UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2015

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from _______ to _______

Commission file number 1-3932

WHIRLPOOL CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 38-1490038 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) | |

| 2000 North M-63, Benton Harbor, Michigan | 49022-2692 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (269) 923-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common stock, par value $1 per share | Chicago Stock Exchange and New York Stock Exchange | |

| 0.625% Senior Notes due 2020 | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: NONE

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yesý No¨ | |||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. | Yes¨ Noý | |||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during | ||||

| the preceding 12 months (or for such shorter period that the registrant was required to file such report), and (2) has been subject to such | ||||

| filing requirements for the past 90 days. | Yesý No¨ | |||

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data | ||||

| File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months | ||||

| (or for such shorter period that the registrant was required to submit and post such files). | Yesý No¨ | |||

| Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained | ||||

| herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by | ||||

| reference in Part III of this Form 10-K or any amendment to this Form 10-K. | ý | |||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting | ||||

| company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. | ||||

| (Check one) | ||||

Large accelerated filer ý | Accelerated filer ¨ | |||

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ | |||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes¨ Noý | |||

On February 12, 2016, the registrant had 77,233,402 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated herein by reference into the Part of the Form 10-K indicated:

| Document | Part of Form 10-K into which incorporated | |

| The registrant’s proxy statement for the 2016 annual meeting of stockholders (the “Proxy Statement”) | Part III | |

WHIRLPOOL CORPORATION

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2015

TABLE OF CONTENTS

| PAGE | ||

| Item 1. | ||

| Item 1A. | ||

| Item 1B. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| Item 5. | ||

| Item 6. | ||

| Item 7. | ||

| Item 7A. | ||

| Item 8. | ||

| Item 9. | ||

| Item 9A. | ||

| Item 9B. | ||

| Item 10. | ||

| Item 11. | ||

| Item 12. | ||

| Item 13. | ||

| Item 14. | ||

| Item 15. | ||

| PART I | ||||

| ITEM 1. | BUSINESS |

Whirlpool Corporation, the world’s leading global manufacturer and marketer of major home appliances, was incorporated in 1955 under the laws of Delaware as the successor to a business that traces its origin to 1898. Whirlpool manufactures products in 14 countries and markets products in nearly every country around the world under brand names such as Whirlpool, KitchenAid, Maytag, Consul, Brastemp, Amana, Bauknecht, Jenn-Air and Indesit. Whirlpool’s reportable segments consist of North America, EMEA (Europe, Middle East and Africa), Latin America and Asia. As of December 31, 2015, Whirlpool had approximately 97,000 employees.

As used herein, and except where the context otherwise requires, “Whirlpool,” “the Company,” “we,” “us,” and “our” refer to Whirlpool Corporation and its consolidated subsidiaries.

Products and Regions

Whirlpool manufactures and markets a full line of major home appliances and related products. Our principal products are laundry appliances, refrigerators and freezers, cooking appliances, dishwashers, mixers and other small domestic appliances. We also produce hermetic compressors for refrigeration systems.

The following table provides the percentage of net sales for each class of products which accounted for 10% or more of our consolidated net sales over the last three years:

| 2015 | 2014 | 2013 | |||||||

| Laundry Appliances | 29 | % | 27 | % | 29 | % | |||

| Refrigerators and Freezers | 28 | % | 28 | % | 29 | % | |||

| Cooking Appliances | 18 | % | 18 | % | 18 | % | |||

| Other | 25 | % | 27 | % | 24 | % | |||

| Net Sales | 100 | % | 100 | % | 100 | % | |||

In North America, Whirlpool markets and distributes major home appliances and small domestic appliances under a variety of brand names. In the United States, we market and distribute products primarily under the Whirlpool, Maytag, KitchenAid, Jenn-Air, Amana, Roper, Admiral, Affresh and Gladiator brand names primarily to retailers, distributors and builders. In Canada, we market and distribute major home appliances primarily under the Inglis, Admiral, Whirlpool, Maytag, Jenn-Air, Amana, Roper, Estate and KitchenAid brand names. In Mexico, we market and distribute major home appliances primarily under the Whirlpool, Maytag, Acros, KitchenAid and Supermatic brand names. We sell some products to other manufacturers, distributors, and retailers for resale in North America under those manufacturers’ and retailers’ respective brand names.

In EMEA, we market and distribute our major home appliances primarily under the KitchenAid, Whirlpool, Indesit and Hotpoint brand names (Whirlpool ownership of the Hotpoint brand in the EMEA and Asia Pacific regions is not affiliated with the Hotpoint brand sold in the Americas), and major and small domestic appliances under the KitchenAid and Hotpoint brand names. In addition to our operations in Western and Eastern Europe, Turkey and Russia, we have sales subsidiaries in Morocco and Dubai. We market and distribute a full line of products under the Whirlpool and KIC brand names in South Africa. Our European operations also market and distribute products under the Whirlpool, Ariston, Bauknecht, Maytag, Amana and Ignis brand names to distributors and dealers in Africa and the Middle East.

In Latin America, we market and distribute our major home appliances and small domestic appliances primarily under the Consul, Brastemp, Whirlpool and KitchenAid brand names. We manage sales and distribution through our local entities in Brazil, Argentina, Chile, Peru, Ecuador, Colombia and Guatemala. We also serve the countries of Bolivia, Paraguay, Uruguay, Venezuela, the Caribbean and Central America countries, where we manage appliances sales and distribution through our accredited distributors. Our Latin America operations also produce hermetic compressors for refrigeration systems.

3

In Asia, we have organized the marketing and distribution of our major home appliances and small domestic appliances into five operating groups: (1) mainland China; (2) Hong Kong and Taiwan; (3) India, which includes Bangladesh, Sri Lanka, Nepal and Pakistan; (4) Oceania, which includes Australia, New Zealand and Pacific Islands; and (5) Southeast Asia, which includes Thailand, Singapore, Malaysia, Indonesia, Vietnam, the Philippines, Korea, Myanmar and Japan. We market and distribute our products in Asia primarily under the Whirlpool, Maytag, KitchenAid, Amana, Bauknecht, Jenn-Air, Diqua, and Royalstar brand names through a combination of direct sales to appliance retailers and chain stores and through full-service distributors to a large network of retail stores.

Competition

Competition in the major home appliance industry is intense, including competitors such as Arcelik, Bosch Siemens, Electrolux, General Electric, Haier, Kenmore, LG, Mabe, Midea, Panasonic and Samsung, many of which are increasingly expanding beyond their existing manufacturing footprint. Moreover, our customer base includes large, sophisticated trade customers who have many choices and demand competitive products, services and prices. Competition in our business is based upon a wide variety of factors, including selling price, product features and design, performance, innovation, energy efficiency, quality, cost, distribution and financial incentives. These financial incentives include cooperative advertising, co-marketing funds, salesperson incentives, volume rebates and terms. We believe that we can best compete in the current environment by focusing on introducing new and innovative products, building strong brands, enhancing trade customer and consumer value with our product offerings, continuing to expand our regional footprint, expanding trade distribution channels, increasing productivity, improving quality, lowering costs, and taking other efficiency-enhancing measures.

Raw Materials and Purchased Components

We are generally not dependent upon any one source for raw materials or purchased components essential to our business. In areas where a single supplier is used, alternative sources are generally available and can be developed within the normal manufacturing environment. Some supply disruptions and unanticipated costs may be incurred in transitioning to a new supplier if a prior single supplier relationship were abruptly interrupted or terminated. Supply constraints due to environmental impacts such as hurricanes and floods have required the qualification and use of alternate materials, some of which were at premium costs. We believe such raw materials and components will be available in adequate quantities to meet forecasted production schedules.

Trademarks, Licenses and Patents

We consider the trademarks, licenses and patents we own, in the aggregate, to be a valuable asset. Whirlpool is the owner of a number of trademarks in the United States and foreign countries. The most important trademarks to North America are Whirlpool, Maytag, Jenn-Air, KitchenAid, Amana and Acros. The most important trademarks to Latin America are Consul, Brastemp, Whirlpool and KitchenAid. The most important trademarks to EMEA are Whirlpool, KitchenAid, Bauknecht, Indesit, Hotpoint (Whirlpool ownership of the Hotpoint brand in the EMEA and Asia Pacific regions is not affiliated with the Hotpoint brand sold in the Americas), Hotpoint-Ariston and Ignis. The most important trademarks to Asia are Whirlpool, Royalstar and Diqua. We receive royalties from licensing our trademarks to third parties to manufacture, sell and service certain products bearing the Whirlpool, Maytag, KitchenAid, and Amana brand names. We continually apply for and obtain United States and foreign patents. The primary purpose in obtaining patents is to protect our designs and technologies.

Research and Development

Expenditures for research and development relating to new and innovative products and the improvement of existing products were approximately $579 million, $563 million and $582 million in 2015, 2014 and 2013, respectively.

Protection of the Environment

Our manufacturing facilities are subject to numerous laws and regulations designed to protect or enhance the environment, many of which require federal, state, or other governmental licenses and permits with regard to wastewater discharges, air emissions, and hazardous waste management. Our policy is to comply with all such laws and regulations. Where laws and regulations are less restrictive, we have established and are following our own standards, consistent with our commitment to environmental responsibility.

We believe that we are in compliance, in all material respects, with presently applicable governmental provisions relating to environmental protection in the countries in which we have manufacturing operations. Compliance with these environmental laws and regulations has not had a material effect on capital expenditures, earnings, or our competitive position during 2015 and is not expected to be material in 2016.

4

The entire major home appliance industry, including Whirlpool, must contend with the adoption of stricter governmental energy and environmental standards. These standards were phased-in over the past several years and include the general phase-out of ozone-depleting chemicals used in refrigeration, energy standards rulemakings for selected major appliances, regulatory restrictions on the materials content specified for use in our products by some jurisdictions and mandated recycling of our products at the end of their useful lives. Compliance with these various standards, as they become effective, will require some product redesign. However, we believe, based on our understanding of the current state of proposed regulations, that we will be able to develop, manufacture, and market products that comply with these regulations.

Whirlpool participates in environmental assessments and cleanup at a number of locations globally. These include operating and non-operating facilities, previously owned properties and waste sites, including "Superfund" (Comprehensive Environmental Response, Compensation and Liability Act (CERCLA)) sites. However, based upon our evaluation of the facts and circumstances relating to these sites along with the evaluation of our technical consultants, we do not presently anticipate any material adverse effect upon our earnings, financial condition, or competitive position arising out of the resolution of these matters or the resolution of any other known governmental proceeding regarding environmental protection matters.

Other Information

For information about the challenges and risks associated with our foreign operations, see “Risks Relating to Our Business” under Item 1A.

For certain other financial information concerning our business segments and foreign and domestic operations, see Note 14 to the Consolidated Financial Statements.

For information on our global restructuring plans, and the impact of these plans on our operating segments, see Note 11 to the Consolidated Financial Statements.

Whirlpool China Acquisition

On October 24, 2014, Whirlpool's wholly-owned subsidiary, Whirlpool (China) Investment Co., Ltd., completed its acquisition of a 51% equity stake in Hefei Rongshida Sanyo Electric Co., Ltd. ("Hefei Sanyo"), a joint stock company whose shares are listed and traded on the Shanghai Stock Exchange, which we have since renamed to Whirlpool (China) Co., Ltd. ("Whirlpool China").

The aggregate purchase price was RMB 3.4 billion (approximately $551 million at the dates of purchase of each step of the transaction). The Company funded the total consideration for the shares with cash on hand. The cash paid for the private placement step is considered restricted cash, which is used to fund capital and technical resources to enhance Whirlpool China’s research and development and working capital.

With this acquisition, Whirlpool also gains manufacturing scale and a competitive cost structure. Further discussion of this transaction can be found in Note 2 of the Notes to the Consolidated Financial Statements.

Indesit Company S.p.A. Acquisition

On December 3, 2014, Whirlpool completed the final step in its acquisition of Indesit Company S.p.A. ("Indesit") and on the same day Indesit delisted from the Electronic Stock Market organized and managed by Borsa Italiana S.p.A. Total consideration paid for Indesit was €1.1 billion (approximately $1.4 billion at the dates of purchase of each step in the transaction) in aggregate net of cash acquired.

The Company funded the aggregate purchase price for Indesit through borrowings under its credit facility and commercial paper programs, and repaid a portion of such borrowings through the issuance of an aggregate principal amount of $650 million in senior notes on November 4, 2014 and an aggregate principal amount of €500 million (approximately $525 million as of the date of issuance) in senior notes on March 12, 2015. Additional information about our 2015 financing arrangements can be found in Note 6.

This transaction builds Whirlpool’s market position within Europe, and we believe will enable sustainable growth given the complementary market positions, product offerings and distribution channels of Whirlpool and Indesit throughout Europe. Further discussion of this transaction can be found in Note 2 of the Notes to the Consolidated Financial Statements.

5

Executive Officers of the Registrant

The following table sets forth the names and ages of our executive officers on February 16, 2016, the positions and offices they held on that date, and the year they first became executive officers:

| Name | Office | First Became an Executive Officer | Age | |||

| Jeff M. Fettig | Director, Chairman of the Board and Chief Executive Officer | 1994 | 58 | |||

| Marc R. Bitzer | Director, President and Chief Operating Officer | 2006 | 51 | |||

| Esther Berrozpe Galindo | Executive Vice President and President, Whirlpool EMEA | 2013 | 46 | |||

| João C. Brega | Executive Vice President and President, Whirlpool Latin America | 2012 | 52 | |||

| Joseph T. Liotine | Executive Vice President and President, Whirlpool North America | 2014 | 43 | |||

| David T. Szczupak | Executive Vice President, Global Product Organization | 2008 | 60 | |||

| Larry M. Venturelli | Executive Vice President and Chief Financial Officer | 2012 | 55 | |||

The executive officers named above were elected by our Board of Directors to serve in the office indicated until the first meeting of the Board of Directors following the annual meeting of stockholders in 2016 and until a successor is chosen and qualified or until the executive officer's earlier resignation or removal. Each of our executive officers has held the position set forth in the table above or has served Whirlpool in various executive or administrative capacities for at least the past five years.

Available Information

Financial results and investor information (including Whirlpool’s Form 10-K, 10-Q, and 8-K reports) are accessible at Whirlpool’s website: investors.whirlpoolcorp.com. Copies of our Form 10-K, 10-Q, and 8-K reports and amendments, if any, are available free of charge through our website on the same day they are filed with, or furnished to, the Securities and Exchange Commission.

6

| ITEM 1A. | RISK FACTORS |

This report contains statements referring to Whirlpool that are not historical facts and are considered “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements, which are intended to take advantage of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, are based on current projections about operations, industry conditions, financial condition and liquidity. Words that identify forward-looking statements include words such as “may,” “could,” “will,” “should,” “possible,” “plan,” “predict,” “forecast,” “potential,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “believe,” “may impact,” “on track,” and words and terms of similar substance used in connection with any discussion of future operating or financial performance, a merger, or our businesses. In addition, any statements that refer to expectations, projections, or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Those statements are not guarantees and are subject to risks, uncertainties, and assumptions that are difficult to predict. Therefore, actual results could differ materially and adversely from these forward-looking statements. These risks and uncertainties include, but are not limited to, the following:

Risks Relating to Our Business

We face intense competition in the major home appliance industry and failure to successfully compete may negatively affect our business and financial performance. Each of our operating segments operates in a highly competitive business environment and faces intense competition from a growing number of competitors, many of which have strong consumer brand equity. Several of these competitors, such as Bosch Siemens, Electrolux, General Electric, Haier, LG, Panasonic and Samsung are large, well-established companies, many ranking among the Global Fortune 150, and have demonstrated a commitment to success in the global market. Moreover, our customer base includes large, sophisticated trade customers who have many choices and demand competitive products, services and prices. Competition in the global appliance market is based on a number of factors including selling price, product features and design, performance, innovation, reputation, energy efficiency, quality, cost, distribution, and financial incentives, such as cooperative advertising, co-marketing funds, sales person incentives, volume rebates and terms. Many of our competitors are increasingly expanding beyond their existing manufacturing footprints. Our competitors, especially global competitors with low-cost sources of supply and/or highly protected home markets outside the United States, have aggressively priced their products and/or introduced new products to increase market share and expand into new geographies. If we are unable to successfully compete in this highly competitive environment, our business and financial performance could be negatively affected.

We face risks associated with our acquisitions and other investments and risks associated with our increased presence in emerging markets. From time to time, we make strategic acquisitions and participate in joint ventures. For example, we acquired Indesit and a majority interest in Hefei Sanyo in the fourth quarter of 2014. These transactions, and other transactions that we have entered into or which we may enter into in the future, can involve significant challenges and risks, including that the transaction does not advance our business strategy or fails to produce a satisfactory return on our investment. We may encounter difficulties in integrating acquisitions with our operations, applying our internal control processes to these acquisitions, and in managing strategic investments. Integrating acquisitions is often costly and may require significant attention from management. Furthermore, we may not realize the degree, or timing, of benefits we anticipate when we first enter into a transaction. While our evaluation of any potential acquisition includes business, legal and financial due diligence with the goal of identifying and evaluating the material risks involved, our due diligence reviews may not identify all of the issues necessary to accurately estimate the cost and potential loss contingencies of a particular transaction, including potential exposure to regulatory sanctions resulting from an acquisition target’s previous activities or costs associated with any quality issues with an acquisition target's legacy products.

Our growth plans include efforts to increase revenue from emerging markets, including through acquisitions. Local business practices in these countries may not comply with U.S. laws, local laws or other laws applicable to us. If our compliance policies, including the requirement to comply with all laws, are not followed, such non-compliant practices may result in increased liability risks. For example, we may incur unanticipated costs, expenses or other liabilities as a result of an acquisition target’s violation of applicable laws, such as the U.S. Foreign Corrupt Practices Act (FCPA) or similar worldwide anti-bribery laws in non-U.S. jurisdictions. We may incur unanticipated costs or expenses, including post-closing asset impairment charges, expenses associated with eliminating duplicate facilities, litigation, and other liabilities. In addition, our recent and future acquisitions may increase our exposure to other risks associated with operating internationally, including foreign currency exchange rate fluctuations; political, legal and economic instability; inflation; changes in tax rates and tax laws; and work stoppages and labor relations. See Note 2 to the Consolidated Financial Statements for additional information regarding the Hefei Sanyo and Indesit acquisitions.

7

The loss of, or substantial decline in, sales to any of our key trade customers, which include Lowe's, Sears, Home Depot, hhgregg, Best Buy, GPA - Grupo Pão De Açúcar, IKEA, Alno, Suning, major buying groups, and builders could adversely affect our financial performance. We sell to a sophisticated customer base of large trade customers that have significant leverage as buyers over their suppliers. Most of our products are not sold through long-term contracts, which facilitates the trade customers' ability to change volume among suppliers. As the trade customers continue to become larger, they may seek to use their position to improve their profitability by various means, including improved efficiency, lower pricing, and increased promotional programs. If we are unable to meet their demand requirements, our volume growth and financial results could be negatively affected. The loss of, or substantial decline in volume of, sales to Lowe's, Sears, Home Depot, hhgregg, Best Buy, GPA - Grupo Pão De Açúcar, IKEA, Alno, Suning, major buying groups, builders, or any other trade customers to which we sell a significant amount of products, could adversely affect our financial performance. Additionally, the loss of market share or financial difficulties, including bankruptcy and financial restructuring, by these trade customers could have a material adverse effect on our liquidity, financial position and results of operations.

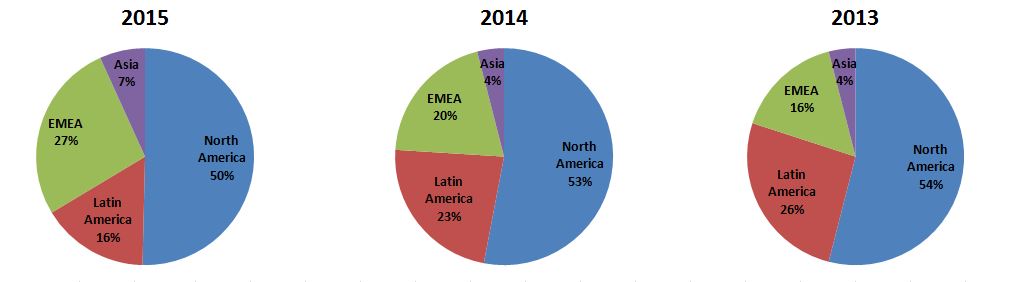

Risks associated with our international operations may decrease our revenues and increase our costs. For the year ended December 31, 2015, we derived approximately 50% of our net sales from outside of North America, including 16% in Latin America, 27% in EMEA and 7% in Asia. We expect that international sales will continue to account for a significant percentage of our net sales in the foreseeable future. Accordingly, we face numerous risks associated with conducting international operations, any of which could negatively affect our financial performance. These risks include the following:

•political, legal, and economic instability and uncertainty;

•foreign currency exchange rate fluctuations;

•changes in foreign tax rules, regulations and other requirements, such as changes in tax rates and statutory and judicial interpretations of tax laws;

•changes in diplomatic and trade relationships, including sanctions resulting from the current political situation in Russia and Ukraine;

•inflation;

•changes in foreign country regulatory requirements;

•various import/export restrictions and the availability of required import/export licenses;

•imposition of foreign tariffs and other trade barriers;

•managing widespread operations and enforcing internal policies and procedures such as compliance with U.S. and foreign anti-bribery and anti-corruption regulations, such as the FCPA, and antitrust laws;

•work stoppages and labor relations;

•disruptions in the shipping of imported and exported products;

•government price controls;

•extended payment terms and the inability to collect accounts receivable; and

•limitations on the repatriation or movement of earnings and cash.

As a U.S. corporation, we are subject to the FCPA, which may place us at a competitive disadvantage to foreign companies that are not subject to similar regulations. Additionally, any determination that we have violated the FCPA or other anti-corruption laws could have a material adverse effect on us.

Terrorist attacks, armed conflicts, labor disputes, natural disasters, governmental actions and epidemics could affect our domestic and international sales, disrupt our supply chain, and impair our ability to produce and deliver our products. Such events could directly impact our physical facilities or those of our suppliers or customers, both in the United States and elsewhere.

Fluctuations and volatility in the cost of raw materials and purchased components could adversely affect our operating results. The primary materials used to produce and manufacture our products are steel, plastic resins, and base metals, such as aluminum, copper, zinc, and nickel. On a global and regional basis, the sources and prices of those materials and components containing those materials are susceptible to significant price fluctuations due to supply/demand trends, transportation costs, government regulations and tariffs, changes in currency exchange rates, price controls, the economic climate, and other unforeseen circumstances. Significant increases in these and other costs in the future could have a material adverse effect on our operating results.

8

Foreign currency fluctuations may affect our financial performance. We generate a significant portion of our revenue and incur a significant portion of our expenses in currencies other than the U.S. dollar. Changes in the exchange rates of functional currencies of those operations affect the U.S. dollar value of our revenue and earnings from our foreign operations. We use currency forwards and options to manage our foreign currency transaction exposures. We cannot completely eliminate our exposure to foreign currency fluctuations, which may adversely affect our financial performance. In addition, because our consolidated financial results are reported in U.S. dollars, if we generate sales or earnings in other currencies, the translation of those results into U.S. dollars can result in a significant increase or decrease in the amount of those sales or earnings. Finally, the amount of legal contingencies related to foreign operations may fluctuate significantly based upon changes in the exchange rates and usually cannot be managed with currency forwards, options or other arrangements. Such fluctuations in exchange rates can significantly increase or decrease the amount of any legal contingency related to our foreign operations and make it difficult to assess and manage the potential exposure.

Unfavorable results of legal and tax proceedings could materially adversely affect our business and financial condition and performance. We are subject to a variety of litigation and legal compliance risks relating to, among other things, products, intellectual property rights, income and non-income taxes, environmental matters, corporate matters, commercial matters, competition laws and distribution, marketing and trade practices. For example, we are currently disputing certain income and non-income tax related assessments issued by the Brazilian authorities relating to BEFIEX, CFC Tax and to IPI tax credits (see Note 7 and Note 12 of the Notes to the Consolidated Financial Statements for additional information on these matters). Unfavorable outcomes regarding these assessments could have a material adverse effect on our financial position, liquidity, or results of operations in any particular reporting period. Results of legal proceedings cannot be predicted with certainty and for some matters, such as class actions, no insurance is likely available. Regardless of merit, legal proceedings may be both time-consuming and disruptive to our operations and could divert the attention of our management and key personnel from our business operations. We estimate loss contingencies and establish accruals as required by generally accepted accounting principles, based on our assessment of contingencies where liability is deemed probable and reasonably estimable, in light of the facts and circumstances known to us at a particular point in time. Subsequent developments in legal proceedings, volatility in foreign currency exchange rates and other factors may affect our assessment and estimates of the loss contingency recorded and could result in an adverse effect on our results of operations in the period in which a liability would be recognized or cash flows for the period in which amounts would be paid. Actual results may significantly vary from our reserves.

We are subject to, and could be further subject to, governmental investigations or actions by other third parties. We are subject to various federal, foreign and state laws, including antitrust laws, violations of which can involve civil or criminal sanctions. Responding to governmental investigations or other actions may be both time-consuming and disruptive to our operations and could divert the attention of our management and key personnel from our business operations. The impact of these and other investigations and lawsuits could have a material adverse effect on our financial position, liquidity and results of operations.

Changes in the legal and regulatory environment could limit our business activities, increase our operating costs, reduce demand for our products or result in litigation. The conduct of our businesses, and the production, distribution, sale, advertising, safety, transportation and use of many of our products, are subject to various laws and regulations administered by federal, state and local governmental agencies in the United States, as well as to foreign laws and regulations administered by government entities and agencies in markets in which we operate. These laws and regulations may change, sometimes dramatically, as a result of political, economic or social events. Changes in laws, regulations or governmental policy and the related interpretations may alter the environment in which we do business and, therefore, may impact our results or increase our costs or liabilities. In addition, we incur and will continue to incur capital and other expenditures to comply with various laws and regulations, especially relating to protection of the environment, human health and safety and energy efficiency. These types of costs could adversely affect our financial performance. Additionally, we could be subjected to future liabilities, fines or penalties or the suspension of product production for failing to comply with various laws and regulations, including environmental regulations. Cleanup obligations that might arise at any of our manufacturing sites or the imposition of more stringent environmental laws in the future could adversely affect us.

Failure to maintain our reputation and brand image could negatively impact our business. Our brands have worldwide recognition, and our success depends on our ability to maintain and enhance our brand image and reputation. Maintaining, promoting and growing our brands depends on our design and marketing efforts, including advertising and consumer campaigns, as well as product innovation. We could be adversely impacted if we fail to achieve any of these objectives or if, whether or not justified, the reputation or image of any of our brands is tarnished or receives negative publicity. In addition, adverse publicity about regulatory or legal action against us, or product quality issues, could damage our reputation and brand image, undermine our customers' confidence in us and reduce long-term demand for our products, even if the regulatory or legal action is unfounded or not material to our operations.

9

In addition, our success in maintaining, extending and expanding our brand image depends on our ability to adapt to a rapidly changing media environment, including our increasing reliance on social media and online dissemination of advertising campaigns. Negative posts or comments about us on social networking and other websites that spread rapidly through such forums could seriously damage our reputation and brand image. If we do not maintain, extend and expand our brand image, then our product sales, financial condition and results of operations could be materially and adversely affected.

An inability to effectively execute and manage our business objectives could adversely affect our financial performance. The highly competitive nature of our industry requires that we effectively execute and manage our business including our global operating platform initiative. Our global operating platform initiative aims to reduce costs, expand margins, drive productivity and quality improvements, accelerate our rate of innovation, and drive shareholder value. Our inability to effectively control costs and drive productivity improvements could affect our profits. In addition, our inability to provide high-quality, innovative products could adversely affect our ability to maintain or increase our sales, which could negatively affect our revenues and overall financial performance. Additionally, our success is dependent on anticipating and appropriately reacting to changes in customer preferences and on successful new product and process development and product relaunches in response to such changes. Our future results and our ability to maintain or improve our competitive position will depend on our capacity to gauge the direction of our key markets and upon our ability to successfully and timely identify, develop, manufacture, market, and sell new or improved products in these changing markets.

We may be subject to information technology system failures, network disruptions, cybersecurity attacks and breaches in data security, which may materially adversely affect our operations, financial condition and operating results. We depend on information technology as an enabler to improve the effectiveness of our operations and to interface with our customers, as well as to maintain financial accuracy and efficiency. Information technology system failures, including suppliers' or vendors' system failures, could disrupt our operations by causing transaction errors, processing inefficiencies, delays or cancellation of customer orders, the loss of customers, impediments to the manufacture or shipment of products, other business disruptions, or the loss of or damage to intellectual property through security breach.

In addition, we have outsourced certain information technology support services and administrative functions, such as payroll processing and benefit plan administration, to third-party service providers and may outsource other functions in the future to achieve cost savings and efficiencies. If the service providers to which we outsource these functions do not perform effectively, we may not be able to achieve the expected cost savings and may have to incur additional costs to correct errors made by such service providers. Depending on the function involved, such errors may also lead to business disruption, processing inefficiencies or the loss of or damage to intellectual property through security breach, or harm employee morale.

Our information systems, or those of our third-party service providers, could also be penetrated by outside parties' intent on extracting information, corrupting information or disrupting business processes. Such unauthorized access could disrupt our business and could result in the loss of assets. Cybersecurity attacks are becoming more sophisticated and include, but are not limited to, malicious software, attempts to gain unauthorized access to data, and other electronic security breaches that could lead to disruptions in critical systems, unauthorized release of confidential or otherwise protected information, and corruption of data. These events could impact our customers and reputation and lead to financial losses from remediation actions, loss of business or potential liability or an increase in expense, all of which may have a material adverse effect on our business.

Product liability or product recall costs could adversely affect our business and financial performance. We are subject to the risk of exposure to product liability and product recall claims if any of our products are alleged to have resulted in injury to persons or damage to property. In the event that any of our products prove to be defective, we may need to recall and/or redesign such products. In addition, any claim or product recall that results in significant adverse publicity, particularly if those claims or recalls cause customers to question the safety or reliability of our products, may negatively affect our business, financial condition, or results of operations. We do maintain product liability insurance, but this insurance may not be adequate to cover losses related to product liability claims brought against us. We may also be involved in certain class action and other litigation, for which no insurance is available. Product liability insurance could become more expensive and difficult to maintain and may not be available on commercially reasonable terms, if at all. In addition, we do not maintain any product recall insurance. Therefore any product recall we are required to initiate could have a significant impact on our operating results and/or cash flows.

We regularly engage in investigations of potential quality and safety issues as part of our ongoing effort to deliver quality products to our customers. We are currently investigating a limited number of potential quality and safety issues, and as necessary, we undertake to effect repair or replacement of appliances. Currently we are implementing a corrective action plan affecting certain of our Indesit and Hotpoint branded dryers (see Note 7 of the Notes to the Consolidated Financial Statements for additional information on these matters). Actual costs of these issues and any future issues depend upon several factors, including the number of consumers who respond to a particular recall, repair and administrative costs, whether the cost of any corrective action is borne initially by Whirlpool or the supplier, and, if initially borne by Whirlpool, whether we will be successful in recovering our costs

10

from the supplier. The actual costs incurred as a result of these issues and any future issues could have a material adverse effect on our business, financial condition or results of operations.

We face inventory and other asset risk. We write-down product and component inventories that have become obsolete or do not meet anticipated demand or net realizable value. We also review our long-lived and intangible assets for impairment whenever events or changed circumstances indicate the carrying amount of an asset may not be recoverable. If we determine that impairment has occurred, we record a write-down to adjust carrying value to fair value. No assurance can be given that, given the unpredictable pace of product obsolescence and business conditions with trade customers and in general, we will not incur additional inventory or asset related charges. Such charges could materially adversely affect our financial condition and operating results.

We are exposed to risks associated with the uncertain global economy. Uncertain and changing economic conditions within our regions, along with national debt and fiscal concerns in various regions and government austerity measures, are posing challenges to the industry in which Whirlpool operates. A number of economic factors, including, but not limited to, gross domestic product, availability of consumer credit, interest rates, consumer sentiment and debt levels, retail trends, housing starts, sales of existing homes, the level of mortgage refinancing and defaults, fiscal and credit market uncertainty, and foreign currency exchange rates, generally affect demand for our products.

Economic uncertainty and related factors exacerbate negative trends in business and consumer spending and may cause certain customers to push out, cancel, or refrain from placing orders for our products. Uncertain market conditions, difficulties in obtaining capital, or reduced profitability may also cause some customers to scale back operations, exit markets, merge with other retailers, or file for bankruptcy protection and potentially cease operations, which can also result in lower sales and/or additional inventory. These conditions may similarly affect key suppliers, which could impair their ability to deliver parts and result in delays for our products or added costs. In addition, these conditions may lead to strategic alliances by, or consolidation of, other appliance manufacturers, which could adversely affect our ability to compete effectively.

A decline in economic activity and conditions in the United States, Latin America, Europe, China and the other areas in which we operate have had an adverse effect on our financial condition and results of operations in recent years, and future declines and adverse conditions could have a similar adverse effect. Regional, political and economic instability in Russia and Ukraine may adversely affect business conditions and may disrupt our operations and have an adverse effect on our financial condition and results of operations. Uncertainty about future economic and industry conditions also makes it more challenging for us to forecast our operating results, make business decisions, and identify and prioritize the risks that may affect our businesses, sources and uses of cash, financial condition and results of operations. We may be required to implement additional cost reduction efforts, including restructuring activities, which may adversely affect our ability to capitalize on opportunities in a market recovery. In addition, our operations are subject to general credit, liquidity, foreign exchange, market and interest rate risks. Our ability to invest in our businesses, fund strategic acquisitions and refinance maturing debt obligations depends in part on access to the capital markets.

If we do not timely and appropriately adapt to changes resulting from the uncertain macroeconomic environment and industry conditions, or to difficulties in the financial markets, or if we are unable to continue to access the capital markets, our business, financial condition and results of operations may be materially and adversely affected.

The ability of suppliers to deliver parts, components and manufacturing equipment to our manufacturing facilities, and our ability to manufacture without disruption, could affect our global business performance. We use a wide range of materials and components in the global production of our products and use numerous suppliers to provide materials and components. Because we generally do not have guaranteed supply arrangements with our suppliers and some key parts may be available only from a single supplier or a limited group of suppliers, we are subject to supply and pricing risk. In addition, certain proprietary component parts used in some of our products are provided by single-source unaffiliated third-party suppliers. We would be unable to obtain these proprietary component parts for an indeterminate period of time if these single-source suppliers were to cease or interrupt production or otherwise fail to supply these components to us, which could adversely affect our product sales and operating results. Our operations and operations at suppliers' facilities are subject to disruption for a variety of reasons, including, but not limited to, work stoppages, labor relations, intellectual property claims against suppliers, information technology failures, and hazards such as fire, earthquakes, flooding, or other natural disasters, insurance for any of which may not be available, affordable or adequate. Such disruption could interrupt our ability to manufacture certain products. Any significant disruption could negatively impact our revenue and earnings performance.

11

Our ability to attract, develop and retain executives and other qualified employees is crucial to our results of operations and future growth. We depend upon the continued services and performance of our key executives, senior management and skilled personnel, particularly our professionals with experience in our business and operations and the home appliance industry. We cannot be sure that any of these individuals will continue to be employed by us. A lengthy period of time is required to hire and develop replacement personnel when skilled personnel depart Whirlpool. An inability to hire, develop, engage and retain a sufficient number of qualified employees could materially hinder our business by, for example, delaying our ability to bring new products to market or impairing the success of our operations.

A deterioration in labor relations could adversely impact our global business. As of December 31, 2015, we had approximately 97,000 employees. We are subject to separate collective bargaining agreements with certain labor unions, which generally have two to three year terms, as well as various other commitments regarding our workforce. We are periodically in negotiations with certain of the unions representing our employees and may be subject to employee work stoppages that, if such events were to occur, may have a material adverse effect on our business, financial condition, or results of operations. Further, we cannot be assured that we will be able to renew collective bargaining agreements on the same or similar terms, or at all, which may also have a material adverse effect on our business, financial condition, or results of operations.

Our intellectual property rights are valuable, and any inability to protect them could reduce the value of our products, services and brands. We consider our intellectual property rights, including patents, trademarks, trade secrets and licensing agreements, to be a significant and valuable aspect of our business. We attempt to protect our intellectual property rights through a combination of patent, trademark, copyright and trade secret laws, as well as licensing agreements and third party nondisclosure and assignment agreements. Our failure to obtain or adequately protect our trademarks, products, new features of our products, or our processes may diminish our competitiveness.

We have applied for patent protection in the United States and other jurisdictions with respect to certain innovations and new products, product features, and processes. We cannot be assured that the U.S. Patent and Trademark Office or any other jurisdiction will approve any of our patent applications. Additionally, the patents we own could be challenged, invalidated, or others could design around our patents and the patents may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, the laws of certain foreign countries in which we do business, or contemplate doing business in the future, do not recognize intellectual property rights or protect them to the same extent as United States law. As a result, these factors could weaken our competitive advantage with respect to our products, services, and brands in foreign jurisdictions, which could adversely affect our financial performance.

Moreover, while we do not believe that any of our products infringe on enforceable intellectual property rights of third parties, others may assert intellectual property rights that cover some of our technology, brands, products, or services. Any litigation regarding patents or other intellectual property could be costly and time-consuming and could divert the attention of our management and key personnel from our business operations. Claims of intellectual property infringement might also require us to enter into costly license agreements. We also may be subject to significant damages or injunctions against development and sale of certain products.

Significant differences between actual results and estimates of the amount of future funding for our pension plans and postretirement health care benefit programs, and significant changes in funding assumptions or significant increases in funding obligations due to regulatory changes, could adversely affect our financial results. We have both funded and unfunded defined benefit pension plans that cover certain employees in North America, Europe, Asia and Brazil. We also have unfunded postretirement health care benefit plans for eligible retired employees. The Employee Retirement Income Security Act of 1974 (ERISA) and the Internal Revenue Code, as amended, govern the funding obligations for our U.S. pension plans, which are our principal pension plans. Our U.S. defined benefit plans were frozen as of December 31, 2006 for substantially all participants. For 2007 and beyond, Whirlpool employees may participate in an enhanced defined contribution plan.

As of December 31, 2015, our projected benefit obligations under our pension plans and postretirement health and welfare benefit programs exceeded the fair value of plan assets by an aggregate of approximately $1.5 billion, ($1.0 billion of which was attributable to pension plans and $0.5 billion of which was attributable to postretirement health care benefits). Estimates for the amount and timing of the future funding obligations of these pension plans and postretirement health and welfare benefit plans are based on various assumptions. These assumptions include discount rates, expected long-term rate of return on plan assets, life expectancies and health care cost trend rates. These assumptions are subject to change based on changes in interest rates on high quality bonds, stock and bond market returns, and health care cost trend rates, all of which are largely outside our control. Significant differences in results or significant changes in assumptions may materially affect our postretirement obligations and related future contributions and expenses.

12

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

Our principal executive offices are located in Benton Harbor, Michigan. On December 31, 2015, our principal manufacturing operations were carried on at 43 locations in 14 countries worldwide. We occupied a total of approximately 90 million square feet devoted to manufacturing, service, sales and administrative offices, warehouse and distribution space. Over 41 million square feet of such space is occupied under lease. Whirlpool properties include facilities which are suitable and adequate for the manufacture and distribution of Whirlpool’s products. The company’s major production sites by operating segment are as follows:

| North America: | ||

| United States: | Amana and Newton, Iowa; Tulsa, Oklahoma; Fall River, Massachusetts; | |

| Greenville, Clyde, Findlay, Marion and Ottawa, Ohio; | ||

| Cleveland, Tennessee | ||

| Mexico: | Celaya; Monterrey; Ramos Arizpe | |

| Latin America: | ||

| Brazil: | Itaiopolis; Joinville; Manaus; Rio Claro | |

| China: | Beijing | |

| Colombia: | Medellin (Joint Venture) | |

| Italy: | Riva di Chieri | |

| Slovakia: | Spisska Nova Ves | |

| Mexico: | Monterrey | |

| Europe, Middle East and Africa: | ||

| France: | Amiens | |

| Italy: | Cassinetta; Comunanza; Fabriano; Naples; Siena; Teverola | |

| Poland: | Lodz; Radomsko; Wroclaw | |

| Russia: | Lipetsk | |

| Slovakia: | Poprad | |

| South Africa: | Isithebe | |

| Turkey: | Manisa | |

| United Kingdom: | Yates | |

| Asia: | ||

| China: | ChangXing (Joint Venture); Hefei; Shunde | |

| India: | Faridabad; Pondicherry; Pune | |

| ITEM 3. | LEGAL PROCEEDINGS |

Information regarding legal proceedings can be found in Note 7 to the Consolidated Financial Statements and is incorporated herein by reference.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

13

| PART II | ||||

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS |

| AND ISSUER PURCHASES OF EQUITY SECURITIES | |

Whirlpool’s common stock is traded on the New York Stock Exchange and the Chicago Stock Exchange. As of February 12, 2016, the number of holders of record of Whirlpool common stock was approximately 10,631.

Quarterly market and dividend information can be found in Note 15 (unaudited) to the Consolidated Financial Statements.

On April 14, 2014, our Board of Directors authorized a new share repurchase program of up to $500 million. Share repurchases are made from time to time on the open market as conditions warrant. The program does not obligate us to repurchase any of our shares. For the years ended December 31, 2015 and 2014, we repurchased 1,505,299 shares at an aggregate purchase price of approximately $250 million and 165,900 shares at an aggregate purchase price of approximately $25 million. At December 31, 2015, there were approximately $225 million in remaining funds authorized under this program.

The following table summarizes repurchases of Whirlpool's common stock in the three months ended December 31, 2015:

| Period (Millions of dollars, except number and price per share) | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan | ||||||

| October 1, 2015 through October 31, 2015 | 984,699 | $ | 157.62 | 984,699 | $ | 225 | ||||

| November 1, 2015 through November 30, 2015 | — | — | — | 225 | ||||||

| December 1, 2015 through December 31, 2015 | — | — | — | 225 | ||||||

| Total | 984,699 | $ | 157.62 | 984,699 | ||||||

The following table summarizes repurchases of Whirlpool's common stock in the twelve months ended December 31, 2015:

| Period (Millions of dollars, except number and price per share) | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan | ||||||

| January 1, 2015 through March 31, 2015 | — | $ | — | — | $ | 475 | ||||

| April 1, 2015 through June 30, 2015 | 267,400 | 186.60 | 267,400 | 425 | ||||||

| July 1, 2015 through September 30, 2015 | 253,200 | 177.30 | 253,200 | 380 | ||||||

| October 1, 2015 through December 31, 2015 | 984,699 | 157.62 | 984,699 | 225 | ||||||

| Total | 1,505,299 | $ | 166.08 | 1,505,299 | ||||||

14

| ITEM 6. | SELECTED FINANCIAL DATA |

FIVE-YEAR SELECTED FINANCIAL DATA

| (Millions of dollars, except share and employee data) | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

| CONSOLIDATED OPERATIONS | ||||||||||||||||||||

| Net sales | $ | 20,891 | $ | 19,872 | $ | 18,769 | $ | 18,143 | $ | 18,666 | ||||||||||

| Restructuring costs | 201 | 136 | 196 | 237 | 136 | |||||||||||||||

| Depreciation and amortization | 668 | 560 | 540 | 551 | 558 | |||||||||||||||

| Operating profit | 1,285 | 1,188 | 1,249 | 869 | 792 | |||||||||||||||

| Earnings (loss) before income taxes and other items | 1,031 | 881 | 917 | 558 | (28 | ) | ||||||||||||||

| Net earnings | 822 | 692 | 849 | 425 | 408 | |||||||||||||||

| Net earnings available to Whirlpool | 783 | 650 | 827 | 401 | 390 | |||||||||||||||

| Capital expenditures | 689 | 720 | 578 | 476 | 608 | |||||||||||||||

| Dividends paid | 269 | 224 | 187 | 155 | 148 | |||||||||||||||

| CONSOLIDATED FINANCIAL POSITION | ||||||||||||||||||||

| Current assets | $ | 7,325 | $ | 8,098 | $ | 7,022 | $ | 6,827 | $ | 6,422 | ||||||||||

| Current liabilities | 7,744 | 8,403 | 6,794 | 6,510 | 6,297 | |||||||||||||||

| Accounts receivable, inventories and accounts payable, net | 746 | 778 | 548 | 694 | 947 | |||||||||||||||

| Property, net | 3,774 | 3,981 | 3,041 | 3,034 | 3,102 | |||||||||||||||

| Total assets | 19,010 | 20,002 | 15,544 | 15,396 | 15,181 | |||||||||||||||

| Long-term debt | 3,470 | 3,544 | 1,846 | 1,944 | 2,129 | |||||||||||||||

Total debt(1) | 3,998 | 4,347 | 2,463 | 2,461 | 2,491 | |||||||||||||||

| Whirlpool stockholders’ equity | 4,743 | 4,885 | 4,924 | 4,260 | 4,181 | |||||||||||||||

| PER SHARE DATA | ||||||||||||||||||||

| Basic net earnings available to Whirlpool | $ | 9.95 | $ | 8.30 | $ | 10.42 | $ | 5.14 | $ | 5.07 | ||||||||||

| Diluted net earnings available to Whirlpool | 9.83 | 8.17 | 10.24 | 5.06 | 4.99 | |||||||||||||||

| Dividends | 3.45 | 2.88 | 2.38 | 2.00 | 1.93 | |||||||||||||||

Book value(2) | 59.54 | 61.39 | 60.97 | 53.70 | 53.50 | |||||||||||||||

| Closing Stock Price—NYSE | 146.87 | 193.74 | 156.86 | 101.75 | 47.45 | |||||||||||||||

| KEY RATIOS | ||||||||||||||||||||

| Operating profit margin | 6.2 | % | 6.0 | % | 6.7 | % | 4.8 | % | 4.2 | % | ||||||||||

Pre-tax margin(3) | 4.9 | % | 4.4 | % | 4.9 | % | 3.1 | % | (0.2 | )% | ||||||||||

Net margin(4) | 3.7 | % | 3.3 | % | 4.4 | % | 2.2 | % | 2.1 | % | ||||||||||

Return on average Whirlpool stockholders’ equity(5) | 16.3 | % | 13.3 | % | 18.0 | % | 9.5 | % | 9.3 | % | ||||||||||

Return on average total assets(6) | 4.0 | % | 3.7 | % | 5.3 | % | 2.6 | % | 2.5 | % | ||||||||||

| Current assets to current liabilities | 0.9 | 1.0 | 1.0 | 1.0 | 1.0 | |||||||||||||||

Total debt as a percent of invested capital(7) | 41.3 | % | 42.9 | % | 33.0 | % | 36.0 | % | 36.8 | % | ||||||||||

Price earnings ratio(8) | 14.9 | 23.7 | 15.3 | 20.1 | 9.5 | |||||||||||||||

| OTHER DATA | ||||||||||||||||||||

| Common shares outstanding (in thousands): | ||||||||||||||||||||

| Average number—on a diluted basis | 79,667 | 79,578 | 80,761 | 79,337 | 78,143 | |||||||||||||||

| Year-end common shares outstanding | 77,221 | 77,956 | 77,417 | 78,407 | 76,451 | |||||||||||||||

| Year-end number of stockholders | 10,663 | 11,225 | 11,889 | 12,759 | 13,527 | |||||||||||||||

| Year-end number of employees | 97,000 | 100,000 | 69,000 | 68,000 | 68,000 | |||||||||||||||

Five-year annualized total return to stockholders(9) | 13.0 | % | 22.0 | % | 34.0 | % | 7.6 | % | (8.1 | )% | ||||||||||

(1) Total debt includes notes payable and current and long-term debt.

(2) Total Whirlpool stockholders’ equity divided by average number of shares on a diluted basis.

(3) Earnings (loss) before income taxes, as a percent of net sales.

(4) Net earnings available to Whirlpool, as a percent of net sales.

(5) Net earnings available to Whirlpool, divided by average Whirlpool stockholders’ equity.

(6) Net earnings available to Whirlpool, divided by average total assets.

(7) Total debt divided by total debt and total stockholders’ equity.

(8) Closing stock price divided by diluted net earnings available to Whirlpool.

(9) Stock appreciation plus reinvested dividends, divided by share price at the beginning of the period.

15

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND |

| RESULTS OF OPERATIONS | |

This Management Discussion and Analysis should be read in connection with the Consolidated Financial Statements, Notes to the Consolidated Financial Statements and Selected Financial Data included in this Form 10-K. Certain references to particular information in the Notes to the Consolidated Financial Statements are made to assist readers.

ABOUT WHIRLPOOL

Whirlpool Corporation (“Whirlpool”) is the number one major appliance manufacturer in the world with net sales of approximately $21 billion and net earnings available to Whirlpool of $783 million in 2015. We are a leading producer of major home appliances in North America, Latin America and Europe, and have a significant presence throughout China and India. We have received worldwide recognition for accomplishments in a variety of business and social efforts, including leadership, diversity, innovative product design, business ethics, social responsibility and community involvement. We conduct our business through four reportable segments, which we define based on geography. Our reportable segments consist of North America, Latin America, EMEA (Europe, Middle East and Africa) and Asia. Our customer base includes large, sophisticated trade customers who have many choices and demand competitive products, services and prices. The major home appliance industry operates in an intensely competitive environment, reflecting the impact of both new and established global competitors, including Asian and European manufacturers.

The charts below summarize the balance of net sales by reportable segment for 2015, 2014 and 2013, respectively:

We monitor country-specific economic factors such as gross domestic product, unemployment, consumer confidence, retail trends, housing starts and completions, sales of existing homes and mortgage interest rates as key indicators of industry demand. In addition to profitability, we also focus on country, brand, product and channel sales when assessing and forecasting financial results.

Our leading portfolio of brands includes Whirlpool, Maytag, KitchenAid, Embraco, Brastemp, Consul and Indesit, each of which generated annual revenues in excess of $1 billion. Our global branded consumer products strategy is to introduce innovative new products, increase brand customer loyalty, expand our presence outside the United States, enhance our trade management platform, improve total cost and quality by expanding and leveraging our global operating platform and, where appropriate, make strategic acquisitions and investments.

As we grow revenues in our core products, our strategy is to extend our business by offering products and services that are dependent on and related to our core business and expand into adjacent products, such as Affresh cleaners and Gladiator GarageWorks, through businesses that leverage our core competencies and business infrastructure.

OVERVIEW

Whirlpool delivered strong results in 2015, driving revenue growth, margin expansion and strong cash generation by leveraging our industry leading brand portfolio and innovative new products within our core appliance and adjacent businesses. We achieved these results through strong focus and decisive action plans in a global environment that saw rapid emerging markets demand decline and strengthening of U.S. dollar against most global currencies. Over the past year, we made moves to reshape our global operating footprint, respond to shifts in the operating environment and invest in our brands and products. We made substantial progress toward integrating Indesit in Europe and Hefei Sanyo in China, our 2014 acquisitions, that create leading

16

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - (CONTINUED)

positions as a western company, in those markets. We have great opportunities for growth as demand in the U.S. continues to recover and we are very well positioned to capitalize when growth returns to emerging markets such as Brazil, China, and Russia.

We believe that continued execution of our business priorities and a focus on long-term growth will allow the Company to adapt to changes in the macroeconomic environment and continue to create shareholder value.

RESULTS OF OPERATIONS

The following table summarizes the consolidated results of operations:

| December 31, | ||||||||||||||||

| Consolidated - Millions of dollars (except per share data) | 2015 | Better/(Worse) | 2014 | Better/(Worse) | 2013 | |||||||||||

| Net sales | $ | 20,891 | 5.1% | $ | 19,872 | 5.9% | $ | 18,769 | ||||||||

| Gross margin | 3,690 | 8.7 | 3,395 | 2.9 | 3,298 | |||||||||||

| Selling, general and administrative | 2,130 | (4.6) | 2,038 | (11.5) | 1,828 | |||||||||||

| Restructuring costs | 201 | (48.2) | 136 | 30.9 | 196 | |||||||||||

| Interest and sundry income (expense) | (89 | ) | 36.7 | (142 | ) | 8.6 | (155 | ) | ||||||||

| Interest expense | (165 | ) | (0.2) | (165 | ) | 6.7 | (177 | ) | ||||||||

| Income tax expense | 209 | 10.1 | 189 | nm | 68 | |||||||||||

| Net earnings available to Whirlpool | 783 | 20.4 | 650 | (21.3) | 827 | |||||||||||

| Diluted net earnings available to Whirlpool per share | $ | 9.83 | 20.3% | $ | 8.17 | (20.2)% | $ | 10.24 | ||||||||

nm: not meaningful

Consolidated Net Sales

The following tables summarize units sold and consolidated net sales by operating segment:

| December 31, | |||||||||||||||

| Units Sold - In thousands | 2015 | Better/(Worse) | 2014 | Better/(Worse) | 2013 | ||||||||||

| North America | 27,273 | 1.4 | % | 26,892 | 3.8 | % | 25,895 | ||||||||

| EMEA | 25,145 | 59.7 | 15,744 | 32.2 | 11,907 | ||||||||||

| Latin America | 10,084 | (21.3 | ) | 12,821 | (4.5 | ) | 13,422 | ||||||||

| Asia | 7,770 | 78.8 | 4,346 | 11.0 | 3,917 | ||||||||||

| Consolidated | 70,272 | 17.5 | % | 59,803 | 8.5 | % | 55,141 | ||||||||

| December 31, | ||||||||||||||||||

| Consolidated Net Sales - Millions of dollars | 2015 | Better/(Worse) | 2014 | Better/(Worse) | 2013 | |||||||||||||

| North America | $ | 10,732 | 0.9 | % | $ | 10,634 | 4.5 | % | $ | 10,178 | ||||||||

| EMEA | 5,601 | 43.4 | 3,905 | 29.1 | 3,024 | |||||||||||||

| Latin America | 3,349 | (28.5 | ) | 4,686 | (4.9 | ) | 4,928 | |||||||||||

| Asia | 1,417 | 73.6 | 816 | 1.2 | 807 | |||||||||||||

| Other/eliminations | (208 | ) | nm | (169 | ) | nm | (168 | ) | ||||||||||

| Consolidated | $ | 20,891 | 5.1 | % | $ | 19,872 | 5.9 | % | $ | 18,769 | ||||||||

nm: not meaningful

Consolidated net sales increased 5.1% compared to 2014 primarily driven by increased volume due to acquisitions and favorable product price/mix, partially offset by the unfavorable impact of foreign currency and a weakened demand environment in emerging markets. Excluding the impact of foreign currency, consolidated net sales increased 18.1% compared to 2014. Consolidated net sales for 2014 increased 5.9% compared to 2013 primarily due to favorable product price/mix, increased volume due to acquisitions, partially offset by the unfavorable impact of foreign currency and lower BEFIEX credits. Excluding the impact of foreign currency and BEFIEX credits, consolidated net sales for 2014 increased 8.4% compared to 2013.

17

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - (CONTINUED)

We provide the percentage change in net sales, excluding the impact of foreign currency and BEFIEX credits, as a supplement to the change in net sales as determined by U.S. generally accepted accounting principles ("GAAP") to provide stockholders with a clearer basis to assess Whirlpool's results over time. This measure is considered a non-GAAP financial measure and is calculated by translating the current period net sales excluding BEFIEX credits, in functional currency, to U.S. dollars using the prior-year period's exchange rate compared to the prior-year period net sales excluding BEFIEX credits.

Significant regional trends were as follows:

| • | North America net sales increased 0.9% compared to 2014 primarily due to a 1.4% increase in units sold and favorable product price/mix, partially offset by foreign currency. Excluding the impact of foreign currency, net sales increased 3.2% in 2015. North America net sales for 2014 increased 4.5% compared to 2013 primarily due to a 3.8% increase in units sold and favorable product/price mix, partially offset by foreign currency. Excluding the impact of foreign currency, net sales increased 5.1% in 2014. |

| • | EMEA net sales increased 43.4% compared to 2014, primarily due to a 59.7% increase in units sold due to the acquisition of Indesit and favorable product mix, partially offset by unfavorable foreign currency. Excluding the impact of foreign currency, net sales increased 75.3% in 2015. In 2014 EMEA net sales increased 29.1% compared to 2013, primarily due to a 32.2% increase in units sold due to the acquisition of Indesit, partially offset by unfavorable product/price mix and foreign currency. Excluding the impact of foreign currency, net sales increased 29.6% in 2014. |

| • | Latin America net sales decreased 28.5% compared to 2014 primarily due to a 21.3% decrease in units sold and unfavorable foreign currency, partially offset by favorable product mix. Excluding the impact of foreign currency, Latin America net sales decreased 5.9% in 2015. Latin America net sales for 2014 decreased 4.9% compared to 2013 primarily due to a 4.5% decrease in units sold, lower BEFIEX credits and unfavorable foreign currency, partially offset by favorable product price/mix. Excluding the impact of foreign currency and BEFIEX credits, Latin America net sales increased 2.5% in 2014. |

We recognized approximately $0, $14 million and $109 million of BEFIEX credits in 2015, 2014 and 2013, respectively. As of December 31, 2015, approximately $34 million of future cash monetization remained for court awarded fees, which is not expected to be payable for several years. For additional information regarding BEFIEX credits, see Notes 7 and 12 of the Notes to the Consolidated Financial Statements.

| • | Asia net sales increased 73.6% compared to 2014 primarily due to the acquisition of Hefei Sanyo. Excluding the impact of foreign currency, Asia net sales increased 78.3% in 2015. Asia net sales for 2014 increased 1.2% compared to 2013 primarily due to the acquisition of Hefei Sanyo, partially offset by foreign currency, product transition costs and unfavorable product price/mix. Excluding the impact of foreign currency, Asia net sales increased 4.1% in 2014. |

Gross Margin

The table below summarizes gross margin percentages by region:

| December 31, | |||||||||||||||

| Percentage of net sales | 2015 | Change | 2014 | Change | 2013 | ||||||||||

| North America | 18.9 | % | 1.5 pts | 17.4 | % | (0.7) pts | 18.1 | % | |||||||

| EMEA | 14.7 | — | 14.7 | 3.5 | 11.2 | ||||||||||

| Latin America | 14.9 | (2.9 | ) | 17.8 | (1.6 | ) | 19.4 | ||||||||

| Asia | 23.4 | 7.5 | 15.9 | (2.7 | ) | 18.6 | |||||||||

| Consolidated | 17.7 | % | 0.6 pts | 17.1 | % | (0.5) pts | 17.6 | % | |||||||

The consolidated gross margin percentage increased 60 basis points to 17.7% compared to 2014, primarily due to ongoing cost productivity, favorable product price/mix, acquisition synergies and capacity optimization initiatives, partially offset by foreign currency.

Significant regional trends were as follows:

| • | North America gross margin increased compared to 2014 primarily due to ongoing cost productivity and recognition of postretirement-benefit curtailment gains, partially offset by unfavorable foreign currency. North America gross margin for 2014 decreased compared to 2013 primarily due to the impact of product transitions, partially offset by productivity. |

18

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - (CONTINUED)

| • | EMEA gross margin was flat compared to 2014 primarily due to benefits from the Indesit acquisition, favorable product price/mix, ongoing cost productivity, and capacity optimization initiatives, partially offset by unfavorable foreign currency, legacy Indesit product corrective action costs and increased investments in marketing, technology and products. During 2014, EMEA gross margin increased compared to 2013 primarily due to increased productivity, acquisition synergies and restructuring benefits, partially offset by unfavorable product price/mix and unfavorable foreign currency. |

| • | Latin America gross margin decreased compared to 2014 primarily due to unfavorable foreign currency and the weakened demand environment in Brazil, partially offset by higher product price/mix. During 2014, Latin America gross margin decreased compared to 2013 primarily due to lower BEFIEX credits, higher material costs and unfavorable foreign currency, partially offset by higher product price/mix. |

| • | Asia gross margin increased in 2015 when compared to 2014, primarily due to acquisition synergies, partially offset by increased investments in marketing, technology and products. During 2014, Asia gross margin decreased compared to 2013 primarily due to expenses related to the acquisition of Hefei Sanyo, foreign currency and unfavorable material costs, partially offset by favorable product price/mix, productivity and acquisition synergies. |

Selling, General and Administrative

The following table summarizes selling, general and administrative expenses as a percentage of sales by region:

| December 31, | ||||||||||||||||||

| Millions of dollars | 2015 | As a % of Net Sales | 2014 | As a % of Net Sales | 2013 | As a % of Net Sales | ||||||||||||

| North America | $ | 762 | 7.1% | $ | 761 | 7.2% | $ | 758 | 7.5% | |||||||||

| EMEA | 604 | 10.8 | 506 | 13.0 | 338 | 11.2 | ||||||||||||

| Latin America | 315 | 9.4 | 359 | 7.7 | 399 | 8.1 | ||||||||||||

| Asia | 226 | 16.0 | 146 | 17.9 | 116 | 14.4 | ||||||||||||

| Corporate/other | 223 | — | 266 | — | 217 | — | ||||||||||||

| Consolidated | $ | 2,130 | 10.2% | $ | 2,038 | 10.3% | $ | 1,828 | 9.7% | |||||||||

Consolidated selling, general and administrative expenses as a percent of consolidated net sales in 2015 remained flat compared to 2014 reflecting the favorable impact of acquisition synergies, partially offset by foreign currency. Selling, general and administrative expenses as a percent of consolidated net sales in 2014 increased compared to 2013, reflecting acquisition-related costs and investment expenses.

Restructuring