As filed with the Securities and Exchange Commission on March 8, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

|

|

|

|

|

|

| Pre-Effective Amendment No. __ |

|

|

|

| Post-Effective Amendment No. |

|

|

(Check appropriate box or boxes)

Exact Name of Registrant as Specified in Charter:

WELLS FARGO VARIABLE TRUST

Area Code and Telephone Number: (800) 552-9612

Address of Principal Executive Offices, including Zip Code:

525 Market Street

San Francisco, California 94163

Name and Address of Agent for Service:

C. David Messman

c/oWellsFargo Funds Management, LLC

525 Market Street, 12th Floor

San Francisco, California 94105

With copies to:

Marco E. Adelfio, Esq.

GOODWIN PROCTER LLP

901 NEW YORK AVENUE, N.W.

WASHINGTON, D.C. 20001

It is proposed that this filing will become effective on April 9, 2010 pursuant to Rule 488.

No filing fee is required under the Securities Act of 1933 because an indefinite number of shares of beneficial interest in the Registrant has previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940, as amended.

WELLS FARGO VARIABLE TRUST

PART A

PROSPECTUS/PROXY STATEMENT

EVERGREEN FUNDS

200 Berkeley Street

Boston, MA 02116-5034

1.800.343.2898

WELLS FARGO VARIABLE TRUST

525 Market Street

San Francisco, CA 94105

1.800.222.8222

____, 2010

Dear Investor,

On December 31, 2008, the parent company of the investment adviser to the Evergreen funds, Wachovia Corporation ("Wachovia"), and the parent company of the investment adviser to Wells Fargo Advantage Funds®, Wells Fargo & Company ("Wells Fargo"), merged. Since that date, the investment adviser to the Evergreen funds, Evergreen Investment Management Company, LLC ("EIMC"), and the investment adviser to Wells Fargo Advantage Funds, Wells Fargo Funds Management, LLC ("Funds Management"), have considered rationalizing and reorganizing their mutual fund businesses. After multiple presentations to and discussions with the Boards of Trustees of both the Evergreen funds and Wells Fargo Advantage Funds regarding these matters, on December 30, 2009, EIMC proposed to the Boards of Trustees of the Evergreen funds, and on January 11, 2010, Funds Management proposed to the Boards of Trustees of Wells Fargo Advantage Funds, the mergers outlined in the table below (each, a "Merger and collectively, the "Mergers"). Both the Boards of Trustees of the Evergreen funds and Wells Fargo Advantage Funds approved the proposed Mergers and the related Agreement and Plan of Reorganization subject to the approval by shareholders of each Target Fund, as part of a comprehensive set of mutual fund mergers across the two fund families.

As a result, if you are a contract owner, you are invited to vote on the proposal to merge your Target Fund into a corresponding Acquiring Fund shown in the table below (each a "Merger," and collectively, the "Mergers"). You may vote on the proposal by providing your voting instruction to your insurance company by completing, dating, signing and returning the enclosed voting instruction card in the postage-paid envelope provided. You may also provide voting instructions by telephone or the internet by following the instructions as outlined at the end of this prospectus/proxy statement. The Boards of Trustees of the Target Funds (shown in the table below) have unanimously approved the Mergers and recommend that you vote FOR these proposals.

Target Fund | Target Trust | Acquiring Fund | Acquiring Trust | |||||

Evergreen VA Core Bond Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Total Return Bond Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Omega Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Large Company Growth Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Special Values Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small/Mid Cap Value Fund1 | Wells Fargo Variable Trust | |||||

Evergreen VA Growth Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small Cap Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA International Equity Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT International Core Fund2 | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Equity Income Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT C&B Large Cap Value Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Fundamental Large Cap Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Large Company Core Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

| 1 | Effective May 1, 2010, the Fund's name will be changed to the Wells Fargo Advantage VT Small Cap Value Fund. |

| 2 | Immediately following the Merger, the Fund's name will be changed to the Wells Fargo Advantage VT International Equity Fund. |

If approved by shareholders, this is a general summary of how each Merger will work:

Each Target Fund will transfer all of its assets to the corresponding Acquiring Fund.

Each Acquiring Fund will assume all of the liabilities of the corresponding Target Fund.

Each Acquiring Fund will issue new shares that will be distributed to each shareholder in an amount equal to that shareholder's value of Target Fund shares.

If the Merger is consummated, each Target Fund shareholder will become a shareholder of the corresponding Acquiring Fund and will have his or her investment managed in accordance with the Acquiring Fund's investment strategies.

You will not incur any sales charges or similar transaction charges as a result of the Merger.

It is expected that the Merger will be a non-taxable event for shareholders for U.S. federal income tax purposes.

Details about each Target Fund's and each Acquiring Fund's investment goals, portfolio management team, past performance, principal risks, fees, and expenses, along with additional information about the proposed Mergers, are contained in the attached prospectus/proxy statement. Please read it carefully.

A special meeting of each Target Fund's shareholders will be held on June 8, 2010. Although shareholders are welcome to attend the meeting in person, they do not need to do so in order to vote shares. If you are a shareholder and do not expect to attend the meeting, please complete, date, sign and return the enclosed proxy card or voting instruction card in the postage-paid envelope provided. You may also vote by telephone or the internet by following the instructions as outlined at the end of this prospectus/proxy statement. If your Target Fund or insurance company does not receive your input after several weeks, you may receive a telephone call from The Altman Group, our proxy solicitor, requesting your input. If you have any questions about the Mergers, the proxy card, or voting instruction card, please call The Altman Group at (866) 342-1635 (toll-free).

IT IS IMPORTANT THAT PROXY CARDS OR VOTING INSTRUCTION CARDS BE RETURNED PROMPTLY. SHAREHOLDERS AND CONTRACT OWNERS ARE URGED TO SIGN WITHOUT DELAY AND RETURN THEIR PROXY CARD OR VOTING INSTRUCTION CARD, AS APPLICABLE, IN THE ENCLOSED POSTAGE-PAID ENVELOPE, OR TO PROVIDE INSTRUCTIONS USING ONE OF THE OTHER METHODS DESCRIBED AT THE END OF THE PROSPECTUS/PROXY STATEMENT SO THAT YOUR VIEWS MAY BE REPRESENTED AT THE MEETING. YOUR PROMPT ATTENTION TO THE PROXY CARD OR VOTING INSTRUCTION CARD WILL HELP TO AVOID THE EXPENSE OF FURTHER SOLICITATION.

Remember, your voice is important to us, no matter how large your investment. Please take this opportunity to provide your input. Thank you for taking this matter seriously and participating in this important process.

Sincerely,

Karla M. Rabusch

President

Wells Fargo Funds Trust

W. Douglas Munn

President

Evergreen Funds

EVERGREEN FUNDS

200 Berkeley Street

Boston, MA 02116-5034

1.800.343.2898

____, 2010

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON JUNE 8, 2010

A Special Meeting (the "Meeting") of Shareholders of your Target Fund, a series of the Target Trust, each set forth in the table below, will be held at the offices of Wells Fargo Advantage Funds®, 525 Market Street, San Francisco, California 94105 on June 8, 2010 at 10:00 a.m., Pacific time.

Target Fund | Target Trust | Acquiring Fund | Acquiring Trust | |||||

Evergreen VA Core Bond Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Total Return Bond Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Omega Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Special Values Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small/Mid Cap Value Fund1 | Wells Fargo Variable Trust | |||||

Evergreen VA Growth Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small Cap Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA International Equity Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT International Core Fund2 | Wells Fargo Variable Trust | |||||

Evergreen VA Fundamental Large Cap Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

| 1 | Effective May 1, 2010, the Fund's name will be changed to the Wells Fargo Advantage VT Small Cap Value Fund. |

| 2 | Immediately following the Merger, the Fund's name will be changed to the Wells Fargo Advantage VT International Equity Fund. |

With respect to your Target Fund, the Meeting is being held for the following purposes:

To consider and act upon an Agreement and Plan of Reorganization (the "Plan") dated as of March 1, 2010, providing for the reorganization of the Target Fund, including the acquisition of all of the assets of the Target Fund by the corresponding Acquiring Fund in exchange for shares of the Acquiring Fund (the "Acquisition Shares") and the assumption by the Acquiring Fund of all of the liabilities of the Target Fund. The Plan also provides for the prompt distribution of the Acquisition Shares to shareholders of the corresponding Target Fund in liquidation of the Target Fund.

To transact any other business which may properly come before the Meeting or any adjournment(s) thereof.

Any adjournment(s) of the Meeting will be held at the above address. The Board of Trustees of your Target Fund has fixed the close of business on March 10, 2010 as the record date (the "Record Date") for the Meeting. Only shareholders of record as of the close of business on the Record Date will be entitled to this notice, and to vote at the Meeting or any adjournment(s) thereof.

IT IS IMPORTANT THAT PROXY CARDS BE RETURNED PROMPTLY. ALL SHAREHOLDERS ARE URGED TO COMPLETE, DATE, SIGN AND RETURN THEIR PROXY CARD IN THE ENCLOSED POSTAGE-PAID ENVELOPE, OR TO VOTE USING ONE OF THE OTHER METHODS DESCRIBED AT THE END OF THE PROSPECTUS/PROXY STATEMENT SO THAT YOUR SHARES MAY BE REPRESENTED AT THE MEETING. YOUR PROMPT ATTENTION TO THE ENCLOSED PROXY CARD WILL HELP TO AVOID THE EXPENSE OF FURTHER SOLICITATION.

By order of the Board of Trustees,

Michael H. Koonce

Secretary

WELLS FARGO VARIABLE TRUST

525 Market Street

San Francisco, CA 94105

1.800.222.8222

____, 2010

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON JUNE 8, 2010

A Special Meeting (the "Meeting") of Shareholders of your Target Fund, a series of the Target Trust, each set forth in the table below, will be held at the offices of Wells Fargo Advantage Funds®, 525 Market Street, San Francisco, California 94105 on June 8, 2010 at 12:00 p.m., Pacific time.

Target Fund | Target Trust | Acquiring Fund | Acquiring Trust | |||||

Wells Fargo Advantage VT Large Company Growth Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Equity Income Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT C&B Large Cap Value Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Large Company Core Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

With respect to your Target Fund, the Meeting is being held for the following purposes:

To consider and act upon an Agreement and Plan of Reorganization (the "Plan") dated as of March 1, 2010, providing for the reorganization of the Target Fund, including the acquisition of all of the assets of the Target Fund by the corresponding Acquiring Fund in exchange for shares of the Acquiring Fund (the "Acquisition Shares") and the assumption by the Acquiring Fund of all of the liabilities of the Target Fund. The Plan also provides for distribution of the Acquisition Shares to shareholders of the corresponding Target Fund and the subsequent liquidation and dissolution of the Target Fund. A vote in favor of the Plan is a vote in favor of the liquidation and dissolution of the Target Fund.

To transact any other business which may properly come before the Meeting or any adjournment(s) thereof.

Any adjournment(s) of the Meeting will be held at the above address. The Board of Trustees of your Target Fund has fixed the close of business on March 10, 2010, as the record date (the "Record Date") for the Meeting. Only shareholders of record as of the close of business on the Record Date will be entitled to this notice, and to vote at the Meeting or any adjournment(s) thereof.

IT IS IMPORTANT THAT PROXY CARDS BE RETURNED PROMPTLY. SHAREHOLDERS WHO DO NOT EXPECT TO ATTEND IN PERSON ARE URGED TO SIGN WITHOUT DELAY AND RETURN PROXY CARD IN THE ENCLOSED POSTAGE-PAID ENVELOPE, OR TO VOTE USING ONE OF THE OTHER METHODS DESCRIBED AT THE END OF THE PROSPECTUS/PROXY STATEMENT SO THAT YOUR SHARES MAY BE REPRESENTED AT THE MEETING. YOUR PROMPT ATTENTION TO THE ENCLOSED PROXY CARD WILL HELP TO AVOID THE EXPENSE OF FURTHER SOLICITATION.

By order of the Board of Trustees,

C. David Messman

Secretary

EVERGREEN FUNDS

200 Berkeley Street

Boston, MA 02116-5034

1.800.343.2898

WELLS FARGO VARIABLE TRUST

525 Market Street

San Francisco, CA 94105

1.800.222.8222

____, 2010

PROSPECTUS/PROXY STATEMENT

This prospectus/proxy statement contains information you should know before voting [or providing voting instructions] on the proposed merger (the "Merger") of your Target Fund into the corresponding Acquiring Fund as set forth and defined in the table below, each of which is a series of a registered open-end management investment company. Your Target Fund serves as an underlying investment option for certain variable annuity contracts and variable life insurance policies (collectively, the "Variable Contracts"). Although insurance company separate accounts are the predominant record owners of your Target Fund's shares, the insurance companies are required to solicit voting instructions from owners of the Variable Contracts issued by those insurance companies, and generally vote all Funds' shares proportionately in accordance with timely received instructions. As a result, if you are a contract owner of a Variable Contract, you are being asked to provide voting instructions on the Merger. If approved, the Merger will result in your receiving shares or an interest in shares of the Acquiring Fund in exchange for your shares or interest in shares of the Target Fund.

Target Fund | Target Trust | Acquiring Fund | Acquiring Trust | |||||

Evergreen VA Core Bond Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Total Return Bond Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Omega Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Large Company Growth Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Omega Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Special Values Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small/Mid Cap Value Fund1 | Wells Fargo Variable Trust | |||||

Evergreen VA Growth Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Small Cap Growth Fund | Wells Fargo Variable Trust | |||||

Evergreen VA International Equity Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT International Core Fund2 | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Equity Income Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT C&B Large Cap Value Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Intrinsic Value Fund | Wells Fargo Variable Trust | |||||

Evergreen VA Fundamental Large Cap Fund | Evergreen Variable Annuity Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

Wells Fargo Advantage VT Large Company Core Fund | Wells Fargo Variable Trust | Wells Fargo Advantage VT Core Equity Fund | Wells Fargo Variable Trust | |||||

| 1 | Effective May 1, 2010, the Fund's name will be changed to the Wells Fargo Advantage VT Small Cap Value Fund. |

| 2 | Immediately following the Merger, the Fund's name will be changed to the Wells Fargo Advantage VT International Equity Fund. |

The Target and Acquiring Funds listed above are collectively referred to as the "Funds." The Target and Acquiring Trusts listed above are collectively referred to as the "Trusts."

Please read this prospectus/proxy statement carefully and retain it for future reference. Additional information concerning each Fund and/or Merger has been filed with the Securities and Exchange Commission ("SEC").

The prospectuses of each Target Fund and each Acquiring Fund (other than the Wells Fargo Advantage VT Core Equity Fund, the Wells Fargo Advantage VT Intrinsic Value Fund and the Wells Fargo Advantage VT Omega Growth Fund) are incorporated into this document by reference and are legally deemed to be part of this prospectus/proxy statement.

The Statement of Additional Information relating to this prospectus/proxy statement (the "Merger SAI"), dated the same date as this prospectus/proxy statement, is also incorporated into this document by reference and is legally deemed to be part of this prospectus/proxy statement.

The Statement of Additional Information ("SAI"), and the annual and semi-annual reports of each Target Fund and each Acquiring Fund (other than the Wells Fargo Advantage VT Core Equity Fund, the Wells Fargo Advantage VT Intrinsic Value Fund and the Wells Fargo Advantage VT Omega Growth Fund) are incorporated into the Merger SAI by reference and are legally deemed to be part of the Merger SAI.

A copy of your Acquiring Fund's prospectus (other than the Wells Fargo Advantage VT Core Equity Fund, the Wells Fargo Advantage VT Intrinsic Value Fund and the Wells Fargo Advantage VT Omega Growth Fund) accompanies this prospectus/proxy statement.

Copies of these documents pertaining to an Evergreen Target Fund are available upon request without charge by writing to the address above, calling 1.800.343.2898 or visiting the Evergreen Funds' Web site at www.evergreeninvestments.com. Copies of these documents pertaining to a Wells Fargo Target Fund and Acquiring Fund (other than the Wells Fargo Advantage VT Core Equity Fund, the Wells Fargo Advantage VT Intrinsic Value Fund and the Wells Fargo Advantage VT Omega Growth Fund) are available upon request without charge by writing to Wells Fargo Advantage Funds®, P.O. Box 8266, Boston, MA 02266-8266, calling 1.800.222.8222 or visiting the Wells Fargo Advantage Funds Web site at www.wellsfargo.com/advantagefunds.

The Wells Fargo Advantage VT Core Equity Fund, the Wells Fargo Advantage VT Intrinsic Value Fund and the Wells Fargo Advantage VT Omega Growth Fund are each a "Shell Fund" being registered with the SEC in order to receive the assets and assume the liabilities of its corresponding Target Fund. As such, prospectuses, SAIs and annual and semi-annual reports for these Acquiring Funds are not yet available as of the date of this prospectus/proxy statement. Additional information about these Acquiring Funds may be found in Exhibit E and the Merger SAI.

You may also view or obtain these documents from the SEC: by phone at 1.800.SEC.0330 (duplicating fee required); in person or by mail at Public Reference Section, Securities and Exchange Commission, 100 F. Street, N.E., Washington, D.C. 20549-0213 (duplicating fee required); by email at publicinfo@sec.gov (duplicating fee required); or by internet at www.sec.gov.

The SEC has not approved or disapproved these securities or determined if this prospectus/proxy statement is truthful or complete. Any representation to the contrary is a criminal offense.

The shares offered by this prospectus/proxy statement are not deposits of a bank, and are not insured, endorsed or guaranteed by the FDIC or any government agency and involve investment risk, including possible loss of your original investment.

| Evergreen VA Core Bond Fund |

| Evergreen VA Diversified Capital Builder Fund |

| Evergreen VA Diversified Income Builder Fund |

| Evergreen VA Fundamental Large Cap Fund |

| Evergreen VA Growth Fund |

| Evergreen VA High Income Fund |

| Evergreen VA International Equity Fund |

| Evergreen VA Omega Fund |

| Evergreen VA Special Values Fund |

| WF VT Asset Allocation Fund |

| WF VT C&B Large Cap Value Fund |

| WF VT Discovery Fund |

| WF VT Equity Income Fund |

| WF VT International Core Fund |

| WF VT Large Company Core Fund |

| WF VT Large Company Growth Fund |

| WF VT Opportunity Fund |

| WF VT Small Cap Growth Fund |

| WF VT Small/Mid Cap Value Fund |

| WF VT Total Return Bond Fund |

Table of Contents

OVERVIEW

The Funds are underlying investment vehicles for certain variable annuity contracts and/or variable life insurance policies offered through separate accounts of participating insurance companies. Depending on the context, references to "you" or "your" in this summary refer either to the holder of a variable annuity contract or variable insurance policy who may select Fund shares to fund his or her investment in the policy or contract or to the insurance company that issues the contract or policy. Throughout this summary, references to a Fund "shareholder" refer only to the insurance company investing in the Fund through a separate account, and not to a holder of a variable annuity contract or variable insurance policy.

This section summarizes the primary features and consequences of your Merger. This summary is qualified in its entirety by reference to the information contained elsewhere in this prospectus/proxy statement, in the Merger SAI, in each Fund's prospectus (other than the Wells Fargo Advantage VT Omega Growth Fund, the Wells Fargo Advantage VT Core Equity Fund, and the Wells Fargo Advantage VT Intrinsic Value Fund), in each Fund's financial statements contained in the annual and semi-annual reports (other than the Wells Fargo Advantage VT Omega Growth Fund, the Wells Fargo Advantage VT Core Equity Fund, and the Wells Fargo Advantage VT Intrinsic Value Fund), and in each Fund's SAI (other than the Wells Fargo Advantage VT Omega Growth Fund, the Wells Fargo Advantage VT Core Equity Fund, and the Wells Fargo Advantage VT Intrinsic Value Fund), and to the Agreement and Plan of Reorganization (the "Plan"), a form of which is attached as Exhibit A hereto.

Key Features of the Mergers

The Plan sets forth the key features of each Merger and generally provides for the following:

the transfer of all of the assets of the Target Fund to the Acquiring Fund in exchange for shares of the Acquiring Fund;

the assumption by the Acquiring Fund of all of the liabilities of the Target Fund;

the liquidation of the Target Fund by distributing the shares of the Acquiring Fund to the Target Fund's shareholders; and

the assumption of the costs of each Merger (other than costs incurred from securities transactions in connection with the Merger) by Wells Fargo Funds Management, LLC ("Funds Management") and/or Evergreen Investment Management Company, LLC ("EIMC") or one of its affiliates.

The Mergers are scheduled to take place on or about _______. For a more complete description of the Mergers, see the section entitled "Agreement and Plan of Reorganization," as well as Exhibit A.

Board of Trustees Recommendation

At a meeting held on December 30, 2009 for the Boards of Trustees of the Evergreen funds, and on January 11, 2010 for the Board of Trustees of the Wells Fargo Advantage Funds, the Trustees of your Target Fund, including a majority of the Trustees who are not "interested persons" of your Target Fund, as that term is defined in the Investment Company Act of 1940, as amended (the "1940 Act") (the "Independent Trustees"), considered and unanimously approved the Merger of your Target Fund.

Before approving the Mergers, the Trustees reviewed, among other things, information about the Funds and the proposed transactions. Those materials set forth a comparison of various factors, such as the relative sizes of the Funds, the performance records of the Funds, and the expenses of the Funds (including pro forma expense information of each surviving fund following the Mergers), as well as similarities and differences between the Funds' investment goals, principal investment strategies and specific portfolio characteristics.

The Board of Trustees of your Target Fund, including all of the Independent Trustees, has concluded that the Merger would be in the best interests of your Target Fund, and that existing shareholders' interests would not be diluted as a result of the Merger. Accordingly, the Trustees have submitted the Plan to the Target Fund's shareholders and unanimously recommend its approval. The Board of Trustees of the Wells Fargo Advantage Funds has also approved the Plan on behalf of each Acquiring Fund.

For further information about the considerations of each Target Trust's Board, please see the section entitled "Reasons for the Mergers."

Merger Summary (Goals, Strategies, Risks, Performance, Expense, Management and Tax Information)

The following section provides a comparison between the Funds with respect to their investment goals, principal investment strategies, fundamental investment policies, risks, performance records, sales charges and expenses. It also provides information about what the management and share class structure of your Acquiring Fund will be after the Merger. The information below is only a summary; for more detailed information, please see the rest of this prospectus/proxy statement and each Fund's prospectus and SAI (other than for the Wells Fargo Advantage VT Omega Growth Fund, the Wells Fargo Advantage VT Core Equity Fund and the Wells Fargo Advantage VT Intrinsic Value Fund, for which information can be found in Exhibit E of this prospectus/proxy statement and the Merger SAI). In this section, percentages of a Wells Fargo Advantage Fund's "net assets" are measured as percentages of net assets plus borrowings for investment purposes. References to "we" in the principal investment strategy discussion for a Wells Fargo Advantage Fund generally refer to Funds Management, a sub-adviser or the portfolio manager(s).

EVERGREEN VA CORE BOND FUND INTO WELLS FARGO ADVANTAGE VT TOTAL RETURN BOND FUND

Share Class Information

The following table illustrates the share class of the Acquiring Fund that shareholders will receive as a result of the Merger in exchange for their shares in the Target Fund.

If you own this class of shares of Evergreen VA Core Bond Fund: | You will get this class of shares of Wells Fargo Advantage VT Total Return Bond Fund: | ||||

Class 2 | Class 21 |

| 1 | Upon completion of the proposed Merger, the Fund will rename its existing single class of shares as Class 2 shares. |

The Acquiring Fund shares that shareholders receive as a result of the Merger will have the same total value as the total value of their Target Fund shares as of the close of business on the business day immediately prior to the Merger.

The procedures for buying, selling and exchanging shares of the Funds are similar. For additional information, see the section entitled "Buying, Selling and Exchanging Fund Shares." This section also contains important information for foreign shareholders of an Evergreen Target Fund, defined as shareholders whose accounts do not currently have both a U.S. address and taxpayer identification number on record with the Funds. Following the Merger, foreign shareholders will no longer be able to make additional investments into a Wells Fargo Advantage Fund.

Investment Goal and Strategy Comparison

The following section compares the investment goals, principal investment strategies and fundamental investment policies of the Funds. The investment goals of the Funds may be changed without shareholder approval.

The Funds' investment goals and investment strategies are similar. Evergreen VA Core Bond Fund seeks to maximize total return through a combination of current income and capital growth. The Wells Fargo Advantage VT Total Return Bond Fund seeks total return, consisting of income and capital appreciation. Each Fund normally invests 80% of its assets in investment-grade debt securities. One difference between the Funds' investment strategies is that the Wells Fargo Advantage VT Total Return Bond Fund limits the amount it may invest in asset-backed securities other than mortgage-backed securities to 25% of its total assets, while the Evergreen VA Core Bond Fund has no such limit. This means the Evergreen VA Core Bond Fund may have a greater percentage of its assets invested in asset-backed securities. Furthermore, the Wells Fargo Advantage VT Total Return Bond Fund may invest up to 20% of its assets in U.S. dollar-denominated debt securities of foreign issuers, while investing in these securities is not principal investment strategy of Evergreen VA Core Bond Fund. This means that the Wells Fargo Advantage VT Total Return Bond Fund may invest in foreign securities to a greater extent than Evergreen VA Core Bond Fund.

Also, the Wells Fargo Advantage VT Total Return Bond Fund seeks to maintain its dollar-weighted average duration within a narrower range, 4 to 5½ years, than does Evergreen VA Core Bond Fund, 2 to 6 years. This means that the Wells Fargo Advantage VT Total Return Bond Fund's portfolio may be more sensitive to movements in prevailing interest rates that Evergreen VA Core Bond Fund's portfolio than under certain circumstances.

A more complete description of each Fund's investment goals and strategies is below.

EVERGREEN VA CORE BOND FUND (Target Fund) | WELLS FARGO ADVANTAGE VT TOTAL RETURN BOND FUND (Acquiring Fund) | ||||

INVESTMENT GOAL | |||||

The Fund seeks to maximize total return through a combination of current income and capital growth. | The Fund seeks total return, consisting of income and capital appreciation. | ||||

PRINCIPAL INVESTMENT STRATEGIES | |||||

The Fund normally invests at least 80% of its assets in U.S. dollar-denominated investment grade debt securities, including debt securities issued or guaranteed by the U.S. Government or by an agency or instrumentality of the U.S. government, corporate bonds, mortgage-backed securities (including collateralized mortgage obligations ("CMOs")), asset-backed securities, and other income producing securities. The Fund currently maintains a bias toward corporate and mortgage-backed securities. The Fund may invest a substantial portion of its assets (including a majority of its assets) in CMOs or other mortgage- or asset-backed securities. The remaining 20% of the Fund's assets may be represented by cash or invested in cash equivalents or shares of registered investment companies, including money market or fixed-income funds. | Under normal circumstances, we invest at least 80% of the Fund's net assets in bonds; at least 80% of the Fund's total assets in investment-grade debt securities; up to 25% of the Fund's total assets in asset-backed securities, other than mortgage-backed securities; and up to 20% of the Fund's total assets in U.S. dollar-denominated debt securities of foreign issuers. We invest principally in investment-grade debt securities, including U.S. Government obligations, corporate bonds and mortgage- and asset-backed securities. | ||||

Security ratings are determined at the time of investment based on ratings received by nationally recognized statistical ratings organizations or, if a security is not rated, it will be deemed to have the same rating as a security determined to be of comparable quality by the Fund's portfolio manager. If a security is rated by more than one nationally recognized statistical ratings organization, the highest rating is used. The Fund may retain any security whose rating has been downgraded after purchase if the Fund's portfolio manager considers the retention advisable. | The Fund invests in debt securities that it believes offer competitive returns and are undervalued, offering additional income and/or price appreciation potential, relative to other debt securities of similar credit quality and interest rate sensitivity. From time to time, the Fund may also invest in unrated bonds that it believes are comparable to investment-grade debt securities. | ||||

As part of its investment strategy, the Fund may engage in dollar roll transactions, which allow the Fund to sell a mortgage-backed security to a dealer and simultaneously contract to repurchase a security that is substantially similar in type, coupon and maturity, on a specified future date. Dollar roll transactions may create investment leverage. | As part of its investment strategy, the Fund may invest in stripped securities or enter into mortgage dollar rolls and reverse repurchase agreements, as well as invest in U.S. dollar-denominated debt securities of foreign issuers. | ||||

The Fund intends to limit its dollar-weighted average duration to a two-year minimum and a six-year maximum, while the dollar-weighted average maturity is expected to be longer than the dollar-weighted average duration. | Under normal circumstances, the Fund expects to maintain an overall dollar-weighted average effective duration range between 4 and 5 1/2 years. | ||||

The Fund may, but will not necessarily, use a variety of derivative instruments, such as futures contracts, options and swaps, including, for example, index futures, Treasury futures, Eurodollar futures, interest rate swap agreements, credit default swaps and total return swaps. The Fund typically uses derivatives as a substitute for taking a position in the underlying asset or basket of assets and/or as part of a strategy designed to reduce exposure to other risks, such as interest rate risk. | The Fund may also use futures, options or swap agreements, as well as other derivatives, to manage risk or to enhance return. | ||||

The Fund will consider selling a portfolio investment when a portfolio manager believes the issuer's investment fundamentals are beginning to deteriorate, when the investment no longer appears consistent with the portfolio manager's investment methodology, when the Fund must meet redemptions, in order to take advantage of more attractive investment opportunities, or for other investment reasons which a portfolio manager deems appropriate. | The Fund may sell a security that has achieved its desired return or if it believes the security or its sector has become overvalued. The Fund may also sell a security if a more attractive opportunity becomes available or if the security is no longer attractive due to its risk profile or as a result of changes in the overall market environment. The Fund may actively trade portfolio securities. | ||||

The Fund may, but will not necessarily, temporarily invest up to 100% of its assets in cash and/or high-quality money market instruments in response to adverse economic, political or market conditions. This strategy is inconsistent with the Fund's investment goal and principal investment strategies and, if employed, could result in a lower return and loss of market opportunity. | The Fund may hold some of its assets in cash or in money market instruments, including U.S. Government obligations, shares of other mutual funds and repurchase agreements, or make other short-term investments to either maintain liquidity or for short-term defensive purposes when the Fund believes it is in the best interests of the shareholders to do so. During these periods, the Fund may not achieve its objective. | ||||

Although the Funds have historically used different terminology and descriptions to describe their fundamental policies, the fundamental investment policies of the Target and Acquiring Funds are substantively similar. For a comparative chart of fundamental invesment policies, please see Exhibit B.

Principal Risk Comparison

Because the Evergreen funds and Wells Fargo Advantage Funds were unaffiliated fund families until recently, the Funds have historically used different terminology and descriptions to describe their principal risks. Nonetheless, due to the similarity of the Funds' investment strategies, the Funds are generally subject to similar types of risks. Listed below are the principal risks that apply to an investment in the Wells Fargo Advantage VT Total Return Bond Fund. A description of those risks can be found in the section of this prospectus/proxy statement entitled "Risk Descriptions." Although both Funds may be subject to the risks listed below, they may be subject to a particular risk to different degrees. For example, because investing in foreign issuers is not a part of the principal investment strategy for Evergreen VA Core Bond Fund, an investment in the Wells Fargo Advantage VT Total Return Bond Fund may be subject to foreign investment risk to a greater extent than an investment in Evergreen VA Core Bond Fund.

Principal Risks

Active Trading Risk

Counter-Party Risk

Debt Securities Risk

Derivatives Risk

Foreign Investment Risk

Issuer Risk

Leverage Risk

Liquidity Risk

Management Risk

Market Risk

Mortgage and Asset-Backed Securities Risk

Regulatory Risk

Stripped Securities Risk

U.S. Government Obligations Risk

A discussion of the principal risks associated with an investment in the Target Fund may be found in the Target Fund's prospectus. In addition, each Fund has other investment policies, practices and restrictions which, together with the Fund's related risks, are also set forth in the Fund's prospectus and SAI.

Fund Performance Comparison

The following bar charts and tables illustrate how the Fund's returns have varied from year to year and compare the each Fund's returns with those of one or more broad-based securities indexes. Past performance (before and after taxes) is not necessarily an indication of future results. Current month-end performance information is available for an Evergreen fund at evergreeninvestments.com and for a Wells Fargo Advantage Fund at www.wellsfargo.com/advantagefunds. The bar charts and tables do not reflect contract, policy, separate account or other charges assessed by participating insurance companies; if they did, returns would be lower than those shown.

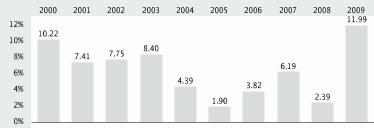

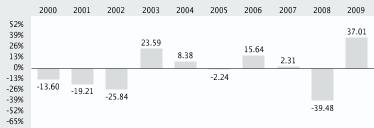

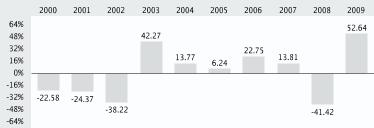

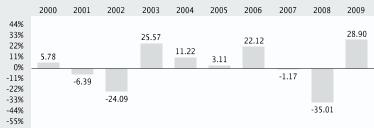

Year-by-Year Total Return for Class 2 Shares (%) for Evergreen VA Core Bond Fund

Highest Quarter: | 2nd Quarter 2009 | +6.84% |

Lowest Quarter: | 3rd Quarter 2008 | -9.76% |

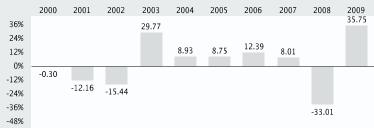

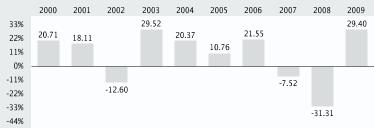

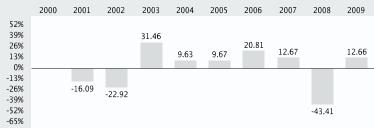

Year-by-Year Total Return (%) for Wells Fargo Advantage VT Total Return Bond Fund

Highest Quarter: | 3rd Quarter 2009 | +4.96% |

Lowest Quarter: | 2nd Quarter 2004 | -2.33% |

Average Annual Total Returns for the periods ended 12/31/2009 | ||||||||||

Evergreen VA Core Bond Fund | Inception Date of Share Class | 1 Year | 5 Year | Performance Since 7/31/2002 | ||||||

Class 2 | 7/31/2002 | 7.89% 7.89% | -0.68% -0.68% | 1.10% 1.10% | ||||||

Barclays Capital U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) | 5.93% 5.93% | 4.97% 4.97% | 5.16% 5.16% | |||||||

Average Annual Total Returns for the periods ended 12/31/2009 | ||||||||||

Wells Fargo Advantage VT Total Return Bond Fund | Inception Date of Share Class | 1 Year | 5 Year | 10 Year | ||||||

Single Class | 9/20/1999 | 11.99% 11.99% | 5.19% 5.19% | 6.40% 6.40% | ||||||

Barclays Capital U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) | 5.93% 5.93% | 4.97% 4.97% | 6.33% 6.33% | |||||||

| 1 | The Barclays Capital U.S. Aggregate Bond Index is composed of the Barclays Capital U.S. Government/Credit Index and the Barclays Capital U.S. Mortgage-Backed Securities Index, and includes Treasury issues, agency issues, corporate bond issues, and mortgage-backed securities. You cannot invest directly in an index. |

Shareholder Fee and Fund Expense Comparison

The expenses for each class of shares of your Target Fund may be different from those of the corresponding class of shares of the Acquiring Fund.

With respect to both the Target and Acquiring Funds, no sales charges are imposed on either purchases or sales of fund shares.

The following tables entitled "Annual Fund Operating Expenses" allow you to compare the annual operating expenses of the Funds. The total annual fund operating expenses (before and after waiver) for both the Target and the Acquiring Funds set forth in the following tables are based on the actual expenses for the twelve-month period ended September 30, 2009. The pro forma expense table shows you what the total annual fund operating expenses (before and after waiver) would have been for the Acquiring Fund for the twelve-month period ended September 30, 2009, assuming the Merger had taken place at the beginning of that period. Exhibit C contains expense tables and examples for both the Target and Acquiring Funds based upon the actual expenses incurred by such Funds during their most recently completed fiscal years. Exhibit C also includes pro forma expense tables and examples for the Acquiring Fund based on the date of the Acquiring Fund's most recent financial statements.

THE TABLES BELOW DO NOT REFLECT THE CHARGES AND FEES ASSESSED BY THE PARTICIPATING INSURANCE COMPANY UNDER YOUR CONTRACT OR POLICY. IF THESE CHARGES WERE REFLECTED, THE EXPENSES SHOWN BELOW WOULD BE HIGHER. PLEASE REFER TO THE PROSPECTUS FOR THE VARIABLE ANNUITY CONTRACT OR VARIABLE LIFE INSURANCE POLICY FOR INFORMATION REGARDING SUCH CHARGES.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

Evergreen VA Core Bond Fund | ||||

Total Annual Fund Operating Expenses1 | ||||

Class 2 | 1.02% 1.02% | |||

| 1 | The Total Annual Fund Operating Expenses in the table above include fees and expenses incurred indirectly by the Fund as a result of its investment in other investment companies. |

Wells Fargo Advantage VT Total Return Bond Fund | ||||||

Total Annual Fund Operating Expenses (Before Waiver)1 | Total Annual Fund Operating Expenses (After Waiver)2 | |||||

Single Class | 1.41% 1.41% | 0.90% 0.90% | ||||

| 1 | Expenses have been adjusted as necessary from amounts incurred during the Fund's most recent fiscal year to reflect current fees and expenses. |

| 2 | Funds Management has committed through 4/30/2011, to waive fees and/or reimburse expenses to the extent necessary to ensure that the Fund's Total Annual Fund Operating Expenses (After Waiver) excluding brokerage commissions, interest, taxes, extraordinary expenses, and the expenses of any money market fund or other fund held by the Fund do not exceed the Total Annual Fund Operating Expenses (After Waiver) shown. After this date, the Total Annual Fund Operating Expenses (After Waiver) may be increased only with the approval of the Board of Trustees. |

Wells Fargo Advantage VT Total Return Bond Fund (Pro Forma) | ||||||

Total Annual Fund Operating Expenses (Before Waiver) | Total Annual Fund Operating Expenses (After Waiver)1,2 | |||||

Class 2 | 1.15% 1.15% | 0.92% 0.92% | ||||

| 1 | The Total Annual Fund Operating Expenses (After Waiver) shown here include the expenses of any money market fund or other fund held by the Fund. |

| 2 | Funds Management has committed for three years after the closing of the Merger to waive fees and/or reimburse expenses to the extent necessary to ensure that the Fund's Total Annual Fund Operating Expenses (After Waiver) excluding brokerage commissions, interest, taxes, extraordinary expenses, and the expenses of any money market fund or other fund held by the Fund do not exceed 0.90% for Class 2. After this time, the Total Annual Fund Operating Expenses (After Waiver) may be increased only with the approval of the Board of Trustees. |

Evergreen VA Core Bond Fund and the Wells Fargo Advantage VT Total Return Bond Fund have each adopted a distribution plan pursuant to Rule 12b-1 under the 1940 Act (a "Distribution Plan"). The fees charged to Class 2 shares of each Fund under each Fund's Distribution Plan are the same, 0.25% of the Fund's average daily net assets.

Portfolio Turnover. The Target and Acquiring Funds pay transaction costs, such as commissions or dealer mark-ups, when each buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect each Fund's performance. During the most recent fiscal year, the Evergreen VA Core Bond Fund's portfolio turnover rate was 510% of the average value of its portfolio and the Wells Fargo Advantage VT Total Return Bond Fund's portfolio turnover rate was 580% of the average value of its portfolio.

Fund Management Information

The following table identifies the investment adviser, investment sub-adviser and portfolio manager(s) for the Acquiring Fund. Further information about the management of the Acquiring Fund can be found under the section entitled "Management of the Funds."

Acquiring Fund | ||

Investment Adviser | Funds Management Funds Management | |

Investment Sub-adviser | Wells Capital Management Incorporated Wells Capital Management Incorporated | |

Portfolio Managers | Troy Ludgood Thomas O'Connor, CFA | |

Tax Information

It is expected that the Merger will be tax-free to shareholders for U.S. federal income tax purposes, and receipt of an opinion substantially to that effect from Proskauer Rose LLP, special tax counsel to the Acquiring Fund, is a condition to the obligation of the Funds to consummate the Merger. This means that neither shareholders nor your Target or Acquiring Fund will recognize a gain or loss directly as a result of the Merger.

Certain other U.S. federal income tax consequences are discussed below under "Material U.S. Federal Income Tax Consequences of the Mergers."

EVERGREEN VA OMEGA FUND AND WELLS FARGO ADVANTAGE VT LARGE COMPANY GROWTH FUND INTO WELLS FARGO ADVANTAGE VT OMEGA GROWTH FUND

In addition to your Target Fund, shareholders in one or more other Target Funds are being asked to approve a Merger into your Acquiring Fund. Your Merger is not contingent upon approval of any other Merger by shareholders of any other Target Fund.

Share Class Information

The following table illustrates the share class of the Acquiring Fund that shareholders will receive as a result of the Merger in exchange for their shares in the Target Fund.

If you own this class of shares of Evergreen VA Omega Fund: | You will get this class of shares of Wells Fargo Advantage VT Omega Growth Fund1: | ||||

Class 1 | Class 1 | ||||

Class 2 | Class 2 |

| 1 | The Fund is a shell fund ("Shell Fund") being created to receive the assets of one or more Target Funds. |

If you own this class of shares of Wells Fargo Advantage VT Large Company Growth Fund: | You will get this class of shares of Wells Fargo Advantage VT Omega Growth Fund1: | ||||

Single Class | Class 2 |

| 1 | The Fund is a shell fund ("Shell Fund") being created to receive the assets of one or more Target Funds. |

The Acquiring Fund shares that shareholders receive as a result of the Merger will have the same total value as the total value of their Target Fund shares as of the close of business on the business day immediately prior to the Merger.

The procedures for buying, selling and exchanging shares of the Funds are similar. For additional information, see the section entitled "Buying, Selling and Exchanging Fund Shares." This section also contains important information for foreign shareholders of an Evergreen Target Fund, defined as shareholders whose accounts do not currently have both a U.S. address and taxpayer identification number on record with the Funds. Following the Merger, foreign shareholders will no longer be able to make additional investments into a Wells Fargo Advantage Fund.

Investment Goal and Strategy Comparison

The following section compares the investment goals, principal investment strategies and fundamental investment policies of the Funds. The investment goals of the Funds may be changed without shareholder approval.

Evergreen VA Omega Fund and Wells Fargo Advantage VT Omega Growth Fund. The Funds' investment goals and investment strategies are similar. Evergreen VA Omega Fund seeks long-term capital growth, while the Wells Fargo Advantage VT Omega Growth Fund seeks long-term capital appreciation. Evergreen VA Omega Fund invests its assets in the equity securities of companies of all market capitalizations, while the Wells Fargo Advantage VT Omega Growth Fund normally invests at least 80% of its assets in equity securities. Both Funds employ a growth style of investing. One difference is that the Wells Fargo Advantage VT Omega Growth Fund may invest up to 25% of its assets in equity securities of foreign issuers, while Evergreen VA Omega Fund does not invest in equity securities of foreign issuers as a part of its principal investment strategy. This means that the Wells Fargo Advantage VT Omega Growth Fund may invest in foreign securities to a greater extent than Evergreen VA Omega Fund.

A more complete description of each Fund's investment goals and strategies is below.

EVERGREEN VA OMEGA FUND (Target Fund) | WELLS FARGO ADVANTAGE VT OMEGA GROWTH FUND (Acquiring Fund) | ||||

INVESTMENT GOAL | |||||

The Fund seeks long-term capital growth. | The Fund seeks long-term capital appreciation. | ||||

PRINCIPAL INVESTMENT STRATEGIES | |||||

The Fund invests primarily, and under normal conditions substantially all of its assets, in common stocks of U.S. companies of any market capitalization. | Under normal circumstances, we invest at least 80% of the Fund's total assets in equity securities; and up to 25% of the Fund's total assets in equity securities of foreign issuers, including ADRs and similar investments. We invest principally in equity securities of companies of all market capitalizations. | ||||

The Fund's portfolio manager employs a growth style of equity management that seeks to emphasize companies with cash flow growth, sustainable competitive advantages, returns on invested capital above their cost of capital and the ability to manage for profitable growth that can create long-term value for shareholders. | The goal of the Fund's fundamental investment process is to identify the small number of high quality companies capable of sustaining above average, long-term cash flow growth and then to invest at a significant discount to its valuation estimate to create long-term value for investors. The Fund's strategy is focused on firms with a strong business franchise that, because of their structural advantages, are best-positioned to benefit from the secular growth trends in their industry. The Fund's investment process is forward looking. Because the Fund approaches research from the perspective of a potential owner, it focuses on future cash flows for measuring intrinsic value. Through fundamental, bottom-up analysis, the Fund forms distinct, company-specific insights. The Fund's disciplined scrutiny of upside potential and downside risk gives it the confidence to make long-term investments regardless of the short-term impact of business cycles. The Fund's portfolio is constructed company by company, based on the Fund's level of conviction. The Fund's portfolio typically has a low average turnover and typically holds 35-60 stocks. | ||||

The Fund may, but will not necessarily, use derivatives. | The Fund may use futures, options or swap agreements, as well as other derivatives, to manage risk or to enhance return. | ||||

A Fund will consider selling a portfolio investment when a portfolio manager believes the issuer's investment fundamentals are beginning to deteriorate, when the investment no longer appears consistent with the portfolio manager's investment methodology, when the Fund must meet redemptions, in order to take advantage of more attractive investment opportunities, or for other investment reasons which a portfolio manager deems appropriate. | The Fund's sell decisions are similarly driven by its long-term fundamental analysis. Always vigilant of the overall portfolio's risk-return profile, the Fund would also sell a stock if it found a more attractive candidate with a better margin of safety. | ||||

A Fund may, but will not necessarily, temporarily invest up to 100% of its assets in cash and/or high-quality money market instruments in response to adverse economic, political or market conditions. This strategy is inconsistent with the Fund's investment goal and principal investment strategies and, if employed, could result in a lower return and loss of market opportunity. | The Fund may hold some of its assets in cash or in money market instruments, including U.S.Government obligations, shares of other mutual funds and repurchase agreements, or make other short-term investments to either maintain liquidity or for short-term defensive purposes when the Fund believes it is in the best interests of the shareholders to do so. During these periods, the Fund may not achieve its objective. | ||||

Wells Fargo Advantage VT Large Company Growth Fund and Wells Fargo Advantage VT Omega Growth Fund. The Funds' investment goals are identical, and their investment strategies are similar. Each Fund seeks long-term capital appreciation. The Wells Fargo Advantage VT Large Company Growth Fund normally invests at least 80% of its net assets in the equity securities of large-capitalization companies, while the Wells Fargo Advantage VT Omega Growth Fund invests at least 80% of its total assets in equity securities of companies of all market capitalizations. This means that an investment in the Wells Fargo Advantage VT Omega Growth Fund may be more sensitive to the price fluctuation of securities of small and medium-cap companies. Another difference is that the Wells Fargo Advantage VT Omega Growth Fund may invest up to 25% of its assets [directly] in equity securities of foreign issuers, while the Wells Fargo Advantage VT Large Company Growth Fund may invest up to 20% of its assets in the equity securities of foreign issuers only through ADRs adn similar investments. This means that the Wells Fargo Advantage VT Omega Growth Fund may invest in the equity securities of foreign issuers to a greater extent than the Wells Fargo Advantage VT Large Company Growth Fund.

A more complete description of each Fund's investment goals and strategies is below.

WELLS FARGO ADVANTAGE VT LARGE COMPANY GROWTH FUND (Target Fund) | WELLS FARGO ADVANTAGE VT OMEGA GROWTH FUND (Acquiring Fund) | ||||

INVESTMENT GOAL | |||||

The Fund seeks long-term capital appreciation. | The Fund seeks long-term capital appreciation. | ||||

PRINCIPAL INVESTMENT STRATEGIES | |||||

Under normal circumstances, the Fund invests at least 80% of its net assets in equity securities of large-capitalization companies and up to 20% of its total assets in equity securities of foreign issuers through ADRs and similar investments. The Fund invest principally in equity securities, focusing on approximately 30 to 50 large capitalization companies that the Fund believes have favorable growth potential. However, the Fund normally does not invest more than 10% of its total assets in the securities of a single issuer. The Fund defines large-capitalization companies as those with market capitalizations of $3 billion or more. | Under normal circumstances, we invest at least 80% of the Fund's total assets in equity securities; and up to 25% of the Fund's total assets in equity securities of foreign issuers, including ADRs and similar investments. We invest principally in equity securities of companies of all market capitalizations. | ||||

In selecting securities for the Fund, the Fund seeks companies that it believes are able to sustain rapid earnings growth and high profitability over a long time horizon. The Fund seeks companies that have high quality fundamental characteristics, including: dominance in their niche or industry; low cost producers; low levels of leverage; potential for high and defensible returns on capital; and management and a culture committed to sustained growth. The Fund utilizes a bottom-up approach to identify companies that are growing sustainable earnings at least 50% faster than the average of the companies comprising the S&P 500 Index. | The goal of the Fund's fundamental investment process is to identify the small number of companies capable of sustaining above average, long-term cash flow growth and then to invest at a significant discount to its valuation estimate to create long-term value for investors. The Fund's strategy is focused on firms with a strong business franchise that, because of their structural advantages, are best-positioned to benefit from the secular growth trends in their industry. The Fund's investment process is forward looking. Because it approaches the research task from the perspective of a potential owner, the Fund focuses on future cash flows for measuring intrinsic value. Through a fundamental, bottom-up analysis, the Fund forms distinct, company-specific insights. A disciplined scrutiny of upside potential and downside risk gives the Fund the confidence to make long-term investments regardless of the short-term impact of business cycles. The Fund's portfolio is constructed company by company, based on its level of conviction. The Fund's portfolio typically has a low average turnover and typically holds 35-60 stocks. | ||||

Furthermore, the Fund may use futures, options or swap agreements, as well as other derivatives, to manage risk or to enhance return. | Furthermore, the Fund may use futures, options or swap agreements, as well as other derivatives, to manage risk or to enhance return. | ||||

The Fund may sell a holding if it believes the holding will no longer produce anticipated growth and profitability, or if the security is no longer favorably valued. | The Fund's sell decisions are similarly driven by its long-term fundamental analysis. Always vigilant of the overall portfolio's risk-return profile, the Fund would also sell a stock if it found a more attractive candidate with a better margin of safety. | ||||

The Fund may hold some of its assets in cash or in money market instruments, including U.S. Government obligations, shares of other mutual funds and repurchase agreements, or make other short-term investments to either maintain liquidity or for short-term defensive purposes when the Fund believes it is in the best interests of the shareholders to do so. During these periods, the Fund may not achieve its objective. | The Fund may hold some of its assets in cash or in money market instruments, including U.S.Government obligations, shares of other mutual funds and repurchase agreements, or make other short-term investments to either maintain liquidity or for short-term defensive purposes when the Fund believes it is in the best interests of the shareholders to do so. During these periods, the Fund may not achieve its objective. | ||||

Although the Funds have historically used different terminology and descriptions to describe their fundamental policies, the fundamental investment policies of the Target and Acquiring Funds are substantively similar. For a comparative chart of fundamental invesment policies, please see Exhibit B.

Principal Risk Comparison

Because the Evergreen funds and Wells Fargo Advantage Funds were unaffiliated fund families until recently, the Funds have historically used different terminology and descriptions to describe their principal risks. Nonetheless, due to the similarity of the Funds' investment strategies, the Funds are generally subject to similar types of risks. Listed below are the principal risks that apply to an investment in the Wells Fargo Advantage VT Omega Growth Fund. A description of those risks can be found in the section of this prospectus/proxy statement entitled "Risk Descriptions." Although each of the Funds may be subject to all or substantially all of the risks listed below, they may be subject to a particular risk to different degrees. For example, because Evergreen VA Omega Fund does not invest in equity securities of foreign issuers as part of its principal investment strategy, an investment in the Wells Fargo Advantage VT Omega Growth Fund may be subject to foreign investment risk to a greater extent than an investment in Evergreen VA Omega Fund.

Because the Wells Fargo Advantage VT Omega Growth Fund invests more of its assets in companies of all market capitalizations than the Wells Fargo Advantage VT Large Company Growth Fund, an investment in the Wells Fargo Advantage VT Omega Growth Fund may be subject to smaller company securities risk to a greater extent than an investment in the Wells Fargo Advantage VT Large Company Growth Fund. In addition, because the Wells Fargo Advantage VT Omega Growth Fund may invest more of its total assets in equity securities of foreign issuers than the Wells Fargo Advantage VT Large Company Growth Fund, an investment in the Wells Fargo Advantage VT Omega Growth Fund may be subject to foreign investment risk to a greater extent than an investment in the Wells Fargo Advantage VT Large Company Growth Fund.

Principal Risks

Counter-Party Risk

Derivatives Risk

Foreign Investment Risk

Growth Style Investment Risk

Issuer Risk

Leverage Risk

Liquidity Risk

Management Risk

Market Risk

Regulatory Risk

Smaller Company Securities Risk

A discussion of the principal risks associated with an investment in the Target Fund may be found in the Target Fund's prospectus. In addition, each Fund has other investment policies, practices and restrictions which, together with the Fund's related risks, are also set forth for the Target Fund in the Fund's prospectus and SAI and, for the Acquiring Fund, in this prospectus/proxy statement and the Merger SAI.

Fund Performance Comparison

The following bar charts and tables illustrate how the Target Funds' returns have varied from year to year and compare the Target Funds' returns with those of one or more broad-based securities indexes. Past performance (before and after taxes) is not necessarily an indication of future results. Current month-end performance information is available for an Evergreen fund at evergreeninvestments.com and for a Wells Fargo Advantage Fund at www.wellsfargo.com/advantagefunds. The bar chart and table do not reflect contract, policy, separate account or other charges assessed by participating insurance companies; if they did, returns would be lower than those shown. Since the Acquiring Fund is a Shell Fund, it has not yet commenced operations and therefore performance information for the Acquiring Fund is not yet available.

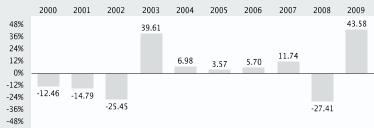

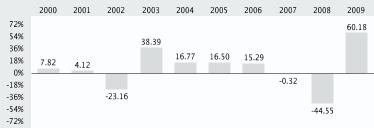

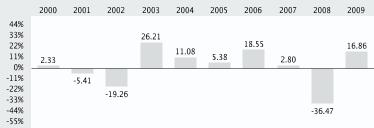

Year-by-Year Total Return for Class 2 Shares (%) for Evergreen VA Omega Fund

Highest Quarter: | 1st Quarter 2000 | +20.94%1 |

Lowest Quarter: | 4th Quarter 2000 | -25.00%1 |

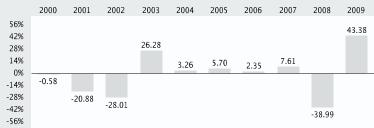

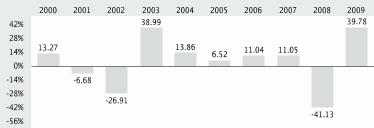

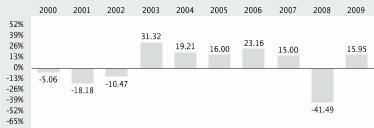

Year-by-Year Total Return (%) for Wells Fargo VT Large Company Growth Fund

Highest Quarter: | 4th Quarter 2001 | +18.25% |

Lowest Quarter: | 4th Quarter 2008 | -23.79% |

Average Annual Total Returns for the periods ended 12/31/20091 | ||||||||||

Evergreen VA Omega Fund | Inception Date of Share Class | 1 Year | 5 Year | 10 Year | ||||||

Class 1 | 3/6/1997 | 43.97% 43.97% | 5.26% 5.26% | 0.77% 0.77% | ||||||

Class 2 | 7/31/2002 | 43.58% 43.58% | 4.98% 4.98% | 0.57% 0.57% | ||||||

Russell 1000 Growth Index (reflects no deduction for fees, expenses, or taxes) | 37.21% 37.21% | 1.63% 1.63% | -3.99% -3.99% | |||||||

| 1 | Historical performance shown for Class 2 prior to its inception is based on the performance of Class 1, the original class offered. The historical returns for Class 2 have not been adjusted to reflect the effect of the class' 12b-1 fee. The fund incurs a 12b-1 fee of 0.25% for Class 2. Class 1 does not pay a 12b-1 fee. If the fee had been reflected, 10 year returns for Class 2 would have been lower. |

Average Annual Total Returns for the periods ended 12/31/2009 | ||||||||||

Wells Fargo Advantage VT Large Company Growth Fund | Inception Date of Share Class | 1 Year | 5 Year | 10 Year | ||||||

Single Class | 9/20/1999 | 43.38% 43.38% | 0.36% 0.36% | -2.81% -2.81% | ||||||

Russell 1000 Growth Index (reflects no deduction for fees, expenses, or taxes) | 37.21% 37.21% | 1.63% 1.63% | -3.99% -3.99% | |||||||

| 1 | The Russell 1000® Growth Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. You cannot invest directly in an index. |

Shareholder Fee and Fund Expense Comparison

The expenses for each class of shares of your Target Fund may be different from those of the corresponding class of shares of the Acquiring Fund.

With respect to both the Target and Acquiring Funds, no sales charges are imposed on either purchases or sales of fund shares.

The following tables entitled "Annual Fund Operating Expenses" allow you to compare the annual operating expenses of the Funds. The total annual fund operating expenses (before and after waiver) for the Target Fund set forth in the following table are based on the actual expenses for the twelve-month period ended September 30, 2009. The pro forma expense table shows you what the total annual fund operating expenses (before and after waiver) would have been for the Acquiring Fund for the twelve-month period ended September 30, 2009, assuming the Merger had taken place at the beginning of that period. If the Merger of Wells Fargo Advantage VT Large Company Growth Fund with the Acquiring Fund was the only Merger proposed, the pro forma expenses shown would have been approximately the same. The pro forma expense table below labeled "Wells Fargo Advantage VT Omega Growth Fund (Pro Forma Assuming Merger of Wells Fargo Advantage VT Large Company Growth Fund Only with Acquiring Fund)" shows you what the total annual fund operating expenses (before and after waiver) would have been for the Acquiring Fund for the twelve-month period ended September 30, 2009, assuming only the Merger of Wells Fargo Advantage VT Large Company Growth Fund with the Acquiring Fund had taken place at the beginning of that period. Exhibit C contains expense tables and examples for the Target Fund based upon the actual expenses incurred by the Target Fund during its most recently completed fiscal year. Exhibit C also includes a pro forma expense table and examples for the Acquiring Fund based on the date of the Target Funds' most recent financial statements. Since the Acquiring Fund has not yet commenced operations, the information presented is based on estimates.

THE TABLES BELOW DO NOT REFLECT THE CHARGES AND FEES ASSESSED BY THE PARTICIPATING INSURANCE COMPANY UNDER YOUR CONTRACT OR POLICY. IF THESE CHARGES WERE REFLECTED, THE EXPENSES SHOWN BELOW WOULD BE HIGHER. PLEASE REFER TO THE PROSPECTUS FOR THE VARIABLE ANNUITY CONTRACT OR VARIABLE LIFE INSURANCE POLICY FOR INFORMATION REGARDING SUCH CHARGES.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

Evergreen VA Omega Fund | ||||

Total Annual Fund Operating Expenses | ||||

Class 1 | 0.75% 0.75% | |||

Class 2 | 1.00% 1.00% | |||

Wells Fargo Advantage VT Large Company Growth Fund | ||||||

Total Annual Fund Operating Expenses (Before Waiver)1 | Total Annual Fund Operating Expenses (After Waiver)2 | |||||

Single Class | 1.20% 1.20% | 1.00% 1.00% | ||||

| 1 | Expenses have been adjusted as necessary from amounts incurred during the Fund's most recent fiscal year to reflect current fees and expenses. |

| 2 | Funds Management has committed through 4/30/2011, to waive fees and/or reimburse expenses to the extent necessary to ensure that the Fund's Total Annual Fund Operating Expenses (After Waiver) excluding brokerage commissions, interest, taxes, extraordinary expenses, and the expenses of any money market fund or other fund held by the Fund do not exceed the Total Annual Fund Operating Expenses (After Waiver) shown. After this date, the Total Annual Fund Operating Expenses (After Waiver) may be increased only with the approval of the Board of Trustees. |

Wells Fargo Advantage VT Omega Growth Fund (Pro Forma) | ||||||

Total Annual Fund Operating Expenses (Before Waiver) | Total Annual Fund Operating Expenses (After Waiver)1 | |||||

Class 1 | 0.80% 0.80% | 0.75% 0.75% | ||||

Class 2 | 1.05% 1.05% | 1.00% 1.00% | ||||

| 1 | Funds Management has committed for three years after the closing of the Merger to waive fees and/or reimburse expenses to the extent necessary to ensure that the Fund's Total Annual Fund Operating Expenses (After Waiver), excluding brokerage commissions, interest, taxes, extraordinary expenses, and the expenses of any money market fund or other fund held by the Fund, do not exceed the Total Annual Fund Operating Expenses (After Waiver) shown. After this time, the Total Annual Fund Operating Expenses (After Waiver) may be increased only with the approval of the Board of Trustees. |

Wells Fargo Advantage VT Omega Growth Fund (Pro Forma) | ||||||

Total Annual Fund Operating Expenses (Before Waiver) | Total Annual Fund Operating Expenses (After Waiver)1 | |||||

Class 2 | 1.12% 1.12% | 1.00% 1.00% | ||||

| 1 | Funds Management has committed for three years after the closing of the Merger to waive fees and/or reimburse expenses to the extent necessary to ensure that the Fund's Total Annual Fund Operating Expenses (After Waiver), excluding brokerage commissions, interest, taxes, extraordinary expenses, and the expenses of any money market fund or other fund held by the Fund, do not exceed the Total Annual Fund Operating Expenses (After Waiver) shown. After this time, the Total Annual Fund Operating Expenses (After Waiver) may be increased only with the approval of the Board of Trustees. |

Evergreen VA Omega Fund, the Wells Fargo Advantage VT Large Company Growth Fund, and the Wells Fargo Advantage VT Omega Growth Fund have each adopted a distribution plan pursuant to Rule 12b-1 under the 1940 Act (a "Distribution Plan"). The fees charged to Class 2 shares of Evergreen VA Omega Fund pursuant to the Fund's Distribution Plan are 0.25%. Class 1 shares of Evergreen VA Omega Fund do not pay a 12b-1 fee. The fees charged to Class 2 shares of the Wells Fargo Advantage VT Omega Growth Fund pursuant to the Fund's Distribution Plan are 0.25%. Class 1 shares of the Wells Fargo Advantage VT Omega Growth Fund do not pay a 12b-1 fee. The fees charged to the single class of shares of the Wells Fargo Advantage VT Large Company Growth Fund pursuant to the Fund's Distribution Plan are 0.25%.

Portfolio Turnover. The Target and Acquiring Funds pay transaction costs, such as commissions or dealer mark-ups, when each buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect each Fund's performance. During the most recent fiscal year, Evergreen VA Omega Fund's portfolio turnover rate was 28% of the average value of its portfolio and the Wells Fargo Advantage VT Large Company Growth Fund's portfolio turnover rate was 27% of the average value of its portfolio. Since the Acquiring Fund has yet to commence operations, its portfolio turnover rate is not yet available.

Fund Management Information

The following table identifies the investment adviser, investment sub-adviser and portfolio manager(s) for the Acquiring Fund. Further information about the management of the Acquiring Fund can be found under the section entitled "Management of the Funds."

Acquiring Fund | ||

Investment Adviser | Funds Management Funds Management | |

Investment Sub-adviser | Wells Capital Management Incorporated Wells Capital Management Incorporated | |

Portfolio Manager | Aziz Hamzaogullari Aziz Hamzaogullari | |

Tax Information

It is expected that the Merger will be tax-free to shareholders for U.S. federal income tax purposes, and receipt of an opinion substantially to that effect from Proskauer Rose LLP, special tax counsel to the Acquiring Fund, is a condition to the obligation of the Funds to consummate the Merger. This means that neither shareholders nor your Target or Acquiring Fund will recognize a gain or loss directly as a result of the Merger.

Certain other U.S. federal income tax consequences are discussed below under "Material U.S. Federal Income Tax Consequences of the Mergers."

EVERGREEN VA FUNDAMENTAL LARGE CAP FUND AND WELLS FARGO ADVANTAGE VT LARGE COMPANY CORE FUND INTO WELLS FARGO ADVANTAGE VT CORE EQUITY FUND

In addition to your Target Fund, shareholders in one or more other Target Funds are being asked to approve a Merger into your Acquiring Fund. Your Merger is not contingent upon approval of any other Merger by shareholders of any other Target Fund.

Share Class Information

The following table illustrates the share class of the Acquiring Fund that shareholders will receive as a result of the Merger in exchange for their shares in the Target Fund.

If you own this class of shares of Evergreen VA Fundamental Large Cap Fund: | You will get this class of shares of Wells Fargo Advantage VT Core Equity Fund1: | ||||

Class 1 | Class 1 | ||||

Class 2 | Class 2 |

| 1 | The Fund is a shell fund ("Shell Fund") being created to receive the assets of one or more Target Funds. |

If you own this class of shares of Wells Fargo Advantage VT Large Company Core Fund: | You will get this class of shares of Wells Fargo Advantage VT Core Equity Fund1: | ||||

Single Class | Class 2 |

| 1 | The Fund is a shell fund ("Shell Fund") being created to receive the assets of one or more Target Funds. |

The Acquiring Fund shares that shareholders receive as a result of the Merger will have the same total value as the total value of their Target Fund shares as of the close of business on the business day immediately prior to the Merger.

The procedures for buying, selling and exchanging shares of the Funds are similar. For additional information, see the section entitled "Buying, Selling and Exchanging Fund Shares." This section also contains important information for foreign shareholders of an Evergreen Target Fund, defined as shareholders whose accounts do not currently have both a U.S. address and taxpayer identification number on record with the Funds. Following the Merger, foreign shareholders will no longer be able to make additional investments into a Wells Fargo Advantage Fund.

Investment Goal and Strategy Comparison

The following section compares the investment goals, principal investment strategies and fundamental investment policies of the Funds. The investment goals of the Funds may be changed without shareholder approval.

Evergreen VA Fundamental Large Cap Fund and Wells Fargo Advantage VT Core Equity Fund. Although the investment goals of the Funds have different focal points, with Evergreen VA Fundamental Large Cap Fund seeking capital growth with the potential for current income, and the Wells Fargo Advantage VT Core Equity Fund seeking long-term capital appreciation, the principal investment strategies of the Funds are similar. Each Fund normally invests at least 80% of its assets in large-capitalization companies and may invest up to 20% in the securities of foreign issuers. One difference is that Evergreen VA Fundamental Large Cap Fund may invest up to 20% of its assets in below investment grade bonds and convertible preferred stocks of any quality, while investing in below investment grade bonds or in convertible preferred stocks are not part of the principal investment strategies of the Wells Fargo Advantage VT Core Equity Fund.

A more complete description of each Fund's investment goals and strategies is below.

EVERGREEN VA FUNDAMENTAL LARGE CAP FUND (Target Fund) | WELLS FARGO ADVANTAGE VT CORE EQUITY FUND (Acquiring Fund) | ||||