Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. 1)

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| x | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| ¨ | Definitive Additional Materials | |

| ¨ | Soliciting Material under § 240.14a-12 | |

Jacksonville Bancorp, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| ||||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| ||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| ||||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| ||||

| (5) | Total fee paid: | |||

| ||||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| ||||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| ||||

| (3) | Filing Party:

| |||

| ||||

| (4) | Date Filed:

| |||

| ||||

Table of Contents

January [—], 2013

Dear Shareholder:

You are cordially invited to attend the Special Meeting of Shareholders of Jacksonville Bancorp, Inc. (the “Company”), which will be held on Wednesday, February 13, 2013, beginning at 9:00 a.m., Eastern Time. The meeting will be held at the Company’s principal executive offices, 100 North Laura Street, Suite 1000, Jacksonville, Florida 32202. The purpose of the meeting is to consider and vote upon the proposals explained in the notice and the Proxy Statement.

A formal notice describing the business to come before the meeting, a Proxy Statement and a proxy card are enclosed.

Your vote is very important to us and we want your shares to be represented at the meeting.Whether or not you plan to attend the Special Meeting in person, please vote your shares immediately by telephone, by Internet or by mail. If you vote by mail, please sign, date and return the enclosed proxy card in the accompanying postage-paid envelope as promptly as possible. If you later decide to attend the Special Meeting and vote in person, or if you wish to revoke your proxy for any reason before the vote at the Special Meeting, you may do so and your proxy will have no further effect.

Thank you for taking the time to vote.

Sincerely,

Gary L. Winfield, M.D.

Chairman of the Board

Table of Contents

Jacksonville Bancorp, Inc.

100 North Laura Street, Suite 1000

Jacksonville, Florida 32202

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To the Holders of Common Stock:

Notice is hereby given that a Special Meeting of Shareholders of Jacksonville Bancorp, Inc. (the “Company”) will be held on Wednesday, February 13, 2013, at 9:00 a.m. Eastern Time, at the Company’s principal executive offices, 100 North Laura Street, Suite 1000, Jacksonville, Florida 32202, to consider and act upon the following matters:

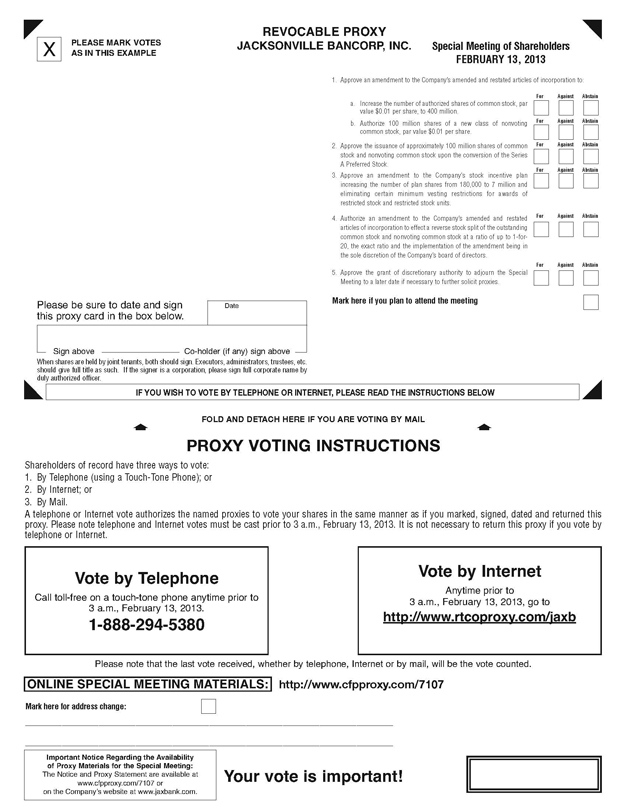

| 1. | To approve an amendment to the Company’s Amended and Restated Articles of Incorporation, as amended (the “Articles of Incorporation”) to: |

| a. | increase the number of authorized shares of the Company’s common stock, par value $0.01 per share (the “Common Stock”), to 400 million; and |

| b. | authorize 100 million shares of a new class of nonvoting common stock of the Company, par value $0.01 per share (the “Nonvoting Common Stock”); |

| 2. | To approve the issuance of an aggregate of approximately 100 million shares of Common Stock and Nonvoting Common Stock upon the conversion (the “Conversion”) of the Company’s recently issued 50,000 shares of Mandatorily Convertible, Noncumulative, Nonvoting, Perpetual Preferred Stock, Series A as described in the Proxy Statement and the Articles of Incorporation, and for purposes of NASDAQ Stock Market Rule 5635; |

| 3. | To approve an amendment to the 2008 Amendment and Restatement of the Jacksonville Bancorp, Inc. 2006 Stock Incentive Plan, as amended (the “Stock Incentive Plan”) to (i) increase the number of shares of Common Stock available for issuance under the plan from 180,000 shares to 7 million shares, and (ii) eliminate certain minimum vesting conditions for awards of restricted stock and restricted stock units; |

| 4. | To authorize an amendment to the Articles of Incorporation to effect a reverse stock split of the outstanding shares of Common Stock and Nonvoting Common Stock (if any) at a ratio of up to 1-for-20, the exact ratio and the implementation of the amendment being in the sole discretion of the Company’s board of directors; and |

| 5. | To approve the grant of discretionary authority to the persons named as proxies to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation of proxies if there are not sufficient votes at the time of the Special Meeting to approve the proposals listed above. |

These proposals are described more fully in the attached Proxy Statement. You should carefully review all of the information set forth in the attached Proxy Statement. Only shareholders of record of the Common Stock at the close of business on December 17, 2012 are entitled to receive notice of, and to vote on, the business that may come before the Special Meeting.

To avoid the unnecessary expense of further solicitation, we urge you to immediately indicate your voting instructions by telephone, by Internet or by mail. If you vote by mail, please sign, date and return the enclosed proxy card as promptly as possible in the accompanying postage-paid envelope to ensure your representation at the Special Meeting. You may revoke the proxy at any time before it is exercised by following the instructions set forth under “Voting of Proxies” on page 2 of the accompanying Proxy Statement. Please note that if you choose to vote in person at the Special Meeting and you hold your shares through a securities broker in street name, you must obtain a proxy from your broker and bring that proxy to the meeting. If you wish to attend the Special Meeting and need directions, please call us at (904) 421-3040.

Table of Contents

Each of Proposals 1a, 1b and 4, relating to amendments to the Articles of Incorporation, will be approved if shareholders holding at least a majority of the outstanding shares of Common Stock entitled to vote on such proposal vote in favor of the proposal. Each of Proposal 2 (regarding the issuance of Common Stock and Nonvoting Common Stock in the Conversion), Proposal 3 (regarding the amendment to the Stock Incentive Plan) and Proposal 5 (relating to the adjournment of the Special Meeting) will be approved if a majority of votes cast on the proposal vote in favor of the proposal. In addition, the approval of Proposal 2 is conditioned upon shareholder approval of Proposal 1a. In other words, if the Company’s shareholders do not approve the amendment to the Articles of Incorporation increasing the number of authorized shares of Common Stock, Proposal 2, relating to the issuance of Common Stock and Nonvoting Common Stock in the Conversion, will fail.

The Board of Directors unanimously recommends that you vote “FOR” each of the proposals described in the attached materials.

BY ORDER OF THE BOARD OF DIRECTORS

Stephen C. Green

President & Chief Executive Officer

January [—], 2013

PLEASE VOTE AS SOON AS POSSIBLE.

YOUR VOTE IS VERY IMPORTANT TO US NO MATTER HOW MANY SHARES YOU OWN.

***********************************

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS

FOR THE SHAREHOLDER MEETING TO BE HELD ON FEBRUARY 13, 2013

The Notice and Proxy Statement are available at

www.cfpproxy.com/7107 or on the Company’s website at www.jaxbank.com.

Table of Contents

| Page | ||||

| 1 | ||||

| 2 | ||||

| 2 | ||||

| 2 | ||||

| 3 | ||||

| 7 | ||||

| 8 | ||||

Proposal 1a: Articles Amendment to Increase Authorized Common Stock | 8 | |||

Proposal 1b: Articles Amendment to Authorize New Class of Nonvoting Common Stock | 11 | |||

| 13 | ||||

| 31 | ||||

Proposal 4: Articles Amendment to Effect Reverse Stock Split in the Board’s Discretion | 40 | |||

| 46 | ||||

Security Ownership of Management and Certain Beneficial Owners | 47 | |||

| 50 | ||||

| 51 | ||||

| 52 | ||||

| 58 | ||||

| 58 | ||||

| 58 | ||||

| 59 | ||||

Appendix A – Form of Capital Amendment to Articles of Incorporation | ||||

Appendix B – Series A Preferred Stock Designation | ||||

Appendix C – Form of Amended and Restated Stock Purchase Agreement | ||||

Appendix D – Form of Subscription Agreement | ||||

Appendix E – Form of Amended and Restated Exchange Agreement | ||||

Appendix F – Hovde Fairness Opinion | ||||

Appendix G – Form of Stock Incentive Plan Amendment | ||||

Appendix H – Stock Incentive Plan, as amended | ||||

Appendix I – Form of Reverse Stock Split Amendment to Articles of Incorporation | ||||

Appendix J – Audited Consolidated Financial Statements as of and for the Years Ended December 31, 2011 and 2010 | ||||

Appendix K – Management’s Discussion and Analysis and Results of Operations, as included in our Form 10-K for the fiscal year ended December 31, 2011 | ||||

Appendix L – Quantitative and Qualitative Disclosures About Market Risk, as included in our Form 10-K for the fiscal year ended December 31, 2011 | ||||

Appendix M – Unaudited Consolidated Financial Statements as of and for the Periods Ended September 30, 2012 | ||||

Appendix N – Management’s Discussion and Analysis and Results of Operations, as included in our Form 10-Q for the fiscal quarter ended September 30, 2012 | ||||

Appendix O – Quantitative and Qualitative Disclosures About Market Risk, as included in our Form 10-Q for the fiscal quarter ended September 30, 2012 | ||||

Table of Contents

Jacksonville Bancorp, Inc.

100 North Laura Street, Suite 1000

Jacksonville, Florida 32202

PROXY STATEMENT

Special Meeting of Shareholders

This Proxy Statement and the accompanying notice and proxy card are being furnished to you as a holder of Jacksonville Bancorp, Inc. common stock, $0.01 par value per share (the “Common Stock”), in connection with the solicitation of proxies by the Company’s Board of Directors (the “Board”) for the Special Meeting of Shareholders (the “Special Meeting”). The Special Meeting will be held on Wednesday, February 13, 2013, beginning at 9:00 a.m., Eastern Time, at the Company’s principal executive offices, 100 North Laura Street, Suite 1000, Jacksonville, Florida 32202. This Proxy Statement and the accompanying notice and proxy card are first being mailed to holders of Common Stock on or about January [—], 2013.

Unless the context requires otherwise, references in this statement to “we,” “us” or “our” refer to Jacksonville Bancorp, Inc., its wholly owned subsidiary, The Jacksonville Bank, and the Bank’s wholly owned subsidiary, Fountain Financial, Inc., on a consolidated basis. References to the “Company” denote Jacksonville Bancorp, Inc. The Jacksonville Bank is referred to as the “Bank.”

The purpose of the Special Meeting is to consider and act upon the following proposals:

| 1. | To approve an amendment to the Company’s Amended and Restated Articles of Incorporation, as amended (the “Articles of Incorporation”) to: |

| a. | increase the number of authorized shares of Common Stock to 400 million; and |

| b. | authorize 100 million shares of a new class of nonvoting common stock of the Company, par value $0.01 per share (the “Nonvoting Common Stock”); |

| 2. | To approve the issuance of an aggregate of approximately 100 million shares of Common Stock and Nonvoting Common Stock upon the conversion (the “Conversion”) of the Company’s recently issued 50,000 shares of Mandatorily Convertible, Noncumulative, Nonvoting, Perpetual Preferred Stock, Series A (the “Series A Preferred Stock”) as described in this Proxy Statement and the Articles of Incorporation, and for purposes of NASDAQ Stock Market Rule 5635; |

| 3. | To approve an amendment to the 2008 Amendment and Restatement of the Jacksonville Bancorp, Inc. 2006 Stock Incentive Plan, as amended (the “Stock Incentive Plan”), to (i) increase the number of shares of Common Stock available for issuance under the plan from 180,000 shares to 7 million shares, and (ii) eliminate certain minimum vesting conditions for awards of restricted stock and restricted stock units; |

| 4. | To authorize an amendment to the Articles of Incorporation to effect a reverse stock split of the outstanding shares of the Common Stock and Nonvoting Common Stock (if any) at a ratio of up to 1-for-20, the exact ratio and the implementation of the amendment being in the sole discretion of the Board; and |

| 5. | To approve the grant of discretionary authority to the persons named as proxies to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation of proxies if there are not sufficient votes at the time of the Special Meeting to approve the proposals listed above. |

Table of Contents

Shares represented by proxies properly signed and returned, unless subsequently revoked, will be voted at the Special Meeting in accordance with the instructions marked on the proxy. If a proxy is signed and returned without indicating any voting instructions, the shares represented by the proxy will be voted FOR approval of the proposals stated in this Proxy Statement.

If you have executed and delivered a proxy, you may revoke such proxy at any time before it is voted by attending the Special Meeting and voting in person, by giving written notice of revocation of the proxy or by submitting a signed proxy bearing a later date. Any notice of revocation or later dated proxy should be sent to the Company’s transfer agent, Registrar and Transfer Company, at the address indicated on the enclosed proxy card. In order for the notice of revocation or later proxy to revoke the prior proxy, the Company’s transfer agent must receive such notice or later proxy before the vote of shareholders at the Special Meeting. Unless you vote at the meeting or take other action, your attendance at the Special Meeting will not revoke your proxy. If you are a beneficial owner but do not hold the shares in your name, you may vote your shares in person at the Special Meeting only if you provide a legal proxy obtained from your broker, trustee or nominee at the Special Meeting.

The Company’s Amended and Restated Bylaws provide that a majority of all votes entitled to be cast by the holders of the outstanding shares of Common Stock entitled to vote, represented in person or by proxy, constitutes a quorum at a meeting of shareholders. The affirmative vote of the holders of a majority of the shares of Common Stock outstanding and entitled to vote on the proposal at the Special Meeting is required to approve each of Proposals 1a, 1b and 4 regarding amendments to the Articles of Incorporation. The affirmative vote of the holders of a majority of the shares of Common Stock cast on the proposal is required to approve each of Proposal 2 (regarding the issuance of Common Stock and Nonvoting Common Stock in the Conversion), Proposal 3 (regarding the amendment to the Stock Incentive Plan) and Proposal 5 (relating to adjournment of the Special Meeting). In addition, the approval of Proposal 2 is conditioned upon shareholder approval of Proposal 1a. In other words, if the Company’s shareholders do not approve the amendment to the Articles of Incorporation increasing the authorized shares of Common Stock, Proposal 2, relating to the issuance of Common Stock and Nonvoting Common Stock in the Conversion, will fail. Abstentions and broker non-votes will be considered present for purposes of constituting a quorum but will have no effect under Florida law with respect to the votes on the proposals.

If you are a beneficial owner and have questions or concerns about your proxy card, you are strongly encouraged to contact your bank, broker or other financial institution through which you hold the Company’s shares.

The Board has fixed the close of business on December 17, 2012 as the record date for determining the holders of the Common Stock entitled to receive notice of, and to vote at, the Special Meeting. At the close of business on December 17, 2012, there were issued and outstanding 5,890,880 shares of the Common Stock entitled to vote at the Special Meeting held by approximately 506 registered holders. You are entitled to one vote upon each matter properly submitted at the Special Meeting for each share of Common Stock held on the record date.

2

Table of Contents

When is the Special Meeting?

Wednesday, February 13, 2013 at 9:00 a.m., Eastern Time.

Where will the Special Meeting be held?

The Special meeting will be held at the Company’s principal executive offices, 100 North Laura Street, Suite 1000, Jacksonville, Florida 32202. If you wish to attend the Special Meeting and need directions, please call us at (904) 421-3040.

What items will be voted upon at the Special Meeting?

You are voting on the following proposals:

| 1. | To approve an amendment to the Articles of Incorporation to: |

| a. | increase the number of authorized shares of Common Stock to 400 million; and |

| b. | authorize 100 million shares of a new class of Nonvoting Common Stock; |

| 2. | To approve the issuance of an aggregate of approximately 100 million shares of Common Stock and Nonvoting Common Stock upon the Conversion of the outstanding shares of Series A Preferred Stock; |

| 3. | To approve an amendment to the Stock Incentive Plan to (i) increase the number of shares of Common Stock available for issuance from 180,000 shares to 7 million shares, and (ii) eliminate certain minimum vesting conditions for awards of restricted stock and restricted stock units; |

| 4. | To authorize an amendment to the Articles of Incorporation to effect a reverse stock split of the outstanding shares of the Common Stock and Nonvoting Common Stock (if any) at a ratio of up to 1-for-20, the exact ratio and the implementation of the amendment being in the sole discretion of the Board; and |

| 5. | To approve the grant of discretionary authority to the persons named as proxies to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation of proxies if there are not sufficient votes at the time of the Special Meeting to approve the proposals listed above. |

How do I vote by proxy?

You may vote by:

| • | Telephone, using the toll-free number listed on your proxy card (if you are a registered shareholder, that is if you hold your stock in your name) or vote instruction card (if your shares are held in “street name,” meaning that your shares are held in the name of a bank, broker or other nominee and your bank, broker or nominee makes telephone voting available); |

| • | Internet, at the address provided on your proxy card (if you are a registered shareholder) or vote instruction card (if your shares are held in “street name” and your bank, broker or nominee makes Internet voting available); or |

| • | Mail, by completing, signing, dating and mailing your proxy card or vote instruction card and returning it in the envelope provided. |

If your shares of Common Stock are held in “street name” by your broker, be sure to give your broker instructions on how you want to vote your shares because your broker will not be able to vote your shares on the proposals at the Special Meeting without instructions from you. See the question below “If my broker holds my shares in ‘street name,’ will my broker vote my shares for me?”

3

Table of Contents

When should I vote?

You should send in your proxy card or vote over the Internet or by telephone as soon as possible to ensure that your shares will be voted at the Special Meeting.

If my broker holds my shares in “street name,” will my broker vote my shares for me?

Yes, but only if you provide specific instructions to your broker on how to vote. You should follow the directions provided by your broker regarding how to instruct your broker to vote your shares. Without these instructions, your shares will not be voted.

May I vote in person?

Yes. You may attend the Special Meeting and vote your shares in person. If your shares are held in “street name,” you must get a proxy card from your broker or bank in order to attend the Special Meeting and vote in person.

You are urged to sign, date and return the enclosed proxy card or to vote over the Internet or by telephone as soon as possible, even if you plan to attend the Special Meeting, as it is important that your shares be represented and voted at the Special Meeting. If you attend the Special Meeting, you may vote in person as you wish, even though you have previously returned your proxy card. See question below “May I change my vote after I have mailed my signed proxy card?”

May I change my vote after I have mailed my signed proxy card?

Yes. You may change your vote at any time before the shares of the Common Stock reflected on your proxy card are voted at the Special Meeting. If your shares are registered in your name, you can do this in one of three ways:

| • | you can deliver to the Company’s transfer agent, Registrar and Transfer Company, a written notice stating that you would like to revoke your proxy; the written notice should bear a date later than the proxy card; |

| • | you can complete, execute and deliver to Registrar and Transfer Company, a new, later-dated proxy card for the same shares, provided the new proxy card is received before the polls close at the Special Meeting; or |

| • | you can attend the Special Meeting and vote in person. |

Any written notice of revocation should be delivered to the Company’s Corporate Secretary at or before the taking of the vote at the Special Meeting. Your attendance at the Special Meeting alone will not revoke your proxy.

If you have instructed your broker to vote your shares, you must follow directions received from your broker to change your vote. You cannot vote shares held in “street name” by returning a proxy card directly to the Company or by voting in person at the Special Meeting, unless you obtain a proxy card from your bank or broker.

How many votes are required to approve the proposals?

The voting requirements to approve the proposals are as follows:

| • | the approval of Proposal 1a regarding the amendment to the Articles of Incorporation to increase the authorized shares of Common Stock requires the affirmative vote of the holders of a majority of the shares of Common Stock outstanding and entitled to vote on the proposal at the Special Meeting; |

| • | the approval of Proposal 1b regarding the amendment to the Articles of Incorporation to authorize the new class of Nonvoting Common Stock requires the affirmative vote of the holders of a majority of the shares of Common Stock outstanding and entitled to vote on the proposal at the Special Meeting; |

| • | the approval of Proposal 2 regarding the issuance of Common Stock and Nonvoting Common Stock upon the Conversion of the outstanding shares of Series A Preferred Stock requires the affirmative vote of the holders of a majority of the shares of Common Stock cast on the proposal in person or by proxy at the Special Meeting; |

4

Table of Contents

| • | the approval of Proposal 3 regarding the amendment to the Stock Incentive Plan requires the affirmative vote of the holders of a majority of the shares of Common Stock cast on the proposal in person or by proxy at the Special Meeting; |

| • | the approval of Proposal 4 regarding the amendment to the Articles of Incorporation to effect a reverse stock split of the outstanding shares of the Common Stock and Nonvoting Common Stock (if any) at a ratio of up to 1-for-20, in the sole discretion of the Board, requires the affirmative vote of the holders of a majority of the shares of Common Stock outstanding and entitled to vote on the proposal at the Special Meeting; and |

| • | the approval of Proposal 5 regarding the grant of discretionary authority to the persons named as proxies to adjourn the Special Meeting to a later date, if necessary, to permit further solicitation of proxies, requires the affirmative vote of the holders of a majority of the shares of Common Stock cast on the proposal in person or by proxy at the Special Meeting. |

Is the adoption of any proposal conditioned on shareholder approval of any of the other proposals?

Yes. The adoption of Proposal 2, relating to the Conversion of the outstanding shares of Series A Preferred Stock into shares of Common Stock and Nonvoting Common Stock, is conditioned upon shareholder approval of Proposal 1a, relating to the amendment to the Articles of Incorporation increasing the authorized shares of Common Stock. The approval of Proposal 2 is conditioned upon the approval of Proposal 1a because, without the approval of Proposal 1a and the filing of the related amendment to the Articles of Incorporation with the Florida Secretary of State, the Conversion of the Series A Preferred Stock would not be triggered under the Articles of Incorporation and the Company would not have enough authorized shares of Common Stock to complete the Conversion.

How will the Conversion and approval of Proposals 1a, 1b and 2 affect existing shareholders?

After the full Conversion, assuming that shareholder approvals are received for Proposals 1a, 1b and 2, you will continue to hold the same number of shares of our Common Stock. However, our existing shareholders (other than any shareholder who exercised its contractual preemptive rights for the Private Placement, as described herein) will incur substantial dilution of their voting power and will own a smaller percentage of our outstanding capital stock. After the Conversion of the Series A Preferred Stock, our existing shareholders are expected to own approximately 78.6% of the outstanding Common Stock; however, only 3.3% of the outstanding Common Stock is expected to be owned by our existing shareholders who did not participate in the Private Placement, as more fully summarized in the ownership table below.

Dilution of Voting Power Immediately Following Conversion

| Aggregate ownership of Common Stock immediately prior to Private Placement | Aggregate ownership of Common Stock immediately following Conversion of Series A Preferred Shares(1) | |||||||

Existing shareholders: | ||||||||

Shareholders who invested in Private Placement | 70.0 | % | 75.3 | % | ||||

Shareholders who did not invest in Private Placement | 30.0 | % | 3.3 | % | ||||

New investors in Private Placement | — | 21.4 | % | |||||

|

|

|

| |||||

TOTAL | 100.0 | % | 100.0 | % | ||||

| (1) | Assumes the Conversion of the outstanding shares of Series A Preferred Stock. 47,640,000 shares of Common Stock are expected to be issued in the Conversion, resulting in 53,530,880 shares of Common Stock outstanding following the Conversion. In addition, 52,360,000 shares of Nonvoting Common Stock are expected to be issued in the Conversion but these shares are not reflected in the table since they will be nonvoting and will not convert into voting Common Stock until transferred by their respective holders in a “permitted transfer,” as more fully described in this Proxy Statement. Assuming all shares of Nonvoting Common Stock are converted into Common Stock upon “permitted transfers” to persons not otherwise shareholders of the Company, existing shareholders who did not invest in the Private Placement will own an aggregate of |

5

Table of Contents

| 1.7% of the outstanding Common Stock and existing shareholders who invested in the Private Placement will own an aggregate of 38.1% of the outstanding Common Stock. |

We also expect there to be a significant dilutive effect on both the earnings (loss) per share of our Common Stock and the book value per share of our Common Stock as a result of the Conversion because the outstanding shares of Series A Preferred Stock will be converted into approximately 100 million shares of Common Stock and/or Nonvoting Common Stock. The loss per share for the Common Stock for the nine months ended September 30, 2012 and the year ended December 31, 2011, on both a basic and diluted basis, was $3.60 and $4.09, respectively, as reported in the Company’s reports on Form 10-Q and Form 10-K for such periods. The loss per share for the Common Stock as adjusted for the pro forma impacts of the full Conversion of the Series A Preferred Stock into shares of Common Stock and Nonvoting Common Stock, and the conversion of the Nonvoting Common Stock into Common Stock, is $0.48 and $0.51 for the same periods ended September 30, 2012 and December 31, 2011, respectively, on both a basic and diluted basis. The historical book value per share for the Common Stock as of September 30, 2012 and December 31, 2011, was $1.46 and $4.98, respectively. The book value per share of the Common Stock, as adjusted for the pro forma impacts of the full Conversion of the Series A Preferred Stock into shares of Common Stock and Nonvoting Common Stock, and the conversion of the Nonvoting Common Stock into Common Stock, is $0.52 and $0.72 as of September 31, 2012 and December 31, 2011 respectively. Please see the section captioned “Potential Consequences if Proposal 2 is Approved—Dilution” under Proposal 2 for more information about the dilutive impact of the Conversion on the earnings (loss) per share and the book value per common share.

Please see the section captioned “Potential Consequences if Proposal 2 is Approved” under Proposal 2 for a discussion of other potential effects of the Conversion.

What constitutes a “quorum” for the Special Meeting?

The presence, whether in person or through the prior submission of a proxy, of the holders of Common Stock representing a majority of the shares outstanding and entitled to vote on December 17, 2012, the record date, will constitute a quorum for purposes of the Special Meeting. A quorum is necessary to conduct business at the Special Meeting. Because there were 5,890,880 shares of Common Stock issued and outstanding as of the record date, at least 2,945,441 shares must be present or represented by proxy at the Special Meeting for a quorum to exist.

Who can vote at the Special Meeting?

You are entitled to vote your Common Stock if the Company’s records show that you held your shares as of the close of business on December 17, 2012, the record date. On that date, there were 5,890,880 shares of Common Stock outstanding and entitled to vote, held by approximately 506 holders of record. The Common Stock is the Company’s only class of outstanding voting securities for purposes of the Special Meeting.

Who pays for the solicitation of proxies?

The expense of soliciting proxies of the Company’s shareholders will be borne by the Company. The Company will reimburse brokers, banks and other custodians, nominees and fiduciaries representing beneficial owners of shares for their reasonable expenses in forwarding soliciting materials to beneficial owners. Proxies may also be solicited by certain of the Company’s directors, officers and employees. No additional compensation will be paid for these services.

Are there any appraisal rights or dissenters’ rights?

Under the Florida Business Corporation Act, the Company’s shareholders are not entitled to dissenters’ rights or appraisal rights with respect to any of the proposals.

What is the voting recommendation of the Board?

The Board recommends a vote “FOR” all of the proposals described in this Proxy Statement.

As more fully described in this Proxy Statement, certain of our directors and executive officers (directly or indirectly) invested in the Private Placement, including Stephen C. Green (President, Chief Executive Officer and

6

Table of Contents

director), Valerie A. Kendall (Chief Financial Officer), Scott M. Hall (Executive Vice President and Bank President), Donald F. Glisson (director), John W. Rose (director), Price W. Schwenck (director) and John P. Sullivan (director). Because the initial conversion price of the Series A Preferred Stock ($0.50) was less than the then-current market price of our Common Stock ($0.80), NASDAQ considers the aggregate difference between the initial conversion price and the market price as a form of “equity compensation” to those directors and executive officers who invested in the Private Placement. This “equity compensation” totaled $999,000, and is more fully described in the section captioned “NASDAQ Shareholder Approval Requirement” under Proposal 2 of this Proxy Statement. For more information about the investments of our directors and executive officers in the Private Placement, please see the sections captioned “Interests of Certain Persons” and “Security Ownership of Management and Certain Beneficial Owners.”

Where can I find the voting results?

We will publish the voting results of the Special Meeting on a Current Report on Form 8-K within four business days after the date of the meeting. You will be able to find such Form 8-K at the Investor Relations section of our website at www.jaxbank.com or on the SEC’s website at www.sec.gov.

Who can help answer my other questions?

If you have additional questions about the Special Meeting, including the procedures for voting your shares, or if you would like additional copies, without charge, of this Proxy Statement, you should contact Jacksonville Bancorp, Inc., 100 North Laura Street, Suite 1000, Jacksonville, Florida 32202, Attention: Corporate Secretary, (904) 421-3040.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Proxy Statement may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and are including this statement for purposes of invoking these safe harbor provisions. You can identify these statements from our use of the words “plan,” “estimate,” “project,” “believe,” “intend,” “anticipate,” “expect,” “target,” “is likely,” “will,” and similar expressions. These forward-looking statements may include, among other things:

| • | statements and assumptions relating to financial performance; |

| • | statements relating to the anticipated effects on results of operations or financial condition from recent or future developments or events; |

| • | statements relating to our capital raising activities, business and growth strategies and our regulatory capital levels; |

| • | statements regarding the disposition of certain of our assets; and |

| • | any other statements, projections or assumptions that are not historical facts. |

Forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from our expectations of future results, performance or achievements expressed or implied by these forward-looking statements. We discuss these and other uncertainties in the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2011, and otherwise in our subsequent reports filed with the Securities and Exchange Commission (the “SEC”), which can be obtained on the SEC’s website at www.sec.gov.

Factors that may cause actual results to differ materially from those contemplated by such forward-looking statements include, without limitation, the following: the results of the Special Meeting; our ability to continue disposing of substandard assets and the disposition prices thereof; economic and political conditions, especially in North Florida; real estate prices and sales in the our markets; competitive circumstances; bank regulation, legislation, accounting principles and monetary policies; the interest rate environment; efforts to increase our capital and reduce our nonperforming assets; and technological changes.

7

Table of Contents

PROPOSAL 1: ARTICLES AMENDMENT TO INCREASE THE NUMBER OF AUTHORIZED SHARES OF COMMON STOCK AND AUTHORIZE A NEW CLASS OF NONVOTING COMMON STOCK

Proposal 1 contemplates an amendment to the Articles of Incorporation (the “Capital Amendment”) to:

| a. | increase the number of authorized shares of Common Stock from 40 million shares to 400 million shares; and |

| b. | authorize 100 million shares of a new class of Nonvoting Common Stock. |

No increase in the number of authorized shares of preferred stock is proposed.

On December 19, 2012, the Board approved the Capital Amendment, which involves the amendment of Section 4.01 of the Articles of Incorporation and the addition of a new Section 4.02 to the Articles of Incorporation (and renumbering the remaining paragraphs of Article IV accordingly). The complete text of the Capital Amendment is set forth onAppendix A to this Proxy Statement. Such text is, however, subject to revision for such changes as may be required if only one of Proposal 1a or 1b is approved by the shareholders or as may be required by the Florida Secretary of State or other changes consistent with this proposal that we may deem necessary or appropriate.

Each of the two proposals comprising Proposal 1 is an element of the Capital Amendment, and is required to effect the full Conversion contemplated by the Articles of Incorporation. In addition, the approval of Proposal 2 (concerning the issuance of Common Stock and Nonvoting Common Stock in the Conversion) is conditioned upon the approval of Proposal 1a. In other words, if the shareholders do not approve Proposal 1a, Proposal 2 will fail.

If the Company’s shareholders approve one or both of the proposals comprising Proposal 1, we intend to file the corresponding amendment to the Articles of the Incorporation with the Florida Secretary of State immediately following the shareholder meeting. The Conversion of the Series A Preferred Stock into Common Stock will occur on the date that both Proposal 1a and Proposal 2 are approved.

Proposal 1a. Articles Amendment to Increase Authorized Common Stock

The Company’s shareholders will be asked to approve the Capital Amendment to increase the number of authorized shares of Common Stock to 400 million shares.

Purpose of the Amendment

The purpose of the amendment is to provide additional shares of Common Stock for issuance in the Conversion, for issuance in the Public Offering (defined below), in order to grant the Contemplated Equity Awards (defined below), and for other future issuances. As of the record date, there were 5,890,880 shares of the Common Stock issued and outstanding, and 172,918 shares reserved for issuance under outstanding options and restricted stock units, leaving approximately 33.94 million shares of Common Stock unissued and not reserved for issuance.

On December 31, 2012, we completed a private placement to 30 accredited investors of an aggregate of 50,000 shares of Series A Preferred Stock (the “Private Placement”). The Private Placement included the 5,000 shares of Series A Preferred Stock issued to CapGen Capital Group IV LP (“CapGen”) in exchange (the “Exchange”) for its outstanding Noncumulative, Nonvoting, Perpetual Preferred Stock, Series B (the “Series B Preferred Stock”) pursuant to the Amended and Restated Exchange Agreement dated December 31, 2012 between the Company and CapGen (the “Exchange Agreement”).The investors in the Private Placement included seven of our executive officers and directors (five of whom were existing shareholders) and ten other current shareholders of the Company (including CapGen); five of the investors are affiliates of CapGen (including our two directors Messrs. Rose and Sullivan). For more information on the investments of our executive officers and directors, please see the sections captioned “Interests of Certain Persons” and “Security Ownership of Management and Certain Beneficial Owners.”

8

Table of Contents

The outstanding shares of Series A Preferred Stock are mandatorily convertible, at an initial conversion price of $0.50 per share and an initial conversion rate of 2,000 shares of Common Stock and/or Nonvoting Common Stock for each outstanding share of Series A Preferred Stock, into an aggregate of approximately 100 million shares of Common Stock and Nonvoting Common Stock, of which approximately 47.6 million shares are expected to be issued as Common Stock, upon receipt of the requisite of shareholder approvals, as more fully discussed under “Proposal 2: Issuance of Approximately 100 Million Shares of Common Stock and Nonvoting Common Stock Upon Conversion of 50,000 Series A Preferred Shares.” Immediately after the Conversion and as a result of their investments in the Private Placement (and/or the investments of investors managed by such entities or investments by affiliates of such entities), we expect CapGen Capital Group IV LP, Sandler O’Neill Asset Management, LLC and Wellington Management Company to remain beneficial owners of at least 5% of our Common Stock, and we expect Sutherland Asset I, LLC to become the beneficial owner of at least 5% of our Common Stock (see “Security Ownership of Management and Certain Beneficial Owners” for more information). Without approval of this Proposal 1a, Conversion will not be triggered under the Articles of Incorporation and the Company would not have enough authorized shares of Common Stock to complete the Conversion. Accordingly, Proposal 2, relating to the issuance of shares of Common Stock in the Conversion, is conditioned upon shareholder approval of Proposal 1a.

In addition, following the Conversion and within six months of the Closing of the Private Placement, the Company intends to conduct a public offering to its existing holders of Common Stock, and potentially to other members of the community, of between 10 million and 20 million shares of Common Stock (or subscription rights to purchase such Common Stock), at the same price per share as the conversion price (initially $0.50 per share) of the Series A Preferred Stock (the “Public Offering”). The increase in authorized shares of Common Stock under this Proposal 1a is required for the Company to complete the Public Offering following the Conversion. Offerees and investors in the Private Placement would not be eligible to participate in the Public Offering.

The Private Placement and the proposed Public Offering are initiatives by the Company to increase capital and strengthen its balance sheet, the need for which is discussed more fully under the subsection “Background of the Private Placement” under Proposal 2. In addition, the Board considers the proposed increase in the number of authorized shares of Common Stock desirable because it would give the Board greater flexibility and provide sufficient shares available for future issuance if needed to further improve the Company’s capital levels. If this Proposal 1a is approved by the Company’s shareholders, the additional authorized shares of Common Stock would also be available from time to time for other corporate purposes, including acquisitions of other companies or other assets, stock dividends, stock split or other stock distributions, and in connection with equity-based incentive plans, including issuances under the Stock Incentive Plan which is proposed to be amended to, among other things, increase the number of authorized shares from 180,000 to 7 million shares of Common Stock (See “Proposal 3: Amendment to Stock Incentive Plan”). As described more fully under Proposal 3, the Company has agreed to issue, subject to receipt of applicable regulatory and shareholder approvals (including the approval of Proposal 3 described herein), to two of its executive officers, Stephen C. Green and Margaret A. Incandela, equity awards under the Stock Incentive Plan representing up to approximately 3.5 million shares of Common Stock (the “Contemplated Equity Awards”). The increase in authorized shares of Common Stock under this Proposal 1a is required in order for the Company to issue the Contemplated Equity Awards, assuming the Conversion occurs.

Authorized but unissued shares of our Common Stock or preferred stock may be issued from time to time upon authorization by the Board, at such times, to such persons, and for such consideration as the Board may determine in its discretion and generally without further approval by our shareholders (except as may be required for any particular transaction by applicable law or regulation).

If shareholders approve the amendment described in this Proposal 1a, it will become effective upon the filing of the Capital Amendment (or relevant portion thereof) with the Florida Secretary of State in substantially the form attached hereto asAppendix A, which the Company expects to occur promptly following shareholder approval.

9

Table of Contents

Effect of the Amendment

The additional shares of Common Stock to be authorized by adoption of the Capital Amendment would have rights identical to the currently outstanding shares of Common Stock (other than the limited contractual preemptive rights of certain shareholders discussed below). Adoption of the proposed amendment and issuance of the Common Stock would not affect the rights of the holders of currently outstanding shares of Common Stock, except for the limited contractual preemptive rights of certain shareholders discussed below and effects incidental to increasing the number of shares of our Common Stock outstanding, such as dilution of the earnings per share and voting power of current holders of Common Stock. Under the Articles of Incorporation, the Company’s shareholders do not have preemptive rights with respect to the Common Stock and only a limited number of the Company’s shareholders have contractual preemptive rights which were granted in connection with the Private Placement and which expire in December 2014. As a result, if the Board decides to issue additional shares of Common Stock, most existing holders of the Common Stock would not have any preferential rights to purchase such shares. See “Effect on Outstanding Common Stock” below for more information regarding the potential dilution to the Company’s current shareholders.

The issuance of additional shares of Common Stock, or the perception that additional shares of Common Stock may be issued, may also adversely affect the market price of our Common Stock.

Material Terms of the Common Stock

Each holder of Common Stock is entitled to one vote for each share held of record on all matters presented to a vote at a shareholders meeting, including the election of directors. Holders of Common Stock have no cumulative voting rights or preemptive rights (other than the limited contractual preemptive rights of certain holders described above) to purchase or subscribe for any additional shares of Common Stock or other securities, and there are no conversion rights or redemption or sinking fund provisions with respect to the Common Stock.

Subject to the prior rights of the holders of shares of preferred stock that may be issued and outstanding, the holders of Common Stock are entitled to receive dividends when, as and if declared by the Board out of funds lawfully available for the payment of dividends.

Effect on Outstanding Common Stock

The authorization of the additional shares of Common Stock would not, by itself, have any effect on the rights of shareholders. However, holders of Common Stock have no preemptive rights to acquire additional shares of Common Stock (other than the limited contractual preemptive rights of certain shareholders described above), so the future issuance of shares of Common Stock, including pursuant to the transactions discussed above or any other potential capital raising initiative, is likely to have an immediate and significant dilutive effect on earnings per share and the voting power of existing shareholders at the time of the issuance.

Vote Required

Provided that a quorum is present, Proposal 1a will be approved if shareholders holding at least a majority of the outstanding shares of Common Stock entitled to vote on this proposal vote in favor of the proposal.

10

Table of Contents

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” THIS PROPOSAL 1a.

Proposal 1b. Articles Amendment to Authorize New Class of Nonvoting Common Stock

The Company’s shareholders will be asked to approve the Capital Amendment to authorize 100 million shares of a new class of Nonvoting Common Stock with the terms set forth in the amendment.

Purpose of the Amendment

The purpose of the amendment is to provide shares of Nonvoting Common Stock for issuance in the Conversion, and for other future issuances. As this amendment would authorize a new class of stock, there are currently no outstanding shares of Nonvoting Common Stock.

Under the terms of the Series A Preferred Stock, as set forth in the Articles of Amendment to the Amended and Restated Articles of Incorporation Designating Mandatorily Convertible, Noncumulative, Nonvoting, Perpetual Preferred Stock, Series A, which was filed with the Florida Secretary of State (the “Series A Designation”), certain Series A Holders (as defined herein) will receive Nonvoting Common Stock upon Conversion of their shares of Series A Preferred Stock to the extent they otherwise would exceed the “conversion limits” set forth in the Series A Designation. The conversion limits were put in place to observe applicable regulatory or investment policy limitations applicable to such Series A Holders. See “Material Terms of Series A Preferred Stock” under Proposal 2 for more information about the conversion limits. We expect approximately 52.4 million shares of Nonvoting Common Stock to be issued in the Conversion, subject to the receipt of the requisite shareholder approvals.

The Nonvoting Common Stock will be identical to Common Stock in all respects, except that the Nonvoting Common Stock will have only those voting rights required by the Florida Business Corporation Act. The Nonvoting Common Stock will be convertible into shares of Common Stock on the terms set forth in the Capital Amendment. See the subsection below “Material Terms of the Nonvoting Common Stock.”

Authorized but unissued shares of the Nonvoting Common Stock may be issued from time to time upon authorization by the Board, at such times, to such persons, and for such consideration as the Board may determine in its discretion and generally without further approval by our shareholders (except as may be required for any particular transaction by applicable law or regulation).

If shareholders approve the amendment described in this Proposal 1b, it will become effective upon the filing of the Capital Amendment (or relevant portion thereof) with the Florida Secretary of State in the form attached hereto asAppendix A, which the Company expects to occur promptly following shareholder approval.

Effect of the Amendment

The new shares of Nonvoting Common Stock to be authorized by adoption of the amendment would have rights identical to the currently outstanding shares of Common Stock, except that the Nonvoting Common Stock will have only those voting rights required by the Florida Business Corporation Act. Adoption of the proposed amendment and issuance of the Nonvoting Common Stock would not affect the rights of the holders of currently outstanding shares of Common Stock, except for the limited contractual preemptive rights of certain shareholders discussed above and effects incidental to increasing the number of shares of our Common Stock outstanding, such as dilution of the earnings per share and voting power of current holders of Common Stock, since the Nonvoting Common Stock would be convertible into Common Stock upon a “permitted transfer” (described under “Material Terms of the Nonvoting Common Stock”). Under the Articles of Incorporation, the Company’s shareholders do not have preemptive rights with respect to the Nonvoting Common Stock. As a result, if the Board decides to issue additional shares of Nonvoting Common Stock, the existing holders of the Common Stock or Nonvoting Common Stock would not have any preferential rights to purchase such shares (other than the limited contractual preemptive rights of certain shareholders discussed above). See “Effect on Outstanding Common Stock” below for more information regarding the potential dilution to the Company’s current shareholders.

11

Table of Contents

The issuance of additional shares of Nonvoting Common Stock, or the perception that additional shares of Nonvoting Common Stock may be issued, may also adversely affect the market price of our Common Stock.

Material Terms of the Nonvoting Common Stock

Holders of Nonvoting Common Stock will not be entitled to vote except as required by the Florida Business Corporation Act. Where the shares of Nonvoting Common Stock are entitled to vote under Florida law, each holder of Nonvoting Common Stock will have one vote for each share of Nonvoting Common Stock held of record solely on the matters to which such shares are entitled to vote, and subject to the rights and limitations specified by the Florida Business Corporation Act. Other than voting rights, the Common Stock and Nonvoting Common Stock have the same rights and privileges, share ratably in all assets of the Company upon its liquidation, dissolution or winding-up, will be entitled to receive dividends in the same amount per share and at the same time when, as and if declared by the Board, and are identical in all other respects as to all other matters (other than voting). Holders of Nonvoting Common Stock have no cumulative voting rights or preemptive rights (other than the limited contractual preemptive rights of certain shareholders described above) to purchase or subscribe for any additional shares of Common Stock or Nonvoting Common Stock or other securities, and there are no conversion rights or redemption or sinking fund provisions with respect to the Nonvoting Common Stock.

Each share of Nonvoting Common Stock will automatically convert into one share of Common Stock in the event of a “permitted transfer” to a transferee. A “permitted transfer” is a transfer of Nonvoting Common Stock (i) in a widespread public distribution; (ii) in which no transferee (or group of associated transferees) would receive 2% or more of any class of voting securities of the Company; or (iii) to a transferee that would control more than 50% of the voting securities of the Company without any transfer from such holder of Nonvoting Common Stock.

Subject to the prior rights of the holders of shares of preferred stock that may be issued and outstanding, the holders of Nonvoting Common Stock are entitled to receive dividends when, as and if declared by the Board out of funds lawfully available for the payment of dividends.

Effect on Outstanding Common Stock

The authorization of the new shares of Nonvoting Common Stock would not, by itself, have any effect on the rights of shareholders. However, holders of Common Stock have no preemptive rights to acquire additional shares of Common Stock or Nonvoting Common Stock (other than the limited contractual preemptive rights of certain shareholders discussed above), so the future issuance of shares of Nonvoting Common Stock, including pursuant to the transactions discussed above or any other potential capital raising initiative, is likely to have a significant dilutive effect on earnings per share at the time of issuance, and on the voting power of existing shareholders at the time of its conversion into Common Stock.

Vote Required

Provided that a quorum is present, Proposal 1b will be approved if shareholders holding at least a majority of the outstanding shares of Common Stock entitled to vote on this proposal vote in favor of the proposal.

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” THIS PROPOSAL 1b.

12

Table of Contents

PROPOSAL 2: ISSUANCE OF APPROXIMATELY 100 MILLION SHARES OF COMMON STOCK AND NONVOTING COMMON STOCK UPON CONVERSION OF 50,000 SERIES A PERFERRED SHARES

The adoption of this Proposal 2 is conditioned upon shareholder approval of Proposal 1a, so shareholders who wish to approve Proposal 2 should also approve Proposal 1a.

Proposal 2 contemplates the issuance of an aggregate of approximately 100 million shares of Common Stock and Nonvoting Common Stock, based on a conversion price of $0.50 per share (subject to certain anti-dilution adjustments), upon Conversion of the 50,000 shares of Series A Preferred Stock issued in the Private Placement pursuant to (i) the Amended and Restated Stock Purchase Agreement, dated as of December 31, 2012 (the “Stock Purchase Agreement”), among the Company, CapGen and the 19 other investors listed on the signature pages thereto (together with CapGen, the “SPA Investors”), (ii) the individual Subscription Agreements, accepted by the Company on December 31, 2012, between the Company and each of ten of the Company’s directors, executive officers and other related persons (collectively, the “Subscription Agreements” and the subscriptions represented thereby, referred to as the “Subscriptions”), and (iii) the Exchange Agreement. The holders of Series A Preferred Stock are collectively referred to herein as the “Series A Holders.” Of the 100 million shares to be issued in the Conversion (assuming shareholder approval of Proposals 1a, 1b and 2), 47.6 million shares are expected to be Common Stock and 52.4 million shares are expected to be Nonvoting Common Stock. The initial conversion price of $0.50 was approved by the special Pricing Committee of the Board, and ratified by the entire Board. Prior to approving the initial conversion price, the Board received a fairness opinion from Hovde Securities, LLC that the initial conversion price of $0.50 was fair, from a financial point of view, to the Company’s shareholders (in their capacity as existing shareholders and not as prospective purchasers in the Private Placement). See the section below captioned “Fairness Opinion of Company’s Financial Advisor.” Immediately after the Conversion and as a result of their investments in the Private Placement (and/or the investments of investors managed by such entities or investments by affiliates of such entities), we expect CapGen Capital Group IV LP, Sandler O’Neill Asset Management, LLC and Wellington Management Company to remain beneficial owners of at least 5% of our Common Stock, and we expect Sutherland Asset I, LLC to become the beneficial owner of at least 5% of our Common Stock (see “Security Ownership of Management and Certain Beneficial Owners” for more information).

Background of the Private Placement

The Jacksonville, Florida market experienced deterioration in its economic condition later in the cycle than other Florida cities. In late 2011, it became apparent that the depth of the decline in the economic condition was larger than Company management anticipated and the expected period for return to stability in the market was longer than first forecasted. Both of these scenarios presented an opportunity for additional capital strain on the Company and the Bank, as existing classified assets (such as loans designated substandard, doubtful and loss by regulatory definitions and other real estate owned) would be slower to eliminate and the environment could create additional classified assets as a borrower’s ability to maintain loans would be diminished with the strain on their personal liquidity and cash flow over a protracted period. Therefore, the Board and Company management determined that it would be prudent to seek additional capital in order for the Company to increase its capital, ensure the Bank remained well capitalized at all times while continuing to eliminate problem loans, work through developing issues with customers and maintain a safe and sound level of operational strength for the Bank, its customers and the Company’s shareholders. The Board also concluded that, in light of a variety of factors, including capital markets volatility, general economic uncertainties, the Company’s capital ratios at the time of the decision and its regulatory mandates, it was important that any process to raise additional capital be executed promptly and with a high degree of certainty of completion. Ultimately, the Board determined that a private placement of preferred stock would allow the Company to raise capital prior to, and without the delay inherent in, seeking the shareholder approval required by NASDAQ Stock Market Rule 5635. The Board designated the Series A Preferred Stock as mandatorily convertible into Common Stock and Nonvoting Common Stock because federal banking laws and regulations require that substantially all of the Company’s capital be in the form of common equity. Finally, the Board designated the Series A Preferred Stock as nonvoting in order to allow the Company to raise capital pending regulatory approval for CapGen to increase its holdings of Common Stock.

13

Table of Contents

Since August 2008, the Bank had been subject to a Memorandum of Understanding with the Federal Deposit Insurance Corporation (the “FDIC”) and the Florida Office of Financial Regulation that required the Bank to maintain a total risk-based capital ratio of 10.00% and a Tier 1 leverage ratio of 8.00%. The Bank entered into a new Memorandum of Understanding in July 2012 that replaced the 2008 Memorandum, and among other things, increased the minimum total risk-based capital requirement to 12.00% as a direct reflection of the increased classified assets since the previous examination. At September 30, 2012 and December 31, 2011, the Bank was adequately capitalized for regulatory purposes, but did not meet the capital requirements of the current or prior Memorandum of Understanding. Further, the classified assets to capital ratio was 146.82% at September 30, 2012 and 165.00% at December 31, 2011, respectively, which were far in excess of regulatory requirements for a safe and sound institution.

The Bank has experienced declining regulatory ratios since the third quarter of 2011, with nonperforming and classified assets increasing at a material rate due to the reasons discussed above. Accordingly, on March 27, 2012, we engaged Sandler O’Neill + Partners, L.P. (“Sandler”) as an independent financial advisor to the Company to assist the Company in raising capital as well to assist the Company in creating a mechanism to expedite the reduction in classified assets. Sandler subsequently engaged The Situs Companies to perform an independent evaluation of the Bank’s loan portfolio, expected imbedded losses on disposition and the adequacy of the loan loss reserve.

Because of the substantial loss exposure to the Bank as determined by this third party study, Sandler recommended, and the Board began to consider, a capital raise with a per share price at a significant discount to current market prices for the Company’s Common Stock. In order for a capital raise to be successful, it was determined that changes needed to occur in senior management to hire individuals with experience in turnarounds, capital raises and market penetration. The Company believed these steps were necessary to stabilize operations and to help persuade existing shareholders and prospective new investors to participate in any capital raise. In light of the above, the Board began to consider changes in senior management, and in May 2012, hired Margaret A. Incandela to serve as the Executive Vice President and Chief Credit Officer of the Company and the Bank. Members of the Board also began to consider candidates for President and Chief Executive of the Company and Chief Executive Officer of the Bank, referred from several sources, and, after interviews with members of management and certain members of the Board, recommended that the Board hire Stephen C. Green to serve in those capacities. The Board also appointed Ms. Incandela as Chief Operating Officer of the Company and the Bank in June 2012.

On June 14, 2012, the Board directed the Company to pursue one or more transactions to raise capital (then estimated to be approximately $50.0 million) through Sandler, on terms acceptable to CapGen, as lead investor, and other investors, structured to the extent practicable to preserve the Company’s net operating losses and deferred tax assets, including a private placement offered to certain eligible investors (including CapGen and the Company’s other shareholders currently holding preemptive rights), followed by one or more public offerings in the form of a rights or similar offering to existing shareholders and select others.

On June 15, 2012, CapGen committed to the Board by letter to purchase up to $25 million in newly issued capital stock of the Company in a private placement as part of an approximately $50 million capital raise.

As of June 30, 2012, the Company did not meet minimum Federal Reserve capital requirements, though the Bank was still considered adequately capitalized.

The Company’s executive management team and the Board discussed the limited options available to restore capital and that pursuing a transaction with CapGen would require a fairness opinion. Capital reductions had occurred in the quarter ending June 30, 2012 due to losses on the disposition of classified assets. The continued high level of classified assets and the relatively short time frame provided to improve capital and reduce classifieds under the Bank’s regulatory mandates limited the approaches that could be taken to improve the financial condition of the Bank. Had the capital markets been stronger, additional alternatives may have been available that would still achieve the capital infusion prior to fiscal year end.

14

Table of Contents

On July 24, 2012, the Board appointed four independent directors, none of whom were affiliates of CapGen, to a special pricing committee of the Board (the “Pricing Committee”). The Pricing Committee was given the authority to determine or approve, as applicable, after taking into consideration a fairness opinion of Hovde Securities, LLC (“Hovde”) and such other information that committee deemed relevant to its determinations, the pricing of the securities to be issued in the Private Placement and the number of shares to be offered and sold in the capital raise.

On August 21, 2012, the Board unanimously approved the offer and sale of at least 50,000 shares of Series A Preferred Stock in a private placement transaction pursuant to the terms of a stock purchase agreement (the “Original Stock Purchase Agreement”) and authorized the creation of the Series A Preferred Stock through the filing of an amendment to the Articles of Incorporation designating such preferred stock, subject to the execution of the Original Stock Purchase Agreement for at least $50 million in shares of Series A Preferred Stock and the determination and approval of the conversion rate and conversion price (relating to the Conversion) by the Pricing Committee and upon receipt of the fairness opinion by Hovde. On the same date, the Board also directed that, following the closing of the Private Placement, the issuance of shares of Common Stock upon the Conversion of the outstanding shares of Series A Preferred Stock be submitted to the Company’s shareholders for approval with a recommendation from the Board of approval of such matter.

On the following day, the Company entered into the Original Stock Purchase Agreement with CapGen for the purchase by CapGen of up to 25,000 shares of Series A Preferred Stock at a purchase price of $1,000 per share, subject to the terms and conditions contained in the Original Stock Purchase Agreement. Sandler and the Company continued discussions with prospective investors in the Private Placement, including those existing shareholders with preemptive rights who participated in the Company’s $35 million private placement that closed on November 16, 2010. Although originally the Company contemplated participation by only institutional investors in the Private Placement, certain prospective investors inquired about management’s participation and, therefore, on September 11, 2012, the Board approved a form of subscription agreement through which directors and executive officers of the Company and/or the Bank could subscribe for shares of Series A Preferred Stock in the Private Placement.

Also in September, the Board began to discuss the potential need for bridge capital by the end of the quarter in order for the Bank to maintain its adequately capitalized level as defined by federal regulations, since the Private Placement had not yet been consummated. On September 25, 2012, the Board approved a bridge financing involving the sale of an aggregate of 5,000 shares of a newly designated class of preferred stock, the Series B Preferred Stock. In order to provide the Company with additional capital on an expedited basis, the Company and CapGen entered into a subscription agreement on September 27, 2012 under which the Company sold to CapGen 5,000 shares of Series B Preferred Stock, for an aggregate purchase price of $5 million (the “Series B Sale”). The Series B Sale was exempt from registration under the Securities Act of 1933, as amended (the “Securities Act”), pursuant to Section 4(a)(2) of the Securities Act and Rule 506 of Regulation D promulgated thereunder.

In connection with the Series B Sale and also on September 27, 2012, the Company and CapGen entered into an exchange agreement (the “Original Exchange Agreement”) whereby the Company agreed to exchange CapGen’s shares of Series B Preferred Stock issued in the Series B Sale for shares of Series A Preferred Stock simultaneously with the issuance of shares of Series A Preferred Stock in the Private Placement, unless such shares of Series B Preferred Stock are first redeemed by the Company. Under the terms of the Original Exchange Agreement, all issued and outstanding shares of Series B Preferred Stock were to be exchanged for the number of shares of Series A Preferred Stock having an aggregate liquidation preference equal to the aggregate Series B liquidation preference. The liquidation preference for the Series B Preferred Stock is equal to $1,000 per share, plus any accrued but unpaid dividends, if any, on such share.

At September 30, 2012, the Company did not meet minimum Federal Reserve capital requirements, though the Bank was still considered adequately capitalized.

Through October and November 2012, Sandler and the Company continued discussions with prospective investors in the Private Placement. Some of the prospective investors negotiated changes to the Original Stock

15

Table of Contents

Purchase Agreement and related Private Placement documents, including the amendment to the Articles of Incorporation designating the Series A Preferred Stock. Other changes to the Original Stock Purchase Agreement and other transaction documents were made in response to regulatory concerns. In October and November, the Board met and discussed the status of the transaction, and in October the Board was provided with interim drafts of the transaction documents being negotiated by certain investors. Over this time period, potential investors were provided the opportunity to complete their independent due diligence of the Company and the market. This time also afforded the Bank an opportunity to begin a plan to enter into a loan sale transaction that would reduce classified assets on a concurrent path with the consummation of the capital raise. Loan sale data was gathered in October and due diligence on the asset pool was completed by November 16th with a tentative purchase price established subject to the negotiation of a definitive asset purchase agreement. This asset sale was ultimately completed immediately prior to the closing of the Private Placement; the asset purchaser was also an investor in the Private Placement.

In early December, as negotiations with the investors were being finalized, the Board delegated to the Pricing Committee the authority to approve the final transaction documents, in addition to the initial conversion price and conversion rate of the Series A Preferred Stock.

On December 13, 2012, CapGen received approval from the Federal Reserve to increase its investment in the Company up to 49.9%.

On December 19, 2012, Hovde delivered to the Board a fairness opinion stating that a conversion price of $0.50 is fair, from a financial point of view, to the Company’s shareholders. On the same date, the Pricing Committee approved the initial conversion price of $0.50 and the initial conversion rate of 2,000 shares of Common Stock and/or Nonvoting Common Stock for each outstanding share of Series A Preferred Stock, and approved substantially final forms of the Stock Purchase Agreement (which amended and restated the Original Stock Purchase Agreement), the Series A Designation and other transaction documents. The initial conversion price and initial conversion rate remain subject to customary anti-dilution adjustments under the Series A Designation.

On December 31, 2012, the Company entered into the Stock Purchase Agreement with CapGen and the other accredited investors named therein, and on the same date closed the sale to such investors under the agreement, of 50,000 shares of Series A Preferred Stock at a purchase price of $1,000 per share. Included in the 50,000 shares of Series A Preferred Stock were the 5,000 shares of Series A Preferred Stock issued in the Exchange to CapGen under the amended and restated Exchange Agreement dated as of the same date. Under the Exchange Agreement, CapGen received one share of Series A Preferred Stock for each share of Series B Preferred Stock owned prior to the Exchange. Also on December 31, 2012, the Company accepted Subscriptions from each of ten of its executive officers, directors and other related persons, for the sale of an aggregate of 2,265 shares of Series A Preferred Stock; such shares of Series A Preferred Stock were sold for $1,000 per share and were part of the 50,000 shares of Series A Preferred Stock sold in the Private Placement.

The Private Placement was exempt from registration under the Securities Act pursuant to Section 4(a)(2) of the Securities Act and Rule 506 of Regulation D promulgated thereunder.

NASDAQ Shareholder Approval Requirement

Because our Common Stock is listed on the NASDAQ Stock Market, we are subject to the NASDAQ Stock Market Rules. NASDAQ Stock Market Rule 5635 requires shareholder approval prior to the issuance of securities in connection with a transaction, other than a public offering, involving the sale, issuance or potential issuance by a company of common stock, or securities convertible into or exercisable for common stock, equal to 20% or more of the common stock or 20% or more of the voting power outstanding before the issuance for less than the greater of book value or market value of the stock. Rule 5635 also requires shareholder approval for certain equity compensation arrangements. Under NASDAQ interpretations of Rule 5635, the issuance of common stock or securities convertible into or exercisable for common stock by a company to its directors, officers or employees in a private placement at a price less than the market value of the stock is considered a form of “equity compensation” by NASDAQ and requires shareholder approval.

16

Table of Contents

The approximately 100 million new shares of Common Stock and Nonvoting Common Stock to be issued upon Conversion of the Series A Preferred Stock, including shares to be issued to certain of the Company’s directors and executive officers (and their related interests), will exceed 20% of the outstanding Common Stock and voting power outstanding prior to the closing of the Private Placement and is expected to exceed 20% of the Common Stock and voting power outstanding prior to the Conversion. The $0.50 per share conversion price for the Series A Preferred Stock was less than the book value and market price per share of our Common Stock at the time of the closing of the Private Placement, and is expected to be less than the book value and market price per share of the Common Stock immediately prior to the Conversion. Therefore, shareholder approval is required pursuant to NASDAQ Stock Market Rule 5635.

The following table shows the amount of shares of Series A Preferred Stock purchased by each of the Company’s directors and executive officers (directly or indirectly) in the Private Placement, the aggregate number of shares of Common Stock and Nonvoting Common Stock into which the shares of Series A Preferred Stock will convert, and the amount of “equity compensation” as interpreted under NASDAQ Stock Market Rule 5635 to each such person as a result of such purchase.

Name and Title | Number of Series A Preferred Shares Purchased | Aggregate Number of Shares of Common Stock and Nonvoting Common Stock Issuable Upon Conversion of Series A Preferred Shares | Aggregate Difference between Market Price and Conversion Price(1) | |||||||||