UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| FOR THE FISCAL YEAR ENDED DECEMBER 31, 2007 |

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-15052

(Exact name of registrant as specified in its charter)

| Connecticut | 06-1541045 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 157 Church Street, New Haven, Connecticut | 06506 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 203-499-2000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Common Stock, no par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X ] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [X] | Accelerated filer [ ] | Non-accelerated filer [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the registrant’s voting stock held by non-affiliates on June 30, 2007 was $834,198,700 computed on the basis of the average of the high and low sale prices of said stock reported in the listing of composite transactions for New York Stock Exchange listed securities, published in The Wall Street Journal on July 1, 2007.

The number of shares outstanding of the registrant’s only class of common stock, as of February 19, 2008 was 25,160,004.

DOCUMENTS INCORPORATED BY REFERENCE

Document Part of this Form 10-K into which document is incorporated

Definitive Proxy Statement for Annual Meeting of the Shareholders to be held on May 14, 2008 III

UIL HOLDINGS CORPORATION

FORM 10-K

December 31, 2007

| Page | ||

| Glossary | 4 | |

| Part I | 7 | |

| Item 1. | Business | 7 |

| General | 7 | |

| Utility Business | 7 | |

Franchises | 8 | |

Regulation | 8 | |

Rates | 8 | |

Power Supply Arrangements | 10 | |

Arrangements with Other Industry Participants | 10 | |

New England Power Pool and ISO-New England | 10 | |

Middletown/Norwalk Transmission Project | 11 | |

Transmission Adjustment Clause | 12 | |

Hydro-Quebec | 12 | |

Environmental Regulation | 12 | |

| Non-Utility Businesses | 13 | |

United Capital Investments, Inc. (UCI) | 13 | |

Zero Stage Capital | 13 | |

Ironwood Mezzanine Fund | 13 | |

Investment in Lease | 13 | |

Thermal Energies, Inc. (TEI) | 13 | |

Xcel Services, Inc. (Xcel) | 13 | |

| Financing | 14 | |

| Employees | 14 | |

| Item 1A. | Risk Factors | 14 |

| Item 1B. | Unresolved Staff Comments | 16 |

| Item 2. | Properties | 16 |

Transmission and Distribution Plant | 16 | |

Administrative and Service Facilities | 17 | |

| Item 3. | Legal Proceedings | 17 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 17 |

Executive Officers | 17 | |

| Part II | 18 | |

| Item 5. | Market for UIL Holdings’ Common Equity, Related Stockholder Matters and Issuer Purchases ofEquity Securities | 18 |

| Item 6. | Selected Financial Data | 21 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22 |

Overview and Strategy | 22 | |

The United Illuminating Company | 22 | |

United Capital Investments, Inc. | 23 | |

Major Influences on Financial Condition | 23 | |

UIL Holdings Corporation | 23 | |

The United Illuminating Company | 24 | |

United Capital Investments, Inc. | 30 | |

Xcelecom, Inc. | 30 |

- 1 -

TABLE OF CONTENTS (continued)

| Part II (continued) | ||

Liquidity and Capital Resources | 31 | |

Financial Covenants | 32 | |

2008 Capital Resource Projections | 33 | |

Contractual and Contingent Obligations | 36 | |

Critical Accounting Policies | 37 | |

Off-Balance Sheet Arrangements | 39 | |

New Accounting Standards | 39 | |

Results of Operations | 39 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 48 |

| Item 8. | Financial Statements and Supplementary Data | 50 |

Consolidated Financial Statements | 50 | |

Consolidated Statement of Income (Loss) for the Years Ended December 31, 2007, 2006 and2005 | 50 | |

Consolidated Statement of Comprehensive Income (Loss) for the Years Ended December 31,2007, 2006 and 2005 | 50 | |

Consolidated Statement of Cash Flows for the Years Ended December 31, 2007, 2006 and2005 | 51 | |

Consolidated Balance Sheet as of December 31, 2007 and 2006 | 52 | |

Consolidated Statement of Changes in Shareholders’ Equity for the Years EndedDecember 31, 2007, 2006 and 2005 | 54 | |

Notes to Consolidated Financial Statements | 55 | |

Statement of Accounting Policies | 55 | |

Capitalization | 63 | |

Regulatory Proceedings | 67 | |

Short-Term Credit Arrangements | 74 | |

Income Taxes | 75 | |

Supplementary Information | 79 | |

Pension and Other Benefits | 80 | |

Related Party Transactions | 86 | |

Lease Obligations | 86 | |

Commitments and Contingencies | 87 | |

Connecticut Yankee Atomic Power Company | 87 | |

Hydro-Quebec | 88 | |

Environmental Concerns | 88 | |

Claim of Dominion Energy Marketing, Inc. | 91 | |

Gross Earnings Tax Assessment | 91 | |

Property Tax Assessment | 92 | |

Cross-Sound Cable Company, LLC | 92 | |

Fair Value of Financial Instruments | 93 | |

Quarterly Financial Data (Unaudited) | 94 | |

Segment Information | 95 | |

Discontinued Operations | 97 | |

| Report of Independent Registered Public Accounting Firm | 99 | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 101 |

| Item 9A. | Controls and Procedures | 101 |

| Item 9B. | Other Information | 102 |

- 2 -

TABLE OF CONTENTS (continued)

| Part III | 102 | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 102 |

| Item 11. | Executive Compensation | 102 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 102 |

| Item 13. | Certain Relationships and Related Transactions and Directors’ Independence | 103 |

| Item 14. | Principal Accounting Fees and Services | 103 |

| Part IV | 103 | |

| Item 15. | Exhibits, Financial Statement Schedules | 103 |

| Signatures | 109 |

- 3 -

GLOSSARY OF TERMS AND ABBREVIATIONS

ABO (Accumulated Benefit Obligation) – The actuarial present value of benefits (whether vested or nonvested) attributed by the pension benefit formula to employee service rendered before a specified date and based on employee service and compensation prior to that date. The accumulated benefit obligation differs from the projected benefit obligation in that the ABO excludes consideration of future compensation levels.

AFUDC (Allowance for Funds Used During Construction) – The cost of utility equity and debt funds used to finance construction projects that is capitalized as part of construction cost.

BFMCC (Bypassable Federally Mandated Congestion Charges) – A federally mandated charge, as defined by Connecticut electric industry restructuring legislation, related to the supply of electricity.

C&LM (assessment/charge) (Conservation and Load Management) – Statutory assessment on electric utility retail customer bills placed in a State of Connecticut fund used to support energy conservation and load management programs.

CTA (Competitive Transition Assessment) – The component of electric utility retail customer bills, in the State of Connecticut, to recover allowable Stranded Costs, as determined by the DPUC.

CDEP– Connecticut Department of Environmental Protection.

Distribution Division - The operating division of the utility that provides distribution services to the utility’s retail electric customers and manages all components related to such service, including the C&LM, CTA, GSC and REI. The Distribution Division excludes transmission operations.

DOE– United States Department of Energy.

DPUC (Connecticut Department of Public Utility Control) – State agency that regulates certain ratemaking, services, accounting, plant and operations of Connecticut utilities.

EIA - Energy Independence Act adopted by the State of Connecticut in 2005.

EPA– United States Environmental Protection Agency.

EPS– Earnings Per Share.

ESOP– Employee Stock Ownership Plan.

FASB (Financial Accounting Standards Board) – A rulemaking organization that establishes financial accounting and reporting standards.

FERC (Federal Energy Regulatory Commission) – Federal agency that regulates interstate transmission and wholesale sales of electricity and related matters.

FIN– FASB Interpretation Number.

FMCC (Federally Mandated Congestion Charges) – A federally mandated charge, as defined by Connecticut electric industry restructuring legislation, related to the supply of electricity or the reliability of supply in the electricity market.

GAAP– Generally accepted accounting principles in the United States of America.

GSC (Generation services charge) – The rate, as determined by the DPUC, charged to electric utility retail customers for the generation service and ancillary products purchased at wholesale and delivered by UI as part of fully bundled services.

ISO–NE (ISO-New England Inc.) – An independent entity contracting with NEPOOL as an independent system operator to operate the regional bulk power system (generation and ancillary products, and transmission) in New England.

ITC– Investment tax credit.

kV (kilovolt) – 1000 volts. A volt is a unit of electromotive force.

kVA (kilovoltampere) – 1,000 voltamperes. A voltampere is the basic unit of apparent power of a circuit.

kW (kilowatt) – 1,000 watts.

KWH (kilowatt-hour) – The basic unit of electric energy equal to one kilowatt of power supplied to or taken from an electric circuit steadily for one hour.

KSOP– 401(k)/Employee Stock Ownership Plan.

LIBOR– Eurodollar Interbank Market in London.

MVA (megavoltampere) – 1,000 kilovoltamperes.

MW (megawatt) – 1,000 kilowatts.

NBFMCC (Non-Bypassable Federally Mandated Congestion Charges) – A federally mandated charge, as defined by Connecticut electric utility restructuring legislation, related to the reliability of supply delivered by the electric system.

NEPOOL (New England Power Pool) – Entity operating in accordance with the New England Power Pool Agreement, as amended, as approved by the FERC, to provide economic, reliable operation of the bulk power system in the New England region.

O&M(Operation and Maintenance) - Costs incurred in running daily business activities and maintaining infrastructure.

OPEB (Other Post-retirement Benefits) – Benefits (other than pension) consisting principally of health care and life insurance provided to retired employees and their dependents.

PCB (Polychlorinated Biphenyl) – Additive to oil used in certain electrical equipment up to the late-1970s. Now classified as a hazardous chemical.

PBO (Projected Benefit Obligation) – A measure of a pension plan's liability at the calculation date assuming that the plan is ongoing and will not terminate in the foreseeable future.

PTF– Pool Transmission Facilities.

RCRA– The federal Resource Conservation and Recovery Act.

REI (Renewable Energy Investment) – Statutory assessment on electric utility retail customer bills which is transferred to a State of Connecticut fund to support renewable energy projects.

RMR– (Reliability-Must-Run) – Resources scheduled to operate out-of-merit order and identified by ISO New England as necessary to preserve the reliability of a Reliability Region. RMR resources provide local voltage or VAR support or meet local regulation or operating-reserve requirements.

RTO (Regional Transmission Organization) – Organization jointly proposed by ISO-NE and the New England transmission owners to strengthen the independent oversight of the region’s bulk power system and wholesale electricity marketplace. The RTO commenced operation effective February 1, 2005.

SBC (Systems Benefits Charge) – The component of electric utility retail customer bills, in the State of Connecticut, representing public policy costs such as generation decommissioning and displaced worker protection costs, as determined by the DPUC.

SEC - United States Securities and Exchange Commission.

SFAS (Statement of Financial Accounting Standards) – Accounting and financial reporting rules issued by the FASB.

SMD (Standard Market Design) – Marketplace changes implemented by ISO-NE, including the implementation of a transmission congestion management system and a multi-settlement system.

Stranded Costs– Costs that are recoverable from retail customers, as determined by the DPUC, including above-market long-term purchased power obligations, regulatory assets, and above-market investments in power plants.

Transmission Division– The operating division of the utility that provides transmission services and manages all related transmission operations.

TSO (Transitional Standard Offer) – UI’s obligation under Connecticut Public Act 03-135, subsequently amended in part by Public Act 03-221, to offer a regulated “transitional standard offer” retail service from January 1, 2004 through December 31, 2006 to each customer who did not choose an alternate electricity supplier.

VEBA (Voluntary Employee Benefit Association Trust) – Trust accounts for health and welfare plans for future payments to employees, retirees or their beneficiaries.

Watt– A unit of electrical power equal to one joule per second.

Part I

Item 1. Business.

GENERAL

UIL Holdings Corporation (UIL Holdings) primarily operates its regulated utility business. The utility business consists of the electric transmission and distribution operations of The United Illuminating Company (UI). UIL Holdings also has non-utility businesses consisting of an operating lease and passive minority ownership interests in two investment funds, (collectively held at United Capital Investments, Inc. (UCI)), a heating and cooling facility and a mechanical contracting business. The non-utility businesses also recently included (1) a minority ownership interest in Bridgeport Energy, LLC (BE) held by United Bridgeport Energy, Inc. (UBE) until the completion of the sale of that interest to an affiliate of Duke Energy on March 28, 2006, (2) UCI’s minority ownership interest in Cross-Sound Cable Company, LLC (Cross-Sound) until the completion of the sale of that interest to Babcock & Brown Infrastructure Ltd. on February 27, 2006, and (3) the operations of Xcelecom, Inc. (Xcelecom), until the substantial completion of the sale of that business effective December 31, 2006. UIL Holdings is headquartered in New Haven, Connecticut, where its senior management maintains offices and is responsible for overall planning, operating and financial functions.

UIL Holdings files electronically with the Securities and Exchange Commission (SEC): required reports on Form 8-K, Form 10-Q and Form 10-K; proxy materials; ownership reports for insiders as required by Section 16 of the Securities and Exchange Act of 1934; and registration statements on Forms S-3 and S-8, as necessary. The public may read and copy any materials UIL Holdings has filed with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Copies of UIL Holdings’ annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports filed with the SEC may be requested, viewed, or downloaded on-line, free of charge, at (www.uil.com).

UIL Holdings makes available on its website (www.uil.com) the charters of its Corporate Governance and Nominating Committee, Compensation and Executive Development Committee and Audit Committee, as well as its corporate governance guidelines, code of business conduct for its employees, code of ethics for financial officers, and code of business conduct for the Board of Directors.

Due to the requirements of Statement of Financial Accounting Standards No. 131, “Disclosures about Segments of an Enterprise and Related Information,” UIL Holdings has also divided its regulated business into distribution and transmission operating segments for financial reporting purposes. See Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (M), Segment Information,” of this Form 10-K, which is hereby incorporated by reference.

UTILITY BUSINESS

UI is a regulated operating electric public utility established in 1899. It is engaged principally in the purchase, transmission, distribution and sale of electricity for residential, commercial and industrial purposes in a service area of about 335 square miles in the southwestern part of the State of Connecticut. The population of this area is approximately 730,000, which represents approximately 21% of the population of the State. The service area, largely urban and suburban, includes the principal cities of Bridgeport (population approximately 140,000) and New Haven (population approximately 124,000) and their surrounding areas. Situated in the service area are retail trade and service centers, as well as large and small industries producing a wide variety of products, including helicopters and other transportation equipment, electrical equipment, chemicals and pharmaceuticals. As of December 31, 2007, UI had approximately 323,000 customers. Of UI’s 2007 retail electric revenues, approximately 53.7% were derived from residential sales, 38.9% from commercial sales, 6.3% from industrial sales and 1.1% from street lighting and other sales. UI’s retail electric revenues vary by season, with the highest revenues typically in the third quarter of the year reflecting seasonal rates, hotter weather and air conditioning use. For additional information regarding UI’s revenues refer to Part II, Item 6, “Selected Financial Data,” of this Form 10-K which is hereby incorporated by reference.

Franchises

UI has valid franchises to engage in the purchase, transmission, distribution and sale of electricity in the area served by it, the right to erect and maintain certain facilities over, on and under public highways and grounds, and the power of eminent domain. These franchises are subject to alteration, amendment or revocation by the Connecticut legislature, and revocation by the Connecticut Department of Public Utility Control (DPUC) under circumstances specified by statute, and subject to certain approvals, permits and consents of public authorities and others prescribed by statute.

Regulation

UI is subject to regulation by several regulatory bodies, including the DPUC. The DPUC has jurisdiction with respect to, among other things, retail electric service rates, accounting procedures, certain dispositions of property and plant, construction of certain electric facilities, mergers and consolidations, the issuance of securities, the condition of plant and equipment and the manner of operation in relation to safety, adequacy and suitability to provide service to customers, including efficiency. The Federal Energy Regulatory Commission (FERC) approves UI’s transmission revenue requirements, which are collected through UI’s retail transmission rates.

The location and construction of certain electric facilities, including electric transmission lines and bulk substations, are subject to regulation by the Connecticut Siting Council with respect to environmental compatibility and public need.

UI is a “public utility” within the meaning of Part II of the Federal Power Act (FPA. Under the FPA, the FERC governs the rates, terms and conditions of transmission of electric energy in interstate commerce (including transmission service provided by UI), interconnection service in interstate commerce (which applies to independent power generators, for example), and the rates, terms and conditions of wholesale sales of electric energy in interstate commerce (which includes cost-based rates and market-based rates and regional capacity and electric energy markets administered by an independent entity, ISO New England, Inc. (ISO-NE). The FERC also has authority to ensure the reliability of the high voltage electric transmission system, monitor and investigate wholesale electric energy markets and entities that have been authorized to sell wholesale power at market-based rates, impose civil and criminal penalties for violations of the FPA (including market manipulation) and require public utilities subject to its jurisdiction to comply with a variety of accounting, reporting and record-keeping requirements. See Part I, Item 1, “Arrangements with Other Industry Participants.”

Connecticut Yankee Atomic Power Company, in which UI has a 9.5% common stock ownership interest, is subject to the jurisdiction of the United States Nuclear Regulatory Commission and the FERC. The Connecticut Yankee nuclear unit was retired in 1996 and has been decommissioned. See Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (J), Commitments and Contingencies – Other Commitments and Contingencies – Connecticut Yankee,” of this Form 10-K, which is hereby incorporated by reference.

Rates

UI’s retail electric service rates are subject to regulation by the DPUC. UI’s present general retail rate structure consists of various rate and service classifications covering residential, commercial, industrial and street lighting services.

Utilities are entitled by Connecticut law to charge rates that are sufficient to allow them an opportunity to cover their reasonable operating and capital costs, to attract needed capital and maintain their financial integrity, while also protecting relevant public interests.

The revenue components of UI’s retail charges to customers, effective as of January 1, 2008, reflect a total average price of 20.0908¢ per kWh and are detailed as follows:

| Unbundled Revenue Component | Description | Authorized Return on Equity | Average Price Per KWH |

| Distribution | The process of delivering electricity through local lines to the customer’s home or business. | 9.75%(1) | 4.0546¢ |

| Transmission | The process of delivering electricity over high voltage lines to local distribution lines. | 12.15%(2) | 1.2824¢ |

| Competitive Transition Assessment (CTA) (3) | Component of retail customer bills determined by the DPUC to recover Stranded Costs. | 9.75%(3) | 1.5987¢ |

| Generation Services Charge (GSC) (4) | The average rate charged, as determined by the DPUC, to retail customers for the generation services purchased at wholesale by UI for standard service and last resort service. | None | 12.0704¢ |

| Systems Benefits Charge (SBC) (5) | Charges representing public policy costs, such as generation decommissioning and displaced worker protection costs, as determined by the DPUC. | None | 0.1949¢ |

| Conservation & Load Management (C&LM) (6) | Statutory assessment placed in a State of Connecticut fund used to support energy conservation and load management programs. | None | 0.2296¢ |

| Non-Bypassable Federally Mandated Congestion Charges (NBFMCC) (7) | Federally mandated charge, as defined by Connecticut electric industry restructuring legislation, related to the reliability of supply delivered by the electric system. | None | 0.5836¢ |

| Renewable Energy Investment (REI) (8) | Statutory assessment which is transferred to a State of Connecticut fund to support renewable energy projects. | None | 0.0765¢ |

| (1) | DPUC authorized return on equity. Earnings above 9.75% will be shared 50% to customers and 50% to shareholders. |

| (2) | Weighted average estimate based upon FERC authorized rates. (See Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (C), Regulatory Proceedings – 2005 Rate Case and Other Regulatory Matters – Regional Transmission Organization for New England,” of this Form 10-K for further information.) |

| (3) | UI earns the authorized distribution return on equity on CTA rate base. UI defers or accrues additional amortization to achieve the authorized return on equity on unamortized CTA rate base. |

| (4) | This rate includes $0.001 per KWH for retail access and load settlement costs. UI has the opportunity to earn a nominal “incentive” for educating, assisting and promoting investment in distributed and emergency generation programs sponsored by the DPUC. Except for this incentive, GSC has no impact on results of operations, because revenue collected equals expense incurred (which is referred to as a “pass-through” in this filing on Form 10-K). |

| (5) | UI accrues or defers other revenues resulting in SBC having no impact on results of operations. |

| (6) | UI has the opportunity to earn a nominal “incentive” for managing the C&LM programs. Except for the incentive, C&LM has no impact on results of operations, because C&LM billing is a “pass-through.” |

| (7) | NBFMCC rate includes funding of customer initiatives such as distributed generation resulting from the Energy Independence Act. Part of the funding is an incentive to UI helping to bring those customer initiatives on-line. Except for the incentive, NBFMCC has no impact on results of operations, because NBFMCC billing is a “pass-through.” |

| (8) | REI has no impact on results of operations, because REI billing is a “pass-through.” |

For further information refer to Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (C), Regulatory Proceedings,” of this Form 10-K, which information is hereby incorporated by reference.

Power Supply Arrangements

UI’s retail electricity customers are able to choose their electricity supplier. UI is required to offer standard service to those of its customers who do not choose a retail electric supplier and who use a demand meter or have a maximum demand of less than 500 kilowatts. In addition, UI is required to offer supplier of last resort service to customers who are not eligible for standard service and who do not choose to purchase electric generation service from a retail electric supplier licensed in Connecticut. Prior to January 1, 2007, UI was required to offer retail service under a regulated “transitional standard offer” rate to each customer who did not choose an alternate electricity supplier.

In December 2001, UI entered into an agreement with Virginia Electric and Power Company, subsequently assigned to its affiliate Dominion Energy Marketing, Inc. (Dominion), for the supply of all of UI’s generation service requirements through 2008 for certain customers who entered into long-term special contracts with UI prior to the enactment of the 1998 Connecticut electric industry restructuring legislation. Through contract expirations or customers choosing an alternate supplier to supply generation service requirements, these requirements ended in August 2007.

UI must procure its standard service power pursuant to a procurement plan approved by the DPUC. The procurement plan must provide for a portfolio of service contracts procured in an overlapping pattern over fixed time periods (a “laddering” approach). In June 2006, the DPUC approved a procurement plan for UI. As required by statute, a third party consultant was retained by the DPUC to work closely with UI in the procurement process and to provide a joint recommendation to the DPUC as to selected bids.

UI has wholesale power supply agreements in place for the supply of all of UI’s standard service customers for all of 2008, and power supply agreements in place for supplier of last resort service for the first quarter of 2008. Under Connecticut legislation passed in 2007, supplier of last resort service will be procured on a quarterly basis going forward. These contracts are derivatives under SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities” (SFAS No. 133) and UI elected the “normal purchase, normal sale” exception under SFAS No. 133.

For further information regarding power supply arrangements, refer to Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations, Major Influences on Financial Conditions – The United Illuminating Company” of this Form 10-K, which information is hereby incorporated by reference.

Arrangements with Other Industry Participants

New England Power Pool and ISO–New England

ISO-NE and RTO-NE

UI has been a member of the New England Power Pool (NEPOOL) since 1971. NEPOOL was formed to ensure reliable and economic operation of the bulk power system in New England. NEPOOL membership includes entities engaged in the electricity business in New England. Until formation of the New England Regional Transmission Organization (RTO-NE) (see below) in 2004, NEPOOL contracted with ISO-NE for the operation of the regional bulk power system, to ensure, among other things, that (1) the bulk power system was operated in accordance with the reliability objectives of NEPOOL, the North American Electric Reliability Corporation, and the Northeast Power Coordinating Council, (2) access to the transmission grid was available on a non-discriminatory basis, and (3) the wholesale power markets were competitive. Market participants purchase electric energy, capacity and ancillary services in the NEPOOL market; in addition, participants may enter into bilateral contracts for the purchase/sale of these products and services. NEPOOL is the major stakeholder group advising the ISO-NE.

In March 2004, the FERC conditionally approved ISO-NE’s joint proposal with the New England Transmission Owners (TOs) for the creation of a RTO-NE. The creation of RTO-NE strengthens the independent oversight of the region’s bulk power system, transmission grid, and wholesale electricity marketplace. UI is a party to all of the agreements that establish RTO-NE, which commenced operation effective February 1, 2005.

Transmission Return on Equity

In conjunction with the RTO-NE filing, the TOs submitted a filing, in November 2003, requesting FERC authorization of a common base return on equity (ROE) of 12.8% to become effective on February 1, 2005. The TOs also proposed a 50 basis point ROE adder for RTO-NE participation and a 100 basis point ROE adder for new transmission investment. The FERC accepted for filing the common base ROE, the 50 basis point ROE adder as applicable to Pool Transmission Facilities (PTFs) and the 100 basis point ROE adder for new PTF investment, made them effective on February 1, 2005, subject to refund, and set these ROEs for hearing. Thus, all of the TOs, including UI, were able to earn the following, subject to refund, pending the hearing and FERC order: (i) common base ROE of 12.8% plus a 50 basis point RTO participation adder (or 13.3%) on their PTF, (ii) the 13.3% plus the 100 basis point ROE adder on new PTF investment, and (iii) the base ROE of 12.8% on their non-PTF.

On October 31, 2006, the FERC issued an initial order establishing allowable ROEs for various types of transmission assets (ROE Order). The ROE Order set a base ROE of 10.20% and approved two ROE adders as follows: (i) a 50 basis point ROE adder on PTF for participation in RTO-NE; and (ii) a 100 basis point ROE adder for new transmission investment included in the ISO-New England Regional System Plan. In addition, the FERC approved an ROE adjustment reflecting updated U.S. Treasury Bond data, applicable prospectively from the date of the order.

As a result of the FERC Order, UI’s ROE on transmission facilities will depend on whether they are PTF or non-PTF. As a member of RTO-NE, UI qualifies for the 50 basis point ROE adder for its PTF. The 100 basis point ROE adder for new investment is available for new PTF identified by ISO-NE in its Regional System Plan. Non-PTF are not eligible for either the 50 basis point ROE adder for RTO participation or the 100 basis point ROE adder for new investment because the TOs’ did not turn over complete operational control over non-PTF to ROE-NE and because non-PTF are not used to provide regional transmission service. A summary of the ROEs for UI’s PTF and non-PTF as authorized by the FERC in its order, as it is currently understood, is as follows:

| Existing Transmission | New Transmission | |||

| PTF | Non-PTF | PTF (1) | Non-PTF | |

| 2/1/05 to 10/30/06 | 10.7% | 10.2% | 11.7% | 10.2% |

| 10/31/06 and forward | 11.4% | 10.9% | 12.4% | 10.9% |

(1) ROE available for new PTF identified by ISO-NE in its Regional System Plan.

UI’s overall transmission ROE will be determined by the mix of UI’s transmission rate base between new and existing transmission assets, and whether such assets are PTF or Non-PTF. UI’s transmission assets are primarily PTF. For 2007, UI’s overall allowed weighted-average ROE for its transmission business was 11.97%.

Various state agencies, public officials and electric cooperatives filed requests for rehearing of the FERC ROE Order. They argue that there was no legitimate basis for the FERC to use the yield on U.S. Treasury Bonds to increase the TOs common base ROE from 10.20% to 10.90%. In addition, they argue that the evidentiary record showed that a 100 basis point ROE adder for new PTF investment would not change the TOs’ behavior and would produce no benefit for customers. The TOs also filed a request for rehearing asserting that there is no record evidence supporting the FERC’s determination of base ROE of 10.20% (instead of 10.50%). In December 2006, the FERC granted rehearing for further consideration, but has not yet issued a substantive order on the rehearing requests.

UI’s analysis of the FERC ROE Order indicated that the authorized ROEs resulted in customer refunds of $3.7 million, covering the period from February 1, 2005 through December 31, 2006. These refunds reduced net income by $2.2 million in 2006 and were refunded to customers in 2007.

Middletown/Norwalk Transmission Project

In April 2005, the Connecticut Siting Council approved a project to construct a 345-kV transmission line from Middletown, Connecticut, to Norwalk, Connecticut, which was jointly proposed by UI and The Connecticut Light and Power Company (CL&P). This project is expected to improve the reliability of the transmission system in southwest

Connecticut. UI is constructing and will own and operate transmission and substation facilities comprising approximately 20% of the total project cost. On May 22, 2007, the FERC issued an order which accepted UI’s request for the inclusion of 100% of Construction Work In Progress (CWIP) in rate base and accepted a 50 basis point adder for advanced transmission technologies, which will only be applied to costs associated with certain elements of the project. UI estimates that approximately 50% of the project costs are associated with the advanced transmission technologies for with respect to which the 50 basis point adder was approved by the FERC. Certain parties have requested rehearing of the FERC’s May 22, 2007 order. On July 23, 2007, the FERC granted rehearing for further consideration, but has not yet issued a substantive order on the requests for rehearing. For further information see Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Major Influences on Financial Condition – The United Illuminating Company,” which information is hereby incorporated by reference.

Transmission Adjustment Clause

UI makes a semiannual transmission adjustment clause (TAC) filing with the DPUC setting forth its actual transmission revenues, projected transmission revenue requirement, and the required TAC charge or credit so that any under- or over-collections of transmission revenues from prior periods are reconciled along with the expected revenue requirements for the next six months from filing. The DPUC holds an administrative proceeding to approve the TAC charge or credit and holds a hearing to determine the accuracy of customer billings under the TAC. The TAC tariff and this semi-annual change of the TAC charge or credit facilitates the timely matching of transmission revenues and transmission revenue requirements.

Hydro-Quebec

UI is a participant in the Hydro-Quebec transmission tie facility linking New England and Quebec, Canada. UI has a 5.45% participating share in this facility, which has a maximum 2,000 megawatt-equivalent generation capacity value.

Environmental Regulation

The National Environmental Policy Act (the Act) requires that detailed statements of the environmental effect of UI’s facilities be prepared in connection with the issuance of various federal permits and licenses. Federal agencies are required by that Act to make an independent environmental evaluation of the facilities as part of their actions during proceedings with respect to these permits and licenses.

Under the federal Toxic Substances Control Act (TSCA), the Environmental Protection Agency (EPA) has issued regulations that control the use and disposal of polychlorinated biphenyls (PCBs). PCBs had been widely used as insulating fluids in many electric utility transformers and capacitors manufactured before TSCA prohibited any further manufacture of such PCB equipment. Fluids with a concentration of PCBs higher than 500 parts per million and materials (such as electrical capacitors) that contain such fluids must be disposed of through burning in high temperature incinerators approved by the EPA. Presently, no transformers having fluids with levels of PCBs higher than 500 parts per million are known by UI to remain in service in its system.

Under the federal Resource Conservation and Recovery Act (RCRA), the generation, transportation, treatment, storage and disposal of hazardous wastes are subject to regulations adopted by the EPA. Connecticut has adopted state regulations that parallel RCRA regulations but are more stringent in some respects. UI has complied with the notification and application requirements of present regulations, and the procedures by which UI handles, stores, treats and disposes of hazardous waste products to comply with these regulations.

RCRA also regulates underground tanks storing petroleum products or hazardous substances, and Connecticut has adopted state regulations governing underground tanks storing petroleum and petroleum products that, in some respects, are more stringent than the federal requirements. UI currently owns eight underground storage tanks, used primarily for gasoline and fuel oil, which are subject to these regulations. A testing program has been implemented to detect leakage from any of these tanks, and substantial costs may be incurred for future actions taken to prevent tanks from leaking, to remedy any contamination of groundwater, and to modify, remove and/or replace older tanks in compliance with federal and state regulations.

In accordance with applicable regulations, UI has disposed of residues from operations at landfills. In recent years it has been determined that such disposal practices, under certain circumstances, can cause groundwater contamination. Although UI has no current knowledge of the existence of any such contamination, UI or regulatory agencies may determine that remedial actions must be taken in relation to past disposal practices.

In complying with existing environmental statutes and regulations and further developments in these and other areas of environmental concern, including legislation and studies in the fields of water and air quality, hazardous waste handling and disposal, toxic substances, and electric and magnetic fields, UI may incur substantial capital expenditures for equipment modifications and additions, monitoring equipment and recording devices, and it may incur additional operating expenses. Litigation expenditures may also increase as a result of ongoing scientific investigations, and speculation and debate, concerning the possibility of harmful health effects of electric and magnetic fields. The total amount of these expenditures is not now determinable.

If any of the aforementioned events occurs, UI may experience substantial costs prior to seeking regulatory recovery. Additional discussion regarding environmental issues may be found in Part II, Item 8 of this Form 10-K under the caption, “Financial Statements and Supplementary Data” – Notes to Consolidated Financial Statements – Note (J), Commitments and Contingencies – Environmental Concerns,” which information is hereby incorporated by reference.

NON-UTILITY BUSINESSES

UIL Holdings’ non-utility businesses are summarized as follows:

United Capital Investments, Inc. (UCI) holds passive, minority equity positions in two investment funds. UCI made these investments to earn reasonable returns and promote local economic development. UCI has no current plans to make additional minority interest investments. UCI also holds an operating lease as further described below under “Investment in Lease”.

Zero Stage Capital– Zero Stage Capital is a private equity firm that invests in small capitalization private and public companies in its areas of expertise: IT and telecommunications, life sciences, energy and homeland security technologies. During 2000 through 2004, UCI invested $4 million in Zero Stage VII. Due to the nature of its investments and market conditions, UCI recorded an impairment charge during 2007 of $0.7 million reducing the carrying value of Zero Stage VII to $0.3 million as of December 31, 2007, as the carrying value of UCI’s investment was greater than the estimated fair market value and the impairment was determined to be other than temporary.

Ironwood Mezzanine Fund(formerly the Ironbridge Mezzanine Fund) – Ironwood is a regional Small Business Investment Company (SBIC) fund committed to investing a portion of its capital in women-owned and minority-owned businesses and businesses located in low and moderate income areas. In 2001, UCI committed $1 million to Ironwood Mezzanine Fund, of which it has funded $0.9 million as of December 31, 2007. UCI received a distribution of $0.5 million from Ironwood in 2007 as a result of the sale of a portfolio company. The remaining capital commitment of $0.1 million is expected to be funded by 2009. The carrying value of UCI’s investment in Ironwood Mezzanine Fund as of December 31, 2007 was $0.8 million.

Investment in Lease – UCI has a lease agreement that conveys the right to a third party to a specific area located in New Haven, Connecticut. UCI’s investment represents the net present value of future cash flows related to a portion of the area. In 1999, UCI paid $1.5 million for the net future lease payments and is amortizing the amount over the life of the lease. UCI’s investment in the lease at December 31, 2007 was $1.2 million.

Thermal Energies, Inc. (TEI) – TEI operates a district heating and cooling facility located in a building in New Haven, Connecticut through a contract that expires in July 2009. TEI has annual revenues of $1 million and its property and equipment consists primarily of boilers and chillers.

Xcel Services, Inc. (Xcel) – Xcel is the mechanical contracting division of Xcelecom’s former M.J. Daly & Sons, Inc. business. With the completion of all remaining mechanical projects, Xcel’s focus is on the collection of outstanding accounts and claim receivables totaling of $2.8 million at December 31, 2007.

FINANCING

Information regarding UIL Holdings’ capital requirements and resources and its financings and financial commitments may be found in Part II, Item 7 of this Form 10-K under the caption, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources,” which information is hereby incorporated by reference.

EMPLOYEES

As of December 31, 2007, UIL Holdings and its subsidiaries had a total of 981 employees, including 401 who were members of Local 470-1, Utility Workers Union of America, AFL-CIO. UI and Union Local 470-1 are parties to a six-year collective bargaining agreement which expires on May 15, 2011.

Item 1A. Risk Factors.

The financial condition and results of operations of UIL Holdings are subject to various risks, uncertainties and other factors, some of which are described below. Additional risks, uncertainties and other factors not presently known or currently deemed not to be material may also affect UIL Holdings’ financial condition and results of operations.

Legislation and regulation can significantly affect UI’s structure and operations.

UI is an electric transmission and distribution utility whose structure and operations are significantly affected by legislation and regulation. UI’s rates and authorized return on equity are regulated by the FERC and the DPUC. Legislation and regulatory decisions implementing legislation establish a framework for UI’s operations. For a further discussion of legislative and regulatory actions, refer to Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Major Influences on Financial Condition – The United Illuminating Company – Legislation & Regulation,” of this Form 10-K.

The loss of key personnel or the inability to hire and retain qualified employees could have an adverse effect on the business, financial condition and results of operations of UIL Holdings and UI.

The operations of UIL Holdings and its subsidiaries depend on the continued efforts of their respective current and future executive officers, senior management and management personnel. UIL Holdings cannot guarantee that any member of management at the corporate or subsidiary level will continue to serve in any capacity for any particular period of time. In addition, a significant portion of UI’s workforce, including many workers with specialized skills maintaining and servicing the electrical infrastructure, will be eligible to retire over the next five years. For further discussion refer to Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Major Influences on Financial Condition,” of this Form 10-K.

The inability of management to maintain good relations and effectively negotiate future collective bargaining agreements with the bargaining unit could have a material adverse impact on UI’s financial condition and results of operations.

Significant portions of the workforce at UI are covered by collective bargaining agreements. The inability of management to maintain good relations and effectively negotiate future collective bargaining agreements with the bargaining unit could have a material adverse impact on UI’s financial condition and results of operations, as a result of increased expenses related to wages and benefits, poor working performance or organized work stoppages. For further discussion refer to Part I, Item 1, “Business – Employees,” and Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Major Influences on Financial Condition – The United Illuminating Company – Operations,” of this Form 10-K.

UIL Holdings’ ability to maintain future cash dividends at the level currently paid to shareholders is dependent upon the ability of its subsidiaries, primarily UI, to pay dividends to UIL Holdings.

UIL Holdings is dependent on dividends from its subsidiaries and from external borrowings to provide the cash in excess of the amount currently on hand that is necessary for debt service, to pay administrative costs, to meet contractual obligations that cannot be met by the non-utility subsidiaries, and to pay common stock dividends to UIL

Holdings’ shareholders. As UIL Holdings’ sources of cash are limited to dividends from its subsidiaries and external borrowings, the ability to maintain future cash dividends at the level currently paid to shareholders will be primarily dependent upon sustained earnings from current operations of UI.

UIL Holdings’ ability to fund its capital requirements may be limited by its ability to obtain external financing.

All capital requirements that exceed available cash will have to be provided by external financing. Although there is no commitment to provide such financing from any source of funds, other than the short-term credit facility currently available to UI and UIL Holdings, future external financing needs are expected to be satisfied by the issuance of additional short-term and long-term debt and equity financing. The continued availability of these methods of financing will be dependent on many factors, including conditions in the securities markets and economic conditions generally, as well as the debt ratings and future income and cash flow of UIL Holdings and UI. See Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (B), Capitalization and Note (D), Short-Term Credit Arrangements” of this Form 10-K for a discussion of UIL Holdings’ financing arrangements.

Weather conditions, retail price, conservation, distributed and emergency generation and economic conditions could have an adverse effect on the financial condition and results of operations of UIL Holdings and UI.

UI’s electricity sales volumes can be significantly impacted by weather conditions, retail price, conservation, distributed and emergency generation and economic conditions. Weather conditions can significantly impact retail electric sales volumes. In addition, weather can cause fluctuations in expenditures, dependent upon the level of work required to restore the delivery of electricity as a result of storms or other extreme conditions. Conservation and distributed and emergency generation could reduce sales volume. Workforce reductions, plant relocations out of UI service territory and contractions of facilities within the UI service territory can all weaken demand for electricity. In addition, rising energy prices can impact demand for electricity and may also cause increases in the time to collect accounts receivable and bad debt expenses.

UIL Holdings and its subsidiaries may incur substantial capital expenditures and operating expenses in complying with environmental regulations, which could have an adverse impact on the results of operations and financial condition of UIL Holdings.

In complying with existing environmental statutes and regulations and further developments in areas of environmental concern, UIL Holdings and its subsidiaries may incur substantial capital expenditures for equipment modifications and additions, monitoring equipment and recording devices, and it may incur additional operating expenses. Environmental damage claims may also arise from the operations of UIL Holdings’ subsidiaries. For further discussion of significant environmental issues known to UIL Holdings at this time, see Part II, Item 8, “Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note (J), Commitments and Contingencies – Environmental Concerns,” of this Form 10-K.

Capital market conditions and increases in interest rates could have an adverse impact on the financial condition and results of operations of UIL Holdings and UI.

UIL Holdings accesses capital through both long-term and short-term financing arrangements. Increases in interest rates could result in increased cost of capital in the refinancing of fixed rate debt at maturity and in the remarketing of multi-annual tax-exempt bonds. In addition, UI and UIL Holdings have a joint short-term revolving credit agreement that permits borrowings (1) for fixed periods of time at fixed interest rates determined by the London Interbank Offered Rate (LIBOR), and (2) at fluctuating interest rates determined by the prime or Federal Funds lending market. Changes in LIBOR or the prime lending market will have an impact on interest expense. For further discussion of UIL Holdings’ cost of capital and interest rate risk, see Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources,” and Item 7A, “Quantitative and Qualitative Disclosures About Market Risk,” of this Form 10-K.

The inability to collect amounts due under a promissory note from the buyers of the divested Xcelecom companies could adversely impact UIL Holdings’ financial condition and results of operations.

The buyer of a certain former Xcelecom company has signed a promissory note payable to Xcelecom or UIL Holdings, which totals $2.4 million as of December 31, 2007. If this note payable is not collected, UIL Holdings could recognize losses and weaker than expected cash flows.

UIL Holdings may be required to make payments under its indemnification agreements with Xcelecom’s sureties, which could adversely impact UIL Holdings’ financial condition and results of operations.

UIL Holdings is contingently liable to sureties on performance and payment bonds issued by those sureties, relating to construction projects entered into by Xcelecom and its former subsidiaries in the normal course of business. These bonds provide a guarantee to the customer that Xcelecom or its former subsidiaries will perform under the terms of a contract and that it will pay subcontractors and vendors.

Surety bonds remain outstanding on certain projects being completed by Xcelecom’s former companies. If Xcelecom’s former companies and the buyers of those companies fail to perform under a contract or to pay subcontractors or vendors, the customer may demand that the surety make payments or provide services under the bond. UIL Holdings must reimburse the surety for any expenses or outlays it incurs and seek recoupment of those expenses from the buyers of Xcelecom’s former companies. An inability to obtain reimbursement from those buyers could result in losses and negatively impact UIL Holdings’ cash flow.

UIL Holdings may be required to make payments under its indemnification agreements with the buyers of former Xcelecom companies, which could adversely impact UIL Holdings’ financial condition and results of operations.

UIL Holdings is obligated to indemnify the buyers of Xcelecom’s former companies for breaches of representations, warranties and covenants made in the transaction documents with those buyers, and for certain actions by, and obligations of, the companies. A requirement that UIL Holdings pay an indemnity claim could result in additional losses and negatively impact UIL Holdings’ cash flow.

Item 1B. Unresolved Staff Comments.

None

Item 2. Properties.

Transmission and Distribution Plant

The transmission lines of UI consist of approximately 100 circuit miles of overhead lines and approximately 17 circuit miles of underground lines, all operated at 345-kV or 115-kV and located within or immediately adjacent to the territory served by UI. These transmission lines are part of the New England transmission grid. A major portion of UI’s transmission lines is constructed on railroad rights-of-way pursuant to two Transmission Line Agreements. One of the agreements expires in May 2030 and will be automatically extended for up to two successive renewal periods of 15 years each, unless UI provides timely written notice of its election to reject the automatic extension. The other agreement will expire in May 2040.

UI owns and operates 25 bulk electric supply substations with a capacity of 1,830 MVA, and 22 distribution substations with a capacity of 113 MVA. UI has 3,045 pole-line miles of overhead distribution lines and 131 conduit-bank distribution miles.

See Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources,” of this Form 10-K concerning the estimated cost of additions to UI’s transmission and distribution facilities, which information is hereby incorporated by reference.

Administrative and Service Facilities

The corporate headquarters of both UIL Holdings and UI are located in New Haven, Connecticut. Additionally, UI occupies several facilities within its service territory for administrative and operational purposes.

Item 3. Legal Proceedings.

There were no legal proceedings required to be reported under this item.

Item 4. Submission of Matters to a Vote of Security Holders.

There were no matters submitted to a vote of security holders, through the solicitation of proxies or otherwise, during the fourth quarter of the fiscal year ended December 31, 2007.

EXECUTIVE OFFICERS

The names and ages of all executive officers of UIL Holdings and all such persons chosen to become executive officers, all positions and offices with UIL Holdings held by each such person, and the period during which he or she has served as an officer in the office indicated, are as follows:

| Name | Age | Position | Effective Date |

| James P. Torgerson | 55 | President and Chief Executive Officer | (1) |

| Richard J. Nicholas | 52 | Executive Vice President and Chief Financial Officer | March 1, 2005 |

| Linda L. Randell | 57 | Senior Vice President, General Counsel and Corporate Secretary | (2) |

| Susan E. Allen | 48 | Vice President Investor Relations, Treasurer and Assistant Corporate Secretary | (3) |

| Anthony J. Vallillo | 59 | President and Chief Operating Officer the United Ulluminating Company | January 1, 2003 |

| Richard J. Reed | 59 | Vice President - Electric System The United Illuminating Company | January 1, 2003 |

| Deborah C. Hoffman | 53 | Vice President of Audit Services and Chief Compliance Officer | July 8, 2005 |

| Steven P. Favuzza | 54 | Vice President and Controller | July 23, 2007 |

_______________________

Age as of December 31, 2007

(1) As previously disclosed in UIL Holdings’ filing on Form 8-K dated January 10, 2006, James P. Torgerson was appointed to the role of President of UIL Holdings, effective January 23, 2006. As previously disclosed in UIL Holdings’ filing on Form 8-K dated July 3, 2006, James P. Torgerson was appointed to the role of Chief Executive Officer of UIL Holdings, effective July 1, 2006.

(2) As previously disclosed in UIL Holdings’ filing on Form 8-K dated March 5, 2007, Linda L. Randell was appointed to the role of Senior Vice President and General Counsel of UIL Holdings commencing March 26, 2007. As previously disclosed in UIL Holdings’ filing on Form 8-K dated July 24, 2007, Linda L. Randell was appointed to the role of Corporate Secretary, effective July 23, 2007.

(3) As previously disclosed in UIL Holdings’ filing on Form 8-K dated June 30, 2005, Susan E. Allen was appointed to the role of Treasurer of UIL Holdings effective June 30, 2005. As previously disclosed in UIL Holdings’ filing on Form 8-K dated July 24, 2007, Susan E. Allen was appointed to the role of Assistant Corporate Secretary, effective July 23, 2007.

There is no family relationship between any director, executive officer, or person nominated or chosen to become a director or executive officer of UIL Holdings. All of the above executive officers and persons chosen to become executive officers have entered into employment agreements. There is no arrangement or understanding between any executive officer of UIL Holdings and any other person pursuant to which such officer was selected as an officer.

A brief account of the business experience during the past five years of each executive officer of UIL Holdings is as follows:

James P. Torgerson. Mr. Torgerson served as President and Chief Executive Officer of the Midwest Independent Transmission System Operator, Inc., during the period January 1, 2003 to January 22, 2006. Mr. Torgerson was appointed to the role of President of UIL Holdings on January 23, 2006, Chief Executive Officer of The United Illuminating Company on April 24, 2006 and Chief Executive Officer of UIL Holdings on July 1, 2006.

Richard J. Nicholas. Mr. Nicholas has served as Vice President, Finance and Chief Financial Officer of The United Illuminating Company since January 2003. Mr. Nicholas was appointed to the role of Executive Vice President and Chief Financial Officer of UIL Holdings on March 1, 2005.

Linda L. Randell. Ms. Randell served as a Partner of Wiggin & Dana LLP prior to March 25, 2007. Ms. Randell was appointed to the role of Senior Vice President and General Counsel of The United Illuminating Company and of UIL Holdings since March 26, 2007 and was appointed to the role of Corporate Secretary of The United Illuminating Company and of UIL Holdings on July 23, 2007.

Susan E. Allen. Ms. Allen has served as Vice President Investor Relations of The United Illuminating Company and of UIL Holdings since January 1, 2003. Ms. Allen served as Assistant Treasurer of The United Illuminating Company and of UIL Holdings from January 1, 2003 to June 30, 2005, at which time she was appointed to the role of Treasurer of The United Illuminating Company and of UIL Holdings. Ms. Allen served as Corporate Secretary of The United Illuminating Company and of UIL Holdings from January 1, 2003 to July 22, 2007 and Assistant Corporate Secretary of The United Illuminating Company and of UIL Holdings since July 23, 2007.

Anthony J. Vallillo. Mr. Vallillo has served as President and Chief Operating Officer of The United Illuminating Company since January 2003.

Richard J. Reed. Mr. Reed has served as Vice President – Electric System The United Illuminating Company since January 2003.

Deborah C. Hoffman. Ms. Hoffman served as Director of Internal Audit of UIL Holdings from January 1, 2003 to July 7, 2005. She has served as Vice President of Audit Services and Chief Compliance Officer of UIL Holdings since July 8, 2005.

Steven P. Favuzza. Mr. Favuzza served as Director – Financial Compliance of The United Illuminating Company from January 1, 2003 to February 28, 2005. Mr. Favuzza served as Assistant Vice President – Corporate Planning of The United Illuminating Company and of UIL Holdings from March 1, 2005. Mr. Favuzza was appointed to the role of Vice President and Controller of The United Illuminating Company and of UIL Holdings on July 23, 2007.

Part II

Item 5. Market for UIL Holdings’ Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

UIL Holdings’ common stock is traded on the New York Stock Exchange, where the high and low closing sale prices during 2007 and 2006 were as follows:

| 2007 Sale Price | 2006 Sale Price | |||

| High | Low | High | Low | |

| First Quarter | $40.40 | $32.73 | $30.08 | $26.45 |

| Second Quarter | $34.52 | $30.76 | $32.95 | $29.20 |

| Third Quarter | $33.15 | $27.24 | $38.14 | $32.29 |

| Fourth Quarter | $37.18 | $30.72 | $43.15 | $37.83 |

Quarterly dividends on the common stock have been paid since 1900. The quarterly cash dividends declared in 2007 and 2006 were at a rate of $0.432 per share.

UIL Holdings expects to continue its policy of paying regular cash dividends, although there is no assurance as to the amount of future dividends because they depend on future earnings, capital requirements, and financial condition.

Further information regarding payment of dividends is provided in Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources,” of this Form 10-K.

As of December 31, 2007, there were 8,707 common stock shareowners of record.

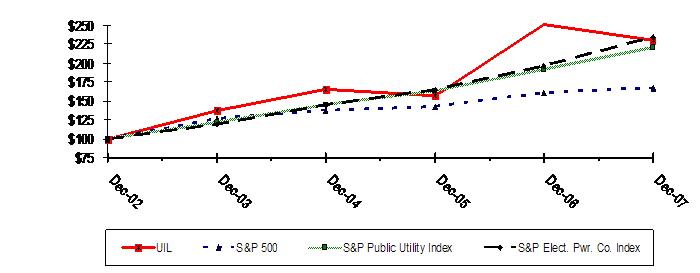

The line graph appearing below compares the yearly change in UIL Holdings’ cumulative total shareowner return on its common stock with the cumulative total return on the S&P Composite-500 Stock Index, the S&P Public Utility Index and the S&P Electric Power Companies Index for the period of five fiscal years commencing 2003 and ending 2007.

| Dec-02 | Dec-03 | Dec-04 | Dec-05 | Dec-06 | Dec-07 | |

| UIL | $100 | $138 | $165 | $157 | $251 | $230 |

| S&P 500 | $100 | $126 | $138 | $142 | $161 | $167 |

| S&P Public Utility Index | $100 | $121 | $145 | $163 | $191 | $221 |

| S&P Elect. Pwr. Co. Index | $100 | $119 | $145 | $165 | $196 | $234 |

| * | Assumes that the value of the investment in UIL Holdings’ common stock and each index was $100 on December 31, 2002 and that all dividends were reinvested. For purposes of this graph, the yearly change in cumulative shareowner return is measured by dividing (i) the sum of (A) the cumulative amount of dividends for the year, assuming dividend reinvestment, and (B) the difference in the fair market value at the end and the beginning of the year, by (ii) the fair market value at the beginning of the year. The changes displayed are not necessarily indicative of future returns measured by this or any other method. |

| Equity Compensation Plan Information | |||

Plan Category | Number of Securities to Be Issued Upon Exercise of Outstanding Options, Warrants and Rights (a) | Weighted Average Exercise Price of Outstanding Options, Warrants and Rights (b) | Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans [Excluding Securities Reflected in Column (a)] (c) |

| Equity Compensation Plans Approved by Security Holders | 875,021 (1) | $31.40 (2) | 195,938 (3) |

| Equity Compensation Plans Not Approved by Security Holders | None | - | - |

| Total | 875,021 (1) | $31.40 (2) | 195,938 (3) |

| (1) | Includes 457,248 shares to be issued upon exercise of outstanding options (238,248 of which include reload rights), 313,588 performance shares to be issued upon satisfaction of applicable performance and service requirements, and 104,185 shares of restricted stock subject to applicable service requirements. |

| (2) | Weighted average exercise price is applicable to outstanding options only. |

| (3) | Includes 21,696 shares authorized for issuance under the UIL Holdings Deferred Compensation Plan, which is a non-qualified benefit plan. |

UIL Holdings repurchased 7,844 shares of common stock in open market transactions to satisfy matching contributions for participants’ contributions into UIL Holdings 401(k) in the form of UIL Holdings stock as follows:

Period | Total Number of Shares Purchased* | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans | Maximum Number of Shares That May Yet Be Purchased Under the Plans | ||||||

| October | 1,770 | $ | 34.24 | None | None | |||||

| November | 6,074 | $ | 35.79 | None | None | |||||

| December | - | - | None | None | ||||||

| Total | 7,844 | $ | 35.44 | None | None | |||||

* All shares were purchased in open market transactions. The effects of these transactions did not change the number of outstanding shares of UIL Holdings’ common stock.

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||||||

| Financial Results of Operation ($000's) | ||||||||||||||||||||

| Sales of electricity | ||||||||||||||||||||

| Utility | ||||||||||||||||||||

| Retail | ||||||||||||||||||||

| Residential | $ | 483,847 | $ | 356,652 | $ | 357,351 | $ | 312,072 | $ | 273,230 | ||||||||||

| Commercial | 350,158 | 316,866 | 312,239 | 281,667 | 248,257 | |||||||||||||||

| Industrial | 56,257 | 86,055 | 87,558 | 87,400 | 82,087 | |||||||||||||||

| Other | 10,188 | 10,810 | 10,397 | 10,415 | 10,311 | |||||||||||||||

| Total Retail | 900,450 | 770,383 | 767,545 | 691,554 | 613,885 | |||||||||||||||

| Wholesale | 36,637 | 29,355 | 35,782 | 24,446 | 24,591 | |||||||||||||||

| Other operating revenues | 43,917 | 46,194 | 9,068 | 48,027 | 31,144 | |||||||||||||||

| Non-utility businesses | 995 | 789 | 828 | 2,313 | 2,124 | |||||||||||||||

| Total operating revenues | $ | 981,999 | $ | 846,721 | $ | 813,223 | $ | 766,340 | $ | 671,744 | ||||||||||

| Operating income from Continuing Operations | $ | 90,165 | $ | 79,156 | $ | 80,132 | $ | 88,113 | $ | 92,049 | ||||||||||

| Income from Continuing Operations, net of tax | $ | 46,693 | $ | 58,716 | $ | 33,476 | $ | 36,617 | $ | 31,376 | ||||||||||

| Discontinued Operations, net of tax (Note N) (2) | (1,996 | ) | (123,880 | ) | (2,222 | ) | 50,328 | (8,090 | ) | |||||||||||

| Net Income (Loss) | $ | 44,697 | $ | (65,164 | ) | $ | 31,254 | $ | 86,945 | $ | 23,286 | |||||||||

| Financial Condition ($000's) | ||||||||||||||||||||

| Property, Plant and Equipment in service - net | $ | 600,305 | $ | 547,741 | $ | 517,251 | $ | 502,310 | $ | 502,304 | ||||||||||

| Deferred charges and regulatory assets | 687,672 | 722,644 | 721,127 | 771,880 | 795,322 | |||||||||||||||

| Assets of discontinued operations | 6,104 | 9,935 | 221,899 | 193,333 | 191,276 | |||||||||||||||

| Total Assets (1) | 1,775,834 | 1,631,493 | 1,799,055 | 1,793,844 | 1,898,166 | |||||||||||||||

| Current portion of long-term debt | 104,286 | 78,286 | 4,286 | 4,286 | - | |||||||||||||||

| Net long-term debt excluding current portion | 479,317 | 408,603 | 486,889 | 491,174 | 495,460 | |||||||||||||||

| Net common stock equity | 464,291 | 460,581 | 544,578 | 548,397 | 492,774 | |||||||||||||||

| Common Stock Data | ||||||||||||||||||||

| Average number of shares outstanding - basic (000's) | 24,986 | 24,441 | 24,245 | 23,983 | 23,818 | |||||||||||||||

| Number of shares outstanding at year-end (000's) | 25,032 | 24,856 | 24,320 | 24,160 | 23,858 | |||||||||||||||

| Earnings per share - basic: | ||||||||||||||||||||

| Continuing Operations | $ | 1.87 | $ | 2.41 | $ | 1.38 | $ | 1.53 | $ | 1.32 | ||||||||||

| Discontinued Operations (Note N) (2) | $ | (0.08 | ) | $ | (5.07 | ) | $ | (0.09 | ) | $ | 2.10 | $ | (0.34 | ) | ||||||

| Net Earnings (Loss) | $ | 1.79 | $ | (2.66 | ) | $ | 1.29 | $ | 3.63 | $ | 0.98 | |||||||||

| Earnings per share - diluted | ||||||||||||||||||||

| Continuing Operations | $ | 1.85 | $ | 2.37 | $ | 1.37 | $ | 1.51 | $ | 1.32 | ||||||||||

| Discontinued Operations (Note N) (2) | $ | (0.08 | ) | $ | (5.00 | ) | $ | (0.09 | ) | $ | 2.09 | $ | (0.27 | ) | ||||||

| Net Earnings (Loss) | $ | 1.77 | $ | (2.63 | ) | $ | 1.28 | $ | 3.60 | $ | 1.05 | |||||||||

| Book value per share | $ | 18.55 | $ | 18.53 | $ | 22.39 | $ | 22.70 | $ | 20.65 | ||||||||||

| Dividends declared per share | $ | 1.728 | $ | 1.728 | $ | 1.728 | $ | 1.728 | $ | 1.728 | ||||||||||

| Market Price: | ||||||||||||||||||||

| High | $ | 40.40 | $ | 43.15 | $ | 33.66 | $ | 32.45 | $ | 27.64 | ||||||||||

| Low | $ | 27.24 | $ | 26.45 | $ | 27.57 | $ | 25.17 | $ | 18.61 | ||||||||||

| Year-end | $ | 36.95 | $ | 42.19 | $ | 27.59 | $ | 30.78 | $ | 27.06 | ||||||||||

| Other Financial and Statistical Data (Utility only) | ||||||||||||||||||||

| Sales by class (millions of kWh's) | ||||||||||||||||||||

| Residential | 2,346 | 2,360 | 2,458 | 2,347 | 2,262 | |||||||||||||||

| Commercial | 2,743 | 2,676 | 2,702 | 2,604 | 2,502 | |||||||||||||||

| Industrial | 785 | 840 | 902 | 957 | 952 | |||||||||||||||

| Other | 43 | 43 | 44 | 44 | 47 | |||||||||||||||

| Total | 5,917 | 5,919 | 6,106 | 5,952 | 5,763 | |||||||||||||||

| Number of retail customers by class (average) | ||||||||||||||||||||

| Residential | 291,247 | 289,913 | 289,122 | 289,057 | 288,405 | |||||||||||||||

| Commercial | 29,526 | 29,067 | 28,934 | 28,956 | 29,687 | |||||||||||||||

| Industrial | 1,180 | 1,278 | 1,356 | 1,497 | 1,595 | |||||||||||||||

| Other | 1,222 | 1,242 | 1,260 | 1,307 | 1,306 | |||||||||||||||

| Total | 323,175 | 321,500 | 320,672 | 320,817 | 320,993 | |||||||||||||||

| (1) Reflects reclassification of accrued asset removal costs from accumulated depreciation to regulatory liabilities for all years presented. | ||||||||||||||||||||

| (2) Note refers to the Notes to the Consolidated Financial Statements included in Item 8. "Financial Statements and Supplementary Data." | ||||||||||||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Certain statements contained herein, regarding matters that are not historical facts, are forward-looking statements (as defined in the Private Securities Litigation Reform Act of 1995). These include statements regarding management’s intentions, plans, beliefs, expectations or forecasts for the future. Such forward-looking statements are based on UIL Holdings’ expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements. Such risks and uncertainties include, but are not limited to, general economic conditions, legislative and regulatory changes, changes in demand for electricity and other products and services, unanticipated weather conditions, changes in accounting principles, policies or guidelines, and other economic, competitive, governmental, and technological factors affecting the operations, markets, products and services of UIL Holdings’ subsidiaries. The foregoing and other factors are discussed and should be reviewed in this Annual Report on Form 10-K and other subsequent periodic filings with the Securities and Exchange Commission. Forward-looking statements included herein speak only as of the date hereof and UIL Holdings undertakes no obligation to revise or update such statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events or circumstances.

OVERVIEW AND STRATEGY

UIL Holdings Corporation (UIL Holdings) primarily operates its regulated utility business. The utility business consists of the electric transmission and distribution operations of The United Illuminating Company (UI). UIL Holdings also has non-utility businesses consisting of an operating lease and passive minority ownership interests in two investment funds, (collectively held at United Capital Investments, Inc. (UCI)), a heating and cooling facility and a mechanical contracting business. The non-utility businesses also recently included (1) a minority ownership interest in Bridgeport Energy, LLC (BE) held by United Bridgeport Energy, Inc. (UBE) until the completion of the sale of that interest to an affiliate of Duke Energy on March 28, 2006, (2) UCI’s minority ownership interest in Cross-Sound Cable Company, LLC (Cross-Sound) until the completion of the sale of that interest to Babcock & Brown Infrastructure Ltd. on February 27, 2006, and (3) the operations of Xcelecom, Inc. (Xcelecom). Effective December 31, 2006, UIL Holdings substantially completed the sale of the Xcelecom business, completing its corporate strategic realignment to focus on its regulated electric utility, UI.

As a result of Connecticut’s 1998 electric industry restructuring legislation, UI divested its ownership interests in generation facilities. Subsequently, UIL Holdings invested the proceeds of the sale of UI’s generation facilities in non-utility businesses to offset the expected reduction in utility earnings resulting from this restructuring. Some of these investments did not generate expected results due to a number of factors, including the following: (1) a change in market conditions resulting in lower profitability for construction business, as well as challenges in realizing operational synergies, for Xcelecom; (2) poor investment market conditions offsetting the value of UCI’s passive investments; and (3) high natural gas prices and change in capacity markets affecting the value of UBE.UIL Holdings’ investments in American Payment Systems, Inc. and Cross-Sound generated positive results with the gain on sale of those investments. UIL Holdings’ current overall corporate strategy is to create shareholder value by investing in the utility business to grow earnings and cash flow through operating and strategic initiatives. The divestiture of the non-utility businesses described above has provided significant financial flexibility in funding the future utility investments.

The United Illuminating Company