UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

☐ | Preliminary Proxy Statement. | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)). | |

| ☐ | Definitive Proxy Statement. | |

| ☒ | Definitive Additional Materials. | |

| ☐ | Soliciting Material Pursuant to §240.14a-12. | |

Nuveen Arizona Quality Municipal Income Fund (NAZ)

Nuveen California AMT-Free Quality Municipal Income Fund (NKX)

Nuveen California Quality Municipal Income Fund (NAC)

Nuveen Massachusetts Quality Municipal Income Fund (NMT)

Nuveen New Jersey Quality Municipal Income Fund (NXJ)

Nuveen Ohio Quality Municipal Income Fund (NUO)

Nuveen Pennsylvania Quality Municipal Income Fund (NQP)

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. | |||

| 1) | Title of each class of securities to which transaction applies:

| |||

| 2) | Aggregate number of securities to which transaction applies:

| |||

| 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| 4) | Proposed maximum aggregate value of transaction:

| |||

| 5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| 1) | Amount Previously Paid:

| |||

| 2) | Form, Schedule or Registration Statement No.:

| |||

| 3) | Filing Party:

| |||

| 4) | Date Filed:

| |||

Nuveen Closed-End Funds Implications of Control Share By-Laws for Preferred Shareholders November [ ], 2020 Nuveen Fund Advisors, LLC Proxy Advisory Firm Presentation

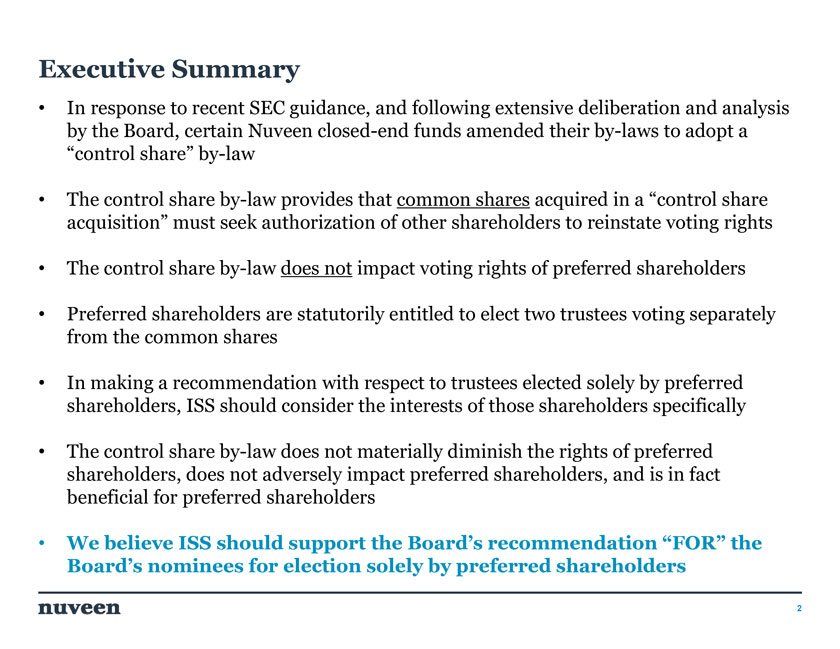

Executive Summary • In response to recent SEC guidance, and following extensive deliberation and analysis by the Board, certain Nuveen closed-end funds amended their by-laws to adopt a “control share” by-law • The control share by-law provides that common shares acquired in a “control share acquisition” must seek authorization of other shareholders to reinstate voting rights • The control share by-law does not impact voting rights of preferred shareholders • Preferred shareholders are statutorily entitled to elect two trustees voting separately from the common shares • In making a recommendation with respect to trustees elected solely by preferred shareholders, ISS should consider the interests of those shareholders specifically • The control share by-law does not materially diminish the rights of preferred shareholders, does not adversely impact preferred shareholders, and is in fact beneficial for preferred shareholders • We believe ISS should support the Board’s recommendation “FOR” the Board’s nominees for election solely by preferred shareholders 2

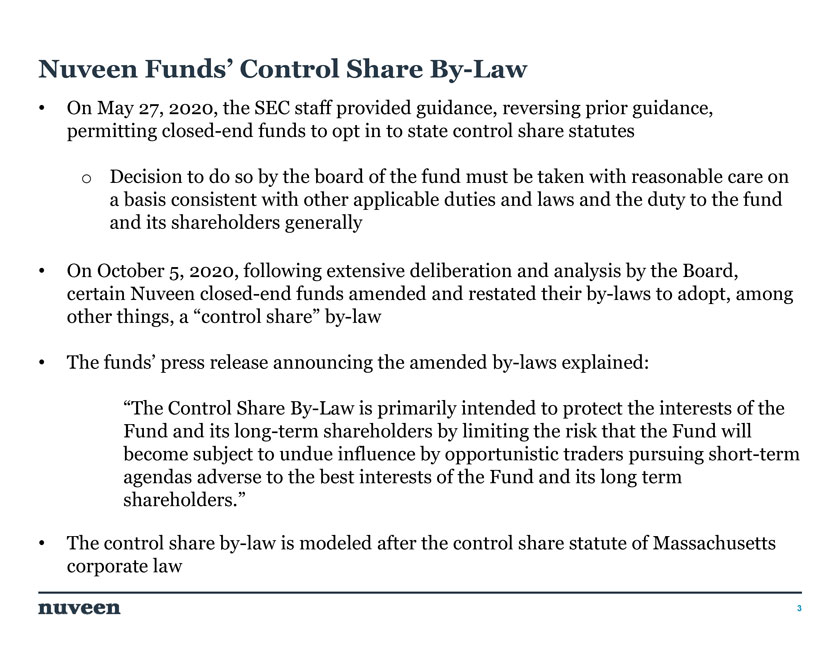

Nuveen Funds’ Control Share By-Law • On May 27, 2020, the SEC staff provided guidance, reversing prior guidance, permitting closed-end funds to opt in to state control share statutes o Decision to do so by the board of the fund must be taken with reasonable care on a basis consistent with other applicable duties and laws and the duty to the fund and its shareholders generally • On October 5, 2020, following extensive deliberation and analysis by the Board, certain Nuveen closed-end funds amended and restated their by-laws to adopt, among other things, a “control share” by-law • The funds’ press release announcing the amended by-laws explained: “The Control Share By-Law is primarily intended to protect the interests of the Fund and its long-term shareholders by limiting the risk that the Fund will become subject to undue influence by opportunistic traders pursuing short-term agendas adverse to the best interests of the Fund and its long term shareholders.” • The control share by-law is modeled after the control share statute of Massachusetts corporate law 3

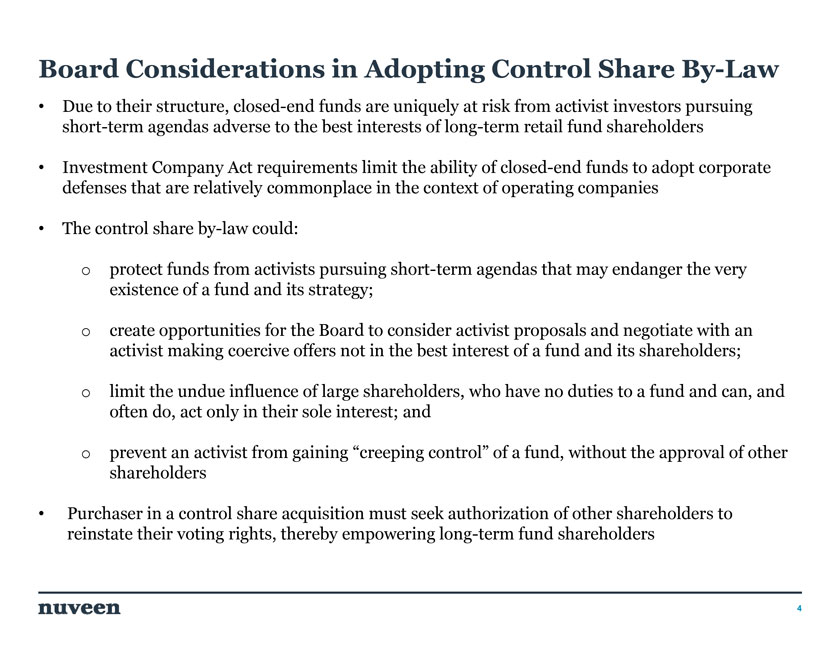

Board Considerations in Adopting Control Share By-Law • Due to their structure, closed-end funds are uniquely at risk from activist investors pursuing short-term agendas adverse to the best interests of long-term retail fund shareholders • Investment Company Act requirements limit the ability of closed-end funds to adopt corporate defenses that are relatively commonplace in the context of operating companies • The control share by-law could: o protect funds from activists pursuing short-term agendas that may endanger the very existence of a fund and its strategy; o create opportunities for the Board to consider activist proposals and negotiate with an activist making coercive offers not in the best interest of a fund and its shareholders; o limit the undue influence of large shareholders, who have no duties to a fund and can, and often do, act only in their sole interest; and o prevent an activist from gaining “creeping control” of a fund, without the approval of other shareholders • Purchaser in a control share acquisition must seek authorization of other shareholders to reinstate their voting rights, thereby empowering long-term fund shareholders 4

Operation of Closed-End Fund Preferred Shares • Many Nuveen closed-end funds have outstanding preferred shares • Closed-end funds utilize preferred shares to implement leveraged investment strategies, allowing a fund to obtain financing at prevailing short-term rates while seeking to invest in higher paying portfolio instruments • The Investment Company Act requires that two trustees of a fund that issues preferred shares be elected solely by the preferred shareholders, voting separately from the common shareholders o Preferred shareholders vote together with the common shareholders to elect the remaining trustees of a fund • Certain types of closed-end fund preferred shares are sold to a limited universe of institutional investors (typically banks) o To mitigate certain regulatory restrictions arising from such ownership, these institutions place the voting rights with respect to such preferred shares in a voting trust o The trustee of a voting trust typically votes such preferred shares in accordance with the recommendations of a proxy advisory firm o As a result, 100% of a fund’s outstanding preferred shares may be voted in accordance with the recommendations of a proxy advisory firm 5

Preferred Share Considerations • Control share by-law applies only to common shares acquired in a control share acquisition • Control share by-law does not impact any voting rights of preferred shareholders o Preferred shareholders, regardless of their percentage ownership, retain all voting rights of such preferred shares, including voting rights established by the Investment Company Act, a fund’s governing documents or the instruments establishing the preferred shares • Preferred shareholders enjoy no potential benefit from typical common share activist agendas: o Common share secondary market discount dynamics do not apply to preferred shareholders o Common share liquidity events typically pursued by activists can only hurt preferred shareholders: ïƒ~ Common share liquidity events reduce a fund’s capital base, thus eroding asset coverage for preferred shares ïƒ~ Common share liquidity often result in redemptions of preferred shares, either to comply with regulatory requirements or to maintain desired leverage levels. Such redemptions take shares out of the hands of preferred shareholders who desire to continue to hold such shares – typically without any redemption premium • Control share by-law protects the interests of preferred shareholders, allowing the Board to consider interests of both common and preferred shareholders in negotiating with activists 6

Preferred Share Recommendation • Recommendation on vote for or against nominees elected solely by preferred shareholders should be determined without regard to the adoption of the control share by-law o The control share by-law does not apply to voting rights of preferred shareholders o A vote against the nominees does not further the interests of preferred shareholders o While reasonable people can debate the potential costs and benefits to common shareholders of a control share by-law, liquidity events pursued by activists are uniformly injurious to preferred shareholders, and thus the control share by-law can only reasonably be seen as beneficial to preferred holders • We believe ISS should support the Board’s recommendation “FOR” the Board’s nominees, particularly the nominees for election solely by preferred shareholders * * * • In the future, we would welcome an opportunity for further discussion regarding the evaluation of, and application of voting guidelines to, adoption of control share by-laws and other defensive measures by closed-end funds, in light of their unique structure and regulatory considerations 7

Appendix A – Upcoming Meetings • On November 16, 2020, the following Nuveen closed-end funds with preferred shares outstanding will hold their annual meeting: Nuveen Arizona Quality Municipal Income Fund (NAZ) Nuveen California AMT-Free Quality Municipal Income Fund (NKX) Nuveen California Quality Municipal Income Fund (NAC) Nuveen Massachusetts Quality Municipal Income Fund (NMT) Nuveen New Jersey Quality Municipal Income Fund (NXJ) Nuveen Ohio Quality Municipal Income Fund (NUO) Nuveen Pennsylvania Quality Municipal Income Fund (NQP) • The nominees for election solely by the holders of preferred shares, voting as a separate class, are: William C. Hunter Albin F. Moschner 8

Appendix B – Nominees for Election by Preferred Shareholders Dr.Hunter isDean Emeritusofthe HenryB. TippieCollege of Business at the University of Iowa. He served as dean of the College from July 2006 until his retirement on June 30, 2012. He had been Dean and Distinguished Professor of Finance at the University of Connecticut School of Business since June 2003. From 1995 to 2003, he was the Senior Vice President and Director of Research at the Federal Reserve Bank of Chicago. While there he served as the Bank’s Chief Economist and was an Associate Economist on the Federal Reserve System’s Federal Open Market Committee (FOMC). In addition to serving as a Vice President in charge of financial markets and basic research at the Federal Reserve Bank in Atlanta, he held faculty positions at Emory University, Atlanta University, the University of Georgia and Northwestern University. A past Director of the Credit Research Center at Georgetown University, past President of the WILLIAM C. Financial Management Association International, and past President of Beta Gamma Sigma, The International Business Honor Society, Dr. HUNTER Hunter has consulted with numerous foreign central banks and official agencies in Western, Central and Eastern Europe, Asia, Central America and South America. From 1990 to 1995, he was a U.S. Treasury Advisor to Central and Eastern Europe. He has been a Director of Wellmark, Inc. since 2009 and was a Director of the Xerox Corporation from 2004 to 2018 and SS&C Technologies, Inc. from 2004 to 2005. Dr. Hunter was elected to the Board in 2003 and he currently serves as a member of the Board’s Audit Committee (since 2018); and Dividend Committee (since 2014); Chair (since 2015). He previously served on the Compliance, Risk Management & Regulatory Oversight Committee (2004-2017); and Closed-End Fund Committee (2012-2015). Mr. Moschner is a consultant in the wireless industry and, in July 2012, founded Northcroft Partners, LLC, a management consulting firm that provides operational, management and governance solutions. Prior to founding Northcroft Partners, LLC, Mr. Moschner held various positions at Leap Wireless International, Inc., a provider of wireless services, where he was as a consultant from February 2011 to July 2012, Chief Operating Officer from July 2008 to February 2011, and Chief Marketing Officer from August 2004 to June 2008. Before he joined Leap Wireless International, Inc., Mr. Moschner was President of the Verizon Card Services division of Verizon Communications, Inc. from 2000 to 2003, and President of One Point Services at One Point Communications from 1999 to 2000. Mr. Moschner also served at Zenith Electronics Corporation as Director, President and Chief Executive Officer from 1995 to 1996, and as Director, President and ALBIN F. MOSCHNER Chief Operating Officer from 1994 to 1995. From 1996 until 2016, he was a member of the Board of Directors of Wintrust Financial Corporation. Since 2019, Mr. Moschner has been the Chairman of the Board of Directors of USA Technologies, Inc. (Director since 2012). He is a board member emeritus of the Advisory Boards of the Kellogg School of Management (since 1995) and previously served as a board member of the Archdiocese of Chicago Financial Council (2012-2018). Mr. Moschner received a Bachelor of Engineering degree in Electrical Engineering from The City College of New York in 1974 and a Master of Science degree in Electrical Engineering from Syracuse University in 1979. Mr. Moschner joined the Fund Board in July, 2016, he currently serves as a member of the Board’s Compliance, Risk Management & Regulatory Oversight Committee (since 2016); Closed-End Fund Committee (since 2016); and Dividend Committee (since 2018). 9