SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 OF

THE SECURITIES EXCHANGE ACT OF 1934

| For the month of November, 2005 |

| Commission File Number 000-29872 |

ATI TECHNOLOGIES INC.

(Translation of Registrant's Name into English)

1 Commerce Valley Drive East, Markham, Ontario, Canada L3T 7X6

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F Form 40-F X

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes No X

Page 1 of 75 Pages

Index is located on Page 2

1 of 75

| INDEX | |||

| Document | Page Number | ||

| 2005 Annual Report | 3 | ||

| Signature Page | 75 | ||

2 of 75

A T I T E C H N O L O G I E S I N C . 2 0 0 5 A N N U A L R E P O R T

3 of 75

ATI Technologies Inc. is a world leader in the design and manufacture of innovative 3D graphics and digital media silicon solutions. An industry pioneer since 1985, ATI is the world’s foremost graphics processor unit (GPU) provider. ATI is dedicated to delivering leading-edge performance solutions for the full range of PC and Mac desktop and notebook platforms, workstation, digital television, game console and handheld markets. With 2005 revenues of approximately $2.2 billion, ATI has more than 3,300 employees in the Americas, Europe and Asia. ATI common shares trade on NASDAQ (ATYT) and the Toronto Stock Exchange (ATY).

4 of 75

T H E P O W E R O F I N N O V A T I O N

IN 1985, THE PC WAS IN ITS INFANCY. THE CELL PHONE WAS STILL A NOVELTY. ONLY 2,000 COMPUTERS WORLDWIDE HAD ACCESS TO THE INTERNET.

TWENTY YEARS LATER, WE FIND OURSELVES AT THE HEART OF A CONNECTED VISUAL WORLD – A KEY PLAYER IN THE DIGITAL REVOLUTION THAT HAS FUNDAMENTALLY ALTERED THE WAY WE ENGAGE, EDUCATE AND ENTERTAIN.

MUCH HAS CHANGED, BUT NOT THIS: WHEN YOU BELIEVE IN THE POWER OF INNOVATION, EVERYTHING IS POSSIBLE.

5 of 75

2 ATI 2005

6 of 75

ATI 2005 3

7 of 75

To Our Shareholders

S E E I T. S A V E I T. S A V O R I T.

8 of 75

| 1985 | On August 18, 2005, ATI Technologies celebrated its 20th anniversary. Since its inception, ATI has been recognized as a world leader in the supply of graphics, video and multimedia products. An industry pioneer, ATI creates revolutionary products that offer customers the ultimate visual experience for their desktop and notebook PCs, digital televisions, mobile phones and game consoles. ATI’s success is firmly built upon the strength of its 3,300 employees worldwide, product excellence and an unwavering commitment to customer satisfaction. | • ATI Technologies Inc. is established on August 20, 1985 • ATI develops its first graphic controller and introduces its first graphics board product |

ATI HAS BEEN A PIONEER AT THE FOREFRONT OF THE GRAPHICS INDUSTRY SINCE IT WAS FOUNDED TWENTY YEARS AGO WITH SIX EMPLOYEES WHO INSTILLED A PASSION FOR INNOVATION AND A VISION OF GREAT THINGS TO COME.

TODAY, THAT VISION HAS BECOME A REALITY, AS OUR REVENUES HAVE SURPASSED $2.2 BILLION, OUR TEAM HAS GROWN TO MORE THAN 3,300, AND AS OUR TOTAL ADDRESSABLE MARKET HAS EXPANDED DRAMATICALLY TO MORE THAN $14 BILLION. ONCE LIMITED TO THE PC, OUR MULTIMEDIA PROCESSORS HAVE BECOME A TECHNOLOGICAL CORNERSTONE OF TODAY’S MOST PERVASIVE CONSUMER ELECTRONICS, INCLUDING MOBILE PHONES, DIGITAL TELEVISIONS AND GAME CONSOLES.

Stepping it up

Innovation is a critical aspect of bringing world-class products to market; however, execution is just as important. In 2005, we discovered that the company’s rapid growth of the last few years had left some gaps in our organizational structure, which impacted our ability to meet a number of our goals. While the first half of fiscal 2005 consisted of our two strongest revenue quarters ever, we lost momentum in the second half amid slower than expected product ramps, a critical product delay, operational challenges and a slowdown in demand for certain products. These factors contributed to reduced revenues and gross margins, an inventory write-down in the fourth quarter, and disappointing financial results for the year.

We are moving quickly to improve our effectiveness in these areas with initiatives aimed at controlling expenses, reducing product costs and improving product margins, expanding our markets and market share, and optimizing our supply chain to improve customer deliveries. In short, we are taking the steps needed to ensure that our vigorous pace of innovation will be accompanied by world-class execution.

Gross margin improvement remains a top priority in 2006. While we fell short of our target margins in the latter part of the year, we are focused on driving margin improvement with the initiatives above and through compelling new desktop products and higher-margin digital consumer products.

ATI 2005 5

9 of 75

| 1987 | • ATI releases EGA Wonder™ and VGA Wonder™, a single card able to work with every graphics interface, software and monitor on the market, providing faster graphics than was previously possible on conventional personal computers | 1989 | • ATI assists in establishment of VESA standard in the graphics industry |

TO OUR SHAREHOLDERS

| TOGETHER, WE WILL CONTINUE TO ENTERTAIN, EDUCATE AND ENGAGE CONSUMERS ON THE MOST PERVASIVE AND POWERFUL DEVICES IN THE CONNECTED VISUAL WORLD. |

Innovative products, unlimited possibilities

As it has for the last two decades, innovation once again led the way in fiscal 2005:

- The Radeon X1000 family of 90 nanometer GPUs, launched in October 2005, have reinvigorated our desktopproduct stack and reclaimed top-to-bottom performance leadership. Additional product introductions over the nextfew months will bring to notebook PC users new levels of performance, power management and overall value.

- We introduced important new platform technologies, such as AvivoTMand CrossFireTM. Leveraging our expertisein PC and DTV visual quality, the Avivo display engine allows users to experience superb video quality on thePC and enjoy premium high-definition video content based on emerging standards such as Blu-Ray and HD-DVD.

CrossFire, our multi-GPU technology aimed at gaming and other PC enthusiasts, is yet another exciting platformstrategy with positive implications for both our GPU and chipset businesses. - Superior performance and functionality have made our Radeon Xpress 200 the industry’s fastest-growingintegrated chipset product line and a significant part of our business, accounting for nearly 20 percent of ourtotal revenues in the fourth quarter. We remain laser-focused on delivering a new wave of cost-improvedintegrated solutions, and improving chipset gross margins.

- In the handheld or mobile phone market, we shipped more than 40 million Imageon processors in fiscal 2005and expanded our customer base to now include four of the top six global handset OEMs. ATI remains extremelywell positioned as the mobile phone continues to claim its share in the “battle for the belt”. We will continueto bring new innovative technologies, such as mobile TV, 3D graphics, and high-quality audio to our Imageonline of multimedia co-processors in 2006.

- Revenues from our Xilleon line of digital television products grew nearly 70%, while continued innovation andinvestment has paved the way for long-term growth. The recently launched Xilleon 240, which combines frontand back-end functionality onto a single chipset, has garnered numerous design wins and is expected to be amajor driver of our DTV revenues in 2006. We continue to focus on the North American market while developingour offerings for international markets such as Europe and China.

- With the Microsoft Xbox 360 GPU, we introduced groundbreaking features such as a unified shaderarchitecture and intelligent memory, and helped to usher in the era of high-definition gaming. We remain veryexcited about our relationships with Microsoft and Nintendo as they bring the next generation of breathtakingnew consoles to market.

6 ATI 2005

10 of 75

| 1991 | • ATI releases ATI Mach8™ in both chip and board products, capable of processing graphics independently of the central processing unit (CPU) | 1992 | • ATI releases Mach32™, an integrated graphics controller and graphics accelerator in one chip | • ATI releases VLB (VESA Local Bus) products and, after that, PCI (peripheral component interconnect) bus products |

Looking ahead

With its incredible versatility, the PC is quickly becoming the centerpiece of the modern home. Consumers are craving richer and more immersive visual experiences, and are turning to their PCs as a storage and delivery mechanism for music, television and other forms of multimedia and digital content. At the same time, its connectivity with other consumer electronics devices in the digital home is driving the industry towards seamless convergence. As a result, the need for powerful and intelligent GPUs to drive the ultimate visual experience has never been greater. With its unsurpassed expertise in visualization on PCs, Digital TVs, handheld devices and gaming platforms, ATI is uniquely poised to seize the opportunities that lie ahead in this emerging connected visual world.

We are entering fiscal 2006 with the strongest product line-up in our history, with top-to-bottom technology leadership across our core market segments, together with exciting platform technologies to drive visual processing to new heights. While challenges remain, we are confident in our ability to deliver new products and platform technologies, make the required changes to drive growth in our PC and digital consumer businesses, and improve our financial performance.

Before closing, we would like to thank our many business partners, customers, employees and shareholders for their ongoing support. Together, we will continue to entertain, educate and engage consumers on the most pervasive and powerful devices in the connected visual world.

| /s/ K.Y. Ho | /s/ David E. Orton | |

| K.Y. Ho | David E. Orton | |

| Chairman of the Board | President and Chief Executive Officer | |

| November 1, 2005 |

MESSAGE FROM THE BOARD OF DIRECTORS AND MANAGEMENT:

After more than 20 years with ATI, as a principal founder, CEO and Chairman, K.Y. Ho has decided to embark upon a well deserved retirement. The Board of Directors and management would like to extend their sincere thanks and gratitude to K.Y. for his vision and leadership in guiding ATI over the past 20 years to its position as the leading graphics company in the world.

Best wishes for the future, K.Y.

ATI 2005 7

11 of 75

| 1993 | • ATI becomes a public company, trading on the Toronto Stock Exchange (TSX), trading symbol: ATY | 1994 | • ATI introduces the Mach64 chip and a new set of graphics boards -- the first graphics boards to accelerate motion video | • ATI localizes application software in 13 different international languages |

Management’s Discussion and Analysis

Table of Contents

The MD&A is presented in seven sections:

About Our Business– p. 9

describes our business, target markets, objectives, strategy and outlook.

Fiscal 2005 Overview and Highlights– p. 13

offers a brief look at our performance and key highlights in fiscal 2005.

Business Outlook for Fiscal 2006– p. 16

provides our business outlook for next fiscal year.

Financial Results Analysis– p. 17

provides a detailed review of our financial and operating performance for the past three years.

Liquidity and Capital Resources– p. 26

explains how we manage our cash and capital resources.

Risks and Uncertainties– p. 30

examines uncertainties and challenges that could affect our business.

Our Critical Accounting Policies– p. 32

describe our critical accounting policies and the key estimates and assumptions that management has made in the preparation of our financial statements. It also provides a description of changes in accounting standards used to prepare our financial statements.

Please refer to the glossary on page 67 for a description of some of the technical terms used throughout this MD&A to describe our business.

This Management’s Discussion and Analysis (“MD&A”) comments on ATI’s operations, performance and financial condition for the two fiscal years ended August 31, 2005 and 2004. The MD&A should be read in conjunction with ATI’s 2005 consolidated financial statements and accompanying notes beginning on page 38 of this Annual Report. All tabular amounts are expressed in thousands of U.S. dollars except per share amounts. Unless otherwise noted, “2005” and “2004” refer to our fiscal 2005 and fiscal 2004 years, respectively. This MD&A is based on information available to us at November 1, 2005, unless otherwise indicated.

As of our fiscal 2005 year-end, an evaluation was carried out under the supervision of and with the participation of Management, including our Chief Executive Officer and Chief Financial Officer, of the effectiveness of our disclosure controls and procedures. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that the design and operation of these disclosure controls and procedures were effective as of August 31, 2005, the end of the period covered by the Annual Report, to ensure that material information relating to ATI Technologies and its consolidated subsidiaries would be made known to them by others within those entities.

About Forward-looking Statements

Forward-looking statements look into the future and provide an opinion as to the effect of certain events and trends on the business. Forward-looking statements may include words such as “plans”, “intends”, “anticipates”, “should”, “estimates”, “expects”, “believes”, “indicates”, “targeting”, “suggests” and similar expressions.

This Annual Report and MD&A, and in particular our Business Outlook for Fiscal 2006 on page 16 and the discussion of our Target Operating Model on page 11, contain forward-looking statements about ATI’s objectives, strategies, financial condition and results, as well as statements with respect to our beliefs, expectations, anticipations, estimates and intentions. These “forward-looking” statements are based on current expectations and various factors and assumptions. Accordingly, these statements entail various risks and uncertainties. The material factors and assumptions that were applied in making the forward-looking statements in this Annual Report and MD&A are as follows:

- the expected rate of growth of the PC andConsumer markets;

- the expected mix of discrete and integratedchipsets that will be sold in the PC market;

- our expected market share across variouscustomers and product segments;

- our expected future design wins both in thePC and Consumer markets;

- our expected product and production costs;

- the timely introduction of our new productsfor the PC and Consumer markets;

- the expected product specific average sellingprice (“ASP”);

- in the digital television (“DTV”) segment, theexpected rate of consumer adoption of high-definition television (“HDTV”); and;

- our overall competitive position and thecompetitiveness of our current and futureproducts.

It is important to note that:

- Unless otherwise indicated, forward-lookingstatements in this Annual Report andMD&A describe our expectations as ofNovember 1, 2005.

8 ATI 2005

12 of 75

| 1995 | • ATI becomes the first graphics company to ship Mac-compatible graphics boards, proving ATI is committed to both PC and Mac platforms | • ATI announces an agreement with United Microelectronics Corporation (UMC) and other joint ventures to build a semiconductor manufacturing facility in Taiwan |

- We caution readers not to place undue relianceon these statements as our actual resultsmay differ materially from our expectations ifknown and unknown risks or uncertaintiesaffect our business, or if our estimates orassumptions prove inaccurate. Therefore, wecannot provide any assurance that forward-lookingstatements will materialize.

- We assume no obligation to update or reviseany forward-looking statement, whether as aresult of new information, future events orany other reason.

For a description of material factors that could cause our actual results to differ materially from the forward-looking statements in this Annual Report and MD&A, please see the Risks and Uncertainties section of this MD&A on page 30 and Item 3.12 “Narrative Description of the Business – Risks and Uncertainties” in our 2005 Annual Information Form.

In this MD&A, the termsATI,we,usandourrefer to ATI Technologies Inc. and its subsidiaries.

Additional informationregarding ATI and our business is contained in our filings with securities regulatory authorities, including our Annual Information Form and Management Information Circular. These documents are available on SEDAR atwww.sedar.comor on our company website atwww.ati.com. Our Form 40-F and other filings we make with the U.S. Securities and Exchange Commission are available atwww.sec.gov.

| ABOUT OUR BUSINESS |

ATI Technologies Inc. is one of the world’s leading providers of graphics processors and technologies. Our graphics processing units (GPUs) are highly specialized semiconductors that increase the speed, complexity and visual fidelity of digital images that can be displayed on graphical interfaces. Our products are found in desktop and notebook computers (PCs), and consumer electronic devices such as mobile phones, digital televisions and game consoles.

At August 31, 2005, we employed more than 3,300 people in the Americas, Europe and Asia. Our common shares trade on the NASDAQ Stock Market under the symbol “ATYT” and on the Toronto Stock Exchange under the symbol “ATY”.

Business Segments

Effective the first quarter of fiscal 2005, we began to report our financial results in two segments –PCandConsumer– reflecting the two primary markets for our semiconductor graphics products.

- The PC segment includes all 3D graphics,video and multimedia products, and chipsetsdeveloped for use in desktop and notebookcomputers, including professional workstations,servers and home media PCs.

- The Consumer segment includes products used in mobile phones, PDAs, DTVs and consumer electronics, as well as royalties and contract engineering services derived from mobile phone and game console products.

Seenote 17to the consolidated financial statements for more information on our segmented reporting.

Products and Target Markets

We develop products and technologies for the markets set out below.Current product information and specifications can be found on our website at www.ati.com.

ATI 2005 9

13 of 75

| 1996 | • | ATI releases the first 3D chip in the graphics industry. Sales exceed one million chips | • | ATI establishes ATEL (ATI Ireland), the Company’s distribution headquarters in Europe | • | ATI announces Macintosh-based boards, making the Company the first manufacturer of PCI-based boards for the Mac, other than Apple itself | |

| One million chips sold |

| MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.) |

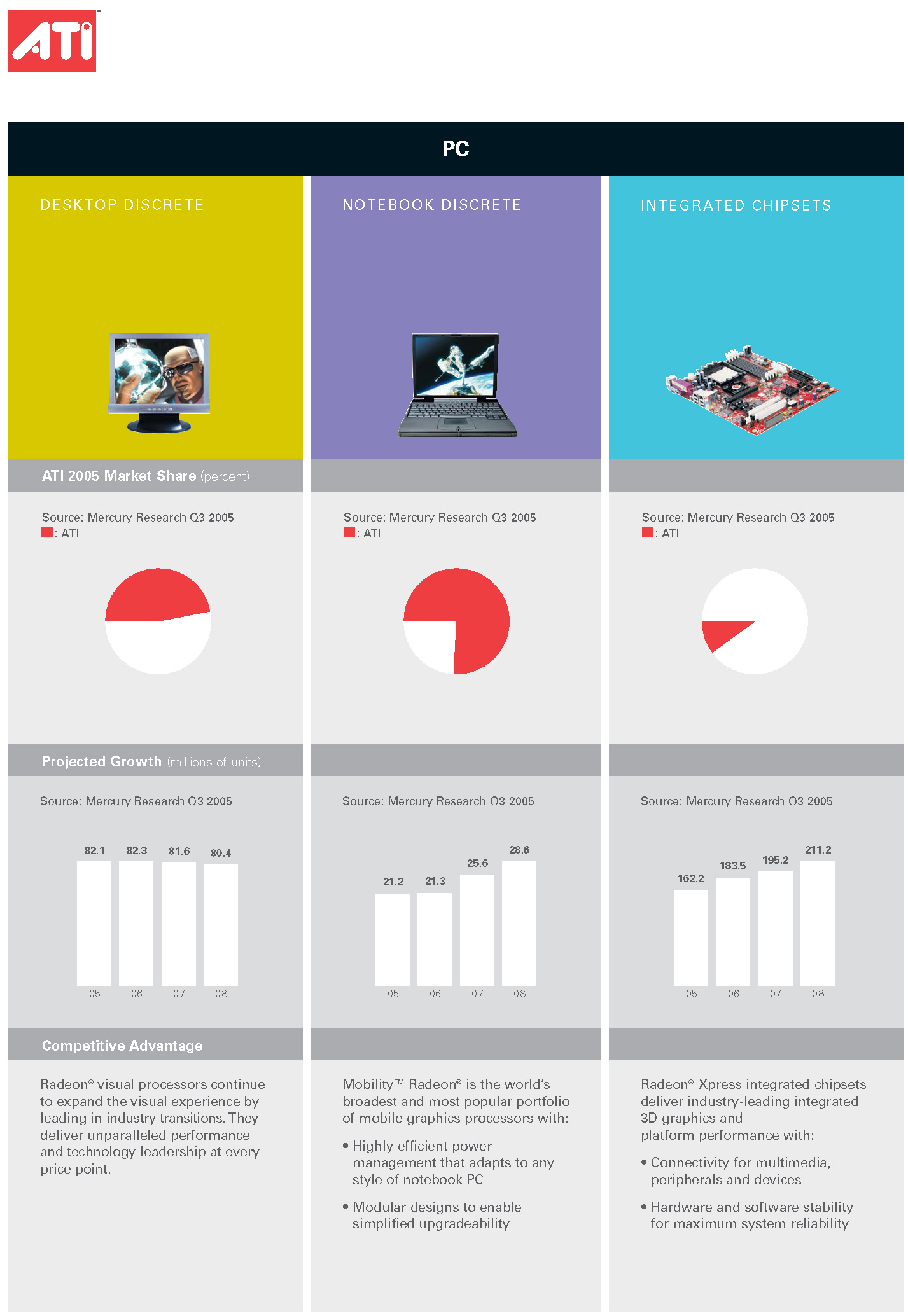

| THE PC SEGMENT INCLUDES ALL 3D GRAPHICS, VIDEO AND MULTIMEDIA PRODUCTS, AND CHIPSETS DEVELOPED FOR USE IN DESKTOP AND NOTEBOOK COMPUTERS, INCLUDING PROFESSIONAL WORKSTATIONS, SERVERS AND HOME MEDIA PCs. |

P C

| Desktop discrete | Notebook discrete | Chipsets (integrated and discrete) | ||

| Our desktop GPUs address desktop PC | Our notebook GPUs address the portable or | Our chipset products feature core logic | ||

| markets where customers expect high levels | laptop computer segment. In this category, | functionality, are targeted to motherboard | ||

| of performance and a compelling visual | low power consumption and visual | manufacturers and OEMs, and are available | ||

| experience. We cater to all four segments of | performance are the uppermost considerations | with or without integrated graphics. Our | ||

| the desktop PC market: value, mainstream, | of our customers. We focus on designing | Radeon Xpress 200 integrated chipsets for | ||

| performance and enthusiast. We also design | notebook GPUs that meet and exceed these | the desktop and notebook markets include | ||

| and build GPU solutions for the advanced | expectations in the enthusiast, performance | graphics functionality and are geared | ||

| workstation and home media markets. | thin, value mainstream, and thin and light | towards the value or price-sensitive segment | ||

| Our primary brands include Radeon | categories. Mobility Radeon is our brand for | of the PC market. Radeon Xpress CrossFire | ||

| (desktop products), FireGLTM(workstations) | notebook discrete products. | Edition chipsets do not contain integrated | ||

| and All-in-Wonder®(multimedia products). | graphics and are designed to be used in | |||

| conjunction with one or more discrete | ||||

| graphics chips in graphically demanding | ||||

| applications such as gaming. |

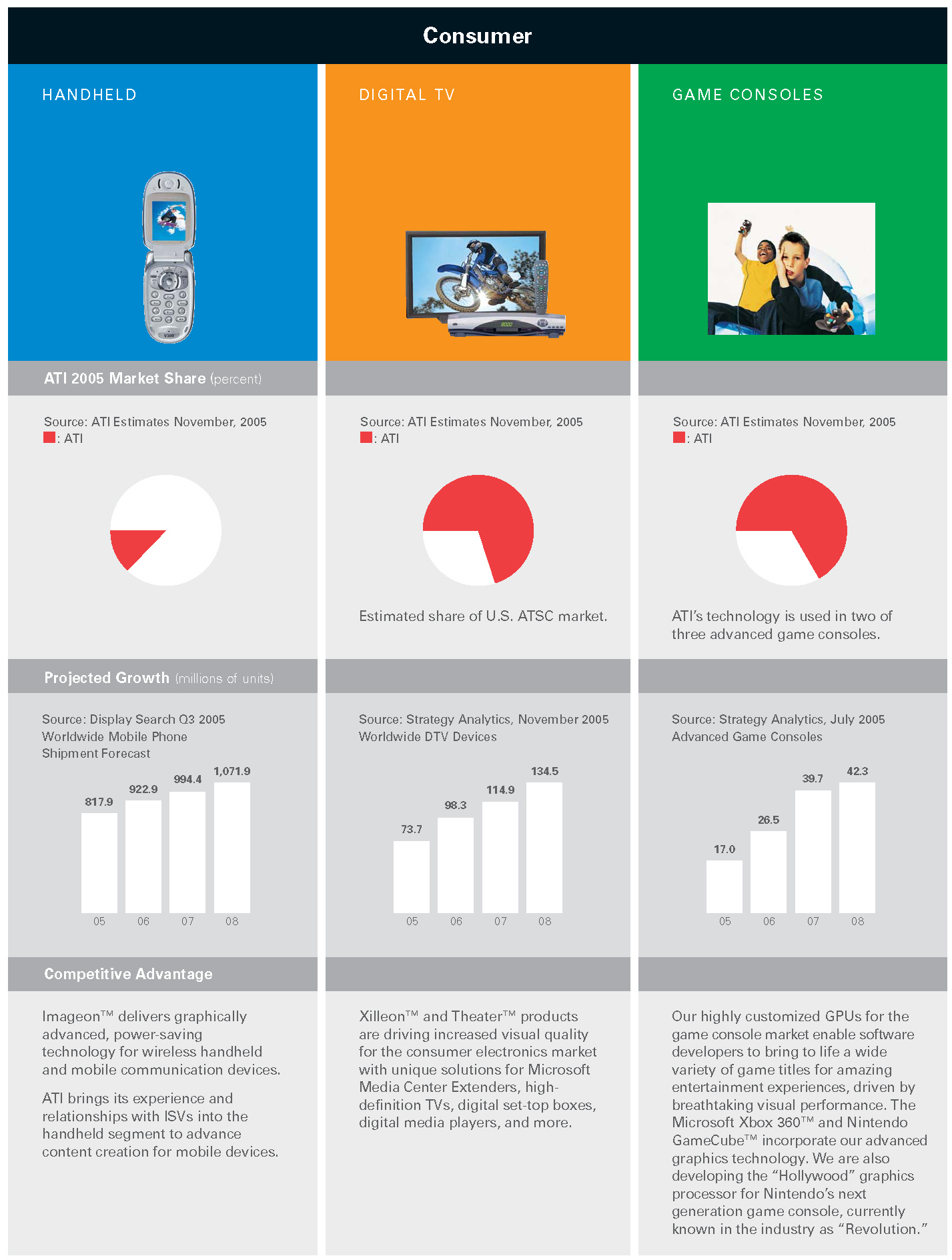

| THE CONSUMER SEGMENT INCLUDES PRODUCTS USED IN MOBILE PHONES, PDAs, DIGITAL TELEVISIONS (“DTVs”) CONSUMER ELECTRONICS, AS WELL AS ROYALTIES AND CONTRACT ENGINEERING SERVICES DERIVED FROM MOBILE PHONE AND GAME CONSOLE PRODUCTS. |

C O N S U M E R

| Handheld devices | Digital television | Game consoles | ||

| Our products are designed to provide | Our Xilleon and Theater products are cost- | In recent years, we have successfully | ||

| advanced visual and audio processing for | effective and highly integrated visual and | leveraged our core visual processing | ||

| color mobile phones and other handheld | signal processing solutions offered to DTV | technology into the game console market. | ||

| devices. Higher resolution panels, higher | and set-top box manufacturers. The U.S. | The Microsoft Xbox 360 and Nintendo | ||

| performing embedded processors as well | Federal Communications Commission has | GameCube both use our technology to deliver | ||

| as increased internal and removable storage | issued a mandate requiring the integration of | breathtaking graphics performance. We are | ||

| are contributing to the revolution in | digital tuners into TV sets by 2007. This | also developing the “Hollywood” graphics | ||

| handheld and mobile communication devices. | mandate, together with the superior picture | processor for Nintendo’s next generation | ||

| Our Imageon product line delivers advanced | quality and functionality offered by digital | game console, currently known | ||

| visual and audio processing along with | technology, is driving consumer interest and | in the industry as “Revolution.” | ||

| power saving technology and a high level | the adoption of DTV. | |||

| of integration to this market. |

10 ATI 2005

14 of 75

| 1996 | • ATI becomes the first graphics company to introduce a hardware chip to display computer graphics on a television | • ATI becomes the first graphics company to introduce a fully 3D-enabled chip for the notebook personal computer market | • ATI becomes the first graphics company to introduce a combination graphics and TV tuner card, enabling users to receive and capture analog TV signals |

Business Strategy and Objectives

We strive to be the foremost innovator and provider of advanced graphics processors and technology for the PC and digital consumer markets. We aim to deliver products that excite our customers while ensuring that our roadmap is aligned with key industry inflection points.

We use a “fabless” manufacturing strategy, whereby we outsource wafer manufacturing, assembly, testing and packaging to suppliers with established expertise in these areas. By outsourcing these functions, we are able to reduce our capital requirements for our PC, handheld and DTV products, lower our fixed costs, and focus resources on the design, development and marketing of our products.

We sell our products through a variety of channels and to different customers, including:

- original equipment manufacturers (OEMs);

- system integrators (SIs) who build our productsinto their PCs;

- original design manufacturers (ODMs) andadd-in-board manufacturers (AIBs) who addour products to their PC motherboard productsor graphic board products; and

- distributors and retailers, both traditionaland online.

In our game console business, rather than supplying actual graphics processors, we typically design highly customized and optimized GPUs in exchange for non-recurring engineering revenues (“NRE”) and royalty payments.

The following are the key strategies used to pursue our objectives:

Sustain product and technology leadership in our GPU products.Maintain performance leadership across our product segments and successfully drive the technology through all segments of the market.

Build a strong and sustainable franchise in the integrated chipset market.Grow our share of the growing desktop and notebook integrated chipset market with products that deliver superior graphics performance and maximum value in the industry.

Expand in select Consumer market segments. Continue to increase the revenue and profit contribution from new products for rapidly growing consumer electronics markets such as handheld, digital television and game consoles.

Innovate cost-effectively and improve operating and financial performance.Translate technology and industry leadership into strong financial performance for our shareholders, and drive efficiencies through scale.

Target Operating Model

The following contains forward-looking statements about our target operating model. Reference should be made to “About forward-looking statements” on page 8. For a description of material factors that could cause our actual results to differ from the forward-looking statements in the following, please see the Risks and Uncertainties section of this MD&A on page 30 and Item 3.12 “Narrative Description of the Business – Risks and Uncertainties” in our 2005 Annual Information Form.

The following discussion and table highlight the target operating model that we are working to achieve over the next several years. Our overall gross margins are highly dependent on product mix, as gross margins may vary considerably by line of business. Gross margins are also influenced by a number of other key factors, including the cost of input materials, the manufacturing yield of wafers received from foundries and the average selling prices of our products. The continuous change in these factors, most of which are beyond our control, cause our overall gross margins to fluctuate from quarter to quarter. As a result, the target operating model reflects our aspirations over the next several years.

ATI 2005 11

15 of 75

| 1997 | • | ATI ships 3D RAGE™ II+ DVD chip, the first graphic accelerator with motion compensation DVD software | • | ATI becomes the first graphics company to release products with full support for the Accelerated Graphics Port (AGP 2X) | • | ATI becomes the first graphics company to provide hardware support for DVD acceleration and display |

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

We are targeting to achieve gross margins in our core PC discrete business of approximately 32%–35% of revenues over the long term. Our target gross margin for chipsets is 25%–30% of revenues. However, we believe that our ability to leverage core technology and resources from the PC discrete business will allow us to maintain operating margins for chipsets that are close to those of PC discrete. In our Consumer segment, which typically carries higher gross margins than the PC segment, we are targeting to maintain gross margins above 40% of revenues.

We are targeting to achieve consolidated gross margins in the range of 34%–38% of revenues while maintaining operating expenses within the ranges listed below, and we are targeting to achieve pre-tax operating income (defined for this purpose as gross margin less research and development, selling and marketing, and administrative expenses) in the range of 11%–15% of revenues.

Please see the Risks and Uncertainties section of this MD&A for a list of the various risk factors that could impact gross margins and operating margins and prevent us from achieving our targets.

| ATI (CONSOLIDATED) | |||||||||||||||||||||||||

| Target | 2005 | 2004 | 2003 | ||||||||||||||||||||||

| As a percentage of revenues | 2005–2007 | Performance | Performance | Performance | |||||||||||||||||||||

| Gross margin | 34%–38% | 27.6% | 34.7% | 31.0% | |||||||||||||||||||||

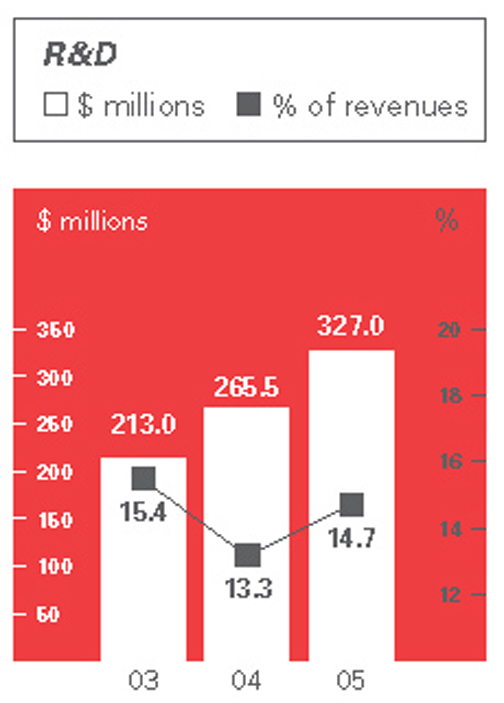

| R&D | 13%–15% | 14.7% | 13.3% | 15.4% | |||||||||||||||||||||

| SG&A | 8%–10% | 9.4% | 8.2% | 9.5% | |||||||||||||||||||||

| Pre-tax operating income | 11%–15% | 3.5% | 13.2% | 6.1% | |||||||||||||||||||||

Fiscal 2006 Strategic Priorities

The following summarizes our key strategic priorities for fiscal 2006:

- Drive PC growth through technology leadership, innovation and strategic platforms

- Increase integrated chipset gross margins through R&D and operational improvements

- Improve operational consistency in product delivery and ramping of new technologies

- Focus on new customers and accelerating growth in the Consumer business

- Implement expense management strategies including expansion into lower-cost geographies

12 ATI 2005

16 of 75

| 1998 | • ATI becomes the first company to introduce a complete set-top box design | • ATI secures more design wins with the top ten OEM personal computer manufacturers than any other graphics company • ATI, the AGP market leader, ships its ten millionth AGP chip | • ATI launches RAGE MAGNUM™ deemed to be OEM's best choice for fastest graphics performance for high-end PC graphics |

FISCAL 2005 OVERVIEW

AND HIGHLIGHTS

Despite solid progress in many key areas, overall financial performance in fiscal 2005 fell below expectations. Results for the first half were positive as we reported the two strongest revenue quarters in our history. However, a number of challenges prevented us from carrying this momentum into the latter part of the year and our performance in the second half suffered as a result.

These challenges included slower than expected product ramps, a critical product delay, operational issues, and a slowdown in demand for certain desktop discrete products in the third and fourth quarters. These factors, combined with the timing of new products, led to gross margin and inventory pressures in the second half of the year and an inventory write-down in the fourth quarter. In addition, sales of integrated chipsets, which currently have considerably lower gross margins than our other products, comprised almost 15% of total revenues in the second half as compared with approximately 6% in the first half. As a result, we were not able to achieve stronger earnings in fiscal 2005 compared to fiscal 2004 as we had anticipated in the MD&A in our 2004 Annual Report.

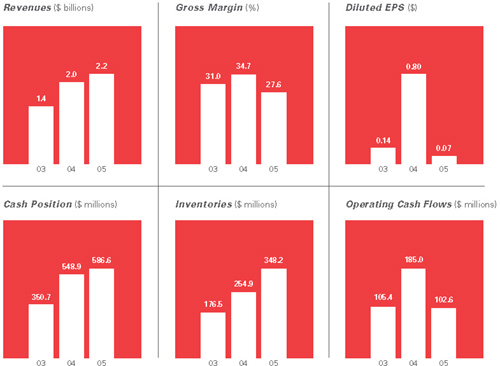

Among our accomplishments in fiscal 2005, revenue increased by 11% to approximately $2.2 billion and shipments approached 115 million units, both new records. We also gained overall market share in discrete graphics and gained significant traction in our consumer, workstation and desktop chipset businesses. Subsequent to fiscal year-end, we launched a new family of desktop discrete products, which we believe will strengthen our competitive position and contribute to stronger performance in discrete graphics going forward.

Looking ahead to fiscal 2006, we have undertaken a number of initiatives aimed at providing greater visibility into the dynamics of our distribution channels. We believe these initiatives will lead to a more solid foundation on which to build our business in fiscal 2006 and beyond.

Product Line Review and Highlights

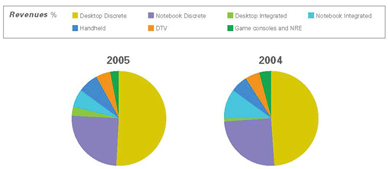

In addition to our segmented reporting, the following section includes a discussion of our results by key product line to give further insight into our results. For competitive reasons, the charts below and on the following two pages do not provide figures for revenue.Current product information and specifications can be found on our website at www.ati.com.

The chart below illustrates the composition of our consolidated revenues by major product line:

ATI 2005 13

17 of 75

| 1998 | • | ATI introduces next-generation RAGE™ 128 GL graphics chip delivering the world’s best performance and features to the high performance PC market | • | ATI’s new RAGE 128 VR graphics chip delivers a new level of 3D graphics performance on the motherboard | • | ATI’s RAGE LT PRO brings no- compromise 2D, 3D and DVD to leading notebooks |

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

P C P R O D U C T S

|

| ||

|

| ||

|

| ||

|

|

14 ATI 2005

18 of 75

| 1998 | • ATI becomes the first graphics company to intro- duce a DTV-enabled chip that allows users to watch DVD on a personal computer | • K.Y. Ho, President & CEO, selected as Canada's Entrepreneur of the Year |

C O N S U M E R P R O D U C T S

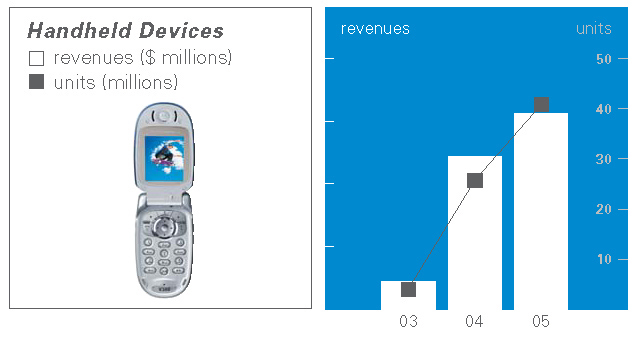

| • | Revenue grew nearly 30% to approximately 7% of consolidated revenues in fiscal 2005. | ||

| • | Shipments increased nearly 60% and exceeded 40 million units. | |||

| • | Ended the year with design wins from four of the top six mobile phone manufacturers. | |||

| • | Acquired CuTe Solutions Private Limited (CuTe), of India, with expertise in audio and digital media solutions. | |||

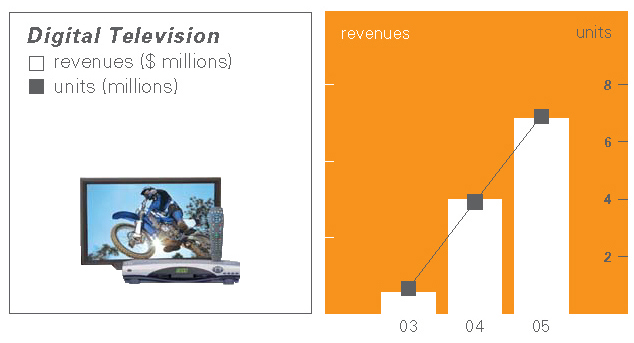

| • | Revenue was up 70% to nearly 5% of consolidated revenues. | ||

| • | Shipments increased 80% and approached seven million units. | |||

| • | Maintained strong market share and secured design wins with leading DTV manufacturers. | |||

| • | Acquired cable modem technology from Terayon Communication Systems Inc. (Terayon), extending ATI's leadership in DTV as the industry moves towards interactive digital cable ready (IDCR) technology. | |||

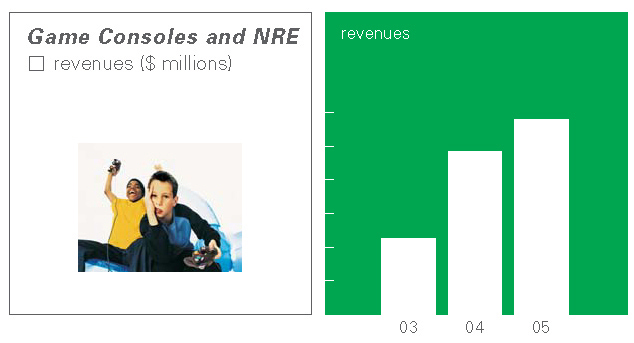

| • | Revenue from royalties and engineering revenues increased approximately $10 million and accounted for approximately 3% of consolidated revenues. | ||

| • | Introduced the GPU for the Microsoft Xbox 360 based on 90 nanometer process technology. | |||

| • | Continued development of graphics technology for Nintendo's next generation game console, Revolution, anticipated in 2006. |

ATI 2005 15

19 of 75

| 1999 | • K.Y. Ho, President & CEO, selected as one of the top 25 business leaders in the world byBusiness Week Magazine | • ATI announces RAGE Mobility M1 – the world’s first notebook PC graphics accelerator with 8MB of integrated memory |

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

BUSINESS OUTLOOK FOR FISCAL 2006

The following contains forward-looking statements about ATI’s business outlook for fiscal 2006. Reference should be made to “About forward-looking statements” on page 8. For a description of material factors that could cause our actual results to differ materially from the forward-looking statements in the following, please see the Risks and Uncertainties section of this MD&A on page 30 and Item 3.12 “Narrative Description of the Business – Risks and Uncertainties” in our 2005 Annual Information Form.

PC

Our success in the PC segment in fiscal 2006 will depend on our ability to introduce and deliver new products in a timely fashion, improve operational efficiencies, manage the ongoing PCI Express and lead-free transitions, and transition to advanced process technologies. We are further working to ensure that we are well-positioned to capitalize on future industry inflection points, including the introduction of Microsoft’s next operating system, Windows Vista, expected by the industry to launch in calendar 2006.

Subsequent to our fiscal year-end, we launched a family of desktop discrete products based on 90 nanometer process technology that targets the enthusiast, performance and mainstream segments of the market. We also began volume shipments of Crossfire, our high-performance multi-GPU chipset platform. In the first half of fiscal 2006, we expect to introduce new 90 nanometer discrete products for the notebook market. One of our key priorities in the PC segment for the coming year is to successfully roll out these new products and reassert broad-based technology leadership in PC graphics.

We expect our sales from integrated chipsets in fiscal 2006 will continue to grow. We remain intently focused on increasing chipset gross margins through aggressive cost reductions including product and packaging redesign and manufacturing and yield improvements.

Consumer

Handheld, DTV and game console revenues are expected to remain key growth and profit drivers for ATI. We expect Consumer revenues in fiscal 2006 to increase both on an absolute basis and as a percentage of consolidated revenues.

Handheld revenue is expected to grow on increased sales of Imageon processors to meet the growing consumer demand for feature-rich multimedia mobile phones. According to Display Search, a market research firm, the mobile phone market is expected to grow from approximately 817.9 million units in calendar 2005 to 1,071.9 million units by 2008, with nearly 98% of mobile phones having color display.

We expect sales of our DTV products to increase in fiscal 2006 with the continued roll-out of digital television in the North American market. In addition, we are beginning to focus our development on products for the European and Asian markets to fuel future growth. According to Strategy Analytics, a market research firm, worldwide DTV shipments are predicted to be 73.7 million units in calendar 2005, climbing to an estimated 134.5 million units by 2008.

We expect a stronger contribution from our game console segment in fiscal 2006 due to the incremental royalties that are expected from sales of Microsoft’s Xbox 360. Nintendo’s Revolution console, the successor to the GameCube, will also contain our graphics technology and is widely expected by the industry to launch sometime in calendar 2006.

Consolidated

We continue to work aggressively to improve our operational capabilities and achieve a higher level of overall efficiency.

While we believe gross margins will remain under some pressure in the near-term due to the growing contribution from integrated chipsets, we expect gross margins to improve modestly as the year progresses. We also expect fiscal 2006 to yield both revenue and earnings growth relative to fiscal 2005.

16 ATI 2005

20 of 75

| 1999 | • ATI’s RAGE 128 first to break the 3DWinBench 99 700 barrier. Mercury Research report proves RAGE 128-based RAGE FURY 32MB board at 743 Winmarks, the fastest in the world | • ATI ships five million RAGE Mobility graphics chips. The family of products sets new industry record, shipping nearly one million 3D units per month |

| Quarterly Financial Data | |||||||||||||||||||||||||||||||||

| FINANCIAL RESULTS | |||||||||||||||||||||||||||||||||

| ANALYSIS | (Unaudited) (In thousands of U.S. dollars, except per share amounts) | ||||||||||||||||||||||||||||||||

| Fiscal 2005 | Fiscal 2004 | ||||||||||||||||||||||||||||||||

| Aug. 31 | May 31 | Feb. 28 | Nov. 30 | Aug. 31 | May 31 | Feb. 29 | Nov. 30 | ||||||||||||||||||||||||||

| 2005 | 2005 | 2005 | 2004 | 2004 | 2004 | 2004 | 2003 | ||||||||||||||||||||||||||

| Revenues | $ 470,227 | $ 530,235 | $ 608,188 | $ 613,859 | $ 572,218 | $ 491,457 | $ 463,337 | $ 469,705 | |||||||||||||||||||||||||

| Gross Margin(1) | 42,345 | 154,429 | 208,303 | 208,850 | 192,382 | 172,539 | 160,423 | 167,571 | |||||||||||||||||||||||||

| Operating Expenses | 159,085 | 157,057 | 141,867 | 131,099 | 119,958 | 112,355 | 103,561 | 107,310 | |||||||||||||||||||||||||

| Net Income (Loss) | (103,522) | (445) | 57,193 | 63,703 | 61,156 | 48,619 | 47,585 | 47,439 | |||||||||||||||||||||||||

| Net Income (Loss) | |||||||||||||||||||||||||||||||||

| per Share (Basic) | $(0.41) | $0.00 | $0.23 | $0.26 | $0.25 | $0.20 | $0.19 | $0.20 | |||||||||||||||||||||||||

| Net Income (Loss) | |||||||||||||||||||||||||||||||||

| per Share (Diluted) | $(0.41) | $0.00 | $0.22 | $0.25 | $0.24 | $0.19 | $0.19 | $0.19 | |||||||||||||||||||||||||

| (1)Gross margin for the fourth quarter of fiscal 2005 includes an inventory write-down of $67 million. | |||||||||||||||||||||||||||||||||

Fourth Quarter Performance

2005 versus 2004

Revenues declined 18% to $470.2 million from $572.2 million in the same period last year. The PC segment accounted for 80% of total revenues in the fourth quarter with the Consumer segment accounting for the remaining 20%.

PC revenues for the quarter declined 22% to $376.9 million on a 4% increase in volumes. The primary reason for the decline was lower sales of performance and enthusiast desktop products in the Add-in-Board (AIB) and retail channels. The combination of lower volumes and reductions in average selling price (ASP) to stimulate demand led to the decline in revenues. In the first quarter of fiscal 2006, we launched a new family of desktop discrete products which we expect will improve our competitive position and performance in this segment. Revenue from notebook discrete products declined approximately 20% reflecting the market trend towards increased use of integrated chipsets.

The sales declines in discrete were partially offset by a significant increase in desktop chipset revenues, which were approximately seven times greater than in the same period in 2004. The increase was driven by OEM design wins and strong demand for the Radeon Xpress 200 product line for AMD and Intel platforms. Sales of notebook integrated chipsets were down slightly year over year.

Consumer revenue increased 6% to $93.3 million. Handheld unit shipments increased 30%, however, revenues only increased by 4% due to a higher concentration of sales to the mainstream market where ASPs are generally lower. Sales of DTV products rose 4% year over year on a unit increase of more than 20%. In DTV, growth was impacted by an expected decline in business from a set-top box customer and a slower-than-expected industry transition to digital. This transition is expected to accelerate in future quarters.

Gross margin fell to $42.3 million from $192.4 million in the same period last year. As a percentage of sales, gross margin fell to 9.0% from 33.6% . We recorded an inventory write-down of $67 million in the quarter largely related to performance and enthusiast level desktop discrete products. This write-down accounted for a majority of the gross margin decline in the quarter. Excluding the inventory write-down, gross margin fell to 23.3%, reflecting weaker product mix and more aggressive ASP reductions to stimulate AIB channel demand. In addition, sales of integrated chipsets, which currently have considerably lower margins than our other products, comprised almost 20% of revenues in the quarter as compared with 10% in the same period last year. Consumer product gross margins remained stable due to a continued focus on cost reduction strategies.

ATI 2005 17

21 of 75

| 1999 | • ATI becomes the first graphics company to ship a fully-enabled DVI chip, permitting direct connection to a digital flat panel monitor | • ATI tops US$1 billion mark in annual revenues |

One Billion

(US) annual revenue

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

Selling and marketing, administrative, and research and development expenses rose 34%, 50% and 16%, respectively, from the same period one year ago. Operating expenses rose due to increased personnel, higher marketing and advertising costs, and increased development and prototyping costs related to new products, including a new family of discrete products based on 90 nanometer process technology.

Stock-based compensation expense was $11.2 million in the fourth quarter of fiscal 2005 as compared with $1.7 million for the same period last year. The increase was primarily related to ATI beginning the expensing of stock options in compliance with Canadian GAAP during the first quarter of fiscal 2005.

Net loss for the fourth quarter was $103.5 million ($0.41 per diluted share), as compared with net income of $61.2 million ($0.24 per diluted share) in the fourth quarter of 2004.

During the fourth quarter, we repurchased and cancelled two million common shares at a total cost of $23.9 million. Our cash position at August 31, 2005 was $586.6 million, up from $548.9 million last year.

Fiscal 2005

Comparison of Operating Results

The following table compares operating results for our three most recent fiscal years. Each line item is also expressed as a percentage of revenues.

| (Unaudited) (In thousands of U.S. dollars, except per share amounts) | |||||||||||||||||||

| 2005 | 2004 | 2003 | |||||||||||||||||

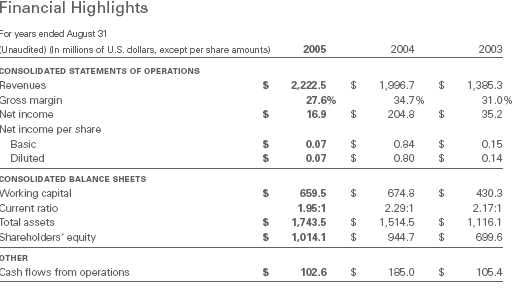

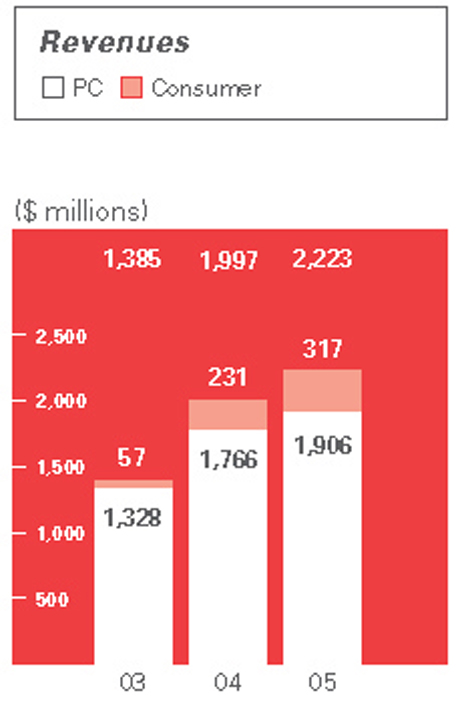

| REVENUES | $ 2,222,509 | 100.0% | $ 1,996,717 | 100.0% | $ 1,385,293 | 100.0% | |||||||||||||

| Cost of revenues | 1,608,582 | 72.4% | 1,303,802 | 65.3% | 956,116 | 69.0% | |||||||||||||

| GROSS MARGIN | 613,927 | 27.6% | 692,915 | 34.7% | 429,177 | 31.0% | |||||||||||||

| OPERATING EXPENSES | |||||||||||||||||||

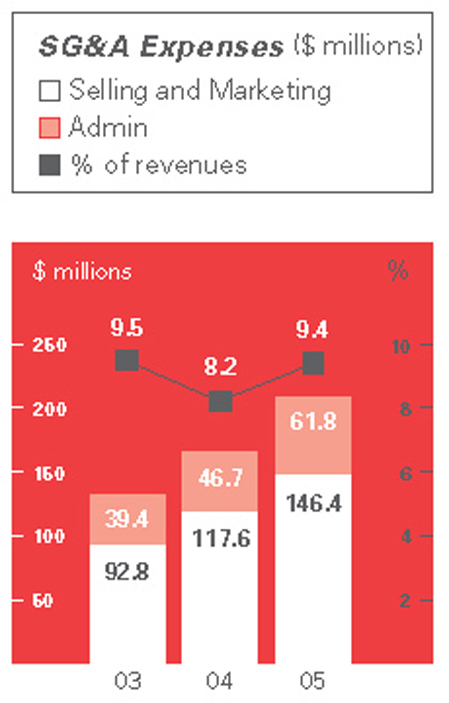

| Selling and marketing | 146,352 | 6.6% | 117,597 | 5.9% | 92,810 | 6.7% | |||||||||||||

| Research and development | 327,017 | 14.7% | 265,491 | 13.3% | 212,976 | 15.4% | |||||||||||||

| Administrative | 61,808 | 2.8% | 46,702 | 2.3% | 39,413 | 2.8% | |||||||||||||

| Amortization of intangible assets | 8,919 | 0.4% | 6,115 | 0.3% | 10,767 | 0.8% | |||||||||||||

| Stock-based compensation | 42,504 | 1.9% | 7,583 | 0.4% | – | – | |||||||||||||

| Other charges (recoveries) | 2,508 | 0.1% | (304) | – | 28,724 | 2.1% | |||||||||||||

| 589,108 | 26.5% | 443,184 | 22.2% | 384,690 | 27.8% | ||||||||||||||

| INCOME FROM OPERATIONS | 24,819 | 1.1% | 249,731 | 12.5% | 44,487 | 3.2% | |||||||||||||

| Interest and other income, net | 14,935 | 0.7% | 2,950 | 0.2% | 4,382 | 0.3% | |||||||||||||

| Interest expense | (2,096) | (0.1%) | (2,058) | (0.1%) | (1,899) | (0.1%) | |||||||||||||

| INCOME BEFORE INCOME TAXES | 37,658 | 1.7% | 250,623 | 12.6% | 46,970 | 3.4% | |||||||||||||

| Income taxes | 20,729 | 0.9% | 45,824 | 2.3% | 11,741 | 0.9% | |||||||||||||

| NET INCOME | $ 16,929 | 0.8% | $ 204,799 | 10.3% | $ 35,229 | 2.5% | |||||||||||||

| NET INCOME PER SHARE | |||||||||||||||||||

| Basic | $0.07 | $0.84 | $0.15 | ||||||||||||||||

| Diluted | 0.07 | 0.80 | 0.14 | ||||||||||||||||

18 ATI 2005

22 of 75

| 2000 | • ATI becomes the worldwide leader in the supply of mobile graphics solutions, according to Mercury Research | • ATI completed the acquisition of ArtX, Inc. – a leading developer of high- performance graphics for both PCs and consumer appliances |

| Revenues |

2005 versus 2004 | |

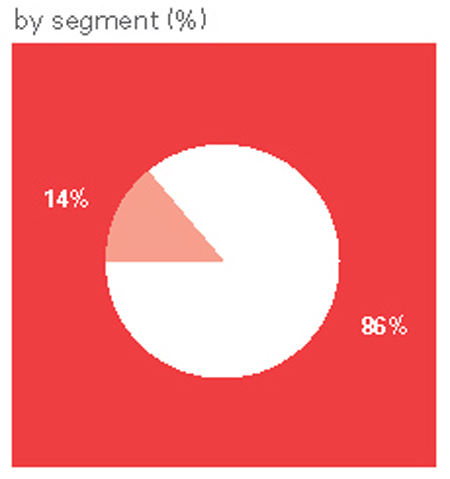

Revenues increased 11% to approximately $2.2 billion from approximately $2.0 billion in 2004. The revenue growth was a result of higher sales in the PC and Consumer segments. The PC segment accounted for 86% of consolidated revenues in fiscal 2005 with Consumer accounting for the remaining 14%. Annual shipments grew more than 30% on broad-based demand and approached 115 million units for the fiscal year. | |

In 2005, two customers accounted for 10.7% and 10.3%, respectively, of our consolidated revenues. In 2004, one customer accounted for 10.6% of total revenues. Our top ten customers accounted for 61.2% of revenues in 2005 compared with 61.9% in 2004. | |

PC | |

Desktop revenue, consisting of both discrete and integrated sales, increased more than 15% in fiscal 2005. While volumes grew more than 30%, a product mix shift towards lower-ASP mainstream and value parts in the second half of the year partially offset the dollar increase. | |

Desktop discrete revenue represented approximately half of our overall business in both 2005 and 2004. Strong sales growth in the first half of the year was partially offset by a decline in AIB and retail desktop discrete sales in the third and fourth quarters. Desktop integrated chipset revenue rose nearly 250% in 2005, making it our fastest-growing product line in 2005. Notebook revenue, consisting of both discrete and integrated sales, was essentially flat year over year. Notebook discrete sales, which accounted for more than three-quarters of total notebook revenues, rose approximately 10%. This was offset by a significant decline in notebook integrated sales. | |

Approximately 30% of consolidated revenues in 2005 were generated by sales from our notebook products, compared with approximately 35% in 2004. The decline in notebook revenue resulted from growth in desktop and consumer, as well as the notebook market’s continued transition towards integrated chipsets, where our market share is well below that of discrete. | |

Consumer | |

Consumer revenues, consisting predominantly of handheld and DTV product sales, as well as royalty income and non-recurring engineering revenues (“NRE”), rose about 37% in fiscal 2005. Handheld products represented nearly half of our Consumer revenues for 2005. While handheld unit shipments rose almost 60%, revenue increased almost 30% due primarily to product mix and more modest ASPs in the mainstream mobile phone segment where sales were concentrated. Increased sales of Imageon processors to OEM customers, primarily Motorola, accounted for the increase in handheld business. |

| DTV revenue rose 70% in fiscal 2005 on higher sales of Xilleon and Theater processors to leading DTV and set-top box manufacturers. While unit shipments increased approximately 80%, the increase in dollar terms was offset by lower blended ASPs. The royalty income we received from Nintendo for our graphics technology used in their GameCube products, which is accounted for at 100% gross margin, was flat relative to the prior year. NRE revenues associated with our development contracts with Microsoft and Nintendo rose approximately $10 million from 2004. On a combined basis, royalties and NRE continued to represent less than 3% of consolidated revenues in 2005. |

| 2004 versus 2003 |

| Our revenues for 2004 increased 44%, to approximately $2.0 billion, compared with approximately $1.4 billion in 2003. The revenue growth was a result of sales increases in all our main business lines. |

ATI 2005 19

23 of 75

| 2000 | • ATI launches Radeon: the world’s most powerful and feature-packed graphics processor. Radeon marks ATI’s entry and market leadership in the high-end gaming and 3D workstation segments | • ATI releases its integrated graphics chip, combining the northbridge chipset function on-chip and providing a low-cost yet full- featured graphics and video solution for OEMs | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

Desktop revenue increased by more than 30% as the number of units sold grew by nearly 50%. Desktop revenues represented a little less than half of our overall business in 2004, versus about 55% in 2003. Overall business grew due to a more competitive product stack, particularly in the mainstream and value segments of the desktop market, and greater penetration in the AIB channel.

Notebook revenue growth was driven by growth in the notebook market overall, as well as improvement in ATI’s notebook discrete market share. This was slightly offset by a decline in our share of the growing notebook integrated graphics market.

About 35% of consolidated revenues in 2004 were generated by our notebook products, compared with approximately 40% in 2003.

In 2004, about three-quarters of total notebook revenue was generated from discrete products while the remainder was integrated. Notebook revenue continued to grow rapidly in fiscal 2004. However, notebook’s share of ATI’s total revenue declined because of the extraordinarily high growth in Consumer revenue.

Approximately 12% of our consolidated 2004 revenues were generated by Consumer products. Our handheld products represented slightly more than one-half of Consumer revenue. DTV accounted for approximately one-quarter of Consumer revenue.

Royalties from our Nintendo business and NRE continued to represent less than 3% of consolidated revenues in 2004, and in absolute dollars more than doubled in 2004 relative to 2003.

In 2004, one customer accounted for 10.6% of total revenues. In 2003, three customers accounted for 16.2%, 13.0% and 10.6%, respectively, of total revenues. Our top 10 customers accounted for 61.9% of revenues in 2004 compared with 69.6% in 2003.

Gross Margin

2005 versus 2004

Gross margin for fiscal 2005 was $613.9 million or 27.6% of sales as compared with $692.9 million or 34.7% of sales in fiscal 2004. Strong gross margins in each of the first two quarters of fiscal 2005 were offset by a decline in PC margins in the second half of the year. During the third and fourth quarters, soft demand among AIB and retail customers for performance and enthusiast level desktop discrete products led to lower volumes, weaker product mix and lower ASPs, which impacted gross margin.

The decline in gross margins relative to last year is mostly attributable to the following factors:

- a net inventory write-down of $67.4 million in the fourth quarter;

- weaker product mix and demand-stimulating initiatives in the AIB and retail channels in the second half; and

- low gross margins on integrated chipsets.

Excluding the impact of the inventory write-down, gross margin for fiscal 2005 was 30.7% .

During fiscal 2005, our desktop chipset business experienced significant revenue growth but at low gross margins. A margin improvement program is in place to increase gross margins in our chipset business and to achieve long-term gross margins of 25% to 30% for this business. The program includes cost improvement initiatives, a focus on new product introductions, and achieving improved cost effectiveness through product design.

Gross margins in handheld and DTV remained strong in fiscal 2005, as cost reduction initiatives helped to offset the effect of normal ASP declines. Handheld gross margins remained level with the prior year while DTV margins increased modestly over 2004.

20 ATI 2005

24 of 75

| 2001 | • ATI unveils the Mobility Radeon chip for the notebook personal computer | • ATI acquires workstation graphics processor pioneer FireGL Graphics, formalizing its entry into the high- performance workstation graphics segment of the PC graphics industry | • ATI unveils new hybrid business model, whereby company permits OEMs and AIBs to use its patented chip technology in their products |

2004 versus 2003

Gross margin percentage for fiscal 2004 was 34.7% or 3.7% higher than the 31.0% achieved in fiscal 2003. Margin improvement was driven by increases in margin levels on PC products as well as by the greater share of revenues resulting from higher-margin consumer electronics products.

The increased competitiveness of our desktop products along with less aggressive ASP reductions drove the improvement in desktop discrete PC margins. As we continued to increase the share of revenues derived from the relatively higher margin Consumer business, the change in revenue mix also contributed to overall margin improvement. This increase was slightly offset by the decline in our PC discrete product margins in the fourth quarter due to the introduction of our PCI Express products.

Operating Expenses

2005 versus 2004

Operating expenses, including selling and marketing, R&D, and administrative expenses, and excluding stock-based compensation, amortization of intangible assets and other charges, increased $105.4 million or 24.5% as compared with fiscal 2004. The percentage growth in operating expenses exceeded percentage growth in revenues due primarily to a revenue shortfall in the second half of the year, as well as increased investments in R&D to develop our next-generation products and marketing efforts on design wins to support our future revenue growth.

Our Canadian overhead and staff costs were approximately Cdn. $260 million in fiscal 2005 compared to approximately Cdn. $220 million in fiscal 2004. The appreciation of the Canadian dollar relative to the U.S. dollar, from an average rate of 75 cents in fiscal 2004 to an average rate of 80 cents in fiscal 2005, had approximately $13 million in negative impact on 2005 operating expenses, as ATI reports and measures its results in U.S. dollars. Continuing strength in the Canadian dollar relative to the U.S. dollar will result in upward pressure on operating expenses in fiscal 2006.

During the third quarter of fiscal 2005, we purchased forward foreign exchange contracts (”Forwards”) to buy $94.5 million Canadian dollars over the next nine months at an average exchange rate of 1.2579. All of the Forwards have become favorable to us since their inception and had a fair value of $4.7 million at August 31, 2005.

In accordance with Canadian GAAP, beginning with the first quarter of fiscal 2005, ATI expensed compensation costs associated with stock options granted to employees after September 1, 2002. This expense item, along with the expense associated with restricted share units and deferred share units, is reflected in the expense for stock-based compensation included in the attached consolidated statements of operations and retained earnings. Prior to the first quarter of fiscal 2005, the expenses associated with restricted share units and deferred share units were reflected in selling and marketing, R&D and administrative expenses. These amounts have been reclassified for comparative purposes.

2004 versus 2003

Our overhead and staffing costs were approximately Cdn. $220 million in fiscal 2004 compared with approximately Cdn. $160 million in fiscal 2003. The rise in the value of the Canadian dollar relative to the U.S. dollar, from an average rate of 67 cents in fiscal 2003 to an average rate of 75 cents in fiscal 2004, had an approximate $18.0 million negative impact on our operating expenses in 2004.

ATI 2005 21

25 of 75

| 2001 | • ATI acquires HydraVision™ desktop management software application from Appian Graphics | • ATI unveils FireGL 8800 workstation graphics board, the first such product to evolve out of its acquisition of FireGL graphics |

MANAGEMENT’S DISCUSSION AND ANALYSIS (CONT.)

| Selling and Marketing Expenses 2005 versus 2004 Selling and marketing expenses consist primarily of salaries, commissions and bonuses, sales promotions and advertising, and travel and entertainment expenses related to product marketing, including trade shows and launch events. Selling and marketing expenses rose $28.8 million or 24.5% in fiscal 2005 due to additional personnel as well as advertising and other promotional expenses related to trade shows and product launches. Other marketing costs such as travel and customer samples contributed to the increase. As a percentage of revenues, our selling and marketing expenses rose to 6.6% from 5.9%. In 2005, we purchased certain assets of RT&C International (RT&C ), one of our third-party sales and distribution partners in South Korea, as well as the remaining assets of AMI Technologies Corp. (AMI), certain assets of which were acquired the previous year. As a result, our fixed selling costs increased in 2005 due to these acquisitions; however, the decrease in commissions paid more than offset the increase. These investments are expected to support further revenue growth in the Asia-Pacific region. 2004 versus 2003 Our selling and marketing expenses in 2004 rose $24.8 million or 26.7% to $117.6 million. As a percentage of revenues, our selling and marketing expenses declined to 5.9% from 6.7% in 2003. The largest contributor to the increase in selling and marketing expenses was staffing costs, including additional sales and marketing personnel in North America and in the Asia-Pacific region, and higher incentive-based compensation that resulted from higher sales. Increased advertising expenditures related to product launches, videogame developer programs and co-marketing programs with our OEM, AIB and retail partners also contributed to the year over year increase. Our purchase of certain assets of AMI, one of our third-party sales and distribution partners in Asia-Pacific, in early 2004 helped to reduce the growth in expenses associated with sales into this region in fiscal 2004. Although fixed selling costs increased in 2004 due to the acquisition, the decrease in commissions paid more than offset the increase. Research and Development (R&D) Expenses 2005 versus 2004 R&D expenses include engineering salaries, costs of development tools and software, component and board prototype costs, consulting fees, licensed technology fees and patent filing fees. R&D expenses increased by $61.5 million or 23.2% in fiscal 2005 primarily due to a $46.2 million increase related to additional personnel and a $21.4 million increase in development and engineering costs related to product tape-outs and prototype materials. R&D as a percentage of revenues was 14.7% and in line with our target range of 13%–15%. In 2005, we acquired CuTe, a company specializing in audio and digital media solutions located in India. We also acquired certain cable modem silicon intellectual property and hired certain employees of Terayon. While this has increased our expenses in the current year, it will allow us to support continued product and technology leadership. Investment in R&D is a key part of our strategy to maintain product and technology leadership. R&D is essential to our continued achievement of our strategic objectives of product and technology leadership, establishing a strong franchise in the integrated chipset market and securing market leadership in consumer digital electronics. Investment in R&D effectively drives ATI’s future revenue growth and we will continue to invest in R&D in support of these strategic objectives. |

22 ATI 2005

26 of 75

| 2001 | • ATI announces Mobility Radeon 7500, the most powerful, feature-rich mobile solution in the world for the notebook personal computer | • ATI introduces the All-in- Wonder Radeon 8500DV, the world’s most advanced multimedia graphics board | • ATI introduces Xilleon 220; the world’s most highly integrated system-on-chip for the digital set-top box market |

| 2004 versus 2003 R&D expenses increased by 24.7% to $265.5 million; however, they declined as a percentage of revenues to 13.3% from 15.4% in 2003. The dollar increase was related to increased staffing costs, particularly in our consumer products business to support our growing color mobile phone business. Other factors include the expansion of our software engineering competencies, as well as higher incentive-based compensation; increased investments in our desktop products business, including an additional $15.0 million in prototyping expenses; the impact of a stronger Canadian dollar; and higher licensing fees, which include increases in computer-aided design (CAD) tool expenditures to support the development of new products. Administrative Expenses 2005 versus 2004 Administrative expenses consist of salaries and expenses of the corporate infrastructure groups, including the operations, human resources, finance, legal and information technology functions. Most of our administrative expenditures are denominated in Canadian dollars. Administrative expenses increased $15.1 million or 32.3% to $61.8 million or 2.8% of revenues, primarily due to increased staffing and professional and consulting fees, including fees related to compliance with evolving regulatory requirements such as those imposed by theSarbanes-Oxley Act of 2002. 2004 versus 2003 Our administrative expenses increased 18.5% to $46.7 million in 2004. As a percentage of revenues, administrative expenses in 2004 declined to 2.3% from 2.8% in 2003. The increase in administrative expenses in 2004 was primarily a result of increased staffing to support our growing business, higher incentive-based compensation, and the stronger Canadian dollar. Stock-based Compensation In accordance with Canadian GAAP, beginning with the first quarter of fiscal 2005, we began expensing compensation costs associated with stock options granted to employees after September 1, 2002. This expense item, along with the expense associated with restricted share units and deferred share units, is reflected in the expense for stock-based compensation in the attached consolidated statements of operations and retained earnings. Prior to fiscal 2005, the expense associated with restricted share units and deferred share units were reflected in the selling and marketing, R&D and administrative expenses. These amounts have been reclassified for comparative purposes. Stock options, restricted share units and deferred share units comprise all stock-based compensation currently awarded by ATI to our employees and directors. Stock-based compensation costs were $42.5 million in 2005 as compared with $7.6 million last year. The increase in stock-based compensation was primarily related to ATI commencing the expensing of stock options in compliance with Canadian GAAP during the first quarter of fiscal 2005. The $42.5 million expense in fiscal 2005 included $34.0 million for compensation costs associated with stock options and $8.5 million for compensation costs associated with restricted share units and deferred share units. Amortization of Intangible Assets 2005 versus 2004 Our total amortization expense increased from $6.1 million to $8.9 million in 2005. The increase is primarily due to incremental amortization related to the core technology and other intangibles assumed as a result of the acquisition of CuTe and the acquisition of certain assets of Terayon, RT&C and AMI. |

ATI 2005 23

27 of 75

| 2001 | • ATI introduces Radeon 7000 and 7200 boards – the latest additions to the most powerful, innovative graphics family in the world | • ATI unveils Mobility™ FireGL 7800 – the world’s fastest and most powerful mobile workstation GPU designed for 3D animation and CAD/CAM | • ATI unveils FireGL 8700 workstation graphics board, a new entry-level offering for the digital content creation, 3D animation and MCAD workstation customer |

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)

| 2004 versus 2003 Our total amortization expense declined by $4.7 million, or 43.2%, to $6.1 million in 2004. The decrease was primarily the result of the completion of the amortization of intangibles related to the acquisition of NxtWave Communications Inc. Other Charges 2005 versus 2004 On March 29, 2005, a panel of the Ontario Securities Commission (“OSC”) approved a settlement agreement reached between Staff of the OSC and us. As part of the settlement, we agreed to pay a total of Cdn. $900,000 in costs and settlement payments. The balance of other charges relate to legal fees incurred in respect of the investigation and OSC proceedings. Seenote 16to the consolidated financial statements. 2004 versus 2003 We recorded a recovery of $0.3 million in respect of other charges in 2004. The amount resulted from recoveries in excess of the estimated amount from the restructuring of our European operations and the reversal of a lease exit charge incurred in 2003, less a charge to address issues related to an investigation by the OSC. Seenote 16to the consolidated financial statements. Interest and Other Income, Net (Unaudited) (In thousands of U.S. dollars) |

| 2005 | 2004 | 2003 | ||

|---|---|---|---|---|

| Interest income on cash and short-term investments | $ 14,330 | $ 4,352 | $ 2,802 | |

| Gain (loss) on investments | (1,580) | (1,307) | 3,876 | |

| Gain on foreign exchange | 1,174 | 540 | 819 | |

| Loss on disposal of fixed assets | (25) | (3,087) | (3,932) | |

| Insurance claim on Taiwan earthquake | -- | 578 | -- | |

| Other income | 1,036 | 1,874 | 817 | |

| Interest and other income, net | $ 14,935 | $ 2,950 | $ 4,382 | |

Interest Expense 2005 versus 2004 Interest expense remained flat year over year at $2.1 million. Our interest expense relates primarily to our capital lease obligation and mortgage for a building facility located in Markham, Ontario, a joint venture in which we hold a 50.0% interest. 2004 versus 2003 Our interest expense increased to $2.1 million in 2004 from $1.9 million in the prior year mostly as a result of the foreign exchange impact of the rise of the Canadian dollar versus the U.S. dollar. |

24 ATI 2005

28 of 75

| 2001 | • ATI unveils its technology for the Nintendo GameCube at the Electronic Entertainment Expo (E3), officially marking its entry into the game console market |

Income Taxes 2005 versus 2004 versus 2003 (Unaudited) (In thousands of U.S. dollars) |

| 2005 | 2004 | 2003 | ||

|---|---|---|---|---|

| Operating income tax expense | $ 29,715 | $ 46,393 | $ 15,570 | |

| Stock-based compensation | (3,360) | -- | -- | |

| Recovery of future tax liability related to intangible assets (other than goodwill) | (312) | (532) | (1,679) | |

| Income tax recovery related to inventory write-down and other charges | (5,314) | (37) | (2,150) | |

| $ 20,729 | $ 45,824 | $ 11,741 | ||

Income tax expense declined to $20.7 million due to our lower net income in 2005. Income tax expense increased to $45.8 million in 2004 from $11.7 million in 2003 due to our higher net income in 2004 as compared with 2003. ATI’s operating tax rate, which excludes the impact of the amortization of intangible assets related to acquisitions, inventory write-down and other charges and stock-based compensation costs was 18.0% in 2005, 18.0% in 2004, and 18.9% in 2003. ATI’s tax rate is affected by the amount of net income earned in its various operating jurisdictions. Seenote 13to the consolidated financial statements. Net Income 2005 versus 2004 Net income in 2005 declined to $16.9 million from $204.8 million in 2004. The decrease in net income was the result of a 7.1% decrease in gross margins and the increase in operating expenses outlined in earlier sections of this MD&A. Diluted earnings per share fell to $0.07 from $0.80 in fiscal 2004. 2004 versus 2003 Net income in 2004 was $204.8 million, an increase of $169.6 million from $35.2 million in 2003. The increase in net income was a result of the significant increase in revenues and continuing strong margins throughout 2004. |

ATI 2005 25

29 of 75

| 2002 | • ATI elevated to permanent membership in OpenGL standards board | • ATI unveils Radeon 8500 Mac Edition and Radeon 7000 Mac Edition dual display PCI graphics card | • ATI enters wireless market with Imageon 100, the most advanced display co-processor for PDAs and smart phones |

MANAGEMENT’S DISCUSSION AND ANALYSIS (CONT.)

| LIQUIDITY AND CAPITAL RESOURCES | This section explains how we manage our cash and capital resources to carry out our strategy and deliver financial results. Cash Position The table below summarizes our cash inflows and outflows for each of the past three years: (Unaudited) (In thousands of U.S. dollars) |

| 2005 | 2004 | 2003 | ||

|---|---|---|---|---|

| Net income | $ 16,929 | $ 204,799 | $ 35,229 | |

| Non-cash add backs | 35,411 | 23,367 | 12,883 | |

| Working capital changes | 50,298 | (43,215) | 57,337 | |

| Issue of common shares | 30,170 | 56,531 | 20,977 | |

| Repurchase of common shares (net of proceeds from sale of ordinary shares) | (23,847) | (22,100) | -- | |

| Bank indebtedness | -- | -- | (12,015) | |

| Net movement in long-term debt | (1,663) | (1,442) | 9,645 | |

| Net purchases of capital assets | (48,831) | (18,182) | (16,390) | |

| Net proceeds from investments, net of purchases | 880 | (98) | 7,569 | |

| Net purchases of short-term investments | (174,062) | (139,524) | (135) | |

| Acquisitions | (22,057) | (2,071) | -- | |

| Other | -- | -- | (1,140) | |

| (136,772) | 58,065 | 113,960 | ||

| Foreign exchange gain (loss) | 441 | 638 | (181) | |

| Net increase (decrease) in cash and cash equivalents | $ (136,331) | $ 58,703 | $ 113,779 | |

| Cash, cash equivalents and short-term investments | $ 586,647 | $ 548,916 | $ 350,689 | |

| | ||||

| | ||||

| | 2005 versus 2004 Our cash position (cash, cash equivalents and short-term investments) at August 31, 2005 increased 7% to $586.6 million from $548.9 million at fiscal 2004 year-end. Our cash position increased mainly as a result of cash flow from operations in the fiscal year. During the year, $23.9 million was spent on the repurchase of two million common shares under a normal course issuer bid. We have access to $21.0 million in credit facilities at August 31, 2005 compared to $43.0 million at August 31, 2004. With our large cash position we took action to reduce our credit facilities during the year and correspondingly reduce costs. There are no amounts outstanding on these facilities as of the date of this MD&A. 2004 versus 2003 Our cash position (cash, cash equivalents and short-term investments) increased 56.5% to $548.9 million in 2004 as a result of increased cash flow from operations throughout the fiscal year. We had access to $43.0 million in credit facilities at August 31, 2004 compared to $25.4 million at August 31, 2003. |

26 ATI 2005

30 of 75

| 2002 | • With ATI’s Remote Wonder™, users can take control of their computer. New remote enables multimedia access from anywhere in your room, house, stage or classroom | • ATI launches System Integrator Partner Program in North America | • ATI acquires NxtWave Communications giving ATI the set-top box technology to provide complete solutions for customers |

Commitments As at August 31, 2005, we were committed to the following minimum payments related to office premises, license and royalty agreements, building under capital lease payments, mortgage payments and non-cancellable inventory purchases: |

| (Unaudited) (In thousands of U.S. dollars) | Total | 2006 | 2007 | 2008 | 2009 | 2010 | Thereafter |

| Commitments related to office premises, license and royalty agreements | $ 87,903 | $ 26,941 | $ 20,937 | $ 16,593 | $ 8,875 | $ 6,946 | $ 7,611 |

| Commitment related to capital lease | 27,285 | 2,078 | 2,164 | 2,285 | 2,285 | 2,285 | 16,188 |

| Commitment related to mortgage | 16,086 | 1,739 | 1,739 | 1,739 | 1,739 | 1,739 | 7,391 |

| Commitment related to non-cancellable inventory purchase | 223,600 | 223,600 | -- | -- | -- | -- | -- |

| Total commitments | $ 354,874 | $ 254,358 | $ 24,840 | $ 20,617 | $ 12,899 | $ 10,970 | $ 31,190 |

We believe that cash flows from operating activities, together with our cash position and borrowings available under our credit facilities, will be sufficient to fund currently anticipated working capital, planned operating and capital expenditures and debt service requirements, during fiscal 2006. Normal Course Issuer Bid Under the terms of a normal course issuer bid announced on March 24, 2005, we may purchase up to 24.7 million common shares, representing approximately 10% of our “public float” as of March 17, 2005. Purchases will be made on the open market by us through the facilities of the TSX or the NASDAQ Stock Market Inc. (“NASDAQ”). The prices we will pay for any purchased common shares will be the market price of such shares on the TSX or NASDAQ, as the case may be, at the time of acquisition. We will make no purchases of common shares other than open-market purchases. In fiscal 2005, a total of two million common shares were repurchased for a total consideration of $23.9 million for cancellation under the terms of the normal course issuer bid. In fiscal 2006, we repurchased 408,100 common shares for a total consideration of $5.69 million for cancellation. The normal course issuer bid will terminate on March 29, 2006 or on such earlier date as we complete our purchases under the terms of the normal course issuer bid. We will cancel any common shares repurchased under this normal course issuer bid. Operating Activities – Working Capital 2005 versus 2004 Accounts Receivable Our accounts receivable increased by 5.6% to $386.3 million at August 31, 2005 compared to the prior year-end, due to the timing of sales during the fourth quarter. Our accounts receivable are within our target range for current sales levels. At August 31, 2005, 93.9% of accounts receivable were less than 60 days outstanding, compared with 94.8% at August 31, 2004. Days’ sales in accounts receivable increased to 65 days in 2005 compared to 50 days in 2004. The increase is attributable to the higher proportion of shipments within the last month of the fiscal year as well as the timing of revenues relating to certain engineering services. At August 31, 2005, one of our customers accounted for 12% of our accounts receivable balance. At August 31, 2004, none of our customers accounted for 10% or more of our accounts receivable balance. Inventories Inventory at August 31, 2005 increased 36.6% to $348.2 million from $254.9 million in fiscal 2004. Our inventory position at fiscal year-end includes the impact of an inventory write-down of $67.4 million in the fourth quarter of fiscal 2005 consisting predominantly of mid- to high-end PCI Express and AGP desktop discrete products. Following the inventory write-down, days of inventory on hand at the end of fiscal 2005 were 85 as compared with our long-term target of 70 days. |

ATI 2005 27

31 of 75

| 2002 | • ATI and Massive render The Lord of the Rings: The Fellowship of the Ring™ in real time in Linux® at SIGGRAPH 2002 | • ATI’s new FireGL X1 powers DCC and CAD workstations into new era of content creation. ATI has the world’s most advanced workstation graphics board with OpenGL®, Microsoft® DirectX® 9.0 and Linux® in one graphics solution |

MANAGEMENT’S DISCUSSION AND ANALYSIS(CONT.)