Exhibit 13

CORPORATE PROFILE

RGC Resources, Inc., provides superior customer service and shareholder value as a preferred provider of energy and diversified products and services in its selected market areas.

At RGC Resources, Inc., we’re committed to our customers. In this past year we have focused on the basics of our business. Every area of our business is undergoing constant improvement – from the customer service department that answers customer calls – to the service team that takes care of their needs – to the pipeline that delivers gas to meet energy requirements. We are constantly working to enhance our energy distribution infrastructure in anticipation of our customers’ future requirements.

We’re planning and executing solutions – before they are required.

| | | | | | | | | | |

Years Ended September 30, | | 2009 | | 2008 | | | 2007 |

Operating Revenue - Natural Gas | | $ | 80,786,228 | | $ | 93,606,593 | | | $ | 89,175,661 |

Other Revenue | | $ | 1,398,245 | | $ | 1,030,233 | | | $ | 725,640 |

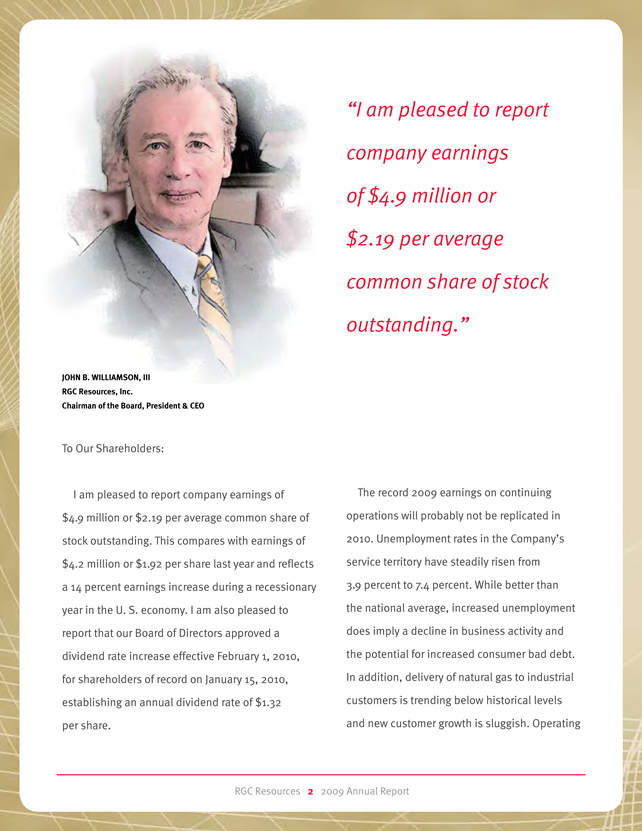

Net Income - Continuing Operations | | $ | 4,869,010 | | $ | 4,257,824 | | | $ | 3,765,669 |

Net Loss - Discontinued Operations | | $ | — | | $ | (36,690 | ) | | $ | 40,540 |

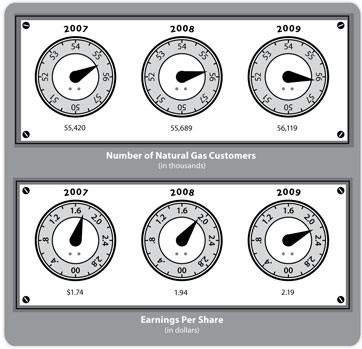

Basic Earnings Per Share - Continuing Operations | | $ | 2.19 | | $ | 1.94 | | | $ | 1.74 |

Basic Earnings Per Share - Discontinued Operations | | | — | | | (0.02 | ) | | | 0.02 |

Regular Dividend Per Share - Cash | | $ | 1.28 | | $ | 1.25 | | | $ | 1.22 |

Number of Customers - Natural Gas | | | 56,119 | | | 55,689 | | | | 55,420 |

Total Natural Gas Deliveries - DTH | | | 9,260,469 | | | 9,251,254 | | | | 9,538,229 |

Total Additions to Plant | | $ | 5,752,780 | | $ | 6,539,369 | | | $ | 6,004,190 |

Downtown illustration adapted from an image provided courtesy of Kurt Konrad.

RGC Resources 9 2009 Annual Report

OFFICERSAND BOARDOF DIRECTORS

| | | | |

| OFFICERS | | DIRECTORS | | Raymond D. Smoot, Jr. |

| | | | Chief Operating Officer and |

| John B. Williamson, III | | Nancy H. Agee | | Secretary-Treasurer |

| Chairman of the Board, President and | | Chief Operating Officer/Executive | | Virginia Tech Foundation, Inc. |

| Chief Executive Officer(1)(2)(3)(4) | | Vice President | | Director:(1) |

| | Carilion Clinic | | |

| John S. D’Orazio | | Director:(1)(2) | | John B. Williamson, III |

| Vice President and | | | | Chairman of the Board, President and |

| Chief Operating Officer(2)(3)(4) | | Abney S. Boxley, III | | Chief Executive Officer |

| | President and | | Director:(1)(2)(3)(4) |

| Howard T. Lyon | | Chief Executive Officer | | |

| Vice President, Treasurer and | | Boxley Materials Company | | |

| Chief Financial Officer(1)(2)(3)(4) | | Director:(1) | | SUBSIDIARY BOARDS OF |

| | | | DIRECTORS: |

| Dale P. Lee | | Frank T. Ellett | | |

| Vice President and | | President | | John S. D’Orazio |

| Secretary(1)(2)(3)(4) | | Virginia Truck Center, Inc. | | Vice President and |

| | Director:(1)(2) | | Chief Operating Officer |

| Robert L. Wells | | | | Roanoke Gas Company |

| Vice President, | | Maryellen F. Goodlatte | | Director:(3)(4) |

| Information Technology, | | Attorney and Principal | | |

| Assistant Secretary and | | Glenn Feldmann Darby & Goodlatte | | Howard T. Lyon |

| Assistant Treasurer(1)(2)(3)(4) | | Director:(1)(2) | | Vice President, Treasurer and |

| | | | Chief Financial Officer |

| | J. Allen Layman | | RGC Resources, Inc. |

| | Private Investor | | Director:(3)(4) |

| | Director:(1)(2) | | |

| | | | Dale P. Lee |

| | George W. Logan | | Vice President and Secretary |

(1) RGC Resources, Inc. | | Chairman of the Board | | RGC Resources, Inc. |

(2) Roanoke Gas Company | | Valley Financial Corporation | | Director:(3)(4) |

(3) Diversified Energy Company | | Principal | | |

(4) RGC Ventures of Virginia, Inc. | | Pine Street Partners | | Robert L. Wells |

| | Faculty | | Vice President, |

| | University of Virginia | | Information Technology, |

| | Darden Graduate School of Business | | Assistant Secretary and |

| | Director:(1)(2) | | Assistant Treasurer |

| | | | RGC Resources, Inc. |

| | S. Frank Smith | | Director:(3)(4) |

| | Vice President Industrial Sales | | |

| | Alpha Coal Sales Company, LLC | | |

| | Director:(1)(2) | | |

RGC Resources 10 2009 Annual Report

SELECTED FINANCIAL DATA

| | | | | | | | | | | | | | | | |

Years Ended September 30, | | 2009 | | 2008 | | | 2007 | | 2006 | | 2005 |

Operating Revenues | | $ | 82,184,473 | | $ | 94,636,826 | | | $ | 89,901,301 | | $ | 94,590,872 | | $ | 88,600,836 |

Gross Margin | | | 27,075,924 | | | 25,913,612 | | | | 25,221,776 | | | 23,208,272 | | | 22,206,395 |

Operating Income | | | 9,844,516 | | | 8,838,026 | | | | 7,958,279 | | | 6,677,500 | | | 6,395,564 |

Net Income - Continuing Operations | | | 4,869,010 | | | 4,257,824 | | | | 3,765,669 | | | 2,961,802 | | | 2,916,798 |

Net Income (Loss) - Discontinued Operations | | | — | | | (36,690 | ) | | | 40,540 | | | 549,729 | | | 590,108 |

Basic Earnings Per Share - Continuing Operations | | $ | 2.19 | | $ | 1.94 | | | $ | 1.74 | | $ | 1.40 | | $ | 1.40 |

Basic Earnings Per Share - Discontinued Operations | | | — | | | (0.02 | ) | | | 0.02 | | | 0.26 | | | 0.29 |

Cash Dividends Declared Per Share | | $ | 1.28 | | $ | 1.25 | | | $ | 1.22 | | $ | 1.20 | | $ | 1.18 |

Book Value Per Share | | | 20.01 | | | 19.79 | | | | 19.38 | | | 18.94 | | | 18.18 |

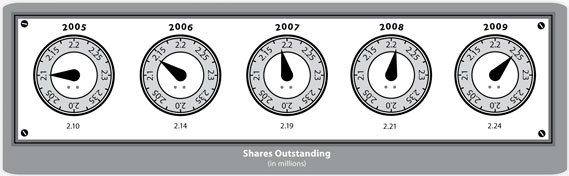

Average Shares Outstanding | | | 2,223,727 | | | 2,201,263 | | | | 2,162,803 | | | 2,120,267 | | | 2,079,851 |

Total Assets | | | 118,801,892 | | | 118,127,714 | | | | 116,332,455 | | | 114,662,572 | | | 113,563,416 |

Long-Term Debt (Less Current Portion) | | | 28,000,000 | | | 23,000,000 | | | | 23,000,000 | | | 28,000,000 | | | 28,000,000 |

Stockholders’ Equity | | | 44,799,871 | | | 43,723,058 | | | | 42,365,233 | | | 40,494,868 | | | 38,157,357 |

Shares Outstanding at Sept. 30 | | | 2,238,987 | | | 2,209,471 | | | | 2,186,143 | | | 2,138,595 | | | 2,098,935 |

RGC Resources 11 2009 Annual Report

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that relate to future transactions, events or expectations. In addition, RGC Resources, Inc. (“Resources” or the “Company”) may publish forward-looking statements relating to such matters as anticipated financial performance, business prospects, technological developments, new products, research and development activities and similar matters. These statements are based on management’s current expectations and information available at the time of such statements and are believed to be reasonable and are made in good faith. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. In order to comply with the terms of the safe harbor, the Company notes that a variety of factors could cause the Company’s actual results and experience to differ materially from the anticipated results or other expectations expressed in the Company’s forward-looking statements. The risks and uncertainties that may affect the operations, performance, development and results of the Company’s business include, but are not limited to, the following: (i) failure to earn on a consistent basis an adequate return on invested capital; (ii) ability to retain and attract professional and technical employees; (iii) the potential loss of large-volume industrial customers to alternate fuels, facility closings or production changes; (iv) volatility in the price and availability of natural gas; (v) uncertainty in the demand for natural gas in the Company’s service area; (vi) general economic conditions both locally and nationally; (vii) increases in interest rates; (viii) increased customer delinquencies and conservation efforts resulting from high fuel costs, difficult economic conditions and/or colder weather; (ix) variations in winter heating degree-days from the 30-year average on which the Company’s billing rates are set; (x) impact of potential climate change legislation regarding limitations on carbon

dioxide emissions; (xi) impact of potential increased regulatory oversight and compliance requirements due to financial, environmental, safety and system integrity laws and regulations; (xii) failure to obtain timely rate relief from regulatory authorities for increasing operating or gas costs; (xiii) capital market conditions and the availability of debt and equity financing to support capital expenditures; (xiv) impact of terrorism; (xv) volatility in actuarially determined benefit costs and plan asset performance; (xvi) effect of natural disasters on production and distribution facilities and the related effect on supply availability and price; and (xvii) changes in accounting regulations and practices, which could change the accounting treatment for certain transactions. All of these factors are difficult to predict and many are beyond the Company’s control. Accordingly, while the Company believes its forward-looking statements to be reasonable, there can be no assurance that they will approximate actual experience or that the expectations derived from them will be realized. When used in the Company’s documents or news releases, the words “anticipate,” “believe,” “intend,” “plan,” “estimate,” “expect,” “objective,” “projection,” “forecast,” “budget,” “assume,” “indicate” or similar words or future or conditional verbs such as “will,” “would,” “should,” “can,” “could” or “may” are intended to identify forward-looking statements.

Forward-looking statements reflect the Company’s current expectations only as of the date they are made. The Company assumes no duty to update these statements should expectations change or actual results differ from current expectations except as required by applicable laws and regulations.

RGC Resources 12 2009 Annual Report

MANAGEMENT’S DISCUSSION & ANALYSIS

OVERVIEW

Resources is an energy services company primarily engaged in the regulated sale and distribution of natural gas to approximately 56,100 residential, commercial and industrial customers in Roanoke, Virginia, and the surrounding areas through its Roanoke Gas Company (“Roanoke Gas”) subsidiary. The utility operations of Roanoke Gas are regulated by the Virginia State Corporation Commission (“SCC” or “Virginia Commission”). Natural gas service is provided at rates and for the terms and conditions approved by the SCC.

Resources also provided the regulated sale and distribution of natural gas to Bluefield, West Virginia, the Town of Bluefield, Virginia, and surrounding areas through its Bluefield Gas Company (“Bluefield Gas”) subsidiary and the Bluefield division of Roanoke Gas (collectively called “Bluefield Operations”). Effective as of October 31, 2007, Resources closed on the sale of the stock of Bluefield Gas to ANGD, LLC and Roanoke Gas completed the sale of the assets of its Bluefield division to Appalachian Natural Gas Company, a subsidiary of ANGD, LLC. The corresponding activities of the Bluefield Operations were classified to discontinued operations in the prior year as discussed in Note 2 of the consolidated financial statements.

Resources also provides certain unregulated natural gas related services through Roanoke Gas and information system services through RGC Ventures of Virginia, Inc., which operates as Application Resources. The unregulated operations represent less than 3% of revenues and margins of Resources.

Local economic conditions, volatility in natural gas prices, and winter weather conditions, have a direct influence on the quantity of natural gas deliveries, and management believes each factor has the potential to significantly impact earnings. Economic downturns generally result in a decline in business and industrial production. For those operations that use natural gas in their production process, lower industrial production has

resulted in a reduction in natural gas usage. Under the current economic climate, the Company has experienced a 12% decline in industrial and transportation volumes from last year’s levels. In addition, significant increases in natural gas commodity prices could have a significant affect on customer usage. Currently, natural gas prices are the lowest the Company has experienced in the last few years; however, sharp increases in the price of natural gas could affect customer usage by encouraging conservation or the use of alternative fuels. Furthermore, a majority of natural gas sales are for space heating during the winter season. Consequently, during warmer winters or unevenly cold winters, customers may significantly reduce their consumption of natural gas. The effect of warmer than normal winters is mitigated by a weather normalization adjustment (“WNA”) factor as discussed below.

The current economic environment has had a negative impact on the local economy as construction activity has slowed significantly and industrial activity has declined. Natural gas consumption by the Company’s industrial and transportation customers has declined by more than 12% from last year’s levels. Much of the decline appears to be related to a reduced level of production activities by these customers; however, the Company anticipates natural gas deliveries to improve as the economy recovers. One of the Company’s transportation customers closed its operations during fiscal 2009 as a result of the economy, which accounted for approximately 50,000 decatherms in deliveries, or $75,000 in margin, annually. A prolonged economic downturn could result in additional closings or lead to further reductions in industrial activity. In addition, growing job losses and deteriorating economic conditions may lead to an increase in customer payment delays and higher bad debt expense. Recent low natural gas commodity prices have reduced customer billings during the current period, which contributed to bad debt expense remaining consistent with prior year amounts. Management continues to closely monitor accounts receivable activity.

RGC Resources 13 2009 Annual Report

Volatility in natural gas prices presents other issues for the Company. The commodity price of natural gas has declined from its peak of more than $13.00 per decatherm during fiscal 2008 to under $4.00 a decatherm in September 2009. Currently, futures prices for natural gas on the NYMEX (New York Mercantile Exchange) range between $5.00 and $7.00 per decatherm over the next 12 months, implying relative stability in prices. A strong economic recovery that increases demand for natural gas or unfavorable environmental legislation could escalate natural gas prices and make natural gas a less attractive energy source and increase the level of bad debts. Supply disruptions, extended periods of cold weather or volatility in the commodities market could also serve to increase natural gas costs.

Because the SCC authorizes billing rates for the utility operations of Roanoke Gas based on normal weather, warmer than normal weather may result in the Company failing to earn its authorized rate of return. The Company has been able to mitigate a significant portion of the risk associated with warmer than normal winter weather by the inclusion of a WNA factor as part of its rate structure. This factor allows the Company to recover revenues equivalent to the margin that would be realized at approximately 6% warmer than the most recent 30-year temperature average for the Company’s service area or refund revenues for any margin realized for weather greater than approximately 6% colder than the 30-year average. The measurement period in determining the weather band extends from April through March with any adjustment to be made to customer bills in late spring. For the WNA period ending March 31, 2009, the Company did not record a WNA adjustment as the number of heating degree-days fell within the 6% weather band during the measurement period. In comparison, the Company recorded approximately $363,000 in additional revenues for the WNA period ended March 31, 2008 for weather that was 11% warmer than the 30-year average. Effective with the WNA period beginning in April 2009, the SCC approved the Company’s request to reduce the weather band for determining WNA from approximately 6% above and below the most recent 30 year average to 3% above and below the most recent 30 year average.

The Company has an approved rate structure in place that mitigates the impact of financing costs of its natural gas inventory. Under this rate structure, Roanoke Gas recognizes revenue for the financing costs or “carrying costs” of its investment in natural gas inventory. The carrying cost revenue factor applied to inventory is based on the Company’s weighted average cost of capital including interest rates on short-term and long-term debt and the Company’s authorized return on equity. During times of rising gas costs and rising inventory levels, the Company recognizes revenues to offset higher financing costs associated with higher inventory balances. Conversely, during times of decreasing inventory costs and lower inventory balances, the Company recognizes less carrying cost revenue as financing costs are lower. The Company recognized approximately $2,328,000 and $2,351,000 in carrying cost revenues for the years ended September 30, 2009 and 2008, respectively. The level of carrying cost revenues for fiscal 2009 was consistent with fiscal 2008; however, due to the much lower price of natural gas in storage at September 30, 2009 compared to September 30, 2008 ($6.05 per decatherm compared to $9.81 per decatherm), carrying cost revenues for fiscal 2010 are expected to be much lower than fiscal 2009, as will be the actual cost for financing inventory levels.

In the short run, as investment in natural gas inventories increases so does the level of borrowing under the Company’s line-of-credit. However, as the factor used in determining the carrying cost revenues is based on the Company’s weighted average cost of capital, carrying cost revenues do not directly correspond with the short-term incremental financing costs. Therefore, when inventory balances decline due to a reduction in commodity prices, net income will decline as carrying cost revenues decrease by a greater amount than short-term financing costs. The inverse occurs when inventory costs increase.

For the fiscal year ended September 30, 2009, the implementation of a non-gas rate increase and a reduction in depreciation expense due to implementation of updated depreciation rates more than offset increases in operation and maintenance expenses.

RGC Resources 14 2009 Annual Report

RESULTSOF OPERATIONS – CONTINUING OPERATIONS

Fiscal Year 2009 Compared with Fiscal Year 2008

Delivered Volumes -The table below reflects volume activity and heating degree-days.

| | | | | | | | | | |

Year Ended September 30, | | 2009 | | 2008 | | Increase/

(Decrease) | | | Percentage | |

Regulated Natural Gas (DTH) | | | | | | | | | | |

Residential and Commercial | | 6,697,738 | | 6,342,950 | | 354,788 | | | 6 | % |

Transportation and Interruptible | | 2,562,731 | | 2,908,304 | | (345,573 | ) | | -12 | % |

| | | | | | | | | | |

Total | | 9,260,469 | | 9,251,254 | | 9,215 | | | 0 | % |

| | | | | | | | | | |

Heating Degree-Days (Unofficial) | | 3,914 | | 3,624 | | 290 | | | 8 | % |

Operating Revenues -The table below reflects operating revenues.

| | | | | | | | | | | | | |

Year Ended September 30, | | 2009 | | 2008 | | Increase/

(Decrease) | | | Percentage | |

Gas Utility | | $ | 80,786,228 | | $ | 93,606,593 | | $ | (12,820,365 | ) | | -14 | % |

Other | | | 1,398,245 | | | 1,030,233 | | | 368,012 | | | 36 | % |

| | | | | | | | | | | | | |

Total Operating Revenues | | $ | 82,184,473 | | $ | 94,636,826 | | $ | (12,452,353 | ) | | -13 | % |

| | | | | | | | | | | | | |

Total gas utility operating revenues for the year ended September 30, 2009 (“fiscal 2009”) decreased by 14% from the year ended September 30, 2008 (“fiscal 2008”) even though total delivered volumes were nearly the same during both periods. The decrease in gas revenues is due to significantly lower gas costs. During fiscal 2008, the commodity price of gas increased significantly from March through July, with the price climbing from $8.00 to nearly $14.00 a decatherm at its peak before dropping below $8.00 a decatherm at the end of September 2008. During fiscal 2009, natural gas prices experienced a steady decline during the year with prices dropping from $8.00 at the beginning of the year to below $4.00 a decatherm by the end of fiscal 2009. For the year, the average per unit cost

of natural gas reflected in cost of sales decreased by 24%. From a volume perspective, tariff sales, consisting primarily of the more weather sensitive residential and commercial customers, increased by 6% corresponding to the 8% rise in the number of heating degree-days. Transportation and interruptible sales declined by 12%, reflecting the economic recession.

Other revenues increased by 36% primarily due to an increase in paving services provided to another local utility under an agreement in effect through the end of January 2010 and a higher level of utility consulting services.

RGC Resources 15 2009 Annual Report

Gross Margin -The table below reflects gross margins.

| | | | | | | | | | | | |

Year Ended September 30, | | 2009 | | 2008 | | Increase/

(Decrease) | | Percentage | |

Gas Utilities | | $ | 26,377,450 | | $ | 25,323,464 | | $ | 1,053,986 | | 4 | % |

Other | | | 698,474 | | | 590,148 | | | 108,326 | | 18 | % |

| | | | | | | | | | | | |

Total Gross Margin | | $ | 27,075,924 | | $ | 25,913,612 | | $ | 1,162,312 | | 4 | % |

| | | | | | | | | | | | |

Gas utility margins increased by 4% due to the combination of higher residential and commercial sales volumes and a non-gas rate increase. Although total delivered volumes were nearly unchanged from last year, the higher margin residential and commercial volumes increased by 6% due to the colder weather. A portion of the margin increase related to the higher volumes was mitigated due to the recognition of approximately $363,000 of WNA revenues in the prior year. In June 2009, the SCC approved the implementation of rates to provide for $1,198,000 in additional annual revenue. The increased rates have been in effect since November 1, 2008. The rate increase provided for both a higher customer base charge, the flat monthly fee billed to each natural gas customer, and a higher volumetric rate. As a result of the rate increase and customer growth, customer base charges accounted for approximately $576,000 of the increase in margin, while volumetric sales margins accounted for approximately $541,000 in additional margin including the WNA offset recognized in fiscal 2008.

Other margins increased by $108,326 due to increased levels of paving and consulting services.

The components of the gas utility margin and other margin increases are summarized below:

Net Utility Margin Increase

| | | | |

Customer Base Charge including rate increase | | $ | 576,238 | |

Volumetric (rate increase and volume) | | | 904,624 | |

WNA | | | (363,376 | ) |

Carrying Cost | | | (23,460 | ) |

Other | | | (40,040 | ) |

| | | | |

Total | | $ | 1,053,986 | |

| | | | |

Other Operating Expenses –Operations expenses increased $458,025, or 5%, in fiscal 2009 compared with fiscal 2008 as a result of increases in employee benefit costs, contractor services and company labor combined with a lower level of capitalized overheads. Employee benefit expenses increased due to an $83,000 increase in pension costs attributable to lower than expected returns on a reduction in plan asset levels and the amortization of an actuarial loss in fiscal 2009 combined with a $95,000 increase in health insurance premiums. The Company expects pension costs to increase significantly in fiscal 2010 due to a higher expected actuarial loss while the increase in medical costs should be more moderate. Contractor services increased $54,000 due to timing related to the completion of leak surveys. Company labor expense increased by $179,000 primarily due to wage adjustments and labor allocations. A reduction in capital expenditures resulted in a $60,000 decline in capitalized overheads. The remaining difference resulted from a variety of other minor expense variances.

Maintenance expenses increased by $295,299, or 20%, due to timing of pipeline leak repairs on the Company’s distribution system identified through leak surveys and the completion of several facilities maintenance projects.

General taxes increased $72,916, or 6%, in fiscal 2009 compared to fiscal 2008 due to higher payroll taxes and property taxes on a greater level of taxable property.

Depreciation expense decreased by $670,418, or 15%, due to the implementation of updated depreciation rates effective as of October 1, 2008. The new rates were the result of a depreciation study that is required to be conducted and filed with the SCC every five years.

RGC Resources 16 2009 Annual Report

The effect of using the new depreciation rates resulted in a reduction of approximately $888,000 in expense. The remaining difference was associated with a greater level of depreciation attributable to higher natural gas plant investment from adding new natural gas customers and pipeline renewal projects.

Other Income (Expense) –Other income (expense) switched from a net income position in fiscal 2008 to a net expense position in 2009 due to significantly lower interest income on cash investments and a greater level of charitable giving.

Interest Expense –Total interest expense for fiscal 2009 decreased by $114,976, or 6%, from fiscal 2008, as a result of declines in the interest rates on the Company’s line-of-credit and a lower interest rate on the new $5,000,000 note which replaced a higher interest rate debt that matured in fiscal 2008.

Income Taxes –Income tax expense from continuing operations increased $405,567, or 16%, from fiscal 2008 corresponding to a 15% increase in pre-tax earnings. The effective tax rate for fiscal 2009 was 38.0% compared to 37.7% in fiscal 2008.

Net Income and Dividends –Income from continuing operations for fiscal 2009 was $4,869,010 compared to $4,257,824 for fiscal 2008. Basic and diluted earnings per share from continuing operations were $2.19 and $2.18 in fiscal 2009, including $0.25 associated with the effect of the change in depreciation rates, compared to $1.94 and $1.93 in fiscal 2008. Dividends declared per share of common stock were $1.28 in fiscal 2009 and $1.25 in fiscal 2008.

ASSET MANAGEMENT

Roanoke Gas uses a third party asset manager to manage its pipeline transportation, storage rights and gas supply inventories and deliveries. In return for being able to utilize the excess capacities of the transportation and storage rights, the third party pays Roanoke Gas a monthly utilization fee, which is used to reduce the cost of gas for customers. The current agreement expires in October 2010.

CAPITAL RESOURCESAND LIQUIDITY

Due to the capital intensive nature of the utility business, as well as the related weather sensitivity, the Company’s primary capital needs are for the funding of its continuing construction program, the seasonal funding of its natural gas inventories and accounts receivable and payment of dividends. To meet these needs, the Company relies on its operating cash flows, line-of-credit agreement, long-term debt and capital raised through the Company’s Dividend Reinvestment and Stock Purchase Plan (“DRIP”).

Cash and cash equivalents increased by $6,546,924 in fiscal 2009 compared to a $532,881 decrease in fiscal 2008. The following table summarizes the categories of sources and uses of cash:

| | | | | | | | |

Cash Flow Summary | | 2009 | | | 2008 | |

Continuing operations: | | | | | | | | |

Provided by operating activities | | $ | 22,705,812 | | | $ | 497,778 | |

Used in investing activities | | | (5,224,954 | ) | | | (3,166,506 | ) |

Provided by (used in) financing activities | | | (10,933,934 | ) | | | 2,061,120 | |

Cash provided by discontinued operations | | | — | | | | 74,727 | |

| | | | | | | | |

Increase (decrease) in cash and cash equivalents | | $ | 6,546,924 | | | $ | (532,881 | ) |

| | | | | | | | |

The seasonal nature of the natural gas business causes operating cash flows to fluctuate significantly during the year as well as from year to year. Factors including weather, energy prices, natural gas storage levels and customer collections all contribute to working capital levels and related cash flows. Generally, operating cash flows are positive during the second and third quarters as a combination of earnings, declining storage gas levels and collections on customer accounts all contribute to higher cash levels. During the first and fourth quarters, operating cash flows generally decrease due to the increases in natural gas storage levels, rising customer receivable balances and construction activity. In fiscal 2009, cash

RGC Resources 17 2009 Annual Report

provided by continuing operating activities increased by approximately $22,208,000, from $498,000 in fiscal 2008 to $22,706,000 in fiscal 2009. The significant increase in over-collection of gas costs combined with reductions in gas in storage, accounts receivable and accounts payable due to the declining commodity price of natural gas accounted for most of the increase in cash provided by operations. Conversely, fiscal 2008 experienced rising gas costs during the year. The circumstances that resulted in the generation of significant levels of cash from operating activities were unusual and are not indicative of historical or expected results. The Company anticipates cash provided by operating activities to be much less or even become a use of cash in fiscal 2010.

Investing activities are generally composed of expenditures under the Company’s construction program, which involves a combination of replacing aging bare steel and cast iron pipe with new plastic or coated steel pipe and expansion of its natural gas system to meet the demands of customer growth. Cash flows used in investing activities increased by approximately $2,058,000 due to the $3,941,000 in net proceeds received from the sale of the Bluefield Operations in fiscal 2008 partially offset by a reduced level of capital expenditures. Total capital expenditures from continuing operations were approximately $5,753,000 and $6,539,000 for the years ended September 30, 2009 and 2008, respectively. Capital expenditures for expanding natural gas service declined from last year due to reductions in new construction, which resulted from the continuing slowdown in real estate development and the current economic environment. Expenditures under the Company’s pipeline renewal program also declined as 5.6 miles of natural gas distribution main were replaced in fiscal 2009 compared to 8.9 miles in fiscal 2008. The decline in pipeline renewal activity was partially attributed to a greater focus on pipeline maintenance and repairs. The Company plans to continue its focus on pipeline renewals in 2010 and expects such expenditures to continue at comparable or higher levels for the next several years. Operating cash flow provided by depreciation contributed approximately $3,815,000 in support of fiscal 2009 capital expenditures, or approximately 66% of the total investment, compared to approximately $4,527,000, or 69% of the total investment in fiscal 2008. The Company also relies on its line-of-credit

agreement, other operating cash flows and long-term debt financing to provide the balance of the underlying funding for its capital expenditures. With the implementation of lower depreciation rates, future capital expenditure funding will be more dependent on corporate borrowing activity.

Financing activities generally consist of long-term and short-term borrowings and repayments, issuance of stock and the payment of dividends. As discussed above, the Company uses its line-of-credit arrangement to fund seasonal working capital needs as well as provide temporary financing for capital projects. Cash flow from continuing financing activities changed by nearly $13,000,000, moving from more than $2,000,000 in cash generated to nearly $11,000,000 in cash used in fiscal 2009. The primary factor in the change corresponds to the net pay down in the Company’s line-of-credit balance due to the cash generated from operating activities and the issuance of a new note. The Company entered into a $5,000,000 variable rate note in October 2008 and used the proceeds to refinance a portion of the line-of-credit balance that provided temporary funding for the retirement of a $5,000,000 first mortgage note that matured in July 2008.

On March 23, 2009 the Company renewed its line-of-credit agreement for Roanoke Gas. Although the Company was able to renew the line-of-credit, the credit markets at the time of renewal resulted in the renewal being on terms less favorable than the expiring agreement. The new agreement increased the variable interest rate to 30-day LIBOR plus 100 basis points and imposed an availability fee of 15 basis points applied to the difference between the face amount of the note and the average outstanding balance during the period. In response to the implementation of an availability fee, the bank agreed to adjust the available limits on a monthly basis to accommodate the Company’s seasonal borrowing demands and minimize overall borrowing costs. Under the agreement, the Company’s total available limits during its term range from $1,000,000 to $18,000,000. Furthermore, the bank also agreed to allow the Company to reduce the available borrowing limits during the term of the agreement in order to minimize the impact of the availability fee on the Company. Subsequent to September 30, 2009, the Company requested a reduction in the

RGC Resources 18 2009 Annual Report

available limits under the line-of-credit agreement due to its current cash position. The Company’s total available limits under the remaining term of the line-of-credit agreement as of September 30, 2009 and as amended subsequently are as follows:

| | | | | | |

Period Beginning | | Available Limit at

September 30, 2009 | | Revised

Limit |

September 30, 2009 | | $ | 3,000,000 | | $ | 3,000,000 |

October 24, 2009 | | | 18,000,000 | | | 7,000,000 |

November 25, 2009 | | | 15,000,000 | | | 7,000,000 |

January 23, 2010 | | | 8,000,000 | | | 8,000,000 |

February 25, 2010 | | | 5,000,000 | | | 5,000,000 |

The line-of-credit agreement will expire March 31, 2010, unless extended. The Company anticipates being able to extend or replace the line-of-credit upon expiration; however, there is no guarantee that the line-of-credit will be extended or replaced under the terms currently in place.

The Company’s $15,000,000 variable rate note is currently scheduled to mature December 1, 2010. The note provides for an interest rate of LIBOR plus 69 basis points and has an interest rate swap that essentially converts the note into a fixed rate instrument at a rate of 5.74%. Due to the current economic climate and its effect on the credit markets, the Company has been unable to extend the note by more than one year without incurring a higher interest rate than is currently in place. The current credit market has increased the interest rate spreads on commercial debt instruments. The Company has had preliminary discussions with the issuing bank regarding extension of the note and anticipates being able to extend the note on a one year basis on terms comparable to the current note.

The remainder of the financing cash flows was associated with approximately $765,000 of proceeds related to stock issuances under the DRIP and Key Employee Stock Option Plan, $87,000 receipt on the note with ANGD, Inc. and approximately $2,800,000 in dividends paid.

At September 30, 2009, the Company’s consolidated long-term capitalization was 62% equity and 38% debt, compared to 65% equity and 35% debt at September 30, 2008.

REGULATORY AFFAIRS

On November 1, 2008, Roanoke Gas Company placed into effect new base rates designed to produce $1,198,000 in additional annual revenues. The Company received a final order from the SCC on June 10, 2009 approving the full amount of the requested revenue.

The final order also included an agreement to modify the WNA mechanism, which mitigates the impact of temperature volatility on the Company’s margin due to weather. The order approved a request to reduce the current weather band from approximately 6% of the 30-year average to a weather band of 3% of the 30-year average starting with the WNA period that began in April 2009. The implementation of this new weather band will further reduce the downside margin exposure that the Company has to warmer than normal weather. In addition, the new weather band will correspondingly limit the upside margin benefit from colder than normal weather to a 3% level.

The Company also filed with the SCC on July 1, 2009 the results of an updated depreciation study, which is required every 5 years. The new depreciation study, which is based on average remaining service life, extended the expected life of the Company’s LNG plant, natural gas service lines and computer equipment resulting in a reduction in the overall composite weighted average depreciation rate from 4.12% to 3.31%, based on September 30, 2008 utility plant balances. The SCC approved the depreciation study filing and instructed the Company to implement the new rates effective October 1, 2008. As a result, the Company recorded the full effect of the change in depreciation rates for the fiscal year ended September 30, 2009 in the Company’s fourth quarter results of operations.

RGC Resources 19 2009 Annual Report

The Company completed an evaluation of its revenue requirements and determined that a rate filing for increased non-gas rates was not warranted in the current year. Management will continue to monitor the Company’s financial performance to determine when to make the next rate filing.

CRITICAL ACCOUNTING POLICIESAND ESTIMATES

The consolidated financial statements of Resources are prepared in accordance with accounting principles generally accepted in the United States of America. The amounts of assets, liabilities, revenues and expenses reported in the Company’s financial statements are affected by accounting policies, estimates and assumptions that are necessary to comply with generally accepted accounting principles. Estimates used in the financial statements are derived from prior experience, statistical analysis and professional judgments. Actual results may differ significantly from these estimates and assumptions.

The Company considers an estimate to be critical if it is material to the financial statements and it requires assumptions to be made that were uncertain at the time the estimate was made and changes in the estimate are reasonably likely to occur from period to period. The Company considers the following accounting policies and estimates to be critical.

Regulatory accounting –The Company’s regulated operations follow the accounting and reporting requirements of

FASB ASC No. 980,Regulated Operations. The economic effects of regulation can result in a regulated company deferring costs that have been or are expected to be recovered from customers in a period different from the period in which the costs would be charged to expense by an unregulated enterprise. When this occurs, costs are deferred as assets in the consolidated balance sheet (regulatory assets) and recorded as expenses when such amounts are reflected in rates. Additionally, regulators can impose liabilities upon a regulated company for amounts previously collected from customers and for current collection in rates of costs that are expected to be incurred in the future (regulatory liabilities).

If, for any reason, the Company ceased to meet the criteria for application of regulatory accounting treatment for all or part of its operations, the Company would remove the regulatory assets or liabilities from the balance sheet related to those portions no longer meeting the criteria and include them in the consolidated statement of income and comprehensive income for the period in which the discontinuance occurred.

Revenue recognition –Regulated utility sales and transportation revenues are based upon rates approved by the SCC. The non-gas cost component of rates may not be changed without a formal rate increase application and corresponding authorization by the SCC; however, the gas cost component of rates are adjusted quarterly through the purchased gas adjustment (“PGA”) mechanism with administrative approval from the SCC.

RGC Resources 20 2009 Annual Report

The Company bills its regulated natural gas customers on a monthly cycle. The billing cycle periods for most customers do not coincide with the accounting periods used for financial reporting. The Company accrues estimated revenue for natural gas delivered to customers not yet billed during the accounting period. Determination of unbilled revenue relies on the use of estimates, weather during the period and current and historical data. The financial statements included unbilled revenue of $1,173,561 and $1,475,406 as of September 30, 2009 and 2008.

Allowance for Doubtful Accounts –The Company evaluates the collectibility of its accounts receivable balances based upon a variety of factors including loss history, level of delinquent account balances and general economic climate.

Pension and Postretirement Benefits –The Company offers a defined benefit pension plan (“pension plan”) and a postretirement medical and life insurance plan (“post- retirement plan”) to eligible employees. The expenses and liabilities associated with these plans, as disclosed in Note 7 to the consolidated financial statements, are based on numerous assumptions and factors, including provisions of the plans, employee demographics, contributions made to the plan, return on plan assets and various actuarial calculations, assumptions and accounting requirements. In regard to the pension plan, specific factors include assumptions regarding the discount rate used in determining future benefit obligations, expected long-term rate of return on plan assets, compensation increases and life expectancies. Similarly, the postretirement medical plan also requires the estimation of many of the same factors as the pension plan in addition to assumptions

regarding the rate of medical inflation and Medicare availability. Actual results may differ materially from the results expected from the actuarial assumptions due to changing economic conditions, volatility in interest rates and changes in life expectancy. Such differences may result in a material impact on the amount of expense recorded in future periods or the value of the obligations on the balance sheet.

In selecting the discount rate to be used in determining the benefit liability, the Company considered the rates of return on high-quality fixed-income investments that corresponded to the benefit streams expected under both the pension plan and postretirement plan. The Company also used an asset/liability model to evaluate the probability of meeting the returns on its targeted investment allocation model. The investment policy as of the measurement date in September reflected a targeted allocation of 60% equity and 40% fixed income for an assumed long-term rate of return of 7.25% on the pension plan and a targeted allocation of 50% equity and 50% fixed income for an assumed long-term rate of return of 5.18% (net of income taxes) for the postretirement plan. Based on the assumptions described above and in Note 7, pension expense is expected to increase from approximately $459,000 in fiscal 2009 to $759,000 in fiscal 2010 and postretirement expense is expected to rise from approximately $540,000 in fiscal 2009 to $606,000 in fiscal 2010. The Company expects to contribute approximately $800,000 to its pension plan and $600,000 to its postretirement plan in fiscal 2010. Funding levels are expected to remain at this level or higher over the next several years. However, funding requirements under the Pension Protection Act of 2006 could require the Company to increase its projected contribution levels in order to prevent any benefit restrictions.

RGC Resources 21 2009 Annual Report

The following schedule reflects the sensitivity of pension costs to changes in certain actuarial assumptions, assuming that the other components of the calculation remain constant.

| | | | | | | | | |

Actuarial Assumption | | Change in

Assumption | | | Impact on

Pension Cost | | Impact on Projected

Benefit Obligation |

Discount rate | | -0.25 | % | | $ | 118,000 | | $ | 690,000 |

Rate of return on plan assets | | -0.25 | % | | | 28,000 | | | N/A |

Rate of increase in compensation | | 0.25 | % | | | 44,000 | | | 238,000 |

The following schedule reflects the sensitivity of postretirement benefit costs from changes in certain actuarial assumptions, while the other components of the calculation remain constant.

| | | | | | | | | |

Actuarial Assumption | | Change in

Assumption | | | Impact on

Postretirement

Benefit Cost | | Impact on

Accumulated

Postretirement

Benefit Obligation |

Discount rate | | -0.25 | % | | $ | 24,000 | | $ | 313,000 |

Rate of return on plan assets | | -0.25 | % | | | 16,000 | | | N/A |

Health care cost trend rate | | 0.25 | % | | | 25,000 | | | 323,000 |

Derivatives –The Company may hedge certain risks incurred in its operation through the use of derivative instruments. The Company applies the requirements of FASB ASC No. 815,Derivatives and Hedging, which requires the recognition of derivative instruments as assets or liabilities in the Company’s balance sheet at fair value. In most instances, fair value is based upon quoted futures prices for natural gas commodities and interest rate futures for interest rate swaps. Changes in the commodity and futures markets will impact the estimates of fair value in the future. Furthermore, the actual market value at the point of realization of the derivative may be significantly different from the values used in determining fair value in prior financial statements.

MARKET RISK

The Company is exposed to market risks through its natural gas operations associated with commodity prices. The Company’s hedging and derivatives policy, as authorized by the Company’s Board of Directors, allows management to enter into both physical and financial transactions for the purpose of managing commodity risk

of its business operations. The policy also specifies that the combination of all commodity hedging contracts for any 12-month period shall not exceed a total hedged volume of 90% of projected volumes. Finally, the policy specifically prohibits the utilization of derivatives for the purposes of speculation.

The Company manages the price risk associated with purchases of natural gas by using a combination of liquefied natural gas (LNG) storage, storage gas, fixed price contracts, spot market purchases and derivative commodity instruments including futures, price caps, swaps and collars.

As of September 30, 2009, the Company has collar agreements outstanding for the purpose of hedging the price of natural gas during the winter period for 800,000 decatherms. In addition, the Company also has a commodity contract for the purchase of 1,057,000 decatherms of gas at a price of $6.36 per decatherm. Any cost incurred or benefit received from the derivative or other hedging arrangements would be expected to be recovered or refunded through the regulated natural gas PGA mechanism. The SCC currently allows for full recovery of prudent costs associated with

RGC Resources 22 2009 Annual Report

natural gas purchases, and any additional costs or benefits associated with the settlement of the derivative contracts will be passed through to customers when realized.

The Company is also exposed to market risk related to changes in interest rates associated with variable interest rates on its debt. The Company has two variable interest rate notes with banks that have corresponding swap agreements that essentially convert the debt to fixed rate debt. The valuation of the swap agreements are reflected in Note 1. The Company also has a variable rate line-of-credit with a bank with the interest rate based on the London Interbank Offered Rate (“LIBOR”). As of September 30, 2009, the Company had no outstanding balance under its line-of-credit.

OTHER RISKS

The Company is exposed to risks other than commodity and interest rates. Such events, situations or conditions have or potentially could have an impact on the future results of operations of the Company. For most of the items described below, Roanoke Gas has a means to recover increased costs through formal rate application filings, as well as the ability to pass along increases in natural gas cost. However, rate applications are generally filed based upon historical expenses, which generally results in the Company lagging in the recovery of rapidly increasing operating expenses. Moreover, there can be no guarantee that the SCC will allow recovery for all such increased costs when rate applications are filed.

Regulatory and Governmental Actions: As discussed above, Virginia has a means to allow the regulated operations of the Company to recover increased costs and earn a reasonable rate of return on equity. The SCC is the state agency responsible for regulating the operations of Roanoke Gas and approves the rates charged to its customers. If the SCC were to impose limitations that delayed or prohibited the Company from placing rates into effect to timely recover costs and earn its authorized rate of return, the earnings of the Company could be negatively impacted. Furthermore, legislation at the state or federal level could result in increased costs and place additional burdens on the Company.

Environmental Legislation:The passage of environmental legislation that mandates reductions in carbon emissions or other similar restrictions could have a negative effect on the Company over the long-term as it relates to the Company’s core operations. Natural gas is a clean and efficient energy source; however, the combustion of natural gas results in carbon related emissions. The extent to which carbon emissions would be restricted under any such legislation and the ability of technological improvements to minimize such emissions would be critical in determining any potential impact to the Company.

RGC Resources 23 2009 Annual Report

Energy Prices:Energy costs represent the single largest expense of the Company with the cost of natural gas representing approximately 76% and 80% for fiscal 2009 and 2008 of the total operating expenses of the Company’s natural gas utility operations. Increases or decreases in natural gas costs are passed through to customers under the present PGA mechanism. As discussed above, increases in the commodity price of natural gas may cause existing customers to conserve or switch to alternate sources of energy. High natural gas prices may also discourage new home developers and new potential customers from selecting natural gas as their energy choice. Furthermore, during periods when natural gas prices are significantly higher than historical levels, customers may have much greater difficulty paying their natural gas bills, resulting in higher bad-debt expense and lower earnings. Roanoke Gas Company’s rate structure provides a level of protection against the impact that rising energy prices may have on bad debts by providing for recovery of these costs. However, the rate structure will not protect the Company from increases in the rate of bad debts.

Pipeline Reliability:Roanoke Gas is served directly by two primary pipelines. These two pipelines provide 100% of the natural gas supplied to the Company’s customers. Depending upon weather conditions and the level of customer demand, failure of one or both of these transmission pipelines could have a major adverse impact on the Company.

Customer Credit:Gas costs represent a major portion of the total customer bill. The Company has worked diligently at

minimizing bad debts and bad-debt write offs. However, significant increases or spikes in natural gas prices could result in an increased rate of delinquencies as customers face higher natural gas bills as well as other higher energy costs. Furthermore, adverse economic conditions and rising unemployment could also lead to an increase in delinquency of customer payments and higher bad debts. In addition, the SCC has specific notice requirements that the Company must first comply with before disconnecting natural gas service for customer nonpayment. The Company has mitigated some of the risk through deposit requirements. Furthermore, the Company’s approved rate structure provides a level of protection against the impact that rising energy prices may have on bad debts. Nevertheless, the Company has no such protection if the percentage of bad debts to revenues increases above recent historical levels.

Weather:The nature of the Company’s business is highly dependent upon weather – specifically, winter weather. Cold weather increases energy consumption by customers and therefore increases revenues and margins. Conversely, warm weather reduces energy consumption and ultimately revenues and margins. Since 2003, Roanoke Gas Company’s rate structure has included a weather normalization adjustment factor that operated around a weather band of approximately 6% above and below the 30 year average for heating degree-days. This exposure to weather related risk was reduced in fiscal 2009 when the SCC approved changes to the WNA by reducing the weather

RGC Resources 24 2009 Annual Report

band from 6% to 3%. Therefore, the Company should be at risk for no more than a 3% swing in heating degree-days above or below the 30 year average.

Credit and Capital Availability:The capital intensive and seasonal nature of the utility operations requires the access to sufficient levels of debt and equity capital. Recent events in the credit and financial markets have impacted the cost and availability of short-term and long-term credit funding. The Company was able to complete the

renewal of its line-of-credit arrangement in March; however, the new agreement was at less favorable terms than the expiring agreement. The new agreement increased the variable interest rate based on 30-day LIBOR and imposed an availability fee applied to the difference between the face amount of the note and the average outstanding balance during the period. The failure to obtain funding when needed, or obtain funding only on unfavorable terms, could have a significant negative impact to the Company.

RGC Resources 25 2009 Annual Report

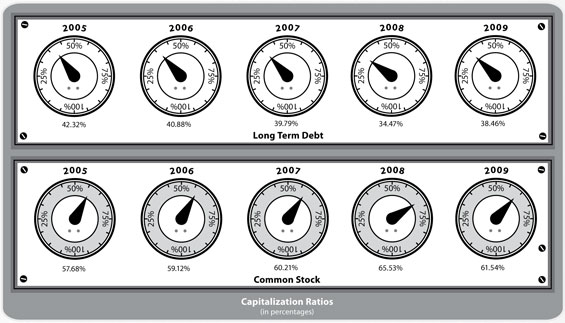

CAPITALIZATION RATIOS

| | | | | | | | | | | | | | | | | | | | |

Years Ended September 30, | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

COMMON STOCK: | | | | | | | | | | | | | | | | | | | | |

Shares Issued | | | 2,238,987 | | | | 2,209,471 | | | | 2,186,143 | | | | 2,138,595 | | | | 2,098,935 | |

Continuing Operations: | | | | | | | | | | | | | | | | | | | | |

Basic Earnings Per Share | | $ | 2.19 | | | $ | 1.94 | | | $ | 1.74 | | | $ | 1.40 | | | $ | 1.40 | |

Diluted Earnings Per Share | | $ | 2.18 | | | $ | 1.93 | | | $ | 1.73 | | | $ | 1.39 | | | $ | 1.39 | |

Discontinued Operations: | | | | | | | | | | | | | | | | | | | | |

Basic Earnings Per Share | | $ | 0.00 | | | $ | (0.02 | ) | | $ | 0.02 | | | $ | 0.26 | | | $ | 0.29 | |

Diluted Earnings Per Share | | $ | 0.00 | | | $ | (0.02 | ) | | $ | 0.02 | | | $ | 0.26 | | | $ | 0.29 | |

Dividends Paid Per Share (Cash) | | $ | 1.28 | | | $ | 1.25 | | | $ | 1.22 | | | $ | 1.20 | | | $ | 1.18 | |

Dividends Paid Out Ratio | | | 58.4 | % | | | 65.1 | % | | | 69.3 | % | | | 72.3 | % | | | 69.8 | % |

CAPITALIZATION RATIOS: | | | | | | | | | | | | | | | | | | | | |

Long-Term Debt, Including Current Maturities | | | 38.5 | | | | 34.5 | | | | 39.8 | | | | 40.9 | | | | 42.3 | |

Common Stock and Surplus | | | 61.5 | | | | 65.5 | | | | 60.2 | | | | 59.1 | | | | 57.7 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | | 100.0 | | | | 100.0 | | | | 100.0 | | | | 100.0 | | | | 100.0 | |

| | | | | | | | | | | | | | | | | | | | |

Long-Term Debt, Including Current Maturities | | $ | 28,000,000 | | | $ | 23,000,000 | | | $ | 28,000,000 | | | $ | 28,000,000 | | | $ | 28,000,000 | |

Common Stock and Surplus | | | 44,799,871 | | | | 43,723,058 | | | | 42,365,233 | | | | 40,494,868 | | | | 38,157,357 | |

| | | | | | | | | | | | | | | | | | | | |

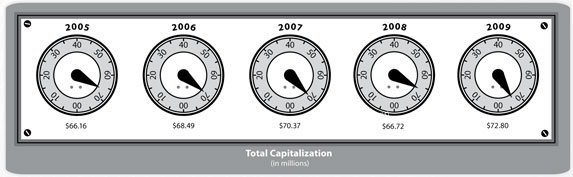

Total Capitalization Plus Current Maturities | | $ | 72,799,871 | | | $ | 66,723,058 | | | $ | 70,365,233 | | | $ | 68,494,868 | | | $ | 66,157,357 | |

| | | | | | | | | | | | | | | | | | | | |

RGC Resources 26 2009 Annual Report

MARKET PRICEAND DIVIDEND INFORMATION

RGC Resources’ common stock is listed on the NASDAQ National Market under the trading symbol RGCO. Payment of dividends is within the discretion of the Board of Directors and will depend on, among other factors, earnings, capital requirements, and the operating and financial condition of the Company. The Company’s long-term indebtedness contains restrictions on dividends based on cumulative net earnings and dividends previously paid.

| | | | | | | | | |

| | | Range of Bid Prices | | Cash Dividends

Declared |

Fiscal Year Ended September 30, | | High | | Low | |

2009 | | | | | | | | | |

First Quarter | | $ | 30.07 | | $ | 24.15 | | $ | 0.320 |

Second Quarter | | | 28.00 | | | 21.92 | | | 0.320 |

Third Quarter | | | 27.38 | | | 22.95 | | | 0.320 |

Fourth Quarter | | | 30.78 | | | 24.94 | | | 0.320 |

| | | |

2008 | | | | | | | | | |

First Quarter | | $ | 33.35 | | $ | 26.02 | | $ | 0.3125 |

Second Quarter | | | 31.43 | | | 27.25 | | | 0.3125 |

Third Quarter | | | 29.25 | | | 27.13 | | | 0.3125 |

Fourth Quarter | | | 32.50 | | | 26.68 | | | 0.3125 |

RGC Resources 27 2009 Annual Report

SUMMARYOF GAS SALESAND STATISTICS

| | | | | | | | | | | | | | | | |

Years Ended September 30, | | 2009 | | 2008 | | | 2007 | | 2006 | | 2005 |

REVENUES: | | | | | | | | | | | | | | | | |

Residential Sales | | $ | 47,544,448 | | $ | 52,927,761 | | | $ | 50,791,195 | | $ | 52,274,204 | | $ | 49,332,645 |

Commercial Sales | | | 29,909,205 | | | 36,507,326 | | | | 34,566,385 | | | 36,159,320 | | | 33,059,542 |

Interruptible Sales | | | 635,301 | | | 1,509,193 | | | | 1,379,870 | | | 3,054,240 | | | 3,029,697 |

Transportation Gas Sales | | | 2,506,958 | | | 2,428,656 | | | | 2,254,594 | | | 2,067,929 | | | 2,110,002 |

Backup Services | | | 300 | | | 3,600 | | | | 3,600 | | | 3,600 | | | 62,756 |

Late Payment Charges | | | 56,718 | | | 55,410 | | | | 55,438 | | | 70,191 | | | 55,109 |

Miscellaneous Gas Utility Revenue | | | 133,298 | | | 174,647 | | | | 124,579 | | | 116,924 | | | 102,918 |

Other | | | 1,398,245 | | | 1,030,233 | | | | 725,640 | | | 844,464 | | | 848,167 |

| | | | | | | | | | | | | | | | |

Total | | $ | 82,184,473 | | $ | 94,636,826 | | | $ | 89,901,301 | | $ | 94,590,872 | | $ | 88,600,836 |

NET INCOME | | | | | | | | | | | | | | | | |

Continuing Operations | | $ | 4,869,010 | | $ | 4,257,824 | | | $ | 3,765,669 | | $ | 2,961,802 | | $ | 2,916,798 |

Discontinued Operations | | | — | | | (36,690 | ) | | | 40,540 | | | 549,729 | | | 590,108 |

| | | | | | | | | | | | | | | | |

Net Income | | $ | 4,869,010 | | $ | 4,221,134 | | | $ | 3,806,209 | | $ | 3,511,531 | | $ | 3,506,906 |

DTH DELIVERED: | | | | | | | | | | | | | | | | |

Residential | | | 3,866,956 | | | 3,557,249 | | | | 3,778,194 | | | 3,588,364 | | | 3,987,368 |

Commercial | | | 2,830,782 | | | 2,785,701 | | | | 2,886,403 | | | 2,793,988 | | | 2,859,471 |

Interruptible | | | 75,061 | | | 128,875 | | | | 138,176 | | | 278,535 | | | 321,860 |

Transportation Gas | | | 2,487,670 | | | 2,779,429 | | | | 2,735,456 | | | 2,853,500 | | | 3,202,923 |

Backup Service | | | — | | | — | | | | — | | | — | | | 5,531 |

| | | | | | | | | | | | | | | | |

Total | | | 9,260,469 | | | 9,251,254 | | | | 9,538,229 | | | 9,514,387 | | | 10,377,153 |

HEATING DEGREE DAYS | | | 3,914 | | | 3,624 | | | | 3,735 | | | 3,714 | | | 3,783 |

NUMBER OF CUSTOMERS: | | | | | | | | | | | | | | | | |

Natural Gas | | | | | | | | | | | | | | | | |

Residential | | | 51,069 | | | 50,630 | | | | 50,371 | | | 49,649 | | | 49,178 |

Commercial | | | 5,018 | | | 5,026 | | | | 5,017 | | | 4,948 | | | 4,939 |

Interruptible and Interruptible | | | | | | | | | | | | | | | | |

Transportation Service | | | 32 | | | 33 | | | | 32 | | | 32 | | | 36 |

| | | | | | | | | | | | | | | | |

Total | | | 56,119 | | | 55,689 | | | | 55,420 | | | 54,629 | | | 54,153 |

GAS ACCOUNT (DTH): | | | | | | | | | | | | | | | | |

Natural Gas Available | | | 9,549,231 | | | 9,528,890 | | | | 9,744,431 | | | 9,703,011 | | | 10,546,259 |

Natural Gas Deliveries | | | 9,260,469 | | | 9,251,254 | | | | 9,538,229 | | | 9,514,387 | | | 10,377,153 |

Storage - LNG | | | 124,925 | | | 122,874 | | | | 65,279 | | | 98,936 | | | 89,896 |

Company Use and Miscellaneous | | | 39,697 | | | 45,180 | | | | 28,862 | | | 36,321 | | | 47,568 |

System Loss | | | 124,140 | | | 109,582 | | | | 112,061 | | | 53,367 | | | 31,642 |

| | | | | | | | | | | | | | | | |

Total Gas Available | | | 9,549,231 | | | 9,528,890 | | | | 9,744,431 | | | 9,703,011 | | | 10,546,259 |

TOTAL ASSETS | | $ | 118,801,892 | | $ | 118,127,714 | | | $ | 116,332,455 | | $ | 114,662,572 | | $ | 113,563,416 |

LONG-TERM OBLIGATIONS | | $ | 28,000,000 | | $ | 23,000,000 | | | $ | 23,000,000 | | $ | 28,000,000 | | $ | 28,000,000 |

RGC Resources 28 2009 Annual Report

RGC Resources, Inc. and Subsidiaries

Consolidated Financial Statements

for the Years Ended September 30, 2009

and 2008, and Report of Independent

Registered Public Accounting Firm

RGC RESOURCES, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

| | |

| | | Page |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | 1 |

| |

CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED SEPTEMBER 30, 2009 AND 2008: | | |

| |

Consolidated Balance Sheets | | 2-3 |

| |

Consolidated Statements of Income and Comprehensive Income | | 4-5 |

| |

Consolidated Statements of Stockholders’ Equity | | 6 |

| |

Consolidated Statements of Cash Flows | | 7-8 |

| |

Notes to Consolidated Financial Statements | | 9-35 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors and Stockholders

RGC Resources, Inc.

Roanoke, Virginia

We have audited the accompanying consolidated balance sheets of RGC Resources, Inc. and Subsidiaries (“the Company”) as of September 30, 2009 and 2008, and the related consolidated statements of income and comprehensive income, stockholders’ equity, and cash flows for the years then ended. The Company’s management is responsible for these financial statements. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of RGC Resources, Inc. and Subsidiaries as of September 30, 2009 and 2008, and the consolidated results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

|

|

|

| CERTIFIED PUBLIC ACCOUNTANTS |

319 McClanahan Street, S.W.

Roanoke, Virginia

December 16, 2009

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

AS OF SEPTEMBER 30, 2009 AND 2008

| | | | | | | | |

| | | 2009 | | | 2008 | |

ASSETS | | | | | | | | |

CURRENT ASSETS: | | | | | | | | |

Cash and cash equivalents | | $ | 7,422,360 | | | $ | 875,436 | |

Short-term investments | | | — | | | | 500,000 | |

Accounts receivable, less allowance for doubtful accounts of $50,687 in 2009 and $63,791 in 2008 | | | 3,562,837 | | | | 5,086,790 | |

Note receivable | | | 87,000 | | | | 87,000 | |

Materials and supplies | | | 587,815 | | | | 553,604 | |

Gas in storage | | | 16,072,911 | | | | 26,122,686 | |

Prepaid income taxes | | | 1,974,917 | | | | 1,479,693 | |

Deferred income taxes | | | 3,424,628 | | | | 2,187,795 | |

Under-recovery of gas costs | | | — | | | | 1,013,087 | |

Other | | | 985,110 | | | | 505,761 | |

| | | | | | | | |

Total current assets | | | 34,117,578 | | | | 38,411,852 | |

| | | | | | | | |

UTILITY PROPERTY: | | | | | | | | |

In service | | | 118,009,532 | | | | 113,533,184 | |

Accumulated depreciation and amortization | | | (41,104,408 | ) | | | (39,038,120 | ) |

| | | | | | | | |

In service, net | | | 76,905,124 | | | | 74,495,064 | |

| | | | | | | | |

Construction work in progress | | | 1,604,046 | | | | 1,113,008 | |

| | | | | | | | |

Utility plant, net | | | 78,509,170 | | | | 75,608,072 | |

| | | | | | | | |

OTHER ASSETS: | | | | | | | | |

Note receivable | | | 1,126,000 | | | | 1,213,000 | |

Regulatory assets | | | 4,989,347 | | | | 2,762,241 | |

Other | | | 59,797 | | | | 132,549 | |

| | | | | | | | |

Total other assets | | | 6,175,144 | | | | 4,107,790 | |

| | | | | | | | |

TOTAL ASSETS | | $ | 118,801,892 | | | $ | 118,127,714 | |

| | | | | | | | |

(Continued)

- 2 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

AS OF SEPTEMBER 30, 2009 AND 2008

| | | | | | | | |

| | | 2009 | | | 2008 | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

CURRENT LIABILITIES: | | | | | | | | |

Borrowings under lines-of-credit | | $ | — | | | $ | 13,960,000 | |

Dividends payable | | | 716,556 | | | | 690,538 | |

Accounts payable | | | 4,449,735 | | | | 8,215,319 | |

Customer credit balances | | | 4,204,556 | | | | 4,237,043 | |

Income taxes payable | | | — | | | | 3,206 | |

Customer deposits | | | 1,601,206 | | | | 1,522,480 | |

Accrued expenses | | | 2,219,587 | | | | 2,111,614 | |

Over-recovery of gas costs | | | 5,651,847 | | | | — | |

Fair value of marked-to-market transactions | | | 2,451,055 | | | | 875,487 | |

| | | | | | | | |

Total current liabilities | | | 21,294,542 | | | | 31,615,687 | |

| | | | | | | | |

LONG-TERM DEBT | | | 28,000,000 | | | | 23,000,000 | |

| | | | | | | | |

DEFERRED CREDITS AND OTHER LIABILITIES: | | | | | | | | |

Asset retirement obligations | | | 2,735,735 | | | | 2,608,995 | |

Regulatory cost of retirement obligations | | | 7,401,024 | | | | 6,843,338 | |

Benefit plan liabilities | | | 7,970,074 | | | | 4,768,785 | |

Deferred income taxes | | | 6,534,621 | | | | 5,471,667 | |

Deferred investment tax credits | | | 66,025 | | | | 96,184 | |

| | | | | | | | |

Total deferred credits and other liabilities | | | 24,707,479 | | | | 19,788,969 | |

| | | | | | | | |

COMMITMENTS AND CONTINGENCIES (Notes 10 and 11) | | | | | | | | |

CAPITALIZATION: | | | | | | | | |

Stockholders’ Equity: | | | | | | | | |

Common Stock, $5 par value; authorized 10,000,000 shares; issued and outstanding 2,238,987 and 2,209,471 shares in 2009 and 2008, respectively | | | 11,194,935 | | | | 11,047,355 | |

Preferred stock, no par; authorized 5,000,000 shares; no shares issued and outstanding in 2009 and 2008 | | | — | | | | — | |

Capital in excess of par value | | | 16,607,897 | | | | 15,990,961 | |

Retained earnings | | | 19,881,745 | | | | 17,909,134 | |

Accumulated other comprehensive loss | | | (2,884,706 | ) | | | (1,224,392 | ) |

| | | | | | | | |

Total stockholders’ equity | | | 44,799,871 | | | | 43,723,058 | |

| | | | | | | | |

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | | $ | 118,801,892 | | | $ | 118,127,714 | |

| | | | | | | | |

(Concluded)

See notes to consolidated financial statements.

- 3 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

YEARS ENDED SEPTEMBER 30, 2009 AND 2008

| | | | | | | | |

| | | 2009 | | | 2008 | |

OPERATING REVENUES: | | | | | | | | |

Gas utilities | | $ | 80,786,228 | | | $ | 93,606,593 | |

Other | | | 1,398,245 | | | | 1,030,233 | |

| | | | | | | | |

Total operating revenues | | | 82,184,473 | | | | 94,636,826 | |

| | | | | | | | |

COST OF SALES: | | | | | | | | |

Gas utilities | | | 54,408,778 | | | | 68,283,129 | |

Other | | | 699,771 | | | | 440,085 | |

| | | | | | | | |

Total cost of sales | | | 55,108,549 | | | | 68,723,214 | |

| | | | | | | | |

GROSS MARGIN | | | 27,075,924 | | | | 25,913,612 | |

| | | | | | | | |

OTHER OPERATING EXPENSES: | | | | | | | | |

Operations | | | 10,565,267 | | | | 10,107,242 | |

Maintenance | | | 1,765,511 | | | | 1,470,212 | |

General taxes | | | 1,240,209 | | | | 1,167,293 | |

Depreciation and amortization | | | 3,660,421 | | | | 4,330,839 | |

| | | | | | | | |

Total other operating expenses | | | 17,231,408 | | | | 17,075,586 | |

| | | | | | | | |

OPERATING INCOME | | | 9,844,516 | | | | 8,838,026 | |

OTHER INCOME (EXPENSE), Net | | | (70,091 | ) | | | 34,622 | |

INTEREST EXPENSE | | | 1,918,106 | | | | 2,033,082 | |

| | | | | | | | |

INCOME FROM CONTINUING OPERATIONS BEFORE INCOME TAXES | | | 7,856,319 | | | | 6,839,566 | |

INCOME TAX EXPENSE FROM CONTINUING OPERATIONS | | | 2,987,309 | | | | 2,581,742 | |

| | | | | | | | |

INCOME FROM CONTINUING OPERATIONS | | | 4,869,010 | | | | 4,257,824 | |

DISCONTINUED OPERATIONS: | | | | | | | | |

Loss from discontinued operations, net of income tax benefit of ($14,628) | | | — | | | | (36,690 | ) |

| | | | | | | | |

NET INCOME | | | 4,869,010 | | | | 4,221,134 | |

| | | | | | | | |

OTHER COMPREHENSIVE LOSS, NET OF TAX | | | (1,671,535 | ) | | | (749,137 | ) |

| | | | | | | | |

COMPREHENSIVE INCOME | | $ | 3,197,475 | | | $ | 3,471,997 | |

| | | | | | | | |

(Continued)

- 4 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

YEARS ENDED SEPTEMBER 30, 2009 AND 2008

| | | | | | | |

| | | 2009 | | 2008 | |

BASIC EARNINGS PER COMMON SHARE: | | | | | | | |

Income from continuing operations | | $ | 2.19 | | $ | 1.94 | |

Discontinued operations | | | — | | | (0.02 | ) |

| | | | | | | |

Net income | | $ | 2.19 | | $ | 1.92 | |

| | | | | | | |

DILUTED EARNINGS PER COMMON SHARE: | | | | | | | |

Income from continuing operations | | $ | 2.18 | | $ | 1.93 | |

Discontinued operations | | | — | | | (0.02 | ) |

| | | | | | | |

Net income | | $ | 2.18 | | $ | 1.91 | |

| | | | | | | |

WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING: | | | | | | | |

Basic | | | 2,223,727 | | | 2,201,263 | |

Diluted | | | 2,231,040 | | | 2,211,226 | |

(Concluded)

See notes to consolidated financial statements.

- 5 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

YEARS ENDED SEPTEMBER 30, 2009 AND 2008

| | | | | | | | | | | | | | | | | | |

| | | Common

Stock | | Capital in

Excess of

Par Value | | Retained

Earnings | | | Accumulated

Other

Comprehensive

Income (Loss) | | | Total

Stockholders’

Equity | |

Balance - September 30, 2007 | | $ | 10,930,715 | | $ | 15,466,756 | | $ | 16,443,017 | | | $ | (475,255 | ) | | $ | 42,365,233 | |

Net income | | | — | | | — | | | 4,221,134 | | | | — | | | | 4,221,134 | |

Losses on hedging activities, net of tax | | | — | | | — | | | — | | | | (466,300 | ) | | | (466,300 | ) |

Change in net loss and transition obligation of defined benefit plans, net of tax | | | — | | | — | | | — | | | | (282,837 | ) | | | (282,837 | ) |

Cash dividends declared ($1.25 per share) | | | — | | | — | | | (2,755,017 | ) | | | — | | | | (2,755,017 | ) |

Issuance of common stock (23,328 shares) | | | 116,640 | | | 524,205 | | | — | | | | — | | | | 640,845 | |

| | | | | | | | | | | | | | | | | | |

Balance - September 30, 2008 | | $ | 11,047,355 | | $ | 15,990,961 | | $ | 17,909,134 | | | $ | (1,224,392 | ) | | $ | 43,723,058 | |

| | | | | | | | | | | | | | | | | | |

Change in measurement date - benefit plans, net of tax | | | — | | | — | | | (44,931 | ) | | | 11,221 | | | | (33,710 | ) |

Net income | | | — | | | — | | | 4,869,010 | | | | — | | | | 4,869,010 | |

Losses on hedging activities, net of tax | | | — | | | — | | | — | | | | (1,000,965 | ) | | | (1,000,965 | ) |

Change in net loss and transition obligation of defined benefit plans, net of tax | | | — | | | — | | | — | | | | (670,570 | ) | | | (670,570 | ) |

Tax benefits from stock option exercise | | | — | | | 16,407 | | | — | | | | — | | | | 16,407 | |

Cash dividends declared ($1.28 per share) | | | — | | | — | | | (2,851,468 | ) | | | — | | | | (2,851,468 | ) |

Issuance of common stock (29,516 shares) | | | 147,580 | | | 600,529 | | | — | | | | — | | | | 748,109 | |

| | | | | | | | | | | | | | | | | | |

Balance - September 30, 2009 | | $ | 11,194,935 | | $ | 16,607,897 | | $ | 19,881,745 | | | $ | (2,884,706 | ) | | $ | 44,799,871 | |

| | | | | | | | | | | | | | | | | | |

See notes to consolidated financial statements.

- 6 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED SEPTEMBER 30, 2009 AND 2008

| | | | | | | | |

| | | 2009 | | | 2008 | |

CASH FLOWS FROM OPERATING ACTIVITIES: | | | | | | | | |

Net income from continuing operations | | $ | 4,869,010 | | | $ | 4,257,824 | |

| | | | | | | | |

Adjustments to reconcile net income to net cash provided by operations: | | | | | | | | |

Depreciation and amortization | | | 3,815,009 | | | | 4,526,670 | |

Cost of removal of utility plant, net | | | (263,446 | ) | | | (202,843 | ) |

Loss on disposal of property | | | — | | | | 7,304 | |

Change in over/under-recovery of gas costs | | | 6,627,084 | | | | (1,542,532 | ) |

Deferred taxes and investment tax credits | | | 812,532 | | | | (730,442 | ) |

Other noncash items, net | | | 39,111 | | | | 28,329 | |

Changes in assets and liabilities which provided (used) cash: | | | | | | | | |

Accounts receivable and customer deposits, net | | | 1,602,679 | | | | (556,147 | ) |

Inventories and gas in storage | | | 10,015,564 | | | | (7,003,735 | ) |

Other current assets | | | (781,945 | ) | | | 310,119 | |

Accounts payable, customer credit balances and accrued expenses, net | | | (4,029,786 | ) | | | 1,403,231 | |

| | | | | | | | |

Total adjustments | | | 17,836,802 | | | | (3,760,046 | ) |

| | | | | | | | |

Net cash provided by continuing operating activities | | | 22,705,812 | | | | 497,778 | |

Net cash used in discontinued operations | | | — | | | | (277,913 | ) |

| | | | | | | | |

Net cash provided by operating activities | | | 22,705,812 | | | | 219,865 | |

| | | | | | | | |

CASH FLOWS FROM INVESTING ACTIVITIES: | | | | | | | | |

Expenditures for utility property | | | (5,752,780 | ) | | | (6,539,369 | ) |

Proceeds from disposal of utility property | | | 27,826 | | | | 17,540 | |

Proceeds from sale of Bluefield Operations | | | — | | | | 3,855,323 | |

Proceeds from sale of short-term investments | | | 500,000 | | | | — | |

Purchase of short-term investments | | | — | | | | (500,000 | ) |

| | | | | | | | |

Net cash used in continuing investing activities | | | (5,224,954 | ) | | | (3,166,506 | ) |

Net cash used in discontinued investing activities | | | — | | | | (12,360 | ) |

| | | | | | | | |

Net cash used in investing activities | | | (5,224,954 | ) | | | (3,178,866 | ) |

| | | | | | | | |

(Continued)

- 7 -

RGC RESOURCES, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED SEPTEMBER 30, 2009 AND 2008

| | | | | | | | |

| | | 2009 | | | 2008 | |

CASH FLOWS FROM FINANCING ACTIVITIES: | | | | | | | | |