UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the quarterly period ended June 30, 2013

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

Commission File Number: 001-14625 (Host Hotels & Resorts, Inc.)

0-25087 (Host Hotels & Resorts, L.P.)

HOST HOTELS & RESORTS, INC.

HOST HOTELS & RESORTS, L.P.

(Exact name of registrant as specified in its charter)

Maryland (Host Hotels & Resorts, Inc.) Delaware (Host Hotels & Resorts, L.P.) (State or Other Jurisdiction of Incorporation or Organization) | | 53-008595 52-2095412 (I.R.S. Employer Identification No.) |

| | |

6903 Rockledge Drive, Suite 1500 Bethesda, Maryland (Address of Principal Executive Offices) | | 20817 (Zip Code) |

(240) 744-1000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Host Hotels & Resorts, Inc. | | Yes þ | | | | No ¨ | |

Host Hotels & Resorts, L.P. | | Yes þ | | | | No ¨ | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Host Hotels & Resorts, Inc. | | Yes þ | | | | No ¨ | |

Host Hotels & Resorts, L.P. | | Yes þ | | | | No ¨ | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Host Hotels & Resorts, Inc. | |

Large accelerated filer þ | Accelerated filer ¨ |

Non-accelerated filer (Do not check if a smaller reporting company) ¨ | Smaller reporting company ¨ |

| |

Host Hotels & Resorts, L.P. | |

Large accelerated filer ¨ | Accelerated filer ¨ |

Non-accelerated filer (Do not check if a smaller reporting company) þ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Host Hotels & Resorts, Inc. | | Yes ¨ | | | | No þ | |

Host Hotels & Resorts, L.P. | | Yes ¨ | | | | No þ | |

As of August 2, 2013 there were 750,030,597 shares of Host Hotels & Resorts, Inc.’s common stock, $.01 par value per share, outstanding.

EXPLANATORY NOTE

This report combines the quarterly reports on Form 10-Q of Host Hotels & Resorts, Inc. and Host Hotels & Resorts, L.P. Unless stated otherwise or the context requires otherwise, references to “Host Inc.” mean Host Hotels & Resorts, Inc., a Maryland corporation, and references to “Host L.P.” mean Host Hotels & Resorts, L.P., a Delaware limited partnership, and its consolidated subsidiaries, in cases where it is important to distinguish between Host Inc. and Host L.P. We use the terms “we” or “our” or “the company” to refer to Host Inc. and Host L.P. together, unless the context indicates otherwise.

Host Inc. operates as a self-managed and self-administered real estate investment trust (“REIT”). Host Inc. owns properties and conducts operations through Host L.P., of which Host Inc. is the sole general partner and of which it holds approximately 98.7% of the partnership interests (“OP units”). The remaining OP units are owned by various unaffiliated limited partners. As the sole general partner of Host L.P., Host Inc. has the exclusive and complete responsibility for Host L.P.’s day-to-day management and control. Management operates Host Inc. and Host L.P. as one enterprise. The management of Host Inc. consists of the same persons who direct the management of Host L.P. As general partner with control of Host L.P., Host Inc. consolidates Host L.P. for financial reporting purposes, and Host Inc. does not have significant assets other than its investment in Host L.P. Therefore, the assets and liabilities of Host Inc. and Host L.P. are substantially the same on their respective condensed consolidated financial statements and the disclosures of Host Inc. and Host L.P. also are substantially similar. For these reasons, we believe that the combination into a single report of the quarterly reports on Form 10-Q of Host Inc. and Host L.P. results in benefits to management and investors.

The substantive difference between Host Inc.’s and Host L.P.’s filings is the fact that Host Inc. is a REIT with public stock, while Host L.P. is a partnership with no publicly traded equity. In the condensed consolidated financial statements, this difference primarily is reflected in the equity (or partners’ capital for Host L.P.) section of the consolidated balance sheets and in the consolidated statements of equity (or partners’ capital for Host L.P.). Apart from the different equity treatment, the condensed consolidated financial statements of Host Inc. and Host L.P. nearly are identical.

This combined Form 10-Q for Host Inc. and Host L.P. includes, for each entity, separate interim financial statements (but combined footnotes), separate reports on disclosure controls and procedures and internal control over financial reporting and separate CEO/CFO certifications. In addition, with respect to any other financial and non-financial disclosure items required by Form 10-Q, any material differences between Host Inc. and Host L.P. are discussed separately herein. For a more detailed discussion of the substantive differences between Host Inc. and Host L.P. and why we believe the combined filing results in benefits to investors, see the discussion in the combined Annual Report on Form 10-K for the year ended December 31, 2012 under the heading “Explanatory Note.”

i

HOST HOTELS & RESORTS, INC. AND HOST HOTELS & RESORTS, L.P.

INDEX

PART I. FINANCIAL INFORMATION

| | | | Page No. |

Item 1. | | Financial Statements for Host Hotels & Resorts, Inc.: | |

| | | |

| | Condensed Consolidated Balance Sheets - June 30, 2013 (unaudited) and December 31, 2012 | 1 |

| | | |

| | Condensed Consolidated Statements of Operations (unaudited) - Quarter and Year-to-date ended June 30, 2013 and June 15, 2012 | 2 |

| | | |

| | Condensed Consolidated Statements of Comprehensive Income (Loss) (unaudited) - Quarter and Year-to-date ended June 30, 2013 and June 15, 2012 | 3 |

| | | |

| | Condensed Consolidated Statements of Cash Flows (unaudited) - Year-to-date ended June 30, 2013 and June 15, 2012 | 4 |

| | | |

| | Financial Statements for Host Hotels & Resorts, L.P.: | |

| | | |

| | Condensed Consolidated Balance Sheets - June 30, 2013 (unaudited) and December 31, 2012 | 6 |

| | | |

| | Condensed Consolidated Statements of Operations (unaudited) - Quarter and Year-to-date ended June 30, 2013 and June 15, 2012 | 7 |

| | | |

| | Condensed Consolidated Statements of Comprehensive Income (Loss) (unaudited) - Quarter and Year-to-date ended June 30, 2013 and June 15, 2012 | 8 |

| | | |

| | Condensed Consolidated Statements of Cash Flows (unaudited) - Year-to-date ended June 30, 2013 and June 15, 2012 | 9 |

| | | |

| | Notes to Condensed Consolidated Financial Statements (unaudited) | 11 |

| | | |

Item 2. | | Management’s Discussion and Analysis of Financial Condition and Results and Operations | 23 |

| | | |

Item 3. | | Quantitative and Qualitative Disclosures about Market Risk | 52 |

| | | |

Item 4. | | Controls and Procedures | 53 |

| | | |

| | PART II. OTHER INFORMATION | |

| | | |

Item 1. | | Legal Proceedings | 54 |

| | | |

Item 2. | | Unregistered Sales of Equity Securities and Use of Proceeds | 54 |

| | | |

Item 6. | | Exhibits | 55 |

ii

HOST HOTELS & RESORTS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

June 30, 2013 and December 31, 2012

(in millions, except share and per share amounts)

| June 30,

2013 | | | December 31,

2012 | |

| (unaudited) | | | | |

ASSETS |

Property and equipment, net | $ | 11,201 | | | $ | 11,588 | |

Due from managers | | 130 | | | | 80 | |

Advances to and investments in affiliates | | 392 | | | | 347 | |

Deferred financing costs, net | | 46 | | | | 53 | |

Furniture, fixtures and equipment replacement fund | | 194 | | | | 154 | |

Other | | 274 | | | | 319 | |

Restricted cash | | 35 | | | | 36 | |

Cash and cash equivalents | | 393 | | | | 417 | |

Total assets | $ | 12,665 | | | $ | 12,994 | |

| | | | | | | |

LIABILITIES, NON-CONTROLLING INTERESTS AND EQUITY |

Debt | | | | | | | |

Senior notes, including $ 363 million and $531 million, respectively, net of discount, of Exchangeable Senior Debentures | $ | 3,210 | | | $ | 3,569 | |

Credit facility, including the $ 500 million term loan | | 702 | | | | 763 | |

Mortgage debt | | 727 | | | | 993 | |

Other | | 85 | | | | 86 | |

Total debt | | 4,724 | | | | 5,411 | |

Accounts payable and accrued expenses | | 175 | | | | 194 | |

Other | | 384 | | | | 372 | |

Total liabilities | | 5,283 | | | | 5,977 | |

| | | | | | | |

Non-controlling interests—Host Hotels & Resorts, L.P. | | 168 | | | | 158 | |

| | | | | | | |

Host Hotels & Resorts, Inc. stockholders’ equity: | | | | | | | |

Common stock, par value $.01, 1,050 million shares authorized; 748.2 million and 724.6 million shares issued and outstanding, respectively | | 7 | | | | 7 | |

Additional paid-in capital | | 8,400 | | | | 8,040 | |

Accumulated other comprehensive income (loss) | | (12 | ) | | | 12 | |

Deficit | | (1,216 | ) | | | (1,234 | ) |

Total equity of Host Hotels & Resorts, Inc. stockholders | | 7,179 | | | | 6,825 | |

Non-controlling interests—other consolidated partnerships | | 35 | | | | 34 | |

Total equity | | 7,214 | | | | 6,859 | |

Total liabilities, non-controlling interests and equity | $ | 12,665 | | | $ | 12,994 | |

See notes to condensed consolidated statements.

1

HOST HOTELS & RESORTS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

Quarter and Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions, except per share amounts)

| Quarter ended | | | Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

REVENUES | | | | | | | | | | | | | | | |

Rooms | $ | 903 | | | $ | 798 | | | $ | 1,677 | | | $ | 1,346 | |

Food and beverage | | 425 | | | | 386 | | | | 800 | | | | 665 | |

Other | | 79 | | | | 77 | | | | 156 | | | | 135 | |

Owned hotel revenues | | 1,407 | | | | 1,261 | | | | 2,633 | | | | 2,146 | |

Other revenues | | 13 | | | | 65 | | | | 30 | | | | 124 | |

Total revenues | | 1,420 | | | | 1,326 | | | | 2,663 | | | | 2,270 | |

EXPENSES | | | | | | | | | | | | | | | |

Rooms | | 230 | | | | 206 | | | | 448 | | | | 364 | |

Food and beverage | | 290 | | | | 268 | | | | 567 | | | | 474 | |

Other departmental and support expenses | | 322 | | | | 306 | | | | 634 | | | | 545 | |

Management fees | | 66 | | | | 55 | | | | 114 | | | | 87 | |

Other property-level expenses | | 93 | | | | 140 | | | | 189 | | | | 263 | |

Depreciation and amortization | | 174 | | | | 153 | | | | 349 | | | | 301 | |

Corporate and other expenses | | 37 | | | | 21 | | | | 63 | | | | 43 | |

Total operating costs and expenses | | 1,212 | | | | 1,149 | | | | 2,364 | | | | 2,077 | |

OPERATING PROFIT | | 208 | | | | 177 | | | | 299 | | | | 193 | |

Interest income | | 1 | | | | 3 | | | | 2 | | | | 7 | |

Interest expense | | (103 | ) | | | (94 | ) | | | (179 | ) | | | (180 | ) |

Net gains on property transactions and other | | 21 | | | | 1 | | | | 32 | | | | 2 | |

Gain (loss) on foreign currency transactions and derivatives | | 1 | | | | — | | | | 3 | | | | (1 | ) |

Equity in earnings of affiliates | | 6 | | | | 5 | | | | 4 | | | | 3 | |

INCOME BEFORE INCOME TAXES | | 134 | | | | 92 | | | | 161 | | | | 24 | |

Benefit (provision) for income taxes | | (15 | ) | | | (12 | ) | | | (7 | ) | | | 1 | |

INCOME FROM CONTINUING OPERATIONS | | 119 | | | | 80 | | | | 154 | | | | 25 | |

Income from discontinued operations, net of tax | | 2 | | | | 3 | | | | 27 | | | | 58 | |

NET INCOME | | 121 | | | | 83 | | | | 181 | | | | 83 | |

Less: Net income attributable to non-controlling interests | | (2 | ) | | | (1 | ) | | | (6 | ) | | | (3 | ) |

NET INCOME ATTRIBUTABLE TO HOST HOTELS & RESORTS, INC. | $ | 119 | | | $ | 82 | | | $ | 175 | | | $ | 80 | |

Basic earnings per common share: | | | | | | | | | | | | | | | |

Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

Discontinued operations | | — | | | | — | | | | .04 | | | | .08 | |

Basic earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

Diluted earnings per common share: | | | | | | | | | | | | | | | |

Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

Discontinued operations | | — | | | | — | | | | .04 | | | | .08 | |

Diluted earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

See notes to condensed consolidated statements.

2

HOST HOTELS & RESORTS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

Quarter and Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions)

| Quarter ended | | | Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

NET INCOME | $ | 121 | | | $ | 83 | | | $ | 181 | | | $ | 83 | |

OTHER COMPREHENSIVE INCOME (LOSS), NET OF TAX: | | | | | | | | | | | | | | | |

Foreign currency translation and other comprehensive income (loss) of unconsolidated affiliates | | (26 | ) | | | (29 | ) | | | (29 | ) | | | (8 | ) |

Change in fair value of derivative instruments | | — | | | | 4 | | | | 5 | | | | 2 | |

OTHER COMPREHENSIVE LOSS, NET OF TAX | | (26 | ) | | | (25 | ) | | | (24 | ) | | | (6 | ) |

COMPREHENSIVE INCOME | | 95 | | | | 58 | | | | 157 | | | | 77 | |

Less: Comprehensive income attributable to non-controlling interests | | (2 | ) | | | (1 | ) | | | (6 | ) | | | (3 | ) |

COMPREHENSIVE INCOME ATTRIBUTABLE TO HOST HOTELS & RESORTS, INC | $ | 93 | | | $ | 57 | | | $ | 151 | | | $ | 74 | |

See notes to condensed consolidated statements.

3

HOST HOTELS & RESORTS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions)

| Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | |

OPERATING ACTIVITIES | | | | | | | |

Net income | $ | 181 | | | $ | 83 | |

Adjustments to reconcile to cash provided by operations: | | | | | | | |

Discontinued operations: | | | | | | | |

Gain on dispositions | | (19 | ) | | | (48 | ) |

Depreciation | | 2 | | | | 11 | |

Depreciation and amortization | | 349 | | | | 301 | |

Amortization of finance costs, discounts and premiums, net | | 14 | | | | 11 | |

Stock compensation expense | | 8 | | | | 8 | |

Deferred income taxes | | (1 | ) | | | (4 | ) |

Net gain on property transactions and other | | (32 | ) | | | (2 | ) |

(Gain) loss on foreign currency transactions and derivatives | | (3 | ) | | | 1 | |

Non-cash loss on extinguishment of debt | | 12 | | | | 4 | |

Equity in earnings of affiliates | | (4 | ) | | | (3 | ) |

Change in due from managers | | (55 | ) | | | (42 | ) |

Changes in other assets | | 34 | | | | 12 | |

Changes in other liabilities | | (26 | ) | | | (30 | ) |

Cash provided by operating activities | | 460 | | | | 302 | |

| | | | | | | |

INVESTING ACTIVITIES | | | | | | | |

Proceeds from sales of assets, net | | 446 | | | | 108 | |

Acquisitions | | (139 | ) | | | (18 | ) |

Advances to and investments in affiliates | | (50 | ) | | | (20 | ) |

Capital expenditures: | | | | | | | |

Renewals and replacements | | (163 | ) | | | (179 | ) |

Redevelopment and acquisition-related investments | | (69 | ) | | | (162 | ) |

New development | | (11 | ) | | | — | |

Change in furniture, fixtures and equipment (“FF&E”) replacement fund | | (39 | ) | | | (2 | ) |

Property insurance proceeds | | — | | | | 4 | |

Cash used in investing activities | | (25 | ) | | | (269 | ) |

| | | | | | | |

FINANCING ACTIVITIES | | | | | | | |

Financing costs | | (4 | ) | | | (7 | ) |

Issuances of debt | | 400 | | | | 450 | |

Draws on credit facility | | 148 | | | | 22 | |

Repayment on credit facility | | (200 | ) | | | — | |

Repurchase/redemption of senior notes | | (601 | ) | | | (893 | ) |

Mortgage debt prepayments and scheduled maturities | | (246 | ) | | | (113 | ) |

Scheduled principal repayments | | (1 | ) | | | (2 | ) |

Issuance of common stock | | 192 | | | | 222 | |

Dividends on common stock | | (140 | ) | | | (78 | ) |

Contributions from non-controlling interests | | 3 | | | | 1 | |

Distributions to non-controlling interests | | (6 | ) | | | (4 | ) |

Change in restricted cash for financing activities | | 1 | | | | 8 | |

Cash used in financing activities | | (454 | ) | | | (394 | ) |

DECREASE IN CASH AND CASH EQUIVALENTS | | (19 | ) | | | (361 | ) |

CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | | 417 | | | | 826 | |

Effects of exchange rate changes on cash held | | (5 | ) | | | — | |

CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | 393 | | | $ | 465 | |

See notes to condensed consolidated statements.

4

HOST HOTELS & RESORTS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited)

Supplemental disclosure of cash flow information (in millions)

| | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | |

| Interest paid – periodic interest expense | $ | 148 | | | $ | 160 | |

| Interest paid – debt extinguishments | | 20 | | | | 9 | |

| Total interest paid | $ | 168 | | | $ | 169 | |

| Income taxes paid | $ | 6 | | | $ | 8 | |

Supplemental disclosure of noncash investing and financing activities:

For the year-to-date periods ended June 30, 2013 and June 15, 2012, Host Inc. issued approximately 0.1 million shares and 0.5 million shares, respectively, upon the conversion of OP units of Host L.P. held by non-controlling partners valued at approximately $2 million and $8 million, respectively.

In March 2013, holders of approximately $174 million of the 3.25% exchangeable debentures elected to exchange their debentures for approximately 11.7 million shares of Host Inc. common stock.

See notes to condensed consolidated statements.

5

HOST HOTELS & RESORTS, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

June 30, 2013 and December 31, 2012

(in millions)

| June 30,

2013 | | | December 31,

2012 | |

| (unaudited) | | | | |

ASSETS |

Property and equipment, net | $ | 11,201 | | | $ | 11,588 | |

Due from managers | | 130 | | | | 80 | |

Advances to and investments in affiliates | | 392 | | | | 347 | |

Deferred financing costs, net | | 46 | | | | 53 | |

Furniture, fixtures and equipment replacement fund | | 194 | | | | 154 | |

Other | | 274 | | | | 319 | |

Restricted cash | | 35 | | | | 36 | |

Cash and cash equivalents | | 393 | | | | 417 | |

Total assets | $ | 12,665 | | | $ | 12,994 | |

| | | | | | | |

LIABILITIES, LIMITED PARTNERSHIP INTERESTS OF THIRD PARTIES AND CAPITAL |

Debt | | | | | | | |

Senior notes, including $ 363 million and $531 million, respectively, net of discount, of Exchangeable Senior Debentures | $ | 3,210 | | | $ | 3,569 | |

Credit facility, including the $ 500 million term loan | | 702 | | | | 763 | |

Mortgage debt | | 727 | | | | 993 | |

Other | | 85 | | | | 86 | |

Total debt | | 4,724 | | | | 5,411 | |

Accounts payable and accrued expenses | | 175 | | | | 194 | |

Other | | 384 | | | | 372 | |

Total liabilities | | 5,283 | | | | 5,977 | |

| | | | | | | |

Limited partnership interests of third parties | | 168 | | | | 158 | |

| | | | | | | |

Host Hotels & Resorts, L.P. capital: | | | | | | | |

General partner | | 1 | | | | 1 | |

Limited partner | | 7,190 | | | | 6,812 | |

Accumulated other comprehensive income (loss) | | (12 | ) | | | 12 | |

Total Host Hotels & Resorts, L.P. capital | | 7,179 | | | | 6,825 | |

Non-controlling interests—consolidated partnerships | | 35 | | | | 34 | |

Total capital | | 7,214 | | | | 6,859 | |

Total liabilities, limited partnership interest of third parties and capital | $ | 12,665 | | | $ | 12,994 | |

See notes to condensed consolidated statements.

6

HOST HOTELS & RESORTS, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

Quarter and Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions, except per unit amounts)

| Quarter ended | | | Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

REVENUES | | | | | | | | | | | | | | | |

Rooms | $ | 903 | | | $ | 798 | | | $ | 1,677 | | | $ | 1,346 | |

Food and beverage | | 425 | | | | 386 | | | | 800 | | | | 665 | |

Other | | 79 | | | | 77 | | | | 156 | | | | 135 | |

Owned hotel revenues | | 1,407 | | | | 1,261 | | | | 2,633 | | | | 2,146 | |

Other revenues | | 13 | | | | 65 | | | | 30 | | | | 124 | |

Total revenues | | 1,420 | | | | 1,326 | | | | 2,663 | | | | 2,270 | |

EXPENSES | | | | | | | | | | | | | | | |

Rooms | | 230 | | | | 206 | | | | 448 | | | | 364 | |

Food and beverage | | 290 | | | | 268 | | | | 567 | | | | 474 | |

Other departmental and support expenses | | 322 | | | | 306 | | | | 634 | | | | 545 | |

Management fees | | 66 | | | | 55 | | | | 114 | | | | 87 | |

Other property-level expenses | | 93 | | | | 140 | | | | 189 | | | | 263 | |

Depreciation and amortization | | 174 | | | | 153 | | | | 349 | | | | 301 | |

Corporate and other expenses | | 37 | | | | 21 | | | | 63 | | | | 43 | |

Total operating costs and expenses | | 1,212 | | | | 1,149 | | | | 2,364 | | | | 2,077 | |

OPERATING PROFIT | | 208 | | | | 177 | | | | 299 | | | | 193 | |

Interest income | | 1 | | | | 3 | | | | 2 | | | | 7 | |

Interest expense | | (103 | ) | | | (94 | ) | | | (179 | ) | | | (180 | ) |

Net gains on property transactions and other | | 21 | | | | 1 | | | | 32 | | | | 2 | |

Gain (loss) on foreign currency transactions and derivatives | | 1 | | | | — | | | | 3 | | | | (1 | ) |

Equity in earnings of affiliates | | 6 | | | | 5 | | | | 4 | | | | 3 | |

INCOME BEFORE INCOME TAXES | | 134 | | | | 92 | | | | 161 | | | | 24 | |

Benefit (provision) for income taxes | | (15 | ) | | | (12 | ) | | | (7 | ) | | | 1 | |

INCOME FROM CONTINUING OPERATIONS | | 119 | | | | 80 | | | | 154 | | | | 25 | |

Income from discontinued operations, net of tax. | | 2 | | | | 3 | | | | 27 | | | | 58 | |

NET INCOME | | 121 | | | | 83 | | | | 181 | | | | 83 | |

Less: Net income attributable to non-controlling interests | | (1 | ) | | | — | | | | (4 | ) | | | (2 | ) |

NET INCOME ATTRIBUTABLE TO HOST HOTELS & RESORTS, L.P. | $ | 120 | | | $ | 83 | | | $ | 177 | | | $ | 81 | |

Basic earnings per common unit: | | | | | | | | | | | | | | | |

Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

Discontinued operations | | — | | | | .01 | | | | .04 | | | | .08 | |

Basic earnings per common unit | $ | .16 | | | $ | .12 | | | $ | .24 | | | $ | .11 | |

Diluted earnings per common unit: | | | | | | | | | | | | | | | |

Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

Discontinued operations | | — | | | | .01 | | | | .04 | | | | .08 | |

Diluted earnings per common unit | $ | .16 | | | $ | .12 | | | $ | .24 | | | $ | .11 | |

See notes to condensed consolidated statements.

7

HOST HOTELS & RESORTS, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

Quarter and Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions)

| Quarter ended | | | Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

NET INCOME | $ | 121 | | | $ | 83 | | | $ | 181 | | | $ | 83 | |

OTHER COMPREHENSIVE INCOME (LOSS), NET OF TAX: | | | | | | | | | | | | | | | |

Foreign currency translation and other comprehensive income (loss) of unconsolidated affiliates | | (26 | ) | | | (29 | ) | | | (29 | ) | | | (8 | ) |

Change in fair value of derivative instruments | | — | | | | 4 | | | | 5 | | | | 2 | |

OTHER COMPREHENSIVE LOSS, NET OF TAX | | (26 | ) | | | (25 | ) | | | (24 | ) | | | (6 | ) |

COMPREHENSIVE INCOME | | 95 | | | | 58 | | | | 157 | | | | 77 | |

Less: Comprehensive income attributable to non-controlling interests | | (1 | ) | | | — | | | | (4 | ) | | | (2 | ) |

COMPREHENSIVE INCOME ATTRIBUTABLE TO HOST HOTELS & RESORTS, L.P. | $ | 94 | | | $ | 58 | | | $ | 153 | | | $ | 75 | |

See notes to condensed consolidated statements.

8

HOST HOTELS & RESORTS, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited, in millions)

| Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | |

OPERATING ACTIVITIES | | | | | | | |

Net income | $ | 181 | | | $ | 83 | |

Adjustments to reconcile to cash provided by operations: | | | | | | | |

Discontinued operations: | | | | | | | |

Gain on dispositions | | (19 | ) | | | (48 | ) |

Depreciation | | 2 | | | | 11 | |

Depreciation and amortization | | 349 | | | | 301 | |

Amortization of financing costs, discounts and premiums, net | | 14 | | | | 11 | |

Stock compensation expense | | 8 | | | | 8 | |

Deferred income taxes | | (1 | ) | | | (4 | ) |

Net gain on property transactions and other | | (32 | ) | | | (2 | ) |

(Gain) loss on foreign currency transactions and derivatives | | (3 | ) | | | 1 | |

Non-cash loss on extinguishment of debt | | 12 | | | | 4 | |

Equity in earnings of affiliates | | (4 | ) | | | (3 | ) |

Change in due from managers | | (55 | ) | | | (42 | ) |

Changes in other assets | | 34 | | | | 12 | |

Changes in other liabilities | | (26 | ) | | | (30 | ) |

Cash provided by operations | | 460 | | | | 302 | |

| | | | | | | |

INVESTING ACTIVITIES | | | | | | | |

Proceeds from sales of assets, net | | 446 | | | | 108 | |

Acquisitions | | (139 | ) | | | (18 | ) |

Advances to and investments in affiliates | | (50 | ) | | | (20 | ) |

Capital expenditures: | | | | | | | |

Renewals and replacements | | (163 | ) | | | (179 | ) |

Redevelopment and acquisition-related investments | | (69 | ) | | | (162 | ) |

New development | | (11 | ) | | | — | |

Change in furniture, fixtures and equipment (“FF&E”) replacement fund | | (39 | ) | | | (2 | ) |

Property insurance proceeds | | — | | | | 4 | |

Cash used in investing activities | | (25 | ) | | | (269 | ) |

| | | | | | | |

FINANCING ACTIVITIES | | | | | | | |

Financing costs | | (4 | ) | | | (7 | ) |

Issuances of debt | | 400 | | | | 450 | |

Draws on credit facility | | 148 | | | | 22 | |

Repayment on credit facility | | (200 | ) | | | — | |

Repurchase/redemption of senior notes | | (601 | ) | | | (893 | ) |

Mortgage debt prepayments and scheduled maturities | | (246 | ) | | | (113 | ) |

Scheduled principal repayments | | (1 | ) | | | (2 | ) |

Issuance of common OP units | | 192 | | | | 222 | |

Distributions on common OP units | | (142 | ) | | | (79 | ) |

Contributions from non-controlling interests | | 3 | | | | 1 | |

Distributions to non-controlling interests | | (4 | ) | | | (3 | ) |

Change in restricted cash for financing activities | | 1 | | | | 8 | |

Cash used in financing activities | | (454 | ) | | | (394 | ) |

DECREASE IN CASH AND CASH EQUIVALENTS | | (19 | ) | | | (361 | ) |

CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | | 417 | | | | 826 | |

Effects of exchange rate changes on cash held | | (5 | ) | | | — | |

CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | 393 | | | $ | 465 | |

See notes to condensed consolidated statements.

9

HOST HOTELS & RESORTS, L.P. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Year-to-date ended June 30, 2013 and June 15, 2012

(unaudited)

Supplemental disclosure of cash flow information (in millions):

| | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | |

| Interest paid – periodic interest expense | $ | 148 | | | $ | 160 | |

| Interest paid – debt extinguishments | | 20 | | | | 9 | |

| Total interest paid | $ | 168 | | | $ | 169 | |

| Income taxes paid | $ | 6 | | | $ | 8 | |

Supplemental disclosure of noncash investing and financing activities:

For the year-to-date periods ended June 30, 2013 and June 15, 2012, limited partners converted OP units valued at approximately $2 million and $8 million, respectively, in exchange for approximately 0.1 million and 0.5 million shares, respectively, of Host Inc. common stock.

In March 2013, holders of approximately $174 million of the 3.25% exchangeable debentures elected to exchange their debentures for approximately 11.7 million shares of Host Inc. common stock. In connection with the debentures exchanged for Host Inc. common stock, Host L.P. issued 11.5 million common OP units.

See notes to condensed consolidated statements.

10

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Description of Business

Host Hotels & Resorts, Inc. operates as a self-managed and self-administered real estate investment trust (“REIT”), with its operations conducted solely through Host Hotels & Resorts, L.P. and its subsidiaries. Host Hotels & Resorts, L.P., a Delaware limited partnership, operates through an umbrella partnership structure, with Host Hotels & Resorts, Inc., a Maryland corporation, as its sole general partner. In the notes to the condensed consolidated financial statements, we use the terms “we” or “our” to refer to Host Hotels & Resorts, Inc. and Host Hotels & Resorts, L.P. together, unless the context indicates otherwise. We also use the term “Host Inc.” specifically to refer to Host Hotels & Resorts, Inc. and the term “Host L.P.” specifically to refer to Host Hotels & Resorts, L.P. in cases where it is important to distinguish between Host Inc. and Host L.P. As of June 30, 2013, Host Inc. holds approximately 98.7% of Host L.P.’s OP units.

Consolidated Portfolio

As of June 30, 2013, our consolidated portfolio, primarily consisting of luxury and upper upscale hotels, is detailed below:

| Hotels |

United States | 103 |

Australia | 1 |

Brazil | 1 |

Canada | 3 |

Chile | 2 |

Mexico | 1 |

New Zealand | 7 |

Total | 118 |

Joint Ventures

We own a non-controlling interest in a joint venture in Europe (“Euro JV”) that owns hotels in two separate funds. We own a 32.1% interest in the first fund (“Euro JV Fund I”) (11 hotels) and a 33.4% interest in the second fund (“Euro JV Fund II”) (8 hotels).

As of June 30, 2013, the Euro JV owned hotels located in the following countries:

| Hotels |

Belgium | 3 |

France | 5 |

Germany | 1 |

Italy | 3 |

Poland | 1 |

Spain | 2 |

The Netherlands | 2 |

United Kingdom | 2 |

Total | 19 |

On April 17, 2013 and June 25, 2013, the Euro JV partners executed amendments of the Euro JV partnership agreement in order to provide the funds necessary for a €95 million principal reduction associated with the refinancing of a mortgage loan secured by a portfolio of five properties, as well as to provide funds for general joint venture purposes and to extend the commitment period of the Euro JV Fund II by one year to June 2014 through the exercise of the extension option. We contributed €37 million ($48 million) to the Euro JV to facilitate these transactions.

In addition, our joint venture in Asia (“Asia/Pacific JV”), in which we own a 25% non-controlling interest, owns one hotel in Australia and a non-controlling interest in an entity with two hotels in India.

11

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Change in Reporting Periods

Effective January 1, 2013, we report quarterly operating results on a calendar cycle, which now is consistent across all of our hotel managers and the majority of companies in the lodging industry. Historically, our annual financial statements have been reported on a calendar basis and are unaffected by this change. However, our quarterly operating results had been reported based on a 52-53 week fiscal calendar used by Marriott International, Inc. (“Marriott”), the manager of approximately 50% of our properties. For 2013, Marriott converted to reporting results based on a 12-month calendar year. During 2012, Marriott used a fiscal year ending on the Friday closest to December 31 and reported twelve weeks of operations for the first three quarters and sixteen weeks for the fourth quarter of the year for its Marriott-managed hotels. Accordingly, our first three quarters of operations in 2012 ended on March 23, June 15 and September 7. In contrast, managers of our other hotels, such as Ritz-Carlton, Hyatt, and Starwood, reported results on a monthly basis. During 2012, we did not report the month of operations that ended after our fiscal quarter until the following quarter for those hotels using a monthly reporting period because these hotel managers did not make mid-month results available to us. Accordingly, the month of operations that ended after our fiscal quarter was included in our quarterly results of operations in the following quarter for those calendar reporting hotel managers. As a result, our 2012 quarterly results of operations include results from hotel managers reporting results on a monthly basis as follows: first quarter (January, February), second quarter (March to May), third quarter (June to August) and fourth quarter (September to December).

We will not restate the previously filed 2012 quarterly financial statements prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) because certain property-level operating expenses for our Marriott-managed properties necessary to restate operations are unavailable on a daily basis. Because we rely upon our operators for the hotel operating results used in our financial statements, the unavailability of this information on a calendar quarter basis for 2012 made restating our financial statements in accordance with GAAP unfeasible. Accordingly, the corresponding 2012 quarterly historical operating results are not comparable to our 2013 quarterly results.

2. | Summary of Significant Accounting Policies |

We have condensed or omitted certain information and footnote disclosures normally included in financial statements presented in accordance with GAAP in the accompanying unaudited condensed consolidated financial statements. We believe the disclosures made herein are adequate to prevent the information presented from being misleading. However, the unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10–K for the year ended December 31, 2012.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

In our opinion, the accompanying unaudited condensed consolidated financial statements reflect all adjustments necessary to present fairly our financial position as of June 30, 2013, and the results of our operations for the quarter and year-to-date periods ended June 30, 2013 and June 15, 2012, respectively, and cash flows for the year-to-date periods ended June 30, 2013 and June 15, 2012. Interim results are not necessarily indicative of full year performance because of the impact of seasonal and short-term variations.

12

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

3. | Earnings Per Common Share (Unit) |

Host Inc. Earnings Per Common Share

Basic earnings per common share is computed by dividing net income available to common stockholders by the weighted average number of shares of Host Inc. common stock outstanding. Diluted earnings per common share is computed by dividing net income available to common stockholders, as adjusted for potentially dilutive securities, by the weighted average number of shares of Host Inc. common stock outstanding plus other potentially dilutive securities. Dilutive securities may include shares granted under comprehensive stock plans, other non-controlling interests that have the option to convert their limited partnership interests to common OP units and convertible debt securities. No effect is shown for any securities that are anti-dilutive. The calculation of basic and diluted earnings per common share is shown below (in millions, except per share amounts):

| | Quarter ended | | | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| Net income | $ | 121 | | | $ | 83 | | | $ | 181 | | | $ | 83 | |

| Less: Net income attributable to non-controlling interests | | (2 | ) | | | (1 | ) | | | (6 | ) | | | (3 | ) |

| Net income attributable to Host Inc. | $ | 119 | | | $ | 82 | | | $ | 175 | | | $ | 80 | |

| Diluted income attributable to Host Inc. | $ | 119 | | | $ | 83 | | | $ | 175 | | | $ | 80 | |

| | | | | | | | | | | | | | | | |

| Basic weighted average shares outstanding | | 745.2 | | | | 718.1 | | | | 736.8 | | | | 712.8 | |

| Diluted weighted average shares outstanding (a) | | 745.9 | | | | 730.6 | | | | 742.4 | | | | 713.8 | |

| | | | | | | | | | | | | | | | |

| Basic earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

| Diluted earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

(a) | There were approximately29 million for both the quarter and year-to-date periods ended June 30, 2013 and approximately 29 million and 40 million for the quarter and year-to-date periods June 15, 2012, respectively, potentially dilutive shares for our exchangeable senior debentures, which shares were not included in the computation of diluted EPS because to do so would have been anti-dilutive for the period. |

13

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Host L.P. Earnings Per Common Unit

Basic earnings per common unit is computed by dividing net income available to common unitholders by the weighted average number of common units outstanding. Diluted earnings per common unit is computed by dividing net income available to common unitholders, as adjusted for potentially dilutive securities, by the weighted average number of common units outstanding plus other potentially dilutive securities. Dilutive securities may include units issued to Host Inc. to support Host Inc. common shares granted under comprehensive stock plans, other non-controlling interests that have the option to convert their limited partnership interests to common OP units and convertible debt securities. No effect is shown for any securities that are anti-dilutive. The calculation of basic and diluted earnings per unit is shown below (in millions, except per unit amounts):

| | Quarter ended | | | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| Net income | $ | 121 | | | $ | 83 | | | $ | 181 | | | $ | 83 | |

| Less: Net income attributable to non-controlling interests | | (1 | ) | | | — | | | | (4 | ) | | | (2 | ) |

| Net income attributable to Host L.P. | $ | 120 | | | $ | 83 | | | $ | 177 | | | $ | 81 | |

| Diluted income attributable to Host L.P. | $ | 120 | | | $ | 84 | | | $ | 177 | | | $ | 81 | |

| | | | | | | | | | | | | | | | |

| Basic weighted average units outstanding | | 739.3 | | | | 713.1 | | | | 731.1 | | | | 708.1 | |

| Diluted weighted average units outstanding (a) | | 740.0 | | | | 725.4 | | | | 736.5 | | | | 709.1 | |

| | | | | | | | | | | | | | | | |

| Basic earnings per common unit | $ | .16 | | | $ | .12 | | | $ | .24 | | | $ | .11 | |

| Diluted earnings per common unit | $ | .16 | | | $ | .12 | | | $ | .24 | | | $ | .11 | |

(a) | There were approximately29 million for both the quarter and year-to-date periods ended June 30, 2013 and approximately 28 million and 39 million for the quarter and year-to-date ended June 15, 2012, respectively, potentially dilutive units for our exchangeable senior debentures, which units were not included in the computation of diluted earnings per unit because to do so would have been anti-dilutive for the period. |

Property and equipment consists of the following (in millions):

| | June 30,

2013 | | | December 31,

2012 | |

| Land and land improvements | $ | 1,939 | | | $ | 1,996 | |

| Buildings and leasehold improvements | | 13,483 | | | | 13,665 | |

| Furniture and equipment | | 2,212 | | | | 2,227 | |

| Construction in progress | | 163 | | | | 199 | |

| | | 17,797 | | | | 18,087 | |

| Less accumulated depreciation and amortization | | (6,596 | ) | | | (6,499 | ) |

| | $ | 11,201 | | | $ | 11,588 | |

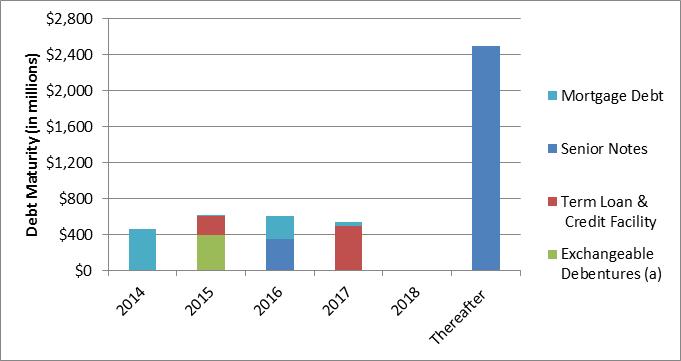

Senior notes. In May 2013, we redeemed the $400 million of 9% Series T senior notes due 2017 for an aggregate price of $418 million with proceeds from the $400 million 3 3∕4% Series D senior notes due October of 2023 that were issued in March 2013 and with available cash.

Also, in May 2013, we called $200 million of our 6 3∕4% Series Q senior notes due 2016 and redeemed them for an aggregate price of $202 million in June 2013. To facilitate this transaction, we drew $100 million on the revolver portion of the credit facility and repaid such draw later in the quarter.

Credit facility. In April and May 2013, we drew €3.4 million ($4.4 million) and €33.4 million ($43.2 million), respectively, under the credit facility to fund our contribution to the Euro JV for our share of the paydown related to the

14

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

refinancing of a mortgage loan. See Note 1 for additional information. As of June 30, 2013, we have $798 million of available capacity under the revolver portion of our credit facility.

Mortgage debt.On May 1, 2013, we repaid the 4.75%, $246 million mortgage loan on the Orlando World Center Marriott.

6. | Equity of Host Inc. and Capital of Host L.P. |

Equity of Host Inc.

Equity of Host Inc. is allocated between controlling and non-controlling interests as follows (in millions):

| | Equity of Host Inc. | | | Non-redeemable

non-controlling

interests | | | Total equity | | | Redeemable

non-

controlling

interests | |

| Balance, December 31, 2012 | $ | 6,825 | | | $ | 34 | | | $ | 6,859 | | | $ | 158 | |

| Net income | | 175 | | | | 4 | | | | 179 | | | | 2 | |

| Issuance of common stock | | 370 | | | | — | | | | 370 | | | | — | |

| Dividends declared on common stock | | (157 | ) | | | — | | | | (157 | ) | | | — | |

| Distributions to non-controlling interests | | — | | | | (4 | ) | | | (4 | ) | | | (2 | ) |

| Other changes in ownership | | (10 | ) | | | 1 | | | | (9 | ) | | | 10 | |

| Other comprehensive loss | | (24 | ) | | | — | | | | (24 | ) | | | — | |

| Balance, June 30, 2013 | $ | 7,179 | | | $ | 35 | | | $ | 7,214 | | | $ | 168 | |

Capital of Host L.P.

As of June 30, 2013, Host Inc. is the owner of approximately 98.7% of Host L.P.’s common OP units. The remaining 1.3% of the common OP units are held by third party limited partners. Each OP unit may be redeemed for cash or, at the election of Host Inc., Host Inc. common stock, based on the conversion ratio of 1.021494 shares of Host Inc. common stock for each OP unit.

In exchange for any shares issued by Host Inc., Host L.P. will issue OP units to Host Inc. based on the applicable conversion ratio. Additionally, funds used by Host Inc. to pay dividends on its common stock are provided by distributions from Host L.P.

Capital of Host L.P. is allocated between controlling and non-controlling interests as follows (in millions):

| | Capital of

Host L.P. | | | Non-controlling

interests | | | Total

Capital | | | Limited

Partnership

Interests of

Third Parties | |

| Balance, December 31, 2012 | $ | 6,825 | | | $ | 34 | | | $ | 6,859 | | | $ | 158 | |

| Net income | | 175 | | | | 4 | | | | 179 | | | | 2 | |

| Issuance of common OP units | | 370 | | | | — | | | | 370 | | | | — | |

| Distributions declared on common OP units | | (157 | ) | | | — | | | | (157 | ) | | | (2 | ) |

| Distributions to non-controlling interests | | — | | | | (4 | ) | | | (4 | ) | | | — | |

| Other changes in ownership | | (10 | ) | | | 1 | | | | (9 | ) | | | 10 | |

| Other comprehensive loss | | (24 | ) | | | — | | | | (24 | ) | | | — | |

| Balance, June 30, 2013 | $ | 7,179 | | | $ | 35 | | | $ | 7,214 | | | $ | 168 | |

For Host Inc. and Host L.P., there were no material amounts reclassified out of accumulated other comprehensive income (loss) to net income.

15

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Issuance of Common Stock

During the second quarter of 2013, Host Inc. issued 4.8 million shares of common stock, at an average price of $18.31 per share, for net proceeds of approximately $87 million. These issuances were made in “at-the-market” offerings pursuant to Sales Agency Financing Agreements with BNY Mellon Capital Markets, LLC and Scotia Capital (USA) Inc. In connection with the common stock issuance, Host L.P. issued 4.7 million common OP units. There is approximately $110 million of issuance capacity remaining under the current agreements. Year-to-date, we have issued 10.9 million shares of common stock, at an average price of $17.45 per share, for net proceeds of approximately $188 million. For year-to-date, Host L.P. has issued 10.7 million common OP units in connection with these issuances.

Dividends/Distributions

On June 17, 2013, Host Inc.’s Board of Directors declared a regular dividend of $0.11 per share on its common stock. The dividend was paid on July 15, 2013 to stockholders of record as of June 28, 2013. Accordingly, Host L.P. made a distribution of $.11236434 per unit on its common OP units based on the current conversion ratio.

On May 31, 2013, we acquired the 426-room Hyatt Place Waikiki Beach in Honolulu, Hawaii for approximately $138.5 million. In connection with the acquisition, we incurred $1 million of acquisition costs and acquired a $0.5 million FF&E replacement fund.

Accounting for the acquisition of a hotel property or other entity as a purchase transaction requires an allocation of the purchase price to the assets acquired and the liabilities assumed in the transaction at their respective estimated fair values. The purchase price allocations are estimated based on current available information; however, we still are in the process of obtaining appraisals and finalizing the accounting for this acquisition.

The following table summarizes the estimated fair value of the assets acquired and liabilities assumed related to this acquisition (in millions):

Property and equipment | $ | 138 | |

Restricted cash, FF&E reserves and other assets | | 1 | |

Total net assets acquired | $ | 139 | |

16

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Our summarized unaudited consolidated pro forma results of operations, assuming the acquisition completed during 2013 occurred on January 1, 2012, are as follows (in millions, except per share and per unit amounts):

| | Quarter ended | | | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| Revenues | $ | 1,424 | | | $ | 1,329 | | | $ | 2,673 | | | $ | 2,274 | |

| Income from continuing operations | | 120 | | | | 79 | | | | 156 | | | | 23 | |

| Net income | | 122 | | | | 82 | | | | 183 | | | | 81 | |

| | | | | | | | | | | | | | | | |

| Host Inc.: | | | | | | | | | | | | | | | |

| Net income attributable to Host Inc. | $ | 120 | | | $ | 81 | | | $ | 177 | | | $ | 78 | |

| | | | | | | | | | | | | | | | |

| Basic earnings per common share: | | | | | | | | | | | | | | | |

| Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

| Discontinued operations | | — | | | | — | | | | .04 | | | | .08 | |

| Basic earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

| | | | | | | | | | | | | | | | |

| Diluted earnings per common share: | | | | | | | | | | | | | | | |

| Continuing operations | $ | .16 | | | $ | .11 | | | $ | .20 | | | $ | .03 | |

| Discontinued operations | | — | | | | — | | | | .04 | | | | .08 | |

| Diluted earnings per common share | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

| | | | | | | | | | | | | | | | |

| Host L.P.: | | | | | | | | | | | | | | | |

| Net income attributable to Host L.P. | $ | 121 | | | $ | 82 | | | $ | 179 | | | $ | 79 | |

| | | | | | | | | | | | | | | | |

| Basic earnings per common unit: | | | | | | | | | | | | | | | |

| Continuing operations | $ | .16 | | | $ | .10 | | | $ | .20 | | | $ | .03 | |

| Discontinued operations | | — | | | | .01 | | | | .04 | | | | .08 | |

| Basic earnings per common unit | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

| | | | | | | | | | | | | | | | |

| Diluted earnings per common unit: | | | | | | | | | | | | | | | |

| Continuing operations | $ | .16 | | | $ | .10 | | | $ | .20 | | | $ | .03 | |

| Discontinued operations | | — | | | | .01 | | | | .04 | | | | .08 | |

| Diluted earnings per common unit | $ | .16 | | | $ | .11 | | | $ | .24 | | | $ | .11 | |

The above pro forma results of operations exclude $1 million of acquisition costs for the quarter and year-to-date ended June 30, 2013. The condensed consolidated statements of operations for 2013 include approximately $2 million of revenues and $1 million of net income for both the quarter and year-to-date, respectively, related to our 2013 acquisition.

During 2013, we disposed of (i) The Ritz-Carlton, San Francisco for approximately $161 million in the second quarter and (ii) the Atlanta Marriott Marquis for $293 million in the first quarter. During 2012, we disposed of three properties.

17

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table summarizes revenues, income before income taxes, and the gain on disposition of the hotels which have been included in discontinued operations for all periods presented (in millions):

| | Quarter ended | | | Year-to-date ended | |

| | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| Revenues | $ | 15 | | | $ | 44 | | | $ | 31 | | | $ | 96 | |

| Income before income taxes | | 2 | | | | 3 | | | | 13 | | | | 9 | |

| Gain on disposition | | — | | | | — | | | | 19 | | | | 48 | |

We have recorded a deferred gain on the sale of The Ritz-Carlton, San Francisco of approximately $25 million, $14 million of which will be recognized upon completion of certain post-closing conditions. The remainder of the deferred gain is subject to performance guarantees through which we have guaranteed certain annual net operating profit levels for the hotel through 2016, with a maximum payment of $4 million per year, not to exceed $11 million in total.

9. | Fair Value Measurements |

The following tables detail the fair value of our financial assets and liabilities that are required to be measured at fair value on a recurring basis, as well as non-recurring fair value measurements, at June 30, 2013 and December 31, 2012, respectively (in millions):

| | | | | Fair Value at Measurement Date Using | |

| | Balance at

June 30,

2013 | | | Quoted Prices

in Active

Markets for

Identical Assets

(Level 1) | | | Significant

Other

Observable

Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | |

| Fair Value Measurements on a Recurring Basis: | | | | | | | | | | | | | | | |

| Assets | | | | | | | | | | | | | | | |

| Interest rate swap derivatives (a) | $ | 4 | | | $ | — | | | $ | 4 | | | $ | — | |

| Forward currency sale contracts (a) | | 7 | | | | — | | | | 7 | | | | — | |

| Liabilities | | | | | | | | | | | | | | | |

| Interest rate swap derivatives (a) | | (4 | ) | | | — | | | | (4 | ) | | | — | |

| | | | | | | | | | | | | | | | |

| | | | | Fair Value at Measurement Date Using | |

| | Balance at

December 31,

2012 | | | Quoted Prices

in Active

Markets for

Identical Assets

(Level 1) | | | Significant

Other

Observable

Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | |

| | | | | | | | | | | | | | | | |

| Fair Value Measurements on a Recurring Basis: | | | | | | | | | | | | | | | |

| Assets | | | | | | | | | | | | | | | |

| Interest rate swap derivatives (a) | $ | 7 | | | $ | — | | | $ | 7 | | | $ | — | |

| Forward currency sale contract (a) | | 5 | | | | — | | | | 5 | | | | — | |

| Liabilities | | | | | | | | | | | | | | | |

| Interest rate swap derivatives (a) | | (6 | ) | | | — | | | | (6 | ) | | | — | |

| | | | | | | | | | | | | | | | |

| Fair Value Measurements on a Non-recurring Basis: | | | | | | | | | | | | | | | |

| Impaired hotel properties held and used (b) | | 34 | | | | — | | | | — | | | | 34 | |

(a) | These derivative contracts have been designated as hedging instruments. |

(b) | The fair value measurements are as of the measurement date of the impairment and may not reflect the book value as of December 31, 2012. |

18

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Derivatives and Hedging

Interest rate swap derivatives designated as cash flow hedges.We have designated our floating-to-fixed interest rate swap derivatives as cash flow hedges. The purpose of the interest rate swaps is to hedge against changes in cash flows (interest payments) attributable to fluctuations in variable rate debt. The derivatives are valued based on the prevailing market yield curve on the date of measurement. We also evaluate counterparty credit risk when we calculate the fair value of the swaps. Changes in the fair value of the derivatives are recorded to accumulated other comprehensive income (loss) within the equity portion of our balance sheets. The hedges were fully effective as of June 30, 2013.

The following table summarizes our interest rate swap derivatives designated as cash flow hedges (in millions):

| | | | | | | | | | | | Change in Fair Value | |

| Transaction

Date | | Total

Notional

Amount | | Maturity

Date | | Swapped

Index | | All-in Rate | | | Gain (Loss)

Quarter ended | | | Gain (Loss)

Year-to-date ended | |

| | | | | | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| November 2011 (1) | | A$ | 62 | | November 2016 | | Reuters BBSY | | | 6.7 | % | | $ | — | | | $ | (3 | ) | | $ | 1 | | | $ | (2 | ) |

| February 2011 (2) | | NZ$ | 79 | | February 2016 | | NZ$ Bank Bill | | | 7.15 | % | | $ | 1 | | | $ | (1 | ) | | $ | 1 | | | $ | — | |

(1) | The swap was entered into in connection with the A$82 million ($85 million) mortgage loan on the Hilton Melbourne South Wharf. |

(2) | The swap was entered into in connection with the NZ$105 million ($87 million) mortgage loan on seven properties in New Zealand. |

Interest rate swap derivatives designated as fair value hedges.We have designated our fixed-to-floating interest rate swap derivatives as fair value hedges. We enter into these derivative instruments to hedge changes in the fair value of fixed-rate debt that occur as a result of changes in market interest rates. The derivatives are valued based on the prevailing market yield curve on the date of measurement. We also evaluate counterparty credit risk in the calculation of the fair value of the swaps. The changes in the fair value of the derivatives largely are offset by corresponding changes in the fair value of the underlying debt due to changes in the 3-month LIBOR rate, which change is recorded as an adjustment to the carrying amount of the debt. Any difference between the change in the fair value of the swap and the change in the fair value of the underlying debt, which was not significant for the periods presented, is considered the ineffective portion of the hedging relationship and is recognized in net income (loss).

We have three fixed-to-floating interest rate swap agreements for an aggregate notional amount totaling $300 million. During the quarters ended June 30, 2013 and June 15, 2012, the fair value of the swaps decreased $2 million and $1 million, respectively. During the year-to-date periods ended June 30, 2013 and June 15, 2012, the fair value of the swaps decreased $3 million and $1 million, respectively.

Foreign Investment Hedging Instruments.We have six foreign currency forward sale contracts that hedge a portion of the foreign currency exposure resulting from the eventual repatriation of our net investment in foreign operations. These derivatives are considered hedges of the foreign currency exposure of a net investment in a foreign operation and are marked-to-market with changes in fair value recorded to accumulated other comprehensive income (loss) within the equity portion of our balance sheets. The forward sale contracts are valued based on the forward yield curve of the foreign currency to U.S. dollar forward exchange rate on the date of measurement. We also evaluate counterparty credit risk when we calculate the fair value of the derivatives.

The following table summarizes our foreign currency sale contracts (in millions):

| | | | | | | | | | | Change in Fair Value | |

| | | Total

Transaction

Amount in

Foreign

Currency | | | Total

Transaction

Amount

in Dollars | | | | | Gain (Loss)

Quarter ended | | | Gain (Loss)

Year-to-date ended | |

| Transaction

Date Range | | | | Forward

Purchase

Date Range | | June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| May 2008-January 2013 | | € | 120 | | | $ | 163 | | | May 2014-January 2016 | | $ | (2 | ) | | $ | 5 | | | $ | 1 | | | $ | 3 | |

| July 2011 | | NZ$ | 30 | | | $ | 25 | | | August 2013 | | $ | 2 | | | $ | — | | | $ | 1 | | | $ | (1 | ) |

In addition to the forward sale contracts, we have designated a portion of the foreign currency draws on our credit facility as hedges of net investments in foreign operations. Changes in fair value in the designated credit facility draws are recorded to accumulated other comprehensive income (loss) within the equity portion of our balance sheets.

19

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table summarizes the draws on our credit facility that are designated as hedges of net investments in international operations:

| Currency | | Balance

Outstanding

US$ | | | Balance

Outstanding in

Foreign Currency | | | Gain (Loss)

Quarter ended | | | Gain (Loss)

Year-to-date ended | |

| June 30,

2013 | | | June 15,

2012 | | | June 30,

2013 | | | June 15,

2012 | |

| Canadian dollars (1) | | $ | 30 | | | C$ | 31 | | | $ | 1 | | | $ | — | | | $ | 2 | | | $ | — | |

| Australian dollars | | $ | 6 | | | A$ | 7 | | | $ | 1 | | | $ | — | | | $ | 1 | | | $ | — | |

| Euros | | $ | 76 | | | € | 59 | | | $ | (1 | ) | | $ | — | | | $ | — | | | $ | — | |

(1) | We have an additional $72 million outstanding on the credit facility in Canadian dollars that has not been designated as a hedging instrument. |

Other Liabilities

Fair Value of Other Financial Liabilities.We did not elect the fair value measurement option for any of our other financial liabilities. Valuations for secured debt and our credit facility are determined based on the expected future payments discounted at risk-adjusted rates. Senior Notes and the Exchangeable Senior Debentures are valued based on quoted market prices. The fair values of financial instruments not included in this table are estimated to be equal to their carrying amounts.

The fair value of certain financial liabilities are shown below (in millions):

| | June 30,

2013 | | | December 31,

2012 | |

| | Carrying

Amount | | | Fair

Value | | | Carrying

Amount | | | Fair

Value | |

| Financial liabilities | | | | | | | | | | | | | | | |

| Senior notes (Level 1) | $ | 2,847 | | | $ | 2,946 | | | $ | 3,038 | | | $ | 3,296 | |

| Exchangeable Senior Debentures (Level 1) | | 363 | | | | 543 | | | | 531 | | | | 725 | |

| Credit facility (Level 2) | | 702 | | | | 702 | | | | 763 | | | | 763 | |

| Mortgage debt and other, net of capital leases (Level 2) | | 811 | | | | 824 | | | | 1,078 | | | | 1,094 | |

10. | Geographic Information |

We consider each of our hotels to be an operating segment, none of which meets the threshold for a reportable segment. We also allocate resources and assess operating performance based on individual hotels. All of our other real estate investment activities (primarily our office buildings) are immaterial and, with our operating segments, meet the aggregation criteria, and thus, we report one segment: hotel ownership. Our consolidated international operations consist of hotels in six countries. There were no intersegment sales during the periods presented.

20

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table presents total revenues and property and equipment for each of the geographical areas in which we operate (in millions):

| | Revenues | | | Property and equipment, net | |

| | Quarter ended | | | Year-to-date ended | | | | |

| | June 30, 2013 | | | June 15, 2012 | | | June 30, 2013 | | | June 15, 2012 | | | June 30, 2013 | | | December 31, 2012 | |

| United States | $ | 1,353 | | | $ | 1,259 | | | $ | 2,531 | | | $ | 2,161 | | | $ | 10,741 | | | $ | 11,095 | |

| Australia | | 10 | | | | 10 | | | | 20 | | | | 16 | | | | 114 | | | | 133 | |

| Brazil | | 8 | | | | 8 | | | | 15 | | | | 14 | | | | 36 | | | | 39 | |

| Canada | | 26 | | | | 23 | | | | 47 | | | | 40 | | | | 89 | | | | 97 | |

| Chile | | 8 | | | | 11 | | | | 17 | | | | 15 | | | | 57 | | | | 63 | |

| Mexico | | 5 | | | | 6 | | | | 11 | | | | 10 | | | | 32 | | | | 26 | |

| New Zealand | | 10 | | | | 9 | | | | 22 | | | | 14 | | | | 132 | | | | 135 | |

| Total | $ | 1,420 | | | $ | 1,326 | | | $ | 2,663 | | | $ | 2,270 | | | $ | 11,201 | | | $ | 11,588 | |

11. | Non-controlling Interests |

Other Consolidated Partnerships.We consolidate five majority-owned partnerships that have third-party, non-controlling ownership interests. The third-party partnership interests are included in non-controlling interests — other consolidated partnerships on the condensed consolidated balance sheets and totaled $35 million and $34 million as of June 30, 2013 and December 31, 2012, respectively. Three of the partnerships have finite lives that terminate between 2081 and 2095, and the associated non-controlling interests are mandatorily redeemable at our option at the end of, but not prior to, the finite life. At June 30, 2013 and December 31, 2012, the fair values of the non-controlling interests in the partnerships with finite lives were approximately $69 million and approximately $65 million, respectively.

Net income attributable to non-controlling interests of consolidated partnerships is included in our determination of net income. Net income attributable to non-controlling interests of third parties, which is included in the determination of net income attributable to Host Inc. and Host L.P., was $1 million for the quarter ended June 30, 2013, and immaterial for the quarter ended June 15, 2012. Net income attributable to non-controlling interests of third parties was $4 million and $2 million for the year-to-date periods ended June 30, 2013 and June 15, 2012, respectively

Host Inc.’s treatment of the non-controlling interests of Host L.P.: Host Inc. adjusts the non-controlling interests of Host L.P. each period so that the amount presented equals the greater of its carrying value based on the accumulated historical cost or its redemption value. The historical cost is based on the proportional relationship between the historical cost of equity held by our common stockholders relative to that of the unitholders of Host L.P. The redemption value is based on the amount of cash or Host Inc. common stock, at our option, that would be paid to the non-controlling interests of Host L.P. if it were terminated. Therefore, the redemption value of the common OP units is equivalent to the number of shares issuable upon conversion of the common OP units held by third parties valued at the market price of Host Inc. common stock at the balance sheet date. One common OP unit may be exchanged into 1.021494 shares of Host Inc. common stock. Non-controlling interests of Host L.P. are classified in the mezzanine section of the balance sheet as they do not meet the requirements for equity classification because the redemption feature requires the delivery of registered shares.

The table below details the historical cost and redemption values for the non-controlling interests:

| | June 30, 2013 | | | December 31, 2012 | |

| OP units outstanding (millions) | | 9.8 | | | | 9.9 | |

| Market price per Host Inc. common share | $ | 16.87 | | | $ | 15.67 | |

| Shares issuable upon conversion of one OP unit | | 1.021494 | | | | 1.021494 | |

| Redemption value (millions) | $ | 168 | | | $ | 158 | |

| Historical cost (millions) | $ | 97 | | | $ | 96 | |

| Book value (millions) (a) | $ | 168 | | | $ | 158 | |

(a) | The book value recorded is equal to the greater of redemption value or historical cost. |

21

HOST HOTELS & RESORTS, INC., HOST HOTELS & RESORTS, L.P., AND SUBSIDIARIES

NOTES TO CONDENSEDCONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Net income is allocated to the non-controlling interests of Host L.P. based on their weighted average ownership interest during the period. Net income attributable to Host Inc. has been reduced by the amount attributable to non-controlling interests in Host L.P. The income attributable to the non-controlling interests of Host L.P. for the quarter and year-to-date ended June 30, 2013 was $1 million and $2 million, respectively, and was $1 million for both the quarter and year-to-date ended June 15, 2012.

We are involved in various legal proceedings in the normal course of business regarding the operation of our hotels and company matters. To the extent not covered by insurance, these legal proceedings generally fall into the following broad categories: disputes involving hotel-level contracts, employment litigation, compliance with laws such as the Americans with Disabilities Act, tax disputes and other general matters. Under our management agreements, our operators have broad latitude to resolve individual hotel-level claims for amounts generally less than $150,000. However, for matters exceeding such threshold, our operators may not settle claims without our consent.

Excluding the San Antonio litigation discussed below, based on our analysis of legal proceedings with which we currently are involved or of which we are aware and our experience in resolving similar claims in the past, we have accrued approximately $11 million as of June 30, 2013 and estimate that, in the aggregate, our losses related to these proceedings could be as much as $53 million. We believe this range represents the maximum potential loss for all of our legal proceedings. We are not aware of any other matters with a reasonably possible unfavorable outcome for which disclosure of a loss contingency is required. No assurances can be given as to the outcome of any pending legal proceedings.

We also have accrued a loss contingency of approximately $67 million, which includes $8 million in the second quarter, related to the litigation concerning the ground lease for the San Antonio Marriott Rivercenter. On June 28, 2013, the Texas Supreme Court issued an order denying our Petition for Review. The Court’s procedures provide for the right to seek rehearing of such an order, and we intend to exercise that right. No assurances can be given as to the outcome of this appeal. In relation to this legal proceeding, we previously funded a court-ordered $25 million escrow reserve, which is included in restricted cash. For further detail on this legal proceeding, see Part II, Item 1, Legal Proceedings of this filing and Part I, Item 3, Legal Proceedings, of our Annual Report on Form 10-K for the year ended December 31, 2012.

22

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with the unaudited condensed consolidated financial statements and related notes included elsewhere in this report. Host Inc. operates as a self-managed and self-administered REIT. Host Inc. is the sole general partner of Host L.P. and holds 98.7% of its partnership interests. Host L.P. is a limited partnership operating through an umbrella partnership structure. The remaining approximately 1.3% of Host L.P.’s common OP units are owned by various unaffiliated limited partners.

Change in Reporting Periods

Effective January 1, 2013, we report quarterly operating results on a calendar cycle, which now is consistent across all of our hotel managers and the majority of companies in the lodging industry. Historically, our annual financial statements have been reported on a calendar basis and are unaffected by this change. However, our quarterly operating results have been reported based on a 52-53 week fiscal calendar used by Marriott International, Inc. (“Marriott”), the manager of approximately 50% of our properties. For 2013, Marriott converted to reporting results based on a 12-month calendar year. During 2012, Marriott used a fiscal year ending on the Friday closest to December 31 and reported twelve weeks of operations for the first three quarters and sixteen weeks for the fourth quarter of the year for its Marriott-managed hotels. Accordingly, our first three quarters of operations in 2012 ended on March 23, June 15 and September 7. In contrast, managers of our other hotels, such as Ritz-Carlton, Hyatt, and Starwood, reported results on a monthly basis. During 2012, we did not report the month of operations that ended after our fiscal quarter until the following quarter for those hotels using a monthly reporting period because these hotel managers did not make mid-month results available to us. Accordingly, the month of operations that ended after our fiscal quarter was included in our quarterly results of operations in the following quarter for those calendar reporting hotel managers. As a result, our 2012 quarterly results of operations include results from hotel managers reporting results on a monthly basis as follows: first quarter (January, February), second quarter (March to May), third quarter (June to August) and fourth quarter (September to December).

We will not restate the previously filed 2012 quarterly financial statements, which are prepared in accordance with GAAP because certain property-level operating expenses for our Marriott-managed properties necessary to restate operations are unavailable on a daily basis. Because we rely upon our operators for the hotel operating results used in our financial statements, the unavailability of this information on a calendar quarter basis for 2012 made restating our financial statements in accordance with GAAP unfeasible. Accordingly, the corresponding 2012 quarterly historical operating results are not comparable to our 2013 quarterly results.

However, to enable investors to better evaluate our performance over comparable periods, we have presented certain 2012 quarterly results and operating statistics on a calendar year basis of reporting, which we will refer to as “2012 As Adjusted” results. The financial information for the 2012 As Adjusted periods presented herein was calculated based on our actual reported operating results for the quarter and year-to-date periods ended June 15, 2012, adjusted as follows:

• | Our 59 hotels operated by Marriott traditionallyhave reported operations on the basis of a 52-53 week fiscal calendar. For the second quarter, operations from March 24, 2012 through June 15, 2012 were included. Based on daily revenue information provided by Marriott, our 2012 second quarter As Reported results for these properties were adjusted to include $101 million of revenue for the 15 days from June 16, 2012 through June 30, 2012 (that previously were included in our results of operations for the third quarter 2012) and to exclude $60 million of revenues for the eight days from March 24, 2012 through March 31, 2012 to determine the 2012 As Adjusted second quarter revenues. Our 2012 As Adjusted year-to-date revenues have been adjusted to include the same 15 days of revenues from June 16, 2012 through June 30, 2012. |

• | Because Marriott is unable to provide us with operating expenses for our Marriott-operated hotels on a daily basis, we derived estimated expenses based on an internally developed allocation methodology based on historical expenses provided by Marriott consistent with its prior 52-53 week reporting calendar. Our 2012 second quarter As Reported operating expenses were adjusted to include approximately $77 million of estimated expenses incurred from June 16, 2012 through June 30, 2012 and to exclude approximately $43 million of operating expenses for the period from March 24, 2012 through March 31, 2012 to determine the 2012 As Adjusted second quarter expenses. Our 2012 As Adjusted year-to-date expenses have also been adjusted to include the 15 days from June 16, 2012 through June 30, 2012. |

• | For our 57 hotels operated by managers other than Marriott (including those by Ritz-Carlton, Hyatt and Starwood) that traditionally have reported operations on a calendar month basis, our 2012 As Adjusted quarter results include $210 million of revenues and $154 million of operating expenses for these hotels for the full calendar month of June 2012 that previously were included in our results of operations for the third quarter 2012 and excluded $226 million of revenues and $163 million of operating expenses for these hotels for the full calendar month of March 2012, which were included in our first quarter “As Adjusted” results. Our 2012 As adjusted year-to-date results have also been adjusted to include the full calendar month of June 2012 for these hotels. |

23