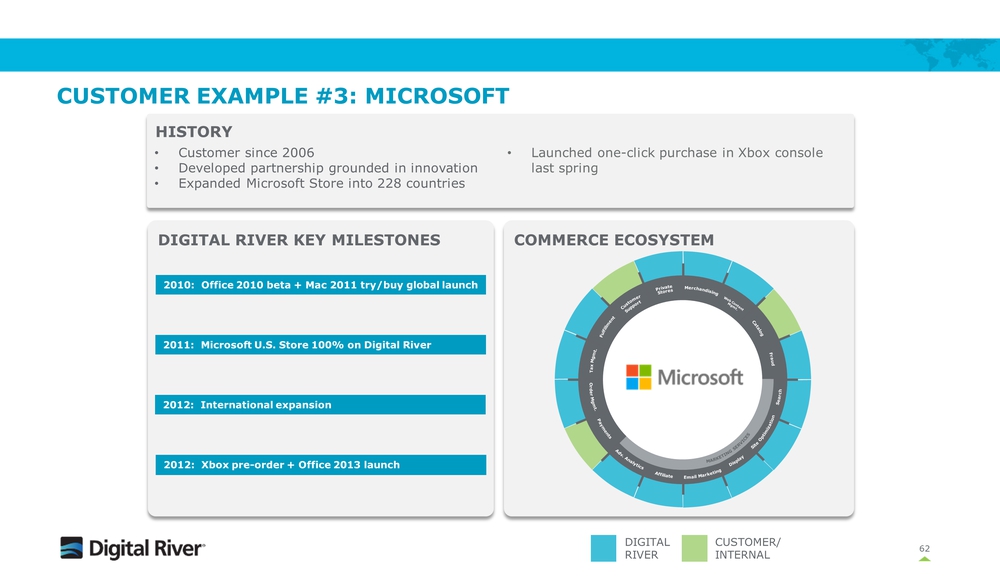

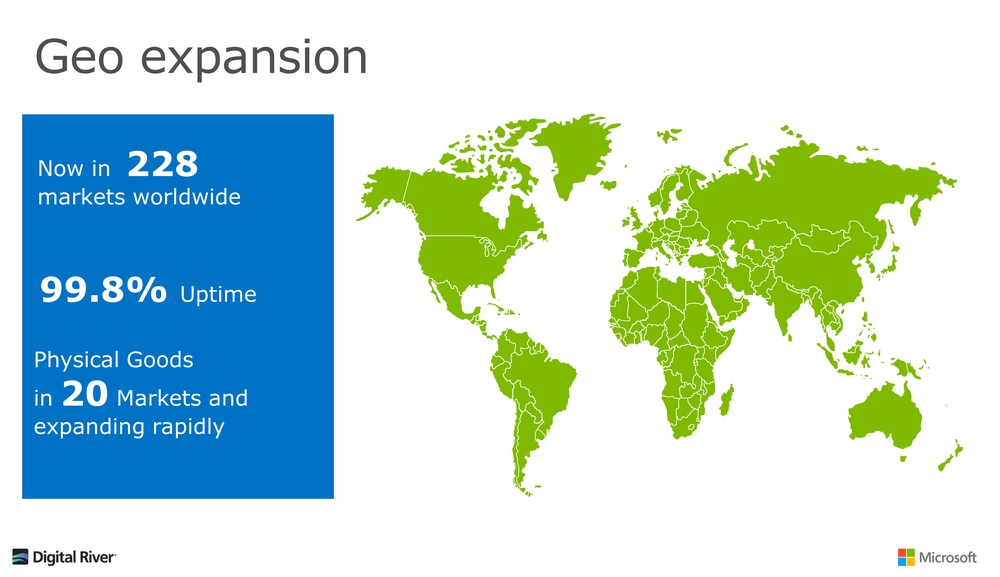

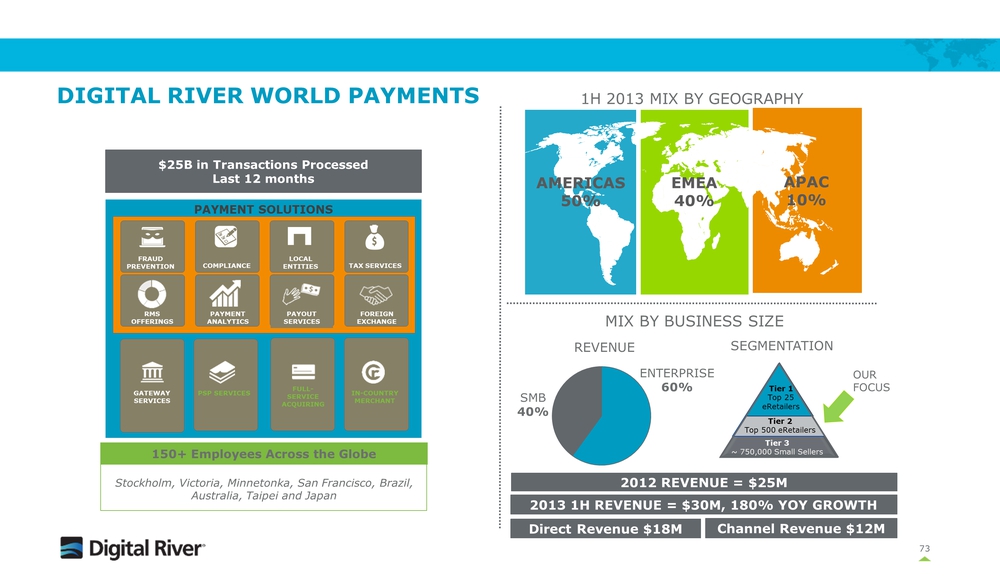

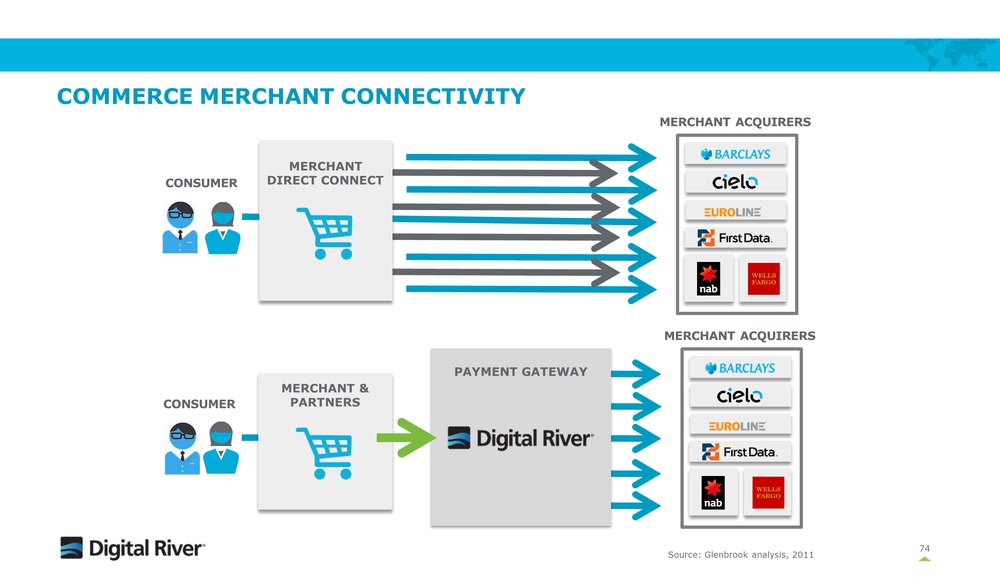

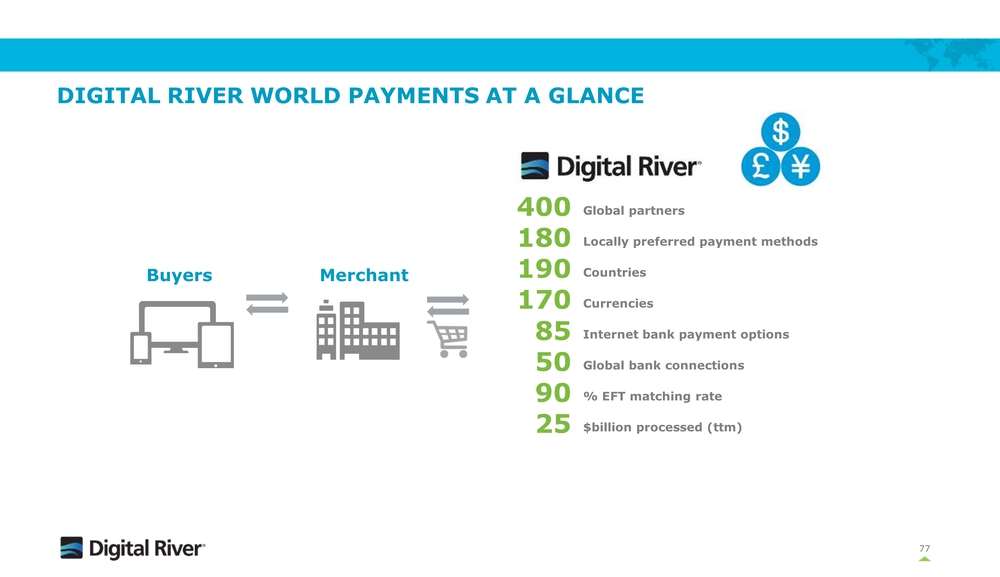

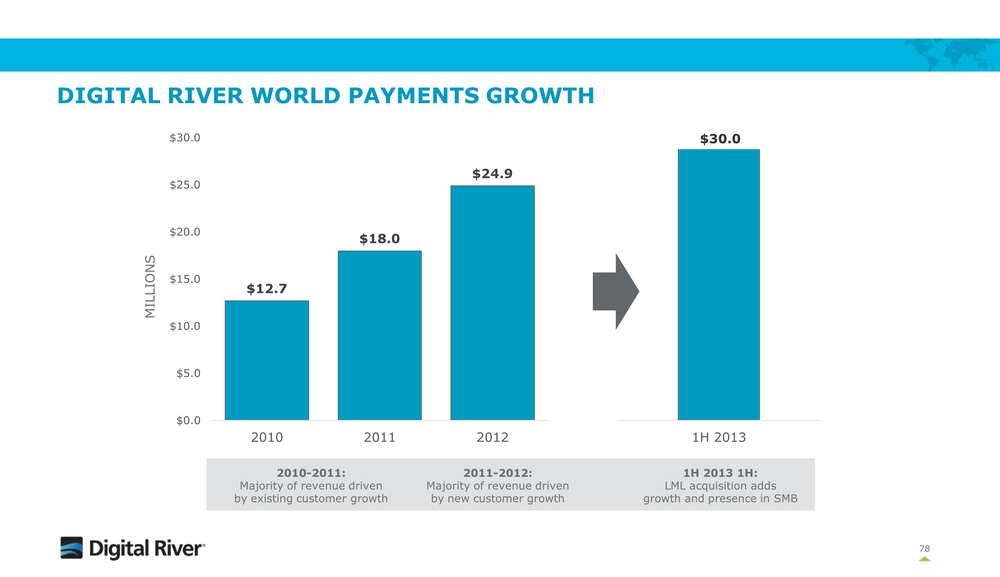

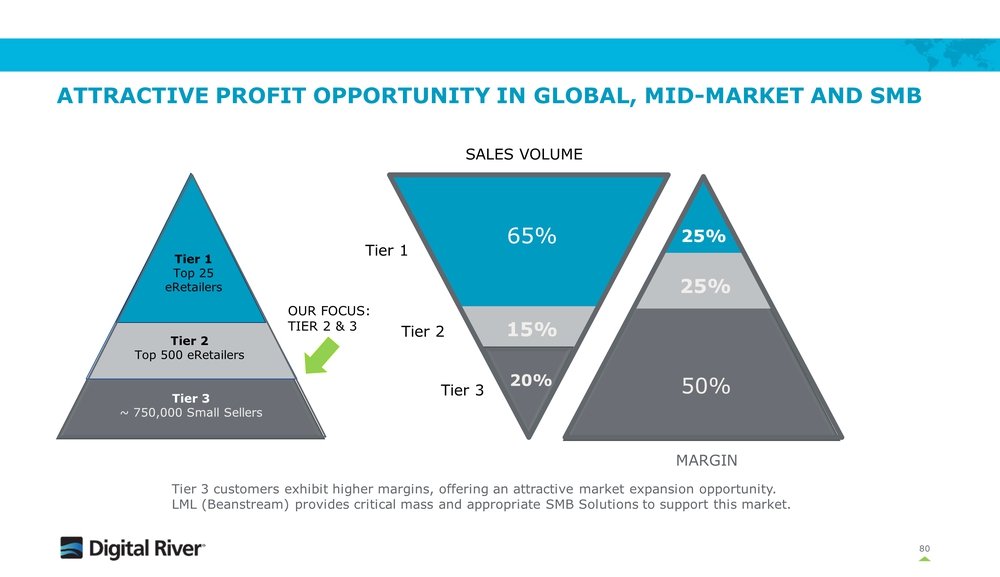

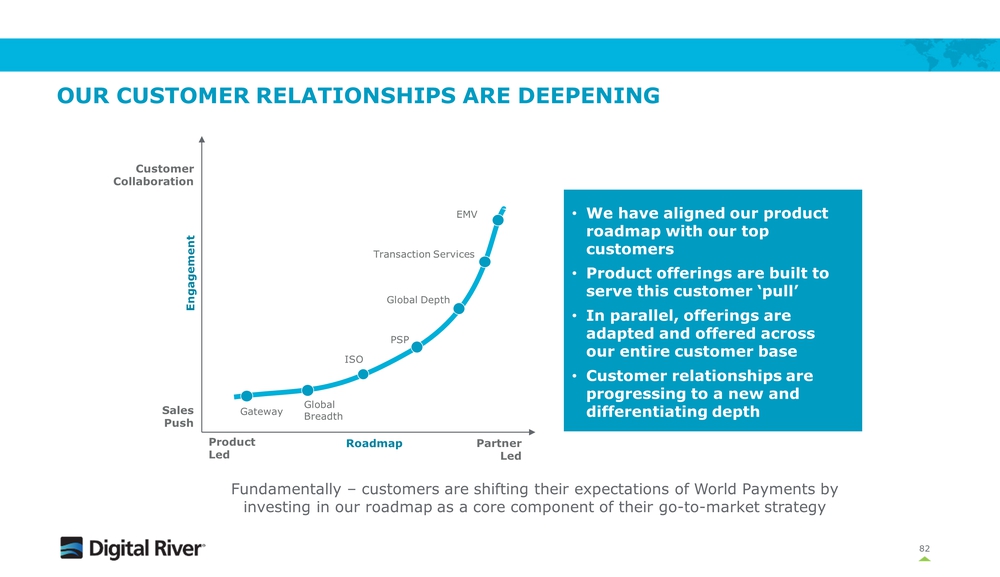

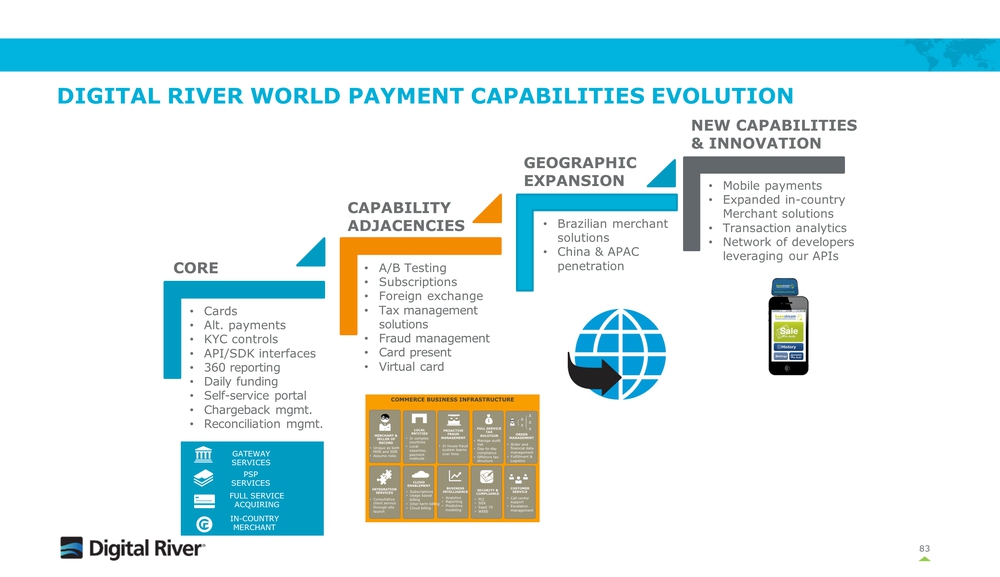

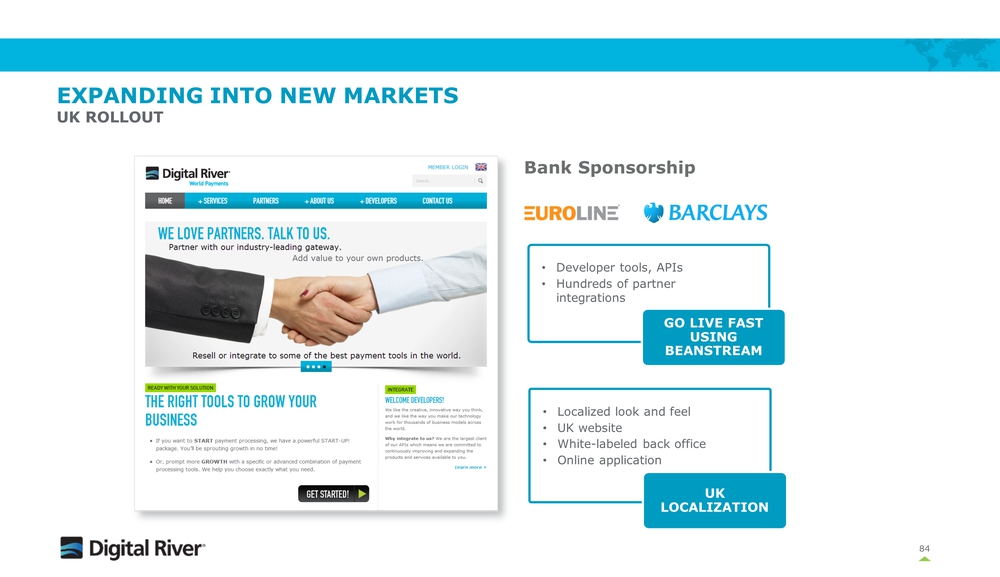

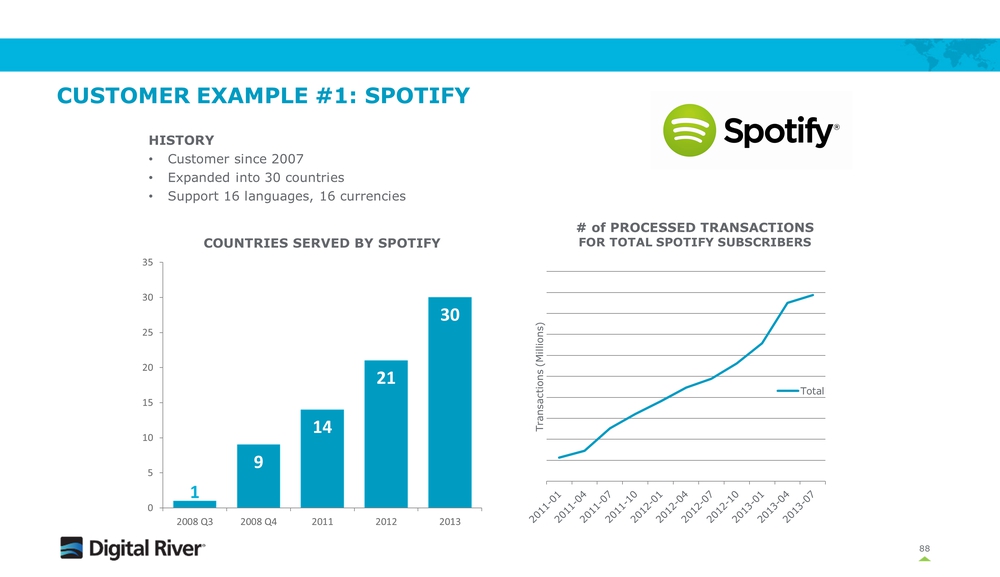

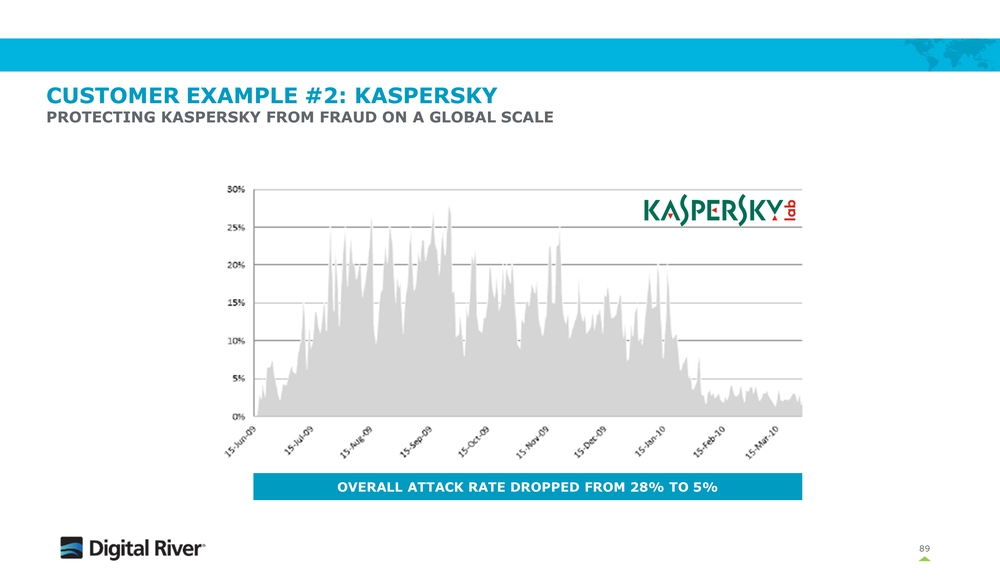

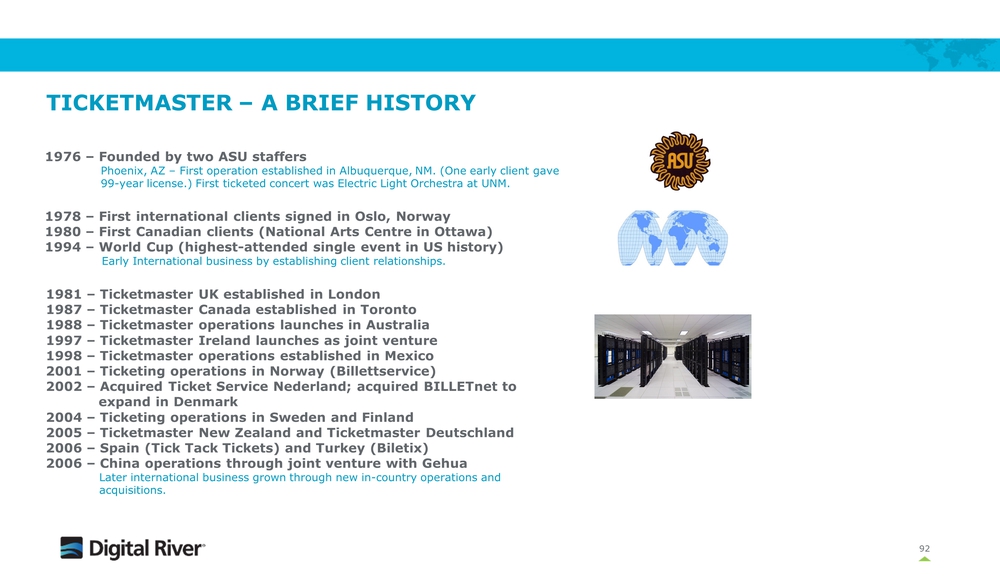

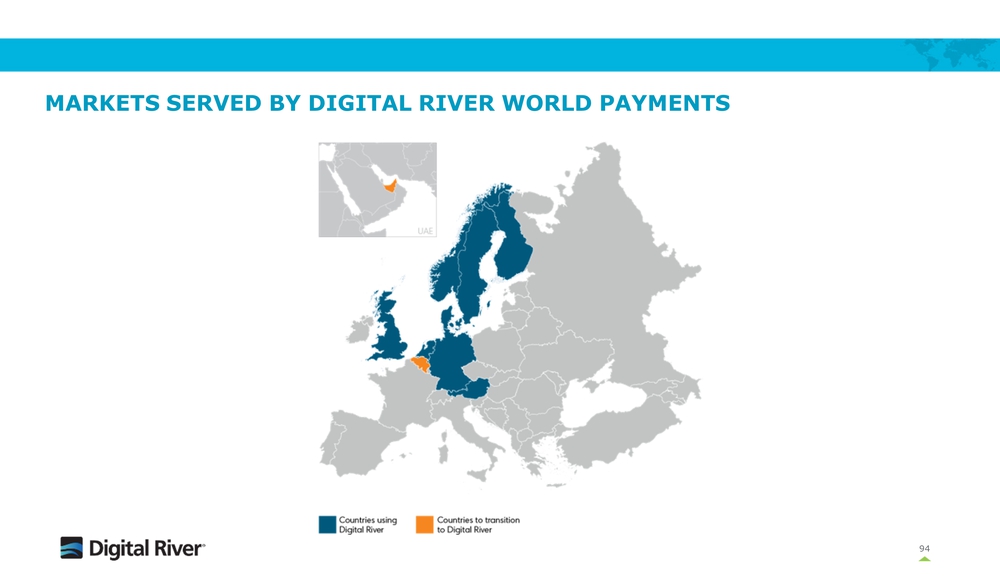

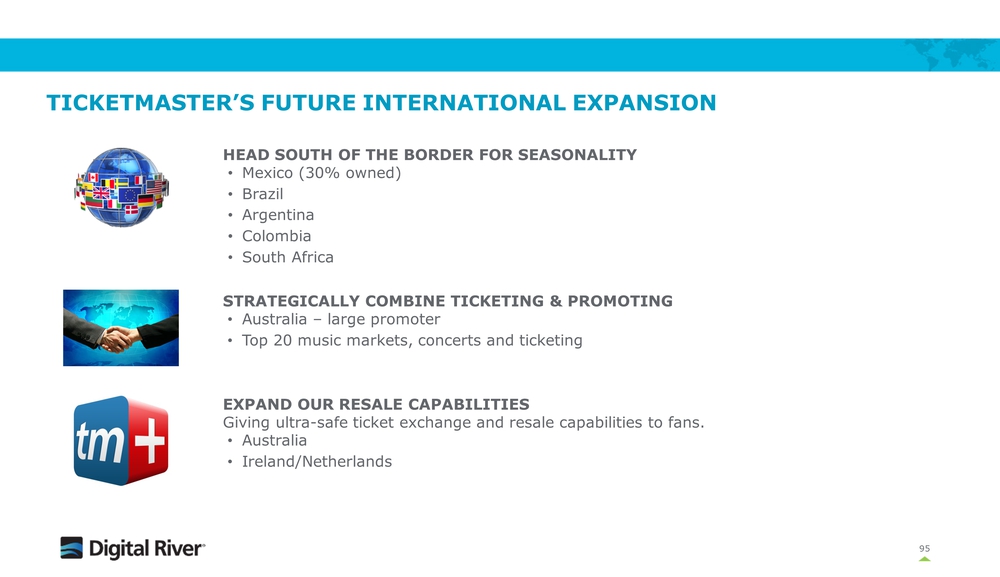

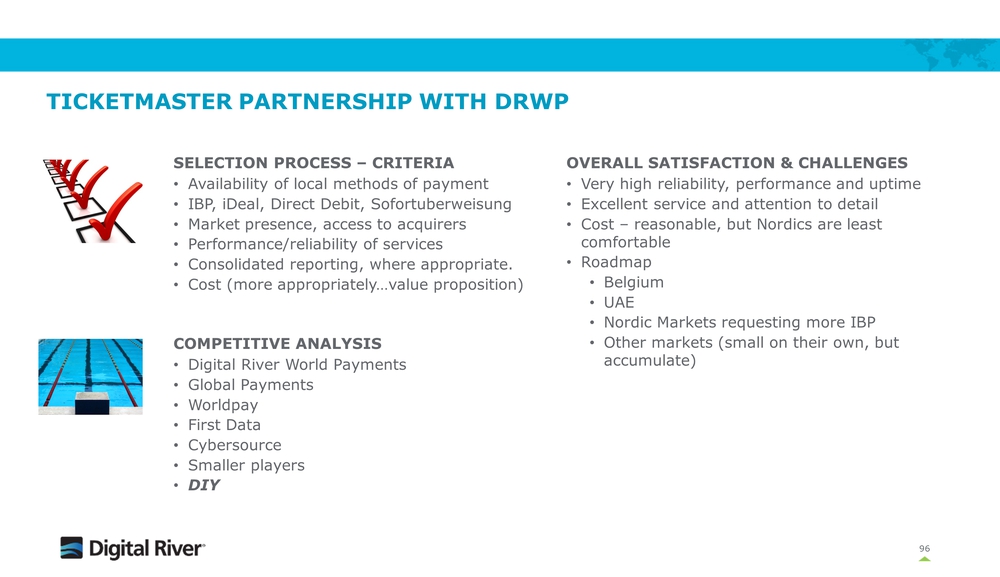

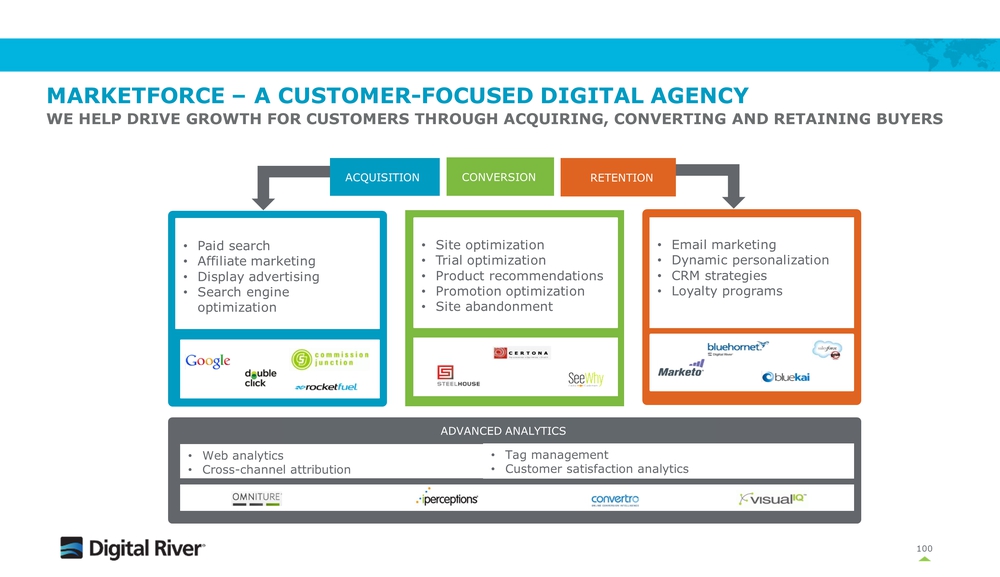

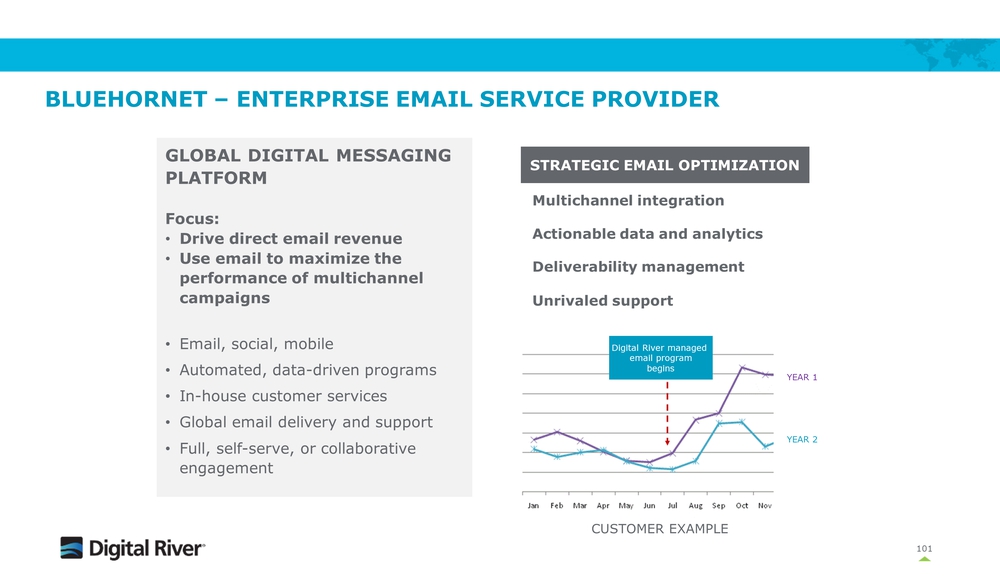

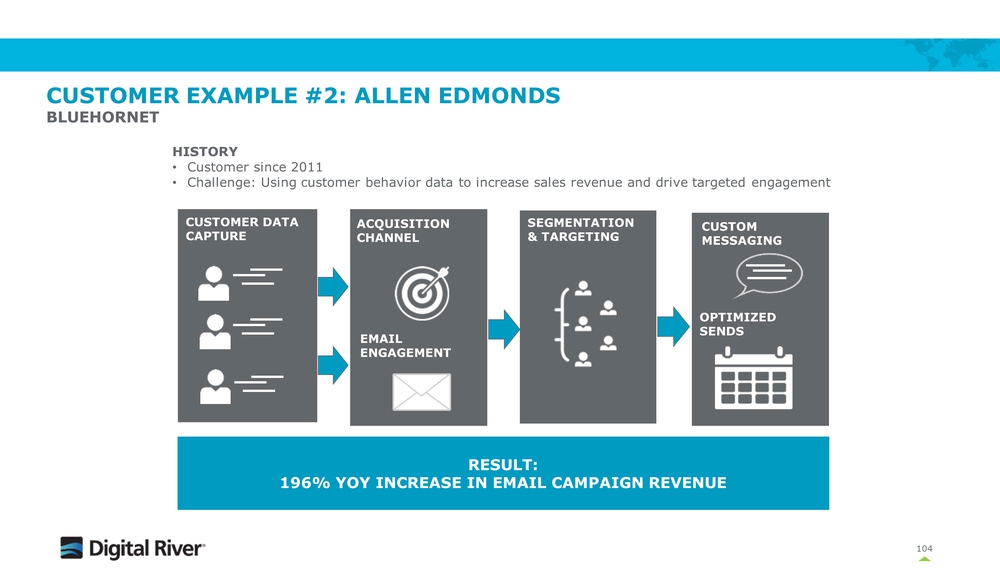

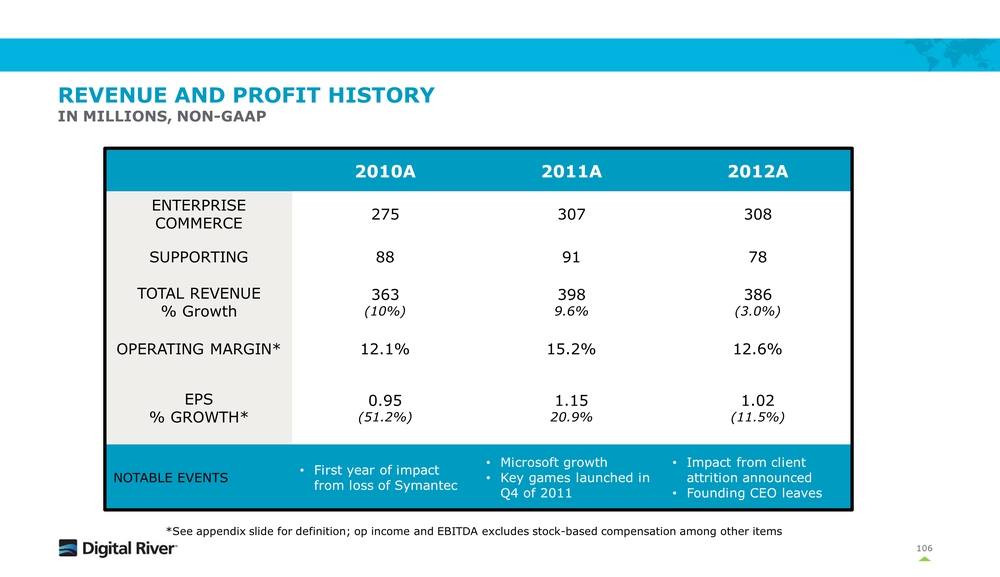

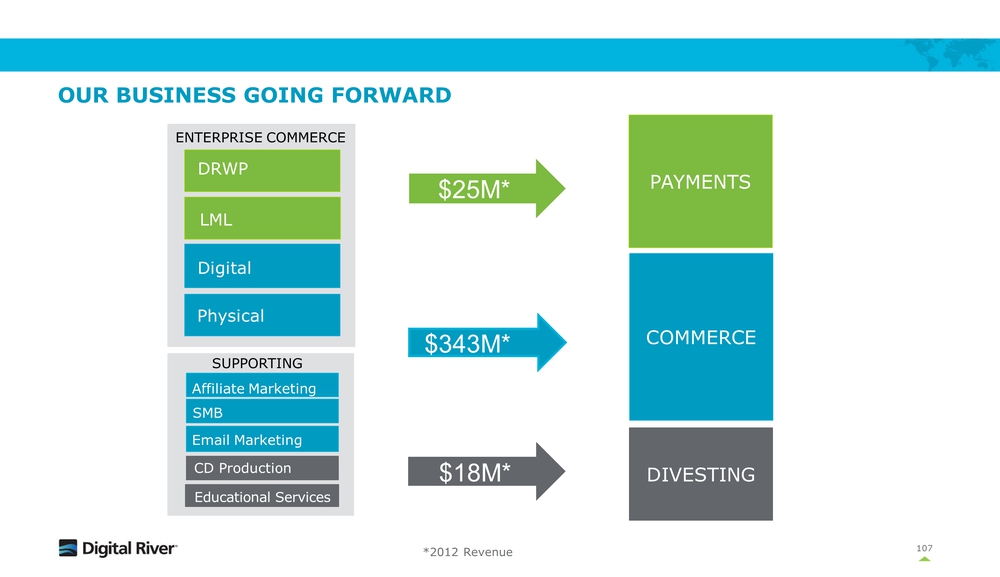

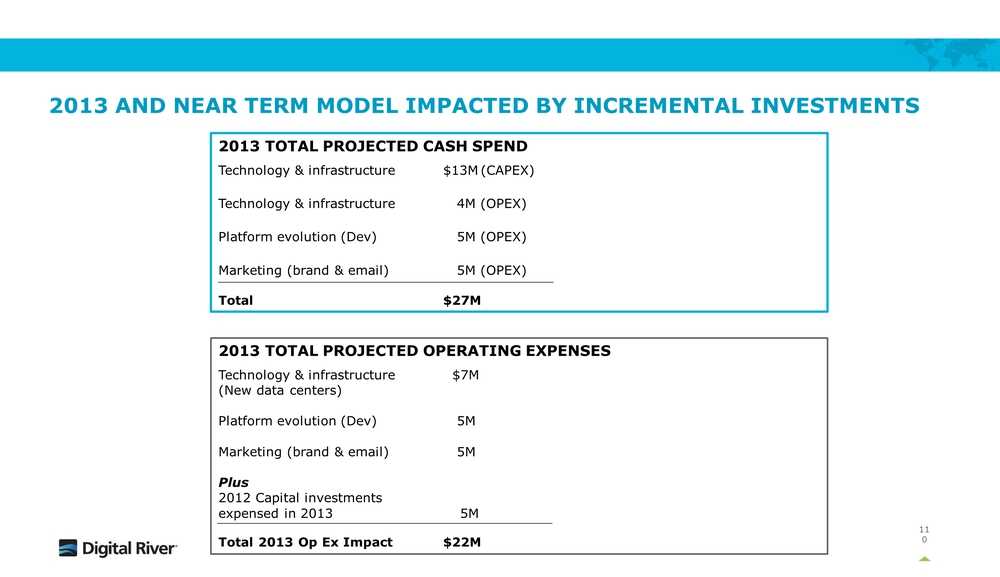

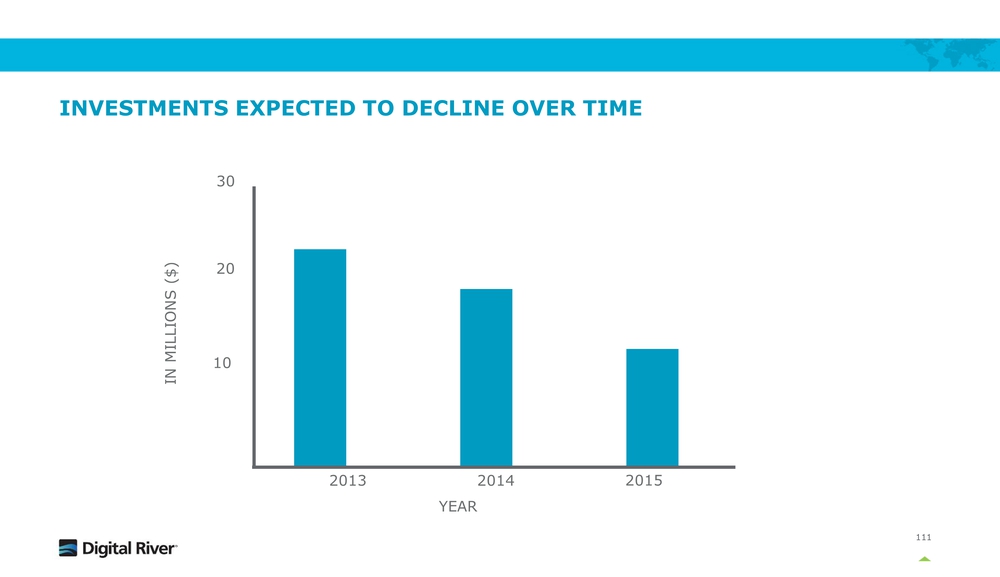

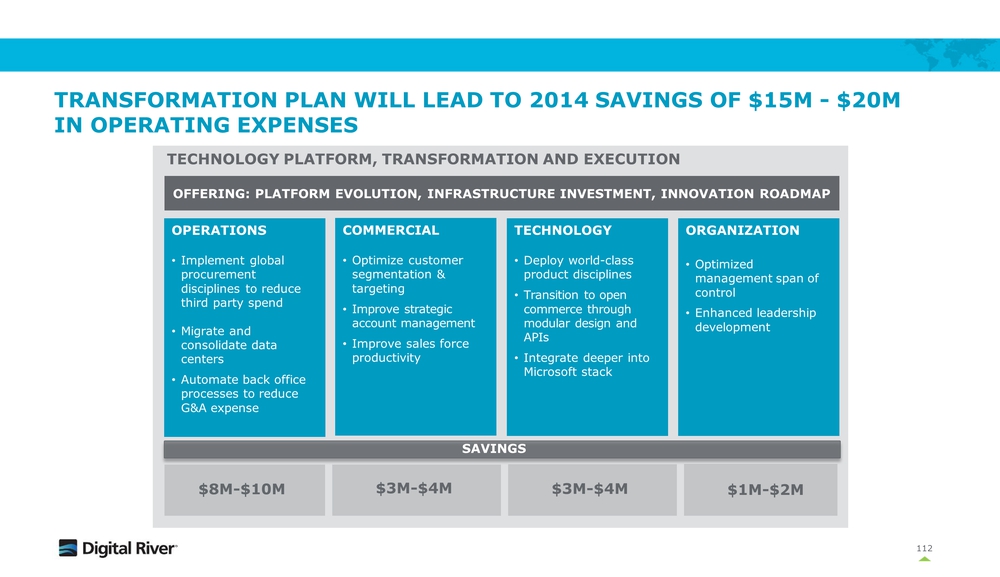

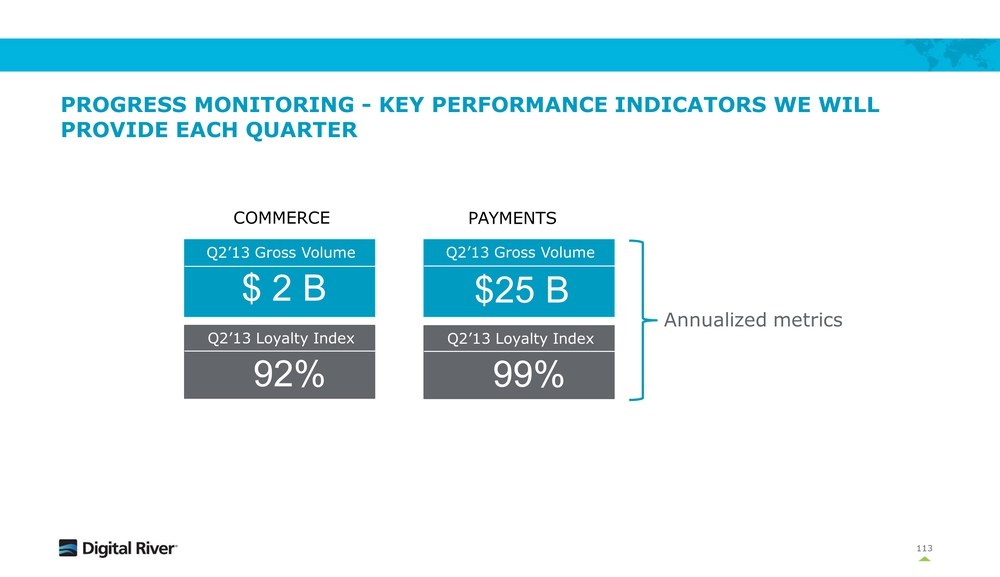

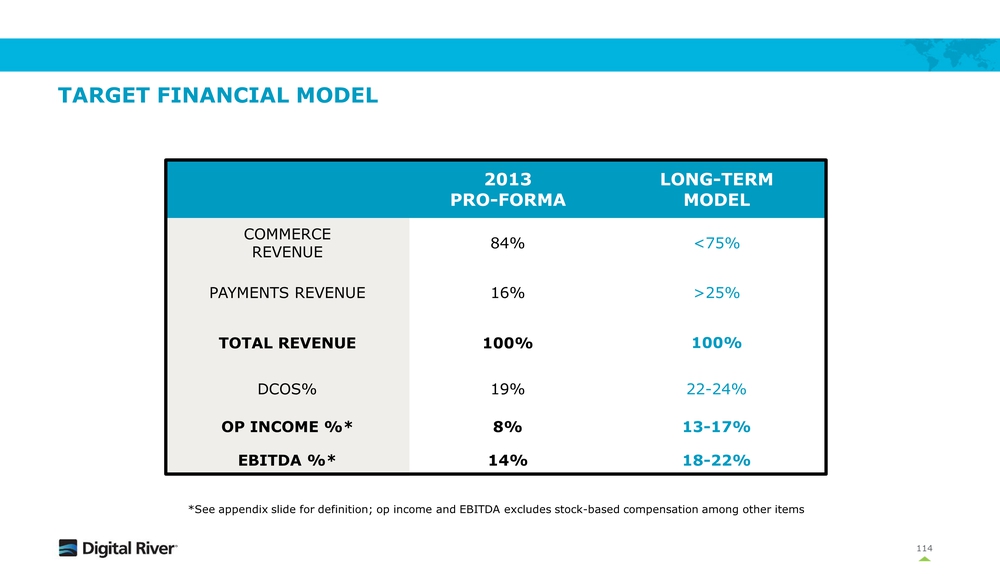

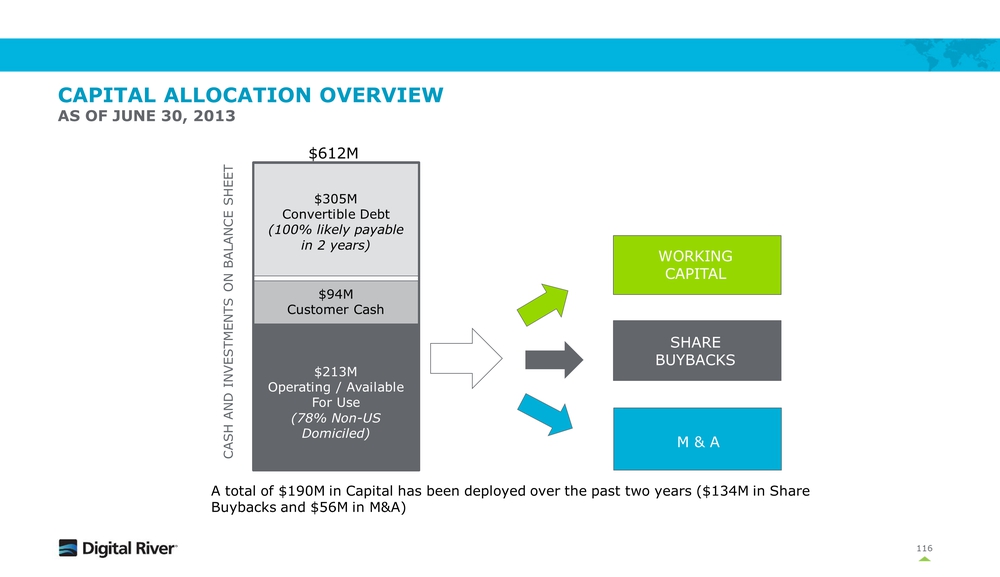

Slide: 1 Body: September 19, 2013 Title: Digital river investor day SubTitle: Omni Berkshire hotelNew York, NY Slide: 2 Body: Melissa Fisher, Vice president investor relationsDigital River Title: WELCOME Slide: 3 Title: Agenda Other Placeholder: 3 Slide: 4 Title: Safe Harbor Other Placeholder: 4 FORWARD-LOOKING STATEMENTSThis presentation contains forward-looking statements, which are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, that are based on our management’s beliefs and assumptions and on information currently available to management. Forward-looking statements include all statements that are not historical facts including, but not limited to, statements regarding our future financial results (including our financial outlook for the full year 2013); potential market and sale opportunities and the size of such opportunities; future acquisitions strategies; product development plans and strategies; anticipated market trends; market demand for, and market adoption of, our products; operating strategies; and any statements of assumptions underlying any of these items mentioned. These statements can be identified by terms such as “estimates,” “expects,” “plans,” “anticipates,” “intends,” “predicts,” “projects,” “likely,” “outlook,” “could,” “should,” “would,” “will” and similar expressions and the negatives of those terms. There can be no assurance that future results will meet the expectations, estimates, or projections conveyed by these forward-looking statements, which involve known and unknown risks, uncertainties and other factors. These factors and other cautionary information relevant to these forward-looking statements are described further in our earnings press releases and in our SEC filings, including our Form 10-K for the year ended December 31, 2012, which we encourage you to review. Except as required by law, we assume no obligation to update these forward-thinking statements publicly. NON-GAAP ITEMSSome of the information included in this presentation is derived from Digital River’s consolidated financial information, but is not presented in Digital River’s financial statements prepared in accordance with U.S. GAAP. Certain of the data are considered to be "Non-GAAP financial measures" under the rules of the Securities and Exchange Commission ("SEC"). Any Non-GAAP financial measures supplement the Company's GAAP disclosures and should not be considered an alternative to the GAAP measures. Our Non-GAAP financial measures may be defined differently from time-to-time and may be defined differently from similar terms used by other companies, and accordingly, care should be exercised in understanding how Digital River defines its Non-GAAP financial measures in this release.© 2013, Digital River. All Rights Reserved. Slide: 5 Body: David Dobson, chief executive officerDigital river Title: Digital river overview Slide: 6 Other Placeholder: 6 Title: OUR AGENDA FOR TODAY: THE NEW DIGITAL RIVER 1. WHO IS DIGITAL RIVER: GLOBAL LEADER IN COMMERCE-AS-A-SERVICEStrong assets, people and customer baseWell-positioned to capitalize on market opportunities2. We are Implementing a Clear Strategy, Improving Focus anD Execution Prior performance led to inconsistent revenue and declining marginsMore importantly—it has impacted some of our customersWe have a plan for significant change3. We Have Begun Executing Our Strategic Transformation PlanTechnology investments to protect existing customers and position for growthAllocated resources to highest growth marketsSignificant improvements to operational excellence4. Our Leadership Team Will Improve Financial PerformancePath to sustainable growth and profit expansionManagement capacity to get it done Slide: 7 Title: Digital river at a glance Other Placeholder: 7 (Gp:) OUR CUSTOMERS INCLUDE TOP GLOBAL BRANDS (Gp:) $386M (Gp:) in 2012 revenue (Gp:) $27B (Gp:) annual online transactions (ttm) (Gp:) 19 (Gp:) years of experience (Gp:) 30 (Gp:) offices around the world (Gp:) 50% (Gp:) revenue outside the Americas in 2012 (Gp:) 1,400+ (Gp:) commerce experts (Gp:) 100+ (Gp:) countries where we do business (Gp:) 180 (Gp:) payment methods Slide: 8 Other Placeholder: 8 Digital river Overview Digital River’s global Commerce-as-a-Service offerings, payments solutions and marketing services help thousands of customers around the world grow their online businesses. COMMERCE-AS-A-SERVICEComplete commerce solution PAYMENTS SOLUTIONSIntegrated commerce and stand-alone offering (Gp:) Commerce Expertise (Gp:) Global Footprint (Gp:) Payments Solutions (Gp:) Market Leadership (Gp:) Strong Balance Sheet (Gp:) PAYMENT SERVICE PROVIDER (Gp:) GATEWAY SERVICES (Gp:) IN-COUNTRY MERCHANT (Gp:) FULL-SERVICE ACQUIRING (Gp:) MULTI-TENANT SAAS PLATFORM (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM Slide: 9 Other Placeholder: 9 first half 2013 Financial summary 1H 2013 MIX BY GEOGRAPHY FY 13 1H ($M) Y/Y GROWTH COMMERCE: ENTERPRISECOMMERCE: SMBPAYMENTSSUPPORTINGTOTAL $296$47$25$18$386M -2%-12%38%-24%-3% COMMERCE:ENTERPRISE72% PAYMENTS15% COMMERCE: SMB10% SUPPORTING3% FY 12 ($M) REVENUE -2%-15%180%-35%7% Y/Y GROWTH $149$21$30$6$206M AMERICAS51% EMEA39% APAC10% REVENUE MIX Slide: 10 Other Placeholder: 10 Digital river history, non-gaap REVENUE MILLIONS NETGIRO ACQUISITION (DRWP) ENTRY INTO SMB MARKETFORCEEXPANSION SIGNED CONTRACT WITH SYMANTEC ENTRY INTO GAMES SIGNED CONTRACT WITH MICROSOFT LOSS OFSYMANTEC LMLACQUISITION OPERATING MARGIN 13% 34% FOCUS ON CONSUMER ELECTRONICS/PHYSICAL YEAR Slide: 11 Other Placeholder: 11 Current markets are LARGE AND GROWING *Digital River estimate (Gp:) COMMERCE BUSINESSCommerce-as-a-Service offering (Gp:) PAYMENTS BUSINESSPayments-only offering (Gp:) *Cross-border commerce revenue (Gp:) Digital River processes $2B online commerce transactions (ttm) (Gp:) Digital River processes $25B online payments transactions (ttm) (Gp:) TOTAL ADDRESSABLE MARKET (Gp:) TOTAL ADDRESSABLE MARKET (Gp:) $25 Billion*Growing at 8% CAGR*Software, games, consumer electronics (Gp:) $160 Billion*Growing at 24% CAGR*Cross-border commerce revenue Slide: 12 Other Placeholder: 12 The new digital river EXPERT GLOBAL GROWTH Slide: 13 Other Placeholder: 13 Strategic transformation framework (Gp:) OPTIMIZE BUSINESS FOUNDATION(Today–Mid 2014) (Gp:) FOCUS AND GROWTH (Gp:) TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION (Gp:) OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP (Gp:) OPERATIONSCost reductionG & A efficienciesGlobal purchasing (Gp:) COMMERCIALSegmentationCoverage modelProductivity (Gp:) TECHNOLOGYAgile developmentPlatform modularizationOptimization (Gp:) ORGANIZATIONCulture evolutionONE Digital RiverStreamline (Gp:) EXPAND OUR CORE MARKETS (Mid-2014–2015) (Gp:) EXPAND INTO NEW MARKETS (2015+) (Gp:) Aggressively grow payments into new marketsGrow core commerce and payments business with current customersDivest non-core businesses (Gp:) Extend digital customer base into cloud and B2BContinue to grow paymentsFocus on global expansion Initial mid-market branded manufacturer focus (Gp:) Aggressively grow mid-market branded manufacturersEstablish strategic partnership programSustain payments growthExpand SMB businessIncrease global brand awareness with key influencers Slide: 14 Other Placeholder: 14 We are focused on key goals and actions that address our challenges GOALS ACTIONS Investing in our technology platform to deliver best-in-class flexibility and rate of innovationLaunching new pricing models to increase customer retention and addressable market Accelerating growth of global payments customer baseExpanding market focus to digital products and branded manufacturersFocusing and optimizing sales force to drive Tier 2 customer retention and growth Driving efficiencies in our business model in the areas of operations, commercial, technology and organization CUSTOMER LOYALTY EXPANDED CUSTOMER BASE INCREASED PROFITABILITY Slide: 15 Other Placeholder: 15 The new digital river (Gp:) WHO IS DIGITAL RIVER? (Gp:) OUR MISSION AND VISION (Gp:) WE HAVE A FOCUSED STRATEGY (Gp:) OUR OPPORTUNITY IS SIGNIFICANT (Gp:) Leading Commerce SaaS company Growth drivers: Commerce-as-a-Service and Digital River World PaymentsKey differentiators: Our commerce business infrastructure, commerce expertise, multi-tenant SaaS platform, world-class cloud infrastructure and global footprint (Gp:) Mission: We drive customer growth through our global commerce expertiseVision: We set the standard for global commerce technology and services (Gp:) Invest in our core technology and new offeringsAllocate resources and expertise to grow in commerce and payments segmentsImprove operational excellence (Gp:) Market is large and moving to where we have strengthGlobal customer expansion and strong growth in paymentsWe expect to return to growth in 2H’14Longer term; at least market growth rates Slide: 16 Other Placeholder: 16 David DobsonChief Executive OfficerIBMCorel CorporationCA Technologies John StrosahlExecutive Vice President and General Managerelement 5Quarterdeck IBM Leadership team Dave MooreSVP, Global Development and EngineeringHomeDepot.comBestBuy.comKeane Christopher RenceSVP, Chief Information OfficerFICO Accenture Stefan SchulzChief Financial OfficerLawson SoftwareBMC Software Arthur Anderson LLP Souheil BadranSVP and General Manager, Digital River World PaymentsFirst DataVeriSignMetavante Corporation Sophanny SchwartzSenior Vice PresidentHuman ResourcesAccentureU.S. Bank Kevin CruddenSVP, General Counsel and Corporate SecretaryRobins, Kaplan, Miller & Ciresi U.S. Steel ALCOA Scott HeimesChief Marketing OfficerWebMD Health ServicesUnitedHealth GroupTarget Corporation Stewart SagastumeSenior Vice President, Microsoft Business UnitFICOZamba Solutions Racotek Michael HechlerSenior Vice President and General ManagerHewlett-Packard Fujitsu-Siemens Glenn StolarSenior Vice President, Global DeliveryUnitedHealth GroupAccenture Slide: 17 Body: Scott Heimes, chief marketing officerDigital river Title: Offering strategy to drive growth Other Placeholder: 17 Slide: 18 Other Placeholder: 18 The new digital river (Gp:) DIFFERENTIATED OFFERING (Gp:) MODULAR OPEN PLATFORM (Gp:) EVOLVED GO-TO-MARKET (Gp:) LARGE ADDRESSABLE MARKET (Gp:) Leading Commerce SaaS company Growth drivers: Commerce-as-a-Service and Digital River World PaymentsKey differentiators: Our commerce business infrastructure, commerce expertise, multi-tenant SaaS platform, world-class cloud infrastructure and global footprint (Gp:) Modularizing our platform to facilitate plug-and-play through open APIsSupports the use of customers’ existing or preferred componentsEnables us to aggressively leverage third-party partners (Gp:) Implementing more flexible pricing approach Opening our business model will grow our customer base, creating new opportunities (Gp:) Current markets are large and growingWe will grow our digital products market and expand into branded manufacturersCommerce TAM = $135BPayments TAM = $160B Slide: 19 Other Placeholder: 19 Offering Strategy today – Commerce and Payments COMMERCE-AS-A-SERVICEComplete commerce solution offered in a full suite PAYMENTSPart of commerce and stand-alone offering PAYMENT SERVICE PROVIDER GATEWAY SERVICES IN-COUNTRY MERCHANT FULL-SERVICE ACQUIRING MULTI-TENANT SAAS PLATFORM (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM Slide: 20 Other Placeholder: 20 COMMERCE-AS-A-sERVICeEnd-to-end suite of commerce solutions (Gp:) Marketing Services (Gp:) (Gp:) SITE OPTIMIZATION (Gp:) SITE SEARCH (Gp:) EMAIL (Gp:) AFFILIATE (Gp:) DISPLAY (Gp:) ANALYTICS (Gp:) (Gp:) (Gp:) (Gp:) Commerce Experience (Gp:) Commerce Business Infrastructure (Gp:) Payments (Gp:) SHOPPING CART (Gp:) CATALOG (Gp:) WCMS (Gp:) SEARCHAN-DIZING (Gp:) MERCHANDISING& PROMOTION (Gp:) LOCALI-ZATION (Gp:) RECOMMENDATION & PERSONALIZATION (Gp:) A/B TESTING (Gp:) PRICING (Gp:) ADMIN TOOLS (Gp:) COMPLIANCE (Gp:) ORDER MANAGEMENT (Gp:) FRAUD (Gp:) LOCAL ENTITIES (Gp:) MERCHANT & SELLER OF RECORD (Gp:) INTEGRATION SERVICES (Gp:) BUSINESS INTELLIGENCE (Gp:) TAX (Gp:) CLOUD ENABLEMENT (Gp:) CUSTOMER SERVICE (Gp:) SINGLE CONNECTION TO PAYMENTS GRID (Gp:) PSP SERVICES (Gp:) GATEWAY SERVICES (Gp:) IN-COUNTRY MERCHANT (Gp:) FULL-SERVICE ACQUIRING Slide: 21 Other Placeholder: 21 Commerce experience POWERFUL TOOLS FOR Delivering and Managing Commerce SITES COMMERCE-AS-A-SERVICE Our set of commerce capabilities allows customers to create and manage world-class commerce sites Commerce experience (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM SHOPPING CART WCMS CATALOG SEARCHAN-DIZING LOCALIZATION MERCHAN-DISING& PROMOTION ADMIN TOOLS PRICING A/B TESTING RECOMMEND-ATION & PERSONALI-ZATION Slide: 22 Other Placeholder: 22 Innovation: Mobile, Social, Local MOBILE SOCIAL LOCAL Responsive designAdaptive designIn-app purchasingMobile POS Localized storesChannel lead Management: Find near you Social influencer segmentationSocial email campaignsSocial tracking Slide: 23 Other Placeholder: 23 Our ability to seamlessly integrate each of these complex capabilities on a global scale is a core differentiator and creates strong barriers to entry Commerce business infrastructureOur unique commerce differentiation Commerce Business Infrastructure MERCHANT & SELLER OF RECORD LOCAL ENTITIES PROACTIVE FRAUD MANAGEMENT FULL-SERVICE TAX SOLUTION INTEGRATION SERVICES ORDER MANAGEMENT CUSTOMER SERVICE SECURITY & COMPLIANCE BUSINESS INTELLIGENCE CLOUD ENABLEMENT COMMERCE-AS-A-SERVICE (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM Slide: 24 Other Placeholder: 24 Enabling the shopper journey Through Commerce Business Infrastructure (Gp:) CUSTOMER SERVICE (Gp:) Provide pre-sales chat support in Japanese to aid purchase decision. (Gp:) Access to native Japanese speaker to aid in transaction and personalize experience (Gp:) INTEGRATION SERVICES (Gp:) CRM, ERP, and financial data sent to customer (Gp:) (Gp:) SECURITY & COMPLIANCE (Gp:) Ensures secure customer journey through PCI, SSAE16, and SOX compliance (Gp:) Consumer has seamless, safe transaction (Gp:) FULL-SERVICE TAX SOLUTION (Gp:) Manages calculation, collection and remittance of taxes (Gp:) Charged the appropriate amount of tax (Gp:) MERCHANT & SELLER OF RECORD (Gp:) Acts as merchant and seller of record, owning transaction risk (Gp:) Presented with local payment types, consumer picks Konbini (Gp:) Consumer visits localized Japanese store (Gp:) Digital River Japanese entity enables on-shore payment types (Gp:) LOCAL ENTITIES (Gp:) ORDER MANAGEMENT (Gp:) Goes to selected Konbini (e.g. 7-11) to pay for product, receives download, account created/updated (Gp:) Real time integrations connecting DRM, MDM and fulfillment (Gp:) CLOUD ENABLEMENT (Gp:) Subscription billing capabilities enable advanced cloud business models (Gp:) Buys software as a monthly subscription (Gp:) PROACTIVE FRAUD MANAGEMENT (Gp:) Review hundreds of heuristics and billions of records to validate customer in less than three milliseconds (Gp:) Screened in real time, quick approval Seamless consumer experience CONSUMER DIGITAL RIVER (Gp:) CONSUMER (Gp:) DIGITAL RIVER Enabled by Digital River software, technology and intellectual property Slide: 25 Other Placeholder: 25 Our ability to offer this suite of core and supporting solutions globally and locally through direct connections and partnerships is a core differentiator PAYMENT PAGE API WHITE LABEL Payments offering strategyintegrated capabilities Delivered Globally (Gp:) PaymentS Solutions (Gp:) GATEWAY SERVICES (Gp:) FULL-SERVICE ACQUIRING (Gp:) IN-COUNTRYMERCHANT (Gp:) FRAUD PREVENTION (Gp:) COMPLIANCE (Gp:) LOCAL ENTITIES (Gp:) FOREIGN EXCHANGE (Gp:) RMS OFFERINGS (Gp:) PAYMENT ANALYTICS (Gp:) PAYOUT SERVICES (Gp:) PSP SERVICES (Gp:) TAX SERVICES COMMERCE-AS-A-SERVICE (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM Slide: 26 Other Placeholder: 26 COMMERCE-AS-A-SERVICE (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM SAAS PLATFORM Extensible technology strategy in evolution Our multi-tenant SaaS commerce platform offers scalability, lower TCO and the benefit of automatic upgrades Multi-tenant saas PLATFORM APIs ADMIN TOOLS SERVICES DATA CENTER DATA MANAGEMENT CLOUD SERVICES Slide: 27 Other Placeholder: 27 Current platform is powerful and feature rich MULTI-TENANT SAAS PLATFORM IT INFRA-STRUCTURE COMMERCE-AS-A-SERVICE OFFERING TODAY – COMPLETE SOLUTION DIGITAL RIVER-OWNEDEIGHT DATA CENTERS ON AN AVERAGE DAY:Serve 2.5 million API callsProcess over 500,000 ordersPresent 5 million page views Host 6+ terabytes of data2.5 authorizations per second*Burst capacity = 60,000 orders per hour *Excludes DRWP Slide: 28 Commerce Technology Platform Evolution Multi-tenant SaaS Platform (Gp:) DIGITAL RIVER-OWNED CLOUD EIGHT DATA CENTERS CURRENT STATESINGLE CODE BASE TARGET PLATFORMMODULAR OPEN API SOLUTIONS (Gp:) FOUR DATA CENTERS + THIRD-PARTY CLOUDS IT Infrastructure Other Placeholder: 28 Slide: 29 Other Placeholder: 29 (Gp:) FOUR DATA CENTERS + THIRD-PARTY CLOUDS (Gp:) MULTI-TENANT SAAS PLATFORM (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Open, modular platform enables plug-and-play configurability Supports the use of Digital River, customer, and third-party partner components CUSTOMER/INTERNAL PARTNER DIGITAL RIVER GO-TO-MARKET OFFERING TECHNOLOGY SUITE Modular and open Opening up our powerful technology platform to attract new, growth markets Slide: 30 Other Placeholder: 30 Platform Evolution Creates offering Flexibility TOTAL SOLUTION MODULAR SOLUTION CUSTOMER/INTERNAL PARTNER DIGITAL RIVER OR (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Full offering provides the complete solution (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Open, modular platform enables plug-and-play configurability Key Benefits: Align with market trendsParticipate in more dealsImprove customer retention Slide: 31 Other Placeholder: 31 Marketing Partners Technology Partners ServicePartners It also Enables a Rich Partner Ecosystem … Definition: Partners that enhance our marketing services offerings Definition: Technology partners that integrate with our platform via APIs Definition: Partners that extend our services offerings Slide: 32 Other Placeholder: 32 (Gp:) SUBSCRIPTION FEES (Gp:) PER TRANSACTION (Gp:) AND/OR … and Supports a more flexible Pricing strategy PERCENTAGE OF SALES (Gp:) AND/OR Aligns with market trends of flexible business modelsSupports selling modularized commerce componentsAllows customers CAPEX and OPEX flexibility Slide: 33 Other Placeholder: 33 platform evolution = New market Opportunities MODEL A MODEL B Serve customers who want entire suitePrice for percentage of sales (traditional model) Serve customers who want componentsOpen up new markets, attract new customersPrice for combination of percentages + fees VALUE OF COMPETITIVE & INTEGRATED COMPONENTS VALUE OF ENTIREOFFERING SUITE (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Full offering provides the complete solution (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Open, modular platform enables plug-and-play configurability % % % FEE FEE (Gp:) % (Gp:) % (Gp:) FEE (Gp:) FEE Slide: 34 Other Placeholder: 34 OPTIMIZE BUSINESS FOUNDATION(Today–Mid 2014) PRODUCT ROADMAP INVESTMENTS FOCUS AND GROWTH TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP OPERATIONSCost reductionG & A efficienciesGlobal purchasing COMMERCIALSegmentationCoverage modelProductivity TECHNOLOGYAgile developmentPlatform modularizationOptimization ORGANIZATIONCulture evolutionONE Digital RiverStreamline EXPAND OUR CORE MARKETS (Mid-2014–2015) EXPAND INTO NEW MARKETS (2015+) Grow core business with current customersPlatform modularization/APIsCloud business enablementDigital B2B foundationPayments roadmap Extend digital customer base into cloud and B2BCloud business enablementContinued B2B evolutionPayments roadmapBranded manufacturer capabilitiesContinued global expansion Aggressive mid-market branded manufacturer growthComplete branded manufacturer product roadmapPartner extensibility Payments roadmap Slide: 35 Other Placeholder: 35 Our Current markets are large and growing current addressable markets of software, games, CONSUMER ELECTRONICS SaaS Homegrown InsourcedOn Premise None of the Above TOTAL ONLINE REVENUE* Enterprise Software Consumer Software & Games Consumer Electronics $182B Digital River Processes $2B Online Commerce Transactions (ttm) 8% CAGR $25.4B SAAS ONLINE REVENUE* *Digital River estimate Enterprise Software Consumer Software & Games Consumer Electronics Slide: 36 Other Placeholder: 36 FUTURE GROWTH FROM EXISTING AND ADJACENT MARKETS TODAY:THREE MARKETS (Gp:) BRANDED MANUFACTURERS (2H 2014, 2015+) (Gp:) Consumer electronicsHousewaresSporting equipmentPower toolsElectronic toysMedical equipmentIndustrial parts & supplies FUTURE STATE:TWO TARGET MARKETS 1 CONSUMER SOFTWARE & GAMES ENTERPRISE SOFTWARE 2 CONSUMER ELECTRONICS 3 (Gp:) DIGITAL PRODUCTS(2014) (Gp:) Software: consumer & enterpriseGamesCloud enablementPublishingServices Slide: 37 Other Placeholder: 37 OPTIMIZE BUSINESS FOUNDATION(Today–Mid 2014) PRODUCT ROADMAP INVESTMENTS FOCUS AND GROWTH EXPAND OUR CORE MARKETS (Mid-2014–2015) EXPAND INTO NEW MARKETS (2015+) Grow core business with current customersPlatform modularization/APIsCloud business enablementDigital B2B foundationPayments roadmap Extend digital customer base into cloud and B2BCloud business enablementContinued B2B evolutionPayments roadmapBranded manufacturer capabilitiesContinued global expansion Aggressive mid-market branded manufacturer growthComplete branded manufacturer product roadmapPartner extensibility Payments roadmap TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP OPERATIONSCost reductionG & A efficienciesGlobal purchasing COMMERCIALSegmentationCoverage modelProductivity TECHNOLOGYAgile developmentPlatform modularizationOptimization ORGANIZATIONCulture evolutionONE Digital RiverStreamline Slide: 38 Other Placeholder: 38 EXPANDED DIGITAL*(2014) SOFTWARE & GAMES(Today) $39B10% CAGR Expanded Digital:PublishingServices Cloud enablementSubscriptionsUsage-based billing $19B8% CAGR $20B14% CAGR TOTAL ADDRESSABLE DIGITAL MARKET(2014+) EVOLUTION OF THE CLOUD IS CREATING NEW BUSINESS MODELS BUILDS ON CORE DIGITAL COMPETENCIES CAGR is projected through 2017 *Digital River estimate Commerce Growth Opportunities Digital PRODUCTS Slide: 39 Other Placeholder: 39 OPTIMIZE BUSINESS FOUNDATION(Today–Mid-2014) Product roadmap investments FOCUS AND GROWTH Grow core business with current customersPlatform modularization/APIsCloud business enablementDigital B2B foundationPayments roadmap EXPAND OUR CORE MARKETS (Mid-2014–2015) Extend digital customer base into cloud and B2BCloud business enablementContinued B2B evolutionPayments roadmapBranded manufacturer capabilitiesContinued global expansion TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP OPERATIONSCost reductionG & A efficienciesGlobal purchasing COMMERCIALSegmentationCoverage modelProductivity TECHNOLOGYAgile developmentPlatform modularizationOptimization ORGANIZATIONCulture evolutionONE Digital RiverStreamline EXPAND INTO NEW MARKETS (2015+) Aggressive mid-market branded manufacturer growthComplete branded manufacturer product roadmapPartner extensibility Payments roadmap Slide: 40 Title: Commerce Growth Opportunities branded manufacturers Other Placeholder: 40 BRANDED MANUFACTURERS*(2H 2014, 2015) CONSUMER ELECTRONICS(Today) $96B25% CAGR HousewaresSporting equipmentPower tools $6B10% CAGR $90B30% CAGR TOTAL ADDRESSABLE BRANDED MANUFACTURER MARKET(2015+) Electronic toysMedical equipmentIndustrial parts & supplies Branded Manufacturers: MANUFACTURERS WANT TO ESTABLISH DIRECT CONSUMER RELATIONSHIPS TOP GROWTH MARKET. BUILDS ON CONSUMER ELECTRONICS COMPETENCY CAGR is projected through 2017 *Digital River estimate Slide: 41 Other Placeholder: 41 Digital River’s Commerce Total Addressable Market 2013 B2C PROJECTION = $1 TRILLION12013 B2B PROJECTION = $559 BILLION1 MARKET SEGMENTATION DIGITAL PRODUCTS(B2C & B2B) BRANDED MANUFACTURERS(B2C & B2B) RETAIL DIGITAL RIVER’S ADDRESSABLE MARKETS $Billions2(B2C & B2B by 2015) Enterprise software Consumer software & games Consumer electronics Expanded digital Branded manufacturers $135.4B DISTRIBUTORS 1Source: Internet Retailer2Digital River estimate Slide: 42 Other Placeholder: 42 Digital River’s Payments Total Addressable Market CUSTOMER GLOBAL EXPANSION GLOBAL PROJECTED 2013 B2C ONLINE SALES1 $1 TRILLION19% CAGR $840B $160B In Country Transactions Cross-Border Transactions Travel Consumer electronics Clothing & footwear Health & beauty Music, games, movie downloads Jewelry & watches Books GLOBAL PROJECTED 2013 CROSS BORDER TRANSACTIONS2(online revenue) Digital River processed $25B online payments transactions over the last 12 Months $160 BILLION24% CAGR 1Source: Internet Retailer2Nielsen and Digital River estimateCAGR is projected through 2017 Slide: 43 Other Placeholder: 43 The new digital river (Gp:) DIFFERENTIATED OFFERING (Gp:) MODULAR OPEN PLATFORM (Gp:) EVOLVED GO-TO-MARKET (Gp:) LARGE ADDRESSABLE MARKET (Gp:) Leading Commerce SaaS company Growth Drivers: Commerce-as-a-Service and Digital River World PaymentsKey differentiators: Our commerce business infrastructure, commerce expertise, multi-tenant SaaS platform, world-class cloud infrastructure and global footprint (Gp:) Modularize our platform to facilitate plug-and-play through open APIsSupport customers’ existing or preferred componentsEnable aggressive leverage of third-party partners (Gp:) Implement a more flexible pricing approach Open our business model to grow our customer base, creating new opportunities (Gp:) Current markets are large and growingGrow our digital products market and expand into branded manufacturersCommerce TAM = $135BPayments TAM = $160B Slide: 44 Other Placeholder: 44 COMMERCE ECOSYSTEM HISTORY GROWTH STRATEGY Customer example: LEnOVO Supported expansion into nine countries in two-year spanDelivered localized shopping experience in six languages and five currencies 2010 2011 2012 2013 Nordic + centralregion expansion Flagship B2Bstores Outlet storelaunch Customer since 2010Look to Digital River to help drive global growth in B2B and B2C markets (Gp:) CUSTOMER/INTERNAL (Gp:) DIGITAL RIVER (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display Slide: 45 Body: John leech, e-commerce director emeaLenovo Title: LENOVO Slide: 46 Body: A $34B global personal technology company with 30,000 people and customers in 160+ countries. Slide: 47 PC USAGE “A Market Share Juggernaut.” Wall Street Journal 2013 LENOVO Lenovo WW PC Market Share 2009 2010 2011 2012 2013 Slide: 48 PC USAGE What we wanted to do …. Roll out eCommerce in EMEASuccessful eCommerce business in NA, Japan and ANZFocused on profitable segments more than revenue growthDo it without impacting the Partner Channel Drive a different eCommerce experience through Configure to OrderMange price transparency and interlock with the country sales teams Slide: 49 PC USAGE The Challenges with that plan…. Securing internal investments required Multiple small country teams meant scaling the Head count numbers was difficult Needing to integrate with multiple banking and payment solutions in different countriesInfrastructure not End Customer focused Major ERP upgrade was the priority for the businessNo centralised Call centre capabilityHow to scale multiple countries easilyTarget of 12 countries Very distributed internal organisation Slide: 50 PC USAGE Why Digital River ?… Ability to integrate with our experienceConfigure to order is central to the customer experience Tight integration on the eCommerce Front endInsulated on the Back end via our B2B gateway from internal IT roadmapDistribution and Logistics partner integrations to expand the product offeringProject team Remove Payments and Fraud issues DR acts as Merchant and Seller of RecordProvides all of our Payments capabilities removes that complexity from our IT roadmapScale customer services capabilityCentral Call Centre to support CustomersAct as an extension to lenovo.com team Slide: 51 PC USAGE Where to next ?… Continue to expand the footprintGrown from Two to Nine Countries so farNew sites targeted at specific audiences (some in conjunction with traditional business partners)Expand the Portfolio Third party relationships and opportunities that DR bring to the table Other Sources of Supply if required for third party optionsOther Payment methods including line of creditEngage Other Marketing CapabilitiesAffiliate Network management is a current project just under way Slide: 52 Body: John Strosahl, executive vice president and general managerDigital River Title: Commerce overview Slide: 53 Other Placeholder: 53 Commerce business ENTERPRISE88% 1H 2013 MIX BY BUSINESS SIZE SMB 12% COMMERCE-AS-A-SERVICEComplete suite of commerce solutions REVENUE COMMERCE EMPLOYEE SUMMARY Marketing Services New Sales AccountManagement Delivery 50 144 161 53 1H 2013 REVENUE = $170M, -2% TRANSACTIONS PROCESSED = $2B (ttm) 2012 REVENUE = $343M, -4% SEGMENTATION TIER 1$1B+ TIER 2$25M - $1B TIER 3<$25M ENTERPRISE SMB 1H 2013 MIX BY GEOGRAPHY (Gp:) AMERICAS59% (Gp:) EMEA31% (Gp:) APAC10% (Gp:) MARKETING SERVICES (Gp:) payments (Gp:) Commerce experience (Gp:) Commerce Business Infrastructure (Gp:) MULTI-TENANT SAAS PLATFORM Slide: 54 Other Placeholder: 54 Current markets and customer examples SOFTWARE & SERVICES 1997 2004 2008 Market Entry: GAMES & ENTERTAINMENT CONSUMER ELECTRONICS Slide: 55 Other Placeholder: 55 TIER 1$1B+ TIER 2$25M - $1B TIER 3<$25M CUSTOMER EXAMPLES ENTERPRISE ONLINE REVENUE SMB STRATEGY Open modular à-la-carte solution will offer maximum solution flexibility Branded manufacturer focusÀ-la-carte or complete solutionTarget growth market Self-serve complete solutionOpportunity to identify rapidly growing businesses to move to Tier 2 Customer segmentation Slide: 56 Other Placeholder: 56 Customer growth strategy EXAMPLE WE BUILD STRONG PARTNERSHIPS WITH CUSTOMERS OVER TIME YEAR 1 YEAR 2 YEAR 3 REVENUE IN MILLIONS TIME Starts with single piece of businessSingle product Single country Single marketing program Relationship grows1-2 additional productsAdditional geographiesMarketing expansion Strong partnership developsAdditional productsAdditional geographic expansionNew capabilities (cloud enablement, B2B, etc.) Slide: 57 Other Placeholder: 57 Strategic transformation framework OFFERING EVOLUTION, FOCUS AND GROWTH TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP EXPAND OUR CORE MARKETS (Mid-2014–2015) EXPAND INTO NEW MARKETS (2015+) Extend digital customer base into cloud and B2BContinued payments growthFocused global expansion Initial mid-market branded manufacturer focus Aggressive mid-market branded manufacturer growthStrategic partnership programSustained payments growthSMB expansionIncrease global brand awareness with key influencers OFFERING EVOLUTION STRATEGIC ACCOUNT MANAGEMENT SALESFORCE PRODUCTIVITY CUSTOMER SEGMENTATION & TARGETING OPTIMIZE BUSINESS FOUNDATION(Today–Mid 2014) Payments aggressive growth into new marketsGrow core commerce and payments business with current customersDivest non-core businesses Slide: 58 Other Placeholder: 58 (Gp:) OFFERINGEVOLUTION (Gp:) OPEX or CAPEX flexibilityExpands addressable market (Gp:) 2H 2014 (Gp:) Percentage of salesPer transactionSubscription fee (Gp:) SALESFORCE PRODUCTIVITY (Gp:) Expand inside sales modelLeverage partnershipsRegional sales model (Gp:) 1H 2014 (Gp:) Increased sales velocityIncreased revenue per sales person (Gp:) STRATEGIC ACCOUNT MANAGEMENT (Gp:) 1H 2014 (Gp:) Improved customer satisfactionIncreased customer loyaltyIncreased revenue growth (Gp:) New pod structureSingle point of contactFocused resources (Gp:) CUSTOMER SEGMENTATION & TARGETING (Gp:) Increased profit per customerFaster speed to revenueGreater stickiness (Gp:) 2H 2014 (Gp:) Tier segmentation Strategic sellingFocused resources Commerce operational AND GO-TO-MARKET EVOLUTION BENEFITS TIMING WHAT WE’RE DOING % FEE Slide: 59 Other Placeholder: 59 Why commerce customers choose Digital river Global scale, ability to execute complex requirements, speed-to-marketSubscription services and our ability to enable sales in emerging, complex markets with relevant payment typesGlobal reach, consumer and private shopping stores, physical and digital order management and fulfillment, subscriptions and marketing programs Flexible and integrated platform, fraud management services, pan- European reach with extensive payment options, flexible business modelMarketing services and SMB commerce capabilities, speed and agility Slide: 60 Other Placeholder: 60 COMMERCE ECOSYSTEM (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display HISTORY GROWTH STRATEGY Provide localized cart experience in 18 languages and 26 available currenciesRecently launched fully hosted store in Japanese Customer example #1: AVAST Customer since 2009Support company’s freemium model in 28 countries across the globe 2010 2011 2012 2013 Migration toEnterprise Commerce 5 new locales & Japan expansion Search & affiliate program (Gp:) CUSTOMER/INTERNAL (Gp:) DIGITAL RIVER Slide: 61 Other Placeholder: 61 COMMERCE ECOSYSTEM (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display HISTORY GROWTH STRATEGY Customer example #2: razer Supported launch of Razer Blade gaming laptop in U.S. store; sold out within 30 minutesImplemented guest checkout for cyber weekend resulting in a 5X sales increase Customer since 2010Leverage commerce expertise to successfully launch exclusive online productsSupport 37 stores in 13 locales, 6 languages 2010 2011 2012 2013 U.S. affiliate launch &3 more locales Razer Blade introduced in U.S. store Cart abandon program & Double Byte store U.S. & 6 international store launches (Gp:) CUSTOMER/INTERNAL (Gp:) DIGITAL RIVER Slide: 62 Other Placeholder: 62 COMMERCE ECOSYSTEM (Gp:) Merchandising (Gp:) Web ContentMgmt. (Gp:) Catalog (Gp:) Search (Gp:) Site Optimization (Gp:) Affiliate (Gp:) Email Marketing (Gp:) Adv. Analytics (Gp:) Payments (Gp:) Order Mgmt. (Gp:) Tax Mgmt. (Gp:) Fulfillment (Gp:) CustomerSupport (Gp:) PrivateStores (Gp:) MARKETING SERVICES (Gp:) Fraud (Gp:) Display HISTORY DIGITAL RIVER KEY MILESTONES Launched one-click purchase in Xbox console last spring Customer example #3: microsoft Customer since 2006Developed partnership grounded in innovationExpanded Microsoft Store into 228 countries 2011: Microsoft U.S. Store 100% on Digital River 2012: International expansion 2012: Xbox pre-order + Office 2013 launch 2010: Office 2010 beta + Mac 2011 try/buy global launch (Gp:) CUSTOMER/INTERNAL (Gp:) DIGITAL RIVER Slide: 63 Body: Kevin Eagan, vice president ecommerceMicrosoft Title: Microsoft Other Placeholder: 63 Slide: 64 Body: Kevin EaganVice President, EcommerceMicrosoft Retail Stores Title: Microsoft Stores Slide: 65 Title: Our ecommerce growth (Gp:) FY09 (Gp:) $119M (Gp:) >500% growth in just 5 years (Gp:) FY13 (Gp:) FY12 (Gp:) FY11 (Gp:) FY10 (Gp:) FY14 (Gp:) > $1B Slide: 66 Title: Catalog expansion (Gp:) Now (Gp:) 2006 Slide: 67 Title: Geo expansion 99.8% Uptime Now in 228 markets worldwide Physical Goods in 20 Markets and expanding rapidly Slide: 68 Title: Challenges & Opportunities (Gp:) Seamless Omni-channel ecommerce platform (Gp:) Evolution from “black box” platforms to open architecture, web service extensible platforms (Gp:) Precise Personalization: Big Data, Loyalty, Social (Gp:) Responsive experiences everywhere: mobile, tablet, voice Slide: 69 Title: Thank you Slide: 70 Body: Kevin Eagan, vice president e-commerce, MicrosoftJohn leech, e-commerce director emea, lenovo Title: Microsoft and Lenovo Q&A Slide: 71 Body: 15 minutes Title: Break Slide: 72 Body: Souheil Badran, senior vice president and general managerDigital River Title: Digital river world payments innovation and growth Other Placeholder: 72 Slide: 73 Other Placeholder: 73 Digital river world payments 1H 2013 MIX BY GEOGRAPHY REVENUE ENTERPRISE60% MIX BY BUSINESS SIZE SMB40% 2013 1H REVENUE = $30M, 180% YOY GROWTH Direct Revenue $18M REVENUE SEGMENTATION Channel Revenue $12M 2012 REVENUE = $25M (Gp:) Tier 1Top 25 eRetailers (Gp:) Tier 2Top 500 eRetailers (Gp:) Tier 3~ 750,000 Small Sellers OUR FOCUS (Gp:) AMERICAS50% (Gp:) EMEA40% (Gp:) APAC10% $25B in Transactions Processed Last 12 months (Gp:) Stockholm, Victoria, Minnetonka, San Francisco, Brazil, Australia, Taipei and Japan (Gp:) 150+ Employees Across the Globe Slide: 74 Other Placeholder: 74 Commerce Merchant Connectivity MERCHANT ACQUIRERS Source: Glenbrook analysis, 2011 CONSUMER MERCHANT &PARTNERS CONSUMER MERCHANT ACQUIRERS (Gp:) PAYMENT GATEWAY MERCHANTDIRECT CONNECT Slide: 75 Other Placeholder: 75 Extensive Reach of Relevant Local Payment methods one central connection to payment types across the globe MORE THAN 180 PAYMENT METHODS WORLDWIDE (Gp:) check Slide: 76 Other Placeholder: 76 Digital river world payments: How we are different MERCHANT SERVING MERCHANTS BROAD & STABLE PAYMENT NETWORK VALUE-ADDED SERVICES We approach payments from a broader, holistic, global view of commerce; as a processor of billions of dollars in payments per year for our own business as a top-five merchant and seller of record in the world today. Global in-country payments offers greater adoption and higher margins. We have an international portfolio with over 50 global bank connections and access to over 180 locally preferred payment methods. Payment page and mobile optimization, fraud prediction and international tax services, recurring billing, batch processing, tokenization, and card updater. Slide: 77 Other Placeholder: 77 Merchant Buyers Global partnersLocally preferred payment methodsCountriesCurrenciesInternet bank payment optionsGlobal bank connections% EFT matching rate$billion processed (ttm) 40018019017085509025 Digital river world payments at a glance Slide: 78 Other Placeholder: 78 2010-2011:Majority of revenue drivenby existing customer growth 2011-2012:Majority of revenue driven by new customer growth 1H 2013 1H:LML acquisition adds growth and presence in SMB MILLIONS digital river world payments growth $30.0 Slide: 79 Other Placeholder: 79 AGGRESSIVE PAYMENTS GROWTH(Today–Mid–2014) Digital river world Payments roadmap for growth PAYMENTS GROWTH STRATEGY TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP OPERATIONSCost reductionG & A efficienciesGlobal purchasing COMMERCIALSegmentationCoverage modelProductivity TECHNOLOGYAgile developmentPlatform modularizationOptimization ORGANIZATIONCulture evolutionONE Digital RiverStreamline CONTINUED PAYMENTS GROWTH(Mid-2014–2015) EXPAND INTONEW MARKETS(2015+) LML integrationSMB growthExpanded bank network in APAC & EMEANew channel relationships Expansion to Russia, China, IndiaMobile payments growthTransaction analyticsExpanded API network and expanded connections into third-party commerce platformsNew global channel relationships Continued global expansion to Russia, India, ChinaThird-party commerce platformsNew global and regional channel relationships CONTINUED EXPANSION OF PARTNER PROGRAMSCALABLE, RELIABLE AND SECURE INFRASTRUCTURE Slide: 80 Other Placeholder: 80 Attractive profit opportunity in Global, mid-market and SMB SALES VOLUME MARGIN 25% 25% 50% 15% 65% 20% Tier 1 Tier 2 Tier 3 Tier 3 customers exhibit higher margins, offering an attractive market expansion opportunity. LML (Beanstream) provides critical mass and appropriate SMB Solutions to support this market. (Gp:) Tier 1Top 25 eRetailers (Gp:) Tier 2Top 500 eRetailers (Gp:) Tier 3~ 750,000 Small Sellers OUR FOCUS:TIER 2 & 3 Slide: 81 Other Placeholder: 81 (Gp:) PAYMENT PAGE (Gp:) API (Gp:) WHITE LABEL (Gp:) Payment Solutions (Gp:) TAX SERVICES (Gp:) GATEWAY SERVICES (Gp:) FULL-SERVICE ACQUIRING (Gp:) IN-COUNTRYMERCHANT (Gp:) FRAUD PREVENTION (Gp:) COMPLIANCE (Gp:) LOCAL ENTITIES (Gp:) FOREIGN EXCHANGE (Gp:) RMS OFFERINGS (Gp:) PAYMENT ANALYTICS (Gp:) PAYOUT SERVICES (Gp:) PSP SERVICES Our ability to offer this suite of core and supporting solutions globally and locally through direct connections and partnerships is a core differentiator Digital river world payments offering strategyintegrated capabilities Delivered Globally Slide: 82 Other Placeholder: 82 Our customer relationships are Deepening We have aligned our product roadmap with our top customersProduct offerings are built to serve this customer ‘pull’ In parallel, offerings are adapted and offered across our entire customer baseCustomer relationships are progressing to a new and differentiating depth (Gp:) Gateway (Gp:) ISO (Gp:) Global Breadth (Gp:) Global Depth (Gp:) EMV (Gp:) Transaction Services (Gp:) PSP (Gp:) Product Led (Gp:) Partner Led (Gp:) Customer Collaboration (Gp:) Sales Push (Gp:) Roadmap (Gp:) Engagement Fundamentally – customers are shifting their expectations of World Payments by investing in our roadmap as a core component of their go-to-market strategy Slide: 83 Other Placeholder: 83 (Gp:) (Gp:) PSP SERVICES (Gp:) GATEWAY SERVICES (Gp:) IN-COUNTRY MERCHANT (Gp:) FULL SERVICE ACQUIRING Digital river world Payment capabilities evolution CORE CAPABILITY ADJACENCIES GEOGRAPHIC EXPANSION NEW CAPABILITIES & INNOVATION Mobile paymentsExpanded in-country Merchant solutions Transaction analyticsNetwork of developers leveraging our APIs Brazilian merchant solutionsChina & APAC penetration A/B TestingSubscriptionsForeign exchangeTax management solutionsFraud managementCard presentVirtual card CardsAlt. paymentsKYC controlsAPI/SDK interfaces360 reportingDaily fundingSelf-service portalChargeback mgmt.Reconciliation mgmt. Slide: 84 Other Placeholder: 84 Expanding into New Markets UK Rollout (Gp:) Developer tools, APIsHundreds of partner integrations (Gp:) GO LIVE FAST USING BEANSTREAM Bank Sponsorship (Gp:) Localized look and feelUK websiteWhite-labeled back officeOnline application (Gp:) UK LOCALIZATION Slide: 85 Other Placeholder: 85 Continued innovation Mobile payment processing CUSTOM STORE FRONT TABLET & mPOS SOLUTIONS End-to-end encryption and multi-currency support Elegant alternative to traditional POS with in-app analytics Slide: 86 Other Placeholder: 86 The partner ecosystem Extending our Footprint Through THIRD Parties WHITE LABEL SOLUTION (Gp:) PARTNER ECOSYSTEM E-COMMERCE DEVELOPERS SHOPPING CART IT SERVICES Slide: 87 Other Placeholder: 87 Top reasons why big brands choose digital river world payments To expand brand and revenue globally.From a Swedish startup to a global game changer in the music industry, Spotify has relied on Digital River to process 100% of credit and debit card transactions and subscriptions worldwide. To optimize card acceptance rates and increase conversion.Vistaprint relies on Digital River’s fully underwritten position to optimize its business across the European Union at the highest acceptance rates in the industry. To increase local lift by offering local payment methods international customers prefer.Ticketmaster has trusted Digital River since 2007 to grow business through locally preferred payment methods including Internet banking connections. To scale investments in time and money around existing business models, processes and systems.Digital River handles transactions across more than 100 merchant IDs for Expedia, back office integrations and develops reporting specific to their needs and processes. Slide: 88 Other Placeholder: 88 COUNTRIES SERVED BY SPOTIFY Customer example #1: Spotify # of PROCESSED TRANSACTIONSFOR TOTAL SPOTIFY SUBSCRIBERS HISTORYCustomer since 2007Expanded into 30 countriesSupport 16 languages, 16 currencies Slide: 89 Other Placeholder: 89 Customer example #2: kaspersky protecting Kaspersky from fraud on a global scale OVERALL ATTACK RATE DROPPED FROM 28% TO 5% Slide: 90 Other Placeholder: 90 Customer example #3: Ticketmaster Connecting European Sites to Key Payment Methods HISTORYCustomer since 2007Supporting 11 payment methods for seven global sitesWork closely on fraud and chargeback mitigation Slide: 91 Body: Paul Kuykendall, Senior Director, Payment Systems Product DevelopmentTicketmaster Title: Ticketmaster Other Placeholder: 91 Slide: 92 Other Placeholder: 92 Ticketmaster – a brief history 1976 – Founded by two ASU staffers Phoenix, AZ – First operation established in Albuquerque, NM. (One early client gave 99-year license.) First ticketed concert was Electric Light Orchestra at UNM. 1978 – First international clients signed in Oslo, Norway1980 – First Canadian clients (National Arts Centre in Ottawa)1994 – World Cup (highest-attended single event in US history) Early International business by establishing client relationships. 1981 – Ticketmaster UK established in London1987 – Ticketmaster Canada established in Toronto1988 – Ticketmaster operations launches in Australia1997 – Ticketmaster Ireland launches as joint venture1998 – Ticketmaster operations established in Mexico2001 – Ticketing operations in Norway (Billettservice)2002 – Acquired Ticket Service Nederland; acquired BILLETnet to expand in Denmark2004 – Ticketing operations in Sweden and Finland2005 – Ticketmaster New Zealand and Ticketmaster Deutschland2006 – Spain (Tick Tack Tickets) and Turkey (Biletix)2006 – China operations through joint venture with Gehua Later international business grown through new in-country operations and acquisitions. Slide: 93 Other Placeholder: 93 Global presence Slide: 94 Other Placeholder: 94 markets served by digital river world payments Slide: 95 Other Placeholder: 95 TICKETMASTER’s future International expansion HEAD SOUTH OF THE BORDER FOR SEASONALITYMexico (30% owned)BrazilArgentinaColombiaSouth Africa STRATEGICALLY COMBINE TICKETING & PROMOTINGAustralia – large promoterTop 20 music markets, concerts and ticketing EXPAND OUR RESALE CAPABILITIESGiving ultra-safe ticket exchange and resale capabilities to fans.AustraliaIreland/Netherlands Slide: 96 Other Placeholder: 96 TICKETMASTER PARTNERSHIP WITH DRWP SELECTION PROCESS – CRITERIAAvailability of local methods of paymentIBP, iDeal, Direct Debit, SofortuberweisungMarket presence, access to acquirersPerformance/reliability of servicesConsolidated reporting, where appropriate.Cost (more appropriately…value proposition) COMPETITIVE ANALYSISDigital River World PaymentsGlobal PaymentsWorldpayFirst DataCybersourceSmaller playersDIY OVERALL SATISFACTION & CHALLENGESVery high reliability, performance and uptimeExcellent service and attention to detailCost – reasonable, but Nordics are least comfortableRoadmapBelgiumUAENordic Markets requesting more IBPOther markets (small on their own, but accumulate) Slide: 97 Body: Paul Kuykendall, Senior Director, Payment Systems Product DevelopmentTicketmaster Title: Ticketmaster Q&A Other Placeholder: 97 Slide: 98 Body: Scott Heimes, chief marketing officerDigital River Title: Marketing services Other Placeholder: 98 Slide: 99 Other Placeholder: 99 Marketing services drives commerce DEEP EXPERTISE GLOBAL REACH DRIVE GROWTH DIGITAL RIVER’S BRAND PROMISE Our marketing services drive customer acquisition and conversion to deliver revenue growth for our customers. CUSTOMER BENEFITS Slide: 100 Other Placeholder: 100 Marketforce – A customer-focused Digital Agency Site optimizationTrial optimizationProduct recommendationsPromotion optimizationSite abandonment Paid searchAffiliate marketingDisplay advertisingSearch engine optimization Email marketingDynamic personalizationCRM strategiesLoyalty programs Web analyticsCross-channel attribution WE HELP DRIVE GROWTH FOR CUSTOMERS THROUGH ACQUIRING, CONVERTING AND RETAINING BUYERS ACQUISITION ADVANCED ANALYTICS CONVERSION RETENTION Tag managementCustomer satisfaction analytics Slide: 101 Other Placeholder: 101 GLOBAL DIGITAL MESSAGING PLATFORMFocus: Drive direct email revenueUse email to maximize the performance of multichannel campaignsEmail, social, mobileAutomated, data-driven programs In-house customer servicesGlobal email delivery and supportFull, self-serve, or collaborative engagement STRATEGIC EMAIL OPTIMIZATION Multichannel integration Actionable data and analytics Unrivaled support Deliverability management bluehornet – enterprise Email Service Provider Digital River managed email programbegins YEAR 1 YEAR 2 CUSTOMER EXAMPLE Slide: 102 Title: Marketing partner ecosystem Other Placeholder: 102 (Gp:) PARTNER ECOSYSTEM Slide: 103 Other Placeholder: 103 Customer Example #1: Kaspersky marketforce 24 STORES 190 COUNTRIES 11 languages WORLDWIDE MARKETING SERVICESPaid search · Tag management · Cart abandonment · MVT · Email · Creative services · Analytics 11 LANGUAGES HISTORYCustomer since 2009Challenge: Providing consumers around the globe with a localized, optimized shopping experience Slide: 104 Other Placeholder: 104 Customer example #2: ALLEN EDmONDS bluehornet CUSTOMER DATACAPTURE CUSTOM MESSAGING OPTIMIZED SENDS EMAIL ENGAGEMENT ACQUISITION CHANNEL HISTORYCustomer since 2011Challenge: Using customer behavior data to increase sales revenue and drive targeted engagement SEGMENTATION& TARGETING RESULT:196% YOY INCREASE IN EMAIL CAMPAIGN REVENUE Slide: 105 Body: Stefan Schulz, chief financial officerDigital river Title: Financial overview Slide: 106 Title: Revenue and profit history In Millions, NON-GAAP Other Placeholder: 106 *See appendix slide for definition; op income and EBITDA excludes stock-based compensation among other items Slide: 107 Title: OUR business going forward Other Placeholder: 107 (Gp:) Educational Services DRES (Gp:) Affiliate Marketing (Gp:) SMB (Gp:) CD Production (Gp:) Email Marketing Digital Physical DRWP LML DIVESTING COMMERCE PAYMENTS ENTERPRISE COMMERCE SUPPORTING $343M* $18M* $25M* *2012 Revenue Slide: 108 (Gp:) TOTAL= $368 Title: Historical Revenue: Payments And Commerce in Millions Other Placeholder: 108 2012 REPORTED 2012 PRO FORMA COMMERCE SUPPORTING COMMERCE PAYMENTS $308 $343 $ 25 (Gp:) DIVESTING (Gp:) $ 18 $ 78 TOTAL= $386 (Gp:) TOTAL= $386 Slide: 109 Title: 2013 guidance $ In Millions Other Placeholder: 109 *See appendix slide for definition; op income and EBITDA excludes stock-based compensation among other items Slide: 110 Title: 2013 and Near term model impacted by INCREMENTAL investments Other Placeholder: 110 2013 TOTAL PROJECTED CASH SPENDTechnology & infrastructure $13M (CAPEX)Technology & infrastructure 4M (OPEX)Platform evolution (Dev) 5M (OPEX)Marketing (brand & email) 5M (OPEX)Total $27M 2013 TOTAL PROJECTED OPERATING EXPENSESTechnology & infrastructure $7M(New data centers) Platform evolution (Dev) 5MMarketing (brand & email) 5MPlus2012 Capital investments expensed in 2013 5MTotal 2013 Op Ex Impact $22M Slide: 111 Title: investments expected to decline over time Other Placeholder: 111 2013 2014 2015 30 20 10 YEAR IN MILLIONS ($) Slide: 112 Other Placeholder: 112 OPERATIONSImplement global procurement disciplines to reduce third party spendMigrate and consolidate data centersAutomate back office processes to reduce G&A expense TECHNOLOGYDeploy world-class product disciplinesTransition to open commerce through modular design and APIsIntegrate deeper into Microsoft stack ORGANIZATIONOptimized management span of controlEnhanced leadership development TECHNOLOGY PLATFORM, TRANSFORMATION AND EXECUTION OFFERING: PLATFORM EVOLUTION, INFRASTRUCTURE INVESTMENT, INNOVATION ROADMAP $8M-$10M $3M-$4M $3M-$4M $1M-$2M SAVINGS Transformation PLAN will lead to 2014 savings of $15M - $20M in operating expenses COMMERCIALOptimize customer segmentation & targetingImprove strategic account managementImprove sales force productivity Slide: 113 Title: Progress monitoring - Key Performance Indicators we will provide each quarter Other Placeholder: COMMERCE Other Placeholder: 113 (Gp:) Q2’13 Gross Volume (Gp:) $ 2 B -6% PAYMENTS (Gp:) Q2’13 Loyalty Index (Gp:) 99% Annualized metrics (Gp:) Q2’13 Loyalty Index (Gp:) 92% (Gp:) Q2’13 Gross Volume (Gp:) $25 B Slide: 114 Title: Target FINANCIAL MODEL Other Placeholder: 114 *See appendix slide for definition; op income and EBITDA excludes stock-based compensation among other items Slide: 115 Title: PRELIMINARY thoughts on 2014 Other Placeholder: Investments in our technology and in our platform will extend through 2014We expect a slight decline in 2014 revenueNon-GAAP EPS should be relatively flat with 2013Continue to expect growth in revenue and Non-GAAP EPS in the second half of 2014 Other Placeholder: 115 Slide: 116 Title: Capital allocation overview As of june 30, 2013 Other Placeholder: 116 WORKING CAPITAL SHAREBUYBACKS M & A $612M $94MCustomer Cash $213MOperating / Available For Use(78% Non-US Domiciled) CASH AND INVESTMENTS ON BALANCE SHEET $305MConvertible Debt(100% likely payable in 2 years) A total of $190M in Capital has been deployed over the past two years ($134M in Share Buybacks and $56M in M&A) Slide: 117 Body: David Dobson, chief executive officerDigital River Title: SUMMARY Other Placeholder: 117 Slide: 118 Other Placeholder: 118 The new digital river (Gp:) WHO IS DIGITAL RIVER? (Gp:) OUR MISSION AND VISION (Gp:) WE HAVE A FOCUSED STRATEGY (Gp:) OUR OPPORTUNITY IS SIGNIFICANT (Gp:) Leading Commerce SaaS company Growth drivers: Commerce-as-a-Service and Digital River World PaymentsKey differentiators: Our commerce business infrastructure, commerce expertise, multi-tenant SaaS platform, world-class cloud infrastructure and global footprint (Gp:) Mission: We drive customer growth through our global commerce expertiseVision: We set the standard for global commerce technology and services (Gp:) Invest in our core technology and new offeringsAllocate resources and expertise to grow in commerce and payments segmentsImprove operational excellence (Gp:) Market is large and moving to where we have strengthGlobal customer expansion and strong growth in paymentsWe expect to return to growth in 2H’14Longer term; at least market growth rates Slide: 119 Title: Q & A Other Placeholder: 119 Slide: 120 Other Placeholder: 120 Slide: 121 Title: Appendix Other Placeholder: 121 Slide: 122 Title: Non-Gaap DEFINITION Other Placeholder: Non-GAAP operating income (loss) is computed by adjusting GAAP operating income (loss) as reported on the company’s statement of operations by adding back, when applicable, amortization of acquisition-related intangibles, stock-based compensation expense, intangible impairments, restructuring related costs, litigation settlement related costs, acquisition and integration costs, and goodwill impairments. EBITDA is calculated by adding back depreciation expense to non-GAAP operating incomeNon-GAAP net income (loss) is computed by adjusting GAAP pre-tax income (loss) as reported on the company’s statement of operations by adding back, when applicable, amortization of acquisition-related intangibles, stock-based compensation expense, intangible impairments, restructuring related costs, litigation settlement related costs, acquisition and integration costs, realized and unrealized investment gains or losses, and goodwill impairments, net of a 21 percent tax rate. Non-GAAP diluted earnings per share is calculated using the “if-converted” method with respect to the issuance of the company’s 2004 and 2010 convertible notes. In computing non-GAAP diluted earnings per share, if an increase in earnings per share will not result, adjust non-GAAP net income to add back debt interest and issuance cost amortization expenses, net of the tax benefit, and then divide this amount by fully diluted shares outstanding. This amount, representing the fully diluted earnings computation, is selected to represent non-GAAP diluted earnings per share for each period presented.Reconciliations of historical non-GAAP figures within this presentation to GAAP figures are included in previously disseminated earnings releases. Fiscal year 2013 non-GAAP earnings per share guidance is reconciled to GAAP guidance within the second quarter of 2013 earnings release. The non-GAAP reconciling items for our previously disclosed fiscal year 2013 guidance are consistent with the reconciling items for our fiscal year 2013 pro-forma projections within this presentation. Previously disseminated earnings releases can be found on the investor page of our website. Other Placeholder: 122