OMB APPROVAL

OMB Number: 3235-0570

Expires: January 31, 2017

Estimated average burden hours per response: 20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08895

Voya Funds Trust

(Exact name of registrant as specified in charter)

| 7337 E. Doubletree Ranch Rd. Suite 100, Scottsdale, AZ | 85258 |

| (Address of principal executive offices) | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: March 31

Date of reporting period: March 31, 2015

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

March 31, 2015

Classes A, B, C, I, O, P*, R, R6 and W

Fixed-Income Funds

| ■ | Voya High Yield Bond Fund |

| ■ | Voya Intermediate Bond Fund |

| ■ | Voya Short Term Bond Fund |

| ■ | Voya Strategic Income Opportunities Fund (formerly, Voya Strategic Income Fund) |

*Patent Pending

E-Delivery Sign-up – details inside

E-Delivery Sign-up – details inside

| | | This report is submitted for general information to shareholders of the Voya mutual funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. | | |

TABLE OF CONTENTS

| | | | | | Go Paperless with E-Delivery! | | | | |

| | | Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. | |

| | | Just go to www.voyainvestments.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll. | |

| | | You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail. | |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Funds use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Funds’ website at www.voyainvestments.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Funds’ website at www.voyainvestments.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. This report contains a summary portfolio of investments for the Funds. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Funds’ Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Fund by calling Shareholder Services toll-free at (800) 992-0180.

PRESIDENT’S LETTER

A question of resources

Dear Shareholder,

Geopolitical strategy and diplomacy — not to mention the global economy — are deeply driven by questions of access to resources. Who has what you need? How much do you have to pay to get it? How friendly do buyers and sellers need to be?

Today we are confronted with a variety of such issues that may profoundly affect the world for decades to come. For example, the renewed prominence of the United States as an energy producer likely will impact the relationships between consumers, like Europe, and producers, such as Russia and OPEC. While the surge of people fleeing wars in the Middle East and Africa may present an integration challenge to Europe, it also may represent an infusion of youth and energy that the aging continent needs. And as traditional supplies of water come under stress, the need for alternative water sources will likely spur the creation of new technologies and new investment opportunities.

Of course, there are more immediate economic concerns, notably whether central bank support — waning in the U.S., expanding pretty much everywhere else — can sustain global economic growth. Add in elements of political uncertainty, and bouts of market volatility should not be unexpected.

What lessons lie here for your investment program? The most important: Don’t try to “game” diversification. No one can be certain how the global economy will turn, or know where the best investment opportunities will arise. Rather than groping for the next hot investment, you’re well advised to remain broadly diversified, retaining the potential to benefit from whatever the next generation of opportunities has to offer. Periodically review your portfolio with your financial advisor to make sure it remains focused on your investing goals. And as always, do not make changes to your portfolio without first discussing them with your financial advisor.

We appreciate your continued confidence in us, and we look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

Voya Family of Funds

May 1, 2015

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and the Voya mutual funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Voya mutual fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any Voya mutual fund. Reference to specific company securities should not be construed as recommendations or investment advice.

For more complete information, or to obtain a prospectus for any Voya mutual fund, please call your financial advisor or Voya Investments Distributor, LLC at (800) 992-0180 or log on to www.voyainvestments.com. A prospectus should be read carefully before investing. Consider a fund’s investment objectives, risks, charges and expenses carefully before investing. A prospectus contains this information and other information about a fund. Check with your financial advisor to determine which Voya mutual funds are available for sale within their firm. Not all funds are available for sale at all firms.

Market Perspective: Year Ended March 31, 2015

As our fiscal year started, global equities, in the form of the MSCI World IndexSM (the “Index”) measured in local currencies, including net reinvested dividends had just recovered from a 5% slump after ending 2013 at a record high. The Index progressed in fits and starts with some wide swings, to end up 13.98% for the fiscal year. (The Index returned 6.03% for the one year ended March 31, 2015, measured in U.S. dollars.)

A cold and snowy winter depressed hiring and other key statistics like durable goods orders and home sales early in 2014. But with the improvement in the season came a pick-up in U.S. economic data. Employment reports looked steadily better and the unemployment rate fell below 6%. The March bulletin marked the twelfth consecutive month in which more than 200,000 jobs were created. National purchasing managers’ activity indices signaled expansion at mostly healthy rates. While the housing market was cooling, the rate of increase in the S&P/Case-Shiller 20-City Composite Home Price Index seemed to be stabilizing in the mid-single digits. The most widely watched measures of consumer confidence touched multi-year high levels. Growth in gross domestic product (“GDP”) was -2.1% (annualized) in the first quarter but rebounded to 5.0% in the third, before pulling back to 2.2% in the fourth.

Yet concerns periodically surfaced about the sustainability of the recovery in the U.S. and worldwide. The improving U.S. employment situation was accompanied by labor force participation rates at or near the lowest since 1978. Wage growth was sluggish, near 2% annually. The U.S. Federal Reserve Board’s (“Fed’s”) monthly Treasury and mortgage-backed securities purchases ended as expected in October. But by then the Fed’s balance sheet had increased fivefold over six years to $4.5 trillion and the aftermath of any attempt to bring the total down was far from clear. In March, the Fed signaled that a rate rise was probably two or three meetings away, even as some measures like industrial production, retail sales and durable goods orders were starting to fade.

Outside of the U.S., growth in China decelerated to 7.4% in 2014, the slowest since 1990, which weighed on global commodity supplying countries. For this and other reasons, oil prices halved between June and December and floundered thereafter. Japan re-entered recession in the third quarter after an April rise in the consumption tax and the rebound, to growth of 1.5% annualized, was a disappointment. But it was predominantly the euro zone that seemed the most problematic. Growth was barely 1% in 2014. Unemployment seemed stuck above 11.0%, while deflation emerged in December. In Greece, a new government was elected with a mandate to ease the terms of its bailout and roll back reforms. At last in January the European Central Bank (“ECB”) announced quantitative easing, the elixir that despite all else, might drive asset prices higher, judging from the experience of the U.S. and Japan. Monthly purchases of bonds worth €60 billion would be made from March 2015 until September 2016.

Securities prices mirrored investors’ mood swings in the later months. The Index actually reached a new peak on September 19, but by October 16 fell 8%. From there the Index rebounded 12% to December 5, fell 5% to December 16 then rose 11% to March 20, before ending the fiscal year 1.7% below its all-time high.

In U.S. fixed income markets, the Barclays Long-Term U.S. Treasury sub-index returned a remarkable 21.40% over the fiscal year; the Barclays U.S. Treasury Bond sub-index just 5.36% as the Treasury yield curve flattened. The Barclays U.S. Aggregate Bond Index (“Barclays Aggregate”) added 5.72%, while the Barclays U.S. Corporate Investment Grade Bond sub-index gained 6.81%. Both outperformed the Barclays High Yield Bond — 2% Issuer Constrained Composite Index (not a part of the Barclays Aggregate), which returned only 2.00%, reflecting the significant representation of the ailing energy industry and perhaps a pull-back after strong returns in recent years.

U.S. equities, represented by the S&P 500® Index including dividends, advanced 12.73% in the fiscal year, completing nine consecutive winning quarters, the best run since 1998. The health care sector was the top performer, returning 26.19%; not surprisingly, the only loser was energy, which dropped 11.11% as oil prices sagged. Record operating earnings per share for S&P 500® companies in the second and third quarters were supported by low interest rates, slow wage growth and historically high share buy-back volumes. Operating margins breached 10% for the first time. Both retreated in the last quarter.

In currencies, the dollar gained ground against most other currencies, surging 28.31% against the euro, as the U.S. ended quantitative easing just as the ECB embarked on it and 16.37% against the yen, on the likelihood of further monetary easing in Japan and an announced partial re-allocation into stocks (including non-yen) for the giant Government Pension Investment Fund (“GPIF”). The dollar gained less, 12.44%, on the pound. The UK had a better growth story than the euro zone, which however is the destination for about 40% of the UK’s exports.

In international markets, the MSCI Japan® Index leaped 30.49% in the fiscal year, boosted in the case of Japan’s large exporters by the falling yen, by continued quantitative easing and by the GPIF’s announcement described above. The MSCI Europe ex UK® Index added 18.85%. The poor economic data were ultimately trumped by the prospect of quantitative easing, plus the declining euro that went with it. The MSCI UK® Index was much weaker, edging up 6.11%. Nearly half of this index is comprised of 15 names, mostly global banking, energy, pharmaceuticals and materials companies, not particularly representative of an improving economy, and which on average returned barely 1%.

Past performance does not guarantee future results. The performance quoted represents past performance.

Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. Each Fund’s performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.voyainvestments.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of Voya Investment Management’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

Benchmark Descriptions

| | | Index | | | | Description | | |

| | | Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index | | | | The Index is designed to track the performance of a synthetic asset paying LIBOR to a stated maturity. The index is based on the assumed purchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. That issue is assumed to be sold the following business day (priced at a yield equal to the current day rate) and rolled into a new instrument. | | |

| | | Barclays GNMA Index | | | | An unmanaged index comprised of all fixed security mortgage pools sponsored by GNMA, including GNMA Graduated Payment Mortgages. | | |

| | | Barclays High Yield Bond — 2% Issuer Constrained Composite Index | | | | An unmanaged index that includes all fixed income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | | |

| | | Barclays Long-Term U.S. Treasury Index | | | | The Index includes all publicly issued, U.S. Treasury securities that have a remaining maturity of 10 or more years, are rated investment grade, and have $250 million or more of outstanding face value. | | |

| | | Barclays U.S. 1-3 Year Government / Credit Bond Index | | | | A widely recognized index of publicly issued fixed rate, investment grade debt securities, including Treasuries, Agencies and credit securities with a maturity of one to three years. | | |

| | | Barclays U.S. Aggregate Bond Index | | | | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | | |

| | | Barclays U.S. Corporate Investment Grade Bond Index | | | | An unmanaged index consisting of publicly issued, fixed rate, nonconvertible, investment grade debt securities. | | |

| | | Barclays U.S. Treasury Bond Index | | | | A market capitalization-weighted index that measures the performance of public obligations of the U.S. Treasury that have a remaining maturity of one year or more. | | |

| | | Barclays U.S. Universal Bond Index | | | | The Index represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index. The index covers USD-denominated, taxable bonds that are rated either investment grade or high-yield. Some U.S. Universal Index constituents may be eligible for one or more of its contributing subcomponents that are not mutually exclusive. These securities are not double-counted in the index. The U.S. Universal index was created on January 1, 1999, with index history backfilled to January 1, 1990. | | |

| | | MSCI Europe ex UK® Index | | | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | | |

| | | MSCI Japan® Index | | | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan. | | |

| | | MSCI UK® Index | | | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | | |

| | | MSCI World IndexSM | | | | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | | |

| | | S&P 500® Index | | | | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | | |

| | | S&P/Case-Shiller 20-City Composite Home Price Index | | | | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor’s. | | |

| Voya GNMA Income Fund | Portfolio Managers’ Report |

| | | |

| | Investment Type Allocation as of March 31, 2015 (as a percentage of net assets) | |

| | | | | | |

| | U.S. Government Agency Obligations | | | 112.0% | |

| | Collateralized Mortgage Obligations | | | 0.2% | |

| | Liabilities in Excess of Other Assets* | | | (12.2)% | |

| | Net Assets | | | 100.0% | |

| | | |

| | * Includes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Voya GNMA Income Fund (the “Fund”) seeks a high level of current income consistent with liquidity and safety of principal through investment primarily in Government National Mortgage Association (“GNMA”) mortgage-backed securities (also known as GNMA Certificates) that are guaranteed as to the timely payment of principal and interest by the U.S. government. The Fund is managed by Peter Guan, Jeff Dutra and Justin McWhorter, Portfolio Managers of Voya Investment Management Co. LLC — the Sub-Adviser.

Securities issued by the U.S. Treasury are backed by the full faith and credit of the federal government. Securities issued by individual agencies and organizations may be backed by the full faith and credit of the federal government as to principal or interest but are not direct obligations of the U.S. Treasury. Securities of some agencies and organizations are backed solely by the entity’s own resources or by the ability of the entity to borrow from the U.S. Treasury. Government securities also include certain mortgage-related securities that are sponsored by a U.S. government agency or organization and are not direct obligations of the U.S. government.

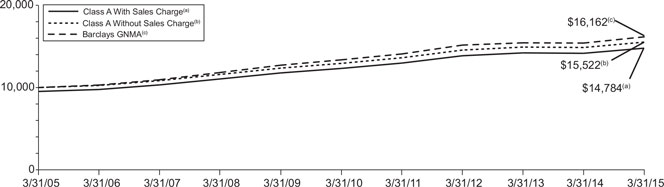

Performance: For the year ended March 31, 2015, the Fund���s Class A shares, excluding sales charges, provided a total return of 4.40%, compared to the Barclays GNMA Index (the “Index” or “Barclays GNMA”), which returned 4.91%, for the same period.

Portfolio Specifics: The first two quarters of the fiscal year were characterized by continued Federal Reserve Board (“Fed”) purchases of agency mortgages and low rate volatility. In response, bond markets performed very well as interest rates decreased due to what we believed were growing concerns about global economic growth and geopolitical instability. By the end of its large scale asset purchase program in October 2014, the Fed owned $1.7 trillion in agency mortgages, accounting for a third of all outstanding mortgage-backed securities (“MBS”). Given this overwhelming technical factor combined with low net supply, “spreads” on agency mortgages tightened throughout 2014 and ended the first three quarters of the fiscal year with 0.64% of excess return. (The “spread” is the yield premium between a bond that entails some credit risk, such as a mortgage-backed bond, and a U.S. Treasury bond of equivalent maturity. Investors demand the spread premium as compensation for taking on the credit risk.) Volatility increased in 2015 as rates plunged in January, rebounded in February, and then fell again in March. The increase in volatility and lower Fed support for mortgages resulted in 0.51% of underperformance of agency MBS relative to Treasuries in the first quarter of 2015.

The Fund outperformed the Index before fees and expenses, but underperformed net of fees during the period. Performance was dampened as the Fund maintained a slight underweight in duration, or interest-rate risk, versus the benchmark throughout the year. Nonetheless, increased exposure to Fannie Mae and Freddie Mac mortgage securities boosted performance as GNMA backed bonds lagged their conventional counterparts. Also, prepayment-protected collateral in the form of pools and collateralized mortgage obligations (“CMOs”) continued to provide positive “carry” versus the Index in volatile markets. (“Carry” is a strategy of holding two offsetting positions, one of which creates an incoming cash flow that is greater than the obligations of the other.)

Additional outperformance was achieved through participation in “dollar rolls”. The dollar roll market is a very large and well developed one, in which MBS are bought and sold again in monthly cycles. The terms on which this is done can be more cost effective than simply holding comparable MBS. This was the case from time to time during the fiscal year.

Current Strategy & Outlook: As the annual period concludes, MBS performance has been mixed versus equal-duration U.S. Treasury securities. In our opinion, due to policy changes handed down by the Federal Housing Administration during the first quarter of 2015, GNMA MBS continued to lag their conventional counterparts, as refinancing activity increased substantially in 2015. Although valuations throughout the coupon stack remain at tight option-adjusted spread levels, lower coupons provide better protection from the current rate environment and from the trend of credit-widening policies from the government. Furthermore, despite the conclusion of Fed balance sheet expansion, the Fed continues to reinvest principal payments on its current holdings. We believe this activity maintains a backstop for agency MBS demand and has helped keep spreads anchored near current levels.

With this in mind, we continue to manage the Fund seeking high current income investments while seeking to modestly reduce interest rate and basis risk. The focus remains on specified GNMA pools and CMOs that provide more attractive current income while seeking to minimize prepayment risks. Moreover, we are reducing exposure to cohorts with higher risk of prepayments either due to the low rate environment or government policy.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions. Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| Portfolio Managers’ Report | Voya GNMA Income Fund |

| | | Average Annual Total Returns for the Periods Ended March 31, 2015 | | |

| | | | | | 1 Year | | | 5 Year | | | 10 Year | | | Since Inception of Class W December 17, 2007 | | |

| | | Including Sales Charge: | | | | | | |

| | | Class A(1) | | | | | 1.80% | | | | | | 3.20% | | | | | | 4.00% | | | | | | — | | | |

| | | Class B(2) | | | | | -1.38% | | | | | | 2.58% | | | | | | 3.72% | | | | | | — | | | |

| | | Class C(3) | | | | | 2.62% | | | | | | 2.93% | | | | | | 3.72% | | | | | | — | | | |

| | | Class I | | | | | 4.70% | | | | | | 4.00% | | | | | | 4.80% | | | | | | — | | | |

| | | Class W | | | | | 4.66% | | | | | | 3.96% | | | | | | — | | | | | | 4.80% | | | |

| | | Excluding Sales Charge: | | | | | | |

| | | Class A | | | | | 4.40% | | | | | | 3.71% | | | | | | 4.50% | | | | | | — | | | |

| | | Class B | | | | | 3.62% | | | | | | 2.93% | | | | | | 3.72% | | | | | | — | | | |

| | | Class C | | | | | 3.62% | | | | | | 2.93% | | | | | | 3.72% | | | | | | — | | | |

| | | Class I | | | | | 4.70% | | | | | | 4.00% | | | | | | 4.80% | | | | | | — | | | |

| | | Class W | | | | | 4.66% | | | | | | 3.96% | | | | | | — | | | | | | 4.80% | | | |

| | | Barclays GNMA | | | | | 4.91% | | | | | | 3.87% | | | | | | 4.92% | | | | | | 4.86% | | | |

| | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya GNMA Income Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| Voya High Yield Bond Fund | Portfolio Managers’ Report |

| | | |

| | Sector Diversification as of March 31, 2015 (as a percentage of net assets) | |

| | | | | | |

| | Consumer, Non-cyclical | | | 21.9% | |

| | Communications | | | 17.4% | |

| | Consumer, Cyclical | | | 16.3% | |

| | Energy | | | 11.2% | |

| | Industrials | | | 7.7% | |

| | Financials | | | 6.3% | |

| | Technology | | | 6.0% | |

| | Basic Materials | | | 5.9% | |

| | Utilities | | | 1.8% | |

| | Diversified | | | 1.4% | |

| | Telecommunication Services | | | 0.3% | |

| | Other Asset-Backed Securities | | | 0.2% | |

| | Information Technology | | | 0.2% | |

| | Consumer Discretionary | | | 0.0% | |

| | Assets in Excess of Other Liabilities* | | | 3.4% | |

| | Net Assets | | | 100.0% | |

| | | | | | |

| | * Includes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Voya High Yield Bond Fund (the “Fund”) seeks to provide investors with a high level of current income and total return. The Fund is managed by Randall Parrish, CFA, Matthew Toms, CFA, and Rick Cumberledge, CFA, Portfolio Managers of Voya Investment Management Co. LLC — the Sub-Adviser.

Performance: For the year ended March 31, 2015, the Fund’s Class A shares, excluding sales charges, provided a total return of 0.98%, compared to the Barclays High Yield Bond — 2% Issuer Constrained Composite Index (the “Index” or “Barclays High Yield Bond — 2% Issuer Constrained Composite”), which returned 2.00%, for the same period.

Portfolio Specifics: A year ago, the ten-year Treasury yield of 2.73% reflected investor expectation of an imminent Federal Reserve Board rate hiking cycle, oil prices above $100 per barrel that gave evidence of emerging market growth and a multi-year run in the S&P 500® Index reflected the continued rebound of the U.S. economy from the Great Recession. What a difference a year makes. The 10-year Treasury yield is now nearly 100 basis points (“bp”) lower, oil is down by more than half and volatility has spiked dramatically in recent months. (A bp equals one one-hundredth of one percent.) Equities did manage a double-digit return over the reporting period, although that was likely driven more by the expectation of continued low rates than by strong earnings growth. The high yield market started off strong, with the market yield hitting an all-time low of 4.83% in June 2014, but ultimately succumbed to concerns about valuations (July), U.S. economic growth (September/October) and oil prices (December), with the most dramatic adjustment the oil-driven one, reflecting the fact that the proportion of energy-related debt in the high yield market had increased dramatically in recent years.

| | | |

| | Top Ten Holdings

as of March 31, 2015*

(as a percentage of net assets) | |

| | | | | | |

| | HCA Holdings, Inc., 6.250%, 02/15/21 | | | 0.6% | |

| | AerCap Ireland Capital Ltd. / AerCap Global Aviation Trust, 4.500%, 05/15/21 | | | 0.6% | |

| | Sprint Corp., 7.125%, 06/15/24 | | | 0.5% | |

| | Ashtead Capital, Inc., 6.500%, 07/15/22 | | | 0.5% | |

| | Univision Communications, Inc., 5.125%, 05/15/23 | | | 0.5% | |

| | Numericable Group SA, 6.250%, 05/15/24 | | | 0.5% | |

| | Parsley Energy LLC / Parsley Finance Corp., 7.500%, 02/15/22 | | | 0.5% | |

| | Hot Topic, Inc., 9.250%, 06/15/21 | | | 0.5% | |

| | Chesapeake Energy Corp., 6.125%, 02/15/21 | | | 0.5% | |

| | First Data Corp., 11.750%, 08/15/21 | | | 0.4% | |

| | | |

| | * Excludes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

The Barclays U.S. High Yield 2% Issuer Constrained Index (“Index”) posted a return of 2.00% for the 12 months ended March 31, 2015, underperforming the return of like-duration Treasuries by 202 bp as spreads widened. The index yield to worst — the lowest potential yield that can be received on the bonds that comprise the index, without an issuer actually defaulting — rose by 0.95% to 6.18% at March 31, 2015, as the spread to Treasuries widened 109 bp to T+5.01%. The total market return was dragged down by the energy (-8.5%) and metals & mining (-5.8%) sectors, reflecting the sharp sell-off in global commodities. Excluding the energy sector, the Index returned 3.9% for the 12 month reporting period, roughly keeping pace with Treasuries. Higher quality outperformed lower quality, with BB-rated bonds returning 4.9% versus a loss of 2.4% for CCC-rated securities. This reflected both general investor caution and the heavier weighting of lower-quality energy companies most exposed to the decline in oil prices. The Index’s par-weighted default rate of 3.0% reflected the large defaults of Energy Future Holdings Corp. (the former TXU Corp.) and Caesars Entertainment Resort Properties LLC, but default activity remained well below historical averages at just 1.7% on an issuer-weighted basis, per JPMorgan.

The Fund outperformed its Index before fees and expenses, but underperformed net of fees during the period. The detractors for the period largely reflected our (ultimately unfounded) desire to avoid significant exposure to potentially rising interest rates. We were underweight long-dated subordinated securities issued by large banks that traded up in price as rates moved lower, as well as higher-quality utilities that also benefited from lower rates. Despite our long-held overweight to independent domestic energy producers and the fourth quarter 2014 sell-off in oil, the energy sector was a net positive contributor to relative performance for the reporting period, as we generally limited our exposure to low-cost operators in the best basins and those who had hedged forward production. We also largely avoided oil service companies. We did exit some holdings with weaker balance sheets (Energy XXI Ltd. and Halcon Resources Corp.) as we became increasingly convinced that oil prices would stay lower for longer than originally anticipated. Our favored companies (Memorial Production Partners L.P., Parsley Energy LLC and Sanchez Energy Corp.) held up reasonably well, while we successfully avoided the bonds of companies that are likely restructuring candidates (Samson Technologies, Quicksilver Resources, Inc. and Sabine Oil & Gas). Outside energy, positive contribution came from our underweight to metals & mining and select issuers within retailing (Hot Topic, Inc., Dollar Tree, Inc. and Murphy Oil USA, Inc.).

| Portfolio Managers’ Report | Voya High Yield Bond Fund |

Current Strategy & Outlook: Our fundamental view of high yield credit quality is largely unchanged. Though we acknowledge the weaker U.S. economic data of late and the potential for further fundamental deterioration in the energy space, we continue to believe that the economy will show improvement with the arrival of spring and that the next broad default cycle is still some distance down the road. We believe the above concerns, combined with weakness in China and global geopolitical risk, justify wider spreads than we saw at the 2014 post-crisis tights, but with ex-energy high yield spreads above their long term average at more than 450 bp above U.S Treasury securities, it seems that high yield investors are being more than adequately compensated for credit risk taken. We believe at current levels, high yield bonds may have the ability to absorb at least a portion of an eventual rise in interest rates. In our opinion, this environment should position high yield to outperform most other fixed income asset classes over the coming year.

We believe the portfolio is well positioned for the environment described above. In keeping with our view of U.S. economic recovery and continuing solid credit fundamentals, we maintain our slight domestic-focused cyclical bias and an overweight to single-B profile credits (underweight BBs and what we view as the most at-risk securities of those rated CCC and below). We remain underweight the most commodity price-sensitive sectors such as metals and mining and oilfield services; the sectors we are overweight include those that benefit from lower energy costs (chemicals) and from increased consumer discretionary income (retailers).

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions. Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| Voya High Yield Bond Fund | Portfolio Managers’ Report |

| | | Average Annual Total Returns for the Periods Ended March 31, 2015 | | |

| | | | | | 1 Year | | | 5 Year | | | 10 Year | | | Since Inception

of Class I

July 31, 2008 | | | Since Inception

of Class P

June 14, 2013 | | | Since Inception

of Class R

January 30, 2014 | | | Since Inception

of Class W

July 29, 2011 | | |

| | | Including Sales Charge: | | | | | | | |

| | | Class A(1) | | | | | -1.57% | | | | | | 7.96% | | | | | | 6.15% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class B(2) | | | | | -4.49% | | | | | | 7.41% | | | | | | 5.88% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class C(3) | | | | | -0.75% | | | | | | 7.70% | | | | | | 5.87% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class I | | | | | 1.48% | | | | | | 8.99% | | | | | | — | | | | | | 9.29% | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class P | | | | | 2.09% | | | | | | — | | | | | | — | | | | | | — | | | | | | 5.81% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | 0.91% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | 2.64% | | | | | | — | | | |

| | | Class W | | | | | 1.26% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | 7.79% | | | |

| | | Excluding Sales Charge: | | | | | | | |

| | | Class A | | | | | 0.98% | | | | | | 8.51% | | | | | | 6.67% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class B | | | | | 0.31% | | | | | | 7.71% | | | | | | 5.88% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | | Class C | | | | | 0.21% | | | | | | 7.70% | | | | | | 5.87% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | |

| | Class I | | | | | 1.48% | | | | | | 8.99% | | | | | | — | | | | | | 9.29% | | | | | | — | | | | | | — | | | | |

| | | Class P | | | | | 2.09% | | | | | | — | | | | | | — | | | | | | — | | | | | | 5.81% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | 0.91% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | 2.64% | | | | | | — | | | |

| | | Class W | | | | | 1.26% | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | 7.79% | | | |

| | | Barclays High Yield Bond – 2% Issuer Constrained Composite | | | | | 2.00% | | | | | | 8.56% | | | | | | 8.17% | | | | | | 10.10% | | | | | | 5.32% | | | | | | 3.63% | | | | | | 7.22% | | | |

| | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya High Yield Bond Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/ or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data

shown. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| Portfolio Managers’ Report | Voya Intermediate Bond Fund |

| | | |

| | Investment Type Allocation as of March 31, 2015 (as a percentage of net assets) | |

| | | | | | |

| | Corporate Bonds/Notes | | | 33.2% | |

| | U.S. Treasury Obligations | | | 28.5% | |

| | U.S. Government Agency Obligations | | | 25.4% | |

| | Collateralized Mortgage Obligations | | | 11.6% | |

| | Asset-Backed Securities | | | 7.5% | |

| | Foreign Government Bonds | | | 1.4% | |

| | Purchased Options | | | 0.0% | |

| | Liabilities in Excess of Other Assets* | | | (7.6)% | |

| | Net Assets | | | 100.0% | |

| | | |

| | * Includes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Voya Intermediate Bond Fund (the “Fund”) seeks to maximize total return through income and capital appreciation. The Fund is managed by Christine Hurtsellers, CFA, and Matthew Toms, CFA, Portfolio Managers of Voya Investment Management Co. LLC — the Sub-Adviser.

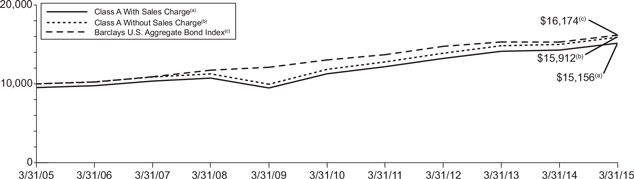

Performance: For the year ended March 31, 2015, the Fund’s Class A shares, excluding sales charges, provided a total return of 6.09% compared to the Barclays U.S. Aggregate Bond Index, which returned 5.72% for the same period.

Portfolio Specifics: For the reporting period, the Fund outperformed its benchmark, the Barclays U.S. Aggregate Bond Index, due to security selection and asset allocation. Security selection was generally additive. Securitized assets helped results, particularly within commercial mortgage-backed securities and asset-backed securities. The risk appetite in the search for yield remained robust and underlying fundamentals provided a supportive backdrop. Issue selection among agency mortgages contributed to performance even though at times we were less constructive on the agency mortgages sector, which we expect will continue to trade directionally with interest rates. Investment grade credit security selection was a drag even though corporate revenue and earnings growth remained fairly stable during the period.

Holding off-benchmark allocations to non-agency mortgages was beneficial. We remained constructive on non-agency mortgage-backed securities, as the housing market continued its recovery and credit access continued to improve across borrower types. The Fund's overweight in high-yield corporate bonds, and its underweight of U.S. Treasury securities, were less favorable to relative results. In our view, high yield fundamentals generally remained in good shape, and the risk of a near-term default spike remained very low. Sector allocation and security selection within the emerging markets contributed to results for the period. The European Central Bank's (“ECB”) asset purchases, as part of its quantitative easing program, increased the attractiveness of yields across emerging markets. In our opinion, it was crucial, however, to be selective about countries and sectors within the asset class and to manage overall volatility.

Duration and yield curve detracted from results for the period. The Fund started the period with a slightly shorter duration and ended close to that of the benchmark’s duration. During the period, the Fund used swaps, options and futures in conjunction with cash bonds to manage interest-rate risk and yield-curve risk. Swaps and options were employed to aid in managing sector allocation and security selection. The Fund used exchange-traded credit default index swaps, such as CDX and iTraxx, to hedge corporate credit exposures. In sum, these investment decisions — i.e., to hold positions in derivative instruments and cash securities — detracted from Fund results over the reporting period.

| | | |

| | Top Ten Holdings

as of March 31, 2015*

(as a percentage of net assets) | |

| | | | | | |

| | United States Treasury Note, 1.000%, 03/15/18 | | | 7.4% | |

| | United States Treasury Note, 0.500%, 03/31/17 | | | 6.5% | |

| | United States Treasury Bond, 2.000%, 02/15/25 | | | 5.4% | |

| | United States Treasury Bond, 3.000%, 11/15/44 | | | 4.0% | |

| | Fannie Mae, 3.000%, 05/01/43 | | | 3.3% | |

| | Freddie Mac, 3.500%, 09/15/41 | | | 3.1% | |

| | United States Treasury Note, 1.750%, 03/31/22 | | | 2.4% | |

| | Freddie Mac, 3.000%, 05/01/43 | | | 1.7% | |

| | Fannie Mae, 2.500%, 11/25/26 | | | 1.5% | |

| | United States Treasury Note, 1.375%, 03/31/20 | | | 1.5% | |

| | | |

| | * Excludes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Current Strategy & Outlook: We believe the removal of “patient” from the Federal Reserve Board’s (“Fed’s”) latest announcement implies a shift in policy could happen in 2015. With forward guidance gone and the emphasis squarely on the economy, we believe the message is clear: the Fed will not be impatient about raising rates. Job growth alone likely isn’t enough to offset the weak global growth forecast. On the other hand, a weaker euro and quantitative easing by the ECB are reviving growth prospects in Europe. Keeping Fed policy on hold allows more time for U.S. labor market improvement to percolate into other areas of the economy. Low commodity prices and a strong U.S. dollar restrain inflation and are also positive tailwinds for consumers.

We believe supportive policy globally will help smooth over economic and seasonal noise. With a quiescent Fed for now, we will likely maintain an overweight to investment grade corporate bonds, which we expect to benefit from the strength and stability of the U.S. economy and from capital seeking more attractive yield than can be found elsewhere. We believe rates are likely to be range-bound and interest rate volatility is likely to decline in the near term. Low short-term interest rates, an elevated Fed balance sheet, low long-term rates in major developed countries, quantitative easing overseas, strong demand for safe assets and disappointments in growth in advanced countries are conspiring to keep long-term interest rates low. If clearer signs emerge that the economy is heating up, we believe we could see rising volatility and rising interest rates later this year.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions. Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| Voya Intermediate Bond Fund | Portfolio Managers’ Report |

| | | Average Annual Total Returns for the Periods Ended March 31, 2015 | | |

| | | | | | 1 Year | | | 5 Year | | | 10 Year | | | Since

Inception

of Class R6

May 31,

2013 | | | Since

Inception

of Class W

December 17,

2007 | | |

| | | Including Sales Charge: | | | | | | | |

| | | Class A(1) | | | | | 3.47% | | | | | | 5.55% | | | | | | 4.25% | | | | | | — | | | | | | — | | | |

| | | Class B(2) | | | | | 0.17% | | | | | | 4.96% | | | | | | 3.96% | | | | | | — | | | | | | — | | | |

| | | Class C(3) | | | | | 4.21% | | | | | | 5.28% | | | | | | 3.96% | | | | | | — | | | | | | — | | | |

| | | Class I | | | | | 6.46% | | | | | | 6.43% | | | | | | 5.09% | | | | | | — | | | | | | — | | | |

| | | Class O | | | | | 6.01% | | | | | | 6.07% | | | | | | 4.75% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | 5.71% | | | | | | 5.83% | | | | | | 4.48% | | | | | | — | | | | | | — | | | |

| | | Class R6 | | | | | 6.38% | | | | | | — | | | | | | — | | | | | | 4.37% | | | | | | — | | | |

| | | Class W | | | | | 6.36% | | | | | | 6.61% | | | | | | — | | | | | | — | | | | | | 5.47% | | | |

| | | Excluding Sales Charge: | | | | | | | | | | | | |

| | | Class A | | | | | 6.09% | | | | | | 6.09% | | | | | | 4.75% | | | | | | — | | | | | | — | | | |

| | | Class B | | | | | 5.17% | | | | | | 5.29% | | | | | | 3.96% | | | | | | — | | | | | | — | | | |

| | | Class C | | | | | 5.21% | | | | | | 5.28% | | | | | | 3.96% | | | | | | — | | | | | | — | | | |

| | | Class I | | | | | 6.46% | | | | | | 6.43% | | | | | | 5.09% | | | | | | — | | | | | | — | | | |

| | | Class O | | | | | 6.01% | | | | | | 6.07% | | | | | | 4.75% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | 5.71% | | | | | | 5.83% | | | | | | 4.48% | | | | | | — | | | | | | — | | | |

| | | Class R6 | | | | | 6.38% | | | | | | — | | | | | | — | | | | | | 4.37% | | | | |

| | | Class W | | | | | 6.36% | | | | | | 6.61% | | | | | | — | | | | | | — | | | | | | 5.47% | | | |

| | | Barclays U.S. Aggregate Bond Index | | | | | 5.72% | | | | | | 4.41% | | | | | | 4.93% | | | | | | 3.47% | | | | | | 4.96% | | | |

| | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya Intermediate Bond Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data

shown. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 4.75%. Effective July 31, 2006, the maximum Class A sales charge was lowered to 2.50%. |

| (2) | Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively. |

| (3) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| Portfolio Managers’ Report | Voya Short Term Bond Fund |

| | | |

| | Investment Type Allocation as of March 31, 2015 (as a percentage of net assets) | |

| | | | | | |

| | Corporate Bonds/Notes | | | 58.7% | |

| | Asset-Backed Securities | | | 18.0% | |

| | Collateralized Mortgage Obligations | | | 10.7% | |

| | U.S. Government Agency Obligations | | | 7.6% | |

| | U.S. Treasury Obligations | | | 3.8% | |

| | Purchased Options | | | 0.0% | |

| | Assets in Excess of Other Liabilities* | | | 1.2% | |

| | Net Assets | | | 100.0% | |

| | | |

| | * Includes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Voya Short Term Bond Fund (the “Fund”) seeks maximum total return. The Fund is managed by Christine Hurtsellers, CFA, and Matthew Toms, CFA, Portfolio Managers of Voya Investment Management Co. LLC — the Sub-Adviser.

Performance: For the year ended March 31, 2015, the Fund’s Class I shares, excluding sales charges, provided a total return of 1.50% compared to the Barclays U.S. 1-3 Year Government/Credit Bond Index (the “Index” or “Barclays U.S. 1-3 Year Government/Credit Bond”), which returned 1.12%, for the same period.

Portfolio Specifics: The Fund outperformed its benchmark for the reporting period; sector allocation was the main driver of results. Duration/yield curve positioning and security selection detracted from results for the period.

An overweighting in asset-backed securities was the most important contributor to return. An overweight to commercial mortgage-backed securities also contributed to relative results. An overweight of high yield corporate bonds also contributed, as did an overweight of investment grade corporate bonds.

During the first half of the reporting period the Fund’s duration, or interest rate risk exposure, was shorter than the benchmark; during the second half of the period, it was neutral. This positioning detracted from results for the period. Toward period-end, the Fund’s yield decreased as short-term rates decreased and spreads moved slightly tighter. At the end of the period duration was neutral versus the benchmark.

Security selection detracted the most among investment grade corporates, partially offsetting the benefit of our overweight in that sector. In addition, off-benchmark allocations to high yield corporates benefited performance.

Current Strategy & Outlook: Punxsutawney Phil won’t be adding “economic soothsayer” to his resume this year. The prescient marmot saw his shadow on Groundhog Day, which typically prognosticates six more weeks of winter. But if the latest U.S. Federal Reserve Board (“Fed”) announcement was any barometer of the economic climate, we believe it would be superstitious to believe in a spring of interest rates anytime soon.

| | | |

| | Top Ten Holdings

as of March 31, 2015*

(as a percentage of net assets) | |

| | | | | | |

| | United States Treasury Note, 0.375%, 03/31/16 | | | 2.9% | |

| | Ginnie Mae, 7.120%, 04/20/39 | | | 1.1% | |

| | LB-UBS Commercial Mortgage Trust, 5.127%, 09/15/40 | | | 0.8% | |

| | Freddie Mac, 6.000%, 12/15/28 | | | 0.9% | |

| | Bank of America Corp., 2.600%, 01/15/19 | | | 0.8% | |

| | Freddie Mac, 5.000%, 07/15/39 | | | 0.8% | |

| | Muir Grove CLO Ltd., 3.256%, 03/25/20 | | | 0.7% | |

| | Barclays Bank PLC, 5.000%, 09/22/16 | | | 0.6% | |

| | BB&T Corp., 1.600%, 08/15/17 | | | 0.6% | |

| | Freddie Mac, 5.500%, 11/01/38 | | | 0.6% | |

| | | |

| | * Excludes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

While the improving labor market points to sunnier days ahead, the Fed’s dovish tone suggests that job growth is being overshadowed by the realities of low wage inflation, a strong dollar and collapsing oil prices. And though snowy weather was partially to blame for housing starts falling in February, the decline was the largest in four years — evidence that the housing market is cooling off.

We believe the removal of “patient” from the Fed’s latest announcement implies a shift in policy could happen in 2015. With forward guidance gone and the emphasis squarely on the economy, we believe the message is clear: the Fed will not be impatient about raising rates. Job growth alone likely isn’t enough to offset the weak global growth forecast. On the other hand, a weaker euro and quantitative easing by the European Central Bank are reviving growth prospects in Europe. Keeping Fed policy on hold allows more time for U.S. labor market improvement to percolate into other areas of the economy. Low commodity prices and a strong dollar restrain inflation and are also positive tailwinds for consumers.

We believe supportive policy globally will help smooth over economic and seasonal noise. With a quiescent Fed for now, we will likely maintain our bias for U.S. dollar-denominated spread sectors, which we expect to benefit from the strength and stability of the U.S. economy and from capital seeking more attractive yield than can be found elsewhere. We believe rates are likely to be range-bound and interest rate volatility is likely to decline in the near term. If clearer signs emerge that the economy is heating up, we believe we could see rising volatility and a spring of interest rates later this year.

Leverage has been on the rise in recent quarters. In our opinion, corporate revenue and earnings growth have remained fairly stable for the past few years. However, we do not see an inflection point on the horizon for the credit cycle. Excluding metals and energy, corporate spreads have moved back into the range of their cycle lows, but flows have been positive and we believe demand remains sound despite heavy issuance.

Though changes in Fed language are a concern, above-trend growth in the U.S. and low inflation expectations in Europe lead us to believe that domestic corporates are attractive and able to generate positive excess returns.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| Voya Short Term Bond Fund | Portfolio Managers’ Report |

| | | Average Annual Total Returns for the Periods Ended March 31, 2015 | | |

| | | | | | 1 Year | | | Since Inception of Classes A, C, I, and W December 19, 2012 | | | Since Inception of Class R July 31, 2014 | | | Since Inception of Class R6 July 31, 2013 | | |

| | | Including Sales Charge: | | | | | | |

| | | Class A(1) | | | | | -1.36% | | | | | | 0.07% | | | | | | — | | | | | | — | | | |

| | | Class C(2) | | | | | -0.56% | | | | | | 0.47% | | | | | | — | | | | | | — | | | |

| | | Class I | | | | | 1.50% | | | | | | 1.51% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | — | | | | | | — | | | | | | 0.72% | | | | | | — | | | |

| | | Class R6 | | | | | 1.53% | | | | | | — | | | | | | — | | | | | | 1.81% | | | |

| | | Class W | | | | | 1.41% | | | | | | 1.43% | | | | | | — | | | | | | — | | | |

| | | Excluding Sales Charge: | | | | | | |

| | | Class A | | | | | 1.20% | | | | | | 1.20% | | | | | | — | | | | | | — | | | |

| | | Class C | | | | | 0.44% | | | | | | 0.47% | | | | | | — | | | | | | — | | | |

| | | Class I | | | | | 1.50% | | | | | | 1.51% | | | | | | — | | | | | | — | | | |

| | | Class R | | | | | — | | | | | | — | | | | | | 0.72% | | | | | | — | | | |

| | | Class R6 | | | | | 1.53% | | | | | | — | | | | | | — | | | | | | 1.81% | | | |

| | | Class W | | | | | 1.41% | | | | | | 1.43% | | | | | | — | | | | | | — | | | |

| | | Barclays U.S. 1-3 Year Government/Credit Bond | | | | | 1.12% | | | | | | 0.90% | | | | | | 0.86% | | | | | | 1.03% | | | |

| | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya Short Term Bond Fund against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current

performance may be lower or higher than the performance data shown. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 2.50%. |

| (2) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

| Portfolio Managers’ Report | Voya Strategic Income Opportunities Fund |

| | | |

| | Investment Type Allocation as of March 31, 2015 (as a percentage of net assets) | |

| | | | | | |

| | Mutual Funds | | | 71.0% | |

| | U.S. Government Agency Obligations | | | 13.2% | |

| | Collateralized Mortgage Obligations | | | 8.4% | |

| | U.S. Treasury Obligations | | | 3.3% | |

| | Corporate Bonds/Notes | | | 1.5% | |

| | Assets in Excess of Other Liabilities* | | | 2.6% | |

| | Net Assets | | | 100.0% | |

| | | |

| | * Includes short-term investments. | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

Voya Strategic Income Opportunities Fund* (the “Fund”) seeks total return through income and capital appreciation through all market cycles. The Fund is managed by Christine Hurtsellers, CFA, and Matthew Toms, CFA, Portfolio Managers of Voya Investment Management Co. LLC — the Sub-Adviser.

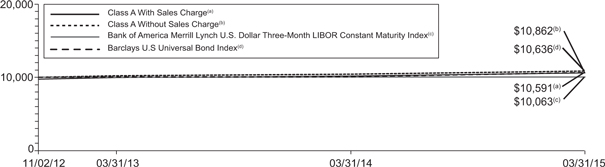

Performance: For the year ended March 31, 2015, the Fund’s Class A shares, excluding sales charges, provided a total return of 3.97% compared to the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index** (the “Index” or Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity”), which returned 0.23%, for the same period.

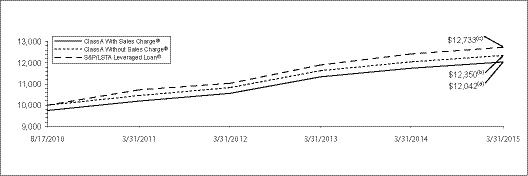

Portfolio Specifics: The Fund outperformed its benchmark during the reporting period. The main contributors to results were the Fund’s overweight of senior loans and high yield bonds, security selection in commercial mortgage-backed securities and residential mortgage-backed securities and the Fund’s duration, or sensitivity to interest-rate changes.

Senior loans performed relatively well during the period, and the Fund’s significant overweight of them was the most important contributor to relative results. In our view, senior loans represent an attractive income opportunity with little interest-rate risk. Because the interest rates that senior loans pay “float,” i.e., are reset at regular, short intervals, there is little chance that loan interest payments will get significantly out of line with market rates. This in turn implies a low likelihood that the prices of senior loans will have to be reduced to compensate for higher market rates. As we head towards eventual rate hikes from the U.S. Federal Reserve Board (“Fed”) and higher market rates, we believe senior loans will continue to offer attractive benefits to investors. Tumult in the energy industry as oil prices fell caused many investors to worry about a spike of defaults in the high yield sector, which contains a fairly high percentage of energy issuers. A default spike did not arise, however; and so without significant, adverse market effects the Fund was able to benefit from the income generated by its high-yield bond holdings. As interest rates fell significantly during the period, the Fund was able to benefit from its slightly longer duration posture versus that of the benchmark. The Fund’s allocation to mortgage-related investments contributed to performance as prepayment speeds increased less than the market feared. Markets subsequently rallied, which caused the Fund’s mortgage valuations to increase, further contributing to performance.

| | | |

| | Top Ten Holdings

as of March 31, 2015

(as a percentage of net assets) | |

| | | | | | |

| | Voya Floating Rate Fund - Class P | | | 28.7% | |

| | Voya High Yield Bond Fund - Class P | | | 18.9% | |

| | Voya Securitized Credit Fund - Class P | | | 14.7% | |

| | Fannie Mae Connecticut Avenue Securities, 5.174%, 11/25/24 | | | 4.5% | |

| | Voya Investment Grade Credit Fund - Class P | | | 4.0% | |

| | Freddie Mac, 6.500%, 06/15/32 | | | 3.0% | |

| | Fannie Mae, 4.500%, 10/25/41 | | | 2.5% | |

| | Voya Emerging Markets Corporate Debt Fund - Class P | | | 2.4% | |

| | Voya Emerging Markets Hard Currency Debt Fund - Class P | | | 2.3% | |

| | Ginnie Mae Series, 0.650%, 11/20/37 | | | 2.1% | |

| | | |

| | Portfolio holdings are subject to change daily. | |

| | | |

On the other hand, some positions detracted from Fund performance. Most significant were the Fund’s exposure to emerging markets, its yield curve positioning and its derivative holdings. Concerns about the wobbly global economy — and higher rates to come in the United States — put pressure on emerging market (“EM”) debt across all venues, most notably in Brazil and Russia. Though the Fund’s exposure to EM debt was small, it nonetheless detracted from results.

The Fund employed interest rate futures to manage exposure to U.S. interest-rate risk; the futures were a drag on results as interest rates fell. We seek to use these instruments as means to protect the Fund from adverse market changes in interest rates or credit conditions.

Current Strategy & Outlook: While the improving labor market points to sunnier days ahead, the Fed’s dovish tone suggests that job growth is being overshadowed by the realities of low wage inflation, a strong dollar and collapsing oil prices. And though snowy weather was partially to blame for housing starts falling in the first quarter of 2015, the decline was the largest in four years — evidence that the housing market advance may be cooling.

We believe the removal of “patient” from the Fed’s latest announcement implies a shift in policy is coming. With forward guidance gone and the emphasis squarely on the economy, we believe the message is clear: although the timing of the first Fed move is approaching, the cumulative magnitude of Fed hikes will remain muted. This measured approach by the Fed will allow more time for U.S. labor market improvement to percolate into other areas of the economy. Low commodity prices and a strong dollar restrain inflation and are also positive tailwinds for consumers. Also, a weaker euro and quantitative easing by the European Central Bank are reviving growth prospects in Europe.

We believe supportive policy globally will help smooth over economic and seasonal noise. With a quiescent Fed for now, we maintain an overweight to investment grade corporates, which we expect to benefit from the strength and stability of the U.S. economy and from capital seeking more attractive yield than can be found elsewhere. Leverage has been on the rise in recent quarters. Corporate revenue and earnings growth have remained fairly stable for the past few years. However, we do not see an inflection point on the horizon for the credit cycle. Excluding metals and energy, corporate spreads have moved back into the range of their cycle lows, but flows have been

| Voya Strategic Income Opportunities Fund | Portfolio Managers’ Report |

positive and we believe demand remains sound despite heavy issuance. We also remain constructive on the forward prospects for below-investment grade credit sectors such as senior loans. This is driven by what we believe are attractive yields and a reasonably sanguine outlook for fundamental credit risk (ex-energy).

We believe interest rates are likely to be range-bound and interest rate volatility is likely to decline in the near term. Low short-term interest rates, an elevated Fed balance sheet, low long-term rates in major advanced countries, QE overseas, strong demand for safe assets and disappointments in growth in advanced countries are conspiring to keep long-term interest rates low. If clearer signs emerge that the economy is heating up, we could see rising volatility and a spring of interest rates later this year. We remain on watch for unexpected weakness in earnings and any resultant shift in investor expectations for the broader economy in general.

| * | Prior to December 1, 2014, the Fund was known as “Voya Strategic Income Fund.” |

| ** | Effective on December 1, 2014, the Fund changed its primary benchmark from the Barclay’s U.S. Universal Bond Index to the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index because the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index is considered by the adviser to be a more appropriate benchmark. |

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions. Fund holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| Portfolio Managers’ Report | Voya Strategic Income Opportunities Fund |

| | | Average Annual Total Returns for the Periods Ended March 31, 2015 | | |

| | | | | | 1 Year | | | Since Inception of Classes A, C, I, R, and W November 2, 2012 | | |

| | | Including Sales Charge: | | | | |

| | | Class A(1) | | | | | 1.41% | | | | | | 2.39% | | | |

| | | Class C(2) | | | | | 2.23% | | | | | | 2.62% | | | |

| | | Class I | | | | | 4.29% | | | | | | 3.70% | | | |

| | | Class R | | | | | 3.70% | | | | | | 3.05% | | | |

| | | Class W | | | | | 4.24% | | | | | | 3.45% | | | |

| | | Excluding Sales Charge: | | | | |

| | | Class A | | | | | 3.97% | | | | | | 3.49% | | | |

| | | Class C | | | | | 3.22% | | | | | | 2.62% | | | |

| | | Class I | | | | | 4.29% | | | | | | 3.70% | | | |

| | | Class R | | | | | 3.70% | | | | | | 3.05% | | | |

| | | Class W | | | | | 4.24% | | | | | | 3.45% | | | |

| | | Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index | | | | | 0.23% | | | | | | 0.26% | | | |

| | | Barclays U.S. Universal Bond Index | | | | | 5.33% | | | | | | 2.58% | | | |

| | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya Strategic Income Opportunities Fund against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund’s performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

| (1) | Reflects deduction of the maximum Class A sales charge of 2.50%. |

| (2) | Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return. |

On December 1, 2014 the Fund changed its primary benchmark from the Barclay’s U.S. Universal Bond Index to the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index because the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index is considered by the adviser to be a more appropriate benchmark.

| SHAREHOLDER EXPENSE EXAMPLES (Unaudited) |

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from October 1, 2014 to March 31, 2015. The Funds’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The left section of the table shown below, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes