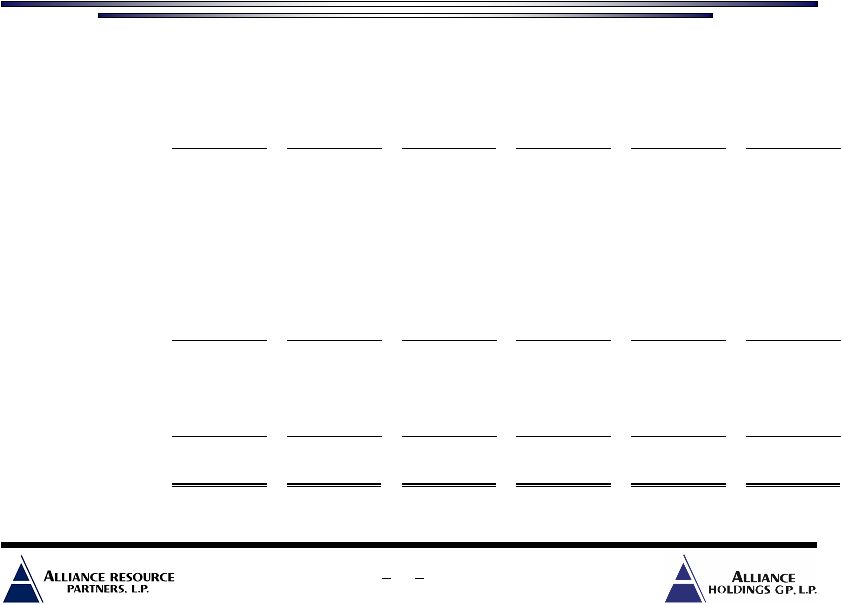

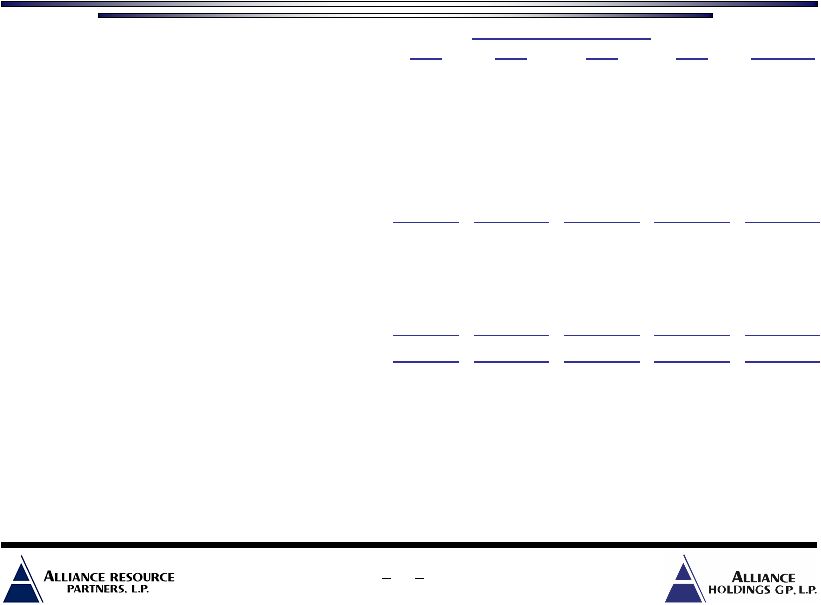

ARLP EBITDA Reconciliation EBITDA is defined as income before net interest expense, income taxes and depreciation, depletion and amortization. Management believes EBITDA is a useful indicator of its ability to meet debt service and capital expenditure requirements and uses EBITDA as a measure of operating performance. EBITDA should not be considered as an alternative to net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with generally accepted accounting principles. EBITDA is not intended to represent cash flow and does not represent the measure of cash available for distribution. The Partnership's method of computing EBITDA may not be the same method used to compute similar measures reported by other companies, or EBITDA may be computed differently by the Partnership in different contexts (i.e. public reporting versus computation under financing agreements). Estimate midpoint reflects the Partnership’s most recent guidance. 24 2006E 2002 2003 2004 2005 Midpoint Cash flows provided by operating activities 101,306 $ 110,312 $ 145,055 $ 193,618 $ 245,000 $ Reclamation and mine closing (1,365) (1,341) (1,622) (1,918) (2,000) Coal inventory adjustment to market (48) (687) (488) (573) - Other 1,014 353 (255) (2,057) (5,200) Net effect of changes in operating assets and liabilities (13,714) (8,240) (12,405) 26,577 400 Interest expense 16,360 15,981 14,963 11,816 9,500 Income taxes (1,094) 2,577 2,641 2,682 2,500 Minority interest income - - - - (200) EBITDA 102,459 $ 118,955 $ 147,889 $ 230,145 $ 250,000 $ Depreciation, depletion and amortization (52,408) (52,495) (53,664) (55,637) (73,200) Interest expense (16,360) (15,981) (14,963) (11,816) (9,500) Income taxes 1,094 (2,577) (2,641) (2,682) (2,500) Minority interest income - - - - 200 Net Income 34,785 $ 47,902 $ 76,621 $ 160,010 $ 165,000 $ Year Ended December 31, |