Filed Pursuant to Rule 424(b)(3)

File Number 333-137362

PROSPECTUS

CYBER MERCHANTS EXCHANGE, INC.

80,450,174 shares of Common Stock

This prospectus covers the resale by selling stockholders named on page 15 of up to 80,450,174 shares of our common stock, no par value, which include:

| ● | 29,310,345 shares of common stock underlying Series B Convertible Preferred Stock issued in conjunction with our private placement completed on August 16, 2006; |

| ● | 32,241,380 shares of common stock issuable upon exercise of outstanding warrants we issued in connection with our issuance of the Series B Convertible Preferred Stock, at an exercise price of $0.326 per share in conjunction with our private placement completed on August 16, 2006; and |

| ● | 18,898,449 shares of common stock. |

This offering is not being underwritten. These securities will be offered for sale by the selling stockholders identified in this prospectus in accordance with the methods and terms described in the section of this prospectus entitled "Plan of Distribution." We will not receive any of the proceeds from the sale of these shares. We will pay all expenses, except for the brokerage expenses, fees, discounts and commissions, which will all be paid by the selling stockholders, incurred in connection with the offering described in this prospectus. Our common stock and warrants are more fully described in the section of this prospectus entitled "Description of Securities."

The prices at which the selling stockholders may sell the shares of common stock that are part of this offering will be determined by the prevailing market price for the shares at the time the shares are sold, a price related to the prevailing market price, at negotiated prices or prices determined, from time to time by the selling stockholders. See "Plan of Distribution."

Our common stock is currently listed on the Over the Counter Bulletin Board under the symbol “CMXG.” On September 14, 2006, the closing price of the shares was $0.59 per share.

AN INVESTMENT IN OUR COMMON STOCK INVOLVES A HIGH DEGREE OF RISK. SEE "RISK FACTORS" BEGINNING AT PAGE 4.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this prospectus is October 11, 2006.

| Prospectus Summary | 2 | |||

| Risk Factors | 4 | |||

| Use of Proceeds | 15 | |||

| Selling Security Holders | 15 | |||

| Plan of Distribution | 18 | |||

| Legal Proceedings | 19 | |||

| Officers and Directors | 20 | |||

| Security Ownership of Certain Beneficial Owners and Management | 21 | |||

| Description of Securities | 23 | |||

| Legal Matters | 29 | |||

| Experts | 29 | |||

| Disclosure of Commission Position of Indemnification for Securities Act Liabilities | 29 | |||

| Description of Business | 30 | |||

| Selected Consolidated Financial Data | 37 | |||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | 38 | |||

| Description of Property | 48 | |||

| Certain Relationships and Related Transactions | 49 | |||

| Market For Common Equity and Related Stockholder Matters | 53 | |||

| Dividend Policy | 53 | |||

| Executive Compensation | 53 | |||

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 56 | |||

| Where You Can Find More Information | 56 | |||

| Financial Statements | 57 |

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Such forward-looking statements include statements regarding, among other things, (a) our projected sales and profitability, (b) our growth strategies, (c) anticipated trends in our industry, (d) our future financing plans, and (e) our anticipated needs for working capital. Forward-looking statements, which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words "may," "will," "should," "expect," "anticipate," "estimate," "believe," "intend," or "project" or the negative of these words or other variations on these words or comparable terminology. This information may involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from the future results, performance, or achievements expressed or implied by any forward-looking statements. These statements may be found under “Prospectus Summary”, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Description of Business," as well as in this prospectus generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under "Risk Factors" and matters described in this prospectus generally. This prospectus may contain market data related to our business, which may have been included in articles published by independent industry sources. Although we believe these sources are reliable, we have not independently verified this market data. This market data includes projections that are based on a number of assumptions. If any one or more of these assumptions turns out to be incorrect, actual results may differ materially from the projections based on these assumptions. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. In addition to the information expressly required to be included in this filing, we will provide such further material information, if any, as may be necessary to make the required statements, in light of the circumstances under which they are made, not misleading.

Each forward-looking statement should be read in context with, and with an understanding of, the various other disclosures concerning our company and our business made elsewhere in this prospectus as well as other pubic reports which may be filed with the United States Securities and Exchange Commission (the "SEC"). You should not place undue reliance on any forward-looking statement as a prediction of actual results or developments. We are not obligated to update or revise any forward-looking statement contained in this prospectus to reflect new events or circumstances, unless and to the extent required by applicable law. Neither the Private Securities Litigation Reform Act of 1995 nor Section 27A of the Securities Act of 1933 provides any protection for statements made in this prospectus.

-1-

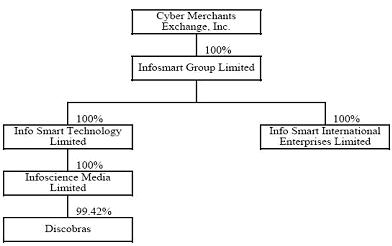

This summary highlights information contained elsewhere in this prospectus. It does not contain all of the information that you should consider before investing in our common stock. You should read the entire prospectus carefully, including the section entitled "Risk Factors" and our consolidated financial statements and the related notes. In this prospectus, we refer to Cyber Merchants Exchange, Inc. and our wholly owned subsidiary, Infosmart Group Limited, and Infosmart’s direct and indirect subsidiaries Info Smart Technology Limited, Info Smart International Enterprises Limited, Infoscience Media Limited and Discobras Industria E Comercio de Electro Eletronica Limiteda as “Cyber”, "our company," "we," "us" and "our."

OUR COMPANY

Cyber Merchants Exchange, Inc. (“Cyber”), through our wholly owned subsidiary Infosmart Group Limited (“Infosmart”), is in the business of developing, manufacturing, marketing and sales of recordable digital versatile disc (“DVDR”) optical media. We currently manufacture DVDRs with 8x and 16x writable speeds and are preparing for manufacturing of high density format DVDR (“HD DVDR”) or Blu-Ray format DVDR discs. We have customers in Western Europe, Australia, China and South America. We currently manufacture and ship our products from Hong Kong where we operate state of the art DVDR manufacturing facilities.

Cyber owns all of the capital stock of Infosmart Group Limited, a holding company incorporated in the British Virgin Islands (“Infosmart”). Infosmart beneficially owns 100% of the issued and outstanding capital stock of both: (i) Info Smart Technology Limited, a company incorporated under the laws of Hong Kong (“IS Technology”); and (ii) Info Smart International Enterprises Limited, a company incorporated under the laws of Hong Kong (“IS International”). IS Technology owns all of the issued and outstanding capital stock of Infoscience Media Limited, a company incorporated under the laws of Hong Kong (“IS Media”). IS Media owns 99.42% of the issued and outstanding capital stock of Discobras Industria E Comercio de Electro Eletronica Limiteda, a company incorporated under the laws of Brazil (“Discobras”), the remaining 0.58% ownership interest in Discobras is held by our local Brazilian partner.

We are constructing a DVDR production facility in Brazil. In March 2006, IS Media formed Discobras, a Brazilian company, with a local partner, with registered capital of US$8 million for our new Brazilian DVDR production facility. We intend to relocate some of our DVDR manufacturing equipment to Brazil in October 2006. We have obtained all required government licenses and all other documents and approvals necessary to operate a DVDR production facility in Brazil. The facility has been leased since April 2006 and is already prepared for DVDR manufacturing equipment to be installed in October 2006. Production in Brazil is expected to start in the fourth quarter of 2006.

In fiscal 2004, Infosmart’s revenues were $22,421,765 and its net income was $3,024,300. In fiscal 2005, Infosmart’s revenues were $24,577,206 and its net income was $4,214,761.

Share Exchange Transaction

Cyber did not become engaged in the DVDR manufacturing business until August of 2006. Before the closing our recent share exchange transaction in August 2006, we were a shell company with nominal assets and operations, whose sole business was to identify, evaluate and investigate various companies with the intent that, if such investigation warrants, a business combination be negotiated and completed pursuant to which Cyber would acquire a target company with an operating business with the intent of continuing the acquired company’s business as a publicly held entity. We entered in an Exchange Agreement dated July 7, 2006 and amended on August 14, 2006 (the “Exchange Agreement”) with KI Equity Partners II, LLC (“KI Equity”), Infosmart, the owners of 100% of the capital shares of Infosmart, namely Chung Kwok, Po Nei Sze, Prime Corporate Developments Limited (“Prime Corporate”) and Hamptons Investment Group Limited (“Hamptons”) (collectively the “Infosmart Shareholders”), and Worldwide Gateway Co., Ltd. The closing of the Exchange Agreement occurred on August 16, 2006. At the closing of the Exchange Agreement, Cyber acquired all of Infosmart’s capital shares (the “Infosmart Shares”) from the Infosmart Shareholders, and the Infosmart Shareholders transferred and contributed all of their Infosmart Shares to Cyber. In exchange, Cyber issued 1,000,000 shares of its Series A Convertible Preferred Stock to the Infosmart Shareholders. Each share of Cyber’s Series A Convertible Preferred Stock (“Series A Preferred Stock”) is convertible into 116.721360 shares of Cyber's common stock, subject to adjustments. The Series A Preferred Stock will immediately and automatically be converted into shares of Cyber's common stock upon the approval by a majority of Cyber's stockholders (voting together on an as-converted-to-common-stock basis), following the closing of the Exchange Agreement, of an increase in the number of authorized shares of Cyber's common stock from 40,000,000 shares to 300,000,000 shares and a change of Cyber's corporate name to Infosmart Group, Inc.

As a result of the closing of the Exchange Agreement, Infosmart became the wholly owned subsidiary of Cyber and became Cyber’s main operational business. The Exchange transaction, for accounting and financial reporting purposes, is deemed to be a reverse acquisition, where Cyber (the legal acquirer) is considered the accounting acquiree and Infosmart (the legal acquiree) is considered the accounting acquirer, and thus the historical financial statements of Infosmart are the financial statements of Cyber. On August 16, 2006, pursuant to the authority granted by Cyber’s bylaws, the Board of Directors of Cyber unanimously changed Cyber’s fiscal year end from May 31 to December 31 of each year.

In connection with the share exchange transaction, Cyber engaged Keating Securities, LLC (“Keating Securities”), an affiliate of Keating Investments, LLC to act as a financial advisor for Cyber in connection with the Exchange transaction. At the closing the Exchange Agreement, Keating Securities was paid an advisory fee of $450,000.

-2-

Recent Financing

The closing of the Exchange Agreement described above was contingent on a minimum of $7,000,000 (or such lesser amount as mutually agreed to by Infosmart and the placement agent) being subscribed for, and funded into escrow, by certain accredited and institutional investors ("Investors") in a private placement offering for the purchase of shares of Cyber's Series B Convertible Preferred Stock ("Series B Preferred Stock") and common stock purchase warrants promptly after the closing of the Exchange transaction under terms and conditions approved by Cyber's board of directors immediately following the Exchange (the “Financing”). The closing of the Financing was contingent on the closing of the Exchange transaction, and the Exchange transaction was contingent on the closing of the Financing. On August 16, 2006, Cyber completed this private placement offering. Cyber received gross proceeds of approximately $7.65 million in connection with the Financing from the Investors. Pursuant to Subscription Agreements entered into with these Investors, Cyber sold 1,092,857.1429 shares of its Series B Preferred Stock and warrants to purchase an additional 29,310,435 shares of Cyber’s common stock to the Investors. The price per unit in the Financing was $7.00. Each share of Series B Preferred Stock is currently convertible into 26.819924 shares of Cyber's common stock, subject to adjustments. On an as-converted basis, the Series B Preferred Shares would currently convert into 29,310,345 shares of Cyber's common stock.

Keating Securities, LLC and Axiom Capital Management, Inc. (“Placement Agents”) acted as placement agents in connection with the Financing. For their services, the Placement Agents received a commission equal to 8% of the gross proceeds from the offering and a non-accountable expense allowance equal to 2% of the gross proceeds. In addition, the Placement Agents received, for nominal consideration, warrants to purchase 10% of the number of shares of common stock into which the Series B Preferred Stock issued in the Financing, which in the aggregate totaled 2,931,035 shares of our common stock on an as-converted basis at an exercise price of $0.326 per share. The warrants are fully vested and have a term of five years. The Placement Agent warrants will have registration rights similar to the registration rights afforded to the holders of Series B Preferred Stock and Warrants. Cyber also paid for the out-of-pocket expenses incurred by the Placement Agent and all purchasers in the amount of $25,000.

The proceeds from the sale of the above securities will be used for general working capital purposes, including funding of the construction of our new production facility in Brazil, the purchase of equipment for HD DVDR and DVDR production lines, advertising and marketing expenses and product development expenses.

In connection with the Exchange Agreement, on September 7, 2006, we filed a Preliminary Information Statement on Schedule 14C (the "Information Statement") with the SEC. In the Information Statement, Cyber discloses that shareholders holding in excess of fifty percent (50%) of all shares entitled to vote have approved the following actions by written consent:

| ● | An amendment to Cyber’s Restated and Amended Articles of Incorporation to increase the number of the Cyber’s authorized shares of common stock from 40,000,000 to 300,000,000 shares with no par value; and |

| ● | An amendment to Cyber’s Restated and Amended Articles of Incorporation to change Cyber’s name to “Infosmart Group, Inc.” |

Cyber is a California corporation. Our principal executive offices are located at 5th Floor, QPL Industrial Building, 126-140 Texaco Road, Tsuen Wan, Hong Kong. Our telephone number is (852) 2944-9905.

The shares issued and outstanding prior to this offering consist of 13,428,810 shares of common stock and 2,092,857.1429 shares of preferred stock. We are registering shares of our common stock for sale by the selling stockholders identified in the section of this prospectus entitled "Selling Security Holders." The shares included in the table identifying the selling stockholders consist of:

| ● | 29,310,345 shares of common stock underlying Series B Convertible Preferred Stock issued in conjunction with our private placement offering completed on August 16, 2006; |

| ● | 32,241,380 shares of common stock underlying warrants issued in conjunction with our private placement offering completed on August 16, 2006; and |

| ● | 18,898,449 shares of common stock. |

The shares of common stock offered under this prospectus may be sold by the selling security holders on the public market, in negotiated transactions with a broker-dealer or market maker as principal or agent, or in privately negotiated transactions not involving a broker or dealer. Information regarding the selling shareholders, the common shares they are offering to sell under this prospectus, and the times and manner in which they may offer and sell those shares is provided in the sections of this prospectus captioned "Selling Security Holders," "Registration Rights" and "Plan of Distribution," respectively. We will not receive any of the proceeds from those sales. Should the selling security holders, in their discretion, exercise any of the common share purchase warrants underlying the common shares offered under this prospectus, we would, however, receive the exercise price for those warrants. The registration of common shares pursuant to this prospectus does not necessarily mean that any of those shares will ultimately be offered or sold by the selling stockholders, or that any of the common share purchase warrants underlying the common shares offered under this prospectus will be exercised.

-3-

You should carefully consider the risks described below together with all of the other information included in this report before making an investment decision with regard to our securities. The statements contained in or incorporated into this offering that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Business

The limited operating history of Infosmart makes evaluation of our business difficult.

We have limited operating histories. Infosmart was incorporated in the British Virgin Islands on August 23, 2005, and IS Technology was founded in August of 2002. These limited operating histories and the unpredictability of our industry make it difficult for investors to evaluate our business and future operating results. An investor in Cyber's securities must consider the risks, uncertainties and difficulties frequently encountered by companies in new and rapidly evolving markets. The risks and difficulties we face include challenges in accurate financial planning as a result of limited historical data and the uncertainties resulting from having had a relatively limited time period in which to implement and evaluate our business strategies as compared to older companies with longer operating histories.

We currently experiences customer concentration, which exposes it to all of the risks faced by our material customers.

Currently, 84% of all of our revenues are derived from three customers. E-Net Distribution, our largest customer, contributes approximately 69% of our revenues. DVD Technology and NaSa Multimedia Technology each contribute approximately 6.5% and 8.7%, respectively, of our revenues. Until we secure additional customer relationships, it is possible that we may experience periods during which it will be highly dependent on one or a limited number of customers. Dependence on a single or a few customers will make it difficult to negotiate satisfactorily attractive prices for Cyber’s products and will expose Cyber to the risk of substantial losses if a single dominant customer stops conducting business with Cyber. Moreover, Cyber will be subject to the risks faced by these major customers to the extent that such risks impede such customer's ability to stay in business and make timely payments to Cyber.

We continually seek to develop new products and standards, which may not be widely adopted by consumers or, if adopted, may reduce demand by consumers for our older products.

We continually seek to develop new products and standards and enhance existing products and standards with higher memory capacities and other enhanced features. We cannot assure you that our new products and standards will gain market acceptance or that we will be successful in penetrating the new markets that we target. As we introduce new products and standards, it will take time for these new products and standards to be adopted, for consumers to accept and transition to these new products and standards and for significant sales to be generated from them, if this happens at all. Moreover, broad acceptance of new products and standards by consumers may reduce demand for our older products and standards. If this decreased demand is not offset by increased demand for our new products and standards, our results of operations could be harmed. We cannot assure you that any new products or standards we develop will be commercially successful.

Our future operating results may fluctuate and cause the price of our common stock to decline.

We expect that our revenues and operating results will continue to fluctuate significantly from quarter to quarter due to various factors, many of which are beyond our control. The factors that could cause our operating results to fluctuate include, but are not limited to:

| ● | price competition; |

| ● | general price increases by suppliers and manufacturers; |

| ● | our ability to maintain and expand our customer relationships; |

| ● | the introduction of new or enhanced products and strategic alliances by us and our competitors; |

| ● | the success of our brand-building and marketing campaigns; |

-4-

| ● | consumer acceptance of our products and general shifts in consumer behavior with respect to our industry; | |

| ● | our ability to maintain, upgrade and develop our production facilities and infrastructure; | |

| ● | technical difficulties and system downtime; | |

| ● | the amount and timing of operating costs and capital expenditures relating to expansion of our business, operations and infrastructure; | |

| ● | general economic conditions as well as economic conditions specific to our industry; and | |

| ● | our ability to attract and retain qualified management and employees. |

If our revenues or operating results fall below the expectations of investors or securities analysts, the price of our common stock could significantly decline.

Our ability to manage our future growth is uncertain.

We are currently anticipating a period of growth as a result of our corporate growth strategy, which aims to, among other things, further develop our manufacturing capabilities, expand our product offerings, and reach new customers. In pursuing these objectives, the resulting strain on our managerial, operational, financial and other resources could be significant. Success in managing such expansion and growth will depend, in part, upon the ability of senior management to manage effectively. Any failure to manage the anticipated growth and expansion could have a material adverse effect on our business.

Increased product returns will decrease our revenues and impact profitability.

We do not make allowances for product returns in our financial statements based on the fact that we have not had a material historical return rate. In order to keep product returns low, we continuously monitor product purchases and returns and may change our product offerings based on the rates of returns. If our actual product returns significantly increase, especially as we expand into new product categories, our revenues and profitability could decrease. Any changes in our policies related to product returns may result in customer dissatisfaction and fewer repeat customers.

Our growth and operating results could be impaired if we are unable to meet our future capital needs.

We may need to raise additional capital in the future to:

| ● | fund more rapid expansion; | |

| ● | acquire or expand into new facilities; | |

| ● | maintain, enhance and further develop our manufacturing systems; | |

| ● | develop new product categories or enhanced services; | |

| ● | fund acquisitions; or | |

| ● | respond to competitive pressures. |

If we raise additional funds by issuing equity or convertible debt securities, the percentage ownership of our stockholders will be diluted. Furthermore, any new securities could have rights, preferences and privileges senior to those of Cyber's preferred shares and the common stock into which Cyber's preferred shares are convertible. We currently do not have any commitments for additional financing. We cannot be certain that additional financing will be available when and to the extent required or that, if available, it will be on acceptable terms. If adequate funds are not available on acceptable terms, we may not be able to fund our expansion, develop or enhance our products or services or respond to competitive pressures.

The loss of key senior management personnel could negatively affect our business.

We depend on the continued services and performance of our senior management and other key personnel, particularly Chung Kwok, our Chief Executive Officer and President, Gavin Wong, our V.P. of Sales and Marketing and Sebastian Tseng, our Regional Director for South America and V.P. of Production and R&D. The loss of any of our executive officers or other key employees could harm our business. Infosmart currently has employment agreements with its key personnel. Further, Cyber expects to assume the employment agreements our executive officers currently have with Infosmart that are described in more detail in the section titled “Executive Compensation - Employment Agreements” in this prospectus. Infosmart has a “key person” life insurance policy for Chung Kwok.

-5-

Rapid changes in technology could adversely affect our business and hurt our competitive position.

We believe that our ability to increase sales by developing appealing, innovative products has an important role to play in our growth. However, it is extremely difficult to predict future demand in the rapidly changing storage media industry and develop new technologies to meet that demand. We may fail to develop and supply in a timely manner attractive, new products with innovative technologies for this industry and its markets. In the event that our management misreads the industry and market and/or is slow in developing innovative technologies on a cost competitive basis, actual earnings could differ significantly from our forecasts. At the same time, we may cease to be able to compete in markets, resulting in a significant adverse effect on our business results and growth prospects.

The use of technologies and intellectual properties for the production of all of our products are derived from two cooperation agreements and the failure to maintain the effectiveness of such agreements could substantially and adversely affect our business.

Our ability to produce our products depends on two cooperation agreements (the “Cooperation Agreements”) with two parties (“Cooperative Partners”) that have been granted licenses (the “Patent Licenses”) for the use of technologies and intellectual properties necessary for the production of all of our products. Such Cooperation Agreements currently expire on December 31, 2006, but we can renew both agreements. A failure to extend and otherwise maintain effectiveness of such agreements could prevent us from conducting our business of manufacturing our products and could substantially and adversely affect our business.

The patents required for manufacturing our DVDR products are owned by multiple companies. Our failure to obtain all of the required patents to manufacture our products may interfere with our current or future product development and sales.

We have never conducted a comprehensive patent search relating to the technology we use in our products. The Patent Licenses held by the parties with whom we have Cooperation Agreements were obtained through a joint patent licensing program (the “DVDR Patent License Program”) that is administered by Koninklijke Philips Electronics, N.V. (“Philips”). Parties acquiring the patent licenses through this DVDR Patent License Program are allowed to use patents owned by companies including Philips, Sony, Pioneer and/or Hewlett Packard (or for which such companies have patent applications pending) that are essential for manufacturing DVDR products. However, there may be other issued or pending patents owned by third parties that are required for manufacturing our products for which our Cooperative Partners do not have a patent license. If so, we could incur substantial costs defending against patent infringement claims or we could even be blocked from selling our products. We cannot determine with certainty whether any other existing third party patents or the issuance of any new third party patents would require us or our Cooperative Partners to alter, or obtain licenses relating to, our processes or products, or implement alternative non-infringing approaches, all at a significant additional cost to Cyber. There is no assurance that we or our Cooperative Partners will be able to obtain any such licenses on terms favorable to us, if at all, and obtaining and paying royalties on new licenses might materially increase our costs. Additionally, the fees in respect of existing licenses could increase materially in the future when these licenses are renewed, and such increase may have a significantly and adversely impact our business.

Our inability to obtain its own Patent Licenses through the DVD Patent License Program prior to the expiration of the Cooperation Agreements could adversely affect its operations.

We are planning to apply for our own Patent Licenses before the expiration of the two Cooperation Agreements within 90 days of the closing of the Exchange Agreement. In the event we are unable to obtain its own Patent Licenses, then it plans to exercise its option to renew Cooperation Agreements. However, if we are unable to obtain our own Patent Licenses then we may not be able to manufacture our products and this could significantly and adversely affect our business results and financial condition. Our inability to either obtain its own Patent Licenses or to renew and maintain the effectiveness of the Cooperation Agreements could result in delays in product development or prevent us from selling our products until equivalent substitute technology can be identified, licensed and/or integrated or until we are able to substantially engineer our products to avoid infringing the rights of third parties. We might not be able to renegotiate agreements, be able to obtain necessary licenses in a timely manner, on acceptable terms, or at all, or be able to re-engineer our products successfully. Moreover, the loss of or inability to extend any of these Patent Licenses would increase the risk of infringement claims being made against us, which claims could have a material adverse effect on our business.

We may be unable to obtain its own new Hong Kong business customs license for its manufacturing facilities in Hong Kong

The Hong Kong government requires companies manufacturing DVDRs to obtain a business license for the manufacture of optical Disc/Stampers (the “Hong Kong Business Licenses”) from the Customs and Excise Department of Hong Kong. We currently manufacturer our products under HK Business Licenses held by its Cooperative Partners under the Cooperation Agreement. In addition, we plan to obtain our own Hong Kong Business Licenses for our Hong Kong factories within 90 days of the closing of the share exchange transaction. However, if we are unable to obtain such business licenses and we are also unable to extend the Cooperation Agreements beyond December 31, 2006, then production of our products at our Hong Kong factories may be halted, causing substantial losses to Cyber.

-6-

Our business may suffer if we are sued for infringing upon the intellectual property rights of third parties.

There may be cases where it is alleged that our products infringe on the intellectual property rights of third parties. As a result, we may suffer damages or may be sued for damages. In either case, settlement negotiations and legal procedures would be inevitable and could be expected to be lengthy and expensive. If our assertions are not accepted in such disputes, we may have to pay damages and royalties and suffer losses such as the loss of our market share. The failure to prevent infringement on the rights of others could have a materially adverse effect on our business development, business results and financial condition.

We are dependent on certain raw materials and other products, and our business will suffer if we are unable to procure such materials and products.

Our manufacturing systems are premised on deliveries of raw materials and other supplies in adequate quality and quantity in a timely manner from many external suppliers. In new product development, we may rely on certain irreplaceable suppliers for materials. Because of this, there may be cases where supplies of raw materials and other products to us are interrupted by: an accident or some other event at a supplier; supply is suspended due to quality or other issues; or there is a shortage of or instability in supply due to a rapid increase in demand for finished products that use certain materials and products. If any of these situations becomes protracted, we may have difficulty finding substitutes in a timely manner from other suppliers, which could have a significant, adverse effect on our production and prevent us from fulfilling our responsibilities to supply products to our customers. Furthermore, if an imbalance arises in the supply-demand equation, there could be a spike in the price of raw materials. In the event of these or other similar occurrences, there could be a material adverse effect on our business results and financial condition.

We compete in a highly competitive industry where some of our competitors are larger and have more resources than us.

We operate in a highly competitive environment. Our competitors are both larger and smaller than us in terms of resources and market share. The marketplaces in which we operate are generally characterized by rapid technological change, frequent new product introductions and declining prices. In these highly competitive markets, our success will depend to a significant extent on its ability to continue to develop and introduce differentiated and innovative products and customer solutions successfully on a timely basis. The success of our product offerings is dependent on several factors including understanding customer needs, strong digital technology, differentiation from competitive offerings, market acceptance and lower costs. Although we believe that we can take the necessary steps to meet the competitive challenges of these marketplaces, no assurance can be given with regard to our ability to take these steps, the actions of competitors, some of which will have greater resources than us, or the pace of technological changes.

Technology in our industry evolves rapidly, potentially causing our products to become obsolete, and we must continue to enhance existing systems and develop new systems or we will lose sales.

Rapid technological advances, rapidly changing customer requirements and fluctuations in demand characterize the current market for our products. Further, there are alternative data storage media and additional media is under development, including high capacity hard drives, new CD-R/DVDR technologies, file servers accessible through computer networks and the Internet. Our existing and development-stage products may become obsolete if our competitors introduce newer or more appealing technologies. If these technologies are patented by or are proprietary to our competitors, then we may not be able to access these technologies. We believe that we must continue to innovate and anticipate advances in the storage media industry in order to remain competitive. If we fail to anticipate or respond to technological developments or customer requirements, or if we are significantly delayed in developing and introducing products, our business will suffer lost sales.

Our market is becoming more competitive. Competition may result in price reductions, lower gross profits and loss of market share.

The storage media industry is becoming more competitive and we face the potential for increased competition in developing and selling our products. Our competitors may have or could develop or acquire significant marketing, financial, development and personnel resources. We cannot assure you that we will be able to compete successfully against our current or future competitors. The storage media industry has increased visibility, which may lead to large, well-known, well-financed companies entering into this market. Increased competition from manufacturers of systems or consumable supplies may result in price reductions, lower gross profit margins, increased discounts to distribution and loss of market share and could require increased spending by us on research and development, sales and marketing and customer support.

If we are unable to compete effectively with existing or new competitors, the loss of its competitive position could result in price reductions, fewer customer orders, reduced revenues, reduced margins, reduced levels of profitability and loss of market share.

We have several competitors, which include the largest DVDR manufacturers in the world. Certain of these competitors compete aggressively on price and seek to maintain very low cost structures. Some of these competitors are seeking to increase their market share, which creates increased pressure, including pricing pressure, within the market. In addition, certain of the competitors, including CMC and Ritek, have financial and human resources that are substantially greater than ours, which increases the competitive pressures we face. Customers make buying decisions based on many factors, including among other things, new product and service offerings and features; product performance and quality; ease of doing business; a vendor’s ability to adapt to customers’ changing requirements; responsiveness to shifts in the marketplace; business model; contractual terms and conditions; vendor reputation and vendor viability. As competition increases, each factor on which we compete becomes more important and the lack of competitive advantage with respect to one or more of these factors could lead to a loss of competitive position, resulting in fewer customer orders, reduced revenues, reduced margins, reduced levels of profitability and loss of market share. We expect competitive pressure to remain intense.

-7-

The products we make have a life cycle. If we are unable to successfully time market entry and exit and manage its inventory, it may fail to enter profitable markets or exit unprofitable markets.

We operate in a highly competitive, quickly changing environment. We are preparing for high density format DVDR (“HD DVDR”) or Blu-Ray format DVDR production. Thirty two (32) of Infosmart’s forty four (44) production lines can be upgraded to HD DVDR production at a time of management’s choosing. However, if the market turns in favor of Blu-Ray, Cyber will have to purchase new equipment to produce Blu-Ray DVRD discs, and thus Cyber’s business and operating results could be adversely affected. If strong competitors challenge us in Brazil and other key markets, we will need to quickly develop an adequate competitive response. If we fail to accurately anticipate market and technological trends, then our business and operating results could be materially and adversely affected.

We must also be able to manufacture the products at acceptable costs. This requires us to be able to accurately forecast customer demand so that it can procure the appropriate inputs at optimal costs. We must also try to reduce the levels of older product inventories to minimize inventory write-offs. If we have excess inventory, it may be necessary to reduce its prices and write down inventory, which could result in lower gross margins. Additionally, our customers may delay orders for existing 8x or 16x writable speed DVDR products in anticipation of new HD DVDR or Blu-Ray product introductions. As a result, we may decide to adjust prices of existing products during this process to try to increase customer demand for these products. Our future operating results would be materially and adversely affected if such pricing adjustments were to occur and we are unable to mitigate the resulting margin pressure by maintaining a favorable mix of products, or if we are unsuccessful in achieving input cost reductions, operating efficiencies and increasing sales volumes.

If we are unable to timely develop, manufacture, and introduce new products in sufficient quantity to meet customer demand at acceptable costs, or if we are unable to correctly anticipate customer demand for our new and existing products, then our business and operating results could be materially adversely affected.

If our products fail to compete successfully with other existing or newly-developed products for the storage media industry, our business will suffer.

The success of our products depends upon end users choosing our DVDR technology for their storage media needs. However, alternative data storage media exist, such as high capacity hard drives, new CD-R/DVDR technologies, file servers accessible through computer networks and the Internet, and additional media is under development. If end users perceive any technology that is competing with ours as more reliable, higher performing, less expensive or having other advantages over our technology, the demand for our DVDR products could decrease. Further, some of our competitors may make strategic acquisitions or establish cooperative relationships with suppliers or companies that produce complementary products such as cameras, computer equipment, software or biometric applications. Competition from other storage media is likely to increase. If our products do not compete successfully with existing or new competitive products, our business will suffer.

Our products may have manufacturing or design defects that we discover after shipment, which could negatively affect our revenues, increase our costs and harm our reputation.

Our products may contain undetected and unexpected defects, errors or failures. If these product defects are substantial, the result could be product recalls, an increased amount of product returns, loss of market acceptance and damage to our reputation, all of which could increase our costs and cause us to lose sales. We do not carry general commercial liability insurance covering our products. In addition, we are preparing to launch production of HD format or Blu-Ray format DVDRs in 2007. HD and Blu-Ray format DVDR production will require us to master new production techniques and modify existing or purchase new machinery and equipment. It is possible that we may fail to achieve mastery of these new techniques and production yields could suffer as a result.

The development of digital distribution alternatives, including the copying and distribution of music and video and other electronic data files could lessen the demand for our products.

We are dependent on the continued viability and growth of physical distribution of music, video and other electronic data through recordable media. Alternative distribution channels and methods, both authorized and unauthorized, for delivering music, video and other electronic data may erode our volume of sales and the pricing of its products and services. The growth of these alternatives is driven by advances in technology that allow for the transfer and downloading of music, video and other electronic data files from the Internet. The proliferation of this copying, use and distribution of such files is supported by the increasing availability and decreasing price of new technologies, such as personal video recorders, DVD burners, portable MP3 music and video players, widespread access to the Internet, and the increasing number of peer-to-peer digital distribution services that facilitate file transfers and downloading. We expect that file sharing and downloading, both legal and illegal, will continue to exert downward pressure on the demand for traditional DVDRs. As current technologies and delivery systems improve, the digital transfer and downloading of music, video and other electronic data files will likely become more widespread. As the speed and quality with which music, video and other electronic data files can be transferred and downloaded improves, file sharing and downloading may in the future exert significant downward pressure on the demand for DVDRs. In addition, our business faces pressure from the emerging distribution alternatives, like video on demand (“VOD”) and personal digital video recorders. As substantially all of our revenues are derived from the sale of DVDRs, increased file sharing, downloading and piracy or the growth of other alternative distribution channels and methods, could materially adversely affect its business, financial condition and results of operations.

-8-

Our revenues, cash flows and operating results may fluctuate for a number of reasons.

Future operating results and cash flows will continue to be subject to quarterly fluctuations based on a wide variety of factors, including seasonality. Although our sales and other operating results can be influenced by a number of factors and historical results are not necessarily indicative of future results, our sequential quarterly operating results generally fluctuate downward in the fourth quarter of each fiscal year when compared with the immediately preceding quarter. For example, our first calendar quarter is modestly affected by the Chinese New Year.

A significant portion of the revenues will depend on the success of Cyber’s new venture in Brazil.

A significant portion of Cyber’s revenues will depend on the success of our new Brazilian venture. We have no prior manufacturing and distribution experience in Brazil, and will rely on the local knowledge of its Brazilian joint venture partner and the general knowledge of the South American marketplace of its regional director Sebastian Tseng. Our results could suffer should its relationships with either of these two parties deteriorate in the early months of the Brazilian venture.

We are at risk of losing our significant investment in Brazil if we are unable to obtain the intellectual property licenses required for our Discobras manufacturing facility.

The owners of the technologies and intellectual property necessary for the production of our products require that we obtain separate Patent Licenses for the use of intellectual property in our new DVDR manufacturing facility in Brazil. We plan to apply for the Patent Licenses for use at the Discobras manufacturing facility in 2006. However, if there is a substantial delay in obtaining approval for our use of the Patent Licenses, then we may be unable to manufacture a sufficient amount of our products to fill our sales orders, and this could cause us to lose substantial revenues. Further, in the event we are unable to obtain the Patent Licenses, then we may not be able to manufacture our products in Brazil, thus placing us at risk of losing its significant investment in the Brazilian venture.

Past activities of Cyber and its affiliates may lead to future liability for the combined companies.

Prior to the closing of the share exchange transaction in August 2006, Cyber engaged in businesses unrelated to that of our current business operations. Any liabilities relating to such prior business against which we are not completely indemnified may have a material adverse effect on Cyber.

Risks Relating To Doing Business in Hong Kong and Brazil

Adverse changes in economic and political policies of the People’s Republic of China government could have a material adverse effect on the overall economic growth of Hong Kong, which could adversely affect our business.

Although, as described above, we are planning a new venture in Brazil, substantially all of our business operations are currently conducted in Hong Kong, a special administrative region in the People’s Republic of China (“PRC”). Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in Hong Kong and the PRC. The PRC’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. While the PRC economy has experienced significant growth in the past 20 years, growth has been uneven across different regions and among various economic sectors of China. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may also have a negative effect on us.

You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in Hong Kong or China based on United States or other foreign laws against us, our management or the experts named in the prospectus.

We currently conduct substantially all of our operations in Hong Kong and substantially all of our assets are located in Hong Kong. In addition, all of our senior executive officers reside within Hong Kong. As a result, it may not be possible to effect service of process within the United States or elsewhere outside Hong Kong upon our senior executive officers, including with respect to matters arising under U.S. federal securities laws or applicable state securities laws. Moreover, neither the PRC nor Hong Kong have treaties with the United States or many other countries providing for the reciprocal recognition and enforcement of judgment of courts.

-9-

Fluctuation in the value of the Hong Kong Dollar may have a material adverse effect on your investment.

The value of the Hong Kong dollar against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions. Although the exchange rate between the Hong Kong dollar and the U.S. dollar has been effectively pegged, there can be no assurance that the Hong Kong dollar will remain pegged, to the U.S. dollar, especially in light of the significant international pressure on the Chinese government to permit the free floatation of the RMB and the Hong Kong dollar, which could result in an appreciation of RMB or the Hong Kong dollar against the U.S. dollar. Our revenues and costs are mostly denominated in Hong Kong dollars, while a significant portion of our financial assets are also denominated in Hong Kong dollars. Any significant revaluation of the Hong Kong dollar may materially and adversely affect our cash flows, revenues, earnings and financial position, and the value of, and any dividends payable on, our stock in U.S. dollars. For example, an appreciation of the Hong Kong dollar against the U.S. dollar would make any new Hong Kong dollar denominated investments or expenditures more costly to us, to the extent that we need to convert U.S. dollars into Hong Kong dollars for such purposes. An appreciation of the Hong Kong dollar against the U.S. dollar would also result in foreign currency translation losses for financial reporting purposes when we translate our U.S. dollar denominated financial assets into the Hong Kong dollar, as the Hong Kong dollar is our reporting currency.

We face risks related to health epidemics and other outbreaks.

Our business could be adversely affected by the effects of SARS or another epidemic or outbreak. China and Hong Kong reported a number of cases of SARS in April 2004. Any prolonged recurrence of SARS or other adverse public health developments in China or in Hong Kong may have a material adverse effect on our business operations. For instance, health or other government regulations adopted in response may require temporary closure of our production facilities or of our offices. Such closures would severely disrupt our business operations and adversely affect our results of operations. We have not adopted any written preventive measures or contingency plans to combat any future outbreak of SARS or any other epidemic.

Changes in Hong Kong or Brazil’s political or economic situation could harm our operational results.

In addition to our operations in Hong Kong, we are currently establishing a production facility and a sales base in Brazil. Economic reforms adopted by the Chinese or Brazilian governments have had positive effects on the economic development of these countries, but the governments could change these economic reforms or any of the legal systems at any time. This could either benefit or damage Cyber’s operations and profitability. Some of the things that could have this effect are:

| · | Level of government involvement in the economy; |

| · | Control of foreign exchange; |

| · | Methods of allocating resources; |

| · | Balance of payments position; |

| · | International trade restrictions; and |

| · | International conflict. |

Any of the foregoing events or other unforeseen consequences of public health problems could damage Cyber’s operations.

The Brazilian government has historically exercised, and continues to exercise, significant influence over the Brazilian economy. Brazilian political and economic conditions will have a direct impact on our business and the market price of our securities.

The Brazilian government frequently intervenes in the Brazilian economy and occasionally makes substantial changes in policy, as often occurs in other emerging economies. The Brazilian government’s actions to control inflation and carry out other policies have in the past involved wage and price controls, currency devaluations, capital controls and limits on imports, among other things. Our business, financial condition and results of operations may be adversely affected by factors in Brazil including:

| ● | Currency volatility; |

| ● | Inflation acceleration; |

| ● | Monetary policy and interest rate increases; |

-10-

| ● | Fiscal policy and tax changes; |

| ● | International trade policy including tariff and non-tariff trade barriers; |

| ● | Foreign exchange controls; |

| ● | Energy shortages; and |

| ● | Other political, social and economic developments in or affecting Brazil. |

In 2005, government figures, legislators and political party officials, especially those of the President’s party, have been the subject of a variety of allegations of unethical or illegal conduct. These accusations, which are currently being investigated by the Brazilian Congress, involve campaign financing and election law violations, and influencing of government officials and Congressmen in exchange for political support. Several members of the President’s party and of the federal government, including the President’s chief of staff, have resigned. We cannot predict what effect these accusations and investigations may have on the Brazilian economy.

Inflation and government measures to curb inflation may contribute significantly to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets and, consequently, may adversely affect our business in Brazil.

Brazil has in the past experienced extremely high rates of inflation, with annual rates of inflation reaching as high as 2,567% in 1993 (as measured by the Índice Geral de Preços do Mercado published by Fundação Getúlio Vargas , or IGP-M Index). More recently, Brazil’s rates of inflation were 10.4% in 2001, 25.3% in 2002, 8.7% in 2003, 12.4% in 2004 and 0.2% in the nine months ended September 30, 2005 (as measured by the IGP-M Index). Inflation, governmental measures to combat inflation and public speculation about possible future actions have in the past had significant negative effects on the Brazilian economy and have contributed to economic uncertainty in Brazil. If Brazil experiences substantial inflation in the future, our costs may increase and our operating and net margins may decrease. Inflationary pressures may also lead to further government intervention in the economy, which could involve the introduction of government policies that may adversely affect the overall performance of the Brazilian economy.

Restrictions on currency exchange may limit our ability to receive and use our revenues effectively .

If we successfully establish our business operations in Brazil, some of our revenues will be settled in the Brazilian Real. Any future restrictions on currency exchanges may limit our ability to use revenue generated in Reals to fund any future business activities outside Brazil or to make dividend or other payments in U.S. dollars. Currently, we can legally exchange and transfer out of Brazil after-tax profits of up to Cyber’s total investment in its Brazilian subsidiary Discobras, which we expect to be approximately $8 million for 2006 and an additional $6 million for 2007.

The value of our securities will be affected by the foreign exchange rate between the U.S. dollar, the Hong Kong dollar and the Real.

The value of our common stock will be affected by the foreign exchange rate between U.S. and Hong Kong dollars and Real, and between those currencies and other currencies in which our sales may be denominated. For example, to the extent that we need to convert U.S. or Hong Kong dollars into Real for our operational needs and should the Real appreciate against the U.S. dollar at that time, our financial position, our business, and the price of our common stock may be harmed. Conversely, if we decide to convert our Reals into U.S. or Hong Kong dollars for the purpose of declaring dividends on our common stock or for other business purposes and the U.S. Dollar appreciates against the Real, the U.S. or Hong Kong dollar equivalent of our earnings from our subsidiaries in Hong Kong and Brazil would be reduced. We will engage in hedging activities to manage our financial exposure related to currency exchange fluctuation. In these hedging activities, we might use fixed-price, forward, futures, financial swaps and option contracts traded in the over-the-counter markets or on exchanges, as well as long-term structured transactions when feasible.

We will depend on Brazil’s foreign investment incentive programs, which provide reductions in taxation or exemptions from taxation for our operations in Brazil. The loss of the tax benefits from these incentive programs may substantially affect our earnings.

Under the State of Bahia’s investment incentive program, our Brazilian subsidiary, Discobras, has been granted a reduction in the Value Added Tax (“VAT”) it is required to pay for products. Discobras pays 2.28% only, as compared to VAT of 12% in Salvador, or 18% in São Paulo. This VAT reduction will be available to us until June 2016. We will also avail ourselves of an incentive program for foreign investment which exempts Discobras from paying Brazil’s ICMS taxes on raw materials it imports for production in Brazil and create substantial tax savings for Cyber. This tax exemption will last through June 2016. In the event that the VAT reduction program is no longer available to us or we are unable to extend the ICMS tax-exemption, our after-tax earnings would decline by the amount of the tax benefits, which may be substantial.

-11-

Risks Relating to this Offering and Ownership of Our Securities

Your rights with respect to ownership of Cyber's Series A and Series B Preferred Shares are set forth in the Certificate of Determination of Rights, Preferences, Privileges and Restrictions for the Series A and Series B Preferred Stock and form of Warrants and such documents should be reviewed carefully with your legal counsel.

Your rights with respect to ownership of our Series A and Series B Preferred Shares and the Warrants are set forth in the Certificate of Determination of Rights, Preferences, Privileges and Restrictions for the Series A and Series B Preferred Stock that were attached as Exhibits 3.3 and 3.4 and in the form of Warrant attached as Exhibit 10.17 to our Current Report on Form 8-K filed with SEC on August 24, 2006. These documents contain important provisions that provide you with rights, limitations and obligations and should be reviewed carefully with your legal counsel. We will also provide copies of these documents upon request.

After the closing of the share exchange transaction and the Financing, we will operate as a public company subject to evolving corporate governance and public disclosure regulations that may result in additional expenses and continuing uncertainty regarding the application of such regulations.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002 and related rules and regulations, are creating uncertainty for public companies. We are presently evaluating and monitoring developments with respect to new and proposed rules and cannot predict or estimate the amount of the additional compliance costs we may incur or the timing of such costs. These new or changed laws, regulations and standards are subject to varying interpretations, in many cases due to their lack of specificity, and as a result, their application in practice may evolve over time as new guidance is provided by courts and regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. Maintaining appropriate standards of corporate governance and public disclosure may result in increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities. In addition, if we fail to comply with new or changed laws, regulations and standards, regulatory authorities may initiate legal proceedings against us and our business and our reputation may be harmed.

Following the closing of the share exchange transaction and the Financing, our shares may have limited liquidity.

Following the closing of the share exchange transaction and the Financing in August 2006, a substantial portion of our shares of common stock became subject to registration, and will be closely held by certain institutional and insider investors. Consequently, the public float for the shares may be highly limited. As a result, should you wish to convert the Series B Preferred Stock and sell your shares into the open market you may encounter difficulty selling large blocks of your shares or obtaining a suitable price at which to sell your shares.

The Series B Preferred Shares sold by us in the Financing initially will not be registered and you will not be able to sell these preferred shares or the shares of common stock underlying the preferred shares of Cyber you obtain in the Financing until such shares are registered. There can be no assurance that we will be able to register the shares of Cyber in a timely manner.

None of the Series B Preferred Stock, the Cyber Merchants shares of common stock underlying the Series B Preferred Stock and the Warrants (collectively the "Financing Securities"), nor the shares of Cyber’s common stock issued to the holders of Infosmart’s capital stock in the Exchange will be registered or freely tradable immediately after the closing of the Financing and Exchange. We are filing this registration statement to register the shares of Cyber’s common stock underlying the Financing Securities that were obtained pursuant to the Financing as required by the Registration Rights Agreement that was entered into by the Series B Preferred stockholders and us in connection with their investment. However, there can be no assurance that we will be able to meet the time frame laid out in the Registration Rights Agreement. Our inability to meet such registration requirements will force you to hold the Financing Securities acquired in the Financing for a substantial period of time without having liquidity for those Financing Securities or the shares of our common stock underlying the Financing Securities.

Our stock price may be volatile, which may result in losses to our shareholders.

The stock markets have experienced significant price and trading volume fluctuations, and the market prices of companies quoted on the Over-The-Counter Bulletin Board, the stock market in which shares of our common stock will be quoted, generally have been very volatile and have experienced sharp share price and trading volume changes. The trading price of our common stock is likely to be volatile and could fluctuate widely in response to many of the following factors, some of which are beyond our control:

| ● | variations in our operating results; |

| ● | announcements of technological innovations, new services or product lines by us or our competitors; |

| ● | changes in expectations of our future financial performance, including financial estimates by securities analysts and investors; |

| ● | changes in operating and stock price performance of other companies in our industry; |

| ● | additions or departures of key personnel; and |

| ● | future sales of our common stock. |

-12-

Domestic and international stock markets often experience significant price and volume fluctuations. These fluctuations, as well as general economic and political conditions unrelated to our performance, may adversely affect the price of our common stock. In particular, following initial public offerings, the market prices for stocks of companies often reach levels that bear no established relationship to the operating performance of these companies. These market prices are generally not sustainable and could vary widely. In the past, following periods of volatility in the market price of a public company’s securities, securities class action litigation has often been initiated.

We have broad discretion as to the use of proceeds from this Financing and may not use the proceeds effectively.

Our management team will retain broad discretion as to the allocation and timing of the use of proceeds from the Financing and may spend these proceeds in ways with which our shareholders may not agree. The failure of our management to apply these funds effectively could result in unfavorable returns and uncertainty about our prospects, each of which could cause the price of our common stock to decline.

Our officers and directors own a substantial portion of our outstanding common stock, which will enable them to influence many significant corporate actions and in certain circumstances may prevent a change in control that would otherwise be beneficial to our shareholders.

As of the closing of the Financing and share exchange transaction in August 2006, our directors and executive officers controlled approximately 64% of our outstanding shares of stock that are entitled to vote on all corporate actions. Specifically, Chung Kwok, our Chief Executive Officer, President and Director and Po Nei Sze, our Chief Financial Officer, Secretary, Treasurer and Director, controlled approximately 64% of the outstanding voting shares as of the completion of the Financing and the share exchange transaction. These stockholders, acting together, could have a substantial impact on matters requiring the vote of the shareholders, including the election of our directors and most of our corporate actions. This control could delay, defer or prevent others from initiating a potential merger, takeover or other change in our control, even if these actions would benefit our shareholders and us. This control could adversely affect the voting and other rights of our other shareholders and could depress the market price of our common stock.

A large number of additional shares may be sold into the public market in the near future, which may cause the market price of our common stock to decline significantly, even if our business is doing well.

Sales of a substantial amount of common stock in the public market, or the perception that these sales may occur, could adversely affect the market price of our common stock. After the Financing and assuming the full conversion of our Series A Preferred Stock and our Series B Preferred Stock, we will have approximately 159,460,515 shares of common stock outstanding. This includes 116,721,360 shares to be received by the shareholders of Infosmart in the Exchange transaction after the conversion of the Series A Preferred Stock. As restrictions on resale of such additional shares end, the market price could drop significantly if the holders of these restricted shares sell them or are perceived by the market as intending to sell them.

A large number of common shares are issuable upon exercise of outstanding common share warrants and upon conversion of our Series A and Series B Preferred Stock. The exercise or conversion of these securities could result in the substantial dilution of your investment in terms of your percentage ownership in Cyber as well as the book value of your common shares. The sale of a large amount of common shares received upon exercise of these warrants on the public market to finance the exercise price or to pay associated income taxes, or the perception that such sales could occur, could substantially depress the prevailing market prices for our shares.

As of August 16, 2006, there are outstanding warrants entitling the holders to purchase up to 32,241,380 common shares at an exercise price of $0.326 per share. There are 116,721,360 shares underlying our convertible Series A Preferred Stock. There are 29,310,345 shares underlying our convertible Series B Preferred Stock at a conversion price per common share of $0.261 per common share. The exercise price for all of the aforesaid warrants may be less than your cost to acquire our common shares. In the event of the exercise of these securities, you could suffer substantial dilution of your investment in terms of your percentage ownership in the company as well as the book value of your common shares. In addition, the holders of the common share purchase warrants may sell common shares in tandem with their exercise of those options or warrants to finance that exercise, or may resell the shares purchased in order to cover any income tax liabilities that may arise from their exercise of the warrants.

We will incur increased costs and compliance risks as a result of becoming a public company with substantial business operations.

As a public company, we will incur significant legal, accounting and other expenses that we did not incur prior to the closing of the share exchange transaction as a shell company with no business operations and nominal assets. We will incur costs associated with our public company reporting requirements. We also anticipate that we will incur costs associated with recently adopted corporate governance requirements, including certain requirements under the Sarbanes-Oxley Act of 2002, as well as new rules implemented by the SEC and the National Association of Securities Dealers (“NASD”). We expect these rules and regulations, in particular Section 404 of the Sarbanes-Oxley Act of 2002, to significantly increase our legal and financial compliance costs and to make some activities more time-consuming and costly. Like many smaller public companies, we face a significant impact from required compliance with Section 404 of the Sarbanes-Oxley Act of 2002. Section 404 requires management of public companies to evaluate the effectiveness of internal control over financial reporting and the independent auditors to attest to the effectiveness of such internal controls and the evaluation performed by management. The SEC has adopted rules implementing Section 404 for public companies as well as disclosure requirements. The Public Company Accounting Oversight Board, or PCAOB, has adopted documentation and attestation standards that the independent auditors must follow in conducting its attestation under Section 404. We are currently preparing for compliance with Section 404; however, there can be no assurance that we will be able to effectively meet all of the requirements of Section 404 as currently known to us in the currently mandated timeframe. Any failure to implement effectively new or improved internal controls, or to resolve difficulties encountered in their implementation, could harm our operating results, cause us to fail to meet reporting obligations or result in management being required to give a qualified assessment of our internal controls over financial reporting or our independent auditors providing an adverse opinion regarding management’s assessment. Any such result could cause investors to lose confidence in our reported financial information, which could have a material adverse effect on our stock price.

We also expect these new rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified individuals to serve on our Board of Directors or as executive officers. We are currently evaluating and monitoring developments with respect to these new rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs.

-13-

If we fail to maintain the adequacy of our internal controls, our ability to provide accurate financial statements and comply with the requirements of the Sarbanes-Oxley Act of 2002 could be impaired, which could cause our stock price to decrease substantially.

We have recently taken measures to address and improve our financial reporting and compliance capabilities and we are in the process of instituting changes to satisfy our obligations in connection with Infosmart’s becoming a public company. We plan to obtain additional financial and accounting resources to support and enhance our ability to meet the requirements of being a public company. We will need to continue to improve our financial and managerial controls, reporting systems and procedures, and documentation thereof. If our financial and managerial controls, reporting systems or procedures fail, we may not be able to provide accurate financial statements on a timely basis or comply with the Sarbanes-Oxley Act of 2002 as it applies to us. Any failure of our internal controls or our ability to provide accurate financial statements could cause the trading price of our common stock to decrease substantially.

Our common shares are thinly traded and, you may be unable to sell at or near ask prices or at all if you need to convert your Series B Preferred Stock and sell your shares to raise money or otherwise desire to liquidate such shares.

We cannot predict the extent to which an active public market for our common stock will develop or be sustained. Our common shares have historically been sporadically or “thinly-traded” on the “Over-The-Counter Bulletin Board,” meaning that the number of persons interested in purchasing our common shares at or near bid prices at any given time may be relatively small or non-existent. This situation is attributable to a number of factors, including the fact that Cyber is a small company which is relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk-averse and would be reluctant to follow an unproven company such as ours or purchase or recommend the purchase of our shares until such time as we became more seasoned and viable. As a consequence, there may be periods of several days or more when trading activity in our shares is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. We cannot give you any assurance that a broader or more active public trading market for our common stock will develop or be sustained, or that current trading levels will be sustained.