FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13s – 16 or 15d – 16 of

the Securities Exchange Act of 1934

For the month of June 2006

Acambis plc

(Translation of registrant’s name into English)

Peterhouse Technology Park

100 Fulbourn Road

Cambridge CB1 9PT

England

(address of principal executive offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of

Form 20-F or Form 40-F).

Forms 20-F ![]() Form 40-F

Form 40-F ![]()

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is

also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the

Securities Exchange Act of 1934).

Yes ![]() No

No

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with

Rule 12g3-2(b): 82- ).

Enclosure:

Annual Report 2005

A future we can see

Preview

Annual Report 2005

| ||

| ||

| ||

| ||

| ||

| ||

| ||

|

‘We aim to make Acambis one of the world’s leading infectious disease companies. Whilst our current focus is on vaccines, we will consider the development of other biological products in due course. With the cash from our smallpox vaccine contracts, we have developed our infrastructure and increased the investment in our pipeline to generate long-term value for shareholders.

In “Preview”, we lay out our strategy for transforming Acambis into a fully integrated infectious disease company, one that invests in innovative new products to make a difference in the war against infectious diseases.

In “Review”, we report on our progress in 2005.’

ALAN SMITH, CHAIRMAN

About Acambis

Acambis is a biopharmaceutical company operating in the infectious disease arena, with a focus on developing new vaccines. We are headquartered in Cambridge, UK. The majority of our operations are based in the US, with R&D in Cambridge, MA, manufacturing in Canton, MA and Rockville, MD, and sales and marketing in Miami, FL. We are a UK public limited company with shares listed on the LSE since 1995 and on NASDAQ, in the form of ADRs, since 2001. We employ around 290 people.

About this Annual Report

This is the Annual Report for the year ended 31 December 2005. It contains the Annual Report and Financial Statements in accordance with UK regulations. The Annual Report on Form 20-F for the US SEC will be filed separately. References to the Group and Acambis throughout this document relate to Acambis plc and all of its subsidiary and associated undertakings. References to the Company are to Acambis plc, the ultimate holding company. For further information on Acambis, please visit our website at www.acambis.com

Cautionary statement regarding forward-looking statements

Under the safe harbour provisions of the US Private Securities Litigation Reform Act of 1995, the Company cautions investors that any forward-looking statements or projections made in this document are subject to risks and uncertainties that may cause actual results to differ materially from those projected. These forward-looking statements are based on estimates and assumptions made by the management of Acambis and are believed to be reasonable, though are inherently uncertain and difficult to predict. Actual results or experience could differ materially from the forward-looking statements. Factors that may affect the Group’s operations are discussed in the performance review and financial review and the corporate governance statement contained within this Annual Report and in documents as filed with the US SEC from time to time.

Definitions for abbreviations used throughout this document are provided on page 96.

1 |

We have a bold vision of the kind of company we want Acambis to be. This is our long-term, ambitious view of where we want to take the business over the next decade and beyond.

Our vision is to win the war against infectious disease.

Our mission is that, by providing innovative products to protect the world from the ravages of infectious disease, we will create a sustainable company that is focused on making a difference.

We are already helping to protect 200 million lives; there are 6.3 billion more to go...

2 | Strategic goals |

Today, infectious diseases cause 25% of deaths worldwide1. At Acambis, we aim to make a difference by turning scientific innovation into products that can save lives.

Healthcare products for combating infectious diseases range from vaccines and monoclonal antibodies to anti-bacterials, anti-virals and immunoglobulins. Commercially, the total ‘anti-infectives’ market is worth an estimated $50bn2, making it the third largest pharmaceutical market. Our immediate focus is on vaccines, which is the fastest-growing infectious disease sector.

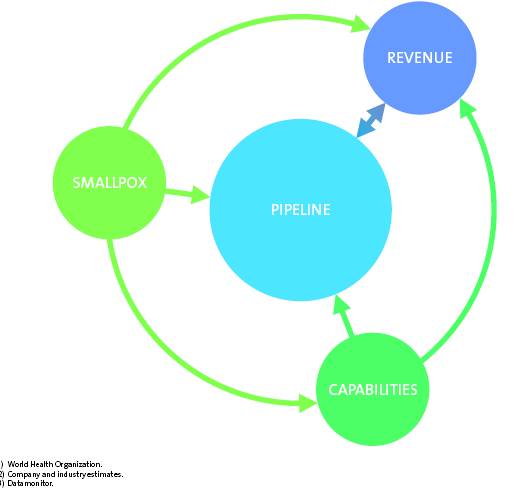

OUR STRATEGY

With the cash generated by our smallpox

franchise and Vivotif® sales, we are investing

in driving our pipeline forward and building

key capabilities to maximise long-term value.

3 | ||

| A clear, simple strategy | |

|

| |

| Four key drivers |

|

|

| |

| Why vaccines? |

|

|

|

‘Vaccines are back | WHY VACCINES? | ||

| GORDON CAMERON, CHIEF EXECUTIVE OFFICER | |||

|

| ||

| Vaccines used to be the ‘poor cousin’ of the pharmaceutical industry; low margin products made by local producers for cents per dose did little to encourage investment in vaccine innovation. In the 1980s and early 1990s, this situation was compounded by rising costs, increasing litigation and ever-more-burdensome regulatory requirements, which conspired to push companies out of the industry. Now, vaccines are being driven back to the top of the healthcare, pharmaceutical and political agenda. From biodefence to pandemic influenza, from hospital-acquired infections to emerging viruses and bacteria, vaccines are the front line of public health. And the statistics prove it: the prophylactic vaccine market has increased rapidly in recent years, reaching an estimated $8.5bn in 2004.3 Over the next decade, that market is expected to grow by a further 15% per annum, driven by three key factors: the launch of new vaccines; greater market penetration; and a paradigm shift around pricing. With new products expected to account for more than 50% of that growth and the groundwork on pricing already laid by the pharmaceutical companies, the potential for companies like Acambis is significant. |

| |

As part of our strategy to build Acambis into a company that can make a difference in the fight against infectious diseases, we have four key goals:

01 | MAXIMISE OUR SMALLPOX FRANCHISE We are the world leader in smallpox vaccines, having supplied more doses to more governments than any other company. By capitalising on our strengths, we aim to make the most of the opportunities available to us – warm-base manufacturing for the US, manufacturing ACAM2000 vaccine for other governments and MVA vaccine for the US – in order to generate funds to invest in our pipeline. |

| 02 | BUILD A BILLION DOLLAR PIPELINE Our pipeline is our principal asset for creating shareholder value. By delivering on what we have today – short- and medium-term projects with a range of commercial opportunities – we are establishing a sound base for our portfolio. By adding, over time, other products that offer significant commercial potential, we can turn today’s base into a billion dollar pipeline. | |

|

|

|

|

| |

03 | FULLY INTEGRATE FROM CONCEPT TO COMMERCIALISATION We want to generate as much value as possible from our pipeline. In time, we will develop, manufacture and sell our own products wherever we can create value by doing so. For now, profits from sales of Vivotif® are already contributing to our pipeline investment and our manufacturing assets are helping us to control our costs and timelines. We complement our strengths where necessary through partnerships with other companies. |

| 04 | INCREASE RECURRING REVENUE STREAMS The cost of developing new products is significant, as is investing in assets that can generate greater value in the long term, such as manufacturing. Our aim is to capitalise on all sources of funding available to us to supplement shareholder investment. In addition to bidding for smallpox contracts, we also aim to increase the size and diversity of our recurring revenue streams, particularly through using our sales and distribution infrastructure. |

4 | Strategic goals |

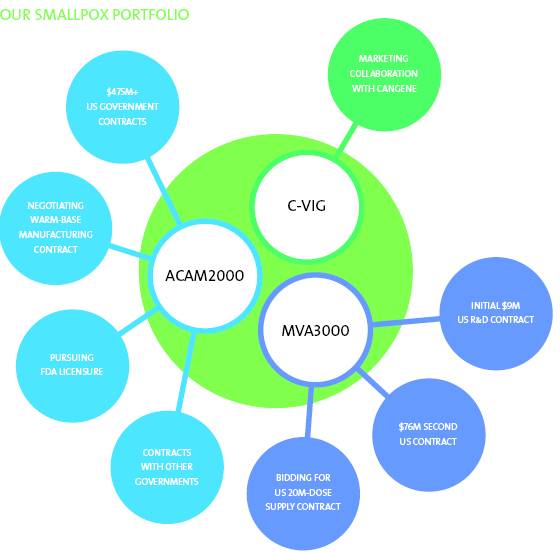

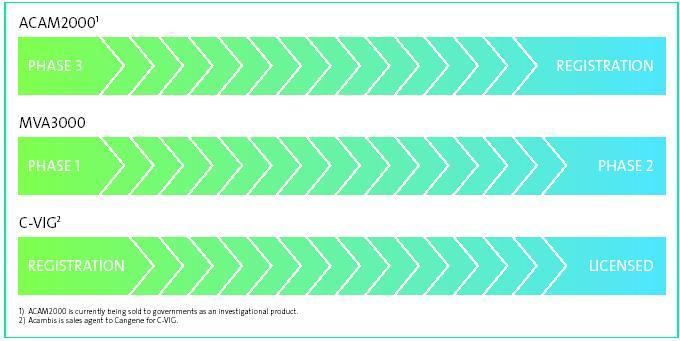

In the field of smallpox vaccines, Acambis is the world leader. We have supplied more doses of smallpox vaccine to more countries than any other company. We are also the only company to have supplied vaccine doses to the US Government’s Strategic National Stockpile, which it is continuing to build under Project Bioshield. This gives us an unrivalled track record. To maximise the revenues we can gain from our smallpox franchise, we are now targeting two principal opportunities: ACAM2000 warm-base manufacturing for the US Government and supply of MVA3000 to the US Government.

5 | ||

| Focused on two principal opportunities | |

|

| |

| Three related products |

|

|

| |

| The smallpox opportunity |

|

|

|

‘Significant support | THE SMALLPOX OPPORTUNITY | ||

| THOMAS MONATH, CHIEF SCIENTIFIC OFFICER | |||

|

| ||

| The environment for biodefence vaccines continues to be challenging, not least because concerns about pandemic influenza are creating competition for government funding. However, significant support still exists for smallpox preparedness efforts, as demonstrated in the US by the ongoing MVA procurement and the CDC entering negotiations on warm-base manufacturing. Speaking at a Congressional hearing in February 2005, Senator Ted Kennedy reflected: ‘America owes a debt of gratitude for what Acambis did in producing 180 million doses of vaccine to keep the nation safe from smallpox. I hope the Administration will build on this success by providing the funds needed to keep the production line for smallpox active.’ This sentiment was reinforced in May when the WHO announced it would hold a stockpile of five million doses of smallpox vaccine in Geneva, called on the world to pledge vaccines to a 200 million-dose ‘virtual’ stockpile and emphasised the need for the world to have warm-base manufacturing at two locations. For Acambis, licensure of ACAM2000 could be key, differentiating our vaccine and giving governments a higher level of confidence in the product. On MVA3000, our track record with both ACAM2000 and MVA3000 puts us in a very competitive position. |

| |

WARM-BASE MANUFACTURING

Having supplied more than 180 million doses of ACAM2000 to the US, our aim now is to meet its need to maintain a state of production readiness through annual production runs, known as ‘warm-base manufacturing’.

In 2005, the CDC confirmed to us its commitment to warm-base manufacturing and we aim to secure a contract in 2006. As part of this, we plan to transfer all manufacturing processes to our Canton, MA and Rockville, MD facilities, thereby providing the US Government with the security of production located entirely on US soil.

Warm-base manufacturing would produce doses of ACAM2000 each year for the Strategic National Stockpile. In future, it could also be used to maintain the stockpile, with production being increased, as required, to replace doses that expire. We hope to secure a contract later in 2006.

US GOVERNMENT MVA PROCUREMENT

Together with our partner, Baxter, we are bidding for a major contract to supply the US Government with doses of our MVA3000 attenuated smallpox vaccine. This vaccine is for the proportion of the population who could suffer adverse reactions to smallpox vaccines such as ACAM2000.

The US Government is looking for companies to supply up to 20 million doses of MVA vaccine for its Strategic National Stockpile. It also anticipates having an option for the US Government to procure up to a further 60 million doses of MVA. We submitted our proposal under the tender process in October 2005 and expect the US Government to make a decision around the end of the second quarter.

SALES OUTSIDE THE US

In addition to these two principal opportunities, we are continuing to pursue sales to other countries.

Outside the US, we have successfully competed for several government contracts but the majority have been for a small number of doses of ACAM2000.

In bidding for contracts, we have a clear advantage: the clinical data package we have generated for ACAM2000. We believe licensure of our vaccine would support future sales by differentiating ACAM2000.

While we continue to expect future sales to be at a relatively low level unless the environment changes significantly, we will ensure that we are positioned to take advantage of whatever opportunities exist.

6 | Strategic goals |

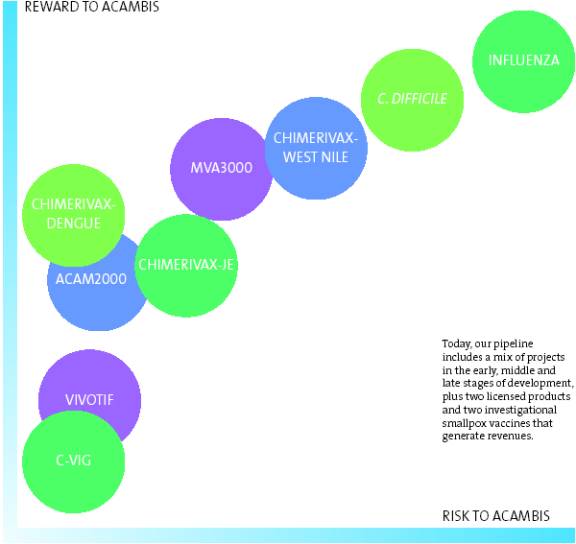

Our pipeline is our greatest asset and maximising its value is our primary goal. To do that, we want to develop, manufacture and market our proprietary products ourselves, wherever it is feasible for us to do so. This also gives us more control over the time it takes to bring our products to market.

ACAMBIS’ PORTFOLIO

RISK/REWARD RATIO

7 | ||

| Towards a balanced pipeline | |

|

| |

| Addressing a regulatory environment |

|

|

| |

| Knowing what it takes |

|

|

|

|

|

|

|

|

| KNOWING WHAT IT TAKES |

|

| PHILIP BEDFORD, SENIOR VICE PRESIDENT, CLINICAL OPERATIONS AND REGULATORY AFFAIRS |

| |

| The ACAM2000 programme transformed Acambis, not only financially but also operationally, building both manufacturing operations to deliver more than 200 million doses of vaccine and clinical and regulatory teams to implement the largest and most rapid product development project we have yet undertaken. This experience has given us a better understanding of what it takes to develop and license a vaccine. In the last six years, we have conducted more than 40 clinical trials on multiple continents in over 15,000 subjects. We have also submitted two licence applications to the US FDA, giving us an invaluable insight into what is, arguably, the toughest regulatory regime in the world. We have also learned the importance of investing early, whether to establish the manufacturing process or to address regulatory questions through early-stage clinical trials, knowing that the more work we do up-front the greater our chance of success when we enter the expensive Phase 3 stage of clinical testing and submit licence applications. |

| |

‘We have an invaluable insight into the toughest regulatory regime in the world.’ |

|

| |

|

|

|

To achieve our vision, we want to build a billion dollar pipeline that delivers a flow of new licensed products and generates recurring revenues to fund our continued investment in innovation.

In addition, to create maximum long-term value for shareholders, we want to retain the rights to our products for as long as possible, wherever feasible.

Holding onto product rights is a long-term goal. For now, our recent success in progressing the projects in our pipeline and our need for more predictable cash-generation from recurring revenue streams means that we continue to make difficult decisions in prioritising our

efforts and resources. With our ChimeriVax-JE vaccine, for instance, we are focusing our initial commercial efforts on key endemic countries where we believe we can gain the greatest return and will stage our entry into other markets. Programmes may also need partners to supplement our existing capabilities if we are to be successful.

Our current pipeline is built around projects successfully transitioned from our research group and we will continue to add both in-house and external earlier-stage opportunities, particularly those of significant commercial value.

THE STAGES OF CLINICAL DEVELOPMENT | ||||||

Clinical testing is a lengthy and complex process that can vary significantly from product to product. Our ChimeriVax-JE vaccine, for instance, underwent seven different Phase 1 and Phase 2 trials before entering late-stage Phase 3 trials in 2005. Broadly, the US FDA defines the product development process for vaccines as follows: | ||||||

PHASE 1 Typically 20-100 subjects, this is the first time the product has been tested in humans. It aims to check that there are no serious side effects associated with the vaccine and generates initial data about the immune system’s response to the product. | PHASE 2 Typically 100-500 subjects, this explores the safety and immunogenicity profile in a larger number of subjects and investigates what effect different dose levels have on the immune system. | PHASE 3 Typically at least 3,000 subjects and possibly tens of thousands, this stage builds an extensive safety and immunogenicity database and tests vaccine efficacy through agreed endpoints.

| LICENCE APPLICATION Pre-clinical, clinical and manufacturing-related data are presented to support approval and the manufacturing facilities are inspected.

| |||

8 | Strategic goals |

We aim to make a difference by targeting unmet medical needs and developing next-generation products that provide improvements over existing products. Our pipeline of two licensed products and seven investigational vaccines targets viruses and bacteria that affect millions of people around the world every year. We also have other programmes at the research stage that will continue to feed new products into our development pipeline.

9 | ||

| Key proprietary programmes | |

|

| |

| Building a high-value portfolio |

|

|

| |

| New oppurtunities |

|

|

|

Our key proprietary programmes are our vaccines against JE,West Nile virus,

C. difficile and influenza.

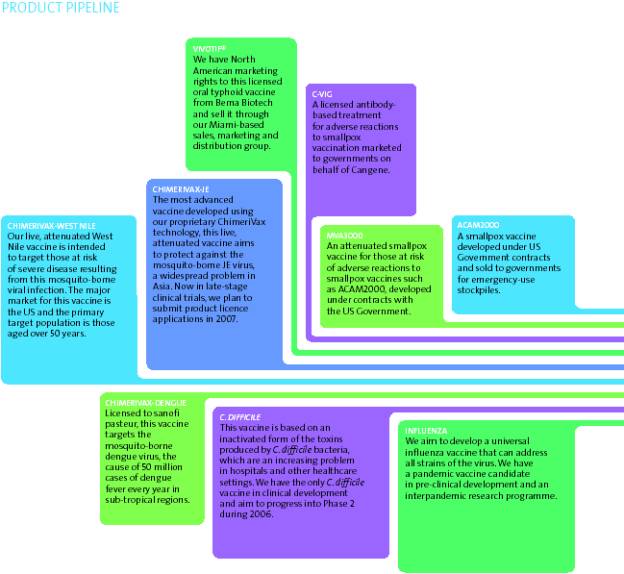

CHIMERIVAX-JE

Use of current JE vaccines is limited by safety concerns and compliance difficulties with multiple-dose products. ChimeriVax-JE has been designed to have the ideal product profile: single-dose administration providing rapid immunity and long-lasting protection, a good safety profile and manufacturing compliant with FDA standards.

Such a vaccine suits both the endemic populations and travellers/military personnel visiting endemic regions. It makes childhood immunisation programmes more viable and facilitates short-notice vaccinations for travellers. We have already established an agreement with Bharat Biotech in India and will work with other partners not only to replace out-of-favour, first-generation products but also to expand the JE vaccine market.

C. DIFFICILE

C. difficile is emerging as the most significant hospital-acquired infection in the developed world. Reported annual numbers – 360,000 cases in the US, 44,000 in the UK – are believed to be underestimated and the severity, as well as the incidence, is increasing because of antibiotic resistance, an ageing population and the emergence of a more virulent strain.

The case for a C. difficile vaccine is a pharmaco-economic one: antibiotic treatment costs upwards of $3,600 per patient and 20% of those infected relapse when antibiotics are discontinued1. We are the only company with a C. difficile vaccine candidate in development.

CHIMERIVAX-WEST NILE

West Nile virus is endemic in the US and causes a spectrum of illness from fever through to polio-like paralysis and fatal encephalitis. There is no treatment and those at highest risk of severe disease are people aged over 50 years, which equates to 100 million people in the US.

Although several companies are developing West Nile vaccines, ours is the most advanced, having entered Phase 2 trials in 2005. Our vaccine was developed using the same ChimeriVax technology that was applied to our JE vaccine, which has been tested in more than 3,300 people, giving us a confidence in ChimeriVax-West Nile that has been borne out by our pre-clinical and Phase 1 results.

INFLUENZA

The market for influenza vaccines is huge: estimates suggest it will be worth $2bn a year by the end of the decade. It is dominated by the major vaccine players with first- or second-generation vaccines using either egg-based or cell-culture manufacture.

To compete in this field, we aim to revolutionise the market by developing the ‘holy grail’ of influenza vaccines: a product that can protect against all human strains of the virus. This ‘universal’ approach would make annual changes to the vaccine formulation unnecessary, provide longer-term immunity and support pandemic preparedness efforts through stockpiling.

PRE-CLINICAL |

| PHASE 1 |

| PHASE 2 |

| PHASE 3 |

| REGISTRATION |

| MARKETED |

| | ||||||||||

| ||||||||||

ACAM2000 is currently being sold to governments under an FDA IND application for emergency-use stockpiling.

1) Kyne et al., Clinical Infectious Diseases, 2002; 34: 346-353.

10 | Strategic goals |

Fully integrate from concept

to commercialisation

The process of developing a new vaccine is highly complex and involves many different capabilities. Over the long term, we plan to invest in our proprietary programmes ourselves, to establish the necessary in-house expertise and to build manufacturing and sales, marketing and distribution efforts, where appropriate, to ensure that we gain the maximum potential return on our investment.

11 | ||

| An increasingly scarce resource | |

|

| |

| Controlling cost and timelines |

|

|

| |

| investing to maximise value |

|

|

|

The most successful those products themselves.’ | INVESTING TO MAXIMISE VALUE | ||

| JOAN FUSCO, SENIOR VICE PRESIDENT, OPERATIONS | |||

|

| ||

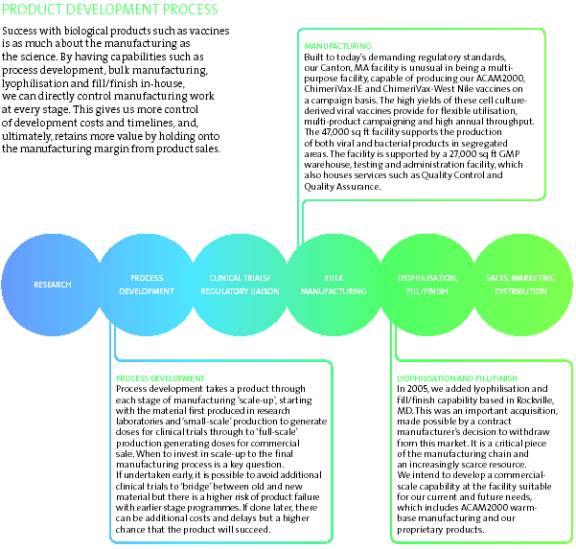

| When looking at the success stories in our industry, the clearest lesson is that the most successful companies are those that develop and license products themselves, instead of out-licensing their proprietary programmes at an earlier stage to other companies. Like most biotechs, Acambis started life as a research and development company. Through our work on ACAM2000, we have built important additional capabilities, including highly trained teams to run our multinational clinical trials and to liaise with regulatory authorities. We have also added three important assets: a bulk manufacturing facility, a lyophilisation and fill/finish facility and a US-based sales, marketing and distribution organisation. Becoming fully integrated, such that we can develop, manufacture and sell our products ourselves, is a long-term goal. Today, we have a manufacturing capability that applies to some but not all of our products, and a sales and distribution group that targets a niche market in the US. As we grow, we aim to build the necessary expertise to capitalise on our assets. Over time, the needs of our existing and future pipeline will become increasingly complex, requiring different types and sizes of clinical trials in multiple countries, various manufacturing methods and a number of sales and distribution channels covering disparate regions of the world. When we put such capabilities in place and which ones we choose to develop in-house will depend upon the priority of a given project within our portfolio. The continuing success of our development programmes means that we are regularly faced with the challenge of prioritising our projects, deciding which we want to invest in ourselves and which should be partnered. Such partnerships can bring many and varied benefits to our programmes, including cash to invest in clinical trials, manufacturing capabilities beyond our own, geographic reach into countries where we have no presence or experience, or more extensive sales, marketing and distribution channels. Over time, as we increase our recurring revenue streams, our ability to retain more rights will also increase. For now, we continue to strike a balance between the financial resource associated with establishing and running such assets, our ability to make maximum use of such assets and the long-term benefits to be gained from holding onto product rights. |

| |

|

|

|

|

12 | Strategic goals |

Our US Government ACAM2000 contract was a major revenue-generator for Acambis between 2002 and 2005. Now, we are exploiting two key assets – our smallpox franchise and our sales, marketing and distribution infrastructure – to bring in other sources of revenue and generate cash to invest in our long-term driver of future revenues, our pipeline.

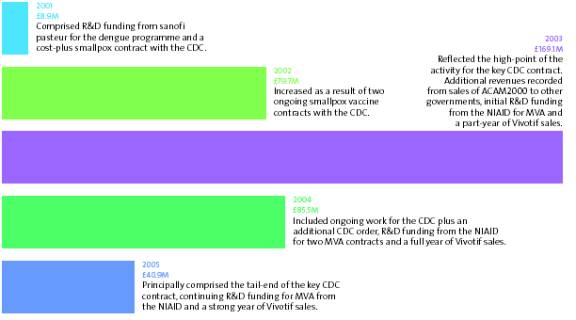

FIVE-YEAR HISTORIC REVENUES

Five years ago, our revenues came from external R&D funding. The US Government smallpox vaccine contract we won in 2001 drove our revenues for the next three years. Our goal now is to supplement further government contracts with recurrent revenues from product sales.

13 | ||

| Funding our growth | |

|

| |

| Revenue-generating opportunities |

|

|

| |

| Building long-term value |

|

|

|

|

|

|

|

‘We have ambitions to grow Acambis into a sustainably profitable company.’ |

| FUNDING OUR GROWTH |

|

|

| ||

| DAVID LAWRENCE, CHIEF FINANCIAL OFFICER |

| |

| |||

| ACAM2000 transformed Acambis: before winning our US Government contract in November 2001, our revenues were minimal, driven primarily by funding from partners for our R&D activities. That contract provided a significant amount of capital for Acambis, giving us the opportunity to invest in driving forward our R&D pipeline and building capabilities that are critical to our success. We have ambitions to grow Acambis into a sustainably profitable company by developing innovative products. We also believe it is important to maximise the value of these products by manufacturing and marketing them ourselves, wherever possible. In the medium and long term, we aim to fund our investment through revenues generated by sales of products that are currently in development and from further products we add to the portfolio over time. The first of our proprietary products expected to reach the market is ChimeriVax-JE, for which we aim to submit licence applications in 2007. In the short term, our investment is likely to out-pace our revenues, so effective management of our cash continues to be a high priority. Inevitably, this means we have to strike a balance between short-term financial requirements and the long-term benefit of increasing value by developing, manufacturing and marketing products ourselves. Therefore, we are looking to maximise our potential revenue sources and will pursue partnering opportunities as appropriate. |

| |

Developing new vaccines is an expensive and time-consuming process. In 2006, we expect to invest up to £40-45m in R&D, a significant portion of which will fund the Phase 3 trials for our ChimeriVax-JE vaccine, reflecting the increased investment required as we progress our programmes into the later stages of development.

We aim, in due course, to sustain our R&D investment through recurring revenues generated by product sales, particularly those vaccines we currently have in development. Our nearest opportunity is ChimeriVax-JE, for which we plan to submit product licence applications in 2007, followed in later years by product licence applications for ChimeriVax-West Nile and our C. difficile vaccine. Early-stage projects are also being pursued to continue the flow of programmes into the pipeline.

Until our pipeline comes to fruition, we are looking to maximise our sources of revenue. To do this, we are principally addressing two broad approaches for increasing revenues.

First, the smallpox franchise continues to be a significant driver for potential revenues in the short term.

As highlighted on pages 4 and 5, we hope to win a US Government MVA stockpiling contract, to secure an ACAM2000 warm-base manufacturing contract with the US Government and to sell ACAM2000 to other governments. Of these, MVA could be a significant revenue generator and warm-base manufacturing could bring in useful recurring revenues over several years.

In addition, we are continuing to pursue opportunities to use certain assets to bring in additional revenues. In particular, there is potential to use our US sales, marketing and distribution infrastructure to sell other companies’ products. Our focus in this effort is licensed products or products close to licensure that might benefit from being sold through a highly targeted sales channel.

Although none of these opportunities would be sufficient in isolation, together they can help to carry us forward into a period when products currently in our development pipeline are expected to reach the market and generate revenues themselves.

‘To achieve our long-term vision for Acambis, we want to build a portfolio of vaccines and other infectious disease products that make a difference by helping millions of people and by generating significant revenues to support our investment in further innovative products. The product opportunities in our pipeline today could contribute useful recurring revenues from around 2008 to help to fund ongoing investment in our pipeline. As the pipeline progresses, we want to bring through programmes that have an increased impact in terms of both the numbers of people they reach and the size of the markets they address. In 2005, a key focus was on driving our pipeline programmes forward and our significant progress during the year has taken us much closer to achieving our goal.’ GORDON CAMERON, CHIEF EXECUTIVE OFFICER

|

|

|

|

| ||

| ||

| Review | |

| ||

| Annual Report 2005 | |

|

| |

|

| |

REVIEW OF 2005 |

| ||

| |||

| |||

| |||

| |||

| |||

| |||

| |||

| |||

| |||

|

| ||

| FINANCIALS: THE FACTS AND FIGURES |

| |

| |||

| |||

| |||

| |||

| |||

| |||

|

| ||

| GENERAL INFORMATION |

| |

| |||

| |||

| |||

|

|

|

17 | |

In our 2004 Annual Report, we set out our 10 strategic priorities for 2005.

Some we’ve completed, others we’re continuing to address in 2006...

|

|

|

| PROGRESS MADE IN 2005 | ||||

|

|

|

| 0% |

|

| 100% | |

01 |

| FILE THE ACAM2000 BLA WITH THE FDA |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

02 |

| SECURE ACAM2000 US GOVERNMENT WARM-BASE MANUFACTURING CONTRACT |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

03 |

| ACHIEVE YEAR-ON-YEAR GROWTH IN SALES OF ACAM2000 TO OTHER GOVERNMENTS |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

04 |

| EXECUTE PLANNED ACTIVITIES UNDER OUR EXISTING US GOVERNMENT MVA CONTRACTS |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

05 |

| IMPLEMENT STRATEGY TO WIN THE US GOVERNMENT’S MVA STOCKPILE CONTRACT |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

06 |

| COMMENCE PHASE 3 TRIAL OF CHIMERIVAX-JE |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

07 |

| COMMENCE PHASE 2 TRIAL OF CHIMERIVAX-WEST NILE |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

08 |

| COMMENCE PHASE 1 TRIAL OF C. DIFFICILE |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

09 |

| UTILISE OUR MANUFACTURING CAPACITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

10 |

| ADD PRODUCTS AND/OR LATE-STAGE PROJECTS TO OUR PORTFOLIO |

|

|

|

|

| |

18 | Chairman’s statement |

|

| |

Investing for growth, |

| |

|

As the operational highlights summary on page 17 illustrates, 2005 was a mixed year. We positioned 2005 as a year of investment aimed at building both our product portfolio and the infrastructure and capabilities. In both areas we had a very successful year.

However, the US Government warm-base manufacturing and MVA opportunities on which we expected decisions in 2005 have not yet crystallised and the start of litigation relating to MVA created a level of uncertainty around that opportunity. Together, these factors resulted in a disappointing share price performance in spite of our success in other areas.

REVIEW OF 2005

Our most notable achievement was the progression of each of our proprietary programmes into the next stage of development, including ChimeriVax-JE, which is now undergoing pivotal Phase 3 trials in Australia and the US. We also expanded the pipeline with the addition of an influenza vaccine programme.

Our capabilities were increased through the acquisition of a fill/finish facility in the US, which has given us the opportunity to bring in-house an increasingly scarce resource and to complete our manufacturing supply chain.

In addition to building our pipeline and capabilities, we have an ongoing aim to exploit our competitive strengths in the smallpox arena to gain as much value as possible from our franchise of products: ACAM2000, MVA3000 and C-VIG. We made good progress with our existing MVA3000 contract, including delivering 500,000 doses to the US Government, and, in April 2006, completed submission of a US licence application for ACAM2000.

We are currently in a litigation process relating to MVA as a result of complaints filed against us by Bavarian Nordic in the US in August 2005. A further suit was filed in Austria in February 2006. Bavarian Nordic alleges that we have used its trade secrets in the development of our MVA3000 vaccine and that we are infringing its patents. We strongly believe these allegations are without foundation and we are vigorously defending our position.

Our financial performance during 2005 was in line with our expectations. The guidance we gave at the beginning of the year was for £40m of predictable revenues and the actual performance was £40.9m. The fact that almost 60% of this revenue was recognised in the fourth quarter of the year highlights one of the principal challenges of predicting and relying on biodefence contract revenues and we continue to pursue opportunities to build more mainstream revenues. In this area, 2005 was a particularly good year for sales of Vivotif as we were able to capitalise on the competitor product’s lack of availability for part of the year to improve revenues and market share.

OUTLOOK FOR ACAMBIS

As one of the leading independent vaccine companies, Acambis is well placed within the sector. We further strengthened our pipeline by driving our development programmes forward in 2005 and have built a useful infrastructure to enable us to develop, manufacture and, in some markets, sell our vaccines.

Our investment in R&D delivered significant progress in 2005 and by continuing that strategy in 2006 we expect to see further good progress from our pipeline. Preliminary results from our ongoing Phase 3 trials of ChimeriVax-JE should be available later in 2006, at which point the

19

| PRIORITIES FOR 2006 |

|

|

| |

| Complete filing of ACAM2000 licence application with the FDA |

|

|

| |

| Secure ACAM2000 US Government warm-base manufacturing contract |

|

|

| |

| Secure MVA3000 US Government contract |

|

|

| |

| Complete MVA litigation process at the ITC |

|

|

| |

| Complete ChimeriVax-JE pivotal Phase 3 trials |

|

|

| |

| Commence ChimeriVax-JE Phase 2 paediatric trial in India |

|

|

| |

| Complete ChimeriVax-West Nile Phase 2 trial |

|

|

| |

| Commence C. difficile Phase 2 trial |

|

|

| |

|

|

|

Phase 2 paediatric trial in India will be ongoing. In addition, in the second half of the year we expect to see results from our Phase 2 trial of ChimeriVax-West Nile and aim to transition our C. difficile vaccine into Phase 2. Based on the fast-track status awarded to our ACAM2000 programme, we would hope to receive the FDA’s decision on our licence application before the end of 2006. Given this extensive clinical trial programme, we expect our investment in R&D to increase to around £40-45m in 2006. This includes a significant investment in the Phase 3 trials for ChimeriVax-JE.

We are confident that during 2006 we will also achieve greater clarity around our smallpox franchise. Based on indications from the CDC, we continue to expect to sign and initiate a US Government warm-base manufacturing contract for ACAM2000 and we also expect to receive a decision on the US MVA stockpiling tender process. In the MVA litigation process, the first of the US court cases is being heard in May at the ITC and a decision is expected in the second half of the year.

As in previous years, some of our revenues in 2006 will be more predictable than others, namely those from sales of Vivotif and existing ACAM2000 and MVA3000 contracts. We estimate that, depending upon the timing of activities for the existing smallpox contracts, our predictable revenues in 2006 will be £20-25m. We would expect the gross profit margin on these activities to be similar to that achieved in 2005. There is significant potential for additional revenues from contracts we are currently pursuing, particularly further ACAM2000 and MVA3000 US Government contracts.

BOARD CHANGES

Since our last Annual Report, we have seen two changes to the composition of the Board: the appointment of Dr Peter Fellner in February 2006 and the resignation of Michael Lytton in April 2006. We were delighted to welcome Peter to our Board given that he is one of the leading figures in the UK biotechnology industry. With his extensive knowledge and experience, we believe his insight and advice will be invaluable as we oversee the continued development of Acambis. Michael stood down following a period of five years on the Board. We thank Michael for the insight and advice he has brought to our Board discussions during that time.

I have been a member of Acambis’ Board for over 10 years and Chairman for more than seven of those years. Based on good corporate governance practices, I have decided that I will stand down from the Board and as Chairman of Acambis later in 2006. We will announce the appointment of my successor at that time.

Acambis is a very different company now from when I joined the Board and I am pleased to have played a part in its growth during that time. I am confident that it will continue to go from strength to strength and wish its Board and our shareholders every success.

ALAN SMITH, CHAIRMAN

20 | Performance review |

|

| |

Driving the pipeline forward |

| |

|

By driving our pipeline forward, generating revenues from our smallpox franchise and building in-house capabilities such as manufacturing and marketing, we aim to ensure Acambis is well placed to participate in our industry’s growth.

SMALLPOX FRANCHISE UPDATE

As part of our efforts to maximise our smallpox franchise, we are continuing to pursue two key US Government contracts. Negotiations are underway for an ACAM2000 warm-base manufacturing contract and we have submitted a tender for an MVA contract. We have also submitted a licence application to the FDA for ACAM2000, which could support other sales of this vaccine.

PROGRESS SINCE THE START OF 2005: OUR SMALLPOX FRANCHISE

21 | |

ACAM2000 |

|

|

Following a pre-BLA meeting with the FDA in November 2005, we started submission of our BLA for ACAM2000 in January 2006 and completed it in April. This is the culmination of over five years of work to provide the US Government with a next-generation, licensed smallpox vaccine. The submission included safety, tolerability and immunogenicity data obtained from clinical trials of ACAM2000 conducted in more than 3,800 subjects. Given ACAM2000’s fast-track status, we expect to receive the FDA’s decision on our application before the end of 2006. |

| Licence application submitted |

We are currently in negotiations with the US Government about a contract for us to provide warm-base manufacturing for ACAM2000 on a long-term basis. This is intended to maintain our facilities in a state of production readiness and, if necessary, to provide the US with ongoing surge capacity in smallpox vaccine production. In September 2005, we reported that the CDC had indicated to us that it would be proceeding with a warm-base manufacturing contract during US Government Fiscal Year 2006, which runs through to 30 September 2006. We are on track to achieve that timeline. We remain confident that there are further opportunities to sell ACAM2000 to other governments. Whilst we did not achieve any significant sales during 2005, discussions with various countries indicate that some are awaiting the outcome of the US product licence application process before proceeding with their procurement decisions. |

| Warm-base manufacturing contract negotiations underway |

|

|

|

MVA3000 |

|

|

During 2005, we made excellent progress on our existing contract with the US Government agency, the NIAID, including delivering 500,000 doses of our MVA vaccine, MVA3000, in December. We also initiated a Phase 2 safety and immunogenicity trial, enrolment for which is now complete. Together with our co-development partner, Baxter, we submitted our bid for a US Government stockpiling contract in October 2005. This was in response to an RFP issued by the Department of Health and Human Services. The RFP is for the manufacture of up to 20 million doses of MVA attenuated smallpox vaccine and advanced clinical testing up to and including obtaining a product licence. It also includes options for the purchase of up to 60 million additional doses of MVA and warm-base manufacturing over the longer term. The 500,000 doses we delivered in December were produced at the scale required for this stockpiling process. We believe that our strong track record with the US Government, our partnership with Baxter and our demonstrated ability to manufacture and deliver large quantities of both MVA3000 and ACAM2000 put us in a very strong competitive position. Based on indications received from the US Government, we expect the award of contract(s) to be made around the end of the second quarter of 2006. |

|

|

|

|

|

C-VIG |

|

|

During 2005, we helped Cangene to win its first major C-VIG contract outside the US. It was awarded a C$17m (c. £8.5m) contract in September to supply doses of its C-VIG product to the UK Government. As sales agent to Cangene, we receive a royalty on the sales achieved. C-VIG was licensed by the FDA in 2005. |

| UK contract secured in 2005 |

22 | Performance review |

MVA LITIGATION |

We are continuing vigorously to oppose any and all legal actions filed by BN with regard to MVA. |

BN has lodged complaints against us with the ITC, the District Court of Delaware and the Commercial Court in Vienna, Austria. BN’s legal actions include claims that relate to patents, trade secrets and misappropriation. We will present evidence that each of these allegations is without merit. |

• Patents: we have always believed and continue to believe that any patents awarded or pending do not restrict our freedom to operate in the field of MVA. We will present factual and expert evidence that: MVA-BN is not novel; the patent is unenforceable through lack of enablement; BN failed to provide the US Patent and Trademark Office with prior art related to its patent claims; and the patents rely on scant scientific evidence. |

• Trade secrets: we will present evidence that, in developing MVA3000, we have called upon our own experience, gained through the ACAM2000 programme, and the experience of our partners, including using established manufacturing practices. We have also used information gleaned from the many articles published on MVA over the last 30 years, including those from Dr Anton Mayr, who worked on the original development of MVA vaccines. In addition, key parameters for the programme were set by the NIAID, including dose level and dosing schedule. |

• Misappropriation: Dr Mayr provided an MVA strain to the NIH/NIAID. The NIAID then provided a version of that strain to Acambis for use as the basis of MVA3000. We will present evidence that Dr Mayr did not restrict the use of the MVA strain he provided to the NIH. We received the NIH MVA under a Material Transfer Agreement. The NIAID stated that ‘prior to distribution of the material NIAID determined that it is within its rights to transfer the material to other parties’. |

BN’s intent is clearly to disrupt and frustrate competition in the MVA procurement process, both in the US and elsewhere. We are, and always have been, very confident of our ability to counter BN’s allegations and will vigorously defend our freedom to compete for, and win, contracts under these important procurements. |

23 | |

RESEARCH AND DEVELOPMENT UPDATE |

|

|

Our aim for 2005 was to take each of our proprietary programmes into the next stage of development. In achieving this goal, we completed or initiated a total of 12 clinical trials, which is a significant achievement for a company of our size and stage of maturity. |

|

|

|

|

|

CHIMERIVAX-JE |

|

|

Our ChimeriVax-JE vaccine against the mosquito-borne JE virus is now undergoing pivotal Phase 3 testing. The two clinical trials, which are being conducted in multiple centres in Australia and the US, are testing the safety and efficacy of a single-dose regimen of ChimeriVax-JE in more than 2,800 subjects. The trials, which were initiated in November 2005, are progressing extremely well, with enrolment now complete. |

|

|

We are also undertaking a Phase 2 paediatric trial in India, where children are the primary target population for a JE vaccine. The paediatric data from this trial and a subsequent Phase 3 trial will supplement those generated in our ongoing Phase 3 trials and our previous Phase 1 and 2 studies to support licence applications for both the endemic regions and the travel market. We are targeting submissions of licence applications in both India and Australia in 2007. There is a large unmet public health need for a single-dose, convenient and affordable vaccine against JE, which could make it simpler, faster, easier and cheaper for healthcare providers to administer vaccines, particularly in regions where achieving compliance to multi-dose regimens can be difficult. An epidemic in northern India in 2005 resulted in 6,340 reported cases and more than 1,200 deaths, mostly of children. |

| Indian paediatric trial starting in 2006 |

India is one of our primary markets for ChimeriVax-JE and to support commercialisation of the vaccine in the region we established a collaboration with one of India’s leading biotechnology companies, Bharat Biotech, at the end of 2005. Under the partnership, Bharat Biotech will undertake end-stage fill/finish processing of ChimeriVax-JE at its facilities in India and will market and distribute the vaccine in India and neighbouring countries once the product is approved. We are currently pursuing the necessary import and export requirements with a view to completing technology transfer to Bharat Biotech in time to use material produced by Bharat Biotech in planned Phase 3 trials in India. We are also pursuing partnerships to target other endemic countries and the travellers’ market. |

|

|

|

|

|

CHIMERIVAX-WEST NILE |

|

|

We are continuing to lead the field in developing a human vaccine against the mosquito-borne West Nile virus, which is endemic in the US. Having become the first company to complete a Phase 1 trial, we were also the first to enter Phase 2 clinical testing. |

|

|

We initiated a Phase 2 trial in December 2005 to test our vaccine in more than 200 subjects in the US. The aim of the randomised, double-blind, placebo-controlled trial is to evaluate the safety, tolerability and immunogenicity of ChimeriVax-West Nile in healthy adults and elderly subjects. Having tested different dose levels in young adults, the optimal dose will be taken forward for testing in elderly subjects. Those aged 50 and above are likely to be the initial target population for a West Nile vaccine as they are most at risk of severe disease following infection. Recruitment for the healthy adults portion of the trial is now complete. In our Phase 1 safety and immunogenicity trial, results from which were announced in April 2005, of the subjects who received a single dose of ChimeriVax-West Nile, 96% in the high-dose group and 100% in the low-dose group developed high titres of West Nile-neutralising antibodies 28 days after vaccination. Intervet, which is the number one manufacturer of animal vaccines, is aiming to launch its West Nile veterinary vaccine in the US during the 2006 season. The West Nile virus is a particular problem for horses. Intervet’s vaccine was developed from the ChimeriVax technology licensed from Acambis and we will receive royalties from sales of the Intervet product. |

| First company into Phase 2 trials |

24 | Performance review |

CHIMERIVAX-DENGUE |

|

|

Following completion of the Phase 1 trial of a tetravalent formulation of our ChimeriVax-Dengue in the first quarter of 2005, the lead responsibility for further clinical testing and development passed during 2005 to SP, to whom we have licensed worldwide rights. Results from the trial showed seroconversion to all four dengue virus serotypes in the majority of subjects. SP has progressed the vaccine into Phase 2 clinical trials. |

| Partner sanofi pasteur progresses into Phase 2 |

|

|

|

C. DIFFICILE |

|

|

We have recently announced results from the first of two Phase 1 trials of our vaccine against C. difficile, a leading cause of hospital-acquired infections. In the 50-subject placebo-controlled trial in healthy adults, antibody responses were seen in all 37 subjects who received our vaccine. No subjects experienced unexpected or serious vaccine-related adverse events. Enrolment is now complete in a second Phase 1 trial designed to explore the safety, tolerability and immunogenicity of our vaccine in healthy elderly subjects at different dose levels. This is the first trial of our vaccine in one of the key target populations for the product. We aim to complete Phase 1 testing in the second half of the year and then to begin Phase 2 trials. |

| Encouraging results from first Phase 1 trial |

|

|

|

INFLUENZA |

|

|

During 2005, we initiated a programme to develop a universal influenza vaccine, which is seen as the “holy grail” of influenza protection. The aim of the programme is to develop a vaccine that can target all strains of influenza, removing the need for annual reformulations and annual vaccinations. To achieve this, we acquired a technology previously being developed by Apovia, a US-based biotechnology company, and established a research collaboration with VIB, a Belgian research institute. A major component of the new candidate(s) is M2e, the extracellular domain of the ion channel protein M2, which is specific to influenza ‘A’. Being highly conserved, M2e is intended to elicit protective immune responses against all strains of influenza ‘A’. While our ultimate goal is to develop a vaccine that is universally effective against all ‘A’ and ‘B’ strains of the influenza virus, which would be required for complete protection against seasonal influenza, we are also pursuing development of an ‘A’ strain candidate as this could be suitable as a vaccine against pandemic influenza. All previous pandemics have been caused by ‘A’ strains of the virus. With a vaccine that targets all ‘A’ strains, governments would be able to stockpile vaccine doses for use in the event of a pandemic instead of waiting for the appropriate strain to be identified before vaccine manufacture can be undertaken. Pre-clinical development of our pandemic vaccine candidate is ongoing and we aim to enter clinical trials in early 2007. Our longer term programme is currently at the research stage. |

| New project added to pipeline could be in clinical trials in 2007 |

|

|

|

VIVOTIF® |

|

|

Vivotif, the oral typhoid vaccine we sell in the US, had a strong year in 2005, with sales volumes 81% up over 2004. This was primarily as a result of our ability to capitalise on the competitor product’s lack of availability for part of the year. |

| Strong Vivotif sales growth |

|

|

|

ARILVAXTM |

|

|

Acambis has US sales and marketing rights to ARILVAX, a yellow fever vaccine that is owned and manufactured by Chiron. We are in ongoing discussions with Chiron and its new parent company, Novartis AG, to resolve a way forward for the ARILVAX programme. To date these have been constructive and we hope to conclude the discussions in the near future. |

|

|

|

|

|

GORDON CAMERON, CHIEF EXECUTIVE OFFICER |

|

|

25 | |

CORPORATE RESPONSIBILITY |

In 2005, we underwent our second annual audit by GoodCorporation, an independent CR verification organisation. We were able to demonstrate that improvement had been made during the year and were delighted to be awarded GoodCorporation membership for a second time. To achieve GoodCorporation membership, organisations are annually assessed and must meet minimum criteria on the existence and effectiveness of management practices in 62 areas. The requirements are practical and designed to ensure that CR is an integral part of everyday management. The verification report is based on site visits and interviews with all stakeholder groups.

ACAMBIS’ PERFORMANCE IN THE GOODCORPORATION AUDIT |

| 0 |

| 5 |

| 10 |

| 15 |

| 20 |

| 25 |

| 30 | |||

|

|

|

|

|

|

| |||||||||||

COMMENDATION |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

MERIT |

| ||||||||||||||||

OBSERVATION |

|

|

|

|

| ||||||||||||

MINOR NON-COMPLIANCES |

|

|

|

|

|

|

|

|

|

|

| ||||||

FAIL | 2005 | ||||||||||||||||

NOT APPLICABLE | 2004 | ||||||||||||||||

In 2005, the audit was extended to encompass our sales and distribution group in Miami, FL. During the year, we implemented several measures to address areas of improvement highlighted by GoodCorporation, including increased employee consultation, employee training on our grievance procedure and development of a bribery policy. In 2006, areas of continuing focus include environmental impact assessments and support for community projects, particularly those involving our employees. For more information, see our website, www.acambis.com.

RISK MANAGEMENT |

This report provides an update on risks highlighted last year and sets out key risks for 2006.

2005 REPORT

Two key risks for 2005 were that:

> The US Government MVA contract is for fewer doses, generates less revenue or materialises later than anticipated or that a contract is not awarded to Acambis at all; and

> The anticipated ACAM2000 warm-base manufacturing contract is delayed, is of less commercial value than anticipated or does not materialise.

Both of these contract awards are pending. To manage expectations during the year, we provided regular updates to investors and, for the first time, broke down our revenue guidance into ‘predictable’ and ‘unpredictable’ revenues to give greater clarity. Throughout the year, we continued to have regular dialogue with US Government personnel and ensured that we remained well positioned by delivering against MVA milestones and moving towards ACAM2000 licensure.

In addition, we highlighted two operational risks, namely that:

> The structural changes that have been implemented as we continue our transition from an R&D organisation into a fully integrated biopharmaceutical company are not successfully integrated; and

> There might be no or insufficient reward in marketing our products in development, that one or more of them fails in development or clinical trials, that development delays first-to-market advantage or that increasing costs negatively impact potential returns.

We continued to improve management practices, establishing a project management function and embedding the corporate planning process. We continue to balance our wish to be fully integrated with our current financial position.

Our annual planning includes a project and portfolio review, incorporating commercial strategies. We invested in progressing all our programmes into the next stage of development during 2005, maintaining

our lead in the West Nile arena and positioning ourselves as the only company with a C. difficile vaccine in development. To maximise the potential return for ChimeriVax-JE, we redefined the licensure strategy to focus on endemic markets.

MAJOR RISKS FOR 2006

Our key risks for 2006 are:

> That we are not awarded a contract under the US Government MVA procurement process or that the award is later than anticipated or for fewer doses;

> That we do not secure a US warm-base manufacturing contract for ACAM2000 or that the contract is later than anticipated or for fewer doses;

> That ACAM2000 is not licensed by the FDA;

> That we do not achieve an acceptable outcome from the MVA litigation process; or

> That one or more products in development fails to achieve the desired safety or efficacy outcomes.

26 | |

|

| |

| ||

|

INCOME STATEMENT HIGHLIGHTS |

| 2005 |

| 2004 |

|

| |||||

Revenue |

| 40.9 | 85.5 |

| |

Cost of sales |

| (27.6 | ) | (35.0 | ) |

| |||||

|

|

|

| ||

Gross profit |

| 13.3 | 50.5 |

| |

Research and development costs |

| (34.1 | ) | (29.3 | ) |

Sales and marketing costs |

| (2.6 | ) | (2.8 | ) |

Administrative costs |

| (7.7 | ) | (5.5 | ) |

Other operating income |

| 0.4 | 10.2 |

| |

|

Operating (loss)/profit |

| (30.7 | ) | 23.1 |

|

Net finance income |

| 3.0 |

| 3.9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Pre-tax (loss)/profit |

| (27.7 | ) | 27.0 | |

Taxation |

| 0.7 | (7.3 | ) | |

| |||||

(Loss)/profit after taxation |

| (27.0 | ) | 19.7 |

|

|

BALANCE SHEET HIGHLIGHTS |

| 2005 | 2004 |

| |

| |||||

|

|

|

| ||

Non-current assets |

| 39.8 | 40.5 |

| |

Current assets |

|

|

| ||

Cash and liquid investments |

| 68.0 | 101.8 |

| |

Inventory |

| 3.6 | 6.0 |

| |

Other current assets |

| 22.0 | 15.6 |

| |

| |||||

Liabilities |

|

|

| ||

Current liabilities |

| (46.8 | ) | (47.6 | ) |

Non-current liabilities |

| (3.6 | ) | (8.8 | ) |

| |||||

Net assets |

| 83.0 | 107.5 |

| |

|

27 | |

COMMENTARY REFLECTS THE 2005 NUMBERS, UNLESS OTHERWISE INDICATED

Revenue: This is in line with the predictable revenue guidance given throughout 2005. The main sources of revenue were: two MVA3000 contracts with the NIAID; fixed-price 155 million-dose ACAM2000 contract with the CDC; and product sales of Vivotif. Cost of sales: This decreased in line with revenues generated in the year. |

|

Gross profit: The change in margin reflects the mix of revenues recorded in the two years. During 2004, the gross margin was positively impacted by the reassessment and reduction of costs under the 155 million-dose contract following the decision to close out the two Phase 3 clinical trials early. Research and development costs: Expenditure on R&D increased as a result of the successful progression of projects into later stages of development. Some manufacturing costs are expensed to R&D as the facility is used for work on our R&D programmes. During 2005, we also started to incur operational costs for our fill/finish facility. Administrative costs: This includes costs and a provision, together totalling around £3m, in relation to the MVA litigation. In 2004, administrative costs included two exceptional items totalling £2.6m. Other operating income: During 2004, Baxter paid Acambis a £10.2m settlement for termination of a contract manufacturing agreement. |

|

Net finance income reduced as a result of lower cash. Interest was paid on the lease-financing facility put in place for the reactivation of our manufacturing plant in Canton, MA. |

|

Pre-tax (loss)/profit: The change compared with 2004 is primarily a result of changes to revenue, the gross profit margin and R&D costs. This is in line with management’s expectations. Taxation: The lower effective tax rate reflects the loss-making position, which led to the refund of certain taxes paid in previous profitable periods, and movements in deferred tax liabilities. |

|

Cash and liquid investments: The reduction is a result of increased investment in the R&D pipeline, together with the capital investments in the US R&D facility and the acquisition of a fill/finish capability. Inventory: This balance principally represents ACAM2000 and Vivotif stock. The reduction is partly a result of provisions made against ACAM2000 inventory during 2005. Other current assets: This includes an amount owing at the end of 2005 relating to the shipment of 500,000 doses of MVA3000 vaccine to the NIAID under the MVA3000 contract, which has been settled since the year-end. |

|

A proportion of this balance relates to accruals and deferred income arising under the ACAM2000 155 million-dose contract with the CDC. At 31 December 2005, deferred income relating to this contract was £2.0m (31 December 2004 – £16.5m). The deferred revenue balance will unwind during 2006 as the BLA submission process concludes. Accruals also include payment owing to Baxter for the production of 500,000 doses of MVA3000, which has been settled since the year-end. |

OTHER ITEMS |

SHORT-TERM BORROWINGS AND FINANCIAL LIABILITIES |

The combined balance of our US dollar-denominated financing facilities was £12.8m at 31 December 2005 (31 December 2004 – £13.0m). The balance on the lease-financing facility was £7.2m at 31 December 2005 (31 December 2004 – £9.4m). The balance on the overdraft facility at 31 December 2005 was £4.0m (31 December 2004 – £3.6m), the increase being attributable to exchange rate movements in the period. The remaining balance of £1.6m at 31 December 2005 (31 December 2004 – £nil) relates to the discounted value of the future payments for the Rockville fill/finish facility acquired earlier in 2005, payable between 2006 and 2017. |

|

INVESTING ACTIVITIES |

During 2005, we spent £1.7m (2004 – £0.8m) on the final payments for the BPC acquisition as a result of achieving higher sales of Vivotif. Capital expenditure in 2005 was £3.7m (2004 – £3.4m). Expenditure during the year related to the costs to redevelop and expand areas of our US R&D facility, as well as the acquisition of assets for our Rockville fill/finish facility, which was purchased in May 2005. |

DAVID LAWRENCE, CHIEF FINANCIAL OFFICER

28 | Chairman’s Board review |

|

| |||

Further strengthening our |

|

| ||

|

| |||

As in previous years, during 2005 we made a number of changes that further strengthened our governance of Acambis. Of note this year, we have reviewed composition of Board Committees and remuneration packages and initiated annual reports from each of our Board Committees.

BOARD EVALUATION AND COMMITTEE CHANGES

For the second year running, we appointed an external consultant to facilitate a formal evaluation of the Board. We again reviewed aspects such as Board size, composition and diversity.

As a result, we agreed to review the composition of our Board Committees. Alan Dalby stepped down from the Audit Committee in January 2006, in the light of his role as Chairman of the Remuneration Committee. In March 2006, we agreed that all Non-executive Directors should sit on the Remuneration Committee as there is an obvious link between management’s performance and remuneration. All Non-executive Directors will also continue to sit on the Nominations Committee.

BOARD TRAINING

As part of our ongoing efforts to ensure Board members are fully informed about key issues affecting Acambis and corporate governance matters, ad hoc presentations are provided to the Board. On governance, during 2005, updates were provided to the Board on corporate responsibility and the new Financial Services Authority Handbook, which came into effect in July 2005. We are introducing a structured programme of updates for the Board during 2006.

As per our commitment in last year’s Annual Report, this year, for those Directors who have professional qualifications, we have included an update within the ‘Biographies’ section on their continuing professional development.

REVIEW OF REMUNERATION PACKAGES

At the time of our last Annual Report, we advised that the Remuneration Committee was reviewing the structure of employee and management remuneration. We appointed Towers Perrin and The Hay Group to assist us with this work.

The purpose of this review was to ensure that we reward and motivate our Executive Directors and staff appropriately and provide the right mix of the four core elements of a remuneration package dependent on an employee’s position in the organisation. The four elements are base pay, benefits, learning and development, and work environment.

We are starting to implement specific changes from 2006. The first element is a new structure for long-term incentives, which is being proposed at the 2006 AGM. The details of this proposal are summarised on page 35.

REPORTS FROM BOARD COMMITTEES

For the first time, on pages 34 and 35 we have disclosed high-level reports from the three Committees of the Board – Audit, Nominations and Remuneration – covering the work each of them has performed during 2005 and thus far in 2006 to discharge their respective responsibilities.

29

BOARD CHANGES

Since the beginning of 2006, we have had two Non-executive Director changes to the Board: Michael Lytton has resigned and we have been joined by Dr Peter Fellner.

As I noted in my Chairman’s statement, I have now served 10 years on the Board of Acambis, seven of those as Chairman. This year, I will offer myself for re-election at the AGM, being required to retire by rotation in accordance with the Company’s Articles of Association, but I am planning to retire from the Board during the year. We will announce the appointment of my successor at that time.

ALAN SMITH, CHAIRMAN

| COMPLY OR EXPLAIN: COMPLIANCE WITH THE COMBINED CODE |

| ||

| The Combined Code (the code) was republished in July 2003 and restated in July 2005 by the Financial Reporting Council and incorporated the previous code (as published in 1998 by the Hampel Committee) and related guidance that had been issued since that date: the Turnbull Guidance on Internal Control; the Smith Guidance On Audit Committees; and various items of good practice guidance from the Higgs Report. The code has been applicable for reporting years beginning on or after 1 November 2003 and, therefore, was adopted by Acambis from our 2004 financial year. The overriding principle of the code is that companies must comply with it or explain why they have not. Our corporate governance statement is shown on pages 36 to 39 and provides details on our compliance with the code. The following section highlights the areas where we previously did not comply with the code and notes the progress we have made to address those areas: |

| ||

|

|

| ||

| CODE PROVISION |

| PROGRESS MADE SINCE PUBLICATION OF THE 2004 ANNUAL REPORT |

|

| B REMUNERATION B.2.1 A statement on whether remuneration consultants have any other connection with the Company should be available on the Company’s website. |

|

|

|

|

|

|

|

|

| C ACCOUNTABILITY AND AUDIT C.3.4 Arrangements should be in place for the reporting and management of concerns raised by staff about possible financial or other improprieties. |

| In November 2004, the Audit Committee approved a whistleblowing policy. The procedure was developed during 2005 and rolled out to the Group in early 2006. |

|

|

|

|

|

|

| DIRECTORS’ ATTENDANCE AT BOARD AND COMMITTEE MEETINGS DURING 20051 |

| ||||||||||||||||

| COMMITTEE/BOARD DIRECTOR |

| ALAN |

| GORDON |

| DAVID |

| DR THOMAS |

| DR RANDAL |

| ALAN |

| ROSS |

| MICHAEL |

|

|

|

|

|

|

|

|

|

|

| |||||||||

| BOARD |

| 8/8 |

| 8/8 |

| 8/8 |

| 8/8 |

| 8/8 |

| 6/8 |

| 8/8 |

| 8/8 |

|

| AUDIT COMMITTEE |

| N/A |

| N/A |

| N/A |

| N/A |

| 6/6 |

| 4/6 |

| 6/6 |

| 6/6 |

|

| REMUNERATION COMMITTEE |

| N/A |

| N/A |

| N/A |

| N/A |

| 2/2 |

| 1/2 |

| 2/2 |

| 2/2 |

|

| NOMINATIONS COMMITTEE6 |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

|

| NOTES 1 Meetings include scheduled Board and Committee meetings. 2 Mr Smith is Chairman of both the Board and the Nominations Committee. 3 Mr Dalby is Chairman of the Remuneration Committee. 4 Mr Graham is Chairman of the Audit Committee. 5 Mr Lytton resigned from the Board on 11 April 2006. 6 No meetings of the Nominations Committee took place during the year.

|

| ||||||||||||||||

30 | Board of Directors’ biographies |

The Board is chaired by Alan Smith and has three Executive Directors. Together, they combine business acumen with scientific expertise to provide Acambis with a clear vision and direction that is firmly grounded in commercial realities.

|

1 ALAN SMITH †

Alan Smith, aged 61, a member of the Chartered Institute of Public Finance and Accountancy, joined the Board of Acambis on 3 November 1995 as a Non-executive Director and was appointed Non-executive Chairman on 20 May 1999. On appointment, Alan met the criteria for independence for Non-executive Directors; however, the independence test is not appropriate in relation to the role of Chairman to which he was subsequently appointed. He is also Chairman of the Nominations Committee. He was Group Managing Director of Anglian Water plc until December 1997 and is currently Chairman of Avlar Bioventures Limited, Chairman of Medical Device Innovations Limited and a Non-executive Director of CeNeS Pharmaceuticals plc. Mr Smith is participating in the Continuing Professional Development programme of the Chartered Institute of Public Finance and Accountancy.

2 GORDON CAMERON, OBE *

Gordon Cameron, aged 40, was appointed Chief Executive Officer on 23 February 2004. He was originally appointed to the Board on 1 March 1997 as Chief Financial Officer (formerly Finance Director), having joined Acambis in 1996 from the corporate finance department at N M Rothschild & Sons Limited where he had advised Acambis on its listing on the London Stock Exchange. From 31 March 2001 until his appointment as Chief Executive Officer, Gordon was additionally President of Acambis’ US division, Acambis Inc.. In 2004, he was appointed an Officer of the Order of the British Empire for services to the British biotechnology industry in the US.

Gordon was instrumental in Acambis’ winning and executing on the major smallpox vaccine supply and R&D contracts with the US Government. He combines considerable financial experience with the extensive industry knowledge he has developed during more than nine years with Acambis.

31

3 DAVID LAWRENCE * David Lawrence, aged 43, was appointed to the Board on 8 July 2004 from Chiron Vaccines, where he was Vice President of Finance. In his role at Chiron, David was responsible for all aspects of finance and accounting, and also for strategic planning and business development. In particular, he played a lead role in Chiron’s acquisition of PowderJect Pharmaceuticals plc and the subsequent disposal of various non-core assets/businesses. Prior to Chiron, the majority of David’s career had been spent with GlaxoSmithKline plc, which he joined in 1988. David has considerable industry knowledge and strong financial and management skills that, coupled with the experience he has gained through playing an active role in the rapid growth of Chiron, is invaluable in the management of Acambis’ continued growth. His responsibilities at Acambis include overseeing the finance function and corporate development. 4 DR THOMAS MONATH * Tom Monath, aged 65, a qualified medical doctor, joined Acambis in 1992 and was appointed to the Board as Chief Scientific Officer on 12 March 2002. Prior to joining Acambis, he worked as Colonel and Chief of the Virology Division of the US Army Medical Research Institute of Infectious Disease. During almost 20 years as Director of the CDC’s Division of Vector-Borne Infectious Diseases, he was instrumental in building the division into a key centre for research into arthropod-borne viruses such as yellow fever. Tom is responsible for the direction of Acambis’ programmes to develop vaccines against infectious diseases such as smallpox, JE, West Nile and C. difficile, and led the development of Acambis’ proprietary ChimeriVax technology. He served as a member of the US National Vaccine Advisory Committee. During his career, he has published more than 300 scientific papers and six books, including a seminal work on flaviviruses. Among other external positions, he is Adjunct Professor of Harvard School of Public Health. Dr Monath attends conferences and publishes papers and chapters with respect to maintaining his professional medical accreditation. |

| † Member of the Nominations Committee. * Member of the Executive Committee. ** Member of the Audit, Nominations and Remuneration Committees. *** Member of the Nominations and Remuneration Committees. | ||

| ||||

|

|

| ||

|

| ELIZABETH BROWN, COMPANY SECRETARY | ||

Elizabeth Brown, aged 34, was appointed Company Secretary on 1 July 2002. Elizabeth is a certified accountant and joined Acambis in 1996. In her core role as Vice President of Financial Management, Elizabeth is responsible for financial performance measurement, budgeting and long-term financial planning. In addition, Elizabeth has, in the last few years, overseen the development of Acambis’ risk management systems. | ||||

DIRECTORS’ INFORMATION The Directors who served during the year were: The usual business address of all the Directors, apart from Dr Thomas Monath, is Peterhouse Technology Park, 100 Fulbourn Road, Cambridge CB1 9PT, UK. Dr Monath’s usual business address is Acambis Inc., 38 Sidney Street, Cambridge, MA 02139, US. In accordance with the Company’s Articles of Association, Alan Smith and Alan Dalby will retire by rotation at this year’s AGM and, being eligible, offer themselves for re-election. In addition, Dr Peter Fellner, who has been appointed to the Board since the last AGM, offers himself for election at the AGM. | ||||

32 | Board of Director’s biographies |

Broad mix of industry expertise |

Our Non-executive Directors are a diverse group of individuals who provide a broad mix of expertise, drawn from several different industries. This includes not only sectors that are close to home – vaccines, biotech and pharmaceuticals – but also wider areas that can provide a different perspective on the issues faced by Acambis.

|