UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 | |

FORM 20-F | |

o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR | |

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2005 OR | |

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR | |

o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT of 1934 Date of event requiring this shell company report ____________________. | |

For the transition period from __________ to __________. | |

Commission File No. 001-14835 | |

ADB SYSTEMS INTERNATIONAL LTD. (Exact name of Registrant as specified in its charter) | |

Not Applicable (Translation of Registrant’s name into English) | |

ONTARIO, CANADA (Jurisdiction of incorporation or organization) | |

302 The East Mall, Suite 300 Toronto, Ontario M9B 6C7 (Address of principal executive offices) | |

Securities registered or to be registered pursuant to Section 12(b) of the Act. None | |

Securities registered or to be registered pursuant to Section 12(g) of the Act. Common Shares | |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None | |

| Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report. | |

74,120,131 Common Shares as of December 31, 2005 | |

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act Yes o No x | |

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934. Yes o No x | |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | |

Yes x No o | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one): Large Accelerated filer o Accelerated filer o Non-accelerated filer x | |

Indicate by check mark which financial statement item the registrant has elected to follow. | |

Item 17 o Item 18x | |

If this an annual report, indicate by check mark whether the registrant is a shell company (as determined in Rule 12b-2 of the Exchange Act). Yes o No x |

ADB SYSTEMS INTERNATIONAL LTD.

Annual Report on Form 20-F for the Fiscal Year

Ended December 31, 2005

FORWARD LOOKING STATEMENTS

From time to time, we make oral and written statements that may be considered "forward looking statements" (rather than historical facts). We are taking advantage of the "safe-harbour" provisions of the Private Securities Litigation Reform Act of 1995 for any forward-looking statements we may make from time to time, including the forward-looking statements in this Annual Report.

You can identify these statements when you see words such as "may", "expect", "anticipate", "estimate", "believe", "intend", and other similar expressions. These forward-looking statements relate, among other items to:

| • | our future capital needs; |

| • | future expectations as to profitability and operating results; |

| • | our ability to further develop business relationships and revenues; |

| • | our expectations about the markets for our products and services; |

| • | acceptance of our products and services; |

| • | competitive factors; |

| • | our ability to repay debt; |

| • | our ability to attract and retain employees; |

| • | new products and technological changes; |

| • | our ability to develop appropriate strategic alliances; |

| • | protection of our proprietary technology; |

| • | our ability to acquire complementary products or businesses and integrate them into our business; and |

| • | geographic expansion of our business. |

We have based these forward-looking statements largely on our current plans and expectations. Forward-looking statements are subject to risks and uncertainties, some of which are beyond our control. Our actual results could differ materially from those described in our forward-looking statements as a result of the factors described in the “Risk Factors” included elsewhere in this Annual Report, including, among others:

| • | the timing of our future capital needs and our ability to raise additional capital when needed; |

| • | our limited operating history in our current business as a combined entity; |

| • | increasingly longer sales cycles; |

| • | increasingly longer collection cycles; |

| • | potential fluctuations in our financial results and our difficulties in forecasting; |

| • | volatility of the stock markets and fluctuations in the market price of our stock; |

| • | your ability to buy and sell our shares on the Over the Counter Bulletin Board; |

2

| • | our ability to compete with other companies in our industry; |

| • | our ability to repay our debt to lenders; |

| • | our ability to retain and attract key personnel; |

| • | risk of significant delays in product development; |

| • | failure to timely develop or license new technologies; |

| • | risks relating to any requirement to correct or delay the release of products due to software bugs or errors; |

| • | risk of system failure or interruption; |

| • | problems which may arise in connection with the acquisition or integration of new businesses, products, services, technologies or other strategic relationships; |

| • | risks associated with international operations; |

| • | risks associated with protecting our intellectual property, and potentially infringing the intellectual property rights of others; and |

| • | sensitivity to the overall economic environment. |

We do not have, and do not undertake, any obligation to publicly update or revise any forward-looking statements contained in this Annual Report, whether as a result of new information, future events or otherwise. Because of these risks and uncertainties, the forward-looking statements and circumstances discussed in this Annual Report might not transpire.

Trademarks or trade names which we own and are used in this Annual Report include: ADB™; PROCUREMATE™; WORKMATE™; BID BUDDY™; SEARCH BUDDY™; DYNAMIC BUYER™ and DYNAMIC SELLER™. Each trademark, trade name, or service mark of any other company appearing in this Annual Report belongs to its holder.

3

TABLE OF CONTENTS

| Page | |||

| PART I | 7 | ||

| ITEM 1 - | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS | 7 | |

| ITEM 2 - | OFFER STATISTICS AND EXPECTED TIMETABLE | 7 | |

| ITEM 3 - | KEY INFORMATION | 7 | |

A. Selected Financial Data | 7 | ||

B. Capitalization and Indebtedness | 9 | ||

C. Reasons For The Offer And Use Of Proceeds | 9 | ||

D. Risk Factors | 9 | ||

| ITEM 4 - | INFORMATION ON THE COMPANY | 16 | |

A. History and Development of the Company | 16 | ||

B. Business Overview | 20 | ||

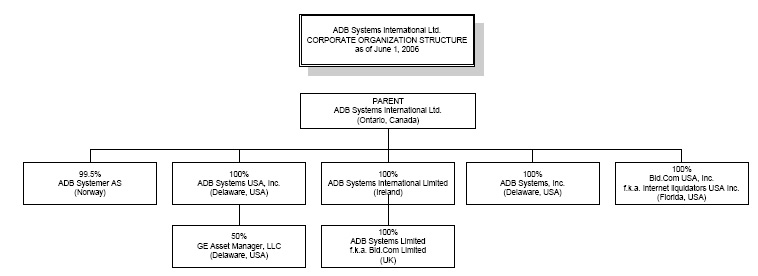

C. Organizational Structure | 29 | ||

D. Property, Plants and Equipment | 29 | ||

| ITEM 4A - | UNRESOLVED STAFF COMMENTS | 29 | |

| ITEM 5 - | OPERATING AND FINANCIAL REVIEW AND PROSPECTS - MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 29 | |

A. Operating Results | 32 | ||

B. Liquidity and Capital Resources | 39 | ||

C. Customer Service and Technology | 41 | ||

D. Trend Information | 41 | ||

E. Off-Balance Sheet Arrangements | 42 | ||

F. Tabular Disclosure of Contractual Obligations | 42 | ||

| ITEM 6 - | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 43 | |

A. Directors And Senior Management | 43 | ||

B. Compensation | 45 | ||

C. Board Practices | 46 | ||

D. Employees | 47 | ||

E. Share Ownership | 48 | ||

| ITEM 7 - | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 49 | |

A. Major Shareholders | 49 | ||

B. Related Party Transactions | 50 | ||

| ITEM 8 - | FINANCIAL INFORMATION | 51 | |

| ITEM 9 - | THE OFFER AND LISTING | 51 |

4

| ITEM 10 - | ADDITIONAL INFORMATION | 54 | |

A. Share Capital | 54 | ||

B. Memorandum and Articles of Association | 54 | ||

C. Material Contracts | 57 | ||

D. Exchange Controls | 59 | ||

E. Taxation | 59 | ||

F. Dividends and Paying Agents | 65 | ||

G. Statements by Experts | 65 | ||

H. Documents on Display | 65 | ||

I. Subsidiary Information | 65 | ||

| ITEM 11 - | QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK | 65 | |

| ITEM 12 - | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 66 | |

| PART II | 66 | ||

| ITEM 13 - | DEFAULT, DIVIDEND ARREARAGES AND DELINQUENCIES | 66 | |

| ITEM 14 - | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 66 | |

| ITEM 15 - | CONTROLS AND PROCEDURES | 66 | |

| ITEM 16 - | [RESERVED] | 66 | |

| ITEM 16 - | 66 | ||

A. Audit Committee Financial Expert | 66 | ||

B. Code of Ethics | 66 | ||

C. Principal Accountant Fees and Services | 66 | ||

D. Exemptions from the Listing Standards For Audit Committees | 67 | ||

E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 67 | ||

| PART III | 67 | ||

| ITEM 17 - | FINANCIAL STATEMENTS | 67 | |

| ITEM 18 - | FINANCIAL STATEMENTS | 67 | |

| ITEM 19 - | EXHIBITS | 67 |

5

Unless otherwise indicated, all references in this Annual Report to “dollars” or “$” are references to Canadian dollars. Our financial statements are expressed in Canadian dollars. Except as otherwise noted, certain financial information presented in this Annual Report has been translated from Canadian dollars to U.S. dollars at an exchange rate of Cdn$1.1656 to US$1.00 (or US$ 0.8579 to Cdn 1.00), the noon buying rate in New York City on December 31, 2005 for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York. These translations are not intended to suggest that Canadian dollars have been or could be converted into U.S. dollars at that or any other rate.

On October 11, 2001, our shareholders approved a two-for-one share consolidation. Unless otherwise indicated, all share and option figures in this Annual Report that relate to the period prior to October 11, 2001 have been adjusted retroactively to reflect the share consolidation.

References to the “Company” and “ADB” refer to ADB Systems International Ltd., as successor to ADB Systems International Inc. as a result of the implementation of the plan of arrangement described on page 17 under the heading “Major Developments.”

PART I

ITEM 1 - IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS

Not applicable.

ITEM 2 - OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3 - KEY INFORMATION

A. | SELECTED FINANCIAL DATA |

The selected financial data set forth below should be read in conjunction with, and is qualified by reference to, our consolidated financial statements and the related notes, and the section "Operating and Financial Review and Prospects" included elsewhere in this Annual Report. The consolidated statement of operations data for the years ended December 31, 2005, 2004, and 2003 and consolidated balance sheet data as of December 31, 2005 and 2004, as set forth below, are derived from our audited consolidated financial statements and the related notes included elsewhere in this Annual Report. The consolidated statement of operations data for the years ended December 31, 2002 and 2001 and the consolidated balance sheet data as at December 31, 2003, 2002, and 2001 have been derived from our audited consolidated financial statements for those years, which are not included in this Annual Report.

We have prepared our consolidated financial statements in accordance with accounting principles generally accepted in Canada, which differ in certain respects from accounting principles generally accepted in the United States. However, as applied to us, for all fiscal periods for which financial data is presented in this Annual Report, Canadian GAAP and U.S. GAAP were substantially identical in all material respects, except as disclosed in Note 23 of our consolidated financial statements.

Historical results are not necessarily indicative of results to be expected for any future period.

6

Statement of Operations Data: | Year Ended December 31 | |||||||||||||||

2005 (Cdn$) | 2004 (Cdn$) | 2003 (Cdn$) | 2002 (Cdn$) | 2001 (Cdn$) | ||||||||||||

(Audited) | ||||||||||||||||

(in thousands except for per share data) | ||||||||||||||||

| Revenue | 5,775 | 4,930 | 5,853 | 5,780 | 4,455 | |||||||||||

| Less: Customer acquisition costs | - | - | - | - | (60 | ) | ||||||||||

| Net Revenue | 5,775 | 4,930 | 5,853 | 5,780 | 4,395 | |||||||||||

| Expenses | ||||||||||||||||

| General and administrative | 4,204 | 4,365 | 4,648 | 6,288 | 7,622 | |||||||||||

| Sales and marketing | 534 | 749 | 1,098 | 1,875 | 4,040 | |||||||||||

| Software development and technology | 3,587 | 3,257 | 2,817 | 4,101 | 3,691 | |||||||||||

| Employee stock options | 154 | 39 | 193 | - | ||||||||||||

| Depreciation and amortization | 132 | 1,190 | 1,901 | 2,602 | 1,572 | |||||||||||

| Interest expense | 707 | 433 | 280 | 155 | (345 | ) | ||||||||||

| Total expenses | 9,318 | 10,033 | 10,937 | 15,021 | 16,580 | |||||||||||

| Loss from operations | 3,543 | (5,103 | ) | (5,084 | ) | (9,241 | ) | (12,185 | ) | |||||||

Loss from continuing operations | ||||||||||||||||

| Net Loss | 3,501 | (5,104 | ) | (2,815 | ) | (9,364 | ) | (18,714 | ) | |||||||

Loss per common share (1) | (0.05 | ) | (0.08 | ) | (0.05 | ) | (0.22 | ) | (0.64 | ) | ||||||

Weighted average number of common shares (2) | 72,904 | 61,938 | 54,324 | 41,968 | 29,130 | |||||||||||

Balance Sheet Data: (3) | ||||||||||||||||

As at December 31 | ||||||||||||||||

2005 (Cdn$) | 2004 (Cdn$) | 2003 (Cdn$) | 2002 (Cdn$) | 2001 (Cdn$) | ||||||||||||

(Audited) | ||||||||||||||||

(in thousands) | ||||||||||||||||

| Working capital | (1,164 | ) | 381 | 486 | (1,757 | ) | 3,115 | |||||||||

| Total assets | 1,843 | 2,493 | 3,211 | 6,355 | 10,592 | |||||||||||

| Shareholders’ (deficiency) equity | (2,710 | ) | (1,009 | ) | 1,026 | 1,198 | 8,014 | |||||||||

| (1) | For each fiscal year, the Company excluded the effect of all convertible debt, stock options and share-purchase warrants, as their impact would have been anti-dilutive. |

| (2) | In October 2001, our shareholders approved a 2 for 1 share consolidation. All per share amounts have been adjusted retroactively to reflect the consolidation. See Note 9(d) of our consolidated financial statements for a discussion regarding the calculation of common shares outstanding and loss per common share. |

| (3) | We have not paid dividends since our formation. |

7

EXCHANGE RATES

The following tables set forth, for the periods indicated, certain exchange rates based on the noon buying rate in New York City for cable transfers in Canadian dollars, as certified for customs purposes by the Federal Reserve Bank of New York. Such rates are the number of U.S. dollars per one Canadian dollar and are the inverse of the rates quoted by the Federal Reserve Board of New York for Canadian Dollars per U.S. $1.00. On May 31, 2006, the exchange rate was US$1.00 = Cdn$0.9069.

| Year Ended December 31, | ||||||||||||||||

| Rate | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||

| Average (1) during year | 0.8254 | 0.7702 | 0.7205 | 0.6344 | 0.6449 | |||||||||||

(1) The average rate is the average of the exchange rates on the last day of each month during the year. |

| Month | High during month | Low during month | |||||

| December 2005 | 0.86900 | 0.8521 | |||||

| January 2006 | 0.8744 | 0.8528 | |||||

| February 2006 | 0.8788 | 0.8634 | |||||

| March 2006 | 0.8834 | 0.8531 | |||||

| April 2006 | 0.8926 | 0.8534 | |||||

| May 2006 | 0.9100 | 0.8903 | |||||

B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

C. | REASONS FOR THE OFFER AND USE OF PROCEEDS. |

Not applicable.

D. | RISK FACTORS |

The following is a summary of certain risks and uncertainties which we face in our business. This summary is not meant to be exhaustive. These Risk Factors should be read in conjunction with other cautionary statements which we make in this Annual Report and in our other public reports, registration statements and public announcements.

WE WILL NEED ADDITIONAL CAPITAL AND IF WE ARE UNABLE TO SECURE ADDITIONAL FINANCING WHEN WE NEED IT, WE MAY BE REQUIRED TO SIGNIFICANTLY CURTAIL OR CEASE OUR OPERATIONS.

We have not yet realized profitable operations and have relied on non-operational sources of financing to fund our operations. Since we began our operations, we have been funded primarily through the sale of securities to investors in a series of private placements, convertible debt instruments, sales of equity to, and investments from, strategic partners, gains from investments, option exercises and, to a limited extent, through cash flow from operations. While our Company’s financial statements for the year-ended December 31, 2005, have been prepared on the basis of accounting principles applicable to a going concern, certain adverse conditions and events cast substantial doubt upon the validity of this assumption. The Company has not yet realized profitable operations and

8

has relied on non-operational sources of financing to fund operations. Our ability to continue as a going concern will be dependent on management’s ability to successfully execute its business plan including a substantial increase in revenue as well as maintaining operating expenses at or near the same level as 2005. Management’s 2006 business plan includes an increase in revenue and operating cash flow primarily from major new contracts in North America. The Company cannot provide assurance that it will be able to execute on its business plan or assure that efforts to raise additional financings would be successful.

Management believes that continued existence beyond 2005 is dependent on its ability to increase revenue from existing products, and to expand the scope of its product offering which entails a combination of internally developed software and partnerships with third parties. As of May 31, 2006, we had cash on hand and marketable securities of approximately $969,000.

We do not have any committed sources of additional financing at this time and we are uncertain whether additional funding will be available when we need it on terms that will be acceptable to us or at all. If we are not able to obtain financing when we need it, we would be unable to carry out our business plan and would have to significantly curtail or cease our operations. We have included in Note 2 to our financial statements for the year ended December 31, 2005, a discussion about the ability of our company to continue as a going concern. Potential sources of financing include strategic relationships, public or private sales of our shares, debt, convertible securities or other arrangements. If we raise funds by selling additional shares, including common shares or other securities convertible into common shares, the ownership interests of our existing shareholders will be diluted. If we raise funds by selling preferred shares, such shares may carry more voting rights, higher dividend payments or more favorable rights upon distribution than those for the common shares. If we incur debt, the holders of such debt may be granted security interests in our assets. Because of our potential long-term capital requirements, we may seek to access the public or private equity or debt markets whenever conditions are favorable, even if we do not have an immediate need for additional capital at that time. The auditors’ report on our 2005 consolidated financial statements includes additional comments for US readers that refers to this uncertainty with respect to our ability to continue as a going concern.

WE ARE NOT PROFITABLE AND WE MAY NEVER BECOME PROFITABLE.

We have accumulated net losses of approximately $108.4 million as of December 31, 2005. For the year ended December 31, 2005 our net loss was $3.5 million. We have never been profitable and expect to continue to incur losses for the foreseeable future. We cannot assure you that we will earn profits or generate positive cash flows from operations in the future.

OUR LIMITED OPERATING HISTORY IN OUR CURRENT BUSINESS AS A COMBINED ENTITY AND OUR JOINT VENTURE WITH GE COMMERCIAL FINANCE MAKES EVALUATING OUR BUSINESS DIFFICULT.

Since we were founded in September 1995 and until 1999 we operated solely as an online retailer of computer and other goods. In 2000, we shifted our focus to providing dynamic pricing solutions. In October 2001, we acquired ADB Systemer ASA of Norway, a provider of enterprise asset management and electronic procurement software and services.

In December 2003 we formed the joint venture, GE Asset Manager LLC, with GE Commercial Finance, Capital Solutions. Growing this business venture has required us to shift focus from a broad spectrum of customers to focusing on a small number of large clients. By further investing in our relationship with GE Commercial Finance, Capital Solutions we are increasing our business risk by becoming substantially dependent on the business generated by the joint venture.

Our business and prospects must be considered in light of the risks, uncertainties and expenses frequently encountered by companies in their early stages of development, particularly companies in new and rapidly evolving markets. Our business strategy may not be successful and we may not successfully address those risks.

9

WE MAY EXPERIENCE INCREASINGLY LONGER SALES CYCLES.

A significant portion of our revenue in any quarter is derived from a relatively small number of contracts. We often experience sales cycles of six (6) to eighteen (18) months. If the length of our sales cycles increases, our revenues may decrease and our quarterly results would be adversely affected. In addition, our current and future expense levels are based largely on our investment plans and estimates of future revenues and are, to a large extent, fixed. We may be unable to adjust spending in a timely manner to compensate for any unexpected revenue shortfall. Any significant shortfall in revenues relative to our planned expenditures would have a material adverse effect on our business, financial condition, cash flows and results of operations.

POTENTIAL FLUCTUATIONS IN OUR FINANCIAL RESULTS MAKE FINANCIAL FORECASTING DIFFICULT.

Our operating results have varied on a quarterly basis in the past and may fluctuate significantly as a result of a variety of factors, many of which are outside our control. Factors that may affect our quarterly operating results include:

| • | general economic conditions as well as economic conditions specific to our industry; |

| • | long sales cycles, which characterize our industry; |

| • | implementation delays, which can affect payment and recognition of revenue; |

| • | any decision by us to reduce prices for our solutions in response to price reductions by competitors; |

| • | the amount and timing of operating costs and capital expenditures relating to monitoring or expanding our business, operations and infrastructure; and |

| • | the timing of, and our ability to integrate, any future acquisition, technologies or products or any strategic investments or relationships into which we may enter. |

Due to these factors, our quarterly revenues and operating results are difficult to forecast. We believe that period-to-period comparisons of our operating results may not be meaningful and should not be relied upon as an indication of future performance. In addition, it is likely that in one or more future quarters, our operating results will fall below the expectations of securities analysts and investors. In such event, the trading price of our common shares would almost certainly be materially adversely affected.

OUR SHARE PRICE HAS FLUCTUATED SUBSTANTIALLY AND MAY CONTINUE TO DO SO.

The trading price of our common shares on The Toronto Stock Exchange and on the Nasdaq Over the Counter Bulletin Board (“OTCBB”) has fluctuated significantly in the past and could be subject to wide fluctuations in the future. The market prices for securities of technology companies have been highly volatile. These companies have experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to their operating performance. Broad market and industry factors may materially and adversely affect the market price of our common shares, regardless of our operating performance. In addition, fluctuations in our operating results and concerns regarding our competitive position can have an adverse and unpredictable effect on the market price of our shares.

In the past, following periods of volatility in the market price of a company’s securities, securities class-action litigation has often been instituted against that company. Such litigation, if instituted against us, could result in substantial costs and a diversion of management’s attention and resources, which could have a material adverse effect on our business, results of operations, cash flow, financial condition and prospects.

YOUR ABILITY TO BUY OR SELL OUR COMMON SHARES ON THE OTCBB MAY BE LIMITED.

On June 3, 2002, we transferred the listing of our common shares from the Nasdaq National Market to the Nasdaq SmallCap Market (now known as the Nasdaq Capital Market). On August 22, 2002, our common shares were delisted from the Nasdaq SmallCap Market because we did not satisfy the minimum bid price per share requirement for continued listing on that market. Our common shares immediately became eligible for and began trading on the OTCBB. The OTCBB is generally considered to be a less efficient market than the Nasdaq

10

National Market or the Nasdaq SmallCap Market on which our shares previously traded. As a result, your ability to buy or sell our common shares on the OTCBB may be limited. In addition, since our shares are no longer listed on the Nasdaq National Market or Nasdaq SmallCap Market, our shares may be subject to the “penny stock” regulations described below. De-listing from the Nasdaq National Market and the Nasdaq SmallCap Market will not affect the listing of the common shares on The Toronto Stock Exchange.

OUR COMMON SHARES ARE SUBJECT TO “PENNY STOCK” REGULATIONS WHICH MAY AFFECT YOUR ABILITY TO BUY OR SELL OUR COMMON SHARES.

Our common shares have traded on the Nasdaq National and Small Cap Markets and on the OTCBB at prices below US$5.00 since April 2000 (on a pre-consolidation basis). As a result, our shares are characterized as “penny stocks” which may severely affect market liquidity. The Securities Enforcement and Penny Stock Reform Act of 1990 requires additional disclosure relating to the market for penny stocks in connection with trades in any stock defined as a penny stock.

Securities and Exchange Commission regulations generally define a penny stock to be an equity security that has a market price of less than US$5.00 per share, subject to certain exceptions. The regulations require, prior to any transaction involving a penny stock, delivery of a disclosure schedule explaining the penny stock market and the risks associated therewith. The penny stock regulations may adversely affect the market liquidity of our common shares by limiting the ability of broker/dealers to trade the shares and the ability of purchasers of our common shares to sell in the secondary market. Certain institutions and investors will not invest in penny stocks.

THE MARKETS IN WHICH WE OPERATE ARE HIGHLY COMPETITIVE.

The market for asset lifecycle management solutions is rapidly evolving and intensely competitive. We face significant competition in each segment of our business (sourcing, procurement, enterprise asset management and asset disposition). We expect that competition will further intensify as new companies enter the different segments of our market and larger existing companies expand their product lines. If the global economy continues to lag, we could face increased competition, particularly in the form of lower prices.

Many of our competitors have longer operating histories, larger customer bases, greater brand recognition and significantly greater financial, marketing and other resources than we. We cannot assure you that we will be able to compete with them effectively. If we fail to do so, it would have a material adverse effect on our business, financial condition, cash flows and results of operations.

WE MAY NOT BE ABLE TO RETAIN OR ATTRACT THE HIGHLY SKILLED PERSONNEL WE NEED, IN PARTICULAR AS A RESULT OF OUR RECENT WORKFORCE REDUCTIONS.

Our success is substantially dependent on the ability and experience of our senior management and other key personnel. We do not have long-term employment agreements with any of our key personnel and maintain no “key person” life insurance policies.

The number of our employees as of May 31, 2006 represents a 6% decrease in our workforce as compared with the number of our employees as of May 31, 2005. We may need to hire new or additional personnel to respond to attrition or future growth of our business. However, there is significant competition for qualified personnel. We cannot be certain we will be able to retain existing personnel or hire additional, qualified personnel when needed.

SIGNIFICANT DELAYS IN PRODUCT DEVELOPMENT WOULD HARM OUR REPUTATION AND RESULT IN LOSS OF REVENUE.

If we experience significant product development delays, our position in the market would be harmed, and our revenues could be substantially reduced, which would adversely affect our operating results. As a result of the complexities inherent in our software, major new product enhancements and new products often require long development and test periods before they are released. On occasion, we have experienced delays in the scheduled release date of new or enhanced products, and we may experience delays in the future. Delays may occur for many reasons, including an inability to hire a sufficient number of developers, discovery of bugs and errors or a failure of our current or future products to conform to industry requirements. Any such delay, or the failure of new products

11

or enhancements in achieving market acceptance, could materially impact our business and reputation and result in a decrease in our revenues.

WE MAY HAVE TO EXPEND SIGNIFICANT RESOURCES TO KEEP PACE WITH RAPID TECHNOLOGICAL CHANGE.

Our industry is characterized by rapid technological change, changes in user and customer requirements, frequent new service or product introductions embodying new technologies and the emergence of new industry standards and practices. Any of these could hamper our ability to compete or render our proprietary technology obsolete. Our future success will depend, in part, on our ability to:

| • | develop new proprietary technology that addresses the increasingly sophisticated and varied needs of our existing and prospective customers; |

| • | anticipate and respond to technological advances and emerging industry standards and practices on a timely and cost-effective basis; |

| • | continually improve the performance, features and reliability of our products in response to evolving market demands; and |

| • | license leading technologies. |

We may be required to make substantial expenditures to accomplish the foregoing or to modify or adapt our services or infrastructure.

OUR BUSINESS COULD BE SUBSTANTIALLY HARMED IF WE HAVE TO CORRECT OR DELAY THE RELEASE OF PRODUCTS DUE TO SOFTWARE BUGS OR ERRORS.

We sell complex software products. Our software products may contain undetected errors or bugs when first introduced or as new versions are released. Our software products may also contain undetected viruses. Further, software we license from third parties and incorporate into our products may contain errors, bugs or viruses. Errors, bugs and viruses may result in any of the following:

| • | adverse customer reactions; |

| • | negative publicity regarding our business and our products; |

| • | harm to our reputation; |

| • | loss of or delay in market acceptance; |

| • | loss of revenue or required product changes; |

| • | diversion of development resources and increased development expenses; |

| • | increased service and warranty costs; |

| • | legal action by our customers; and |

| • | increased insurance costs. |

SYSTEMS DEFECTS, FAILURES OR BREACHES OF SECURITY COULD CAUSE A SIGNIFICANT DISRUPTION TO OUR BUSINESS, DAMAGE OUR REPUTATION AND EXPOSE US TO LIABILITY.

We host certain websites and sub-sites for our customers. Our systems are vulnerable to a number of factors that may cause interruptions in our ability to enable or host solutions for third parties, including, among others:

| • | damage from human error, tampering and vandalism; |

| • | breaches of security; |

12

| • | fire and power losses; |

| • | telecommunications failures and capacity limitations; and |

| • | software or hardware defects. |

Despite the precautions we have taken and plan to take, the occurrence of any of these events or other unanticipated problems could result in service interruptions, which could damage our reputation, and subject us to loss of business and significant repair costs. Certain of our contracts require that we pay penalties or permit a customer to terminate the contract if we are unable to maintain minimum performance levels. Although we continue to take steps to enhance the security of our systems and ensure that appropriate back-up systems are in place, our systems are not now, nor will they ever be, fully secure.

OUR BUSINESS HAS UNDERGONE DRAMATIC EXPANSION AND RETRACTION PHASES SINCE OUR FORMATION. WE MAY NOT BE ABLE TO MANAGE FURTHER DRAMATIC EXPANSIONS AND RETRACTIONS IN THE FUTURE.

Our business has undergone dramatic expansion and retraction since our formation, which has placed significant strain on our management resources. If we should grow or retract dramatically in the future, there may be further significant demands on our management, administrative, operating and financial resources. In order to manage these demands effectively, we will need to expand and improve our operational, financial and management information systems and motivate, manage and retain employees. We cannot assure you that we will be able to do so, that our management, personnel or systems will be adequate, or that we will be able to achieve levels of revenue commensurate with the resulting levels of operating expenses.

INTERNATIONAL SALES ACCOUNT FOR A SIGNIFICANT PORTION OF OUR REVENUE, WHICH EXPOSES US TO CERTAIN RISKS.

We currently operate in Canada, Norway, Ireland, the United States and England. In the 2005 fiscal year, sales to customers outside North America represented approximately 88.6% of our revenues. There are risks inherent in doing business on a global level, including:

| • | difficulties in managing and staffing an organization spread across several continents; |

| • | differing laws and regulatory requirements; |

| • | political and economic risks; |

| • | currency and foreign exchange fluctuations and controls; |

| • | tariffs, customs, duties and other trade barriers; |

| • | longer payment cycles and problems in collecting accounts receivable in certain countries; |

| • | export and import restrictions; |

| • | the need for product compliance with local language and business customs; |

| • | seasonal reductions in business activity during the summer months in Europe and elsewhere; and |

| • | potentially adverse tax consequences. |

| Any of these risks could adversely affect the success of our global operations. |

ACQUISITIONS OF COMPANIES OR TECHNOLOGIES MAY RESULT IN DISRUPTIONS TO OUR BUSINESS AND/OR DISTRACTIONS FOR OUR MANAGEMENT.

We acquired ADB Systemer ASA (“ADB Systemer”) of Norway in October 2001. On May 18, 2006, the Company entered into an agreement with ADB Systemer Holding AS to sell 100 percent of its shares in ADB Systemer. For additional information regarding the sale of ADB Systemer see Item 4. B under the heading “BUSINESS OVERVIEW.”

13

In the future, we may seek to acquire other businesses or make investments in complementary businesses or technologies. We may not be able to acquire or manage additional businesses profitably or successfully integrate any acquired businesses with our business. Businesses that we acquire may have liabilities that we underestimate or do not discover during our pre-acquisition investigations. Certain liabilities, even if we do not expressly assume them, may be imposed on us as the successor to the business. Further, each acquisition may involve other special risks that could cause the acquired businesses to fail to meet our expectations. For example:

| • | the acquired businesses may not achieve expected results; |

| • | we may not be able to retain key personnel of the acquired businesses; |

| • | we may incur substantial, unanticipated costs, delays or other operational or financial problems when we try to integrate businesses we acquire with our own; |

| • | our management’s attention may be diverted; or |

| • | our management may not be able to manage the combined entity effectively or to make acquisitions and grow our business internally at the same time. |

The occurrence of one or more of these factors could have a material adverse effect on our business, financial condition, cash flows and results of operations. In addition, we may incur debt or issue equity securities to pay for any future acquisitions or investments, which could dilute the ownership interest of our existing shareholders.

IF WE ARE UNABLE TO SUCCESSFULLY PROTECT OUR INTELLECTUAL PROPERTY OR OBTAIN CERTAIN LICENSES, OUR COMPETITIVE POSITION MAY BE WEAKENED.

Our performance and ability to compete are dependent in part on our technology. We rely on a combination of patent, copyright, trademark and trade secret laws as well as confidentiality agreements and technical measures, to establish and protect our rights in the technology we develop. We cannot guarantee that any patents issued to us will afford meaningful protection for our technology. Competitors may develop similar technologies which do not conflict with our patents. Others may challenge our patents and, as a result, our patents could be narrowed or invalidated.

Our software is protected by common law copyright laws, as opposed to registration under copyright statutes. Common law protection may be narrower than that which we could obtain under registered copyrights. As a result, we may experience difficulty in enforcing our copyrights against certain third parties. The source code for our proprietary software is protected as a trade secret. As part of our confidentiality protection procedures, we generally enter into agreements with our employees and consultants and limit access to, and distribution of, our software, documentation and other proprietary information. We cannot assure you that the steps we take will prevent misappropriation of our technology or that agreements entered into for that purpose will be enforceable. In order to protect our intellectual property, it may be necessary for us to sue one or more third parties. While this has not been necessary to date, there can be no guarantee that we will not be required to do so in future to protect our rights. The laws of other countries may afford us little or no protection for our intellectual property.

We also rely on a variety of technology that we license from third parties, including our database and Internet server software, which is used to perform key functions. These third-party technology licenses may not continue to be available to us on commercially reasonable terms, or at all. If we are unable to maintain these licenses or obtain upgrades to these licenses, we could be delayed in completing or prevented from offering some products or services.

OTHERS COULD CLAIM THAT WE INFRINGE ON THEIR INTELLECTUAL PROPERTY RIGHTS, WHICH MAY RESULT IN COSTLY AND TIME-CONSUMING LITIGATION.

Our success will also depend partly on our ability to operate without infringing upon the proprietary rights of others, as well as our ability to prevent others from infringing on our proprietary rights. We may be required at times to take legal action in order to protect our proprietary rights. Also, from time to time, we may receive notice from third parties claiming that we infringe their patent or other proprietary rights. In the past, a certain third party claimed that certain of our technology infringed their intellectual property rights. The Company does not believe it

14

does or ever has infringed the intellectual property rights of any third party. The claim with the particular third party has been resolved through a licensing arrangement. There can be no assurances that other third parties will not make similar claims in the future.

We believe that infringement claims will increase in the technology sector as competition intensifies. Despite our best efforts, we may be sued for infringing on the patent or other proprietary rights of others. Such litigation is costly, and even if we prevail, the cost of such litigation could harm us. If we do not prevail or cannot fund a complete defense, in addition to any damages we might have to pay, we could be required to stop the infringing activity or obtain a license. We cannot be certain that any required license would be available to us on acceptable terms, or at all. If we fail to obtain a license, or if the terms of a license are burdensome to us, this could have a material adverse effect on our business, financial condition, cash flows and results of operations.

OUR BUSINESS IS SENSITIVE TO THE OVERALL ECONOMIC ENVIRONMENT. ANY SLOWDOWN IN INFORMATION TECHNOLOGY SPENDING BUDGETS COULD HARM OUR OPERATING RESULTS.

Any significant downturn in our customers' markets or in general economic conditions that results in reduced information technology spending budgets would likely result in a decreased demand for our products and services, longer selling cycles and lower prices, any of which may harm our business.

WE ARE SUBJECT TO RISKS ASSOCIATED WITH EXCHANGE RATE FLUCTUATIONS.

Substantially all of our revenues are in European currencies or U.S. dollars, while the majority of our operating expenses are in Canadian dollars and Norwegian kroner. We do not have any hedging programs in place to manage the potential exposure to fluctuations in the Canadian dollar and Norwegian kroner exchange rates. Fluctuations in the exchange rates of these currencies or the exchange rate of other currencies against the Canadian dollar or Norwegian kroner could have a material adverse effect on our business, financial condition, cash flows and results of operations.

OUR PREFERRED SHARES COULD PREVENT OR DELAY A TAKEOVER THAT SOME OR A MAJORITY OF SHAREHOLDERS CONSIDER FAVORABLE.

Our Board of Directors, without any further vote of our shareholders, may issue preference shares and determine the price, preferences, rights and restrictions of those shares. The rights of the holders of common shares will be subject to, and may be adversely affected by, the rights of the holders of any series of preference shares that may be issued in the future. That means, for example, that we can issue preference shares with more voting rights, higher dividend payments or more favorable rights upon distribution than those for our common shares. If we issue certain types of preference shares in the future, it may also be more difficult for a third party to acquire a majority of our outstanding voting shares and such issuance may, in certain circumstances, deter or delay mergers, tender offers or other possible transactions that may be favored by some or a majority of our shareholders.

IT MAY BE DIFFICULT FOR YOU TO ENFORCE LEGAL CLAIMS AGAINST US OR OUR OFFICERS OR DIRECTORS.

We are incorporated under the laws of the Province of Ontario, Canada. Certain of our directors and officers are residents of Canada and Norway and substantially all of our assets and the assets of such persons are located outside the United States. As a result, it may be difficult for holders of common shares to effect service of legal process within the United States upon those directors and officers who are not residents of the United States. It may also be difficult to realize in the United States upon judgments of courts of the United States without enforcing such judgments in our home jurisdiction or the jurisdiction of residence of the director or officer concerned.

ITEM 4 - INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

The name of the company is ADB Systems International Ltd (“ADB,” “ADB Systems” or the “Company”). The Company was formed pursuant to the Business Corporations Act (Ontario). The business began as Internet

15

Liquidators Inc. (“IL Inc.”), a business corporation formed under the laws of Ontario, Canada, in September 1995 and after a series of corporate reorganizations, as described below, developed into the present Company. In May 1996, Internet Liquidators International Inc. (“ILI Inc.”), also an Ontario company, acquired all of the shares of IL Inc. These two companies were amalgamated on January 9, 1997. By articles of amendment dated June 25 1998, ILI Inc. changed its name to Bid.Com International Inc.

Prior to October 24, 2000, we operated two national business-to-consumer auction sites at www.bid.com, one in the United States and one in Canada. Following an extensive strategic review by ADB’s Board of Directors and management, ADB decided late in 2000 to focus on its software business.

On October 11, 2001, Bid.Com acquired substantially all of the shares of ADB Systemer ASA, a public limited liability company organized under the laws of the Kingdom of Norway. As part of the acquisition of ADB Systemer, Bid.Com completed a two for one share consolidation and changed its name to ADB Systems International Inc. (“ADB Inc.”) by articles of amendment dated October 11, 2001.

During 2002, ADB Systems International Inc. (“ADB Inc.”), entered into a series of agreements with the Brick Warehouse Corporation (“The Brick”), which are described below under the heading “The Brick Transaction” and subsequently ADB Inc. changed its name to Bid.com International Ltd.

On August 20, 2002, ADB Systems International Ltd., was incorporated by certificate and Articles of Incorporation. On October 31, 2002, the shareholders of ADB Inc. exchanged their shares of ADB Inc. for shares of the Company on a one-for-one basis. This exchange was implemented pursuant to a plan of arrangement approved by the shareholders of ADB Inc. on October 22, 2002 and by the Ontario Superior Court of Justice on October 24, 2002 (which we refer to in this form as the “Arrangement”). As a result of the Arrangement, the business of ADB Inc., including all assets and liabilities of ADB Inc. (other than those related to retail activities), was transferred to the Company in the form of a return of capital. ADB Inc. subsequently changed its name to Bid.Com International Ltd.

The principal place of business and registered office of the Company is located at 302 The East Mall, Suite 300 Toronto, Ontario, Canada, M9B 6C7 and our telephone number is (416) 640-0400. In Norway, our principal business offices are located at Vingveien 2, 4050 Sola, Norway and our telephone number is +47 51 64 71 00.

Our shares trade on the Toronto Stock Exchange under the symbol “ADY” and are traded on the OTCBB under the symbol “ADBYF”. Additional information about the Company can be obtained at our web site - www.adbsys.com. The information contained on our web site is not deemed to be part of this Annual Report.

MAJOR DEVELOPMENTS

Fiscal 2005

| • | Throughout 2005, ADB expanded existing customer relationships while making efforts to add new customer organizations. Cross selling of ancillary software and services within established customer relationships continued and ADB was able to expand its working relationship with National Health Service (UK), Paramount (Canada), and GE Commercial Finance, Capital Solutions (US) (“GE CS”), among others. New customers included Mesta as (Norway), Star Energy (UK) and Trilogy (Canada). |

| • | In North America, ADB continued to focus on the expansion of activities related to GE’s Asset Manager, LLC, (GEAM) the joint venture co-owned by ADB Systems and GE CS. Incrementally through the year, software was refined in order to expand GEAM’s array of offerings to its clients and sales efforts broadened to include the appraisal industry, a commercial segment vital to the valuation and financing of assets. In this area, the joint venture successfully established a co-operation agreement with the North American Auctioneers Association (“NAA”) for the provision of appraisal services online. |

| • | ADB undertook a number of software development initiatives in 2005 to ensure continued technology leadership. The most substantial single project involved the re-architecture of certain WorkMate elements and resulted in enhanced functionality for a number of customers. |

16

Fiscal 2004

| • | ADB was engaged in a number of activities aimed at expanding our relationships with existing customers and developing relationships with new customer organizations. Through these efforts, which included the introduction of new technology enhancements to our suite of product offerings, the cross selling of ancillary applications, and the increase in the number of users of our technology, ADB was able to expand our working relationships with BP the National Health Services (UK), and GE CEF, among others. |

| • | In North America, the primary thrust of our activities in 2004 concentrated on the rollout of Asset Manager from GE, our joint venture with GE Commercial Finance. This joint venture is designed to combine GE’s equipment financing and asset management expertise together with our experience in providing mission-critical technology solutions for asset lifecycle management. Together, we have developed web-based solutions to help our customers: |

| • | Track and re-deploy assets more effectively; |

| • | Automate equipment appraisals; |

| • | Efficiently market and sell surplus equipment; and |

| • | Automate sourcing and tendering processes. |

| • | Through the joint venture, we signed a customer agreement with Kraft Foods Global, Inc. (“Kraft”) and continued to service our customer agreement with the General Electric Company, acting through its GE Aircraft Engines division (“GE Aircraft Engines”). |

| • | ADB made a number of enhancements to our suite of technology product offerings in 2004. These enhancements, which centered on re-architecting the under-lying platform of our Dyn@mic Buyer solution and expanding the functionality of our WorkMate and Material Transfer applications, allow us to stay current with the latest technology trends while maintaining a competitive advantage. |

| • | A key cornerstone of our technology activities focused on the development of Asset Tracker, a new, web-based asset-tracking offering that is delivered through our joint venture with GE. |

| • | Effective November 15, 2004 our stock symbol on the OTCBB was changed to ADBYF. The addition of the F to the symbol was a requirement of the OTCBB to signify that we are a foreign issuer. |

The Brick Transaction

On August 30, 2002, we entered into a series of agreements with The Brick Warehouse Corporation (“The Brick”) which contemplated a series of transactions among The Brick, ADB Systems International Inc. (“Old ADB”) and ADB. We refer to those transactions in this Form 20-F Annual Report as “The Brick Transaction”.

Pursuant to The Brick Transaction:

| • | The Brick made a $2.0 million secured loan to Old ADB and ADB at an interest rate of 12% per year; |

| • | ADB and Old ADB agreed to enter into the an arrangement agreement (the “Arrangement”); and |

| • | The Brick and Old ADB agreed to utilize the online retail technology, experience and expertise of ADB developed and operated under the name “Bid.Com International Inc.” for the online sale of consumer products to be supplied by The Brick (which we refer to in this report as the “Retail Business”). |

The $2.0 million secured loan made by The Brick matured on June 30, 2003. At maturity, ADB had the right, at its option, to: (i) repay the loan in cash or (ii) transfer to The Brick all of the issued shares of Old ADB owned by ADB in satisfaction of the outstanding principal amount and accrued interest then owing to The Brick. The obligations of Old ADB and ADB were secured by a general security agreement delivered by ADB to The

17

Brick covering all the property and assets of ADB. On June 30, 2003, ADB exercised its option to transfer to The Brick all of the issued shares of Old ADB in satisfaction of the outstanding principal amount and accrued interest then owing to The Brick.

The principal consequences of the Arrangement, which was effective as of October 31, 2002, are as follows:

| 1. | Shareholders of Old ADB received from ADB one common share of ADB in exchange for each of their common shares of Old ADB. As a result (i) Old ADB became a wholly owned subsidiary of ADB and (ii) each former shareholder of Old ADB owns the same number of shares in ADB that it owned in Old ADB prior to the exchange. |

| 2. | Old ADB transferred all of its assets to ADB and ADB assumed all of the liabilities and obligations of Old ADB, except that Old ADB retained specific assets and liabilities of the Retail Business. |

| 3. | The registered office, articles of incorporation, by-laws, directors and executive officers of Old ADB immediately prior to the Arrangement became the registered office, articles, by-laws, directors and executive officers of ADB upon consummation of the Arrangement. |

| 4. | ADB adopted the Stock Option Plan of Old ADB. Upon consummation of the Arrangement, all options, warrants or debt that was exercisable or convertible into shares of Old ADB became convertible into the same number of shares of ADB. |

| 5. | The articles of amalgamation of Old ADB were amended to: (i) change the name of Old ADB to Bid.Com International Ltd. and (ii) delete the authorized Preference Shares (as defined in such articles) and the rights, preferences and restrictions on the transfer of such Preference Shares. |

Upon completion of the Arrangement, the Toronto Stock Exchange approved the listing of the ADB common shares issued in exchange for Old ADB common shares or issuable upon the exercise of options or warrants or conversion of debt. ADB common shares are listed on the Toronto Stock Exchange for trading under the symbol “ADY”. The shares of Old ADB ceased trading on the Toronto Stock Exchange on November 5, 2002. On April 2, 2003 an order was issued by the Ontario Securities Commission pursuant to which Old ADB has ceased to be a reporting issuer in all jurisdictions in Canada in which it was a reporting issuer.

Joint Venture with GE Commercial Finance, Commercial Equipment Financing

On December 31, 2003 ADB Systems USA, Inc. (“ADB USA”), a wholly owned subsidiary of ADB, entered into an Amended and Restated Operating Agreement (the “Operating Agreement”) with General Electric Capital Corporation through is business division GE Commercial Finance, Capital Solutions (then, GE Commercial Finance, Commercial Equipment Financing) (“GE Commercial Finance”). This agreement was entered into in connection with the establishment of GE Asset Manager, LLC a joint business venture in which both GE Commercial Finance and ADB USA hold a 50% interest. Pursuant to this business venture, GE Commercial Finance and ADB USA also entered into the following agreements: ADB License Agreement, ADB Services Agreement, GE License Agreement and GE Service Agreement. GE Asset Manager LLC, which carries on business under the name GE Commercial Finance Asset Manager (“Asset Manager”), is an integrated, web-based business enabling mid- and large-size organizations to reduce operating costs by simplifying and consolidating their asset management programs. Asset Manager features all-in-one capabilities designed for sourcing of new equipment, tracking and reallocation of existing assets, automated appraisal management and disposition of surplus equipment.

PRINCIPAL CAPITAL EXPENDITURES AND DIVESTITURES

For a description of principal capital expenditures and divestitures, see Item 5 - OPERATING AND FINANCIAL REVIEW AND PROSPECTS - REALIZED GAINS AND LOSSES ON MARKETABLE SECURITIES AND STRATEGIC INVESTMENTS and CAPITAL ASSETS. As of May 31, 2006 we do not have any significant current capital divestitures or any current capital expenditures so far in 2006.

18

B. BUSINESS OVERVIEW

ADB Systems develops and sells software products and services that allow our customers to source, buy, track, manage and sell assets, primarily in asset intensive industries. We refer to our product and services suite as asset lifecycle management solutions. Our solutions can reduce sourcing, procurement and tracking costs, improve tracking and monitoring of asset performance and reduce operational downtime.

We acquired ADB Systemer ASA (“ADB Systemer”), in October 2001. For more than ten years, ADB Systemer provided enterprise asset management solutions (EAM) to customers in Norway and Europe. For the past three years, we have provided EAM solutions to customers in North America and Europe and during the past two years we have introduced sourcing and procurement solutions to customers in North America and Europe.

On May 18, 2006, the Company entered into an agreement with ADB Holding AS (the "Buyer") to sell 100 percent of the Company's interest in its Norwegian subsidiary ADB Systemer AS, (ADB Systemer") for NOK 15,000,000 or approximately Canadian $2.80 million in cash subject to shareholder approval. On June 21, 2006 the Company received approval from shareholders at its annual general meeting to proceed with the Share Sale, which is scheduled to close on June 30, 2006. Sale of the shares of ADB Systemer include sale of the ADB Systems name. Following the sale of ADB Systemer, the Company will retain access to all existing technology that will be used to service existing customers. In addition, the Company obtained Shareholder approval to change its name to Northcore Technologies Inc. by filing Articles of Amendment upon closing of the Share Sale transaction.

Our customers include a number of leading organizations, such as BP p.l.c. (“BP”), GE Commercial Finance, Capital Solutions (“GE CS”), National Health Service (UK), permanent TSB (the retail banking division of Irish Life Permanent p.l.c.) Talisman Energy Inc. (North Sea) (“Talisman Energy”), Vesta Insurance Group, Inc. (Norway) (“Vesta Insurance”), Paramount Resources Ltd. (Canada) (“Paramount”), Trilogy Energy Trust (Canada) (“Trilogy”), AS Vinmonopolet (Norway) (“Vinmonopolet”), Mesta as (Norway) and Star Energy HG Gas Storage Limited (UK)(“Star Energy”).

INDUSTRY BACKGROUND AND OVERVIEW

Asset management software has existed for more than thirty years, initially through computerized maintenance management systems (CMMS), and more recently including more comprehensive and robust enterprise asset management (EAM) and enterprise resource planning (ERP) solutions. The early CMMS systems automated daily management of assets, while ERP solutions consolidate basic asset information with financial information at the corporate level. EAM solutions encompass elements of both, serving as the next evolution of CMMS solutions by bridging the gap between asset management and corporate-level planning and tracking requirements.

The key value proposition for EAM solutions is that they can provide a quick and quantifiable return on investment (ROI) and return on assets (ROA). Cost and productivity improvements can immediately and measurably benefit organizations, and thus are highly desirable to potential customers, particularly in difficult economic times where the focus is increasingly bottom line oriented.

In addition to EAM solutions, we offer sourcing and procurement solutions as well as sales solutions. These are natural extensions to EAM solutions, as organizations seek to extend asset management and corporate-level planning and tracking onto other elements of the asset lifecycle.

PRODUCTS AND SERVICES

ADB offers solutions to manage all aspects of the asset lifecycle - sourcing/procurement, maintenance, materials management and disposition. Below is a detailed description of our products/services:

19

WorkMate (TM)

The Company’s flagship solution, WorkMate provides integrated capabilities for enterprise asset management. WorkMate is a client-server solution that operates as an extension of (and can be fully integrated with) a customer’s existing ERP system. The most advanced version of WorkMate incorporates asset maintenance, asset tracking, materials management and procurement functionality.

WorkMate is designed for use by customers in asset intensive industries - typically those where maintenance, repair and operations purchases outnumber raw material purchases by more than ten to one on a transaction volume basis. Examples of asset intensive industries are oil and gas, process industries (such as mining) and the utilities sector.

The three main modules (procurement, materials management and maintenance functionality) may be licensed independently or together as a fully integrated system:

| • | Procurement Module - for sophisticated domestic and international purchasing operations. Key capabilities include: order requisitioning, quotations, purchase orders, contracts, cost controls and vendor catalogues. The procurement module also monitors supplier performance in terms of accuracy, punctuality and cost. |

| • | Materials Management Module - for managing inventory and logistics operations. Key features include: inventory status, goods receipt, stock issue, reordering, packing/unpacking, transportation, goods return and equipment rentals. This Module will log all movements of an item and generates the necessary financial transactions. |

| • | Maintenance Module - for all types of maintenance, including corrective, preventive or condition-based activities. Customers can automate manual routines and track maintenance costs and equipment history. |

Each WorkMate module also includes workflow and reporting tools.

WorkMate is a licensed client-server application and pricing is based on the number of users named by the customer. Service fees are charged separately for implementation, systems integration, training and other consulting activities. Our WorkMate customers include some of the largest global players in the oil and gas sector, such as: BP (Norway), Halliburton Productous, Prosafe, Talisman Energy (Canada)., Paramount Resources and Mesta AS.

ProcureMate (TM)

ProcureMate is our web-based business-to-business e-Procurement solution designed to reduce purchase costs, improve purchasing efficiencies and reduce maverick buying. ProcureMate allows users to select goods for purchase from a web-based catalog and automatically issue purchase orders to their suppliers.

Key features of ProcureMate include:

| • | The ability to notify suppliers automatically of purchase orders requiring processing. |

| • | Functionality for allowing on-line dialogue to take place between buyers and suppliers. |

| • | The ability to integrate to enterprise resource planning and financial systems, reducing manual efforts for processing and consolidating purchase orders, goods receipt and payment activities. |

| • | Functionality for facilitating direct payment and electronic funds transfer. |

| • | The ability to integrate user workflow and approvals into the procurement process. |

ProcureMate is licensed to customers and license fees for ProcureMate are based on the number of users named by the customer. Service fees are charged separately for implementation, systems integration, training and other consulting activities. ProcureMate can be bundled with our other on-line purchasing solutions or used separately depending on customer requirements. Existing ProcureMate customers include BP (Norway), National Health Services (UK), Vesta Insurance, Vinmonopolet, Norway’s government-run retailer of wine and spirits and Hordaland HFK County, a large local government entity in Norway.

Dyn@mic Buyer (TM)

An on-line sourcing solution, Dyn@mic Buyer automates the tendering process, and can be used to improve the decision-making process involved in sourcing goods by providing automated analysis and selection

20

among competing bids, based on a variety of pre-determined factors. The current release of Dyn@mic Buyer can be delivered on a hosted or client-server (licensed) basis.

Key features of the product include:

| • | The ability for buyers to create tenders using automated tools that accelerate the purchasing process and reduce procurement costs. |

| • | Capabilities for buyers to post and distribute their tenders on-line to qualified suppliers. |

| • | The ability for buyers to assign values to criteria involved in the purchase decision, such as price, product availability, post-sales support and certification standards. Suppliers’ responses to tender questions are then weighed for evaluation by buyers. |

| • | Functionality that allows for the posting of detailed technical information, question and answer forums, and automatic e-mail notification of amended or new buyer-posted documents. |

| • | Capabilities to allow for the use of sealed bid sourcing formats enabling users to post their product or service requirements to selected vendors. The sealed bid system differs from the request for quotation in that the vendors only have one opportunity to supply a bid. Only after the close of the auction is the user able to view the vendor bids. |

Dyn@mic Buyer is licensed to our customers. Fees for Dyn@mic Buyer are determined on an annual basis, depending on the number of sourcing events identified by customers. Service fees are charged separately for implementation, systems integration, training and other consulting activities. Dyn@mic Buyer can be bundled with our procurement solutions or used separately depending on customer requirements. Current customers using Dyn@mic Buyer include the National Health Services (UK) and Vesta Insurance.

Dyn@mic Seller (TM)

Dyn@mic Seller is an on-line sales solution designed to help our customers with the disposition of surplus assets and equipment. Dyn@mic Seller integrates multiple pricing methods, such as fixed priced, top bid (auction), dutch (declining price) and hybrids, through private-labeled websites. Dyn@mic Seller is delivered through an application service provider model. (remotely through the internet).

Key capabilities of the product include:

| • | Traditional rising price auctions, where the highest bids win the items being sold. The rising price auction allows participants to competitively bid on available products by incrementally adjusting their bid amounts. Our user interface allows users to easily identify current leading bidders, minimum new bids and initial bid pricing. Participants are informed of their bid status, stating whether they have won, been outbid, approved or declined via electronic mail. |

| • | A patented Dutch (declining) auction format, in which a starting price is set and a limited time period is allocated for a fixed quantity of the product to be sold. As time advances, the price drops in small increments until the asset is sold. The declining bid auction allows participants to bid in a real-time format utilizing on-screen data which provides the time and quantity remaining as well as the falling price of the items for sale. |

| • | Hybrid auction formats that blend multiple pricing formats to meet a customer’s particular needs. |

| • | Fixed price sales where assets are sold in a catalogue or directory format. The purchaser cannot bid on the price, but merely elects whether or not to purchase the good or service. |

Our customers pay monthly hosting fees for use of Dyn@mic Seller and typically also enter into a revenue sharing arrangement with us. Service fees for implementation, systems integration, training and other consulting activities are charged separately. Current customers of Dyn@mic Seller include GE Capital Solutions. and permanent TSB (Ireland).

Related Services

In connection with our software offerings, we provide the following services to our customers:

Consulting. A significant number of our customers request our advice regarding their business and technical processes, often in conjunction with a scoping exercise conducted both before and after the execution of a contract. This advice can relate to development or streamline of assorted business processes, such as sourcing or

21

procurement activities, assisting in the development of technical specifications, and recommendations regarding internal workflow activities.

Customization and Implementation. Based generally upon the up-front scoping activities, we are able to customize our solutions as required to meet the customer's particular needs. This process can vary in length depending on the degree of customization, the resources applied by the customer and the customer's business requirements. We work closely with our customers to ensure that new features and functionality meet their expectations. We also provide the professional services work required for the implementation of our customer solutions, including loading of data, identification of business processes, and integration to other systems applications.

Training. Upon completion of implementation (and often during implementation), we train customer personnel to utilize our Solutions through our administrative tools. Training can be conducted in one-on-one or group situations. We also conduct “train the trainer” sessions.

Maintenance and Support. We provide regular software upgrades and ongoing support to our customers.

GE’s Asset Manager

GE's Asset Manager is a joint venture between GE Commercial Finance, Capital Solutions and ADB Systems International Ltd. that combines GE’s equipment financing and asset management expertise together with ADB's experience in providing mission critical technology solutions for asset lifecycle management.

With organizations needing to generate improved bottom-line results and comply with new financial regulatory requirements, GE's Asset Manager has introduced a new suite of integrated, web-based solutions that are designed to help organizations gain greater control of their capital assets and implement new process efficiencies to their operational activities.

Our industry-proven solutions enable our customers to:

| • | Track and re-deploy assets more effectively |

| • | Automate equipment appraisals |

| • | Efficiently market and sell surplus equipment |

| • | Automate sourcing and tendering processes |

The four key components to Asset Manager’s offerings are as follows:

Asset Tracker

Designed to allow organizations to more effectively utilize their assets, Asset Manager is a web-based solution for keeping track of the location, details and status of capital equipment - regardless of where the equipment is being deployed.

Using a dedicated tracking site that is password protected, Asset Manager provides users the ability to search and locate capital assets throughout their organization. Users can search for equipment in a number of ways. Assets can be searched by business unit, function, or by specific piece of equipment category.

Once an asset is located, users can determine its status and take appropriate action. Idle or under-utilized assets, for example, can be re-deployed, helping to increase their value to the organization and reducing capital spending on new equipment.

Assets no longer required or deemed surplus can be earmarked for disposition through traditional or on-line sales methods, such as Asset Seller.

With Asset Tracker, users can:

| • | Search and request for capital equipment within their organization, across multiple locations or facilities |

| • | Review asset details, such as equipment description, image, financial information, and contact information |

| • | Add new asset details by uploading data from spreadsheet applications |

| • | Extract asset details and generate asset management reports |

| • | Instantly determine the status of capital equipment |

| • | Transfer and re-deploy idle assets |

22

| • | Dispose of unnecessary or surplus equipment |

Asset Appraiser

Asset Appraiser is a web-based solution that allows organizations to more effectively manage the capital equipment appraisal process. With Asset Appraiser organizations can create an appraisal scope, source, confirm appraisal data, distribute documents and data collection tools, compile appraisal results and access stored appraisals on-line in a protected environment.

Asset Appraiser allows users to:

| • | Create the full scope of appraisals on-line |

| • | Automate and accelerate the appraisal process using web-based tools |

| • | Gain instant access to ongoing project details from anywhere in the world |

| • | Store asset data in a secure repository for future reference, retrieval and analysis |

| • | Confirm appraisal details via electronic drafts |

| • | Access appraisals in a 24 x 7 environment |

| • | Capture all relevant data through drop down text boxes |

| • | Store and review appraisals in a secure environment |

| • | Download spreadsheet templates into reports |

| • | Add attachments, such as image, text or movie files, to reports |

| • | Ability to add an addendum to a completed appraisal report |

| • | An aid to Sarbanes-Oxley compliance |

| • | Ensure compliance with the Uniform Standards of Professional Appraisal Practice |

Asset Seller

Asset Seller facilitates instant and global access to a buying community by presenting your surplus equipment or inventory on geasset.com, GE's off-lease equipment re-marketing website. Asset Seller is a proven take-to-market solution that will connect your company's equipment to a global community of qualified organizational buyers using multiple sales platforms, all developed to help maximize asset recovery value and improve cycle time.

Asset Seller brings together multiple sales platforms into one integrated on-line environment, providing flexibility, while maximizing the yield for your surplus equipment.

Asset Seller's direct sale platform features equipment showcases that are designed to promote private treaty sales. Other sales platforms available through Asset Seller include ranked sealed bid and top bid sale events that enable you to market equipment in an auction-like environment.

Utilizing GE's patent pending ranked sealed bid method, Asset Seller encourages multiple bids and retains buyer anonymity, creating competitive sales environments that generate a higher recovery for asset investment.

Asset Seller also enables organizations to feature equipment specifications, photos, videos and contact information, and allows them to coordinate off-line sales activities such as equipment inspections.

Asset Buyer

Asset Buyer is a web-based solution designed for automating sourcing activities and improving purchasing decisions. Using Asset Buyer, purchasers can determine the factors that are the most important to their procurement decisions and identify suppliers that deliver the greatest value - from the lowest price to the ability to match exact specification requirements.

Asset Buyer also streamlines the procurement process, making it easier to create and distribute tenders, select vendors and negotiate with suppliers.

With Asset Buyer, organizations can:

| • | generate cost savings on sourcing activities |

23

| • | reduce purchasing cycle times |

| • | take advantage of multiple sourcing formats including request for proposals, reverse auction, and sealed bid |

| • | rank suppliers based on their ability to match buying criteria |

| • | improve relations with suppliers through on-line collaborations. |

Third Party Partnerships

In addition to the sale of our core solutions and services, we have entered into marketing or co-marketing agreements with a number of companies that offer services that are complementary to our products and services. We market these complementary services to our customers and prospects and can earn a referral fee if these services are purchased. In some cases our marketing partner has agreed to market our solutions to its customers and prospects and can earn a referral fee. Our marketing partners include:

Partner | Service or Offering |

AMEC Services Limited | Engineering Services |

| Production Access, Inc. | Oil and Gas Data Management Solutions |

Business Cycles