RGC RESOURCES IS SITTING FRONT AND CENTER, ENJOYING THE VIEW AS THE WORLD TURNS MORE AND MORE TO NATURAL GAS AS A PREFERRED FUEL. WE’RE SECURE IN OUR POSITION, POISED TO TAKE FULL ADVANTAGE OF THE INDUSTRY’S METAMORPHOSIS AS WE SERVE OUR LOCAL COMMUNITY’S NEEDS, STAKE OUR CLAIM AS A REGIONAL LEADER IN THE INCREASED USE OF NATURAL GAS, AND CELEBRATE THE RISING GLOBAL PERSPECTIVE OF NATURAL GAS AS THE MOST ECONOMICAL, ECOLOGICAL AND INCREASINGLY PLENTIFUL FUEL OF THE PRESENT AND FUTURE.

RGC CONTINUES TO GROW STRONG AND STEADY. OUR INVESTORS CONSISTENTLY SEE IMPRESSIVE DIVIDENDS AS STOCK PRICES RISE, FOLLOWING AN INDUSTRY TREND. HISTORICALLY LOW PRICES OF NATURAL GAS, COMBINED WITH A MULTITUDE OF ALTERNATIVE USES, ARE BOLSTERING THE DRAMATICALLY EMERGING POPULARITY OF THE CLEANER FUEL.

THE FUTURE FOR OUR INDUSTRY IS AS BRIGHT AND DYNAMIC AS THE BUTTERFLIES IN THEIR SPECTACULAR NEW HABITAT AT THE REVITALIZED CENTER IN THE SQUARE, A GREEN FACILITY IN DOWNTOWN ROANOKE ON TRACK TO BE LEED-CERTIFIED. IT’S REFLECTIVE OF A NEW DAY IN ROANOKE, STANDING AS OUR CITY’S OWN MICROCOSM OF POSITIVE CHANGE HAPPENING WORLDWIDE.

FROM GENERATING ELECTRICITY ON A GLOBAL SCALE TO HEATING HOMES AROUND ROANOKE, NATURAL GAS HAS GROWN INTO A MAJOR PLAYER, AND IT’S HERE TO STAY. AT RGC, NATURAL GAS IS ENSURING OUR FUTURE.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 1 |

THE WORLD LOOKS TO NATURAL GAS

GLOBAL DEMAND FOR NATURAL GAS IS ON THE RISE, AND THE UNITED STATES IS READY TO ANSWER THE CALL WITH SUPPLIES MADE SUDDENLY ABUNDANT THROUGH UNCONVENTIONAL RESOURCES. FORTUNATELY FOR RGC, ONE OF THE MOST IMPRESSIVE SITES FOR SHALE GAS PRODUCTION IS THE APPALACHIAN BASIN’S HUGE MARCELLUS SHALE FORMATION. THE MARCELLUS IS ONE OF THE LARGEST NATURAL GAS FIELDS IN THE WORLD, ENRICHING US WITH VAST, INEXPENSIVE SUPPLIES CLOSE TO HOME. IN A DRAMATIC TURNAROUND, DEVELOPMENT OF THESE UNCONVENTIONAL RESOURCES IS EXPECTED TO MAKE THE UNITED STATES A NET EXPORTER IN YEARS TO COME. AND THE WORLD IS READY FOR IT — NATURAL GAS’ APPLICATIONS ARE MANY, FROM HEATING AND COOLING HOMES TO CHEMICAL PRODUCTION ESSENTIAL IN THE MANUFACTURE OF EVERYDAY ITEMS INCLUDING CLOTHING, CARPET, ELECTRONICS, FURNITURE AND FERTILIZER. LOW PRICES AND SUPPLY SURPLUSES ARE BRINGING INVESTMENT INTO THE UNITED STATES AS WELL, AS FOREIGN COMPANIES EXPAND THEIR PLANTS AND INDUSTRIAL PROJECTS.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 3 |

AS THE NATION SHIFTS, SO DOES THE SOUTHEAST

U.S. COMPANIES ARE BUILDING AND ADAPTING TO TAKE ADVANTAGE OF NATURAL GAS — ESPECIALLY IN THE SOUTHEAST, WHERE GAS IS BECOMING MORE USEFUL FOR POWER GENERATION. MANUFACTURERS ARE INCREASINGLY EXPANDING THEIR GAS USE IN PRODUCTION. AT STEEL DYNAMICS, RGC’S LARGEST INDUSTRIAL CUSTOMER, NATURAL GAS IS USED TO EXPEDITE THE MELTING PROCESS, REDUCING MELT TIMES AND IMPROVING OVERALL EFFICIENCY. IMPROVED EFFICIENCIES TRANSLATE TO REDUCED COSTS AND A STRONGER COMPETITIVE POSITION IN THE GLOBAL MARKETPLACE. ON THE ECONOMY FRONT, THE BOOM IN NATURAL GAS PRODUCTION HAS LED TO ECONOMIC GROWTH AND JOB CREATION. AND WHAT’S GOOD FOR THIS REGION AND THIS NATION IS GOOD FOR THE PLANET: BURNING NATURAL GAS PRODUCES ABOUT HALF THE CARBON EMISSIONS AS DOES BURNING COAL. AMONG OTHER APPLICATIONS, NATURAL GAS IS BEING USED AS AN ENVIRONMENTALLY FRIENDLY ALTERNATIVE TO POWER VEHICLES AS PRIVATE COMPANIES AND SOME LOCAL GOVERNMENTS CONVERT VEHICLES TO NATURAL GAS.

| | |

| 4 | | RGC RESOURCES | ANNUAL REPORT 2013 |

We continue to aggressively modernize our distribution system through the

replacement of cast iron and bare steel pipeline with plastic or coated steel pipe.

We invested more than $10 million in capital improvements in 2013.

a period of high prices and long-term natural gas supply concerns to what now appears to be a future of supply abundance and relative price stability. Natural gas in America is truly helping to ensure our future. With appropriate and reasonable regulatory policy, natural gas should improve the competitiveness of the nation’s manufacturing sector and enhance economic opportunity.

We continue to aggressively modernize our distribution system through the replacement of cast iron and bare steel pipeline with plastic or coated steel pipe. We invested more than $10 million in capital improvements in 2013. After 20 years of a steady replacement program, we approximately doubled our prior annual replacement efforts starting in 2012. We plan to invest approximately $13 million in capital improvements in 2014 and anticipate replacing all remaining cast iron and bare steel pipe by 2017. We also will upgrade some

crucial equipment at our liquefied natural gas facility, which is used to ensure adequate gas supply on extremely cold days.

The new-home construction market remains weak compared with pre-2008 levels. However, we are experiencing modest customer growth, including conversion to natural gas of homes previously heated with fuel oil or electricity. Industrial deliveries remained steady in 2013. While always difficult to predict, we anticipate similar activity in 2014, assuming the U.S. economy does not dip back into recession.

We continue to be active in regulatory filings with the Virginia State Corporation Commission to ensure timely cost recovery. We filed a rate case in September 2013 to recover the added cost of 2013 investment in capital improvements, along with increased depreciation and operating expense. We filed for an amendment to a separate regulatory plan designed to recover

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 5 |

We announced a management succession plan in 2013. John D’Orazio was

appointed President and CEO of Roanoke Gas Company, our largest and primary

subsidiary, while John Williamson continued as Chairman, President and CEO

of RGC Resources, Inc., on a part-time basis.

the increased cost and depreciation expense associated with future planned pipeline replacement through 2018, modernization of our liquefied natural gas facility in 2014, and replacement of one of our gas transfer stations on the interstate pipeline system.

We announced a management succession plan in 2013. John D’Orazio was appointed President and CEO of Roanoke Gas Company, our largest and primary subsidiary, while John Williamson continued as Chairman, President and CEO of RGC Resources, Inc., on a part-time basis. The Board of Directors’ approved succession plan is progressing nicely and Mr. Williamson is expected to step down as President and CEO of RGC Resources following the shareholder meeting in February 2014. Under the provisions of the succession plan, Mr. D’Orazio will become President and CEO of RGC Resources at that time. Mr. Williamson is expected to

remain as Chairman and to be available in an advisory capacity when needed.

On behalf of our employees and the Board of Directors, we thank you for your interest in our operations and your continuing decision to own RGC Resources stock. We are pleased to be part of an exciting new era for natural gas in America, and continue to believe it is in the long-term interest of our shareholders to invest in the natural gas distribution business and the Roanoke, Va., region.

| | |

| Sincerely, | | |

| | |

| John B. Williamson, III | | |

| Chairman, President & CEO - RGC Resources, Inc. | | |

| |  |

| | |

| John S. D’Orazio | | |

| President & CEO -Roanoke Gas Company | | |

| | |

| 6 | | RGC RESOURCES | ANNUAL REPORT 2013 |

HERE AT HOME, GREEN INITIATIVES TAKE FLIGHT

GREEN CONSTRUCTION HAS EMERGED AS A THING OF BEAUTY IN DOWNTOWN ROANOKE. FOR ITS ENERGY EFFICIENCY AND FORWARD FOCUS, WE AT RGC SALUTE THE NEWLY REVITALIZED CENTER IN THE SQUARE. IT’S A PHENOMENAL SPACE CONCEIVED AS A “LIVING” FACILITY WHERE BUTTERFLIES CAPTURE THE SPIRIT OF SUSTAINABLE LIVING AS PART OF THE SCIENCE MUSEUM OF WESTERN VIRGINIA. BUTTERFLIES RULE INSIDE THE FACILITY, FROM THE CREATURES FLUTTERING FREELY ON THE FIFTH FLOOR TO THE 66-FOOT BUTTERFLY DESIGN INLAID INTO THE LOBBY FLOOR BELOW. CENTER IN THE SQUARE’S REDESIGN IS ONE OF INTERCONNECTIVITY, FILLED WITH MUSEUMS AND EDUCATIONAL EXHIBITS. A LIVING CORAL REEF AQUARIUM IS FULL OF TROPICAL FISH, AND OTHER AQUARIUMS ARE HOME TO JELLYFISH, SEAHORSES, FRESHWATER FISH AND TURTLES. ON THE ROOFTOP, A KOI AND GOLDFISH POND COMPLEMENTS ATTRACTIVE VEGETATION IRRIGATED BY RAINWATER. THE ROOFTOP PAVILION ALSO FEATURES A GLASS DOME ALLOWING VISITORS TO LOOK DOWN INTO THE BUTTERFLY HABITAT. CENTER IN THE SQUARE IS DESIGNED AS A CUTTING-EDGE, ENERGY-EFFICIENT FACILITY ABLE TO GROW WITH TECHNOLOGICAL ADVANCES IN THE FUTURE.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 7 |

SELECTED FINANCIAL DATA

| | | | | | | | | | | | | | | | | | | | |

Years Ended September 30, | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

OPERATING REVENUES | | $ | 63,205,666 | | | $ | 58,799,687 | | | $ | 70,798,871 | | | $ | 73,823,914 | | | $ | 82,184,473 | |

GROSS MARGIN | | | 27,602,891 | | | | 26,933,097 | | | | 27,269,566 | | | | 26,440,273 | | | | 27,075,924 | |

OPERATING INCOME | | | 8,795,055 | | | | 8,786,535 | | | | 9,313,046 | | | | 8,982,181 | | | | 9,844,516 | |

NET INCOME | | | 4,262,052 | | | | 4,296,745 | | | | 4,653,473 | | | | 4,445,436 | | | | 4,869,010 | |

BASIC EARNINGS PER SHARE | | $ | 0.91 | | | $ | 0.92 | | | $ | 1.01 | | | $ | 0.98 | | | $ | 1.09 | |

CASH DIVIDENDS DECLARED PER SHARE | | | 1.72 | | | | 0.70 | | | | 0.68 | | | | 0.66 | | | | 0.64 | |

BOOK VALUE PER SHARE | | | 10.51 | | | | 10.85 | | | | 10.55 | | | | 10.18 | | | | 10.00 | |

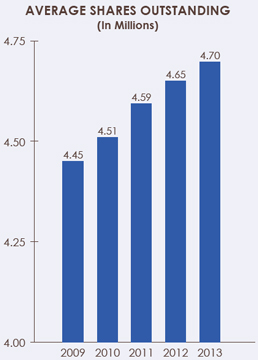

AVERAGE SHARES OUTSTANDING | | | 4,698,727 | | | | 4,647,439 | | | | 4,592,713 | | | | 4,514,262 | | | | 4,447,454 | |

TOTAL ASSETS | | $ | 124,526,701 | | | $ | 129,756,338 | | | $ | 125,549,049 | | | $ | 120,683,316 | | | $ | 118,801,892 | |

LONG-TERM DEBT (Less Current Portion) | | | 13,000,000 | | | | 13,000,000 | | | | 13,000,000 | | | | 28,000,000 | | | | 28,000,000 | |

STOCKHOLDERS’ EQUITY | | | 49,502,422 | | | | 50,682,930 | | | | 48,785,778 | | | | 46,309,747 | | | | 44,799,871 | |

SHARES OUTSTANDING AT SEPT. 30 | | | 4,709,326 | | | | 4,670,567 | | | | 4,624,682 | | | | 4,548,864 | | | | 4,477,974 | |

| | |

| 10 | | RGC RESOURCES | ANNUAL REPORT 2013 |

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that relate to future transactions, events or expectations. In addition, RGC Resources, Inc. (“Resources” or the “Company”) may publish forward-looking statements relating to such matters as anticipated financial performance, business prospects, technological developments, new products, research and development activities and similar matters. These statements are based on management’s current expectations and information available at the time of such statements and are believed to be reasonable and are made in good faith. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. In order to comply with the terms of the safe harbor, the Company notes that a variety of factors could cause the Company’s actual results and experience to differ materially from the anticipated results or expectations expressed in the Company’s forward-looking statements. The risks and uncertainties that may affect the operations, performance, development and results of the Company’s business include, but are not limited to those set forth in the

following discussion and within Item 1A “Risk Factors” of this Annual Report on Form 10-K. All of these factors are difficult to predict and many are beyond the Company’s control. Accordingly, while the Company believes its forward-looking statements to be reasonable, there can be no assurance that they will approximate actual experience or that the expectations derived from them will be realized. When used in the Company’s documents or news releases, the words “anticipate,” “believe,” “intend,” “plan,” “estimate,” “expect,” “objective,” “projection,” “forecast,” “budget,” “assume,” “indicate” or similar words or future or conditional verbs such as “will,” “would,” “should,” “can,” “could” or “may” are intended to identify forward-looking statements.

Forward-looking statements reflect the Company’s current expectations only as of the date they are made. The Company assumes no duty to update these statements should expectations change or actual results differ from current expectations except as required by applicable laws and regulations.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 11 |

MANAGEMENT’S DISCUSSION & ANALYSIS

OVERVIEW

Resources is an energy services company primarily engaged in the regulated sale and distribution of natural gas to approximately 58,200 residential, commercial and industrial customers in Roanoke, Virginia and the surrounding localities through its Roanoke Gas Company (“Roanoke Gas”) subsidiary. Resources also provides certain unregulated services through Roanoke Gas and utility consulting and information system services through RGC Ventures of Virginia, Inc., which operates as The Utility Consultants and Application Resources. The unregulated operations represent less than 3% of revenues and margins of Resources.

The utility operations of Roanoke Gas are regulated by the Virginia State Corporation Commission (“SCC”) which oversees the terms, conditions, and rates to be charged to customers for natural gas service, safety standards, extension of service, accounting and depreciation. The Company is also subject to federal regulation from the Department of Transportation in regard to the construction, operation, maintenance, safety and integrity of its transmission and distribution pipelines. The Federal Energy Regulatory Commission regulates the prices for the transportation and delivery of natural gas to the Company’s distribution system and underground storage services. The Company is also subject to other regulations which are not necessarily industry specific.

The Company is committed to the safe and reliable delivery of natural gas to its customers. Since 1991, the Company has placed an emphasis on the modernization of its distribution system through the renewal and replacement of its cast iron and bare steel natural gas distribution pipelines. With recent regulatory actions placing a greater focus on pipeline safety, the Company continues to focus its efforts on completing its renewal and replacement program. Management anticipates replacing all remaining cast iron and bare steel pipe within the next four years.

The Company is also dedicated to the safeguarding of its information technology systems. These systems contain confidential customer, vendor and employee information as well as important financial data. There is risk associated with the unauthorized access of this information with a malicious intent to corrupt data, cause operational disruptions, or compromise information. Management believes it has taken reasonable security measures to protect these systems from cyber security attacks and other types of breaches; however, there can be no guarantee that a breach will not occur. In the event of a breach, the Company is prepared to execute its Security Incident Response Plan to reduce the impact of the incident. The Company also maintains cyber-insurance coverage to mitigate financial implications resulting from a potential breach of confidential information.

| | |

| 12 | | RGC RESOURCES | ANNUAL REPORT 2013 |

The SCC authorizes the rates and fees that the Company charges its customers for regulated natural gas service. These rates are designed to provide the Company with the opportunity to recover its gas and non-gas expenses and to earn a reasonable rate of return for shareholders. The Company’s business is seasonal in nature and weather dependent as a majority of natural gas sales are for space heating during the winter season. Volatility in winter weather and the commodity price of natural gas can impact the effectiveness of the Company’s rates in recovering its costs and providing a reasonable rate of return for its shareholders. Over the past several years, the Company has implemented certain approved rate mechanisms that reduce some of the volatility in earnings associated with variations in winter weather and the cost of natural gas, including the weather normalization adjustment mechanism and inventory carrying cost revenue.

The weather normalization adjustment mechanism (“WNA”) is based on a weather measurement band around the most recent 30- year temperature average. Because the SCC authorizes billing rates for the utility operations

of Roanoke Gas based on normal weather, warmer than normal weather may result in the Company failing to earn its authorized rate of return. Therefore, the WNA provides the Company with a level of earnings protection when weather is significantly warmer than normal and provides its customers with price protection when the weather is significantly colder than normal. The WNA mechanism provides for a weather band of 3% above and below the 30-year average, whereby the Company would bill its customers for the lost margin (excluding gas costs) for the impact of weather that was more than 3% warmer than normal or refund customers the excess margin earned for weather that was more than 3% colder than normal. The annual WNA period extends from April to March. For the most recently completed WNA period ending in March 2013, total heating degree days fell within the 3% weather band and thereby did not trigger the WNA mechanism for the current WNA period. Weather during the corresponding WNA period in fiscal 2012 was approximately 22% warmer than the 30-year normal with 883 fewer heating degree days (an industry measure by which the average daily temperature falls below 65 degrees

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 13 |

Fahrenheit) compared to normal. As a result, the Company recorded approximately $1,747,000 in additional revenues to reflect the impact of the WNA in fiscal 2012 for the difference in margin not realized for warmer weather between 3% and 22% of the 30-year average. The Company did not record any WNA revenues during the WNA period in fiscal 2011 as total heating degree days were within the 3% weather band.

The Company also has an approved rate structure in place that mitigates the impact of financing costs of its natural gas inventory. Under this rate structure, Roanoke Gas recognizes revenue for the financing costs, or “carrying costs”, of its investment in natural gas inventory. The carrying cost revenue factor applied to inventory is based on the Company’s weighted-average cost of capital including interest rates on short-term and long-term debt and the Company’s authorized return on equity. During times of rising gas costs and rising inventory levels, the Company recognizes revenues to offset higher financing costs associated with higher inventory balances. Conversely, during times of decreasing gas costs and declining inventory balances, the Company recognizes less carrying cost revenue as financing costs are lower. Although the price of natural gas in storage at September 30, 2013 was higher than the price in storage at September 30, 2012, the average price of gas in storage during fiscal 2013 was $0.61 a decatherm or 14% lower than last year’s levels. Correspondingly, carrying cost revenues declined by $299,000 in fiscal 2013. After five years of decline, natural gas commodity prices appeared to have bottomed out in 2012 and have rebounded to a small degree. The cost of gas delivered into storage during the 2013 summer fill months was higher compared to the prior year,

resulting in the higher gas in storage balances at September 30, 2013. As a result, carrying cost revenues are expected to increase modestly during the next fiscal year.

Generally, as investment in natural gas inventory increases so does the level of borrowing under the Company’s line-of-credit. However, as the carrying cost factor used in determining carrying cost revenues is based on the Company’s weighted-average cost of capital, carrying cost revenues do not directly correspond with incremental short-term financing costs. Therefore, when inventory balances decline due to a reduction in commodity prices, net income will decline as carrying cost revenues decrease by a greater amount than short-term financing costs decrease. The inverse occurs when inventory costs increase.

The economic environment has a direct correlation with business and industrial production, customer growth and natural gas utilization. The local economy continues to show signs of modest improvement from the economic downturn that began in 2008, and industrial production activities and the related interruptible and transportation sales to support those activities have returned to pre-2008 levels. Although there are signs of improvement, residential construction and housing starts continue to remain below historical levels, thereby limiting new customer growth opportunities. If economic uncertainty continues, industrial activity and new customer growth could be negatively impacted. In addition to economic considerations, natural gas consumption continues to be impacted by technological improvements to heating equipment which improve efficiency and reduce energy usage.

| | |

| 14 | | RGC RESOURCES | ANNUAL REPORT 2013 |

RESULTSOF OPERATIONS

Fiscal Year 2013 Compared with Fiscal Year 2012

The table below reflects operating revenues, volume activity and heating degree-days.

Operating Revenues

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2013 | | | 2012 | | | Increase | | | Percentage | |

Gas Utilities | | $ | 62,024,174 | | | $ | 57,657,940 | | | $ | 4,366,234 | | | | 8 | % |

Other | | | 1,181,492 | | | | 1,141,747 | | | | 39,745 | | | | 3 | % |

| | | | | | | | | | | | | | | | |

Total Operating Revenues | | $ | 63,205,666 | | | $ | 58,799,687 | | | $ | 4,405,979 | | | | 7 | % |

| | | | | | | | | | | | | | | | |

Delivered Volumes

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2013 | | | 2012 | | | Increase/

(Decrease) | | | Percentage | |

Regulated Natural Gas (DTH) | | | | | | | | | | | | | | | | |

Residential and Commercial | | | 6,498,783 | | | | 5,335,836 | | | | 1,162,947 | | | | 22 | % |

Transportation and Interruptible | | | 2,910,111 | | | | 2,981,660 | | | | (71,549 | ) | | | -2 | % |

| | | | | | | | | | | | | | | | |

Total Delivered Volumes | | | 9,408,894 | | | | 8,317,496 | | | | 1,091,398 | | | | 13 | % |

| | | | | | | | | | | | | | | | |

Heating Degree Days (Unofficial) | | | 4,001 | | | | 3,189 | | | | 812 | | | | 25 | % |

Total gas utility operating revenues for the year ended September 30, 2013 increased by 7% from the year ended September 30, 2012. The increase in gas revenues is primarily attributable to a 22% increase in residential and commercial delivery volumes, partially offset by lower natural gas commodity prices during the winter heating season. The increase in delivered volumes was driven by the much colder winter heating season than the prior year, evidenced by the 25% increase

in heating degree days. The total heating degree days for 2013 approximated the 30-year average. Transportation and interruptible volumes, which are primarily driven by production activities rather than weather, declined by 2%. Other revenues increased by 3% due to the completion of a one-time project more than offsetting declines in the level of certain other contract services from last year.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 15 |

The table below reflects gross margin.

Gross Margin

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2013 | | | 2012 | | | Increase/

(Decrease) | | | Percentage | |

Gas Utility | | $ | 27,108,112 | | | $ | 26,379,767 | | | $ | 728,345 | | | | 3 | % |

Other | | | 494,779 | | | | 553,330 | | | | (58,551 | ) | | | -11 | % |

| | | | | | | | | | | | | | | | |

Total Gross Margin | | $ | 27,602,891 | | | $ | 26,933,097 | | | $ | 669,794 | | | | 2 | % |

| | | | | | | | | | | | | | | | |

Regulated natural gas margins from utility operations increased by 3% from the same period last year primarily as a result of significantly higher residential and commercial sales volumes, the implementation of a non-gas rate increase and the addition of the SAVE Plan rider. Residential and commercial volumes (which are strongly correlated to the weather) increased due to the much colder winter season. The higher margins generated by the increased residential and commercial volume was mostly offset by the $1,747,000 in WNA revenues recorded last year. The Company also implemented a non-gas rate increase effective November 1, 2012 and a SAVE Plan Rider beginning January 1, 2013. The non-gas rate increase was designed to provide approximately $650,000 in additional non-gas revenues annually. The implementation of the new rates in November accounted for approximately $254,000 of the $280,000 increase in customer base charges, a flat monthly fee billed to each natural gas customer, and $328,000 of the $2,344,000 additional volumetric revenue. The SAVE Plan Rider, as discussed in more detail under Regulatory Affairs below, provided an additional $169,000 in margin. Carrying cost revenues continued to decline with a $299,000 reduction due to lower average price of gas in storage during the current fiscal year as discussed above.

Other margins, consisting of non-utility related services, decreased by $58,551 due to a reduction in the services requested. Some of these non-utility services are subject to annual or semi-annual contract renewals and the level of activity under these contracts will fluctuate. If the Company is unable to continue renewing or extending the largest contracts, or if activity under these contracts continues to decline, margins from other revenues would be negatively impacted. The Company intends to continue to pursue these contracts where profitable; however, future continuation of some of these contracted services is uncertain.

The changes in the components of the gas utility margin are summarized below:

Net Utility Margin Increase

| | | | |

Customer Base Charge | | $ | 279,872 | |

Volumetric | | | 2,343,618 | |

SAVE Plan | | | 168,747 | |

WNA | | | (1,747,150 | ) |

Carrying Cost | | | (299,029 | ) |

Other | | | (17,713 | ) |

| | | | |

Total | | $ | 728,345 | |

| | | | |

| | |

| 16 | | RGC RESOURCES | ANNUAL REPORT 2013 |

Operations and Maintenance Expense –Operations and maintenance expenses increased by $305,906, or 2%, in fiscal 2013 compared with fiscal 2012 primarily due to higher labor costs, contracted services, bad debt expense, corporate insurance expense and stock option expense more than offsetting greater capitalization of Company overheads on construction projects and LNG (liquefied natural gas) production. Labor costs and contracted services increased by $453,000 primarily due to an increase in operations staffing, timing of leak surveys and pipeline right-of-way clearing, costs related to an SCC mandated meter installation inspection and remediation program, and network services support and training. Bad debt expense increased by approximately $74,000. Total bad debt expense was 0.13% of gross natural gas billings for the year and is consistent with the five-year average. Last year’s bad debt expense ratio was only 0.02%. This unusually low rate was due to much warmer weather and low gas prices, resulting in the lowest bad debt write-off in over twenty-five years. Corporate property and liability insurance increased by $126,000 due to a combination of higher premiums and increased general liability coverage limits. A similar increase in premiums is expected in fiscal 2014. The Company also recognized $85,000 in expense related to the granting of stock options. These were the first option grants since 2002. These higher costs were partially offset by greater capitalization of overheads due to a higher level of pipeline construction expenditures and increased LNG production. The Company continued to increase activity under its pipeline renewal program, with

total capital expenditures rising by more than $1.3 million over last year, resulting in a greater capitalization of overheads.

General Taxes –General taxes increased $114,066, or 8%, primarily due to higher property taxes associated with increases in utility property.

Depreciation – Depreciation expense increased by $241,302, or 6%, corresponding to the increase in utility plant investment.

Other Income (Expense) –Other expense, net, increased by $40,161 primarily due to the reduction in interest income related to the payoff of the ANGD note.

Interest Expense –Total interest expense remained virtually unchanged from last year as the Company only briefly accessed its line-of-credit during fiscal 2013.

Income Taxes –Income tax expense was nearly unchanged on slightly less pre-tax earnings. The effective tax rate for fiscal 2013 was 38.3% compared to 38.0% for 2012.

Net Income and Dividends –Net income for fiscal 2013 was $4,262,052 compared to $4,296,745 for fiscal 2012. Basic and diluted earnings per share were $0.91 in fiscal 2013 compared to $0.92 in fiscal 2012. Dividends declared per share of common stock were $1.72, which includes the one-time special dividend of $1.00 paid in December, in fiscal 2013 and $0.70 in fiscal 2012.

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 17 |

Fiscal Year 2012 Compared with Fiscal Year 2011

The table below reflects operating revenues, volume activity and heating degree-days.

Operating Revenues

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2012 | | | 2011 | | | (Decrease) | | | Percentage | |

Gas Utilities | | $ | 57,657,940 | | | $ | 69,483,620 | | | $ | (11,825,680 | ) | | | -17 | % |

Other | | | 1,141,747 | | | | 1,315,251 | | | | (173,504 | ) | | | -13 | % |

| | | | | | | | | | | | | | | | |

Total Operating Revenues | | $ | 58,799,687 | | | $ | 70,798,871 | | | $ | (11,999,184 | ) | | | -17 | % |

| | | | | | | | | | | | | | | | |

Delivered Volumes

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2012 | | | 2011 | | | Increase/

(Decrease) | | | Percentage | |

Regulated Natural Gas (DTH) | | | | | | | | | | | | | | | | |

Residential and Commercial | | | 5,335,836 | | | | 6,582,487 | | | | (1,246,651 | ) | | | -19 | % |

Transportation and Interruptible | | | 2,981,660 | | | | 2,962,111 | | | | 19,549 | | | | 1 | % |

| | | | | | | | | | | | | | | | |

Total Delivered Volumes | | | 8,317,496 | | | | 9,544,598 | | | | (1,227,102 | ) | | | -13 | % |

| | | | | | | | | | | | | | | | |

Heating Degree Days (Unofficial) | | | 3,189 | | | | 4,091 | | | | (902 | ) | | | -22 | % |

Total gas utility operating revenues for the year ended fiscal 2012 decreased by 17% from fiscal 2011 as total delivered volumes decreased by 13%. The decrease in gas revenues was due to significantly reduced natural gas sales attributed to a much warmer winter heating season combined with a continued downward trend in gas costs. Residential and commercial volumes declined by 19% compared to fiscal 2011 as total heating degree days during the period fell by 22%. A majority of residential and commercial sales volumes are dependent on weather and the significantly warmer winter resulted in a decrease in usage.

Transportation and interruptible volumes were nearly unchanged with a small increase of 1% with volumes returning to the pre-2008 levels. Natural gas commodity prices were approximately $3 a decatherm as of the end of September 2012 and were below $3 a decatherm for much of calendar 2012. For fiscal 2012, the average commodity price per unit cost of natural gas reflected in cost of sales decreased by 22% compared to the prior year while the average total price per unit (including pipeline demand fees) decreased by 11%. Other revenues declined by 13% due to the decline in the level of certain contract services.

| | |

| 18 | | RGC RESOURCES | ANNUAL REPORT 2013 |

The table below reflects gross margin.

Gross Margin

| | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2012 | | | 2011 | | | (Decrease) | | | Percentage | |

Gas Utility | | $ | 26,379,767 | | | $ | 26,667,821 | | | $ | (288,054 | ) | | | -1 | % |

Other | | | 553,330 | | | | 601,745 | | | | (48,415 | ) | | | -8 | % |

| | | | | | | | | | | | | | | | |

Total Gross Margin | | $ | 26,933,097 | | | $ | 27,269,566 | | | $ | (336,469 | ) | | | -1 | % |

| | | | | | | | | | | | | | | | |

Regulated natural gas margins from utility operations decreased 1% from the same period last year primarily as a result of significantly less total natural gas deliveries. Much of the margin lost due to the reduction in volumes delivered was recovered through the triggering of the WNA mechanism during the period. The Company recorded approximately $1,747,000 in additional revenues during the period to mitigate the shortfall in volumetric sales activity attributable to the warmer winter season. The Company also implemented a non-gas base rate increase designed to provide approximately $235,000 in additional annual revenues based on normal weather. The rate increase in non-gas billing rates accounted for approximately $200,000 in higher margins with approximately $90,000 attributable to customer base charges, a flat monthly fee billed to each natural gas customer, with the remaining balance related to volumetric sales. The remaining increase in customer base charges was primarily attributable to a higher number of billed meter accounts related to the conversion of six apartment complexes from a single master meter for each building to individual meters for each apartment that occurred during fiscal 2011. Carrying cost revenues declined $159,000 due to the lower average price of gas in storage combined with lower inventory balances.

Other margins, consisting of non-utility related services, decreased by $48,415 due to a reduction in the level of certain contract services.

The changes in the components of the gas utility margin are summarized below:

Net Utility Margin Decrease

| | | | |

Customer Base Charge | | $ | 178,106 | |

Volumetric | | | (2,014,190 | ) |

WNA | | | 1,747,150 | |

Carrying Cost | | | (159,164 | ) |

Other | | | (39,956 | ) |

| | | | |

Total | | $ | (288,054 | ) |

| | | | |

Operations and Maintenance Expense –Operations and maintenance expenses decreased by $114,288, or 1%, in fiscal 2012 compared with fiscal 2011 primarily due to greater capitalization of Company labor and overheads on related construction projects and lower bad debt expense more than offsetting higher employee benefit costs. The Company increased activity under its pipeline renewal program resulting in total capital expenditures rising by more than $1 million, or 14%, over the prior year. As a result of higher

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 19 |

capital spending and increased employee costs, the Company capitalized approximately $385,000 more in related overheads. Employee benefit costs increased by approximately $294,000, which also contributed to the increase in capitalized overheads. The major components of the higher employee benefit costs related to increases in health insurance premiums and higher pension and post-retirement medical plan costs attributable to a decline in the discount rate used to measure the benefit liabilities and the underperformance of the plan assets in the prior year. Both components were used in determining fiscal 2012 expense. The Company also realized a $55,000 reduction in bad debt expense. The lower bad debt expense was primarily attributable to significantly reduced natural gas deliveries and lower natural gas prices contributing to lower customer billings and reduced delinquencies. The remaining difference in operation and maintenance expenses primarily resulted from a $62,000 increase in corporate insurance premiums and a variety of other minor expense variances.

General Taxes – General taxes increased $75,945, or 6%, primarily due to higher property taxes associated with increases in utility property partially offset by greater capitalization of payroll taxes.

Depreciation –Depreciation expense increased by $228,385, or 6%, corresponding to the increase in utility plant investment as part of the ongoing pipeline renewal program.

Other Income (Expense) –This line item moved from a net other income to a net other expense primarily due to reduction in investment earnings related to lower interest rates.

Interest Expense –Total interest expense for fiscal 2012 remained virtually unchanged from fiscal

2011 as total debt remained consistent between both years.

Income Taxes –Income tax expense decreased by $208,162, or 7%, from fiscal 2011 corresponding to a comparable decrease in pre-tax earnings. The effective tax rate for fiscal 2012 and 2011 was 38.0%.

Net Income and Dividends –Net income for fiscal 2012 was $4,296,745 compared to $4,653,473 for fiscal 2011. Basic and diluted earnings per share were $0.92 in fiscal 2012 compared to $1.01 in fiscal 2011. Dividends declared per share of common stock were $0.70 in fiscal 2012 and $0.68 in fiscal 2011.

ASSET MANAGEMENT

Roanoke Gas uses a third-party asset manager to manage its pipeline transportation, storage rights and gas supply inventories and deliveries. In return for being able to utilize the excess capacities of the transportation and storage rights, the third party pays Roanoke Gas a monthly utilization fee, which is used to reduce the cost of gas for customers. Under the provision of the asset management contract, the Company has an obligation to purchase its winter storage requirements during the spring and summer injection periods at the market price in place at the time of purchase. This commitment amounts to approximately 2,100,000 decatherms per year or approximately one-third of the Company’s total annual purchases. In addition to the storage purchase requirements, the Company generally purchases its monthly supply requirements from the asset manager based on market price. In October 2013, Roanoke Gas executed a new agreement with a new asset manager under terms similar to the expiring contract. The new agreement expires in March 2017.

| | |

| 20 | | RGC RESOURCES | ANNUAL REPORT 2013 |

CAPITAL RESOURCESAND LIQUIDITY

Due to the capital intensive nature of the utility business, as well as the related weather sensitivity, the Company’s primary capital needs are for the funding of its continuing construction program, the seasonal funding of its natural gas inventories and accounts receivables and payment of dividends. To meet these needs, the Company relies on its operating cash flows, line-of-credit

agreement, long-term debt and to a lesser extent, capital raised through the Company’s Dividend Reinvestment and Stock Purchase Plan (“DRIP”).

Cash and cash equivalents decreased by $6,063,647 in fiscal 2013 compared to an increase of $958,442 in fiscal 2012 and an increase of $1,205,799 in fiscal 2011. The following table summarizes the categories of sources and uses of cash:

Cash Flow Summary

| | | | | | | | | | | | |

Year Ended September 30, | | 2013 | | | 2012 | | | 2011 | |

Provided by operating activities | | $ | 10,037,070 | | | $ | 11,783,041 | | | $ | 10,683,344 | |

Used in investing activities | | | (9,947,510 | ) | | | (8,650,715 | ) | | | (7,589,102 | ) |

Used in financing activities | | | (6,153,207 | ) | | | (2,173,884 | ) | | | (1,888,443 | ) |

| | | | | | | | | | | | |

Increase (decrease) in cash and cash equivalents | | $ | (6,063,647 | ) | | $ | 958,442 | | | $ | 1,205,799 | |

| | | | | | | | | | | | |

As discussed below, a special $1.00 per share dividend was paid by the Company on December 17, 2012, resulting in additional cash used in financing activities of $4,675,337, of which $425,630 was returned to the Company under the DRIP Plan.

Cash Flows from Operating Activities:

The seasonal nature of the natural gas business causes operating cash flows to fluctuate significantly during the year as well as from year to year. Factors, including weather, energy prices, natural gas storage levels and customer collections, all contribute to working capital levels and related cash flows. Generally, operating cash flows are positive during the second and third quarters as a combination of earnings, declining storage gas levels and collections on customer accounts all contribute to higher cash levels. During the first and fourth quarters, operating cash flows generally decrease due to the combination of increases in natural gas storage levels and rising customer receivable balances.

Cash provided by operating activities was $10,037,070 in fiscal 2013, $11,783,041 in fiscal 2012 and $10,683,344 in fiscal 2011. Cash provided by operating activities declined from last year primarily as a result of an increase in cost of gas in storage partially offset by a current year over-collection on gas costs and the continued tax

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 21 |

deferral benefits of bonus depreciation. The cost of gas in storage had declined for the last few years as the commodity price of gas declined; however, when the Company began its fiscal 2013 summer storage program to refill the storage balances, the commodity price of gas was higher than the prior year resulting in higher storage balances by year-end. The average price of natural gas in storage was $4.08, $3.51, $4.92 and $5.26 as of September 30, 2013, 2012, 2011 and 2010, respectively. Fiscal 2012 had the biggest reduction in cost as the price of gas in storage declined by 29% which generated $3.4 million in cash while the higher injection prices during fiscal 2013 used a net $850,000 in cash. Cash provided by operations were positively impacted by the over-collection of gas costs. As provided under the provisions of the Company’s Purchased Gas Adjustment (“PGA”) clause, the Company is allowed to recover the actual cost of natural gas from its customers. Any amounts billed in excess of the actual cost are considered an over-collection of these costs and are reflected as a liability on the financial statements. Conversely, any actual costs incurred in excess of amounts billed are considered an under-collection of gas costs and are reflected as an asset on the financial statements. During fiscal 2013, the Company went from an under-collected position of $687,000 to an over-collected position of $1,027,000, which generated $1,714,000 in operating cash. During fiscal 2012, the Company had an operating use of cash of $1,043,000 as the Company went from an over-collected position to an under-collected position. In addition, 50% bonus depreciation for tax purposes was extended through December 31, 2013. As a result, the Company’s deferred income tax liability associated with its utility property increased by $1,700,000 in fiscal 2013 and more than $2,200,000 in fiscal 2012, thereby deferring payment of income taxes until future periods. The Company has approximately $16,600,000 in

deferred tax liabilities related to accelerated and bonus depreciation on its utility plant that will begin to reverse in 2014 or later, assuming bonus depreciation is not extended, resulting in additional cash outflows for payment of the deferred taxes.

Cash Flows Used in Investing Activities:

Investing activities are generally composed of expenditures under the Company’s construction program, which involves a combination of replacing aging bare steel and cast iron pipe with new plastic or coated steel pipe, making improvements to the LNG plant and, to a lesser extent, expansion of its natural gas system to meet the demands of customer growth. The Company’s expenditures related to its pipeline renewal program and other system and infrastructure improvements and expansion have continued to trend upward with nearly $10,000,000 spent in fiscal 2013 compared to $8,700,000 in fiscal 2012 and $7,600,000 in fiscal 2011. The Company renewed 13 miles of bare steel and cast iron natural gas distribution main and replaced 1,064 services in fiscal 2013. This compares to 15.8 miles of main and 1,429 services in fiscal 2012 and 8.9 miles of gas main and 720 services in fiscal 2011. Total costs related to the renewal program are higher this year even though the total mileage of mains and the number of services replaced were less than last year. As the renewal program has progressed, most of the less complex and more highly concentrated areas of the Company’s natural gas distribution system have been completed leaving the more difficult and smaller sections to be done. Completion of the remaining pipeline replacement will more than likely be at a higher per foot cost, as indicated by fiscal 2013 activity. RGC Resources is committed to the safe and reliable delivery of natural gas to its customers and, as a result, plans to commit the necessary resources to its pipeline renewal program with an expectation to replace all remaining cast

| | |

| 22 | | RGC RESOURCES | ANNUAL REPORT 2013 |

iron and bare steel pipe within the next four years. Depreciation provided approximately 47% of the current year’s capital expenditures compared to 51% for 2012 and 55% for 2011. In addition to the continuation of the pipeline renewal program in fiscal 2014, the Company is also planning two major projects, one at its LNG plant and the other at its Gala transfer station. These two projects are estimated to increase capital expenditures an additional $4.3 million over fiscal 2013. With future capital expenditures projected to remain at higher than historical levels, the Company expects additional corporate borrowing activity will be required.

Cash Flows Used in Financing Activities:

Financing activities generally consist of long-term and short-term borrowings and repayments, issuance of stock and the payment of dividends. As discussed above, the Company uses its line-of-credit arrangement to fund seasonal working capital and provide temporary financing for capital projects, as needed. For the first time since 2009, the Company accessed its line-of-credit during the winter months. Cash flows used in financing activities were $6,153,000 for fiscal 2013 compared to $2,174,000 for fiscal 2012 and $1,888,000 in fiscal 2011. The increase in cash used in financing activities was primarily due to the special $1.00 per share dividend paid by the Company on December 17, 2012. The special dividend totaled $4,675,337, of which $425,630 was returned to the Company under the DRIP Plan. The intent of the dividend was to distribute a portion of equity capital previously deployed and to allow for the realignment of the Company’s capital structure to be more in line with regulatory expectations. The Company’s consolidated capitalization, including the note payable, was 64.4% equity and 35.6% debt at September 30, 2012. As of September 30, 2013,

the consolidated capitalization only changed by 50 basis points to 63.9% equity and 36.1% debt. The decrease in the equity component would have been greater if not for the significant reduction in accumulated other comprehensive loss.

The remaining difference in cash used in financing activities related to the receipt for the pay-off of the balance on the two remaining notes offset by an increase in the regular annual dividend payment rate from $0.70 per share to $0.72 per share.

On March 31, 2013, the Company entered into a new line-of-credit agreement. This new agreement maintains the same terms and rates as provided for under the expired agreement. The interest rate is based on 30-day LIBOR plus 100 basis points and includes an availability fee of 15 basis points applied to the difference between the face amount of the note and the average outstanding balance during the period. The Company maintained the multi-tiered borrowing limits to accommodate

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 23 |

seasonal borrowing demands and minimize overall borrowing costs, with available limits ranging from $1,000,000 to $7,000,000 during the term of the agreement. The line-of-credit agreement will expire March 31, 2014, unless extended. The Company anticipates being able to extend or replace the line-of-credit upon expiration; however, there is no guarantee that the line-of-credit will be extended or replaced under the same or equivalent terms currently in place.

Also on March 31, 2013, the Company executed an unsecured term note in the amount of $15,000,000. This term note extends the maturity date of the original promissory note dated November 28, 2005. The term note, which has a maturity date of March 31, 2014, retains all other terms and conditions provided for in the original promissory note. The Company anticipates being able to renew this note on comparable terms as currently in place until such time the note

co-terminates with the corresponding interest rate swap on November 30, 2015.

As mentioned above, the Company accessed its line-of-credit facility for the first time in four years. The key factors behind the Company’s recent strong cash position have been declining commodity prices of natural gas and the availability of bonus depreciation deductions for tax purposes. With natural gas prices beginning to rise and the continued high levels of capital expenditures anticipated over the next few years, in addition to the anticipated expiration of bonus depreciation, the Company expects to increase utilization of its line-of-credit to provide funding for these cash needs.

OFF-BALANCE SHEET ARRANGEMENTS

The Company has no off-balance sheet arrangements as defined in Regulation S-K, Item 303(a)(4)(ii).

| | |

| 24 | | RGC RESOURCES | ANNUAL REPORT 2013 |

CONTRACTUAL OBLIGATIONSAND COMMITMENTS

The Company has incurred various contractual obligations and commitments in the normal

course of business. As of September 30, 2013, the estimated recorded and unrecorded obligations are as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Payments Due By Period | |

| | | Less Than

1 Year | | | 1-3

Years | | | 4-5

Years | | | After

5 Years | | | Total | |

RecordedContractual obligations: | | | | | | | | | | | | | | | | | | | | |

Long-Term Debt(1) | | $ | — | | | $ | 8,200,000 | | | $ | 3,200,000 | | | $ | 1,600,000 | | | $ | 13,000,000 | |

Short-Term Debt(2) | | | 15,000,000 | | | | — | | | | — | | | | — | | | | 15,000,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | $ | 15,000,000 | | | $ | 8,200,000 | | | $ | 3,200,000 | | | $ | 1,600,000 | | | $ | 28,000,000 | |

| | | | | | | | | | | | | | | | | | | | |

| (1) | See Note 4 to the consolidated financial statements. |

| (2) | See Note 3 to the consolidated financial statements. |

| | | | | | | | | | | | | | | | | | | | |

| | | Payments Due By Period | |

| | | Less Than

1 Year | | | 1-3

Years | | | 4-5

Years | | | After

5 Years | | | Total | |

Unrecorded Contractual obligationsNOT reflected in consolidated balance sheets in accordance with U.S. GAAP: | | | | | | | | | | | | | | | | | | | | |

Pipeline and Storage Capacity(3) | | $ | 11,328,754 | | | $ | 20,765,336 | | | $ | 15,830,608 | | | $ | 7,574,341 | | | $ | 55,499,039 | |

Gas Supply(4) | | | — | | | | — | | | | — | | | | — | | | | — | |

Interest on Short-Term Debt(5) | | | 1,589,322 | | | | — | | | | — | | | | — | | | | 1,589,322 | |

Interest on Long-Term Debt(6) | | | 902,300 | | | | 1,236,524 | | | | 408,534 | | | | 20,427 | | | | 2,567,785 | |

Pension Plan Funding(7) | | | 500,000 | | | | 2,450,000 | | | | 2,400,000 | | | | — | | | | 5,350,000 | |

Other Obligations(8) | | | 93,997 | | | | 115,289 | | | | 29,178 | | | | — | | | | 238,464 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | $ | 14,414,373 | | | $ | 24,567,149 | | | $ | 18,668,320 | | | $ | 7,594,768 | | | $ | 65,244,610 | |

| | | | | | | | | | | | | | | | | | | | |

| (3) | Recoverable through PGA process. |

| (4) | Volumetric obligation for the purchase of contracted decatherms of natural gas at market prices in effect at the time of purchase. See Note 9 to the consolidated financial statements. |

| (5) | Includes payments under the Swap agreement including the estimated settlement of the Swap assuming the corresponding note was not extended. The Company expects to extend this note until such time as the Swap matures. See Note 3 to the consolidated financial statements. |

| (6) | Includes payment under the Swap agreement. See Note 4 to the consolidated financial statements. |

| (7) | Estimated funding beyond five years is not available. See Note 6 to the consolidated financial statements. |

| (8) | Various lease, maintenance, equipment and service contracts. |

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 25 |

REGULATORY AFFAIRS

On November 1, 2012, the Company placed into effect new base rates, subject to refund, that would provide approximately $1,840,000 in additional non-gas revenues on an annual basis. On April 16, 2013, the SCC issued a final order granting a rate award of $649,639 in annual non-gas revenues based on a 9.75% authorized return on equity. In May 2013, the Company completed its refund of excess non-gas revenues collected for rates placed into effect on November 1, 2012 and the rates approved in the final order.

On August 16, 2013, the Company filed an application for a modification to the Company’s SAVE (Steps to Advance Virginia’s Energy) Plan and Rider. The original SAVE Plan and Rider were approved by the SCC through an order issued on August 29, 2012. The original SAVE Plan was designed to facilitate the accelerated replacement of aging natural gas infrastructure assets by providing a mechanism for the Company to recover the related depreciation and expenses and return on rate base of the additional capital investment without the filing of a formal application for an increase in non-gas base rates. Under the original filing, the SAVE Plan primarily covered replacement of the Company’s bare steel and cast iron natural gas distribution pipe. Under the modification, the Company is seeking to include two unique projects; the replacement of the boil-off compressor at the Company’s LNG plant and replacement of the natural gas transfer station located in Gala, VA in the 2014 SAVE Plan year. These replacements will enhance the safety and reliability of the Company’s gas distribution system.

On September 13, 2013, the Company filed a request for an expedited increase in rates with the SCC. The request was for an increase of

approximately $1,664,000 in annual non-gas revenues. As provided for under this expedited rate request, the Company was able to place the increased rates into effect for service rendered on and after November 1, 2013, subject to refund pending a final order by the SCC. The public hearing on the request for this rate increase is scheduled for March 25, 2014, with a final order expected after that date.

During 2011, the Company completed its Distribution Integrity Management Plan (“DIMP”) as required by federal regulations issued by the Pipeline and Hazardous Materials Safety Administration (PHMSA). Under these regulations, distribution operators are required to develop and implement a written DIMP plan that includes the following elements: (i) an operator must demonstrate an understanding of the gas distribution system, (ii) an operator must define the potential threats to the gas distribution pipeline and determine the relative probability of each threat (a risk based approach), (iii) an operator must determine and implement measures designed to reduce the risks of failure of its gas distribution system, (iv) an operator must develop and monitor performance measures to evaluate the effectiveness of its plan, and (v) an operator must continually re-evaluate threats and risks on its entire system and update its plan as necessary.

The Company had been proactive in the area of pipeline safety well before implementation of the DIMP regulations. Over the past 20 years, the Company has replaced much of its cast iron and bare steel pipe. As this pipe has been underground for well over 60 years, the leak potential from such pipe is much higher than the plastic or coated steel pipe currently being installed. The Company prioritized its replacement program using a risk-based evaluation that included leak

| | |

| 26 | | RGC RESOURCES | ANNUAL REPORT 2013 |

history, population density and other factors. The Company expects to replace the remaining pipe within the next four years.

The Company’s provision for depreciation is computed principally based on composite rates determined by depreciation studies. These depreciation studies are required to be performed on the regulated utility assets of Roanoke Gas Company every five years. The last depreciation study was completed and implemented in fiscal 2009. The Company is currently in the process of conducting a new depreciation study for submission to the SCC for approval. Once approved, any changes to the current depreciation rates will be implemented in fiscal 2014. The potential impact of the new depreciation study is not known at this time.

CRITICAL ACCOUNTING POLICIESAND ESTIMATES

The consolidated financial statements of Resources are prepared in accordance with accounting principles generally accepted in the United States of America. The amounts of assets, liabilities, revenues and expenses reported in the Company’s financial statements are affected by accounting policies, estimates and assumptions that are necessary to comply with generally accepted accounting principles. Estimates used in the financial statements are derived from prior experience, statistical analysis and professional judgments. Actual results may differ significantly from these estimates and assumptions.

The Company considers an estimate to be critical if it is material to the financial statements and requires assumptions to be made that were uncertain at the time the estimate was made and changes in the estimate are reasonably likely

to occur from period to period. The Company considers the following accounting policies and estimates to be critical.

Regulatory accounting –The Company’s regulated operations follow the accounting and reporting requirements of FASB ASC No. 980, Regulated Operations. The economic effects of regulation can result in a regulated company deferring costs that have been or are expected to be recovered from customers in a period different from the period in which the costs would be charged to expense by an unregulated enterprise. When this occurs, costs are deferred as assets in the consolidated balance sheet (regulatory assets) and recorded as expenses when such amounts are reflected in rates. Additionally, regulators can impose liabilities upon a regulated company for amounts previously collected from customers and for current collection in rates of costs that are expected to be incurred in the future (regulatory liabilities).

If, for any reason, the Company ceases to meet the criteria for application of regulatory accounting treatment for all or part of its operations, the Company would remove the applicable regulatory assets or liabilities from the balance sheet and include them in the consolidated statements of income and comprehensive income for the period in which the discontinuance occurred.

Revenue recognition –Regulated utility sales and transportation revenues are based upon rates approved by the SCC. The non-gas cost component of rates may not be changed without a formal rate increase application and corresponding authorization by the SCC in the form of a Commission order; however, the gas cost component of rates may be adjusted quarterly through the purchased gas adjustment (“PGA”)

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 27 |

mechanism with administrative approval from the SCC. When the Company files a request for a non-gas rate increase, the SCC may allow the Company to place such rates into effect subject to refund pending a final order. Under these circumstances, the Company estimates the amount of increase it anticipates will be approved based on the best available information.

The Company bills its regulated natural gas customers on a monthly cycle. The billing cycle for most customers does not coincide with the accounting periods used for financial reporting. The Company accrues estimated revenue for natural gas delivered to customers but not yet billed during the accounting period based on weather during the period and current and historical data. The financial statements include unbilled revenue of $1,056,253 and $951,301 as of September 30, 2013 and 2012, respectively.

Allowance for Doubtful Accounts –The Company evaluates the collectability of its accounts receivable balances based upon a variety of factors including loss history, level of delinquent account balances, collections on previously written off accounts and general economic climate.

Pension and Postretirement Benefits –The Company offers a defined benefit pension plan (“pension plan”) and a postretirement medical and life insurance plan (“postretirement plan”) to eligible employees. The expenses and liabilities associated with these plans, as disclosed in Note 6 to the consolidated financial statements, are based on numerous assumptions and factors, including provisions of the plans, employee demographics, contributions made to the plan, return on plan assets and various actuarial calculations, assumptions and accounting requirements. In regard to the pension plan, specific factors include assumptions

regarding the discount rate used in determining future benefit obligations, expected long-term rate of return on plan assets, compensation increases and life expectancies. Similarly, the postretirement medical plan also requires the estimation of many of the same factors as the pension plan in addition to assumptions regarding the rate of medical inflation and Medicare availability. Actual results may differ materially from the results expected from the actuarial assumptions due to changing economic conditions, differences in actual returns on plan assets, different rates of medical inflation, volatility in interest rates and changes in life expectancy. Such differences may result in a material impact on the amount of expense recorded in future periods or the value of the obligations on the balance sheet.

In selecting the discount rate to be used in determining the benefit liability, the Company evaluated the IRS yield curves and the Citigroup yield curves which incorporate the rates of return on high-quality, fixed-income investments that corresponded to the length and timing of benefit streams expected under both the pension plan and postretirement plan. The Company used a discount rate of 4.82% and 4.73% for valuing its pension benefit liability and postretirement plan liability at September 30, 2013, representing an increase of 0.76% and 0.78% in their respective rates from the prior year. The increase in the discount rates corresponded with similar increases in long-term interest rates. The 30-year Treasury rate increased from 2.82% to 3.69%. Likewise, the Moody’s Aaa and Moody’s Baa increased by 1.14% and 0.67%, respectively. The increase in discount rates for valuing the benefit liabilities nearly reversed the reduction in rates experienced in the prior fiscal year. The pension and postretirement plan liability discount rates dropped by 0.98% and 1.01% for the September 30, 2012 valuation from

| | |

| 28 | | RGC RESOURCES | ANNUAL REPORT 2013 |

those used for the September 30, 2011 valuation. The increase in the discount rates for both plans resulted in a significant reduction in the benefit obligation at September 30, 2013. In addition, both plans experienced better than expected returns on the related pension and postretirement assets. The

combination of the discount rate increase and the strong asset performance improved both plans’ funded status significantly and will result in lower pension and postretirement medical plan expense in fiscal 2014.

| | | | | | | | | | | | |

Funded Status – September 30, 2013 | | Pension | | | Postretirement | | | Total | |

Benefit obligation | | $ | 21,468,769 | | | $ | 13,028,628 | | | $ | 34,497,397 | |

Fair value of assets | | | 18,801,262 | | | | 10,114,062 | | | | 28,915,324 | |

| | | | | | | | | | | | |

Funded status | | $ | (2,667,507 | ) | | $ | (2,914,566 | ) | | $ | (5,582,073 | ) |

| | | | | | | | | | | | |

| | | |

Funded Status – September 30, 2012 | | Pension | | | Postretirement | | | Total | |

Benefit obligation | | $ | 23,570,451 | | | $ | 13,707,309 | | | $ | 37,277,760 | |

Fair value of assets | | | 16,063,381 | | | | 8,673,128 | | | | 24,736,509 | |

| | | | | | | | | | | | |

Funded status | | $ | (7,507,070 | ) | | $ | (5,034,181 | ) | | $ | (12,541,251 | ) |

| | | | | | | | | | | | |

The current economic environment makes it difficult to project interest rates and future investment returns. If the economy improves, long-term interest rates could continue to increase and reduce the benefit liabilities and investment returns could be higher. However, if the economy stagnates or declines, interest rates could drop again and lead to an increase in the benefit liabilities and investment returns could be lower. The Company also annually evaluates the returns on its targeted investment allocation model. The investment policy as of the measurement date in September reflected a targeted allocation of 60% equity and 40% fixed income on the pension plan and a targeted allocation of 50% equity and 50% fixed income for the postretirement plan. As a result of this evaluation, the Company set its

expected return on pension assets at 7.00% and postretirement assets at 4.92% (net of income taxes) for fiscal 2014. These rates represent a small reduction from the current year due to the lower expected returns from the fixed income portfolios resulting from a rising interest rate environment.

In early July 2012, the President of the United States signed into law the “Moving Ahead for Progress in the 21st Century Act” (MAP- 21), which provided funding relief for defined benefit pension plans. The requirements of the Employee Retirement Income Security Act of 1974 (ERISA) and the Pension Protection Act of 2006 (PPA) subject defined benefit plans to minimum funding rules. As a result, when interest rates are low, pension plan liabilities increase thereby

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 29 |

resulting in higher mandatory contributions to meet minimum funding obligations. The MAP-21 provides funding relief by allowing pension plans to adjust the interest rate used in determining funding requirements so that they are within 10% of the average of interest rates for the 25-year period preceding the current year for funding calculations for 2013 to within 30% for funding periods beginning in 2016. MAP-21 also provides for increases in the PBGC (Pension Benefit Guaranty Corporation) premiums paid by sponsors of pension plans to protect participants in the event of default by the employer. Although

MAP-21 allows the Company some short-term funding relief, management expects to continue to fund its pension plan at the greater of any minimum pension contribution requirement or its expense level for subsequent years. As a result, the Company expects to contribute approximately $500,000 to its pension plan and $500,000 to its postretirement plan in fiscal 2014. The Company will continue to evaluate its benefit plan funding levels in light of funding requirements and ongoing investment returns and make adjustments, as necessary, to avoid benefit restrictions.

The following schedule reflects the sensitivity of pension costs to changes in certain actuarial assumptions, assuming that the other components of the calculation remain constant.

| | | | | | | | | | | | |

Actuarial Assumption | | Change In

Assumption | | | Increase In

Pension Cost | | | Increase In Projected

Benefit Obligation | |

Discount rate | | | -0.25 | % | | $ | 71,000 | | | $ | 866,000 | |

Rate of return on plan assets | | | -0.25 | % | | | 27,000 | | | | N/A | |

Rate of increase in compensation | | | 0.25 | % | | | 47,000 | | | | 253,000 | |

The following schedule reflects the sensitivity of postretirement benefit costs from changes in certain actuarial assumptions, while the other components of the calculation remain constant.

| | | | | | | | | | | | |

Actuarial Assumption | | Change In

Assumption | | | Increase In

Postretirement

Benefit Cost | | | Increase In

Accumulated

Postretirement

Benefit Obligation | |

Discount rate | | | -0.25 | % | | $ | 23,000 | | | $ | 458,000 | |

Rate of return on plan assets | | | -0.25 | % | | | 25,000 | | | | N/A | |

Healthcare cost trend rate | | | 0.25 | % | | | 60,000 | | | | 478,000 | |

Derivatives –The Company may hedge certain risks incurred in its operation through the use of derivative instruments. The Company applies the requirements of FASB ASC No. 815,Derivatives and Hedging,which requires the recognition of derivative instruments as assets or liabilities in the Company’s balance sheet at fair value. In most instances, fair value is based upon quoted futures

prices for natural gas commodities and interest rate futures for interest rate swaps. Changes in the commodity and futures markets will impact the estimates of fair value in the future. Furthermore, the actual market value at the point of realization of the derivative may be significantly different from the values used in determining fair value in prior financial statements.

| | |

| 30 | | RGC RESOURCES | ANNUAL REPORT 2013 |

MARKET PRICEAND DIVIDEND INFORMATION

RGC Resources’ common stock is listed on the Nasdaq Global Market under the trading symbol RGCO. Payment of dividends is within the discretion of the Board of Directors and will depend on, among other factors, earnings, capital

requirements and the operating and financial condition of the Company. The Company’s long-term indebtedness contains restrictions on dividends based on cumulative net earnings and dividends previously paid.

| | | | | | | | | | | | |

| | | Range of Bid Prices | | | Cash Dividends | |

Fiscal Year Ended September 30, | | High | | | Low | | | Declared | |

2013 | | | | | | | | | | | | |

First Quarter | | $ | 19.72 | | | $ | 17.51 | | | $ | 0.180 | |

Second Quarter | | | 19.40 | | | | 17.96 | | | | 0.180 | |

Third Quarter | | | 21.94 | | | | 18.44 | | | | 0.180 | |

Fourth Quarter | | | 20.97 | | | | 17.86 | | | | 0.180 | |

Special Dividend | | | | | | | | | | | 1.000 | |

| | | |

2012 | | | | | | | | | | | | |

First Quarter | | $ | 19.19 | | | $ | 17.14 | | | $ | 0.175 | |

Second Quarter | | | 19.52 | | | | 17.03 | | | | 0.175 | |

Third Quarter | | | 18.88 | | | | 16.99 | | | | 0.175 | |

Fourth Quarter | | | 18.81 | | | | 17.49 | | | | 0.175 | |

CAPITALIZATION STATISTICS

| | | | | | | | | | | | | | | | | | | | |

Year Ended September 30, | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

COMMON STOCK: | | | | | | | | | | | | | | | | | | | | |

Shares Issued | | | 4,709,326 | | | | 4,670,567 | | | | 4,624,682 | | | | 4,548,864 | | | | 4,477,974 | |

Earnings Per Share | | | | | | | | | | | | | | | | | | | | |

Basic Earnings Per Share | | $ | 0.91 | | | $ | 0.92 | | | $ | 1.01 | | | $ | 0.98 | | | $ | 1.09 | |

Diluted Earnings Per Share | | $ | 0.91 | | | $ | 0.92 | | | $ | 1.01 | | | $ | 0.98 | | | $ | 1.09 | |

Dividends Paid Per Share (Cash) | | $ | 1.72 | | | $ | 0.70 | | | $ | 0.68 | | | $ | 0.66 | | | $ | 0.64 | |

Dividends Paid Out Ratio | | | 189.0 | % | | | 76.1 | % | | | 67.3 | % | | | 67.3 | % | | | 58.7 | % |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

CAPITALIZATION RATIOS: | | | | | | | | | | | | | | | | | | | | |

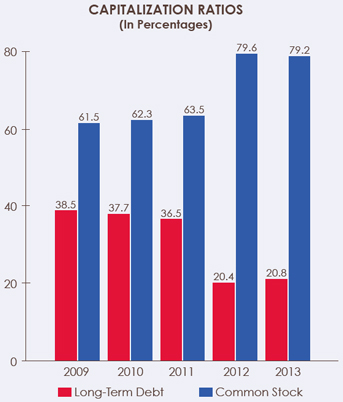

Long-Term Debt, Including Current Maturities | | | 20.8 | % | | | 20.4 | % | | | 36.5 | % | | | 37.7 | % | | | 38.5 | % |

Common Stock And Surplus | | | 79.2 | % | | | 79.6 | % | | | 63.5 | % | | | 62.3 | % | | | 61.5 | % |

| | | | | | | | | | | | | | | | | | | | |

Total | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | |

Long-Term Debt, Including Current Maturities | | $ | 13,000,000 | | | $ | 13,000,000 | | | $ | 28,000,000 | | | $ | 28,000,000 | | | $ | 28,000,000 | |

Common Stock And Surplus | | | 49,502,422 | | | | 50,682,930 | | | | 48,785,778 | | | | 46,309,747 | | | | 44,799,871 | |

| | | | | | | | | | | | | | | | | | | | |

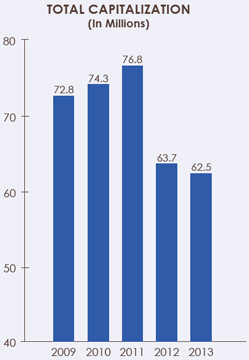

Total Capitalization Plus Current Maturities | | $ | 62,502,422 | | | $ | 63,682,930 | | | $ | 76,785,778 | | | $ | 74,309,747 | | | $ | 72,799,871 | |

| | | | | | | | | | | | | | | | | | | | |

| | |

| RGC RESOURCES | ANNUAL REPORT 2013 | | 31 |

SUMMARYOF GAS SALESAND STATISTICS

| | | | | | | | | | | | | | | | | | | | |

Years Ended September 30, | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

REVENUES: | | | | | | | | | | | | | | | | | | | | |

Residential Sales | | $ | 36,271,831 | | | $ | 32,784,791 | | | $ | 40,051,923 | | | $ | 42,277,903 | | | $ | 46,215,441 | |

Commercial Sales | | | 20,597,084 | | | | 19,164,789 | | | | 23,463,529 | | | | 25,166,672 | | | | 28,936,307 | |

Interruptible Sales | | | 1,205,788 | | | | 1,397,353 | | | | 1,572,270 | | | | 573,946 | | | | 609,698 | |

Transportation Gas Sales | | | 2,912,550 | | | | 2,957,344 | | | | 2,843,115 | | | | 2,674,151 | | | | 2,506,958 | |

Backup Services | | | — | | | | — | | | | — | | | | — | | | | 300 | |

Inventory Carrying Cost Revenues | | | 937,684 | | | | 1,236,713 | | | | 1,395,877 | | | | 1,546,544 | | | | 2,327,508 | |

Late Payment Charges | | | 37,407 | | | | 37,519 | | | | 44,252 | | | | 63,949 | | | | 56,718 | |

Miscellaneous Gas Utility Revenue | | | 61,830 | | | | 79,431 | | | | 112,654 | | | | 123,493 | | | | 133,298 | |

Other | | | 1,181,492 | | | | 1,141,747 | | | | 1,315,251 | | | | 1,397,256 | | | | 1,398,245 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | $ | 63,205,666 | | | $ | 58,799,687 | | | $ | 70,798,871 | | | $ | 73,823,914 | | | $ | 82,184,473 | |

NET INCOME | | $ | 4,262,052 | | | $ | 4,296,745 | | | $ | 4,653,473 | | | $ | 4,445,436 | | | $ | 4,869,010 | |

DTH DELIVERED: | | | | | | | | | | | | | | | | | | | | |

Residential | | | 3,821,200 | | | | 3,036,076 | | | | 3,866,489 | | | | 3,910,639 | | | | 3,866,956 | |

Commercial | | | 2,677,583 | | | | 2,299,760 | | | | 2,715,998 | | | | 2,712,692 | | | | 2,830,782 | |

Interruptible | | | 247,069 | | | | 286,326 | | | | 263,851 | | | | 79,858 | | | | 75,061 | |

Transportation Gas | | | 2,663,042 | | | | 2,695,334 | | | | 2,698,260 | | | | 2,610,962 | | | | 2,487,670 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | | 9,408,894 | | | | 8,317,496 | | | | 9,544,598 | | | | 9,314,151 | | | | 9,260,469 | |

HEATING DEGREE DAYS | | | 4,001 | | | | 3,189 | | | | 4,091 | | | | 4,047 | | | | 3,914 | |

NUMBER OF CUSTOMERS: | | | | | | | | | | | | | | | | | | | | |

Natural Gas | | | | | | | | | | | | | | | | | | | | |

Residential | | | 53,093 | | | | 52,836 | | | | 52,579 | | | | 51,922 | | | | 51,069 | |

Commercial | | | 5,110 | | | | 5,072 | | | | 5,073 | | | | 5,020 | | | | 5,018 | |

Interruptible and Transportation | | | 35 | | | | 33 | | | | 32 | | | | 33 | | | | 32 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | | 58,238 | | | | 57,941 | | | | 57,684 | | | | 56,975 | | | | 56,119 | |

GAS ACCOUNT (DTH): | | | | | | | | | | | | | | | | | | | | |

Natural Gas Available | | | 9,622,988 | | | | 8,521,983 | | | | 9,772,756 | | | | 9,561,029 | | | | 9,549,231 | |

Natural Gas Deliveries | | | 9,408,894 | | | | 8,317,496 | | | | 9,544,598 | | | | 9,314,151 | | | | 9,260,469 | |

Storage - LNG | | | 139,875 | | | | 111,735 | | | | 114,670 | | | | 136,972 | | | | 124,925 | |

Company Use And Miscellaneous | | | 50,282 | | | | 41,620 | | | | 42,147 | | | | 47,759 | | | | 39,697 | |

System Loss | | | 23,937 | | | | 51,132 | | | | 71,341 | | | | 62,147 | | | | 124,140 | |

| | | | | | | | | | | | | | | | | | | | |

Total Gas Available | | | 9,622,988 | | | | 8,521,983 | | | | 9,772,756 | | | | 9,561,029 | | | | 9,549,231 | |

TOTAL ASSETS | | $ | 124,526,701 | | | $ | 129,756,338 | | | $ | 125,549,049 | | | $ | 120,683,316 | | | $ | 118,801,892 | |

LONG-TERM OBLIGATIONS | | $ | 13,000,000 | | | $ | 13,000,000 | | | $ | 13,000,000 | | | $ | 28,000,000 | | | $ | 28,000,000 | |

| | |

| 32 | | RGC RESOURCES | ANNUAL REPORT 2013 |

RGC Resources, Inc. and Subsidiaries

Consolidated Financial Statements

for the Years Ended September 30, 2013, 2012

and 2011, and Report of Independent

Registered Public Accounting Firm

RGC RESOURCES, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors and Stockholders

RGC Resources, Inc.

Roanoke, Virginia

We have audited the accompanying consolidated balance sheets of RGC Resources, Inc. and Subsidiaries (“the Company”) as of September 30, 2013 and 2012, and the related consolidated statements of income, comprehensive income, stockholders’ equity, and cash flows for each of the years in the three-year period ended September 30, 2013. RGC Resources, Inc.’s management is responsible for these financial statements. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.