UIL Holdings Corporation

Northeast Utilities Conference

Richard Nicholas – Executive VP and Chief Financial Officer

Susan Allen – VP Investor Relations, Secretary and Treasurer

March 12, 2007 Boston

1

Certain statements contained herein, regarding matters that are not historical facts, are forward-looking statements (as defined in the Private Securities Litigation Reform Act of 1995). These include statements regarding management’s intentions, plans, beliefs, expectations or forecasts for the future. Such forward-looking statements are based on the Corporation’s expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements. Such risks and uncertainties include, but are not limited to, general economic conditions, legislative and regulatory changes, changes in demand for electricity and other products and services, unanticipated weather conditions, changes in accounting principles, policies or guidelines, and other economic, competitive, governmental, and technological factors affecting the operations, timing, markets, products, services and prices of the Corporation’s subsidiaries. The foregoing and other factors are discussed and should be reviewed in the Corporation’s most recent Annual Report on Form 10-K and other subsequent periodic filings with the Securities and Exchange Commission. Forward-looking statements included herein speak only as of the date hereof and the Corporation undertakes no obligation to revise or update such statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events or circumstances.

n

UI Service Territory in CT

Safe Harbor Provision

For more information, contact:

Susan Allen – V.P. IR, 203.499.2409, Susan.Allen@uinet.com

Michelle Hanson – Mgr. IR, 203.499.2481, Michelle.Hanson@uinet.com

2

Today’s Topics

Ø

Corporate Structure

Ø

2006 Consolidated Financial Results & Key

Developments

Ø

The United Illuminating Company

Ø

Financing Plan

Ø

2007 Earnings Guidance and Beyond

Ø

Strategic Direction

3

Xcelecom

United Illuminating

Cross-Sound

Cable

Bridgeport

Energy

Wholesale

Transmission

Systems

Integration

Electrical

Contracting

UIL Holdings

Corporation

CTA

Retail

Distribution

Operations

UIL Holdings Structure

4

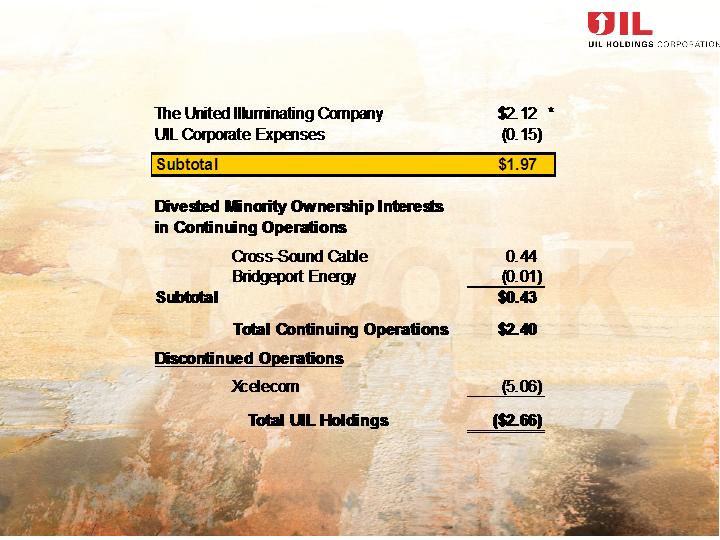

* Includes impact of IRS private letter ruling, $0.27 per share

2006 Financial Results (EPS)

5

Key Developments in 2006

Ø

Non-utility divestitures – total 2006 proceeds $143

million

q

Bridgeport Energy – proceeds of $71 million

q

Cross-Sound Cable – proceeds of $53 million

q

Xcelecom – proceeds of $19 million (excluding tax benefit)

Ø

Tax benefit of $38 million from taxes paid on prior

capital gains

q

Cash realized in 2006, $12 million

q

Remaining $26 million to be realized in late 2007, early 2008

6

The United Illuminating Company

7

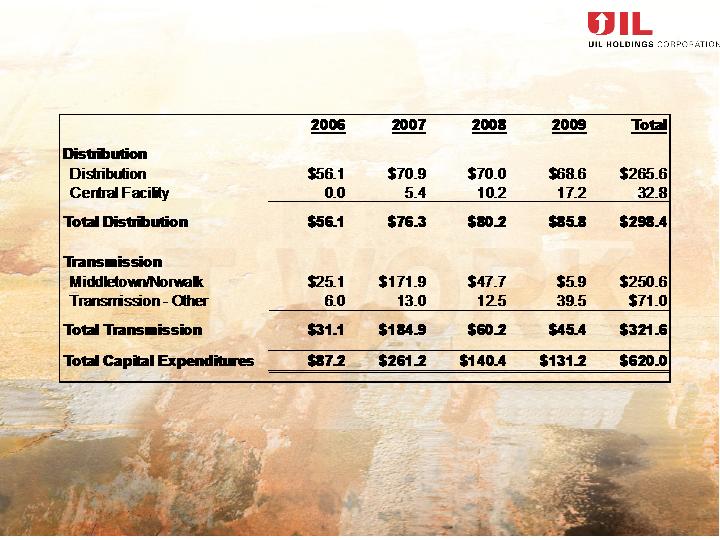

Capital Expenditure Program 2006-2009

8

Total $747 $890 $1,002 $1,024

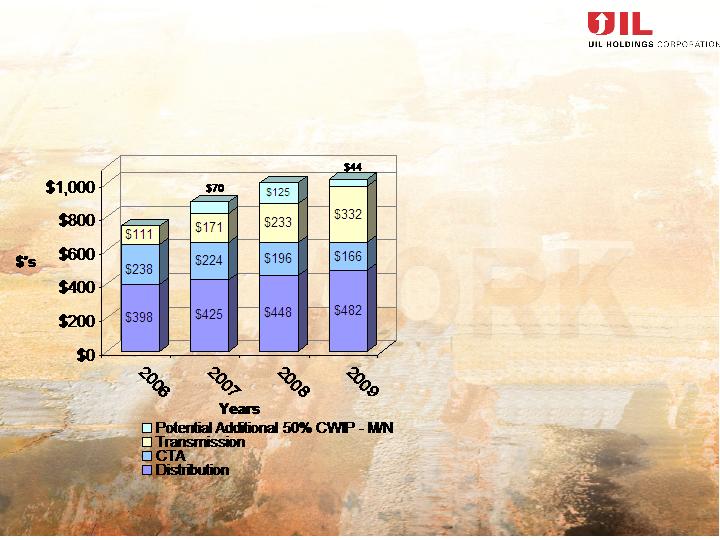

Average Rate Base 2006-2009

Ø

Invest in aging distribution

infrastructure

Ø

M/N project triples investment in

transmission

q

Expected rate base growth $255 - $285

million

Ø

CTA expected to be fully amortized

between 2013-2015

q

Provides steady cash flow

9

Energy Procurement

Ø

Transitional Standard Offer Service through December ’06

Ø

2007 and Beyond

q

Standard Service

•

Requires series of laddered contracts

•

Procured requirement for first half of 2007 and a portion of the requirement

for second half of 2007 and 2008

•

March 5th – RFPs issued. Bids are due by April 11th.

q

Supplier of Last Resort greater than 500 KW

•

Single contracts of six months

•

Procured first half of 2007

q

Significant increase to customer rates

q

Settlement approved by DPUC

•

Acceleration of revenue requirement reductions

•

Reduction of working capital balances

•

Target working capital balance recovered by UI, including carrying charges,

by end of 2007

10

Potential CT Legislation

Ø

UI’s view

q

Electricity prices are too high

q

Bills represent solutions which recognize CT must intervene in

the wholesale electric market by encouraging the building of new

generation facilities

•

Facilities of the right type, in the right place, with the right fuel

q

Fully support the development of a comprehensive energy plan

that will include consideration of the three basic resource

elements necessary for reasonably priced, reliable electric

service:

elements necessary for reasonably priced, reliable electric

service:

•

Conservation and load management, generation and transmission

11

Potential CT Legislation - Continued

q

UI strongly supports increased funding for conservation

•

At a minimum, 3 mills/kWh should be available

q

Hurdles must be overcome to build new generation

•

Financing and siting

•

Non-utility generation can play an important role in the electric

supply of CT

•

Need for long-term contracts

•

Potential for utility rate base generation

12

Transmission

Ø

Approved Middletown/Norwalk transmission project

to be complete by 2009

q

$230 - $260 million commitment

q

$255 - $285 million increase in transmission rate base

Ø

Transmission tracker

q

Tracks FERC-approved transmission revenue requirements

q

Rates are looking forward

q

Adjusted every six months, trued-up annually

Ø

Approved 50% of CWIP in rate base

13

Transmission - Continued

Ø

In the process of applying for additional FERC incentives (order

#679) for M/N project

q

Increase of CWIP in rate base to 100%

q

Additional ROE incentives – 50 basis points

Ø

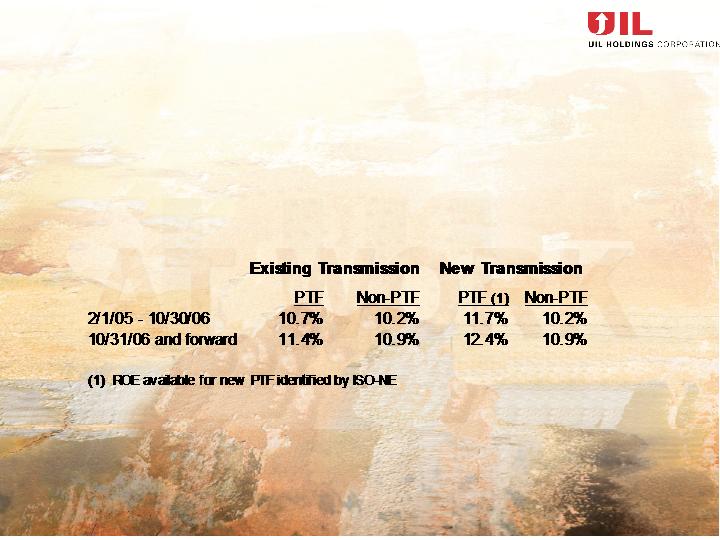

FERC New England Transmission Owner ROE (order #489)

q

Estimating an overall weighted average ROE of 11.85% in 2007,

excluding additional FERC incentives

14

Transmission - Continued

Ø

Transmission Business Unit formed in 2006

q

Charged to explore future transmission opportunities

q

Pursue FERC incentives

q

Influence ISO-NE planning process

q

Working with Black & Veatch, LLP. on long-term plan

Ø

Capital expenditure program of $291 million 2007 through 2009

q

$226 million relating to the Middletown/Norwalk project

q

$65 million, other transmission projects (substations, switch

replacements, circuit breakers, etc.)

Ø

Average year-end 2006 rate base of $111 million

q

Growing to $332 million, or 200% by 2009, excluding 100% CWIP

request

15

Distribution

Ø

Rate case decision through 2009

Ø

Allowed ROE 9.75%, achieved 9.88% after sharing in 2006

Ø

Capital structure – 48% equity, 52% debt

Ø

Sales forecast – 1% growth per year

Ø

Earnings sharing 50/50 from first dollar

Ø

Approved capital expenditure program through 2009

16

Distribution - Continued

Ø

Capital expenditure program of $242 million 2007

through 2009

q

Aging infrastructure maintenance; transformers, cables,

substations

q

Recloser program

q

Central facility

Ø

Average year-end 2006 rate base of $398 million

q

Growing to $482 million, or 21% by 2009

17

Competitive Transition Assessment

Ø

Earnings of $11.4 million, or $0.465 per share in ’06

Ø

Earns allowed ROE of 9.75%, no more, no less

Ø

Expected to be fully amortized between 2013-2015

Ø

Year-end 2006 rate base, $237 million

q

Declining to $166 million by 2009

Ø

Cash flow from operations in 2006, $26 million

18

Other UI

Ø

Other UI or below the line earnings consist of:

q

Non-operating interest income / expense

q

Conservation and Load Management incentive

q

AFUDC

q

GSC Procurement fee

•

No GSC procurement fee and incentive beginning January 1, 2007

•

2004, 2005 & 2006 incentive yet to be approved by DPUC

q

ISO load response

q

Miscellaneous other income

19

Financing Plan

20

Financing Plan

Consolidated cash on hand at UIL at year-end $62 million

Ø

Proceeds from non-utility divestitures

q

Paid off short-term debt

q

Provide equity infusion to UI

q

Anticipation of 2011 payoff of UIL Senior Notes

Ø

M/N transmission project

q

No new equity issuance by UIL is expected

q

Combination of short-term bank borrowings and;

q

Long-term debt

Ø

Utility capital structure will be maintained

q

Long-term debt matched with equity infusion from UIL

21

Earnings Guidance

22

Disclaimer

The following information reflects management’s forecasts using information that is available at the time of this presentation. Factors that may affect future earnings estimates include, but are not limited to, inflation, the level of capital spending in the wires distribution and transmission divisions, amortization of the CTA rate base, weather, timing, economic conditions and the level of operating and maintenance expenses.

23

(1)

Business unit expectations are not intended to be additive. Also, expectations do not include any

earnings or losses from Xcelecom that would need to be included in continuing operations.

(2)

CAGR based on actual 2006 results, excluding the impact of IRS private letter ruling, $0.27 per

share.

2007 Earnings Guidance and Beyond

24

Guidance Drivers

Ø

UI

q

Distribution

•

Will manage to 9.75% allowed ROE

•

Maintain allowed capital structure of 48% equity / 52% debt

q

Transmission

•

Earn allowed ROE based on current composition of rate base and projected

capital spending

•

Does not assume additional FERC incentives

•

M/N transmission project expected to be completed in 2009

•

Will seek out additional transmission opportunities

q

CTA

•

Earn allowed ROE of 9.75%, no more, no less

•

Maintain allowed capital structure of 48% equity / 52% debt

q

Other

•

Projections reflect recognition of the Energy Independence Act Incentives

•

Inclusion of prior year procurement incentives

25

Guidance Drivers - Continued

Ø

UIL Corporate, including remaining UCI

investments

q

Administrative costs

q

Interest charges

q

Results from remaining UCI investments

q

Assumes no additional investments in 2007

26

Strategic Direction

27

UIL - Positioned for Success

Ø

Seeks maximum shareholder value

Ø

Investing in the regulated utility business through

capital spending, $533 million 2007 through 2009

q

Large commitment for a company our size

q

Pure T&D company with earnings growth

Ø

Consistent dividend policy

q

$1.72 per share paid for more than 12 consecutive years

28

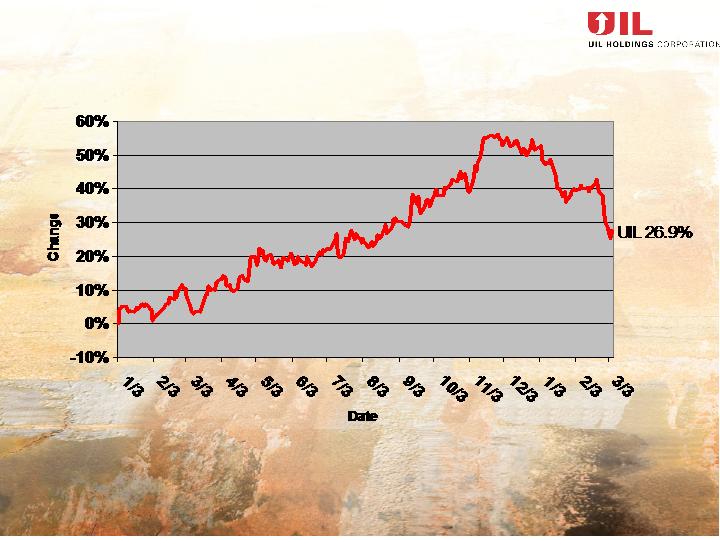

Ranked #1 among EEI listed companies with a 2006

total shareowner return, including dividends, of 60.4%

Why Invest in UIL?

Stock Appreciation – Jan. ‘06 – March ‘07

29

30