Exhibit 99.1

ENCORE

CAPITAL GROUP

Encore Capital Group Investor Presentation

May 11, 2011

CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS

FORWARD-LOOKING STATEMENTS

The statements in this presentation that are not historical facts, including, most importantly, those statements preceded by, or that include, the words “may,” “believe,” “projects,” “expects,” “anticipates” or the negation thereof, or similar expressions, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 (the “Reform Act”). These statements may include, but are not limited to, statements regarding our future operating results and growth. For all “forward-looking statements,” the Company claims the protection of the safe harbor for forward-looking statements contained in the Reform Act. Such forward-looking statements involve risks, uncertainties and other factors which may cause actual results, performance or achievements of the Company and its subsidiaries to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These risks, uncertainties and other factors are discussed in the reports filed by the Company with the Securities and Exchange Commission, including the most recent reports on Forms 10-K, 10-Q and 8-K, each as it may be amended from time to time. The Company disclaims any intent or obligation to update these forward-looking statements.

ENCORE

CAPITAL GROUP

2

INVESTMENT HIGHLIGHTS

• Favorable supply and demand dynamics have existed since 2008, with a few credible, large buyers

• Analytic insights inform our valuation and operating strategies and allow for a closer partnership with consumers

• Operational and financial leverage is increasing, largely due to the success of our operating center in India

• Strong performance is expected to continue

ENCORE

CAPITAL GROUP

3

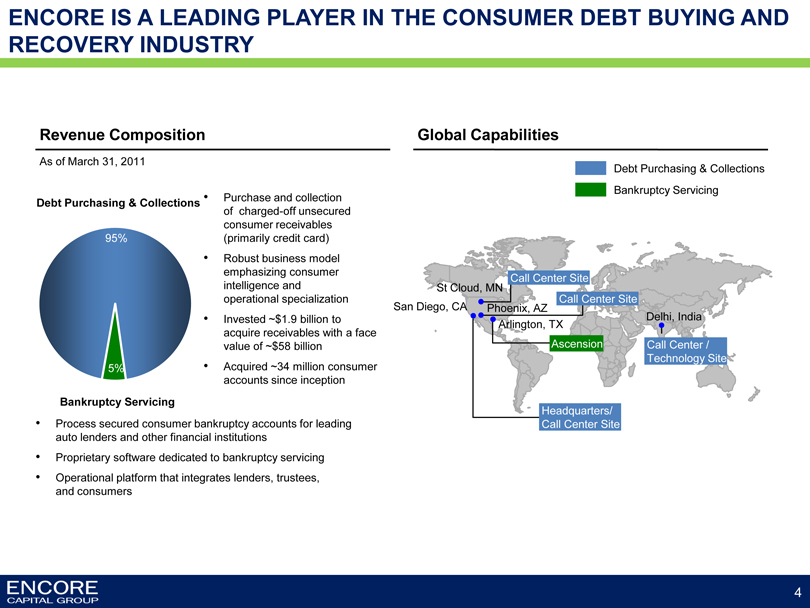

ENCORE IS A LEADING PLAYER IN THE CONSUMER DEBT BUYING AND RECOVERY INDUSTRY

Revenue Composition

As of March 31, 2011

Debt Purchasing & Collections

95%

5%

• Purchase and collection of charged-off unsecured consumer receivables (primarily credit card)

• Robust business model emphasizing consumer intelligence and operational specialization

• Invested ~$1.9 billion to acquire receivables with a face value of ~$58 billion

• Acquired ~34 million consumer accounts since inception

Bankruptcy Servicing

• Process secured consumer bankruptcy accounts for leading auto lenders and other financial institutions

• Proprietary software dedicated to bankruptcy servicing

• Operational platform that integrates lenders, trustees, and consumers

Global Capabilities

Debt Purchasing & Collections

Bankruptcy Servicing

St Cloud, MN

Call Center Site

Call Center Site

San Diego, CA

Phoenix, AZ

Delhi, India

Arlington, TX

Ascension

Call Center / Technology Site

Headquarters/ Call Center Site

ENCORE

CAPITAL GROUP

4

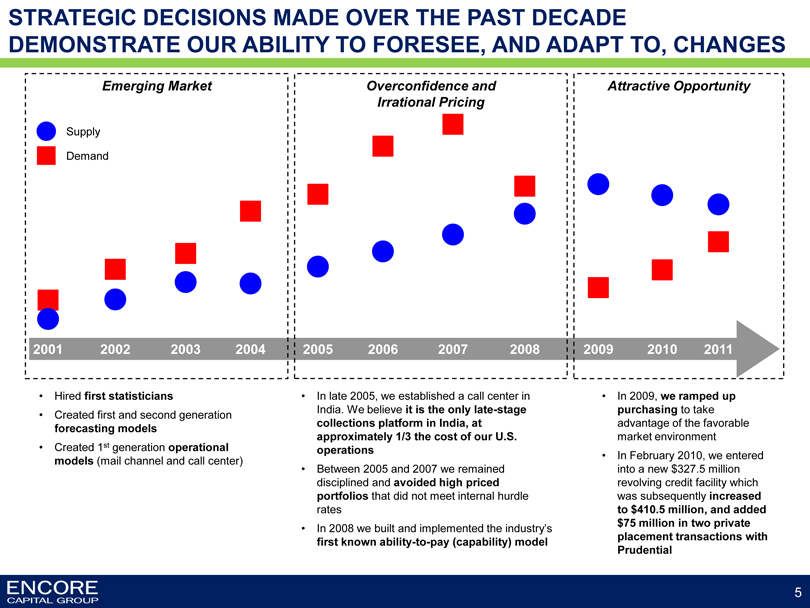

STRATEGIC DECISIONS MADE OVER THE PAST DECADE DEMONSTRATE OUR ABILITY TO FORESEE, AND ADAPT TO, CHANGES

Emerging Market

Overconfidence and Irrational Pricing

Attractive Opportunity

Supply

Demand

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

• Hired first statisticians

• Created first and second generation forecasting models

• Created 1st generation operational models (mail channel and call center)

• In late 2005, we established a call center in India. We believe it is the only late-stage collections platform in India, at approximately 1/3 the cost of our U.S. operations

• Between 2005 and 2007 we remained disciplined and avoided high priced portfolios that did not meet internal hurdle rates

• In 2008 we built and implemented the industry’s first known ability-to-pay (capability) model

• In 2009, we ramped up purchasing to take advantage of the favorable market environment

• In February 2010, we entered into a new $327.5 million revolving credit facility which was subsequently increased to $410.5 million, and added $75 million in two private placement transactions with Prudential

ENCORE

CAPITAL GROUP

5

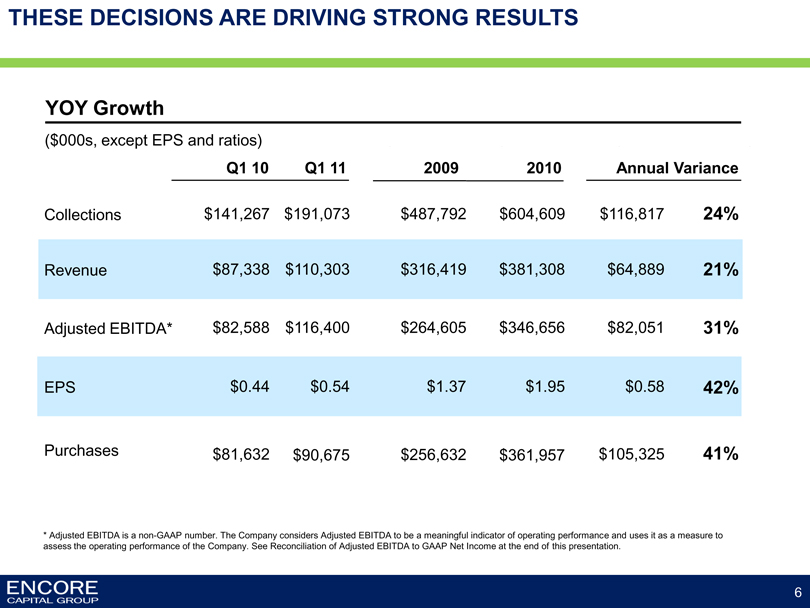

THESE DECISIONS ARE DRIVING STRONG RESULTS

YOY Growth

($000s, except EPS and ratios)

Q1 10 Q1 11 2009 2010 Annual Variance

Collections $141,267 $191,073 $487,792 $604,609 $116,817 24%

Revenue $87,338 $110,303 $316,419 $381,308 $64,889 21%

Adjusted EBITDA* $82,588 $116,400 $264,605 $346,656 $82,051 31%

EPS $0.44 $0.54 $1.37 $1.95 $0.58 42%

Purchases $81,632 $90,675 $256,632 $361,957 $105,325 41%

* Adjusted EBITDA is a non-GAAP number. The Company considers Adjusted EBITDA to be a meaningful indicator of operating performance and uses it as a measure to assess the operating performance of the Company. See Reconciliation of Adjusted EBITDA to GAAP Net Income at the end of this presentation.

ENCORE

CAPITAL GROUP

6

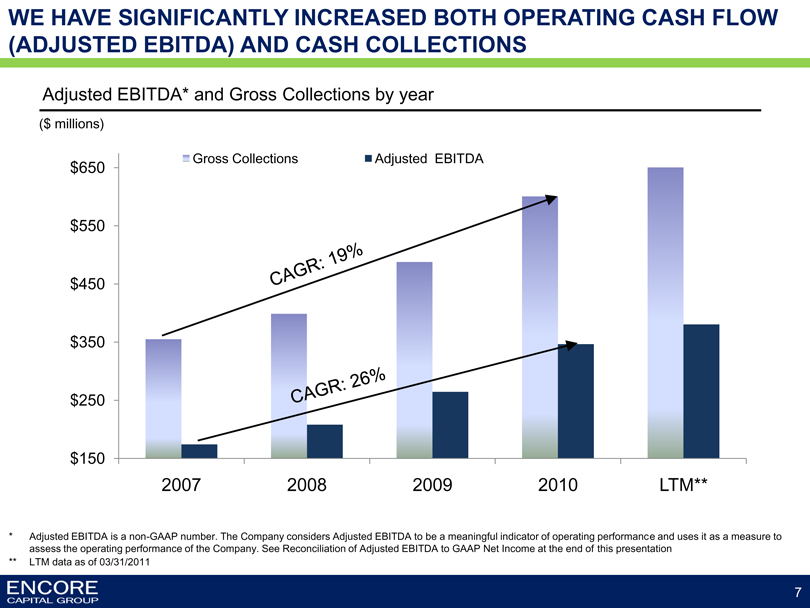

WE HAVE SIGNIFICANTLY INCREASED BOTH OPERATING CASH FLOW (ADJUSTED EBITDA) AND CASH COLLECTIONS

Adjusted EBITDA* and Gross Collections by year

($ millions)

$650 $550 $450 $350 $250 $150

Gross Collections Adjusted EBITDA

CAGR: 19%

CAGR: 26%

2007 2008 2009 2010 LTM**

* Adjusted EBITDA is a non-GAAP number. The Company considers Adjusted EBITDA to be a meaningful indicator of operating performance and uses it as a measure to assess the operating performance of the Company. See Reconciliation of Adjusted EBITDA to GAAP Net Income at the end of this presentation

** LTM data as of 03/31/2011

ENCORE

CAPITAL GROUP

7

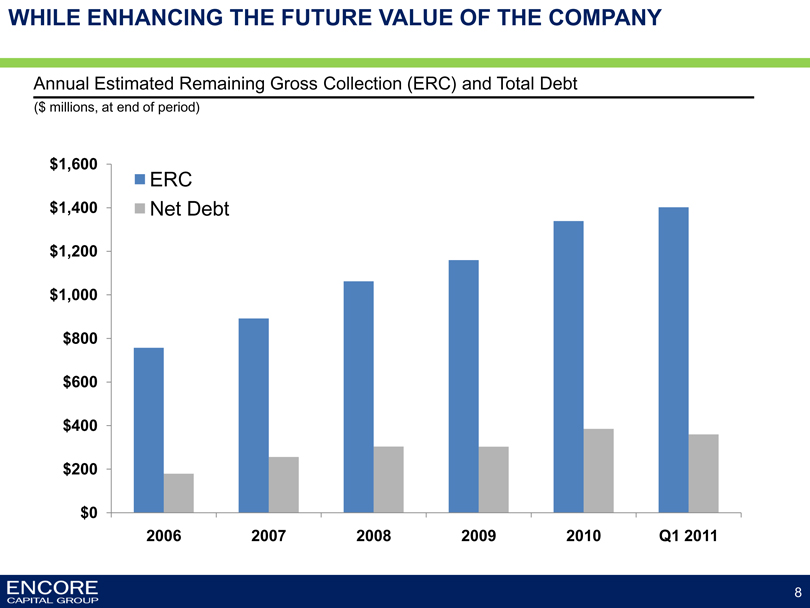

WHILE ENHANCING THE FUTURE VALUE OF THE COMPANY

Annual Estimated Remaining Gross Collection (ERC) and Total Debt

($ millions, at end of period)

$1,600 $1,400 $1,200 $1,000 $800 $600 $400 $200 $0

ERC Net Debt

2006 2007 2008 2009 2010 Q1 2011

ENCORE

CAPITAL GROUP

8

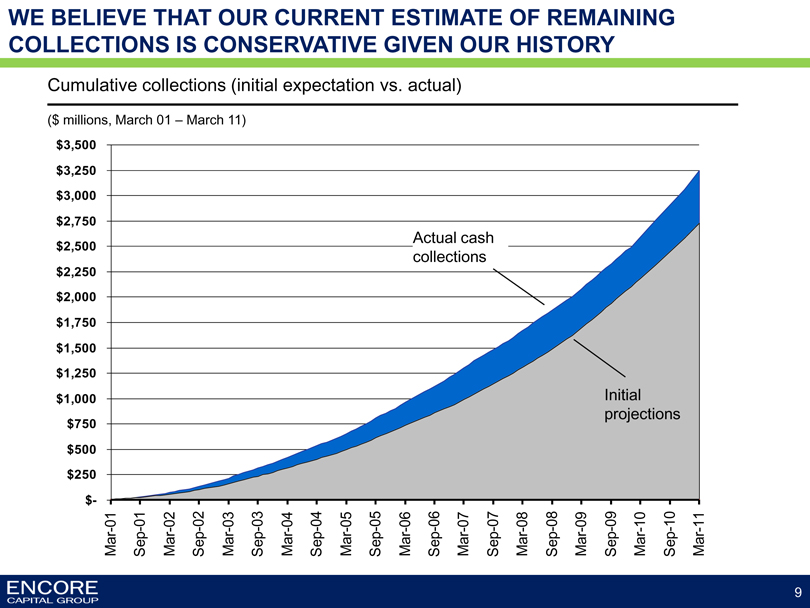

WE BELIEVE THAT OUR CURRENT ESTIMATE OF REMAINING COLLECTIONS IS CONSERVATIVE GIVEN OUR HISTORY

Cumulative collections (initial expectation vs. actual)

($ millions, March 01 – March 11)

$3,500

$3,250

$3,000

$2,750

$2,500

$2,250

$2,000

$1,750

$1,500

$1,250

$1,000

$750

$500

$250

$-

Actual cash collections

Initial projections

Mar-01 Sep-01

Mar-02 Sep-02

Mar-03 Sep-03

Mar-04 Sep-04

Mar-05 Sep-05

Mar-06 Sep-06

Mar-07 Sep-07

Mar-08 Sep-08

Mar-09 Sep-09

Mar-10 Sep-10

Mar-11

ENCORE

CAPITAL GROUP

9

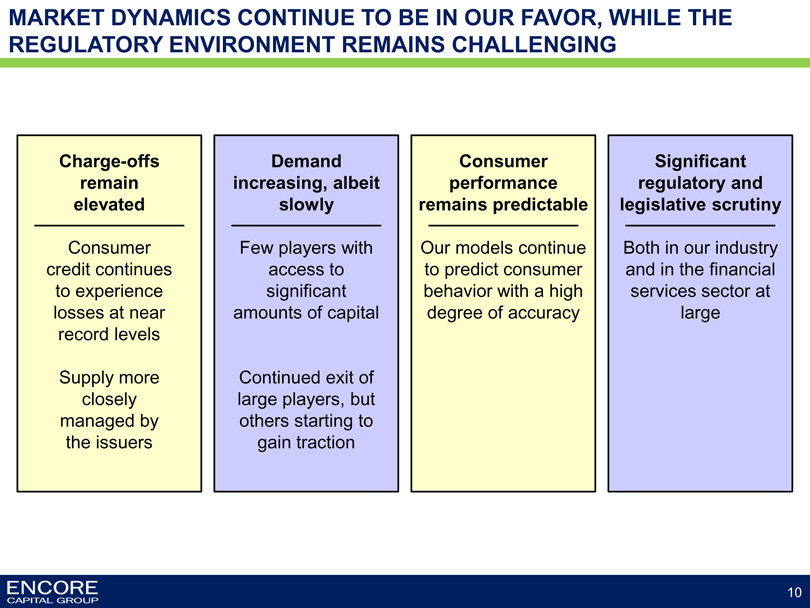

MARKET DYNAMICS CONTINUE TO BE IN OUR FAVOR, WHILE THE REGULATORY ENVIRONMENT REMAINS CHALLENGING

Charge-offs remain elevated

Consumer credit continues to experience losses at near record levels

Supply more closely managed by the issuers

Demand increasing, albeit slowly

Few players with access to significant amounts of capital

Continued exit of large players, but others starting to gain traction

Consumer performance remains predictable

Our models continue to predict consumer behavior with a high degree of accuracy

Significant regulatory and legislative scrutiny

Both in our industry and in the financial services sector at large

ENCORE

CAPITAL GROUP

10

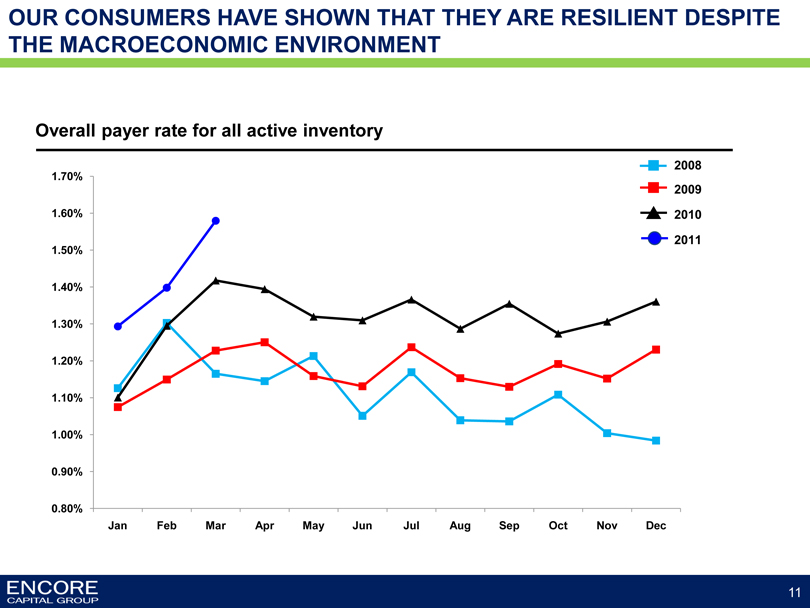

OUR CONSUMERS HAVE SHOWN THAT THEY ARE RESILIENT DESPITE THE MACROECONOMIC ENVIRONMENT

Overall payer rate for all active inventory

1.70%

1.60%

1.50%

1.40%

1.30%

1.20%

1.10%

1.00%

0.90%

0.80%

2008

2009

2010

2011

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

11

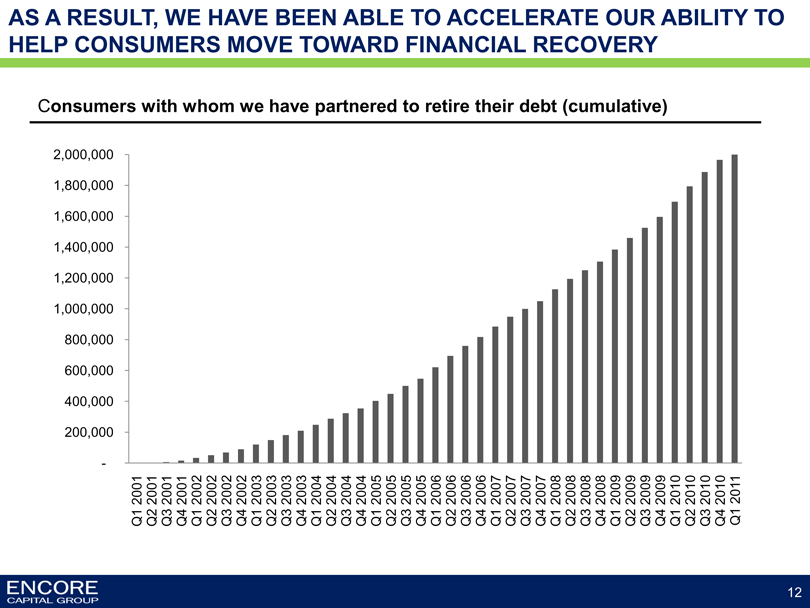

AS A RESULT, WE HAVE BEEN ABLE TO ACCELERATE OUR ABILITY TO HELP CONSUMERS MOVE TOWARD FINANCIAL RECOVERY

Consumers with whom we have partnered to retire their debt (cumulative)

2,000,000

1,800,000

1,600,000

1,400,000

1,200,000

1,000,000

800,000

600,000

400,000

200,000

-

Q1 2001 Q2 2001 Q3 2001 Q4 2001 Q1 2002 Q2 2002 Q3 2002 Q4 2002 Q1 2003 Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004 Q4 2004 Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011

ENCORE

CAPITAL GROUP

12

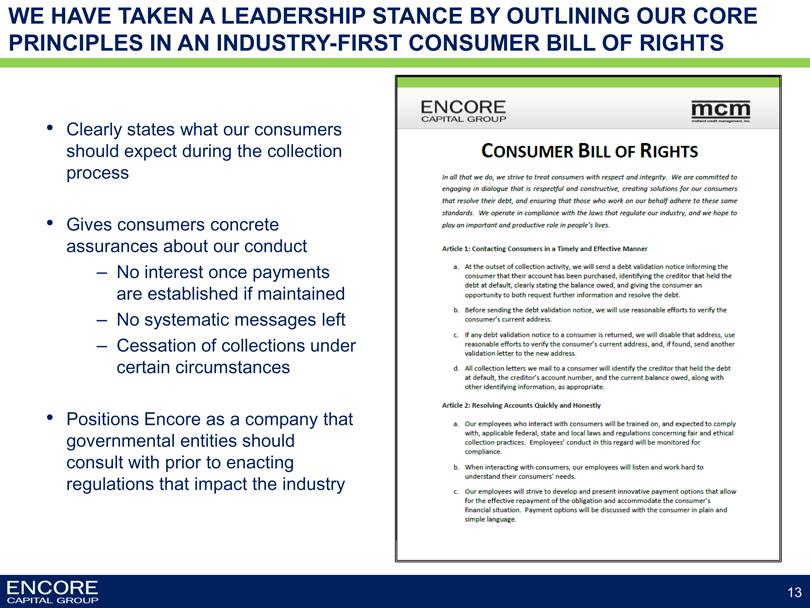

WE HAVE TAKEN A LEADERSHIP STANCE BY OUTLINING OUR CORE PRINCIPLES IN AN INDUSTRY-FIRST CONSUMER BILL OF RIGHTS

• Clearly states what our consumers should expect during the collection process

• Gives consumers concrete assurances about our conduct

– No interest once payments are established if maintained

– No systematic messages left

– Cessation of collections under certain circumstances

• Positions Encore as a company that governmental entities should consult with prior to enacting regulations that impact the industry

ENCORE

CAPITAL GROUP

mcm

midland credit management, inc.

CONSUMER BILL OF RIGHTS

In all that we do, we strive to treat consumers with respect and integrity. We are committed to engaging in dialogue that is respectful and constructive, creating solutions for our consumers that resolve their debt, and ensuring that those who work on our behalf adhere to these same standards. We operate in compliance with the laws that regulate our industry, and we hope to play an important and productive role in people’s lives.

Article 1: Contacting Consumers in a Timely and Effective Manner

a. At the outset of collection activity, we will send a debt validation notice informing the consumer that their account has been purchased, identifying the creditor that held the debt at default, clearly stating the balance owed, and giving the consumer an opportunity to both request further information and resolve the debt.

b. Before sending the debt validation notice, we will use reasonable efforts to verity the consumer’s current address.

c. if any debt validation notice to a consumer is returned, we will disable that address, use reasonable efforts to verity the consumer’s current address, and, if found, send another validation letter to the new address.

d. All collection letters we mail to a consumer will identify the creditor that held the debt at default, the creditor’s account number, and the current balance owed, along with other identifying information, as appropriate.

Article 2: Resolving Accounts Quickly and Honestly

a. Our employees who interact with consumers will be trained on, and expected to comply with, applicable federal, state and local laws and regulations concerning fair and ethical collection practices. Employees’ conduct in this regard will be monitored for compliance.

b. When interacting with consumers, our employees will listen and work hard to understand their consumers’ needs.

c. Our employees will strive to develop and present innovative payment options that allow for the effective repayment of the obligation and accommodate the consumer’s financial situation. Payment options will be discussed with the consumer in plain and simple language.

ENCORE

CAPITAL GROUP

13

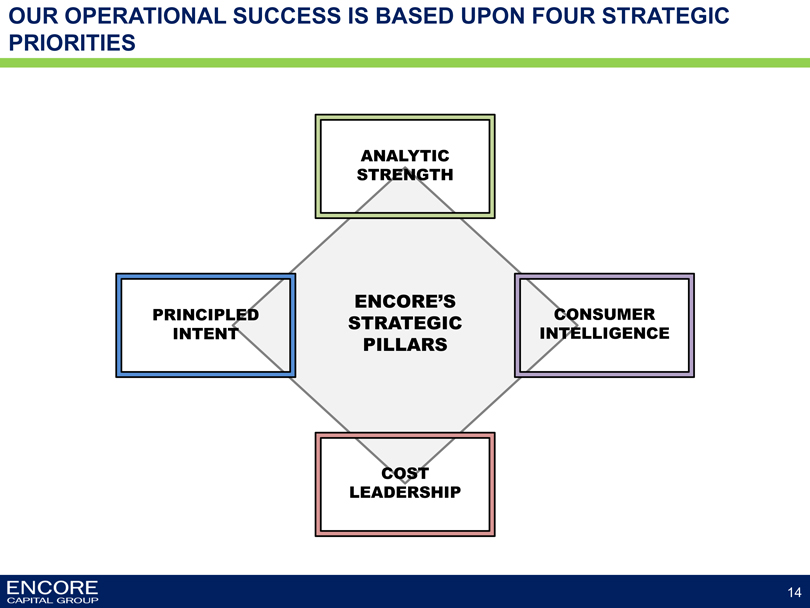

OUR OPERATIONAL SUCCESS IS BASED UPON FOUR STRATEGIC PRIORITIES

ENCORE’S STRATEGIC PILLARS

ANALYTIC STRENGTH

CONSUMER INTELLIGENCE

COST LEADERSHIP

PRINCIPLED INTENT

ENCORE

CAPITAL GROUP

14

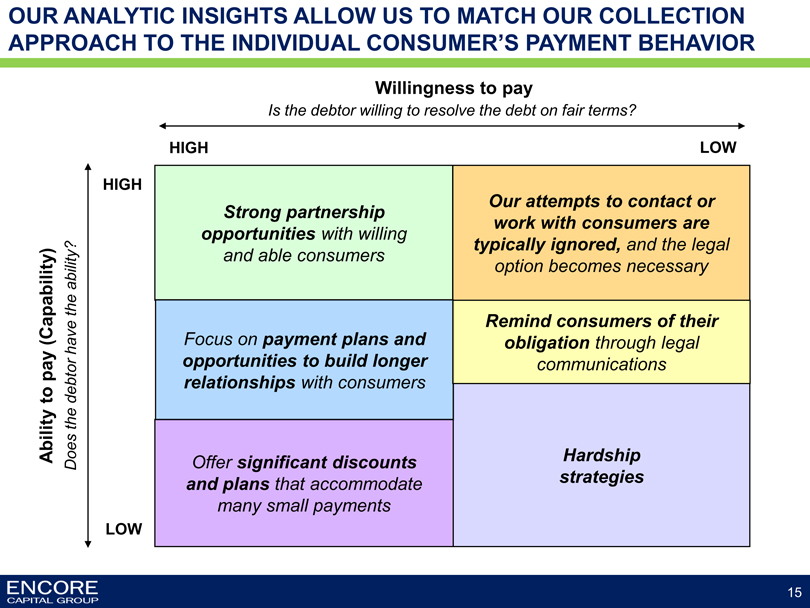

OUR ANALYTIC INSIGHTS ALLOW US TO MATCH OUR COLLECTION APPROACH TO THE INDIVIDUAL CONSUMER’S PAYMENT BEHAVIOR

Willingness to pay

Is the debtor willing to resolve the debt on fair terms?

HIGH

LOW

Ability to pay (Capability)

Does the debtor have the ability?

HIGH

LOW

Strong partnership opportunities with willing and able consumers

Focus on payment plans and opportunities to build longer relationships with consumers

Offer significant discounts and plans that accommodate many small payments

Our attempts to contact or work with consumers are typically ignored, and the legal option becomes necessary

Remind consumers of their obligation through legal communications

Hardship strategies

ENCORE

CAPITAL GROUP

15

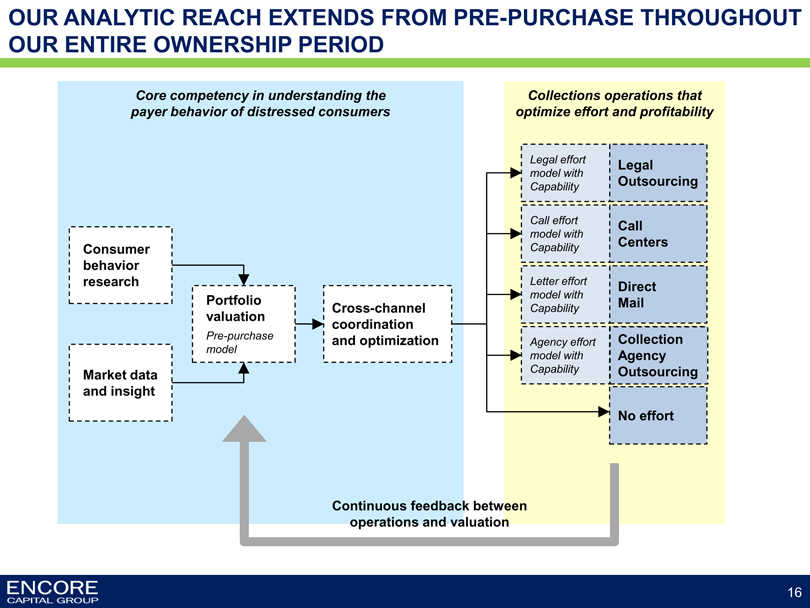

OUR ANALYTIC REACH EXTENDS FROM PRE-PURCHASE THROUGHOUT OUR ENTIRE OWNERSHIP PERIOD

Core competency in understanding the payer behavior of distressed consumers

Collections operations that optimize effort and profitability

Consumer behavior research

Market data and insight

Portfolio valuation

Pre-purchase model

Cross-channel coordination and optimization

Legal effort model with Capability

Call effort model with Capability

Letter effort model with Capability

Agency effort model with Capability

Legal Outsourcing

Call Centers

Direct Mail

Collection Agency Outsourcing

No effort

Continuous feedback between operations and valuation

ENCORE

CAPITAL GROUP

16

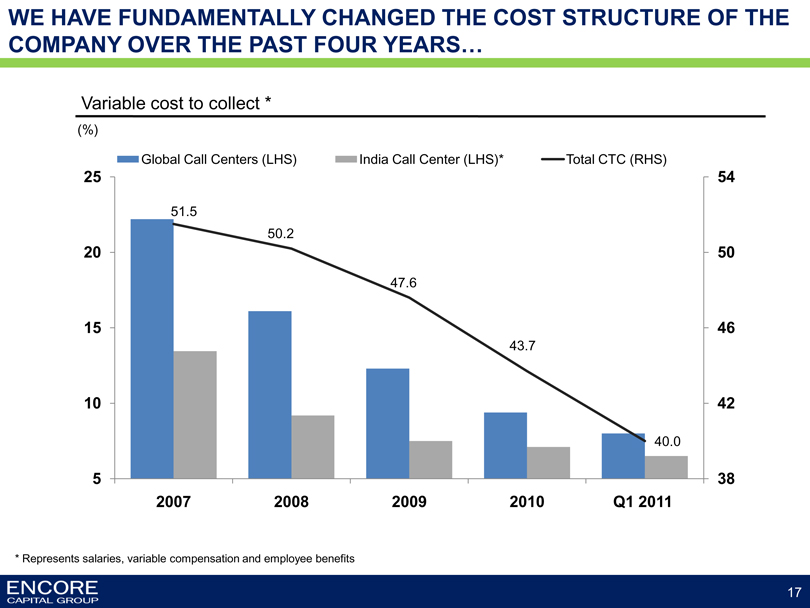

WE HAVE FUNDAMENTALLY CHANGED THE COST STRUCTURE OF THE COMPANY OVER THE PAST FOUR YEARS…

Variable cost to collect *

(%)

Global Call Centers (LHS)

India Call Center (LHS)*

Total CTC (RHS)

25 54

51.5

50.2

20 50

47.6

15 46

43.7

10 42

40.0

5 38

2007 2008 2009 2010 Q1 2011

* Represents salaries, variable compensation and employee benefits

ENCORE

CAPITAL GROUP

17

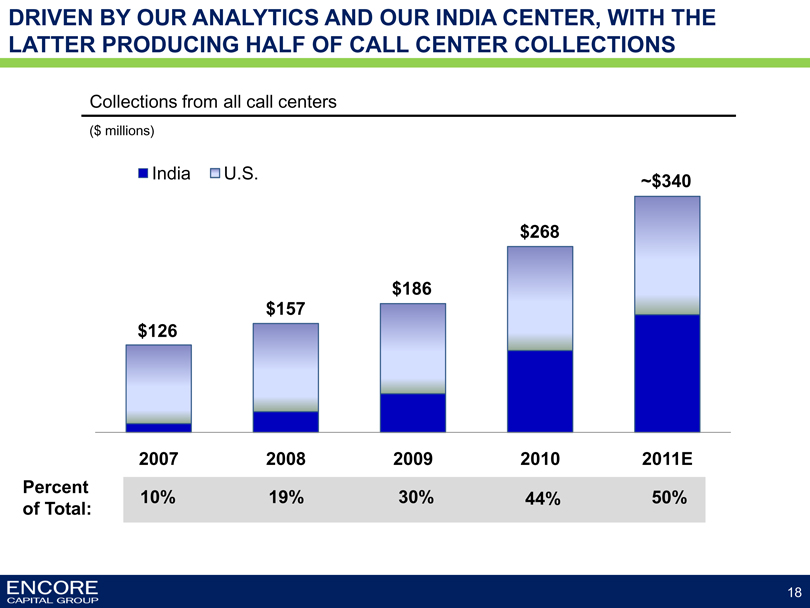

DRIVEN BY OUR ANALYTICS AND OUR INDIA CENTER, WITH THE LATTER PRODUCING HALF OF CALL CENTER COLLECTIONS

Collections from all call centers

($ millions)

India

U.S.

~$340

$268

$186

$157

$126

2007 2008 2009 2010 2011E

Percent of Total: 10% 19% 30% 44% 50%

ENCORE

CAPITAL GROUP

18

SUMMARY

• Favorable supply and demand dynamics have existed since 2008, with a few credible, large buyers

• Analytic insights inform our valuation and operating strategies and allow for a closer partnership with consumers

• Operational and financial leverage is increasing, largely due to the success of our operating center in India

• Strong performance is expected to continue

ENCORE

CAPITAL GROUP

19

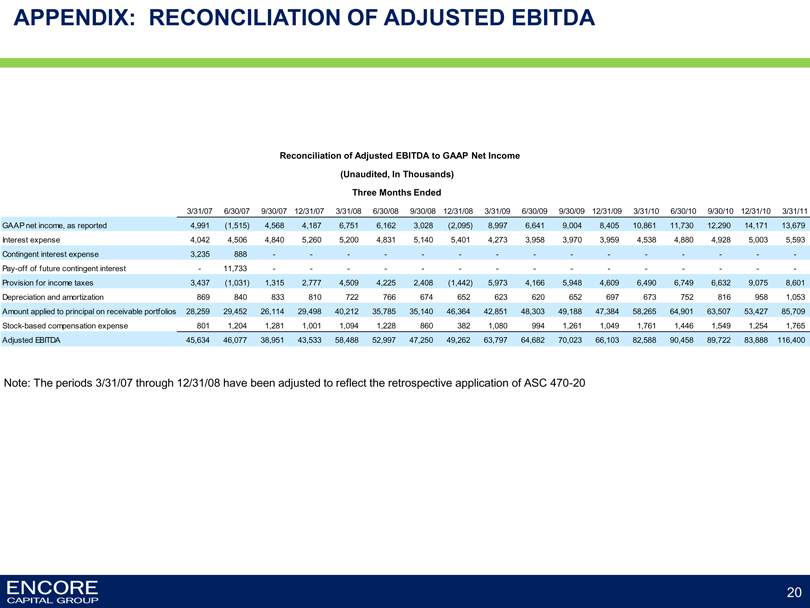

APPENDIX: RECONCILIATION OF ADJUSTED EBITDA

Reconciliation of Adjusted EBITDA to GAAP Net Income

(Unaudited, In Thousands)

Three Months Ended

GAAP net income, as reported

Interest expense

Contingent interest expense

Pay-off of future contingent interest

Provision for income taxes

Depreciation and amortization

Amount applied to principal on receivable portfolios

Stock-based compensation expense

Adjusted EBITDA

3/31/07 4,991 4,042 3,235 - 3,437 869 28,259 801 45,634

6/30/07 (1,515) 4,506 888 11,733 (1,031) 840 29,452 1,204 46,077

9/30/07 4,568 4,840 - - 1,315 833 26,114 1,281 38,951

12/31/07 4,187 5,260 - - 2,777 810 29,498 1,001 43,533

3/31/08 6,751 5,200 - - 4,509 722 40,212 1,094 58,488

6/30/08 6,162 4,831 - - 4,225 766 35,785 1,228 52,997

9/30/08 3,028 5,140 - - 2,408 674 35,140 860 47,250

12/31/08 (2,095) 5,401 - - (1,442) 652 46,364 382 49,262

3/31/09 8,997 4,273 - - 5,973 623 42,851 1,080 63,797

6/30/09 6,641 3,958 - - 4,166 620 48,303 994 64,682

9/30/09 9,004 3,970 - - 5,948 652 49,188 1,261 70,023

12/31/09 8,405 3,959 - - 4,609 697 47,384 1,049 66,103

3/31/10 10,861 4,538 - - 6,490 673 58,265 1,761 82,588

6/30/10 11,730 4,880 - - 6,749 752 64,901 1,446 90,458

9/30/10 12,290 4,928 - - 6,632 816 63,507 1,549 89,722

12/31/10 14,171 5,003 - - 9,075 958 53,427 1,254 83,888

3/31/11 13,679 5,593 - - 8,601 1,053 85,709 1,765 116,400

Note: The periods 3/31/07 through 12/31/08 have been adjusted to reflect the retrospective application of ASC 470-20

ENCORE

CAPITAL GROUP

20