UIL Holdings Corporation

42nd Annual EEI Financial Conference

Orlando, Florida

November 2007

Transforming Investment

into Future Value

EXHIBIT 99.1

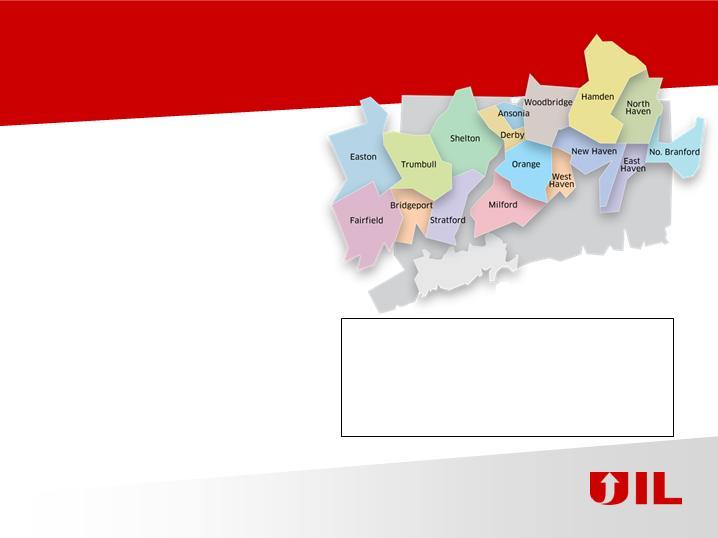

UI Service Territory in Connecticut

Certain statements contained herein, regarding matters that are

not historical facts, are forward-looking statements (as defined in

the Private Securities Litigation Reform Act of 1995). These

include statements regarding management’s intentions, plans,

beliefs, expectations or forecasts for the future. Such

forward-looking statements are based on the Corporation’s

expectations and involve risks and uncertainties; consequently,

actual results may differ materially from those expressed or

implied in the statements. Such risks and uncertainties include,

but are not limited to, general economic conditions, legislative and

regulatory changes, changes in demand for electricity and other

products and services, unanticipated weather conditions, changes

in accounting principles, policies or guidelines, and other

economic, competitive, governmental, and technological factors

affecting the operations, timing, markets, products, services and

prices of the Corporation’s subsidiaries. The foregoing and other

factors are discussed and should be reviewed in the Corporation’s

most recent Annual Report on Form 10-K and other subsequent

periodic filings with the Securities and Exchange Commission.

Forward-looking statements included herein speak only as of the

date hereof and the Corporation undertakes no obligation to

revise or update such statements to reflect events or

circumstances after the date hereof or to reflect the occurrence of

unanticipated events or circumstances.

not historical facts, are forward-looking statements (as defined in

the Private Securities Litigation Reform Act of 1995). These

include statements regarding management’s intentions, plans,

beliefs, expectations or forecasts for the future. Such

forward-looking statements are based on the Corporation’s

expectations and involve risks and uncertainties; consequently,

actual results may differ materially from those expressed or

implied in the statements. Such risks and uncertainties include,

but are not limited to, general economic conditions, legislative and

regulatory changes, changes in demand for electricity and other

products and services, unanticipated weather conditions, changes

in accounting principles, policies or guidelines, and other

economic, competitive, governmental, and technological factors

affecting the operations, timing, markets, products, services and

prices of the Corporation’s subsidiaries. The foregoing and other

factors are discussed and should be reviewed in the Corporation’s

most recent Annual Report on Form 10-K and other subsequent

periodic filings with the Securities and Exchange Commission.

Forward-looking statements included herein speak only as of the

date hereof and the Corporation undertakes no obligation to

revise or update such statements to reflect events or

circumstances after the date hereof or to reflect the occurrence of

unanticipated events or circumstances.

For more information, contact:

Sue Allen - V.P. IR, 203.499.2409

Susan.Allen@uinet.com

Michelle Hanson - Mgr. IR, 203.499.2481

Michelle.Hanson@uinet.com

James P. Torgerson

Chief Executive Officer

Anthony J. Vallillo

President and Chief Operating Officer, UI

Richard J. Nicholas

Executive Vice President and Chief Financial Officer

Safe Harbor Provision

Discussion Topics

lIntroduction

l2007 Accomplishments

l10-year capital expenditure plan and future opportunities

l2007 Financial results and earnings guidance

l2007-2009 Financing plan

lWhy invest in UIL?

Who We Are…

lThe United Illuminating Company, a wholly owned subsidiary of UIL Holdings

Corporation

Corporation

lPure-play utility

n320,000 customers in Connecticut

u290,000 residential customers

u30,000 commercial & industrial customers

l$1.78B Total Assets

l$885M Market Capitalization*

l920 Employees

* As of October 31, 2007

Pure-play utility with earnings growth.

Why UIL?

UIL. A smart investment for smart investors.

lCompetitively positioned for continued success

nSolid enterprise foundation

nSeasoned management team with industry expertise

nAttractive investment opportunities in both distribution and transmission

businesses

businesses

nFuture investment opportunities in generation on the horizon

nTrusted by customers and stakeholders

lFocused on regulated utility

nPure-play utility with earnings growth

lContinued committment to the dividend

nConsistent dividend for more than 12 years, returning an annual dividend of

$1.728 per share

$1.728 per share

2007 Accomplishments

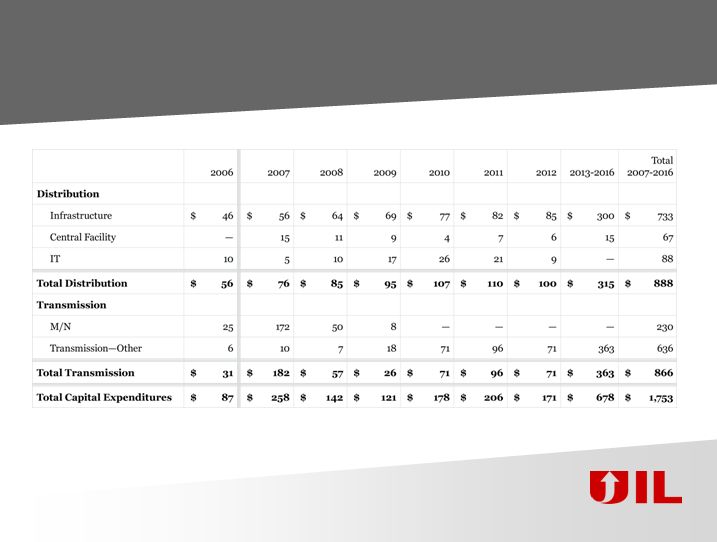

lAnnounced 10-year, $1.75B capital expenditure program

n$887 in Distribution, $866 in Transmission

nTo support robust infrastructure and customer needs

lContinued progress on the Middletown/Norwalk transmission project

nNearing 50% complete

nIn service in 2009

lPartnering with NRG Energy enables new generation investment opportunities

nHybrid generation model can deliver the “best of both worlds”

nWin for customers and shareowners

lUI was honored as the winner for the Global AMI Utility Peer Group Revenue Assurance

Initiative

Initiative

nAward for best practices related to business case development, implementation and operation of

advanced metering systems

advanced metering systems

lFavorable FERC rulings

nTransmission investment incentives

nAttractive ROEs

lSuccessfully working out residual Xcelecom issues

nAchieved settlement agreements that accelerate certain collections

and reduce on-going risk

Working for our customers and shareowners.

Delivering on our commitments.

Customer

Value

lInfrastructure investments to ensure reliable service into

the future

the future

lCustomer programs with incentives to promote energy

conservation and peak reduction

conservation and peak reduction

Shareowner

Value

lValue through regulatory-supported investments

lInvestment deployment which will produce minimum

volatility at a good return

volatility at a good return

Transforming Investment Into….

Conservation

lUI energy efficiency and demand response programs are recognized

nationally for innovation and excellence

nationally for innovation and excellence

Leveraging our Core Competencies

lUpgrading aging infrastructure

lAdding capacity to meet peak demand

lMeeting customer needs

Transmission

Generation

Distribution

lUpgrading aging infrastructure

lAdding capacity to meet peak demand

lStandards compliance

l2007 legislation recognized the need for new peaking generation

lPartnering with NRG offers an innovative response to meet

generation needs while delivering customer and business value

generation needs while delivering customer and business value

Understanding what we do best.

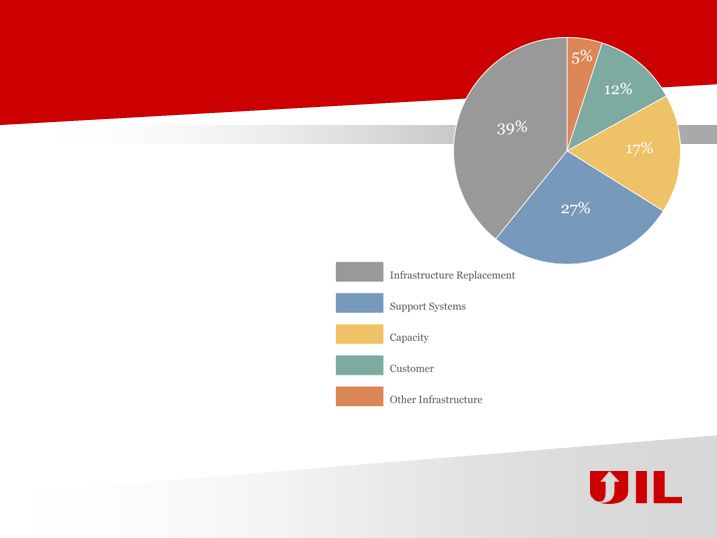

$887 MILLION IN PROJECTS (2007-2016)

Distribution Opportunities

The time to invest is now.

lInfrastructure Replacement

nUpgrading substations

nNetwork facilities

nDistribution transformers

nSplicing chambers

lSupport Systems

nIT related projects

lCapacity

nSix new substations

lCustomer

nConnecting customer loads

lOther Infrastructure

nCentral facility

Transmission Opportunities

Opportunities are largely in our control.

lCapacity

nSix new substations

lAging Infrastructure

nSubstation rebuilds

nOverhead and underground

transmission upgrades

transmission upgrades

lStandards Compliance

nFault duty mitigation

nTransmission upgrades

lMiddletown/Norwalk

nOne of, if not the largest, 345-kV

Gas Insulated Switchgear

Substations in North America

Gas Insulated Switchgear

Substations in North America

n5.6 miles of XLPE underground

cable

cable

lOther

nCustomer driven

nRegional solutions

$866 MILLION IN PROJECTS (2007-2016)

Magnitude of Our Investment

Prudently investing in infrastructure to support customer needs.

Based on current estimates

Overall CAGR - 8%

MORE THAN TRIPLING

TRANSMISSION RATE BASE

TRANSMISSION RATE BASE

Note: Includes only capital expenditures through 2012. Total capital expenditures through 2016 are $1.75B

($887 in distribution and $866 in transmission)

Recent Connecticut Legislation

An Act Concerning Electricity and Energy Efficiency

(“2007 Energy Act”)

(“2007 Energy Act”)

lProvides for:

nCost of service generation including utility-owned

nDecoupling of distribution revenues from sales

nIncreasing support for energy efficiency programs

nComprehensive procurement plan for needed resources

Constructive regulation - win, win for our customers and shareowners.

A New Opportunity:

The Hybrid Generation Model

The Hybrid Generation Model

“We’re ready to go...”

l2007 legislation recognized the need for more peaking generation in Connecticut

lUI/NRG team will propose new “cost of service” peaking generation projects that will

deliver customer value

deliver customer value

lPartnering with NRG combines UI’s record of delivering customer benefits with NRG’s

expertise in developing, building and operating generation assets

expertise in developing, building and operating generation assets

lPotential project benefits include:

nIncreased system reliability

nCompetitive cost of construction & operation

nEnvironmental benefits

nPrice stability of cost of service investment

lThe Hybrid model provides a template to expand into “base-load” generation

investments that can provide additional consumer and business value

investments that can provide additional consumer and business value

lTimeframe

nBy February 1, 2008-proposal submitted to DPUC

nJune 1, 2008-decision expected on proposal

nIf approved by DPUC, COS peaking generation potentially in 2009

THE HYBRID GENERATION MODEL CAN PROVIDE THE “BEST OF BOTH WORLDS”

Energy Efficiency and Load Management

Conservation helps the customer, community, environment and UI.

lTwo decades of success in the design and delivery of innovative CLM services that

provide significant customer, system and environmental benefits

provide significant customer, system and environmental benefits

lEnergy Efficiency

nPrograms achieve an average of 650,000 lifetime MWH reduction each year

nApproximately 1% per year of permanent peak demand reduction

nNationally recognized “on-bill” financing program

nFirst provider of Class III trading certificates in innovative energy efficiency

renewable program

renewable program

lLoad Management & Demand Response

nMore than 5% of system peak load participating in demand response programs (75

MW)

MW)

nDemand response contract for two of the nation’s largest retail providers throughout

New England (291 locations)

New England (291 locations)

nNearly 1% of system peak is shifted through thermal storage applications

UI IS ESTABLISHED AS A NATIONAL LEADER IN THE ENERGY EFFICIENCY & LOAD MANAGEMENT FIELD

Third Quarter Earnings

Decreased earnings volatility with divestiture of non-regulated businesses.

| Three Months Ended September 30, | Nine Months Ended September 30, | |||

2007 | 2006 | 2007 | 2006 | |

Continuing Operations | ||||

| United Illuminating | $0.95 | $0.96 | $1.58 | $1.73 |

| Non-Recurring Item | — | 0.27 | — | 0.27 |

Subtotal United Illuminating | $0.95 | $1.23 | $1.58 | $2.00 |

| Corporate | (0.03) | (0.02) | (0.06) | (0.10) |

| Divested Businesses–CSC & UBE | – | – | — | 0.43 |

Total Continuing Operations | $0.92 | $1.21 | $1.52 | $2.33 |

| Discontinued Operations–Xcelecom | (0.08) | (0.73) | (0.07) | (3.27) |

Total UIL Holdings | $0.84 | $0.48 | $1.45 | $(0.94) |

For Year Over Year Comparative Purposes | ||||

| Total UIL Holdings Continuing Operations, excluding non-recurring item and divested businesses | $0.92 | $0.94 | $1.52 | $1.63 |

2007 Financial Highlights

lM/N incentive rate filing decision issued and effective in May, granting 100% CWIP

in Rate Base and 50 bps incentive adder to ROE on advanced technology portion of

project (approx. 50%)

in Rate Base and 50 bps incentive adder to ROE on advanced technology portion of

project (approx. 50%)

lFinancing Plan approved by DPUC in June. Successfully priced $175M of Senior

Notes in July. Issued $100M in September, $75M to be issued in December

Notes in July. Issued $100M in September, $75M to be issued in December

lIn March, cash settlements of $2.5M for Terry’s Electric, and in

September/October, $0.5M for ABW and $7.3M for Phalcon. Significantly moves

the Xcelecom “tail” towards final resolution from both a financial and management

attention perspective

September/October, $0.5M for ABW and $7.3M for Phalcon. Significantly moves

the Xcelecom “tail” towards final resolution from both a financial and management

attention perspective

lPass through of all generation service costs

Successes to move us to the future.

On track to meet 2007 earnings guidance.

2007 Earnings Guidance & Beyond

as of November 1, 2007

l2007-2009 Earnings Guidance Drivers

nContinued growth in distribution and transmission rate base

nEarning the allowed rate of returns

nMaintaining our capital structure, 48% equity / 52% debt

(1) CAGR based on actual 2006 results, excluding the impact of IRS private letter ruling of $0.27 per share. Assumes UI earns the

distribution allowed rate of return. If unable to earn return, management will make the appropriate regulatory filings to seek regulatory

orders that provide the opportunity to earn the appropriate allowed return.

* Includes the impact of the IRS private letter ruling of $0.27 per share

** Expectations are not intended to be additive

| 2006 Actual | Nine Months Ended September 30, 2007 | 2007 EPS Guidance | 2007-2009 CAGR(1) | |

| United Illuminating Company | $2.12* | $1.58 | $1.85-$1.95 | |

| Corporate | (0.15) | (0.06) | (0.10)-(0.05) | |

Total Continuing Operations | $1.97* | $1.52 | $1.78-$1.88** | 5%-8% |

Financing Plan 2007-2009

lConsolidated cash on hand at UIL on 9/30/07, $52.7 million

nPrimarily proceeds from non-utility divestitures

nUsed to infuse equity into UI

lDPUC approved a 3-year debt financing plan of $375 million

nSuccessfully priced $175 million in July ‘07

nClosed on $100 million in September ‘07

nWill close on additional $75 million in December ‘07

lUIL Holdings to infuse equity into UI to maintain allowed capital structure of 48%

equity, 52% debt

equity, 52% debt

lNo equity issuance planned to support capital expenditure program through 2010,

excluding potential generation spending

excluding potential generation spending

Using cash effectively to increase shareowner value.

UIL is an Attractive Investment

Above average potential returns for our shareowners.

(1)As of October 31, 2007

* Assumes achieving distribution allowed rate of return

Why UIL?

UIL. A smart investment for smart investors.

lCompetitively positioned for continued success

nSolid enterprise foundation

nSeasoned management team with industry expertise

nAttractive investment opportunities in both distribution and transmission

businesses

businesses

nFuture investment opportunities in generation on the horizon

nTrusted by customers and stakeholders

lFocused on regulated utility

nPure-play utility with earnings growth

lContinued committment to the dividend

nConsistent dividend for more than 12 years, returning an annual dividend of

$1.728 per share

$1.728 per share

Appendix

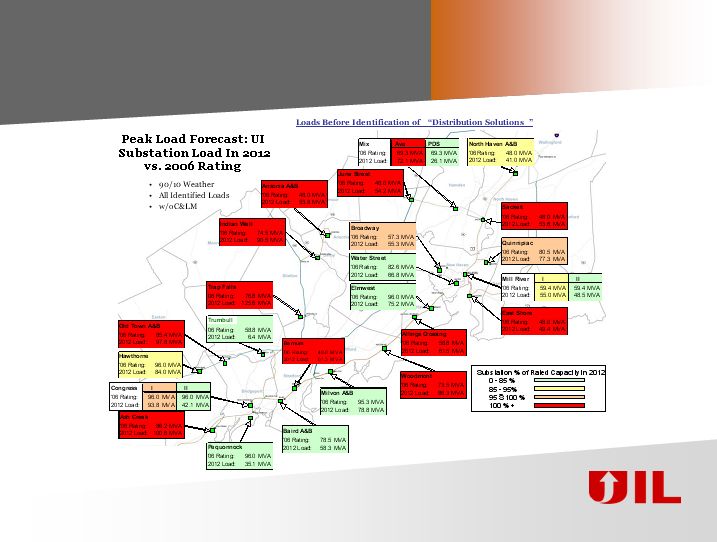

10-Year Transmission Planning

Aging Infrastructure

Standards Compliance

Distribution Capacity

PROJECTS IN THREE CATEGORIES

Distribution capacity solutions exhausted

lDistribution load transfers

lExisting substation expansion

Majority of assets exceeding useful lives

lSubstation rebuilds

lLine/Cable replacements

lComponent replacement

program

program

North American Electric Reliability

Council Standards

Council Standards

Distribution Capacity

Impact of Load Growth

2012

Aging Infrastructure

OVERVIEW OF AN AGING SYSTEM

lMajority of current assets installed in the

1960’s and 1970’s

1960’s and 1970’s

lCommon useful lives: 35 to 50+ years

n At end of life, risk of failure increases

nReliability diminishes

SUBSTATIONS

Standards Compliance

lNorth American Electric Reliability Council/Northeast Power Coordinating

Council/ISO-NE Reliability Standards:

Council/ISO-NE Reliability Standards:

nThermal

uStandards intended to ensure that equipment and components

remain within acceptable operating limits

remain within acceptable operating limits

nVoltage

uStandards intended to keep system voltage within acceptable limits

nShort Circuit

uStandards designed to prevent equipment from failing

nBulk Power System Protection Criteria

lPrioritization Criteria:

nProjected future date that condition creating violation could develop

nThe identified early-phase projects address concerns in all four areas above

$1.75B Capital Expenditure Details

Investments for the Customer Results in

Returns to our Shareowners

Returns to our Shareowners

Substantial, sustained growth in rate base.

Average Rate Base

EXPERIENCE & DEMONSTRATED CAPABILITIES

Middletown to Norwalk

Transmission Project

Transmission Project

lCap Ex: $255-$285

million

million

lIn service in 2009

lAll underground

lOne of, if not the largest

345-kV Gas Insulated

Switchgear substation in

North America

345-kV Gas Insulated

Switchgear substation in

North America

lRate base growth:

$260-$290 million

$260-$290 million

lFERC incentives

approved pending

requests for rehearing

approved pending

requests for rehearing

l100% CWIP, ROE adder

granted

granted

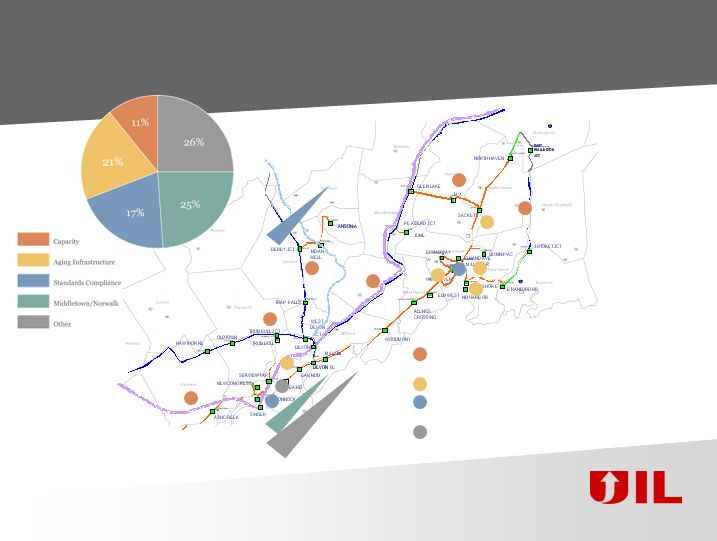

UI Transmission Project Locations

Sampling of Some of the Major Projects:

Capacity:Trumbull, Shelton, Fairfield, Orange,

Hamden, North Branford Substations

Hamden, North Branford Substations

Aging:Grand, Baird, Sackett Substation Rebuilds

Standards Compliance: Naugatuck Valley,

Pequonnock Fault Duty, Underground transmission

Pequonnock Fault Duty, Underground transmission

Other: e.g. customer driven needs, regional solutions, etc.

Top 7 (Immediate) Major Projects (1-4)

lMiddletown to Norwalk

nApproximate total T-CapEx: $255-$285 million

nNearly 50% complete

nExpected in service: 2009

lTrumbull Substation

nApproximate total T-CapEx: $12 million

nApproximately 50% complete

nExpected in service: 2008

lShelton Substation

nDriven by Distribution demand

nPreliminary T-CapEx estimate: $21 million

nExpected in service: 2010

lGrand Avenue Switching Station

nOperational limitations due to ring bus design, wiring and steel deterioration, no

expansion capability, breaker concerns, etc.

expansion capability, breaker concerns, etc.

nPreliminary T-CapEx estimate: $37 million

nExpected in service: 2012

Top 7 (Immediate) Major Projects (5-7)

lPequonnock Station

nShort circuit over-duty issues.

nSolution may allow for future generation connection

nPreliminary T-CapEx estimate: $45 million

nExpected in service: 2011

lNaugatuck Valley Reliability

nCurrent severe low voltage conditions at multiple substations. Single contingency causing

loss in excess of 100 MW. Future Thermal contingency issues.

loss in excess of 100 MW. Future Thermal contingency issues.

nPreliminary T-CapEx estimate: $54 million

nExpected in service: 2012

l115Kv High Pressure Fluid Filled (HPFF) under ground cable upgrade

nDriven by demand and generation placement.

nFuture Thermal contingency issues. Preliminary T-CapEx estimate: $45 million

nExpected in service: 2015

ALL THREE PROJECTS CURRENTLY UNDER IN-DEPTH STUDY WITH ISO-NE (SWCT WORKING GROUP)

Highlights

lDistribution rate case decision in January 2006

nAllows for an increase in rates annual on each January 1st to 1/1/09

nAllowed ROE 9.75%, achieved 9.88% after sharing in 2006

nCapital structure - 48% equity, 52% debt

nSales forecast 1% growth per year

n50/50 sharing on earnings in excess of allowed ROE

lTransmission

nApproved Middletown/Norwalk transmission project to be complete in 2009

u$255-$285 million commitment

nFERC incentives for M/N project - pending requests for rehearing

uIncrease of CWIP in rate base to 100%

uAdditional ROE incentive - 50 basis points for advanced transmission technologies

(estimated at approximately 50% of project costs)

(estimated at approximately 50% of project costs)

nRetail Transmission tracker

uTracks FERC-approved Transmission revenue requirements

uRates are looking forward

uAdjusted every six months

l10-year Distribution and Transmission capital expenditure plan

lFinancial flexibility - total 2006 proceeds from non-utility divestitures, $143 million

lLabor stability - collective bargaining agreement through 2011