Filed by: Weyerhaeuser Company

Pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Weyerhaeuser Company

Commission File No.: 001-04825

“Building a Best-in-Class Homebuilder”

Investor Presentation

June 2014

Forward Looking Statements

This presentation contains forward-looking statements concerning Weyerhaeuser Company (“Weyerhaeuser”) and TRI Pointe Homes, Inc. (“TRI Pointe”). These statements are based on various assumptions and the current expectations of the management of Weyerhaeuser and TRI Pointe, and may not be accurate because of risks and uncertainties surrounding these assumptions and expectations. Factors listed below, as well as other factors, may cause actual results to differ significantly from these forward-looking statements. There is no guarantee that any of the events anticipated by these forward-looking statements will occur. If any of the events occur, there is no guarantee what effect they will have on the operations or financial condition of Weyerhaeuser or TRI Pointe. There is no assurance that lots under contract under contract will be acquired or that we will proceed to build and sell homes on any lots that we control. Forward-looking statements included herein are made as of the date hereof, and Weyerhaeuser and TRI Pointe undertake no obligation to publicly update or revise any forward-looking statement unless required to do so by the federal securities laws.

Some forward-looking statements discuss Weyerhaeuser’s and TRI Pointe’s plans, strategies and intentions. They use words such as “expects,” “may,” “will,” “believes,” “should,” “would,” “could,” “approximately,” “anticipates,” “estimates,” “targets,” “intends,” “likely,” “projects,” “positioned,” “strategy,” “future,” and “plans.” In addition, these words may use the positive or negative or other variations of those terms. Forward-looking statements in this document include statements regarding the expected effects on Weyerhaeuser, Weyerhaeuser Real Estate Company (“WRECO”) and TRI Pointe of the proposed distribution of WRECO to Weyerhaeuser’s shareholders and combination of WRECO with a subsidiary of TRI Pointe (the “Transaction”), the anticipated timing and benefits of the Transaction and whether the Transaction will be tax-free for Weyerhaeuser and its shareholders for U.S. federal income tax purposes. Forward-looking statements also include all other statements in this document that are not historical facts.

These statements are based on the current expectations of the management of Weyerhaeuser and TRI Pointe (as the case may be) and are subject to uncertainty and to changes in circumstances. Major risks, uncertainties and assumptions include, but are not limited to: the satisfaction of the conditions to the Transaction and other risks related to the completion of the Transaction and actions related thereto; Weyerhaeuser’s and TRI Pointe’s ability to complete the Transaction on the anticipated terms and schedule, including the ability to obtain shareholder and regulatory approvals and the anticipated tax treatment of the Transaction and related transactions; risks relating to any unforeseen changes to or effects on liabilities, future capital expenditures, revenues, expenses, earnings, synergies, indebtedness, financial condition, losses and future prospects; TRI Pointe’s ability to integrate WRECO successfully after the closing of the Transaction and to achieve anticipated synergies; the risk that disruptions from the Transaction will harm Weyerhaeuser’s or TRI Pointe’s businesses; the effect of general economic conditions, including employment rates, housing starts, interest rate levels, availability of financing for home mortgages, and the strength of the U.S. dollar; and other factors described under “Risk Factors” in each of Weyerhaeuser’s and TRI Pointe’s Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q. However, it is not possible to predict or identify all such factors. Consequently, while the list of factors presented here is considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties.

2 |

|

Additional Disclaimer

Additional Information and Where to Find It

In connection with the proposed “Reverse Morris Trust” transaction between TRI Pointe Homes, Inc. (“TRI Pointe”) and Weyerhaeuser Company (“Weyerhaeuser”), pursuant to which the homebuilding subsidiary of Weyerhaeuser, Weyerhaeuser Real Estate Company (“WRECO”) (with certain exclusions), will be combined with TRI Pointe, TRI Pointe has filed a registration statement on Form S-4 (No. 333-193248) with the Securities and Exchange Commission (“SEC”), which includes a prospectus. TRI Pointe has also filed a definitive proxy statement which has been sent to the TRI Pointe shareholders in connection with their vote required in connection with the transaction. In addition, WRECO has filed a registration statement on Forms S-4 and S-1 (No. 333-193251) in connection with its separation from Weyerhaeuser. Investors and security holders are urged to read the proxy statement and registration statement/prospectus and any other relevant documents, because they contain important information about TRI Pointe, the real estate business of Weyerhaeuser and the proposed transaction. The proxy statement and registration statement/prospectus and any amendments and other documents relating to the proposed transaction can be obtained free of charge from the SEC’s website at www.sec.gov. These documents can also be obtained free of charge from Weyerhaeuser upon written request to Weyerhaeuser Company, 33663 Weyerhaeuser Way South, Federal Way, Washington 98003, Attention: Vice President, Investor Relations, or by calling (253) 924-2058, or from TRI Pointe upon written request to TRI Pointe Homes, Inc., 19520 Jamboree Road, Irvine, California 92612, Attention: Investor Relations, or by calling (949) 478-8696.

Tender Offer Documents

On May 22, 2014, Weyerhaeuser Company (“Weyerhaeuser”) filed with the SEC a tender offer statement on Schedule TO regarding the proposed exchange offer for the split-off of the Weyerhaeuser real estate business as part of the proposed “Reverse Morris Trust” transaction between TRI Pointe Homes, Inc. and Weyerhaeuser. Investors and security holders are urged to read the tender offer statement (as updated and amended) filed by Weyerhaeuser with the SEC regarding the tender offer because it contains important information. Investors and security holders may obtain a free copy of the tender offer statement and other documents filed by Weyerhaeuser with the SEC on the SEC’s web site at www.sec.gov. The tender offer statement and these other documents may also be obtained free of charge from Weyerhaeuser by directing a request to Weyerhaeuser Company, 33663 Weyerhaeuser Way South, Federal Way, Washington 98003, Attention: Vice President, Investor Relations, or by calling Weyerhaeuser at (253) 924-2058.

Participants in the Solicitation

This presentation is not a solicitation of a proxy from any security holder of TRI Pointe Homes, Inc. (“TRI Pointe”) or Weyerhaeuser Company

(“Weyerhaeuser”). However, Weyerhaeuser, TRI Pointe and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from TRI Pointe’s shareholders in connection with the proposed transaction. Information about the Weyerhaeuser’s directors and executive officers may be found in its Annual Report on Form 10-K for the year ended December 31, 2013, filed with the Securities and Exchange Commission (“SEC”) on February 18, 2014, and the definitive proxy statement relating to its 2014 Annual Meeting of Shareholders filed with the SEC on February 25, 2014. Information about the TRI Pointe’s directors and executive officers may be found in its Annual Report on Form 10-K/A for the year ended December 31, 2013, filed with the SEC on April 30, 2014 and the definitive proxy statement relating to its 2014 Annual Meeting of Stockholders filed with the SEC on May 20, 2014. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the direct and indirect interests of these participants, whether by security holdings or otherwise, has been included in the registration statement/prospectus, proxy statement and other relevant materials filed with the SEC.

3 |

|

Transaction Overview

Transaction Summary

In November 2013, TRI Pointe Homes (“TPH” or “TRI Pointe”) and Weyerhaeuser Company

(“Weyerhaeuser”) entered into a definitive agreement whereby Weyerhaeuser Real Estate Company (“WRECO”) will be combined with TRI Pointe in a “Reverse Morris Trust” transaction

TRI Pointe will issue 129.7 million shares to Weyerhaeuser shareholders(1)

Weyerhaeuser and TRI Pointe shareholders will own approximately 80.4% and 19.6%, respectively, of the combined company immediately after closing(2) Weyerhaeuser will receive a $739 million cash payment as part of the transaction funded by $900 million in senior unsecured notes recently priced at various rates / tenors (funds will be held in escrow pending the close of the merger) Expected to be tax-free to Weyerhaeuser shareholders

Transaction combines industry-leading management at TRI Pointe with WRECO’s strong local market franchises and management teams

— Corporate name will be TRI Pointe while regional brands will be maintained

— Central functions to be consolidated in Irvine HQ, with limited integration planned at the WRECO homebuilding companies

— Anticipate annual synergies of $21 million by the end of 2015 and $30 million annually thereafter

The combined company will focus on some of the most attractive housing markets in the U.S. and have a combined land position of approximately 31,000 lots owned or controlled

Top 10 homebuilder by expected combined equity market value(3)

2013 combined home sales revenue of $1.5 billion and Adj. EBITDA of $207 million(4)

Growth-oriented, pure-play homebuilder represents attractive investment at current point in the housing cycle

Transaction targeted to close early in the third quarter of 2014 with Weyerhaeuser exchange offer expected to expire at midnight on June 30, 2014

(1) Excluding shares to be issued on exercise or vesting of equity awards held by WRECO employees that are being assumed by TPH in connection with the transaction. (2) Following the consummation of the Merger, outstanding equity awards of WRECO and TRI Pointe employees are expected to represent 0.78% and 0.18%, respectively, of the then outstanding TRI Pointe common stock on a fully diluted basis.

(3) Expected equity market value of $2.7bn based on 161,332,533 shares outstanding after closing and TPH closing price of $16.50 on May 21, 2014. (4) Excludes pro forma adjustments. See “Reconciliation of Non-GAAP Financial Measures” beginning on page 34.

5 |

|

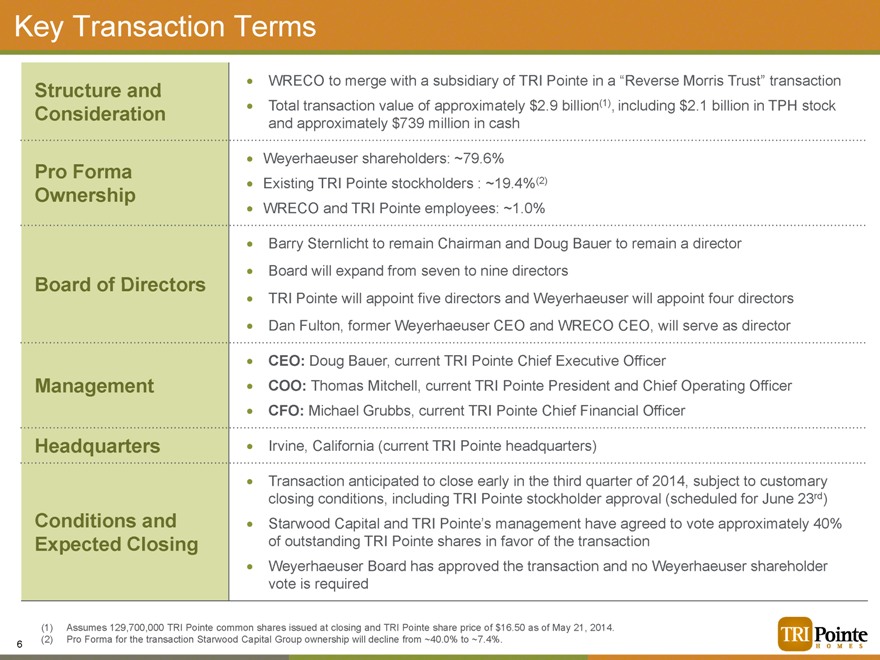

Key Transaction Terms

Structure and WRECO to merge with a subsidiary of TRI Pointe in a “Reverse Morris Trust” transaction

Consideration Total transaction value of approximately $2.9 billion(1), including $2.1 billion in TPH stock

and approximately $739 million in cash

Weyerhaeuser shareholders: ~79.6%

Pro Forma Existing TRI Pointe stockholders : ~19.4%(2)

Ownership

WRECO and TRI Pointe employees: ~1.0%

Barry Sternlicht to remain Chairman and Doug Bauer to remain a director

Board will expand from seven to nine directors

Board of Directors

TRI Pointe will appoint five directors and Weyerhaeuser will appoint four directors

Dan Fulton, former Weyerhaeuser CEO and WRECO CEO, will serve as director

CEO: Doug Bauer, current TRI Pointe Chief Executive Officer

Management COO: Thomas Mitchell, current TRI Pointe President and Chief Operating Officer

CFO: Michael Grubbs, current TRI Pointe Chief Financial Officer

Headquarters Irvine, California (current TRI Pointe headquarters)

Transaction anticipated to close early in the third quarter of 2014, subject to customary

closing conditions, including TRI Pointe stockholder approval (scheduled for June 23rd)

Conditions and Starwood Capital and TRI Pointe’s management have agreed to vote approximately 40%

Expected Closing of outstanding TRI Pointe shares in favor of the transaction

Weyerhaeuser Board has approved the transaction and no Weyerhaeuser shareholder

vote is required

(1) Assumes 129,700,000 TRI Pointe common shares issued at closing and TRI Pointe share price of $16.50 as of May 21, 2014. (2) Pro Forma for the transaction Starwood Capital Group ownership will decline from ~40.0% to ~7.4%.

6 |

|

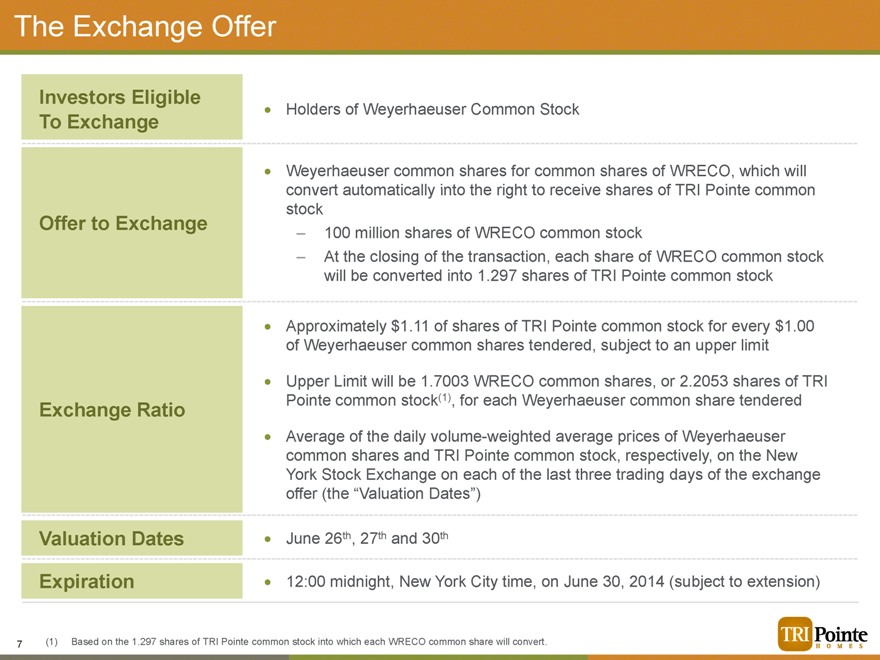

The Exchange Offer

Investors Eligible Holders of Weyerhaeuser Common Stock

To Exchange

Weyerhaeuser common shares for common shares of WRECO, which will

convert automatically into the right to receive shares of TRI Pointe common

stock

Offer to Exchange – 100 million shares of WRECO common stock

– At the closing of the transaction, each share of WRECO common stock

will be converted into 1.297 shares of TRI Pointe common stock

Approximately $1.11 of shares of TRI Pointe common stock for every $1.00

of Weyerhaeuser common shares tendered, subject to an upper limit

Upper Limit will be 1.7003 WRECO common shares, or 2.2053 shares of TRI

Exchange Ratio Pointe common stock(1), for each Weyerhaeuser common share tendered

Average of the daily volume-weighted average prices of Weyerhaeuser

common shares and TRI Pointe common stock, respectively, on the New

York Stock Exchange on each of the last three trading days of the exchange

offer (the “Valuation Dates”)

Valuation Dates June 26th, 27th and 30th

Expiration 12:00 midnight, New York City time, on June 30, 2014 (subject to extension)

(1) |

| Based on the 1.297 shares of TRI Pointe common stock into which each WRECO common share will convert. |

7 |

|

Company Overview

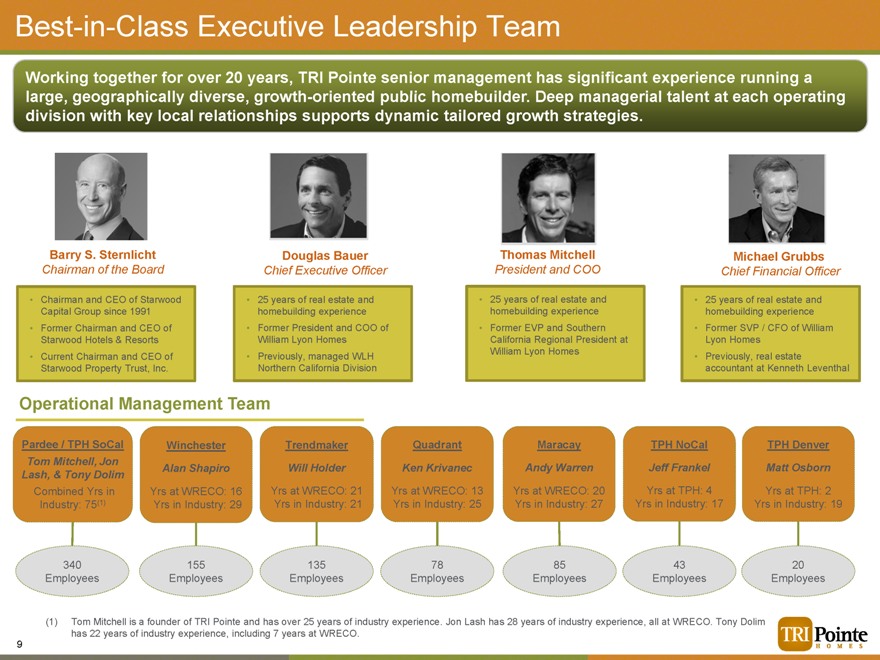

Best-in-Class Executive Leadership Team

Working together for over 20 years, TRI Pointe senior management has significant experience running a

large, geographically diverse, growth-oriented public homebuilder. Deep managerial talent at each operating division with key local relationships supports dynamic tailored growth strategies.

Barry S. Sternlicht Douglas Bauer Thomas Mitchell Michael Grubbs

Chairman of the Board Chief Executive Officer President and COO Chief Financial Officer

• |

| Chairman and CEO of Starwood 25 years of real estate and 25 years of real estate and 25 years of real estate and |

Capital Group since 1991 homebuilding experience homebuilding experience homebuilding experience

• |

| Former Chairman and CEO of Former President and COO of Former EVP and Southern Former SVP / CFO of William |

Starwood Hotels & Resorts William Lyon Homes California Regional President at Lyon Homes

William Lyon Homes

• Current Chairman and CEO of • Previously, managed WLH • Previously, real estate

Starwood Property Trust, Inc. Northern California Division accountant at Kenneth Leventhal

Operational Management Team

Pardee / TPH SoCal Winchester Trendmaker Quadrant Maracay TPH NoCal TPH Denver

Tom Mitchell, Jon Alan Shapiro Will Holder Ken Krivanec Andy Warren Jeff Frankel Matt Osborn

Lash, & Tony Dolim

Combined Yrs in Yrs at WRECO: 16 Yrs at WRECO: 21 Yrs at WRECO: 13 Yrs at WRECO: 20 Yrs at TPH: 4 Yrs at TPH: 2

Industry: 75(1) Yrs in Industry: 29 Yrs in Industry: 21 Yrs in Industry: 25 Yrs in Industry: 27 Yrs in Industry: 17 Yrs in Industry: 19

340 155 135 78 85 43 20

Employees Employees Employees Employees Employees Employees Employees

(1) Tom Mitchell is a founder of TRI Pointe and has over 25 years of industry experience. Jon Lash has 28 years of industry experience, all at WRECO. Tony Dolim has 22 years of industry experience, including 7 years at WRECO.

9

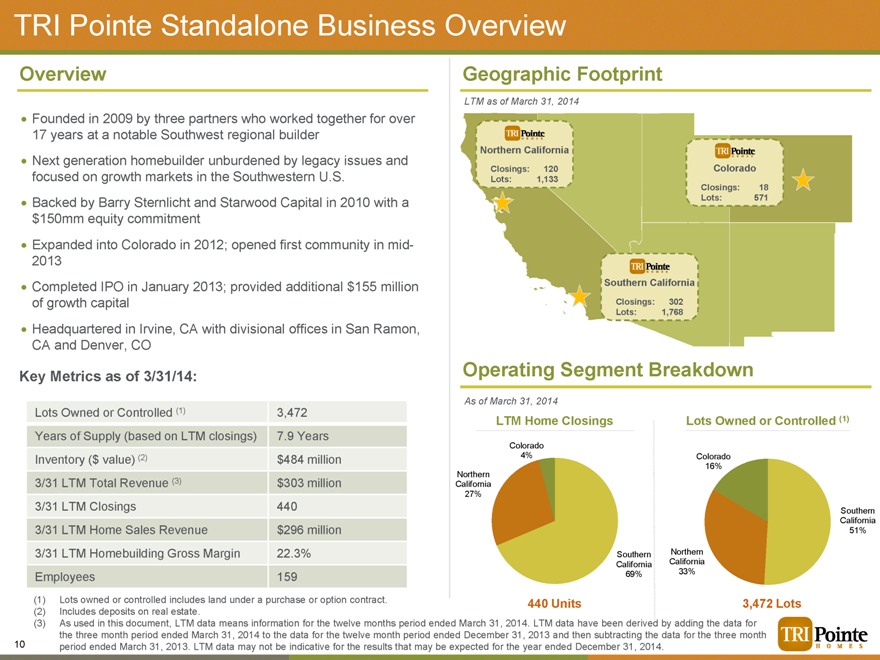

TRI Pointe Standalone Business Overview

Overview

Founded in 2009 by three partners who worked together for over

17 years at a notable Southwest regional builder

Next generation homebuilder unburdened by legacy issues and

focused on growth markets in the Southwestern U.S.

Backed by Barry Sternlicht and Starwood Capital in 2010 with a

$150mm equity commitment

Expanded into Colorado in 2012; opened first community in mid-

2013

Completed IPO in January 2013; provided additional $155 million

of growth capital

Headquartered in Irvine, CA with divisional offices in San Ramon,

CA and Denver, CO

Geographic Footprint

LTM as of March 31, 2014

Northern California

Closings: 120 Colorado

Lots: 1,133

Closings: 18

Lots: 571

Southern California

Closings: 302

Lots: 1,768

Key Metrics as of 3/31/14:

Lots Owned or Controlled (1) 3,472

Years of Supply (based on LTM closings) 7.9 Years

Inventory ($ value) (2) $484 million

3/31 LTM Total Revenue (3) $303 million

3/31 LTM Closings 440

3/31 LTM Home Sales Revenue $296 million

3/31 LTM Homebuilding Gross Margin 22.3%

Employees 159

Operating Segment Breakdown

As of March 31, 2014

LTM Home Closings Lots Owned or Controlled (1)

Colorado

4% Colorado

16%

Northern

California

27%

Southern

California

51%

Southern Northern

California California

69% 33%

440 Units 3,472 Lots

(1) |

| Lots owned or controlled includes land under a purchase or option contract. |

(2) |

| Includes deposits on real estate. |

(3) As used in this document, LTM data means information for the twelve months period ended March 31, 2014. LTM data have been derived by adding the data for the three month period ended March 31, 2014 to the data for the twelve month period ended December 31, 2013 and then subtracting the data for the three month period ended March 31, 2013. LTM data may not be indicative for the results that may be expected for the year ended December 31, 2014.

10

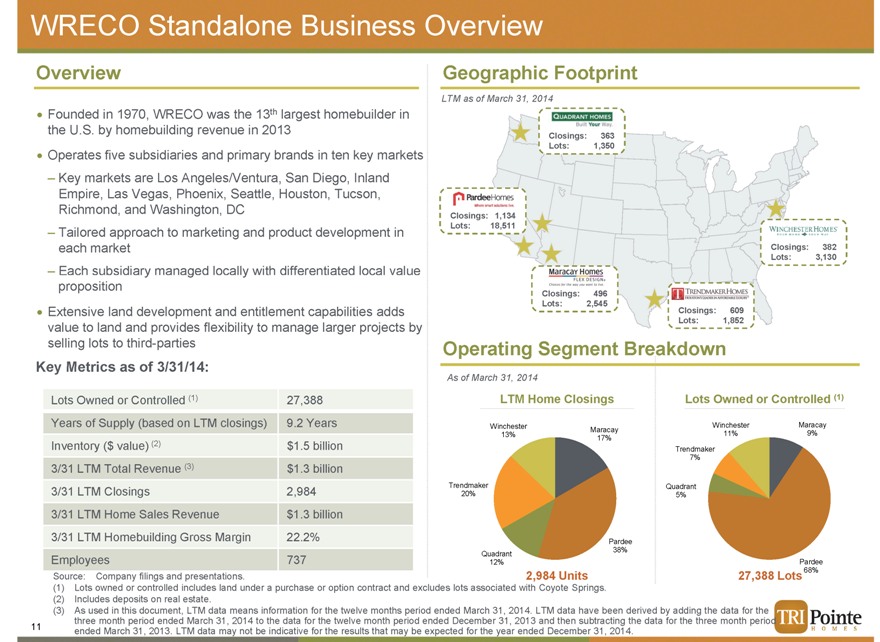

WRECO Standalone Business Overview

Overview

Founded in 1970, WRECO was the 13th largest homebuilder in

the U.S. by homebuilding revenue in 2013

Operates five subsidiaries and primary brands in ten key markets

–

Key markets are Los Angeles/Ventura, San Diego, Inland

Empire, Las Vegas, Phoenix, Seattle, Houston, Tucson,

Richmond, and Washington, DC

–

Tailored approach to marketing and product development in

each market

–

Each subsidiary managed locally with differentiated local value

proposition

Extensive land development and entitlement capabilities adds

value to land and provides flexibility to manage larger projects by

selling lots to third-parties

Geographic Footprint

LTM as of March 31, 2014

Closings: 363

Lots: 1,350

Closings: 1,134

Lots: 18,511

Closings: 382

Lots: 3,130

Closings: 496

Lots: 2,545

Closings: 609

Lots: 1,852

Key Metrics as of 3/31/14:

Lots Owned or Controlled (1) 27,388

Years of Supply (based on LTM closings) 9.2 Years

Inventory ($ value) (2) $1.5 billion

3/31 LTM Total Revenue (3) $1.3 billion

3/31 LTM Closings 2,984

3/31 LTM Home Sales Revenue $1.3 billion

3/31 LTM Homebuilding Gross Margin 22.2%

Employees 737

Operating Segment Breakdown

As of March 31, 2014

LTM Home Closings Lots Owned or Controlled (1)

Winchester Winchester Maracay

Maracay

13% 11% 9%

17%

Trendmaker

7%

Trendmaker Quadrant

20% 5%

Pardee

Quadrant 38%

12% Pardee

2,984 Units 27,388 Lots 68%

Source: Company filings and presentations.

(1) Lots owned or controlled includes land under a purchase or option contract and excludes lots associated with Coyote Springs. (2) Includes deposits on real estate.

(3) As used in this document, LTM data means information for the twelve months period ended March 31, 2014. LTM data have been derived by adding the data for the three month period ended March 31, 2014 to the data for the twelve month period ended December 31, 2013 and then subtracting the data for the three month period ended March 31, 2013. LTM data may not be indicative for the results that may be expected for the year ended December 31, 2014.

11

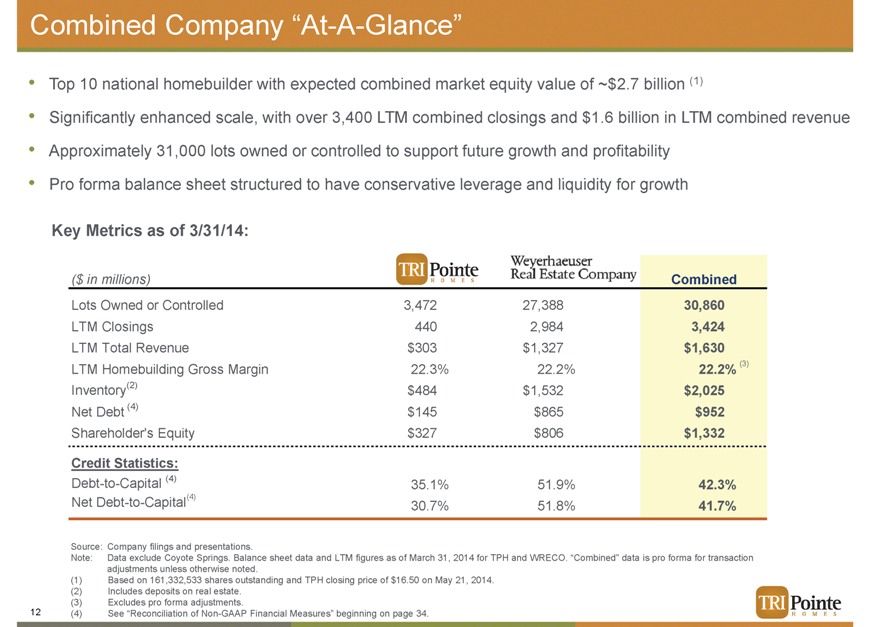

Combined Company “At-A-Glance”

• |

| Top 10 national homebuilder with expected combined market equity value of ~$2.7 billion (1) |

• |

| Significantly enhanced scale, with over 3,400 LTM combined closings and $1.6 billion in LTM combined revenue |

• |

| Approximately 31,000 lots owned or controlled to support future growth and profitability |

• |

| Pro forma balance sheet structured to have conservative leverage and liquidity for growth |

Key Metrics as of 3/31/14:

($ in millions) Weyerhaeuser Real Estate Company Combined

Lots Owned or Controlled 3,472 27,388 30,860

LTM Closings 440 2,984 3,424

LTM Total Revenue $303 $1,327 $1,630

LTM Homebuilding Gross Margin 22.3% 22.2% 22.2% (3)

Inventory(2) $484 $1,532 $2,025

Net Debt (4) $145 $865 $952

Shareholder’s Equity $327 $806 $1,332

Credit Statistics:

Debt-to-Capital (4) 35.1% 51.9% 42.3%

Net Debt-to-Capital(4) 30.7% 51.8% 41.7%

Source: Company filings and presentations.

Note: Data exclude Coyote Springs. Balance sheet data and LTM figures as of March 31, 2014 for TPH and WRECO. “Combined” data is pro forma for transaction adjustments unless otherwise noted.

(1) Based on 161,332,533 shares outstanding and TPH closing price of $16.50 on May 21, 2014. (2) Includes deposits on real estate.

(3) |

| Excludes pro forma adjustments. |

(4) |

| See “Reconciliation of Non-GAAP Financial Measures” beginning on page 34. |

12

Leading Brand Names Targeted to Specific Markets

Markets: Orange County, Los Angeles,

San Diego, San Francisco Bay Area,

Denver Market: Greater Puget Sound Area

LTM Single-Family Closings: 440 LTM Single-Family Closings: 363

Lots Owned or Controlled: 3,472 Lots Owned or Controlled: 1,350

Markets: Los Angeles/Ventura, Inland

Empire, San Diego, Las Vegas Markets: Washington DC, Richmond

LTM Single-Family Closings: 1,134 LTM Single-Family Closings: 382

Lots Owned or Controlled: 18,511 Lots Owned or Controlled: 3,130

Markets: Phoenix, Tucson Market: Houston

LTM Single-Family Closings: 496 LTM Single-Family Closings: 609

Lots Owned or Controlled: 2,545 Lots Owned or Controlled: 1,852

Combined Lots Owned or Controlled: 30,860 Combined LTM Single-Family Closings: 3,424

Note: All lots owned or controlled as well as LTM closings as of March 31, 2014.

13

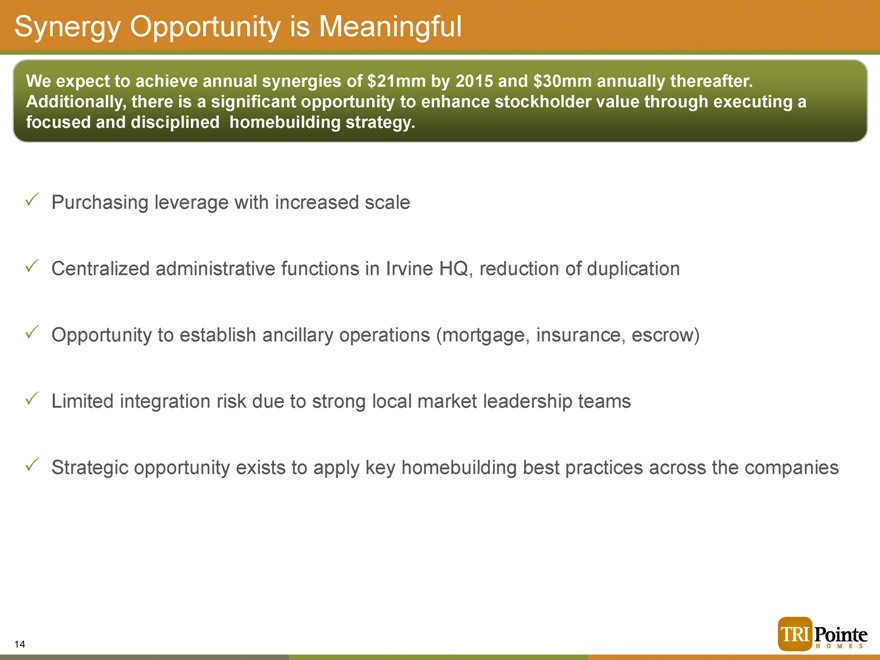

Synergy Opportunity is Meaningful

We expect to achieve annual synergies of $21mm by 2015 and $30mm annually thereafter.

Additionally, there is a significant opportunity to enhance stockholder value through executing a focused and disciplined homebuilding strategy.

Purchasing leverage with increased scale

Centralized administrative functions in Irvine HQ, reduction of duplication Opportunity to establish ancillary operations (mortgage, insurance, escrow) Limited integration risk due to strong local market leadership teams

Strategic opportunity exists to apply key homebuilding best practices across the companies

14

Investment Highlights

TRI Pointe & WRECO: A Powerful Combination and Strong Fit

1 Best-in-Class Management Team Forming a Top 10 National Homebuilder with Expected Combined Equity Market Value of ~$2.7bn(1)

2 Significant Land Supply to Fuel Growth at the Right Point in the Housing Recovery 3 Complementary Footprint: Merchant Building Model with Long California Land Position 4 Premium Brands and Quality Product Enhance Strong Partnerships With Land Owners 5 Core Focus on Move-Up Segment with Expertise Across a Broad Range of Products 6 Leadership Positions and Differentiated Strategies in Long Term Growth Markets 7 Development Capabilities and Operating Efficiency Drive Attractive Margin Profile 8 Balance Sheet Structured to Have Conservative Leverage and Liquidity for Growth

(1) |

| Based on 161,332,533 shares outstanding after closing and TPH closing price of $16.50 on May 21, 2014. |

16

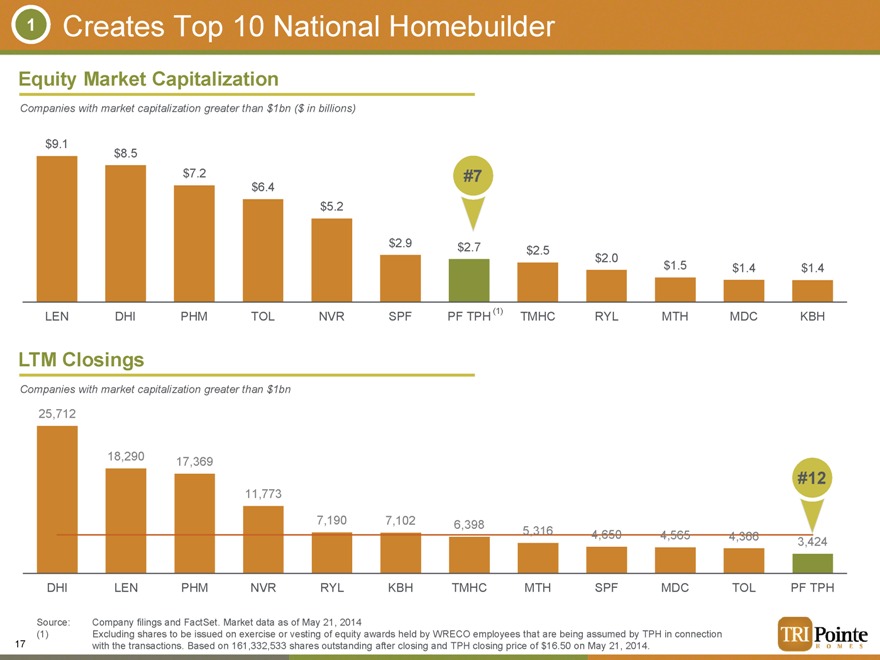

1

Creates Top 10 National Homebuilder

Equity Market Capitalization

Companies with market capitalization greater than $1bn ($ in billions)

$9.1

$8.5

$7.2 #7

$6 4.

$5.2

$2.9 $2.7 $2.5

$2.0 $1.5 $1.4 $1.4

LEN DHI PHM TOL NVR SPF PF TPH (1) TMHC RYL MTH MDC KBH

LTM Closings

Companies with market capitalization greater than $1bn

25,712

18,290 17,369

#12

11,773

7,190 7,102 6,398

5,316 4,650 4,565 4,366 3,424

DHI LEN PHM NVR RYL KBH TMHC MTH SPF MDC TOL PF TPH

Source: Company filings and FactSet. Market data as of May 21, 2014

(1) Excluding shares to be issued on exercise or vesting of equity awards held by WRECO employees that are being assumed by TPH in connection with the transactions. Based on 161,332,533 shares outstanding after closing and TPH closing price of $16.50 on May 21, 2014.

17

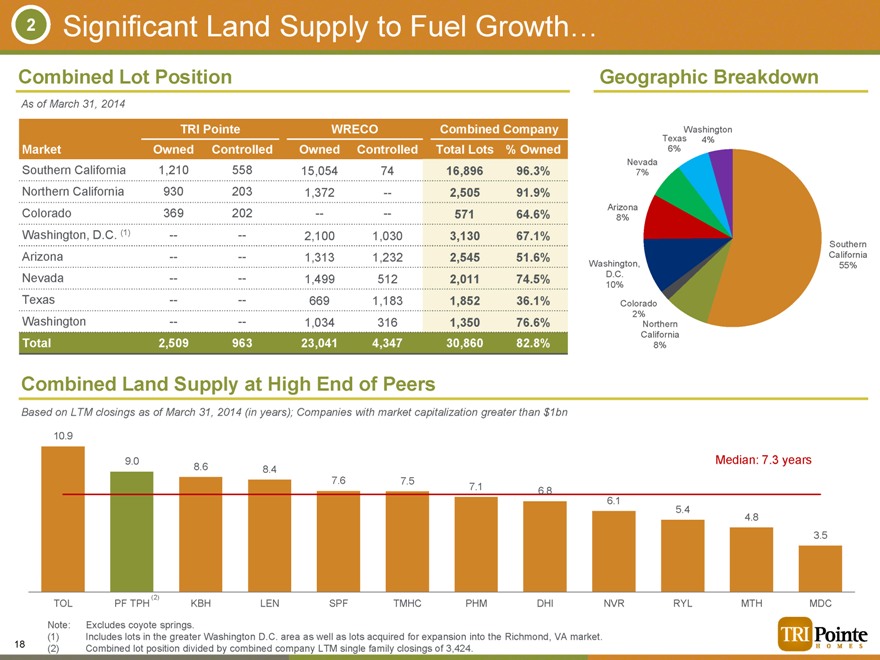

2 |

| Significant Land Supply to Fuel Growth… |

Combined Lot Position

As of March 31, 2014

TRI Pointe WRECO Combined Company

Market Owned Controlled Owned Controlled Total Lots % Owned

Southern California 1,210 558 15,054 74 16,896 96.3%

Northern California 930 203 1,372 — 2,505 91.9%

Colorado 369 202 — — 571 64.6%

Washington, D.C. (1) — — 2,100 1,030 3,130 67.1%

Arizona — — 1,313 1,232 2,545 51.6%

Nevada — — 1,499 512 2,011 74.5%

Texas — — 669 1,183 1,852 36.1%

Washington — — 1,034 316 1,350 76.6%

Total 2,509 963 23,041 4,347 30,860 82.8%

Geographic Breakdown

Washington

Texas 4%

6%

Nevada

7%

Arizona

8%

Southern

California

Washington, 55%

D.C.

10%

Colorado

2%

Northern

California

8%

Combined Land Supply at High End of Peers

Based on LTM closings as of March 31, 2014 (in years); Companies with market capitalization greater than $1bn

10.9

9.0 Median: 7.3 years

8.6 8.4

7.6 7.5

7.1 6.8

6.1

5.4

4.8

3.5

TOL PF TPH (2) KBH LEN SPF TMHC PHM DHI NVR RYL MTH MDC

Note: Excludes coyote springs.

(1) Includes lots in the greater Washington D.C. area as well as lots acquired for expansion into the Richmond, VA market. (2) Combined lot position divided by combined company LTM single family closings of 3,424.

18

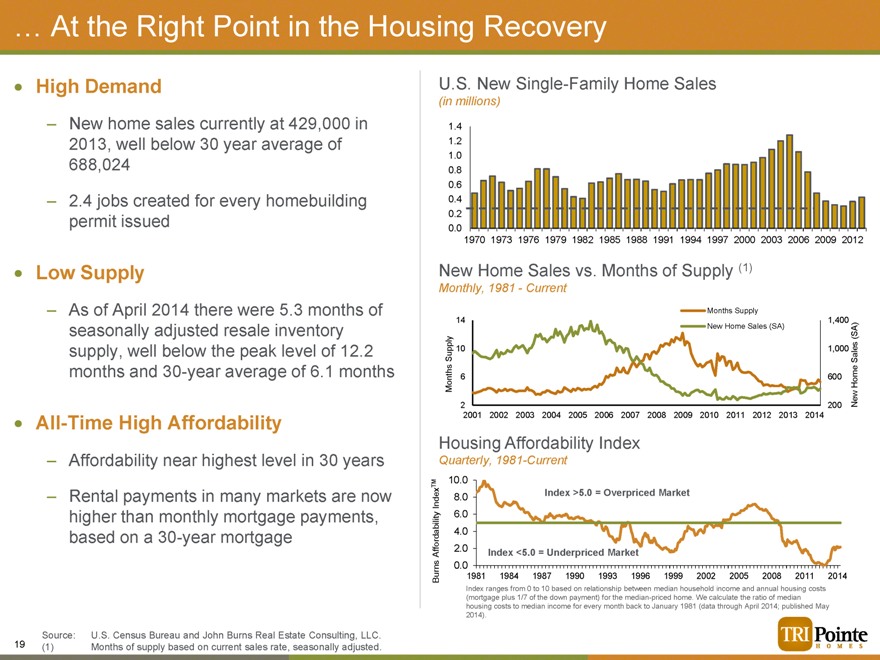

… At the Right Point in the Housing Recovery

High Demand

– New home sales currently at 429,000 in 2013, well below 30 year average of 688,024

– 2.4 jobs created for every homebuilding permit issued

Low Supply

– As of April 2014 there were 5.3 months of seasonally adjusted resale inventory supply, well below the peak level of 12.2 months and 30-year average of 6.1 months

All-Time High Affordability

– Affordability near highest level in 30 years

– Rental payments in many markets are now higher than monthly mortgage payments, based on a 30-year mortgage

U.S. New Single-Family Home Sales

(in millions)

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

New Home Sales vs. Months of Supply (1)

Monthly, 1981—Current

Months Supply

14 1,400

New Home Sales (SA)(SA)

Supply 10 1,000 Sales

6 600

Months Home

2 200 New

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Housing Affordability Index

Quarterly, 1981-Current

TM 10.0

Index 8.0 Index >5.0 = Overpriced Market

6.0

4.0

Affordability 2.0 Index <5.0 = Underpriced Market

0.0

Burns 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

Index ranges from 0 to 10 based on relationship between median household income and annual housing costs

(mortgage plus 1/7 of the down payment) for the median-priced home. We calculate the ratio of median

housing costs to median income for every month back to January 1981 (data through April 2014; published May

2014).

Source: U.S. Census Bureau and John Burns Real Estate Consulting, LLC. (1) Months of supply based on current sales rate, seasonally adjusted.

19

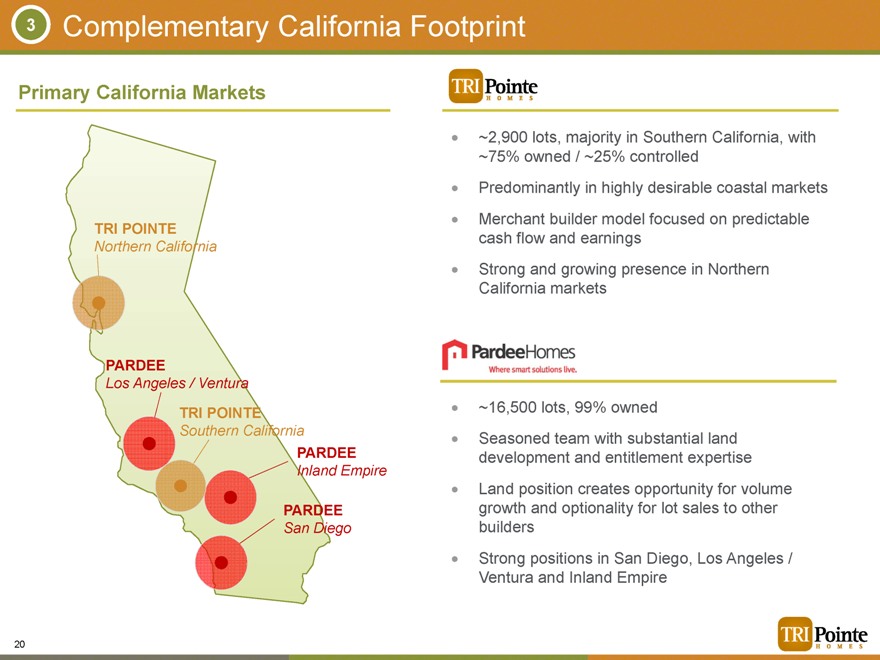

3 |

| Complementary California Footprint |

Primary California Markets

TRI POINTE

Northern California

PARDEE

Los Angeles / Ventura

TRI POINTE

Southern California

PARDEE

Inland Empire

PARDEE

San Diego

~2,900 lots, majority in Southern California, with

~75% owned / ~25% controlled

Predominantly in highly desirable coastal markets

Merchant builder model focused on predictable

cash flow and earnings

Strong and growing presence in Northern

California markets

~16,500 lots, 99% owned

Seasoned team with substantial land

development and entitlement expertise

Land position creates opportunity for volume

growth and optionality for lot sales to other

builders

Strong positions in San Diego, Los Angeles /

Ventura and Inland Empire

20

4 |

| Important Land Owner and Developer Partnerships |

Diverse product expertise and premium brands will continue to make the combined company an attractive homebuilding partner for master plan communities

Entitlement, land development and community planning expertise, which adds value to land through the development cycle

Existing TRI Pointe Relationships Existing WRECO Relationships

21

5 |

| Lifestyle Builder Focused on Move-Up Segment |

Average Selling Price

(Last Reported Quarter, $ in ‘000s, companies with market cap > $1.0bn)

$694

$525

$449

$422 Median: $364

$377 $366 $361

$327 $317 $307 $305

$271

TOL PF TPH SPF TMHC MDC MTH NVR RYL PHM LEN KBH DHI

U.S. 5-Year Forecasted vs. LTM Demand

25%

20%

15%

10%

5%

0%

100– 150– 200– 250– 300– 350– 400– 450– 500– 550– 600– or

$ 150K $ 200K $ 250K $ 300K $ 350K $ 400K $ 450K $ 500K $ 550K $ 600K $ 750K 750 more

$

Distribution of potential demand by price range

Dist. of actual new home closings over LTM by price range

Quality Product Across the Spectrum

TRI Pointe WRECO

Executive

Level

Chantrea, San Jose Alta Del Mar, San Diego

Move-Up

Woodson, Playa Vista Montelena, Phoenix

Entry-Level

Detached

Sendero, Tehaleh, Puyallup

Rancho Mission Viejo

Entry-Level

Attached

Aldea, Temecula Heatheridge, Santa

Clarita

Source: Company filings and Hanley Wood.

22

6 |

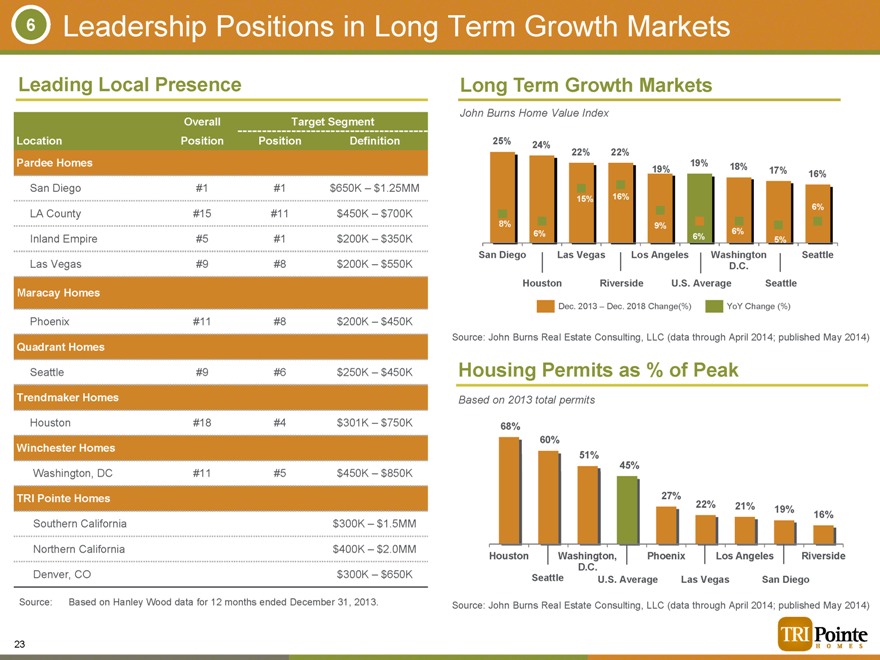

| Leadership Positions in Long Term Growth Markets |

Leading Local Presence

Overall Target Segment

Location Position Position Definition

Pardee Homes

San Diego #1 #1 $650K – $1.25MM

LA County #15 #11 $450K – $700K

Inland Empire #5 #1 $200K – $350K

Las Vegas #9 #8 $200K – $550K

Maracay Homes

Phoenix #11 #8 $200K – $450K

Quadrant Homes

Seattle #9 #6 $250K – $450K

Trendmaker Homes

Houston #18 #4 $301K – $750K

Winchester Homes

Washington, DC #11 #5 $450K – $850K

TRI Pointe Homes

Southern California $300K – $1.5MM

Northern California $400K – $2.0MM

Denver, CO $300K – $650K

Source: Based on Hanley Wood data for 12 months ended December 31, 2013.

Long Term Growth Markets

John Burns Home Value Index

25% 24%

22% 22%

19% 19% 18% 17%

16%

15% 16%

6%

8% 9%

6% 6% 6%

5%

San Diego Las Vegas Los Angeles Washington Seattle

D.C.

Houston Riverside U.S. Average Seattle

Dec. 2013 – Dec. 2018 Change(%) YoY Change (%)

Source: John Burns Real Estate Consulting, LLC (data through April 2014; published May 2014)

Housing Permits as % of Peak

Based on 2013 total permits

68%

60%

51%

45%

27%

22% 21% 19%

16%

Houston Washington, Phoenix Los Angeles Riverside

D.C.

Seattle U.S. Average Las Vegas San Diego

Source: John Burns Real Estate Consulting, LLC (data through April 2014; published May 2014)

23

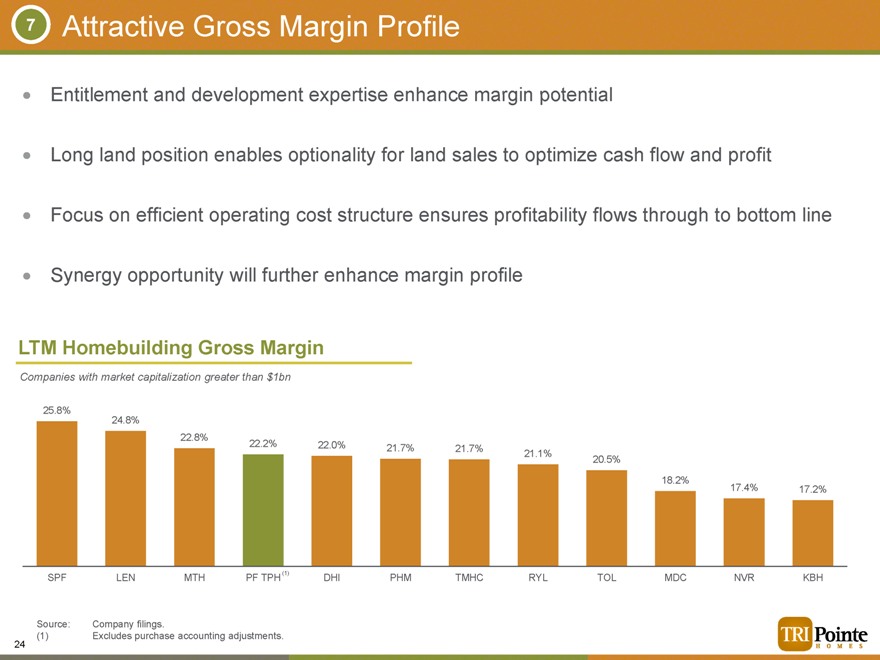

7 |

| Attractive Gross Margin Profile |

Entitlement and development expertise enhance margin potential

Long land position enables optionality for land sales to optimize cash flow and profit Focus on efficient operating cost structure ensures profitability flows through to bottom line Synergy opportunity will further enhance margin profile

LTM Homebuilding Gross Margin

Companies with market capitalization greater than $1bn

25.8%

24.8%

22.8%

22.2% |

| 22.0% 21.7% 21.7% 21.1% |

20.5%

18.2%

17.4% |

| 17.2% |

SPF LEN MTH PF TPH (1) DHI PHM TMHC RYL TOL MDC NVR KBH

Source: Company filings.

(1) |

| Excludes purchase accounting adjustments. |

24

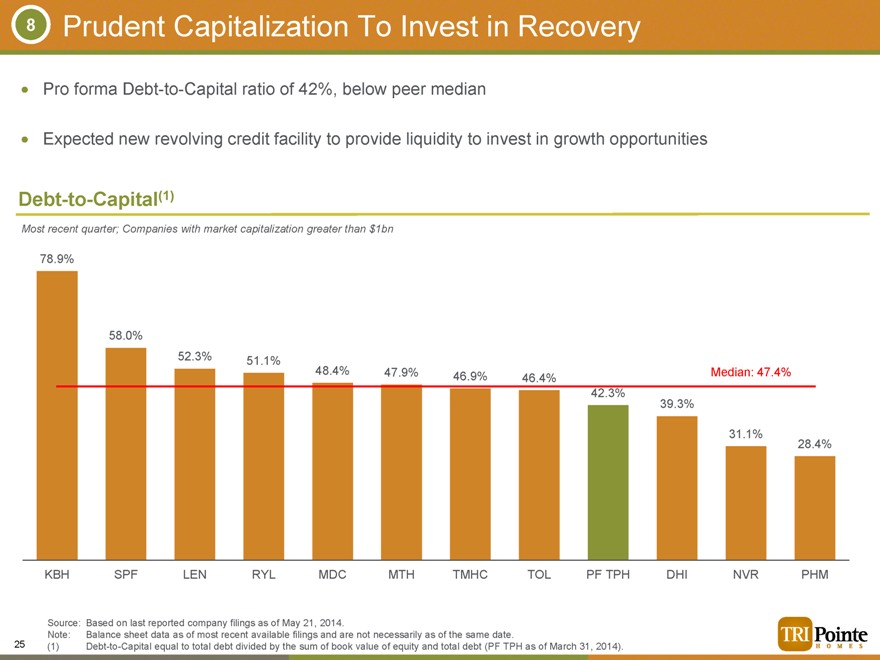

8 |

| Prudent Capitalization To Invest in Recovery |

Pro forma Debt-to-Capital ratio of 42%, below peer median

Expected new revolving credit facility to provide liquidity to invest in growth opportunities

Debt-to-Capital(1)

Most recent quarter; Companies with market capitalization greater than $1bn

78.9%

58.0%

52.3% |

| 51.1% |

48.4% |

| 47.9% 46.9% 46.4% Median: 47.4% |

42.3%

39.3%

31.1%

28.4%

KBH SPF LEN RYL MDC MTH TMHC TOL PF TPH DHI NVR PHM

Source: Based on last reported company filings as of May 21, 2014.

Note: Balance sheet data as of most recent available filings and are not necessarily as of the same date.

(1) Debt-to-Capital equal to total debt divided by the sum of book value of equity and total debt (PF TPH as of March 31, 2014).

25

Financial Overview

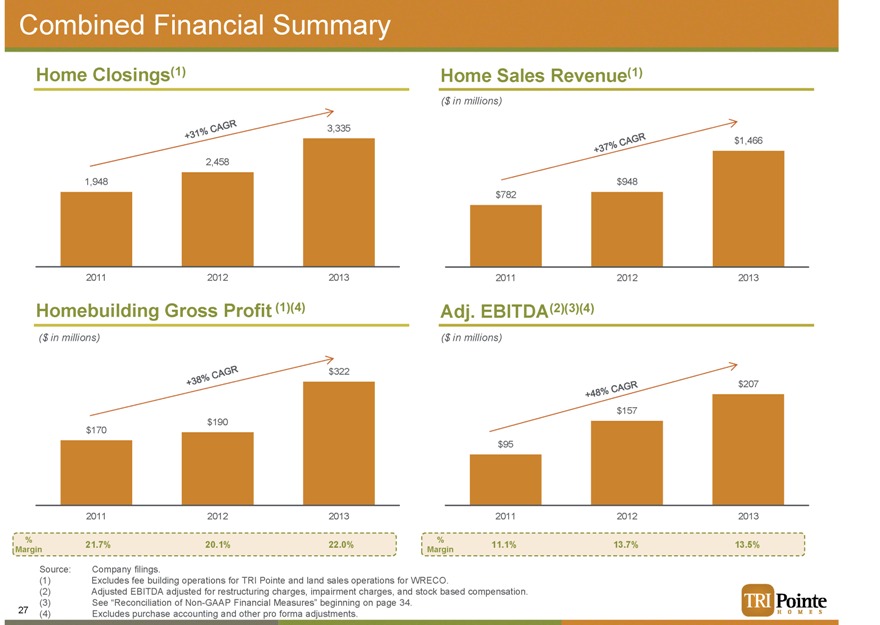

Combined Financial Summary

Home Closings(1) Home Sales Revenue(1)

($ in millions)

3,335

$1,466

2,458

1,948 $948

$782

2011 2012 2013 2011 2012 2013

Homebuilding Gross Profit (1)(4) Adj. EBITDA(2)(3)(4)

($ in millions)($ in millions)

$322

$207

$157

$190

$170

$95

2011 2012 2013 2011 2012 2013

%%

21.7% |

| 20.1% 22.0% 11.1% 13.7% 13.5% |

Margin Margin

Source: Company filings.

(1) |

| Excludes fee building operations for TRI Pointe and land sales operations for WRECO. |

(2) Adjusted EBITDA adjusted for restructuring charges, impairment charges, and stock based compensation. (3) See “Reconciliation of Non-GAAP Financial Measures” beginning on page 33.

(4) Excludes purchase accounting and other pro forma adjustments.

+31% CAGR +37% CAGR +38% CAGR +48% CAGR

27

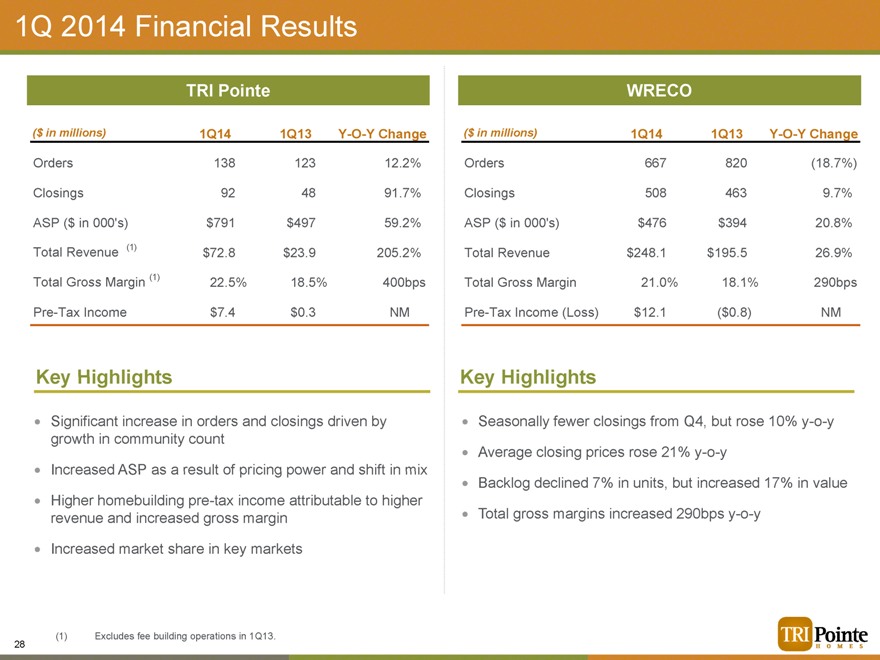

1Q 2014 Financial Results

TRI Pointe WRECO

($ in millions) 1Q14 1Q13 Y-O-Y Change($ in millions) 1Q14 1Q13 Y-O-Y Change

Orders 138 123 12.2% Orders 667 820(18.7%)

Closings 92 48 91.7% Closings 508 463 9.7%

ASP ($ in 000’s) $791 $497 59.2% ASP ($ in 000’s) $476 $394 20.8%

Total Revenue (1) $72.8 $23.9 205.2% Total Revenue $248.1 $195.5 26.9%

Total Gross Margin (1) 22.5% 18.5% 400bps Total Gross Margin 21.0% 18.1% 290bps

Pre-Tax Income $7.4 $0.3 NM Pre-Tax Income (Loss) $12.1($0.8) NM

Key Highlights Key Highlights

Significant increase in orders and closings driven by Seasonally fewer closings from Q4, but rose 10% y-o-y

growth in community count

Average closing prices rose 21% y-o-y

Increased ASP as a result of pricing power and shift in mix

Backlog declined 7% in units, but increased 17% in value

Higher homebuilding pre-tax income attributable to higher

revenue and increased gross margin Total gross margins increased 290bps y-o-y

Increased market share in key markets

(1) |

| Excludes fee building operations in 1Q13. |

28

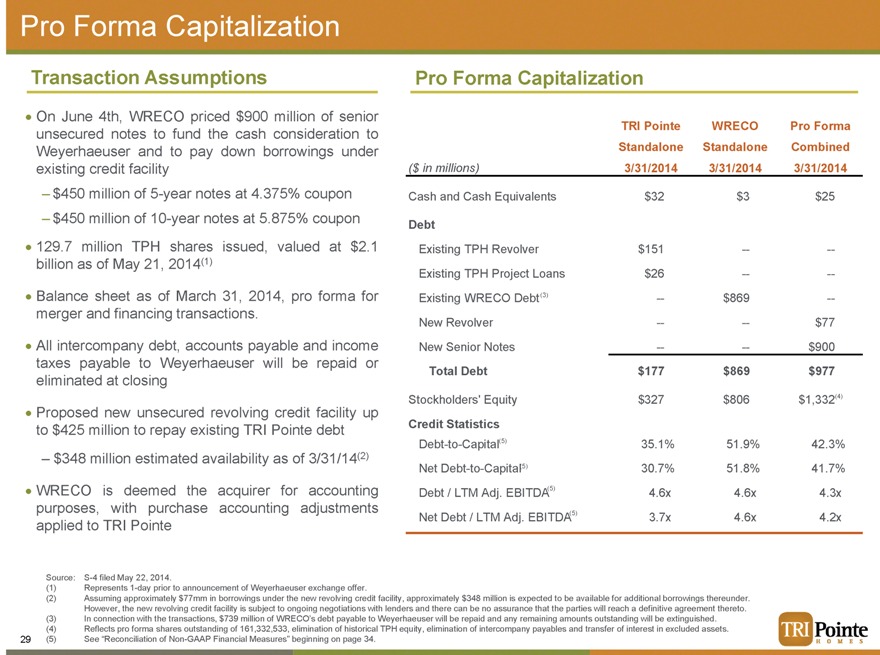

Pro Forma Capitalization

Transaction Assumptions

On June 4th, WRECO priced $900 million of senior unsecured notes to fund the cash consideration to Weyerhaeuser and to pay down borrowings under existing credit facility

– $450 million of 5-year notes at 4.375% coupon

– $450 million of 10-year notes at 5.875% coupon 129.7 million TPH shares issued, valued at $2.1 billion as of May 21, 2014(1)

Balance sheet as of March 31, 2014, pro forma for merger and financing transactions.

All intercompany debt, accounts payable and income taxes payable to Weyerhaeuser will be repaid or eliminated at closing

Proposed new unsecured revolving credit facility up to $425 million to repay existing TRI Pointe debt

$348 million estimated availability as of 3/31/14(2)

WRECO is deemed the acquirer for accounting purposes, with purchase accounting adjustments applied to TRI Pointe

Pro Forma Capitalization

TRI Pointe WRECO Pro Forma

Standalone Standalone Combined

($ in millions) 3/31/2014 3/31/2014 3/31/2014

Cash and Cash Equivalents $32 $3 $25

Debt

Existing TPH Revolver $151 — —

Existing TPH Project Loans $26 — —

Existing WRECO Debt (3) — $869 —

New Revolver — — $77

New Senior Notes — — $900

Total Debt $177 $869 $977

Stockholders’ Equity $327 $806 $1,332(4)

Credit Statistics

Debt-to-Capital(5) 35.1% 51.9% 42.3%

Net Debt-to-Capital(5) 30.7% 51.8% 41.7%

Debt / LTM Adj. EBITDA(5) 4.6x 4.6x 4.3x

Net Debt / LTM Adj. EBITDA(5) 3.7x 4.6x 4.2x

Source: S-4 filed May 22, 2014.

(1) |

| Represents 1-day prior to announcement of Weyerhaeuser exchange offer. |

(2) Assuming approximately $77mm in borrowings under the new revolving credit facility, approximately $348 million is expected to be available for additional borrowings thereunder. However, the new revolving credit facility is subject to ongoing negotiations with lenders and there can be no assurance that the parties will reach a definitive agreement thereto. (3) In connection with the transactions, $739 million of WRECO’s debt payable to Weyerhaeuser will be repaid and any remaining amounts outstanding will be extinguished.

(4) Reflects pro forma shares outstanding of 161,332,533, elimination of historical TPH equity, elimination of intercompany payables and transfer of interest in excluded assets. (5) See “Reconciliation of Non-GAAP Financial Measures” beginning on page 34.

29

Conclusion

TRI Pointe & WRECO: A Powerful Combination and Strong Fit

Top 10 National Homebuilder with Expected Combined Equity Market Value of ~$2.7bn(1) TRI Pointe’s Industry-Leading Management + WRECO’s Strong Local Market Franchises Significant Land Supply to Fuel Growth at the Right Point in the Housing Recovery Portfolio of Quality Brands with Leadership Positions in Long-Term Growth Markets

(1) |

| Based on 161,332,533 shares outstanding and TPH closing price of $16.50 on May 21, 2014. |

Balance Sheet Structured to Have Conservative Leverage and Liquidity for Growth

31

Appendix

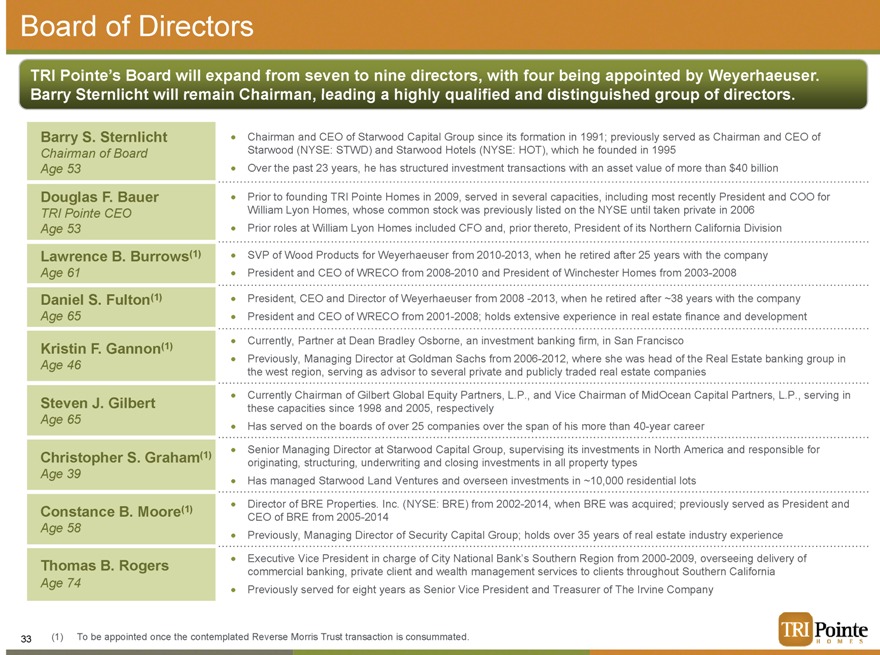

Board of Directors

TRI Pointe’s Board will expand from seven to nine directors, with four being appointed by Weyerhaeuser. Barry Sternlicht will remain Chairman, leading a highly qualified and disdinguished group of directors.

Barry S. Sternlicht

Chairman of Board Age 53

Douglas F. Bauer

TRI Pointe CEO Age 53

Lawrence B. Burrows(1)

Age 61

Daniel S. Fulton(1)

Age 65

Kristin F. Gannon(1)

Age 46

Steven J. Gilbert

Age 65

Christopher S. Graham(1)

Age 39

Constance B. Moore(1)

Age 58

Thomas B. Rogers

Age 74

Chairman and CEO of Starwood Capital Group since its formation in 1991; previously served as Chairman and CEO of Starwood (NYSE: STWD) and Starwood Hotels (NYSE: HOT), which he founded in 1995 Over the past 23 years, he has structured investment transactions with an asset value of more than $40 billion

Prior to founding TRI Pointe Homes in 2009, served in several capacities, including most recently President and COO for William Lyon Homes, whose common stock was previously listed on the NYSE until taken private in 2006 Prior roles at William Lyon Homes included CFO and, prior thereto, President of its Northern California Division

SVP of Wood Products for Weyerhaeuser from 2010-2013, when he retired after 25 years with the company President and CEO of WRECO from 2008-2010 and President of Winchester Homes from 2003-2008

President, CEO and Director of Weyerhaeuser from 2008 -2013, when he retired after ~38 years with the company President and CEO of WRECO from 2001-2008; holds extensive experience in real estate finance and development

Currently, Partner at Dean Bradley Osborne, an investment banking firm, in San Francisco

Previously, Managing Director at Goldman Sachs from 2006-2012, where she was head of the Real Estate banking group in the west region, serving as advisor to several private and publicly traded real estate companies

Currently Chairman of Gilbert Global Equity Partners, L.P., and Vice Chairman of MidOcean Capital Partners, L.P., serving in these capacities since 1998 and 2005, respectively Has served on the boards of over 25 companies over the span of his more than 40-year career

Senior Managing Director at Starwood Capital Group, supervising its investments in North America and responsible for originating, structuring, underwriting and closing investments in all property types Has managed Starwood Land Ventures and overseen investments in ~10,000 residential lots

Director of BRE Properties. Inc. (NYSE: BRE) from 2002-2014, when BRE was acquired; previously served as President and CEO of BRE from 2005-2014 Previously, Managing Director of Security Capital Group; holds over 35 years of real estate industry experience

Executive Vice President in charge of City National Bank’s Southern Region from 2000-2009, overseeing delivery of commercial banking, private client and wealth management services to clients throughout Southern California Previously served for eight years as Senior Vice President and Treasurer of The Irvine Company

(1) To be appointed once the contemplated Reverse Morris Trust transaction is consummated.

33

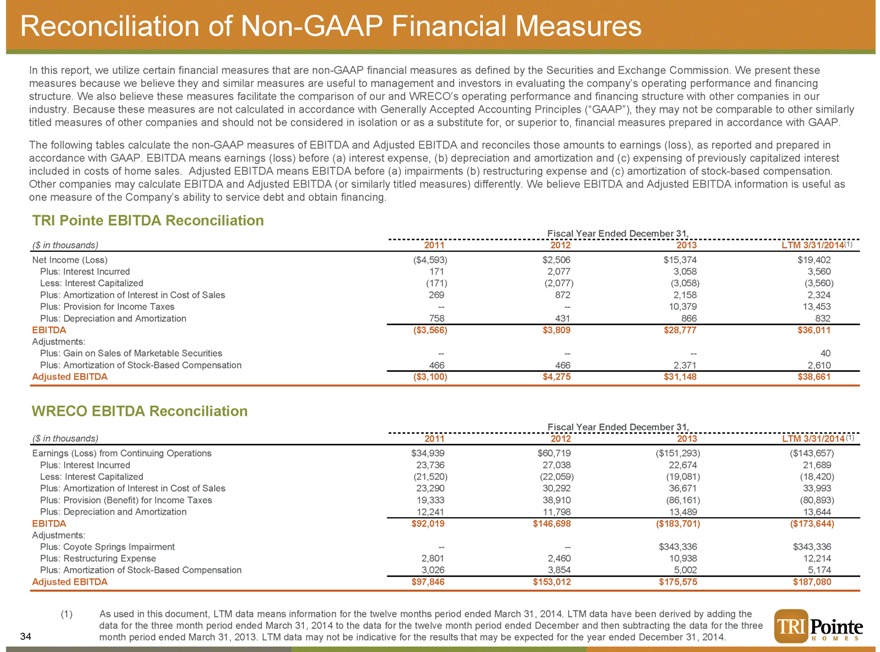

Reconciliation of Non-GAAP Financial Measures

In this report, we utilize certain financial measures that are non-GAAP financial measures as defined by the Securities and Exchange Commission. We present these measures because we believe they and similar measures are useful to management and investors in evaluating the company’s operating performance and financing structure. We also believe these measures facilitate the comparison of our and WRECO’s operating performance and financing structure with other companies in our industry. Because these measures are not calculated in accordance with Generally Accepted Accounting Principles (“GAAP”), they may not be comparable to other similarly titled measures of other companies and should not be considered in isolation or as a substitute for, or superior to, financial measures prepared in accordance with GAAP.

The following tables calculate the non-GAAP measures of EBITDA and Adjusted EBITDA and reconciles those amounts to earnings (loss), as reported and prepared in accordance with GAAP. EBITDA means earnings (loss) before (a) interest expense, (b) depreciation and amortization and (c) expensing of previously capitalized interest included in costs of home sales. Adjusted EBITDA means EBITDA before (a) impairments (b) restructuring expense and (c) amortization of stock-based compensation. Other companies may calculate EBITDA and Adjusted EBITDA (or similarly titled measures) differently. We believe EBITDA and Adjusted EBITDA information is useful as one measure of the Company’s ability to service debt and obtain financing.

TRI Pointe EBITDA Reconciliation

Fiscal Year Ended December 31,

($ in thousands) 2011 2012 2013 LTM 3/31/2014(1)

Net Income (Loss)($4,593) $2,506 $15,374 $19,402

Plus: Interest Incurred 171 2,077 3,058 3,560

Less: Interest Capitalized(171)(2,077)(3,058)(3,560)

Plus: Amortization of Interest in Cost of Sales 269 872 2,158 2,324

Plus: Provision for Income Taxes — — 10,379 13,453

Plus: Depreciation and Amortization 758 431 866 832

EBITDA($3,566) $3,809 $28,777 $36,011

Adjustments:

Plus: Gain on Sales of Marketable Securities — — — 40

Plus: Amortization of Stock-Based Compensation 466 466 2,371 2,610

Adjusted EBITDA($3,100) $4,275 $31,148 $38,661

WRECO EBITDA Reconciliation

Fiscal Year Ended December 31,

($ in thousands) 2011 2012 2013 LTM 3/31/2014 (1)

Earnings (Loss) from Continuing Operations $34,939 $60,719($151,293)($143,657)

Plus: Interest Incurred 23,736 27,038 22,674 21,689

Less: Interest Capitalized(21,520)(22,059)(19,081)(18,420)

Plus: Amortization of Interest in Cost of Sales 23,290 30,292 36,671 33,993

Plus: Provision (Benefit) for Income Taxes 19,333 38,910(86,161)(80,893)

Plus: Depreciation and Amortization 12,241 11,798 13,489 13,644

EBITDA $92,019 $146,698($183,701)($173,644)

Adjustments:

Plus: Coyote Springs Impairment — — $343,336 $343,336

Plus: Restructuring Expense 2,801 2,460 10,938 12,214

Plus: Amortization of Stock-Based Compensation 3,026 3,854 5,002 5,174

Adjusted EBITDA $97,846 $153,012 $175,575 $187,080

(1) As used in this document, LTM data means information for the twelve months period ended March 31, 2014. LTM data have been derived by adding the data for the three month period ended March 31, 2014 to the data for the twelve month period ended December and then subtracting the data for the three month period ended March 31, 2013. LTM data may not be indicative for the results that may be expected for the year ended December 31, 2014.

34

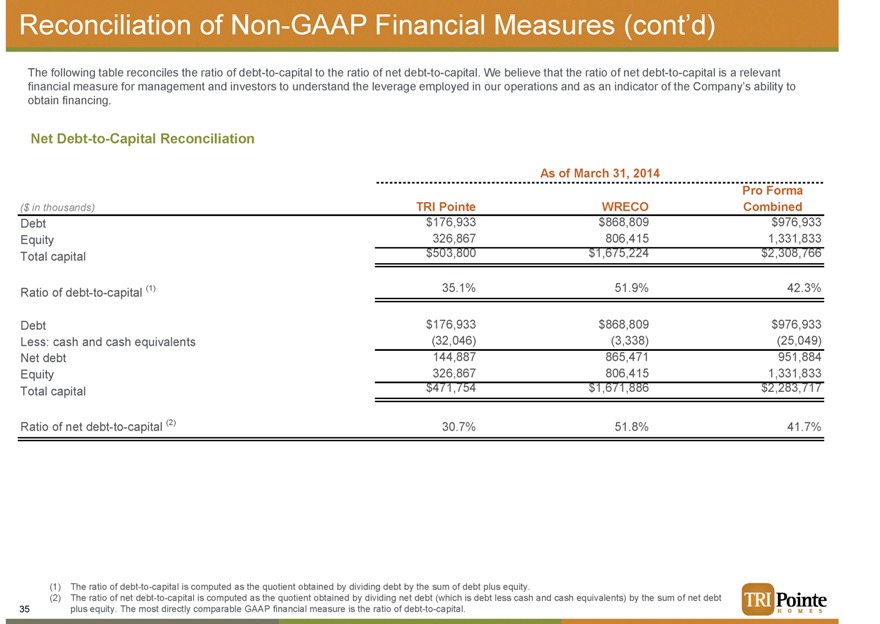

Reconciliation of Non-GAAP Financial Measures (cont’d)

The following table reconciles the ratio of debt-to-capital to the ratio of net debt-to-capital. We believe that the ratio of net debt-to-capital is a relevant financial measure for management and investors to understand the leverage employed in our operations and as an indicator of the Company’s ability to obtain financing.

Net Debt-to-Capital Reconciliation

As of March 31, 2014

Pro Forma

($ in thousands) TRI Pointe WRECO Combined

Debt $176,933 $868,809 $976,933

Equity 326,867 806,415 1,331,833

Total capital $503,800 $1,675,224 $2,308,766

Ratio of debt-to-capital (1) 35.1% 51.9% 42.3%

Debt $176,933 $868,809 $976,933

Less: cash and cash equivalents(32,046)(3,338)(25,049)

Net debt 144,887 865,471 951,884

Equity 326,867 806,415 1,331,833

Total capital $471,754 $1,671,886 $2,283,717

Ratio of net debt-to-capital (2) 30.7% 51.8% 41.7%

(1) |

| The ratio of debt-to-capital is computed as the quotient obtained by dividing debt by the sum of debt plus equity. |

(2) The ratio of net debt-to-capital is computed as the quotient obtained by dividing net debt (which is debt less cash and cash equivalents) by the sum of net debt plus equity. The most directly comparable GAAP financial measure is the ratio of debt-to-capital.

35