Exhibit 99.1

UIL HOLDINGS CORPORATION

Northeast Utilities Seminar

February 28, 2006

1

Safe Harbor Provisions

Certain statements contained herein, regarding matters that are not historical facts, are forward-looking statements (as defined in the Private Securities Litigation Reform Act of

1995). These include statements regarding management’s intentions, plans, beliefs,

expectations or forecasts for the future. Such forward-looking statements are based on the

Corporation’s expectations and involve risks and uncertainties; consequently, actual

results may differ materially from those expressed or implied in the statements. Such risks

and uncertainties include, but are not limited to, general economic conditions, legislative

and regulatory changes, changes in demand for electricity and other products and services,

unanticipated weather conditions, changes in accounting principles, policies or guidelines,

and other economic, competitive, governmental, and technological factors affecting the

operations, timing, markets, products, services and prices of the Corporation’s

subsidiaries. The foregoing and other factors are discussed and should be reviewed in the

Corporation’s most recent Annual Report on Form 10-K and other subsequent periodic

filings with the Securities and Exchange Commission. Forward-looking statements included

herein speak only as of the date hereof and the Corporation undertakes no obligation to

revise or update such statements to reflect events or circumstances after the date hereof

or to reflect the occurrence of unanticipated events or circumstances.

1995). These include statements regarding management’s intentions, plans, beliefs,

expectations or forecasts for the future. Such forward-looking statements are based on the

Corporation’s expectations and involve risks and uncertainties; consequently, actual

results may differ materially from those expressed or implied in the statements. Such risks

and uncertainties include, but are not limited to, general economic conditions, legislative

and regulatory changes, changes in demand for electricity and other products and services,

unanticipated weather conditions, changes in accounting principles, policies or guidelines,

and other economic, competitive, governmental, and technological factors affecting the

operations, timing, markets, products, services and prices of the Corporation’s

subsidiaries. The foregoing and other factors are discussed and should be reviewed in the

Corporation’s most recent Annual Report on Form 10-K and other subsequent periodic

filings with the Securities and Exchange Commission. Forward-looking statements included

herein speak only as of the date hereof and the Corporation undertakes no obligation to

revise or update such statements to reflect events or circumstances after the date hereof

or to reflect the occurrence of unanticipated events or circumstances.

2

Today’s Topics

Presented by Nathaniel D. Woodson - Chairman & CEO

and

Richard J. Nicholas – Executive VP & CFO

Richard J. Nicholas – Executive VP & CFO

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

3

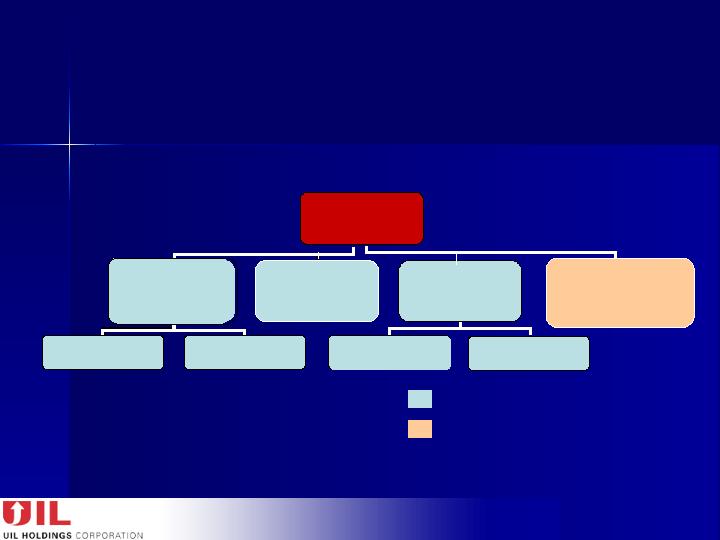

A project and service based business

Operating Businesses

Minority Interest Investment

Divestiture Pending

UIL Holdings

Wholesale Distribution

(Transmission)

*

Operations

CTA

United Illuminating

Retail Distribution

United Illuminating

Xcelecom

Electrical Contracting

Systems Integration

Energy Infrastructure *

United Bridgeport Energy

Cross-Sound Cable

Mechanical Contracting

UIL Holdings Structure

4

The United Illuminating Company (Total) $ 3.08

Distribution $ 1.64

CTA $ 0.88

Transmission $ 0.38

Other $ 0.19

Xcelecom (Total) $(0.15)

Project loss $(0.39)

All Other $ 0.24

UIL Corporate Expenses (Total) $(0.31)

Interest $(0.25)

Administrative $(0.06)

United Capital Investments $(0.03)

United Bridgeport Energy $(0.43)

Total UIL Holdings $ 2.16

Subtotal $ 2.62

2005 Financial Results (EPS)

5

Key Developments in 2005

Ø

4-Year Distribution Rate Case Decision

q

Return on Equity - 9.75%

q

Capital Structure – 48% equity, 52% debt

q

Sales Forecast – 1% per year

q

Earnings sharing 50/50 from first dollar

q

Approved Central Facility Plan

Ø

Transmission

q

Approved Middletown/Norwalk (M/N) Transmission project

q

Transmission Tracker mechanism approved by CT DPUC

q

FERC approved 50% Construction Work in Progress (CWIP)

immediately in rate base

6

Key Developments in 2005 (cont.)

Ø

Infrastructure Divestitures

q

UBE

§

Interest in BE to be sold for $71 million, net proceeds approximately $65

million

§

Resolves certain matters in dispute

§

Expected to close first quarter 2006, subject to FERC approval

q

Cross-Sound Cable

§

Sold for $53.25 million, net proceeds approximately $46 million

§

Sale closed February 27, 2006

Ø

6-Year Union Contract

7

What it Means Going Forward

Ø

Distribution revenue predictability for next 4 years

Ø

Transmission

q

Investment Incentives

q

Enhanced regulatory diversity

q

Market providing higher P/E

Ø

Significant financial flexibility through planned

divestitures

Ø

Labor stability for the next 6 years

8

Strategic Management Guidelines

Ø

Continue to support Dividend

Ø

UIL will stay on course

q

Invest in Regulated Utility Business

Ø

Cash to be managed

q

Support equity base of utility

q

Develop maximum shareholder return

9

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

10

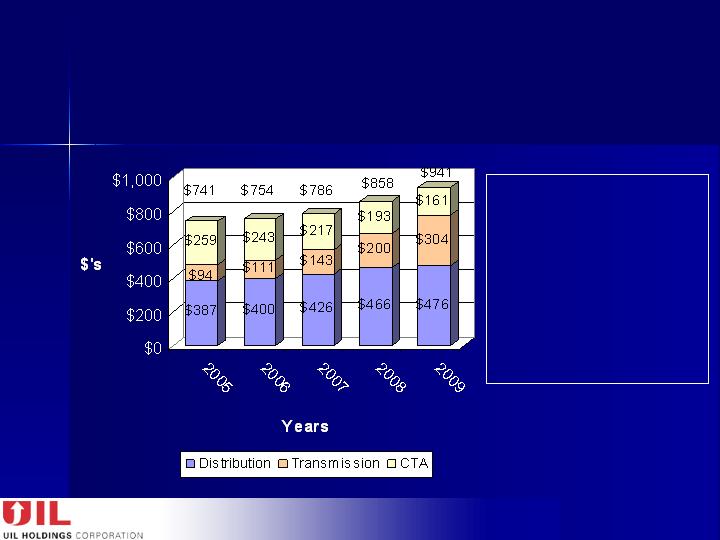

§

Invest in aging distribution

infrastructure

§

M/N project expected to triple

investment in transmission

•

Expected growth in

Transmission rate base -$245

to $275 million

to $275 million

§

CTA expected to be fully amortized

between 2013-2015

•

Provides steady cash flow

Average Rate Base 2005 - 2009

Distribution, Transmission & CTA

11

Middletown

Middletown

Scovill

Scovill

Rock

Rock

S/S

S/S

East Devon

East Devon

S/S

S/S

Singer

Singer

S/S

S/S

Norwalk

Norwalk

S/S

S/S

Beseck

Beseck

S/S

S/S

~

~

~

~

Norwalk

Norwalk

7 Miles of

345kV OH

15 Miles of -

345kV

8 Miles of

-

345kV

3 Miles of

345kV OH

33 Miles of

345kV OH

2 Miles of

345kV OH

UI to Own, Construct

Operate 345kV Singer

&Substation and 5.9

Miles of 345kV

Middletown/Norwalk Transmission Project

Ø

UI to own, construct and operate approximately 20% of total project

Ø

UI’s portion is all underground

Ø

Expected Growth in Transmission Rate Base - $245 to $275 million

12

Transmission

Ø

Transmission tariff fully tracks the FERC-approved

transmission revenue requirements

q

Rates are looking forward

q

Adjusted every 6 months, trued-up annually

Ø

50% of CWIP in rate base – approved

q

Allows earlier recovery of investment

Ø

Attractive RTO ROE

q

12.8% plus 50 basis point participation adder, pending approval and

potential refund

13

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

14

Strategic Objective

United Bridgeport Energy & Cross-Sound Cable

15

United Bridgeport Energy, Inc. (UBE)

Ø

UBE – To be divested

q

33 1/3% ownership interest in Bridgeport Energy, LLC, a 520 MW

gas-fired, combined cycle electric generating facility located in

Bridgeport, Connecticut

Bridgeport, Connecticut

q

Interest in BE to be sold for $71 million, approximate book value

q

Net proceeds approximately $65 million

q

Resolves all matters in dispute

q

Closing expected 1Q 2006, pending approval by FERC

16

Expected Total Cash from BE and CSC – approx. $111 million

Provides Financial Flexibility to Execute Strategy

United Capital Investments, Inc.

(UCI)

Ø

Cross-Sound Cable – Divested

q

25% ownership interest in Cross-Sound Cable Company LLC, an

important transmission line connecting Connecticut to Long

Island under the Long Island Sound

Island under the Long Island Sound

q

Sold for $53.25 million

q

Net proceeds approximately $46 million

q

Sale closed February 27, 2006

17

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

18

Ø

Founded in 1992 and headquartered in Hamden, CT

Ø

Leading provider of Specialty Contracting and

Systems Integrations Solutions

Ø

Operates along I-95 corridor from Boston to Florida,

an area representing more than 25% of the

nation’s commerce

nation’s commerce

Ø

Approximately $401 million in annual revenue:

q

Specialty Contracting $337 million, 84%

q

Systems Integration $64 million, 16%

Ø

19 operating locations in eight states along the

eastern seaboard from 13 acquisitions made

during 1999-2004

during 1999-2004

Xcelecom, Inc.

19

Xcelecom, Inc. - Overview

Ø

Operates in a cyclical industry

Ø

Disappointing results in 2005, loss of $2.1 million

q

Net project loss at Allan/Briteway $5.9 million

q

All other – net income of $3.8 million

Ø

We have the right scale, right management team in

place

Ø

Even with 2005 project loss, cash exposure to UIL

was only $5 million

20

Xcelecom, Inc. - Strategy

Ø

Build on strong performers – address weak

performers

q

Protect and improve operating margins

q

Reduce operating risk

q

Reduce earnings volatility

q

Enhance earnings visibility

Ø

Focused on Operations, Continuing to Eye Value

21

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

22

Financing Options

Ø

No new equity issuance to fund M/N project

Ø

Proceeds from divestitures of BE & CSC to be

used to pay off short-term debt and support UI

equity additions

equity additions

Ø

Free cash flow at the parent expected to earn 3%

after-tax

23

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom, Inc.

Ø

Financial Assumptions

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

24

Disclaimer

The following information reflects management’s forecasts using information that is available at the time of this presentation. There are regulations pending at

FERC, which could change transmission earnings estimates. Other factors that

may affect future earnings estimates include, but are not limited to, inflation, the

level of capital spending in the wires distribution and transmission divisions,

amortization of the CTA rate base, weather, timing, economic conditions and the

level of operating and maintenance expenses.

FERC, which could change transmission earnings estimates. Other factors that

may affect future earnings estimates include, but are not limited to, inflation, the

level of capital spending in the wires distribution and transmission divisions,

amortization of the CTA rate base, weather, timing, economic conditions and the

level of operating and maintenance expenses.

25

2006 and Beyond

2005 Actual 2006 Forecast* 2007-2009 CAGR**

UI (Total) $ 3.08 $ 2.90 - $ 3.10 4% - 5%

Distribution $ 1.64 $1.40 - $1.55

CTA $ 0.88 $0.78 (7)% - (5)%

Other $ 0.19 $0.19

Transmission $ 0.38 $0.50 - $0.60 32% - 36%

Xcelecom

Project loss $(0.39) $0

All Other $ 0.24 $0.10 - $ 0.25 1% - 3%

Corporate $(0.31) $(0.25) - $(0.15)

UCI $(0.03) $ 0.65 - $ 0.70

UBE $(0.43) $(0.05) - $ 0.00

Total UIL $ 2.16 $ 3.50 - $ 3.70

* BU expectations are not intended to be additive to derive consolidated expectations

** CAGR from 2006 forecast

Subtotal $2.62 $2.90 - $3.00 4% - 6%

26

Today’s Topics

Ø

Corporate Structure

Ø

2005 Consolidated Financial Results

q

Key Developments

Ø

The United Illuminating Company

Ø

Infrastructure

Ø

Xcelecom

Ø

Financing Plan

Ø

Earnings 2006 and Beyond

Ø

Strategic Direction

27

Strategic Direction

Invest in Regulated Utility Business

Ø

Pay the Dividend

Ø

Earn allowed ROEs

Ø

Produce predictable T&D earnings

Ø

Seek out additional Transmission investment opportunities

Ø

Realize value in remaining non-utility investments

28

Why Invest in UIL???????

Ø

UIL continues to seek maximum shareholder value from all of its

investments

Ø

Consistent Dividend Policy, $2.88 per share

q

Cash to support the dividend

q

Strong Dividend Yield at 2/17/06 of 5.75%

Ø

2006 Payout Ratio, 96% to 99%, excluding divestitures

q

Earnings growth will lower P/O ratio consistent with a predictable, regulated

T&D Company

q

At least $94 million in cash at the parent in 2006

Ø

Committed to long-term growth in Operating Businesses

q

4-year revenue predictability – Distribution

q

Growth in earnings from Transmission investments

29

Q&A

30