|

Exhibit 99.1

|

Howard Weil Energy Conference

Alan Armstrong, Chief Executive Officer

March 25, 2014

Forward-looking statements

The reports, filings, and other public announcements of The Williams Companies, Inc. (Williams) and Williams Partners L.P. (W PZ) may contain or incorporate by reference statements that do not directly or exclusively relate to historical facts. Such statements are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We make these forward-looking statements in reliance on the safe harbor protections provided under the Private Securities Litigation Reform Act of 1995. You typically can identify forward-looking statements by various forms of words such as “anticipates,” “believes,” “seeks,” “could,” “may,” “should,” “continues,” “estimates,” “expects,” “forecasts,” “intends,” “might,” “goals,” “objectives,” “targets,” “planned,” “potential,” “projects,” “scheduled,” “will,” “assumes,” “guidance,” “outlook,” “in service date” or other similar expressions. These forward-looking statements are based on management’s beliefs and assumptions and on information currently available to management and include, among others, statements regarding:

Amounts and nature of future capital expenditures; Expansion and growth of our business and operations; Financial condition and liquidity; Business strategy; Cash flow from operations or results of operations;

The levels of dividends to Williams stockholders and of cash distributions to WPZ unitholders; Natural gas, natural gas liquids, and olefins prices, supply, and demand; and Demand for our services.

Forward-looking statements are based on numerous assumptions, uncertainties and risks that could cause future events or results to be materially different from those stated or implied in this presentation. Many of the factors that will determine these results are beyond our ability to control or predict. Specific factors that could cause actual results to differ from results contemplated by the forward-looking statements include, among others, the following:

Whether Williams has sufficient cash to enable it to pay current and expected levels of dividends;

Whether WPZ has sufficient cash from operations to enable it to pay current and expected levels of cash distributions, if any, following establishment of cash reserves and payment of fees and expenses, including payments to WPZ’s general partner;

Availability of supplies, market demand, and volatility of prices;

Inflation, interest rates, and fluctuation in foreign exchange rates and general economic conditions (including future disruptions and volatility in the global credit markets and the impact of these events on our customers and suppliers); The strength and financial resources of our competitors and the effects of competition;

© 2014 The Williams Companies, Inc. All rights reserved.

2 Howard Weil Energy Conference | 3/25/14

Forward-looking statements continued

Whether we are able to successfully identify, evaluate and execute investment opportunities;

Ability to acquire new businesses and assets and successfully integrate those operations and assets into our existing businesses, as well as successfully expand our facilities; Development of alternative energy sources; The impact of operational and development hazards and unforeseen interruptions; Costs of, changes in, or the results of laws, government regulations (including safety and environmental regulations), environmental liabilities, litigation, and rate proceedings;

Williams’ costs and funding obligations for defined benefit pension plans and other postretirement benefit plans sponsored by its affiliates; WPZ’s allocated costs for defined benefit pension plans and other post retirement benefit plans sponsored by its affiliates;

Changes in maintenance and construction costs; Changes in the current geopolitical situation;

Our exposure to the credit risk of our customers and counterparties;

Risks related to financing, including restrictions stemming from our debt agreements, future changes in our credit ratings and the availability and cost of capital; The amount of cash distributions from and capital requirements of our investments and joint ventures in which we participate; Risks associated with weather and natural phenomena, including climate conditions; Acts of terrorism, including cybersecurity threats and related disruptions; and Additional risks described in our filings with the Securities and Exchange Commission (SEC).

Given the uncertainties and risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement, we caution investors not to unduly rely on our forward-looking statements. We disclaim any obligations to and do not intend to update the above list or to announce publicly the result of any revisions to any of the forward-looking statements to reflect future events or developments.

In addition to causing our actual results to differ, the factors listed above may cause our intentions to change from those statements of intention set forth in this announcement. Such changes in our intentions may also cause our results to differ. We may change our intentions, at any time and without notice, based upon changes in such factors, our assumptions, or otherwise.

With respect to WPZ, limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which WPZ is subject are similar to those that would be faced by a corporation engaged in a similar business.

Investors are urged to closely consider the disclosures and risk factors in Williams’ and WPZ’s annual reports on Form 10-K filed with the SEC on Feb. 26, 2014, and each of our quarterly reports on Form 10-Q available from our offices or from our websites at www.williams.com and www.williamslp.com.

© 2014 The Williams Companies, Inc. All rights reserved.

3 Howard Weil Energy Conference | 3/25/14

Built to deliver long-term growth

Winning strategy

Be the premier provider of large-scale infrastructure designed to maximize the opportunities created by the vastly greater supply of natural gas and natural gas products now known to exist in

North America’s unconventional

Underpinned by scale, competitive advantage

Be big – the No. 1 or No. 2 largest – in gathering, processing and transportation in basins and markets where we operate Grow position in areas where we have unique competitive advantages Maximize returns in established markets where we have the No. 1 or No. 2 position

Well-aligned with commodity environment

Low prices grow demand in natural gas, NGLs, olefins – all are infrastructure-constrained Natural gas products price-advantaged against crude and naphtha products Rapidly growing fee-based business Well-positioned to capture opportunities associated with ethane cracking

© 2014 The Williams Companies, Inc. All rights reserved.

4 Howard Weil Energy Conference | 3/25/14

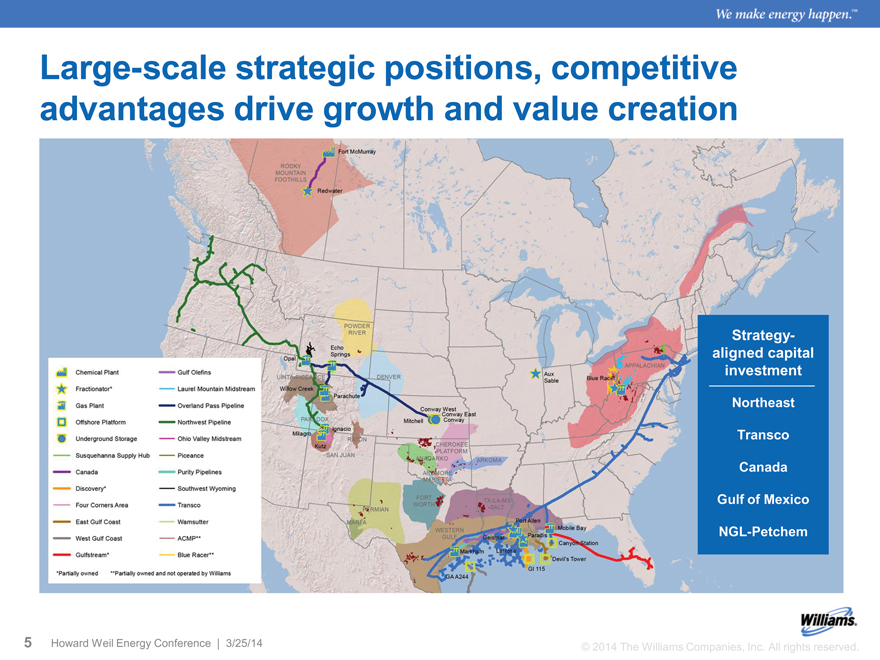

Large-scale strategic positions, competitive advantages drive growth and value creation

Strategy-aligned capital investment

Northeast Transco Canada Gulf of Mexico NGL-Petchem

© 2014 The Williams Companies, Inc. All rights reserved.

5 Howard Weil Energy Conference | 3/25/14

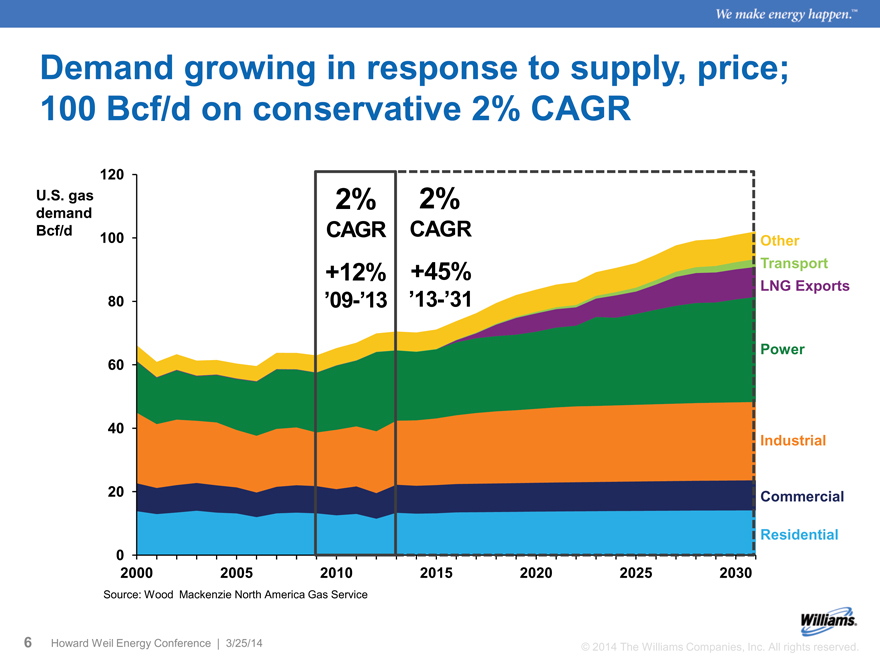

Demand growing in response to supply, price;

100 Bcf/d on conservative 2% CAGR

U.S. gas demand Bcf/d

2%

CAGR

+12%

’09-’13

2%

CAGR

+45%

’13-’31

Other Transport LNG Exports

Power

Industrial

Commercial

Residential

120 100 80 60 40 20 0

2000 2005 2010 2015 2020 2025 2030

Source: Wood Mackenzie North America Gas Service

© 2014 The Williams Companies, Inc. All rights reserved.

6 Howard Weil Energy Conference | 3/25/14

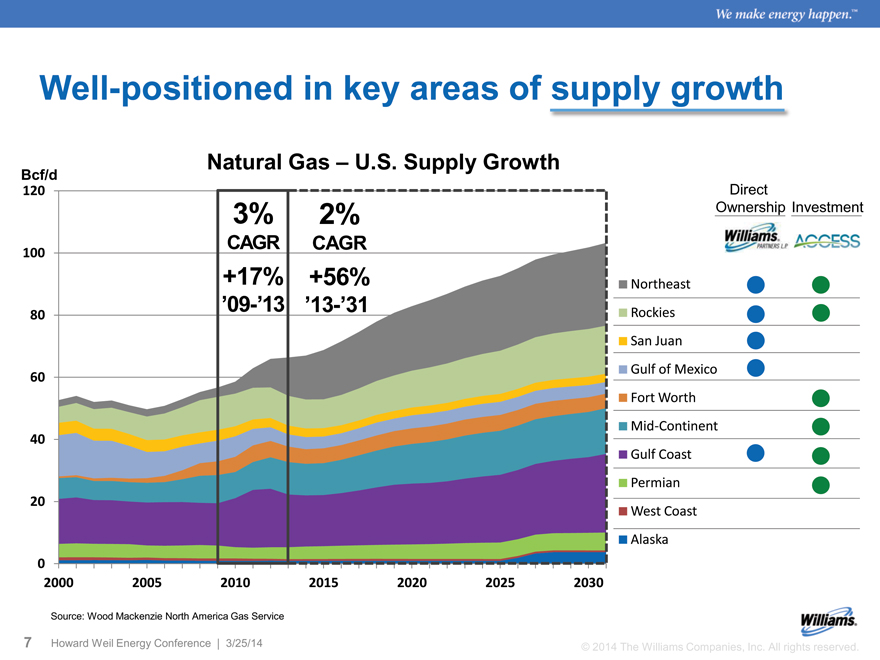

Well-positioned in key areas of supply growth

Direct

Ownership Investment

Northeast

Rockies

San Juan

Gulf of Mexico

Fort Worth

Mid-Continent

Gulf Coast

Permian

West Coast

Alaska

Natural Gas – U.S. Supply Growth

Bcf/d

120

3% 2%

100 CAGR CAGR

+17% +56%

80 ’09-’13 ’13-’31

60

40

20

0

2000 2005 2010 2015 2020 2025 2030

Source: Wood Mackenzie North America Gas Service

© 2014 The Williams Companies, Inc. All rights reserved.

7 Howard Weil Energy Conference | 3/25/14

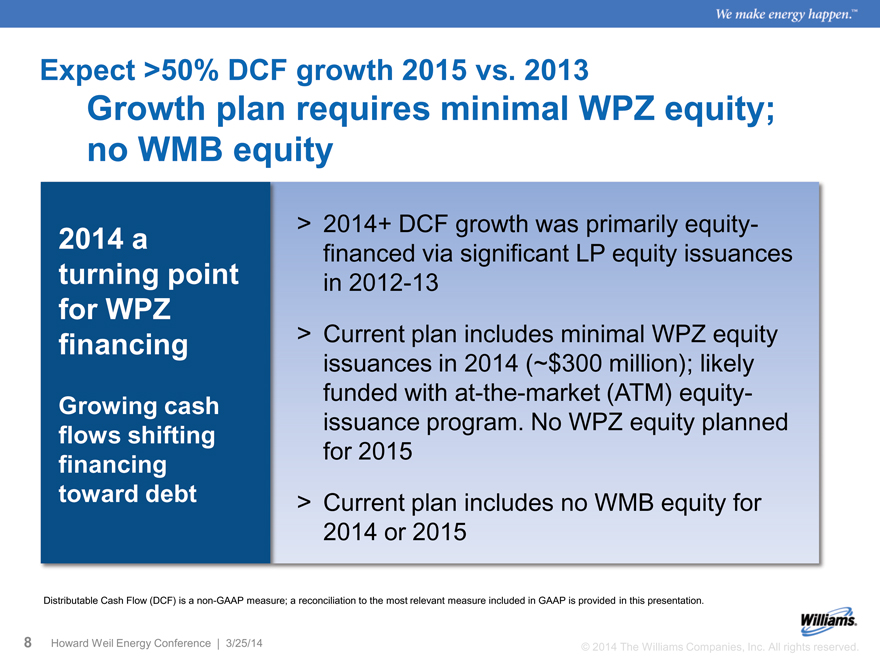

Expect >50% DCF growth 2015 vs. 2013

Growth plan requires minimal WPZ equity; no WMB equity

2014 a > 2014+ DCF growth was primarily equity-

financed via significant LP equity issuances

turning point in 2012-13

for WPZ

financing > Current plan includes minimal WPZ equity

issuances in 2014 (~$300 million); likely

Growing cash funded with at-the-market (ATM) equity-

flows shifting issuance program. No WPZ equity planned

financing for 2015

toward debt > Current plan includes no WMB equity for

2014 or 2015

Distributable Cash Flow (DCF) is a non-GAAP measure; a reconciliation to the most relevant measure included in GAAP is provided in this presentation.

8 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

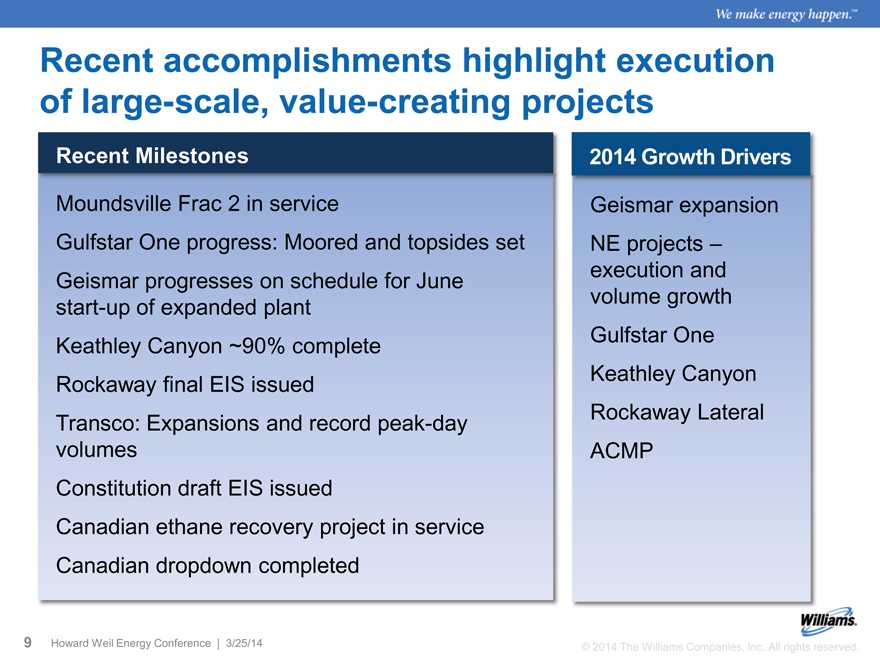

Recent accomplishments highlight execution of large-scale, value-creating projects

Recent Milestones 2014 Growth Drivers

Moundsville Frac 2 in service Geismar expansion

Gulfstar One progress: Moored and topsides set NE projects –

Geismar progresses on schedule for June execution and

start-up of expanded plant volume growth

Keathley Canyon ~90% complete Gulfstar One

Rockaway final EIS issued Keathley Canyon

Transco: Expansions and record peak-day Rockaway Lateral

volumes ACMP

Constitution draft EIS issued

Canadian ethane recovery project in service

Canadian dropdown completed

9 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

Major-project execution in action

Moundsville Frac 2

In-service

Gulfstar One

Moored in place and topsides set Hook-up and commissioning underway Tieback expansion fully contracted to serve Gunflint producers

Video replay available on williams.com

10 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

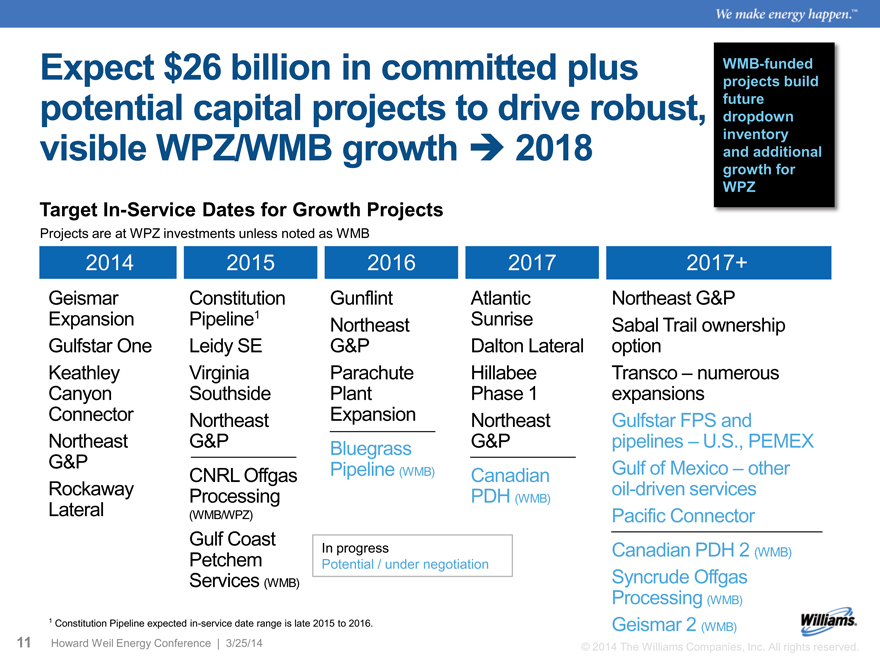

Expect $26 billion in committed plus potential capital projects to drive robust, visible WPZ/WMB growth 2018

Target In-Service Dates for Growth Projects

Projects are at WPZ investments unless noted as WMB

2014 2015 2016 2017 2017+

Geismar Constitution Gunflint Atlantic Northeast G&P

Expansion Pipeline1 Northeast Sunrise Sabal Trail ownership

Gulfstar One Leidy SE G&P Dalton Lateral option

Keathley Virginia Parachute Hillabee Transco – numerous

Canyon Southside Plant Phase 1 expansions

Connector Northeast Expansion Northeast Gulfstar FPS and

Northeast G&P Bluegrass G&P pipelines – U.S., PEMEX

G&P Pipeline Gulf of Mexico – other

CNRL Offgas (WMB) Canadian

Rockaway Processing PDH (WMB) oil-driven services

Lateral (WMB/WPZ) Pacific Connector

Gulf Coast In progress Canadian PDH 2 (WMB)

Petchem Potential / under negotiation

Services (WMB) Syncrude Offgas

Processing (WMB)

1 Constitution Pipeline expected in-service date range is late 2015 to 2016. Geismar 2 (WMB)

11 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

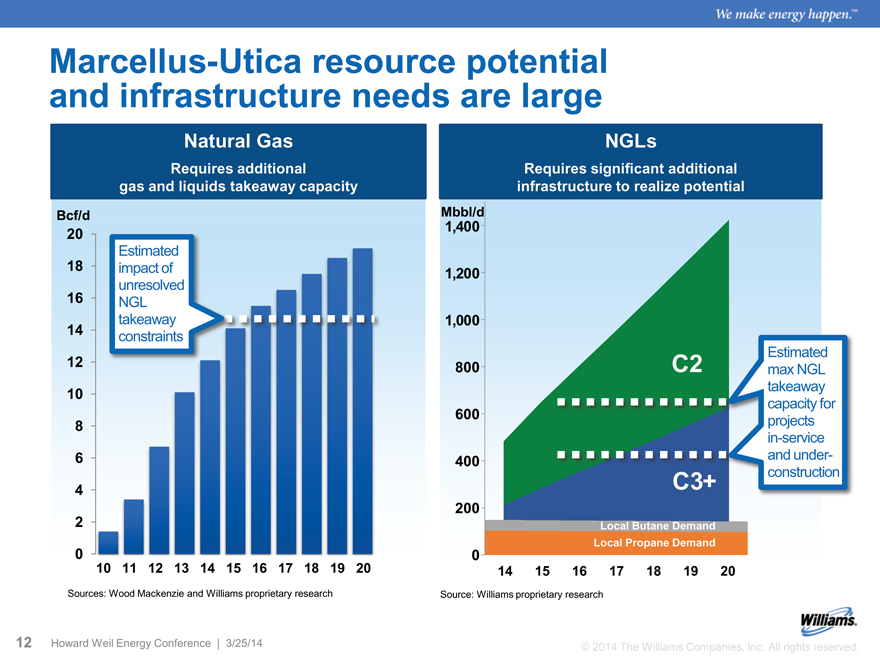

Marcellus-Utica resource potential and infrastructure needs are large

Natural Gas NGLs

Requires additional Requires significant additional

gas and liquids takeaway capacity infrastructure to realize potential

Bcf/d

20

Estimated

18 impact of

unresolved

16 NGL

takeaway

14 constraints

12

10

8

6

4

2

0

10 11 12 13 14 15 16 17 18 19 20

Mbbl/d

1,400

1,200

1,000

Estimated

800 C2 max NGL

takeaway

capacity for

600 projects

in-service

400 and under-

C3+ construction

200

Local Butane Demand

Local Propane Demand

0

Sources: Wood Mackenzie and Williams proprietary research Source: Williams proprietary research

12 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

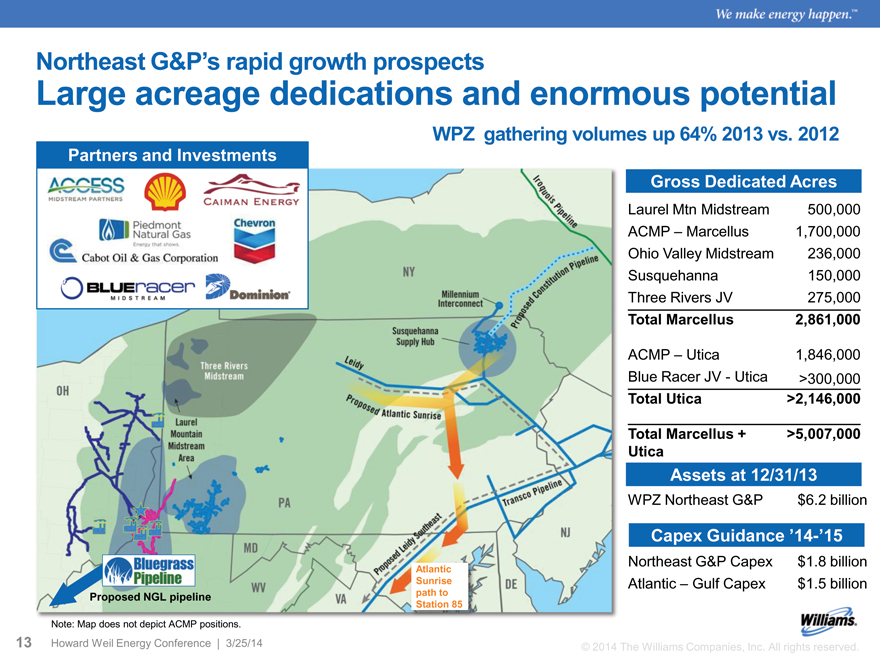

Northeast G&P’s rapid growth prospects

Large acreage dedications and enormous potential

WPZ gathering volumes up 64% 2013 vs. 2012

Partners and Investments

Proposed NGL pipeline

Note: Map does not depict ACMP positions.

13 Howard Weil Energy Conference | 3/25/14

Atlantic Sunrise path to Station 85

Gross Dedicated Acres

Laurel Mtn Midstream 500,000

ACMP – Marcellus 1,700,000

Ohio Valley Midstream 236,000

Susquehanna 150,000

Three Rivers JV 275,000

Total Marcellus 2,861,000

ACMP – Utica 1,846,000

Blue Racer JV - Utica >300,000

Total Utica >2,146,000

Total Marcellus + >5,007,000

Utica

Assets at 12/31/13

WPZ Northeast G&P $ 6.2 billion

Capex Guidance ’14-’15

Northeast G&P Capex $ 1.8 billion

Atlantic – Gulf Capex $ 1.5 billion

© 2014 The Williams Companies, Inc. All rights reserved.

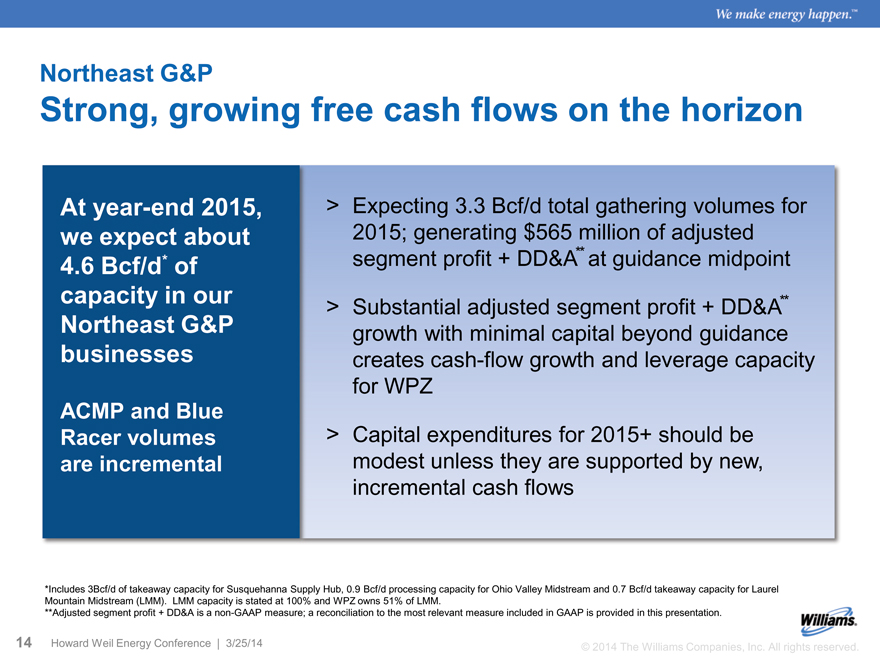

Northeast G&P

Strong, growing free cash flows on the horizon

At year-end 2015, > Expecting 3.3 Bcf/d total gathering volumes for

we expect about 2015; generating $565 million of adjusted

4.6 Bcf/d* of segment profit + DD&A** at guidance midpoint

capacity in our > Substantial adjusted segment profit + DD&A**

Northeast G&P growth with minimal capital beyond guidance

businesses creates cash-flow growth and leverage capacity

for WPZ

ACMP and Blue

Racer volumes > Capital expenditures for 2015+ should be

are incremental modest unless they are supported by new,

incremental cash flows

*Includes 3Bcf/d of takeaway capacity for Susquehanna Supply Hub, 0.9 Bcf/d processing capacity for Ohio Valley Midstream and 0.7 Bcf/d takeaway capacity for Laurel Mountain Midstream (LMM). LMM capacity is stated at 100% and WPZ owns 51% of LMM.

**Adjusted segment profit + DD&A is a non-GAAP measure; a reconciliation to the most relevant measure included in GAAP is provided in this presentation.

14 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

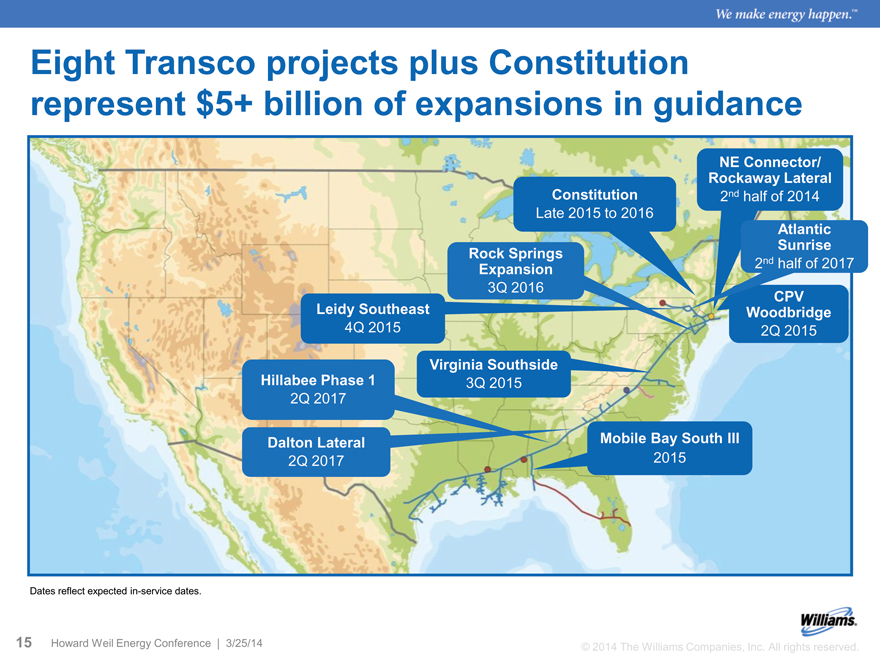

Eight Transco projects plus Constitution represent $5+ billion of expansions in guidance

NE Connector/

Rockaway Lateral

Constitution 2nd half of 2014

Late 2015 to 2016

Atlantic

Rock Springs Sunrise

Expansion 2nd half of 2017

3Q 2016 CPV

Leidy Southeast Woodbridge

4Q 2015 2Q 2015

Virginia Southside

Hillabee Phase 1 3Q 2015

2Q 2017

Dalton Lateral Mobile Bay South III

2Q 2017 2015

Dates reflect expected in-service dates.

15 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

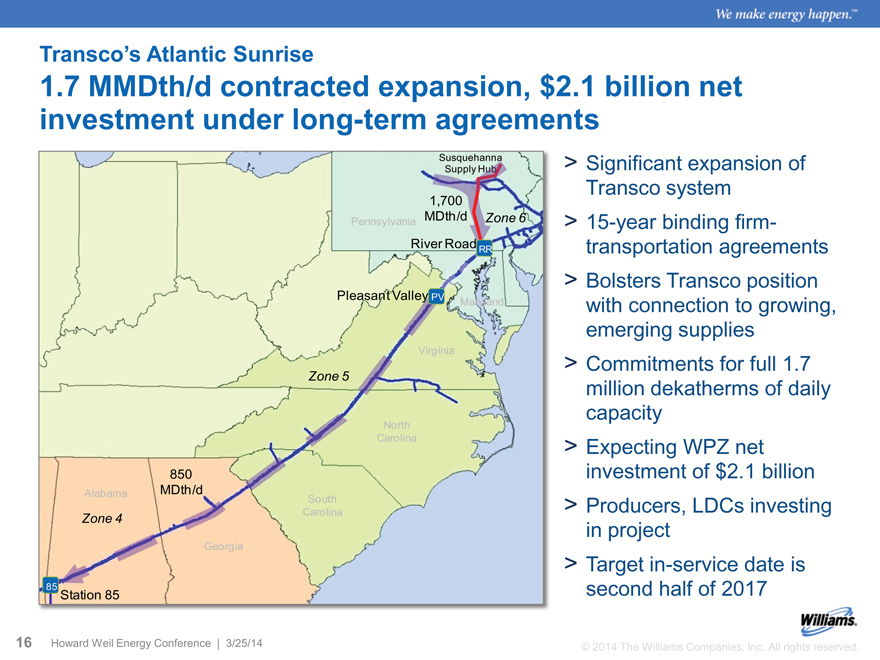

Transcos Atlantic Sunrise

1.7 MMDth/d contracted expansion, $2.1 billion net investment under long-term agreements

Significant expansion of Transco system 15-year binding firm-transportation agreements Bolsters Transco position with connection to growing, emerging supplies Commitments for full 1.7 million dekatherms of daily capacity Expecting WPZ net investment of $2.1 billion Producers, LDCs investing in project Target in-service date is second half of 2017

Susquehanna

Supply Hub

1,700

Pennsylvania MDth/d Zone 6

River Road RR

Pleasant Valley PV Maryland

Virginia

Zone 5

North

Carolina

850

Alabama MDth/d

South

Zone 4 Carolina

Georgia

85 Station 85

© 2014 The Williams Companies, Inc. All rights reserved.

Howard Well Energy Conference 3/25/14

16

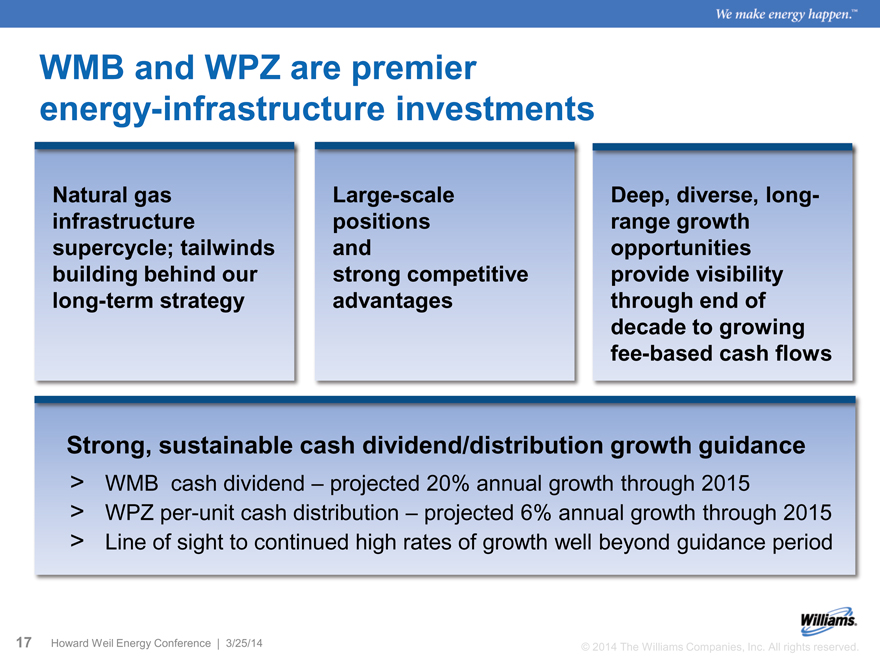

WMB and WPZ are premier energy-infrastructure investments

Natural gas Large-scale Deep, diverse, long-

infrastructure positions range growth

supercycle; tailwinds and opportunities

building behind our strong competitive provide visibility

long-term strategy advantages through end of

decade to growing

fee-based cash flows

Strong, sustainable cash dividend/distribution growth guidance

WMB cash dividend – projected 20% annual growth through 2015

WPZ per-unit cash distribution – projected 6% annual growth through 2015

Line of sight to continued high rates of growth well beyond guidance period

17 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

WPZ Non-GAAP Reconciliations

WPZ non-GAAP disclaimer

This presentation includes certain financial measures, adjusted segment profit, adjusted segment profit + DD&A, and distributable cash flow that are non-GAAP financial measures as defined under the rules of the Securities and Exchange Commission.

For Williams Partners L.P., adjusted segment profit excludes items of income or loss that we characterize as unrepresentative of our ongoing operations. Adjusted segment profit + DD&A is further adjusted to add back depreciation and amortization expense. Management believes these measures provide investors meaningful insight into Williams Partners L.P.’s results from ongoing operations.

For Williams Partners L.P. we define distributable cash flow as net income plus depreciation and amortization and cash distributions from our equity investments less our earnings from equity investments, income attributable to noncontrolling interests and maintenance capital expenditures. We also adjust for payments and/or reimbursements under omnibus agreements with Williams and certain other adjustments. Total distributable cash flow is reduced by any amounts associated with operations which occurred prior to our ownership of the underlying assets to arrive at distributable cash flow attributable to partnership operations.

This presentation is accompanied by a reconciliation of these non-GAAP financial measures to their nearest GAAP financial measures. Management uses these financial measures because they are accepted financial indicators used by investors to compare company performance. In addition, management believes that these measures provide investors an enhanced perspective of the operating performance of the Partnership’s assets and the cash that the business is generating. Neither adjusted segment profit, adjusted segment profit + DD&A, nor distributable cash flow are intended to represent cash flows for the period, nor are they presented as an alternative to net income or cash flow from operations. They should not be considered in isolation or as substitutes for a measure of performance prepared in accordance with United States generally accepted accounting principles.

19 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

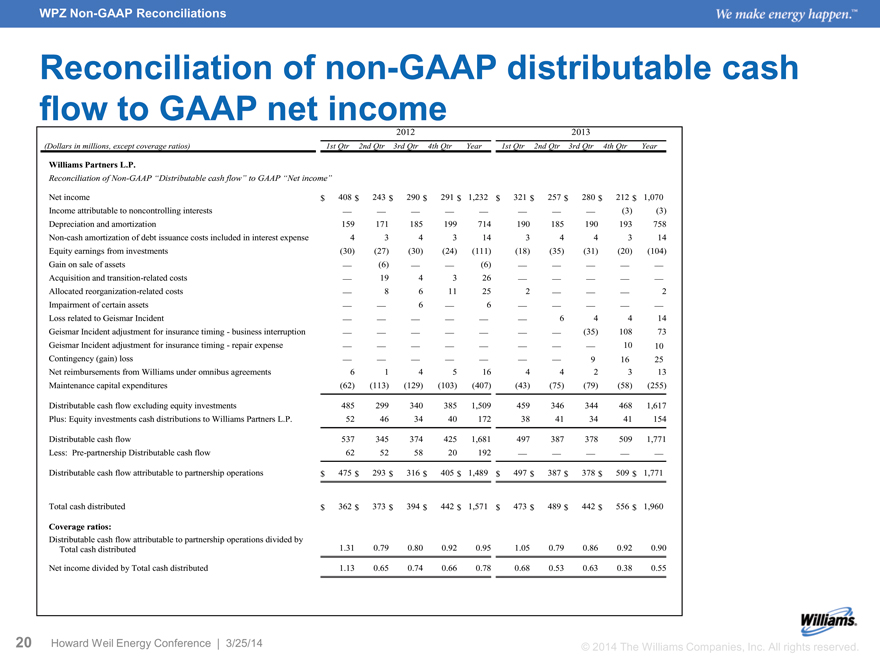

Reconciliation of non-GAAP distributable cash flow to GAAP net income

2012 2013

(Dollars in millions, except coverage ratios) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year

Williams Partners L.P.

Reconciliation of Non-GAAP “Distributable cash flow” to GAAP “Net income”

Net income $ 408 $ 243 $ 290 $ 291 $ 1,232 $ 321 $ 257 $ 280 $ 212 $ 1,070

Income attributable to noncontrolling interests — — — — — — — — (3) (3)

Depreciation and amortization 159 171 185 199 714 190 185 190 193 758

Non-cash amortization of debt issuance costs included in interest expense 4 3 4 3 14 3 4 4 3 14

Equity earnings from investments (30) (27) (30) (24) (111) (18) (35) (31) (20) (104)

Gain on sale of assets — (6) — — (6) — — — — —

Acquisition and transition-related costs — 19 4 3 26 — — — — —

Allocated reorganization-related costs — 8 6 11 25 2 — — — 2

Impairment of certain assets — — 6 — 6 — — — — —

Loss related to Geismar Incident — — — — — — 6 4 4 14

Geismar Incident adjustment for insurance timing - business interruption — — — — — — — (35) 108 73

Geismar Incident adjustment for insurance timing - repair expense — — — — — — — — 10 10

Contingency (gain) loss — — — — — — — 9 16 25

Net reimbursements from Williams under omnibus agreements 6 1 4 5 16 4 4 2 3 13

Maintenance capital expenditures (62) (113) (129) (103) (407) (43) (75) (79) (58) (255)

Distributable cash flow excluding equity investments 485 299 340 385 1,509 459 346 344 468 1,617

Plus: Equity investments cash distributions to Williams Partners L.P. 52 46 34 40 172 38 41 34 41 154

Distributable cash flow 537 345 374 425 1,681 497 387 378 509 1,771

Less: Pre-partnership Distributable cash flow 62 52 58 20 192 — — — — —

Distributable cash flow attributable to partnership operations $ 475 $ 293 $ 316 $ 405 $ 1,489 $ 497 $ 387 $ 378 $ 509 $ 1,771

Total cash distributed $ 362 $ 373 $ 394 $ 442 $ 1,571 $ 473 $ 489 $ 442 $ 556 $ 1,960

Coverage ratios:

Distributable cash flow attributable to partnership operations divided by

Total cash distributed 1.31 0.79 0.80 0.92 0.95 1.05 0.79 0.86 0.92 0.90

Net income divided by Total cash distributed 1.13 0.65 0.74 0.66 0.78 0.68 0.53 0.63 0.38 0.55

20 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

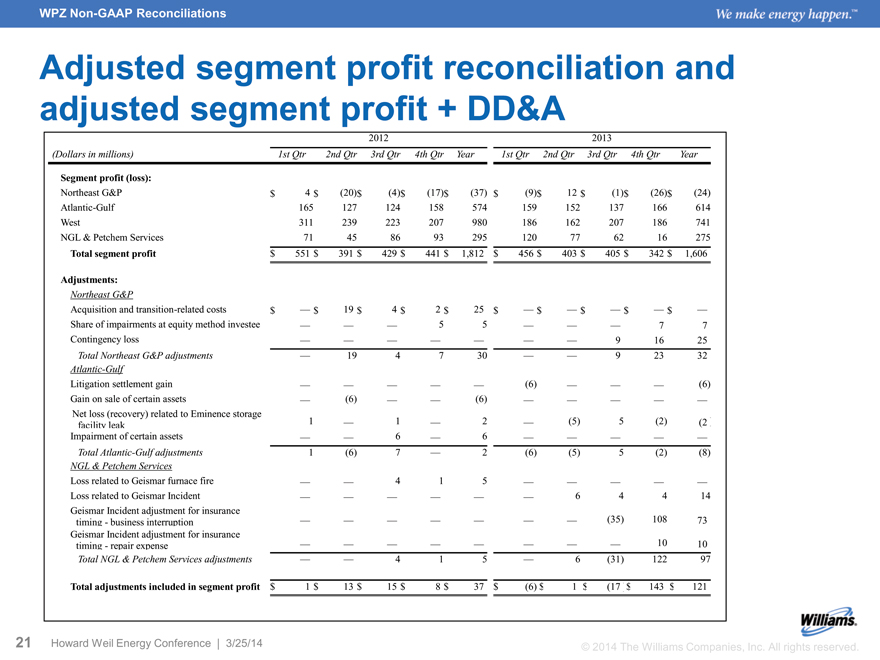

Adjusted segment profit reconciliation and adjusted segment profit + DD&A

2012 2013

(Dollars in millions) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year

Segment profit (loss):

Northeast G&P $ 4 $ (20)$ (4)$ (17)$ (37) $ (9)$ 12 $ (1)$ (26)$ (24)

Atlantic-Gulf 165 127 124 158 574 159 152 137 166 614

West 311 239 223 207 980 186 162 207 186 741

NGL & Petchem Services 71 45 86 93 295 120 77 62 16 275

Total segment profit $ 551 $ 391 $ 429 $ 441 $ 1,812 $ 456 $ 403 $ 405 $ 342 $ 1,606

Adjustments:

Northeast G&P

Acquisition and transition-related costs $ — $ 19 $ 4 $ 2 $ 25 $ — $ — $ — $ — $ —

Share of impairments at equity method investee — — — 5 5 — — — 7 7

Contingency loss — — — — — — — 9 16 25

Total Northeast G&P adjustments — 19 4 7 30 — — 9 23 32

Atlantic-Gulf

Litigation settlement gain — — — — — (6) — — — (6)

Gain on sale of certain assets — (6) — — (6) — — — — —

Net loss (recovery) related to Eminence storage

facility leak 1 — 1 — 2 — (5) 5 (2) (2)

Impairment of certain assets — — 6 — 6 — — — — —

Total Atlantic-Gulf adjustments 1 (6) 7 — 2 (6) (5) 5 (2) (8)

NGL & Petchem Services

Loss related to Geismar furnace fire — — 4 1 5 — — — — —

Loss related to Geismar Incident — — — — — — 6 4 4 14

Geismar Incident adjustment for insurance

timing - business interruption — — — — — — — (35) 108 73

Geismar Incident adjustment for insurance

timing - repair expense — — — — — — — — 10 10

Total NGL & Petchem Services adjustments — — 4 1 5 — 6 (31) 122 97

Total adjustments included in segment profit $ 1 $ 13 $ 15 $ 8 $ 37 $ (6) $ 1 $ (17) $ 143 $ 121

21 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

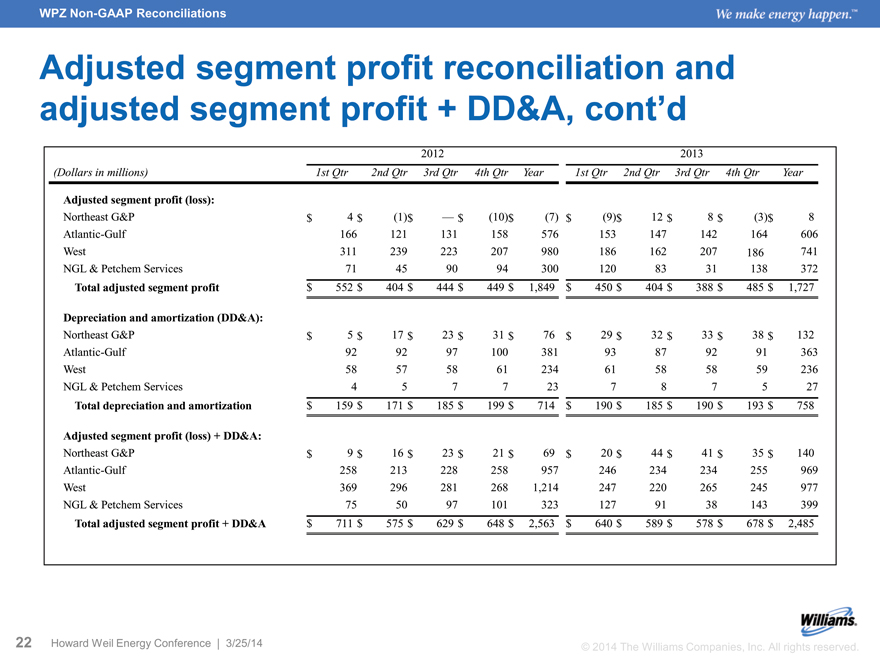

Adjusted segment profit reconciliation and adjusted segment profit + DD&A, cont’d

2012 2013

(Dollars in millions) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year

Adjusted segment profit (loss):

Northeast G&P $ 4 $ (1)$ — $ (10)$ (7) $ (9)$ 12 $ 8 $ (3)$ 8

Atlantic-Gulf 166 121 131 158 576 153 147 142 164 606

West 311 239 223 207 980 186 162 207 186 741

NGL & Petchem Services 71 45 90 94 300 120 83 31 138 372

Total adjusted segment profit $ 552 $ 404 $ 444 $ 449 $ 1,849 $ 450 $ 404 $ 388 $ 485 $ 1,727

Depreciation and amortization (DD&A):

Northeast G&P $ 5 $ 17 $ 23 $ 31 $ 76 $ 29 $ 32 $ 33 $ 38 $ 132

Atlantic-Gulf 92 92 97 100 381 93 87 92 91 363

West 58 57 58 61 234 61 58 58 59 236

NGL & Petchem Services 4 5 7 7 23 7 8 7 5 27

Total depreciation and amortization $ 159 $ 171 $ 185 $ 199 $ 714 $ 190 $ 185 $ 190 $ 193 $ 758

Adjusted segment profit (loss) + DD&A:

Northeast G&P $ 9 $ 16 $ 23 $ 21 $ 69 $ 20 $ 44 $ 41 $ 35 $ 140

Atlantic-Gulf 258 213 228 258 957 246 234 234 255 969

West 369 296 281 268 1,214 247 220 265 245 977

NGL & Petchem Services 75 50 97 101 323 127 91 38 143 399

Total adjusted segment profit + DD&A $ 711 $ 575 $ 629 $ 648 $ 2,563 $ 640 $ 589 $ 578 $ 678 $ 2,485

22 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

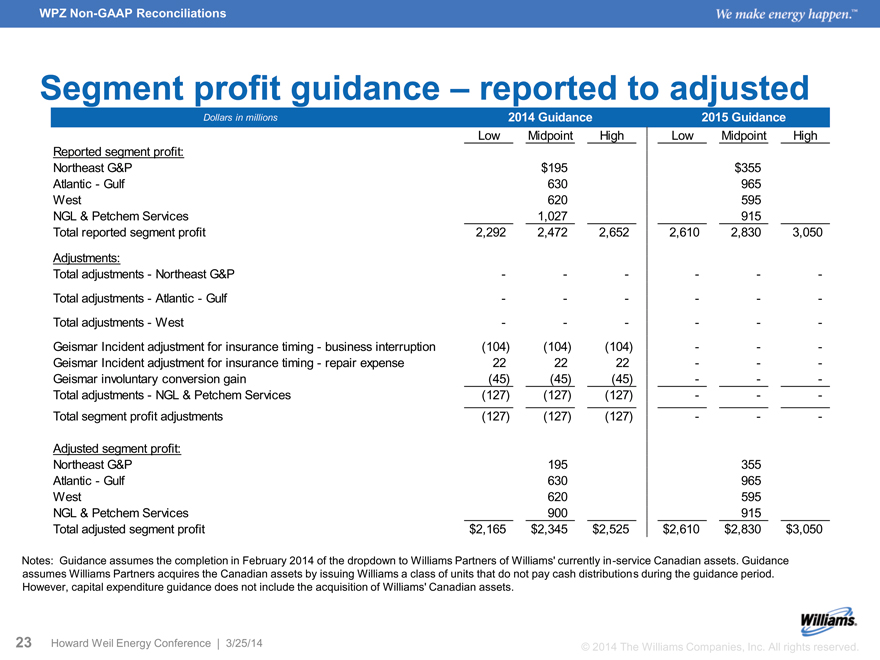

Segment profit guidance – reported to adjusted

Dollars in millions 2014 Guidance 2015 Guidance

Low Midpoint High Low Midpoint High

Reported segment profit:

Northeast G&P $195 $355

Atlantic - Gulf 630 965

West 620 595

NGL & Petchem Services 1,027 915

Total reported segment profit 2,292 2,472 2,652 2,610 2,830 3,050

Adjustments:

Total adjustments - Northeast G&P - - - - - -

Total adjustments - Atlantic - Gulf - - - - - -

Total adjustments - West - - - - - -

Geismar Incident adjustment for insurance timing - business interruption (104) (104) (104) - - -

Geismar Incident adjustment for insurance timing - repair expense 22 22 22 - - -

Geismar involuntary conversion gain (45) (45) (45) - - -

Total adjustments - NGL & Petchem Services (127) (127) (127) - - -

Total segment profit adjustments (127) (127) (127) - - -

Adjusted segment profit:

Northeast G&P 195 355

Atlantic - Gulf 630 965

West 620 595

NGL & Petchem Services 900 915

Total adjusted segment profit $2,165 $2,345 $2,525 $2,610 $2,830 $3,050

Notes: Guidance assumes the completion in February 2014 of the dropdown to Williams Partners of Williams’ currently in-service Canadian assets. Guidance assumes Williams Partners acquires the Canadian assets by issuing Williams a class of units that do not pay cash distributions during the guidance period. However, capital expenditure guidance does not include the acquisition of Williams’ Canadian assets.

23 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

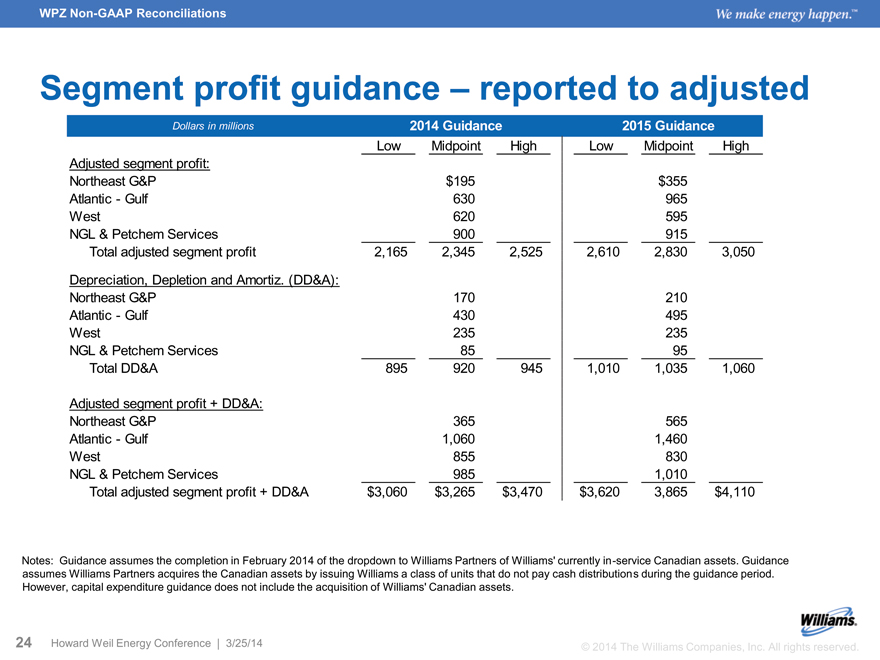

Segment profit guidance – reported to adjusted

Dollars in millions 2014 Guidance 2015 Guidance

Low Midpoint High Low Midpoint High

Adjusted segment profit:

Northeast G&P $195 $355

Atlantic - Gulf 630 965

West 620 595

NGL & Petchem Services 900 915

Total adjusted segment profit 2,165 2,345 2,525 2,610 2,830 3,050

Depreciation, Depletion and Amortiz. (DD&A):

Northeast G&P 170 210

Atlantic - Gulf 430 495

West 235 235

NGL & Petchem Services 85 95

Total DD&A 895 920 945 1,010 1,035 1,060

Adjusted segment profit + DD&A:

Northeast G&P 365 565

Atlantic - Gulf 1,060 1,460

West 855 830

NGL & Petchem Services 985 1,010

Total adjusted segment profit + DD&A $3,060 $3,265 $3,470 $3,620 3,865 $4,110

Notes: Guidance assumes the completion in February 2014 of the dropdown to Williams Partners of Williams’ currently in-service Canadian assets. Guidance assumes Williams Partners acquires the Canadian assets by issuing Williams a class of units that do not pay cash distributions during the guidance period. However, capital expenditure guidance does not include the acquisition of Williams’ Canadian assets.

24 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.

WPZ Non-GAAP Reconciliations

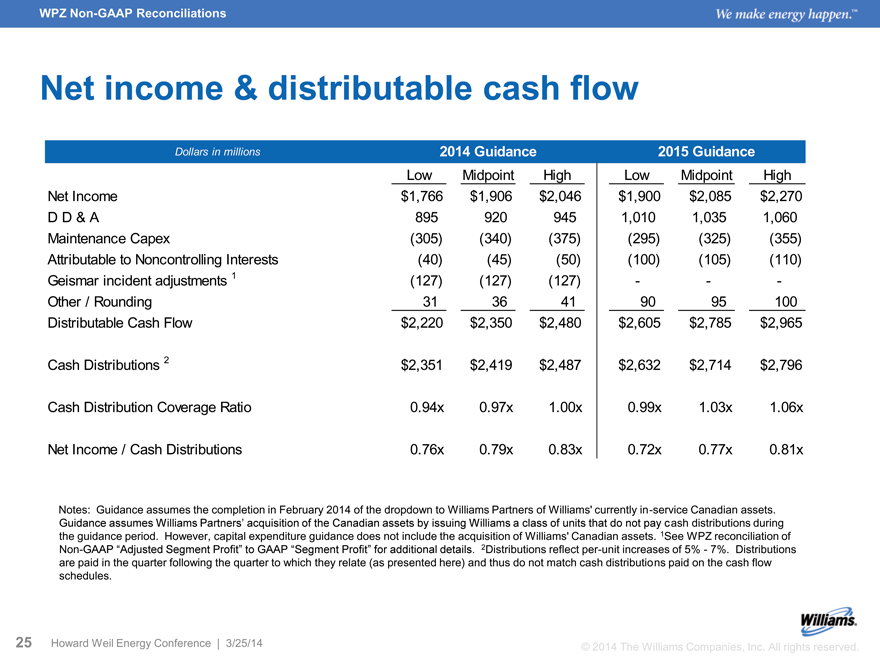

Net income & distributable cash flow

Dollars in millions 2014 Guidance 2015 Guidance

Low Midpoint High Low Midpoint High

Net Income $1,766 $1,906 $2,046 $1,900 $2,085 $2,270

D D & A 895 920 945 1,010 1,035 1,060

Maintenance Capex (305) (340) (375) (295) (325) (355)

Attributable to Noncontrolling Interests (40) (45) (50) (100) (105) (110)

Geismar incident adjustments 1 (127) (127) (127) - - -

Other / Rounding 31 36 41 90 95 100

Distributable Cash Flow $2,220 $2,350 $2,480 $2,605 $2,785 $2,965

Cash Distributions 2 $2,351 $2,419 $2,487 $2,632 $2,714 $2,796

Cash Distribution Coverage Ratio 0.94x 0.97x 1.00x 0.99x 1.03x 1.06x

Net Income / Cash Distributions 0.76x 0.79x 0.83x 0.72x 0.77x 0.81x

Notes: Guidance assumes the completion in February 2014 of the dropdown to Williams Partners of Williams’ currently in-service Canadian assets.

Guidance assumes Williams Partners’ acquisition of the Canadian assets by issuing Williams a class of units that do not pay cash distributions during the guidance period. However, capital expenditure guidance does not include the acquisition of Williams’ Canadian assets. 1See WPZ reconciliation of Non-GAAP “Adjusted Segment Profit” to GAAP “Segment Profit” for additional details. 2Distributions reflect per-unit increases of 5% - 7%. Distributions are paid in the quarter following the quarter to which they relate (as presented here) and thus do not match cash distributions paid on the cash flow schedules.

25 Howard Weil Energy Conference | 3/25/14 © 2014 The Williams Companies, Inc. All rights reserved.