UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT

TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the 2006 Annual Report for the year ended April 30, 2006

Commission File Number: 333-10100

ALIMENTATION COUCHE-TARD INC.

1600 St-Martin Boulevard East

Tower B, Suite 200

Laval, Quebec, Canada

H7G 4S7

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40 F.

Form 20-F |_| Form 40-F |X|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes |_| No |X|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes |_| No |X|

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g-3 under the Securities Exchange Act of 1934.

Yes |_| No |X|

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b):

SIGNATURES:

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| ALIMENTATION COUCHE-TARD INC. | |

| July 14, 2006 | |

| Per: /s/ Sylvain Aubry | |

| Sylvain Aubry | |

| Corporate Secretary |

| |

| 2006 ANNUAL REPORT |

The little

corner store

is getting

bigger…

| Contents | |

| Highlights | 2 |

| Message to Shareholders | 6 |

| Human Potential | 12 |

| Brand Potential | 16 |

| Growth Potential | 18 |

| Helping People | 22 |

| Report on Operations | 26 |

| Teams | 31 |

| Financial Review | 32 |

| Management Discussion and Analysis | |

| Financial Statements | |

| Notes to Financial Statements | |

| Directors and Officers |

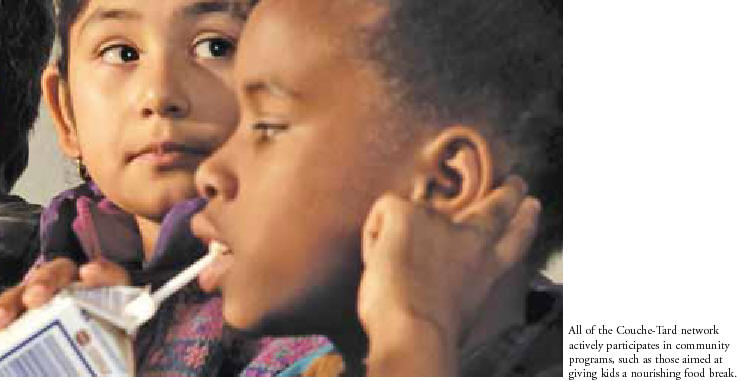

The first Couche-Tard acquisition 21 years ago was 11 corner stores in Quebec City, just like the one pictured on the cover. Today’s Couche-Tard store, such as the one here, is a multi-service convenience centre aimed at making life easier for millions of customers every day.

and bigger.

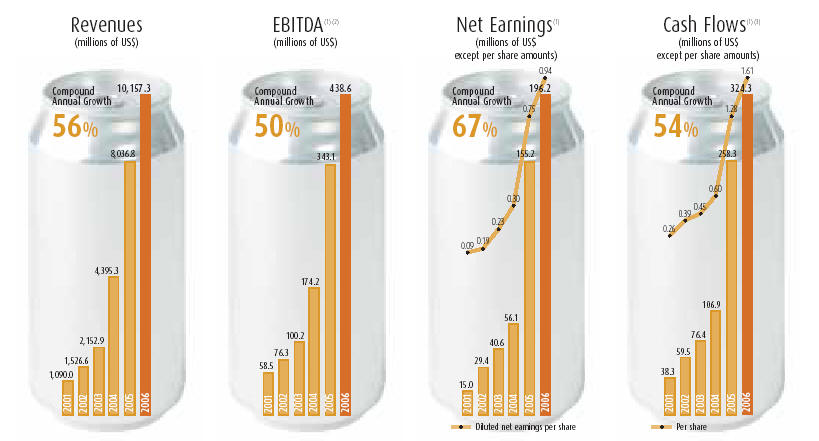

$10 billion

in revenues (US$)37,000

motivated staff members5,000

stores within the network3

powerful brands1

goal: fulfill our growth potential

Highlights

• Increase of 26.4% in revenues since last year

• Increase of 26.4% in net earnings

• Implementation of IMPACT program at 446 stores

• Increase of 151 corporate stores

2 / Alimentation Couche-Tard

Financial Highlights

(in millions of US dollars, except per share amounts)

2006(1) | 2005 | 2004(2) | 2003(2) | 2002(2) | 2001(2) | |

$ | $ | $ | $ | $ | $ | |

|

|

|

|

|

| |

| Consolidated Results |

|

|

|

|

|

|

Revenues | 10,157.3 | 8,036.8 | 4,395.3 | 2,152.9 | 1,526.6 | 1,090.0 |

EBITDA(3) | 438.6 | 343.1 | 174.2 | 100.2 | 76.3 | 58.5 |

Net earnings | 196.2 | 155.2 | 56.1 | 40.6 | 29.4 | 15.0 |

Cash flows(4) | 324.3 | 258.3 | 106.9 | 76.4 | 59.5 | 38.3 |

| Per Share |

|

|

|

|

|

|

Net Earnings |

|

|

|

|

|

|

Basic | 0.97 | 0.77 | 0.31 | 0.24 | 0.19 | 0.10 |

Diluted | 0.94 | 0.75 | 0.30 | 0.23 | 0.19 | 0.09 |

Cash flows(4) | 1.61 | 1.28 | 0.60 | 0.45 | 0.39 | 0.26 |

Book value | 4.78 | 3.63 | 2.71 | 1.74 | 1.40 | 0.94 |

| Financial Position |

|

|

|

|

|

|

Total assets | 2,369.2 | 1,995.7 | 1,650.8 | 739.7 | 499.5 | 358.5 |

Property and equipment | 1,014.1 | 812.0 | 663.3 | 298.5 | 195.7 | 131.4 |

Interest-bearing debt | 524.1 | 530.9 | 536.8 | 204.6 | 115.7 | 96.6 |

Shareholders’ equity | 966.0 | 733.2 | 535.0 | 293.9 | 231.3 | 139.7 |

| Ratios |

|

|

|

|

|

|

Interest-bearing net debt/ |

|

|

|

|

|

|

total capitalization | 0.17:1 | 0.28:1 | 0.42:1 | 0.37:1 | 0.31:1 | 0.40:1 |

Interest-bearing net debt/ |

|

|

|

|

|

|

EBITDA(3) | 0.44:1 | 0.81:1 | 2.20:1 | 1.71:1 | 1.32:1 | 1.54:1 |

|

|

|

|

|

|

(1) 53 weeks.

(2) Restated.

(3) EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) is presented for information purposes only and represents a performance measure used especially in financial circles.It does not have a standardized meaning prescribed by Canadian GAAP and therefore may not be comparable to similar measures presented by other public companies.

(4) These cash flows and cash flows per share are presented for information purposes only and represent performance measures used especially in financial cir-cles.They represent cash flows from net earnings, plus depreciation and amortization, write-off of financing costs, loss on disposal of assets and future income taxes.They do not have a standardized meaning prescribed by Canadian GAAP and therefore may not be comparable to similar measures presented by other public companies.

Alimentation Couche-Tard / 3

(1) Restated figures for 2001 to 2004.

(2) EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) is presented for information purposes only and represents a performance measure used especially in financial circles.It does not have a standardized meaning prescribed by Canadian GAAP and therefore may not be comparable to similar measures presented by other public companies.

(3) These cash flows and cash flows per share are presented for information purposes only and represent performance measures used especially in financial circles. They represent cash flows from net earnings, plus depreciation and amortization, write-off of financing costs, loss on disposal of assets and future income taxes. They do not have a standardized meaning prescribed by Canadian GAAP and therefore may not be comparable to similar measures presented by other public companies.

4 / Alimentation Couche-Tard

Stock Performance

Couche-Tard’s strong stock performance has outpaced the TSX index and consistently delivered outstanding shareholder value.

Over the past fiscal year the stock appreciated 51% and the average return over five years is 37%.

Alimentation Couche-Tard / 5

GREAT RESULTS

Unlimited Potential

Fiscal 2006 was the most successful year yet in our 25-year history and brought Couche-Tard to a new level of maturity and capability. Its value is not just in the year’s accomplishments but in our excellent positioning for the future.

6 / Alimentation Couche-Tard

This year’s Annual Report presents a closer look at our strategy and identifies our strengths for moving forward.

A year ago, I wrote that we could claim to have successfully integrated the Circle K network. The mood then was one of accomplishment. Twelve months later, as both our strategies and execution perform to, and often exceed, high expectations, we are developing a greater sense of just how open-ended our future can be. And the mood is one of excitement!

As we move through the second 25 years of our journey we have, I believe, arrived at a new maturity as an enterprise.

The numbers being generated continue to set a record pace that now stretches back 12 years. At the end of the latest fiscal year, our five-year Compound Annual Growth Rate for revenues stood at 56% and for net earnings 67%. We remain the most profitable publicly held convenience store operator in North America not integrated with a petroleum company.

|

|

Alimentation Couche-Tard / 7

| Flavours for top-selling frozen drink Sloche, which appeals to a young crowd, include Tropical Cheddar and Winchire Wacheur.

|

| Three times, Couche-Tard has doubled its size by acquisition. Each time means a bigger bite and a tougher challenge. |

Our network continues to grow and we have added 633 stores since the big Circle K acquisition of December 2003 to complete the year at 5,097, including binding agreements.

We continue to build our financial muscle, with shareholders’ equity now close to one billion dollars US.

Although history shows us that two-thirds of merger and acquisition strategies actually diminish shareholder value, we are an established member of that other third. Our growth model has demonstrated robust and sustainable value creation: our share price has appreciated 114% in the past two years and average return over the past five years is 37%. Market capitalization since 2003 has more than tripled to Cdn$5 billion.

The Board of Directors approved a policy for a quarterly dividend of Cdn$0.025 per share, effective since the second quarter. Our cash flow makes it appropriate to share some of the benefits of our growth with shareholders.The addition of a dividend also qualifies us for investment by a wider range of investors.

On its own, this is an inspiring picture. Taken in context with the Company’s strong and consistent performance over and extended period, it is also a key inflection point. I see it as an important transition into a high-return North American business model with sustainable and internally financed organic and acquisition growth. equity

Three times, Couche-Tard has doubled its size by acquisition. Each time means a bigger bite and a tougher challenge. When the third opportunity – Circle K – meant integrating and managing 1,663 corporate stores in one go, people questioned our ability to realize the promised efficiencies and unlock the value that we were seeking.

After carefully analyzing two complete years of data with improved tools, we are fully satisfied not just with this integration, but with the effectiveness of our business model on this much grander scale. This was a tough test of our benchmarking processes, our supply and distribution logistics and our highly decentralized supervisory structure. By any business performance measurement, I am delighted to report that we passed with flying colours. Couche-Tard consistently outperforms the industry overall. This has convincingly demonstrated the power and scalability of the highly decentralized, consumer-centred structure that is uniquely ours. But, as the fine print always says, past achievement is no guarantee of future performance. The intent, therefore, of this year’s Annual Report is to present a closer look at the main elements of our strategy and identify our strengths for moving forward.

8 / Alimentation Couche-Tard

First, as they say, you have to fish where the fish are. Where is the industry going? Will it continue to remain a source of strong growth?

Only a decade ago, it was fashionable to say that convenience stores were a thing of the past. Today, the industry is undergoing a growth spurt and is teeming with opportunity. In 2004, North American c-store sales grew over 16%, for the second year in a row – significantly faster than any other major retail channel. Total store count increased almost 6%.

THE INDUSTRY IS NOT ONLY EXPANDING, BUT EVOLVING

We can no longer assume a pricing premium for convenience. Contemporary society is developing in a time-constrained environment where convenience has become a service staple.

Big supermarkets, drugstores and mass merchandisers now play the convenience game with products available sometimes 24 hours a day. Giant retailers in other sectors become our competitors with their gas fill-up service and mini-marts in a bid to build store traffic.

This does not stress our operating model. In fact, it leads to more opportunity. Convenience stores are one of the most fragmented of industry sectors with small independents, heavily reliant on motor fuel sales, representing 60% of the market. Facing more competition and the added threat of continuing high gasoline pricing, many smaller chains and family owners will consider selling as an option. In the segment of most interest to us, that of chains between 10 and 100 outlets, there are no fewer than 21,000 stores.

Alimentation Couche-Tard / 9

Convenience stores are a volume-driven business that depends for profitability on economies of scale and store-level execution. This tends to result in standardization, but even with a winning network model, a cookie-cutter approach has a built-in ceiling. A convenience store is a neighbourhood store and neighbourhoods change. Tastes and product preferences differ as you move across the continent, meaning that a hierarchical structure that standardizes inventories and merchandise display can only be optimal in one region.

By contrast, the Couche-Tard model is boundaryless. We research and analyze the market for each individual store and then respond to those local needs and preferences. We do this by pushing out the decision-making, investing in the latest technology, continually upgrading our premises and hiring and retaining truly outstanding people.

The result, we feel, is unlimited potential for growth, for the development of our brands and for our people. All three are vital components in our ongoing value creation and you will read more about them in this year’s report.

- Our financial strength increases each year and growth expectations remain high, both for internal growth and for further acquisitions. We are continually reviewing quality opportunities and we can afford to be selective.

- Our brands continue to build valuable equity. During the past year, we completed the rebranding of all our corporate assets in the United States to the Circle K brand, which has a powerful consumer association. So we now have Couche-Tard in Eastern Canada, Mac’s through Central and Western Canada and Circle K throughout the U.S. A priority task for us is to build the customer’s loyalty to these brands and to further differentiate our stores in every region. We will be the destination where consumers will find ambience, quick and friendly service, proprietary products and a quick and nutritious breakfast or lunch.

- Most important of all is giving our people the opportunity to grow and excel. No industry is more driven by the people in the front lines than convenience stores. There are no big corporate contracts here; the year’s revenue is made one customer at a time. And success comes from efficiency, friendliness, an report. instinctive desire to serve and help, innovation, and the kind of will to succeed that is seen in the mirror every morning.

10 / Alimentation Couche-Tard

New hit energy drinks are sold in Couche-Tard, Mac’s and Circle K stores.

|

|

We are here to serve the store managers and we can do that best by meeting them at their place of work and getting to know their issues. |

People are without question the most important element and the greatest strength of our network. They are the first thing we look for in an acquisition opportunity; the quality people at Couche-Tard are hugely responsible for the stunning success since the acquisition of Circle K. I am proud that our beliefs, values and hard work are creating the best team in retailing.

There are two activities in particular which I enjoy. The first is being out in the stores, feeling the pulse of the Company, meeting the truly outstanding people who are managing these stores and serving our customers with flair and imagination. I spend almost half of my time on the road, as do other members of the executive group. Our corporate leadership philosophy is that we are here to serve the store managers and we can do that best by meeting them at their place of work and getting to know their issues.

The second is seeing first-hand the rollout of our IMPACT store program, which is new to the industry and a powerful business generator. As with our people, this configuration – which we have been refining over several years and which we will introduce throughout the entire network – is proving itself a winner in all of our eight markets.

In terms of both people and facilities, I feel that this year our company found a new sense of self. I view it as the most important year to date in our 25-year history. After convincingly mastering our toughest organizational challenge ever – the integration of Circle K – we find ourselves at a new level of capability and confidence, primed and ready to sustain our powerful growth.

On behalf of all my colleagues, I wish to thank our shareholders for their continued support, our Board of Directors for their wise and considered counsel - notably Josée Goulet, who is leaving after six years of precious collaboration - our business partners and our managers and employees throughout the network.

![]()

Alain Bouchard

Chairman of the Board,

President and Chief Executive Officer

Alimentation Couche-Tard / 11

Unlimited

HUMAN POTENTIAL

THE COMPANY BUILDS ON THE STRENGTH OF PEOPLE

The two most important people in Couche-Tard’s business face each other every day. On one side of the counter is the customer; on the other, the store manager or employee.

“Convenience store retailing is a people business,” says CEO Alain Bouchard. “I tell our people the only person more important than them is the customer.”

He gets to tell a lot of people. A feature of the Company’s operating methodology is the time spent by senior management in the field. In F’06, the Chief Executive and Chief Operating Officers each spent almost 50% of their time visiting stores. Two North American Division managers, each responsible for four divisions spend by far the greatest amount of their time on the road.

12 / Alimentation Couche-Tard

A very flat operating structure keeps management close to the action.

| |||

| “I am only in the office maybe one day a week,” says Stéphane Gonthier, Senior Vice-President, Eastern North America. “There’s nothing in my desk drawers.” The Company from the beginning has an empowerment-oriented structure. Starting with our corporate stores, every management level is given a high degree of decision-making power. Two results come from this: first, most in-store decisions are taken locally to meet local opportunities, and second, management believes that people perform to a higher standard when given responsibility and a clear career path. |

| “The spirit of what Couche-Tard stands for is to put the right people in the right job and set the boundaries,” says Brian Hannasch , Senior Vice-President, Western North America. “Then give them room to do their job.” The process of empowerment is embedded in an enterprise-wide succession plan. For every manager, an individual is identified as that person’s likely successor and is trained into the job. The process can take a few years, involving just on-site and job-specific training, or it could require sending the person to college. |

Alimentation Couche-Tard / 13

Froster hits the same audience for Mac’s as Sloche does for Couche-Tard.

|

|

The performance of the stores is way above average. |

The Company’s eight business units each maintain a “school” or training facility for its corporate stores. Every store manager in the system undergoes in-school training for 7-10 days. This is followed up with regular shorter courses on technology, aspects of management or topical issues.

Employee input and training is built into the IMPACT store conversion program which will ultimately upgrade every corporate store in the network (read more on page 26). Before the conversion, the manager and staff are fully consulted on the planned changes and their input is sought. Staff follow in-depth training in customer service and needs.

The value that Couche-Tard places in its human assets became a touch point in the Circle K acquisition. Senior management insisted on personally visiting 25% of the outlets being acquired – some 400 stores – even though it would mean re-drawing deadlines and threatened to scuttle the deal.

“It turned out that the performance of the stores was way above average and the people were outstanding”, says Réal Plourde, Chief Operating Officer. “But we were prepared to end the talks if we were not able to do that evaluation. The people closest to the customer are absolutely key in this business.”

14 / Alimentation Couche-Tard

Two years later, the great majority of former Circle K employees are still in place and many have moved to more senior positions. Couche-Tard outperforms the industry average in many forms of measurement. A key area in which we are the industry leader is employee turnover – a reflection of both hiring effectiveness and good employee relations. “I think a lot of our success is due to empowering people,” says Plourde. “Each store manager is considered an owner of that store and he or she makes many decisions on their own without having to ask some superior. They really appreciate that, and the results back up the method.”

Both hiring effectiveness

|  |

Unlimited

BRAND POTENTIAL

PUTTING A FACE ON CONVENIENCE

Customer loyalty changes the game from convenience store to destination of choice. The Company is rapidly building three consistent brands in the marketplace.

Once upon a time, it didn’t matter whose name was over the doorway. It was the convenience store on the corner where you went when you ran out of basics. Because there was little or no barrier to entry, convenience stores have become the most proliferated form of retailing in North America – approximately 140,000 stores, more than three times the number of grocery stores.

But times change. As we live in an increasingly time-constrained world, every consumer wants convenience and every vendor wants to provide it. Companies across the retail spectrum are adding on services frequently outside of their core business – such as gasoline bars, ATMs and food service counters – as a means of attracting the customer by simplifying his or her day. The result is rapidly rising competitive pressure which prompts Couche-Tard to innovate more and more.

16 / Alimentation Couche-Tard

Creating loyalty requires knowing the customer’s expectations and then being able to meet them consistently.

The Company is set on making the customer experience so distinctive, so pleasant and rewarding, that the store becomes a destination of choice. |

The arrival of big, branded competitors might seem a serious threat to a convenience store operator. Unless he was already building his own brand.

“I want people to go to a Couche-Tard, Mac’s or a Circle K,” says CEO Alain Bouchard. “Not just to a convenience store. I am a big believer in evolution and I think we are at a stage where consumers will support a store that responds to their needs.”

The Company is set on making the customer experience so distinctive, so pleasant and rewarding, that the store becomes a destination of choice, not only of convenience. Capturing the customer’s loyalty means building and differentiating each of the Company’s three mega-brands – creating an identity that the consumer empathizes with and trusts.

For Couche-Tard, this relationship building is well documented. In Arizona, where the Circle K brand has been around for 50 years, customer loyalty is extraordinarily high.

“Every research survey we do will show some customers started shopping with Circle K when they were kids,” says Brian Hannasch, Senior Vice-President, Western North America. “And they are still shopping with us now –we’ve been able to grow with them and meet their expectations as they age.”

There are also indications that consumers in the Arizona markets will make purchases at multiple Circle K stores in the course of the day. They stop for gas and a coffee on the way to work, grab a sandwich at lunchtime and then stop on the way home to pick up something they need for dinner.

Creating loyalty doesn’t have to take 50 years but it does require knowing the customer’s expectations and then being able to meet them consistently. Couche-Tard is already a leader in this field through a system of benchmarking that shares best practices throughout the store network. It is also among the early leaders in deploying new technology for gathering and analyzing customer data.

In F’06, the Company completed the installation of point-of-sale scanning equipment in every store, data that greatly enhances purchasing, inventory turns and profit margins. With the addition of Business Intelligence software, product mix can be optimized, buying intentions identified and displays modified, if necessary by the hour, to capitalize on time-of-day purchasing patterns.

Customers are also drawn by specific products and brands. The Company uses in-store branding strate- loyalty means building gies, including proprietary and national brands, to three differentiate its offerings, especially fresh food, from other convenience stores, build customer loyalty and promote return shopping.

It markets its own brand in frozen drinks, sandwiches, freshly brewed coffee, milk, gasoline and financial services among a total of over 25 private or licensed brands. These include La Maisonnée fresh sandwiches and breakfast selections; Sunshine Joe coffee; Sloche, Froster, Thirst Buster and The Frozen Zone brands of beverages; new Énergie and Joker energy drinks; Lawson’s Milk; ATM’s; long distance calling cards and gift cards.

The Company also continues to build on existing partnerships with national coffee brand names such as Van Houtte, Millstone and Seattle’s Best Coffees.

Couche-Tard has branded and proprietary Quick Service Restaurants in almost 300 stores. Branded partners include Subway, Dunkin’ Donuts, Blimpie, M&M, Noble Roman’s and Quiznos.

Alimentation Couche-Tard / 17

Unlimited

GROWTH POTENTIAL

BUSINESS WITHOUT BOUNDARIES

The outlook is excellent for further growth. We have the strongest balance sheet in the industry, probably the best operating model and conditions are fertile for small and medium sized acquisitions.

Couche-Tard’s objective is to be the largest and most profitable convenience store operator in North America. In nine major deals to date, it has laid down a strong track record in the acquisition and integration of competitor stores and chains.

Acquisition is responsible for the major part of Couche-Tard’s expansion. The last major deal, the December 2003 purchase of the Circle K network, bolted on another 2,290 corporate and affiliated stores and vaulted it into the industry top tier in North America: third in total stores, second among independent chains (not integrated with an petroleum company) and first in profitability as a publicly traded company within our business sector. Since Circle K, the Company has added a further 633 corporate and affiliated stores including binding agreements.

18 / Alimentation Couche-Tard

Couche-Tard has built a reputation a shrewd acquirer and excellent integrator.

Couche-Tard has built a reputation as a shrewd acquirer and excellent integrator. Each deal creates strong revenue growth, margin improvement and significant savings through synergies.

“Our expectations with Circle K have been exceeded,” says Richard Fortin, Executive Vice-President and Chief Financial Officer. “It was the biggest deal we have made and it’s been the biggest success we have had.”

Two core strategies underpin Couche-Tard’s success in growing its network. The first is a financial strategy that has built credibility and strength. The second is an operating model that removes the boundaries limiting a fundamentally local business.

“Our financial model has been the same since the start – conservative,” says Fortin, “We don’t play the leverage game, seldom go above 50% debt, and do not take on a project unless we are confident of a 25% return on capital.”

The Company has a record of acquiring assets at very attractive prices. It will monetize acquired properties rapidly to reimburse lenders and put cash where it prefers to see it – in operating improvements. Promptly following the Circle K signing, it entered into a sale-leaseback of 322 properties for nearly US$253 million. Altogether, US$329 million was reimbursed to the banks within the first six months.

Couche-Tard’s net debt to total capitalization at the end of F’06 was at an all-time low of 17%, giving it the capacity to fund a US$1.5 billion acquisition without resorting to equity. That could be the next 2,000 U.S. stores.

|

|

Alimentation Couche-Tard / 19

| With our business structure, where you can adapt yourself to the community, you can have a store anywhere in North America. |

“Conditions are excellent for further growth,” maintains Fortin. “We have the strongest balance sheet in the industry and probably the most successful operating model, and conditions are fertile for small and medium-sized acquisitions.”

The most important characteristic of Couche-Tard’s growth philosophy is the scalability of its business model. At one end of a very flat, decentralized business structure, stores successfully adapt to meet localized customer preferences. At the other end, network growth is virtually open-ended with all but the highest level of general and administrative functions parceled out on a regional basis.

The leaders of each of the eight business units function like a CEO. They benefit from network strengths such as knowledge-sharing, technology, purchasing leverage and financial stability. At a regional level, they can respond rapidly to market changes and fine-tune merchandising and in-store layouts to meet regional or local taste –fundamental to the convenience store business.

“You can’t be everywhere with only one standardized approach,” points out Fortin. “But with our business structure, where you can adapt yourself to the community, you can have a store anywhere in North America.”

With the North American industry rapidly consolidating and U.S. real estate prices escalating, only a handful of large acquisition opportunities remain both desirable and doable. In the meantime, Couche-Tard’s network is quietly growing year-round. Development teams in each of the eight divisions are mandated to seek out and qualify acquisition opportunities from single stores up to 100 and decisions in the low ranges are taken at the regional level.

In F’06 the Company added 151 new corporate stores.

20 / Alimentation Couche-Tard

A Growing Network

Alimentation Couche-Tard / 21

HELPING PEOPLE

Weather the Storm

Couche-Tard’s business is all in the when times get tough. Each year the Company donates millions of dollars to aid others. But the past year witnessed a remarkable effort as staff, customers and suppliers rallied to help those caught in the devastation of Hurricane Katrina.

KATRINA

| In-store fund raising and company donations raised more than US$1million for Katrina relief.

|

Back in 2004, the first year after acquiring the Circle K stores, Couche-Tard was welcomed to the U.S. Sunbelt by the most crippling storms to hit Florida in 40 years. The onsite teams showed their commitment to helping their neighbours and large donations were organized on behalf of the Florida Hurricane Relief Fund.

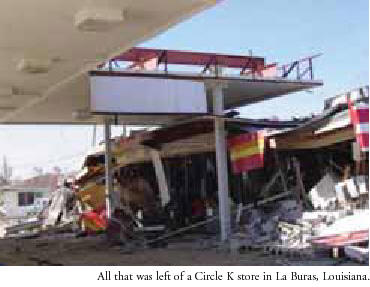

Then one year later, Hurricanes Katrina and Wilma displaced hundreds of thousands in the Gulf Coast region and caused devastation on a scale not seen since the 1906 San Francisco earthquake. Over 160 store sites were affected, 14 of them a total loss.

Employees in the region responded with two relief campaigns totaling well over half a million dollars US. One campaign was directed to their fellow employees in distress and the second to others suffering from the disasters. Other regions, all the way up to Canada, also mobilized and pushed the total raised to over one million US dollars.

“In this region, we have for years contributed to the United Cerebral Palsy campaign,” says Mick Parker, Vice-President, Operations, for the U.S. Florida and Gulf Region. “So we had a very effective donations system in place. For 60 days, we made our focus the Hurricane Katrina Employee Relief Fund and we set up fundraising activities such as car washes.”

Donations from employees and customers were supplemented at the Division and Head Office level. In total, US$418,000 was distributed to approximately 100 employees, 35 of whom had suffered total loss of all their belongings in the flooding that followed Katrina.

“It was a great outpouring of support from our colleagues,” says Kenny Hodges, Region Operations Director and the person who distributed the cheques to employees. “Especially for our employees. Those guys had lost everything and I had trouble locating everyone. I don’t think they ever expected the Company to come to their help and there were some very moving moments when I presented them with the cheques.”

Even though their place of work was scattered over the state, the Company kept managers and employees on the payroll until new jobs within the Company’s network could be found.

“People were very resilient,” says Hodges. “The attitude and the spirit were really remarkable.”

|

Alimentation Couche-Tard / 23

|

AN AMAZING ENGINE

For Good

CLOSE TO CDN$15 MILLION RAISED TO HELP OTHERS IN F’06

A well-run convenience store touches a lot of people. In Phoenix, for example, the equivalent of the entire metro population – 3.8 million people – passes through the city’s 350 Circle K stores every 10 days.

Push that out on even a more modest count and Couche-Tard’s network could conceivably access 4 to 5 million consumers on any given day. That’s a powerful capability. It’s especially powerful when the corner store is also a fixture of the community. As such, it has a major influence on mobilizing the population around it.

The Company puts this to good use. All three primary brands – Couche-Tard, Mac’s and Circle K – have long and proud histories of commitment to the communities they serve. Each year, dozens of organizations – from giant national bodies such as the Red Cross and United Way to the local centre for homeless children – become beneficiaries of a vast, supportive network anchored by canisters on thousands of counters.

In Fiscal 2006, this network contributed an extraordinary Cdn$5.9 million. In addition, Central Canada Mac’s stores turned over an amazing $8.5 million to charities within its division from the sale of Nevada lottery tickets.

Here is a cross-section of the year’s efforts by a dedicated team of tens of thousands of caring and concerned people.

24 / Alimentation Couche-Tard

Each year the Company commits at least 1% of its net earnings to the support of youth, health, welfare and humanitarian causes.

YOUTH

The welfare of young people has historically been the primary focus of the Company’s social commitment. In F’06, over $2 million US dollars was distributed to benefit such youth-related activities as:

- The Big Brothers and Big Sisters, a mentoring organization for children 6-16.

The Easter Seal Campaign which helps children with disabilities.

The Boys and Girls Club of America, which helps boys and girls develop the qualities needed to become responsible citizens.

- The Children’s Miracle Network, which raises funds for 170 children’s hospitals across North America.

Opération Enfants Soleil, Jeunesse J’écoute and Le club des petits déjeuners,which seek to provide emotional and physical nourishment for children.

HEALTH & WELFARE

Providing adequate health care to people of all ages is another target of the Company fundraising, to the tune of US$2.9 million. The latter was distributed namely to the following organizations:

- The United Cerebral Palsy association has been the preferred agency of the Circle K organization since 1998. This past year over US$1.8 million was raised by stores in the U.S.

- The Canadian Cystic Fibrosis Foundation.

- The March of Dimes, which seeks to avert premature births.

- Organizations for muscular dystrophy.

- Educational and medical institutions; in Canada a five year committment was taking towards such organizations.

HUMANITARIAN AID

In addition to the campaign specifically to help relocate displaced employees, the Company’s stores across North America raised over US$670,000 for the Katrina hurricane survivors. The largest part of these contributions was turned over to the major disaster relief agencies:

- The Red Cross received donations totaling over US$623,000.

- The United Way was presented with a cheque for just under US$50,000.

| Alimentation Couche-Tard / 25 |

STAYING ONE STEP

Ahead.

MAKING AN IMPACT

The Company’s store conversion program is creating a dynamic and differentiated new network for today’s consumer

The Company’s organic growth is driven largely by a far-reaching store conversion program known as IMPACT. The acronym, an employee contest winner, stands for Innovation-Marketing-People-Alimentation-Couche-Tard. The program is leading a radical, industry-wide makeover in convenience store concepts.

“Consumers are not buying what they bought 20 years ago,” says Réal Plourde, Executive Vice-President and Chief Operating Officer. “They have many choices now for the same product. That means our stores have to evolve and also offer more choice with better ambience.”

The IMPACT program, to which our people actively contribute, usually means the total makeover of a site.

The end result is

a more attractive ambience – brighter, with graphic themes reflecting local culture and more space to move around.

innovative merchandising displays which are tied in to a point-of-sale system scanning data for optimum results. Features differ by geographic region and include Beer Caves, premium coffee stations and food facilities.

- newly motivated, trained and skilled people (the “P” in the IMPACT system).

- enhanced product mix, especially in fresh-food products and financial services.

- quick service restaurants (QSR) which are either branded (Subway, Quiznos, Dunkin’ Donuts, etc) or proprietary. QSRs are in just under 300 stores or 6% of the network. The long term objective is to increase services and proprietary fresh food offerings within the corporate stores.

“The addition of prepared food services is an industry evolution over the past few years,” comments Réal Plourde. “At Couche-Tard we’re pretty good at breakfast now and we’ve got the hang of lunches. We’ve all got a long way to go, though, when it comes to the end of the day.”

26 / Alimentation Couche-Tard

Before&AFTER

The IMPACT store conversion program is setting the pace for strong organic growth throughout the network. The small photo shows this Circle K store before conversion; the large photo shows the spacious, remodeled premises with inviting displays and a convenient coffee station.

Alimentation Couche-Tard / 27

The conversions have been hugely successful both in terms of financial returns and the presentation of a dynamic, contemporary brand.

| We focus on innovation to stimulate sales and differentiate our stores. |

The IMPACT conversions have been hugely successful both in terms of financial returns and the presentation of a dynamic, contemporary brand representing many more services than the average consumer would historically expect. The investment is usually around Cdn$100,000, ranging up to Cdn$200,000 if food services are included. Return on the investment consistently shows sales increases and margin improvements. The Company is also continually building out new stores and follows the same IMPACT formula.

The IMPACT program was first successfully rolled out under the Couche-Tard and Mac’s banners in Canada. In F’06, the Company doubled up the conversion rate–particularly with regard to updating the aged Circle K stores–and completed 406 makeovers and 40 new stores. Nearly half of the Company’s corporate network - - 1,722 stores - are now IMPACT stores and the long-term objective is to upgrade all stores in the network within an eight year cycle pursuant to such program.

The Company plans to keep up the pace in F’07 adding approximately 100 new store locations through new store development and small acquisitions.

The program is delivering significant value to Couche-Tard beyond the improved sales and margins. For one thing, it clearly differentiates the Company’s brands, stimulating customer loyalty and making them a choice whether the banner is Couche-Tard, Mac’s or Circle K.

For another, it acts as a sparkplug generating innovation and fresh in–store thinking. New products include financial services such as gift cards, cheque-cashing and ATMs, and a growing number of proprietary products such as coffee, sandwiches and energy drinks.

“We can’t push walls out and make more space,” says Plourde. “So we focus on innovation to stimulate sales and differentiate our stores.”

A third and highly important benefit is the effect on local management and staff. People and customer service are widely viewed as the means to success in the c-store business and they are integral to the IMPACT program. The makeovers are undertaken at the regional level and fully involve the local manager and staff. Employees are re-trained in service and customer needs.

“The effect on morale and motivation is tremendous,” says Plourde. “Take Circle K as an example. The previous operator stores–are now IMPACT had a different model with little or no reinvestment in the locations. Now we have really strong people, newly empowered with the IMPACT program, involved in the change process and ending up with a fantastic new atmosphere in which to serve their clients. It’s just great to see the results.”

Healthier fresh food |  |

28 / Alimentation Couche-Tard

| The Company’s stores offer as many as 3,200 items – almost twice that of a decade ago. |

GROWTH WITH INNOVATION

Store owners take an entrepreneurial approach.

With an average of 2,500 square feet in store size – roughly 5% the size of a supermarket – and as many items ininventory, getting the product mix right is an unforgiving task.

“Every square inch has to produce. You have to innovate to differentiate your store, but there’s little room for mistakes,” explains Stéphane Gonthier, Senior Vice-President, Eastern North America. “This business is not for everyone. You can’t be risk-averse and sleep at night.”

Couche-Tard’s growth can be traced in part to and entrepreneurial mindset that has become ingrained in the culture, from street level to the management of its eight divisions.

“There are several reasons for our in-store growth,” says Gonthier. “Among those, innovations and well-targeted marketing strategies.”

New product development tends to reflect regional preferences. In Canada, customer acceptance is strong for the proprietary breakfast product, a roller toasting station and a single-serve coffee station. Closer to the Pacific, Western Canada is seeing significant new sales from fresh fruit, sushi and Chinese food.

In the U.S. Sunbelt, where “cold” is the biggest single attribute that sells beer, Beer Caves eliminate warm beer and soft drink displays. A priority of the Arizona Division is to build a reputation for cold dispensed beverages.

Frozen drinks are also a differentiator in Canada. In the east, Couche-Tard’s proprietary traffic builder is Sloche, and in Central and Western Canada, Mac’s has Froster.

Private and controlled brands play a major role in building customer loyalty and return traffic. Among 25 or so products are coffees (Millstone, Seattle’s Best and Van Houtte), energy drinks (Énergie and Joker) and sandwiches (La Maisonnée). Proprietary brands are oriented towards the largest gross profit contributors, those being foodservice and beverages.

Alimentation Couche-Tard / 29

We can now analyze the data to improve marketing strategies on a store-by-store basis. |

High-growth and high-margin foodservices are a staple of the IMPACT store conversion program. At the close of F’06, 6% of the network includes Quick Service Restaurant facilities. All of the IMPACT stores feature sandwiches and prepared foods. The Florida/Gulf Coast Division is getting a strong reception for its “Grab ‘n Go” breakfast and lunches.

Not all innovations are food stuffs. The US Southeast Division is generating significant revenues from 76 car wash locations. Eastern Canada boosted fuel sales with a joint promotion with the Canadian Automobile Association (CAA).

Financial services are a recent and promising addition. ATM machines are now at almost every location. Elsewhere in the network, services include bill payment, gift cards, prepaid American Express cards and cheque cashing (as many as twelve million people in the U.S. do not have a bank account).

The Company’s operations are built around a benchmarking and best practices procedure shared by all eight divisions. The result is a streamlined and effective process for bringing new winners to market rapidly and with minimum wasted effort.

“I think we are a leader in bringing to market new convenience products, especially foodstuffs, that will attract consumers to our brand,” says Brian Hannasch, Senior Vice-President, Western North America. “The slogan they use in Florida and Arizona is ‘What else do you need?’ That kind of sums it up.”

| 30 / Alimentation Couche-Tard |  |

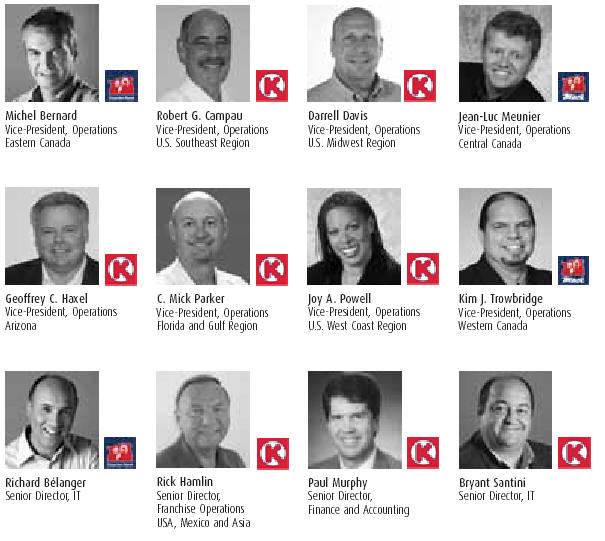

Teams with an Edge in Every Market

OPERATIONS TEAM

CORPORATE TEAM

Alimentation Couche-Tard / 31

STRONG ORGANIC

Growth

The fiscal year ended April 30, 2006 was marked by the continuation of the Company’s strong growth. Revenues increased 26.4% to US$10.2 billion and net earnings grew 26.4% to reach US$196.2 million.

It was a satisfying year, especially considering that this growth was almost entirely organic. The Company’s expansion has historically been by acquisition, with the last major deal being the addition of 1,663 Circle K corporate stores in December 2003. The year just ended demonstrates the effective integration of these assets and a steady increase in same-store sales. This is due to a rigorous network operating model and a commitment to customer service in each store.

“The year shows solid growth, continuing margin improvement and excellent financial health,” comments Richard Fortin, Executive Vice-President and CFO. “Frankly, I consider it quite a rarity for a company of our size to be showing such strong numbers. I believe it confirms both the vision and the business model.”

SOLID GROWTH, PROGRESSING MARGINS AND FINANCIAL HEALTH

(IN US DOLLARS)

| Revenues | $ | 10,157.3M | +26.4% |

| EBITDA(1) | $ | 438.6M | +27.8% |

| Net earnings | $ | 196.2M | +26.4% |

| Shareholders’ equity | $ | 966.0M | +31.8% |

| Merchandise and service gross margin | |||

| United States | 33.2% | ||

| Canada | 33.9% | ||

| Consolidated | 33.4% | ||

| Growth of same-store merchandise revenues(2) | |||

| United States | 5.2% | ||

| Canada | 3.9% | ||

| Growth of same-store motor fuel volume(2) | |||

| United States | 6.0% | ||

| Canada | 2.8% |

(1) EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) is presented for information purposes only and represents a performance measure used especially in financial circles. It does not have a standardized meaning prescribed by Canadian GAAP and therefore may not be comparable to similar measures presented by other public companies.

(2) Adjusted over a normal 52-week period.

Couche-Tard confirms the effectiveness of its controls over financial reporting as at April 30, 2006 thus conforming to legal and regulatory requirements in advance of the applicable implementation date set by Canada and United States regulatory authorities. For further detail, see page 46.

Full details of F’06 and comparison with the previous year will be found in the following Management Discussion & Analysis section.

32 / Alimentation Couche-Tard

MANAGEMENT’S DISCUSSION AND ANALYSIS

The purpose of this Management’s Discussion and Analysis (MD&A) is, as required by regulators, to explain management’s point of view on Alimentation Couche-Tard Inc.’s (Couche-Tard) financial condition and results of operations as well as past performance. More specifically, it outlines our development strategy, performance in relation to objectives, future expectations and how we address risk and manage our available financial resources. This MD&A also provides information to improve the reader’s understanding of the consolidated financial statements and related notes. It should therefore be read in conjunction with those documents. By “we”, “our”, “us” and “the Company”, we refer collectively to Couche-Tard and its subsidiaries.

Except where otherwise indicated, all financial information reflected herein is expressed in United States dollars (US dollars) and determined on the basis of Canadian generally accepted accounting principles (Canadian GAAP). You should read the following MD&A in conjunction with the annual consolidated financial statements and related notes included in this 2006 Annual Report. Additional information relating to Couche-Tard, including the Annual Information Form, is available on SEDAR at www.sedar.com and on the SEC’s website at www.sec.gov.

Forward-Looking Statements

This MD&A includes certain statements that are “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Any statement in this MD&A that is not a statement of historical fact may be deemed to be a forward-looking statement. When used in this MD&A, the words “believe”, “intend”, “expect”, “estimate” and other similar expressions are generally intended to identify forward-looking statements.

It is important to know that the forward-looking statements in this MD&A describe our expectations as at July 12, 2006 and are not guarantees of future performance of Couche-Tard or its industry and involve known and unknown risks and uncertainties which may cause the Company’s or the industry’s outlook, actual results or performance to be materially different from any future results or performance expressed or implied by such statements. Our actual results could be materially different from what we expect if known or unknown risks affect our business, or if our estimates or assumptions turn out to be inaccurate. As a result, we cannot guarantee that any forward-looking statement will materialize and, accordingly, you are cautioned not to place undue reliance on these forward-looking statements. Forward-looking statements do not take into account the effect that transactions or special items announced or occurring after the statements are made may have on our business. For example, they do not include the effect of sales of assets, monetizations, mergers, acquisitions, other business combinations or transactions, asset write-downs or other charges announced or occurring after forward-looking statements are made.

Unless otherwise required by applicable securities laws, Couche-Tard disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

The foregoing risks and uncertainties include the risks set forth below under “Business Risks” as well as other risks detailed from time to time in reports filed by Couche-Tard with securities regulators in Canada and the United States.

Change in Reporting Currency

Since our first quarter of fiscal 2006, we have reported our financial results and financial position in US dollars and accordingly, our Canadian assets and liabilities are translated into US dollars using the exchange rate in effect at the balance sheet date. Revenues and expenses are translated at the average rate in effect during the period. Gains and losses are included in the Cumulative translation adjustments account in the Shareholders’ equity. The functional currency of the Company and the functional currencies of each of its subsidiaries remain unchanged. All comparative amounts for prior periods have been restated and are presented in US dollars.

Our Business

We are the leader in the Canadian convenience store industry. In North America, we are the third largest convenience store operator and the second largest independent convenience store operator (not integrated with a petroleum company) and the most profitable public company within such category. We currently operate a network of 4,983 convenience stores, 3,085 of which include motor fuel dispensing, located in eight large geographic markets, including three in Canada and five in the United States, covering 23 states. Some 37,000 people are employed throughout Couche-Tard’s retail convenience network and executive offices in North America.

We sell food and beverage items, motor fuel and other products and services targeted to meet our customers’ demand for convenience and quality in a clean and welcoming environment. We believe that our business model has differentiated Couche-Tard from its competition through its decentralized management structure, commitment to operational expertise, focus on in-store merchandise, particularly the higher growth and higher margin grocery categories, and continued investment in store modernization and technology.

Alimentation Couche-Tard / 33

In light of improvements made to the Store 2000 differentiation concept in recent years through the addition of various marketing and merchandizing approaches and components, we have renamed our various concepts under one acronym – IMPACT (Innovation, Marketing and People at Alimentation Couche-Tard). This acronym reflects not only the impact our differentiation strategies have on our customers, sales and earnings but also the diversity of the dynamic programs designed by the Couche-Tard teams in order to create a unique, warm, friendly and inviting environment for customers.

We conduct our business through different modes of operations. Although the majority of our stores are Company-operated, some are part of our affiliate program, which includes franchised and licensed stores. The amount of operating income generated from the affiliates amounted to $14.1 million or 4.3% of our total operating income for fiscal 2006, including $2.7 million or 1.0% of our total operating income generated by licensees outside North America.

The convenience store industry is fragmented, with the top ten operators representing only approximately 25% of the estimated total of 138,200 stores in the United States. Industry consolidation by highly leveraged operators in the 1990’s, combined with competition and fluctuations in motor fuel margins, has led to numerous corporate restructurings and rationalizations in recent years. As a result, we believe the opportunity exists for well-capitalized, established industry participants to grow through mergers and acquisitions.

2006 Overview

We announced record results for fiscal 2006, up 26.4% over last year to $196.2 million or $0.94 per share on a diluted basis. This performance primarily reflects growth in merchandise and service revenues and motor fuel revenues as well as an increase in the corresponding gross margins in our Canadian and American markets.

Excluding non-recurring items and items for which we have little or no control, net earnings would have been $195.8 million(1) or $0.94 per share on a diluted basis, an increase of 26.2% compared to last fiscal year.

Also, net earnings of the fourth quarter of 2006 amounted to $32.1 million or $0.15 per share on a diluted basis, a decrease of 1.2%. However, excluding the items mentioned above, net earnings would have been $36.7 million(1) or $0.18 per share on a diluted basis, which represents an increase of 35.9 % compared with the net earnings of the fourth quarter of the previous year (adjusted based on the annual effective income tax rate of 2005).

During the year, we experienced significant increases in the retail price of motor fuel in our U.S markets, primarily attributable to the volatility in the world prices for crude oil. The average retail price of motor fuel in our U.S. markets amounted to $2.40 per gallon in fiscal 2006 compared with $1.94 per gallon in fiscal 2005. The gross margin on motor fuel revenues varies primarily as a result of product cost volatility and competition. Although motor fuel gross margins can be volatile from one quarter to the next, they generally even out on an annual basis. For each of our four quarters commencing with the first quarter of fiscal 2006, motor fuel gross margins for the Company-operated stores in the U.S. markets stood at 14.86¢, 17.05¢, 17.63¢ and 10.96¢ per gallon respectively - with a weighted average of 15.14¢ per gallon for 2006 compared with 14.17¢ per gallon for the previous year. Net of electronic payment modes related expense, these same gross margins were 11.88¢(2), 13.55¢(2), 14.39¢(2) and 7.65¢ per gallon, with a weighted average of 11.88¢ per gallon in fiscal 2006, compared with 11.52¢ per gallon in fiscal 2005. In fiscal 2006, this increase in the motor fuel gross margin had a positive impact of $19.7 million on our operating income ($25.3 million including Company-operated stores in Canada). Net of the increase in electronic payment modes related expense, excluding volume effect, the positive impact is reduced to $7.2 million ($11.6 million including Company-operated stores in Canada).

Dividends

On November 15, 2005, the Company’s Board of Directors adopted a quarterly dividend policy of Cdn0.025$ per share on Class A multiple voting shares and Class B subordinate voting shares (the shares). Following the adoption of this dividend policy, the Board of Directors declared and approved quarterly dividends of Cdn0.025$ per share for both second and third quarters of fiscal 2006. Subsequent to year end, the Board of Directors declared and approved a quarterly dividend of Cdn0.025$ per share for the fourth quarter of fiscal 2006, payable July 31, 2006.

| (1) | These adjusted net earnings are presented for information purposes only. They do not have a standardized meaning prescribed by Canadian GAAP. Management believes this information is a relevant complement to information published based on Canadian GAAP. | |

| (2) | Restated following improvements in analysis and available data. | |

34 / Alimentation Couche-Tard

Business acquisitions

During fiscal 2006, we made the following business acquisitions:

| • | effective March 14, 2006: purchase of 34 Company-operated stores and 19 affiliated stores, all operating under the Shell banner in the Indianapolis area of Indiana, United States, from Shell Oil Products US. At the closing date, two Company-operated stores were closed; |

| • | effective December 14, 2005: purchase of 16 Company-operated stores operating under the Winners banner in New Mexico, United States, from Conway Oil Company and Conway Real Estate Company; |

| • | effective December 8, 2005: purchase of 18 Company-operated stores and 8 affiliated stores, all operating under the BP banner in the Memphis area of Tennessee, United States, from BP Products North America, Inc.; |

| • | effective November 3, 2005: purchase of seven Company-operated stores operating under the Fuel Mart banner in Ohio, United States, from Ports Petroleum Co. |

We expect those 73 new Company-operated stores and 27 affiliated stores to represent additional annual sales of approximately $341.0 million and to contribute to our net earnings on an annual basis.

These four acquisitions were carried out for a total cash consideration of $91.6 million, financed using the Company’s available cash. The net assets acquired include $4.6 million in working capital, $81.4 million in property and equipment, $2.0 million in trademarks and licences, $1.3 million in other assets, $3.9 million in goodwill and $1.6 million in deferred credits and other liabilities. Most of the goodwill related to the transactions is deductible for tax purposes.

Internal controls

We confirm the effectiveness of our controls over financial reporting as at April 30, 2006 thus conforming to legal and regulatory requirements prior to the applicable implementation date set by Canadian and American regulatory authorities.

Franchises and licences

During fiscal 2006, we entered into an agreement with ConocoPhillips Company resulting in the addition of 75 new franchises operating under the Circle K banner in the Western United States, which will bring the total to 251 franchises operated by ConocoPhillips Company and 672 franchises in the entire North American network. Also during fiscal 2006, we decided not to renew the agreement with the licence holder of 800 stores operated in Taiwan under the Circle K banner since we did not agree on conditions of renewal. Overall, the impact of these events on our financial position and operating results will not be significant.

Hurricanes

Fiscal 2006

During 2006, Florida and the Gulf of Mexico region was affected by three hurricanes, which resulted in some damages to certain of our sites. We estimates that assets and leased properties that were damaged have a total replacement value of approximately $16.7 million, which will result in a net claim of about $13.0 million. The net book value of the damaged assets is lower than the net claim. As at April 30, 2006, we have received $2.0 million in insurance proceeds. We do not expect these hurricanes to have a significant effect on our financial position and operating results.

In total, 163 sites were affected to various degrees, 15 of which are still closed as of today. Of these sites, we expect that approximately 13 will remain permanently closed because they did not have the potential to meet our contribution expectations, while the other two should reopen in fiscal year 2008. As at April 30, 2006, and from the date of occurrence of those events, we estimate that we have lost approximately 5,500 store-days.

As part of our risk management process, we have decided not to renew our insurance coverage for material damage related to hurricanes. This decision is based on the fact that the renewal conditions proposed by the insurance companies were considered to be unacceptable from an economic perspective. In fact, based on the proposals received, we would have had to assume the majority of the risk. In addition, we believe that we have the financial strength and available funds to absorb the risk. This decision will be reviewed and re-evaluated on a regular basis in light of changing market conditions.

Alimentation Couche-Tard / 35

Fiscal 2005

During 2005, certain areas of our business in Florida experienced damages resulting from four hurricanes. Assets and leased properties that were damaged have a total replacement value of $23.5 million, which resulted in a net claim of about $16.6 million. The net book value of the damaged assets is lower than the net claim. As at April 30, 2006, we have received $15.9 million in insurance proceeds. We consider that these hurricanes had no significant effect on our financial position and operating results.

In total, 92 sites were affected to various degrees, four of which will remain permanently closed because they did not have the potential to meet our contribution expectations. As at April 30, 2006, and from the date of occurrence of those events, we estimate that we have lost approximately 4,800 store-days.

Subsequent events

Acquisitions

On June 12, 2006, we finalized the transaction with Spectrum Holding, Inc. regarding the acquisition of 90 stores operating under the Spectrum banner in the States of Georgia and Alabama in the United States. The transaction was carried out for a cash consideration of $130.0 million, financed using the Company’s available cash. We expect that the 90 new stores will represent additional annual revenues of approximately $325.0 million and that they will contribute to our net earnings on an annual basis.

In addition, again on June 12, 2006, we signed an agreement with Moore Oil Company, LLC in order to acquire a network of 24 stores operating under the Stop-n-Save banner in the Monroe area of Louisiana in the U.S. Of the 24 stores, six are operated by the company, 17 are operated by independent store operators and one store is currently under construction. If the transaction is completed as expected in July 2006, we anticipate that these stores will contribute to our operating income on an annual basis.

Income taxes

On June 9, 2006, the Government of Québec adopted Bill 15 in the National Assembly of Québec regarding amendments to the Taxation Act and other legislative provisions. As a result, an unusual retroactive income tax expense of approximately $9.8 million, excluding other associated expenses, will be recognized in the first quarter of fiscal 2007. This modification will not have a significant impact on the effective income tax rate of the Company in the future.

Outstanding shares and stock options

As at June 30, 2006, Couche-Tard had 56,388,652 Class A multiple voting shares and 145,651,434 Class B subordinate voting shares issued and outstanding. In addition, as at the same date, Couche-Tard had 9,307,980 outstanding stock options for the purchase of Class B subordinate voting shares.

Income Statement Categories

Merchandise and Service Revenues. In-store merchandise revenues are comprised primarily of the sale of tobacco products, grocery items, candy and snacks, beverages, beer/wine and fresh food offerings, including quick service restaurants (QSRs). Service revenues include the commission on sale of lottery tickets and issuance of money orders, fees from automatic teller machines, sales of calling cards and gift cards, fees for cashing cheques and sales of postage stamps and bus tickets, as well as revenues from car washes. Service revenues also include franchise fees, license fees from affiliates and royalties from franchisees.

Motor Fuel Revenues. We include in our revenues the total dollar amount of motor fuel sales, including any imbedded taxes, if we take ownership of the motor fuel inventory. In the United States, we purchase motor fuel and sell it to approximately 112 independent store operators at cost plus a mark-up. We record the full value of these revenues (cost plus mark-up) as motor fuel revenues. Where we act as a selling agent for a petroleum distributor, only the commission we have earned is recorded as revenues. Gross profit from motor fuel is derived by deducting the cost of the motor fuel from the motor fuel revenues, except for commission stores where the gross profit is equal to the recorded commission from the sale.

Gross Profit. Gross profit consists mainly of revenues less the cost of goods and motor fuel sold. For in-store merchandise, the cost of inventory is generally determined using the retail method (retail price less a normal margin), and for motor fuel, it is determined using the average cost method.

36 / Alimentation Couche-Tard

Operating, Selling, Administrative and General Expenses. The primary components of operating, selling, administrative and general expenses are labor, occupancy costs, commissions to dealers and overhead and include advertising expenses that are charged as incurred.

Key performance indicators used by management, which can be found under “Results of Operations-Other Operating Data”, are merchandise and service gross margin, growth of same-store merchandise revenues, motor fuel gross margin and growth of same-store motor fuel volume.

Summary of Fourth Quarter Results: 13-Week Period Ended April 30, 2006 Compared to the 12-Week Period Ended April 24, 2005

The following table highlights certain information regarding the movement of our stores during the 13-week period ended April 30, 2006:

| Company-operated | Affiliated | Total | |

| stores | stores | ||

| Number of stores, beginning of period | 3,605 | 1,304 | 4,909 |

Acquired | 32 | 19 | 51 |

Opened | 22 | 33 | 55 |

Closed | (25) | (7) | (32) |

Converted into affiliated stores | (2) | 2 | - |

| Number of stores, end of period | 3,632 | 1,351 | 4,983 |

During the quarter, we also implemented our IMPACT program in 182 Company-operated stores for a total of 446 in 2006. As a result, 47.6% of our Company-operated stores have now been converted to our IMPACT program, which gives us considerable potential for future internal growth.

All of our Company-operated stores that were closed did not have the potential to meet our contribution expectations. Most of these stores were part of the Circle K network acquired December 17, 2003.

The following table highlights certain information regarding our operations for the 13-week period ended April 30, 2006 and the 12-week period ended April 24, 2005:

| (In millions of US dollars, unless otherwise stated, unaudited) | 13-week period | 12-week period |

| ended | ended | |

| April 30, 2006 | April 24, 2005 | |

| Revenues | 2,638.9 | 1,961.7 |

| Operating income | 57.2 | 47.1 |

| Net earnings | 32.1 | 32.5 |

| Selected Operating Data: | ||

| Growth of same-store merchandise revenues on a 12-week basis (1) (2): | ||

Canada | 4.3% | 3.3%(3) |

United States | 4.6% | 6.6%(3) |

| Growth of same-store motor fuel volume on a 12-week basis (2): | ||

Canada | 4.1% | 7.4%(3) |

United States | 5.8% | 4.5%(3) |

| (1) | Excludes other revenues derived from franchise fees, royalties and rebates on some purchases by franchisees and licensees. (Growth in Canada is calculated based on Canadian dollars.) | |

| (2) | Since our first quarter of fiscal 2006, growth in both merchandise revenues and motor fuel volume has been reported on a same-store basis. | |

| (3) | For the comparative period, growth in merchandise revenues and motor fuel volume is reported on an average per store basis to be constant with our prior practices. Growth in the United States excludes the Circle K acquisition. | |

Alimentation Couche-Tard / 37

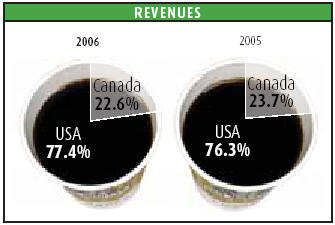

For the 13-week period ended April 30, 2006, we achieved revenues of $2.64 billion, compared with $1.96 billion for the same period in fiscal 2005, an increase of 34.5% or $677.2 million. We recorded 78.9% of our revenues in the United States, compared with 77.7% in the fourth quarter last year.

In the United States, growth of same-store merchandise revenues (on a 12-week standardized basis) was 4.6 % while it was 4.3% in Canada. In both the U.S. and Canada, this growth is partially due to the results from investment in our IMPACT program conversions, as well as the results from the launch of new products that were well received by customers and from the implementation of our pricing strategies on certain product categories. In Canada, the growth was negatively affected by growing smuggling on tobacco products.

In the United States, the growth of same-store motor fuel volume (on a 12-week standardized basis) was 5.8 % in the fourth quarter of 2006 while it was 4.1% in Canada, which reflects the positive impact, in both the U.S. and Canada, of certain pricing strategies. Growth in Canada also reflects the positive consumer response in Ontario to our rebranding of several motor fuel locations, which now operate under Mac’s in addition to a strong economy in Western Canada.

Net earnings stood at $32.1 million or $0.16 per share ($0.15 per share on a diluted basis), compared with $32.5 million or $0.16 per share ($0.16 per share on a diluted basis), which represents a decrease of 1.2%. By applying the annual effective tax rate in effect for 2005 (32.08%) to earnings of the fourth quarter of 2005, the net earnings for this quarter would have been $27.0 million or $0.13 per share on a diluted basis. In addition, net earnings in the fourth quarter of 2006 were affected by the following items, presented net of income tax:

Net earnings for the 4th quarter of 2006, as presented | Negative impact related to the increase in electronic payment modes related expense (1) | Negative impact related to non-recurring termination fees (2) | Negative impact related to the increase in the effective tax rate (3) | Positive impact related to changes in the exchange rate (4) | Positive impact related to the 13th week of the 4th quarter of 2006 | Net earnings for the fourth quarter of 2006, adjusted (5) |

$32.1 million | $4.0 million | $3.3 million | $1.0 million | ($1.0) million | ($2.7) million | $36.7 million |

(1) | Related to the increase in the retail price and sales volume of motor fuel. |

(2) | Recognition of a non-recurring charge relating to penalties for the termination of two contracts governing the operation of automatic teller machines in some of our stores in the United States. The termination of these contracts will allow us to operate the automatic teller machines in these stores ourselves and to increase their contribution. |

(3) | Impact of the increase in the effective tax rate, which was 34.09% in the fourth quarter of this year compared with 32.08% for fiscal year 2005. |

(4) | Impact of the increase in the value of the Canadian dollar compared with the US dollar. |

(5) | These adjusted net earnings are presented for information purposes only. They do not have a standardized meaning prescribed by Canadian GAAP. Management believes this information is a relevant complement to information published based on Canadian GAAP. |

Thus, by taking into account all of these factors for which the nature is non-recurring or for which the Company has little or no control, the net earnings for the fourth quarter of 2006 would have been $36.7 million ($0.18 per share on a diluted basis), which represents an increase of 35.9% compared with the net earnings of the fourth quarter of the previous year (adjusted based on the annual effective income tax rate of 2005).

Exchange Rate Data

The Company’s US dollar reporting currency provides shareholders with more relevant information giving consideration to the predominance of our operations in the United States and our US dollar denominated debt.

The following table sets forth information about exchange rates based upon the Bank of Canada closing rates expressed as US dollars per Cdn$1.00:

| 53-week period ended | 52-week periods ended | ||

| April 30, 2006 | April 24, 2005 | April 25, 2004 | |

| Average for the period (1) | 0.8417 | 0.7779 | 0.7431 |

| Period end | 0.8945 | 0.8098 | 0.7349 |

| (1) | Calculated by taking the average of the closing exchange rates of each day in the applicable period. | |

38 / Alimentation Couche-Tard

Selected Consolidated Financial Information

The following table highlights certain information regarding our operations for the 53-week period ended April 30, 2006 and the 52-week periods ended April 24, 2005 and April 25, 2004:

| (In millions of US dollars, unless otherwise stated) | 53-week period ended | 52-week periods | |

| April 30, 2006 | April 24,2005 | April 25, 2004 restated | |

| Statement of Operations Data: | |||

| Merchandise and service revenues (1) : | |||

Canada | 1,426.7 | 1,239.5 | 1,130.6 |

United States | 2,812.0 | 2,564.7 | 1,195.3 |

Total merchandise and service revenues | 4,238.7 | 3,804.2 | 2,325.9 |

| Motor fuel revenues | |||

Canada | 873.7 | 664.8 | 507.1 |

United States | 5,044.9 | 3,567.8 | 1,562.3 |

Total motor fuel revenues | 5,918.6 | 4,232.6 | 2,069.4 |

| Total revenues | 10,157.3 | 8,036.8 | 4,395.3 |

| Merchandise and service gross profit (1) : | |||

Canada | 483.1 | 415.7 | 367.4 |

United States | 932.3 | 834.9 | 389.7 |

Total merchandise and service gross profit | 1,415.4 | 1,250.6 | 757.1 |

| Motor fuel gross profit: | |||

Canada | 63.6 | 51.3 | 47.3 |

United States | 312.5 | 255.9 | 110.1 |

Total motor fuel gross profit | 376.1 | 307.2 | 157.4 |

| Total gross profit | 1,791.5 | 1,557.8 | 914.5 |

| Operating, selling, administrative and general expenses | 1,352.9 | 1,214.7 | 740.3 |

| Depreciation and amortization of property and equipment and other assets | 106.9 | 83.9 | 57.7 |

| Operating income | 331.7 | 259.2 | 116.5 |

| Financial expenses | 34.0 | 30.7 | 23.5 |

| Write-off of financing costs | - | - | 9.2 |

| Earnings before income taxes | 297.7 | 228.5 | 83.8 |

| Income taxes | 101.5 | 73.3 | 27.7 |

| Net earnings | 196.2 | 155.2 | 56.1 |

| Other Operating Data: | |||

| Merchandise and service gross margin (1) : | |||

Consolidated | 33.4% | 32.9% | 32.6% |

Canada | 33.9% | 33.5% | 32.5% |

United States | 33.2% | 32.6% | 32.6% |

| Growth of same-store merchandise revenues on a 52-week basis (2) (5): | |||

Canada | 3.9% | 2.6%(6) | 3.1%(6) |

United States | 5.2% | 10.4%(6) | 3.9%(6) |

| Motor fuel gross margin: | |||

Canada (Cdn cents per litre) | 5.00 | 4.61 | 4.77 |

United States (cents per gallon) (3) | 15.14 | 14.17 | 11.57 |

| Volume of motor fuel sold (4) : | |||

Canada (millions of litres) | 1,509.6 | 1,413.5 | 1,329.2 |

United States (millions of gallons) | 2,116.1 | 1,858.1 | 996.1 |

| Growth of same-store motor fuel volume on a 52-week basis: | |||

Canada | 2.8% | 6.6%(6) | 6.7%(6) |

United States | 6.0% | 6.3%(6) | 6.4%(6) |

| Per Share Data: | |||

Basic net earnings per share (dollars per share) | 0.97 | 0.77 | 0.31 |

Diluted net earnings per share (dollars per share) | 0.94 | 0.75 | 0.30 |

Dividends paid on common shares (Cdn dollars per share) | 0.05 | - | - |

| Balance Sheet Data: | |||

Total assets | 2,369.2 | 1,995.7 | 1,650.8 |

Interest-bearing debt | 524.1 | 530.9 | 536.9 |

| (1) | Includes other revenues derived from franchise fees, royalties and rebates on some purchases by franchisees and licensees. | |