Exhibit 99.1

The World that Information Built

The Thomson Corporation Annual Report 2004

![]()

The world that information built

has no borders.

The business that information built

has no limits.

| |

| |

| |

| |

| |

| |

| |

|

Thomson builds the information

that helps the people

who administer the law,

who search for cures and develop better medicine,

who streamline the mechanisms of the market,

and who create new ways of educating the people

who become the citizens of the world

that information built.

Over the past decade, The Thomson Corporation has become a global leader in the evolving information services industry. We have stepped beyond our success as a print publisher and content provider to become a pioneer in information solutions that integrate digital content with software tools and applications. We are focused on four markets – legal & regulatory, learning, financial and scientific & healthcare – that are essential to the growing knowledge economy. And we are building the scale and scope to compete successfully in each of these markets.

Each year our information solutions gain more traction in the global markets we serve, and those markets are themselves evolving in ways that play to our strengths as a corporation. Our strategy is translating into solid financial results, as evidenced by our 2004 performance.

2004 results

Revenues, operating profit and earnings per share all rose substantially in 2004. Revenues increased 9% to $8.1 billion. Operating profit increased 14% to $1.3 billion, and adjusted earnings per share rose 16% to $1.23, driven by our revenue growth and improved efficiencies. We surpassed $1.1 billion in free cash flow, a 14% increase over 2003. Our strong free cash flow enables us to fund growth initiatives, maintain a strong balance sheet and return value to shareholders through dividends.

Customers continue to migrate to digital solutions, and we experienced double-digit growth from electronic products, software and services. This accounted for two-thirds of our 2004 revenues. Moreover, nearly two-thirds of our revenues came from subscription-based products and services, many of which have renewal rates exceeding 90%.

In addition, we continue to become more efficient by taking advantage of our scale and by sharing technology platforms across our businesses, thus expanding margins. As we shift from print to digital solutions, a higher percentage of our cost base becomes fixed, which offers the potential for greater operating leverage.

Business highlights

2004 highlights included increased sales of innovative offerings such as Thomson ONE, which delivers tailored information solutions for different types of financial professionals, and Westlaw Litigator, which integrates content and tools to meet the distinct needs of litigation attorneys. Another major highlight was the development of new solutions that position us for further growth ahead. After an intensive development effort, we launched Thomson Pharma at the end of 2004. This is the first integrated information solution for the pharmaceutical industry. Customer migration to this solution has begun with excellent initial market reaction.

In 2004 we invested about $1.5 billion in acquisitions that help us build out our information solutions and expand into adjacent markets. For example, the acquisition of Information Holdings Inc. enhances the capabilities and comprehensiveness of Thomson Pharma in important areas such as patent information and regulatory filings.

By acquiring KnowledgeNet, we gained state-of-the-art web-based classroom technology that enables teachers to instruct students remotely. This will help

2

drive sales in both corporate e-learning and higher education. We also acquired TradeWeb, the leading electronic trading platform in the fixed income market. It is a growing business in its own right, but it also enables us to introduce other Thomson Financial offerings to this large and expanding market. In 2005, we will focus on fully integrating these acquisitions, and on leveraging the added skills and scale we have gained to drive growth.

Despite the high level of acquisition spending in 2004, we began and ended the year with a strong balance sheet.

New market opportunities

When we broaden our vision to include information services, not just content, we see myriad opportunities to serve our existing customers in new ways and to expand into adjacent markets. We estimate that the total size of the markets we are able to serve has almost doubled as a result of expanding the current and potential role we play for our customers.

Our markets are experiencing fundamental change, which is driving new demand for information solutions. For example, the Sarbanes-Oxley Act and other regulations are changing the environment in which public corporations do business, which creates additional demands for our legal and regulatory solutions. Changing demographics and spiraling costs are reshaping the healthcare industry; Thomson tailors solutions that help tackle these problems. By creating products that combine print and software tools for students, we help students and educators chart their inevitable journey from dependence on the textbook to adoption of digital learning solutions. These are just a few examples of how our markets are evolving and relying on the kinds of solutions Thomson can offer.

Core values and long-term value

As the knowledge economy expands, Thomson has transformed itself to meet customers’ evolving needs. However, our core values have not changed. The board of directors and management of Thomson are firmly committed to creating long-term value for the company’s shareholders. We manage the company to deliver consistent growth and dependable returns in a changing world.

Thomson takes great pride in its employees. Their expertise, energy and dedication remain the cornerstone of our company’s success. They show the same energy and skill in community service. Thomson fosters a culture of volunteerism that manifests itself in hundreds of worthy projects around the world.

Jack Fraser, who has been on our board of directors since 1989, is retiring at our annual meeting of shareholders in May. We all are indebted to Jack for his role on our board during a period of remarkable transformation.

We look forward to the future with confidence in our people and in our strategy. On behalf of the board and management, we would like to express our continuing appreciation to all our stakeholders: the investors, customers and employees who create such an exciting role for Thomson in the world that information built.

Sincerely,

/s/ David K.R. Thomson |

| /s/ Richard J. Harrington |

|

David K.R. Thomson | Richard J. Harrington | ||

Chairman of the Board | President & Chief Executive Officer | ||

3

The Thomson Corporation

|

| 04 |

| 03 |

| change |

| |||

Revenues |

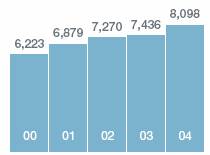

| 8,098 |

| 7,436 |

| + | 9 | % | ||

Operating profit |

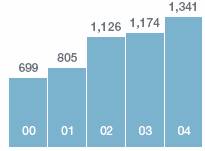

| 1,341 |

| 1,174 |

| + | 14 | % | ||

Earnings attributable to common shares |

| 1,008 |

| 877 |

| + | 15 | % | ||

Earnings per common share (EPS) |

| $ | 1.54 |

| $ | 1.34 |

| + | 15 | % |

Adjusted earnings from continuing operations(1) |

| 805 |

| 694 |

| + | 16 | % | ||

Adjusted EPS from continuing operations(1) |

| $ | 1.23 |

| $ | 1.06 |

| + | 16 | % |

Shareholders’ equity |

| 9,962 |

| 9,193 |

|

|

|

| ||

Net cash provided by operating activities |

| 1,808 |

| 1,654 |

| + | 9 | % | ||

Free cash flow(2) |

| 1,123 |

| 983 |

| + | 14 | % | ||

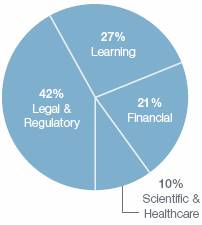

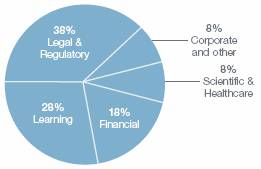

Revenue by Market Group

A balanced portfolio serving large and growing markets provides a diversified revenue stream

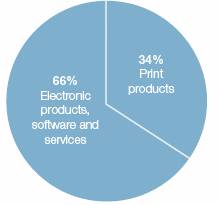

Revenue by Media

Continuing evolution from print to electronic products, software and services – which now account for two-thirds of revenues

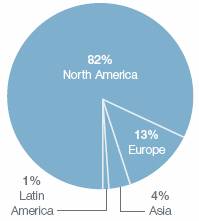

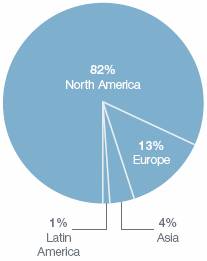

Revenue by Geography

Building from a strong position in North America, while continuing to expand current offerings and seek new opportunities in international markets

4

Growth Metrics

Revenues

Revenues grew 9%, driven by strategic acquisitions and organic growth, which included strong sales of electronic products, software and services

Operating Profit

Operating profit grew 14% as a result of solid revenue growth and improved efficiencies company-wide

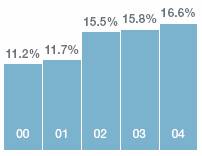

Operating Profit Margin

Operating profit margin increased by 80 basis points, the fifth consecutive year of margin expansion

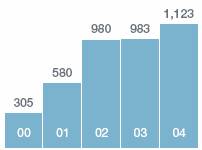

Free Cash Flow(2)

Free cash flow, a key measure of financial strength, grew 14%, to over $1.1 billion

Adjusted EPS from Continuing Operations(1)

Strong operating performance drove adjusted earnings up 16% to $1.23 per share

Dividends Per Common Share

Steadily increasing cash dividends have enhanced total returns to shareholders

† Millions of U.S. dollars except per common share amounts. Adjusted earnings from continuing operations, adjusted EPS from continuing operations and free cash flow are non-GAAP financial measures, which are reconciled to the most directly comparable GAAP financial measures within the MD&A.

(1) Excludes one-time items. For a full reconciliation to reported earnings, see the six-year summary on page 114.

(2) Net cash provided by operating activities less net additions to property and equipment, other investing activities and dividends paid on preference shares.

(3) Excludes a special dividend of $0.428 related to the sale of our 20% interest in Bell Globemedia Inc. (see Note 22 to consolidated financial statements on page 105).

5

Long-Term Financial Targets

Grow revenues 7 to 9% annually

2004 Results: Total revenues grew 9% to $8.1 billion

• All market groups grew organically

• Strategic acquisitions provided new revenue streams and expanded capabilities in market groups

• Electronic products, software and services grew to 66% of revenues, compared to 51% five years ago

• Recurring revenues were 65% of total

Expand profit margins

2004 Results: Operating profit margins expanded 80 basis points to 16.6%

• Fifth consecutive year of margin expansion

• Continued to increase efficiency by leveraging technology and other assets across the company and taking advantage of size and scale

• Successfully integrated recently acquired companies

Generate strong free cash flow

2004 Results: Free cash flow exceeded $1 billion

• Free cash flow grew 14% for the year; up nearly 40% compounded annually since 2000

• 14% of total revenues, versus 5% in 2000

• Fourth consecutive year of growth

6

Market Group Performance††

Legal & Regulatory

|

| 04 |

| change |

| ||

Revenues |

| $ | 3,393 |

| + | 8 | % |

Adjusted operating profit* |

| $ | 882 |

| + | 11 | % |

Adjusted operating profit margin* |

| 26.0 | % | + | 60 | bp | |

2004 Highlights

• Checkpoint, our online tax service, delivered strong growth

• Westlaw Litigator, an integrated solution for litigation attorneys, continued to achieve high growth

• FindLaw growth was fueled by strong new sales and acquisitions

2005 Priorities

• Continue to grow our software and services offerings

• Continue to pursue integrated offerings that add value to our customers’ workflow

• Continue implementation of Novus, our next generation online delivery platform

Learning

|

| 04 |

| change |

| ||

Revenues |

| $ | 2,174 |

| + | 6 | % |

Adjusted operating profit* |

| $ | 327 |

| - | 3 | % |

Adjusted operating profit margin* |

| 15.0 | % | - | 140 | bp | |

2004 Highlights

• Enhanced print publications for the U.S. higher education market with online research and homework tools

• Expanded corporate e-learning and e-testing technology platform and business opportunities through KnowledgeNet and Capstar acquisitions

2005 Priorities

• Continue to focus on growth and profitability of core textbook business

• Capitalize on the growing trend of education as a lifelong pursuit

• Lead the migration to integrated digital solutions by leveraging ongoing investment in products and technology

Financial

|

| 04 |

| change |

| ||

Revenues |

| $ | 1,734 |

| + | 15 | % |

Adjusted operating profit* |

| $ | 298 |

| + | 31 | % |

Adjusted operating profit margin* |

| 17.2 | % | + | 210 | bp | |

2004 Highlights

• Delivered strong revenue growth in corporate and fixed income markets

• Grew Thomson ONE workstations +56%

• Expanded capabilities in adjacent markets through strategic acquisitions of TradeWeb, CCBN and Starquote

2005 Priorities

• Continue to develop product offerings tailored to end-user needs

• Leverage assets to create end-to-end workflow solutions

Scientific & Healthcare

|

| 04 |

| change |

| ||

Revenues |

| $ | 836 |

| + | 10 | % |

Adjusted operating profit* |

| $ | 222 |

| + | 19 | % |

Adjusted operating profit margin* |

| 26.6 | % | + | 210 | bp | |

2004 Highlights

• Launched Thomson Pharma – the first integrated information solution for the pharmaceutical market

• Expanded content offerings with selective acquisitions of BIOSIS, Information Holdings Inc., Newport Strategies and Scientific Connexions

2005 Priorities

• Drive rollout of Thomson Pharma

• Continue transformation from delivering discrete products to providing customers with integrated solutions

• Integrate acquisitions to take full advantage of new capabilities

†† Amounts are in millions of U.S. dollars and represent results from ongoing businesses, which exclude businesses sold or held for sale that do not qualify as discontinued operations.

* Before amortization.

7

The business that information built has no limits.

Thomson builds the information that helps the people

In a world built on information, knowledge becomes the critical resource The rise of the information economy has changed the way the world does business. Digital information flows in all directions, streaming across national borders and work/life boundaries. But the information economy is still young. The demand for tools that transform information into knowledge and put it to work will continue to grow. In this globally competitive knowledge economy, it’s not only what you know that counts –it’s how fast and effectively you can apply this knowledge.

Information is only the beginning

The world that information built is awash in content. Knowledge workers are drowning in data. Thomson delivers timely, accurate, high-quality information – but that’s just the starting point. We add further value by helping customers sort and interpret that information, and use the knowledge to make quicker, more intelligent decisions. That’s what sets us apart from the Internet search companies that deliver oceans of information of uncertain relevance and validity.

Here, there, and everywhere

It no longer matters where information resides – which library, which database, which server. Information should be available wherever it’s needed, in whatever medium suits the user. A physician can look up our drug information in a book, access it via the hospital’s information systems or call it up on her PDA. A student reading one of our textbooks at home can use our online tools to locate supplemental information, self-assess his learning or get tutoring.

Workflow depends on information flow

From litigation lawyers to librarians, knowledge workers rely on specialized information and research/analytical tools to do their daily work. We partner with thousands of customers across our markets to map their workflows: what are the key tasks, in which sequence, using which data and tools? We then develop information solutions that let our customers spend their workday applying expert judgment rather than battling information bottlenecks.

The Thomson Corporation is a world leader in providing integrated information solutions to business and professional customers. Our comprehensive databases offer unsurpassed breadth and depth of information. We tailor our information solutions to meet customer needs, adding workflow applications, powerful technology and services that help our customers become not only better informed but also more productive. Our best-in-class solutions wed content with technology to help our customers – accountants, attorneys, bankers, brokers, doctors, educators, scientists and students – make better decisions faster. Thomson has 40,000 employees and operations in 45 countries.

who administer the law,

Managing the business of law Thomson West has long been the leading U.S. information resource for the practice of law. Building upon that strong foundation, we have expanded our services to assist legal professionals in all aspects of their professional development and practice, helping them provide their clients with high-quality legal advice and service. Thomson Elite’s suite of applications streamlines the essential tasks involved in running a successful practice, from client relationship management to accurate billing and record keeping. West LegalEdcenter offers lawyers web-based continuing legal education courses. And our FindLaw client development services bring individuals and businesses together with the right law firms.

Keeping pace with change

Dramatic changes in the regulatory environment, brought on by the Sarbanes-Oxley Act and related requirements, have increased the amount of work for accounting firms. Companies face additional accounting and legal requirements, fueling demand for our compliance information and services. As firms devote more time to regulatory changes, they need our labor-saving solutions to keep up with their expanding workload.

Specialized resources to meet specialized needs

Today, more and more law firms are establishing specialist practice groups, such as those which help clients with legal issues concerning homeland security, privacy or outsourcing. Meeting the specialist’s information needs requires comprehensive databases, sophisticated data management tools and, most of all, insight into the specialist’s workflow. The trend toward specialization calls for tailored solutions like Westlaw Litigator, which delivers information and tools designed to meet a litigator’s unique needs.

Integrating knowledge to create value

Firms consolidate, regulations become more stringent and productivity pressures keep mounting. Legal and regulatory professionals are challenged to deliver more value faster. As our customers strive to optimize the business performance of their practices, they find that our integrated solutions outperform individual, stand-alone products. Our solutions accelerate practice development by simplifying workflows and aligning front and back-office functions firmly behind a practice’s goals.

Thomson Legal & Regulatory is a global market-share leader with one million customer accounts. We are the top provider of legal information services in the United States and we continue to expand globally. For tax and accounting professionals, Checkpoint has become the online solution of choice by integrating the most trusted information and analysis with unsurpassed cross-linking and functionality on a state-of-the-art technology platform. Thomson Legal & Regulatory has 17,250 employees and operations in 22 countries.

who search for cures and develop better medicine,

Safer drugs, faster Thomson Pharma is a comprehensive information solution designed to support the drug development process – from research and discovery, through clinical trials, licensing and launching the product, all the way to patent expiry. To develop it, we spent time with biologists, chemists, clinical researchers, regulatory affairs professionals and others involved in drug development. We asked them what they do each workday, what questions arise and where they turn for answers. Then we built a highly customizable solution that integrates data and technology from across Thomson businesses, including our Scientific & Healthcare, Financial and Legal & Regulatory databases.

As scientific borders dissolve, innovation thrives

Our scientific business is our most global business, with half its revenues coming from outside North America. ISI Web of Science, our patent and intellectual property information, and information solutions like the Web of Knowledge have worldwide relevance and credibility. Today, the traditional boundaries between sciences are dissolving. Thomson has the breadth of data and expertise to support new research that flows across boundaries –the kind of research that will drive tomorrow’s breakthroughs.

Helping to curb healthcare costs

The rising cost of care is one of the most challenging economic issues confronting nations, businesses and families today. The aging population in more developed countries further increases the need for high-quality, low-cost care – and thus the need for information solutions that facilitate effective and efficient healthcare delivery. The Advantage Suite of cost management solutions from Thomson Medstat helps U.S. healthcare institutions address this need.

Supporting critical point-of-care decisions

Driven by the aging population, the demand for healthcare services is expected to outpace available doctors and nurses. At the same time, continued innovation in clinical practice expands the knowledge base. We mine information and use our expertise to create tools that make clinicians more effective and productive. We will continue to integrate Thomson data and technology to ensure that healthcare professionals have information on hand to make better, faster point-of-care decisions.

Thomson Scientific & Healthcare provides information solutions that advance innovation and discovery in science, technology and healthcare. We help doctors to prescribe the most effective drugs for their patients, hospitals to manage costs, and corporations and universities to accelerate their research and development activities. Our products are among the most trusted and widely used in their fields, from the drug labeling data in PDR to the research information in ISI Web of Science, and from the drug and disease databases of Micromedex to global patent information from MicroPatent and Delphion. Thomson Scientific & Healthcare has 4,300 employees and operations in 19 countries.

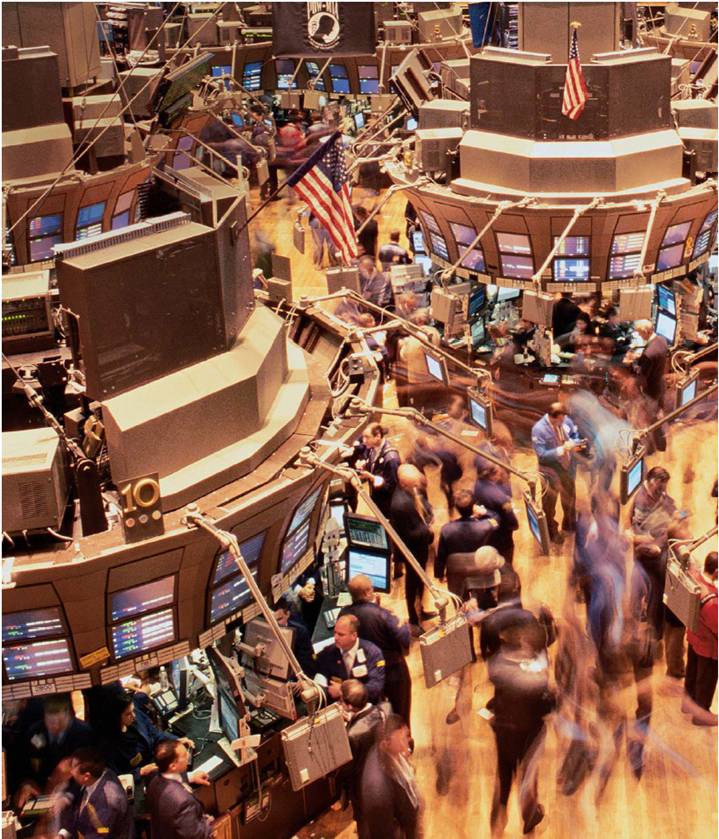

who streamline the mechanisms of the market,

More, better, faster transactions Every day, financial professionals make decisions and execute transactions in which seconds can make the difference between profit and loss. Thomson ONE solutions integrate and configure information and analytics, and tailor them to the customer’s workflow. By aggregating information and automating workflow, Thomson ONE helps make financial markets more efficient, transparent and accurate. As a result, our clients trust Thomson Financial to facilitate over $100 billion of fixed income and equity trades a day.

Partners in productivity

Faced with ongoing consolidation, financial services firms are feeling intense productivity pressure. So we asked 5,000 customers how they do their daily work, where the bottlenecks arise, and what would help them work faster and with greater precision. We built Thomson ONE based on what they told us, partnering with our customers to solve their workflow problems. And because Thomson ONE is modular, customers pay only for what they use.

We’re open about our standards

Some of our competitors base their business model on proprietary technology. We believe that customers benefit from open standards. Thomson ONE is an open, flexible technology platform designed to flow into our customers’ existing information systems. Thomson ONE combines our content with third-party data and the customers’ own proprietary information. It delivers all that content seamlessly to the customers’ desktops.

High volume, high speed

By dollar volume, more transactions are done over the Internet on Thomson TradeWeb than on the New York Stock Exchange. Prior to TradeWeb, trading in the bond markets was mostly done over the telephone. TradeWeb took trading online and made the transactions instantaneous. Combined with other Thomson content and tools, TradeWeb positions us to deliver comprehensive workflow solutions for the fixed income markets.

Thomson Financial is a Big Three provider of information solutions to the global financial services market. We operate as one integrated entity that delivers tailored solutions to investment banks, retail wealth managers, institutional traders, investment managers and corporate issuers. Our flagship solution, Thomson ONE, integrates leading branded products such as TradeWeb, FirstCall and AutEx with innovative analytics to create a new industry standard platform – and, most importantly, helps financial services professionals be more efficient and effective. Thomson Financial has 8,200 employees and operations in 22 countries.

and who create new ways of educating the people

The know-how of learning now Thomson Learning works closely with students and teachers on campus to explore the impact of electronic instructional solutions on learning. In a pilot program at the University of Virginia, for example, we have partnered with Microsoft and Hewlett-Packard to provide students with tablet computers and wireless access to course content, interactive simulations and diagnostic tutorials. Students are able to study anytime, anywhere and interact online with instructors, each other, course materials and tutorials. The diagnostic tools help professors monitor progress, and help students understand their own learning gaps so they can study more efficiently.

The evolution of learning

Like other areas of the knowledge economy, higher education is shifting from print to digital – but at a slower, less predictable pace. To meet the needs of students and institutions in all phases of this digital evolution, we integrate academic and library reference content to create tailored products in all media: print, e-products and print/digital hybrids such as textbooks supported by online research and homework tools.

The changing face of the student

The residential student, 18–21 years old, has become a minority among college students. Thomson provides solutions for the rapidly expanding number of older and non-traditional learners. We help meet the knowledge economy’s growing need for remedial education in colleges, on-the-job training for professionals and distance learning for students who don’t spend their days on campus.

The changing face of the educational institution

A global workforce, an aging population, technology mandating new job skills – these trends force more employers to become educators. Meanwhile, back in academia, growing enrollment outside traditional colleges – e.g., in online universities – is beginning to transform instruction. By providing digital course materials, testing services and productivity tools, we help institutions, whether academic or corporate, meet the needs of lifelong learners.

Thomson Learning is among the largest providers of tailored learning solutions in a world where education must evolve to meet the needs of a borderless knowledge economy and where learning is a lifelong activity. Through imprints like Thomson Wadsworth, Thomson South-Western and Thomson Gale, we publish some of the most widely adopted college textbooks and reference materials. We supplement our print publications with software tools and applications that support the different learning styles of diverse students. Businesses like Thomson Prometric and Thomson NETg offer a broad array of training and assessment solutions for knowledge workers in all phases of their careers. Thomson Learning has 9,800 employees and operations in 40 countries.

who become the citizens of the world that information built.

Financial and Corporate Information

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

24

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

25

Management’s Discussion and Analysis

The following management’s discussion and analysis is intended to assist you in better understanding and evaluating material changes in our financial condition and operations for the year ended December 31, 2004, compared to the preceding fiscal year. We recommend that you read this discussion and analysis in conjunction with our consolidated financial statements prepared in accordance with accounting principles generally accepted in Canada, or Canadian GAAP, and the related notes to those financial statements. All dollar amounts in this discussion are in U.S. dollars unless otherwise specified. Unless otherwise indicated, references in this discussion to “we,” “our” and “us” are to The Thomson Corporation and its subsidiaries. This management’s discussion and analysis contains forward-looking statements. Readers are cautioned that these forward-looking statements are subject to risks and uncertainties, including those identified on page 56 of this management’s discussion and analysis and in the “Risk Factors” section of our annual information form, which is also contained in our annual report on Form 40-F. This management’s discussion and analysis is dated as of February 22, 2005.

Our Business

We are one of the world’s leading information services providers to business and professional customers. We generate revenues by supplying our customers with business-critical information, which we make more valuable by adding expert analysis, insight and commentary, and couple it with software tools and applications that our customers can use to search, compare, synthesize and communicate the information. To further enhance our customers’ workflows, we increasingly deliver information and services electronically, integrate our solutions with our customers’ own data and tailor the delivery of information to meet specific customer needs. As we integrate critical information with analysis, tools and applications, we place greater focus on the way our customers use our content, rather than simply on selling the content itself.

As a global company that provides services in approximately 130 countries, we are affected by the market dynamics, governmental regulations and business conditions for each market and country in which we operate. Our business continues to evolve in conjunction with changes in our customers’ workflows. Our customers’ increasing desire for information, along with their increasing technological sophistication, has translated into gains in strategically important areas of our businesses such as online information, software and service offerings. However, while we face unique challenges in each of our markets, the European financial market and the IT testing market in the United States in particular have experienced difficult economic conditions and strong competition, which have led to increasing pricing pressures and affected revenue growth. During the past few years, we have concentrated on driving efficiencies, primarily through leveraging resources, which has helped us increase our profitability and is reflected in our higher profit margins. We also generated significant cash flow from operations, reflecting our strong results and the quality of our earnings.

26

The following table summarizes selected financial information for 2004 and 2003, including certain metrics that are non-GAAP financial measures. Please see the section below entitled “Use of Non-GAAP Financial Measures” for definitions of these terms and refer to the “Reconciliations” section at the end of this management’s discussion and analysis for a reconciliation of these measures to the most directly comparable Canadian GAAP measures.

|

| Year ended December 31 |

|

|

| ||||

(millions of U.S. dollars, except per share amounts) |

| 2004 |

| 2003 |

| Change |

| ||

Consolidated statement of earnings data |

|

|

|

|

|

|

| ||

Revenues |

| 8,098 |

| 7,436 |

| 9 | % | ||

Operating profit |

| 1,341 |

| 1,174 |

| 14 | % | ||

Earnings attributable to common shares(1) |

| 1,008 |

| 877 |

| 15 | % | ||

Basic and diluted earnings per common share(1) |

| $ | 1.54 |

| $ | 1.34 |

| 15 | % |

Consolidated balance sheet data |

|

|

|

|

|

|

| ||

Cash and cash equivalents |

| 405 |

| 683 |

|

|

| ||

Total assets |

| 19,643 |

| 18,685 |

|

|

| ||

Total liabilities |

| 9,681 |

| 9,492 |

|

|

| ||

Shareholders’ equity |

| 9,962 |

| 9,193 |

|

|

| ||

Other data(2) |

|

|

|

|

|

|

| ||

Adjusted EBITDA |

| 2,247 |

| 2,040 |

| 10 | % | ||

Adjusted earnings from continuing operations |

| 805 |

| 694 |

| 16 | % | ||

Adjusted earnings per common share from continuing operations |

| $ | 1.23 |

| $ | 1.06 |

| 16 | % |

Net debt |

| 3,718 |

| 3,373 |

|

|

| ||

Free cash flow |

| 1,123 |

| 983 |

|

|

| ||

(1) Results are not directly comparable due to certain one-time items. For more information, please see the “Results of Operations” section of this management’s discussion and analysis.

(2) Non-GAAP financial measures.

We organize our operations into four market groups that are structured on the basis of the customers they serve:

• THOMSON LEGAL & REGULATORY is a leading provider of integrated information solutions to legal, tax, accounting, intellectual property, compliance and other business professionals, as well as government agencies. Major brands include Westlaw, Aranzadi, BAR/BRI, Carswell, Checkpoint, Compu-Mark, Creative Solutions, Dialog, Thomson Elite, FindLaw, Gee, IOB, Lawbook, RIA, Sweet & Maxwell and Thomson & Thomson.

• THOMSON LEARNING is a leading provider of tailored learning solutions to colleges, universities, professors, students, libraries, reference centers, government agencies, corporations and professionals. Major brands include Thomson Course Technology, Thomson Delmar Learning, Thomson Gale, Thomson Heinle, Thomson Nelson, Thomson NETg, Thomson Peterson’s, Thomson Prometric, Thomson South-Western and Thomson Wadsworth.

• THOMSON FINANCIAL is a leading provider of products and integration services to financial and technology professionals in the corporate, investment banking, institutional, retail wealth management, and fixed income sectors of the global financial community. Its flagship brand is Thomson ONE. Other major businesses and brands include AutEx, Baseline, BETA Systems, CCBN, Datastream, First Call, I/B/E/S, IFR, Investext, IR Channel, SDC Platinum and TradeWeb.

27

• THOMSON SCIENTIFIC & HEALTHCARE is a leading provider of information and services to researchers, physicians and other professionals in the healthcare, academic, scientific, corporate and government marketplaces. Major businesses and information solutions include Derwent World Patents Index, Medstat, Micromedex, MicroPatent, PDR (Physicians’ Desk Reference), Thomson Pharma, ISI Web of Science and Web of Knowledge, and continuing medical education providers Physicians World and Gardiner-Caldwell.

We also report financial results for a corporate and other reporting category, as well as discontinued operations. The corporate and other category principally includes corporate expenses and costs associated with our stock-related compensation.

We face a changing competitive landscape. Certain of our traditional competitors are trying to follow our solutions strategy and narrow our lead in many areas of technology. But in the years ahead, other competitors could come from outside our traditional competitive set. For instance, Internet service companies could pose a threat to some of our businesses by providing more in-depth offerings. In response to this, we are continuing to move forward aggressively in segmenting our markets and developing solutions tailored to our customers’ workflows.

We expect full-year 2005 revenue growth to be in line with our long-term target of 7% to 9%, excluding the effects of currency translation. Full-year 2005 revenue growth will continue to be driven by growth from existing businesses and supplemented by tactical acquisitions.

Adjusted EBITDA margins are expected to expand slightly in 2005, reflecting continued operating improvements, partially offset by higher pension costs and corporate expenses.

We also expect to continue to generate strong free cash flow in 2005.

Revenues

The following graphs show the percentage of our 2004 revenues by geography, media and type.

REVENUE BY GEOGRAPHY

REVENUE BY MEDIA

REVENUE BY TYPE

28

Our revenues are derived from a diverse customer base. In both 2004 and 2003, no single customer accounted for more than 2% of our total revenues.

We segment our revenues geographically by origin of sale in our financial statements. In 2004, 82% of our revenues were from our operations in North America, consistent with that in 2003. In the long-term, we are seeking to increase our revenues from outside North America as a percentage of our overall revenues. We can modify and offer internationally many of the products and services we developed originally for customers in North America without excessive customization or translation. This represents an opportunity for us to earn incremental revenues. For some of the products and services we sell internationally, we incur additional costs to customize our products and services for the local market and this can result in lower margins if we cannot achieve adequate scale. Development of additional products and services and expansion into new geographic markets are integral parts of our growth strategy. While development and expansion present an element of risk, particularly in foreign countries where local knowledge of our products may be lacking, we believe that the quality and brand recognition of our products and services help to mitigate that risk.

We use a variety of media to deliver our products and services to our customers. Increasingly, our customers are seeking products and services delivered electronically and are migrating away from print-based products. We deliver information electronically over the Internet, through dedicated transmission lines, CDs and, more recently, through handheld wireless devices. We expect that electronic, software and services revenues as a percentage of our total revenues will increase slightly in 2005 compared to 2004 as we continue to emphasize electronic delivery, add solution-based and software-based acquisitions to our portfolio, and as markets outside North America continue to incorporate technology into their workflow. In 2004, electronic, software and services revenues, as a percentage of our total revenues, increased primarily due to acquisitions within our financial group and the continued evolution of customers’ preferences towards electronic products and solutions. Electronic delivery of our products and services improves our ability to provide additional products and services to our existing customers and to access new customers around the world.

Approximately 65% of our revenues are generated from subscription or similar contractual arrangements, which we refer to as recurring revenues. Subscription revenues are from sales of products and services that are delivered under a contract over a period of time. Our subscription arrangements are most often for a term of one year, after which they automatically renew or are renewable at our customers’ option, and the renewal dates are spread over the course of the year. Because a high proportion of our revenues come from subscription and similar arrangements where our customers contract with us for a period of time, our revenue patterns are generally more stable compared to other business models that sell products in discrete or one-off arrangements. In the case of some of our subscription arrangements, we realize additional fees based upon usage. We recognize revenues from sales of some products, primarily our textbooks, after we estimate customer returns. We sell our textbooks and related products to bookstores on terms that allow them to return the books to us if they are not sold. In 2004, revenues from recurring arrangements remained consistent with that of the prior year at 65% of total revenues. As a result of acquisitions in 2004, we anticipate that this percentage will increase.

Expenses

As an information provider, our most significant expense is labor. Our labor costs include all costs related to our employees, including salaries, bonuses, commissions, benefits and payroll taxes, but do not include costs related to our stock-related compensation. Labor represented approximately 57% of our cost of sales, selling, marketing, general and administrative expenses (operating costs) in 2004 compared to approximately 58% in 2003. No other category of expenses accounted for more than 15% of our operating costs in either 2004 or 2003.

29

Acquisitions and Dispositions

During 2003 and 2004, we completed 84 acquisitions for an aggregate cost of approximately $1.7 billion through cash outlays and other financing arrangements. Many of these acquisitions were tactical in nature and related to the purchase of information, products or services that we integrated into our operations to broaden the range of our product and service offerings to better serve our customers. This is the key principle that drives our overall acquisition strategy. As alternatives to the development of new products and services, tactical acquisitions often have the advantages of faster integration into our product and service offerings and cost efficiencies. During 2003 and 2004, acquired businesses generated a significant portion of the growth in our total revenues and a lesser portion of the growth in our operating profit. Generally, the businesses that we acquired in 2003 and 2004 have initially had lower margins than our existing businesses. In 2004, our largest acquisitions were Information Holdings Inc. (IHI), a provider of intellectual property and regulatory information, for $445 million, net of cash and cash equivalents received, and TradeWeb, an online trading platform for fixed income securities, for $361 million, net of cash received, plus contingent payments of up to $150 million over the next three years based upon the achievement of certain growth targets. In 2005, we expect that the total amount of cash outlays for acquisitions will decrease from the 2004 level of $1.3 billion.

When integrating acquired businesses, we focus on eliminating cost redundancies and combining the acquired products and services with our existing offerings. We may incur costs, such as severance payments to terminate employees and contract cancellation fees, when we integrate businesses. We include many of these costs in deriving our operating profit.

During 2003 and 2004, we completed 16 dispositions for aggregate consideration of approximately $1.0 billion. While a number of these businesses possessed strong brand equity, loyal customer bases and talented employees, these businesses did not provide the type of synergies that strengthen our core integrated information solutions. The more significant of these dispositions were the sale of our 20% interest in Bell Globemedia Inc., or BGM, in April 2003 for $279 million, the sale of our healthcare magazines in October 2003 for $135 million and the sale of Thomson Media group in October 2004 for gross proceeds of $350 million. The BGM transaction is discussed in the section entitled “Related Party Transactions” and the healthcare magazines and Thomson Media group transactions are discussed in the section entitled “Discontinued Operations.”

Seasonality

We typically derive a much greater portion of our operating profit and operating cash flow in the second half of the year as customer buying patterns are concentrated in the second half of the year, particularly in the learning and regulatory markets. Costs are incurred more evenly throughout the year. As a result, our operating margins generally increase as the year progresses, though the seasonality of our overall results between the first and second halves has been reducing over the past several years. For these reasons, it may not be possible to compare the performance of our businesses quarter to consecutive quarter, and our quarterly results should be considered on the basis of results for the whole year or by comparing results in a quarter with the results in the same quarter of the previous year. While we report results quarterly, we view and manage our business from a longer-term perspective.

30

Use of Non-GAAP Financial Measures

In addition to our results reported in accordance with Canadian GAAP, we use non-GAAP financial measures as supplemental indicators of our operating performance and financial position. We use these non-GAAP financial measures internally for comparing actual results from one period to another, as well as for future planning purposes. We have historically reported non-GAAP financial results as we believe their use provides more insight into our performance. The following discussion defines the measures that we use and explains why we believe they are useful measures of our performance, including our ability to generate cash flow:

• ADJUSTED EBITDA. We define adjusted EBITDA as earnings from continuing operations before interest, taxes, depreciation and amortization, net other income (expense) and equity in net losses of associates, net of tax. Because adjusted EBITDA excludes amortization, interest and taxes, it provides a more standard comparison among businesses by eliminating the differences that arise between them due to the manner in which they were acquired or funded. We use the measure as a supplemental cash flow metric as adjusted EBITDA also excludes depreciation and amortization of identifiable intangible assets, which are both non-cash charges. Net other income, which normally includes non-operating items such as gains and losses on sales of investments, is excluded from adjusted EBITDA as this item is not considered relevant to operating performance. Finally, as the results of equity in associates are not directly under our control, we exclude this item from our analysis of current operating performance. We also use adjusted EBITDA margin, which we define as adjusted EBITDA as a percentage of revenues.

• ADJUSTED OPERATING PROFIT. Adjusted operating profit is defined as operating profit before amortization of identifiable intangible assets. We use this measure for our segments because we do not consider amortization to be a controllable operating cost for purposes of assessing the current performance of our segments. We also use adjusted operating profit margin, which we define as adjusted operating profit as a percentage of revenues.

• FREE CASH FLOW. We evaluate our operating performance based on free cash flow, which we define as net cash provided by operating activities less additions to property and equipment, other investing activities and dividends paid on our preference shares. We use free cash flow as a performance measure because it represents cash available to repay debt, pay common dividends and fund new acquisitions.

• ADJUSTED EARNINGS AND ADJUSTED EARNINGS PER COMMON SHARE FROM CONTINUING OPERATIONS. We measure our earnings attributable to common shares and per share amounts to adjust for non-recurring items, discontinued operations and other items affecting comparability, which we refer to as adjusted earnings from continuing operations and adjusted earnings per common share from continuing operations. We use these measures to assist in comparisons from one period to another. Adjusted earnings per common share from continuing operations do not represent actual earnings per share attributable to shareholders.

• NET DEBT. We measure our indebtedness including associated hedging instruments (swaps) on our debt less cash and cash equivalents. Given that we hedge some of our debt to reduce risk, we include hedging instruments as a better measure of the total obligation associated with our outstanding debt. We reduce gross indebtedness by cash and cash equivalents on the basis that they could be used to pay down debt.

These and related measures do not have any standardized meaning prescribed by Canadian GAAP and, therefore, are unlikely to be comparable with the calculation of similar measures used by other companies. You should not view these measures as alternatives to operating profit, cash flow from operations, net earnings, total debt or other measures of financial performance calculated in accordance with GAAP. We encourage you to review the reconciliations of these non-GAAP financial measures to the most directly comparable Canadian GAAP measure within this management’s discussion and analysis.

31

The following discussion compares our results in the fiscal years and the three-month periods ended December 31, 2004 and 2003 and provides analyses of results from continuing operations and discontinued operations.

Basis of Analysis

Our results from continuing operations include the performance of acquired businesses from the date of their purchase and exclude results from operations classified as discontinued. Results from operations that qualify as discontinued operations have been reclassified to that category for all periods presented. Please see the section entitled “Discontinued Operations” for a discussion of these operations. In analyzing the results of our operating segments, we measure the performance of existing businesses and the impact of acquired businesses and foreign currency translation. Additionally, our operating segment results represent ongoing businesses, which exclude the results of businesses sold or held for sale that do not qualify as discontinued operations, i.e., disposals. The principal businesses included in disposals were various businesses in our financial market group.

The following table summarizes our consolidated results for the years indicated.

|

| Year ended December 31 |

|

|

| ||||

(millions of U.S. dollars, except per share amounts) |

| 2004 |

| 2003 |

| Change |

| ||

Revenues |

| 8,098 |

| 7,436 |

| 9 | % | ||

Adjusted EBITDA |

| 2,247 |

| 2,040 |

| 10 | % | ||

Adjusted EBITDA margin |

| 27.7 | % | 27.4 | % |

|

| ||

Operating profit |

| 1,341 |

| 1,174 |

| 14 | % | ||

Operating profit margin |

| 16.6 | % | 15.8 | % |

|

| ||

Net earnings |

| 1,011 |

| 865 |

| 17 | % | ||

Earnings attributable to common shares |

| 1,008 |

| 877 |

| 15 | % | ||

Earnings per share attributable to common shares |

| $ | 1.54 |

| $ | 1.34 |

| 15 | % |

See the “Reconciliations” section for a reconciliation of the above non-GAAP financial measures to the most directly comparable Canadian GAAP measures.

REVENUES. The increase in revenues was primarily attributable to contributions from acquisitions and from growth in existing businesses and, to a lesser extent, the impact of favorable foreign currency translation. Excluding the impact of foreign currency translation, revenues grew 7%. Growth from existing businesses was exhibited by all of our market groups. Contributions from acquisitions were primarily from CCBN and TradeWeb in our financial group and BIOSIS in our scientific and healthcare group.

OPERATING PROFIT. Operating profit and related margin growth in 2004 reflected the higher revenues from existing businesses, continued efficiency efforts across the corporation and, to a lesser extent, contributions from acquisitions and the favorable impact of foreign currency translation. Included in the results for 2004 were insurance recoveries related to September 11, 2001 of $19 million and a $7 million benefit from an adjustment to accrued expenses related to health insurance claims for active employees. See “Corporate and Other” for further discussion regarding the insurance claims. Results for 2004 also included a benefit for stock appreciation rights of $6 million compared to an expense in the prior year of $7 million. Operating profit growth in 2004 was tempered by a $27 million increase in pension and other defined benefit plans expense compared to the prior year.

32

ADJUSTED EBITDA AND ADJUSTED OPERATING PROFIT. Adjusted EBITDA and Adjusted operating profit and related margins increased for the same reasons discussed in the “Operating profit” discussion in the immediately preceding paragraph.

DEPRECIATION AND AMORTIZATION. Depreciation in 2004 increased $33 million, or 6%, compared to the prior year. This increase reflected recent acquisitions and capital expenditures. Amortization increased $7 million, or 3%, compared to the prior year, as increases due to the amortization of newly acquired assets were partially offset by decreases arising from the completion of amortization for certain intangible assets acquired in previous years.

NET OTHER INCOME. In 2004, net other income was $24 million, compared to $74 million in 2003. The 2004 amount primarily consisted of a $35 million gain on the sale of an investment, the receipt of the second settlement payment of $22 million from Skillsoft PLC and a $14 million gain on the sale of a wholly-owned subsidiary, whose only asset consisted of tax losses, to a company controlled by Kenneth R. Thomson (discussed under “Related Party Transactions”). These gains were partially offset by a $53 million loss associated with our early redemption of certain debt securities (discussed in the section entitled “Cash Flows”). In 2003, net other income primarily consisted of a gain on the sale of our 20% interest in BGM (discussed in the section entitled “Related Party Transactions”), and the receipt of the first $22 million settlement payment from Skillsoft.

NET INTEREST EXPENSE AND OTHER FINANCING COSTS. Our net interest expense and other financing costs in 2004 decreased 7% compared to 2003. This decrease in net interest expense and other financing costs reflected lower average levels of outstanding net debt and lower interest rates in 2004 compared with 2003. Included in net interest expense and other financing costs in 2004 was a net benefit of $1 million related to new accounting guidance on derivatives. See the section entitled “Accounting Changes” for more information.

INCOME TAXES. Our income tax expense in 2004 represented 23.6% of our earnings from continuing operations before income taxes and our proportionate share of losses on investments accounted for using the equity method of accounting. This compares with an equivalent effective rate of 15.1% in 2003. Included in the 2004 income tax provision was a benefit resulting from the release of a valuation allowance of $41 million related to new legislation in the United Kingdom. In 2003, the income tax provision included a benefit of $64 million principally related to the release of tax contingencies in the United Kingdom associated with a favorable tax settlement.

Our effective income tax rates in 2004 and 2003 were lower than the Canadian corporate income tax rate of 36.0% and 36.6%, respectively, due principally to the lower tax rates and differing tax rules applicable to certain of our operating and financing subsidiaries outside Canada. Specifically, while we generate revenues in numerous jurisdictions, the tax provision on earnings is computed after taking account of intercompany interest and other charges among our subsidiaries resulting from their capital structure and from the various jurisdictions in which operations, technology and content assets are owned. For these reasons, our effective tax rate differs substantially from the Canadian corporate tax rate. In 2005, our businesses expect to continue with initiatives to consolidate the ownership of their technology platforms and content and we expect that a proportion of our profits will continue to be taxed at lower rates than the Canadian statutory tax rate. Therefore, we expect our effective tax rate in 2005 to approximate the 2004 rate of 23.6%. Our effective tax rate and our cash tax cost depend on the laws of numerous countries and the provisions of multiple income tax conventions between various countries in which we operate. Our ability to maintain our effective rate at levels similar to those in 2004 will be dependent upon such laws and conventions remaining unchanged as well as the geographic mix of our profits. We are not aware of any significant changes in existing laws or conventions at this time that would cause our effective tax rate to increase.

33

The balance of our valuation allowance against our deferred tax assets at December 31, 2004 was $408 million compared to $440 million at December 31, 2003. The net movement in the valuation allowance from 2003 to 2004 primarily relates to:

• Reversals related to UK losses and tax credit carryforwards which are now considered more likely than not to be used due to changes in tax laws; lower required allowances against Canadian losses which, while still fully provided against, are first offset by deferred tax liabilities which increased in 2004 from the revaluation of debt and currency swaps; and reversals due to the sale of Canadian net operating losses which previously had full valuation allowances offsetting the related assets (see the section entitled “Related Party Transactions” for further discussion).

• Additions from Canadian losses sustained in 2004; certain tax losses arising on the disposal of businesses; and the impact of currency translation.

We maintain a liability for contingencies associated with known issues under discussion with tax authorities and transactions yet to be settled and we regularly assess the adequacy of this liability. We record liabilities for known tax contingencies when, in the judgment of management, it is probable that a liability has been incurred. We reverse contingencies to income in the period when management assesses that they are no longer required or, when they become no longer required as a result of statute or resolution through the normal tax audit process. Our contingency reserves principally comprise possible issues for the years 2001 to 2004. It is anticipated that these reserves will either result in a cash payment or be reversed to income between 2005 and 2009. In particular, the outcome of audits currently underway may result in the release of a significant part of such reserves in 2005, in which case our 2005 effective tax rate would be less than our 2004 effective tax rate.

In the normal course of business, we enter into numerous intercompany transactions related to the sharing of data and technology. The tax rules governing such transactions are complex and depend on numerous assumptions. At this time, we believe that it is not probable that any such transactions will result in additional tax liabilities, and therefore we have not established contingencies related to these items. However, because of the volume and complexity of such transactions, it is possible that at some future date an additional liability could result from audits by the relevant taxing authorities.

EQUITY IN NET LOSSES OF ASSOCIATES, NET OF TAX. Equity in net losses of associates, net of tax, includes our proportionate share of net losses of investments accounted for using the equity method. In 2004, equity in net losses of associates, net of tax, improved compared to the prior year due to the performance of equity method investees.

EARNINGS ATTRIBUTABLE TO COMMON SHARES AND EARNINGS PER COMMON SHARE. Earnings attributable to common shares were $1,008 million in 2004 compared to $877 million in 2003. Earnings per common share were $1.54 in 2004 compared to $1.34 in 2003. The increases in reported earnings and earnings per common share were largely the result of higher operating profit and gains on the sales of discontinued operations. However, these results are not directly comparable because of certain one-time items, as well as the variability in discontinued operations due to the timing of dispositions.

34

The following table presents a summary of our earnings and our earnings per common share from continuing operations for the periods indicated, after adjusting for items affecting comparability in both years.

|

| Year ended December 31 |

| ||||

(millions of U.S. dollars, except per common share amounts) |

| 2004 |

| 2003 |

| ||

Earnings attributable to common shares |

| 1,008 |

| 877 |

| ||

Adjustments for one-time items: |

|

|

|

|

| ||

Net other income |

| (24 | ) | (74 | ) | ||

Tax on above item |

| 10 |

| 8 |

| ||

Release of tax credits |

| (41 | ) | (64 | ) | ||

Net gain on redemption of Series V preference shares |

| — |

| (21 | ) | ||

Discontinued operations |

| (148 | ) | (32 | ) | ||

Adjusted earnings from continuing operations attributable to common shares |

| 805 |

| 694 |

| ||

Adjusted earnings per common share from continuing operations |

| $ | 1.23 |

| $ | 1.06 |

|

On a comparable basis, our adjusted earnings from continuing operations for 2004 increased, largely as a result of higher operating profit stemming from higher revenues and improved operating efficiencies. These results also reflected benefits from insurance recoveries, stock appreciation rights and an accrual adjustment associated with health insurance claims for active employees, as well as lower net interest expense, offset by higher pension and other benefit plans expense and a higher effective tax rate.

Operating Results by Business Segment

See the “Reconciliations” section for a reconciliation of the non-GAAP financial measures to the most directly comparable Canadian GAAP measures.

Thomson Legal & Regulatory

|

| Year ended December 31 |

|

|

| ||

(millions of U.S. dollars) |

| 2004 |

| 2003 |

| Change |

|

Revenues |

| 3,393 |

| 3,138 |

| 8 | % |

Adjusted EBITDA |

| 1,085 |

| 979 |

| 11 | % |

Adjusted EBITDA margin |

| 32.0 | % | 31.2 | % |

|

|

Adjusted operating profit |

| 882 |

| 797 |

| 11 | % |

Adjusted operating profit margin |

| 26.0 | % | 25.4 | % |

|

|

In 2004, revenues for Thomson Legal & Regulatory increased 8%. Excluding the impact of foreign currency translation, revenues increased 6%. The increase was primarily driven by higher revenues from existing businesses with strong performances by Westlaw, Checkpoint, the International online services, FindLaw and our legal education business. This revenue growth was offset, in part, by continued weakness in the news and business information sector, which experienced a decline in transactional activity. Revenue from print and CD products decreased from that of the prior year as customers continue to migrate towards our online solutions. Growth attributable to newly acquired businesses had a smaller impact in 2004 and was principally attributable to Thomson Elite, which we acquired in May 2003.

35

In 2004, North American Westlaw revenue experienced growth in all of its major market segments: law firm, government, corporate and academic. Outside of North America, Westlaw revenues increased particularly in Europe and the Asia-Pacific region. The North American tax and accounting businesses experienced higher revenues in 2004, led by the Checkpoint online service and higher tax software sales. Revenue from our legal education business also increased in 2004 primarily due to higher enrollments. Finally, FindLaw revenue increased as a result of continued strong new sales performance and the benefit of acquisitions.

The growth in adjusted EBITDA and adjusted operating profit in 2004 resulted from the revenue growth described above. The increase in the corresponding margins was attributable to this revenue growth and the impact of improved operating efficiencies.

Growth in the overall legal information market remains modest but steady. We expect that customer spending on print and CD products will continue to decline, but will be more than offset by growth in spending for online products and integrated information offerings such as Westlaw Litigator. The impact of Sarbanes-Oxley Act requirements has significantly affected the accounting labor market, increasing the demand for compliance information and software and for labor saving and outsourcing solutions. In this environment, we anticipate continued strong demand for our tax and accounting compliance products and outsourcing solutions.

Thomson Learning

|

| Year ended December 31 |

|

|

| ||

(millions of U.S. dollars) |

| 2004 |

| 2003 |

| Change |

|

Revenues |

| 2,174 |

| 2,052 |

| 6 | % |

Adjusted EBITDA |

| 521 |

| 520 |

| 0 | % |

Adjusted EBITDA margin |

| 24.0 | % | 25.3 | % |

|

|

Adjusted operating profit |

| 327 |

| 336 |

| (3 | )% |

Adjusted operating profit margin |

| 15.0 | % | 16.4 | % |

|

|

Revenues for Thomson Learning increased 6% in 2004 compared to the prior year. Excluding the impact of foreign currency translation, revenues increased 4%. This increase was attributable to both acquired businesses and growth from existing businesses.

In the Academic group, revenues increased primarily due to higher sales in our international markets, driven by growth in our English language training business. In higher education, overall textbook sales increased largely as a result of custom product offerings. However, growth in other offerings was tempered and return levels increased, particularly in the United States, as students seek alternate sources for their course materials to address pricing concerns. To minimize the impact of supply from alternate sources, our higher education businesses focused on shifting demand for older editions to customized or specialized products and services only available from the original publisher. Revenues in 2004 from our library reference business increased slightly compared to the prior year as increased sales of electronic products more than offset declines in print offerings. An accelerated migration of collections to electronic products reflected state government budget constraints, which have impacted the funds that libraries have to spend on multiple media formats of reference material.

Lifelong Learning’s revenues increased primarily due to growth in the government and professional testing offerings, sales in the vocational and career markets, and the impact of acquired businesses. Growth was moderated by the expiration in the fourth quarter of 2004 of a significant e-testing government contract in the United Kingdom, for which a subsequent contract was awarded to a business headquartered in the United Kingdom. The competitive environment and ongoing corporate budget constraints in the corporate e-training and information technology markets continued to limit growth for our businesses in these segments in 2004.

36

In 2004, adjusted EBITDA, adjusted operating profit and the related margins were impacted by restructuring costs of $9 million which were recorded in the fourth quarter and were associated with consolidating operations of existing and acquired businesses. Additionally, comparisons with the prior year and the fourth quarter were affected by net credits of $11 million recorded in the fourth quarter of 2003. The net credits of $11 million were comprised of a $27 million benefit largely related to the reversal of incentive accruals, partially offset by $16 million of charges related to severance and lease termination costs. Excluding these items, the adjusted EBITDA and adjusted operating profit margins declined slightly due to additional product and market investments and the impact of acquired businesses that have lower initial margins.

Education has become a lifelong pursuit in a global knowledge-based economy, and we expect to benefit from this growing trend. Technology will continue to transform the learning market and allow us to deliver high-value solutions designed to meet customer needs. For example, we are currently collaborating with professors, students and institutions to design, build and deliver new instructional solutions that leverage our content, media assets, test banks, applications and expertise, which we expect will improve instructors’ productivity and students’ learning efficiency. However, in the short term, we anticipate that tough competition in the corporate training market will depress the prices of our offerings in businesses in that market. Additionally, as electronic offerings continue to grow as a percentage of total revenues, we expect that, over time, the dramatic seasonal swings in our revenues from quarter to quarter will lessen. However, since revenues from electronic offerings are generally recognized in equal installments over a period of time, as opposed to all at once on the sale of a print product, our reported revenue growth may be tempered as this transition occurs.

Thomson Financial

|

| Year ended December 31 |

|

|

| ||

(millions of U.S. dollars) |

| 2004 |

| 2003 |

| Change |

|

Revenues |

| 1,734 |

| 1,510 |

| 15 | % |

Adjusted EBITDA |

| 480 |

| 403 |

| 19 | % |

Adjusted EBITDA margin |

| 27.7 | % | 26.7 | % |

|

|

Adjusted operating profit |

| 298 |

| 228 |

| 31 | % |

Adjusted operating profit margin |

| 17.2 | % | 15.1 | % |

|

|

Revenues for Thomson Financial increased 15% over those of the prior year. Excluding the impact of foreign currency translation, revenues increased 12%. This increase was primarily due to the impact of acquired businesses, including CCBN and TradeWeb, but also reflected growth from existing businesses. Revenues from existing businesses in the United States increased in 2004 as a result of new sales and higher usage and transaction revenues. Thomson ONE workstations increased 56% for the twelve-month period, due to user migration from legacy products and new client wins. In 2004, European revenues from existing businesses declined compared with the prior year due to difficult market conditions. European market conditions began to exhibit certain positive trends in 2004, but continued to lag the improvements being exhibited in the United States. Many of our customers responded to these difficult market conditions by tightening their capital spending and budgets, which in turn led to some product cancellations and pressure on our pricing.

Adjusted EBITDA and adjusted operating profit increased due to the increase in revenues. Included in both adjusted EBITDA and adjusted operating profit were insurance recoveries related to September 11, 2001 of $19 million in 2004 and $4 million in 2003. Excluding the insurance recoveries related to September 11, 2001 in both the current and prior year, the adjusted EBITDA margin in 2004 was consistent with that of the prior year as increases in operating efficiency were offset by acquisition-related expenses and investments for our online news service and a data center, as well as higher data costs. The adjusted operating margin increased as a result of lower depreciation, as a percentage of revenues, due to the timing of capital spending.

37

We anticipate mixed market conditions in 2005, with the North American market expected to achieve the highest growth, Europe to continue lagging behind North America, and Asia to be essentially flat. We expect limited growth in technology investments by our customers and continued pressure on pricing. Revenue growth is anticipated as a result of the full year impact of acquisitions made in 2004 and from existing businesses, especially those associated with transactional activity.

Thomson Scientific & Healthcare

|

| Year ended December 31 |

|

|

| ||

(millions of U.S. dollars) |

| 2004 |

| 2003 |

| Change |

|

Revenues |

| 836 |

| 760 |

| 10 | % |

Adjusted EBITDA |

| 251 |

| 217 |

| 16 | % |

Adjusted EBITDA margin |

| 30.0 | % | 28.6 | % |

|

|

Adjusted operating profit |

| 222 |

| 186 |

| 19 | % |

Adjusted operating profit margin |

| 26.6 | % | 24.5 | % |

|

|

Revenues for Thomson Scientific & Healthcare increased 10% compared to the prior year. Excluding the impact of foreign currency translation, revenues increased 7%. This increase was attributable to higher revenues from existing businesses and contributions from acquired companies, primarily BIOSIS, a provider of databases and services for life sciences research acquired in January 2004. Revenue growth benefited from higher subscription revenues for the ISI Web of Science, Web of Knowledge and the Micromedex electronic product portfolio, as well as increased customer spending for healthcare decision support products. These increases reflect continuing investments by our customers in basic research and drug development and the increasing demand for healthcare point-of-care and management information solutions.

The increases in adjusted EBITDA, adjusted operating profit and the corresponding margins compared to the prior year reflected the higher 2004 revenues and effective integration and cost management efforts.

In November 2004, we completed our acquisition of IHI for $445 million, net of cash and cash equivalents received. IHI provides intellectual property and regulatory information to the scientific, legal, and corporate markets. This acquisition will allow our scientific and healthcare group to offer our pharmaceutical and corporate customers a significantly broader range of intellectual property and drug development workflow solutions.

We believe that demand for scientific information will continue to grow because scientific research and development funding are considered to be necessary, not discretionary, expenditures for our customers. Within the healthcare information market, we see a continuation of the trend toward delivering information to physicians and other healthcare professionals at the point of care.

Corporate and Other

Corporate and other expenses were $98 million in 2004, virtually unchanged from the prior year. Increases in expenses for pensions and other defined benefit plans, as well as other corporate expenses, were offset by an accrual reversal related to insurance claims and a benefit associated with stock appreciation rights. A benefit of $7 million resulted from an adjustment to accrued expenses related to health insurance claims for active employees. Results in 2004 also reflected a benefit associated with stock appreciation rights of $6 million compared to an expense of $7 million in 2003.

38

Discontinued Operations

The following businesses, along with one other small business from Thomson Learning, which was sold in June 2003, are classified as discontinued operations within the consolidated financial statements for all periods presented. None of these businesses was considered fundamental to our integrated information offerings.

In October 2003, we sold our portfolio of healthcare magazines for $135 million and recorded the related post-tax gain of $63 million in the fourth quarter of 2003. The magazines had previously been managed within our scientific and healthcare group.

In February 2004, we sold DBM, a provider of human resource solutions, which had been managed within our learning group. Based on the status of negotiations at December 31, 2003, an impairment charge relating to goodwill of $62 million before income taxes was recorded in the fourth quarter of 2003. We recorded a post-tax gain of $7 million in 2004 related to the completion of the sale.

In the second quarter of 2004, we sold Sheshunoff Information Services Inc., a provider of critical data, compliance and management tools to financial institutions, which had been managed within Thomson Media. Based on estimates of fair value, an impairment charge relating to identifiable intangible assets and goodwill of $24 million before income taxes was recorded in the fourth quarter of 2003 and a charge of $6 million relating to intangible assets was recorded in the first quarter of 2004. We recorded a post-tax gain of $6 million in 2004 related to the completion of the sale.

In November 2004, we sold the Thomson Media group, a provider of largely print-based information products focused on the banking, financial services and related technology markets, for gross proceeds of $350 million. We recorded a post-tax gain on this transaction of $94 million in the fourth quarter of 2004 related to the sale. The results of Thomson Media had previously been reported within our Corporate and other segment.

For more information on these discontinued operations, see Note 6 to our consolidated financial statements.

Return on Invested Capital