KEEFE, BRUYETTE & WOODS

2010 TEXAS FIELD TRIP

February 9 - 11th, 2010

Houston, Texas

Presentation by: George M. Lee

Executive Vice Chairman, President & CEO

2/9/2010

1

The statements contained in this presentation that are not historical facts

are forward-looking statements made pursuant to the Safe Harbor

provisions of the Private Securities Litigation Reform Act of 1995. Forward-

looking statements describe MetroCorp’s future plans, projections,

strategies and expectations, are based on assumptions, and involve a

number of risks and uncertainties, many of which are beyond MetroCorp’s

control. Actual results could differ materially from those projected due to

changes in interest rates, competition in the industry, changes in local and

national economic conditions and various other factors. Additional

information concerning such factors that could affect MetroCorp is

contained in MetroCorp’s 2008 Annual Report on Form 10-K and other

reports and documents filed from time to time with the SEC.

are forward-looking statements made pursuant to the Safe Harbor

provisions of the Private Securities Litigation Reform Act of 1995. Forward-

looking statements describe MetroCorp’s future plans, projections,

strategies and expectations, are based on assumptions, and involve a

number of risks and uncertainties, many of which are beyond MetroCorp’s

control. Actual results could differ materially from those projected due to

changes in interest rates, competition in the industry, changes in local and

national economic conditions and various other factors. Additional

information concerning such factors that could affect MetroCorp is

contained in MetroCorp’s 2008 Annual Report on Form 10-K and other

reports and documents filed from time to time with the SEC.

2

Forward Looking Statements

§ Expense Management

§ NIM

§ Capital

§ Balance Sheet

§ Asset / Loan Quality (Terry Tangen)

3

Today’s Agenda

4

5

Expense Management

2007 | 2008 | 2009 | |

FTE | 348 | 321 | 296 |

Compensation | $ 24,846 | $ 24,298 | $ 20,406 |

Legal & Professional | $ 1,443 | $ 2,048 | $ 2,505 |

Regulatory | $ 451 | $ 906 | $ 4,252 |

ORE Related | $ 278 | $ 289 | $ 4,107 |

Net Charge Off | $ 1,456 | $ 5,539 | $ 17,592 |

Loan Loss Provision | $3,145 | $16,649 | $23,513 |

($ in 000’s)

6

7

8

9

Net Interest Margin (%)

10

NIM vs Peer Banks

MCBI | EWBC* | CATY | PFBC | |

2009 Q4 | 3.73 | 3.61 | 2.65 | 2.58 |

2008 Q4 | 3.72 | 2.72 | 2.85 | 3.31 |

2007 Q4 | 4.30 | 3.91 | 3.43 | 4.82 |

2006 Q4 | 4.61 | 3.81 | 4.01 | 5.19 |

2005 Q4 | 4.56 | 4.20 | 4.34 | 4.81 |

* Non-GAAP excluding discount on covered loans from UCBH purchase

11

12

Total Risk-Based Capital Ratio

Tangible Common Equity Ratio

MB | MUB | MCBI | |

12/31/2009 | 14.07% | 12.87% | 13.88% |

12/31/2008 | 10.39% | 10.41% | 10.17% |

MB | MUB | MCBI | |

12/31/2009 | 11.23% | 9.32% | 5.87% |

12/31/2008 | 8.64% | 8.29% | 6.22% |

13

14

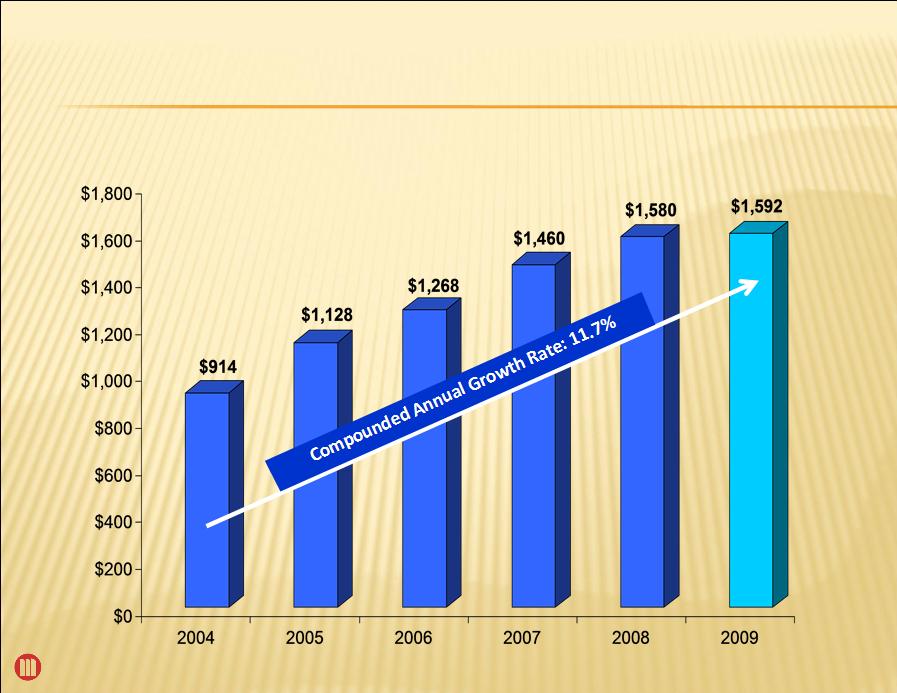

MCBI Total Asset Growth

$ in millions

15

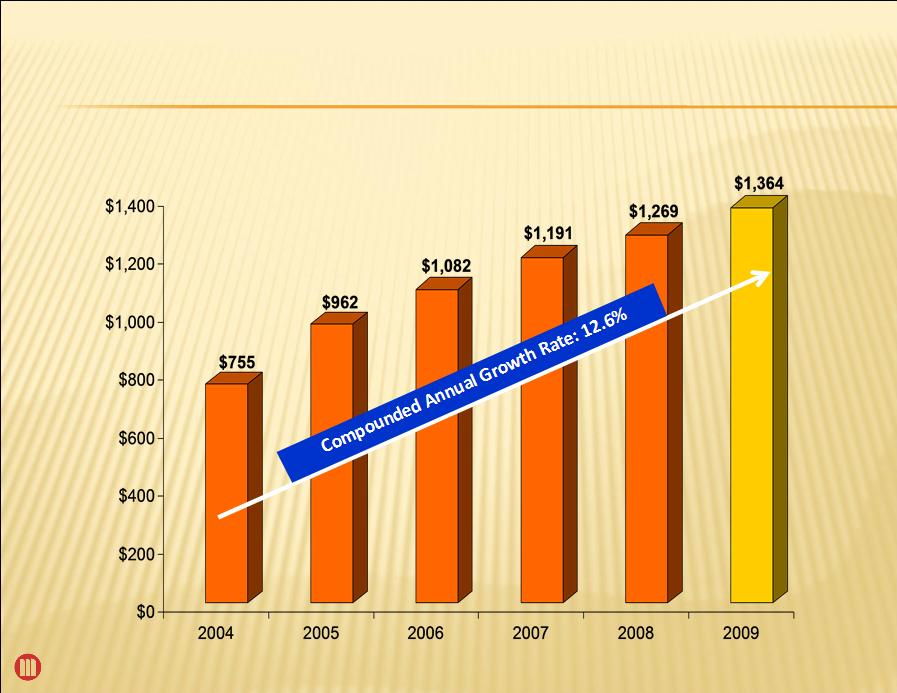

MCBI Total Deposit Growth

$ in millions

16

Deposit Composition

17

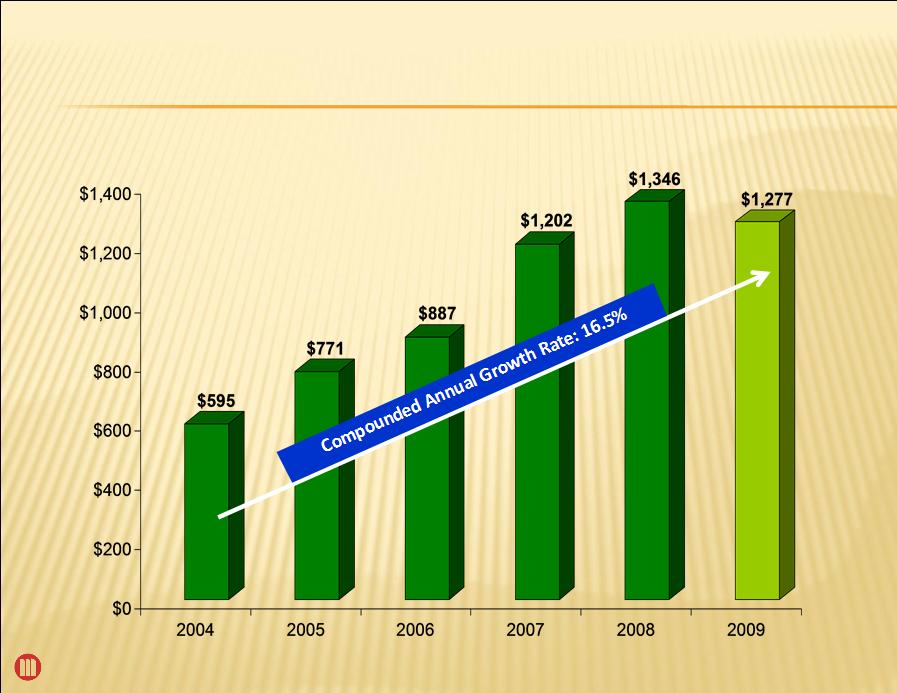

MCBI Total Loan Growth

$ in millions

18

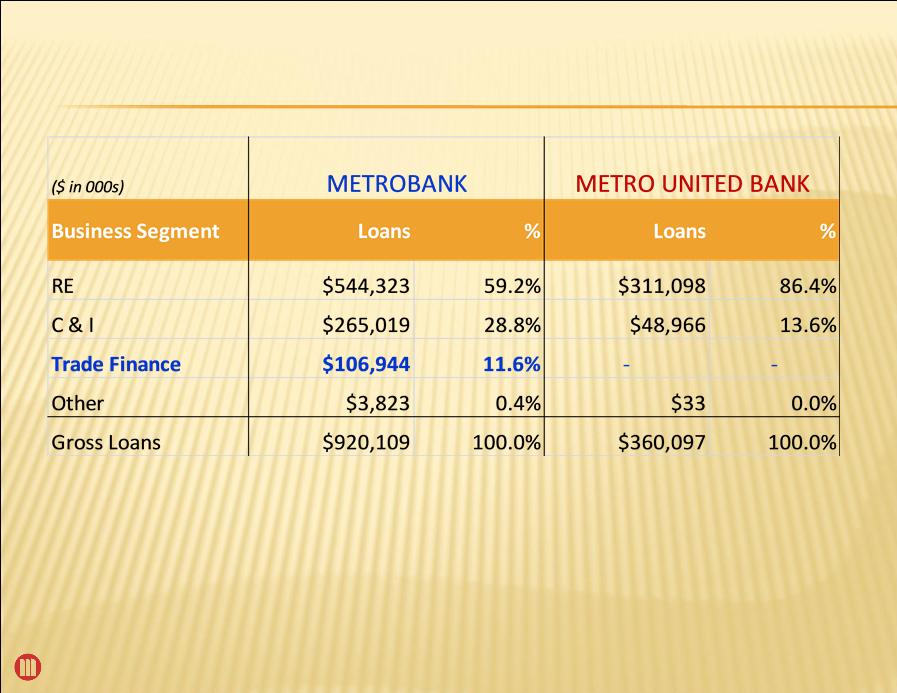

Loan Concentration

19

OPERATING ENVIRONMENT

§ Panama Canal Expansion

§ Turn Houston into potentially the largest port city in the country

§ Trade Business between Texas & China

§ China is Texas’ third largest trading partner

§ Texas is the second largest exporting state to China

§ Houston metro area provides 2/3 of total trade business

§ Dallas/Fort Worth provides 20%

§ Imports from China in 2008: $18 billion

§ Exports to China in 2008: $8.4 billion

§ Strategic Location of Representative Offices in China

§ Chongqing will be the focus of China’s growth into the inland provinces

§ Xiamen is an important import & export port in China

20

METROBANK’S COMPETITIVE EDGE

§ MetroBank vs. Money Center Banks

§ Location - Headquartered in Texas

§ Trade finance centers of other national banks

located in NY, CA, etc.

located in NY, CA, etc.

§ Language

§ Money center banks focus on very large accounts

21

METROBANK’S COMPETITIVE EDGE

§ MetroBank vs. Community Banks

§ Only few community banks in Texas are able to

handle trade finance

handle trade finance

§ MetroBank has a stronger international

business team

business team

§ MetroBank is the only bank headquartered in

Texas with presence in China

Texas with presence in China

22

METROBANK’S COMPETITIVE EDGE

§ MetroBank vs. Small Ethnic Banks

§ MetroBank has more complete service

§ Two representative offices in China

§ Stronger network of bank relationship in China

§ Branches in the second largest exporting state -

California

California

23

BUSINESS & EARNING OPPORTUNITIES

§ Business Development

§ Export - L/C Advising, Negotiation, & Discounting

§ Import - L/C Issuance & L/C Refinancing

§ Correspondent Banking

§ Related Private Business or Personal Accounts

§ Depository Relationships

24

STRENGTHENING OUR COMPETENCE

§ Staffing

§ Lenders & underwriters to be more international

business minded

business minded

§ Hire a high level international credit professional

§ Monitoring Process

§ Lending Process

25

26

28

29

30

31

KEEFE, BRUYETTE & WOODS

2010 TEXAS FIELD TRIP

February 9 - 11th, 2010

Houston, Texas

Presentation by: Terrance J. Tangen

Executive Vice President & Chief Credit Officer

2/9/2010

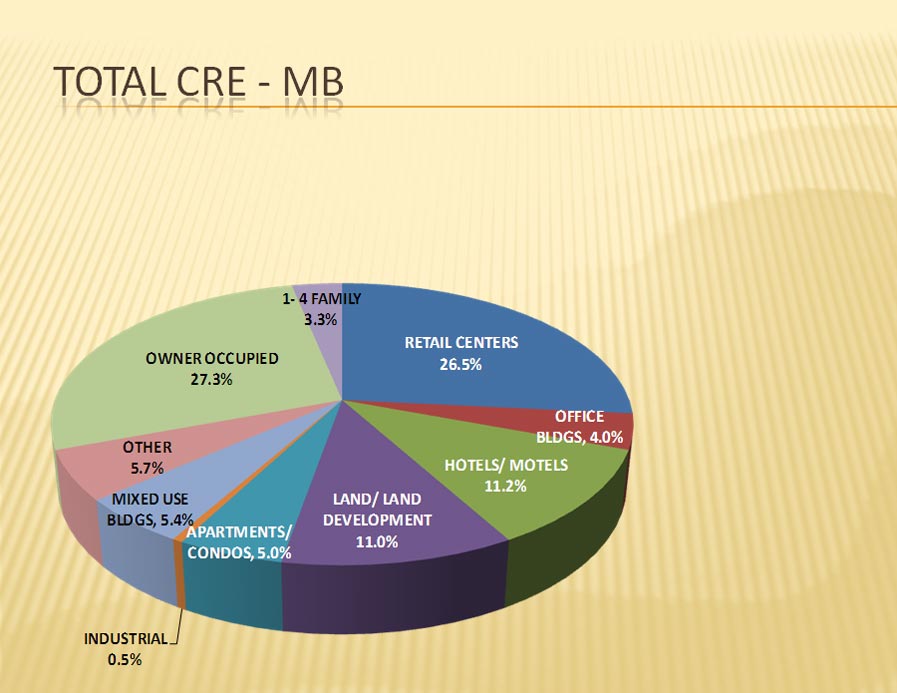

TOTAL REAL ESTATE PORTFOLIO

33

OWNER OCCUPIED

27.3%

RETAIL CENTERS

26.5%

HOTELS/ MOTELS

11.2%

DEVELOPMENT

11.0%

OTHER

5.7%

MIXED USE BLDGS

5.4%

APARTMENTS/CONDOS

5.0%

OFFICE BLDGS

4.0%

1- 4 FAMILY

3.3%

INDUSTRIAL

0.5%

CATEGORY | NET ACTIVE PRINCIPAL BALANCE | % OF BANK CAPITAL | % OF GROSS LOANS |

TOTAL INCOME PRODUCING | $ 561,932,608 | 371.3% | 61.1% |

OWNER OCCUPIED | $ 220,975,716 | 146.0% | 24.0% |

1- 4 FAMILY | $ 26,642,301 | 17.6% | 2.9% |

TOTAL REAL ESTATE SECURED | $ 809,550,625 | 534.9% | 88.0% |

ALL OTHERS | $ 110,558,693 | 73.1% | 12.0% |

TOTAL BANK GROSS LOANS | $ 920,109,319 | 100.0% |

34

35

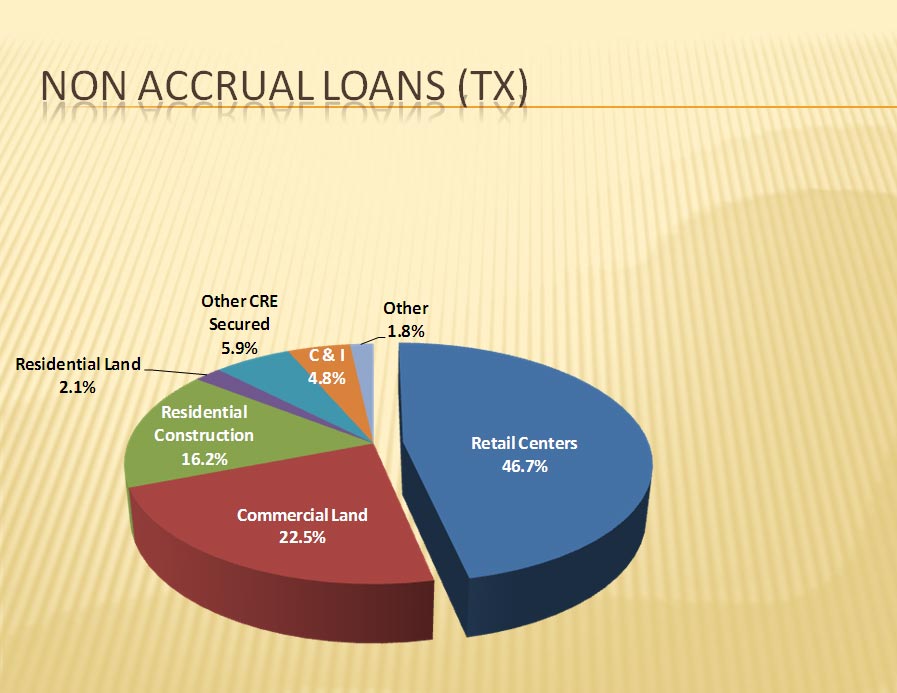

Retail Centers

46.7%

Commercial Land

22.5%

Residential Construction

16.2%

Residential Land

2.1%

Other CRE Secured

5.9%

C & I

4.8%

Other

1.8%

ORE - MB

36

Hospital | $5.4 MM |

Commercial Land | $8.2 MM |

Office / Warehouse | $0.9 MM |

Residential | $0.6 MM |

Total | $15.1 MM |

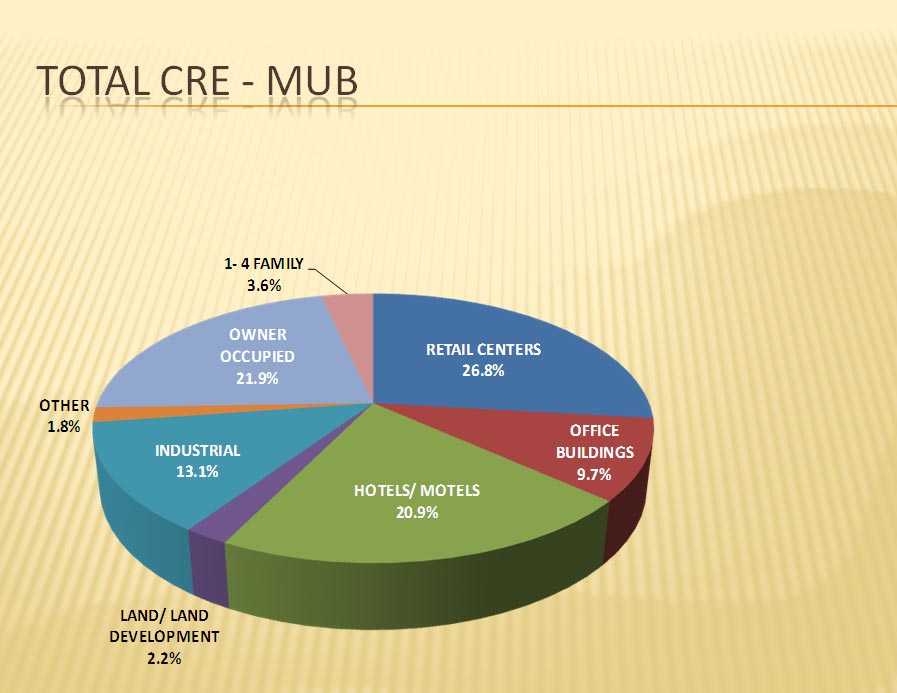

TOTAL REAL ESTATE PORTFOLIO

37

RETAIL CENTERS

26.8%

OWNER OCCUPIED

21.9%

HOTELS/ MOTELS

20.9%

INDUSTRIAL

13.1%

OFFICE BUILDINGS

9.7%

1- 4 FAMILY

3.6%

LAND/ LAND

2.2%

OTHER

1.8%

CATEGORY | NET ACTIVE PRINCIPAL BALANCE | % OF BANK CAPITAL | % OF GROSS LOANS |

TOTAL INCOME PRODUCING | $ 262,556 | 533% | 72.9% |

OWNER OCCUPIED | $ 77,119 | 157% | 21.4% |

1- 4 FAMILY | $ 12,850 | 26% | 3.6% |

TOTAL REAL ESTATE SECURED | $ 352,525 | 718% | 97.9% |

ALL OTHERS | $ 7,572 | 15% | 2.1% |

TOTAL BANK GROSS LOANS | $ 360,097 | 100.0% |

38

39

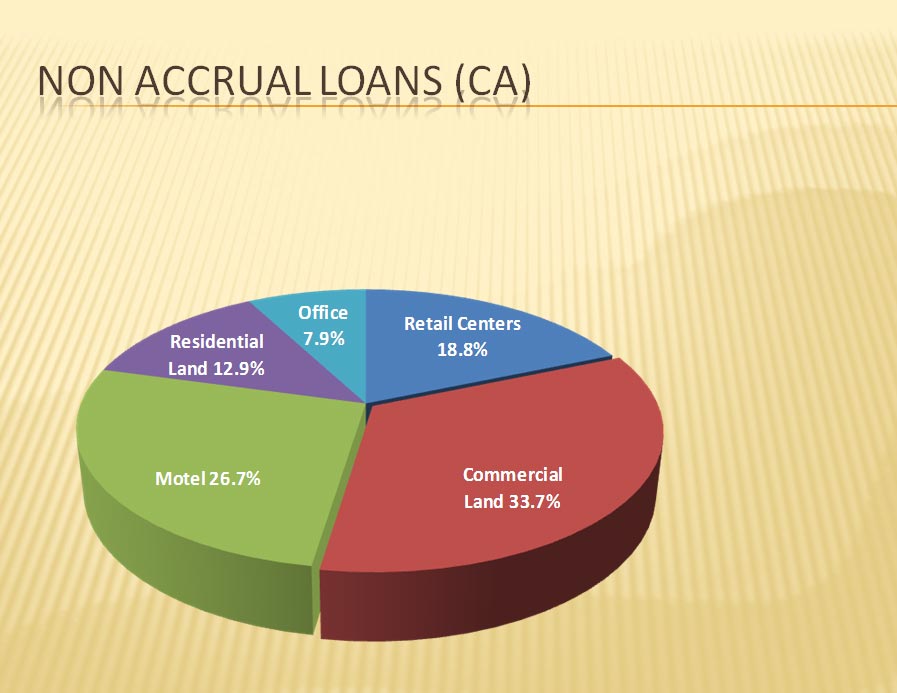

Commercial Land

33.7%

Motel

26.7%

Retail Centers

18.8%

Residential Land

12.9%

Office

7.9%

ORE - MUB

40

Hospital | $1.6 MM |

Residential Land | $2.3 MM |

Retail | $2.8 MM |

Commercial Land | $0.4 MM |

Office | $0.1 MM |

Total | $7.2 MM |

41

In $000’s | 2005 | 2006 | 2007 | 2008 | 2009 |

Net Nonperforming Assets * | $17,262 | $9,304 | $5,501 | $55,695 | $103,262 |

Net Nonperforming Assets to Total Assets % | 1.53% | 0.73% | 0.38% | 3.52% | 6.49% |

* Net Nonperforming Assets are net of guarantee and accruing loans > 90 days delinquent.

In $000’s | 2005 | 2006 | 2007 | 2008 | 2009 |

Allowance for Loan Losses | $13,169 | $11,436 | $13,125 | $24,235 | $30,156 |

Allowance to Net Nonperforming Loans % * | 98.31% | 174.41% | 325.93% | 47.64% | 37.24% |

42

* Net Nonperforming Loans are net of guarantee and accruing loans > 90 days delinquent.