we are... CFM

| |

| During the past 16 years, CFM has grown from a small regional hearth manufacturer into a diversified home products company, with annual sales of $686 million and more than 2,700 employees in North America and the United Kingdom. This record of rapid growth and evolution has been made possible by an unwavering focus on the high-quality, high performance home products that today's consumers are looking for and the systematic expansion of our presence in leading retail distribution networks. As explained in this year's annual report, it's an approach that continues to bode well for CFM in the years ahead.

| |

| |

| |

| |

* EBITDA before restructuring costs is defined as earnings before the taking of any deductions in respect of interest, taxes, amortization and restructuring costs. EBITDA before restructuring costs is presented before deductions for interest expense, tax expense, amortization and restructuring costs as this is a widely accepted measure of a company's normal operating performance. EBITDA before restructuring costs is not a recognized measure for financial statement presentation under Canadian generally accepted accounting principles ("GAAP"). Non-GAAP measures (such as EBITDA before restructuring costs) do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other issuers. Investors are encouraged to consider these financial measures in the context of CFM's GAAP results, as provided in the attached financial statements.

| |

C O N T E N T S CFM at a Glance inside front cover Financial Highlights 2 Letter from the Chairman 3 Corporate Governance 14 Employee Listing inside back cover

| |

CFM AT A GLANCE

| hearth & heating products | ||

|

|

|

| gas fireplaces CFM manufactures an extensive line of gas fireplaces. The economic, environmental and aesthetic benefits of natural gas bode well for CFM, an industry leader that derives more than 50% of its hearth revenues from high-margin, gas-fuelled products. | wood fireplaces CFM's factory-built wood fireplaces meet increasingly stringent demands for efficiency, convenience and safety. Loaded with features such as advanced heat circulation and zero-clearance designs, CFM wood fireplaces combine traditional charm with unprecedented versatility. | gas and wood stoves With a complete range of direct-vent, natural-vent and vent-free gas stoves, and an elegant line of fuel-efficient low emission cast-iron wood-burning models, CFM's high-quality stoves are aimed at the growing retrofit/remodelling markets, where consumers are seeking elegant and efficient space heating. |

|

|

|

| electric fireplaces and stoves CFM's electric fireplaces and stoves have extended the Company's presence into condominiums, apartment buildings, offices, retail locations and increased the Company's penetration of hearth products in the mass merchant channel. With patented light filtering technology that creates astounding realism and ambience, these innovative products can be "plugged-in" just about anywhere. | space heating products CFM's full line of space heaters has helped the Company expand its presence in the fast-growing mass merchant sales channel. The Company's focus on product innovation makes it well positioned to benefit from strong demand and continued consolidation in this sector.

| gas log sets Used in tandem with CFM's patented Insta-Flame burner, the Company's ceramic fibre log sets create an intense, realistic glow. Gas logs make it easy and cost-effective to convert any traditional fireplace to gas.

|

| ||

| mantels and accessories CFM's mantels, cabinets and other hand crafted accessories provide consumers with the choice and quality they need to enhance the value and appearance of their homes. |

we are...

leveraging

core markets

barbeque & outdoor

products

|

|

| barbeques CFM's entry into the mid- to high-end segment of the barbeque market has leveraged the Company's core manufacturing expertise, provided important counter-seasonal benefits and fuelled its penetration of mass merchant sales channels. In just three short years, CFM has become a major player in the growing North American barbeque industry. | outdoor fireplaces The rising popularity of outdoor leisure and entertainment activities is taking the conveniences of the home outside. CFM is meeting this trend with specialized outdoor fireplaces that feature realistic masonry design and durable stainless steel construction. |

|

|

| patio heaters CFM's gas infrared patio heaters take the chill off cool evenings and extend the outdoor season, two reasons for their growing popularity in home, restaurant and other commercial applications. | garden products Supported by strong demographic fundamentals, CFM's garden products business continuesto provide counter-seasonal opportunities to enhance capacity utilization and revenue growth. |

| home water products | |

|

|

| dispensing and filtration Focused on value-added appliances for the home market, CFM offers a growing range of innovative water dispensing, filtration and purification products under the Greenway, Polar and Vitapur brand names. | purification CFM's unique Vitapur UV water purification system delivers whole-home protection against organic contaminants. |

how we are... | |

| we are... creating a strong foundation CFM has rapidly evolved from a hearth manufacturer into a diversified home products leader, with solid foundations for growth in some of the most attractive segments of the market. page 6 |

| we are... doing more of what we do best Industry leaders in research and development, we are focused on meeting emerging consumer needs with innovative products that are known for their quality, visual appeal and convenience. page 8 |

| we are... raising the bar on performance After several years of rapid growth and diversification CFM has reached a new stage in its evolution - one in which we plan to benefit from a range of productivity and margin enhancement initiatives. page 10 |

| we are... staying nimble and focused During the past year, CFM implemented a series of initiatives that are designed to foster the company's unique entrepreneurial culture, despite the increasing scale and complexity of our business. page 12 |

we are...

positioning for growth

| FINANCIAL HIGHLIGHTS | |||||

| ($ thousands except per share amounts) | 2003 | 2002 | % change | ||

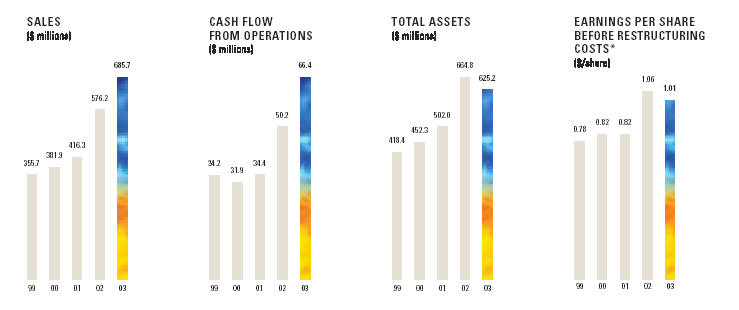

| Sales | 685,663 | 576,232 | 19% | ||

| Net income | 35,857 | 42,081 | (15%) | ||

| Earnings per share | $ | 0.89 | $ | 1.06 | (16%) |

| Earnings per share before restructuring costs* | $ | 1.01 | $ | 1.06 | (5%) |

| EBITDA before restructuring costs* | 86,754 | 81,964 | 6% | ||

| Cash flow from operations | 66,375 | 50,181 | 32% | ||

| Debt to total capitalization* | 0.33 | 0.37 | n/a |

* Earnings per share before restructuring costs have been determined by taking net income for the applicable period, adding to it the restructuring costs, deducting provision for income taxes applicable to the restructuring charge to arrive at net income before restructuring costs for the applicable period and dividing net income before restructuring costs by the average number of shares outstanding during such period. Earnings per share before restructuring costs is presented as a measure of the normal operating performance of the Company. EBITDA before restructuring costs is defined as earnings before the taking of any deductions in respect of interest, taxes, amortization and restructuring costs. EBITDA before restructuring costs is presented before deductions for interest expense, tax expense, amortization and restructuring costs as this is a widely accepted measure of a company's normal operating performance. Debt to total capitalization is defined as total net debt divided by total net debt and shareholders' equity. Net debt is defined as debt (current and long-term) plus bank indebtedness less cash. Earnings per share before restructuring costs, EBITDA before restructuring costs and debt to total capitalization are not recognized measures for financial statement presentation under Canadian generally accepted accounting principles ("GAAP"). Non-GAAP measures (such as earnings per share before restructuring costs, EBITDA before restructuring costs and debt to total capitalization) do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other issuers. Investors are encouraged to consider these financial measures in the context of CFM's GAAP results, as provided in the attached financial statements. |

| LETTER FROM THE CHAIRMAN Fiscal 2003 was another year of record revenue at CFM. It was also a period of important management and organizational changes that have helped fortify our foundations. We are ready for a higher level of development in CFM's ongoing evolution. COLIN ADAMSON

|

we are...

ready to reach

the next level

The past five years have represented a remarkable period of growth at CFM, one in which the company has more than doubled sales and successfully transformed itself from a hearth manufacturer into a leading and diversified home products company. In fiscal 2003, CFM continued to build on this record, although our earnings growth was tempered by a number of factors including a stronger Canadian dollar, higher than anticipated returns at the end of the mass merchant hearth season and the loss of hearth placement at one of our major customers. Despite these challenges, CFM ended the year with a solid foundation for future growth. It's one that includes more products, more distribution channels and a more diversified customer base than ever before. Just as important, we have invested in the skills and resources required to take CFM to the next level of development in its ongoing evolution.

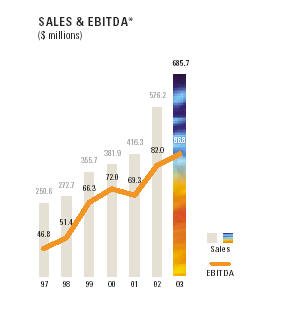

Record sales For the 12-month period ending September 27, 2003, sales increased 19% or $109 million to a record $686 million. This record was achieved despite the negative impact on the translation of our U.S. revenues from the strengthening of the Canadian dollar relative to the U.S. dollar. In real terms, before the impact of foreign exchange, our total sales grew by almost 25%. Sales of hearth and heating products rose by 2% from the previous year but were up 8% when adjusted for the impact of a rising Canadian dollar. This is a considerable accomplishment given the lossof some significant hearth products placement that had a significantly negative impact on hearth revenues during fiscal 2003. Fortunately, our efforts to mitigate this development and further diversify our revenue stream were successful. In barbeque and outdoor products, revenues increased a remarkable 63% to $216 million on the strength of growing sales in the mass merchant arena and a full year's contribution from Keanall and The Great Outdoors Grill Company, which were acquired in January and May of 2002, respectively. This was quite an achievement given the unseasonably wet and cool weather that occurred during the critical April to July selling period. Fiscal 2003 was a successful first year for CFM's water products with revenues reaching $17 million thanks to a combination of new product introductions and an expanding list of customers.

CFM CORPORATION 2003 ANNUAL REPORT 3

The prospects for our most recent growth platform - water and air purification - are similarly robust. Since purchasing Greenway Home Products Inc. in October 2002, CFM has been taking advantage of this opportunity with a growing range of high-quality products in more and more retailers throughout North America. Our success can be measured by the growth of sales in this business to $17 million during fiscal 2003.

A stronger foundation for growth The most significant accomplishments of the past year will only be evident in the months and years ahead. More specifically, fiscal 2003 was not just another year of growth for CFM, it was a year of foundation strengthening and organizational improvement as we moved to reinforce the leadership positions we have built in our markets and set the stage for stronger growth and increasing profitability going forward. In July, we welcomed Mark Proudfoot to CFM as the company's new President and Chief Operating Officer. Formerly Vice President of International Business Development for Emerson Electric Company, Mark has brought many skills to CFM including the discipline gained from operating multiple manufacturing facilities in a best-cost environment. Under Mark's direction, CFM announced a major restructuring program designed to optimize the benefits of past acquisitions, significantly improving customer service capabilities, and to reduce our annual cost base by more than $15 million. This includes a realignment of our manufacturing and distribution assets as well as moving certain production to low-cost jurisdictions. At the same time, we've implemented major organizational changes which are designed to focus our operations along specific product lines and further strengthen our relationship with customers. You can read more about these initiatives on pages 12 and 13 of this report.

Abundant opportunities During all my years at CFM, I have never been more optimistic about the company's prospects for long-term growth and rising profitability. We are market leaders in the North American hearth industry, which, as it continues to consolidate, will provide further opportunity for CFM to increase profitability and expand market share. Moreover, while the industry's rate of growth may have slowed recently, it will continue to be supported by strong fundamentals for many years. These include, among other fundamentals, the compelling economic and environmental benefits of natural gas, and the cocooning behaviour of an aging population.

Meanwhile, our leading position in the hearth industry continues to fuel our evolution into complementary consumer product categories. In fact, in fiscal 2003, a larger portion of CFM's revenue was derived from the consumer as opposed to the home building market, a percentage that will continue to increase as CFM takes advantage of its opportunities for growth. This includes a barbeque business that has grown in three short years from a good idea into a $216 million business. Today, management believes that CFM is among the top five players in a North American gas barbeque industry that enjoyed double-digit growth in 2002, the latest year for which industry-wide production data is available.

CFM CORPORATION 2003 ANNUAL REPORT 4

LETTER FROM THE CHAIRMAN

The prospects for our most recent growth platform - water and air purification - are similarly robust. Water quality is a serious and growing concern for North American consumers and the reason why more than two-thirds of Americans already use bottled water, water filtration or a combination of both products in their homes. Since purchasing Greenway Home Products Inc. in October 2002, CFM has been taking advantage of this opportunity with a growing range of high-quality products in more and more retailers throughout North America. Our success can be measured by the growth of sales in this business to $17 million during fiscal 2003. During the next few months, we'll be extending our presence in this burgeoning consumer product segment with our new generation Vitapur whole-home UV water purifier in conjunction with a series of filtration products designed to remove harmful chemicals and metals from the home water supply. These are the types of high-margin home products that retailers want to offer their customers. As an industry leader in product development with a steadilyincreasing presence in the mass retail market, CFM is exceptionally well positioned to provide them.

At the same time, we are more focused than ever on unleashing the synergies in our organization, particularly with regard to manufacturing and distribution cost efficiencies. During the past few years, CFM has enjoyed tremendous revenue and EBITDA growth and we've been a low-cost producer in our traditional businesses. But today's challenging business environment, which includes new global competitors and a surprisingly buoyant Canadian dollar, requires that we set the bar even higher. It's a challenge I am confident we'll meet thanks to our recently announced restructuring programs, the acquisition of low cost manufacturing facilities in Mexico and the growing importance of our product sourcing and manufacturing relationships in Asia.

A commitment to good corporate governance We have also continued to strengthen our board with the addition of four new directors whose experience will prove to be crucial in guiding CFM through its next stage of development. This seasoned group of business leaders includes David Colcleugh, Past Chairman and President of Dupont Canada Inc., Paul Houston, President and CEO of Alderwoods Group Inc., John Mayberry, former Chair and CEO of Dofasco Inc. and Bruce Mitchell, Chairman and CEO of Permian Industries Limited.

At the same time, we have continued to enhance the company's approach to corporate governance. During the past year, we have implemented important changes to our corporate governance policies that reflect our commitment to the highest possible standards of individual and corporate integrity. You can learn more about CFM's approach to corporate governance, as well as the qualifications and experience of our board of directors, on pages 14 and 15.

A word of thanks Once again, CFM's progress has been made possible by the more than 2,700 employees whose everyday commitment has helped us deliver strong financial results while building a stronger foundation for the future. I would also like to thank Jim Lutes, CFM's Former President and Chief Operating Officer, for his contribution in building CFM to what it is today. With the continued dedication of our employees and the support of our valued customers, I know that CFM's growth and evolution will continue and that the best is yet to come.

| SINCERELY, | COLIN ADAMSON | COLIN ADAMSON |

| CHAIRMAN AND | ||

| CHIEF EXECUTIVE OFFICER |

CFM CORPORATION 2003 ANNUAL REPORT 5

CFM's emphasis on quality, convenience and design has created a strong foundation for growth in home products. The Vermont Castings' Encore wood stove (main photo) combines old-fashioned charm with market-leading features like a thermostatically controlled temperature system. Also featured: the Dragonfire outdoor gas log set; the Sequoia direct vent fireplace; the DynaGlo propane portable space heater; and Vermont Castings' VC200 gourmet barbeque.

we are...

creating

a strong

foundation

Since its creation in 1987, CFM has evolved from a small regional hearth manufacturer into a diversified home products company with annual sales of $686 million.This thriving foundation was built around our core hearth business which, thanks to strong internal growth and a series of timely acquisitions has made us a leader in the North American hearth industry, with an unsurpassed reputation for quality and innovation.

| More recently, CFM has leveraged its expertise in burner technology and metal fabrication to create a growing line-up of high-margin, high-quality home products. In 2000, we created our first Vermont Castings barbeque and sold a few units through a receptive dealer network. By the end of fiscal 2003, revenues from our barbeque and outdoor products had reached $216 million and our growing range of customers included North America's largest home improvement retailers and mass merchants. In October 2002, our evolution into a leading home products company accelerated with the acquisition of Greenway Home Products, a Canadian-based manufacturer of home water purification, filtration and dispensing products. Sales of CFM's newest business have grown to $17 million in one year as we leveraged CFM's strong retail presence across North America. This new business has allowed CFM to gain access to many new customers including major retailers such as Sears Canada, Best Buy, Target and Office Depot. By the same token, CFM Greenway has enabled us to expand existing relationships with another category of high-quality home products. Together, these businesses have given CFM a strong presence in the home products business and many arrows in our quiver to expand upon hard-earned relationships with North America's leading retailers. |

CFM CORPORATION 2003 ANNUAL REPORT 7

CFM has leveraged its manufacturing expertise and retail presence to enter a growing number of high-margin home product markets. Products such as the Vermont Castings VC400 Connoisseur Series grill (main photo) have helped vault CFM into a leading position in the North American barbeque industry. Also featured: a Polar brand portable ice machine, the VC200 barbeque, the Vitapur whole-home water purification system, and the Pyromaster electric fireplace.

we are...

doing more

of what we

do best

| One of the primary contributors to CFM's growth is an unwavering focus on product development and innovation. We are industry leaders in research and development and we concentrate our resources on meeting emerging consumer needs with products that are known for their quality, good looks and convenience. CFM's innovative electric fireplaces are a case in point. Working in partnership with retail customers, CFM helped to create an innovative product segment that has extended the warmth and ambience of a fireplace to an entirely new set of customers. The same spirit of innovation applies to our water business. There is a growing thirst for products like our full range of water purification and filtration products, which answers the call for clean and fresh water on demand at a fraction of the cost of bottled water. Even more so than in other segments of our business, research and development is key in development of our water purification business. After a year in beta test, our new generation Vitapur whole home UV water purification system is ready to be launched throughout North America. One of the few such systems to earn the National Sanitation Foundation's highest effectiveness rating, this unique point-of-entry system eliminates organic contaminants from the entire household water supply. In addition, a full line of UV technology based products will also be introduced in 2004. In combination with our several new water filtration products planned for introduction in 2004, this expanding product line is designed to deliver unprecedented value and peace of mind to the growing numbers of North American families concerned about water quality and safety. Looking ahead, CFM will continue to take advantage of opportunities to expand customer relationships through new product development. More and more, our retail distributors prefer to work with a smaller number of full-service providers who can provide expanding lines of higher margin home products with full sales and service support. With a heritage of innovative product development, and proven capabilities in retail program management, CFM is an increasingly preferred supplier. |

CFM CORPORATION 2003 ANNUAL REPORT 9

Higher standards of performance - in our products and our manufacturing facilities - have been driving CFM's growth. The Chateau 44 direct vent fireplace (main photo) combines the warmth of traditional open-hearth masonry with modern electronics and easy installation. Also featured: manufacturing facilities in China and Mexico (bottom photos) are lowering costs for high-volume hearth, barbeque and water products.

we are...

raising the bar

on performance

CFM has produced a remarkable track record of growth over the years while creating or pursuing leading market positions in each of its chosen businesses. We've done it by bringing innovative consumer products to market, by expanding our distribution channels and by developing or acquiring the businesses we need to deliver a growing line of high-value-added products and services to our customers. This natural inclination for growth isn't about to change at CFM, but we've reached a new stage in the company's evolution - one in which we are applying the same kind of energy to a wide range of productivity and margin enhancement initiatives.

| In November, we hired our first Vice President of Procurement and plan to quickly move to unleash the benefits of centralized buying programs with targeted significant annual cost savings. We also announced plans to rationalize certain production facilities and distribution centres throughout our mass merchant operations. We plan to consolidate four manufacturing plants and four warehouses as well as the back office functions within our mass merchant group. At the same time, we've introduced a consolidated mass merchant distribution strategy that maximizes efficiency of the network while improving customer service. We've also recently completed the acquisition of Temtex Industries, a small manufacturer of gas fireplaces in the southwestern U.S. In addition to acquiring a business that will be integrated into our existing hearth operations and provide a positive contribution to earnings from day one, the Temtex acquisition provides a solid low-cost manufacturing presence in Mexico. With Temtex's Mexican facility as a base, we plan to move other existing high-volume, price sensitive product lines to Mexico to further reduce our overall cost of manufacturing. We are also continuing to source more product from China and other parts of Asia to enhance our competitive position. This includes everything from the manufacture of hearth and barbeque components to the production of CFM Greenway water dispensers and purification products, RMC space heaters and some lower priced barbeques. It's a trend that may include new partnerships, acquisitions, and even greenfield operations as we continue to improve quality and minimize production costs. |

CFM CORPORATION 2003 ANNUAL REPORT 11

we are...

staying nimble

and focused

(from left to right) PETER PLOWS - Senior Vice President, Operations DAVID BRASH - Director, Corporate Finance CATHERINE GRIFFIN - Corporate Controller COLIN ADAMSON - Chairman and Chief Executive Officer J. DAVID WOOD - Vice President and Chief Financial Officer PAUL KROETSCH - Treasurer SONYA STARK - Director, Legal Affairs, Investor Relations and Corporate Secretary DAVID MYERS - Vice President and Chief Human Resources Officer MARK PROUDFOOT - President and Chief Operating Officer EILEEN FOLEY - Director, Tax EDDIE CHOW - Vice President, Information Technology SCOTT DUNLOP - Vice President, Corporate Development and General Counsel

At CFM, our success has always been fuelled by a uniquely entrepreneurial culture - one that has encouraged risk taking, innovation and individual responsibility in meeting performance objectives. During the past year, we implemented a series of initiatives that are designed to foster those behaviours despite the increasing scale and complexity of our business.

In October 2003, CFM implemented a series of organizational changes that are designed to devolve authority to newly empowered category managers while further strengthening our relationships with customers. In each of our product areas - from electric fireplaces to hearth accessories to space heaters - we have moved managers into place and given them responsibility for these lines of business. Similar responsibility has been assigned to the men and women who manage our relationships with customers in the dealer and mass merchant retail sales channels. Together, these sales and product specialists are forming fluid, nimble business teams - small enough to drive product sales and responsive enough to deliver the kind of service that will set us apart in the eyes of our customers.

CFM CORPORATION 2003 ANNUAL REPORT 12

| CFM implemented important organizational changes in 2003 that are designed to foster an entrepreneurial style of management while accommodating the increasing scale and complexity of the Company's business. These changes reflect a complementary focus on strong customer relationships and operating improvements. Within the new structure, Dan Downing and Steve Haramaras, along with their respective management teams at CFM Specialty Home Products and CFM Home Products, are focused on determining the distinct needs of our customers in the dealer and mass merchant retail channels. Delivering the innovative products they require on a timely and profitable basis is the responsibility of newly appointed management teams for each of our major product lines: fireplace, stove, grill, grill accessories, water and portable comfort products. |

(from left to right) MIKE COOK - Vice President, Sales, CFM Home Products MICHAEL MILLER - Managing Director, CFM Europe Limited DAVID JAKOB - Vice President and General Manager, CFM Grill Group SHEILA HAMILTON - Vice President, Customer Service, CFM Specialty Home Products PETER OLIEROOK - Vice President, Operations, CFM Home Products STEVE HARAMARAS -President, CFM Home Products DOUG GREENWAY - Vice President and General Manager, CFM Water Group DAN DOWNING - President, CFM Specialty Home Products MIKE BURNS - Vice President, Sales, CFM Specialty Home Products STEVE McCALLEY - Vice President and General Manager, CFM Portable Comfort Products DICK ANDERSON - Vice President and General Manager, CFM Fireplace Group DALE TROMBLEY - Vice President and General Manager, CFM Stove Group PETER ALBION - Vice President and General Manager, CFM Grill Accessories Group

On a broader scale, we'll also continue to promote successful attitudes and behaviours throughout CFM's operations with the support of our incentive compensation, profit sharing and equity compensation plans.

At the same time, we remain a company with a genetic predisposition toward growth and evolution. Over the years, CFM has developed a set of core skills that allows us to recognize opportunity, accurately measure value, assimilate new businesses, and migrate best practices across our operations. We will keep taking advantage of these abilities as CFM continues to grow and evolve in the years ahead.

CFM CORPORATION 2003 ANNUAL REPORT 13

CORPORATE GOVERNANCE

Good corporate governance depends on an effective board of directors. That's why CFM has recruited a diverse group of business leaders whose experience, judgement and integrity provide a wide perspective on the issues affecting the Company. Nine of CFM's ten directors are unrelated as defined by the TSX Guidelines for Corporate Governance. This means that they are considered independent of management and free from any interest or relationship (other than shareholdings) that could materially interfere with their ability to act in the best interests of the Company.

we are...

committed to

good governance

At CFM, we believe that good corporate governance is essential in the effective management of our company. That's why we work hard to ensure that CFM's Corporate Governance and Disclosure Policies are in full compliance with current rules, guidelines and standards, and make a dedicated effort to continually improve these systems.

The past couple of years have been busy for CFM on the governance front with the appointment of four new independent board members. The Company also implemented several other important initiatives designed to position the Company in compliance with the Sarbanes-Oxley Act as well as several other developing best practices including:

- The appointment of an independent lead director.

- The adoption of formal disclosure controls and procedures.

- Certification of our annual audited financial statements.

- The review of our interim financial statements by our auditors.

- The adoption of expanded charters for all Board committees.

- A policy of mandatory share ownership for directors.

- Publishing of director biographies and board attendance records.

You can read more about these initiatives in CFM's Management Information Circular dated December 31, 2003.

CFM CORPORATION 2003 ANNUAL REPORT 14

(from left to right) PATRICK KEANE, COLIN ADAMSON, PAUL HOUSTON, CARLO DE PELLEGRIN, BRUCE MITCHELL, WILLIAM CULLENS, WILLIAM CORBETT, JOHN MAYBERRY, HEINZ RIEGER and DAVID COLCLEUGH

| Director since 1992 | Director since 1994 | Director since 2003 |

| COLIN ADAMSON co-founded CFM Corporation in | CARLO DEPELLEGRIN has been a Partner | JOHN MAYBERRY is the former Chairman and |

| 1987 and since then has held senior positions in the | of Williams & Partners, Chartered Accountants LLP | CEO of Dofasco Inc. and a former Director and Chairman |

| company including Vice President, Secretary & Treasurer | since 1997. Mr. De Pellegrin received his B.A. from | of the International Iron and Steel Institute. During his 36- |

| from 1987 to 1994, President from 1994 to 1996, Chief | the University of Toronto in 1969 and earned his | year career with Dofasco, he was appointed Vice |

| Executive Officer since 1994 and Chairman since 1996. | CA designation with PricewaterhouseCoopers in 1972 | President and Works Manager in 1987, Executive Vice |

| In recognition of his achievements, Colin received the | where he worked with large public corporations | President in 1989, President and CEO in 1993 and |

| Ontario Entrepreneur of the Year Award in the Manu- | and private companies. From 1972 to 1977 he worked | Chairman in 2002. Mr. Mayberry is also a director of Inco |

| facturing - Consumer Products sector in 1999. Mr. Adamson | in private industry, primarily within the construction, | Inc., the Bank of Nova Scotia, Decoma International, |

| is on the Board of four private holding companies. | real estate development and manufacturing sectors. | Tradeport International and Hatchcos Holdings. |

| Mr. De Pellegrin is on the boards of two private | ||

| Director since 2002 | companies and one non-profit organization and is a | Director since 2003 |

| DAVID COLCLEUGH is the former Chairman of | member of the Institute of Corporate Directors. | BRUCE MITCHELL is Chairman, CEO and owner |

| Dupont Canada and was the President and CEO of the | of Permian Industries Limited whose subsidiaries include | |

| company from 1997 to 2003. Mr. Colcleugh received his | Director since 2003 | Ajax Precision Manufacturing Limited, Integrated Solutions |

| Ph.D. from the University of Toronto and joined Dupont | PAUL HOUSTON is President and Chief Executive | Group Inc. and Trophy Foods Inc. After receiving his B.Sc. |

| Canada in 1963 as a Research Engineer. He held a number | Officer of Alderwoods Group Inc. (formerly the Loewen | in Civil Engineering from Queens University in 1968 and |

| of senior positions with E.I. Dupont over the years | Group) and has held senior management and board | an MBA from Harvard in 1970, Mr. Mitchell was a |

| including Principal Consultant, Corporate Plans at | positions with several international companies. Prior to | Management Consultant and Principal at Woods Gordon |

| Dupont's global headquarters in Wilmington, Delaware | joining Alderwoods Group, Mr. Houston served as the | and Company from 1972 to 1976, Chairman of Corvair |

| and President of Dupont Asia Pacific in Tokyo, Japan. | President and CEO of Scott's Restaurants from 1995 to | Oils from 1994 to 1997 and Chairman of Promanad |

| Mr. Colcleugh is on the boards of Hudson's Bay Co. and | 1999 and President and CEO of Blacks Photo Corporation | Communications from 1991 to 1998. Mr. Mitchell is on |

| Zenon Environmental Inc. | from 1992 to 1995. Mr. Houston is a director of | the boards of Bank of Montreal, GSW Inc., Permian |

| Alderwoods Group Inc. | Industries Ltd., Trophy Foods Inc., and Integrated Solutions | |

| Director since 2003 | Group Inc. | |

| WILLIAM CORBETT is the former Chairman of | Director since 2002 | |

| The New Providence Development Company, a real | PATRICK KEANE founded Keanall Holdings Ltd., a | Director since 1992 |

| estate development firm. Following graduation from | manufacturer and distributor of quality aftermarket | HEINZ RIEGER is the former Chairman and |

| the University of Toronto (B.Comm 1953) and Osgoode | barbeque parts and accessories, in October 1981 and | Co-Founder of CFM Corporation. Mr. Rieger immigrated |

| Hall Law School in 1957, Mr. Corbett practised with | served as the company's President and Chief Executive | to Canada in 1957 and for the next 11 years worked in |

| Fraser and Beatty until his retirement in 1995, primarily | Officer from that time until December 2001. After selling | the construction and sheet metal industries, primarily |

| in corporate and securities law. He was appointed Vice | Keanall Holdings to CFM Corporation in January 2002, | engaged in manufacturing, engineering and design. In 1968 |

| Chairman of Fraser and Beatty in 1986 and Chairman of | Mr. Keane became the Company's Executive Vice President | he earned his Bachelor of Commerce degree from |

| the firm in 1989. Mr. Corbett is a director of Windfields | of Operations. In June 2003, Mr. Keane resigned his | Concordia University and subsequently worked in the |

| Farm Limited. | position as Executive Vice President of Operations but | stove and fireplace industries in various manufacturing, |

| continues as a director of the company. Mr. Keane is on | production and R&D-related capacities. Mr. Rieger is on | |

| Director since 1994 | the boards of two private holding companies. | the Board of Koralm Holdings Inc. |

| WILLIAM CULLENS is the former Chairman and | ||

| Chief Executive Officer of Canron Inc., a leading Canadian | Full biographies are included in the Management Information | |

| industrial manufacturer. Upon graduating from the | Circular dated December 31, 2003. | |

| University of Glasgow with a B.Sc. in Civil Engineering, | ||

| Mr. Cullen held a variety of senior engineering positions | ||

| before joining Canron in 1960. He was appointed President | ||

| and Chief Executive Officer of the company in 1980 and | ||

| served as Canron's chairman from 1990 until his retirement | ||

| in 1997. Mr. Cullens is on the Board of Ivanco Inc. |

CFM CORPORATION 2003 ANNUAL REPORT 15

MANAGEMENT'S DISCUSSION AND ANALYSIS

INTRODUCTION

The following management's discussion and analysis ("MD&A") provides a review of important events, the results of operations of CFM for the year ended September 27, 2003, in comparison with those for the year ended September 28, 2002, and a review of the financial position of CFM Corporation ("CFM") as at September 27, 2003. This MD&A should be read in conjunction with CFM's audited consolidated financial statements for the year ended September 27, 2003, and the accompanying notes.

CFM is a leading integrated manufacturer of home products and related accessories in North America and the United Kingdom. CFM designs, develops, manufactures and distributes a line of hearth products, including gas, wood-burning and electric fireplaces, free-standing stoves, gas logs, and hearth accessories. CFM also manufactures and imports barbeques, barbeque parts and accessories, water dispensing and purification products, outdoor garden accessories and imports indoor and outdoor space heating products. The Company maintains an ongoing program of research and development aimed at continually improving the quality, design, features and efficiency of its products.

This MD&A contains forward-looking statements that reflect CFM's current expectations concerning future results and events. These forward-looking statements generally can be identified by the use of statements that include phrases such as "believed," "expect," "anticipate," "intend," "foresee," "likely," "will" or other similar words or phrases. These forward-looking statements involve certain risks and uncertainties, which could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Important factors that could affect these statements include, without limitation, those risks and uncertainties listed under the heading "Risks and Uncertainties" below. CFM considers the assumptions on which these forward-looking statements are based to be reasonable at the time they were prepared, but cautions the reader that these assumptions regarding future events, many of which are beyond the control of CFM, may ultimately prove to be incorrect. In addition, CFM does not assume any obligation to publicly update any previously issued forward-looking statements.

YEAR ENDED SEPTEMBER 27, 2003 RESULTS OF OPERATIONS

CFM's consolidated sales increased 19% to $685.7 million for the year ended September 27, 2003, compared to $576.2 million in the prior year. Excluding the impact of exchange rate fluctuations on the translation of the Company's U.S. dollar revenues, sales grew by 25% due primarily to increased volume with minimal effect from changes in selling prices. This significant growth was reduced by 6% as a result of the negative impact on the Company's sales caused by the strengthening of the Canadian dollar against the U.S. dollar in the year when compared to the prior year, which led to a reduction in the Canadian dollar value of the U.S. dollar sales of the Company's subsidiaries from the value of such sales based on the exchange rates in effect last year. The average exchange rate used to translate the Company's U.S. dollar revenues and expenses to Canadian dollars for the year ended September 27, 2003 was $1.4675, representing a 7% reduction from the rate of $1.5731 used last year.

Sales by product category and geographic segment were as follows:

| 12 months ended | September 27 | September 28 |

| (in millions of dollars) | 2003 | 2002 |

| $ | $ | |

| Hearth and heating products | 452.6 | 443.2 |

| Barbeque and outdoor products | 216.4 | 133.0 |

| Water products | 16.7 | - |

| 685.7 | 576.2 | |

| United States | 534.8 | 472.8 |

| Canada | 118.7 | 81.6 |

| Other | 32.2 | 21.8 |

685.7 | 576.2 |

Sales of hearth and heating products were $452.6 million in the year, an increase of 2% from the prior year. Sales volume growth in the year was $35.2 million or 8% when compared to the prior year; however, this growth was reduced by 6% due to the impact of the strengthening Canadian dollar on the conversion

CFM CORPORATION 2003 ANNUAL REPORT 16

of the Company's U.S. dollar revenues. Of the year-over-year increase in sales volume, 44% was the result of volume increases across most products and channels and 56% resulted from significant growth in sales of heating products from new customer placement. The overall sales growth for the year was achieved despite lower fourth quarter sales when compared to the fourth quarter last year as a result of the loss of placement of certain hearth products with a major customer for their hearth program in calendar 2003. As previously announced, in May, 2003, CFM lost a significant portion of the placement of hearth products it had obtained with a major customer during the previous fiscal year due to competitive pressures. The loss of this product placement resulted in a decline of sales of hearth and heating products of $16.4 million in the fourth quarter when compared to sales of these products in the fourth quarter of fiscal 2002. Sales growth during the year was also reduced by significant product returns of hearth products from certain large mass merchant retail customers following the end of the hearth season in calendar 2002. This unusually high level of returns arose primarily as a consequence of balancing excess end-of-season inventories of hearth products by these customers. Although a certain level of product returns is inevitable in the normal course of doing business with certain large mass merchant customers, it is not CFM's practice or policy to accept significant returns of excess or overstocked inventories from customers. In order to further reduce the risk of being faced with a request for significant product returns in the future, management has implemented new processes designed to enable the Company to work with its customers to monitor and manage the level of inventories carried by these customers during their selling season. Had these product returns not occurred, sales for the year would have increased by an additional $11 million.

Sales of barbeque and outdoor products were $216.4 million in the year, an increase of $83.4 million or 63% from the prior year. Sales volume growth in the year was $90.8 million or 68% when compared to the prior year, however, this growth was reduced by 5% due to the impact of the strengthening Canadian dollar on the conversion of the Company's U.S. dollar revenues. The sales increase was partially a result of the incremental sales of barbeque grills of $45.6 million at The Great Outdoors Grill Company ("TGO"), which was acquired by CFM in the third quarter of fiscal 2002. Continuing sales success with domestically manufactured and imported barbeque grills and accessories and expanded placement of product to existing customers increased sales by a further 33%.

Greenway Home Products Inc. ("Greenway"), acquired on October 3, 2002, generated $16.7 million of incremental sales of water dispensing and purification products in the year.

Sales in the year grew in all geographic segments. Growth in sales in both the United States and Canada in the year was primarily due to the increased sales of barbeque products noted above.

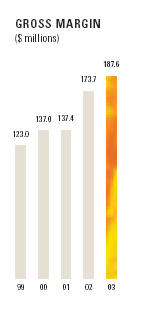

GROSS PROFIT

Gross profit increased by $13.9 million or 8% from the prior year to $187.6 million. As a percentage of sales, gross profit decreased to 27.4% from 30.1% in the previous year.

In addition to the higher sales, several factors contributed to the growth in gross profit in the year. The most significant factor was the improved operating efficiencies experienced at the Company's Canadian barbeque manufacturing operation which lowered manufacturing costs by approximately $3.0 million when compared to the same period a year ago. Gross profit was further enhanced by lower relative distribution costs in the year as compared to the prior year as distribution costs grew approximately 18% in support of a 25% increase in sales volume.

Despite the increase in gross profit during the fiscal year ended September 27, 2003, several factors contributed to a decline in gross profit as a percentage of sales. The unusually high level of customer returns referred to above are estimated to have contributed to a 1% drop in gross profit as a percentage of sales for the year ended September 27, 2003 when compared to the year ended September 28, 2002. Sales of barbeque grills and accessories, which generally sell at margins lower than the historic margins realized on hearth products, accounted for 32% of sales in the year ended September 27, 2003 in comparison with 23% for the year ended September 28, 2002. Management estimates that this shift in sales mix contributed to an approximate 1% drop in the overall gross margin percentage for the year ended September 27, 2003.

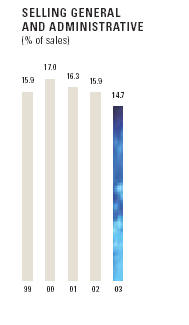

SELLING, ADMINISTRATIVE, RESEARCH AND DEVELOPMENT EXPENSES

Operating expenses for the year increased $9.2 million or 10% to $100.9 million when compared to the prior year. Before the effect of the Canadian dollar strengthening and the related positive impact on translation of U.S. dollar expenses, overall operating expenses increased by 14% compared to the same period a year ago. The incremental increase in expenses relates primarily to the addition of the Greenway and TGO operations. The positive impact of the strengthening Canadian dollar on the translation of U.S. dollar expenses into Canadian dollars offset this real increase in expenses. The increase in operating expenses of 10% was realized relative to a 19% increase in sales and as a result operating expenses, as a percentage of sales, declined to 14.7% from 15.9% in the prior year.

CFM CORPORATION 2003 ANNUAL REPORT 17

MANAGEMENT'S DISCUSSION AND ANALYSIS

RESTRUCTURING COSTS

As previously announced, the Company initiated a plan to restructure its operations in order to better realize benefits available from a number of acquisitions completed during the last several years. The restructuring will focus on streamlining operating processes and consolidation of facilities which serve the Company's mass merchant customers and improving the Company's manufacturing operations through anticipated product line rationalization and shifting manufacturing of certain product lines to lower wage cost locations. The restructuring will be completed in stages and will involve the closure of certain of the Company's manufacturing locations and the transfer of manufacturing and administrative activities, as well as certain assets, to other CFM facilities. In addition, as part of this restructuring, several of the Company's warehouses in the United States will be closed and distribution centralized into two larger distribution centres to more efficiently serve the Company's mass merchant customers. Management anticipates annualized savings from the restructuring to exceed $15 million and expects to begin to realize these savings in the later half of fiscal 2004. Currently, management expects the restructuring activities to be completed by the end of fiscal 2004.

In connection with this restructuring, CFM anticipates incurring restructuring costs, including the write-off of certain fixed assets and inventory, within the range of $30 million to $35 million. Of these total costs, CFM anticipates non-cash expenses for the impairment in the value of inventory and accelerated amortization of fixed assets to be within the range of $20 million to $25 million, with the balance of the restructuring costs related to employee relocation, termination and severance, termination of certain leases and other contracts and asset relocation. In accordance with Canadian Generally Accepted Accounting Principles ("GAAP"), these restructuring costs will be recognized and expensed in the period the actual cost or liability for the cost is incurred.

As of September 27, 2003, the following restructuring costs had been incurred:

| (in millions of dollars) | |

| $ | |

| Provision for severance and benefits | 0.3 |

| Asset impairment: | |

| Inventory | 4.0 |

| Fixed Asset | 3.7 |

8.0 |

As of September 27, 2003, none of the restructuring charges listed above had been paid.

EBITDA BEFORE RESTRUCTURING COSTS*

Earnings before interest, taxes, amortization and restructuring costs ("EBITDA before restructuring costs") were $86.8 million, up $4.8 million or 6% from the prior year as a result of the significant sales increase and improved gross profit without a commensurate increase in operating expenses. EBITDA margins before restructuring costs were 12.7%, down from 14.2% last year. The decline in EBITDA margins before restructuring costs is primarily attributable to the above-noted decline in gross profit as a percentage of sales. The following is a reconciliation of EBITDA before restructuring costs to net income for the year:

| For the 12 months ended | September 27 | September 28 |

| (in millions of dollars) | 2003 | 2002 |

| $ | $ | |

| Net income for the period | 35.9 | 42.1 |

| Add back (deduct): | ||

| Restructuring costs | 8.0 | - |

| Amortization | 17.3 | 13.3 |

| Interest income | (0.2) | (0.2) |

| Interest expense | 8.3 | 7.1 |

| Income taxes | 17.5 | 19.7 |

| EBITDA before restructuring costs | 86.8 | 82.0 |

* EBITDA before restructuring costs is defined as earnings before the taking of any deductions in respect of interest, taxes, amortization and restructuring costs. EBITDA before restructuring costs is presented before deductions for interest expense and income, tax expense, amortization and restructuring costs as this is a widely accepted measure of a company's normal operating performance. EBITDA before restructuring costs has been determined by taking net income for the period from the Consolidated Statement of Operations and adding to it interest expense and income, amortization

CFM CORPORATION 2003 ANNUAL REPORT 18

and income taxes and restructuring costs which are disclosed as individual line items within the Consolidated Statement of Operations. EBITDA margin before restructuring costs is defined as EBITDA before restructuring costs expressed as a percentage of sales.

EBITDA before restructuring costs, and EBITDA margin before restructuring costs are not recognized measures for financial statement presentation under GAAP. Non-GAAP measures (such as EBITDA before restructuring costs and EBITDA margin before restructuring costs) do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other issuers. Investors are encouraged to consider these financial measures in the context of CFM's GAAP results, as provided in the attached financial statements.

NET INTEREST EXPENSE

Net interest expense of $8.2 million for the year ended September 27, 2003 increased $1.4 million over the prior year. Interest costs increased primarily due to higher rates. Weighted average interest rate on the Company's bank debt was 5.41% for the year, up from 4.44% last year.

NET INCOME

Net income for the year ended September 27, 2003 was $35.9 million, down 15% from $42.1 million in the previous year. The decline is primarily due to the impact of the restructuring costs discussed above. Higher amortization expenses of $4.0 million related to fixed asset additions in fiscal 2002 and 2003 and higher net interest expense, as mentioned above, also contributed to reduced earnings. In addition, strengthening of the Canadian dollar had a negative impact on net income. As mentioned above, the strengthening of the Canadian dollar against the U.S. dollar had an impact on the translation of the Company's U.S. dollar revenues and expenses as well as on the Company's U.S. dollar raw material purchases this year as compared to a year ago. The negative impact of the translation of U.S. dollar denominated earnings to Canadian dollars was partially offset by lower manufacturing costs realized through foreign exchange gains on U.S. dollar raw material purchases within the Company's Canadian manufacturing operations. Management believes that the overall net effect of the strengthening Canadian dollar during the fiscal year ended September 27, 2003 has been a reduction in net income in the range of $3.5 million to $4.5 million when compared to the prior year.

EARNINGS PER SHARE

Earnings per share ("EPS") for fiscal 2003 were $0.89 compared to $1.06 earned in the previous year. The restructuring charges discussed above accounted for $0.12 of the overall decline in EPS. Earnings per share before restructuring costs* were $1.01, a $0.05 or 5% decrease from $1.06 earned in the prior year. The strengthening of the Canadian dollar against the U.S. dollar had a negative impact on EPS for the year. Management believes earnings per share before restructuring costs would have been approximately $1.11 but for the impact of the strengthening Canadian dollar. In addition, the increase in the weighted average number of shares (see below) contributed to a further $0.01 reduction in EPS. The following is a reconciliation of earnings per share before restructuring costs to earnings per share for the year:

| For the 12 months ended | September 27 | September 28 | ||||

| (in millions of dollars, except earnings per share amounts) | 2003 | 2002 | ||||

| Earnings | EPS | Earnings | EPS | |||

| Net income | 35.9 | $ | 0.89 | 42.1 | $ | 1.06 |

| Restructuring costs | 8.0 | $ | 0.20 | - | $ | - |

| Income tax related to restructuring costs | (3.2) | $ | (0.08) | - | $ | - |

| Earnings before restructuring costs | 40.7 | $ | 1.01 | 42.1 | $ | 1.06 |

The weighted average number of shares outstanding increased to 40,215,000 from 39,836,000 in fiscal 2002 primarily as a result of shares issued in connection with the making of the first contingent payment due in connection with the acquisition of Greenway (126,494 shares), and as a result of shares issued on the exercise of stock options in the year (358,840 shares) plus the full year effect of the 2,526,314 shares issued in connection with the 2002 purchase of Keanall, partially offset by the repurchase of 685,600 shares in the year under the Company's Normal Course Issuer Bid.

Diluted EPS was $0.88, a $0.15 or 15% decrease from $1.03 last year as a result of lower overall earnings per share. The restructuring charge accounted for $0.12 of the overall decline in diluted EPS.

* Earnings per share before restructuring costs have been determined by taking net income for the applicable period, adding to it the restructuring costs, deducting provision for income taxes applicable to the restructuring charge to arrive at net income before restructuring costs for the applicable period and dividing net income before restructuring costs by the average number of shares outstanding during such period. Earnings per share before restructuring costs is presented as a measure of the normal operating performance of the Company. Earnings per share before restructuring costs is not a recognized measure for financial statement presentation under GAAP. Non-GAAP measures (such as earnings per share before restructuring costs) do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other issuers. Investors are encouraged to consider these financial measures in the context of CFM's GAAP results, as provided in the attached financial statements.

CFM CORPORATION 2003 ANNUAL REPORT 19

MANAGEMENT'S DISCUSSION AND ANALYSIS

QUARTERLY FINANCIAL RESULTS

(in millions of dollars, except earnings per share amounts)

| Q1 | Q2 | Q3 | Q4 | Full Year | ||||||||||||||||

| 2003 | 2002 | 2003 | 2002 | 2003 | 2002 | 2003 | 2002 | 2003 | 2002 | |||||||||||

| $ | $ | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||

| Sales | 179.9 | 127.7 | 148.4 | 113.1 | 171.8 | 152.4 | 185.6 | 183.0 | 685.7 | 576.2 | ||||||||||

| Net income | 16.5 | 13.9 | 4.4 | 6.3 | 10.1 | 7.3 | 4.9 | 14.6 | 35.9 | 42.1 | ||||||||||

| EBITDA* | 31.3 | 25.4 | 11.8 | 13.2 | 21.4 | 15.8 | 22.3 | 27.6 | 86.8 | 82.0 | ||||||||||

| Per share | ||||||||||||||||||||

| Earnings | $ | 0.41 | $ | 0.37 | $ | 0.11 | $ | 0.15 | $ | 0.25 | $ | 0.18 | $ | 0.12 | $ | 0.36 | $ | 0.89 | $ | 1.06 |

| Earnings before restructuring costs* | $ | 0.41 | $ | 0.37 | $ | 0.11 | $ | 0.15 | $ | 0.25 | $ | 0.18 | $ | 0.24 | $ | 0.36 | $ | 1.01 | $ | 1.06 |

| Diluted earnings | $ | 0.39 | $ | 0.36 | $ | 0.11 | $ | 0.15 | $ | 0.25 | $ | 0.18 | $ | 0.12 | $ | 0.35 | $ | 0.88 | $ | 1.03 |

* see previous note regarding EBITDA and earnings per share before restructuring costs

CASH FLOW

In fiscal 2003, CFM generated $66.4 million in cash flow from operations, consumed $17.3 million cash in investing activities and consumed another $41.4 million in financing activities. In addition, the effect of exchange rate fluctuations and foreign currency translation on cash and cash equivalents resulted in a further $1.3 million use of cash. The net effect of the above resulted in a net increase in cash during the year of $6.4 million.

The $66.4 million in cash flow from operations generated by CFM in the year ended September 27, 2003, compares to $50.2 million generated in the year ended September 28, 2002, an increase of $16.2 million or 32%. This significant increase is primarily due to a $20.3 million lower incremental investment in working capital as compared to the prior year; however, net income, after adding back items not involving cash (including the above described non-cash restructuring costs), decreased by $4.1 million from the prior year, which partially offset the favourable change in working capital investment between years.

Despite the growth in sales in fiscal 2003 and incremental working capital required for the newly acquired Greenway and Century Heating operations (see below), working capital decreased by $8.1 million at September 27, 2003 when compared to September 28, 2002. This was due mainly to the loss of placement of certain hearth products at a major customer for the fall/winter 2003 hearth season as discussed above, which resulted in lower account receivables and inventory as at September 27, 2003 compared to September 28, 2002. As well, the Company's initial inventory investment related to its newly introduced mass merchant grill offering in fiscal 2002 required significantly less new investment in fiscal 2003.

Cash flows from investing activities were $17.3 million for the year ended September 27, 2003, relating principally to capital expenditures of $12.3 million, the payment of the cash portion of the first contingent payment due in relation to the Greenway acquisition in the amount of $1.8 million and $2.2 million paid to acquire certain assets of Century Heating Products, a manufacturer of plate steel wood stoves located in Orillia, Ontario.

Financing activities consumed $41.4 million in net cash. During the year, CFM completed the issuance of US$125 million of ten-year senior unsecured notes through a private placement (see discussion under "Financial Position, Liquidity and Capital Resources"). The first US$60 million (CD$82.1 million) of proceeds from this private placement was received on September 12, 2003 and the remaining US$65 million was received subsequent to year-end on November 21, 2003. The proceeds were principally used to repay CFM's existing term bank debt and for general corporate purposes. Additional repayments of existing bank debt were also made which brought total payments of bank debt to $100.9 million. As well, scheduled repayments of $15.0 million were made on the outstanding note payable issued in connection with the acquisition of Keanall in fiscal 2002. As at September 27, 2003, four remaining payments totalling $5.0 million were outstanding in relation to this note. In addition, with the objective of maximizing return on capital employed, CFM purchased and cancelled 685,600 of its outstanding shares at an average price of $11.78 per share during the year ended September 27, 2003 for a total cash cost of $8.1 million. The issuance of 360,000 shares to employees and directors exercising options previously granted to purchase CFM shares generated $2.8 million in cash flow.

CFM CORPORATION 2003 ANNUAL REPORT 20

FINANCIAL POSITION, LIQUIDITY AND CAPITAL RESOURCES

The seasonal nature of the hearth and heating market and the barbeque market impacts the Company's cash flow and investment in working capital. In both categories, pre-season inventories are built in order to meet the seasonal demands of the Company's customers, which are then converted to accounts receivable as those inventories are sold through the season and ultimately to cash as the accounts receivable are collected. To support the growth of its barbeque products, the Company has and will continue to be required to make additional investments in working capital; however, as the barbeque selling season is counter-seasonal to the Company's traditional hearth business, this additional investment in barbeque-related working capital generally occurs as investment in hearth-related working capital is falling to its lowest point in the cycle. Water products tend to be a less seasonal product category than hearth and barbeque products; however, retailers generally advertise and promote water products to the consumer for the summer and pre-Christmas periods. As a consequence, inventories of water products are built in advance of those periods to meet the anticipated demand.

As CFM's fiscal year end falls in the middle of the hearth season and at the early part of the pre-Christmas water products selling season, working capital at year-end is typically at a high point in the cycle. Consolidated net working capital* at September 27, 2003 was $167.9 million, which compares to $197.9 million at the end of fiscal 2002. The 17% appreciation in the Canadian dollar against the US dollar as at September 27, 2003 when compared to a year ago resulted in an approximate $23.0 million reduction in net working capital when compared to levels at September 28, 2002; however, before the impact of foreign exchange rate fluctuations, consolidated net working capital decreased by $7.0 million when compared to a year ago. As noted previously, this decrease occurred despite continued growth in CFM's business, due primarily to the loss of placement of certain hearth products at a major customer as well as a lower incremental investment in barbeque inventory in 2003.

As part of its capital management, the Company reviews certain working capital metrics. For example, the Company evaluates its accounts receivable and inventory levels through the computation of days' sales outstanding and inventory turnover. After improving significantly in fiscal 2002 over 2001, the number of days' sales outstanding in accounts receivable as at September 27, 2003 remained consistent at approximately 68 days. Despite the incremental inventories from the acquisition of Century Heating and as required to support the rapid growth in CFM's barbeque and water products businesses, inventory turns improved slightly from 3.7 at September 28, 2002 to almost 4.0 at September 27, 2003.

Management expects investment in working capital to decrease in the first quarter of fiscal 2004 as the seasonally high levels of inventories of hearth and heating products and water products are sold through their respective channels and accounts receivable from those sales are collected. Working capital is expected to increase again towards the end of the first quarter and into the second quarter of fiscal 2004 as barbeque inventories are built in anticipation of the upcoming barbeque season.

Net bank debt** at September 27, 2003 was $152.6 million, down $29.0 million from September 28, 2002, due primarily to lower working capital requirements. CFM was capitalized*** as at September 27, 2003 with net bank debt to total capitalization of 32%.

In the fourth quarter of fiscal 2003, CFM completed the sale of US$125 million of senior unsecured notes through a private placement. With long-term interest rates in fiscal 2003 reaching their lowest levels in 45 years, management took advantage of the lower rates to secure long-term cost effective debt financing. The notes were issued in two series with funding on the first series of US$60 million occurring on September 12, 2003 and funding on the second series of US$65 million occurring on November 21, 2003. The proceeds from the sale of these notes were used principally to repay debt under CFM's existing bank credit facilities and for general corporate purposes. The notes have a fixed coupon rate of 6.1% and ten-year maturities with principal due at maturity. In order to hedge against exposure to interest rate increases prior to the coupon rate on the notes being set, the Company entered into a series of interest rate swap contracts. These contracts were settled on August 20, 2003 resulting in the prepayment of interest of approximately $2.0 million. In accordance with GAAP, this prepayment was deferred and will be amortized to interest expense over the ten-year term of the notes.

* Net working capital is defined as accounts receivable, inventory and prepaid expenses less accounts payable and accrued liabilities and tax payable net of any taxes recoverable. Net working capital is presented because it is a widely accepted measure of the extent to which a company has net current assets available to support its operations.

** Net bank debt is defined as bank debt (current and long-term), plus bank indebtedness plus senior unsecured notes payable less cash. This measure is widely accepted by the financial markets as a measure of credit availability.

*** Capitalization is defined as net bank debt plus shareholders' equity. Capitalization is presented as a measure of the Company's total financing structure.

Net bank debt, capitalization and net working capital are not recognized measures for financial statement presentation under Canadian GAAP. Non-GAAP measures do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other issuers. Investors are encouraged to consider these financial measures in the context of CFM's GAAP results, as provided in the attached statements.

CFM CORPORATION 2003 ANNUAL REPORT 21

MANAGEMENT'S DISCUSSION AND ANALYSIS

The unused and available credit under CFM's existing bank credit facilities stood at $106.5 million at September 27, 2003. In conjunction with the issue of the long-term notes referred to above, CFM and its banking syndicate have amended and extended its existing bank credit facilities. Effective November 25, 2003, these credit facilities were amended to provide up to $190 million in revolving term debt for a period which extends to November 25, 2006. The terms under this amended credit facility are largely the same as those under the Company's previous credit facility agreement with the exception of a 25 basis point increase in interest rates under the amended agreement. Approximately $20 million in debt was outstanding under the amended credit facility put in place on November 25, 2003.

CFM will continue to have cash requirements to support its seasonal working capital needs and capital expenditures, as well as to pay interest under its bank credit facility, service its debt and fund share purchases under its Normal Course Issuer Bid. In addition, the restructuring recently initiated by the Company, as discussed above, will place additional demand on the Company's capital resources in fiscal 2004; however, most of the costs anticipated as part of this restructuring relate to the writedown of inventory and fixed assets to reflect the impairment in the value of inventory and accelerated amortization of fixed assets and do not involve cash. In order to meet its cash requirements in fiscal 2004, CFM intends to use internally generated funds as well as the proceeds from the offering of the unsecured notes and its amended credit facilities, as required. Management believes that cash flow from operations, the proceeds from the sale of the unsecured notes and capacity under the amended credit facilities will be sufficient to meet CFM's cash requirements over the remainder of fiscal 2004.

CFM was in compliance with all covenants under its existing bank credit facility and unsecured notes as at September 27, 2003. While the restructuring is anticipated to reduce earnings and, as a result, impact cash flows and borrowing levels in fiscal 2004, management is confident the Company will remain in compliance with its debt covenants throughout 2004 and have access to sufficient levels of financing to operate and grow the Company's business.

TRENDS, RISKS AND UNCERTAINTIES

CFM is subject to a number of the usual risks associated with operating in a durable consumer products industry. These risks include:

General economic conditions, consumer confidence and level of housing starts

Demand for the Company's products is affected by general economic conditions influencing the level of consumer confidence and the level of housing starts. Reduced new home construction activity, as a result of high interest rates or other economic factors, can lead to a reduction in sales by the Company in the hearth and heating market segment. In addition, reduced consumer spending on home improvement items, as a result of interest rate factors or other economic developments, can lead to a reduction in sales by the Company at the retail and mass merchant levels. The Company has taken steps to reduce these risks by diversifying its product portfolio. The Company's barbeque parts and accessories products are less affected by the general state of the economy since, in management's opinion, in a strong economy consumers will tend to purchase new barbeques and barbeque accessories and in a weak economy consumers will tend to purchase barbeque replacement parts, given the relative lower costs of these expenditures. Similarly, demand for the Company's water purification, filtration and dispensing appliances is less sensitive to general economic conditions, given increasing consumer concerns regarding water quality; however, Greenway's other water products, such as portable icemakers and air treatment appliances, involve a greater level of discretion on the part of consumers and, therefore, sales of these products can be influenced by reduced consumer spending levels. With the expansion into barbeque, barbeque replacement parts and accessories and water purification, filtration and dispensing appliances, management believes the Company is positioned to be successful in a variety of economic conditions, although there can be no assurances that reductions in earnings as a result of reduced sales in specific product categories will be fully offset as a result of increased sales in other product categories.

Demographics

Management believes that demographic trends, such as the tendency of aging, affluent baby-boomers to spend more leisure time in larger, better-appointed homes, patios and gardens will contribute to the Company's growth. Management believes that these consumers will be drawn to gas and electric hearth products for their elegance, performance and convenience. Management also anticipates that demand for the Company's increasingly diverse line of other home products, such as the Company's barbeque products, indoor and outdoor space heaters and garden accessories, is poised for growth due to the same demographic trend.

Ability to develop new products

The Company's market position is primarily the result of its ability to effectively anticipate consumer habits and expectations and develop new or modified products in a timely fashion to satisfy these expectations. New product introductions represent a significant portion of gas hearth and barbeque product sales in any given year and management believes that new product introductions will continue to sustain the Company's market share and revenue growth

CFM CORPORATION 2003 ANNUAL REPORT 22

in these parts of its business. While the Company continues to invest significant resources in new product development, should the Company's ability to successfully develop and introduce new products in relation to its competitors be constrained in the future, its results of operations and financial condition could be negatively affected.

Patent protection

The Company continually develops and improves its products and technological processes and management believes that this will enable it to maintain its competitive position. In light of the continuous nature of these developments, the Company does not, except perhaps in the case of substantial improvements, intend to apply for patents covering most of these processes. Consequently, no assurance can be given that others will not independently develop substantially similar technology or that the Company can meaningfully protect such unpatented trade secrets. In addition, even though the Company's current strategy is not focused on patent protection, there can be no assurance that any of the Company's issued patents will be held valid and enforceable, if challenged, or that a competitor will not be able to circumvent an issued patent by the adoption of a competitive, though non-infringing, product or process. Also, no assurance can be given that others do not have or will not obtain patents that the Company would need to license, or that if such a licence is required it would be available on reasonable terms, or that if a licence is not obtained, that the Company will be able to circumvent, through a reasonable investment of time and expense, such outside patents. From time to time the Company has been involved in patent-related litigation that has resulted in the incurring by the Company of significant legal costs. While the Company considers such litigation to be outside the ordinary course of its business, there can be no guarantee that similar claims will not be advanced against it in the future.

Weather and related customer buying patterns and manufacturing issues

Management believes that there have been trends towards more moderate autumn and winter temperatures throughout many parts of North America in recent years. Record warm temperatures throughout these areas in the falls of both 2001 and 2002 had a negative impact on the Company's sales growth as the weather resulted in lower demand for hearth and heating products in the Company's retail hearth and distribution channels. While the Company believes that opportunities for growth in the hearth products and space heating markets remain, recent trends towards more moderate fall and early winter temperatures throughout much of North America create risks of reduced demand for the Company's products. Similarly, for barbeque products, the weather can have an impact on the sales of these products. Barbeque sales are adversely affected by cold and/or wet spring weather as most sales to the Company's customers are made between January and June.

Weather may also extend or delay consumer purchases of certain products. For example, the cold winter temperatures that finally arose in December 2002 and January 2003 extended the hearth and heating season but delayed the commencement of the barbeque season. The Company is able to manage this risk by offering products in both the hearth and heating products category and the barbeque and outdoor products category.