Exhibit 99

|

Exhibit 99

Jefferies Group

2013 Fixed Income Investor Day

October 10, 2013

|

Note on Forward Looking Statements

This document contains “forward looking statements” within the meaning of the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward looking statements include statements about our future and statements that are not historical facts. These forward looking statements are usually preceded by the words “should,” “expect,” “intend,” “may,” “will,” or similar expressions. Forward looking statements may contain expectations regarding revenues, earnings, operations, and other results, and may include statements of future performance, plans, and objectives. Forward looking statements also include statements pertaining to our strategies for future development of our business and products. Forward looking statements represent only our belief regarding future events, many of which by their nature are inherently uncertain. It is possible that the actual results may differ, possibly materially, from the anticipated results indicated in these forward-looking statements. Information regarding important factors, including our Risk Factors, that could cause actual results to differ, perhaps materially, from those in our forward looking statements is contained in reports we file with the SEC. You should read and interpret any forward looking statement together with reports we file with the SEC.

i

|

Agenda

Section

Leucadia Overview 1 Jefferies Overview 2 Jefferies Business Review 3 Jefferies Operating Results 4 Risk Management 5 Capital and Liquidity Management 6

1 |

|

|

Leucadia Overview

2 |

|

|

Leucadia – Jefferies Merger

Leucadia – Jefferies merger closed on March 1, 2013

Jefferies continues to operate in a manner consistent with its historical business model and remains a client-focused, conservatively capitalized and full-service global investment banking firmLeucadia continues to pursue compelling value opportunities, consistent with its track record established over more than three decades as one of the world’s leading long-term investors

Investment criteria are consistent with the disciplined approach to risk that Leucadia has publicly affirmed

3 |

|

|

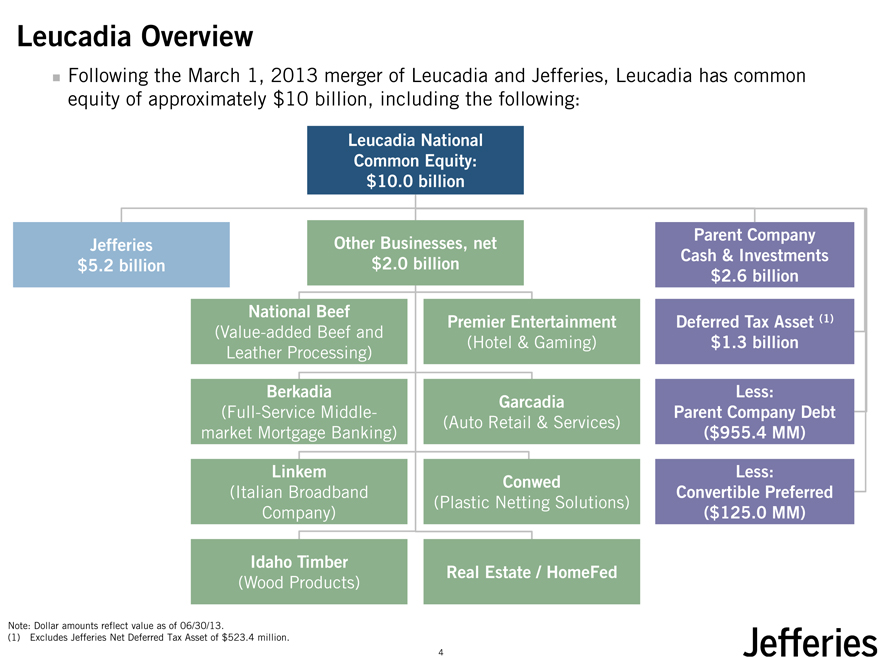

Leucadia Overview

Following the March 1, 2013 merger of Leucadia and Jefferies, Leucadia has common equity of approximately $10 billion, including the following:

Leucadia National Common Equity:

$10.0 billion

Jefferies Other Businesses, net

$5.2 billion $2.0 billion

National Beef

Premier Entertainment

(Value-added Beef and

(Hotel & Gaming) Leather Processing)

Berkadia

Garcadia

(Full-Service Middle-

(Auto Retail & Services) market Mortgage Banking)

Linkem

Conwed

(Italian Broadband

(Plastic Netting Solutions) Company)

Idaho Timber

Real Estate / HomeFed

(Wood Products)

Note: Dollar amounts reflect value as of 06/30/13.

(1) |

| Excludes Jefferies Net Deferred Tax Asset of $523.4 million. |

Parent Company Cash & Investments

$2.6 billion

Deferred Tax Asset (1)

$1.3 billion

Less: Parent Company Debt

($955.4 MM)

Less: Convertible Preferred

($125.0 MM)

4 |

|

|

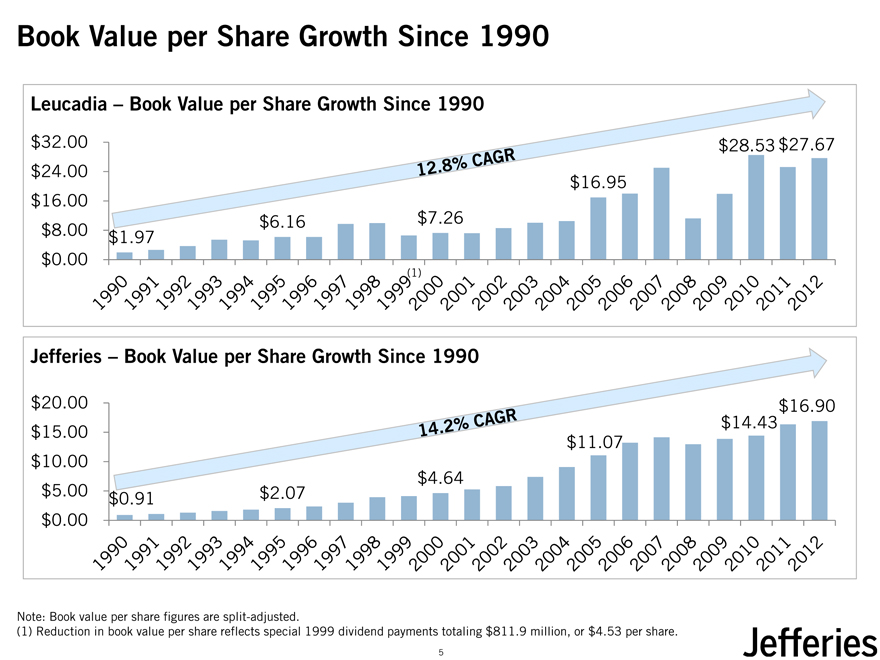

Book Value per Share Growth Since 1990

Leucadia – Book Value per Share Growth Since 1990

$32.00 $28.53 $27.67

$24.00

$16.95

$16.00

$6.16 $7.26

$8.00 $1.97

$0.00 (1)

Jefferies – Book Value per Share Growth Since 1990

$20.00 $16.90

$14.43

$15.00

$11.07

$10.00 $4.64

$5.00 $0.91 $2.07

$0.00

Note: Book value per share figures are split-adjusted.

(1) Reduction in book value per share reflects special 1999 dividend payments totaling $811.9 million, or $4.53 per share.

5 |

|

|

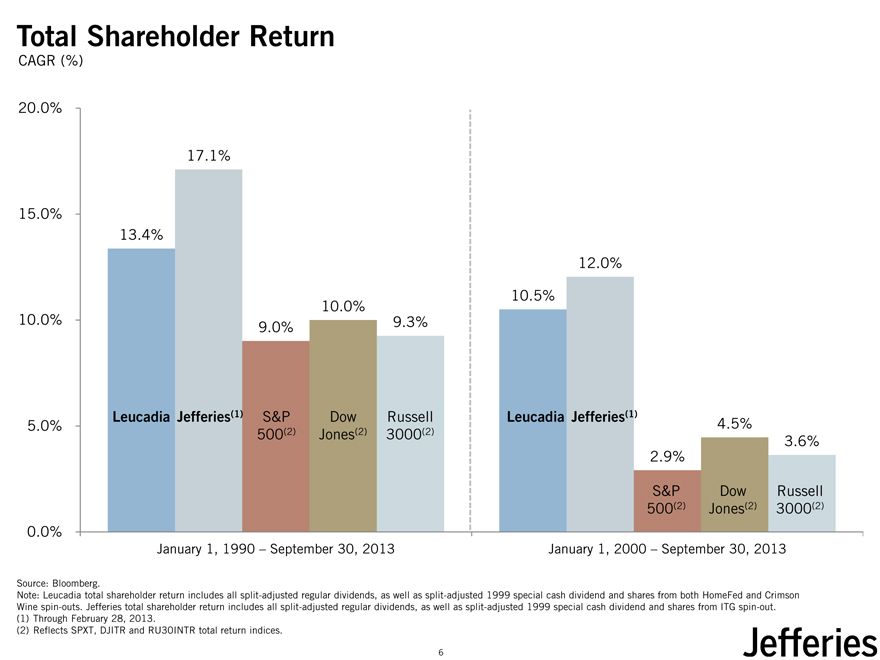

Total Shareholder Return

CAGR (%)

20.0%

17.1%

15.0%

13.4%

12.0%

10.5%

10.0% 10.0%

9.0% 9.3%

Leucadia Jefferies(1) S&P Dow Russell Leucadia Jefferies(1)

5.0% 4.5% 500(2) Jones(2) 3000(2)

3.6%

2.9%

S&P Dow Russell 500(2) Jones(2) 3000(2)

0.0%

January 1, 1990 – September 30, 2013 January 1, 2000 – September 30, 2013

Source: Bloomberg.

Note: Leucadia total shareholder return includes all split-adjusted regular dividends, as well as split-adjusted 1999 special cash dividend and shares from both HomeFed and Crimson Wine spin-outs. Jefferies total shareholder return includes all split-adjusted regular dividends, as well as split-adjusted 1999 special cash dividend and shares from ITG spin-out.

(1) |

| Through February 28, 2013. |

(2) |

| Reflects SPXT, DJITR and RU30INTR total return indices. |

6 |

|

|

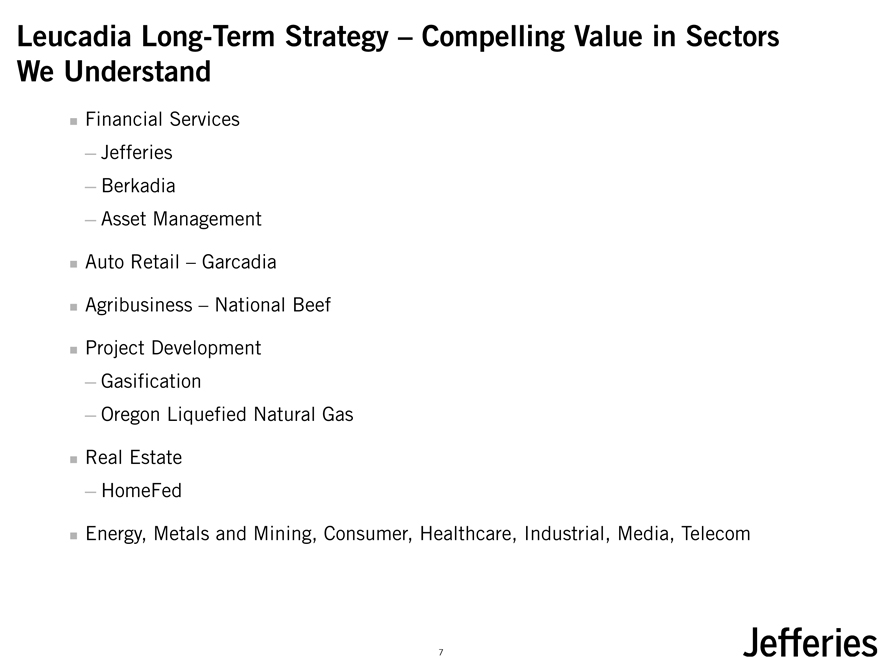

Leucadia Long-Term Strategy – Compelling Value in Sectors We Understand

Financial Services

Jefferies

Berkadia

Asset ManagementAuto Retail – GarcadiaAgribusiness – National Beef

Project Development

Gasification

Oregon Liquefied Natural Gas

Real Estate

HomeFed

Energy, Metals and Mining, Consumer, Healthcare, Industrial, Media, Telecom

7 |

|

|

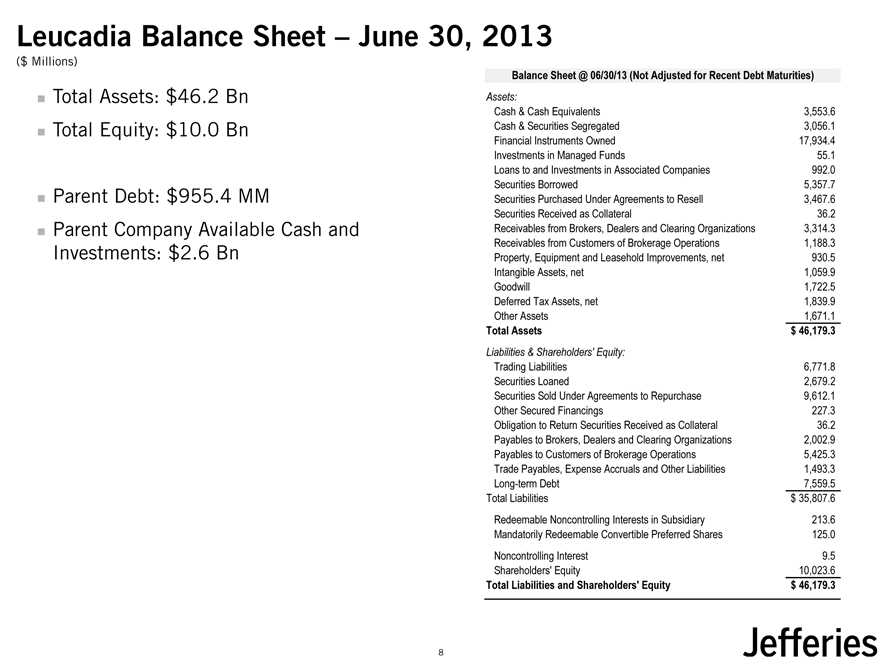

Leucadia Balance Sheet – June 30, 2013

($ Millions)

Total Assets: $46.2 BnTotal Equity: $10.0 Bn

Parent Debt: $955.4 MM

Parent Company Available Cash and Investments: $2.6 Bn

Balance Sheet @ 06/30/13 (Not Adjusted for Recent Debt Maturities)

Assets:

Cash & Cash Equivalents 3,553.6 Cash & Securities Segregated 3,056.1 Financial Instruments Owned 17,934.4 Investments in Managed Funds 55.1 Loans to and Investments in Associated Companies 992.0 Securities Borrowed 5,357.7 Securities Purchased Under Agreements to Resell 3,467.6 Securities Received as Collateral 36.2 Receivables from Brokers, Dealers and Clearing Organizations 3,314.3 Receivables from Customers of Brokerage Operations 1,188.3 Property, Equipment and Leasehold Improvements, net 930.5 Intangible Assets, net 1,059.9 Goodwill 1,722.5 Deferred Tax Assets, net 1,839.9 Other Assets 1,671.1

Total Assets $ 46,179.3

Liabilities & Shareholders’ Equity:

Trading Liabilities 6,771.8 Securities Loaned 2,679.2 Securities Sold Under Agreements to Repurchase 9,612.1 Other Secured Financings 227.3 Obligation to Return Securities Received as Collateral 36.2 Payables to Brokers, Dealers and Clearing Organizations 2,002.9 Payables to Customers of Brokerage Operations 5,425.3 Trade Payables, Expense Accruals and Other Liabilities 1,493.3 Long-term Debt 7,559.5 Total Liabilities $ 35,807.6 Redeemable Noncontrolling Interests in Subsidiary 213.6 Mandatorily Redeemable Convertible Preferred Shares 125.0 Noncontrolling Interest 9.5 Shareholders’ Equity 10,023.6

Total Liabilities and Shareholders’ Equity $ 46,179.3

8 |

|

|

Liquid Assets Overview

($ Millions)

Leucadia has available parent company cash and investments of $2.6 billion, considerably in excess of its $955.4 MM parent company debt

Parent Company Available Cash and Investments of $2.6 billionParent Company Liquid Assets / Parent Company Debt: 2.7xLeucadia’s existing parent company debt matures by 2015

2013: $402 MM (matured and repaid in August 2013)

2014: $98 MM (convertible bond)

2015: $459 MM

9

|

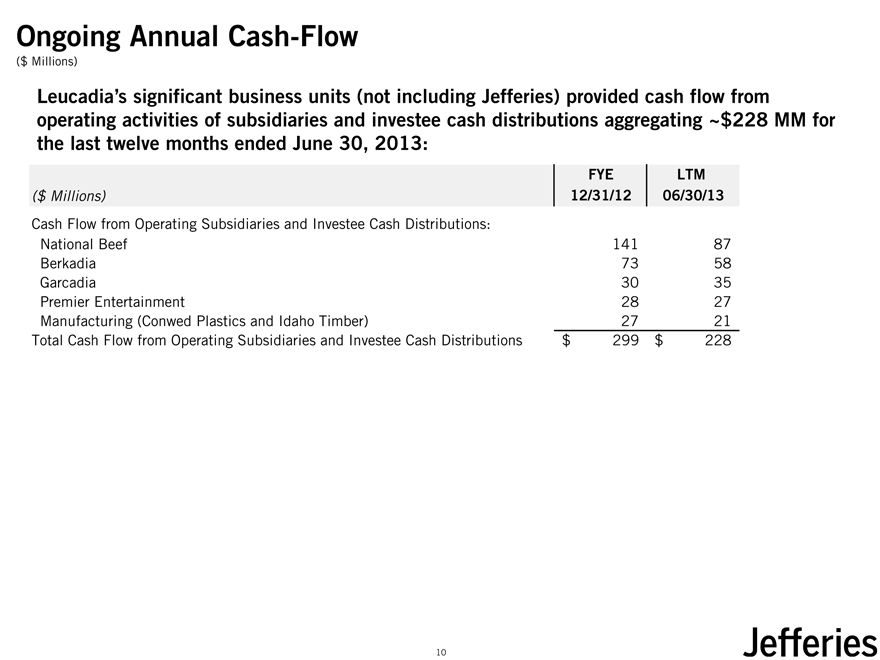

Ongoing Annual Cash-Flow

($ Millions)

Leucadia’s significant business units (not including Jefferies) provided cash flow from operating activities of subsidiaries and investee cash distributions aggregating ~$228 MM for the last twelve months ended June 30, 2013:

FYE LTM

($ Millions) 12/31/12 06/30/13

Cash Flow from Operating Subsidiaries and Investee Cash Distributions:

National Beef 141 87 Berkadia 73 58 Garcadia 30 35 Premier Entertainment 28 27 Manufacturing (Conwed Plastics and Idaho Timber) 27 21 Total Cash Flow from Operating Subsidiaries and Investee Cash Distributions $ 299 $ 228

10

|

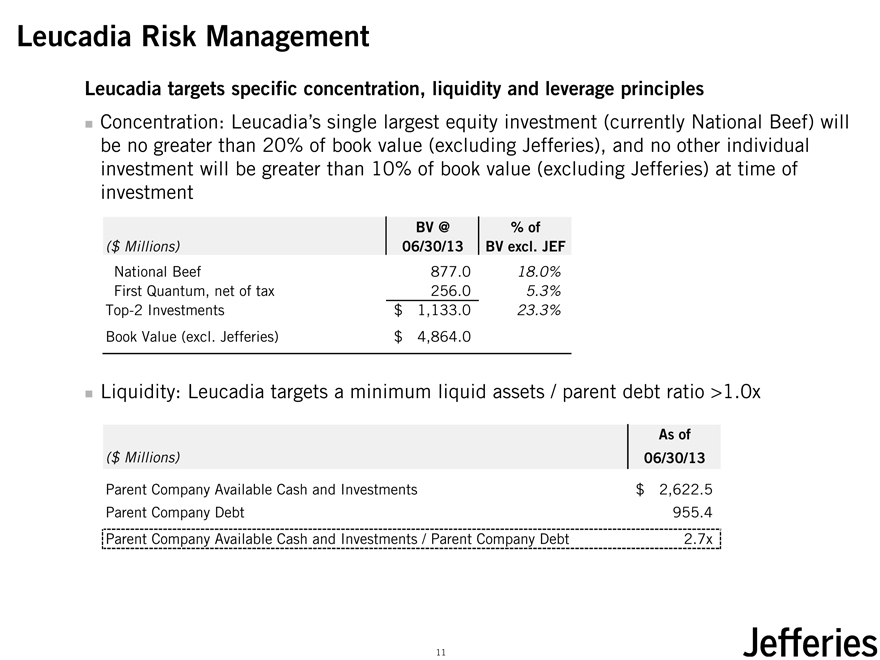

Leucadia Risk Management

Leucadia targets specific concentration, liquidity and leverage principles

Concentration: Leucadia’s single largest equity investment (currently National Beef) will be no greater than 20% of book value (excluding Jefferies), and no other individual investment will be greater than 10% of book value (excluding Jefferies) at time of investment

BV @ % of

($ Millions) 06/30/13 BV excl. JEF

National Beef 877.0 18.0% First Quantum, net of tax 256.0 5.3% Top-2 Investments $ 1,133.0 23.3% Book Value (excl. Jefferies) $ 4,864.0

Liquidity: Leucadia targets a minimum liquid assets / parent debt ratio >1.0x

As of

($ Millions) 06/30/13

Parent Company Available Cash and Investments $ 2,622.5 Parent Company Debt 955.4 Parent Company Available Cash and Investments / Parent Company Debt 2.7x

11

|

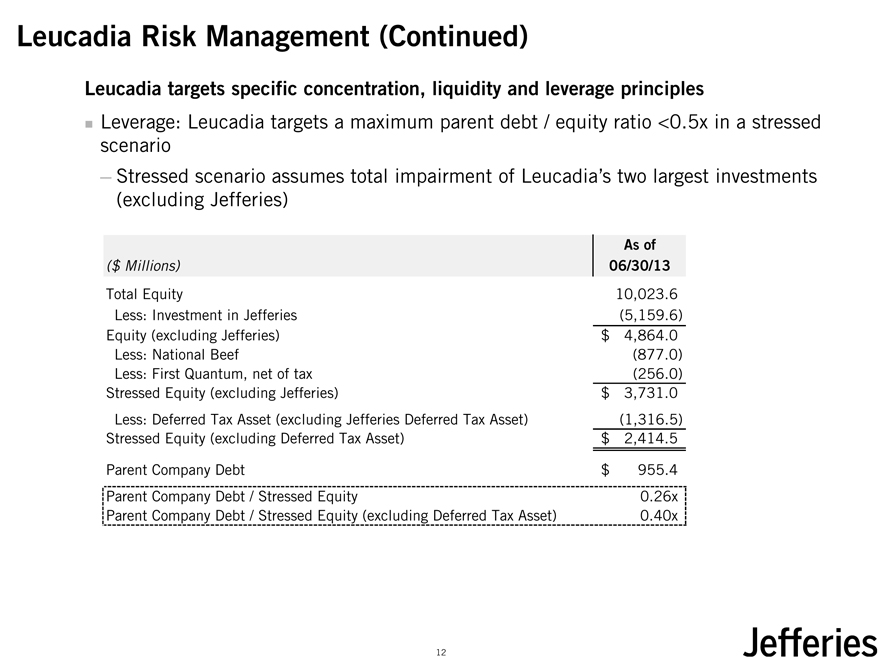

Leucadia Risk Management (Continued)

Leucadia targets specific concentration, liquidity and leverage principles

Leverage: Leucadia targets a maximum parent debt / equity ratio <0.5x in a stressed scenario

Stressed scenario assumes total impairment of Leucadia’s two largest investments (excluding Jefferies)

As of

($ Millions) 06/30/13

Total Equity 10,023.6 Less: Investment in Jefferies (5,159.6) Equity (excluding Jefferies) $ 4,864.0 Less: National Beef (877.0) Less: First Quantum, net of tax (256.0) Stressed Equity (excluding Jefferies) $ 3,731.0 Less: Deferred Tax Asset (excluding Jefferies Deferred Tax Asset) (1,316.5) Stressed Equity (excluding Deferred Tax Asset) $ 2,414.5 Parent Company Debt $ 955.4 Parent Company Debt / Stressed Equity 0.26x Parent Company Debt / Stressed Equity (excluding Deferred Tax Asset) 0.40x

12

|

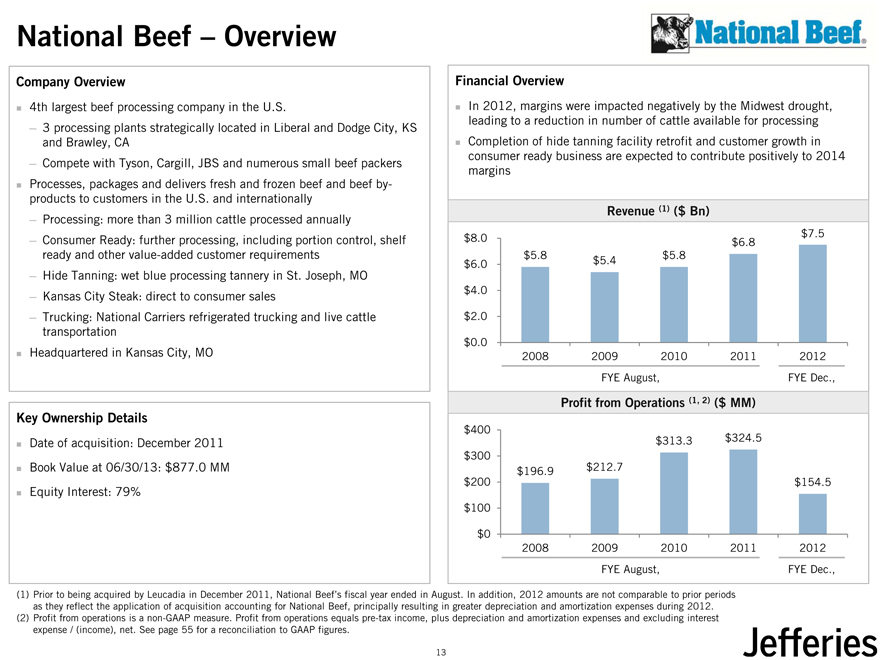

National Beef – Overview

Company Overview

4th largest beef processing company in the U.S.

3 processing plants strategically located in Liberal and Dodge City, KS and Brawley, CA

Compete with Tyson, Cargill, JBS and numerous small beef packersProcesses, packages and delivers fresh and frozen beef and beef by-products to customers in the U.S. and internationally

Processing: more than 3 million cattle processed annually

Consumer Ready: further processing, including portion control, shelf ready and other value-added customer requirements

Hide Tanning: wet blue processing tannery in St. Joseph, MO

Kansas City Steak: direct to consumer sales

Trucking: National Carriers refrigerated trucking and live cattle transportationHeadquartered in Kansas City, MO

Key Ownership Details

Date of acquisition: December 2011Book Value at 06/30/13: $877.0 MM

Equity Interest: 79%

Financial Overview

In 2012, margins were impacted negatively by the Midwest drought, leading to a reduction in number of cattle available for processing Completion of hide tanning facility retrofit and customer growth in consumer ready business are expected to contribute positively to 2014 margins

Revenue (1) ($ Bn)

$8.0 $7.5

$6.8

$5.8 $5.4 $5.8

$6.0

$4.0

$2.0

$0.0

2008 2009 2010 2011 2012 FYE August, FYE Dec.,

Profit from Operations (1, 2) ($ MM)

$400 $313.3 $324.5 $300 $196.9 $212.7 $200 $154.5

$100

$0

2008 2009 2010 2011 2012 FYE August, FYE Dec.,

(1) Prior to being acquired by Leucadia in December 2011, National Beef’s fiscal year ended in August. In addition, 2012 amounts are not comparable to prior periods as they reflect the application of acquisition accounting for National Beef, principally resulting in greater depreciation and amortization expenses during 2012. (2) Profit from operations is a non-GAAP measure. Profit from operations equals pre-tax income, plus depreciation and amortization expenses and excluding interest expense / (income), net. See page 55 for a reconciliation to GAAP figures.

13

|

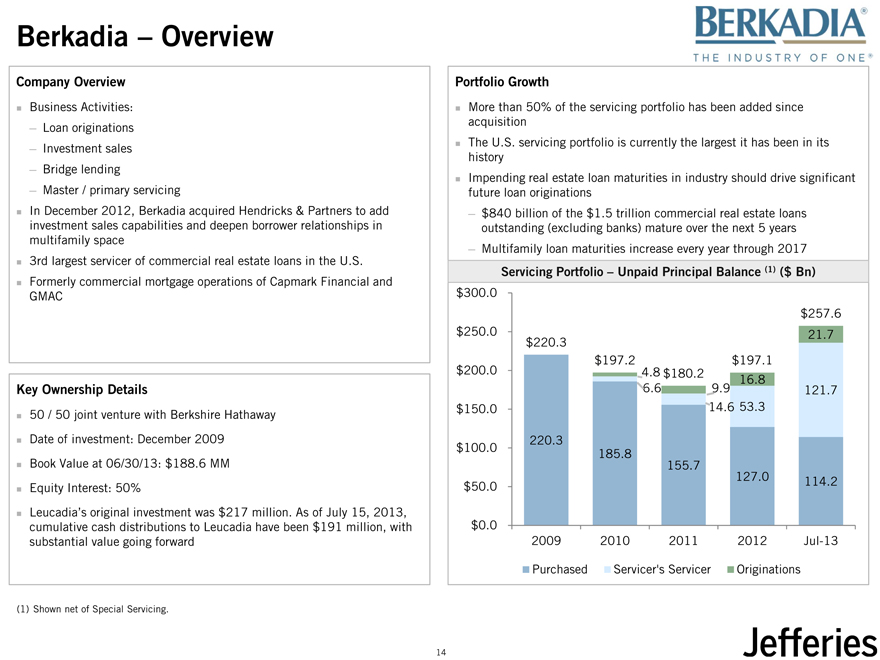

Berkadia – Overview

Company Overview

Business Activities:

Loan originations

Investment sales

Bridge lending

Master / primary servicing

In December 2012, Berkadia acquired Hendricks & Partners to add investment sales capabilities and deepen borrower relationships in multifamily space3rd largest servicer of commercial real estate loans in the U.S. Formerly commercial mortgage operations of Capmark Financial and GMAC

Key Ownership Details

50 / 50 joint venture with Berkshire HathawayDate of investment: December 2009Book Value at 06/30/13: $188.6 MMEquity Interest: 50%

Leucadia’s original investment was $217 million. As of July 15, 2013, cumulative cash distributions to Leucadia have been $191 million, with substantial value going forward

(1) |

| Shown net of Special Servicing. |

Portfolio Growth

More than 50% of the servicing portfolio has been added since acquisitionThe U.S. servicing portfolio is currently the largest it has been in its historyImpending real estate loan maturities in industry should drive significant future loan originations

$840 billion of the $1.5 trillion commercial real estate loans outstanding (excluding banks) mature over the next 5 years

Multifamily loan maturities increase every year through 2017

Servicing Portfolio – Unpaid Principal Balance (1) ($ Bn) $300.0 $257.6 $250.0 21.7 $220.3 $197.2 $197.1 $200.0 4.8 $180.2

16.8

6.6 9.9 121.7 $150.0 14.6 53.3

220.3 $100.0

185.8 155.7

127.0 114.2

$50.0

$0.0

2009 2010 2011 2012 Jul-13

Purchased Servicer’s Servicer Originations

14

|

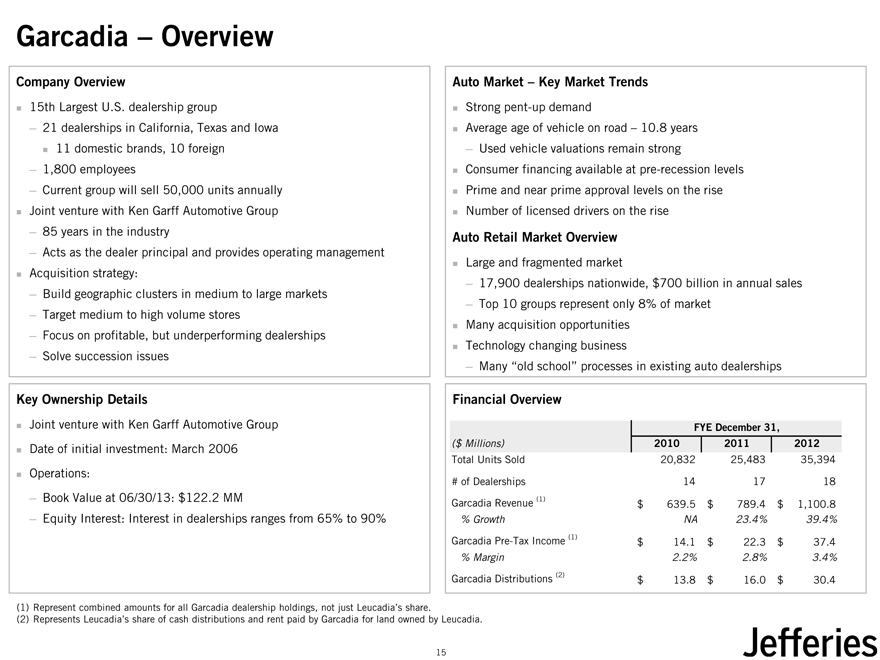

Garcadia – Overview

Company Overview

15th Largest U.S. dealership group

21 dealerships in California, Texas and Iowa11 domestic brands, 10 foreign

1,800 employees

Current group will sell 50,000 units annuallyJoint venture with Ken Garff Automotive Group

85 years in the industry

Acts as the dealer principal and provides operating managementAcquisition strategy:

Build geographic clusters in medium to large markets

Target medium to high volume stores

Focus on profitable, but underperforming dealerships

Solve succession issues

Key Ownership Details

Joint venture with Ken Garff Automotive GroupDate of initial investment: March 2006Operations:

Book Value at 06/30/13: $122.2 MM

Equity Interest: Interest in dealerships ranges from 65% to 90%

Auto Market – Key Market Trends

Strong pent-up demand

Average age of vehicle on road – 10.8 years

Used vehicle valuations remain strong

Consumer financing available at pre-recession levelsPrime and near prime approval levels on the riseNumber of licensed drivers on the rise

Auto Retail Market Overview

Large and fragmented market

17,900 dealerships nationwide, $700 billion in annual sales

Top 10 groups represent only 8% of marketMany acquisition opportunitiesTechnology changing business

Many “old school” processes in existing auto dealerships

Financial Overview

FYE December 31,

($ Millions) 2010 2011 2012

Total Units Sold 20,832 25,483 35,394 # of Dealerships 14 17 18 Garcadia Revenue (1) $ 639.5 $ 789.4 $ 1,100.8

% Growth NA 23.4% 39.4%

Garcadia Pre-Tax Income (1) $ 14.1 $ 22.3 $ 37.4

% Margin 2.2% 2.8% 3.4%

Garcadia Distributions (2) $ 13.8 $ 16.0 $ 30.4

(1) |

| Represent combined amounts for all Garcadia dealership holdings, not just Leucadia’s share. |

(2) |

| Represents Leucadia’s share of cash distributions and rent paid by Garcadia for land owned by Leucadia. |

15

|

Other Businesses

Premier Entertainment

Hard Rock Hotel & Casino Biloxi, MS – 325 room hotel with 50,000 square feet of gamingCurrently constructing a 154-room tower addition to hotel06/30/13 LTM Cash Flow from Operating Activities: $26.5 MM

Manufacturing (Conwed Plastics and Idaho Timber)

06/30/13 LTM Cash Flow from Operating Activities: $21.4 MM

Conwed Plastics

A market leader in lightweight oriented and extruded plastic netting

Partners with customers to customize core technology into innovative solutions

Idaho Timber

Wood product manufacture and distribution

Operations in primary milling, clear boards and dimensional lumber remanufacturing

Linkem

Acquired wireless spectrum licenses in 2008 at highly attractive pricing

Wireless broadband services provider in Italy

Real Estate / HomeFed

Residential and commercial U.S. real estate portfolio

HomeFed is a developer of residential real estate projects

16

|

Other Businesses (continued)

Gasification

Potential development of gasification project in Lake Charles, Louisiana

Will convert various low grade fossil fuels into clean energy products, including methanol and hydrogen

Off-take agreements signed for the vast majority of the project’s production

Awarded significant tax-exempt financing, grants and tax credits for the project

Project is fully permitted

Oregon LNG

Leasehold interest and pursuing permits for onshore LNG terminal in Warrenton, Oregon

Capacity to supply Asian LNG markets at low expected shipping costs

Access to existing underutilized Western gas pipeline grid and storage infrastructure

17

|

Jefferies Overview

18

|

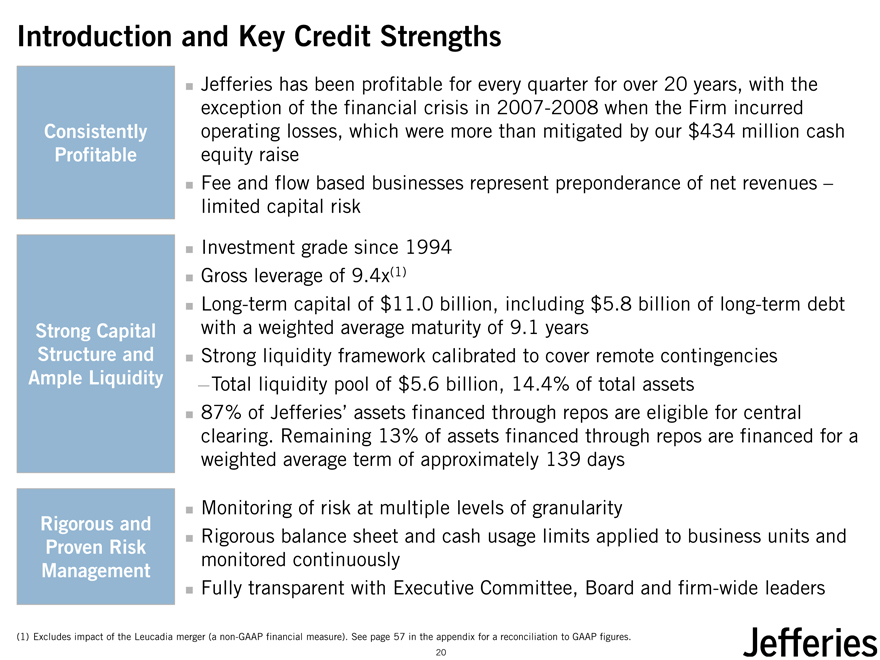

Introduction and Key Credit Strengths

Jefferies is a wholly owned subsidiary of Leucadia National Corp. (NYSE: LUK)Richard Handler and Brian Friedman, with over 60 years of combined experience (more than half at Jefferies), have led Jefferies for over 12 years Committed, and empowered Executive Committee comprised of 15 members of

Aligned, Highly Active

Experienced senior management including the CEO and Chairman of the Committee Leadership These 15 members average over 28 years of industry experience and over 10 Team years at JefferiesStrongly aligned with long-term successExecutive management team is experienced

Consistent business model

Trading is focused on clients – limited proprietary trading / investing activityHighly liquid trading inventory, 97% of our inventory is Level 1 or Level 2

Client Focused,

Liquid & All funding is secured, and readily and consistently available through clearing Straight-Forward houses, or fixed for periods of time that exceed the expected tenure of the Business Model inventory it is fundingNo material exposure to highly structured derivatives or difficult-to-price securities

19

|

Introduction and Key Credit Strengths

Jefferies has been profitable for every quarter for over 20 years, with the exception of the financial crisis in 2007-2008 when the Firm incurred Consistently operating losses, which were more than mitigated by our $434 million cash Profitable equity raiseFee and flow based businesses represent preponderance of net revenues –limited capital riskInvestment grade since 1994 Gross (1) leverage of 9.4xLong-term capital of $11.0 billion, including $5.8 billion of long-term debt Strong Capital with a weighted average maturity of 9.1 years Structure and Strong liquidity framework calibrated to cover remote contingencies Ample Liquidity Total liquidity pool of $5.6 billion, 14.4% of total assets87% of Jefferies’ assets financed through repos are eligible for central clearing. Remaining 13% of assets financed through repos are financed for a weighted average term of approximately 139 days

Monitoring of risk at multiple levels of granularity

Rigorous and

Rigorous balance sheet and cash usage limits applied to business units and

Proven Risk monitored continuously

Management

Fully transparent with Executive Committee, Board and firm-wide leaders

(1) Excludes impact of the Leucadia merger (a non-GAAP financial measure). See page 57 in the appendix for a reconciliation to GAAP figures.

20

|

Jefferies Group

Full-Service Capital Markets Platform: expertise and depth across equities, fixed income, commodities and investment bankingClient-Focused: providing investor and issuer clients with the highest quality advice and executionGlobal Footprint: sales & trading and investment banking presence across the United States, Europe and AsiaStrong, Stable Foundation: robust long-term capital base, comparatively low leverage and free from dependence upon government supportPositioned to Seize Market Share: having broadened our product offering and hired additional key talent during the downturn, Jefferies is positioned to grow rapidly

21

|

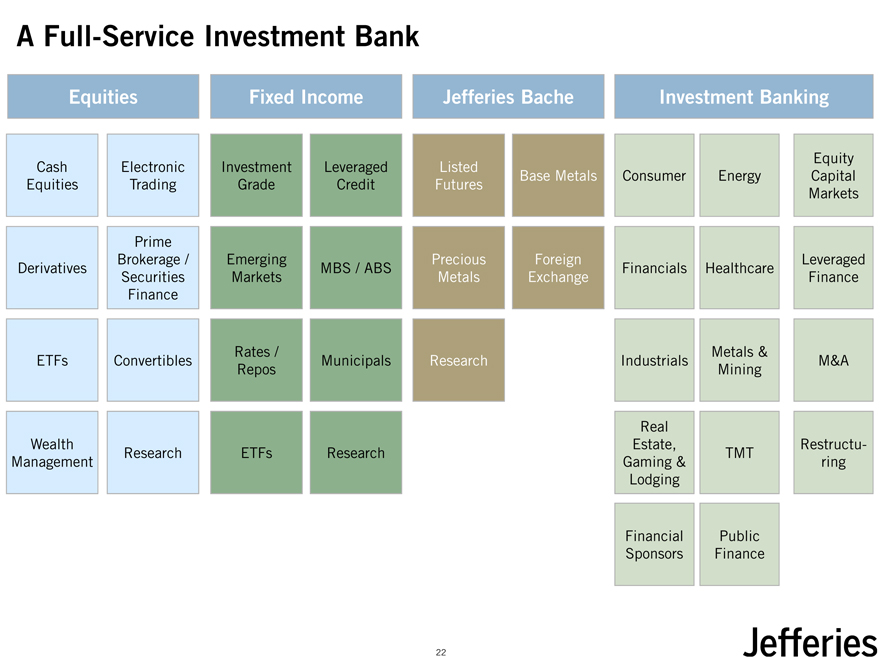

A Full-Service Investment Bank

Equities Fixed Income Jefferies Bache Investment Banking

Equity Cash Electronic Investment Leveraged Listed Base Metals Consumer Energy Capital Equities Trading Grade Credit Futures Markets

Prime

Brokerage / Emerging Precious Foreign Leveraged Derivatives MBS / ABS Financials Healthcare Securities Markets Metals Exchange Finance Finance

Rates / Metals &

ETFs Convertibles Municipals Research Industrials M&A Repos Mining

Real

Wealth Estate, Restructu-Research ETFs Research TMT

Management Gaming & ring Lodging

Financial Public Sponsors Finance

22

|

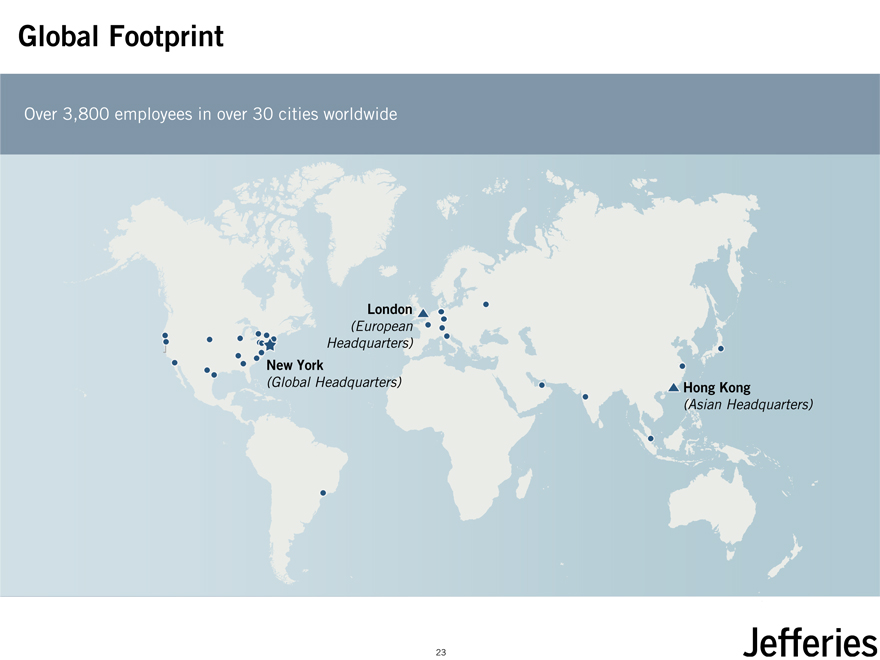

Global Footprint

Over 3,800 employees in over 30 cities worldwide

London

(European Headquarters)

New York

(Global Headquarters) Hong Kong

(Asian Headquarters)

23

|

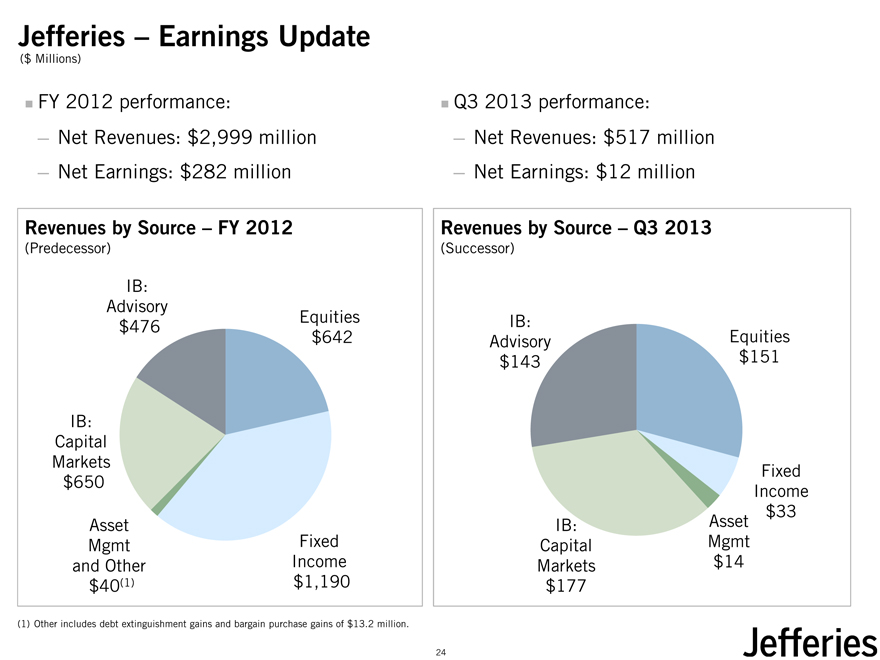

Jefferies – Earnings Update

($ Millions)

FY 2012 performance:

Net Revenues: $2,999 million

Net Earnings: $282 million

Revenues by Source – FY 2012

(Predecessor)

IB: Advisory

Equities $476 $642

IB: Capital Markets $650

Asset Fixed Mgmt Income and Other

$40(1) $1,190

(1) |

| Other includes debt extinguishment gains and bargain purchase gains of $13.2 million. |

Q3 2013 performance:

Net Revenues: $517 million

Net Earnings: $12 million

Revenues by Source – Q3 2013

(Successor)

IB:

Advisory Equities $143 $151

Fixed Income $33 IB: Asset Capital Mgmt Markets $14 $177

24

|

Jefferies Strategic Outlook

Post the Leucadia merger, Jefferies remains one of the world’s best capitalized investment banking firmsJefferies continues to win market share and deliver consistent profitability

Investment Banking revenues underline the quality and durability of Jefferies’ platform

Solid growth in Equities revenues (new senior leadership)

Durable Fixed Income, Commodities and Currencies platforms, despite recent market volatilityContinued emphasis on earnings growth through increased employee productivity and cross-product client penetrationFull-service capabilities and momentum outside the U.S. present a significant growth opportunityWell-positioned to capitalize on ongoing regulatory and business challenges faced by our competitors

25

|

Jefferies Business Review

26

|

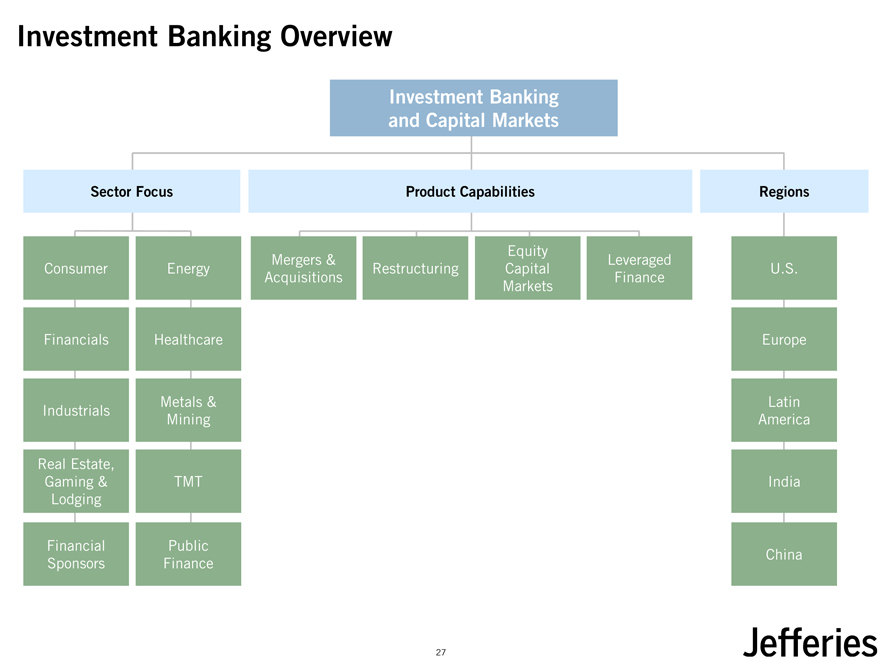

Investment Banking Overview

Investment Banking and Capital Markets

Sector Focus Product Capabilities Regions

Equity

Mergers & Leveraged

Consumer Energy Restructuring Capital U.S. Acquisitions Finance Markets

Financials Healthcare Europe

Metals & Latin Industrials Mining America

Real Estate,

Gaming & TMT India Lodging

Financial Public

China Sponsors Finance

27

|

Investment Banking – Strategic Priorities

Continue to increase productivity

Productivity has increased steadily

Further productivity increases expected as recent senior hires reach targeted productivity levels

Increase U.S. market share across investment banking

Significant incremental opportunity in TMT, Consumer, Industrials, FIG and Real Estate

Capitalize on full-service capabilities and momentum in Europe and Asia

192 investment bankers in Europe and Asia

Strong presence in Healthcare, Energy, TMT and Consumer

Significant momentum in local debt and equity capital markets

28

|

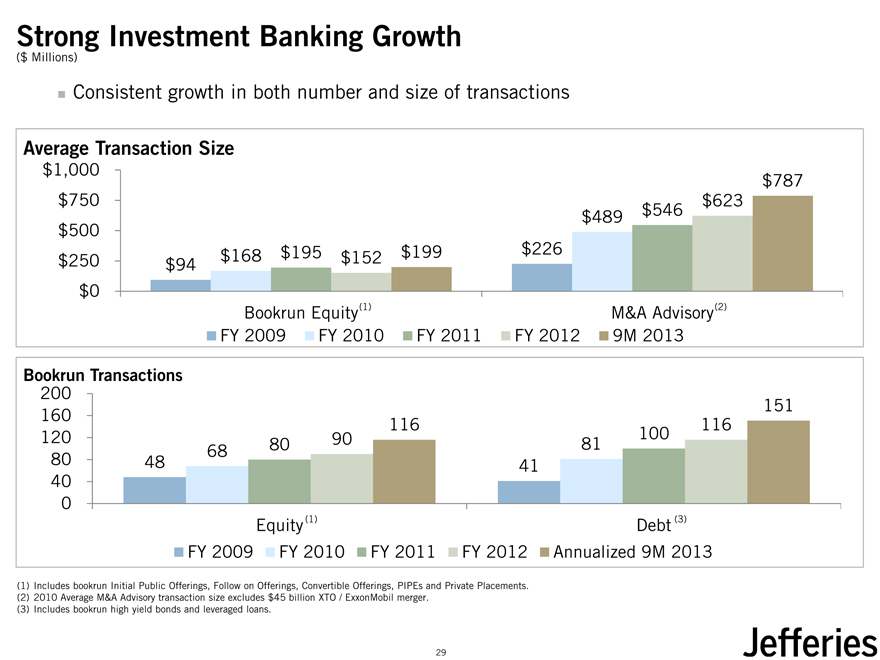

Strong Investment Banking Growth

($ Millions)

Consistent growth in both number and size of transactions

Average Transaction Size

$1,000 $787 $750 $623 $489 $546 $500 $168 $195 $199 $226 $250 $94 $152 $0 Bookrun Equity(1) M&A Advisory(2) FY 2009 FY 2010 FY 2011 FY 2012 9M 2013

Bookrun Transactions

200

151 160 116 116 120 90 100

68 80 81

80 48 41 40 0

Equity(1) Debt (3) FY 2009 FY 2010 FY 2011 FY 2012 Annualized 9M 2013

(1) Includes bookrun Initial Public Offerings, Follow on Offerings, Convertible Offerings, PIPEs and Private Placements. (2) 2010 Average M&A Advisory transaction size excludes $45 billion XTO / ExxonMobil merger.

(3) |

| Includes bookrun high yield bonds and leveraged loans. |

29

|

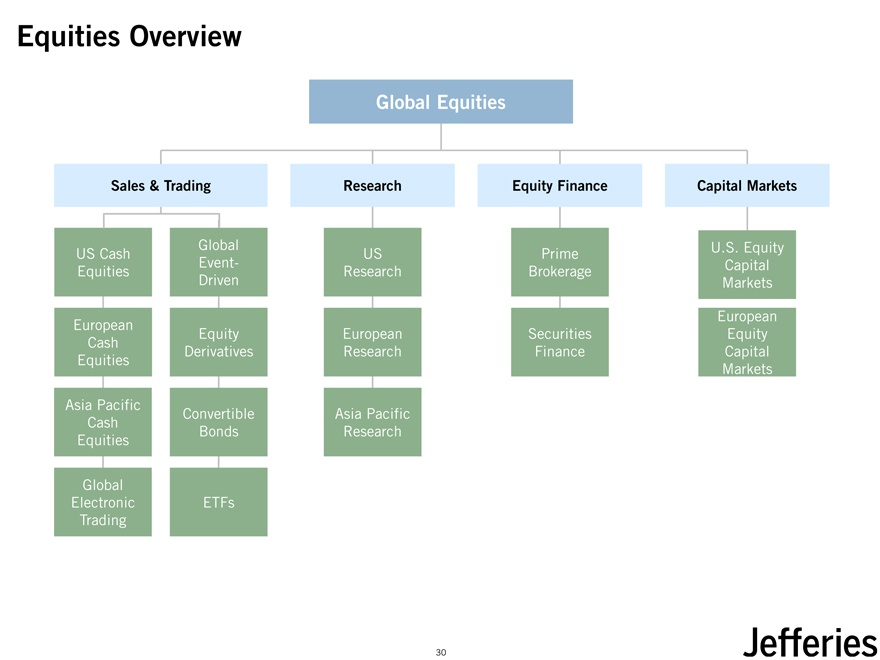

Equities Overview

Global Equities

Sales & Trading Research Equity Finance Capital Markets

Global U.S. Equity US Cash US Prime Event- Capital Equities Research Brokerage Driven Markets European European Equity European Securities Equity Cash Derivatives Research Finance Capital Equities Markets

Asia Pacific

Convertible Asia Pacific Cash Bonds Research Equities

Global

Electronic ETFs Trading

30

|

Equities – Strategic Priorities

Grow market share

Capture market share through superior execution and value-added research

Expand electronic offerings to match client demand

Grow European and Asian revenues

High quality sales, trading and research capabilities in London and Hong Kong

Significant opportunity to grow market share and meaningfully increase revenues

Equity capital markets and corporate broking leverage local investment banking strength

Increase productivity

Drive productivity by increasing share of client wallet

Increase cross-product client penetration

Leverage relationships across Jefferies to win new clients and grow penetration across all products

31

|

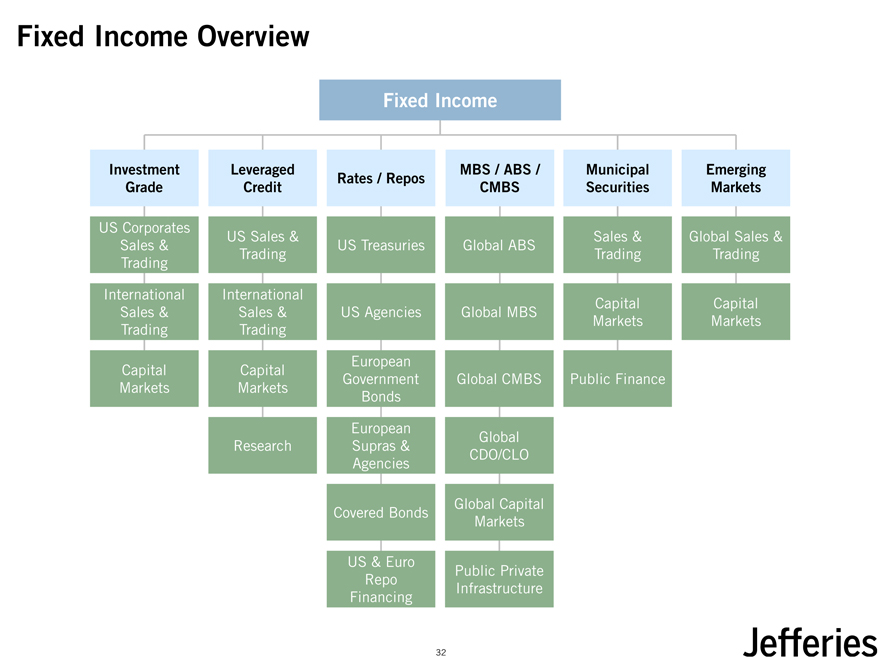

Fixed Income Overview

Fixed Income

Investment Leveraged

Rates / Repos Grade Credit

US Corporates

US Sales &

Sales & US Treasuries Trading Trading International International Sales & Sales & US Agencies Trading Trading European Capital Capital Government Markets Markets Bonds European Research Supras & Agencies

Covered Bonds

US & Euro Repo Financing

MBS / ABS / Municipal Emerging CMBS Securities Markets

Sales & Global Sales & Global ABS

Trading Trading

Capital Capital Global MBS

Markets Markets

Global CMBS Public Finance

Global CDO/CLO

Global Capital Markets

Public Private Infrastructure

32

|

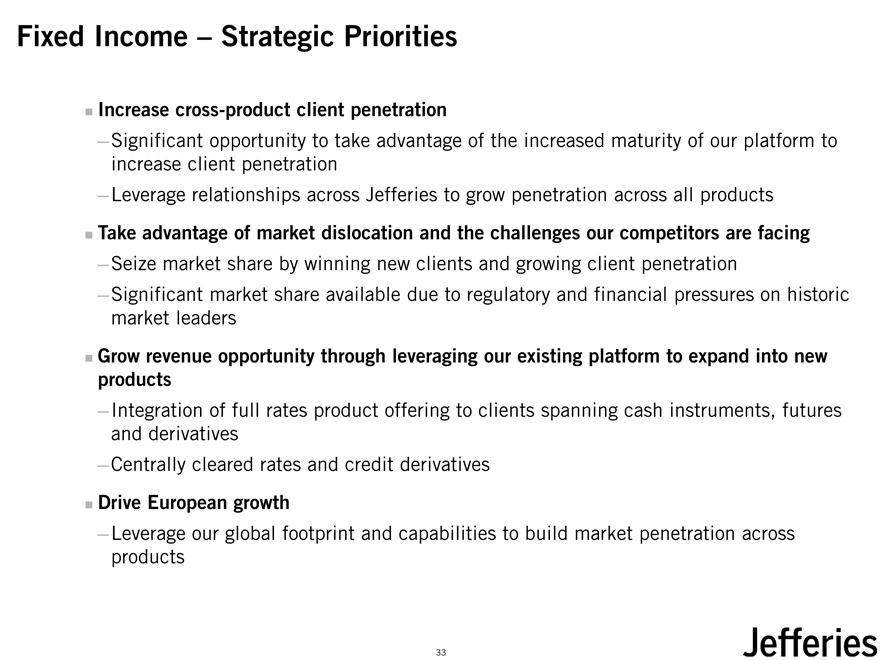

Fixed Income – Strategic Priorities

Increase cross-product client penetration

Significant opportunity to take advantage of the increased maturity of our platform to increase client penetration

Leverage relationships across Jefferies to grow penetration across all products

Take advantage of market dislocation and the challenges our competitors are facing

Seize market share by winning new clients and growing client penetration

Significant market share available due to regulatory and financial pressures on historic market leaders

Grow revenue opportunity through leveraging our existing platform to expand into new products

Integration of full rates product offering to clients spanning cash instruments, futures and derivatives

Centrally cleared rates and credit derivatives

Drive European growth

Leverage our global footprint and capabilities to build market penetration across products

33

|

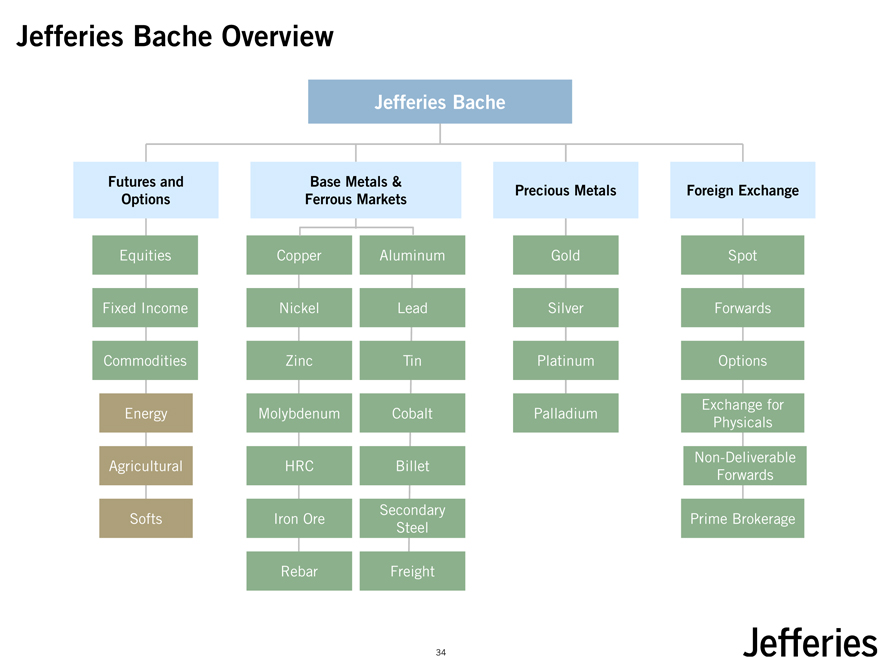

Jefferies Bache Overview

Jefferies Bache

Futures and Base Metals &

Precious Metals Foreign Exchange Options Ferrous Markets

Equities Copper Aluminum Gold Spot Fixed Income Nickel Lead Silver Forwards Commodities Zinc Tin Platinum Options

Exchange for Energy Molybdenum Cobalt Palladium Physicals

Non-Deliverable Agricultural HRC Billet Forwards

Secondary

Softs Iron Ore Prime Brokerage Steel

Rebar Freight

34

|

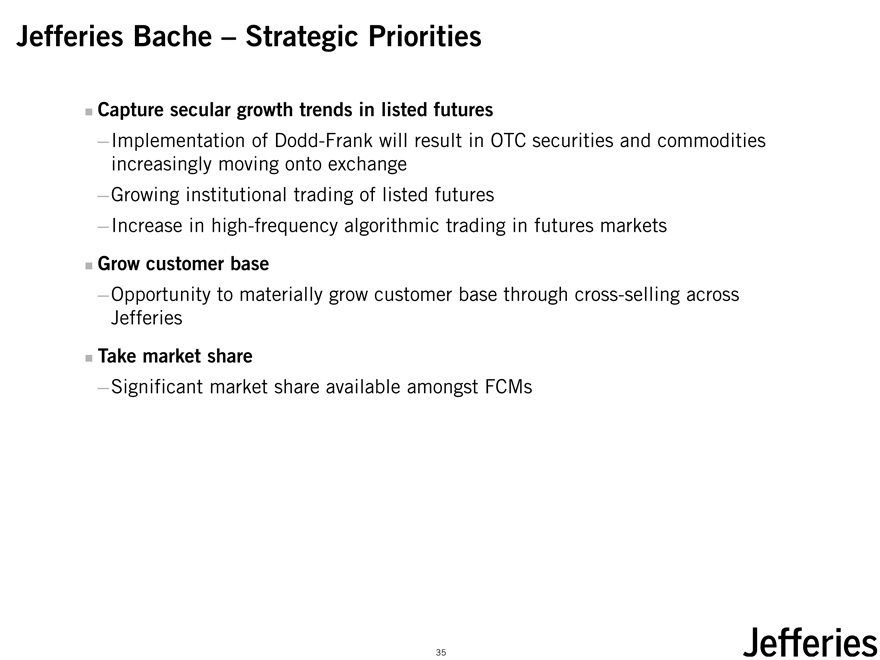

Jefferies Bache – Strategic Priorities

Capture secular growth trends in listed futures

Implementation of Dodd-Frank will result in OTC securities and commodities increasingly moving onto exchange

Growing institutional trading of listed futures

Increase in high-frequency algorithmic trading in futures markets

Grow customer base

Opportunity to materially grow customer base through cross-selling across Jefferies

Take market share

Significant market share available amongst FCMs

35

|

Regional Positioning

Jefferies is growing market share in Europe

Full-service European capabilities; 950 professionals in the UK and Continental Europe

Investment Banking: significant growth in advisory and capital markets issuance, materially enhanced by the acquisition of Hoare Govett in February 2012

Equities: client momentum and recovering European markets are driving growth

Fixed Income: strong local presence and the ability to capitalize on ongoing volatility in European credit markets

Strong momentum in Asia

Strong local investment banking presence

Full-service equity sales, trading and research capabilities across Asia Pacific

36

|

Regulatory Outlook

Jefferies is well-positioned to capitalize on upcoming global regulatory change

Unlike many of our competitors, Jefferies is client-focused and not materially leveraged to earnings from proprietary activities

Since Jefferies is not a bank holding company, it is less impacted by the provisions of the Dodd-Frank Act

Jefferies expects to benefit from regulatory changes in both the U.S. and Europe

In the U.S., Jefferies is well-positioned to take market share from competitors scaling down or exiting from trading activities, particularly in fixed income

In Europe, regulatory pressure has forced major banks to re-evaluate capital markets platforms and has led several banks to exit certain businesses

OTC swaps moving on to exchange will meaningfully expand Jefferies’ revenue opportunity

Jefferies anticipates actively participating in centrally cleared exchange traded swap and other derivative markets

37

|

Jefferies Operating Results

38

|

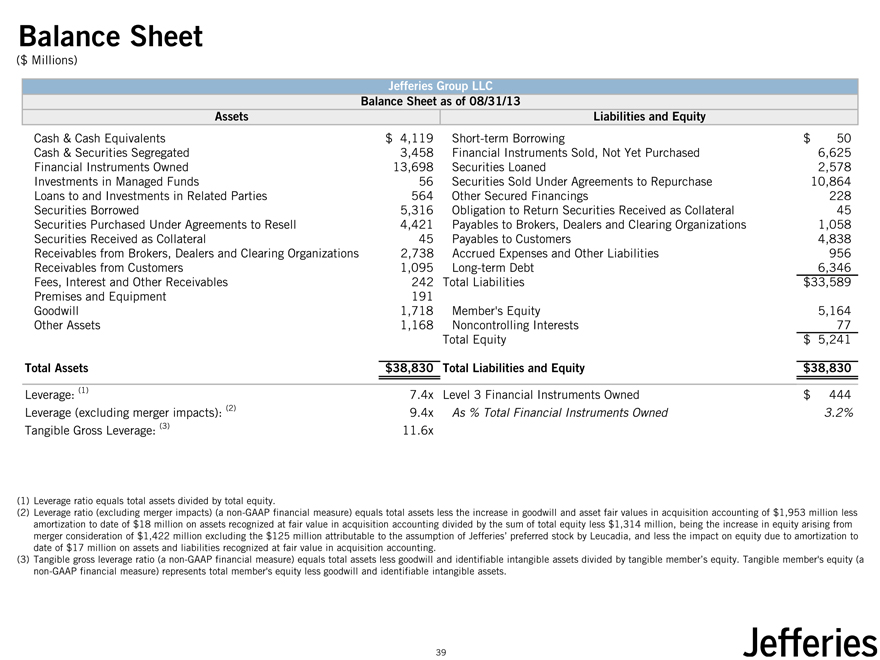

Balance Sheet

($ Millions)

Jefferies Group LLC Balance Sheet as of 08/31/13

Assets Liabilities and Equity

Cash & Cash Equivalents $ 4,119 Short-term Borrowing $ 50 Cash & Securities Segregated 3,458 Financial Instruments Sold, Not Yet Purchased 6,625 Financial Instruments Owned 13,698 Securities Loaned 2,578 Investments in Managed Funds 56 Securities Sold Under Agreements to Repurchase 10,864 Loans to and Investments in Related Parties 564 Other Secured Financings 228 Securities Borrowed 5,316 Obligation to Return Securities Received as Collateral 45 Securities Purchased Under Agreements to Resell 4,421 Payables to Brokers, Dealers and Clearing Organizations 1,058 Securities Received as Collateral 45 Payables to Customers 4,838 Receivables from Brokers, Dealers and Clearing Organizations 2,738 Accrued Expenses and Other Liabilities 956 Receivables from Customers 1,095 Long-term Debt 6,346 Fees, Interest and Other Receivables 242 Total Liabilities $33,589 Premises and Equipment 191 Goodwill 1,718 Member’s Equity 5,164 Other Assets 1,168 Noncontrolling Interests 77 Total Equity $ 5,241

Total Assets $38,830 Total Liabilities and Equity $38,830

Leverage: (1) 7.4x Level 3 Financial Instruments Owned $ 444 Leverage (excluding merger impacts): (2) 9.4x As % Total Financial Instruments Owned 3.2%

Tangible Gross Leverage: (3) 11.6x

(1) |

| Leverage ratio equals total assets divided by total equity. |

(2) Leverage ratio (excluding merger impacts) (a non-GAAP financial measure) equals total assets less the increase in goodwill and asset fair values in acquisition accounting of $1,953 million less amortization to date of $18 million on assets recognized at fair value in acquisition accounting divided by the sum of total equity less $1,314 million, being the increase in equity arising from merger consideration of $1,422 million excluding the $125 million attributable to the assumption of Jefferies’ preferred stock by Leucadia, and less the impact on equity due to amortization to date of $17 million on assets and liabilities recognized at fair value in acquisition accounting.

(3) Tangible gross leverage ratio (a non-GAAP financial measure) equals total assets less goodwill and identifiable intangible assets divided by tangible member’s equity. Tangible member’s equity (a non-GAAP financial measure) represents total member’s equity less goodwill and identifiable intangible assets.

39

|

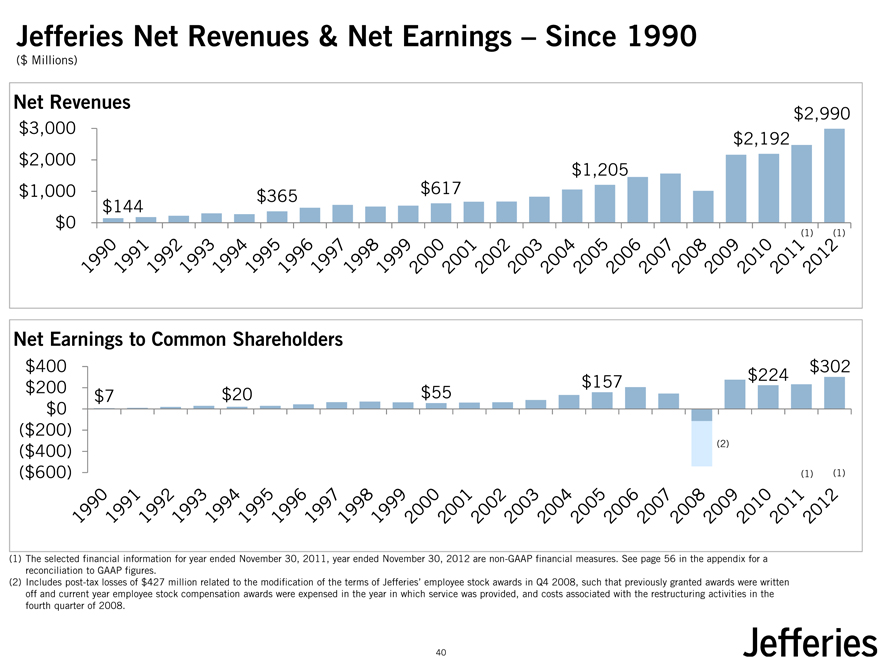

Jefferies Net Revenues & Net Earnings – Since 1990

($ Millions)

Net Revenues

$2,990 $3,000 $2,192 $2,000 $1,205 $1,000 $365 $617

$0 $144

(1) |

| (1) |

Net Earnings to Common Shareholders

$400 $302 $157 $224 $200 $20 $55 $7 $0

($200)

($400) (2)

($600) (1) (1)

(1) The selected financial information for year ended November 30, 2011, year ended November 30, 2012 are non-GAAP financial measures. See page 56 in the appendix for a reconciliation to GAAP figures.

(2) Includes post-tax losses of $427 million related to the modification of the terms of Jefferies’ employee stock awards in Q4 2008, such that previously granted awards were written off and current year employee stock compensation awards were expensed in the year in which service was provided, and costs associated with the restructuring activities in the fourth quarter of 2008.

40

|

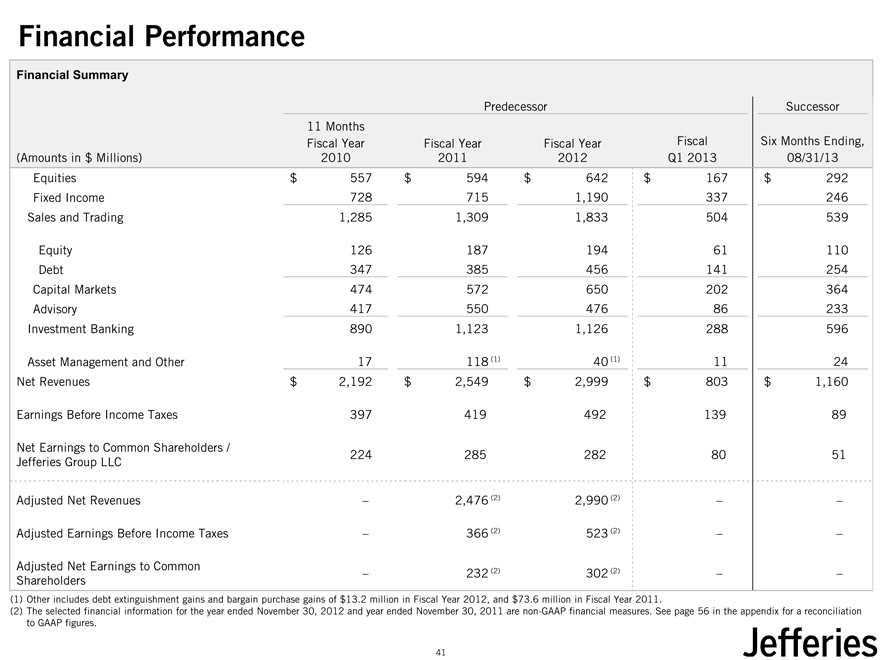

Financial Performance

Financial Summary

Predecessor Successor

11 Months

Fiscal Year Fiscal Year Fiscal Year Fiscal Six Months Ending, (Amounts in $ Millions) 2010 2011 2012 Q1 2013 08/31/13 Equities $ 557 $ 594 $ 642 $ 167 $ 292 Fixed Income 728 715 1,190 337 246 Sales and Trading 1,285 1,309 1,833 504 539

Equity 126 187 194 61 110 Debt 347 385 456 141 254 Capital Markets 474 572 650 202 364 Advisory 417 550 476 86 233 Investment Banking 890 1,123 1,126 288 596

Asset Management and Other 17 118 (1) 40 (1) 11 24 Net Revenues $ 2,192 $ 2,549 $ 2,999 $ 803 $ 1,160

Earnings Before Income Taxes 397 419 492 139 89

Net Earnings to Common Shareholders /

224 285 282 80 51 Jefferies Group LLC

Adjusted Net Revenues – 2,476 (2) 2,990 (2) – –

Adjusted Earnings Before Income Taxes – 366 (2) 523 (2) – –

Adjusted Net Earnings to Common (2) (2)

– 232 302 – – Shareholders

(1) Other includes debt extinguishment gains and bargain purchase gains of $13.2 million in Fiscal Year 2012, and $73.6 million in Fiscal Year 2011.

(2) The selected financial information for the year ended November 30, 2012 and year ended November 30, 2011 are non-GAAP financial measures. See page 56 in the appendix for a reconciliation to GAAP figures.

41

|

Compensation Overview

Jefferies has taken advantage of the challenges faced by our competitors by upgrading talent across our firm

Many competitors have significantly reduced compensation levels, leading to an exodus of talentOur new professionals have been a key driver of growthLag between hiring senior employees and their achieving run-rate revenue production has elevated Jefferies’ compensation ratio

This lag particularly impacts senior investment bankers, who have comprised a meaningful portion of Jefferies’ senior hiring since 2010Although Jefferies has successfully remained within our stated upper-bound 60% compensation ratio, we expect the ratio to decline over time as our hires reach their targeted productivity, net revenue grows and start-up amortization declines Over the past two years, compensation has also been impacted by amortization of certain compensation expenses typically associated with senior hires

Amortization expense is expected to decline significantly over the next three years, reducing the firm’s overall compensation ratio

42

|

Risk Management

43

|

Risk Principles

Jefferies’ comprehensive risk management framework has been a foundation for our success across market cycles

Culture

We are all risk managers. Our firm is built on every individual taking responsibility for risk management, including our senior management

Hands-on

Our senior management is deeply involved in the “nuts and bolts” of how and where we are taking risks across the firm

Integrated

Our risk management group and our business leaders are deeply integrated into our trading desks, ensuring a clear and comprehensive view of the firm’s risk

Asset Quality

Jefferies is dedicated to serving our clients in liquid, transparent products. We limit illiquid assets and derivatives to ensure the overall liquidity and health of our balance sheet

44

|

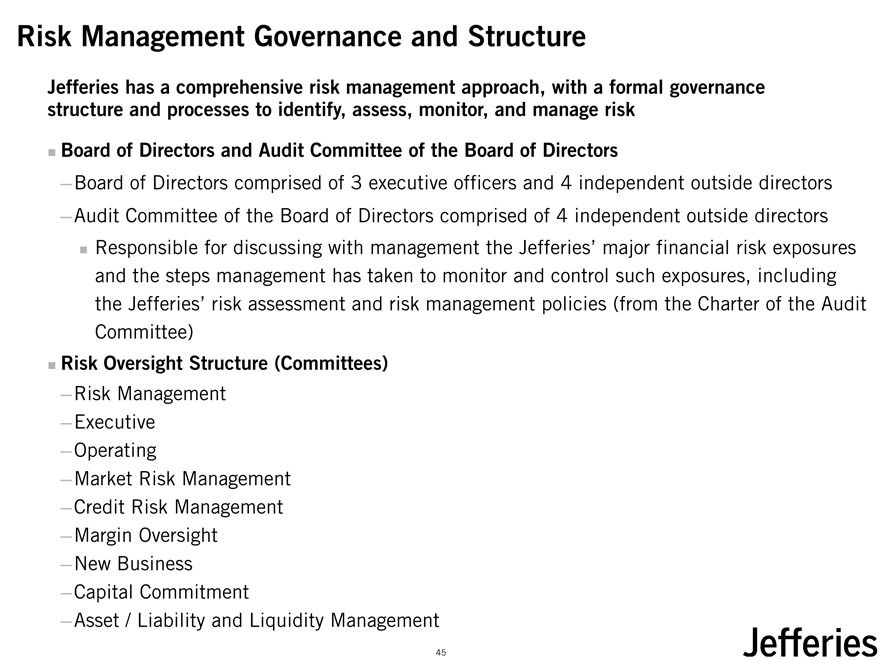

Risk Management Governance and Structure

Jefferies has a comprehensive risk management approach, with a formal governance structure and processes to identify, assess, monitor, and manage risk

Board of Directors and Audit Committee of the Board of Directors

Board of Directors comprised of 3 executive officers and 4 independent outside directors

Audit Committee of the Board of Directors comprised of 4 independent outside directorsResponsible for discussing with management the Jefferies’ major financial risk exposures and the steps management has taken to monitor and control such exposures, including the Jefferies’ risk assessment and risk management policies (from the Charter of the Audit Committee)

Risk Oversight Structure (Committees)

Risk Management

Executive

Operating

Market Risk Management

Credit Risk Management

Margin Oversight

New Business

Capital Commitment

Asset / Liability and Liquidity Management

45

|

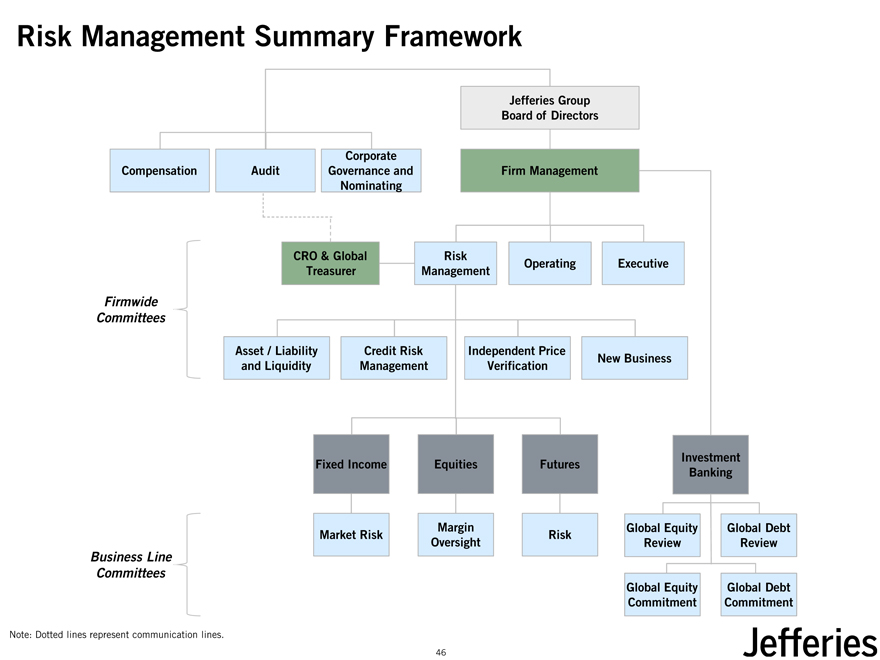

Risk Management Summary Framework

Jefferies Group Board of Directors

Corporate

Compensation Audit Governance and Firm Management Nominating

Firmwide

Committees

CRO & Global Risk

Operating Executive Treasurer Management

Asset / Liability Credit Risk Independent Price

New Business and Liquidity Management Verification

Investment Fixed Income Equities Futures Banking

Margin Global Equity Global Debt Market Risk Risk Oversight Review Review

Business Line Committees

Global Equity Global Debt Commitment Commitment

Note: Dotted lines represent communication lines.

46

|

Capital and Liquidity Management

47

|

Liquidity and Funding Principles

Jefferies’ long-standing liquidity and funding principles have maintained the strength and soundness of our platform across market cycles

Owning inventory that is composed of liquid assets that turn over regularly, with a minimal amount of Level 3 AssetsMaintaining a sound, long-term capital base and reasonable leverage relative to our business activityNo material reliance on short-term unsecured funding or customer balancesShort term secured funding that is readily and consistently available through clearing houses, or fixed for periods of time that exceed the expected tenure of the inventory they are fundingAssessing capital reserves and maintaining liquidity (including intraday liquidity) to withstand adverse changes in the trading or financing marketsWhere appropriate, entering into partnerships and joint ventures with complementary long-term partners to pursue business opportunities that otherwise will exceed our capital capacity or risk tolerance

48

|

Strong Capital Structure and Ample Liquidity

Jefferies maintains a highly liquid balance sheet, with low gross leverage and exposure to illiquid assets, and significant structural liquidityJefferies continues to manage the size of its balance sheet in response to market conditions and volatility

Total assets: $38.8 billion

Leverage: 7.4x (1)

Leverage (excluding merger impacts): 9.4x (2)

Tangible gross leverage: 11.6x (3)

Long-term capital of $11.0 billion, including $5.8 billion of long-term debt with a weighted average maturity of 9.1 years

Note: All figures as of 08/31/13.

(1) |

| Leverage ratio equals total assets divided by total equity. |

(2) Leverage ratio (excluding merger impacts) (a non-GAAP financial measure) equals total assets less the increase in goodwill and asset fair values in acquisition accounting of $1,953 million less amortization to date of $18 million on assets recognized at fair value in acquisition accounting divided by the sum of total equity less $1,314 million, being the increase in equity arising from merger consideration of $1,422 million excluding the $125 million attributable to the assumption of Jefferies’ preferred stock by Leucadia, and less the impact on equity due to amortization to date of $17 million on assets and liabilities recognized at fair value in acquisition accounting.

(3) Tangible gross leverage ratio (a non-GAAP financial measure) equals total assets less goodwill and identifiable intangible assets divided by tangible member’s equity. Tangible member’s equity (a non-GAAP financial measure) represents total member’s equity less goodwill and identifiable intangible assets.

49

|

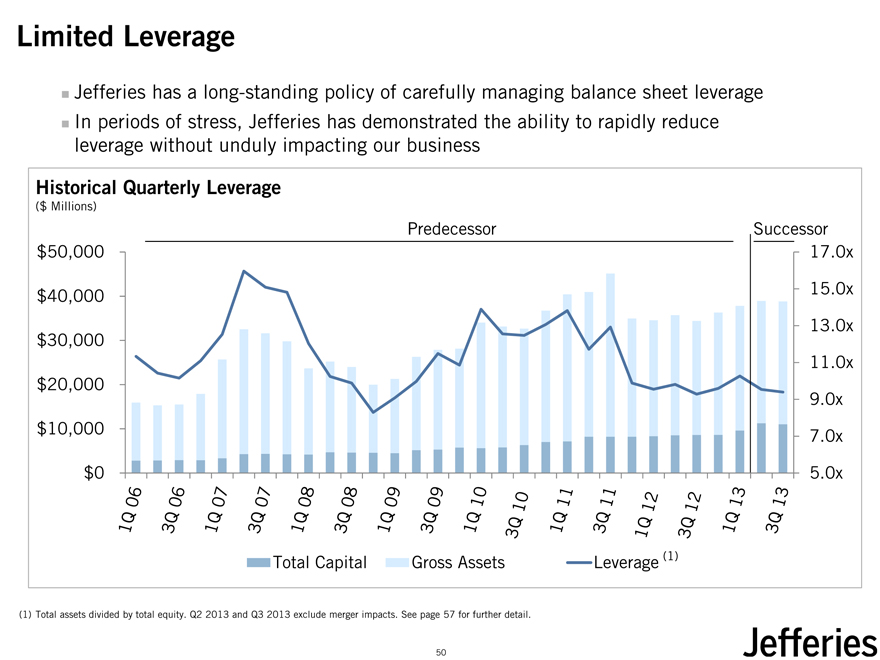

Limited Leverage

Jefferies has a long-standing policy of carefully managing balance sheet leverageIn periods of stress, Jefferies has demonstrated the ability to rapidly reduce leverage without unduly impacting our business

Historical Quarterly Leverage

($ Millions)

Predecessor Successor $50,000 17.0x $40,000 15.0x

13.0x $30,000

11.0x $20,000

9.0x $10,000 7.0x

$0 5.0x

Total Capital Gross Assets Leverage (1)

(1) |

| Total assets divided by total equity. Q2 2013 and Q3 2013 exclude merger impacts. See page 57 for further detail. |

50

|

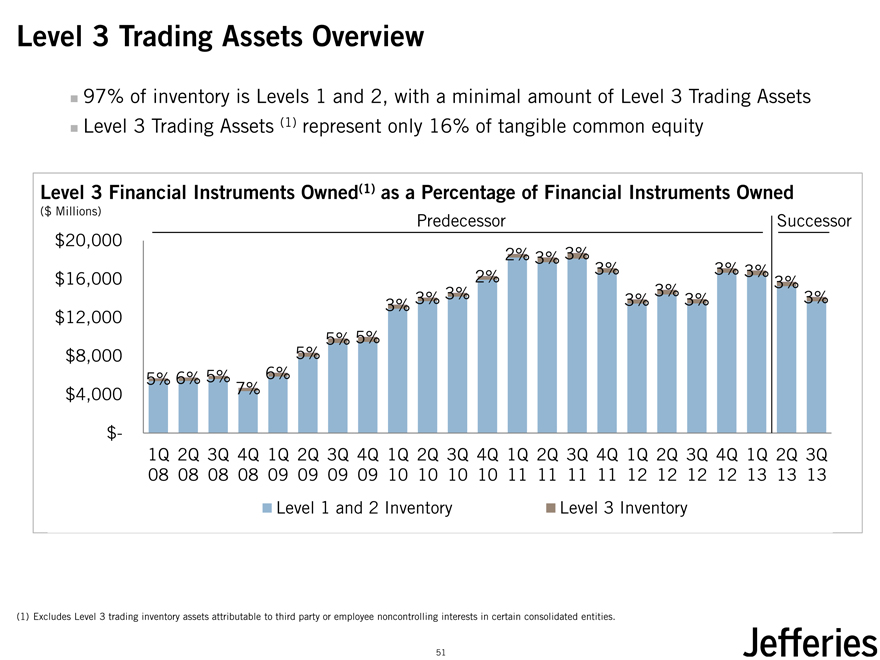

Level 3 Trading Assets Overview

97% of inventory is Levels 1 and 2, with a minimal amount of Level 3 Trading Assets Level 3 Trading Assets (1)represent only 16% of tangible common equity

Level 3 Financial Instruments Owned(1) as a Percentage of Financial Instruments Owned

($ Millions)

Predecessor Successor $20,000

2% 3% 3%

2% 3% 3% 3% $16,000 3%

3% 3% 3% 3%

3% 3% 3% $12,000

5% 5% 5% $8,000

5% 6% 5% 6% $4,000 7% $-

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

08 08 08 08 09 09 09 09 10 10 10 10 11 11 11 11 12 12 12 12 13 13 13

Level 1 and 2 Inventory

Level 3 Inventory

(1) Excludes Level 3 trading inventory assets attributable to third party or employee noncontrolling interests in certain consolidated entities.

51

|

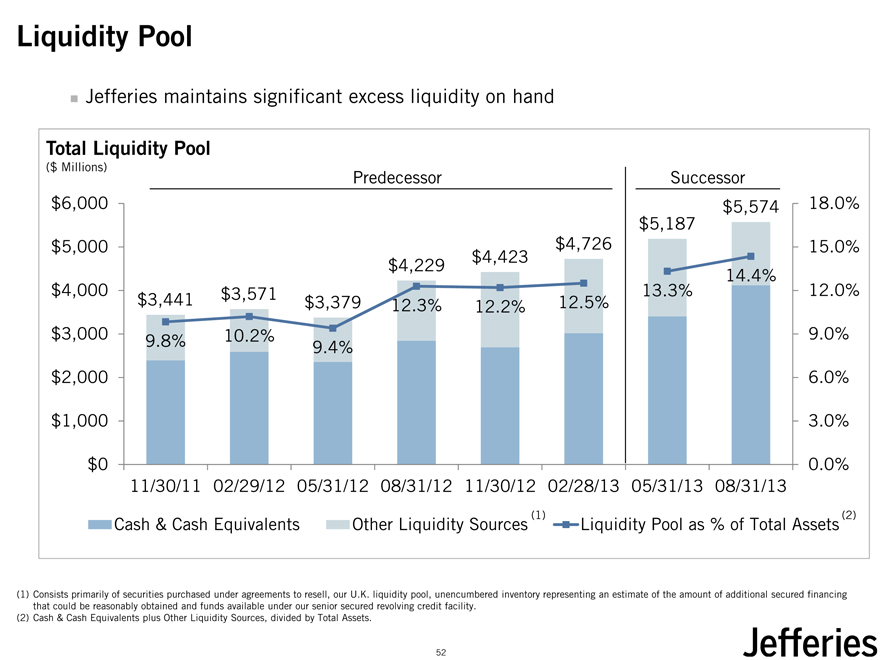

Liquidity Pool

Jefferies maintains significant excess liquidity on hand

Total Liquidity Pool

($ Millions)

Predecessor Successor $6,000 $5,574 18.0% $5,187 $5,000 $4,726 15.0% $4,423 $4,229

14.4% $4,000 $3,571 13.3% 12.0% $3,441 $3,379 12.3% 12.2% 12.5% $3,000 9.8% 10.2% 9.0%

9.4% $2,000 6.0%

$1,000 3.0%

$0 0.0% 11/30/11 02/29/12 05/31/12 08/31/12 11/30/12 02/28/13 05/31/13 08/31/13

(1) |

| (2) |

Cash & Cash Equivalents Other Liquidity Sources Liquidity Pool as % of Total Assets

(1) Consists primarily of securities purchased under agreements to resell, our U.K. liquidity pool, unencumbered inventory representing an estimate of the amount of additional secured financing that could be reasonably obtained and funds available under our senior secured revolving credit facility.

(2) |

| Cash & Cash Equivalents plus Other Liquidity Sources, divided by Total Assets. |

52

|

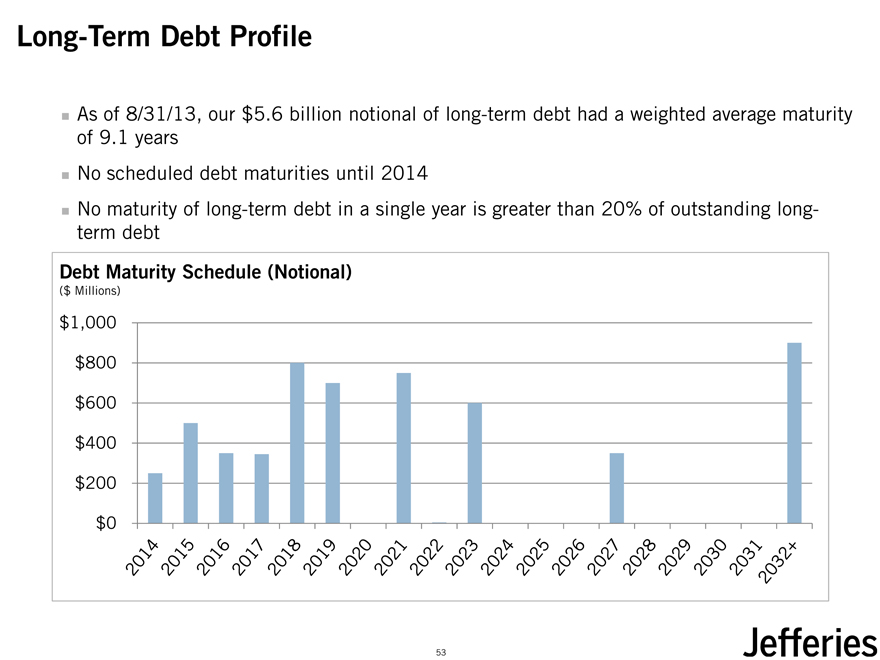

Long-Term Debt Profile

As of 8/31/13, our $5.6 billion notional of long-term debt had a weighted average maturity of 9.1 yearsNo scheduled debt maturities until 2014No maturity of long-term debt in a single year is greater than 20% of outstanding long-term debt

Debt Maturity Schedule (Notional)

($ Millions)

$1,000 $800 $600 $400 $200 $0

53

|

Appendix

54

|

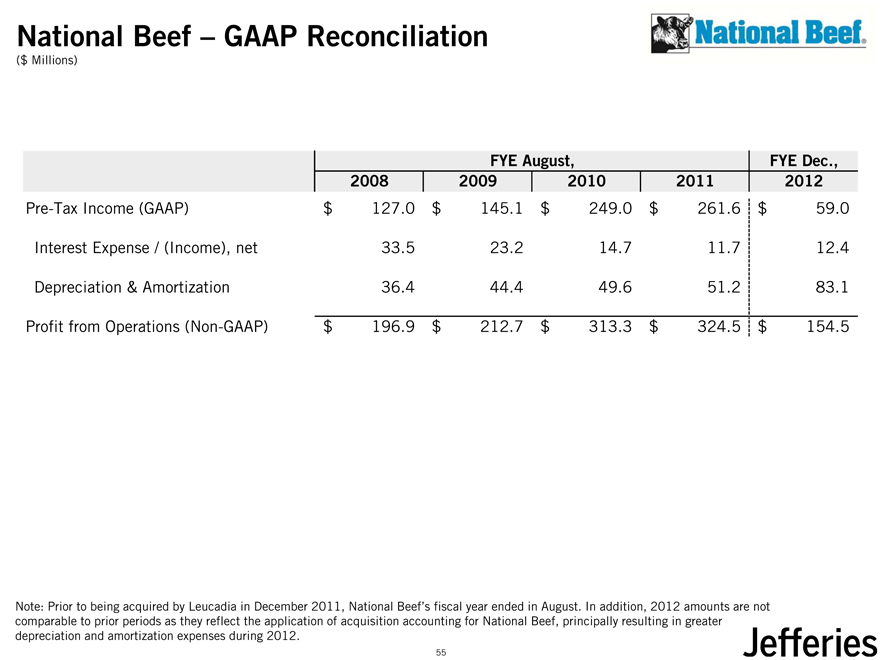

National Beef – GAAP Reconciliation

($ Millions)

FYE August, FYE Dec., 2008 2009 2010 2011 2012

Pre-Tax Income (GAAP) $ 127 .0 $ 145.1 $ 249.0 $ 261.6 $ 59.0 Interest Expense / (Income), net 33.5 23.2 14.7 11.7 12.4 Depreciation & Amortization 36.4 44.4 49.6 51.2 83.1 Profit from Operations (Non-GAAP) $ 196.9 $ 212.7 $ 313.3 $ 324.5 $ 154.5

Note: Prior to being acquired by Leucadia in December 2011, National Beef’s fiscal year ended in August. In addition, 2012 amounts are not comparable to prior periods as they reflect the application of acquisition accounting for National Beef, principally resulting in greater depreciation and amortization expenses during 2012.

55

|

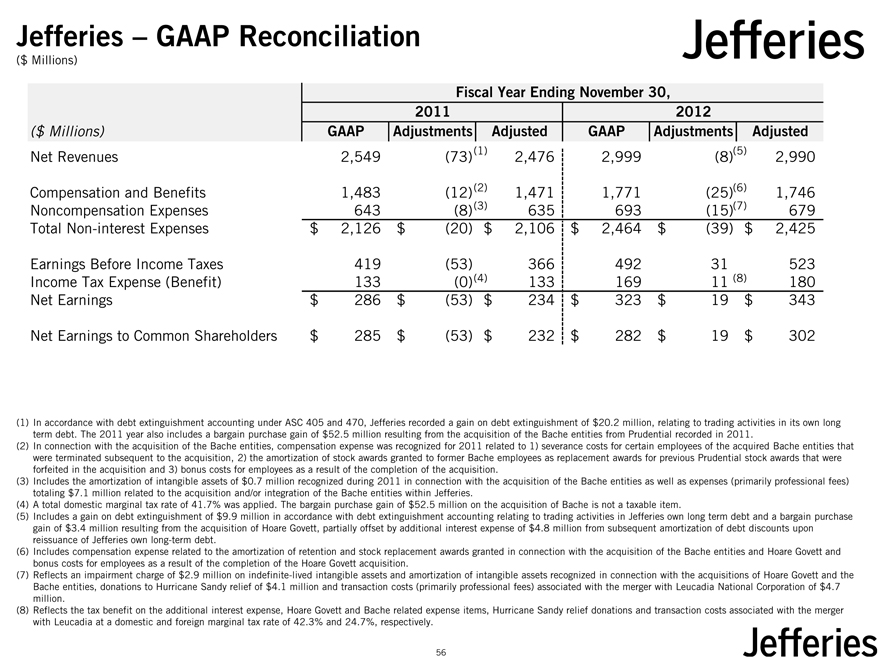

Jefferies – GAAP Reconciliation

($ Millions)

Fiscal Year Ending November 30, 2011 2012

($ Millions) GAAP Adjustments Adjusted GAAP Adjustments Adjusted

Net Revenues 2,549 (73)(1) 2,476 2,999 (8)(5) 2,990 Compensation and Benefits 1,483 (12)(2) 1,471 1,771 (25)(6) 1,746 Noncompensation Expenses 643 (8)(3) 635 693 (15)(7) 679 Total Non-interest Expenses $ 2,126 $ (20) $ 2,106 $ 2,464 $ (39) $ 2,425

Earnings Before Income Taxes 419 (53) 366 492 31 523 Income Tax Expense (Benefit) 133 (0)(4) 133 169 11 (8) 180 Net Earnings $ 286 $ (53) $ 234 $ 323 $ 19 $ 343

Net Earnings to Common Shareholders $ 285 $ (53) $ 232 $ 282 $ 19 $ 302

(1) In accordance with debt extinguishment accounting under ASC 405 and 470, Jefferies recorded a gain on debt extinguishment of $20.2 million, relating to trading activities in its own long term debt. The 2011 year also includes a bargain purchase gain of $52.5 million resulting from the acquisition of the Bache entities from Prudential recorded in 2011.

(2) In connection with the acquisition of the Bache entities, compensation expense was recognized for 2011 related to 1) severance costs for certain employees of the acquired Bache entities that were terminated subsequent to the acquisition, 2) the amortization of stock awards granted to former Bache employees as replacement awards for previous Prudential stock awards that were forfeited in the acquisition and 3) bonus costs for employees as a result of the completion of the acquisition.

(3) Includes the amortization of intangible assets of $0.7 million recognized during 2011 in connection with the acquisition of the Bache entities as well as expenses (primarily professional fees) totaling $7.1 million related to the acquisition and/or integration of the Bache entities within Jefferies.

(4) A total domestic marginal tax rate of 41.7% was applied. The bargain purchase gain of $52.5 million on the acquisition of Bache is not a taxable item.

(5) Includes a gain on debt extinguishment of $9.9 million in accordance with debt extinguishment accounting relating to trading activities in Jefferies own long term debt and a bargain purchase gain of $3.4 million resulting from the acquisition of Hoare Govett, partially offset by additional interest expense of $4.8 million from subsequent amortization of debt discounts upon reissuance of Jefferies own long-term debt.

(6) Includes compensation expense related to the amortization of retention and stock replacement awards granted in connection with the acquisition of the Bache entities and Hoare Govett and bonus costs for employees as a result of the completion of the Hoare Govett acquisition.

(7) Reflects an impairment charge of $2.9 million on indefinite-lived intangible assets and amortization of intangible assets recognized in connection with the acquisitions of Hoare Govett and the Bache entities, donations to Hurricane Sandy relief of $4.1 million and transaction costs (primarily professional fees) associated with the merger with Leucadia National Corporation of $4.7 million.

(8) Reflects the tax benefit on the additional interest expense, Hoare Govett and Bache related expense items, Hurricane Sandy relief donations and transaction costs associated with the merger with Leucadia at a domestic and foreign marginal tax rate of 42.3% and 24.7%, respectively.

56

|

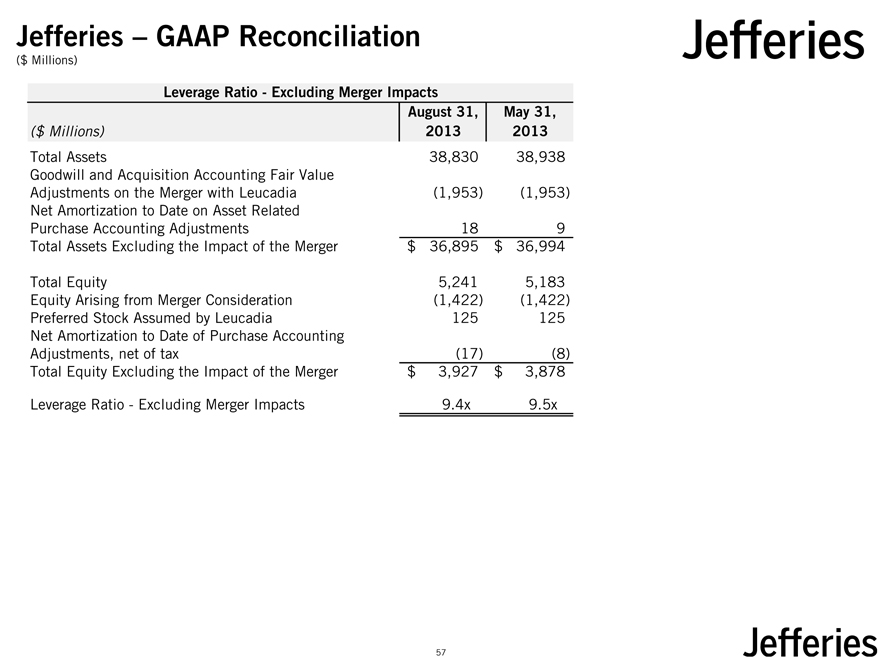

Jefferies – GAAP Reconciliation

($ Millions)

Leverage Ratio—Excluding Merger Impacts

August 31, May 31,

($ Millions) 2013 2013

Total Assets 38,830 38,938 Goodwill and Acquisition Accounting Fair Value Adjustments on the Merger with Leucadia (1,953) (1,953) Net Amortization to Date on Asset Related Purchase Accounting Adjustments 18 9 Total Assets Excluding the Impact of the Merger $ 36,895 $ 36,994

Total Equity 5,241 5,183 Equity Arising from Merger Consideration (1,422) (1,422) Preferred Stock Assumed by Leucadia 125 125 Net Amortization to Date of Purchase Accounting Adjustments, net of tax (17) (8) Total Equity Excluding the Impact of the Merger $ 3,927 $ 3,878

Leverage Ratio—Excluding Merger Impacts 9.4x 9.5x

57

|

Jefferies Group

2013 Fixed Income Investor Day

October 10, 2013