QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on May 31, 2002

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Collegis, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 7379 | 23-2414968 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

2300 Maitland Center Parkway

Suite 340

Maitland, Florida 32751

(407) 660-1199

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Thomas V. Huber

Collegis, Inc.

2300 Maitland Center Parkway

Suite 340

Maitland, Florida 32751

(407) 660-1199

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| R. Cabell Morris, Jr. Winston & Strawn 35 West Wacker Drive Chicago, Illinois 60601 (312) 558-5600 | Lawrence D. Levin, Esq. Katten Muchin Zavis Rosenman 525 West Monroe Street, Suite 1600 Chicago, Illinois 60661 (312) 902-5200 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee(2) | ||

|---|---|---|---|---|

| Common Stock, par value $0.01 per share | $75,000,000.00 | $6,900.00 | ||

- (1)

- Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933.

- (2)

- In accordance with Rule 457(p), the registration fee of $20,084.00 paid by Collegis, Inc. in connection with the filing of Registration Statement on Form S-1 (Reg. No. 333-60093) on July 29, 1998 that was subsequently withdrawn has been offset against the currently due registration fee.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information contained in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 31, 2002

Shares

Common Stock

Prior to this offering, there has been no public market for our common stock. The initial public offering price of the common stock is expected to be between $ and $ per share. We will apply to have our common stock quoted on The Nasdaq Stock Market's National Market under the symbol "CLGS."

We are selling shares of common stock and the selling stockholders are selling an aggregate of shares of common stock. We will not receive any of the proceeds from the shares of common stock sold by the selling stockholders.

The underwriters have an option to purchase a maximum of additional shares from certain selling stockholders to cover over-allotments of shares.

Investing in our common stock involves risks. See "Risk Factors" on page 6.

| | Price to Public | Underwriting Discounts and Commissions | Proceeds to Collegis | Proceeds to Selling Stockholders | ||||

|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | $ | ||||

| Total | $ | $ | $ | $ |

Delivery of the shares will be made on or about , 2002.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse First Boston | Banc of America Securities LLC |

| U.S. Bancorp Piper Jaffray | |

The date of this prospectus is , 2002

| | Page | |

|---|---|---|

| PROSPECTUS SUMMARY | 1 | |

| RISK FACTORS | 6 | |

| FORWARD-LOOKING STATEMENTS | 12 | |

| USE OF PROCEEDS | 13 | |

| DIVIDEND POLICY | 13 | |

| CAPITALIZATION | 14 | |

| DILUTION | 15 | |

| SELECTED FINANCIAL DATA | 16 | |

| UNAUDITED PRO FORMA FINANCIAL DATA | 17 | |

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 19 | |

| BUSINESS | 26 | |

| MANAGEMENT | 38 | |

| RELATED PARTY TRANSACTIONS | 47 | |

| PRINCIPAL AND SELLING STOCKHOLDERS | 48 | |

| DESCRIPTION OF CAPITAL STOCK | 51 | |

| SHARES ELIGIBLE FOR FUTURE SALE | 54 | |

| UNDERWRITING | 56 | |

| NOTICE TO CANADIAN RESIDENTS | 59 | |

| LEGAL MATTERS | 60 | |

| EXPERTS | 60 | |

| ADDITIONAL INFORMATION | 60 | |

| INDEX TO FINANCIAL STATEMENTS | F-1 |

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

Dealer Prospectus Delivery Obligation

Until , 2002 (25 days after the commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our common stock. We urge you to read this entire prospectus carefully, especially the risks of investing in our common stock discussed under "Risk Factors" and our financial statements and notes to those statements.

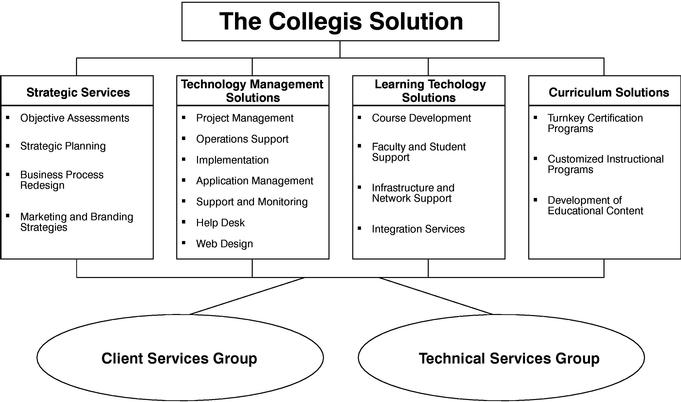

We are a leading provider of integrated strategic advisory, education delivery and technology management solutions to colleges and universities in the United States. Our solutions address an array of technology-related issues facing colleges and universities, including institutional strategic assessment and planning, implementation of learning technology initiatives, new curricula design and long-term management of technology resources. Our integrated service offering, rather than a single-point solution, enables us to deliver an identifiable return on investment to our clients from a strategic, operational and financial perspective.

We believe we are uniquely positioned to be the long-term strategic partner of choice to U.S. colleges and universities. Unlike technology vendors, systems integrators, broader consulting organizations and specialty service providers, we offer our clients all of the following:

- •

- dedicated focus and specialized expertise in higher education;

- •

- a comprehensive service offering that drives both revenue growth and cost savings;

- •

- objective assessment and advice due to our vendor neutral approach;

- •

- ongoing technology management with a focus on continuous improvement and accountability; and

- •

- size, stability and a proven track record of success within the higher education market.

Our business model captures best practices developed from our broad experience within the higher education market, providing a scalable resource base to benefit our clients. We utilize our centralized expertise to provide our clients with technical solutions that they could not easily develop or acquire on their own. At the same time, we tailor our on-site service offerings to the unique needs of each client, providing clear accountability and defined results from a single, comprehensive service partner.

We offer a full suite of academic and administrative services that enhance our clients' competitiveness and institutional reputations. We enable post-secondary institutions to:

- •

- maximize returns on technology and infrastructure investments;

- •

- generate revenue by attracting new students and developing new educational programs;

- •

- utilize emerging teaching, learning and student management technologies to better serve a growing, dispersed and increasingly technology-savvy student base; and

- •

- increase efficiencies in operations, information technology systems and administration.

Our mission is to partner with our clients to enhance the post-secondary educational experience for students, faculty and administrators.

1

A foundation of our business is the relationships that we develop with our clients under our technology management agreements, which typically have initial terms of three to seven years. Although these contracts are for a fixed term, they are ordinarily renewed or expanded prior to expiration. Our business model provides us with a significant component of recurring and predictable revenue with over 75% of our total annual revenue having been contractually committed at the beginning of each of the last five years. We achieved compound annual revenue growth of 31.0% from 1997 to 2001.

We offer our services to community, regional and national colleges and universities in the United States. According to the U.S. Department of Education, as of Spring 2001, there were approximately 4,100 of these institutions with aggregate annual operating budgets of over $270 billion serving approximately 15 million degree-seeking students. The DOE estimates that by 2010 post-secondary enrollments will increase to approximately 17 million degree-seeking students. We expect that enrollments will also rise as more working adults and other non-traditional students elect to continue their educations to obtain additional skills training or specialized certifications to increase their earning potential. The rising numbers of high school graduates, escalating enrollments by working adults and other non-traditional students and rapid growth in non-degree studies are straining the physical and faculty resources of many institutions, particularly mid-sized institutions and community colleges.

In addition to increasing enrollments, U.S. colleges and universities currently face a number of other challenges, including managing budgetary constraints, outdated technology and administrative systems, rising demand for technology-enhanced education and services and increased competition for students. A growing number of for-profit, post-secondary education providers has further intensified competition among schools for students. Although prevalent among institutions of all sizes, these challenges are particularly acute at mid-sized colleges and universities and community colleges in large, metropolitan areas. Currently, we focus primarily on this market segment because we believe these institutions can benefit most from our services.

We have a proven track record of delivering consistent results to our clients, helping them address their most critical business and technology issues. Our goal is to become the primary provider of integrated strategic advisory, education delivery and technology management solutions to post-secondary institutions of all sizes. We intend to pursue the following growth strategies to attain this goal:

- •

- expand our client base by capitalizing on our established reputation and existing relationships within the higher education market;

- •

- broaden and upgrade existing client relationships to enhance our position as their strategic and technology partner;

- •

- further develop our curriculum solutions division to create additional revenue sources for our clients; and

- •

- expand services through internal development and acquisitions to further enhance our value as a comprehensive solutions provider.

We were formed in Pennsylvania in 1986. On May 23, 1996, we reincorporated in Delaware. On August 31, 2001, we acquired Eduprise, Inc. in exchange for shares of our common stock.

Our principal executive offices are located at 2300 Maitland Center Parkway, Suite 340, Maitland, Florida 32751. Our telephone number at that location is (407) 660-1199. Our web site is http://www.collegis.com. The information contained on our web site is not incorporated by reference into this prospectus. References in this prospectus to "Collegis", "we", "us" and "our" refer to Collegis, Inc.

2

| Common stock offered by us | shares | |

Common stock offered by selling stockholders | shares | |

Common stock to be outstanding after this offering | shares | |

Use of proceeds | To provide working capital for our operations and to fund general corporate purposes. | |

Proposed Nasdaq National Market symbol | CLGS |

Except as otherwise indicated, the information in this prospectus assumes the inclusion of 731,994 shares of common stock issuable to certain selling stockholders for resale in this offering upon exercise of all outstanding warrants and does not assume inclusion of the following:

- •

- 5,105,837 shares of common stock issuable upon exercise of stock options outstanding as of May 15, 2002 at a weighted average exercise price of $2.94 per share;

- •

- shares of common stock available for issuance under our 2002 Stock Incentive Plan; and

- •

- any shares to be sold by any selling stockholders upon exercise of the underwriters' over-allotment option.

3

The following table summarizes our statement of operations during the periods indicated. You should read the data set forth below in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our financial statements and related notes thereto included elsewhere in this prospectus. The summary pro forma financial data have been derived from the unaudited pro forma financial data included elsewhere in this prospectus, which have been prepared by applying certain pro forma adjustments resulting from our acquisition of Eduprise, Inc. on August 31, 2001. The pro forma data assumes that the Eduprise acquisition occurred on January 1, 2001. The pro forma financial statements are presented for information purposes only and have been derived from, and should be read in connection with, our financial statements, including the notes thereto included elsewhere in this prospectus. For additional information regarding the pro forma financial statements, see "Unaudited Pro Forma Financial Data" included elsewhere in this prospectus.

| | Years ended December 31, | Three months ended March 31, | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 1999 | 2000 | 2001 | Pro Forma 2001 | 2001 | Pro Forma 2001 | 2002 | ||||||||||||||||

| | (in thousands, except per share data) | ||||||||||||||||||||||

| Statement of Income Data: | |||||||||||||||||||||||

| Revenue | $ | 49,707 | $ | 56,376 | $ | 70,359 | $ | 75,756 | $ | 15,851 | $ | 17,627 | $ | 22,790 | |||||||||

| Operating expenses: | |||||||||||||||||||||||

| Cost of services | 30,361 | 34,022 | 42,893 | 46,357 | 9,739 | 11,076 | 14,263 | ||||||||||||||||

| Selling, general and administrative | 11,526 | 12,539 | 18,709 | 24,987 | 3,757 | 5,874 | 5,909 | ||||||||||||||||

| Depreciation and amortization | 429 | 1,312 | 1,297 | 1,582 | 143 | 365 | 407 | ||||||||||||||||

| Other operating expenses | 702 | 797 | 679 | 922 | — | 230 | 115 | ||||||||||||||||

| Total operating expenses | 43,018 | 48,670 | 63,578 | 73,848 | 13,639 | 17,545 | 20,694 | ||||||||||||||||

| Operating income | 6,689 | 7,706 | 6,781 | 1,908 | 2,212 | 82 | 2,096 | ||||||||||||||||

| Interest expense (income), net | 354 | 282 | 58 | (135 | ) | 27 | (83 | ) | 52 | ||||||||||||||

| Income before income taxes | 6,335 | 7,424 | 6,723 | 2,043 | 2,185 | 165 | 2,044 | ||||||||||||||||

| Income tax expense | 2,535 | 2,972 | 2,676 | 818 | 874 | 66 | 818 | ||||||||||||||||

| Income from continuing operations | 3,800 | 4,452 | 4,047 | 1,225 | 1,311 | 99 | 1,226 | ||||||||||||||||

| Loss from discontinued operations(1) | 551 | — | — | — | — | — | — | ||||||||||||||||

| Net income | $ | 3,249 | $ | 4,452 | $ | 4,047 | $ | 1,225 | $ | 1,311 | $ | 99 | $ | 1,226 | |||||||||

Earnings Per Share — Diluted: | |||||||||||||||||||||||

| Income from continuing operations | $ | 0.25 | $ | 0.31 | $ | 0.26 | $ | 0.07 | $ | 0.09 | $ | 0.01 | $ | 0.07 | |||||||||

| Net income | $ | 0.21 | $ | 0.31 | $ | 0.26 | $ | 0.07 | $ | 0.09 | $ | 0.01 | $ | 0.07 | |||||||||

| Weighted average shares outstanding | 15,682 | 14,258 | 15,516 | 18,392 | 13,948 | 18,240 | 18,659 | ||||||||||||||||

Additional Financial Information: | |||||||||||||||||||||||

| Cash flows from operating activities | $ | 3,592 | $ | 7,007 | $ | 6,059 | $ | 846 | $ | (216 | ) | ||||||||||||

| Cash flows from investing activities | (833 | ) | (187 | ) | 3,203 | (321 | ) | (101 | ) | ||||||||||||||

| Cash flows from financing activities | (1,241 | ) | (3,879 | ) | (2,789 | ) | (128 | ) | (551 | ) | |||||||||||||

| EBITDA(2) | 7,118 | 9,018 | 8,078 | 2,355 | 2,503 | ||||||||||||||||||

- (1)

- In June 1999, we sold our learning technology solutions division to a group of investors who operated it as Eduprise, Inc. We have reflected the division's results through the time of disposition as a discontinued operation.

- (2)

- EBITDA equals income before interest, taxes, depreciation and amortization. EBITDA is presented because we believe that it provides a meaningful measurement from which to further analyze our results of operations. EBITDA should not be considered as an alternative to, nor is there any implication that it is more meaningful than, any measure of performance or liquidity as promulgated under accounting principles generally accepted in the United States.

4

The following table is a summary of our balance sheets as of December 31, 1999, 2000 and 2001 and March 31, 2002, and as adjusted assuming completion of this offering, as of March 31, 2002. To calculate the "As Adjusted" data, we have assumed the sale by us of shares of common stock in this offering at an assumed initial public offering price of $ per share, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us, and the application of the net proceeds from this offering.

| | December 31, | March 31, 2002 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 1999 | 2000 | 2001 | Actual | As Adjusted | ||||||||||

| | (in thousands) | ||||||||||||||

| Balance Sheet Data: | |||||||||||||||

| Cash and cash equivalents | $ | 5,296 | $ | 8,237 | $ | 14,710 | $ | 13,842 | $ | ||||||

| Working capital | 5,485 | 6,614 | 13,657 | 15,236 | |||||||||||

| Intangible assets | 681 | — | 10,343 | 10,223 | |||||||||||

| Total assets | 15,766 | 19,529 | 44,857 | 46,471 | |||||||||||

| Long-term obligations | 4,630 | 3,515 | 1,723 | 1,652 | |||||||||||

| Stockholders' equity | 2,471 | 4,611 | 29,407 | 30,753 | |||||||||||

5

This offering involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this prospectus, before deciding whether to invest in our common stock. If any of the following risks actually occurs, there could be a material adverse effect on our business, financial condition or results of operations. In this case, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Related to Our Business

We are dependent on the higher education industry.

Substantially all of our clients are colleges and universities. Unfavorable events or economic conditions adversely impacting the higher education market could have a material adverse effect on our business, financial condition and results of operations. For example, a general economic downturn could further intensify the competitive pressures facing colleges and universities that constitute a significant market for our services. Unfavorable events or adverse economic conditions could decrease our pool of potential clients or affect the willingness or financial ability of post-secondary institutions to engage us as a service provider.

If our existing clients do not renew or upgrade our services upon expiration of a contract or if we fail to persuade additional post-secondary institutions to use our services, our revenues and results of operations will be adversely affected.

Historically, when providing technology management services, we have formed long-term relationships with our clients. A significant portion of our revenues comes from renewals of or upgrades to existing contracts prior to their expiration. If our clients do not renew or upgrade expired contracts, our revenues and results of operations will be adversely affected. Because our services typically cost more than our clients have historically budgeted for such expenses, we must convince clients that our services will generate a sufficient return to justify the additional investment. Our ability to increase revenues will be impaired if we are unsuccessful in persuading additional colleges and universities to use our services.

A failure or inability to meet a client's expectations may harm our reputation and adversely affect our business.

We believe the higher education market is unique in the importance that colleges and universities place on reputation and trust. We depend on our existing relationships with clients and our reputation for high-quality professional services and integrity to attract and retain clients. Because client referrals are an important component in obtaining new engagements in the higher education market, a failure or inability to meet a client's expectations could seriously damage our reputation and adversely affect our ability to attract new business.

A reduction in government funding to our clients could have a negative effect on our revenues.

Federal and state governments provide various forms of direct and indirect support for higher education in the form of direct appropriations, subsidies, grants and guaranteed student loan programs. Accordingly, most of the colleges and universities that we serve or intend to serve depend substantially on government funding. The government appropriations process is often slow, unpredictable and subject to economic and political factors outside our control. During 2001, we derived 16% of our revenue from services provided to New Jersey-based community colleges and 16% from services provided to Florida-based community colleges. Curtailments or substantial reductions in government-funded or sponsored institutions and programs, or termination or renegotiation of government-funded contracts, could have a material adverse impact on or result in the delay or termination of our revenues

6

associated with these programs and contracts. Additionally, certain of our contracts provide that if the client is affected by a reduction in funding, then the amounts owed to us may be reduced, subject to a pro rata reduction in the level of services we provide.

Our business depends on the continued growth in the use of technology in higher education.

Our business is dependent upon continued growth in the use of technology in education by our clients and prospective clients. The successful use of new technology in education generally requires that students, faculty and administrators understand and accept the new technology. Institutions that have already invested substantial resources in traditional operations, systems, administration and educational techniques may be reluctant or slow to adopt a new approach if they perceive that the new technology will be rejected by students, faculty or administrators or that it may make some of their existing personnel and infrastructure obsolete. If the growth in the use of technology does not continue or continues more slowly than we expect, demand for our services may decrease and our revenues could decline.

Our success is dependent on our ability to attract and retain key personnel in a highly competitive marketplace.

Our business involves the delivery of professional and technical services and is labor intensive. Our performance depends on the continued service of our key technical employees and client managers and our ability to continue to attract, train, retain and motivate such personnel. Competition for such personnel is intense, particularly for highly skilled and experienced technology personnel who also have backgrounds serving higher education. Such technical personnel are in great demand and are likely to remain a limited resource for the foreseeable future. Competitive forces may require us to increase the compensation of our personnel. We may not be able to pass any such increase on to our clients. As a result, we may not be able to attract or retain sufficient numbers of highly skilled employees in the future. The inability to do so could have a material adverse effect upon our business, operating results or financial condition. Our ability to achieve our growth strategy also depends in large part upon the efforts of our senior management. The loss of the services of one or more of our key officers could adversely affect our business and operating results.

Our success depends on our ability to anticipate technological advances and meet evolving industry standards.

Our success will depend, in part, on our ability to anticipate and develop solutions that keep pace with changes in information technology, evolving industry standards and changing client needs and preferences. Our failure to anticipate and address these developments could have a material adverse effect on our business, financial condition or results of operations. In addition, services or technologies developed by third parties may render our services less competitive.

Potential liability claims from our services may adversely affect our business.

Our services, especially the management of a substantial portion of an institution's technology resources, involve key aspects of computer systems and are typically critical to a client's operations. Failures in a client's system, or a failure in our systems, could result in a claim for substantial damages against us, regardless of our actual responsibility or the terms in our client contracts. We maintain general liability insurance coverage, including coverage for errors and omissions. However, such coverage may not continue to be available on acceptable terms, or may not be available in sufficient amounts to cover one or more large claims. The successful assertion of one or more large claims against us that exceed available insurance coverage, or the occurrence of changes in our insurance policies, including premium increases or the imposition of large deductible or co-insurance requirements, could each have a material adverse effect on our business, financial condition and results

7

of operations. Although we attempt to contractually limit our liability, we may be legally prevented from doing so with respect to certain clients.

Our failure to accurately estimate the expenses required to complete our contracts may adversely impact our financial condition and results of operations.

Substantially all of our revenues are generated under long-term contracts. If we fail to accurately estimate the resources and related expenses required for a contract or fail to complete our contractual obligations in a manner consistent with the budget upon which the contract was based, our business, financial condition and results of operations could be adversely impacted.

The variability and length of the sales cycle for our services may make our operating results unpredictable and volatile.

The period between our initial contact with a potential customer and the purchase of our services by that customer typically ranges from three to nine months. Factors that contribute to our long sales cycle include:

- •

- the large size and scope of our potential engagement;

- •

- our need to educate potential clients about the benefits of our services;

- •

- competitive evaluations by clients; and

- •

- the client's internal budgeting and approval processes.

Our long sales cycle makes it difficult for us to predict if and when a potential engagement will actually occur.

Our revenues, operating results and profitability will fluctuate from quarter to quarter, which may result in increased volatility of our share price.

Variations in our revenues, operating results and profitability from quarter to quarter have occurred in the past, and are likely to occur in the future. These variations may result from a number of factors, including:

- •

- the timing, size and scope of new client engagements;

- •

- the termination of, or failure to renew or upgrade existing client engagements;

- •

- fluctuations in our reported gross profit due to expenses in excess of budgeted amounts; and

- •

- general economic conditions.

Due to the foregoing factors, it is possible that in some future periods our results of operations will be below the expectations of public market analysts and investors. This may lead to volatility in our share price.

Our success is dependent upon our relationships and contracts with certain key clients.

We have derived and expect to continue to derive a significant portion of our revenue from a relatively limited number of clients. Our top five clients accounted for approximately 24.3% of our revenue in 2001. For the three months ended March 31, 2002, our top five clients accounted for approximately 26.2% of our revenue. The loss of any one or more of our major clients could have a material adverse effect on our business, financial condition or results of operations.

8

We may be unable to manage our growth, which may harm our business.

We continue to experience significant growth, which has placed, and could continue to place, a strain on our financial, managerial and human resources. From December 31, 1997 through May 15, 2002, the number of our full-time employees increased from approximately 290 to over 780. We expect that the number of our employees will continue to increase for the foreseeable future and such increases may occur in large groups as a result of signing large client contracts. Our future performance and profitability will depend on our ability to integrate new employees into our workforce successfully, particularly in light of the decentralized nature of our workforce. To manage our growth, we must continue to implement and improve our managerial controls and procedures along with our operational and financial systems. We may not have made adequate allowances for the costs associated with this expansion, our systems, procedures or controls may be inadequate to support our operations and our management may be unable to successfully offer and expand our services. If we are unable to manage our growth effectively, our business, results of operations and financial condition could be materially adversely affected.

We operate in a highly competitive market and increasing competition could result in decreased demand for our services, lower margins and loss of market share.

The market for professional and technology management services is competitive, highly fragmented and subject to rapid technological change. Our primary competitive challenge is overcoming the initial resistance to our services from the internal information technology departments of our prospective clients. We compete for clients and experienced personnel with a number of companies having significantly greater financial, technical and marketing resources and revenues than we have. Our competitors include systems consulting and integration services providers, software and professional service organizations and general management consulting firms. Current and potential competitors may make strategic acquisitions or establish cooperative relationships to increase their service offerings to post-secondary institutions. Accordingly, it is possible that new competitors or alliances may emerge and rapidly gain significant market share. Increased competition could result in downward pricing pressures and loss of market share for us.

Our failure to successfully integrate any future acquisitions could strain our managerial, operational and financial resources.

We may, from time to time, pursue acquisitions of businesses, products or technologies that complement or expand our existing business to meet client and market demands for new services or enhanced skills. Our success in executing our acquisition strategy will depend on our ability to identify potential targets that meet our criteria, including a reputation as a leading service provider with strong client relationships and a complementary culture. Our management has had limited experience in making acquisitions, and we may not be able to complete the acquisitions on acceptable terms or we may not be able to successfully integrate any acquired assets or businesses into our operations. Acquisitions involve a number of risks, including the diversion of management's attention from day-to-day operations to the assimilation of the operations and personnel of the acquired companies and the incorporation of acquired operations, customer lists, products or technologies. In addition, we may require additional debt or equity financing to consummate future acquisitions, which financing may not be available on terms satisfactory to us, if at all. We may issue shares of our common stock as part of the consideration for an acquisition, which may dilute our earnings per share. We cannot assure you that any acquisitions will be successfully completed or that, if one or more acquisitions is completed, the acquired businesses, products or technologies will generate sufficient revenue to offset the associated costs or other adverse effects.

9

Misuse or misappropriation of our proprietary rights could adversely affect our results of operations.

Although we do not develop software or systems for license, our performance is in part dependent upon our internal information and communication systems, databases, tools, and the methodologies that we have developed to serve our clients. We have no patents and consequently, we rely on a combination of nondisclosure and other contractual arrangements and copyright, trademark and trade secret laws to protect our proprietary systems, information and procedures. In addition, we enter into and rely upon confidentiality agreements with our employees and clients and limit access to and distribution of our proprietary information. The steps that we take to protect our proprietary rights may not be adequate to prevent the misappropriation of our proprietary rights. In addition, we may not detect unauthorized use or take appropriate steps to enforce our proprietary rights. Ownership of intellectual property created in providing services to our clients is the subject of negotiation and is frequently assigned to the client. We generally retain the right to use any intellectual property that is developed during a client engagement that is of general applicability and is not specific to the client engagement. Issues relating to the ownership of and rights to use intellectual property developed during the course of a client engagement can be complicated, and clients may demand assignment of ownership or restrict the use of the work that we produce in the future. In addition, disputes may arise that affect our ability to resell or reuse such intellectual property.

Risks Related to this Offering

There has been no prior public market for our common stock.

Prior to this offering, there has been no public market for our common stock. We cannot predict the extent to which investor interest in our common stock will lead to the development of an active trading market or how liquid that market might become. The market price of the common stock may decline below the initial public offering price. The initial public offering price for the shares has been determined by negotiations between us and the representatives of the underwriters and may not be indicative of prices that will prevail in the trading market following the completion of this offering.

The trading price of our common stock could fluctuate significantly.

The stock market has experienced significant price and volume fluctuations that have affected the market prices of companies in recent years. These fluctuations may continue to occur and disproportionately impact our stock price. Factors that could have a significant impact on the market price of our common stock include:

- •

- actual or anticipated variation in quarterly operating results;

- •

- failure to achieve, or changes in, financial estimates or recommendations of securities analysts;

- •

- a downturn in the higher education market generally;

- •

- additions or departures of key personnel;

- •

- announcements by us of significant acquisitions, strategic partnerships, joint ventures or capital commitments;

- •

- reductions in funding for post-secondary institutions; and

- •

- general market conditions.

In particular, the realization of any of the risks described in these "Risk Factors" could have a dramatic and material adverse impact on the market price of our common stock. In the past, following periods of volatility in the market price of a company's securities, securities class-action litigation has often been instituted. This type of litigation could result in substantial costs and a diversion of

10

management's attention and resources, which could materially affect our business, financial condition or results of operations.

The future sale of shares of our common stock by existing stockholders may negatively affect our stock price.

If our existing stockholders sell substantial amounts of our common stock, including shares issuable upon the exercise of outstanding options in the public market following this offering, the market price of our common stock could fall. These sales also might make it more difficult for us to sell equity securities in the future at a time and price that we deem appropriate. After this offering, we will have outstanding shares of common stock. Of these shares, the shares being offered in this offering will be freely tradable. Our directors, executive officers, existing stockholders and warrant holders and substantially all of our option holders have agreed to the lock-up restrictions described in "Underwriting." After these lock-up agreements expire 180 days from the date of this prospectus, an additional shares will be eligible for sale in the public market. Sales of substantial amounts of common stock (including shares issued in connection with future acquisitions that may be issued with registration rights), or the availability of such shares for sale, may adversely affect the prevailing market price for the common stock and could impair our ability to obtain additional capital through an offering of our equity securities.

You will incur immediate and substantial dilution and may experience further dilution.

The initial public offering price of our common stock is substantially higher than the pro forma net tangible book value per share of the outstanding common stock immediately after the offering. If you purchase common stock in this offering, you will incur immediate and substantial dilution in the pro forma net tangible book value per share of the common stock from the price you pay for the common stock. To the extent outstanding options and warrants to purchase common stock are exercised, there will be further dilution. Moreover, there can be no assurance that we will not require additional funds to support our working capital requirements or for other purposes, in which case we may seek to raise such additional funds through public or private equity financings or from other sources. Any such financing may result in additional dilution to our stockholders.

Control by principal stockholders could adversely affect our stockholders.

Upon completion of this offering, certain of our existing shareholders will continue to beneficially own a significant percentage of our outstanding common stock and will have substantial ability to control matters submitted to our stockholders for approval, including the election and removal of directors and any merger, consolidation or sale of all or substantially all of our assets, and to control our management and affairs. Accordingly, this concentration of ownership may have the effect of delaying, deferring or preventing a change in control of us, impeding a merger, consolidation, takeover or other business combination involving us or discouraging a potential acquirer from making a tender offer or otherwise attempting to obtain control of us, which in turn could materially adversely affect the market price of our common stock.

A third-party could be prevented from acquiring your shares of stock at a premium to the market price because of our anti-takeover provisions in our charter and bylaws and Delaware law.

The following provisions of our certificate of incorporation and by-laws may discourage, delay or prevent a merger or acquisition that you may consider favorable, including transactions in which you might otherwise receive a premium for your shares:

- •

- the ability of our board of directors to issue preferred stock, and determine its terms, without a stockholder vote;

11

- •

- our classified board of directors, which effectively prevents stockholders from electing a majority of the directors at any one annual meeting of stockholders;

- •

- the requirement that any business combination transaction be approved by the holders of at least 662/3% of our outstanding common stock;

- •

- the prohibition against stockholder actions by written consent; and

- •

- the inability of stockholders to call a special meeting of stockholders.

In addition, some provisions of Delaware law, particularly the "business combinations" statute in Section 203 of the Delaware General Corporation Law, may also discourage, delay or prevent someone from acquiring us or merging with us. See "Description of Capital Stock" for detailed information on these provisions.

We have broad discretion to use the proceeds from this offering, and our use of these proceeds may not yield a favorable return.

We have not identified specific uses for a significant portion of the net proceeds of this offering. Accordingly, our management will have significant flexibility in applying the net proceeds of this offering. Although we have no plans, commitments or agreements with respect to any material acquisitions as of the date of this prospectus, we may seek acquisitions of businesses that are complementary to ours, and a portion of the net proceeds may be used for such acquisitions.

Because it is unlikely that we will pay dividends, you will only be able to benefit from holding our stock if the stock price appreciates.

We have never declared or paid any cash dividends on our capital stock and do not anticipate paying any cash dividends in the foreseeable future. We presently intend to retain any future earnings for funding growth and, therefore, do not expect to pay any dividends in the foreseeable future. As a result of not collecting a dividend, you will not experience a return on your investment, unless the price of our common stock appreciates and you sell your shares of common stock.

This prospectus contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are subject to the safe harbor provisions of the Reform Act. Such forward-looking statements are contained principally in the sections entitled "Prospectus Summary," "Risk Factors," "Management's Discussion and Analysis of Results of Operations and Financial Condition" and "Business." These forward-looking statements include, but are not limited to, statements about our plans, objectives, expectations and intentions and other statements contained in this prospectus that are not historical facts.

When used in this prospectus, the words "anticipate," "believe," "continue," "could," "estimate," "expect," "intend," "may," "plan," "seek," "should," "will" or "would" or the negative of these terms or similar expressions are generally intended to identify forward-looking statements. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements, including our plans, objectives, expectations and intentions and other factors discussed under "Risk Factors." Also, these forward-looking statements represent our estimates and assumptions only as of the date of this prospectus. We undertake no obligation to update publicly any forward-looking statements for any reason, even if new information becomes available or other events occur in the future.

12

We estimate that our net proceeds from the sale of the shares of common stock we are offering pursuant to this prospectus will be approximately $ , at an assumed initial public offering price of $ per share and after deducting the underwriting discounts and commissions and our estimated offering expenses. We will not receive any proceeds from the sale of shares by the selling stockholders.

The principal purposes of this offering are to provide working capital to expand our operations and to fund general corporate purposes. In addition, we may use a portion of the net proceeds to acquire or invest in complementary businesses, although we currently have no commitments or agreements with respect to any such transactions. Pending such uses, the net proceeds will be invested in short-term investment-grade instruments, certificates of deposit or direct or guaranteed obligations of the U.S. government. See "Risk Factors — We have broad discretion to use the proceeds from this offering, and our use of these proceeds may not yield a favorable return" for a description of several risks relating to our use of proceeds.

We have never declared or paid any cash dividends on our capital stock and do not anticipate paying any cash dividends in the foreseeable future. We presently intend to retain future earnings, if any, to finance the expansion of our business. Any payments of dividends will be at the discretion of our board of directors and will be dependent upon our financial condition, results of operations, capital requirements, general business conditions and other factors that our board of directors may deem relevant.

13

The following table sets forth our actual and our as adjusted capitalization as of March 31, 2002. Our as adjusted capitalization gives effect to:

- •

- the sale of shares of common stock offered by us pursuant to this prospectus at an assumed offering price per share of $ , after deducting the underwriting discounts and commissions and our estimated offering expenses; and

- •

- the issuance of 731,994 shares of common stock to certain selling stockholders for resale in this offering upon exercise of all outstanding warrants for an aggregate consideration of $1.1 million.

This table should be read in conjunction with "Selected Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the financial statements and the notes to those statements included elsewhere in this prospectus.

| | As of March 31, 2002 | |||||||

|---|---|---|---|---|---|---|---|---|

| | Actual | As Adjusted | ||||||

| | (in thousands, except share and per share data) | |||||||

| Current maturities of long-term debt | $ | 1,822 | ||||||

| Long-term debt | 1,652 | |||||||

| Stockholders' equity: | ||||||||

| Preferred stock, $0.01 par value per share; 1,000,000 shares authorized; no shares issued and outstanding | — | |||||||

| Common stock, $0.01 par value per share; 25,000,000 shares authorized; 17,378,236 shares issued and outstanding; shares issued and outstanding as adjusted | 174 | |||||||

| Warrants | 438 | |||||||

| Paid-in capital | 28,627 | |||||||

| Deferred compensation | (793 | ) | ||||||

| Treasury stock | (11,731 | ) | ||||||

| Retained earnings | 14,038 | |||||||

| Total stockholders' equity | 30,753 | |||||||

| Total capitalization | $ | 34,227 | ||||||

The preceding table does not include:

- •

- 5,105,837 shares of common stock issuable upon exercise of stock options outstanding as of May 15, 2002 at a weighted average exercise price of $2.94 per share;

- •

- shares of common stock available for issuance under our 2002 Stock Incentive Plan; and

- •

- any shares to be sold by any selling stockholder upon exercise of the underwriters' over-allotment option.

14

Our net tangible book value as of March 31, 2002 was approximately $20.5 million or $1.18 per share, based on the number of shares of common stock outstanding as of March 31, 2002. Net tangible book value per share is equal to the amount of our total tangible assets less total liabilities, divided by the number of outstanding shares of common stock. After giving effect to the sale of common stock offered by us pursuant to this prospectus at an assumed initial public offering price of $ per share, our receipt of the estimated net proceeds from this offering and the issuance of 731,994 shares of common stock upon the exercise of all outstanding warrants, our pro forma net tangible book value as of March 31, 2002 would have been approximately $ million, or $ per share. This represents an immediate increase in pro forma net tangible book value of $ per share to existing stockholders and an immediate dilution of $ per share to new investors purchasing shares of common stock in this offering. The following table illustrates this per share dilution:

| Assumed initial public offering price per share | $ | ||||||

Net tangible book value per share at March 31, 2002 | $ | 1.18 | |||||

Increase per share attributable to new investors in this offering | |||||||

Pro forma net tangible book value per share after this offering | |||||||

Net tangible book value dilution per share to new investors in this offering | $ | ||||||

The following table summarizes the differences between existing stockholders and the new investors with respect to the number of shares of common stock purchased from us, the total consideration paid and the average price per share paid before deducting the underwriting discounts and commissions and our estimated offering expenses.

| | Shares Purchased | Total Consideration | | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Average Price Per Share | |||||||||||

| | Number | Percent | Amount | Percent | ||||||||

| Existing stockholders | % | $ | % | $ | ||||||||

| New investors | $ | |||||||||||

| Total | 100.0 | % | $ | 100.0 | % | |||||||

The foregoing discussion and table assumes the issuance of 731,994 shares of common stock to certain selling stockholders for resale in this offering upon exercise of all outstanding warrants. The foregoing discussion and table assumes no exercise of any outstanding stock options. As of May 15, 2002, there were 5,105,837 options outstanding to purchase common stock. To the extent that any of these options are exercised, there will be further dilution to the new investors.

If the underwriters exercise their over-allotment option in full, the following will occur:

- •

- the number of shares of our common stock held by existing stockholders will decrease to , or approximately % of the total number of shares of our common stock outstanding after this offering;

- •

- the number of shares of our common stock held by new investors will increase to , or approximately % of the total number of shares of our common stock outstanding after this offering; and

- •

- pro forma net tangible book value will increase to $ per share to existing stockholders, and there will be an immediate dilution in pro forma net tangible book value of $ per share to new investors.

15

The following selected financial data is qualified by reference to, and should be read in conjunction with, our financial statements and the notes to such statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations" included elsewhere in this prospectus. The selected statement of income data presented for the years ended December 31, 1999, 2000 and 2001 and the balance sheet data as of December 31, 2000 and 2001, are derived from our audited financial statements and are included elsewhere in this prospectus. The selected statement of income data presented for the years ended December 31, 1997 and 1998 and the balance sheet data as of December 31, 1997, 1998 and 1999 have been derived from our audited financial statements not included in this prospectus. The selected statement of income data for the three months ended March 31, 2001 and 2002 and the balance sheet data as of March 31, 2002 are derived from our unaudited financial statements included elsewhere in this prospectus. These unaudited financial statements have been prepared on the same basis as our audited financial statements and, in our opinion, include all material adjustments, consisting only of normal recurring adjustments, necessary to present fairly this unaudited financial information. Such financial information may not be indicative of results for a full year.

| | Years Ended December 31, | Three Months Ended March 31, | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 1997 | 1998 | 1999 | 2000 | 2001 | 2001 | 2002 | |||||||||||||||

| | (in thousands, except per share data) | |||||||||||||||||||||

| Statement of Income Data: | ||||||||||||||||||||||

| Revenue | $ | 23,882 | $ | 36,890 | $ | 49,707 | $ | 56,376 | $ | 70,359 | $ | 15,851 | $ | 22,790 | ||||||||

| Operating expenses: | ||||||||||||||||||||||

| Cost of services | 14,147 | 21,929 | 30,361 | 34,022 | 42,893 | 9,739 | 14,263 | |||||||||||||||

| Selling, general and administrative | 6,002 | 8,751 | 11,526 | 12,539 | 18,709 | 3,757 | 5,909 | |||||||||||||||

| Depreciation and amortization | 153 | 229 | 429 | 1,312 | 1,297 | 143 | 407 | |||||||||||||||

| Other operating expenses(1) | 487 | 3,357 | 702 | 797 | 679 | — | 115 | |||||||||||||||

| Total operating expenses | 20,789 | 34,266 | 43,018 | 48,670 | 63,578 | 13,639 | 20,694 | |||||||||||||||

| Operating income | 3,093 | 2,624 | 6,689 | 7,706 | 6,781 | 2,212 | 2,096 | |||||||||||||||

| Interest expense, net | 869 | 650 | 354 | 282 | 58 | 27 | 52 | |||||||||||||||

| Income before income taxes | 2,224 | 1,974 | 6,335 | 7,424 | 6,723 | 2,185 | 2,044 | |||||||||||||||

| Income tax expense | 938 | 802 | 2,535 | 2,972 | 2,676 | 874 | 818 | |||||||||||||||

| Income from continuing operations | 1,286 | 1,173 | 3,800 | 4,452 | 4,047 | 1,311 | 1,226 | |||||||||||||||

| Loss from discontinued operations(2) | — | 53 | 551 | — | — | — | — | |||||||||||||||

| Net income(3) | $ | 1,016 | $ | 1,120 | $ | 3,249 | $ | 4,452 | $ | 4,047 | $ | 1,311 | $ | 1,226 | ||||||||

| Earnings Per Share — Diluted: | ||||||||||||||||||||||

| Income from continuing operations | $ | 0.09 | $ | 0.08 | $ | 0.25 | $ | 0.31 | $ | 0.26 | $ | 0.09 | $ | 0.07 | ||||||||

| Net income | $ | 0.07 | $ | 0.07 | $ | 0.21 | $ | 0.31 | $ | 0.26 | $ | 0.09 | $ | 0.07 | ||||||||

| Weighted average shares outstanding | 13,682 | 14,995 | 15,682 | 14,258 | 15,516 | 13,948 | 18,659 | |||||||||||||||

| | As of December 31, | | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 31, 2002 | |||||||||||||||||

| | 1997 | 1998 | 1999 | 2000 | 2001 | |||||||||||||

| | (in thousands) | |||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||

| Cash and cash equivalents | $ | 3,568 | $ | 3,778 | $ | 5,296 | $ | 8,237 | $ | 14,710 | $ | 13,842 | ||||||

| Working capital | 2,793 | 4,491 | 5,485 | 6,614 | 13,657 | 15,236 | ||||||||||||

| Intangible assets | — | 569 | 681 | — | 10,343 | 10,223 | ||||||||||||

| Total assets | 8,257 | 12,480 | 15,766 | 19,529 | 44,857 | 46,471 | ||||||||||||

| Long-term obligations | 8,150 | 6,900 | 4,630 | 3,515 | 1,723 | 1,652 | ||||||||||||

| Stockholders' equity (deficit) | (4,340 | ) | 119 | 2,471 | 4,611 | 29,407 | 30,753 | |||||||||||

- (1)

- Other operating expenses consisted of corporate office relocation expense in 1997, stock compensation expenses ($2.7 million) and terminated transaction expense ($0.6 million) in 1998, terminated transaction expense in 1999, and stock compensation expense in 2000 and 2001.

- (2)

- In June 1999, we sold our learning technology solutions division to a group of investors who operated it as Eduprise, Inc. We have reflected the division's results through the time of disposition as a discontinued operation.

- (3)

- Results of operations for the year ended December 31, 1997 included an extraordinary loss of $270 on the early extinguishment of debt.

16

UNAUDITED PRO FORMA FINANCIAL DATA

On August 31, 2001, we acquired all of the outstanding capital stock of Eduprise, Inc. Eduprise's historical data for the eight months ended August 31, 2001 are derived from Eduprise's financial statements that are included elsewhere in this prospectus. Eduprise's historical data for the three months ended March 31, 2001 are derived from Eduprise's financial statements that are not included in this prospectus. The pro forma data assumes that this transaction occurred as of January 1, 2001 for both periods.

The total purchase price for Eduprise was approximately $20.3 million, consisting of shares of common stock ($19.4 million), other equity securities ($0.7 million) and related costs ($0.3 million). The purchase price was allocated to tangible assets ($9.5 million), intangible assets ($1.4 million), which will be amortized over three years, and goodwill ($9.4 million).

The pro forma financial information should be read in conjunction with our historical financial statements for the year ended December 31, 2001, the unaudited historical financial statements for the three months ended March 31, 2001 and the unaudited historical financial information for Eduprise for the eight months ended August 31, 2001, included elsewhere in this prospectus. The pro forma information is not necessarily indicative of future earnings or earnings that would have been reported for the periods presented had the Eduprise acquisition been completed at the beginning of the earliest period presented. Further, the unaudited pro forma income statement for the three months ended March 31, 2001 should not necessarily be taken as an indication of the earnings for a full year.

| | Year Ended December 31, 2001 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Collegis Historical | Eduprise 8 months ended August 31, 2001 | Pro Forma Adjustments | Pro Forma | ||||||||||

| | (in thousands, except per share data) | |||||||||||||

| Revenue | $ | 70,359 | $ | 5,684 | $ | (287 | )(1) | $ | 75,756 | |||||

| Operating expenses: | ||||||||||||||

| Cost of services | 42,893 | 3,751 | (287 | )(1) | 46,357 | |||||||||

| Selling, general and administrative | 18,709 | 6,278 | — | 24,987 | ||||||||||

| Depreciation and amortization | 1,297 | 285 | — | (2) | 1,582 | |||||||||

| Stock compensation | 679 | 180 | 63 | (3) | 922 | |||||||||

| Total operating expenses | 63,578 | 10,494 | (224 | ) | 73,848 | |||||||||

| Operating income (loss) | 6,781 | (4,810 | ) | (63 | ) | 1,908 | ||||||||

| Interest expense (income), net | 58 | (193 | ) | — | (135 | ) | ||||||||

| Income (loss) before income taxes | 6,723 | (4,617 | ) | (63 | ) | 2,043 | ||||||||

| Income tax expense (benefit) | 2,676 | — | (1,858 | )(4) | 818 | |||||||||

| Net income (loss) | $ | 4,047 | $ | (4,617 | ) | $ | 1,795 | $ | 1,225 | |||||

| Earnings per share: | ||||||||||||||

| Basic | $ | 0.28 | $ | 0.07 | ||||||||||

| Weighted average shares outstanding | 14,504 | 17,380 | ||||||||||||

| Diluted | $ | 0.26 | $ | 0.07 | ||||||||||

| Weighted average shares outstanding | 15,516 | 18,392 | ||||||||||||

17

| | Three Months Ended March 31, 2001 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Collegis Historical | Eduprise Historical | Pro Forma Adjustments | Pro Forma | ||||||||||

| | (in thousands, except per share data) | |||||||||||||

| Revenue | $ | 15,851 | $ | 1,876 | $ | (100 | )(1) | $ | 17,627 | |||||

| Operating expenses: | ||||||||||||||

| Cost of services | 9,739 | 1,437 | $ | (100 | )(1) | 11,076 | ||||||||

| Selling, general and administrative | 3,757 | 2,117 | — | 5,874 | ||||||||||

| Depreciation and amortization | 143 | 102 | 120 | (2) | 365 | |||||||||

| Stock compensation | — | 68 | 162 | (3) | 230 | |||||||||

| Total operating expenses | 13,639 | 3,724 | 182 | 17,545 | ||||||||||

| Operating income (loss) | 2,212 | (1,848 | ) | (282 | ) | 82 | ||||||||

| Interest expense (income), net | 27 | (110 | ) | — | (83 | ) | ||||||||

| Income (loss) before income taxes | 2,185 | (1,738 | ) | (282 | ) | 165 | ||||||||

| Income tax expense (benefit) | 874 | — | (808 | )(4) | 66 | |||||||||

| Net income (loss) | $ | 1,311 | $ | (1,738 | ) | $ | 526 | $ | 99 | |||||

| Earnings per share: | ||||||||||||||

| Basic | $ | 0.10 | $ | 0.01 | ||||||||||

| Weighted average shares outstanding | 13,075 | 17,367 | ||||||||||||

| Diluted | $ | 0.09 | $ | 0.01 | ||||||||||

| Weighted average shares outstanding | 13,948 | 18,240 | ||||||||||||

- (1)

- During the periods presented, we sold certain services that were performed by Eduprise under a subcontract arrangement. This adjustment eliminates the service revenue recognized by Eduprise and the cost of service recorded by us in the period from January 1, 2001 to August 31, 2001 and in the three months ended March 31, 2001.

- (2)

- Because we recorded a full year of intangible asset amortization related to the Eduprise acquisition in the year ended December 31, 2001, no adjustment is required for the pro forma year ended December 31, 2001. For the three months ended March 31, 2001, the adjustment reflects amortization of intangible asset related to the Eduprise acquisition.

- (3)

- This adjustment increases stock compensation for the amortization of the costs of unvested replacement options issued to former Eduprise employees and deferred compensation related to options granted to our employees (aggregating $243 for the eight months ended August 31, 2001 and aggregating $230 for the three months ended March 31, 2001), and eliminates the stock compensation recorded by Eduprise prior to the acquisition.

- (4)

- This adjustment relates to the tax effect of the above adjustments and the recognition of a tax benefit for the loss incurred by Eduprise.

18

MANAGEMENT'S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read with "Selected Financial Data" and our financial statements and notes included elsewhere in this prospectus. The discussion in this prospectus contains forward-looking statements that involve risks and uncertainties, such as statements of our plans, objectives, expectations and intentions. The cautionary statements made in this prospectus should be read as applying to all related forward-looking statements wherever they appear in this prospectus. Our actual results could differ materially from those discussed here. Factors that could cause or contribute to these differences include those discussed in "Risk Factors," as well as those discussed elsewhere in this prospectus.

Overview

We are a leading provider of integrated strategic advisory, education delivery and technology management solutions to colleges and universities in the United States. Our solutions address an array of technology-related issues facing colleges and universities, including institutional strategic assessment and planning, implementation of learning technology initiatives, new curricula design and long-term management of technology resources.

Revenue recognition. Substantially all of our revenue is generated through the delivery of services under multi-year, fixed-priced contracts. We do not sell hardware or software. Revenue is recognized as services are provided, primarily on a straight-line basis over each contract year. Revenue from contracts to provide strategic consulting, instructional design and support, course development and program management services is recognized as the services are performed. For these contracts, changes in scope of services to be provided, estimates of percentage completed or profitability may result in revisions to revenue and are recognized in the period in which such revisions are determined. Revenue includes reimbursable expenses charged to the client in accordance with Emerging Issues Task Force Topic No. D-103. Reimbursable expenses have averaged approximately 4% of revenue. In the early periods of new contracts, the percentage of reimbursable expenses to revenue is slightly higher. Billings are based on payment schedules that may differ from the timing of revenue recognition. These differences are reflected in our balance sheets as either unbilled receivables on contracts or deferred revenue.

Fixed-price contracts subject us to the risk of cost overruns and inflation. This risk is partially mitigated by contract clauses that allow for fee increases in the event of inflation and by the active management of individual project costs by our on-site, regional and corporate management teams. To date, we have not incurred a loss under a fixed-price contract.

Because our services are provided under multi-year agreements, a substantial portion of our revenue is committed at the beginning of the year. Committed revenue at the beginning of each of the last five years represented in excess of 75% of the total annual revenue for such year. Remaining revenues are derived from new client engagements and additional services sold to existing clients. As of January 1, 2002, we had approximately $74.9 million of full year 2002 revenue contracted for under multi-year agreements.

Cost of services. Cost of services consists of direct costs to provide services to our customers and primarily includes salaries and wages and related fringe benefits of our employees directly serving customers through our strategic services, client services and technical services groups. Cost of services also includes any cost of subcontractors and outside consultants and other direct costs, such as travel expenses.

Selling, general and administrative. Selling, general and administrative expenses include the salaries and wages and related fringe benefits of our employees not performing work directly for customers, and occupancy and other costs necessary to support those employees. Among the functions included in these expenses are sales and marketing, corporate services (accounting, information systems support,

19

legal, human resources and recruiting) and senior management and its support staff. In future periods we expect our general and administrative expenses to increase as a result of our incurring customary costs associated with being a public company.

Accounting for Eduprise Acquisition

We acquired all of the capital stock of Eduprise, Inc. on August 31, 2001 in exchange for 4,291,950 shares of our common stock and the assumption of options and warrants to purchase 342,238 shares of our common stock. Eduprise became an integral part of our learning technology services division. In June 1999, we sold our learning technology solutions division to a group of investors who operated it as Eduprise. In 1998 and 1999, we reflected the division's results as a discontinued operation. After our disposition of the division, we continued to provide related services under our existing contracts through a subcontract with Eduprise. Prior to June 1999, the division was engaged in the development of instructional and Internet software applications. Subsequent to our disposition, Eduprise discontinued its focus on the development of software applications and shifted its focus to developing and enhancing services related to the integration of technology into the learning process. The results of Eduprise have been included in our financial statements since September 1, 2001. For more detailed information about our acquisition of Eduprise, see "Unaudited Pro Forma Financial Data" and "Business — Eduprise Acquisition" included elsewhere in this prospectus.

The acquisition of Eduprise was accounted for in accordance with Statement of Financial Accounting Standard ("SFAS") No. 141"Business Combinations" ("SFAS 141"), which requires all business combinations initiated after June 30, 2001 to be accounted for under the purchase method. SFAS 141 also sets forth guidelines for applying the purchase method of accounting in the determination of intangible assets, including goodwill acquired in a business combination, and expands financial disclosures concerning business combinations. The assets acquired and liabilities assumed were recorded at estimated fair values as determined by our management, based on information available and on assumptions as to future operations. We obtained independent appraisals of the fair values of the acquired property and equipment and identified intangible assets and their remaining useful lives. We also completed the review and determination of the fair values of the other assets acquired and liabilities assumed.

Critical Accounting Policies

Our financial statements are prepared in accordance with accounting principles generally accepted in the United States, which require us to make estimates and assumptions. Our most critical accounting policies relate to revenue recognition (discussed above), compensation costs related to our stock-based compensation plans and the assumptions and estimates used in accounting for our acquisition of Eduprise, particularly those related to the fair value of certain acquired assets including the intangible asset related to contractual customer relationships and a deferred tax asset related to operating loss carryforwards.

20

Results of Operations

The following table sets forth, for the periods indicated, statements of income data as a percentage of revenue:

| | Years Ended December 31, | Three Months Ended March 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 1999 | 2000 | 2001 | 2001 | 2002 | ||||||||

| Revenue | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||

| Operating expenses: | |||||||||||||

| Cost of services | 61.1 | 60.3 | 61.0 | 61.4 | 62.6 | ||||||||

| Selling, general and administrative | 23.2 | 22.2 | 26.6 | 23.7 | 25.9 | ||||||||

| Depreciation and amortization | 0.9 | 2.3 | 1.8 | 0.9 | 1.8 | ||||||||

| Stock compensation expenses | — | 1.4 | 1.0 | — | 0.5 | ||||||||

| Terminated transaction costs | 1.4 | — | — | — | — | ||||||||

| Total operating expenses | 86.5 | 86.3 | 90.4 | 86.0 | 90.8 | ||||||||

| Operating income | 13.5 | 13.7 | 9.6 | 14.0 | 9.2 | ||||||||

| Interest expense, net | 0.7 | 0.5 | 0.1 | 0.2 | 0.2 | ||||||||

| Income before income taxes | 12.7 | 13.2 | 9.6 | 13.8 | 9.0 | ||||||||

| Income tax expense | 5.1 | 5.3 | 3.8 | 5.5 | 3.6 | ||||||||

| Income from continuing operations | 7.6 | 7.9 | 5.8 | 8.3 | 5.4 | ||||||||

| Loss from discontinued operations(1) | 1.1 | — | — | — | — | ||||||||

| Net income | 6.5 | % | 7.9 | % | 5.8 | % | 8.3 | % | 5.4 | % | |||

- (1)

- In June 1999, we sold our learning technology solutions division to a group of investors who operated it as Eduprise, Inc. We have reflected the division's results through the time of disposition as a discontinued operation.

Three Months Ended March 31, 2002 Compared to Three Months Ended March 31, 2001

Revenue. Revenue increased 43.8% from $15.9 million for the three months ended March 31, 2001 to $22.8 million for the three months ended March 31, 2002. Of the total increase, $2.7 million was attributable to our acquisition of Eduprise. The balance of the increase in our revenue reflects the addition of new clients after the first quarter of 2001 and our undertaking additional work for existing clients. Exclusive of the impact of our Eduprise acquisition, our revenue increased $4.2 million or 26.4%.

Cost of services. Cost of services increased 46.5% from $9.7 million for the three months ended March 31, 2001 to $14.3 million for the three months ended March 31, 2002. The increase was due primarily to the number of additional professional staff required to support our growth during the period. We increased the number of our professional staff from 531 at March 31, 2001 to 716 at March 31, 2002. As a percentage of revenue, cost of services increased to 62.6% in the three months ended March 31, 2002 from 61.4% in the three months ended March 31, 2001 primarily due to the signing in late 2001 and early 2002 of several large client contracts with margins somewhat lower than our historical average and a relative increase in reimbursable expenses.

Selling, general and administrative. Selling, general and administrative expenses increased 57.3% from $3.8 million in the three months ended March 31, 2001 to $5.9 million in the three months ended March 31, 2002. Of this increase, $1.6 million was attributable to the acquisition of Eduprise and $0.5 million was from continued investment in corporate infrastructure to support our growth. As a

21

percentage of revenue, selling, general and administrative expenses increased from 23.7% in the three months ended March 31, 2001 to 25.9% in the three months ended March 31, 2002. This increase is due primarily to Eduprise's higher level of selling, general and administrative expenses relative to its revenue recognized by us since the date of acquisition. We believe that as we realize the synergies of the merger, further consolidate Eduprise's operations and eliminate certain redundant support activities, the percentage of selling, general and administrative expenses to revenue will return to historical levels.

Depreciation and amortization. Depreciation and amortization was $0.1 million in the three months ended March 31, 2001 and $0.4 million in the three months ended March 31, 2002. Depreciation expense increased from $0.1 million in the three months ended March 31, 2001 to $0.3 million in the three months ended March 31, 2002 due to equipment additions related to our acquisition of Eduprise and to support the growth in our corporate infrastructure. Amortization expense of intangible assets related to the Eduprise acquisition was $0.1 million in the three months ended March 31, 2002.

Stock compensation expense. Stock compensation expense in the three months ended March 31, 2002 of $0.1 million relates to amortization of the costs of unvested replacement options issued to former Eduprise employees and deferred compensation costs.