UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-8985

Citigroup Investments Corporate Loan Fund Inc.

(Exact name of registrant as specified in charter)

| | |

| 125 Broad Street, New York, | | NY 10004 |

| (Address of principal executive offices) | | (Zip code) |

Robert I. Frenkel, Esq.

Smith Barney Fund Management LLC

300 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: September 30

Date of reporting period: September 30, 2004

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

Citigroup

Investments

Corporate

Loan Fund Inc.

Annual Report September 30, 2004 Ticker Symbol: TLI |

WHAT’S INSIDE

LETTER FROM THE CHAIRMAN

R. JAY GERKEN, CFA

Chairman, President and

Chief Executive Officer

Dear Shareholder,

I am pleased to report that Citigroup Investments Corporate Loan Fund Inc. continued to perform well during the year ended September 30, 2004. Please read on for a more detailed review of the corporate loan market and the prevailing economic and market conditions during the fund’s fiscal year, and to learn how those conditions have affected fund performance.

Information About Your Fund

In recent months several issues in the mutual fund industry have come under the scrutiny of federal and state regulators. The fund’s Adviser and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The fund has been informed that the Adviser and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

In November 2003, Citigroup Asset Management (“CAM”) disclosed an investigation by the Securities and Exchange Commission (“SEC”) and the U.S. Attorney relating to CAM’s entry into the transfer agency business during 1997-1999. Citigroup has disclosed that the Staff of the SEC is considering recommending a civil injunctive action and/or an administrative proceeding against certain advisory and transfer agent entities affiliated with Citigroup, the former CEO of CAM, a former employee and a current employee of CAM, relating to the creation, operation and fees of its internal transfer agent unit that serves various CAM-managed funds. This internal transfer agent did not provide services to the fund. Citigroup is cooperating with the SEC and will seek to resolve this matter in discussion with the SEC Staff. Although there can be no assurance, Citigroup does not believe that this matter will have a material adverse effect on the fund.

Citigroup Investments Corporate Loan Fund Inc.

1

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

November 10, 2004

2004 Annual Report

2

MANAGER OVERVIEW

Market Overview

The macro trends in the loan market have not changed materially since our last report. The environment for credit risk remains benign. Credit spreadsi remain tight and secondary market prices remain at lofty levels in reaction to the low risk macro environment and technical pressure within the loan market. There continues to be an excess of investment capital available to invest in loans. Credit structures remain under pressure and this continues to be one of our primary concerns for the future.

The lagging 12-month default rate has remained at approximately 1.00% and currently stands at 1.12% (by number of loans), according to Standard & Poor’s Leveraged Commentary and Data (“LCD”)ii. We believe that we will remain in a low risk environment with low default rates for some time. This belief is grounded on our expectation that the odds are in favor of the economy continuing to expand for the remainder of 2004 and into 2005 and that the capital markets will be accommodative. According to LCD, “Any way you cut it, the short-term default outlook remains upbeat... Looking ahead, all qualitative and quantitative factors continue to signal that default rates will remain at or near current low levels in the near term.”

In 2004, new investment opportunities have barely outpaced capital flows into the loan market. This has left the massive cash build-up from 2003 largely intact. In addition, early loan repayments by the companies we invest in have continued at an accelerated pace relative to historical trends. As a result, the technical pressure that we have commented on in earlier reports continues. Once again, we do not expect to see a significant change in these conditions.

As expected, primary market credit spreads and secondary market prices have remained in a range since our last report. Absent an unforeseen change in the credit markets, we expect spreads to continue to be range-bound in the next quarter, albeit trading towards the lower end of the range.

The soundness of credit structures remains one of our main concerns for the future. Average debt multiples on new issues remain at acceptable levels from a historical perspective. However, relative to past trends, we have continued to see a larger number of credits rated below Ba3 and BB- by Moody’s and Standard & Poor’siii entering the new issue market. While this is not of significant concern at this point due to the benign credit environment, it does indicate that an increasing number of new credits being created have less protection. This, in turn, leaves them more vulnerable should a downturn in the

Citigroup Investments Corporate Loan Fund Inc.

3

credit cycle occur. As a result, credit selection has taken on increasing importance in our strategy.

On June 30, 2004, the Federal Reserve Board (“Fed”) made its first of three consecutive 25 basis pointiv increases to short-term interest rates, increasing it from a four-decade low of 1.00% to 1.75% in September. Following the end of the funds reporting period, at its November meeting, the Fed once again raised its target for the federal fund rate by 0.25% to 2.00%. We expect that the Fed will continue to raise short-term interest rates over time. However, the economy has slowed somewhat, which has increased the odds that the Fed will slow the pace of rate increases as it continues to evaluate economic data. Certainly, the rising cost of energy and commodities in general have increased inflationary risks and, at the same time, the possibility that the economy will continue to expand at a slower pace than had been expected several months ago.

We continue to believe a rising rate environment will favor floating-rate loans relative to fixed-income and equity investments on a risk-adjusted basis. All things being equal, a rising interest rate environment historically has had a positive effect on floating-rate loans because the income earned on loans increases as short-term interest rates rise. On the other hand, fixed-income securities historically have suffered as their fixed-interest payments erode in value as interest rates increase. Similarly, equity securities generally have not performed as well in a rising interest rate environment as price-to-earning (“P/E”)v multiples typically come under pressure.

Fund Performance

During the 12 months ended September 30, 2004, the Citigroup Investments Corporate Loan Fund Inc. returned 5.79%, based on its New York Stock Exchange (“NYSE”) market price and 7.55% based on its net asset value (“NAV”)vi per share. In comparison, its Lipper loan participation closed-end funds category averagevii was 7.84%. Please note that Lipper performance returns are based on each fund’s NAV.

During the 12-month period, the fund distributed dividends to shareholders totaling $0.6775 per share. The performance table shows the fund’s 30-day SEC yield as well as its 12-month total return based on its NAV and market price as of September 30, 2004. Past performance is no guarantee of future results. The fund’s yields will vary.

2004 Annual Report

4

FUND PERFORMANCE AS OF SEPTEMBER 30, 2004

| | | | |

| Price Per Share | | 30-Day

SEC Yield | | 12 Month

Total Return |

| | | | | |

| $14.29 (NAV) | | 5.20% | | 7.55% |

| | | | | |

| $14.58 (NYSE) | | 5.09% | | 5.79% |

All figures represent past performance and are not a guarantee of future results. The fund’s yields will vary.

Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all dividends and/or capital gains distributions, if any, in additional shares. The “SEC yield” is a return figure often quoted by bond and other fixed-income mutual funds. This quotation is based on the most recent 30-day (or one-month) period covered by the fund’s filings with the SEC. The yield figure reflects the dividends and interest earned during the period after deduction of the fund’s expenses for the period. This yield is as of September 30, 2004 and is subject to change.

Fund Overview

On October 12, 2004, the fund declared a regular monthly dividend for October of $0.055 per share. This marks the ninth consecutive month that dividends have been maintained at that level. We continue to expect that the fund’s cash flow will be positively affected by the Fed’s moves to increase the federal funds rateviii. Unlike fixed-rate investments, interest rates on loans periodically will adjust in response to changes in short-term interest rates. These rate adjustments have provided investors with higher income during periods of rising interest rates and lower income during periods of declining interest rates, all other things being equal.

At the same time, the fund’s cash flow continues to be negatively impacted as the effect of the decrease in credit spreads across the loan market works its way into the portfolio and the cost of leverage increases as interest rates rise. We will continue to monitor the effects of these changes in cash flows and adjust the dividend accordingly. As noted in earlier reports, at times, a portion of the fund’s undistributed income has been used to support the dividend in prior months. The fund typically maintains a balance of undistributed income to smooth dividend fluctuations that could occur from changes in month-to-month cash flow generated by the portfolio.

Consistent with our original investment mandate, the fund’s portfolio is largely made up of floating- or variable-rate senior secured corporate loans. As of September 30, 2004 the fund had total net assets of approximately $141.2 million. The total market value of loans in which the fund invested was approximately $212.9 million. Those loans were made to 160 issuers, had an average equivalent rating of Ba3 and were invested in 32 industry sectors, with the largest industry concentration being 8.1% of total investments in the Hotels/Motels/Inns and Casinos industry.

Citigroup Investments Corporate Loan Fund Inc.

5

Since the Manager Commentary in our last report at the end of July 2004, the NAV of the fund has continued to perform well. As of October 15, 2004, the NAV of the fund was $14.33, a marginal decrease of $0.05 or 0.35% since July 16, 2004 and nearly equivalent to the S&P/LSTA Leveraged Loan, Market Value Indexix that showed a 0.26% decrease over the same period. It is the fund’s policy that its NAV is calculated on a “mark-to-market”x basis using current market prices for each loan in the fund, as determined weekly by a third-party pricing service.

Since our last report, we have seen little movement in the prices of loans in the portfolio. As expected, secondary market prices have remained in a range since our last report making NAV gains harder to achieve. From July 16, 2004 to October 15, 2004, the majority of loans in the portfolio stayed within a trading range, as predicted in our last report. During that period, the average price of loans in the portfolio decreased approximately 0.60% and approximately 94% of the price changes were less than 1.00%.

On October 15, 2004, the fund’s share price closed at $14.48, a 2.43% decline since July 16, 2004. In a trend that began prior to the period covered in this report and ending in April 2004, the fund’s share price steadily rose. The share price spiked up to $15.89 on April 20, 2004 and then quickly dropped below $15.00 per share by May 7, 2004. Since the latter part of July, the fund has traded in a range around $14.50 per share.

Since our last report, the fund has continued to trade at a premium to its NAV. On October 15, 2004, the fund traded at a 1.05% premium, a decrease from a 3.20% premium as of July 16, 2004. Over that period, the fund’s NAV decreased marginally and its share price also fell, resulting in a decrease in its premium. As noted in our last report, we believe the primary reason the fund continues to trade at a premium to its NAV is the relative value of loans to other asset classes on a risk-adjusted basis.

Asset levels in the fund remain at acceptable levels but have decreased since our last report. While new issue supply has grown in 2004 relative to the past several years, the demand for assets in the loan market continues to exceed supply. As noted earlier, new investment capital continues to flow into the market at a rapid pace and the companies we invest in are repaying loans at a faster rate than we have historically experienced. Credit selection has become more challenging as we are seeing a higher level of risk in new investment opportunities being brought to market. We continue to find new loans to invest in while maintaining our high credit standards but, of late, not enough to compensate for loans in the portfolio that repay before their stated maturity. We will continue to add new assets whenever we find loans that meet our risk and return requirements.

2004 Annual Report

6

Looking for Additional Information?

The fund is traded under the symbol “TLI” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under symbol XTLIX. Barron’s and The Wall Street Journal’s Monday editions carry closed-end fund tables that will provide additional information. In addition, the fund issues a quarterly press release that can be found on most major financial websites as well as www.citigroupassetmanagement.com.

In a continuing effort to provide information concerning the fund, shareholders may call 1-888-735-6507, Monday through Friday from 8:00 a.m. to 6:00 p.m. Eastern time, for the fund’s current net asset value, market price, and other information.

Thank you for your investment in the Citigroup Investments Corporate Loan Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the fund’s investment goals.

Sincerely,

Glenn N. Marchak

Vice President and Investment Officer

November 10, 2004

Citigroup Investments Corporate Loan Fund Inc.

7

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Risks: All investments involve risk. The fund invests in fixed income securities which are subject to Credit Risks, including the risk of nonpayment of scheduled interest or loan payments, which could lower the fund’s value. As interest rates rise, the value of a fixed income portfolio generally declines, reducing the value of the fund. The fund may invest in foreign securities which are subject to certain risks not associated with domestic investing, such as currency fluctuations, and changes in political and economic conditions. High yield/lower rated securities involve greater credit and liquidity risks than investment grade securities. The fund is not diversified which may entail greater risks than is normally associated with more widely diversified funds.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | Credit spread is the difference between the yield of a particular corporate security and a benchmark security that has the same maturity as that particular corporate security. |

| ii | | Standard & Poor’s Leveraged Commentary and Data, formerly known as Portfolio Management Data, is a leading information provider to the leveraged finance community. |

| iii | | Moody’s Investors Service and Standard & Poor’s are nationally recognized credit rating agencies. |

| iv | | A basis point is one one-hundredth (1/100 or 0.01) of one percent. |

| v | | The price-to-earnings (P/E) ratio is a stock's price divided by its earnings per share. |

| vi | | NAV is calculated by subtracting total liabilities and outstanding preferred stock from the closing value of all securities held by the fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the fund has invested. However, the price at which an investor may buy or sell shares of the fund is at the fund’s market price as determined by supply of and demand for the fund’s shares. |

| vii | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended September 30, 2004, including the reinvestment of dividends and capital gains, if any, calculated among the 38 funds in the fund’s Lipper category. |

| viii | | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| ix | | The S&P/LSTA Leveraged Loan, Market Value Index is a total return index that captures accrued interest, repayments, and market value changes. |

| x | | Mark-to-market is the process of valuing a security or portfolio at current market prices. |

2004 Annual Report

8

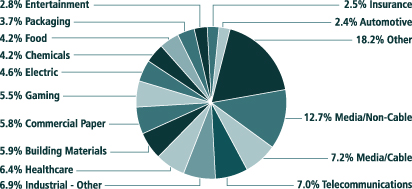

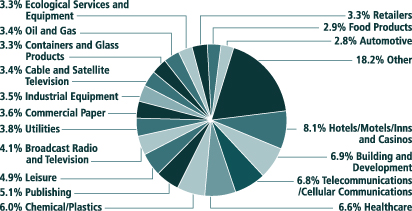

Fund at a Glance (unaudited)

Investment Breakdown†

March 31, 2004

September 30, 2004

| † | | As a percentage of total investments. Please note that Fund holdings are subject to change. |

| | | Industry classifications at March 31, 2004 were based on Lehman categories, whereas at September 30, 2004, they were based on S&P categories, which will be utilized going forward. |

Citigroup Investments Corporate Loan Fund Inc.

9

Take Advantage of the Fund’s Dividend Reinvestment Plan!

As an investor in the Fund, you can participate in its Dividend Reinvestment Plan (“Plan”) which is a convenient, simple and efficient way to reinvest your dividends and capital gains, if any, in additional shares of the Fund. Below is a summary of how the Plan works.

Plan Summary

If you participate in the Dividend Reinvestment Plan, your dividends and capital gains distributions will be reinvested automatically in additional shares of the Fund.

The number of shares of common stock in the Fund you will receive in lieu of a cash dividend is determined in the following manner. If the market price of the common stock is equal to or higher than the net asset value (“NAV”) per share as of the determination date (defined as the fourth New York Stock Exchange trading day preceding the payment of the dividend or distribution), plan participants will be issued new shares of common stock at a price per share equal to the greater of: (a) the NAV per share on the valuation date or (b) 95% of the market price per share on the valuation date.

If the market price is less than the NAV per share as of the determination date, PFPC Inc. (“Plan Agent”) will buy common stock for your account in the open market. If the Plan Agent begins to purchase additional shares in the open market and the market price of the shares subsequently exceeds the NAV per share, before the purchases are completed, the Plan Agent will cease making open-market purchases and have the Fund issue the remaining dividend or distribution in shares at a price per share equal to the greater of either the NAV per share on the valuation date or 95% of the market price at which the Fund issues the remaining shares.

A more complete description of the current Plan appears in the section of this report beginning on page 33. To find out more detailed information about the Plan and about how you can participate, please call the Plan Agent at 1-800-331-1710.

2004 Annual Report

10

| | |

| Schedule of Investments | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | SENIOR COLLATERALIZED LOANS — 96.1% |

| | Aerospace/ Defense — 2.0% | | | | | | | | | |

| $ | 692,265 | | Anteon Corp. | | Term B | | 3.725 | | 12/3/10 | | $ | 700,485 |

| | 1,391,988 | | CACI International, Inc. | | Term B | | 3.210 to 3.450 | | 5/3/11 | | | 1,401,124 |

| | 136,902 | | Ceradyne, Inc. | | Term | | 3.750 to 3.937 | | 8/18/11 | | | 138,528 |

| | 460,466 | | DeCrane Aircraft Holdings, Inc. | | Term B | | 7.110 | | 3/31/07 | | | 458,163 |

| | 745,575 | | DeCrane Aircraft Holdings, Inc. | | Term D | | 7.610 | | 12/31/07 | | | 741,847 |

| | 678,532 | | Standard Aero Holdings Inc. | | Term B | | 4.340 | | 8/20/12 | | | 687,862 |

| | 193,183 | | TransDigm Holding Corp. | | Term C | | 3.936 | | 7/22/10 | | | 195,899 |

|

|

| | | | | | | | | | | | | 4,323,908 |

|

|

| | Automotive — 2.8% | | | | | | | | | |

| | 1,661,750 | | Dura Operating Corp. | | Term C | | 4.340 | | 3/23/06 | | | 1,675,772 |

| | 1,799,182 | | The Goodyear Tire & Rubber Co. | | Term | | 3.250 | | 9/30/07 | | | 1,822,571 |

| | 476,087 | | Keystone Automotive Industries, Inc. | | Term B | | 4.670 to 6.500 | | 10/30/09 | | | 482,187 |

| | 697,702 | | Plastech, Inc. | | Term B | | 4.730 | | 2/12/10 | | | 708,312 |

| | 1,523,785 | | Progressive Moulded Products Ltd. | | Term B | | 4.520 to 4.844 | | 8/16/11 | | | 1,529,023 |

|

|

| | | | | | | | | | | | | 6,217,865 |

|

|

| | Beverage and Tobacco — 0.7% | | | | | | | | | |

| | 1,596,333 | | Commonwealth Brands, Inc. | | Term | | 5.875 | | 8/28/07 | | | 1,614,292 |

|

|

| | Broadcast Radio and Television — 4.1% | | | | | | | |

| | 2,102,759 | | Canwest Media Inc. | | Term E | | 4.065 | | 8/15/09 | | | 2,130,358 |

| | 698,250 | | Cumulus Media Inc. | | Term E | | 3.562 | | 3/28/10 | | | 707,269 |

| | 976,478 | | Freedom Communications | | Term B | | 3.750 to 3.790 | | 4/12/12 | | | 992,346 |

| | 157,895 | | Lamar Media Corp. | | Term A | | 3.187 to 3.312 | | 12/17/04 | | | 158,832 |

| | 1,222,222 | | Lamar Media Corp. | | Term D | | 3.437 to 3.500 | | 11/12/04 | | | 1,233,681 |

| | 1,314,456 | | Sun Media Corp. | | Term B | | 3.930 to 4.090 | | 2/7/09 | | | 1,329,039 |

| | 2,428,414 | | Susquehanna Media Co. | | Term B | | 3.840 to 4.070 | | 3/31/12 | | | 2,458,769 |

|

|

| | | | | | | | | | | | | 9,010,294 |

|

|

| | Building and Development — 6.9% | | | | | | | |

| | 205,879 | | Atrium Cos., Inc. | | Term | | 4.410 to 4.730 | | 12/10/08 | | | 208,238 |

| | 1,662,378 | | Hanley-Wood, Inc. | | Term B | | 4.340 to 4.920 | | 9/30/07 | | | 1,612,507 |

| | 228,872 | | Juno Lighting, Inc. | | Term | | 4.340 to 6.250 | | 11/21/10 | | | 232,305 |

| | 121,038 | | Juno Lighting, Inc. | | 2nd Lien | | 7.240 to 7.440 | | 5/21/11 | | | 122,551 |

| | 1,419,724 | | Landsource Communities Development, LLC | | Term B | | 4.375 | | 1/9/10 | | | 1,441,907 |

| | 3,656,870 | | Masonite International Corp. | | Term C | | 4.562 | | 8/31/08 | | | 3,699,725 |

| | 1,736,698 | | Masonite International Corp. | | Term C2 | | 4.062 | | 8/31/08 | | | 1,766,548 |

| | 240,680 | | NCI Building Systems, Inc. | | Term B | | 3.820 to 3.840 | | 6/18/10 | | | 243,764 |

| | 933,092 | | Nortek, Inc. | | Term | | 4.620 to 6.250 | | 8/27/11 | | | 945,145 |

| | 1,855,130 | | Panolam Industries International, Inc. | | Term B | | 6.125 | | 11/24/06 | | | 1,860,927 |

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

11

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Building and Development — 6.9% (continued) | | | | | | | |

| $ | 391,685 | | Panolam Industries International, Inc. | | 2nd Lien | | 9.937 | | 11/24/06 | | $ | 395,602 |

| | 278,731 | | PGT Industries, Inc. | | Term A | | 4.670 | | 1/29/10 | | | 282,912 |

| | 142,355 | | PGT Industries, Inc. | | Term B | | 7.920 | | 7/29/10 | | | 143,423 |

| | 583,637 | | Pike Electric Inc. | | Term B | | 3.937 | | 7/1/12 | | | 594,215 |

| | 2,219,402 | | Trussway Holdings Inc. | | Term B | | 6.320 to 8.000 | | 1/23/08 | | | 1,761,650 |

|

|

| | | | | | | | | | | | | 15,311,419 |

|

|

| | Business Equipment and Services — 2.0% | | | | | | | |

| | 418,523 | | Allied Security Holdings | | Term B | | 6.230 | | 6/30/10 | | | 423,755 |

| | 967,116 | | Buhrmann U.S., Inc. | | Term | | 4.320 | | 12/31/10 | | | 980,414 |

| | 537,068 | | Coinstar, Inc. | | Term | | 3.840 | | 7/7/11 | | | 546,131 |

| | 539,074 | | Global Cash Access, L.L.C. | | Term B | | 4.590 | | 3/10/10 | | | 546,823 |

| | 713,475 | | Verifone Inc. | | Term B | | 4.180 | | 6/30/11 | | | 721,947 |

| | 1,250,000 | | Verifone Inc. | | 2nd Lien | | 7.680 | | 12/31/11 | | | 1,272,656 |

|

|

| | | | | | | | | | | | | 4,491,726 |

|

|

| | Cable and Satellite Television — 3.4% | | | | | | | |

| | 426,722 | | Atlantic Broadband Finance LLC | | Term B | | 5.050 | | 9/1/11 | | | 432,456 |

| | 667,987 | | Bragg Communications, Inc. | | Term B | | 4.293 | | 8/31/11 | | | 674,667 |

| | 2,500,000 | | Century Cable Holdings LLC | | Term B | | 6.750 | | 6/30/11 | | | 2,461,980 |

| | 3,970,000 | | Insight Midwest LLC | | Term B | | 4.750 | | 12/31/09 | | | 4,025,691 |

|

|

| | | | | | | | | | | | | 7,594,794 |

|

|

| | Chemicals/Plastics — 6.0% | | | | | | | | | |

| | 1,214,046 | | Celanese | | Term B | | 4.480 | | 4/6/11 | | | 1,235,103 |

| | 2,452,666 | | Celanese | | Term C | | 6.230 | | 11/3/11 | | | 2,499,676 |

| | 676,700 | | Compression Polymers Corp. | | Term | | 5.040 | | 3/12/10 | | | 681,353 |

| | 1,085,252 | | Georgia Gulf Corp. | | Term D | | 3.875 | | 12/2/10 | | | 1,101,757 |

| | 1,258,336 | | Hercules Inc. | | Term B | | 2.975 to 3.725 | | 10/8/10 | | | 1,269,346 |

| | 842,169 | | Huntsman LLC | | Term A | | 5.812 | | 3/31/07 | | | 844,801 |

| | 163,470 | | Huntsman LLC | | Term B | | 11.562 to 11.625 | | 3/31/07 | | | 163,981 |

| | 221,532 | | Innophos Inc. | | Term B | | 4.070 | | 8/13/10 | | | 224,440 |

| | 132,528 | | Kraton Polymers | | Term B | | 4.375 to 4.625 | | 12/24/10 | | | 133,273 |

| | 369,007 | | Polypore, Inc. | | Term B | | 4.125 | | 11/12/11 | | | 372,121 |

| | 916,975 | | Resolution Specialty Materials LLC | | Term B | | 4.437 | | 8/2/10 | | | 925,859 |

| | 2,500,000 | | Rockwood Specialties Group Inc. | | Term B | | 4.210 | | 7/30/12 | | | 2,519,727 |

| | 1,068,002 | | Unifrax Corp. | | Term | | 5.375 | | 5/19/10 | | | 1,084,022 |

| | 301,667 | | Westlake Chemical Corp. | | Term B | | 5.350 to 5.750 | | 7/31/10 | | | 305,626 |

|

|

| | | | | | | | | | | | | 13,361,085 |

|

|

See Notes to Financial Statements.

2004 Annual Report

12

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Conglomerates — 0.7% | | | | | | | | | |

| $ | 863,580 | | TriMas Corp. | | Term B | | 5.187 | | 6/6/09 | | $ | 870,926 |

| | 677,283 | | Western Industries Inc. | | Term B | | 12.750 | | 6/30/05 | | | 640,032 |

|

|

| | | | | | | | | | | | | 1,510,958 |

|

|

| | Containers and Glass products — 3.3% | | | | | | | |

| | 228,122 | | Bway Corp. | | Term B | | 3.937 to 4.062 | | 6/30/11 | | | 231,615 |

| | 3,960,000 | | Graphic Packaging Corp. | | Term B | | 4.350 | | 8/8/09 | | | 3,990,690 |

| | 1,316,512 | | Kerr Group, Inc. | | Term | | 5.480 to 7.000 | | 8/13/10 | | | 1,329,841 |

| | 1,755,227 | | Printpack Holdings Inc. | | Term C | | 4.125 | | 3/31/09 | | | 1,772,779 |

|

|

| | | | | | | | | | | | | 7,324,925 |

|

|

| | Drugs — 0.4% | | | | | | | | | |

| | 600,436 | | Leiner Health Products Group, Inc. | | Term B | | 4.890 | | 5/26/11 | | | 608,505 |

| | 345,624 | | NBTY, Inc. | | Term C | | 3.750 | | 7/25/09 | | | 348,864 |

|

|

| | | | | | | | | | | | | 957,369 |

|

|

| | Ecological Services and Equipment — 3.3% | | | | | | | |

| | 3,168,000 | | Casella Waste Systems, Inc. | | Term B | | 4.437 to 4.687 | | 5/11/07 | | | 3,210,572 |

| | 2,002,500 | | IESI Corp. | | Term B | | 4.580 to 5.750 | | 9/30/10 | | | 2,033,789 |

| | 933,673 | | National Waterworks, Inc. | | Term B | | 4.730 | | 11/22/09 | | | 948,262 |

| | 1,000,000 | | Waste Connections, Inc. | | Term | | 3.370 to 3.430 | | 10/22/10 | | | 1,010,625 |

|

|

| | | | | | | | | | | | | 7,203,248 |

|

|

| | Electronics/Electric — 1.8% | | | | | | | | | |

| | 3,520,000 | | Amphenol Corp. | | Term | | 3.686 to 3.810 | | 5/6/10 | | | 3,544,200 |

| | 543,689 | | Bridge Information Systems, Inc. (d) | | Multi-Draw | | 0.00 | | 5/29/05 | | | 31,942 |

| | 960,252 | | Bridge Information Systems, Inc. (d) | | Term B | | 0.00 | | 5/29/05 | | | 56,415 |

| | 296,250 | | Fairchild Semiconductor Corp. | | Term B | | 4.187 | | 6/19/08 | | | 300,231 |

|

|

| | | | | | | | | | | | | 3,932,788 |

|

|

| | Equipment Leasing — 0.2% | | | | | | | | | |

| | 536,083 | | Kinetic Concepts, Inc. | | Term B1 | | 3.980 | | 8/11/10 | | | 542,561 |

|

|

| | Farming/Agriculture — 0.5% | | | | | | | | | |

| | 1,007,578 | | AGCO Corp. | | Term | | 3.590 to 3.975 | | 1/31/06 | | | 1,021,747 |

|

|

| | Food/Drug Retailers — 2.2% | | | | | | | | | |

| | 1,953,112 | | General Nutrition Centers Inc. | | Term | | 4.840 to 6.250 | | 12/7/09 | | | 1,975,084 |

| | 2,953,005 | | Jean Coutu Group Inc. | | Term B | | 4.125 | | 7/30/11 | | | 2,993,945 |

|

|

| | | | | | | | | | | | | 4,969,029 |

|

|

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

13

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Food Products — 2.9% | | | | | | | | | |

| $ | 878,879 | | American Seafoods Group LLC | | Term B | | 5.090 | | 4/11/09 | | $ | 883,548 |

| | 389,991 | | Atkins Nutritionals, Inc. | | Term | | 5.230 | | 10/29/09 | | | 346,117 |

| | 137,100 | | Atkins Nutritionals, Inc. | | 2nd Lien | | 7.730 | | 10/29/09 | | | 102,596 |

| | 637,570 | | Del Monte Corp. | | Term B | | 3.930 to 4.090 | | 12/31/10 | | | 647,931 |

| | 833,368 | | Keystone Foods Holdings LLC | | Term | | 4.125 to 4.437 | | 6/16/11 | | | 840,660 |

| | 500,207 | | Merisant Co. | | Term B | | 4.430 | | 1/11/10 | | | 502,959 |

| | 992,500 | | Michael Foods, Inc. | | Term B | | 3.714 to 3.990 | | 11/21/10 | | | 1,004,286 |

| | 197,059 | | NSC Operating Co. | | Term B | | 6.125 | | 6/30/06 | | | 197,551 |

| | 442,500 | | NSC Operating Co. | | 2nd Lien | | 8.625 | | 12/31/07 | | | 438,075 |

| | 234,232 | | Osi Foods GMBH & Co. KG | | Term B | | 3.920 | | 9/2/11 | | | 236,355 |

| | 527,023 | | Osi Group, LLC | | Term B | | 3.920 | | 9/2/11 | | | 531,799 |

| | 292,790 | | Osi-Holland Finance B.V. | | Term B | | 3.920 | | 9/2/11 | | | 295,444 |

| | 297,000 | | Reddy Ice Group Inc. | | Term B | | 4.340 | | 8/15/09 | | | 301,084 |

| | 49,500 | | Reddy Ice Group Inc. | | Term B | | 4.340 | | 8/15/09 | | | 50,139 |

|

|

| | | | | | | | | | | | | 6,378,544 |

|

|

| | Food Services — 1.7% | | | | | | | | | |

| | 2,520,041 | | Buffets, Inc. | | Term B | | 4.590 to 5.140 | | 6/28/09 | | | 2,539,993 |

| | 906,207 | | Dr. Pepper Bottling Co. of Texas | | Term B | | 4.077 | | 12/19/10 | | | 917,393 |

| | 346,215 | | Jack In The Box, Inc. | | Term B | | 2.250 to 4.420 | | 1/9/10 | | | 350,976 |

|

|

| | | | | | | | | | | | | 3,808,362 |

|

|

| | Forest Products — 0.5% | | | | | | | | | |

| | 119,803 | | Smurfit-Stone Container Corp. | | Term C | | 4.187 | | 6/30/09 | | | 120,627 |

| | 911,353 | | Stone Container Corp. | | Term B | | 4.187 | | 6/30/09 | | | 917,761 |

|

|

| | | | | | | | | | | | | 1,038,388 |

|

|

| | Healthcare — 6.6% | | | | | | | | | |

| | 294,493 | | Advanced Medical Optics, Inc. | | Term B | | 3.831 to 4.090 | | 6/25/09 | | | 299,187 |

| | 947,459 | | Alderwoods Group, Inc. | | Term B1 | | 4.420 to 6.500 | | 9/29/09 | | | 961,868 |

| | 323,741 | | AMN Healthcare Inc. | | Term B | | 4.980 | | 10/2/08 | | | 324,348 |

| | 3,213,635 | | Community Health Systems Inc. | | Term B | | 3.540 | | 8/19/11 | | | 3,220,522 |

| | 771,066 | | Conmed Corp. | | Term C | | 4.082 to 4.150 | | 12/15/09 | | | 779,901 |

| | 1,973,064 | | Davita, Inc. | | Term B | | 3.600 to 4.170 | | 6/30/10 | | | 1,994,182 |

| | 166,667 | | Davita, Inc. | | Term C | | 3.500 to 3.590 | | 6/30/10 | | | 168,155 |

| | 933,864 | | EMPI Corp. | | Term | | 4.700 | | 11/24/09 | | | 936,198 |

| | 1,563,950 | | Hanger Orthopedic Group, Inc. | | Term B | | 5.475 | | 9/30/09 | | | 1,563,950 |

| | 239,000 | | Medical Device Manufacturing, Inc. | | Term B | | 4.680 to 4.840 | | 6/30/10 | | | 241,390 |

| | 824,582 | | Multiplan, Inc. | | Term | | 4.730 | | 3/4/09 | | | 832,828 |

See Notes to Financial Statements.

2004 Annual Report

14

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Healthcare — 6.6% (continued) | | | | | | | | | |

| $ | 2,502,273 | | Orthofix International LLC | | Term B | | 4.710 to 4.730 | | 12/30/08 | | $ | 2,521,040 |

| | 858,779 | | Rotech Healthcare Inc. | | Term B | | 4.980 | | 3/26/08 | | | 869,111 |

|

|

| | | | | | | | | | | | | 14,712,680 |

|

|

| | Home Furnishings — 1.8% | | | | | | | | | |

| | 531,915 | | Home Interiors & Gifts, Inc. | | Term | | 6.230 to 6.420 | | 3/31/11 | | | 512,500 |

| | 1,236,124 | | Sealy Mattress Co. | | Term C | | 4.196 to 4.290 | | 8/6/12 | | | 1,251,575 |

| | 268,827 | | Sealy Mattress Co. | | Sr. - Unsec. PL | | 6.290 | | 4/5/13 | | | 275,324 |

| | 274,076 | | Simmons Co. | | Sr. - Unsec. PL | | 5.125 | | 6/19/12 | | | 278,301 |

| | 684,536 | | Simmons Co. | | Term | | 3.875 to 4.437 | | 12/19/11 | | | 691,274 |

| | 987,500 | | Tempur-Pedic International Inc. | | Term B | | 4.225 | | 8/18/09 | | | 993,672 |

|

|

| | | | | | | | | | | | | 4,002,646 |

|

|

| | Hotels/Motels/Inns and Casinos — 8.1% |

| | 2,565,975 | | Alliance Gaming Corp. | | Term B | | 3.537 | | 9/5/09 | | | 2,600,187 |

| | 1,842,552 | | Ameristar Casinos, Inc. | | Term B1 | | 4.000 | | 12/20/06 | | | 1,867,312 |

| | 850,786 | | Boyd Gaming Corp. | | Term B | | 3.690 to 3.920 | | 6/30/11 | | | 860,889 |

| | 1,678,009 | | Greektown Casino, LLC | | Term D | | 5.190 to 5.340 | | 12/31/05 | | | 1,687,448 |

| | 270,953 | | Green Valley Ranch Gaming, LLC | | Term B | | 4.725 | | 12/24/10 | | | 275,017 |

| | 1,583,840 | | Isle of Capri Casinos BlackHawk, LLC | | Term C | | 4.590 to 4.950 | | 12/31/07 | | | 1,606,113 |

| | 854,790 | | Penn National Gaming, Inc. | | Term D | | 4.340 to 4.480 | | 9/1/07 | | | 868,467 |

| | 347,354 | | Pinnacle Entertainment | | Term B | | 4.980 | | 8/27/10 | | | 351,695 |

| | 4,539,695 | | Scientific Games Corp. | | Term C | | 4.340 | | 12/31/09 | | | 4,605,897 |

| | 1,004,991 | | Venetian Casino Resorts LLC | | Term B | | 4.290 | | 6/15/11 | | | 1,020,694 |

| | 1,399,277 | | Wyndham International, Inc. | | Term I | | 6.500 | | 6/30/06 | | | 1,391,990 |

| | 746,501 | | Wyndham International, Inc. | | Term II | | 7.500 | | 4/1/06 | | | 745,381 |

|

|

| | | | | | | | | | | | | 17,881,090 |

|

|

| | Industrial Equipment — 3.5% |

| | 179,296 | | Ames True Temper, Inc. | | Term B | | 4.420 to 6.500 | | 6/28/11 | | | 181,761 |

| | 132,930 | | Douglas Dynamics, LLC | | Term B | | 4.430 to 4.725 | | 3/31/10 | | | 134,592 |

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

15

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Industrial Equipment — 3.5% (continued) |

| $ | 67,276 | | Douglas Dynamics, LLC | | 2nd Lien | | 7.586 to 7.790 | | 3/31/11 | | $ | 68,621 |

| | 1,004,115 | | Enersys, Inc. | | Term B | | 3.730 to 3.921 | | 3/17/11 | | | 1,016,039 |

| | 990,196 | | Flowserve Corp. | | Term C | | 4.375 to 6.500 | | 6/30/09 | | | 1,004,740 |

| | 876,276 | | Mueller Group, Inc. | | Term | | 4.540 to 4.930 | | 4/23/11 | | | 883,396 |

| | 754,231 | | Norcross Safety Products LLC | | Term B | | 5.725 to 5.920 | | 3/20/09 | | | 759,416 |

| | 669,813 | | Roper Industries Inc. | | Term B | | 3.660 to 4.010 | | 12/29/08 | | | 679,861 |

| | 2,874,032 | | SPX Corp. | | Term B1 | | 3.937 | | 9/30/09 | | | 2,914,898 |

|

|

| | | | | | | | | | | | | 7,643,324 |

|

|

| | Insurance — 1.8% |

| | 630,000 | | Connecticare, Inc. | | Term B | | 5.249 to 5.725 | | 10/31/09 | | | 633,150 |

| | 1,955,000 | | Hilb, Rogal and Hamilton Co. | | Term B | | 4.250 | | 6/30/07 | | | 1,980,659 |

| | 1,287,000 | | USI Holdings Corp. | | Term B | | 4.180 | | 8/11/08 | | | 1,301,479 |

|

|

| | | | | | | | | | | | | 3,915,288 |

|

|

| | Leisure — 4.9% |

| | 801,404 | | Detroit Red Wings, Inc. | | Term A | | 4.725 | | 8/30/06 | | | 802,406 |

| | 2,644,619 | | Metro-Goldwyn-Mayer Studios, Inc. | | Term B | | 4.480 | | 4/30/11 | | | 2,655,197 |

| | 4,032,728 | | Regal Cinemas, Inc. | | Term B | | 4.225 to 3.881 | | 11/10/10 | | | 4,083,137 |

| | 67,754 | | Wallace Theaters | | Term B | | 5.230 | | 8/9/09 | | | 68,432 |

| | 67,924 | | Wallace Theaters | | 2nd Lien | | 8.980 | | 8/9/09 | | | 68,349 |

| | 3,095,850 | | Warner Music Group | | Term B | | 4.025 to 4.531 | | 2/28/11 | | | 3,142,564 |

|

|

| | | | | | | | | | | | | 10,820,085 |

|

|

| | Non-Ferrous Metals/Minerals — 1.2% |

| | 319,548 | | Compass Minerals Group, Inc. | | Term B | | 4.180 to 4.560 | | 11/28/09 | | | 324,441 |

| | 862,128 | | Jostens, Inc. | | Term B | | 4.150 | | 7/29/10 | | | 870,318 |

| | 1,528,611 | | Peabody Energy Corp. | | Term B | | 3.510 to 3.590 | | 3/21/10 | | | 1,547,081 |

|

|

| | | | | | | | | | | | | 2,741,840 |

|

|

| | Oil and Gas — 3.4% |

| | 1,125,000 | | Alon USA, Inc. | | Term B | | 10.000 | | 1/15/09 | | | 1,158,750 |

| | 1,348,749 | | Dresser Inc. | | Term C | | 4.340 | | 4/10/09 | | | 1,364,344 |

| | 2,249,295 | | La Grange Acquistion, L.P. | | Term B | | 4.840 | | 1/18/08 | | | 2,282,333 |

| | 362,206 | | Lyondell-Citgo Refining, L.P. | | Term B | | 4.090 to 4.370 | | 5/21/07 | | | 364,923 |

| | 678,301 | | Quest Cherokee, LLC | | Term B | | 5.760 | | 7/8/10 | | | 683,388 |

| | 84,770 | | Quest Cherokee, LLC | | L/C Facility | | 5.715 | | 7/8/09 | | | 85,406 |

| | 1,511,250 | | Tesoro Petroleum Corp. | | Term B | | 7.260 | | 4/15/08 | | | 1,558,005 |

|

|

| | | | | | | | | | | | | 7,497,149 |

|

|

See Notes to Financial Statements.

2004 Annual Report

16

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Publishing — 5.1% |

| $ | 3,993,073 | | American Media Operation Inc. | | Term C | | 4.375 to 4.750 | | 4/1/07 | | $ | 4,056,715 |

| | 917,945 | | American Media Operation Inc. | | Term C1 | | 4.375 | | 4/1/07 | | | 931,141 |

| | 2,065,119 | | Dex Media East LLC | | Term B | | 3.710 to 3.840 | | 5/8/09 | | | 2,092,224 |

| | 3,372,777 | | Dex Media West LLC | | Term B | | 3.620 to 4.090 | | 3/9/10 | | | 3,420,357 |

| | 857,939 | | The Reader’s Digest Association, Inc. | | Term B | | 3.570 | | 5/20/08 | | | 868,797 |

|

|

| | | | | | | | | | | | | 11,369,234 |

|

|

| | Retailers — 3.3% | | | | | | | |

| | 424,650 | | Alimentation Couche — Tard, Inc. | | Term | | 3.562 to 5.500 | | 12/17/10 | | | 428,809 |

| | 1,987,778 | | CSK Auto, Inc. | | Term | | 3.600 | | 6/19/09 | | | 2,011,383 |

| | 1,500,546 | | Harbor Freight Tools | | Term B | | 4.400 to 4.461 | | 6/24/10 | | | 1,511,332 |

| | 1,200,000 | | Kmart Corp. | | Term B | | 4.014 | | 5/6/06 | | | 1,206,750 |

| | 2,181,560 | | TravelCenters of America, Inc. | | Term B | | 4.530 to 5.120 | | 11/14/08 | | | 2,210,646 |

|

|

| | | | | | | | | | | | | 7,368,920 |

|

|

| | Steel — 0.4% | | | | | | | |

| | 959,797 | | The Techs | | Term | | 4.150 | | 1/14/10 | | | 962,196 |

|

|

| | Telecommunications/Cellular Communications — 6.8% | | | |

| | 929,961 | | Block Communications Inc. | | Term B | | 4.730 | | 11/15/09 | | | 936,936 |

| | 2,079,550 | | Centennial Cellular Operating Co. | | Term B | | 4.338 to 4.920 | | 2/9/11 | | | 2,097,908 |

| | 591,880 | | D&E Communications, Inc. | | Term B | | 4.500 to 6.500 | | 3/2/12 | | | 601,313 |

| | 266,598 | | Entravision Communications Corp. | | Term B | | 3.650 | | 2/24/12 | | | 268,931 |

| | 2,933,616 | | FairPoint Communications, Inc. | | Term C | | 6.375 | | 3/31/07 | | | 2,956,537 |

| | 3,050,000 | | Qwest Corp. | | Sr. - Unsec. PLA | | 6.500 | | 6/30/07 | | | 3,163,103 |

| | 2,372,922 | | RCN Cable Systems, Inc. | | Term B | | 7.750 | | 6/3/07 | | | 2,366,990 |

| | 493,501 | | SBA Senior Finance, Inc. | | Term B | | 5.340 to 5.560 | | 10/31/08 | | | 498,359 |

| | 2,130,705 | | Western Wireless Corp. | | Term B | | 4.600 to 4.840 | | 5/31/11 | | | 2,163,047 |

|

|

| | | | | | | | | | | | | 15,053,124 |

|

|

| | Utilities — 3.8% | | | | | | | |

| | 3,000,000 | | Calpine Generating Co. LLC | | Term | | 5.400 | | 4/1/09 | | | 3,015,000 |

| | 1,000,000 | | Centerpoint Energy Houston Electric, LLC | | Term | | 12.750 | | 11/12/05 | | | 1,105,000 |

| | 716,219 | | NRG Energy, Inc. | | Term B | | 5.930 | | 6/23/10 | | | 737,706 |

| | 405,766 | | NRG Energy, Inc. | | Term B | | 5.486 | | 6/23/10 | | | 417,939 |

| | 1,111,328 | | NUI Corp. | | Term | | 8.000 | | 11/21/05 | | | 1,115,496 |

| | 373,457 | | NUI Corp. | | Term | | 6.000 | | 11/23/04 | | | 374,857 |

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

17

| | |

| Schedule of Investments (continued) | | September 30, 2004 |

| | | | | | | | | | | | |

FACE AMOUNT | | SECURITY | | LOAN

TYPE | | INTEREST

RATE(a) | | STATED

MATURITY(b) | | VALUE(c) |

| | | | | | | | | | | | | |

| | Utilities — 3.8% (continued) | | | | | | | |

| $ | 217,908 | | NUI Corp. | | Term | | 7.000 | | 11/21/05 | | $ | 218,725 |

| | 1,327,431 | | Orion Power Midwest LP | | Term | | 4.890 to 5.060 | | 10/28/05 | | | 1,329,506 |

|

|

| | | | | | | | | | | | | 8,314,229 |

|

|

| | | | TOTAL SENIOR COLLATERALIZED LOANS

(Cost — $212,191,419) | | | 212,895,107 |

|

|

| | |

| SHARES | | SECURITY | | VALUE |

| | Common Stock — 0.3% | | | |

| | 17,356 | | Gentek, Inc. (e) (Cost — $607,460) | | | 695,108 |

|

|

| | |

| WARRANTS | | SECURITY | | VALUE |

| | Warrants (e) — 0.0% | | | | | | | | | |

| | 19 | | Gentek, Inc., Expires 10/31/08 (f) | | | 56 |

| | 9 | | Gentek, Inc., Expires 10/31/10 (f) | | | 40 |

|

|

| | | | TOTAL WARRANTS

(Cost — $0) | | | 96 |

|

|

| | SHORT-TERM INVESTMENTS — 3.6% | | | | | |

| | Commercial Paper — 3.6% | | | | | |

| | $7,900,000 | | UBS Finance Delaware LLC, 1.880% due 10/1/04

(Cost — $7,900,000) | | | 7,900,000 |

|

|

| | | | TOTAL INVESTMENTS — 100.0%

(Cost — $220,698,879*) | | $ | 221,490,311 |

|

|

| (a) | | Interest rates represent the effective rates on loans and debt securities. Ranges in interest rates are attributable to multiple contracts under the same loan. |

| (b) | | The maturity dates represent the latest maturity dates. |

| (c) | | Market value is determined using current market prices which are supplied weekly by an independent third party pricing service. |

| (d) | | Security is currently in default. |

| (e) | | Non-income producing security. |

| (f) | | Security is valued in good faith by or under the direction of the Board of Directors. |

| * | | Aggregate cost for Federal income tax purposes is $221,116,835. |

| | |

Abbreviations used in this schedule

|

| 2nd Lien | | — Subordinate Loan to 1st Lien |

| L/C Facility | | — Letter of Credit Facility |

| Multi-Draw | | — Multi-Draw Term Loan |

| Sr. - Unsec. PL | | — Senior Unsecured Term Loan |

| Term | | — Term Loan typically with a

1st Lien on specified assets |

Certain term loans have different letter designations which may generally indicate differences in maturities, pricing, and other terms and conditions. A letter designation could also result from the consolidation of two or more previously issued term loans.

See Notes to Financial Statements.

2004 Annual Report

18

| | |

| Statement of Assets and Liabilities | | September 30, 2004 |

| | | | |

| ASSETS: | | | | |

Investments, at value (Cost — $220,698,879) | | $ | 221,490,311 | |

Cash | | | 3,404,255 | |

Interest receivable | | | 1,205,150 | |

Receivable for securities sold | | | 663,537 | |

Paydown receivable | | | 97,361 | |

|

|

Total Assets | | | 226,860,614 | |

|

|

| LIABILITIES: | | | | |

Payable for securities purchased | | | 258,029 | |

Management fee payable | | | 194,467 | |

Dividends payable to Auction Rate Cumulative Preferred Stockholders | | | 60,166 | |

Accrued expenses | | | 128,827 | |

|

|

Total Liabilities | | | 641,489 | |

|

|

Series A and B Auction Rate Cumulative Preferred Stock (1,700 shares authorized and issued at $25,000 per share for each Series) (Note 5) | | | 85,000,000 | |

|

|

Total Net Assets | | $ | 141,219,125 | |

|

|

| NET ASSETS: | | | | |

Par value of capital shares | | $ | 9,883 | |

Capital paid in excess of par value | | | 146,360,044 | |

Undistributed net investment income | | | 10,069 | |

Accumulated net realized loss from investment transactions | | | (5,952,303 | ) |

Net unrealized appreciation of investments | | | 791,432 | |

|

|

Total Net Assets | | | | |

(Equivalent to $14.29 per share on 9,883,215 capital shares of $0.001 par

value outstanding; 50,000,000 common shares authorized) | | $ | 141,219,125 | |

|

|

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

19

| | |

| Statement of Operations | | For the Year Ended September 30, 2004 |

| | | | |

| INVESTMENT INCOME: | | | | |

Interest | | $ | 10,335,796 | |

|

|

| EXPENSES: | | | | |

Management fee (Note 2) | | | 2,393,755 | |

Auction participation fees (Note 5 ) | | | 215,992 | |

Audit and legal | | | 117,467 | |

Shareholder communications | | | 103,651 | |

Interest expense (Note 4) | | | 69,912 | |

Transfer agency services | | | 65,158 | |

Directors’ fees | | | 57,600 | |

Commitment fees (Note 4) | | | 37,603 | |

Custody | | | 21,012 | |

Stock exchange listing fees | | | 19,971 | |

Auction agency fees | | | 16,000 | |

Excise tax | | | 12,300 | |

Rating agency fees | | | 11,449 | |

Other | | | 7,166 | |

|

|

Total Expenses | | | 3,149,036 | |

|

|

Net Investment Income | | | 7,186,760 | |

|

|

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS (NOTE 3): | | | | |

Net Realized Gain From Investments Transactions | | | 35,309 | |

|

|

Net Increase in Unrealized Appreciation of Investments | | | 4,135,987 | |

|

|

Net Gain on Investments | | | 4,171,296 | |

|

|

Dividends Paid to Auction Rate Cumulative Preferred Stockholders

From Net Investment Income | | | (1,133,931 | ) |

|

|

Increase in Net Assets From Operations | | $ | 10,224,125 | |

|

|

See Notes to Financial Statements.

2004 Annual Report

20

| | |

Statements of Changes in Net Assets | | |

For the Years Ended September 30,

| | | | | | | | |

| | | 2004 | | | 2003 | |

| OPERATIONS: | | | | | | | | |

Net investment income | | $ | 7,186,760 | | | $ | 7,372,861 | |

Net realized gain (loss) | | | 35,309 | | | | (4,913,856 | ) |

Increase in net unrealized appreciation | | | 4,135,987 | | | | 12,780,168 | |

Dividends paid to Auction Rate Cumulative Preferred Stockholders from net investment income | | | (1,133,931 | ) | | | (1,201,497 | ) |

|

|

Increase in Net Assets From Operations | | | 10,224,125 | | | | 14,037,676 | |

|

|

| DISTRIBUTIONS PAID TO COMMON STOCK SHAREHOLDERS FROM: | | | | | | | | |

Net investment income | | | (6,667,271 | ) | | | (7,376,019 | ) |

|

|

Decrease in Net Assets From Distributions

Paid to Common Stock Shareholders | | | (6,667,271 | ) | | | (7,376,019 | ) |

|

|

| FUND SHARE TRANSACTIONS (Note 6): | | | | | | | | |

Net asset value of shares issued for

reinvestment of dividends | | | 1,186,590 | | | | 255,910 | |

|

|

Increase in Net Assets From Fund Share Transactions | | | 1,186,590 | | | | 255,910 | |

|

|

Increase in Net Assets | | | 4,743,444 | | | | 6,917,567 | |

NET ASSETS: | | | | | | | | |

Beginning of year | | | 136,475,681 | | | | 129,558,114 | |

|

|

End of year* | | $ | 141,219,125 | | | $ | 136,475,681 | |

|

|

* Includes undistributed net investment income of: | | | $10,069 | | | | $131,889 | |

|

|

See Notes to Financial Statements.

Citigroup Investments Corporate Loan Fund Inc.

21

Financial Highlights

For a share of capital stock outstanding throughout each year ended September 30, unless otherwise noted:

| | | | | | | | | | | | | | | |

| | | 2004 | | | 2003 | | | 2002 | | | 2001 | | | 2000 | |

Net Asset Value, Beginning of Year | | $13.93 | | | $13.24 | | | $14.15 | | | $15.14 | | | $15.19 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | |

Net investment income | | 0.73 | | | 0.75 | | | 0.90 | | | 1.22 | | | 1.40 | |

Net realized and unrealized gain (loss) | | 0.42 | | | 0.81 | | | (0.79 | ) | | (0.93 | ) | | 0.02 | |

Dividends Paid to Auction Rate Cumulative Preferred Stockholders from net investment income | | (0.11 | ) | | (0.12 | ) | | (0.09 | ) | | — | | | — | |

|

|

Total Income From Operations | | 1.04 | | | 1.44 | | | 0.02 | | | 0.29 | | | 1.42 | |

|

|

Underwriting Commissions and Expenses for the Issuance of Auction Rate Cumulative Preferred Stock | | — | | | — | | | (0.12 | ) | | — | | | — | |

|

|

| Distributions Paid to Common Stock Shareholders From: | | | | | | | | | | | | | | | |

Net investment income | | (0.68 | ) | | (0.75 | ) | | (0.81 | ) | | (1.26 | ) | | (1.44 | ) |

Net realized gains | | — | | | — | | | — | | | (0.02 | ) | | (0.03 | ) |

|

|

Total Distributions | | (0.68 | ) | | (0.75 | ) | | (0.81 | ) | | (1.28 | ) | | (1.47 | ) |

|

|

Net Asset Value, End of Year | | $14.29 | | | $13.93 | | | $13.24 | | | $14.15 | | | $15.14 | |

|

|

Total Return, Based on Market Value | | 5.79 | % | | 29.61 | % | | (1.67 | )% | | (4.33 | )% | | 13.35 | % |

|

|

Total Return, Based on Net Asset Value | | 7.55 | % | | 11.64 | % | | (0.30 | )% | | 2.44 | % | | 10.55 | % |

|

|

Net Assets, End of Year (millions) | | $141 | | | $136 | | | $130 | | | $138 | | | $148 | |

|

|

| Ratios to Average Net Assets(1): | | | | | | | | | | | | | | | |

Expenses | | 2.25 | % | | 2.40 | % | | 2.63 | % | | 4.57 | % | | 4.74 | % |

Net investment income | | 5.14 | | | 5.62 | | | 6.48 | | | 8.31 | | | 9.20 | |

|

|

Portfolio Turnover Rate | | 110 | % | | 55 | % | | 57 | % | | 23 | % | | 59 | % |

|

|

Market Value, End of Year | | $14.58 | | | $14.45 | | | $11.83 | | | $12.82 | | | $14.6875 | |

|

|

Auction Rate Cumulative Preferred Stock(2): | | | | | | | | | | | | | | | |

Total Amount Outstanding (000s) | | $85,000 | | | $85,000 | | | $85,000 | | | — | | | — | |

Asset Coverage Per Share | | 66,535 | | | 65,140 | | | 63,105 | | | — | | | — | |

Involuntary Liquidating Preference Per Share(3) | | 25,000 | | | 25,000 | | | 25,000 | | | — | | | — | |

Average Market Value Per Share(3) | | 25,000 | | | 25,000 | | | 25,000 | | | — | | | — | |

|

|

| (1) | | Calculated on the basis of average net assets of common shareholders. Ratios do not reflect the effect of dividend payments to preferred shareholders. |

| (2) | | On March 14, 2002, the Fund issued 3,400 shares of Auction Rate Cumulative Preferred Stock at $25,000 a share. |

| (3) | | Excludes accrued or accumulated dividends. |

2004 Annual Report

22

Notes to Financial Statements

| 1. | Organization and Significant Accounting Policies |

The Citigroup Investments Corporate Loan Fund Inc. (“Fund”), a Maryland corporation, is registered under the Investment Company Act of 1940, as amended, as a non-diversified, closed-end management investment company.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ.

(a) Investment Valuation. U.S. government agency obligations are valued at the mean between the bid and asked prices. Securities traded on national securities markets are valued at the closing price on such markets. Securities traded in the over-the-counter market and listed securities for which no sales prices were reported are valued at the mean between the bid and asked prices. Securities listed on the NASDAQ National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price on that day, at the last sale price. Collateralized senior loans will be valued at readily ascertainable market values. Securities, for which market quotations are not available will be valued in good faith at fair value by or under the direction of the Board of Directors. In fair valuing a loan, Smith Barney Fund Management LLC (“SBFM”), an indirect wholly-owned subsidiary of Citigroup Inc. (“Citigroup”), the Fund’s investment adviser, with the assistance of the Travelers Asset Management International Company LLC (“TAMIC”), another indirect wholly-owned subsidiary of Citigroup, the subadviser, will consider among other factors: (1) the creditworthiness of the borrower and any party interpositioned between the Fund and the borrower; (2) the current interest rate, period until next interest rate reset and maturity date of the collateralized senior loan; (3) recent market prices for similar loans, if any; and (4) recent prices in the market for instruments with similar quality, rate, period until next interest rate reset, maturity, terms and conditions. SBFM may also consider prices or quotations, if any, provided by banks, dealers or pricing services which may represent the prices at which secondary market transactions in the collateralized senior loans held by the Fund have or could have occurred. Securities maturing within 60 days are valued at cost plus accreted discount, or minus amortized premium, which approximates value.

(b) Investment Transactions and Investment Income. Security transactions are accounted for on trade date. Gains or losses on the sale of securities are

Citigroup Investments Corporate Loan Fund Inc.

23

Notes to Financial Statements (continued)

calculated by using the specific identification method. Interest income, adjusted for amortization of premium and accretion of discount, is recorded on an accrual basis. Facility fees and upfront fees, incurred by the Fund on loan agreements, are amortized over the remaining term of the loan.

(c) Dividends and Distributions to Shareholders. Dividends to shareholders are recorded monthly by the Fund on the ex-dividend date for the shareholders of Common Stock. The holders of the Auction Rate Cumulative Preferred Stock shall be entitled to receive dividends in accordance with an auction that will normally be held monthly and out of funds legally available to shareholders. The Fund distributes capital gains, if any, at least annually. The character of income and gains to be distributed is determined in accordance with income tax regulations which may differ from GAAP.

(d) Net Asset Value. The net asset value (“NAV”) of the Fund’s Common Stock is determined by dividing the value of the net assets available to Common Stock by the total number of shares of common stock outstanding. For the purpose of determining the NAV per share of the common stock, the value of the Fund’s net assets shall be deemed to equal the value of the Fund’s assets less (1) the Fund’s liabilities, (2) the aggregate liquidation value (i.e. $25,000 per outstanding share) of the Auction Rate Cumulative Preferred Stock and (3) accumulated and unpaid dividends on the outstanding Auction Rate Cumulative Preferred Stock.

(e) Federal and Other Taxes. It is the Fund’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, the Fund intends to distribute substantially all of its taxable income and net realized gains on investments, if any, to shareholders each year. Therefore, no federal income tax provision is required. Under the applicable foreign tax law, a withholding tax may be imposed on interest, dividends and capital gain at various rates.

(f) Reclassification. GAAP require that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. Accordingly, during the current year, $480,322 has been reclassified between accumulated net realized loss from investment transactions and undistributed net investment income as a result of permanent differences due to book/tax differences in the treatment of consent fees and $12,300 has been reclassified between capital paid in excess of par value and undistributed net investment income due to a non-deductible excise tax paid by the fund. This reclassification has no effect on net assets or net asset values per share.

2004 Annual Report

24

Notes to Financial Statements (continued)

| 2. | Management Agreement and Transactions with Affiliated Persons |

SBFM acts as investment adviser to the Fund. The Fund pays SBFM a management fee for its investment advisory and administration services calculated at an annual rate of 1.05% of the Fund’s average daily net assets. For purposes of calculating the advisory fee, the liquidation value of any preferred stock of the Fund is not deducted in determining the Fund’s average daily net assets. This fee is calculated daily and paid monthly.

SBFM has entered into a sub-investment advisory agreement with TAMIC. Pursuant to the sub-investment advisory agreement, TAMIC is responsible for certain investment decisions related to the Fund. SBFM pays TAMIC a fee of 0.50% of the value of the Fund’s average daily net assets for the services TAMIC provides as sub-adviser. For purposes of calculating the sub-advisory fee, the liquidation value of any preferred stock of the Fund is not deducted in determining the Fund’s average daily net assets.

All officers and one Director of the Fund are employees of Citigroup or its affiliates and do not receive compensation from the Fund.

During the year ended September 30, 2004, the aggregate cost of purchases and proceeds from sales of investments (including maturities of long-term investments, but excluding short-term investments) were as follows:

| | | |

|

Purchases | | $ | 245,940,190 |

|

Sales | | | 256,314,514 |

|

At September 30, 2004, the aggregate gross unrealized appreciation and depreciation of investments for Federal income tax purposes were as follows:

| | | | |

|

|

Gross unrealized appreciation | | $ | 2,475,737 | |

Gross unrealized depreciation | | | (2,102,261 | ) |

|

|

Net unrealized appreciation | | $ | 373,476 | |

|

|

The Fund has a three-year revolving credit agreement with a financial institution, which allows the Fund to borrow up to an aggregate amount of $25 million. This agreement terminates on May 31, 2005. The Fund pays a facility fee quarterly at 0.15% per annum for the three-year revolving credit agreement. The interest on the loan is calculated at a variable rate based on the LIBOR, Fed Funds or Prime

Citigroup Investments Corporate Loan Fund Inc.

25

Notes to Financial Statements (continued)

Rates plus any applicable margin. Interest expense related to the loan for the period ended September 30, 2004 was $48,431. At September 30, 2004 the Fund did not have any borrowings outstanding per this credit agreement.

| 5. | Auction Rate Cumulative Preferred Stock |

As of September 30, 2004, the Fund has 3,400 outstanding shares of Auction Rate Cumulative Preferred Stock (“ARCPS”).

The ARCPS’ dividends are cumulative at a rate determined at an auction and the dividend period will typically be 28 days. The dividend rates ranged from 1.08% to 2.09% during the year ended September 30, 2004. At September 30, 2004, the current dividend rates were as follows:

| | | | | | |

| | | Series A | | | Series B | |

Current Dividend Rates | | 1.90 | % | | 2.09 | % |

|

|

The ARCPS are redeemable under certain conditions by the Fund at a redemption price equal to the liquidation preference, which is the sum of $25,000 per share plus accumulated and unpaid dividends.

The Fund is required to maintain certain asset coverages with respect to the ARCPS. If the Fund fails to maintain these asset coverages and does not cure any such failure within the required time period, the Fund is required to redeem a requisite number of the ARCPS in order to meet the applicable requirement. Additionally, failure to meet the foregoing asset coverage requirements would restrict the Fund’s ability to pay dividends to common shareholders.

Citigroup Global Markets Inc. (“CGM”), another indirect wholly-owned subsidiary of Citigroup, currently acts as a broker/dealer in connection with the auction of ARCPS. After each auction, the auction agent will pay to each broker/dealer, from monies the Fund provides, a participation fee at the annual rate of 0.25% of the purchase price of the ARCPS that the broker/dealer places at the auction. For the year ended September 30, 2004, CGM earned $215,992 as a participating broker/dealer.

Capital stock transactions were as follows:

| | | | | | | | | | |

| | | Year Ended

September 30, 2004

| | Year Ended

September 30, 2003

|

| | | Shares | | Amount | | Shares | | Amount |

Shares issued on reinvestment | | 83,041 | | $ | 1,186,590 | | 18,507 | | $ | 255,910 |

|

2004 Annual Report

26

Notes to Financial Statements (continued)

| 7. | Income Tax Information & Distributions to Shareholders |

The tax character of distributions paid during the fiscal years ended September 30, were as follows:

| | | | | | |

| | | 2004 | | 2003 |

Ordinary income | | $ | 7,801,202 | | $ | 8,577,516 |

|

As of September 30, 2004, the components of accumulated earnings on a tax basis were as follows:

| | | | |

|

|

Undistributed ordinary income | | $ | 487,769 | |

Capital loss carryforward | | | (5,499,827 | )* |

Other book/tax temporary differences | | | (512,220 | )** |

Unrealized appreciation | | | 373,476 | *** |

|

|

Total accumulated losses | | $ | (5,150,802 | ) |

|

|

| * | | On September 30, 2004, the Fund had a net capital loss carryforward of approximately $5,499,827, of which $43,917 expires in 2009, $224,102 expires in 2010, $221,575 expires in 2011 and $5,010,233 expires in 2012. This amount will be available to offset like amounts of any future taxable gains. |

| ** | | Other book/tax temporary differences are attributable primarily to the deferral of post-October capital losses for tax purposes. |

| *** | | The difference between book-basis and tax-basis unrealized appreciation is attributable primarily to the tax deferral of losses on wash sales and the difference between book and tax methods for recognizing consent fees. |

In connection with an investigation previously disclosed by Citigroup, the Staff of the Securities and Exchange Commission (“SEC”) has notified Citigroup Asset Management (“CAM”), the Citigroup business unit that includes the funds’ investment manager and other investment advisory companies; Citicorp Trust Bank (“CTB”), an affiliate of CAM; Thomas W. Jones, the former CEO of CAM; and two other individuals, one of whom is an employee and the other of whom is a former employee of CAM, that the SEC Staff is considering recommending a civil injunctive action and/or an administrative proceeding against each of them relating to the creation and operation of an internal transfer agent unit to serve various CAM-managed funds.

In 1999, CTB entered the transfer agent business. CTB hired an unaffiliated subcontractor to perform some of the transfer agent services. The subcontractor, in exchange, had signed a separate agreement with CAM in 1998 that guaranteed investment management revenue to CAM and investment banking revenue to a CAM affiliate. The subcontractor’s business was later

Citigroup Investments Corporate Loan Fund Inc.

27

Notes to Financial Statements (continued)

taken over by PFPC Inc., and at that time the revenue guarantee was eliminated and a one-time payment was made by the subcontractor to a CAM affiliate.

CAM did not disclose the revenue guarantee when the boards of various CAM-managed funds hired CTB as transfer agent. Nor did CAM disclose to the boards of the various CAM-managed funds the one-time payment received by the CAM affiliate when it was made.

In addition, the SEC Staff has indicated that it is considering recommending action based on the adequacy of the disclosures made to the fund boards that approved the transfer agency arrangement, CAM’s initiation and operation of, and compensation for, the transfer agent business and CAM’s retention of, and agreements with, the subcontractor.

Citigroup is cooperating fully in the investigation and will seek to resolve the matter in discussions with the SEC Staff. Although there can be no assurance, Citigroup does not believe that this matter will have a material adverse effect on the Fund. As previously disclosed, CAM has already agreed to pay the applicable funds, primarily through fee waivers, a total of approximately $17 million (plus interest) that is the amount of the revenue received by Citigroup relating to the revenue guarantee.

The Fund did not implement the contractual arrangement described above and therefore will not receive any portion of such payment.

2004 Annual Report

28

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors of

Citigroup Investments Corporate Loan Fund Inc.:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Citigroup Investments Corporate Loan Fund Inc. (“Fund”) as of September 30, 2004, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2004 by correspondence with the agent and custodian. As to securities purchased or sold but not yet received or delivered, we performed other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund as of September 30, 2004, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

November 19, 2004

Citigroup Investments Corporate Loan Fund Inc.

29

Additional Information (unaudited)

Information about Directors and Officers

The business and affairs of the Citigroup Investments Corporate Loan Fund Inc. (“Fund”) are managed under the direction of the Board of Directors. Information pertaining to the Directors and Officers of the Fund is set forth below.

| | | | | | | | | | |

| Name, Address and Age | | Position(s) Held with Fund | | Term of Office* and Length of Time Served | | Principal Occupation(s) During Past Five Years | | Number of Portfolios in Fund Complex Overseen by Director | | Other Directorships Held by Director |

| Non-Interested Directors: | | | | | | | | | | |

| | | | | |

Allan J. Bloostein 27 West 67th Street Apt. 5FW New York, NY 10023 Age 74 | | Class I Director | | Since

1992 | | President, Allan J. Bloostein Associates | | 34 | | Taubman Centers, Inc. (retail shopping centers) |

| | | | | |

Dwight B. Crane Harvard Business School Soldiers Field Morgan Hall #375 Boston, MA 02163 Age 66 | | Class III Director | | Since

1992 | | Professor, Harvard Business School | | 49 | | None |

| | | | | |

Paolo M. Cucchi Drew University 108 Brothers College Madison, NJ 07940 Age 62 | | Class I Director | | Since

2001 | | Vice President and Dean of College of Liberal Arts at Drew University | | 7 | | None |

| | | | | |

Robert A. Frankel 1961 Deargrass Way Carlsbad, CA 92009 Age 77 | | Class II Director | | Since

1994 | | Managing Partner of Robert A. Frankel Management Consultants | | 24 | | None |

| | | | | |

Paul Hardin 12083 Morehead Chapel Hill, NC 27514-8426 Age 72 | | Class II Director | | Since

2001 | | Chancellor Emeritus and Professor of Law at the University of North Carolina at Chapel Hill | | 34 | | None |

| | | | | |

William R. Hutchinson 535 N. Michigan Suite 1012 Chicago, IL 60611 Age 61 | | Class III Director | | Since

1995 | | President, W.R. Hutchinson & Associates, Inc.; Formerly Group Vice President, Mergers & Acquisitions BP Amoco p.l.c. | | 42 | | Director, Associated Bank and Associated Banc-Corp. |

| | | | | |

George M. Pavia 600 Madison Avenue New York, NY 10022 Age 76 | | Class III Director | | Since

2001 | | Senior Partner, Pavia & Harcourt Attorneys | | 7 | | None |

2004 Annual Report

30

Additional Information (unaudited) (continued)

| | | | | | | | | | |

| Name, Address and Age | | Position(s) Held with Fund | | Term of Office* and Length of Time Served | | Principal Occupation(s) During Past Five Years | | Number of Portfolios in Fund Complex Overseen by Director | | Other Directorships Held by Director |

| Interested Director: | | | | | | | | | | |

| | | | | |

R. Jay Gerken, CFA** Citigroup Asset Management (“CAM”) 399 Park Avenue 4th Floor New York, NY 10022 Age 53 | | Class I Director/ Chairman, also serves as President and Chief Executive Officer | | Since

2002 | | Managing Director of Citigroup Global Markets Inc. (“CGM”); Chairman, President and Chief Executive Officer of Smith Barney Fund Management LLC (“SBFM”), Travelers Investment Adviser, Inc. (“TIA”) and Citi Fund Management Inc. (“CFM”); President and Chief Executive Officer of certain mutual funds associated with Citigroup Inc. (“Citigroup”); Formerly Portfolio Manager of Smith Barney Allocation Series Inc. (from 1996 to 2001) and Smith Barney Growth and Income Fund (from 1996 to 2000) | | 221 | | None |

| | | | | |

| Officers: | | | | | | | | | | |

| | | | | |

Andrew B. Shoup CAM 125 Broad Street 11th Floor New York, NY 10004 Age 47 | | Senior Vice President and Chief

Administrative

Officer | | Since

2003 | | Director of CAM; Senior Vice President and Chief Administrative Officer of mutual funds associated with Citigroup; Head of International Funds Administration of CAM (from 2001 to 2003); Director of Global Funds Administration of CAM (from 2000 to 2001); Head of U.S. Citibank Funds Administration of CAM (from 1998 to 2000) | | N/A | | N/A |

| | | | | |

Kaprel Ozsolak CAM 125 Broad Street 11th Floor New York, NY 10004 Age 39 | | Chief Financial Officer and Treasurer | | Since

2004 | | Vice President of CGM; Chief Financial Officer and Treasurer or Controller of certain mutual funds associated with Citigroup | | N/A | | N/A |

Citigroup Investments Corporate Loan Fund Inc.

31

Additional Information (unaudited) (continued)

| | | | | | | | | | |

| Name, Address and Age | | Position(s) Held with Fund | | Term of Office* and Length of Time Served | | Principal Occupation(s) During Past Five Years | | Number of Portfolios in Fund Complex Overseen by Director | | Other Directorships Held by Director |

| | | | | |

Glenn N. Marchak 399 Park Avenue 7th Floor New York, NY 10022 Age 48 | | Vice President and Investment Officer | | Since 1998 | | Senior Vice President of the Travelers Asset Management International Company LLC; Managing Director of CGM from 1997 to 1998 | | N/A | | N/A |

| | | | | |