Table of Contents

Filed pursuant to Rule 424(b)(1)

Registration No. 333-132182

333-130879

PROSPECTUS

2,850,000 Shares

NATURAL GAS SERVICES GROUP, INC.

Common Stock

We are selling 2,468,000 shares of our common stock and the selling stockholders are selling 382,000 shares of our common stock. We will not receive any proceeds from the sale of our common stock by the selling stockholders.

Our common stock trades on the American Stock Exchange under the symbol “NGS”. On March 2, 2006, the last sale price reported for our common stock on the American Stock Exchange was $18.43 per share.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 9.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Public offering price | $ | 17.50 | $ | 49,875,000 | ||||

| Underwriting discount | $ | 1.01 | $ | 2,867,813 | ||||

| Proceeds to us before expenses | $ | 16.49 | $ | 40,706,575 | ||||

| Proceeds to selling stockholders | $ | 16.49 | $ | 6,300,613 | ||||

We have granted Morgan Keegan & Company, Inc. a30-day option to purchase up to an aggregate of 427,500 shares of common stock, solely to cover over-allotments, if any.

Morgan Keegan & Company, Inc. expects to deliver the shares of common stock to purchasers on or about March 8, 2006.

MORGAN KEEGAN & COMPANY, INC.

The date of this prospectus is March 2, 2006.

Table of Contents

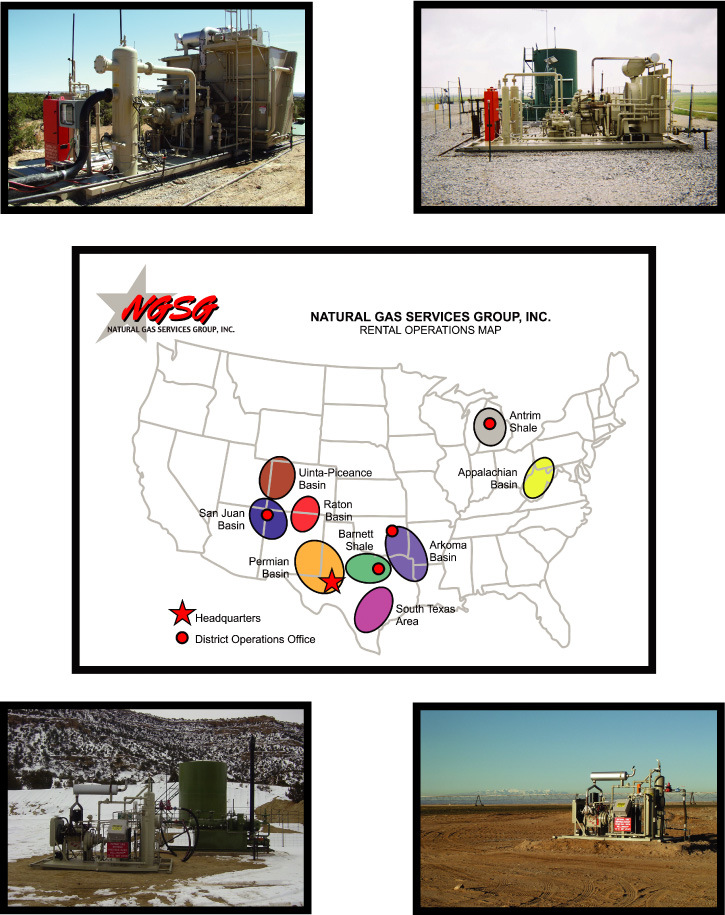

| NATURAL GAS SERVICES GROUP, INC. RENTAL OPERATIONS MAP |

| Headquarters District Operations Office Uinta-Piceance Basin Barnett Shale Appalachian Basin Antrim Shale Raton Basin San Juan Basin Permian Basin South Texas Area Arkoma Basin |

TABLE OF CONTENTS

| Page | ||||

| 1 | ||||

| 9 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 25 | ||||

| 27 | ||||

| 40 | ||||

| 48 | ||||

| 57 | ||||

| 59 | ||||

| 62 | ||||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 66 | ||||

| 67 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. You should not assume that the information in this prospectus is accurate as of any date other than the date on the front of this prospectus.

Unless the context otherwise requires, references in this prospectus to “Natural Gas Services Group,” “we,” “us,” “our” or “ours” refer to Natural Gas Services Group, Inc., together with our operating subsidiary. When the context requires, we refer to these entities separately. References in this prospectus to the “selling stockholders” refer to the selling stockholders identified under “Principal and Selling Stockholders.” Certain specialized terms used in describing our natural gas compressor business are defined in “Glossary of Industry Terms”. Unless otherwise indicated, the information in this prospectus assumes that the underwriter does not exercise its over-allotment option.

i

Table of Contents

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the information under the heading “Risk Factors,” our consolidated financial statements and the notes to those consolidated financial statements included elsewhere in this prospectus.

The Company

We are a leading provider of small to medium horsepower compression equipment to the natural gas industry. We focus primarily on the non-conventional natural gas production business in the United States (such as coalbed methane, gas shales and tight gas), which, according to data from the Energy Information Administration, is the single largest and fastest growing segment of U.S. gas production. We manufacture, fabricate and rent natural gas compressors that enhance the production of natural gas wells and provide maintenance services for those compressors. In addition, we sell custom fabricated natural gas compressors to meet customer specifications dictated by well pressures, production characteristics and particular applications. We also manufacture and sell flare systems for gas plant and production facilities.

The vast majority of our rental operations are in non-conventional natural gas areas which typically have lower initial reservoir pressures and faster well decline rates. These areas usually require compression to be installed sooner and with greater frequency.

Historically, the majority of our revenue has been derived from our compressor rental business. In January 2005, we acquired Screw Compression Systems, Inc., or “SCS,” which predominantly focuses on the custom fabrication sales business. By acquiring SCS, we increased our fabrication capacity by over 91,000 square feet. We intend to use this capacity to expand our rental fleet while continuing SCS’ core business of custom fabrication.

Natural gas compressors are used in a number of applications for the production and enhancement of gas wells and in gas transportation lines and processing plants. Compression equipment is often required to boost a well’s production to economically viable levels and enable gas to continue to flow in the pipeline to its destination. We believe that most producing gas wells in North America, at some point, will utilize compression. The World Oil Magazine reported that, as of December 31, 2004, there were approximately 395,000 producing gas wells in the United States. The states of New Mexico, Texas, Michigan, Colorado, Wyoming, Utah, Oklahoma, Pennsylvania, West Virginia and Kansas, our present areas of operation, account for approximately 297,000 of these wells.

We increased our revenue to $49.3 million in 2005 from $10.3 million in 2002, the year we completed our initial public offering. During the same period, income from operations increased to $8.9 million from $1.8 million. Our compressor rental fleet has grown from 302 compressors at the end of 2002 to 865 compressors at December 31, 2005.

Our Operating Units

Gas Compressor Rental. Our rental business is primarily focused on non-conventional gas production. We provide rental of small to medium horsepower compression equipment to customers via contracts typically having minimum initial terms of six to 24 months. Historically, in our experience, most customers retain the equipment beyond the expiration of the initial term. By outsourcing their compression needs, we believe our customers are able to increase their revenues by producing a higher volume of natural gas due to greater equipment run-time. Outsourcing also allows our customers to reduce their compressor downtime, operating and maintenance costs and capital investments and more efficiently meet their changing compression needs. As of December 31, 2005, approximately 94.8% of our rental fleet was utilized. In 2006, we intend to increase the number of units in our rental fleet by 30% to 40%.

1

Table of Contents

Engineered Equipment Sales

| • | Compressor fabrication. Fabrication involves the assembly of compressor components manufactured by us or other third parties into compressor units that are ready for rental or sale. In addition to fabricating compressors for our rental fleet, we engineer and fabricate natural gas compressors for sale to customers to meet their specifications based on well pressure, production characteristics and the particular applications for which compression is sought. | |

| • | Compressor manufacturing. We design and manufacture our own proprietary line of reciprocating compressor frames, cylinders and parts known as our “CiP”, orCylinder-in-Plane, product line. We use the finished components to fabricate compressor units for our rental fleet or for sale to third parties. We also sell finished components to other fabricators. | |

| • | Flare fabrication. We design, fabricate, sell, install and service flare stacks and related ignition and control devices for the onshore and offshore incineration of gas compounds such as hydrogen sulfide, carbon dioxide, natural gas and liquefied petroleum gases. Applications for this equipment are often environmentally and regulatory driven, and we believe we are a leading supplier to this market. | |

| • | Parts sales and compressor rebuilds. To provide customer support for our compressor and flare sales businesses, we stock varying levels of replacement parts at our Midland, Texas facility and at field service locations. We also provide an exchange and rebuild program for screw compressors and maintain an inventory of new and used compressors to facilitate this part of our business. |

Service and Maintenance. We service and maintain compressors owned by our customers on an “as needed” or contractual basis. Natural gas compressors require routine maintenance and periodic refurbishing to prolong their useful life. Routine maintenance includes physical and visual inspections and other parametric checks that indicate a change in the condition of the compressors. We perform wear-particle analysis on all packages and perform overhauls on a condition-based interval or a time-based schedule. Based on our past experience, these maintenance procedures maximize component life and unit availability and minimize downtime.

Business Strategy

We intend to grow our revenue and profitability by pursuing the following business strategies:

| • | Expand rental fleet. With a portion of the proceeds from this offering and using the additional fabrication capacity gained with the SCS acquisition, we intend to increase our market share by expanding our rental fleet 30% to 40% by the end of 2006. We believe our growth will continue to be primarily driven through our placement of small to medium horsepower wellhead gas compressors for non-conventional gas production, which is the single largest and fastest growing segment of U.S. gas production according to data from the Energy Information Administration. As of December 31, 2005, we had 820 natural gas compressors rented to third parties. | |

| • | Operational expansion. With the planned increase in our rental fleet, we intend to expand our operations in existing areas, as well as pursue focused expansion into new geographic regions. We have recently entered new markets in Appalachia and the Rocky Mountains. | |

| • | Expand CiP(Cylinder-in-Plane) product line. The CiP, orCylinder-in-Plane, is our proprietary reciprocating compressor product line. This product line has allowed us to expand our compressor rentals and sales into higher pressure gas gathering and transmission lines. We intend to establish new distributorship relationships and after-market sales and services networks. | |

| • | Selectively pursue acquisitions. We intend to evaluate potential acquisitions that would provide us with access to new markets or enhance our current market position. |

2

Table of Contents

Competitive Strengths

We believe we are well positioned to execute our business strategy because of the following competitive strengths:

| • | Superior customer service. Our emphasis on the small to medium horsepower markets has enabled us to effectively meet the evolving needs of our customers. We believe these markets have been under-serviced by our larger competitors which, coupled with our personalized services and in-depth knowledge of our customers’ operating needs and growth plans, have allowed us to enhance our relationships with existing customers as well as attract new customers. The size, type and geographic diversity of our rental fleet enables us to provide customers with a range of compression units that can serve a wide variety of applications. We are able to select the correct equipment for the job, rather than the customer trying to fit its application to our equipment. | |

| • | Diversified product line. Our compressors are available as high and low pressure rotary screw and reciprocating packages. They are designed to meet a number of applications, including wellhead production, natural gas gathering, natural gas transmission, vapor recovery and gas and plunger lift. In addition, our compressors can be built to handle a variety of gas mixtures, including air, nitrogen, carbon dioxide, hydrogen sulfide and hydrocarbon gases. A diversified product line helps us compete by being able to satisfy widely varying pressure, volume and production conditions that customers encounter. | |

| • | Purpose built rental compressors. Our rental compressor packages have been designed and built to address the primary requirements of our customers in the producing regions in which we operate. Our units are compact in design and are easy, quick and inexpensive to move, install andstart-up. Our control systems are technically advanced and allow the operator to start and stop our units remotely and/or in accordance with well conditions. We believe our rental fleet is also one of the newest with an average age of less than three years old. | |

| • | Experienced management team. On average, our executive and operating management team has over 20 years of oilfield services industry experience. We believe our management team has successfully demonstrated its ability to grow our business both organically and through selective acquisitions. | |

| • | Broad geographic presence. We presently provide our products and services to a customer base of oil and natural gas exploration and production companies operating in New Mexico, Texas, Michigan, Colorado, Wyoming, Utah, Oklahoma, Pennsylvania, West Virginia and Kansas. Our footprint allows us to service many of the natural gas producing regions in the United States. We believe that operating in diverse geographic regions allows us better utilization of our compressors, minimal incremental expenses, operating synergies, volume-based purchasing, leveraged inventories and cross-trained personnel. | |

| • | Long-standing customer relationships. We have developed long-standing relationships providing compression equipment to many major and independent oil and natural gas companies. Our customers generally continue to rent our compressors after the expiration of the initial terms of our rental agreements, which we believe reflects their satisfaction with the reliability and performance of our services and products. |

Recent Developments

We have included below a summary of our unaudited results of operations and financial condition for the year ended December 31, 2005. This summary should be read in conjunction with our unaudited consolidated financial statements as of and for the year ended December 31, 2005 included elsewhere in

3

Table of Contents

this prospectus, which financial statements have not been reviewed by our independent auditors, but have been prepared on a basis consistent with our audited consolidated financial statements.

Total revenues for the year ended December 31, 2005 increased 209.0% to $49.3 million, as compared to $16.0 million for the year ended December 31, 2004. The increase in revenue reflects the increase in our rental revenue and the addition of revenue from our acquisition of SCS.

Sales revenue increased from $3.6 million to $30.3 million, or 742.7%, for the year ended December 31, 2005, compared to the year ended December 31, 2004. The increase is mainly the result of the sale of compressor units to outside third parties by SCS.

Service and maintenance revenue increased from $1.9 million to $2.4 million, or 29.3%, for the year ended December 31, 2005, compared to the year ended December 31, 2004. The increase is mainly the result of additional third party labor sales in our New Mexico and Michigan branches.

Rental revenue increased from $10.5 million to $16.6 million, or 58.3%, for the year ended December 31, 2005, compared to the year ended December 31, 2004. The increase is mainly the result of units added to our rental fleet and rented to third parties. At December 31, 2005, we had 865 compressor packages in our rental fleet, up from 586 units at December 31, 2004. The average monthly rental rate per unit at December 31, 2005 was $2,075, as compared to $1,962 at December 31, 2004.

Net income for the year ended December 31, 2005 increased 33.9% to $4.4 million ($.52 per diluted share), as compared to $3.3 million ($.52 per diluted share) for the year ended December 31, 2004. Our 2004 net income included life insurance proceeds in the amount of $1.5 million we received upon the death in March 2004 of our former President and Chief Executive Officer.

At December 31, 2005, current assets were $24.6 million, which included $3.3 million of cash. Current liabilities were $11.2 million, and long-term debt was $22.2 million. Our stockholders’ equity as of December 31, 2005 was $45.7 million.

Corporate Information

We were incorporated in Colorado on December 17, 1998. We maintain our executive offices at 2911 South County Road 1260, Midland, Texas 79706, and our telephone number is (432) 563-3974. Our website is located athttp://www.ngsgi.com. The information on or that can be accessed through our website is not part of this prospectus.

4

Table of Contents

The Offering

| Common stock offered by us(1) | 2,468,000 shares. | |

| Common stock offered by the selling stockholders | 382,000 shares. | |

| Shares outstanding prior to the offering(2) | 9,031,783 shares as of February 13, 2006. | |

| Shares to be outstanding after the offering(1)(2) | 11,499,783 shares. | |

| Use of proceeds | We intend to use the net proceeds from the sale of shares of our common stock by us for capital expenditures, including expansion of our rental fleet, debt reduction, working capital and general corporate purposes. We will not receive any proceeds from the sale of shares by the selling stockholders. | |

| American Stock Exchange symbol | NGS | |

| Risk factors | Please read “Risk Factors” for a discussion of factors you should consider carefully before deciding to invest in shares of our common stock. |

| (1) | Assuming no exercise by the underwriter of its over-allotment option to purchase an additional 427,500 shares of common stock from us. |

| (2) | Excludes 146,668 shares issuable upon the exercise of outstanding stock options and 133,028 shares issuable upon the exercise of outstanding warrants. |

5

Table of Contents

Summary Historical and Pro Forma Consolidated Financial Information

The following summary historical consolidated financial information for each of the years in the three year period ended December 31, 2004, has been derived from our audited consolidated financial statements. The following summary historical consolidated financial information for the year ended December 31, 2005 has been derived from our unaudited consolidated financial statements, which have not been reviewed by our independent auditors, but have been prepared on a basis consistent with our audited consolidated financial statements. The following summary historical consolidated financial information has been derived from our unaudited consolidated financial statements and, in the opinion of our management, includes all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation. The summary pro forma consolidated statement of income and other information for the year ended December 31, 2004 gives effect to our acquisition of SCS, as if the acquisition was consummated on January 1, 2004. This information is only a summary and you should read it in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which discusses factors affecting the comparability of the information presented, and in conjunction with our financial statements and related notes included elsewhere in this prospectus, including the pro forma financial statements. Results for interim periods may not be indicative of results for full fiscal years.

| Year Ended December 31, | |||||||||||||||||||||

| Pro Forma | |||||||||||||||||||||

| 2002 | 2003 | 2004 | 2004 | 2005(1) | |||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||

| (in thousands, except per share amounts, compressor | |||||||||||||||||||||

| units andutilization) | |||||||||||||||||||||

CONSOLIDATED STATEMENTS OF INCOME AND OTHER INFORMATION: | |||||||||||||||||||||

| Revenues | $ | 10,297 | $ | 12,750 | $ | 15,958 | $ | 37,382 | $ | 49,311 | |||||||||||

| Costs of revenues, exclusive of depreciation shown separately below | 5,572 | 6,057 | 6,951 | 23,123 | 31,338 | ||||||||||||||||

| Gross profit | 4,725 | 6,693 | 9,007 | 14,259 | 17,973 | ||||||||||||||||

| Depreciation and amortization | 1,166 | 1,726 | 2,444 | 2,772 | 4,224 | ||||||||||||||||

| Other operating expenses | 1,718 | 2,292 | 2,652 | 5,167 | 4,890 | ||||||||||||||||

| Operating income | 1,841 | 2,675 | 3,911 | 6,320 | 8,859 | ||||||||||||||||

Total other income (expense)(2) | (471 | ) | (671 | ) | 603 | (39 | ) | (1,798 | ) | ||||||||||||

| Income before income taxes | 1,370 | 2,004 | 4,514 | 6,281 | 7,061 | ||||||||||||||||

| Total income tax expense | 584 | 697 | 1,140 | 2,080 | 2,615 | ||||||||||||||||

| Net income | 786 | 1,307 | 3,374 | 4,201 | 4,446 | ||||||||||||||||

| Preferred dividends | 107 | 121 | 53 | 53 | — | ||||||||||||||||

| Net income available to common stockholders | $ | 679 | $ | 1,186 | $ | 3,321 | $ | 4,148 | $ | 4,446 | |||||||||||

| Net income per common share: | |||||||||||||||||||||

| Basic | $ | 0.19 | $ | 0.24 | $ | 0.59 | $ | 0.67 | $ | 0.59 | |||||||||||

| Diluted | $ | 0.16 | $ | 0.23 | $ | 0.52 | $ | 0.59 | $ | 0.52 | |||||||||||

| Weighted average shares of common stock outstanding: | |||||||||||||||||||||

| Basic | 3,649 | 4,947 | 5,591 | 6,201 | 7,564 | ||||||||||||||||

| Diluted | 4,305 | 5,253 | 6,383 | 6,993 | 8,481 | ||||||||||||||||

EBITDA(3) | $ | 3,511 | $ | 4,397 | $ | 7,796 | $ | 10,903 | $ | 13,282 | |||||||||||

| Total compressor units in rental fleet (end of period) | 302 | 399 | 586 | 587 | 865 | ||||||||||||||||

Compressor utilization (end of period)(4) | 79.1% | 90.7% | 95.9% | 95.9% | 94.8% | ||||||||||||||||

6

Table of Contents

| As of | ||||||||

| December 31, 2005 | ||||||||

| As | ||||||||

| Actual | Adjusted(5) | |||||||

| (unaudited) | ||||||||

| (in thousands) | ||||||||

BALANCE SHEET INFORMATION: | ||||||||

| Cash and cash equivalents | $ | 3,271 | $ | 38,553 | ||||

| Total assets | 86,369 | 121,651 | ||||||

| Long-term debt (including current portion) | 28,205 | 23,205 | ||||||

| Stockholders’ equity | 45,690 | 85,972 | ||||||

| (1) | The information for the periods presented may not be comparable because of our acquisition of SCS in January 2005. For additional information regarding this acquisition, you should read the information under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Transactions with Selling Stockholders and Other Related Parties — Acquisition of Screw Compression Systems, Inc.” in this prospectus. |

| (2) | Total other income (expense) for the year ended December 31, 2004 includes $1.5 million in life insurance proceeds paid to us upon the death of our former Chief Executive Officer. |

| (3) | “EBITDA” is a non-GAAP financial measure of earnings (net income) before interest, taxes, depreciation, and amortization. This term, as used and defined by us, may not be comparable to similarly titled measures employed by other companies and is not a measure of performance calculated in accordance with GAAP. EBITDA should not be considered in isolation or as a substitute for operating income, net income or loss, cash flows provided by operating, investing and financing activities, or other income or cash flow statement data prepared in accordance with GAAP. However, management believes EBITDA is useful to an investor in evaluating our operating performance because: |

| • | it is widely used by investors in the energy industry to measure a company’s operating performance without regard to items excluded from the calculation of EBITDA, which can vary substantially from company to company depending upon accounting methods and book value of assets, capital structure and the method by which assets were acquired, among other factors; | |

| • | it helps investors to more meaningfully evaluate and compare the results of our operations from period to period by removing the impact of our capital structure and asset base from our operating structure; and | |

| • | it is used by our management for various purposes, including as a measure of operating performance, in presentations to our Board of Directors, as a basis for strategic planning and forecasting, and as a component for setting incentive compensation. |

7

Table of Contents

| There are material limitations to using EBITDA as a measure of performance, including the inability to analyze the impact of certain recurring items that materially affect our net income or loss, and the lack of comparability of results of operations of different companies. The following table reconciles EBITDA to our net income, the most directly comparable GAAP financial measure: |

| Year Ended December 31, | ||||||||||||||||||||

| Pro Forma | ||||||||||||||||||||

| 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| EBITDA | $ | 3,511 | $ | 4,397 | $ | 7,796 | $ | 10,903 | $ | 13,282 | ||||||||||

| Depreciation and amortization | 1,166 | 1,726 | 2,444 | 3,071 | 4,224 | |||||||||||||||

| Interest expense, net | 975 | 667 | 838 | 1,551 | 1,997 | |||||||||||||||

| Income taxes | 584 | 697 | 1,140 | 2,080 | 2,615 | |||||||||||||||

| Net income | $ | 786 | $ | 1,307 | $ | 3,374 | $ | 4,201 | $ | 4,446 | ||||||||||

| (4) | Compressor utilization is the percentage of compressors within our rental fleet that are rented to third parties. |

| (5) | Gives effect to this offering and our receipt of net proceeds of approximately $40.3 million, and the use of $5.0 million of net proceeds for the repayment of debt, as if this offering had been completed on December 31, 2005. Assumes no exercise of the underwriter’s over-allotment option. |

8

Table of Contents

RISK FACTORS

You should carefully consider the following risks before you decide to buy our common stock. If any of the following risks actually occur, our business, financial condition or results of operations would likely suffer. If this occurs, the trading price of our common stock could decline, and you could lose all or part of the money you paid to buy our common stock. Although the risks described below are the risks that we believe are material, they are not the only risks relating to our industry, our business and our common stock. Additional risks and uncertainties, including those that are not yet identified or that we currently believe are immaterial, may also adversely affect our business, financial condition or results of operations.

Risks Associated With Our Industry

Decreased oil and natural gas prices and oil and gas industry expenditure levels would adversely affect our revenue.

Our revenue is derived from expenditures in the oil and natural gas industry which, in turn, are based on budgets to explore for, develop and produce oil and natural gas. If these expenditures decline, our revenue will suffer. The industry’s willingness to explore for, develop and produce oil and natural gas depends largely upon the prevailing view of future oil and natural gas prices. Prices for oil and gas historically have been, and are likely to continue to be, highly volatile. Many factors affect the supply and demand for oil and natural gas and, therefore, influence oil and natural gas prices, including:

| • | the level of oil and natural gas production; | |

| • | the level of oil and natural gas inventories; | |

| • | domestic and worldwide demand for oil and natural gas; | |

| • | the expected cost of developing new reserves; | |

| • | the cost of producing oil and natural gas; | |

| • | the level of drilling and producing activity; | |

| • | inclement weather; | |

| • | domestic and worldwide economic activity; | |

| • | regulatory and other federal and state requirements in the United States; | |

| • | the ability of the Organization of Petroleum Exporting Countries to set and maintain production levels and prices for oil; | |

| • | political conditions in or affecting oil and natural gas producing countries; | |

| • | terrorist activities in the United States and elsewhere; | |

| • | the cost of developing alternate energy sources; | |

| • | environmental regulation; and | |

| • | tax policies. |

If the demand for oil and natural gas decreases, then demand for our compressors likely will decrease.

Depending on the market prices of oil and natural gas, companies exploring for oil and natural gas may cancel or curtail their drilling programs, thereby reducing demand for our equipment and services. Our rental contracts are generally short-term, and oil and natural gas companies tend to respond quickly to upward or downward changes in prices. Any reduction in drilling and production activities may materially erode both pricing and utilization rates for our equipment and services and adversely affect our financial results. As a result, we may suffer losses, be unable to make necessary capital expenditures and be unable to meet our financial obligations.

9

Table of Contents

The intense competition in our industry could result in reduced profitability and loss of market share for us.

In our business segments, we compete with the oil and natural gas industry’s largest equipment and service providers who have greater name recognition than we do. These companies also have substantially greater financial resources, larger operations and greater budgets for marketing, research and development than we do. They may be better able to compete because of their broader geographic dispersion, the greater number of compressors in their fleet or their product and service diversity. As a result, we could lose customers and market share to those competitors. These companies may also be better positioned than us to successfully endure downturns in the oil and natural gas industry.

Our operations may be adversely affected if our current competitors or new market entrants introduce new products or services with better prices, features, performance or other competitive characteristics than our products and services. Competitive pressures or other factors also may result in significant price competition that could harm our revenue and our business. Additionally, we may face competition in our efforts to acquire other businesses.

Our industry is highly cyclical, and our results of operations may be volatile.

Our industry is highly cyclical, with periods of high demand and high pricing followed by periods of low demand and low pricing. Periods of low demand intensify the competition in the industry and often result in rental equipment being idle for long periods of time. We may be required to enter into lower rate rental contracts in response to market conditions in the future, and our sales may decrease as a result of such conditions.

Due to the short-term nature of most of our rental contracts, changes in market conditions can quickly affect our business. As a result of the cyclicality of our industry, our results of operations may be volatile in the future.

We are subject to extensive environmental laws and regulations that could require us to take costly compliance actions that could harm our financial condition.

Our fabrication and maintenance operations are significantly affected by stringent and complex federal, state and local laws and regulations governing the discharge of substances into the environment or otherwise relating to environmental protection. In these operations, we generate and manage hazardous wastes such as solvents, thinner, waste paint, waste oil, washdown wastes, and sandblast material. We attempt to use generally accepted operating and disposal practices and, with respect to acquisitions, will attempt to identify and assess whether there is any environmental risk before completing an acquisition. Based on the nature of the industry, however, hydrocarbons or other wastes may have been disposed of or released on or under properties owned or leased by us or on or under other locations where such wastes have been taken for disposal. The waste on these properties may be subject to federal or state environmental laws that could require us to remove the wastes or remediate sites where they have been released. We could be exposed to liability for cleanup costs, natural resource and other damages as a result of our conduct or the conduct of, or conditions caused by, prior owners, lessees or other third parties. Environmental laws and regulations have changed in the past, and they are likely to change in the future. If existing regulatory requirements or enforcement policies change, we may be required to make significant unanticipated capital and operating expenditures.

Any failure by us to comply with applicable environmental laws and regulations may result in governmental authorities taking actions against our business that could harm our operations and financial condition, including the:

| • | issuance of administrative, civil and criminal penalties; | |

| • | denial or revocation of permits or other authorizations; | |

| • | reduction or cessation in operations; and | |

| • | performance of site investigatory, remedial or other corrective actions. |

10

Table of Contents

Risks Associated With Our Company

We might be unable to employ adequate technical personnel, which could hamper our plans for expansion or increase our costs.

Many of the compressors that we sell or rent are mechanically complex and often must perform in harsh conditions. We believe that our success depends upon our ability to employ and retain a sufficient number of technical personnel who have the ability to design, utilize, enhance and maintain these compressors. Our ability to expand our operations depends in part on our ability to increase our skilled labor force. The demand for skilled workers is high and supply is limited. A significant increase in the wages paid by competing employers could result in a reduction of our skilled labor force or cause an increase in the wage rates that we must pay or both. If either of these events were to occur, our cost structure could increase and our operations and growth potential could be impaired.

We could be subject to substantial liability claims that could harm our financial condition.

Our products are used in hazardous drilling and production applications where an accident or a failure of a product can cause personal injury, loss of life, damage to property, equipment or the environment, or suspension of operations.

While we maintain insurance coverage, we face the following risks under our insurance coverage:

| • | we may not be able to continue to obtain insurance on commercially reasonable terms; | |

| • | we may be faced with types of liabilities that will not be covered by our insurance, such as damages from significant product liabilities and from environmental contamination; | |

| • | the dollar amount of any liabilities may exceed our policy limits; and | |

| • | we do not maintain coverage against the risk of interruption of our business. |

Any claims made under our policy will likely cause our premiums to increase. Any future damages caused by our products or services that are not covered by insurance, are in excess of policy limits or are subject to substantial deductibles, would reduce our earnings and our cash available for operations.

We will require a substantial amount of capital to expand our compressor rental fleet and grow our business.

During 2006, we plan to spend approximately $25.0 million to $30.0 million in capital expenditures to expand our rental fleet. The amount and timing of these capital expenditures may vary depending on a variety of factors, including the level of activity in the oil and natural gas exploration and production industry and the presence of alternative uses for our capital, including any acquisitions that we may pursue.

Historically, we have funded our capital expenditures through internally generated funds, borrowings under bank credit facilities and the proceeds of equity financings. Although we believe that the proceeds of this offering, cash flows from our operations and borrowings under our existing bank credit facility will provide us with sufficient cash to fund our planned capital expenditures for 2006, we cannot assure you that these sources will be sufficient. We may require additional capital to fund any unanticipated capital expenditures, including any acquisitions, and to fund our growth beyond 2006, and necessary capital may not be available to us when we need it or on acceptable terms. Our ability to raise additional capital will depend on the results of our operations and the status of various capital and industry markets at the time we seek such capital. Failure to generate sufficient cash flow, together with the absence of alternative sources of capital, could have a material adverse effect on our business, consolidated financial condition, results of operations or cash flows.

11

Table of Contents

Our current debt level is high and may negatively impact our current and future financial stability.

As of December 31, 2005, we had an aggregate of approximately $28.2 million of outstanding indebtedness, not including outstanding letters of credit in the aggregate face amount of $2.0 million, and accounts payable and accrued expenses of approximately $5.1 million. As a result of our significant indebtedness, we might not have the ability to incur any substantial additional indebtedness. The level of our indebtedness could have several important effects on our future operations, including:

| • | our ability to obtain additional financing for working capital, acquisitions, capital expenditures and other purposes may be limited; | |

| • | a significant portion of our cash flow from operations may be dedicated to the payment of principal and interest on our debt, thereby reducing funds available for other purposes; and | |

| • | our significant leverage could make us more vulnerable to economic downturns. |

If we are unable to service our debt, we will likely be forced to take remedial steps that are contrary to our business plan.

As of December 31, 2005, our principal payments for our debt service requirements were approximately $473,000 on a monthly basis; $1.4 million on a quarterly basis; and $5.7 million on an annual basis. It is possible that our business will not generate sufficient cash flow from operations to meet our debt service requirements and the payment of principal when due. If this were to occur, we may be forced to:

| • | sell assets at disadvantageous prices; | |

| • | obtain additional financing; or | |

| • | refinance all or a portion of our indebtedness on terms that may be less favorable to us. |

Our current bank loan agreement contains covenants that limit our operating and financial flexibility and, if breached, could expose us to severe remedial provisions.

Under the terms of our loan agreement, we must:

| • | comply with a minimum current ratio; | |

| • | maintain minimum levels of tangible net worth; | |

| • | not exceed specified levels of debt; | |

| • | comply with a debt service coverage ratio; and | |

| • | comply with a debt to tangible net worth ratio. |

Our ability to meet the financial ratios and tests under our bank loan agreement can be affected by events beyond our control, and we may not be able to satisfy those ratios and tests. A breach of any one of these covenants could permit the bank to accelerate the debt so that it is immediately due and payable. If a breach occurred, no further borrowings would be available under our loan agreement. If we were unable to repay the debt, the bank could proceed against and foreclose on our assets.

If we fail to acquire or successfully integrate additional businesses, our growth may be limited and our results of operations may suffer.

As part of our business strategy, we intend to evaluate potential acquisitions of other businesses or assets. However, there can be no assurance that we will be successful in consummating any such acquisitions. Successful acquisition of businesses or assets will depend on various factors, including, but not limited to, our ability to obtain financing and the competitive environment for acquisitions. In addition, we may not be able to successfully integrate any businesses or assets that we acquire in the future. The integration of acquired businesses is likely to be complex and time consuming and place a significant strain

12

Table of Contents

on management and may disrupt our business. We also may be adversely impacted by any unknown liabilities of acquired businesses, including environmental liabilities. We may encounter substantial difficulties, costs and delays involved in integrating common accounting, information and communication systems, operating procedures, internal controls and human resources practices, including incompatibility of business cultures and the loss of key employees and customers. These difficulties may reduce our ability to gain customers or retain existing customers, and may increase operating expenses, resulting in reduced revenues and income and a failure to realize the anticipated benefits of acquisitions.

As of December 31, 2005, a significant majority of our compressor rentals were for terms of six months or less which, if terminated or not renewed, would adversely impact our revenue and our ability to recover our initial equipment costs.

The length of our compressor rental agreements with our customers varies based on customer needs, equipment configurations and geographic area. In most cases, under currently prevailing rental rates, the initial rental periods are not long enough to enable us to fully recoup the average cost of acquiring or fabricating the equipment. We cannot be sure that a substantial number of our customers will continue to renew their rental agreements or that we will be able tore-rent the equipment to new customers or that any renewals orre-rentals will be at comparable rental rates. The inability to timely renew orre-rent a substantial portion of our compressor rental fleet would have a material adverse effect upon our business, consolidated financial condition, results of operations and cash flows.

The loss of one or more of our current customers could adversely affect our results of operations. It is likely that we will not continue to receive the same level of revenues we have received in the past from one of our customers.

Our business is dependent not only on securing new customers but also on maintaining current customers. In connection with our acquisition in March 2001 of the compression related assets of Dominion Michigan Petroleum Services, Inc., an affiliate of Dominion Michigan, Dominion Exploration & Production, Inc., committed to purchase compressors from us or enter into five year rental contracts with us for compression totaling five-thousand horsepower. This obligation expired December 31, 2005. In August 2005, we and competing third parties were invited to submit bids for providing continued rental and maintenance services to Dominion. In October 2005, we were advised that we will retain Dominion’s screw compressor rental business and the associated maintenance and service business, but that an unaffiliated third party will maintain and service Dominion’s reciprocating compressors. We estimate that the screw compressor rental, maintenance and service business we have retained from Dominion Exploration represented approximately 78% and 86% of our revenues from Dominion Exploration in the year ended December 31, 2004 and the nine months ended September 30, 2005, respectively. Dominion Exploration & Production, Inc. accounted for approximately 21% of our consolidated revenue for the year ended December 31, 2004, and approximately 10% of our consolidated revenue for the nine months ended September 30, 2005. XTO Energy, Inc. accounted for approximately 31% of our consolidated revenue for the nine months ended September 30, 2005. Unless we are able to retain our existing customers, or secure new customers if we lose one or more of our significant customers, our revenue and results of operations would be adversely affected.

Loss of key members of our management could adversely affect our business.

We depend on the continued employment and performance of Stephen C. Taylor, our Chairman of the Board of Directors, President and Chief Executive Officer, and other key members of our management. If any of our key managers resigns or becomes unable to continue in his present role and is not adequately replaced, our business operations could be materially adversely affected.

13

Table of Contents

Failure to effectively manage our growth and expansion could adversely affect our business and operating results and our internal controls.

We have rapidly and significantly expanded our operations in recent years and anticipate that our growth will continue if we are able to execute our strategy. Our rapid growth has placed significant strain on our management and other resources which, given our expected future growth rate, is likely to continue. To manage our future growth, we must, among other things:

| • | accurately assess the number of additional officers and employees we will require and the areas in which they will be required; | |

| • | attract, hire and retain additional highly skilled and motivated officers and employees; | |

| • | train and manage our work force in a timely and effective manner; | |

| • | upgrade and expand our office infrastructure so that it is appropriate for our level of activity; and | |

| • | improve our financial and management controls, reporting systems and procedures. |

Liability to customers under warranties may materially and adversely affect our earnings.

We provide warranties as to the proper operation and conformance to specifications of the equipment we manufacture. Our equipment is complex and often deployed in harsh environments. Failure of this equipment to operate properly or to meet specifications may increase our costs by requiring additional engineering resources and services, replacement of parts and equipment or monetary reimbursement to a customer. We have in the past received warranty claims and we expect to continue to receive them in the future. To the extent that we incur substantial warranty claims in any period, our reputation, our ability to obtain future business and our earnings could be materially and adversely affected.

Failure to maintain effective internal controls could have a material adverse effect on our operations.

We are in the process of documenting and testing our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act, which requires annual management assessments of the effectiveness of our internal control over financial reporting and a report by our independent auditors addressing these assessments. During the course of our testing we may identify deficiencies which we may not be able to remediate in time to meet the deadline imposed by SEC rules under the Sarbanes-Oxley Act for compliance with the requirements of Section 404. In addition, if we fail to achieve and maintain the adequacy of our internal controls, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act. Moreover, effective internal controls are necessary for us to produce reliable financial reports and to help prevent financial fraud. If, as a result of deficiencies in our internal controls, we cannot provide reliable financial reports or prevent fraud, our business decision process may be adversely affected, our business and operating results could be harmed, investors could lose confidence in our reported financial information, and the price of our stock could decrease as a result.

We must evaluate our intangible assets annually for impairment.

Our intangible assets are recorded at cost less accumulated amortization and consist of goodwill and patent costs and other identifiable intangibles acquired as part of the SCS acquisition. Through December 31, 2001, goodwill was amortized using the straight-line method over 15 years and patent costs were amortized over 13 to 15 years.

In June 2001, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets.” FAS 142 provides that: (1) goodwill and intangible assets with indefinite lives will no longer be amortized; (2) goodwill and intangible assets with indefinite lives must be tested for impairment at least annually; and (3) the amortization period for intangible assets with finite lives will no longer be limited to 40 years. If we determine that our intangible assets with indefinite lives have been impaired, we must record a write-down of those assets on our

14

Table of Contents

consolidated statements of income during the period of impairment. Our determination of impairment will be based on various factors, including any of the following factors, if they materialize:

| • | significant underperformance relative to expected historical or projected future operating results; | |

| • | significant changes in the manner of our use of the acquired assets or the strategy for our overall business; | |

| • | significant negative industry or economic trends; | |

| • | significant decline in our stock price for a sustained period; and | |

| • | our market capitalization relative to net book value. |

We adopted FAS 142 as of January 1, 2002. Based on an independent valuation in July 2002 and June 2003 and an internal evaluation in December 2004 and June 2005 of our reporting units with goodwill, adoption of FAS 142 did not have a material adverse effect on us in 2003 or 2004. In the future it could result in impairments of our intangible assets or goodwill. We expect to continue to amortize our intangible assets with finite lives over the same time periods as previously used, and we will test our intangible assets with indefinite lives for impairment at least once each year. In addition, we are required to assess the consumptive life, or longevity, of our intangible assets with finite lives and adjust their amortization periods accordingly. Our net intangible assets were recorded on our balance sheet at approximately $2.7 million as of December 31, 2004, and at September 30, 2005, the carrying value of net intangible assets had increased to approximately $12.2 million with the acquisition of Screw Compression Systems, Inc. in January 2005. Any impairment in future periods of those assets, or a reduction in their consumptive lives, could materially and adversely affect our consolidated statements of income and financial position.

Risks Associated With Our Common Stock and the Offering

The price of our common stock may fluctuate which may cause our common stock to trade at a substantially lower price than the price which you paid for our common stock.

The trading price of our common stock and the price at which we may sell securities in the future is subject to substantial fluctuations in response to various factors, including our ability to successfully accomplish our business strategy, the trading volume of our stock, changes in governmental regulations, actual or anticipated variations in our quarterly or annual financial results, our involvement in litigation, general market conditions, the prices of oil and natural gas, announcements by us and or competitors, our liquidity, our ability to raise additional funds, and other events.

Future sales of our common stock could adversely affect our stock price.

Substantial sales of our common stock in the public market following this offering, or the perception by the market that those sales could occur, may lower our stock price or make it difficult for us to raise additional equity capital in the future. These potential sales could include sales of shares of our common stock by our Directors and officers, who beneficially owned approximately 18.51% of the outstanding shares of our common stock as of February 13, 2006. We have filed registration statements with the Securities and Exchange Commission registering the resale of approximately 649,574 shares of our currently outstanding common stock and approximately 297,195 shares of common stock that may be issued upon exercise of outstanding stock options and warrants. In January 2005, we issued a total of 609,756 shares of our common stock to the former stockholders of SCS in partial payment of the total purchase price for SCS. These shares are “restricted” securities within the meaning of Rule 144 under the Securities Act of 1933, as amended. Under Rule 144, shares of our common stock that have been held for at least one year may generally be sold in brokers transactions if the amount of shares sold by any stockholder (and the stockholder’s transferees under certain circumstances) in any three-month period does not exceed the greater of 1% of the outstanding stock (currently approximately 90,157 shares) or the

15

Table of Contents

four-week average weekly trading volume of the common stock. The 609,756 shares of common stock we issued to the former stockholders of SCS became eligible for sale under Rule 144 on January 3, 2006. Substantially all other outstanding shares of common stock held by non-affiliates are freely tradable.

If securities analysts downgrade our stock or cease coverage of us, the price of our stock could decline.

The trading market for our common stock relies in part on the research and reports that industry or financial analysts publish about us or our business. We do not control these analysts. Furthermore, there are many large, well-established, publicly traded companies active in our industry and market, which may mean that it is less likely that we will receive widespread analyst coverage. If one or more of the analysts who do cover us downgrade our stock, our stock price would likely decline rapidly. If one or more of these analysts cease coverage of our company, we could lose visibility in the market, which in turn could cause our stock price to decline.

We may invest or spend the net proceeds of this offering in a manner with which you do not agree or in ways that may not earn a profit.

We intend to use the net proceeds from this offering for capital expenditures, including expansion of our rental fleet, and for debt reduction. However, we will retain broad discretion over the use of the proceeds from this offering, and may use the proceeds for other purposes. You may not agree with the ways we decide to use the proceeds, and our use of the proceeds may not yield any profits.

If we issue debt or equity securities, you may lose certain rights and be diluted.

If we raise funds in the future through the issuance of debt or equity securities, the securities issued may have rights and preferences and privileges senior to those of holders of our common stock, and the terms of the securities may impose restrictions on our operations or dilute your ownership in Natural Gas Services Group, Inc.

We do not intend to pay, and have restrictions upon our ability to pay, dividends on our common stock.

We have not paid cash dividends in the past and do not intend to pay dividends on our common stock in the foreseeable future. Net income from our operations, if any, will be used for the development of our business, including capital expenditures, and to retire debt. In addition, our bank loan agreement contains restrictions on our ability to pay cash dividends on our common stock.

We have a comparatively low number of shares of common stock outstanding and, therefore, our common stock may suffer from limited liquidity and its prices will likely be volatile and its value may be adversely affected.

Because of our relatively low number of outstanding shares of common stock, the trading price of our common stock will likely be subject to significant price fluctuations and limited liquidity. This may adversely affect the value of your investment. In addition, our common stock price could be subject to fluctuations in response to variations in quarterly operating results, changes in management, future announcements concerning us, general trends in the industry and other events or factors as well as those described above.

Provisions contained in our governing documents could hinder a change in control of us.

Our articles of incorporation and bylaws contain provisions that may discourage acquisition bids and may limit the price investors are willing to pay for our common stock. Our articles of incorporation and bylaws provide that:

| • | directors will be elected for three-year terms, with approximately one-third of the board of directors standing for election each year; |

16

Table of Contents

| • | cumulative voting is not allowed, which limits the ability of minority shareholders to elect any directors; | |

| • | the unanimous vote of the board of directors or the affirmative vote of the holders of not less than 80% of the votes entitled to be cast by the holders of all shares entitled to vote in the election of directors is required to change the size of the board of directors; and | |

| • | directors may be removed only for cause and only by holders of not less than 80% of the votes entitled to be cast on the matter. |

Our Board of Directors has the authority to issue up to five million shares of preferred stock. The Board of Directors can fix the terms of the preferred stock without any action on the part of our stockholders. The issuance of shares of preferred stock may delay or prevent a change in control transaction. In addition, preferred stock could be used in connection with the Board of Directors’ adoption of a shareholders’ rights plan (also known as a poison pill), which would make it much more difficult to effect a change in control of our company through acquiring or controlling blocks of stock. Also, after completion of this offering, our Directors and officers as a group will continue to beneficially own stock. Although this is not a majority of our stock, it confers substantial voting power in the election of Directors and management of our company. This would make it difficult for other minority stockholders, such as the investors in this offering, to effect a change in control or otherwise extend any significant control over the management of our company. This may adversely affect the market price and interfere with the voting and other rights of our common stock.

17

Table of Contents

USE OF PROCEEDS

Our net proceeds from the sale of the 2,468,000 shares of common stock in this offering will be approximately $40.3 million. If the underwriter exercises its over-allotment option in full, our net proceeds will be approximately $47.3 million. Our net proceeds is the amount we expect to receive from this offering after deducting the underwriting discounts and estimated offering expenses payable by us. We intend to use the net proceeds for the following purposes:

| • | $5.0 million to reduce bank indebtedness; and | |

| • | $27.0 million to $32.0 million for our 2006 capital expenditure budget; and | |

| • | the remainder for working capital and general corporate purposes. |

We intend to use $5.0 million of the net proceeds to reduce bank debt. As of December 31, 2005, the interest rate on our bank borrowings was 7.75%, and the principal amounts outstanding have maturity dates between December 2006 and January 2012. The borrowings under our loan agreement, which are secured by substantially all of our assets, were incurred to finance the addition of compressors to our rental fleet and for the acquisition of SCS.

The previous paragraphs describe our present estimates of our use of the net proceeds of this offering based on our current plans and estimates of anticipated expenses. Our actual expenditures may vary from these estimates. We may also find it necessary or advisable to reallocate the net proceeds within the uses outlined above or to use portions of the net proceeds for other purposes, which may include acquisitions.

Pending these uses, we will invest the net proceeds of this offering primarily in cash equivalents or direct or guaranteed obligations of the United States government.

No part of the proceeds from the sale of the common stock offered by the selling stockholders will be received by us.

DIVIDEND POLICY

We have never declared or paid any dividends on our common stock. We currently intend to continue our policy of retaining earnings for use in our business and we do not anticipate paying cash dividends on our common stock. Our ability to pay cash dividends in the future on the common stock will be dependent upon our:

| • | financial condition; | |

| • | results of operations; | |

| • | current and anticipated cash requirements; | |

| • | plans for expansion; and | |

| • | restrictions under our debt obligations, |

as well as other factors that our Board of Directors deems relevant. The loan agreement with our bank lender contains provisions that restrict us from paying dividends on our common stock.

18

Table of Contents

PRICE RANGE OF COMMON STOCK

Our common stock is traded on the American Stock Exchange under the symbol “NGS.” The following table sets forth for the periods indicated the high and low sales prices for our common stock as reported by the American Stock Exchange.

| Common Stock | ||||||||

| Low | High | |||||||

| Year Ended | ||||||||

| December 31, 2003 | ||||||||

| First Quarter | $ | 3.70 | $ | 4.30 | ||||

| Second Quarter | 3.65 | 7.25 | ||||||

| Third Quarter | 5.45 | 6.75 | ||||||

| Fourth Quarter | 5.25 | 6.24 | ||||||

| Year Ended | ||||||||

| December 31, 2004 | ||||||||

| First Quarter | $ | 5.41 | $ | 7.20 | ||||

| Second Quarter | 7.20 | 10.04 | ||||||

| Third Quarter | 7.12 | 9.45 | ||||||

| Fourth Quarter | 8.07 | 9.43 | ||||||

| Year Ended | ||||||||

| December 31, 2005 | ||||||||

| First Quarter | $ | 9.08 | $ | 11.11 | ||||

| Second Quarter | 9.51 | 11.85 | ||||||

| Third Quarter | 11.55 | 36.00 | ||||||

| Fourth Quarter | 15.67 | 39.99 | ||||||

| Year Ending | ||||||||

| December 31, 2006 | ||||||||

| First Quarter (through March 2, 2006) | $ | 15.86 | $ | 25.40 | ||||

As of February 13, 2006, there were approximately 36 holders of record of our common stock. The number of holders of record does not include holders whose securities are held in street name. On March 2, 2006, the last reported sale price of our common stock as reported by the American Stock Exchange was $18.43 per share.

19

Table of Contents

CAPITALIZATION

The following table sets forth our unaudited cash and capitalization as of December 31, 2005 on an actual basis and as adjusted basis to reflect our receipt of the estimated net proceeds from the sale of 2,468,000 shares of common stock, after deducting underwriting discounts and other estimated offering expenses, and the use of $5.0 million of such proceeds for the repayment of bank debt. You should read this table in conjunction with our consolidated financial statements included elsewhere in this prospectus.

| At December 31, 2005 | ||||||||||

| Actual | As Adjusted | |||||||||

| (unaudited) | ||||||||||

| (in thousands) | ||||||||||

| Cash and cash equivalents | $ | 3,271 | $ | 38,553 | ||||||

| Long-term debt, including current maturities: | ||||||||||

| Term notes payable to bank | $ | 24,905 | $ | 19,905 | ||||||

Revolving note payable to bank(1) | 300 | 300 | ||||||||

| Subordinated notes | 3,000 | 3,000 | ||||||||

| Total long-term debt | 28,205 | 23,205 | ||||||||

| Stockholders’ equity: | ||||||||||

| Preferred stock, $0.01 par value; 5,000 shares authorized | — | — | ||||||||

| Common stock, $0.01 par value; 30,000 shares authorized; 9,022 shares issued and outstanding, 11,490 shares issued and outstanding, as adjusted | 90 | 115 | ||||||||

| Additional paid-in capital | 34,667 | 74,924 | ||||||||

| Retained earnings | 10,933 | 10,933 | ||||||||

| Total stockholders’ equity | 45,690 | 85,972 | ||||||||

| Total capitalization | $ | 73,895 | $ | 109,177 | ||||||

| (1) | On January 5, 2006, we entered into a Sixth Amended and Restated Loan Agreement with our bank lender. Under this agreement, our revolving line of credit was renewed, the maturity was extended from January 1, 2006 to December 1, 2006, and the principal amount we are able to borrow under this revolving facility was increased from $2.0 million to $10.0 million, subject to borrowing base limitations. |

20

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains certain forward-looking statements, within the meaning of Section 27A of the Securities Act of 1933, and information pertaining to us, our industry and the oil and natural gas industry that is based on the beliefs of our management, as well as assumptions made by and information currently available to our management. All statements, other than statements of historical facts contained in this prospectus, including statements regarding our future financial position, growth strategy, budgets, projected costs, plans and objectives of management for future operations, are forward-looking statements. We use the words “may,” “will,” “expect,” “anticipate,” “estimate,” “believe,” “continue,” “intend,” “plan,” “budget” and other similar words to identify forward-looking statements. You should read statements that contain these words carefully and should not place undue reliance on these statements because they discuss future expectations, contain projections of results of operations or of our financial condition and/or state other “forward-looking” information. We do not undertake any obligation to update or revise publicly any forward-looking statements. Although we believe our expectations reflected in these forward-looking statements are based on reasonable assumptions, no assurance can be given that these expectations or assumptions will prove to have been correct. Important factors that could cause actual results to differ materially from the expectations reflected in the forward-looking statements include, but are not limited to, the following factors and the other factors described in this prospectus under the caption “Risk Factors”:

| • | conditions in the oil and natural gas industry, including the demand for natural gas and fluctuations in the prices of oil and natural gas; | |

| • | competition among the various providers of compression services and products; | |

| • | changes in safety, health and environmental regulations; | |

| • | changes in economic or political conditions in the markets in which we operate; | |

| • | failure of our customers to continue to rent equipment after expiration of the primary rental term; | |

| • | the inherent risks associated with our operations, such as equipment defects, malfunctions and natural disasters; | |

| • | our inability to comply with covenants in our debt agreements and the decreased financial flexibility associated with our substantial debt; | |

| • | future capital requirements and availability of financing; | |

| • | general economic conditions; | |

| • | events similar to September 11, 2001; and | |

| • | fluctuations in interest rates. |

We believe that it is important to communicate our expectations of future performance to our investors. However, events may occur in the future that we are unable to accurately predict or that we are unable to control. When considering our forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this prospectus.

21

Table of Contents

UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR

THE YEAR ENDED DECEMBER 31, 2005

The following unaudited consolidated financial statements as of and for the year ended December 31, 2005 have not been reviewed by our independent auditors, but have been prepared on a basis consistent with our historical audited consolidated financial statements, but omit all footnotes that normally accompany and are an integral part of the audited consolidated financial statements.

NATURAL GAS SERVICES GROUP, INC. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEET

(all amounts in thousands, except per-share amounts)

| December 31, | ||||||

| 2005 | ||||||

| ASSETS | ||||||

CURRENT ASSETS: | ||||||

| Cash and cash equivalents | $ | 3,271 | ||||

| Trade accounts receivable, net of doubtful accounts of $75 | 6,192 | |||||

| Inventory | 14,723 | |||||

| Prepaid expenses and other | 456 | |||||

| Total current assets | 24,642 | |||||

RENTAL EQUIPMENT,net of accumulated depreciation of $7,598 | 41,201 | |||||

PROPERTY AND EQUIPMENT,net of accumulated depreciation of $2,458 | 6,424 | |||||

GOODWILL,net of accumulated amortization of $325 | 10,039 | |||||

INTANGIBLES,net of accumulated amortization of $326 | 3,978 | |||||

OTHER ASSETS | 85 | |||||

| Total assets | $ | 86,369 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||

CURRENT LIABILITIES: | ||||||

| Current portion of long-term debt | $ | 5,680 | ||||

| Line of credit | 300 | |||||

| Accounts payable and accrued liabilities | 5,124 | |||||

| Deferred income | 103 | |||||

| Total current liabilities | 11,207 | |||||

LONG-TERM DEBT,less current portion | 20,225 | |||||

SUBORDINATED NOTES | 2,000 | |||||

DEFERRED TAX LIABILITY | 7,247 | |||||

COMMITMENTS | ||||||

STOCKHOLDERS’ EQUITY: | ||||||

| Common stock, 30,000 shares authorized, par value $0.01; 9,022 shares issued and outstanding | 90 | |||||

| Additional paid-in capital | 34,667 | |||||

| Retained earnings | 10,933 | |||||

| Total stockholders’ equity | $ | 45,690 | ||||

| Total liabilities and stockholders’ equity | $ | 86,369 | ||||

22

Table of Contents

NATURAL GAS SERVICES GROUP, INC. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENT OF INCOME

(all amounts in thousands, except per-share amounts)

| For the Year Ended | ||||||

| December 31, 2005 | ||||||

REVENUE: | ||||||

| Sales, net | $ | 30,278 | ||||

| Service and maintenance income | 2,424 | |||||

| Rental income | 16,609 | |||||

| Total revenue | 49,311 | |||||

OPERATING COSTS AND EXPENSES: | ||||||

| Cost of sales, exclusive of depreciation shown separately below | 23,331 | |||||

| Cost of service, exclusive of depreciation shown separately below | 1,479 | |||||

| Cost of rental, exclusive of depreciation shown separately below | 6,528 | |||||

| Selling expenses | 1,034 | |||||

| General and administrative | 3,856 | |||||

| Depreciation and amortization | 4,224 | |||||

| Total operating costs and expenses | 40,452 | |||||

OPERATING INCOME | 8,859 | |||||

OTHER INCOME (EXPENSE): | ||||||

| Interest expense | (1,997 | ) | ||||

| Other income (expense) | 199 | |||||

| Total other income (expense) | (1,798 | ) | ||||

INCOME BEFORE PROVISION FOR INCOME TAXES | 7,061 | |||||

PROVISION FOR INCOME TAXES: | ||||||

| Current | 207 | |||||

| Deferred | 2,408 | |||||

| Total income tax expense | 2,615 | |||||

NET INCOME | 4,446 | |||||

INCOME AVAILABLE TO COMMON STOCKHOLDERS | $ | 4,446 | ||||

EARNINGS PER COMMON SHARE: | ||||||

| Basic | $ | 0.59 | ||||

| Diluted | $ | 0.52 | ||||

WEIGHTED AVERAGE COMMON SHARES OUTSTANDING: | ||||||

| Basic | 7,564 | |||||

| Diluted | 8,481 | |||||

23

Table of Contents

NATURAL GAS SERVICES GROUP, INC. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENT OF CASH FLOWS

(all amounts in thousands)

| For the Year Ended | ||||||||

| December 31, 2005 | ||||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net income | $ | 4,446 | ||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Depreciation and amortization | 4,224 | |||||||

| Deferred taxes | 2,408 | |||||||

| Amortization of debt issuance costs | 49 | |||||||

| Employee stock option expense | 135 | |||||||

| Loss (gain) on disposal of assets | (28 | ) | ||||||

| Changes in current assets: | ||||||||

| Trade and other receivables | (1,352 | ) | ||||||

| Inventory | (5,699 | ) | ||||||

| Prepaid expenses and other | (362 | ) | ||||||

| Changes in current liabilities: | ||||||||

| Accounts payable and accrued liabilities | 524 | |||||||

| Deferred income | (855 | ) | ||||||

| Other assets | 299 | |||||||

| Net cash provided by operating activities | 3,789 | |||||||

CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchase of property and equipment | (17,708 | ) | ||||||

| Assets acquired, net of cash | (7,584 | ) | ||||||

| Proceeds from sale of property and equipment | 264 | |||||||

| Change in restricted cash | 2,000 | |||||||

| Net cash used in investing activities | (23,028 | ) | ||||||

CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Net proceeds from lines of credit | 300 | |||||||

| Proceeds from long-term debt | 21,517 | |||||||

| Repayments of long-term debt | (13,077 | ) | ||||||

| Proceeds from exercise of stock options and warrants, net of transaction costs | 13,085 | |||||||

| Net cash provided by financing activities | 21,825 | |||||||

NET CHANGE IN CASH | 2,586 | |||||||

CASH AT BEGINNING OF PERIOD | 685 | |||||||

CASH AT END OF PERIOD | $ | 3,271 | ||||||

24

Table of Contents

SELECTED HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

The following selected historical consolidated financial information for each of the years in the five-year period ended December 31, 2004, has been derived from our audited consolidated financial statements. The following selected historical consolidated financial information for the nine months ended September 30, 2004 and 2005 has been derived from our unaudited consolidated financial statements, and, in the opinion of our management, includes all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation. This information is only a summary and you should read it in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which discusses factors affecting the comparability of the information presented, and in conjunction with our consolidated financial statements and related notes included elsewhere in this prospectus. Results for interim periods may not be indicative of results for full fiscal years.

| Nine Months Ended | |||||||||||||||||||||||||||||

| Year Ended December 31, | September 30, | ||||||||||||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | 2005(1) | |||||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||||||||

| (in thousands, except per share amounts) | |||||||||||||||||||||||||||||

CONSOLIDATED STATEMENTS OF INCOME AND OTHER INFORMATION: | |||||||||||||||||||||||||||||

| Revenues | $ | 3,652 | $ | 8,762 | $ | 10,297 | $ | 12,750 | $ | 15,958 | $ | 11,220 | $ | 35,532 | |||||||||||||||

| Costs of revenue, exclusive of depreciation shown separately below | 1,535 | 4,942 | 5,572 | 6,057 | 6,951 | 4,903 | 22,661 | ||||||||||||||||||||||

| Gross profit | 2,117 | 3,820 | 4,725 | 6,693 | 9,007 | 6,317 | 12,871 | ||||||||||||||||||||||

| Depreciation and amortization | 356 | 901 | 1,166 | 1,726 | 2,444 | 1,751 | 3,026 | ||||||||||||||||||||||

| Other operating expenses | 1,238 | 1,720 | 1,718 | 2,292 | 2,652 | 1,998 | 3,600 | ||||||||||||||||||||||

| Operating income | 523 | 1,199 | 1,841 | 2,675 | 3,911 | 2,568 | 6,245 | ||||||||||||||||||||||

Total other income (expense)(2) | (159 | ) | (503 | ) | (471 | ) | (671 | ) | 603 | 916 | (1,388 | ) | |||||||||||||||||

| Income before income taxes | 364 | 696 | 1,370 | 2,004 | 4,514 | 3,484 | 4,857 | ||||||||||||||||||||||

| Income tax expense | 147 | 314 | 584 | 697 | 1,140 | 774 | 1,797 | ||||||||||||||||||||||

| Income before discontinued operations | 217 | 382 | 786 | 1,307 | 3,374 | 2,710 | 3,060 | ||||||||||||||||||||||

Discontinued operations(3) | 692 | — | — | — | — | — | — | ||||||||||||||||||||||

| Net income | 909 | 382 | 786 | 1,307 | 3,374 | 2,710 | 3,060 | ||||||||||||||||||||||

| Preferred dividends | — | 11 | 107 | 121 | 53 | 53 | — | ||||||||||||||||||||||