Investor Presentation

(Based upon Second Quarter 2005 results)

July 25, 2005

www.j2global.com

1

Future operating results

Subscriber growth and retention

Earnings growth and expectations

New products, services and features

Corporate spending

Liquidity

Network capacity and coverage

Regulatory developments

Taxes

Certain statements in this presentation constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, particularly those contained in the slide entitled “2005 Financial Guidance”. These forward-looking statements are based on management’s current expectations or beliefs as of July 25, 2005 and are subject to numerous assumptions, risks and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. Readers should carefully review the risk factors described in this presentation. Such statements address the following subjects:

Safe Harbor for Forward-Looking Statements

All information in this presentation speaks as of July 25, 2005 and any

distribution of this presentation after that date is not intended and will not be

construed as updating or confirming such information.

2

Risk Factors

Inability to sustain growth in our customer base, revenue or profitability

Competition in price, quality, features and geographic coverage

Inability to obtain telephone numbers in sufficient quantities on acceptable terms in desirable locations

Enactment of burdensome telecommunications or Internet regulations

Reduced use of fax services due to increased use of email or widespread adoption of digital signatures

Inadequate intellectual property protection or violations of third party intellectual property rights

System failures or breach of system or network security

Failure to expand and upgrade our systems and network infrastructure to accommodate increased traffic

Inability to adapt to technological change, or third party development of new technologies superior to ours

Economic downturns in industries which rely heavily on fax transmissions

Loss of services of executive officers and other key employees

Loss of third party suppliers and marketing relationships, and inability to enter into new such relationships

on acceptable terms

Other factors set forth in our Annual Report on Form 10-K filed on 3/28/05 and the other reports filed by

us from time to time with the Securities and Exchange Commission

The following factors, among others, could cause our business, prospects, financial condition, operating results

and cash flows to be materially adversely affected:

3

j2 Global deploys the power of the

Internet to deliver business critical

communication and messaging services to

individuals and corporations throughout

the world.

4

All brand names and logos are trademarks of j2 Global Communications, Inc. or its affiliates in the U.S. and/or internationally.

5

Unique Assets

9.3 million subscribed telephone numbers (DIDs)

Global advanced messaging network

1,500+ cities in 25 countries on 5 continents

13.6MM+ unique DIDs worldwide in inventory

Patented technology

A portfolio of 23 issued U.S. patents, and numerous pending U.S. patent

applications, issued foreign patents and pending foreign applications

Expertise

Effective customer acquisition strategies and Web marketing

Breadth, depth and management of a complex network & architecture

Strong financial position

33 consecutive quarters of Revenues growth

14 consecutive quarters of positive and growing Operating Earnings

35% year-over-year Revenues growth

$108.6MM of cash & investments to fund growth (as of 6/30/05)

Nominal amount of debt

6

Subscriber Profile

Vertical Markets

Financial institutions

Real estate

Law firms & corporate legal departments

Medical

Government

Hospitality

Remote workers & “road warriors”

Value Proposition

Digitization (paper reduction)

Security

Privacy

Regulatory Compliance

Efficiency

Cost

Infrastructure replacement

7

Subscriber Acquisition

Individuals

Targeted Web marketing

(e.g. AOL, Hotmail, Yahoo!, Google, AT&T, United Online, etc.)

Sold primarily through: www.eFax.com and www.j2.com

Use of proprietary Life Cycle Management (i.e. Free Paid conversions)

Advertising & Calling-Party-Pays revenue supports the Free base

Small to Mid-Sized Businesses

Sold through: www.eFaxCorporate.com, supported by Telesales

Self-service Web-based broadcast fax engine at www.jblast.com

Outsourced email, spam & virus protection through Electric Mail

Use of proprietary Life Cycle Management (i.e. usage stimulation)

Large Enterprise/Government

Direct sales force

Marketed through Web and traditional direct selling methods

Use of proprietary Life Cycle Management (i.e. usage stimulation)

8

Paid Subscription Drivers

Six drivers for Paid subscription additions:

Subscribers coming directly to the Company’s Websites

Brand awareness

Search engine discovery

Free-to-Paid subscriber upgrades

Life Cycle Management

eFax Corporate SME sales

Hybrid Website and human interaction (i.e. Telesales)

Direct enterprise & government sales

Through the outside Corporate Sales team

Direct marketing spend for Paid subscribers

Targeted marketing

CPA deals

International marketing programs in Western Europe

9

1,500+ cities

in 25 countries

on 5 continents

Everyone has a fax number

on their business cards…

but the smart ones get

their faxes delivered to

their email.

Current population of j2 Global-served

countries: 758 million

Representing 246+ million Internet users

j2 Global has >638,000 international

subscribers

137 million total US employees

j2 Global has 8.6 million U.S. subscribers

10

Initiative Updates

Enterprise Sales

14 Enterprise accounts with 1,000+ DIDs – all under annual or

multi-year contracts

Signed another 3,000 DID account during Q2

Pipeline: 42 qualified 1,000+ DID opportunities, of which 13

are international

International

54% increase in Paid net subscriber additions between Q1 and

Q2 2005

Signed marketing agreement with Lycos for 8 E.U. countries

Taipei, Taiwan service to be introduced in Q3

eVoice

Approximately 2,000 Paid subscribers – acquired with virtually

no external marketing (which starts this quarter)

International (Europe) eVoice launch in Q3 2005

11

Product Roadmap

Inbound Fax to Email

Outbound Fax via Email

Fax broadcasting

Secure fax

OCR

PDF delivery

Fax storage/archive

“Smart” Caller ID

New notification methods

Voice

Services

Inbound VM to Email

Voicemail management

Telephone access

Conference Calling

Enhanced voicemail

Call screening

Call forwarding

Voicemail interrupt

Collaboration

Unified

Messaging

& Comm.

Services

Integrated Email,

voicemail & fax services

Find me/Follow me

Wireless messaging and

notification

Virtual PBX

ProtoFax®

Messenger 4.0

HotSend®

PaperMaster Pro®

Currently offered

Future opportunities

Document

Management

Services

Permission-based

Email marketing

Outsourced Email

Spam control

Virus filtering

Message storage

Hosted ExchangeTM

IP

Fax

Exchange is a registered Trademark of the Microsoft Corporation

12

Financial Highlights

13

Historical Revenue & Operating Income Growth

33 consecutive quarters of Revenue growth

14 consecutive quarter of Operating Earnings growth

14

Cost Trends

*

*

* Reflects a reclassification of certain network operations and depreciation expenses

into Cost of Revenues, which was implemented in Q1 2005 (and is on-going),

versus their historical inclusion in General & Administrative expenses. See Slide

#19 for a reconciliation to previously reported numbers.

15

2005 Financial Guidance

(1) Assumes an effective annual tax rate of 27% and 25.5 million fully diluted shares outstanding

$0.48 – 0.49

$37.4 – 38.0

Q3

2005

$1.82 – 1.87

Net Earnings per Share (1)

$145 – 148

Revenues (millions)

Year-End

2005

16

Recent Events

j2 Global’s network expanded to 25 countries with the

introduction of local telephone numbers in Spain and

Portugal

Acquired the assets of Data On Call, a profitable fax-to-

email provider to businesses

Electric Mail launched PerimeterProtect™ services,

offering up-front email messaging protection and

continuity through SPAM and content filtering, as well as

virus blocking

OneBox Receptionist introduced, providing virtual PBX

functionality to small- and medium-sized businesses

Increased analyst coverage with the addition of Morgan

Keegan and First Albany

17

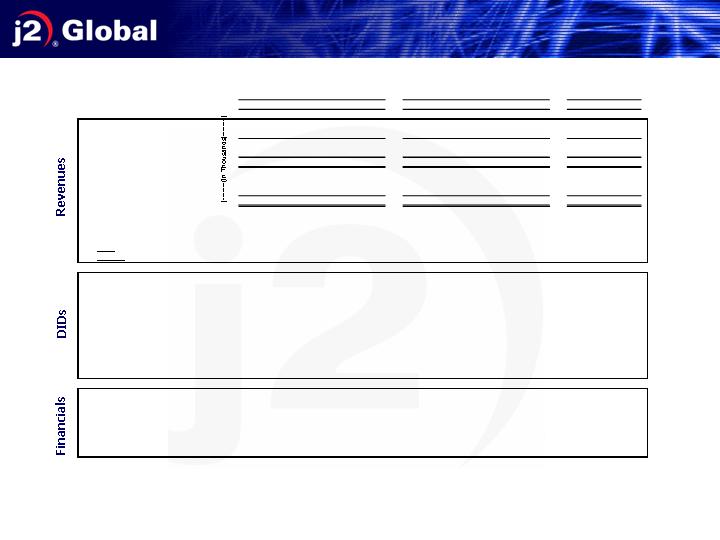

Metrics

18

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Fixed Subscriber Revenues

$9,916

$11,177

$12,121

$13,976

$16,021

$17,750

$19,122

$20,823

$22,773

$23,756

Variable Subscriber Revenues

4,538

5,130

5,685

5,542

6,041

7,314

7,863

8,226

8,502

10,323

Subscriber Revenues

$14,454

$16,307

$17,806

$19,517

$22,062

$25,063

$26,985

$29,050

$31,275

$34,079

Other Revenues

754

730

1,097

957

880

768

786

749

949

806

Total Revenues

$15,208

$17,037

$18,903

$20,474

$22,942

$25,831

$27,771

$29,799

$32,224

$34,885

DID Based Revenues

$14,063

$15,835

$17,478

$19,216

$21,664

$24,057

$25,994

$27,937

$30,186

$33,009

Non-DID Revenues

1,145

1,202

1,424

1,258

1,278

1,774

1,777

1,862

2,038

1,876

Total Revenues

$15,208

$17,037

$18,903

$20,474

$22,942

$25,831

$27,771

$29,799

$32,224

$34,885

Subscriber Revenue/Total Revenues

95.0%

95.7%

94.2%

95.3%

96.2%

97.0%

97.2%

97.5%

97.1%

97.7%

DID Based/Total Revenues

92.5%

92.9%

92.5%

93.9%

94.4%

93.1%

93.6%

93.8%

93.7%

94.6%

%

Fixed

Subscriber Revenues

68.6%

68.5%

68.1%

71.6%

72.6%

70.8%

70.9%

71.7%

72.8%

69.7%

%

Variable

Subscriber Revenues

31.4%

31.5%

31.9%

28.4%

27.4%

29.2%

29.1%

28.3%

27.2%

30.3%

Paid DIDs

(4)

304,969

348,988

380,230

400,245

434,616

469,328

515,162

553,949

598,490

641,720

Average Monthly Revenue/DID

$15.59

$15.52

$15.36

$15.73

$16.68

$17.22

$16.95

$16.87

$16.85

$17.21

Cancel Rate

(1)

3.6%

3.0%

2.8%

3.3%

2.9%

2.4%

2.6%

2.7%

2.8%

2.5%

Free DIDs

4,320,975

4,825,991

5,146,838

5,150,388

5,843,167

6,873,083

7,106,249

8,180,452

8,448,517

8,653,386

Average Monthly Revenue/DID

$0.05

$0.04

$0.05

$0.05

$0.05

$0.04

$0.04

$0.04

$0.04

$0.04

Total DID Inventory (MM)

5.8

6.5

6.7

7.1

8.6

9.5

11.3

11.9

12.7

13.6

Cities Covered

1,000

1,000

1,100

1,100

1,300

1,350

1,400

1,500

1,500

1,500

Countries Covered

18

19

20

20

20

20

20

22

23

25

Gross Margin

(3)

80.2%

80.9%

81.5%

82.6%

84.1%

84.3%

84.3%

85.1%

79.8%

80.2%

Operating Margin

34.2%

36.1%

39.2%

41.4%

43.5%

42.6%

43.0%

44.0%

41.4%

44.0%

Cash/Funds Available for Growth

(millions)

$38.7

$46.5

$54.5

$63.8

$67.4

$74.2

$83.9

$93.8

$98.2

$108.6

Free Cash Flow

(2)

(millions)

$5.0

$7.1

$7.7

$9.5

$9.9

$11.6

$11.9

$10.9

$11.3

$13.8

(1)

Cancel Rate is defined as individual customer DIDs with greater than 4 months of continuous service (continuous service includes customer DIDs which are administratively cancelled and

reactivated within a calendar month), and DIDs realted to enterprise customers beginning with their first day of service. Calculated monthly and expressed here as an average over the three

months of the quarter.

(2)

Free Cash Flow is net cash provided by operating activities, less purchases of property and equipment. In Q4 2003, it excludes the benefit of $9.5 million to record the reversal of certain

valuation allowances of defered tax assets.

(3)

Reflects the inclusion of certain network operations and depreciation expense in Cost of Revenues in Q1 2005 versus its historical inclusion in General & Administrative expense.

(4)

For Q1 2005, reduced by 6,625 DIDs due to the discontinuance of a marketing trial.

2005

2003

2004

19

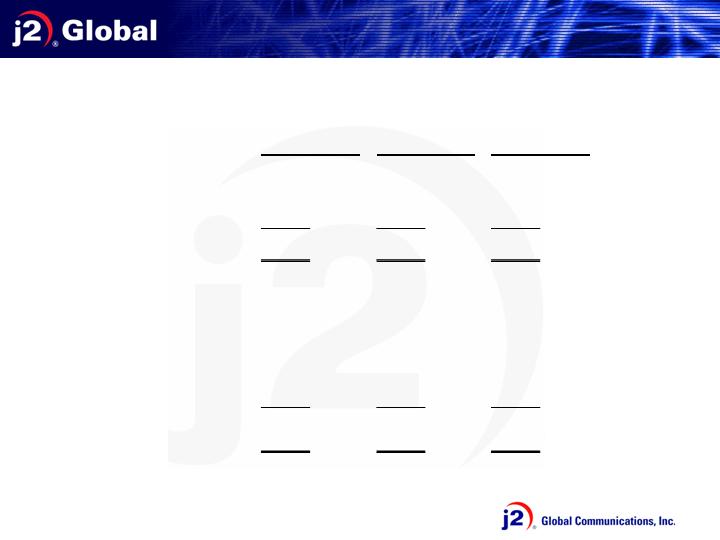

Reconciliation of previously reported

Cost of Revenues and General & Administrative Expenses for 2004

($ in thousands)

Q2-2004

% of Rev

Q3-2004

% of Rev

Q4-2004

% of Rev

Cost of Revenues

Previously reported

4,063

$

15.7%

4,363

$

15.7%

4,448

$

14.9%

Add: Certain network operations

and depreciation expenses

1,070

1,092

1,128

Adjusted Cost of Revenues

5,133

$

19.9%

5,455

$

19.6%

5,576

$

18.7%

Gross Margin

Previously reported

84.3%

84.3%

85.1%

Adjusted Gross Margin

80.1%

80.4%

81.3%

General and Administrative Expenses

Previously reported

4,734

$

18.3%

5,321

$

19.2%

5,506

$

18.5%

Less: Certain network operations

and depreciation expenses

1,070

1,092

1,128

Adjusted General

and Administrative Expenses

3,664

$

14.2%

4,229

$

15.2%

4,378

$

14.7%

(1) In Q4 2003, excludes benefit of $9.5 million to record the reversal of certain valuation allowances of our deferred tax assets.

(2) Prior to Q4 2003, the Company accrued tax expense at the rate of 5% or less.

(3) Net cash provided by operating activities, less purchases of property & equipment. Free Cash Flow amounts are not meant

as a substitute for GAAP, but are solely for informational purposes.

Computation of Free Cash Flow

($ in millions)

(1,2)

20

Q1 '03

Q2 '03

Q3 '03

Q4 '03

Q1 '04

Q2 '04

Q3 '04

Q4 '04

Q1 '05

Q2 '05

Net cash provided by operating activities

$5.308

$8.542

$8.623

$10.375

$10.252

$13.044

$13.240

$14.785

$13.762

$15.227

Purchases of property & equipment

(0.300)

(1.414)

(0.947)

(0.906)

(0.319)

(1.442)

(1.337)

(3.883)

(2.473)

(1.420)

Free Cash Flow

(3)

$5.008

$7.128

$7.676

$9.469

$9.933

$11.602

$11.903

$10.902

$11.289

$13.807

®

21