UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year endedDecember 31, 2010

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

| | | | | | | | |

Commission File Number | | | | Name of Registrant, State of Incorporation, Address of Principal Executive Offices and Telephone Number | |

| IRS Employer

Identification Number |

|

1-9894 | | | | ALLIANT ENERGY CORPORATION | | | 39-1380265 | |

| | | | (a Wisconsin corporation) | | | | |

| | | | 4902 N. Biltmore Lane | | | | |

| | | | Madison, Wisconsin 53718 | | | | |

| | | | Telephone (608)458-3311 | | | | |

| | | |

0-4117-1 | | | | INTERSTATE POWER AND LIGHT COMPANY | | | 42-0331370 | |

| | | | (an Iowa corporation) | | | | |

| | | | Alliant Energy Tower | | | | |

| | | | Cedar Rapids, Iowa 52401 | | | | |

| | | | Telephone (319)786-4411 | | | | |

| | | |

0-337 | | | | WISCONSIN POWER AND LIGHT COMPANY | | | 39-0714890 | |

| | | | (a Wisconsin corporation) | | | | |

| | | | 4902 N. Biltmore Lane | | | | |

| | | | Madison, Wisconsin 53718 | | | | |

| | | | Telephone (608)458-3311 | | | | |

This combined Form 10-K is separately filed by Alliant Energy Corporation, Interstate Power and Light Company and Wisconsin Power and Light Company. Information contained in the Form 10-K relating to Interstate Power and Light Company and Wisconsin Power and Light Company is filed by such registrant on its own behalf. Each of Interstate Power and Light Company and Wisconsin Power and Light Company makes no representation as to information relating to registrants other than itself.

Securities registered pursuant to Section 12 (b) of the Act:

| | | | |

| | Title of Class | | Name of Each Exchange on Which Registered |

| Alliant Energy Corporation | | Common Stock, $0.01 Par Value | | New York Stock Exchange |

| Alliant Energy Corporation | | Common Share Purchase Rights | | New York Stock Exchange |

| Interstate Power and Light Company | | 8.375% Series B Cumulative Preferred Stock,

$0.01 Par Value | | New York Stock Exchange |

| Interstate Power and Light Company | | 7.10% Series C Cumulative Preferred Stock,

$0.01 Par Value | | New York Stock Exchange |

| Wisconsin Power and Light Company | | 4.50% Preferred Stock, No Par Value | | NYSE Amex LLC |

Securities registered pursuant to Section 12 (g) of the Act: Wisconsin Power and Light Company Preferred Stock

(Accumulation without Par Value)

Indicate by check mark if the registrants are well-known seasoned issuers, as defined in Rule 405 of the Securities Act.

| | | | | | | | | | |

| Alliant Energy Corporation | | Yes [X] | | | | No [ ] | | | | |

| Interstate Power and Light Company | | Yes [ ] | | | | No [X] | | | | |

| Wisconsin Power and Light Company | | Yes [ ] | | | | No [X] | | | | |

Indicate by check mark if the registrants are not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports) and (2) have been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrants were required to submit and post such files).

| | | | | | | | | | | | |

| Alliant Energy Corporation | | | | Yes [X] | | | | No [ ] | | | | |

| Interstate Power and Light Company | | | | Yes [ ] | | | | No [ ] | | | | |

| Wisconsin Power and Light Company | | | | Yes [ ] | | | | No [ ] | | | | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrants’ knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrants are large accelerated filers, accelerated filers, non-accelerated filers, or smaller reporting companies. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| | | | Large AcceleratedFiler | | | | AcceleratedFiler | | | | Non-accelerated Filer | | | | Smaller Reporting CompanyFiler | | | | |

| Alliant Energy Corporation | | | | [X] | | | | | | | | | | | | | | | | |

| Interstate Power and Light Company | | | | | | | | | | | | [X] | | | | | | | | |

| Wisconsin Power and Light Company | | | | | | | | | | | | [X] | | | | | | | | |

Indicate by checkmark whether the registrants are shell companies (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by nonaffiliates as of June 30, 2010:

| | |

| Alliant Energy Corporation | | $3.5 billion |

| Interstate Power and Light Company | | $-- |

| Wisconsin Power and Light Company | | $-- |

Number of shares outstanding of each class of common stock as of Jan. 31, 2011:

| | |

| Alliant Energy Corporation | | Common stock, $0.01 par value, 110,881,189 shares outstanding |

| Interstate Power and Light Company | | Common stock, $2.50 par value, 13,370,788 shares outstanding (all of which

are owned beneficially and of record by Alliant Energy Corporation) |

| Wisconsin Power and Light Company | | Common stock, $5 par value, 13,236,601 shares outstanding (all of which

are owned beneficially and of record by Alliant Energy Corporation) |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statements relating to Alliant Energy Corporation’s and Wisconsin Power and Light Company’s 2011 Annual Meetings of Shareowners are, or will be upon filing with the Securities and Exchange Commission, incorporated by reference into Part III hereof.

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

Statements contained in this Annual Report on Form 10-K that are not of historical fact are forward-looking statements intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can be identified as such because the statements include words such as “expect,” “anticipate,” “plan” or other words of similar import. Similarly, statements that describe future financial performance or plans or strategies are forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, such statements. Some, but not all, of the risks and uncertainties of Alliant Energy Corporation (Alliant Energy), Interstate Power and Light Company (IPL) and Wisconsin Power and Light Company (WPL) include:

| • | | federal and state regulatory or governmental actions, including the impact of energy, tax, financial and health care legislation, and of regulatory agency orders; |

| • | | IPL’s and WPL’s ability to obtain adequate and timely rate relief to allow for, among other things, the recovery of operating costs, fuel costs, transmission costs, deferred expenditures, capital expenditures, and remaining costs related to generating units that may be permanently closed, the earning of reasonable rates of return, and the payments to their parent of expected levels of dividends; |

| • | | the ability to continue cost controls and operational efficiencies; |

| • | | the impact of IPL’s retail electric base rate freeze in Iowa through 2013; |

| • | | the state of the economy in IPL’s and WPL’s service territories and resulting implications on sales, margins and ability to collect unpaid bills; |

| • | | IPL’s potential rate refunds to customers resulting from final rates set by the Minnesota Public Utilities Commission (MPUC) that are less than the interim rate increases IPL is currently collecting from its Minnesota retail customers; |

| • | | developments that adversely impact their ability to implement their strategic plans including unanticipated issues in connection with construction and operation or regulatory approval of a new wind generating facility to utilize the remaining 100 megawatts (MW) of Vestas-American Wind Technology, Inc. (Vestas) wind turbine generator sets, new emission control equipment for various coal-fired generating facilities, WPL’s potential purchases of the Riverside Energy Center (Riverside) and Wisconsin Electric Power Company’s (WEPCO’s) 25% interest in the Edgewater Generating Station Unit 5 (Edgewater Unit 5), and Alliant Energy’s ability to complete the proposed divestiture of its Industrial Energy Applications, Inc. business; |

| • | | weather effects on results of operations; |

| • | | successful resolution of the pending challenge by interveners of the approval by the Public Service Commission of Wisconsin (PSCW) of WPL’s Bent Tree - Phase I wind project; |

| • | | issues related to the availability of generating facilities and the supply and delivery of fuel and purchased electricity and price thereof, including the ability to recover and to retain the recovery of purchased power, fuel and fuel-related costs through rates in a timely manner; |

| • | | the impact that fuel and fuel-related prices may have on IPL’s and WPL’s customers’ demand for utility services; |

| • | | the ability to defend against environmental claims brought by state and federal agencies, such as the United States of America (U.S.) Environmental Protection Agency (EPA), or third parties, such as the Sierra Club; |

| • | | issues associated with environmental remediation efforts and with environmental compliance generally, including changing environmental laws and regulations; |

| • | | potential impacts of changing regulations on the ability to utilize already-purchased emission allowances and forward contracts to purchase additional emission allowances; |

| • | | the ability to recover through rates all environmental compliance costs, including costs for projects put on hold due to uncertainty of future environmental laws and regulations; |

| • | | potential impacts of any future laws or regulations regarding global climate change or carbon emissions reductions, including those that contain proposed regulations (including cap-and-trade) of greenhouse gas (GHG) emissions; |

| • | | continued access to the capital markets on competitive terms and rates; |

1

| • | | inflation and interest rates; |

| • | | financial impacts of risk hedging strategies, including the impact of weather hedges or the absence of weather hedges on earnings; |

| • | | changes to the creditworthiness of counterparties which Alliant Energy, IPL and WPL have contractual arrangements including participants in the energy markets and fuel suppliers and transporters; |

| • | | sales and project execution for RMT, Inc. (RMT), the level of growth in the wind and solar development market and the impact of the American Recovery and Reinvestment Act of 2009 and the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010, and future legislation; |

| • | | issues related to electric transmission, including operating in Regional Transmission Organization (RTO) energy and ancillary services markets, the impacts of potential future billing adjustments and cost allocation changes from RTOs and recovery of costs incurred; |

| • | | unplanned outages, transmission constraints or operational issues impacting fossil or renewable generating facilities and risks related to recovery of resulting incremental costs through rates; |

| • | | Alliant Energy’s ability to successfully pursue appropriate appeals with respect to, and any liabilities arising out of, the alleged violation of the Employee Retirement Income Security Act of 1974 by Alliant Energy’s Cash Balance Pension Plan; |

| • | | Alliant Energy’s ability to successfully resolve with the Internal Revenue Service (IRS) issues related to Alliant Energy’s Cash Balance Pension Plan; |

| • | | current or future litigation, regulatory investigations, proceedings or inquiries; |

| • | | Alliant Energy’s ability to sustain its dividend payout ratio goal; |

| • | | employee workforce factors, including changes in key executives, collective bargaining agreements and negotiations, work stoppages or additional restructurings; |

| • | | impacts that storms or natural disasters in IPL’s and WPL’s service territories may have on their operations and recovery of and rate relief for costs associated with restoration activities; |

| • | | access to technological developments; |

| • | | any material post-closing adjustments related to any past asset divestitures; |

| • | | increased retirement and benefit plan costs; |

| • | | the impact of necessary accruals for the terms of incentive compensation plans; |

| • | | the effect of accounting pronouncements issued periodically by standard-setting bodies; |

| • | | the ability to utilize tax credits and net operating losses generated to date, and those that may be generated in the future, before they expire; |

| • | | the ability to successfully complete tax audits and appeals with no material impact on earnings and cash flows; |

| • | | the direct or indirect effects resulting from terrorist incidents or responses to such incidents; and |

| • | | factors listed in Management’s Discussion and Analysis of Financial Condition and Results of Operations (MDA) and in Item 1A Risk Factors. |

Alliant Energy, IPL and WPL assume no obligation, and disclaim any duty, to update the forward-looking statements in this Annual Report on Form 10-K.

WEBSITE ACCESS TO REPORTS

Alliant Energy makes its periodic and current reports, and amendments to those reports, available, free of charge, on its website atwww.alliantenergy.com/investors on the same day as such material is electronically filed with, or furnished to, the Securities and Exchange Commission (SEC). Alliant Energy is not including the information contained on its website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K.

2

PART I

This Annual Report on Form 10-K includes information relating to Alliant Energy, IPL and WPL (as well as Alliant Energy Resources, LLC (Resources) and Alliant Energy Corporate Services, Inc. (Corporate Services)). Where appropriate, information relating to a specific entity has been segregated and labeled as such. Unless otherwise noted, the information herein has been revised to exclude discontinued operations for all periods presented. Refer to Note 17 of the “Combined Notes to Consolidated Financial Statements” for information on businesses reported as discontinued operations.

ITEM 1. BUSINESS

A. GENERAL

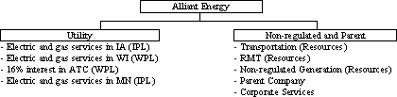

Alliant Energy was incorporated in Wisconsin in 1981 and maintains its principal executive offices in Madison, Wisconsin. Alliant Energy operates as a regulated investor-owned public utility holding company. Alliant Energy’s primary focus is to provide regulated electricity and natural gas service to approximately 1 million electric and approximately 412,000 natural gas customers in the Midwest through its two public utility subsidiaries. The primary first tier subsidiaries of Alliant Energy are: IPL, WPL, Resources and Corporate Services. An illustration of Alliant Energy’s first tier subsidiaries is shown below.

A brief description of the primary first tier subsidiaries of Alliant Energy is as follows:

1) IPL - was incorporated in 1925 in Iowa as Iowa Railway and Light Corporation. IPL is a public utility engaged principally in the generation and distribution of electricity and the distribution and transportation of natural gas in selective markets in Iowa and southern Minnesota. In Iowa, IPL provides utility services to incorporated communities as directed by the Iowa Utilities Board (IUB) and utilizes non-exclusive franchises, which cover the use of public right-of-ways for utility facilities in incorporated communities for a maximum term of 25 years. At Dec. 31, 2010, IPL supplied electric and gas service to 525,657 and 233,792 retail customers, respectively. IPL is also engaged in the generation and distribution of steam for two customers in Cedar Rapids, Iowa. In 2010, 2009 and 2008, IPL had no single customer for which electric, gas, steam and/or other sales accounted for 10% or more of IPL’s consolidated revenues.

2) WPL - was incorporated in 1917 in Wisconsin as Eastern Wisconsin Electric Company. WPL is a public utility engaged principally in the generation and distribution of electricity and the distribution and transportation of natural gas in selective markets in southern and central Wisconsin. WPL operates in municipalities pursuant to permits of indefinite duration and state statutes authorizing utility operation in areas annexed by a municipality. At Dec. 31, 2010, WPL supplied electric and gas service to 454,776 and 178,570 retail customers, respectively. In 2010, 2009 and 2008, WPL had no single customer for which electric, gas and/or other sales accounted for 10% or more of WPL’s consolidated revenues. WPL Transco LLC is a wholly-owned subsidiary of WPL and holds WPL’s investment in the American Transmission Company LLC (ATC).

3) RESOURCES - was incorporated in 1988 in Wisconsin. In 2008, Resources was converted to a limited liability company. Alliant Energy’s non-regulated investments are organized under Resources. Refer to “D. Information Relating to Non-regulated Operations” for additional details.

4) CORPORATE SERVICES - was incorporated in 1997 in Iowa. Corporate Services provides administrative services to Alliant Energy and its subsidiaries.

Refer to Note 14 of the “Combined Notes to Consolidated Financial Statements” for further discussion of business segments, which information is incorporated herein by reference.

3

B. INFORMATION RELATING TO ALLIANT ENERGY ON A CONSOLIDATED BASIS

1) EMPLOYEES -At Dec. 31, 2010, Alliant Energy’s consolidated subsidiaries had the following full- and part-time employees:

| | | | | | | | | | | | | | |

| | | Number of

Bargaining Unit

Employees | | | Number of

Other

Employees | | | Total

Number of

Employees | | | Percentage of Employees

Covered by Collective

Bargaining Agreements |

IPL | | | 1,157 | | | | 257 | | | | 1,414 | | | 82% |

Corporate Services | | | 28 | | | | 1,366 | | | | 1,394 | | | 2% |

WPL | | | 1,150 | | | | 94 | | | | 1,244 | | | 92% |

Resources: | | | | | | | | | | | | | | |

RMT | | | -- | | | | 527 | | | | 527 | | | -- |

Other | | | 87 | | | | 38 | | | | 125 | | | 70% |

| | | | | | | | | | | | | | |

| | | 2,422 | | | | 2,282 | | | | 4,704 | | | 51% |

| | | | | | | | | | | | | | |

At Dec. 31, 2010, Alliant Energy employees covered by collective bargaining agreements were as follows:

| | | | | | | | |

| | | Number of

Employees | | | Contract

Expiration Date | |

IPL: | | | | | | | | |

International Brotherhood of Electrical Workers (IBEW) Local 1439 | | | 17 | | | | 6/30/11 | |

IBEW Local 1455 | | | 5 | | | | 6/30/11 | |

IBEW Local 204 (Emery) | | | 12 | | | | 11/30/11 | |

IBEW Local 949 | | | 231 | | | | 9/30/12 | |

IBEW Local 204 (Dubuque) | | | 99 | | | | 9/30/12 | |

IBEW Local 204 (Mason City) | | | 43 | | | | 9/30/12 | |

IBEW Local 204 (Cedar Rapids) | | | 750 | | | | 8/31/13 | |

| | | | | | | | |

| | | 1,157 | | | | | |

WPL - IBEW Local 965 | | | 1,150 | | | | 5/31/11 | |

Resources - Various | | | 87 | | | | Various | |

Corporate Services - IBEW Local 204 | | | 28 | | | | Negotiating | |

| | | | | | | | |

| | | 2,422 | | | | | |

| | | | | | | | |

2) CAPITAL EXPENDITURE AND INVESTMENT PLANS -Refer to “Liquidity and Capital Resources - Cash Flows - Investing Activities - Construction and Acquisition Expenditures” in MDA for discussion of anticipated construction and acquisition expenditures for 2011, 2012 and 2013.

3) REGULATION -Alliant Energy, IPL and WPL are subject to regulation by various federal, state and local agencies. The following includes the primary regulations impacting Alliant Energy’s, IPL’s and WPL’s businesses.

Federal Energy Regulatory Commission (FERC) - -

Public Utility Holding Company Act of 2005 (PUHCA 2005) - Alliant Energy is registered with FERC as a public utility holding company, pursuant to PUHCA 2005, and is required to maintain certain records and to report certain transactions involving its public utilities and other entities regulated by FERC. IPL and WPL are subject to regulation by FERC under PUHCA 2005 for various issues including, but not limited to, affiliate transactions, public utility mergers, acquisitions and dispositions, issuance of securities (IPL only) and books and records requirements.

Energy Policy Act - The Energy Policy Act requires creation of an Electric Reliability Organization (ERO) to provide oversight by FERC. FERC designated the North American Electric Reliability Corporation (NERC) as the overarching ERO. The Midwest Reliability Organization (MRO), which is a regional member of NERC, has direct responsibility for mandatory electric reliability standards for IPL and WPL.

4

Federal Power Act - FERC also has jurisdiction, under the Federal Power Act, over certain electric utility facilities and operations, electric wholesale and transmission rates, dividend payments and accounting practices of IPL and WPL.

Electric Wholesale Rates - Corporate Services, as agent for both IPL and WPL, has received wholesale electric market-based rate authority from FERC. Market-based rate authorization allows for wholesale sales of electricity within the Midwest Independent Transmission System Operator (MISO) and PJM Interconnection, LLC (PJM) markets and in bilateral markets, based on the market value of the transactions.

Electric Transmission Rates - FERC regulates the rates charged for electric transmission facilities used in interstate commerce. Neither IPL nor WPL own or operate electric transmission facilities; however, both IPL and WPL pay for the use of the interstate electric transmission system based upon FERC-regulated rates. IPL relies primarily upon the use of the ITC Midwest LLC (ITC) transmission system. WPL relies primarily upon the use of the ATC transmission system.

National Gas Act - FERC regulates the transportation and sale for resale of natural gas in interstate commerce under the Natural Gas Act. Under the Natural Gas Act, FERC has authority over certain natural gas facilities and operations of IPL and WPL.

Environmental - The EPA administers certain federal regulatory programs and has delegated the administration of other environmental regulatory programs to the applicable state environmental agencies. In general, the state agencies have jurisdiction over air and water quality, hazardous substances management and transportation, and solid waste management requirements. In certain cases, the state environmental agencies have delegated the administration of environmental programs to local agencies. Alliant Energy, IPL and WPL are subject to these environmental regulations as a result of their current and past operations.

IUB -IPL is subject to regulation by the IUB related to its operations in Iowa for various issues including, but not limited to, retail utility rates and standards of service, accounting requirements and approval of the location and construction of electric generating facilities.

Retail Utility Base Rates -IPL files periodic requests with the IUB for retail rate relief. These filings are based on historical test periods. The historical test periods may be adjusted for certain known and measurable capital additions placed in service by IPL within nine months from the end of the historical test period and certain known and measurable operating and maintenance expenses incurred by IPL within 12 months of the commencement of the proceeding. The IUB must decide on requests for retail rate relief within 10 months of the date of the application for which relief is filed, or the interim rates granted become permanent. Interim retail rates can be placed in effect 10 days after the rate application filing, subject to refund, and must be based on past precedent. Refer to “Rate Matters” in MDA for details of a retail electric base rate freeze effective for IPL’s Iowa customers through 2013.

Retail Commodity Cost Recovery Mechanisms -IPL’s retail electric and natural gas tariffs contain automatic adjustment clauses for changes in prudently incurred commodity costs required to serve its retail customers in Iowa. Any over- or under-collection of commodity costs for each given month are automatically reflected in future billings to retail customers.

Retail Electric Transmission Cost Recovery Mechanism - Effective in the first quarter of 2011, electric transmission service expenses will be removed from base rates and billed to IPL’s Iowa electric retail customers through a transmission cost rider approved by the IUB in January 2011. This new cost recovery mechanism will provide for subsequent adjustments to electric rates charged to Iowa electric retail customers for changes in electric transmission service expenses.

Energy Efficiency Cost Recovery Mechanism - -IPL’s electric and natural gas tariffs contain an energy efficiency cost recovery (EECR) factor to recover prudently incurred energy efficiency costs incurred on behalf of IPL’s Iowa customers. EECR factors are revised annually, subject to approval by the IUB, and include a reconciliation to eliminate any over- or under-recovery of energy efficiency expenses from prior periods.

New Electric Generating Facilities -A Certificate of Public Convenience, Use and Necessity (GCU Certificate) application is required to be filed with the IUB for construction approval of any new electric generating facility located in Iowa with 25 MW or more of capacity.

5

Advance Rate Making Principles -Iowa Code §476.53 provides Iowa utilities with rate making principles prior to making certain generation investments in Iowa. Under Iowa Code §476.53, IPL must file for, and the IUB must provide, rate making principles for electric generating facilities located in Iowa that have received construction approval including new base-load (primarily defined as nuclear or coal-fired generation) facilities with a capacity of 300 MW or more, combined-cycle natural gas-fired facilities of any size and renewable generating resources, such as wind facilities, of any size. Upon approval of rate making principles by the IUB, IPL must either build the facility under the approved rate making principles, or not at all.

PSCW -Alliant Energy is subject to regulation by the PSCW for the type and amount of Alliant Energy’s investments in non-utility businesses and other affiliated interest activities, among other issues. WPL is also subject to regulation by the PSCW related to its operations in Wisconsin for various issues including, but not limited to, retail utility rates and standards of service, accounting requirements, issuance and use of proceeds of securities, approval of the location and construction of electric generating facilities and certain other additions and extensions to facilities.

Retail Utility Base Rates -WPL files periodic requests with the PSCW for retail rate relief. These filings are required to be based on forward-looking test periods. There is no statutory time limit for the PSCW to decide retail rate requests. However, the PSCW attempts to process base retail rate cases in approximately 10 months and has the ability to approve interim retail rate relief, subject to refund, if necessary.

Retail Commodity Cost Recovery Mechanisms -

Electric - WPL’s retail electric base rates include estimates of annual fuel-related costs (fuel and purchased power energy costs) anticipated during the test period. During each electric retail rate proceeding or in a separate fuel cost plan approval proceeding, the PSCW sets fuel monitoring ranges based on the forecasted fuel-related costs used to determine rates in such proceeding. If WPL’s actual fuel-related costs fall outside these fuel monitoring ranges, WPL is authorized to defer the incremental over- or under-collection of fuel-related costs from electric retail customers that are outside the approved ranges. Any over- or under-collection of fuel-related costs for each year are reflected in future billings to retail customers. This cost recovery mechanism became effective for WPL on Jan. 1, 2011.

Natural Gas - WPL’s retail natural gas tariffs contain an automatic adjustment clause for changes in prudently incurred natural gas costs required to serve its retail gas customers. Any over- or under-collection of natural gas costs for each given month are automatically reflected in future billings to retail customers.

Energy Efficiency Cost Recovery Mechanism -WPL contributes a certain percentage of its annual retail utility revenues to help fund Focus on Energy, Wisconsin’s statewide energy efficiency and renewable energy resource program. Contributions to Focus on Energy are recovered from WPL’s retail customers through changes in base rates determined during periodic rate proceedings and include a reconciliation to eliminate any over- or under-recovery of contributions from prior periods.

New Electric Generating Facilities - A Certificate of Authority application is required to be filed with the PSCW for construction approval of any new electric generating facility with a capacity of less than 100 MW. A Certificate of Public Convenience and Necessity application is required to be filed with the PSCW for construction approval of any new electric generating facility with a capacity of 100 MW or more. In addition, WPL’s ownership and operation of electric generating facilities (including those located outside the state of Wisconsin) to serve Wisconsin customers is subject to retail utility rate regulation by the PSCW.

Advance Rate Making Principles - Wisconsin Statutes §196.371 provide Wisconsin utilities with the opportunity to request rate making principles prior to the purchase or construction of any nuclear or fossil-fueled electric generating facility or renewable generating resource, such as a wind facility, utilized to serve Wisconsin customers. WPL is not obligated to file for or accept authorized rate making principles under Wisconsin Statutes §196.371. WPL can proceed with an approved project under traditional rate making terms.

MPUC - IPL is subject to regulation by the MPUC related to its operations in Minnesota for various issues including, but not limited to, retail utility rates and standards of service, accounting requirements, issuance and use of proceeds of securities that encumber property in Minnesota and approval of the location and construction of electric generating facilities located in Minnesota with a capacity in excess of 50 MW.

6

Retail Utility Rates - Requests for retail rate relief can be based on either historical or projected data and interim retail rates are permitted. IPL typically files requests for retail rate relief based on historical test periods. The historical test periods may be adjusted for certain known and measurable capital additions placed in service by IPL and operating and maintenance expenses incurred by IPL within 12 months of the end of the test year. Unless otherwise ordered, the MPUC must reach a final decision within 10 months of filing for retail rate relief; however, the MPUC can extend the timing by 90 days.

Refer to Notes 1(b), 1(h), 2 and 12(e) of the “Combined Notes to Consolidated Financial Statements,” and “Rate Matters,” “Environmental Matters” and “Legislative Matters” in MDA for additional information regarding regulation and utility rate matters.

4) STRATEGIC OVERVIEW - Refer to “Strategic Overview” in MDA for discussion of various strategic actions by Alliant Energy, IPL and WPL.

C. INFORMATION RELATING TO UTILITY OPERATIONS

Alliant Energy’s utility business (IPL and WPL) has three segments: a) electric operations; b) gas operations; and c) other, which includes IPL’s steam operations, various other energy-related products and services, and the unallocated portions of the utility business. In 2010, IPL’s and WPL’s operating revenues and operating income (loss) for these three utility business segments were as follows:

| | | | | | | | |

| | | IPL | | WPL |

| | | Operating

Revenues | | Operating

Income (Loss) | | Operating

Revenues | | Operating

Income (Loss) |

Electric | | 82% | | 92% | | 85% | | 90% |

Gas | | 15% | | 9% | | 14% | | 11% |

Other | | 3% | | (1%) | | 1% | | (1%) |

| | | | | | | | |

| | 100% | | 100% | | 100% | | 100% |

| | | | | | | | |

1) ELECTRIC UTILITY OPERATIONS

General - Electric utility operations represent the largest operating segment for Alliant Energy, IPL and WPL. Alliant Energy’s electric utility operations are located in the Midwest with IPL and WPL providing electric service in Iowa, southern and central Wisconsin and southern Minnesota. Refer to the “Electric Operating Information” tables for additional details regarding electric utility operations.

Jurisdictions - Electric utility revenues by state were as follows (dollars in millions):

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2010 | | | 2009 | | | 2008 | |

| | | Amount | | | Percent | | | Amount | | | Percent | | | Amount | | | Percent | |

IPL: | | | | | | | | | | | | | | | | | | | | | | | | |

Iowa | | | $1,386.0 | | | | 52% | | | | $1,242.3 | | | | 50% | | | | $1,184.3 | | | | 49% | |

Minnesota | | | 78.3 | | | | 3% | | | | 73.3 | | | | 3% | | | | 74.0 | | | | 3% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Subtotal | | | 1,464.3 | | | | 55% | | | | 1,315.6 | | | | 53% | | | | 1,258.3 | | | | 52% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

WPL: | | | | | | | | | | | | | | | | | | | | | | | | |

Wisconsin | | | 1,209.9 | | | | 45% | | | | 1,160.3 | | | | 47% | | | | 1,153.0 | | | | 48% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | $2,674.2 | | | | 100% | | | | $2,475.9 | | | | 100% | | | | $2,411.3 | | | | 100% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

The percentage of electric utility revenues regulated by IPL’s and WPL’s respective state commissions and FERC were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | IPL | | | WPL | |

| | | 2010 | | | 2009 | | | 2008 | | | 2010 | | | 2009 | | | 2008 | |

Respective state commissions | | | 96% | | | | 95% | | | | 96% | | | | 84% | | | | 80% | | | | 84% | |

FERC | | | 4% | | | | 5% | | | | 4% | | | | 16% | | | | 20% | | | | 16% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | 100% | | | | 100% | | | | 100% | | | | 100% | | | | 100% | | | | 100% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

7

Customers - The number of electric customers and communities served at Dec. 31, 2010 was as follows:

| | | | | | | | | | |

| | | Retail Customers | | Wholesale Customers | | Other Customers | | Total Customers | | Communities Served |

IPL | | 525,657 | | 9 | | 1,357 | | 527,023 | | 752 |

WPL | | 454,776 | | 21 | | 2,245 | | 457,042 | | 606 |

| | | | | | | | | | |

| | 980,433 | | 30 | | 3,602 | | 984,065 | | 1,358 |

| | | | | | | | | | |

IPL and WPL provide electric utility service to a diversified base of retail customers in several industries, with the largest concentrations in the food manufacturing, chemical (including ethanol) and paper industries. IPL’s retail customers in the above table are billed under base rates established by the IUB or MPUC that include a return on investments in electric infrastructure and recovery of purchased electric capacity costs and other costs required to serve customers. Base rates charged to IPL’s Minnesota customers also include recovery of electric transmission service costs. Effective in the first quarter of 2011, electric transmission service expenses will be removed from base rates charged to IPL’s Iowa electric retail customers and billed separately through a transmission cost rider. IPL’s electric production fuel and energy purchases costs are recovered pursuant to fuel adjustment clauses. WPL’s retail customers in the above table are billed under base rates established by the PSCW that include a return on investments in electric infrastructure and recovery of electric production fuel and purchased energy costs, purchased electric capacity costs, electric transmission service costs and other costs required to serve customers. Effective in the first quarter of 2011, a new electric fuel cost recovery mechanism was implemented for utilities in Wisconsin that allows WPL to defer electric production fuel and energy purchases costs that exceed or fall below established fuel monitoring ranges.

Wholesale customers in the above table, which primarily consist of municipalities and rural electric cooperatives, are billed under wholesale service agreements. These agreements include standardized pricing mechanisms that are detailed in tariffs approved by FERC through wholesale rate case proceedings. A significant majority of IPL’s and WPL’s wholesale service agreements have terms that end after 2016.

In addition, IPL and WPL have bulk power customers, included in “Other customers” in the above table, that are billed according to negotiated, long-term customer-specific contracts, pursuant to FERC-approved tariffs.

Seasonality -Electric sales are seasonal to some extent with the annual peak normally occurring in the summer months due to air conditioning requirements. In 2010, the maximum peak hour demands were as follows:

| | | | | | |

| | | Alliant Energy | | IPL | | WPL |

MW | | 5,425 | | 2,963 | | 2,654 |

Date | | Aug. 11 | | July 27 | | Aug. 12 |

Competition -Retail electric customers in Iowa, Wisconsin and Minnesota currently do not have the ability to choose their electric supplier. However, IPL and WPL attempt to attract new customers into their service territories in an effort to keep energy rates low for all. Although electric service in Iowa, Wisconsin and Minnesota is regulated, IPL and WPL still face competition from self-generation by large industrial customers, alternative energy sources, and petitions to municipalize (Iowa) as well as service territory expansions by municipal utilities through annexations (Wisconsin). Refer to “Rate Matters - Proposed Changes to Rate Recovery Mechanisms - Economic Development Program” for discussion of the PSCW’s approval of an economic development program to attract and retain industrial customers in WPL’s service territory, which is currently being challenged by the Citizens Utility Board.

Renewable Energy Standards -

Iowa -Electric utilities in Iowa are required to purchase or own their proportionate share of 105 MW of capacity and associated energy from alternate energy or small hydro facilities located in the utilities’ service area. IPL’s proportionate share is approximately 50 MW. As of Dec. 31, 2010, IPL had met the requirements of this renewable energy standard.

Wisconsin -A Wisconsin Renewable Portfolio Standard (RPS) was established in 2006 that requires electric utilities in Wisconsin, including WPL, to increase the portion of their total Wisconsin retail electric sales supplied by renewable energy sources above a benchmark of average retail sales from renewables in 2001, 2002 and 2003. The RPS requires a 2% increase above the benchmark by 2010 and a 6% increase above the benchmark by 2015. Based on this RPS, WPL was required to supply a minimum of 6% of its total Wisconsin retail electric sales with renewable energy sources by 2010 and will be required to increase this amount to 10% by 2015. Wisconsin utilities may reach the RPS with renewable energy

8

generated by the utility, acquired under purchased power agreements (PPAs), or through the use of renewable resource credits. As of Dec. 31, 2010, WPL had met the requirements of this renewable energy standard for 2010.

Minnesota -A Minnesota Renewable Energy Standard (RES) was established in 2007 that requires electric utilities operating in Minnesota, including IPL, to supply a minimum level of their total Minnesota retail electric sales with renewable energy sources by certain future dates. Based on this RES, IPL’s total Minnesota retail electric sales supplied with renewable energy sources must be at least 12% by 2012; 17% by 2016; 20% by 2020; and 25% by 2025. Utilities in Minnesota may meet the requirements of the RES with renewable energy generated by the utility, renewable energy acquired under PPAs or the use of renewable resource credits.

Refer to “Strategic Overview - Generation Plans” in MDA for discussion of Alliant Energy’s generation plan, which includes additional supply from wind generation that contributed towards meeting renewable energy requirements discussed above.

Energy Conservation -IPL and WPL continue to promote energy conservation, including their customers’ ability to efficiently manage their energy use. Refer to “Strategic Overview - Energy Efficiency Programs” in MDA for discussion of current energy efficiency programs at IPL and WPL.

Electric Supply - Alliant Energy, IPL and WPL have met historical customer demand of electricity and expect to continue meeting future demand through internally generated electric supply, electric supply from long-term PPAs and additional electric supply purchases from wholesale energy markets. Alliant Energy’s mix of electric supply experienced changes in recent years with WPL’s purchase of the Neenah Energy Facility in 2009, the completion of IPL’s Whispering Willow - East wind project in late 2009 and the completion of WPL’s Bent Tree - Phase I wind project in early 2011. In addition, IPL retired various generating units in 2010, which are discussed in Note 1(e) of the “Combined Notes to Consolidated Financial Statements.” Alliant Energy expects its mix of electric supply to change further in the next few years with WPL’s anticipated purchases of Riverside and WEPCO’s 25% interest in Edgewater Unit 5 and the anticipated retirement of additional generating units at IPL. Alliant Energy, IPL and WPL periodically update their generation plans to identify longer term generation needs. These long-term generation plans are intended to meet customer demand, reduce reliance on PPAs and mitigate the impacts of future plant retirements while maintaining compliance with long-term electric demand planning reserve margins and renewable energy standards established by regulators. Alliant Energy, IPL and WPL currently expect to meet utility customer demand in the future. However, unanticipated regional or local reliability issues could still arise in the event of unexpected delays in the construction of new generating and/or transmission facilities, retirement of generating facilities, generating facility outages, transmission system outages or extended periods of extreme weather conditions. Refer to the “Electric Operating Information” tables for a profile of the sources of electric supply used to meet customer demand for Alliant Energy, IPL and WPL from 2006 to 2010. Refer to “Strategic Overview - Generation Plans” in MDA for details of Alliant Energy’s future generation plan.

Electric Demand Planning Reserve Margin (PRM) - IPL and WPL are required to maintain a PRM above their projected annual peak demand forecast to help ensure reliability of electric service to their customers. WPL is required to maintain a 14.5% PRM for long-term planning (planning years two through 10) and a PRM established by MISO for short-term planning. PRM requirements for IPL follow MISO’s reserve requirements. IPL and WPL currently have adequate capacity to meet the MISO PRM requirements.

Generation -IPL and WPL own a portfolio of electric generating facilities located in Iowa, Wisconsin and Minnesota with a diversified fuel mix including coal, natural gas and renewable resources. Refer to Item 2 Properties for details of IPL’s and WPL’s electric generating stations.

Generating Capacity - The generating capacity of IPL’s and WPL’s electric generating facilities is based upon MISO’s resource adequacy process, which uses the unforced capacity of the generating facilities. The generating capacity for the June 2010 to May 2011 planning period by fuel type in MWs was as follows:

| | | | | | | | | | | | |

| | | IPL | | | WPL | | | Total | |

Coal | | | 1,542 | | | | 1,231 | | | | 2,773 | |

Natural gas | | | 715 | | | | 582 | | | | 1,297 | |

Oil | | | 261 | | | | -- | | | | 261 | |

Wind (a) | | | -- | | | | 5 | | | | 5 | |

Hydro | | | -- | | | | 17 | | | | 17 | |

| | | | | | | | | | | | |

Total | | | 2,518 | | | | 1,835 | | | | 4,353 | |

| | | | | | | | | | | | |

9

| (a) | Represents 0% and 8% of the capacity of wind projects owned by IPL and WPL, respectively, based upon the MISO resource adequacy process, which is determined separately for each wind site, during the planning period from June 2010 to May 2011. As of Dec. 31, 2010, wind projects owned by Alliant Energy included IPL’s 200 MW Whispering Willow - East wind project in Franklin County, Iowa and WPL’s 68 MW Cedar Ridge wind project in Fond du Lac County, Wisconsin. WPL’s 200 MW Bent Tree - Phase I wind project in Freeborn County, Minnesota was completed in early 2011 and was not included in the June 2010 to May 2011 MISO planning period. |

Fuel Costs - The average cost of delivered fuel per million British Thermal Units used for electric generation was as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | IPL | | | WPL | |

| | | 2010 | | | 2009 | | | 2008 | | | 2010 | | | 2009 | | | 2008 | |

All fuels | | | $2.17 | | | | $2.29 | | | | $2.09 | | | | $2.17 | | | | $2.13 | | | | $2.06 | |

Coal | | | 1.73 | | | | 1.56 | | | | 1.58 | | | | 2.06 | | | | 2.02 | | | | 1.93 | |

Natural gas (a) | | | 9.79 | | | | 13.31 | | | | 8.18 | | | | 12.83 | | | | 18.53 | | | | 8.64 | |

| (a) | The average cost of natural gas is impacted by gains and losses from swap contracts used to hedge the price of natural gas volumes expected to be used by Alliant Energy’s natural gas-fired electric generating facilities. |

Coal - Coal is the primary fuel source for Alliant Energy’s, IPL’s and WPL’s internally generated electric supply and generally represents approximately 50% to 55% of their total sources of electric energy. Alliant Energy, through Corporate Services as agent for IPL and WPL, has entered into contracts with different suppliers to help ensure that a specified supply of coal is available at known prices for IPL’s and WPL’s coal-fired generating facilities for 2011 through 2013. As of Dec. 31, 2010, existing contracts provide for a portfolio of coal supplies that cover approximately 78%, 17%, and 9% of Alliant Energy’s estimated coal supply needs for 2011, 2012 and 2013, respectively. Alliant Energy, IPL and WPL believe this portfolio of coal supplies represents a reasonable balance between the risks of insufficient supplies and those associated with being unable to respond to future coal market changes. Alliant Energy, IPL and WPL expect to meet remaining coal requirements from either future contracts or purchases in the spot market. Alliant Energy, through its subsidiaries Corporate Services, IPL and WPL, also enters into various coal transportation agreements to meet its coal supply requirements. As of Dec. 31, 2010, existing coal transportation agreements cover approximately 70%, 70%, 50% and 50% of Alliant Energy’s estimated coal transportation needs for 2011 through 2014, respectively.

The majority of the coal utilized by IPL and WPL is from the Wyoming Powder River Basin. A majority of this coal is transported by rail-car directly from Wyoming to IPL’s and WPL’s generating stations, with the remainder transported from Wyoming to the Mississippi River by rail-car and then via barges to the final destination. As protection against interruptions in coal deliveries, IPL and WPL strive to maintain average coal inventory supply targets of 25 to 50 days for generating stations with year-round deliveries and 30 to 150 days (depending upon the time of year) for generating stations with seasonal deliveries. Actual inventory averages for 2010 were 50 days for generating stations with year-round deliveries and 138 days for generating stations with seasonal deliveries. The average days on hand were computed based on actual tons of inventory divided by estimated average daily tons burned in 2010. Alliant Energy, IPL and WPL periodically test coal from sources other than the Wyoming Powder River Basin to determine which alternative sources of coal are most compatible with their generating stations. Access to alternative sources of coal is expected to provide Alliant Energy, IPL and WPL with further protection against interruptions and lessen their dependence on their primary coal source.

Average delivered fossil fuel costs are expected to increase in the future due to price structures and adjustment provisions in existing coal contracts, rate structures and adjustment provisions in existing transportation contracts, fuel-related surcharges incorporated by transportation carriers and recent coal and transportation market trends. Existing coal commodity contracts with terms of greater than one year have fixed future year prices that generally reflect recent market trends. A few of Alliant Energy’s existing coal contracts have provisions for price adjustments should specific indices change. Rate adjustment provisions in older transportation contracts are primarily based on changes in the Rail Cost Adjustment Factor as published by the U.S. Surface Transportation Board. Rate adjustment provisions in more recent transportation contracts are based on changes in the All Inclusive Index Less Fuel as published by the Association of American Railroads. These more recent transportation contracts also contain fuel surcharges that are subject to change monthly based on changes in diesel fuel prices. Other factors that may impact coal prices for future commitments are increasing costs for supplier mineral rights, increasing costs to mine the coal and changes in various associated laws and regulations. For example, emission restrictions related to sulfur dioxide (SO2), nitrogen oxide (NOx) and mercury, along with other environmental limitations on generating stations, continue to increase and will likely limit the ability to obtain, and further increase the cost of, adequate coal supplies. Factors that may impact future transportation rates include, but are not limited to: the need for railroads to enhance/expand infrastructure for demand growth, corresponding investments in locomotives and the desire to improve margins on coal movements commensurate with margins on non-coal movements.

10

Given their current coal procurement process, the specific coal market in their primary purchase region and regulatory cost-recovery mechanisms, Alliant Energy, IPL and WPL believe they are reasonably insulated against coal price volatility. Alliant Energy’s coal procurement process stresses periodic purchases, staggering of contract terms, stair-stepped levels of supply going forward for multiple years and supplier diversity. Similarly, given the term lengths of its transportation agreements, Alliant Energy, IPL and WPL believes they are reasonably insulated against future higher coal transportation rates from the major railroads.

Natural Gas - Alliant Energy owns several natural gas-fired generating facilities including IPL’s 565 MW Emery Generating Station, WPL’s 300 MW Neenah Energy Facility and Resources’ 300 MW Sheboygan Falls Energy Facility. WPL has exclusive rights to the output of the Sheboygan Falls Energy Facility under an affiliated lease agreement. These facilities help meet customer demand for electricity generally during peak hour demands. Internally generated electric supply from natural gas-fired generating facilities generally represent less than 5% of Alliant Energy’s, IPL’s and WPL’s total sources of electric energy.

Alliant Energy has responsibility to supply natural gas to the generating facilities it owns as well as Riverside, which WPL has rights to under a PPA. WPL has contracted with ANR Pipeline to provide firm pipeline transportation of 60,000 dekatherms (Dths) per day for Riverside and 2 million Dths of storage capacity for WPL’s natural gas-fired generating facilities.

Nuclear - In 2006, IPL sold its interest in the Duane Arnold Energy Center (DAEC) to a subsidiary of NextEra Energy, Inc. (NextEra) and upon closing of the sale entered into a PPA with NextEra to purchase energy and capacity from DAEC through February 2014. In 2005, WPL sold its interest in the Kewaunee Nuclear Power Plant (Kewaunee) to a subsidiary of Dominion Resources, Inc. (Dominion) and upon closing of the sale entered into a long-term PPA with Dominion to purchase energy and capacity from Kewaunee through December 2013. As a result of these transactions, Alliant Energy, IPL and WPL no longer have ownership interests in any nuclear generating facilities. Alliant Energy, IPL and WPL entered into these transactions to reduce the financial and operational uncertainty associated with nuclear generating facility ownership and operations while still retaining the benefit of the output from such nuclear generating facilities.

Wind - IPL’s 200 MW Whispering Willow - East wind project in Franklin County, Iowa began generating electricity in 2009. WPL’s 68 MW Cedar Ridge wind project in Fond du Lac County, Wisconsin began generating electricity in 2008. WPL’s 200 MW Bent Tree - Phase I wind project in Freeborn County, Minnesota began full generating electricity in early 2011. These wind projects are the first fully owned and operated wind projects for IPL and WPL.

Purchased Power - IPL and WPL enter into PPAs and purchase electricity from wholesale energy markets to meet a portion of their customer demand for electricity. Purchased power represented almost 45% of Alliant Energy’s, IPL’s and WPL’s total sources of electric energy in 2010. IPL’s most significant PPA is with NextEra for the purchase of energy and capacity from DAEC through February 2014. WPL’s most significant PPAs are with Dominion for the purchase of energy and capacity from Kewaunee through December 2013 and with a subsidiary of Calpine Corporation for the purchase of energy and capacity from Riverside through May 2013.

Refer to Note 1(h) for discussion of IPL’s and WPL’s rate recovery of electric production fuel and purchased energy costs, Note 3(a) for details regarding PPAs accounted for as operating leases and Note 12(b) for details on IPL’s and WPL’s coal, natural gas and other purchased power commitments in the “Combined Notes to Consolidated Financial Statements.”

Electric Transmission-

IPL - IPL completed the sale of its electric transmission assets located in Iowa, Minnesota and Illinois to ITC in 2007. IPL sold its electric transmission assets in order to monetize the value of the assets to help fund future capital expenditures, to capture tax benefits under federal tax policy that allowed deferral of gains on sales of qualifying electric transmission assets completed prior to Jan. 1, 2008 (based on regulations at the time of the sale) and to promote regional transmission expansion that is expected to improve transmission reliability and access for its customers in Iowa and Minnesota. ITC is an independent for-profit, transmission-only company and is a transmission-owning member of the MISO RTO, MRO and Reliability First Corporation Regional Entities. ITC has transmission interconnections at various locations with other transmission owning utilities in the Midwest. These interconnections enhance the overall reliability of the IPL delivery system and provide access to multiple sources of economic and emergency energy. IPL currently receives substantially all its transmission services from ITC. The annual transmission service rates that ITC charge its customers is calculated each calendar year using a FERC-approved cost of service formula rate template referred to as Attachment “O.” Refer to “Other Matters - Other Future Considerations - Electric Transmission Service Charges” in MDA for additional information

11

regarding transmission services charges from ITC. Refer to “Rate Matters - Recent Retail Base Rate Filings - IPL’s Iowa Retail Electric Rate Case (2009 Test Year)” for discussion of a new transmission cost rider for recovery of electric transmission service expenses approved by the IUB in January 2011.

WPL - WPL transferred its transmission assets to ATC in 2001 in exchange for an ownership interest in ATC. As of Dec. 31, 2010, WPL held a 16% ownership interest in ATC with a carrying value of $228 million. WPL currently anticipates making capital contributions of $5 million, $5 million and $2 million to ATC in 2011, 2012 and 2013, respectively, to maintain its current ownership percentage. During 2010, ATC distributed to WPL, in the form of dividends, $31 million or approximately 80% of WPL’s equity earnings from ATC. Although no assurance can be given, WPL anticipates ATC will continue this dividend payout ratio in the future. ATC is an independent for-profit, transmission-only company and is a transmission-owning member of the MISO RTO, MRO and Reliability First Corporation Regional Entities. ATC has transmission interconnections with various other transmission owning utilities in the Midwest. These interconnections enhance the overall reliability of the WPL delivery system and provide access to multiple sources of economic and emergency energy. WPL currently receives substantially all its transmission services from ATC. Refer to Note 20 of the “Combined Notes to Consolidated Financial Statements” for details of agreements between ATC and WPL.

MISO Markets - IPL and WPL are members of MISO, a FERC-approved RTO, which is responsible for monitoring and ensuring equal access to the transmission system in their service territories. IPL and WPL participate in the wholesale energy market and ancillary services markets operated by MISO, which are discussed in more detail below. IPL and WPL are parties to a system coordination and operating agreement whereby Corporate Services serves as agent on behalf of IPL and WPL. The agreement, which has been approved by FERC, provides a contractual basis for coordinated planning, construction, operation and maintenance of the interconnected electric generation systems of IPL and WPL. As agent of the agreement, Corporate Services enters into energy, capacity, ancillary services, and transmission service sale and purchase transactions. Corporate Services allocates such sales and purchases among IPL and WPL based on procedures included in the agreement. The procedures were approved by FERC and all state regulatory bodies having jurisdiction. Refer to Note 20 of the “Notes to Consolidated Financial Statements” for additional discussion of these allocated amounts.

Wholesale Energy Market -IPL and WPL began participation in the wholesale energy market operated by MISO in 2005. The market impacts the way IPL and WPL buy and sell wholesale electricity, obtain transmission services, schedule generation and ensure resource adequacy to reliably serve load. In the market, IPL and WPL submit day-ahead and/or real-time bids and offers for energy at locations across the MISO region. MISO evaluates IPL’s, WPL’s and other market participants’ offers, bids and energy injections into, and withdrawals from, the system to economically dispatch the entire MISO system on an hourly basis. MISO settles these hourly offers and bids based on locational marginal prices, which are market-driven values based on the specific time and location of the purchase and/or sale of energy. The market is intended to send price signals to stakeholders where generation or transmission system expansion is needed. This market-based approach is expected to result in lower overall costs in areas with abundant transmission capacity. In addition, MISO may dispatch generators that support reliability needs, but that would not have operated based on economic needs. In these cases, MISO’s settlement assures that these generators are made whole financially for their variable costs. IPL and WPL also periodically engage in related transactions in PJM’s bid/offer-based wholesale energy market, which are accounted for similar to the MISO transactions.

Financial Transmission Rights (FTRs) and Auction Revenue Rights (ARRs) - In areas of constrained transmission capacity, such as Wisconsin, costs could be higher due to congestion and their impact on locational marginal prices. As part of the MISO market restructuring in 2005, physical transmission rights of IPL and WPL were replaced with FTRs. FTRs provide a hedge for congestion costs that occur in the MISO day-ahead energy market. Both IPL and WPL are allocated ARRs from MISO each year based on historical use of the transmission system. The revenue rights associated with these ARRs are used by IPL and WPL to acquire FTRs through the FTR auctions operated by MISO. IPL’s and WPL’s current FTRs acquired from ARRs extend through May 31, 2011. MISO re-allocates ARRs annually based on a fiscal year from June 1 through May 31. Based on the FTRs awarded to IPL and WPL to-date and future expected allocations of ARRs, along with the expected regulatory recovery treatment of MISO costs, the financial impacts associated with FTRs have not differed significantly from the financial impacts associated with physical transmission rights that existed prior to the MISO wholesale energy market.

Ancillary Services Market - In 2009, MISO launched an ancillary services market, which integrates the procurement and use of regulation and contingency reserves with the existing wholesale energy market implemented in 2005. Regulation refers to the moment-to-moment changes in generation that are necessary to meet changes in electricity demand. Contingency reserves refer to additional generation or demand response resources, either on-line or that can be brought on-

12

line within 10 minutes, to meet certain major events such as the loss of a large generating unit or transmission line. MISO plans to address refinements to its ancillary services market in 2011.

MISO and PJM Market Flow Corrections - In 2009, MISO and PJM disclosed an error in the calculation of market flow data between the two independent system operators that began in 2005. The error resulted in incorrect payments between MISO and PJM during 2005 through 2009. Because IPL and WPL participated in both the MISO and PJM markets during the period of the error, IPL and WPL may have been entitled to refunds or may have been required to make additional payments to the two independent system operators. In 2010, MISO and PJM filed complaints against each other with FERC. In January 2011, MISO and PJM filed a settlement, which is pending final FERC approval. Under the proposed settlement, payments would not be exchanged between MISO and PJM. Instead, process changes would be established, including a baseline review of market-to-market processes and accounting, establishment of a change management process regarding the same biennial review of process changes, and enhanced access to pertinent data enabling independent verification of calculations related to settlements. Future market-to-market billing adjustment claims would be limited to one year before the error is discovered compared to the current two-year limitation.

Electric Environmental Matters -Alliant Energy, IPL and WPL are subject to environmental regulations issued by federal, state and local agencies. Such regulations are the result of a number of environmental laws passed by the U.S. Congress, state legislatures and local governments and enforced by federal, state and local regulatory agencies. The laws impacting Alliant Energy’s, IPL’s and WPL’s electric operations include, but are not limited to, the Safe Drinking Water Act; Clean Water Act; Clean Air Act (CAA); National Environmental Policy Act of 1969; Toxic Substances Control Act; Resource Conservation and Recovery Act; Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended by the Superfund Amendments and Reauthorization Act and Emergency Planning and Community Right-to-Know Act of 1986; Endangered Species Act; Occupational Safety and Health Act; National Energy Policy Act, as amended; Federal Insecticide, Fungicide and Rodenticide Act; Hazardous Materials Transportation Act; Pollution Prevention Act; and Department of Homeland Security Appropriations Act. Alliant Energy, IPL and WPL regularly obtain federal, state and local permits to assure compliance with environmental protection laws and regulations. Costs associated with such compliance have increased in recent years and are expected to continue to increase in the future. Alliant Energy, IPL and WPL anticipate these prudently incurred costs for IPL and WPL will be recoverable through future rate case proceedings. Refer to “Environmental Matters” in MDA and Note 12(e) of the “Combined Notes to Consolidated Financial Statements” for further discussion of electric environmental matters including current or proposed environmental regulations under the Clean Air Interstate Rule, Proposed Clean Air Transport Rule, Clean Air Visibility Rule, Utility Maximum Achievable Control Technology (MACT) Rule, Wisconsin State Mercury Rule, Wisconsin Reasonably Available Control Technology Rule, Ozone National Ambient Air Quality Standard (NAAQS) Rule, Fine Particle NAAQS Rule, Nitrogen Dioxide NAAQS Rule, SO2 NAAQS Rule, Industrial Boiler and Process Heater MACT Rule, Emission Standards for Internal Combustion Engines, Federal Clean Water Act including Section 316(b), Wisconsin State Thermal Rule, Hydroelectric Fish Passages and Fish Protective Devices, Coal Combustion Residuals, Polychlorinated Biphenyls and various legislation and EPA regulations to monitor and regulate the emission of GHG including the Mandatory GHG Reporting Rule, New Source Performance Standard for GHG Emissions from Electric Utilities and GHG Tailoring Rule. Refer to “Strategic Overview - Environmental Compliance Plans” in MDA for details of Alliant Energy’s, IPL’s and WPL’s future environmental compliance plans to adhere to environmental regulations.

13

Alliant Energy Corporation

| | | | | | | | | | | | | | | | | | |

| |

| Electric Operating Information | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 |

| |

Operating Revenues (in millions) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | $1,001.5 | | | | $868.6 | | | | $844.7 | | | | $847.5 | | | $857.1 |

Commercial | | | 619.0 | | | | 556.8 | | | | 537.5 | | | | 535.2 | | | 549.8 |

Industrial | | | 762.8 | | | | 710.7 | | | | 734.7 | | | | 731.9 | | | 763.7 |

| | | |

Retail subtotal | | | 2,383.3 | | | | 2,136.1 | | | | 2,116.9 | | | | 2,114.6 | | | 2,170.6 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 196.8 | | | | 190.1 | | | | 201.9 | | | | 179.8 | | | 145.2 |

Bulk power and other | | | 44.1 | | | | 98.3 | | | | 31.1 | | | | 56.7 | | | 68.5 |

Other (includes wheeling) | | | 50.0 | | | | 51.4 | | | | 61.4 | | | | 59.7 | | | 58.7 |

| | | |

Total | | | $2,674.2 | | | | $2,475.9 | | | | $2,411.3 | | | | $2,410.8 | | | $2,443.0 |

| | | |

| | | | |

Electric Sales (000s megawatt-hours (MWh)) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | 7,836 | | | | 7,532 | | | | 7,664 | | | | 7,753 | | | 7,670 |

Commercial | | | 6,219 | | | | 6,108 | | | | 6,181 | | | | 6,222 | | | 6,187 |

Industrial | | | 11,213 | | | | 10,948 | | | | 12,490 | | | | 12,692 | | | 12,808 |

| | | |

Retail subtotal | | | 25,268 | | | | 24,588 | | | | 26,335 | | | | 26,667 | | | 26,665 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 3,325 | | | | 3,251 | | | | 3,813 | | | | 3,547 | | | 3,064 |

Bulk power and other | | | 1,378 | | | | 2,583 | | | | 983 | | | | 2,550 | | | 2,632 |

Other | | | 153 | | | | 155 | | | | 164 | | | | 167 | | | 171 |

| | | |

Total | | | 30,124 | | | | 30,577 | | | | 31,295 | | | | 32,931 | | | 32,532 |

| | | |

| | | | |

Customers (End of Period) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | 841,726 | | | | 840,927 | | | | 840,644 | | | | 840,122 | | | 855,948 |

Commercial | | | 135,832 | | | | 135,099 | | | | 134,536 | | | | 134,235 | | | 135,822 |

Industrial | | | 2,875 | | | | 2,881 | | | | 2,934 | | | | 2,964 | | | 3,064 |

Other | | | 3,632 | | | | 3,555 | | | | 3,534 | | | | 3,529 | | | 3,391 |

| | | |

Total | | | 984,065 | | | | 982,462 | | | | 981,648 | | | | 980,850 | | | 998,225 |

| | | |

| | | | |

Other Selected Electric Data: | | | | | | | | | | | | | | | | | | |

Maximum peak hour demand (MW) | | | 5,425 | | | | 5,491 | | | | 5,491 | | | | 5,751 | | | 5,989 |

Cooling degree days (b): | | | | | | | | | | | | | | | | | | |

Cedar Rapids, Iowa (IPL) (normal - 754) | | | 923 | | | | 406 | | | | 583 | | | | 846 | | | 765 |

Madison, Wisconsin (WPL) (normal - 623) | | | 829 | | | | 368 | | | | 538 | | | | 781 | | | 637 |

Sources of electric energy (000s MWh): | | | | | | | | | | | | | | | | | | |

Coal | | | 16,366 | | | | 15,321 | | | | 17,495 | | | | 18,643 | | | 17,578 |

Purchased power: | | | | | | | | | | | | | | | | | | |

Nuclear | | | 5,667 | | | | 5,428 | | | | 5,465 | | | | 5,103 | | | 5,128 |

Wind | | | 1,254 | | | | 957 | | | | 853 | | | | 872 | | | 840 |

Other | | | 6,260 | | | | 8,585 | | | | 7,013 | | | | 7,426 | | | 8,088 |

Gas | | | 633 | | | | 661 | | | | 1,037 | | | | 1,894 | | | 1,541 |

Wind | | | 588 | | | | 222 | | | | 30 | | | | - | | | - |

Other | | | 232 | | | | 180 | | | | 215 | | | | 309 | | | 527 |

| | | |

Total | | | 31,000 | | | | 31,354 | | | | 32,108 | | | | 34,247 | | | 33,702 |

| | | |

Revenue per kilowatt-hour (KWh) sold to retail customers (cents) | | | 9.43 | | | | 8.69 | | | | 8.04 | | | | 7.93 | | | 8.14 |

| |

| (a) | In February 2007, Alliant Energy sold its electric distribution properties in Illinois. At the date of the sale, Alliant Energy had approximately 22,000 electric retail customers in Illinois. Prior to the asset sales, the electric sales to retail customers in Illinois are included in residential, commercial and industrial sales in the tables above. Following the asset sales, any electric sales associated with these customers are included in wholesale electric sales. |

| (b) | Cooling degree days are calculated using a simple average of the high and low temperatures each day compared to a 65 degree base. Normal degree days are calculated using a rolling 20-year average of historical cooling degree days. |

14

Interstate Power and Light Company

| | | | | | | | | | | | | | | | | | |

| |

| Electric Operating Information | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 |

| |

Operating Revenues (in millions) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | $561.9 | | | | $478.9 | | | | $455.2 | | | | $451.2 | | | $471.2 |

Commercial | | | 378.7 | | | | 336.8 | | | | 319.4 | | | | 316.2 | | | 337.4 |

Industrial | | | 441.9 | | | | 412.5 | | | | 407.0 | | | | 402.0 | | | 440.7 |

| | | |

Retail subtotal | | | 1,382.5 | | | | 1,228.2 | | | | 1,181.6 | | | | 1,169.4 | | | 1,249.3 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 29.8 | | | | 23.5 | | | | 23.4 | | | | 21.3 | | | 1.9 |

Bulk power and other | | | 23.5 | | | | 37.3 | | | | 21.1 | | | | 42.2 | | | 47.8 |

Other (includes wheeling) | | | 28.5 | | | | 26.6 | | | | 32.2 | | | | 37.2 | | | 32.6 |

| | | |

Total | | | $1,464.3 | | | | $1,315.6 | | | | $1,258.3 | | | | $1,270.1 | | | $1,331.6 |

| | | |

| | | | |

Electric Sales (000s MWh) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | 4,295 | | | | 4,113 | | | | 4,218 | | | | 4,204 | | | 4,157 |

Commercial | | | 3,944 | | | | 3,851 | | | | 3,911 | | | | 3,912 | | | 3,910 |

Industrial | | | 6,961 | | | | 6,829 | | | | 7,742 | | | | 7,750 | | | 7,860 |

| | | |

Retail subtotal | | | 15,200 | | | | 14,793 | | | | 15,871 | | | | 15,866 | | | 15,927 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 425 | | | | 403 | | | | 449 | | | | 406 | | | 35 |

Bulk power and other | | | 683 | | | | 901 | | | | 682 | | | | 1,581 | | | 1,550 |

Other | | | 83 | | | | 84 | | | | 90 | | | | 93 | | | 99 |

| | | |

Total | | | 16,391 | | | | 16,181 | | | | 17,092 | | | | 17,946 | | | 17,611 |

| | | |

| | | | |

Customers (End of Period) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | 443,694 | | | | 443,615 | | | | 443,589 | | | | 444,974 | | | 455,346 |

Commercial | | | 80,063 | | | | 79,805 | | | | 79,508 | | | | 79,473 | | | 81,045 |

Industrial | | | 1,900 | | | | 1,914 | | | | 1,939 | | | | 1,954 | | | 2,018 |

Other | | | 1,366 | | | | 1,376 | | | | 1,381 | | | | 1,398 | | | 1,299 |

| | | |

Total | | | 527,023 | | | | 526,710 | | | | 526,417 | | | | 527,799 | | | 539,708 |

| | | |

| | | | |

Other Selected Electric Data: | | | | | | | | | | | | | | | | | | |

Maximum peak hour demand (MW) | | | 2,963 | | | | 2,981 | | | | 2,943 | | | | 3,085 | | | 3,070 |

Cooling degree days (b): | | | | | | | | | | | | | | | | | | |

Cedar Rapids, Iowa (normal - 754) | | | 923 | | | | 406 | | | | 583 | | | | 846 | | | 765 |

Sources of electric energy (000s MWh): | | | | | | | | | | | | | | | | | | |

Coal | | | 8,663 | | | | 8,162 | | | | 9,517 | | | | 10,547 | | | 9,919 |

Purchased power: | | | | | | | | | | | | | | | | | | |

Nuclear | | | 3,623 | | | | 3,577 | | | | 3,619 | | | | 3,066 | | | 3,297 |

Wind | | | 606 | | | | 571 | | | | 616 | | | | 656 | | | 644 |

Other | | | 3,014 | | | | 3,744 | | | | 2,538 | | | | 2,445 | | | 3,099 |

Gas | | | 578 | | | | 636 | | | | 983 | | | | 1,778 | | | 1,426 |

Wind | | | 353 | | | | 42 | | | | - | | | | - | | | - |

Other | | | 22 | | | | 16 | | | | 23 | | | | 127 | | | 344 |

| | | |

Total | | | 16,859 | | | | 16,748 | | | | 17,296 | | | | 18,619 | | | 18,729 |

| | | |

| | | | | |

Revenue per KWh sold to retail customers (cents) | | | 9.10 | | | | 8.30 | | | | 7.45 | | | | 7.37 | | | 7.84 |

| |

| (a) | In February 2007, IPL sold its electric distribution properties in Illinois. At the date of the sale, IPL had approximately 13,000 electric retail customers in Illinois. Prior to the asset sale, the electric sales to retail customers in Illinois are included in residential, commercial and industrial sales in the tables above. Following the asset sale, any electric sales associated with these customers are included in wholesale electric sales. |

| (b) | Cooling degree days are calculated using a simple average of the high and low temperatures each day compared to a 65 degree base. Normal degree days are calculated using a rolling 20-year average of historical cooling degree days. |

15

Wisconsin Power and Light Company

| | | | | | | | | | | | | | | | | | |

| |

| Electric Operating Information | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 |

| |

Operating Revenues (in millions) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | $439.6 | | | | $389.7 | | | | $389.5 | | | | $396.3 | | | $385.9 |

Commercial | | | 240.3 | | | | 220.0 | | | | 218.1 | | | | 219.0 | | | 212.4 |

Industrial | | | 320.9 | | | | 298.2 | | | | 327.7 | | | | 329.9 | | | 323.0 |

| | | |

Retail subtotal | | | 1,000.8 | | | | 907.9 | | | | 935.3 | | | | 945.2 | | | 921.3 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 167.0 | | | | 166.6 | | | | 178.5 | | | | 158.5 | | | 143.3 |

Bulk power and other | | | 20.6 | | | | 61.0 | | | | 10.0 | | | | 14.5 | | | 20.7 |

Other | | | 21.5 | | | | 24.8 | | | | 29.2 | | | | 22.5 | | | 26.1 |

| | | |

Total | | | $1,209.9 | | | | $1,160.3 | | | | $1,153.0 | | | | $1,140.7 | | | $1,111.4 |

| | | |

| | | | | | | | | | | | | | | | | | | |

Electric Sales (000s MWh) (a): | | | | | | | | | | | | | | | | | | |

Residential | | | 3,541 | | | | 3,419 | | | | 3,446 | | | | 3,549 | | | 3,513 |

Commercial | | | 2,275 | | | | 2,257 | | | | 2,270 | | | | 2,310 | | | 2,277 |

Industrial | | | 4,252 | | | | 4,119 | | | | 4,748 | | | | 4,942 | | | 4,948 |

| | | |

Retail subtotal | | | 10,068 | | | | 9,795 | | | | 10,464 | | | | 10,801 | | | 10,738 |

Sales for resale: | | | | | | | | | | | | | | | | | | |

Wholesale | | | 2,900 | | | | 2,848 | | | | 3,364 | | | | 3,141 | | | 3,029 |

Bulk power and other | | | 695 | | | | 1,682 | | | | 301 | | | | 969 | | | 1,082 |

Other | | | 70 | | | | 71 | | | | 74 | | | | 74 | | | 72 |

| | | |

Total | | | 13,733 | | | | 14,396 | | | | 14,203 | | | | 14,985 | | | 14,921 |

| | | |

| | | | |

Customers (End of Period) (a): | | | | | | | | | | | | | | | | | | |