UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of March, 2020

Commission File Number: 001-14475

TELEFÔNICA BRASIL S.A.

(Exact name of registrant as specified in its charter)

TELEFONICA BRAZIL S.A.

(Translation of registrant’s name into English)

Av. Eng° Luís Carlos Berrini, 1376 - 28º andar

São Paulo, S.P.

Federative Republic of Brazil

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F | X |

| Form 40-F |

|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes |

|

| No | X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes |

|

| No | X |

![]()

MANAGEMENT REPORT

TELEFÔNICA BRASIL S.A.

Dear shareholders,

In accordance with legal and statutory provisions, the Management of Telefônica Brasil S.A. (“Telefônica Brasil”, “Company” or “Vivo”) hereby submits for your appreciation the Company’s Management Report and individual and consolidated Financial Statements, together with the Independent Auditors’ report and the opinions of the Company’s Board of Directors, Fiscal Council and Audit and Control Committee for the year ended December 31, 2019.

1. Message from Management

We are beginning a new decade, in which technology is even more present, exponentially transforming people's daily lives. We are currently going through new stages of this evolution, with accelerated digital connection between people, things, businesses and society as a whole. As Vivo, we want to continue to contribute to the digitalization of Brazil, from North to South.

In both urban and rural areas, the population demands high-quality connectivity. As the leading company in the country, we have consistently invested in the development of a differentiated infrastructure, focusing on superior technologies, such as fiber, 4G and 4.5G, to offer our 100 million users a unique experience in mobile and fixed connections.

In 2019, even in a context of a gradual economic recovery, Vivo’s investments reached an all-time high of R$9 billion, equivalent to approximately 20% of our revenue. By the end of 2020, Vivo will have invested R$26.5 billion in the Brazilian economy, completing its three-year investment plan announced two years ago on the New York Stock Exchange (NYSE). To shareholders and investors, we presented a consistent financial result, with a unique combination of revenue growth, EBITDA expansion, increased cash generation and higher shareholder remuneration. Cash generation reached a record level of R$8.2 billion in 2019, 19% more than in 2018, despite the cycle of higher investments.

In 2020, we will further accelerate this transformation, guided by a purpose that goes far beyond financial results and will define the way we work:Digitalizing to bring people closer, with content, entertainment, technology and education. To achieve this, we have four strategic pillars that will guide our activities.

The first of them is#TemVivopratudo(#Vivoservesallpurposes). Here, we present the best mobile and fixed connection technologies and our expansion in Brazil, which will be intensified throughout 2020. In 2019, we expanded our fiber presence to 43 new cities, far exceeding the expansion carried out in 2018. Altogether, we cover 164 municipalities and about 11 million homes and businesses. In terms of mobile coverage, we started to serve 89% of the populationwith 4G network, and 66% with 4.5G. We were elected the best mobile network in Brazil, according to the results of the “P3 Mobile Benchmark Brazil” survey1.

1

We also use two business models to expand our capillarity: the Vivo Fiber franchising project and a partnership with American Tower, which will drive expansion in Minas Gerais over the next three years.

The second pillar is#TemtudonaVivo(#YoufindeverythingatVivo), which translates into the vision that we are a technology company focused on all the needs of our customers, delivering the most desired digital content on the market through partnerships with major brands, such as NBA, NFL, Amazon Prime Video, Tidal, Spotify, Rappi and Netflix. We have changed the concept of our stores, which are now true technology hubs that offer a consultative and participative environment. There, our customers can find all kinds of devices, such as handsets, cameras, sensors, smart lamps, accessories and even drones.

We also made progress on other fronts and launched Vivo Car, a Wi-Fi device that turns cars into connected vehicles. In the financial segment, we are piloting an uncomplicatedloan service for our customers, calledVivo Money. In the corporate market, companies have also chosen us to digitalize their business, with the best cyber security, cloud computing, internet of things and big data services, in partnership with important global players, such as Cisco, Dell, Microsoft and Nokia.

All our initiatives are linked to the third pillar,#DNAVivo (#Vivo’sDNA):reliable, easy, efficient and dazzling. We are turning Vivo into a benchmark in customer service. In order to achieve this goal, we are seeking to engage our employees in all points of contact.

We want to deliver a unique and differentiated experience in our stores, call centers and digital channels. Meu Vivo, for example, already has more than 16 million unique users. A survey shows that 80% of users rate the interaction as close and clear. AURA, our artificial intelligence, performs around 20 million monthly transactions, with more than 90% accuracy, providing personalized answers about services, data consumption, account, recharge and other questions.

We are an inclusive company that wants diversity to be increasingly present, both in terms of gender, color, LGBTQ+ and people with disabilities and in terms of behavior, skills and attitudes. We look for people who have a passion for innovation and a desire to live in an environment in which difference enriches and inspires creativity and the achievement of sustainable results.

Without a doubt, Vivo's cultural change goes hand in hand with the digital transformation process. Our employees work based on agile models, such as squads, with multidisciplinary teams using Design Thinking and Agile to improve the customer experience. We have adopted coworking spaces that favor a collaborative environment and expanded remote work to two days a week. This change in culture has increased business agility and company satisfaction levels, as reflected in our latest e-NPS, an indicator that shows how likely employees are to recommend Vivo as a good place to work, which reached 72.5 points in 2019, a very high number for the Technology and Telecom sectors worldwide.

However, being close to customers and employees is not enough. We need to understand our leading role in the country's development, with results beyond the financial area and benefits to society.

With# Vivosustentável (#SustainableVivo), our fourth pillar, we developed actions, practices and initiatives that promote the well-being of society. Our approach to sustainability is based on economic, environmental and social balance. In the economic area, we are a publicly traded company that employs 33 thousand direct employees across Brazil and produces consistent results.

1 Analysis conducted by P3’s benchmarking experts and by Connect magazine on Brazil’s mobile network quality

2

In the social sphere, the Telefônica Vivo Foundation celebrated its 20th anniversary in 2019, providing digital training to 66 thousand educators, with an impact on 1.5 million students in 745 public schools. It has also provided capacity building in social entrepreneurship to 162 thousand young people by creating new solutions and opportunities for them and their communities through digital thinking. Innovating again, in 2019, the Foundation enabled the arrival of “42” in São Paulo, a pioneering initiative in Latin America that originated in Europe, focused on providing free disruptive training to data programmers.

Regarding environmental issues, 100% of our energy came from renewable sources. We reduced our emissions by more than 50% in absolute terms in 2019, exceeding the global targets for 2025 and offsetting 100% of the remaining emissions.

In theRecicle com a Vivo (Recycle with Vivo) program, we were pioneers in electronics reverse logistics. Since 2006, we have collected more than 110 tons of unused handsets, chargers and batteries, encouraging the ecological disposal of these materials. We have recycled over 62 thousand tons of electronic waste and cables from our operation in the past seven years. In addition, working used handsets can be exchanged for new devices with special discounts throughVivo Renova (Vivo Renews). We also maintained our participation in B3's Corporate Sustainability Index - ISE portfolio for the eighth consecutive year in 2019.

All these initiatives have been and will be increasingly reflected in the positioning of our brand, which was born to connect millions of people from all over Brazil. We connect people through sports, by sponsoring the Brazilian Soccer Team, cheering together with the country; through art, by supporting museums and maintaining the Vivo Theater; and through awareness-raising campaigns, with theTem Hora pra Tudo (There is a time for everything) campaign, which proposes a reflection on the conscious use of technology.

At the end of last year, we launchedVivo Brincar (Vivo Play) campaign, encouraging parents and children to redress the balance between technology and free play, bringing this reflection to the children's universe in a playful way.

As I complete my first year as CEO of Telefônica Brasil, I would like to thank our shareholders for their trust, our suppliers for their partnership and, above all, our employees for their dedication.

We will continue to work daily to strengthen our purpose, digitalizing and bringing people together.

Christian Gebara

CEO of Telefônica Brasil

2. Economic and Industry Environment

2.1.Economic Environment

After facing a period of uncertainty in the first half of 2019, the second semester was marked by the consolidation of economic recovery in Brazil. The external scenario was less favorable to emerging economies. The risk of a slowdown in global economic activity that emerged as of the third quarter increased risk aversion and contributed to reducing global liquidity. On the domestic front, the approval of the pension reform, together with advances in privatization and microeconomic reforms, reinforced the government's commitment to a pro-market economic policy. In an environment of low interest rates and inflation, economic agents regained confidence and started making new consumption and investment decisions as of the third quarter of the year. The effects of improved confidence and low interest rates should continue to be seen in the medium term. Risks associated with the evolution of the external scenario and domestic governance have to be monitored, since they can negatively impact financial assets.

3

On the fiscal front, the cumulative 12-month public sector primary deficit decreased to 0.7% of GDP in 20192, against 1.6% of GDP in 2018. The government's strict control of expenditures, the improvement in revenue stemming from economic recovery and additional revenue mainly generated by auctions contributed to the significant improvement in the fiscal result compared to the previous year. Nonetheless, gross debt rose from 74.2% in 2018 to 75.8% in 2019. However, the nominal public deficit fell from 7.1% of GDP to 5.9% of GDP, on the same comparison basis, as a result of the drop in interest rates.

Inflation accelerated in 2019. Wholesale inflation accelerated under the influence of the appreciation of the dollar. Retail inflation slowed down slightly, amid anchored inflation expectations. The IGP-DI, the General Price Index - Internal Availability, calculated by the Getúlio Vargas Foundation, stood at 7.7% in 2019, versus 7.1% in 2018, reflecting the increase in the IPA-DI, the Wholesale Price Index, which stood at 9.6% in 2019, versus 8.8% in 2018, and the IPC, Consumer Price Index, which stood at 4.1% in 2019, versus 4.3% in 2018. IPCA, the Extended Consumer Price Index, calculated by the Brazilian Institute of Geography and Statistics (IBGE) and used by the Central Bank of Brazil as a benchmark for its inflation targeting system, came to 4.3% in 2019, a 0.6 percentage point hike over the 3.7% recorded in 2018, close to the inflation target of 4.25% for the year.

In light of the benign inflation scenario, the Monetary Policy Committee (Copom) began a new cycle of cuts in the Selic interest rate in the second half of 2019, reducing it from 6.5% at the end of 2018 to 4.5% at the end of 2019. If we deduct annual inflation from this rate, we obtain a real interest rate of 0.2% at the end of 2019, versus 2.8% at the end of 2018.

Despite the positive balance in the domestic environment in 2019, the external environment was less favorable to emerging economies, amid risk of a slowdown in global economic activity and constant trade tensions between the United States and China.

This scenario contributed to the depreciation of the real over the course of the year, ending 2019 at US$1/R$4.03 (against US$1/R$3.87 at the end of 2018). The real depreciated 4.0% compared to the previous year. The average exchange rate for the year, of US$1/R$3.95, was 7.9% higher than in the previous year.

Last year was less favorable to external accounts.Brazil posted a US$50.8 billion trade surplus in 2019 (versus US$41.5 billion in 2018), as imports declined 6.3% and exports fell only 0.8%. Thus, the current account deficit increased to 2.8% of GDP at the end of 2019, versus 2.2% of GDP at the end of 2018. In terms of the country’s international reserves, Brazil ended the year with US$356.9 billion, compared to US$374.7 billion at the end of the previous year. The decline was mainly due to the use of part of the reserves to curb exchange rate volatility.

The recovery in economic activity became more consistent in 2019. After a first semester marked by uncertainty regarding governance and its impacts on the progress of economic reforms, the most important reform (social security) was approved in the second semester. Meanwhile, the government has also moved forward on the privatization and microeconomic reform agendas. As a result, economic agents regained confidence, in an environment of low inflation and interest rates, which stimulated consumption and investment decisions. GDP is estimated to have grown about 1.2% in 20193, after the 1.3% print recorded in 2018.

2.2.Competitive Environment

With the gradual improvement in the country's economic activity, investments in the telecommunications market continued to grow, reflecting an increase in confidence in the sector. Traditional businesses continued to be under pressure, with lower consumption of Landline Voice and Pay TV services being offset by the strong performance of the Fixed Broadband andPostpaid segments. On the other hand, digital services are becoming increasingly relevant in terms of the value perceived by consumers and companies. Given this situation, operators attempted to gain market share by increasing the number of bundled users, intensifying competition for high-end customers and delivering greater quality and innovation to consumers.

2Market expectation according to the Focus Bulletin.

4

In the Fixed market, Broadband continued to be the main driver of growth, increasing the number of accesses by 1.3 million in 2019, reaching over 32 million accesses4. Fiber expansion stood out once again, driven by the growth of regional providers, which gained market share both in large cities and in underserved locations.

The large operators, in turn, have focused on investments in expanding the next generation network in response to the market demand. Pay TV did not show the same resilience observed in previous years and accelerated the pace of customer base decline (reduction of 1.7 million in 20192), while demand for Over-the-top (OTT) video services increased. Landline Voice services continued to decline sharply, losing more than 3 million accesses in 20192.

With regard to the Mobile market, the operators remained focused on the prepaid-to-postpaid migration and competition for high-end customers, with delivery of coverage and better access quality, adapting their infrastructure to serve the growing demand for data. In the market, 4.5G coverage reached 2,693 municipalities in 2019 and is now available to 86% of the Brazilian population (versus 79% at the end of 2018)5. The Mobile dynamic was also marked by more aggressive commercial offers, with an increase in data allowances not accompanied a proportional price adjustment. Prepaid revenue fell less than in the previous year, positively influenced by increased use of data and the improvement in the country's economic activity.

The industry focused even more on market consolidation in 2019. One of the main drivers of this movement is the large fragmentation of regional fixed broadband providers, with 116 M&A transactions involving internet providers in the first half of 2019 (against 73 in the first half of 2018)6. Among the major operators, we highlight the acquisition of Nextel by Grupo América Móvil and the hiring by Oi of a financial advisory firm to assess its mobile operation.

Telefônica Brasil maintained its track record of delivering significant results throughout the year. In the Mobile business, it remained the leader in the Postpaid segment, with the largest share of high-end customers on the market, as a result of its commitment to quality and to delivering innovative solutions. In the Landline business, the year was marked by the expansion of its fiber network, reinforcing its positioning as the Brazilian operator with the greatest FTTH (Fiber to the Home) coverage. The Company also announced alternative models to accelerate the Fiber expansion with lower CAPEX and a better time-to-market, via a partnership with American Tower in more than 40 cities in the state of Minas Gerais and via a franchise model focused on neighborhoods and Brazilian municipalities in which it is not available.

2.3.Regulatory Environment

On the regulatory front, there were important events for the sectors. The main regulatory issues on the agenda of Telefônica Brasil, Anatel (National Telecommunications Agency) and the federal government are listed below:

· 5G Auction

· National IoT Plan

· New Regulatory Framework for Telecommunications

· International Roaming

· Silent Consent and Right of Passage

· New Quality Regulations

4Source: Anatel.

5Source: Teleco.

6Source: KPMG – Mergers and Acquisitions in the second quarter of 2019.

5

· Code of Conduct for Reducing Telesales Calls

The issues listed above are detailed in item 7.5 of the Company’s Reference Form, available on the Investor Relations websitewww.telefonica.com.br/ir

3. Business Strategy

In 2019, small players grew significantly in the fixed broadband market. These players have different pricing and positioning strategies and, in general, operate locally, but together they were the ones that grew the most in the year.

Despite the growth of these competitors, we continue to focus on expanding the fiber optic network in the country to deliver high-quality, high-speed broadband. Additionally, the Company continued to invest in digital transformation, increasing the number of customers with access to Meu Vivo and reducing the dependence on traditional contact channels.

With regard to offers in the fixed business, we increased the value proposition by offering speed trial periods in Fiber (FTTH), with a focus on delivering high speeds ranging from 100Mbps to 200Mbps.

In the Postpaid segment, the Company continues to lead the market with a 39.4% share, thanks to its strong positioning in the Vivo Postpaid Family category, which has evolved to deliver more benefits to customers, including increased allowances and more days of use outside the country for these customers. In addition, the Company drove growth in the postpaid segment through customer totalization, offering benefits, such as aggressive discounts and allowance bonuses for customers with Vivo broadband. This way, the Company was able to increase the volume of sales of postpaid plans.

Betting on digital transformation, we kept investing in Vivo Easy, a plan that is customizable trough the app by clients. We kept reinforcing that there is no monthly fees nor validity period for purchased services, such as internet and apps. There were also advances in the structure (back/front-end), contributing to product performance, and, mainly, in app interface and usability, improving the customer experience. In order to further diversify the portfolio, new partners were added, such as the TIKTOK social network and the MOOVIT mobility app. Internet allowance prices have been adjusted to make them more attractive and competitive for new and existing customers. In addition to these changes, aggressive offers now include cashback rewards, a practice that is widespread in digital media. The results of these actions, coupled with a broad digital media strategy focused on conversion, had a positive impact in the last quarter of 2019, with a significant increase in Vivo Easy plan adhesions and positive customer reviews of the app.

The Prepaid segment recorded significantly better results in 2019, supported by the expansion of the offer portfolio with new weekly and fortnightly options. These launches give customers more choice and maximize the profitability of the base. Vivo also maintained its Giga Chip offer, with double the amount of internet for 6 months, unlimited WhatsApp and 15 days free of charge. We innovated with a more segmented performance, using algorithms and machine learning to understand key moments in the customer's relationship with Vivo and provide a more personalized experience.

Finally, in line with the trend of delivering an increasingly personalized customer experience, theVivo Valoriza (Vivo Values) relationship program was restructured and relaunched in early 2020, delivering rewards based on the interests and preferences of each client in a simple and digital journey through the Meu Vivo app. The Company also launched a project to create and implement a customer relationship scale to establish a transparent, effective and dazzling dialogue throughout the life cycle, adjusting the content, timing, recurrence and channels by customer profile and implementing a new communication tone that brings Vivo closer to its customers.

6

3.1.Corporate Business

In 2019, the B2B market was again impacted by low economic growth, which forced companies to rationalize expenses, affecting the consumption of telecommunications services. Unemployment rates remained high and the informality ratio reached an all-time high. This scenario required an adjustment of the value proposition of mobile and fixed offers. In IT, growing demand for business digitalization and infrastructure upgrades, supported by the expansion of our portfolio of products and offers, led to consistent revenue growth.

In the Mobile business, the operating strategy for theSmart Empresas (Smart Companies) portfolio, focused on plans with unlimited voice and shared data packages, proved to be effective and adherent to market expectations. The portfolio already represents 60% of the mobile access base, and its value proposition increased due to its positioning as a secure connection for companies through digital solutions. International roaming offers have also become more robust and more cost-effective after the launch of Vivo Travel with monthly voice and data packages.

In the Corporate Fixed segment, the growth of FTTH Broadband highlights our positioning and commitment to offering high-speed connectivity. Fiber already represents 70% of adhesions, 75% of which at speeds starting at 300Mbps, boosting ARPU. This strategy was reinforced by the launch of speeds of up to 1Gbps throughout 2019 and played a major role in the success of Black Friday. In advanced data, we improved our value proposition through new dedicated internet plans, which already accounted for 58% of sales.

4. Business Performance

Telefônica Brasil S.A. and its wholly owned subsidiaries operate mainly as nationwide providers of landline and mobile telephone services through a Concession Agreement for Switched Fixed Telephone Services (STFC) and authorizations granted by ANATEL to provide other telecommunications services, such as data communication, broadband internet and pay TV, as well as value-added services not classified as telecommunications.

4.1.Customer Service

In 2019, digitalization and operational improvements led to a drop of over 20% in calls to the call center compared to 2018. Moreover, there was an improvement in the customer experience, with a reduction in average wait times and greater representative autonomy, improving the first call resolution indicator. This was partly due to the efforts to expand the digital channels and develop more self-service options.

The main digitalization projects include the new features implemented in the Meu Vivo app, increasing its adoption and reaching 15 million unique users at the end of 2019. The app is connected to Aura, Vivo's artificial intelligence, and plays an essential role in the migration of traditional calls to a digital experience. In addition, the launch of WhatsApp as a service channel has already served a significant number of customers in 2019.

Despite efforts to attract customers to our digital channels, some of them still prefer the traditional channel. To ensure that all customers have access to their preferred channel, we expanded our Cognitive Call Center, with more than 20 million contacts served by Bot in 2019, providing a friendly, fast and humanized experience and helping improve retention on electronic channels.

To assess the perceived quality of all contact points, we launched the DNA Thermometer program, a methodology to capture the customer's perception of our services, ensuring monitoring and agile solutions. The purpose of all these actions is to further improve the customer experience, aligning their journey with our corporate culture of being reliable, easy, pleasant and efficient.

7

4.2. Infrastructure and Network

Since 2013, the Company has been consolidating a robust network capable of fulfilling customers’ expectations. We have been able to make progress on migration from Time Division Multiplex (TDM) to Next Generation Networks (NGN), reaching 72.8% of migrated landline traffic, while modernizing central offices and adapting the data center infrastructure.

At the end of 2019, the Company’s mobile network provided LTE Advanced Pro, LTE, WCDMA, GSM/EDGE and CDMA digital technologies to 4,658 municipalities. This represents 83.6% of all Brazilian municipalities, or 96.5% of the population. The 2G/GSM-EDGE network ended 2019 with coverage in 645 municipalities in the state of São Paulo and in 3,758 municipalities in Brazil. In the same period, the 3G/WCDMA network was running in 645 municipalities in the state of São Paulo and 4,502 municipalities in Brazil.

The 4G (LTE) technology, launched in 2013, was an important step forward for the mobile network, since its transmission rates surpass those of the 3G network. We are continuing to expand the coverage of this technology, ending the year with 3,206 municipalities covered by the 4G network in Brazil.

The nationwide expansion of the LTE Advanced Pro (or 4.5G) network was an important milestone for the Company. This technology allows customers with compatible handsets to achieve even higher transmission rates than those of traditional 4G. In 2019, we finally managed to roll out this technology in 1,208 municipalities.

The implementation of the fiber network (GPON technology) achieved total coverage of 21.1 million homes passed in 2019, of which 9.1 million in the state of São Paulo and 12 million in other Brazilian states, with speeds of up to 300Mbps. Our fiber optics product portfolio includes a high-definition IPTV service (HDTV). In addition to IPTV, the Company’s portfolio of advanced products for corporate customers includes the GPON fiber optic service.

4.3.Sales

Telefônica Brasil’s commercial structure ended 2019 with approximately 1.6 thousand points of sale, including its own and those managed by authorized resellers, and approximately 14 thousand points of sale in retail outlets, in addition to remote channels such as telephone and online sales. The capillarity strategy focused on efficiency and operational excellence, combined with acceleration in the channel digitalization process, has enabled us to intelligently allocate resources and maintain our leadership in the Brazilian telecommunications market, dominating the high-end segment.

In the case of stores, we continued the process of transforming our points of sale into points of experience by making continuous significant advances towards improving infrastructure, systems, customer service, micromanagement and capillarity in order to ensure an even more efficient, profitable and dazzling operation. Lastly, the Company reached the mark of eight iconic stores, five stores in store and 142 Plus stores, a store concept created to serve small and medium towns.

The Distribution channel, which comprises newsstands, drugstores, bakeries and other small retailers, currently accounts for 87% of prepaid captures and 70% of recharges. The channel continued to boost commercial and operational efficiency by improving its micromanagement tools, which can manage capillarity and supply in real time, optimizing the performance of the sales force from end to end of the chain.

In the Retail channel, we seek to simplify the calculation of commissions, processes and KPIs, in addition to strengthening structural sales and the entry in new retail chains.

Door-to-door sales are undergoing change through the optimization of the partner network, the introduction of more structured national partners (without increasing unit costs) and capillarityfocused on the Fiber network. With an increasing focus on quality, this channel accounted for more than 70% of Fiber sales in the months of launch in new cities. In addition, the door-to-door channel's continuous improvements have increased sales in high-end condominiums, reaching a representation of 40% on this segment.

8

Telesales closed, on average, 560 thousand sales per month. The channel focused on expanding the base with quality, seeking new customers and migrating current customers to plans more suited to the consumption profile. There were 3.8 million migrations in the Control portfolio and 360 thousand Fiber sales, accounting for 38% of the Company's sales. The channel relies on artificial intelligence, connecting customers to the most appropriate operator. This match helps map better business arguments and generated more than 83 thousand additional sales.

In 2019, the Company launched the Digital Sales Acceleration project, which has already benefited e-commerce results, mainly B2C mobile sales, up 60% in the year, and fiber, up 58%. Finally, the partnership with Mercado Pago on Recarga Digital (Digital Recharge) brought higher revenue and decreased unit costs, resulting in lower sales commissions.

Meu Vivo, the Company’s main self-service channel, strengthened its digital service strategy and contributed to the positive performance of the digital channels: the number of unique users of the app rose 21% in 2019, and app recharges grew 86% over 2018.

4.4.Information Systems

In 2019, we worked focused on the three priorities for IT: Business Transformation, with programs that promote the digitalization and simplification of our system map; Delivery Acceleration, seeking to add more value to the business; and Operational Excellence, ensuring a robust and resilient operation.

Business Transformation - the FullStack B2C project continues to advance and already has 7.6 million postpaid and control mobile accesses. In addition, we started developing convergence with fiber products, which will allow us to have a complete view of our customers. As for FullStack B2B, we made the first deliveries of features in the pre-sale cycle, such as product migration and implementation in the face-to-face sales channel, generating better and more assertive sales. In the new OCS (Online Charging System), we have already started business simulations with postpaid customers. As for digital services, we have also started to restructure our sales channels through investments in the development of a new e-commerce platform.

Delivery Acceleration – the TI2X program celebrated its first anniversary with surprising results, such as doubling the project delivery capacity, increasing on-time delivery and reducing the time to market, without increasing investment levels. These results were achieved through process improvement actions and internalization of knowledge of technologies and critical IT functions, through the hiring of 971 people, reducing the outsourcing level from 73% to 59%.

Operational Excellence – we continue to pursue the server virtualization strategy, reaching 83.7% of the total, increasing management efficiency and reducing obsolescence. We seek to make our architecture increasingly simple, secure and robust, and address the root causes of availability offenders.

The sum of these efforts can be seen in our 99.89% system availability in 2019.

5. Corporate Governance

The fundamental principles of corporate governance at Telefônica Brasil S.A. are set forth in its Bylaws and in the internal rules and regulations that supplement the concepts contained in the law and standards governing the securities market. The purpose of these principles, which guide the activities of the Company’s management, can be summarized as follows:

9

· | Maximizing the Company’s value; |

· | Transparency in the Company’s accounts and disclosure of material information of interest to the market; |

· | Transparency in relations with shareholders, employees, investors, customers and public agencies; |

· | Equal treatment of shareholders; |

· | Engagement of the Board of Directors in overseeing and managing the Company and in accountability to shareholders; |

· | Engagement of the Board of Directors with Corporate Responsibility, ensuring the Company’s continuity. |

Inspired by these concepts and in an effort to promote good corporate governance, the Company has instituted measures that render its actions clear and objective, while avoiding conflicts of interest.

The Company’s Board of Directors currently consists of twelve members, one of whom is elected by preferred shareholders in a separate vote and without the participation of the parent company, while the others are elected by a general vote of common shareholders. In 2019, the Board of Directors met 19 times in the exercise of its functions.

The Fiscal Council of the Company consists of three full members and three alternates and, in 2019, it met nine times in the exercise of its duties.

The Executive Board currently consists of three members with the following positions: Chief Executive Officer, Chief Financial and Investor Relations Officer, and General-Secretary and Legal Officer.

5.1.Investor Relations

In order for its shares to achieve fair valuation, the Company adopts practices designed to provide transparency on its strategy, business evolution, policies and any events to shareholders, investors and analysts.

Material information is made available on the Company’s internet portal (www.telefonica.com.br/ir), with versions in Portuguese and English. The Company also has an Investor Relations team that answers questions by telephone or in one-to-one meetings, when so requested.

5.2.Independent Auditors

In compliance with CVM Instruction 381, of January 14, 2003, and Circular Letter CVM/SNC/SEP 01/2007, of February 14, 2007, the Company and its subsidiaries state that the Company’s policy regarding its independent auditors and their services not related to the independent audit is based on principles that preserve the independence of the auditors. These principles state that the auditors should never audit their own work, function as management, act as an advocate for their client or render any other services that are prohibited by current regulations, thus maintaining the independence of the audit work.

In 2019, no services other than the independent audit were contracted with the independent auditors, PriceWaterhouseCoopers Auditores Independentes.

6. Human Resources

In 2019, the Company consolidated its global strategic plan, #RECONECTA, launched in 2018.

10

Attentive to a fast-changing world and with the goal to support the Company’s growth plan, the Vice-Presidency of People elected four strategic challenges: Promote a high-performance culture; Attract and retain the best talents; Drive efficient management with a focus on processes, management and systems; and Improve employee satisfaction and make employees proud to work at Vivo. Faced with this challenge, the Company has transformed its way of working and delivering results.

New forms of work and other assertive and innovative management methods, such as OKRs (Objectives and Key Results) and Design Thinking, were used to deliver plans for strategic challenges.

To support our transformation, we carried out a culture study that allowed us to identify Vivo's strengths in the face of our long-term strategy through a survey, answered by more than 17 thousand employees, in addition to interviews with leaders and focus groups with employees. The Motivation Survey has also been restructured and is more focused on employee needs, corporate culture and market trends and is aligned with our strategy. The main employee satisfaction indicator of this survey is the eNPS (Employee Net Promoter Score), based on the same methodology used to measure customer satisfaction (NPS). The motivation survey was answered by 87% of employees and the e-NPS was 72.5 points.

Changing Environment

In 2019, the Vice-Presidency of People worked to provide an environment in which self-expression, flexibility and diversity of people and ideas are embodied in management principles to attract and retain the best talents. The Vivo Diversity program, which celebrated its first anniversary, values diversity of points of view, origins, identities and orientation, so that everyone feels comfortable to be the way they are in an environment of respect for differences.

The Company defined goals for increasing representativeness of all the strategic pillars of diversity (gender, race, LGBTI+ and people with disabilities), and the platform was structured with two objectives: promoting an inclusive culture and increasing the representativeness of different groups across all hierarchical levels of the Company. We work with affinity groups formed by volunteer employees engaged with the issues, who discuss and suggest affirmative actions to ensure equal growth conditions within the organization.

Collaborative spaces also gained prominence in 2019, being implemented in other regions, with new buildings that fit the concept. In addition, the mobility initiative was expanded to allow eligible employees to work remotely two days a week. This change increased productivity and improved the quality of life of employees.

In this collaborative environment, which values the participation and expression of all our staff, internal communication implemented innovative actions and channels, such as Workplace, generating an open, accessible and transparent dialogue. In addition, we have the DNA in Action program, in which more than 350 members of management, including VPs, officers and managers, visited stores, door-to-door, field, call center and court hearings and had the opportunity to learn more about and experience the service offered to our customers.

Employee Value Proposition

In December 2019, the Company had 32,793 employees (versus 32,638 employees in December 2018). To attract and retain the best talents, the Company implemented a new recruitment and selection model and created the employee value proposition – EVP.A survey conducted with several employees identified the value proposition they recognize in relation to working at Vivo and listed four attributes: Human Connections, Leading Company in Transformation, Challenges and Development, and Benefits.

The new recruitment model reflects the journeys of candidates and managers with new digital and innovative processes and solutions. We have invested in new recruitment and selectionplatforms that use artificial intelligence and provide a better user experience. Among the new digital platforms, we highlight a personalized videobot solution for sending hiring proposals and a tool for receiving admission documents digitally using mobile devices, thus reducing costs with external consultants.

11

6.1.Compensation and Benefits

In order to attract and retain the best talents and recognize their individual performance, the Company adopts compensation strategies compatible with the best market practices. Overall employee compensation is composed of fixed compensation, variable short- and long-term compensation and benefits.

In 2019, the Company adopted a new compensation strategy and repositioned its executives. In 2019, 3,761 professionals were promoted and 7,615 were included in the salary increase process, which adds up to 11,376 professionals who received an increase in compensation, in addition to the legal adjustments applied.

6.2.Education and Development Programs

In 2019, the Company invested around R$55.7 million in education, based on a face-to-face and online training strategy that tripled the participation of employees and partners compared to 2018, reaching over 1,900 thousand participations.

6.3.Safety and Prevention

In 2019, we carried out mandatory training and recycling for work at height (NR 35), totaling more than 21 thousand hours; work in proximity to electrical installation (NR 10), totaling more than 20 thousand; and call center work (NR 17), totaling 3 thousand hours.

The Company maintains areas dedicated to Occupational Health and Safety, focused on promoting a healthy work environment, supported by services provided by health professionals (doctors, nutritionists, psychologists, physical therapists) and vaccination campaigns, among others. Held in September, the Health Week reached 25,523 employees with the goal of raising awareness and encouraging healthy and safe behavior in the daily lives of employees.

7. Sustainability

Applying sustainability in our strategy allows us to identify opportunities offered by new technologies for creating value for society and effectively managing the impacts that are inherent in our activities, making our business increasingly responsible.

The conduct of our business establishes targets to be achieved by 2021, which implies acting in an upright and transparent way and making a commitment to sustainable development, in order to generate a positive social impact and create shared value, with a vision of sustainability that puts people at the very center of what we do and reduces the negative impacts on our operation.

For this reason, the Telefônica Group developed its Global Responsible Business Plan, which is based on seven pillars:

· Promise to the Customer and Digital Trust

· Supply Chain Sustainability Management

· Diversity and Talent Management

· Environment

· Sustainable Innovation

12

· Contribution to Progress

· Ethics

In line with these commitments, the most relevant and priority issues in our business are addressed within Telefônica Brasil through projects and goals that involve all of the Company’s areas, within the scope of our Responsible Business Plan.

Issues such as climate change, diversity and digital trust, among others, are becoming increasingly important to society and can change the way we relate to our customers and other stakeholders in our value chain.

In addition, we were the first Brazilian telecommunications company to launch a Privacy Center to discuss and provide clarifications regarding this matter. According to a survey carried out by Internet Lab, an independent center for direct interdisciplinary research in law and technology, in October 2019, we were the Brazilian internet operator most committed to the privacy of user data, both in fixed broadband and in mobile internet.

We are a signatory to and actively participate in other relevant initiatives that also contribute to sustainable development, such as theGlobal Compact, theGHG Protocol (Gold Seal) and theCarbon Disclosure Project (CDP), and we have also made public commitments to the organizations that work on the pillars of the Vivo Diversity Program: the Principles of Women's Empowerment,Movimento Mulher 360(Women 360 Movement),Fórum de Empresas e Direitos LGBT+ (Forum of Business and LGBT+ Rights),Rede Empresarial de Inclusão Social (Business Network for Social Inclusion) andCoalizão Empresarial para Equidade Racial e de Gênero (Business Coalition for Racial and Gender Equity). In this context, we were awarded the Gold Seal at the third edition of the WEPs Brazil Award, an important recognition of our efforts to promote equality in the work environment, value chain and communities.

In 2019, Telefônica Brasil was included in the main domestic and international sustainability rankings. For the eighth consecutive quarter, the Company was included in B3’s Corporate Sustainability Index - ISE. Once again, we figured in theSustainability Guide of EXAME magazineand were included, for the fifth consecutive year, in the Best Emerging Markets Performers Ranking of VIGEO EIRIS.

Once a year, the Company publishes its Annual Sustainability Report, which is prepared in accordance with the standards of the Global Reporting Initiative (GRI). The report is available at the Sustainability area of our website www.telefonica.com.bror on the Investor Relations website www.telefonica.com.br/ri.

7.1. Private Social Investment

The Telefônica Vivo Foundation, which is responsible for Vivo’s social projects, believes in educational innovation as a way of inspiring new paths for Brazil’s development based on education. The Foundation develops projects in the areas of education, social entrepreneurship and volunteer work. Present in Brazil since 1999, the Foundation is part of a network that consists of 17 other Telefônica Group foundations located in Europe and Latin America. In 2019, we benefitted roughly 1.4 million people and invested R$72 million.

To find out more about Telefônica Vivo Foundation, visitwww.fundacaotelefonica.org.br

8. Operating Performance

At the end of 2019, the Company totaled 74,582 thousand mobile accesses, confirming its leadership position with a 32.9% market share. The postpaid customer base accounted for 57.9% of the mobile base at the end of 2019, 2.7 p.p. more than in 2018.

13

In relation to landline service, the Company ended 2019 with 19,044 thousand revenue generating units, a decline of 13.5% from the previous year, mainly on account of the maturity of landline voice service and the more selective strategy for the pay-TV service.

Broadband - totaled 6,908 thousand customers at the end of 2019, a decline of 7.4% from 2018. Fiber optic accesses (FTTH) registered 2,477 thousand customers, moving up 30.8% over 2018 and representing 35.9% of all broadband accesses.

Lines in Service - totaled 10,817 thousand customers in 2019, a 16.8% decrease in relation to 2018, mainly due to the maturity of the landline voice service and the fixed-to-mobile substitution.

Pay-TV - totaled 1,320 thousand customers in 2019, a 15.8% reduction against 2018, reflecting the Company’s selectivity and focus on high-end customers and the strategic decision to stop selling DTH services. IPTV totaled 715 thousand users, 23.4% more than in 2018.

As a result, the Company ended 2019 with 93,627 thousand customers, a 1.6% drop in relation to the previous year, mainly due to disconnections of landline voice customers and prepaid mobile customers.

9. Financial Performance

9.1.Net Operating Revenue

In 2019, the Company posted consolidated net operating revenue of R$44,268.2 million, up 1.9% over 2018, when we recorded net revenue of R$43,462.7 million. This growth was driven by higher data and mobile digital service revenue, as well as higher fixed broadband revenue, partially offset by lower voice and pay-TV revenue.

9.2.Operating Costs and Expenses

Operating costs and expenses, excluding depreciation and amortization, totaled R$26,134.5 million in 2019, an increase of 1.9% over 2018 (R$25,637.9 million), below inflation for the period (4.3%). The increase was chiefly due to the non-recurring effect related to a judicial decision in favor of the Company regarding the tax contingency recorded in 2018, in addition to the higher cost of goods sold, reflecting the strategy of greater focus on the sale of handsets and equipment with a margin. On the other hand, the intense digitization and automation process the Company is going through resulted in lower printing and mailing costs, thanks to the adoption of e-billing; lower commission costs, due to growth in e-commerce of products, services and recharges; and lower customer service costs, as a result of the increased penetration of the Meu Vivo app.

9.3.EBITDA

EBITDA totaled R$18,133.7 million in 2019, a 1.7% increase from R$17,824.8 million in 2018. The EBITDA margin stood at 41.0% in 2019.This result was due to higher revenue from mobile, ultra-broadband, corporate data and IT services, as well as the efficiency and digitalization measures adopted by the Company, partially offset by a non-recurring effect in connection with a favorable judicial decision regarding tax contingency. Excluding this effect, the recurring EBITDA margin increased 4.7 p.p. from 35.8% in 2018.

14

In millions of reais – Consolidated |

|

| ||

|

| 2019 |

| 2018 |

Operating income before financial income and expenses and equity pick-up (*) |

| 7,213.9 |

| 9,456.2 |

Depreciation and amortization expenses |

|

|

|

|

In service costs |

| 8,624.2 |

| 6,487.9 |

In selling expenses |

| 1,501.1 |

| 1,352.6 |

In general and administrative expenses |

| 794.5 |

| 528.1 |

EBITDA |

| 18,133.7 |

| 17,824.8 |

|

|

|

|

|

EBITDA margin |

|

|

|

|

a) EBITDA |

| 18,133.7 |

| 17,824.8 |

b) Net operating revenue (*) |

| 44,268.2 |

| 43,462.7 |

a) / b) |

| 41.0% |

| 41.0% |

Recurring EBITDA margin |

| 40.5% |

| 35.8% |

(*) See income statements.

9.4.Indebtedness

In millions of reais – Consolidated |

| 2019 |

| 2018 |

|

|

|

|

|

Loans and financing |

| (1,045.1) |

| (2,106.8) |

Debentures |

| (3,104.4) |

| (3,173.9) |

Leases |

| (9,191.2) |

| (393.0) |

GVT contingent consideration |

| (484.0) |

| (465.7) |

Total indebtedness |

| (13,824.7) |

| (6,139.4) |

Derivative transactions |

| 16.0 |

| 56.1 |

Indebtedness after derivatives |

| (13,808.7) |

| (6,083.3) |

The Company ended 2019 with gross debt of R$13,808.7 million (R$6,083.3 million in 2018), equivalent to 19.6% of shareholders’ equity (8.5% in 2018). The funds raised are fully denominated in local currency,

9.5.Net Result

The consolidated result for the year, in accordance with the requirements of Brazilian Corporate Law, shows net income of R$5,001.0 million in 2019 (R$8,928.3 million in 2018), a decline of 44.0% from 2018. Telefônica Brasil’s net margin stood at 11.3% in 2019 (20.5% in 2018).

In millions of reais |

| 2019 |

| 2018 |

|

|

|

|

|

a) Net income for the year (*) |

| 5,001.0 |

| 8,928.3 |

b) Net operating revenue (*) |

| 44,268.2 |

| 43,462.7 |

a) / b) |

| 11.3% |

| 20.5% |

(*) See income statements.

9.6.Investments

In 2019, the Company invested R$8,844.3 million, 7.9% more than in 2018 (R$8,199.9 million).

15

In 2019, we continued to expand our landline services by providing fiber optic services (FTTH) in an additional 43 cities and building roughly 2.3 million new homes passed. As a result, Telefônica Brasil provides FTTH services in more than 164 cities and has approximately 11 million homes passed in the country.

In 2019, we invested heavily in the maintenance and expansion of mobile internet and voice services and consolidated the implementation of 4G, reaching the impressive mark of 3,206 municipalities. In addition, we have improved signal quality in a number of regions and invested significant resources in maintenance actions (both proactive and reactive).

Telefônica Brasil also invested in integrating the systems of its landline and mobile business, as well as improving its business support infrastructure (systems, points of sale and service). In 2019, we continued to invest in improving, expanding and integrating operating systems, especially the ongoing transformation of the billing environment and the Big Data projects, which will provide support for the rollout of new products and services, focusing primarily on the customer experience.

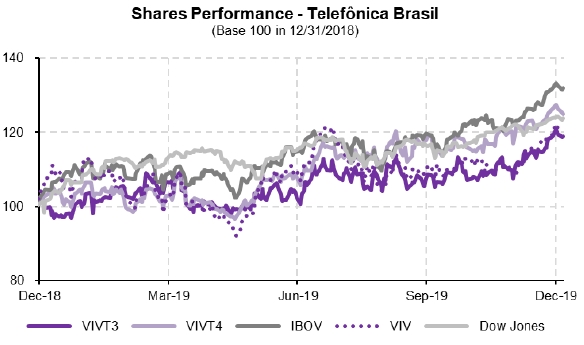

10. Capital Market

The Company’s common (VIVT3) and preferred (VIVT4) shares closed 2019 at R$49.04 and R$57.98, respectively, recording an appreciation of 18.8% and 25.4%, respectively, over the closing price at the end of 2018. In the same period, the daily trading volume of VIVT3 and VIVT4 averaged R$2,252 thousand and R$87,061 thousand respectively. Total shareholder return (TSR) reached 26.9% for common shares and 33.4% for preferred shares in the last twelve months.

The ADRs (VIV) traded on the NYSE closed 4Q19 at US$14.32, up 20.0% over the closing price at the end of 2018. The daily trading volume of ADRs averaged US$19,819 thousand in the same period.

The chart below shows the performance of the shares in 2019:

16

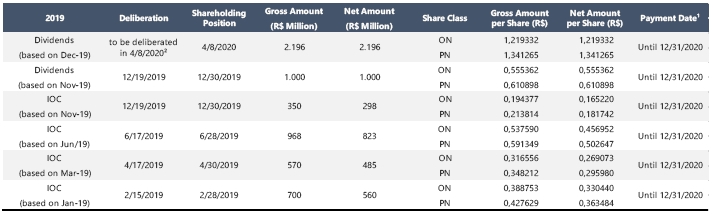

10.1 Shareholder Remuneration

Under its bylaws, the Company is required to distribute a minimum of 25% of its annual adjusted net income as dividends, while the holders of preferred shares are guaranteed an amount 10% higher than that attributed to each common share.

Interest on shareholders’ equity and dividends declared by Telefônica Brasil based on net income for 2019 totaled R$5.8 billion, which translates into a payout ratio of 116%, as detailed in the table below:

1 – The Company’s Executive Board resolved that the interest on equity declared and the dividends proposed, if approved, will be paid on the dates listed above.

2 – Dividends proposed by Management to be resolved by the Annual Shareholders’ Meeting, to be held on April 8th, 2020.

11. Outlook

The growing importance of digital services is changing consumption patterns in the telecommunications sector. Customers demand not only better connections and higher traffic speeds, but also bundles of relevant digital services that provide an increasingly personalized experience. In addition, brand reputation and data security and privacy concerns are becoming increasingly important in customer choice, supported by the new General Data Protection Regulation (LGPD), which will come into force in 2020.

The macroeconomic scenario should continue to recover, as the new government is calling for significant political and economic reforms, such as the approval of the Social Security Reform. A more pro-market approach also tends to favor the regulatory scenario, as embodied by the approval of PLC 79. Such measures contribute to the recovery of the telecommunications sector. On the revenue side, the offer of bundled services and the exponential consumption of data and digital connectivity services will continue to be essential for growth. In addition, the competitive environment should become more conducive to mergers and acquisitions and focused on offering unique traditional and digital products and services, combined with high quality and a better customer experience, which will require more investments in newer and more efficient technologies, such as FTTH and 4.5G.

In this context, Telefônica Brasil is well structured to maintain its leadership position in the Brazilian telecommunications market and continue to serve its more than 93 million customers. Relevance, Revenue, Return, Responsibility and Motivation make up the Company’s strategic pillars that will enable it to fulfill its purpose of digitalizing to bring people closer.

Christian Mauad Gebara

Chief Executive Officer

David Melcon Sanchez-Friera

Chief Financial and Investor Relations Officer

17

Breno Rodrigo Pacheco de Oliveira

General-Secretary and Legal Officer

Carlos Cesar Mazur

Accountant – CRC – 1PR-028067

18

OPINION OF THE AUDIT AND CONTROL COMMITTEE

The members of the Audit and Control Committee of Telefônica Brasil S.A. (“Company” or “Telefônica Brasil”), in the exercise of their duties and legal responsibilities, have examined and analyzed the Company’s Financial Statements, together with the Independent Auditors’ Report and the Annual Management Report for the year ended December 31, 2019 (“2019 Annual Financial Statements”), as well as the Proposed Capital Budget for the year 2020, including the 2019 budget implementation report and the Proposed Allocation of Net Income for 2019, and, taking into account the information provided by Telefônica Brasil’s Executive Board and the independent auditors, PriceWaterhouseCoopers Auditores Independentes, vote unanimously in favor of the aforesaid documents and declare that they fairly represent, in all material aspects, the Company’s equity and financial position. Accordingly, they recommend their approval by Telefônica Brasil’s Board of Directors and their submission to the Annual Shareholders’ Meeting, under the terms of Brazilian Corporate Law.

São Paulo, February 14, 2020.

José María Del Rey Osorio

Chairman of the Audit and Control Committee

Julio Esteban Linares Lopez

Member of the Audit and Control Committee

Narcís Serra Serra

Member of the Audit and Control Committee

19

OPINION OF THE BOARD OF DIRECTORS

The members of the Board of Directors of Telefônica Brasil S.A. (“Company” or “Telefônica Brasil”), in the exercise of their duties and legal responsibilities, as set forth in Brazilian Corporate Law and in the company’s Bylaws, have examined and analyzed the Company’s Financial Statements, together with the Independent Auditors’ Report and the Annual Management’s Report for the year ended December 31, 2019 (“2019 Annual Financial Statements”), as well as the Proposed Capital Budget for the year 2020, including the 2019 budget implementation report and the Proposed Allocation of Net Income for 2019, and, taking into account the information provided by Telefônica Brasil’s Executive Board and the independent auditors, PriceWaterhouseCoopers Auditores Independentes, and the favorable opinion of the Fiscal Council members and the members of the Audit and Control Committee, vote unanimously in favor of the aforesaid documents and declare that they fairly represent, in all material aspects, the Company’s equity and financial position. Accordingly, they determine that the aforesaid documents be submitted for approval by the Annual Shareholders’ Meeting, under the terms of Brazilian Corporate Law.

São Paulo, February 14, 2020.

Eduardo Navarro de Carvalho Chairman of the Board of Directors

| Luiz Fernando Furlan Member of the Board of Directors

|

Julio Esteban Linares Lopez Member of the Board of Directors

| Francisco Javier de Paz Mancho Member of the Board of Directors

|

Ana Theresa Masetti Borsari Member of the Board of Directors

| Christian Mauad Gebara Member of the Board of Directors

|

Antonio Carlos Valente da Silva Member of the Board of Directors

| Sonia Julia Sulzbeck Villalobos Member of the Board of Directors

|

José María Del Rey Osorio Member of the Board of Directors

| Claudia Maria Costin Member of the Board of Directors

|

Luis Miguel Gilpérez Lopez Member of the Board of Directors | Narcís Serra Member of the Board of Directors |

20

OPINION OF THE FISCAL COUNCIL

The members of the Fiscal Council of Telefônica Brasil S.A. (“Company” or “Telefônica Brasil”), in the exercise of their duties and legal responsibilities, as provided for in article 163 of Brazilian Corporate Law, have examined and analyzed the Company’s Financial Statements, together with the Independent Auditors’ Report and the Annual Management Report for the year ended December 31, 2019 (“2019 Annual Financial Statements”), as well as the Proposed Capital Budget for the year 2020, including the 2019 budget implementation report and the Proposed Allocation of Net Income for 2019, and, taking into account the information provided by Telefônica Brasil’s Executive Board and the independent auditors, PriceWaterhouseCoopers Auditores Independentes, vote unanimously in favor of the aforesaid documents and declare that they fairly represent, in all material aspects, the Company’s equity and financial position. Accordingly, they determine that the aforesaid documents be submitted to the Annual Shareholders’ Meeting, under the terms of Brazilian Corporate Law.

São Paulo, February 14, 2020.

Flavio Stamm Full member of the Fiscal Council | Cremênio Medola Netto Full member of the Fiscal Council | Charles Edwards Allen Full member of the Fiscal Council |

21

Telefônica Brasil S.A.

Consolidated Financial Statements

On December 31, 2019 and 2018 and for the years ended December 31, 2019, 2018 and 2017

Contents

Report of independent registered

public accounting firm

To the Board of Directors and Shareholders

Telefônica Brasil S.A.

Opinions on the financial statements and

internal control over financial reporting

We have audited the accompanying consolidated balance sheets of Telefônica Brasil S.A. and its subsidiaries (the “Company”) as of December 31, 2019 and December 31, 2018, and the related consolidated statements of income, other comprehensive income, changes in equity and cash flows for each of the three years in the period ended December 31, 2019, including the related notes (collectively referred to as the “consolidated financial statements”). We also have audited the Company's internal control over financial reporting as of December 31, 2019, based on criteria established in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 2019 and December 31, 2018, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2019 in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board. Also in our opinion, the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2019, based on criteria established in Internal Control - Integrated Framework (2013) issued by the COSO.

Change in accounting principle

As discussed in Note 2f to the consolidated financial statements, the Company changed the manner in which it accounts for leases in 2019. This matter is also described in the “Critical Audit Matters” section of our report.

Basis for opinions

The Company's management is responsible for these consolidated financial statements, for maintaining effective internal control over financial reporting, and for its assessment of the effectiveness of internal control over financial reporting, included in item 15 – Controls and Procedures – Management´s Annual Report on Internal Control over Financial Reporting. Our responsibility is to express opinions on the Company’s consolidated financial statements and on the Company's internal control over financial reporting based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

F-1

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud, and whether effective internal control over financial reporting was maintained in all material respects.

Our audits of the consolidated financial statements included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. Our audits also included performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

Definition and limitations of internal control over financial reporting

A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Critical audit matters

The critical audit matters communicated below are matters arising from the current period audit of the consolidated financial statements that were communicated or required to be communicated to the audit committee and that (i) relate to accounts or disclosures that are material to the consolidated financial statements and (ii) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate.

F-2

First-time adoption of IFRS 16 Leases

As described in Note 2F to the consolidated financial statements, the Company adopted the IFRS 16-Leases as effective dated January 1, 2019. The Company transitioned to IFRS 16 using the modified retrospective approach. The comparative information for prior-year periods was not restated. The adoption of this new standard gave rise to right of use assets and lease liabilities of R$8,618,072 thousand as of January 1, 2019. As described by management in Note 2, the adoption was complex due to factors such as the high number of contracts affected that required an evaluation to consider if the contracts contain a lease under this standard, the diversity of data source systems, the implementation of new systems to map all the leases information and the management judgement involved in some assumptions like lease terms and discount rate.

The principal considerations for our determination that performing procedures relating to the first-time adoption of IFRS 16-Leases is a critical audit matter are the degree of complexity of the process due to the volume of contracts, among others, and estimation and judgment applied to the initial application of the new standard. This in turn led to a high degree of auditor subjective and effort in performing the procedures designed to evaluate the first-time adoption of IFRS 16-Leases.

Our approach to addressing the matter involved performing procedures and evaluating audit evidence in connection with forming our overall opinion on the consolidated financial statements. These procedures included testing the effectiveness of controls related to the first-time adoption of IFRS 16-Leases standard. The procedures also included, among others, (1) assessing the accounting policies employed by management in the determination, calculation and accounting of leases under this standard, as well as the practical expedients employed, (2) testing the completeness and accuracy of the lease contracts identified and recorded in the systems, (3) evaluating the significant assumptions utilized by management such as the lease terms and discount rates and (4) evaluating the appropriateness of the Company’s disclosures. Professionals with specialized skill and knowledge were used to assist in the evaluation of Company´s adoption of this standard and the reasonableness of the discount rate. This matter is also described in the Change in Accounting Principle section of our report.

Tax and regulatory litigations

As described in Notes 7(g) and 19 to the consolidated financial statements, the Company has recorded

provision for tax and regulatory litigations of R$2,808,197 thousand and has disclosed contingent liabilities related to these tax litigations of R$ 41,559,190 as of December 31, 2019. The Company recognizes provision in the consolidated financial statements for the resolution of pending litigation when the Company has a present obligation as a result of a past event and management determines that a loss is probable and the amount of the loss can be reasonably estimated. No provision for tax litigation is recognized in the consolidated financial statements for unfavorable outcomes when, after assessing the information available, (i) management concludes that it is not probable that a loss has been incurred in any of the pending litigation; or (ii) management is unable to estimate the loss of the pending matters. In case of income tax pending litigations, management determines whether is probable or not that taxation authority will accept the uncertain tax treatment. If the Company concludes it is not probable that taxation authority will accept the uncertain tax treatment, a provision for income tax is recognized. The Company also discloses the contingency in circumstances where management concludes (i) no loss is probable or reasonably estimable, but it is reasonably possible that a loss may be incurred or, (ii) in case of income tax pending litigations, is probable that the taxation authority will accept the uncertain tax treatment.

F-3

The principal considerations for our determination that performing procedures relating to litigation contingencies is a critical audit matter are there was significant judgment by management when assessing the likelihood of a loss being incurred and when determining whether a reasonable estimate of the loss and possible outcomes for each claim can be made, which in turn led to a high degree of auditor judgment, effort, and subjectivity in evaluating management´s assessment of the loss contingencies associated with tax and regulatory litigations.

Addressing the matter involved performing procedures and evaluating audit evidence in connection with forming our overall opinion on the consolidated financial statements. These procedures included testing the effectiveness of controls relating to management´s evaluation of pending litigation, including controls over determining whether a loss is probable and whether the amount of loss can be reasonably estimated or whether the taxation authority will probably not accept the income tax pending litigations , as well as financial statement disclosures. These procedures also included among others, (1) obtaining and evaluating the letters of audit inquiry with internal and external legal counsel, (2) evaluating the reasonableness of management´s assessment regarding unfavorable outcomes, and (3) evaluating the sufficiency of the Company´s disclosures. Professionals with specialized skill and knowledge were used to assist in the evaluation of Company´s assessment regarding unfavorable outcomes.

Revenue recognition - unbilled

As described in Notes 4 and 24 to the consolidated financial statements, of the total gross revenue recognized by the Company for the year ended December 31, 2019, R$ 2,866,196 thousand relates to services rendered and not yet billed. When the revenue billing cycle does not align with the account closing date, management estimates the amount to be recognized for services rendered and not yet billed at the year-end. These estimates are based on different cycles of information, on data obtained from different sources and processed by a large number of applications and systems.

The principal considerations for our determination that performing procedures relating to unbilled revenue, is a critical audit matter are the judgments made by management for estimating the amount of unbilled revenue. This in turn led to a high degree of auditor judgment and effort in performing audit procedures to evaluate unbilled revenue recognition.

Our approach to addressing the matter involved performing procedures and evaluating audit evidence in connection with forming our overall opinion on the consolidated financial statements. These procedures included testing the effectiveness of controls relating to unbilled revenue recognition. The procedures also included, among others, (1) testing billings completed following the year-end and consistency with the estimates made and (2) assessing the reasonableness of the criteria employed by management to estimate revenue rendered and not yet billed including the accuracy of the underlying data.

São Paulo, February20, 2020

/s/ PricewaterhouseCoopers

Auditores Independentes

We have served as the Company´s auditor since 2017.

F-4

Consolidated Balance Sheets

On December 31, 2019 and 2018

(In thousands of reais)

ASSETS |

| Note |

| 12.31.19 |

| 12.31.18 |

Current assets |

|

|

| 18,644,678 |

| 18,362,992 |

Cash and cash equivalents |

| 3 |

| 3,393,377 |

| 3,381,328 |

Trade accounts receivable |

| 4 |

| 8,719,497 |

| 8,304,382 |

Inventories |

| 5 |

| 578,003 |

| 462,053 |

Income and social contribution taxes recoverable |

| 7 |

| 411,595 |

| 274,589 |

Taxes, charges and contributions recoverable |

| 8 |

| 4,176,362 |

| 4,674,218 |

Judicial deposits and garnishments |

| 9 |

| 277,468 |

| 313,007 |

Prepaid expenses |

| 6 |

| 686,503 |

| 581,743 |

Derivative financial instruments |

| 31 |

| 19,282 |

| 69,065 |

Other assets |

| 10 |

| 382,591 |

| 302,607 |

|

|

|

|

|

|

|

Non-current assets |

|

|

| 89,645,044 |

| 84,198,326 |

Short-term investments pledged as collateral |

|

|

| 63,766 |

| 76,934 |

Trade accounts receivable |

| 4 |

| 440,453 |

| 426,252 |

Taxes, charges and contributions recoverable |

| 8 |

| 841,198 |

| 3,222,262 |

Deferred taxes |

| 7 |

| 171,042 |

| 230,097 |

Judicial deposits and garnishments |

| 9 |

| 3,393,417 |

| 3,597,007 |

Prepaid expenses |

| 6 |

| 220,082 |

| 134,232 |

Derivative financial instruments |

| 31 |

| 52,881 |

| 26,468 |

Other assets |

| 10 |

| 235,738 |

| 47,105 |

Investments |

| 11 |

| 104,251 |

| 101,657 |

Property, plant and equipment |

| 12 |