Exhibit 99.2

Caution regarding forward-looking statements

This document contains forward-looking statements within the meaning of the “safe harbour” provisions of Canadian provincial securities laws and the U.S. Private Securities Litigation Reform Act of 1995. The forward-looking statements in this document include, but are not limited to, statements with respect to our 2016 management objectives for core earnings and core ROE, our 2016 goal for pre-tax run rate savings related to our Efficiency and Effectiveness Initiative, statements with respect to the anticipated benefits and the completion of and timing for completion of the acquisition of New York Life’s retirement plan services business, and the benefits and costs of the acquisition of the Canadian-based operations of Standard Life plc, the anticipated effect of the acquisition on Manulife’s strategy, operations and financial performance, including its EPS, earnings capacity, capital and MCCSR ratio, dividends, financial leverage, 2016 management objectives for core earnings and Core ROE, products, services and capabilities, earnings contributions, cost savings and transition and integration costs, revenue synergies. . The forward-looking statements in this document also relate to, among other things, our objectives, goals, strategies, intentions, plans, beliefs, expectations and estimates, and can generally be identified by the use of words such as “may”, “will”, “could”, “should”, “would”, “likely”, “suspect”, “outlook”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “plan”, “forecast”, “objective”, “seek”, “aim”, “continue”, “goal”, “restore”, “embark” and “endeavour” (or the negative thereof) and words and expressions of similar import, and include statements concerning possible or assumed future results. Although we believe that the expectations reflected in such forward-looking statements are reasonable, such statements involve risks and uncertainties, and undue reliance should not be placed on such statements and they should not be interpreted as confirming market or analysts’ expectations in any way. Certain material factors or assumptions are applied in making forward-looking statements, including that: the acquisition of New York Life’s retirement plan services business will be completed in the first half of 2015; in respect of the acquisition of the Canadian-based operations of Standard Life plc, estimates for 2015 and 2016 EPS; estimated after-tax cost savings, including estimated savings as a result of synergies from areas such as information technology, real estate and personnel costs; estimated integration costs; revenue synergies increasing over time; and, in the case of our 2016 management objectives for core earnings and core ROE, the assumptions described under “Key Planning Assumptions and Uncertainties” in this document and actual results may differ materially from those expressed or implied in such statements. Important factors that could cause actual results to differ materially from expectations include but are not limited to: the factors identified in “Key Planning Assumptions and Uncertainties” in this document; general business and economic conditions (including but not limited to the performance, volatility and correlation of equity markets, interest rates, credit and swap spreads, currency rates, investment losses and defaults, market liquidity and creditworthiness of guarantors, reinsurers and counterparties); changes in laws and regulations; changes in accounting standards; our ability to execute strategic plans and changes to strategic plans; downgrades in our financial strength or credit ratings; our ability to maintain our reputation; impairments of goodwill or intangible assets or the establishment of provisions against future tax assets; the accuracy of estimates relating to morbidity, mortality and policyholder behaviour; the accuracy of other estimates used in applying accounting policies and actuarial methods; our ability to implement effective hedging strategies and unforeseen consequences arising from such strategies; our ability to source appropriate assets to back our long dated liabilities; level of competition and consolidation; our ability to market and distribute products through current and future distribution channels, including through our proposed collaboration arrangements with Standard Life plc; unforeseen liabilities or asset impairments arising from acquisitions and dispositions of businesses, including with respect to the acquisition of the retirement plan services business of New York Life and the Canadian-based operations of Standard Life plc; the realization of losses arising from the sale of investments classified as available-for-sale; our liquidity, including the availability of financing to satisfy existing financial liabilities on expected maturity dates when required; obligations to pledge additional collateral; the availability of letters of credit to provide capital management flexibility; accuracy of information received from counterparties and the ability of counterparties to meet their obligations; the availability, affordability and adequacy of reinsurance; legal and regulatory proceedings, including tax audits, tax litigation or similar proceedings; our ability to adapt products and services to the changing market; our ability to attract and retain key executives, employees and agents; the appropriate use and interpretation of complex models or deficiencies in models used; political, legal, operational and other risks associated with our non-North American operations; acquisitions and our ability to complete acquisitions including the availability of equity and debt financing for this purpose; the failure to realize some or all of the expected benefits of the acquisition of New York Life’s retirement plan services business and the Canadian-based operations of Standard Life plc; the disruption of or changes to key elements of the Company’s or public infrastructure systems; environmental concerns; and our ability to protect our intellectual property and exposure to claims of infringement. Additional information about material risk factors that could cause actual results to differ materially from expectations and about material factors or assumptions applied in making forward-looking statements may be found in the body of this document as well as under “Risk Management and Risk Factors” and “Critical Accounting and Actuarial Policies” in the Management’s Discussion and Analysis and in the “Risk Management” note to the consolidated financial statements as well as under “Risk Factors” in our most recent Annual Information Form and elsewhere in our filings with Canadian and U.S. securities regulators. We do not undertake to update any forward-looking statements, except as required by law.

| | | | |

| 1 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

2014 Manulife Financial Corporation

Management’s Discussion and Analysis

TABLE OF CONTENTS

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 2 |

Management’s Discussion and Analysis

This Management’s Discussion and Analysis (“MD&A”) is current as of February 19, 2015.

Overview

Manulife is a leading Canada-based financial services company with principal operations in Asia, Canada and the United States. Manulife’s vision is to be the most professional financial services organization in the world, providing strong, reliable, trustworthy and forward-thinking solutions for our clients’ big significant financial decisions. Our international network of more than 87,000 employees and agents offers our clients a broad range of financial protection and wealth management products and services. We offer personal and corporate products to millions of customers across our three operating divisions: Asia, Canada and the United States.

Assets under management1 by Manulife and its subsidiaries were $691 billion as at December 31, 2014.

Manulife’s net income attributed to shareholders was $3.5 billion in 2014 compared with $3.1 billion in 2013. Net income attributed to shareholders is comprised of core earnings1 (consisting of items we believe reflect the underlying earnings capacity of the business), which amounted to $2.9 billion in 2014 compared with $2.6 billion in 2013, and items excluded from core earnings, of $0.6 billion in 2014 compared with $0.5 billion in 2013. Net income per common share for 2014 was $1.82, compared with $1.63 in 2013. Return on common shareholders’ equity for 2014 was 11.9%, compared with 12.8% for 2013.

In 2014, we delivered strong growth in both net income and core earnings, announced two important acquisitions, and increased our dividend 19%. Our strategy is delivering results and this year continued a trend of improvement over the last five years. While the current macro environment, including low interest rates, produced headwinds, our results for 2014 were essentially on plan and show that we continue to make progress toward our financial goals.

In 2014, we established strong momentum in our life insurance sales and achieved our 25th consecutive quarter of record assets under management. Our business growth will be supplemented by the strategic acquisitions of the Canadian-based operations of Standard Life plc and, subject to receipt of regulatory approvals, New York Life’s pension business. Despite the global economy continuing to face serious headwinds, our forward-thinking approach to our business will continue to help us in 2015 and beyond.

Insurance sales1 were $2.5 billion in 2014, a decline of 10%2 compared with 2013 largely due to a decrease in Group Benefits sales reflecting our disciplined approach to pricing in the very competitive market. Excluding Group Benefits, insurance sales increased 13% compared with the prior year. In Asia, we achieved record insurance sales on a constant currency basis, up 31% over 2013, driven by continued momentum in corporate products in Japan, successful sales campaigns and product launches in Hong Kong, and double digit sales growth in our Asia Other businesses. In Canada, retail insurance sales grew reflecting the successful launch of a simplified universal life solution. In the U.S., insurance sales increased sequentially in each quarter of the year, but decreased compared with 2013 amid a sluggish estate planning market.

Wealth sales1 were a record $52.6 billion in 2014, a 1% increase from the previous record reported in 2013. Excluding new bank loan volumes (which we include in wealth sales), wealth sales increased 3% over the prior year, with solid contributions from all three geographies. In Asia, we achieved record wealth sales on a constant currency basis that trended upward throughout the year as a result of new product launches, marketing campaigns, and improved market sentiment. In Canada, wealth sales excluding new bank loan volumes increased, led by our second highest annual group retirement sales on record. In the U.S., mutual fund sales continued to be strong and outpaced the industry3, outweighing the negative impact of intensified competitive pressures in the group retirement market.

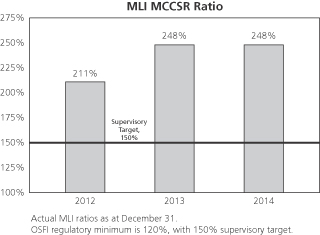

The Minimum Continuing Capital and Surplus Requirements (“MCCSR”) ratio for The Manufacturers Life Insurance Company (“MLI”) was 248% at the end of 2014, the same ratio as at December 31, 2013. MFC’s financial leverage ratio was 27.8% at December 31, 2014 compared with 31.0% at the end of 2013.

Strategic Direction

In 2014, we made significant progress towards our strategic priorities:

| n | | Developing our Asian opportunity to the fullest – Achieved record insurance sales on a constant currency basis with new product launches and channel expansion accelerating our growth, notably in Japan (+60%), China (+28%) and Hong Kong (+15%); delivered record wealth sales in line with the levels set in 2013; strengthened our bancassurance footprint by entering into nine new insurance distribution agreements, two of which are exclusive. |

| n | | Growing our wealth and asset management businesses around the world – Achieved our 25th consecutive quarter of record assets under management; delivered record institutional sales at Manulife Asset Management across a broad variety of mandates, including $1.1 billion in mandates from our Private Markets business in its inaugural year; generated over $18 billion of net flows into our asset management and group retirement businesses. |

| 1 | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| 2 | Growth (declines) in sales, premiums and deposits and assets under management are stated on a constant currency basis. Constant currency basis is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| 3 | Strategic Insight: ICI Confidential. Direct Sold mutual funds, fund-of-funds and ETF’s are excluded. Organic sales growth rate is calculated as: net new flows divided by beginning period assets. Industry data through December 2014. |

| | | | |

| 3 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

| n | | Building on our balanced Canadian business – Announced the acquisition of the Canadian-based operations of Standard Life plc, which closed on January 30, 2015; delivered solid Group Retirement Solutions and mutual fund sales; generated Retail Insurance sales growth, driven by the successful launch of a simplified universal life product; reported lower lending volumes at Manulife Bank and a decline in Group Benefits sales amid competitive pressures. |

| n | | Continuing to drive sustainable earnings and opportunistic growth in the U.S. – Announced our agreement to acquire New York Life’s Retirement Plan Services (“RPS”) business; delivered record wealth sales with strong mutual fund volumes outweighing the negative impact of intensified competitive pressures in the RPS market; continued to build momentum in insurance sales over the course of the year, driven by product changes. |

Our strategy builds on these priorities and will set the course for attaining our vision of “helping people with their significant financial decisions”.

The first theme of our strategy is to develop more holistic and long-lasting customer relationships. Our strategy is to:

| n | | Build a 360-degree view of our customer to engage them in more personalized and thoughtful sales conversations. |

| n | | Deliver a simpler, more customer needs-focused experience. |

| n | | Equip our distributors with tools that enable them to effectively meet a broader range of customer needs. |

| n | | And where appropriate, grow the channels where we have more control of the end-to-end customer experience and where a broader range of customer needs can be met. This includes growing direct channels and advice channels that can be accessed anytime, anywhere. |

Our second theme is to continue to build and integrate our global wealth and asset management businesses in existing markets, as well as expand our investment and sales offices into new markets in order to meet the needs of our customers, from individual investors to institutions such as pension funds and sovereign wealth funds. The need for wealth and asset management services is growing around the world, including locations where we do not currently have operations, and the opportunity for asset managers to add value also exists in those locations. We will not restrict ourselves to geographies where we currently have, or expect to have, insurance operations.

Our third theme is to leverage skills and experience across our international operations. If we are going to get maximum advantage from the investments we are making, we need to amortize our investment across our global organization.

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 4 |

Financial Performance

| | | | | | | | | | | | | | |

As at and for the years ended December 31, (C$ millions, unless otherwise stated) | | 2014 | | | 2013 | | | 2012 | | | |

Net income attributed to shareholders | | $ | 3,501 | | | $ | 3,130 | | | $ | 1,810 | | | |

Preferred share dividends | | | (126 | ) | | | (131 | ) | | | (112 | ) | | |

Common shareholders’ net income | | $ | 3,375 | | | $ | 2,999 | | | $ | 1,698 | | | |

Reconciliation of core earnings to net income attributed to shareholders: | | | | | | | | | | | | | | |

Core earnings(1) | | $ | 2,888 | | | $ | 2,617 | | | $ | 2,249 | | | |

Investment-related experience in excess of amounts included in core earnings | | | 359 | | | | 706 | | | | 949 | | | |

Core earnings and investment-related experience in excess of amounts included in core earnings | | $ | 3,247 | | | $ | 3,323 | | | $ | 3,198 | | | |

Other items to reconcile core earnings to net income attributed to shareholders: | | | | | | | | | | | | | | |

Direct impact of equity markets and interest rates and variable annuity guarantee liabilities | | | 412 | | | | (336 | ) | | | (582 | ) | | |

Changes in actuarial methods and assumptions | | | (198 | ) | | | (489 | ) | | | (1,081 | ) | | |

Disposition of Taiwan insurance business(2) | | | 12 | | | | 350 | | | | (50 | ) | | |

Other items | | | 28 | | | | 282 | | | | 325 | | | |

Net income attributed to shareholders | | $ | 3,501 | | | $ | 3,130 | | | $ | 1,810 | | | |

Basic earnings per common share (C$) | | $ | 1.82 | | | $ | 1.63 | | | $ | 0.94 | | | |

Diluted earnings per common share (C$) | | $ | 1.80 | | | $ | 1.62 | | | $ | 0.92 | | | |

Diluted core earnings per common share (C$)(1) | | $ | 1.48 | | | $ | 1.34 | | | $ | 1.15 | | | |

Return on common shareholders’ equity (“ROE”) (%) | | | 11.9% | | | | 12.8% | | | | 7.8% | | | |

Core ROE (%)(1) | | | 9.8% | | | | 10.6% | | | | 9.8% | | | |

Sales(1) | | | | | | | | | | | | | | |

Insurance products(3) | | $ | 2,544 | | | $ | 2,757 | | | $ | 3,279 | | | |

Wealth products | | $ | 52,604 | | | $ | 49,681 | | | $ | 35,940 | | | |

Premiums and deposits(1) | | | | | | | | | | | | | | |

Insurance products | | $ | 25,015 | | | $ | 24,549 | | | $ | 24,221 | | | |

Wealth products | | $ | 72,986 | | | $ | 63,701 | | | $ | 51,280 | | | |

Assets under management (C$ billions)(1) | | $ | 691 | | | $ | 599 | | | $ | 531 | | | |

Capital (C$ billions)(1) | | $ | 39.6 | | | $ | 33.5 | | | $ | 29.2 | | | |

MLI’s MCCSR ratio | �� | | 248% | | | | 248% | | | | 211% | | | |

| (1) | This item is a non-GAAP measure. For a discussion of our use of non-GAAP measures, see “Performance and Non-GAAP Measures” below. |

| (2) | The $12 million amount in 2014 relates primarily to closing adjustments to the 2013 disposition of our Taiwan insurance business sale and the $50 million charge in 2012 represents closing adjustments to the 2011 disposition of our Life Retrocession business. |

| (3) | Insurance sales have been adjusted to exclude Taiwan for all periods due to the sale of our Taiwan insurance business at the end of 2013. |

Analysis of Net Income

Manulife’s full year 2014 net income attributed to shareholders was $3.5 billion compared with $3.1 billion for full year 2013. Net income attributed to shareholders is comprised of core earnings (consisting of items we believe reflect the underlying earnings capacity of the business), which amounted to $2.9 billion in 2014 compared with $2.6 billion in 2013, and items excluded from core earnings, which amounted to $0.6 billion in 2014 compared with $0.5 billion in 2013.

The $271 million increase in core earnings compared with 2013 was due to higher fee income on higher asset levels in our wealth management businesses, lower net hedging costs and the favourable impact of a stronger U.S. dollar, partially offset by unfavourable policyholder experience in the U.S. On a divisional basis, Asia core earnings increased 16% over the prior year after adjusting for increased dynamic hedging costs (there is a corresponding decrease in macro hedging costs in the Corporate and Other segment), changes in currency rates and the sale of our Taiwan insurance business at the end of 2013. Core earnings increased by 2% over the prior year in Canada and declined by 15% in the U.S. primarily due to the second order impact of market factors along with risk management activities and unfavourable policyholder experience. The second order impact of market factors included the unfavourable impact that declines in the yield curve and corporate spreads had on the release of provisions for adverse deviation in the insurance business and the impact that higher equity markets and risk management activities had on releases of margins in the variable annuity business. The first order impact of market factors is included in the direct impact of equity markets and interest rates and is excluded from core earnings.

The $100 million year-over-year increase in items excluded from core earnings was primarily due to a $291 million reduction in charges related to changes in actuarial methods and assumptions and a $748 million increase from the direct impact of equity markets and interest rates and variable annuity guarantee liabilities, partially offset by one-time items in 2013 and lower investment-related experience in 2014. In addition, while investment-related experience was strong in both years, the $359 million gain reported in 2014 (in excess of the $200 million of investment gains included in core earnings) was $347 million lower than in 2013.

The investment-related experience gains are a combination of reported investment experience as well as the impact of investing activities on the measurement of our policy liabilities. Investment-related experience gains in 2014 of $559 million (2013 – $906 million), including the $200 million reported in core earnings, were composed of: $667 million (2013 – $571 million) primarily related to the impact of investing activities (both fixed income and alternative long-duration assets) on the measurement of our policy liabilities; and $103 million (2013 – $162 million) due to favourable credit experience relative to our long-term assumptions, partly offset by the $211 million (2013 – $55 million) impact of fair value related losses on alternative long-duration assets.

| | | | |

| 5 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

Investment-related experience gains in 2013 also included $228 million related to asset allocation activities that enhanced surplus liquidity and resulted in higher yielding assets in the respective liability segments.

The table below reconciles 2014 net income attributed to shareholders of $3,501 million to core earnings of $2,888 million.

| | | | | | | | | | | | | | |

For the years ended December 31, (C$ millions, unaudited) | | 2014 | | | 2013 | | | 2012 | | | |

Core earnings(1) | | | | | | | | | | | | | | |

Asia Division(2) | | $ | 1,008 | | | $ | 921 | | | $ | 963 | | | |

Canadian Division(2) | | | 927 | | | | 905 | | | | 835 | | | |

U.S. Division(2) | | | 1,383 | | | | 1,510 | | | | 1,085 | | | |

Corporate and Other (excluding expected cost of macro hedges and core investment gains) | | | (446 | ) | | | (506 | ) | | | (345 | ) | | |

Expected cost of macro hedges(2),(3) | | | (184 | ) | | | (413 | ) | | | (489 | ) | | |

Investment-related experience in core earnings(4) | | | 200 | | | | 200 | | | | 200 | | | |

Total core earnings | | $ | 2,888 | | | $ | 2,617 | | | $ | 2,249 | | | |

Investment-related experience in excess of amounts included in core earnings(4) | | | 359 | | | | 706 | | | | 949 | | | |

Core earnings and investment-related experience in excess of amounts included in core earnings | | $ | 3,247 | | | $ | 3,323 | | | $ | 3,198 | | | |

Changes in actuarial methods and assumptions(5) | | | (198 | ) | | | (489 | ) | | | (1,081 | ) | | |

Direct impact of equity markets and interest rates and variable annuity guarantee liabilities(6) (see table below) | | | 412 | | | | (336 | ) | | | (582 | ) | | |

Disposition of Taiwan insurance business in 2013(7) | | | 12 | | | | 350 | | | | (50 | ) | | |

Impact of in-force product changes and recapture of reinsurance treaties(8) | | | 24 | | | | 261 | | | | 260 | | | |

Material and exceptional tax related items(9) | | | 4 | | | | 47 | | | | 322 | | | |

Goodwill impairment charge | | | – | | | | – | | | | (200 | ) | | |

Restructuring charge related to organizational design(10) | | | – | | | | (26 | ) | | | (57 | ) | | |

Net income attributed to shareholders | | $ | 3,501 | | | $ | 3,130 | | | $ | 1,810 | | | |

| (1) | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| (2) | The decrease in expected cost of macro hedges in 2014 compared with 2013 was partially offset by an increase in dynamic hedging costs included in Asia, Canada and U.S. core earnings. |

| (3) | The 2014 net loss from macro equity hedges was $304 million and consisted of a $184 million charge related to the estimated expected cost of the macro equity hedges relative to our long-term valuation assumptions and a $120 million charge because actual markets outperformed our valuation assumptions (included in the direct impact of equity markets and interest rates and variable annuity guarantee liabilities below). |

| (4) | As outlined under “Critical Accounting and Actuarial Policies” below, net insurance contract liabilities under IFRS for Canadian insurers are determined using the Canadian Asset Liability Method (“CALM”). Under CALM, the measurement of policy liabilities includes estimates regarding future expected investment income on assets supporting the policies. Experience gains and losses are reported when current period activity differs from what was assumed in the policy liabilities at the beginning of the period. These gains and losses can relate to both the investment returns earned in the period, as well as to the change in our policy liabilities driven by the impact of current period investing activities on future expected investment income assumptions. The direct impact of interest rates and equity markets is reported separately. The inclusion of up to $200 million per annum of favourable investment experience will be increasing to $400 million per annum commencing 1Q15. See “Performance and Non-GAAP Measures” below for more information. |

| (5) | Of the $198 million charge for change in actuarial methods and assumptions in 2014, $69 million was reported in the third quarter as part of the comprehensive annual review of valuation assumptions. Over the full year, charges due to lapse assumption changes, and updates to actuarial standards related to segregated fund bond calibration criteria, were partially offset by benefits due to refinements related to the projection of asset and liability cash flows, including an in depth review of the modelling of future tax cash flows for our U.S. Insurance business, updates to mortality and morbidity assumptions, and updates to actuarial standards related to economic reinvestment assumptions. |

| (6) | The direct impact of equity markets and interest rates is relative to our policy liability valuation assumptions and includes changes to interest rate assumptions, as well as experience gains and losses on derivatives associated with our macro equity hedges. We also include gains and losses on the sale of available-for-sale (“AFS”) debt securities as management may have the ability to partially offset the direct impacts of changes in interest rates reported in the liability segments. See table below for components of this item. |

| (7) | The $12 million amount in 2014 relates primarily to closing adjustments to the 2013 disposition of our Taiwan insurance business sale and the $50 million charge in 2012 represents closing adjustments to the Life Retrocession sale in 2011. |

| (8) | The 2014 amount relates to the recapture of a reinsurance treaty in Canada. The 2013 gain of $261 million includes the impact on the measurement of policy liabilities of policyholder-approved changes to the investment objectives of separate accounts that support our Variable Annuity products in the U.S. and a reinsurance recapture transaction in Asia. The $260 million gain in 2012 largely relates to a recapture of a reinsurance treaty and in-force segregated funds product changes in Canada. |

| (9) | The $4 million gain in 2014 relates to tax rate changes in Asia. The 2013 tax item primarily reflects the impact on our deferred tax asset position of Canadian provincial tax rate changes. Included in the 2012 tax items are $264 million of material and exceptional U.S. tax items and $58 million for changes to tax rates in Japan. |

| (10) | The restructuring charge is related to severance, pension and consulting costs for the Company’s Organizational Design Project, which was completed in the second quarter of 2013. |

The net gain (loss) related to the direct impact of equity markets and interest rates and variable annuity guarantee liabilities in the table above is attributable to:

| | | | | | | | | | | | | | |

For the years ended December 31, (C$ millions, unaudited) | | 2014 | | | 2013 | | | 2012 | | | |

Direct impact of equity markets and variable annuity guarantee liabilities(1) | | $ | (182 | ) | | $ | 458 | | | $ | 851 | | | |

Fixed income reinvestment rates assumed in the valuation of policy liabilities(2) | | | 729 | | | | (276 | ) | | | (740 | ) | | |

Sale of AFS bonds and derivative positions in the Corporate and Other segment | | | (40 | ) | | | (262 | ) | | | (16 | ) | | |

Charges due to lower fixed income ultimate reinvestment rate (“URR”) assumptions used in the valuation of policy liabilities(3) | | | (95 | ) | | | (256 | ) | | | (677 | ) | | |

Direct impact of equity markets and interest rates and variable annuity guarantee liabilities | | $ | 412 | | | $ | (336 | ) | | $ | (582 | ) | | |

| (1) | In 2014, gross equity exposure losses of $2,179 million and gross equity hedging charges of $120 million from macro hedge experience were partially offset by gains of $2,117 million from dynamic hedging experience which resulted in a loss of $182 million. |

| (2) | The gain in 2014 for fixed income reinvestment assumptions was driven by the favourable impact on the measurement of policy liabilities of changes in yield curves primarily in the U.S. and Canada. |

| (3) | The periodic URR charges have ceased effective 4Q14 due to revisions to the Canadian Actuarial Standards of Practice related to economic reinvestment assumptions. |

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 6 |

Earnings per Common Share and Return on Common Shareholders’ Equity

Net income per common share for 2014 was $1.82, compared with $1.63 in 2013. Return on common shareholders’ equity for 2014 was 11.9%, compared with 12.8% for 2013.

Revenue

Revenues include (i) premiums received on life and health insurance policies and fixed annuity products, net of premiums ceded to reinsurers; (ii) investment income comprised of income earned on general fund assets, credit experience and realized gains and losses on assets held in the Corporate segment; (iii) fee and other income received for services provided; and, (iv) realized and unrealized gains (losses) on assets supporting insurance and investment contract liabilities and on macro hedging program. Premium and deposit equivalents from administrative services only (“ASO”), as well as deposits received by the Company on investment contracts such as segregated funds, mutual funds and managed funds are not included in revenue; however, the Company does receive fee income from these products, which is included in revenue. These fee generating deposits and ASO premium and deposit equivalents are an important part of our business and as a result, revenue does not fully represent sales and other activity taking place during the respective periods. The premiums and deposits metric below includes these factors.

For 2014, revenue before realized and unrealized gains (losses) was $37.4 billion, an increase of 5% over 2013, after adjusting for the one-time gain on the sale of our Taiwan insurance business in 4Q13. The increase was driven by higher fee income due to higher asset levels in our wealth management businesses and the strengthening of the U.S. dollar. Net premium income on a constant currency basis increased in Asia by 12%, but declined in Canada and the U.S. by 2% and 13%, respectively.

Net unrealized and realized gains (losses) on assets supporting insurance and investment contract liabilities and on our macro hedging program primarily related to the impact of movements in interest rates on the fair value of our bond and fixed income derivative holdings. In 2014, the general decrease in interest rates resulted in an increase in revenue while in 2013 the increase in interest rates resulted in a decrease in revenue.

See “Financial Performance – Impact of Fair Value Accounting” below.

Revenue

| | | | | | | | | | | | | | |

For the years ended December 31, (C$ millions, unaudited) | | 2014 | | | 2013 | | | 2012 | | | |

Gross premiums | | $ | 25,226 | | | $ | 24,892 | | | $ | 24,617 | | | |

Ceded premiums | | | (7,343 | ) | | | (7,382 | ) | | | (7,194 | ) | | |

Net premium income prior to fixed deferred annuity coinsurance | | $ | 17,883 | | | $ | 17,510 | | | $ | 17,423 | | | |

Premiums ceded relating to fixed deferred annuity coinsurance | | | – | | | | – | | | | (7,229 | ) | | |

Investment income | | | 10,808 | | | | 9,860 | | | | 9,802 | | | |

Other revenue(1) | | | 8,739 | | | | 8,876 | | | | 7,289 | | | |

Total revenue before net realized and unrealized gains (losses) on assets supporting insurance and investment contract liabilities and on macro hedging program | | $ | 37,430 | | | $ | 36,246 | | | $ | 27,285 | | | |

Realized and unrealized gains (losses) on assets supporting insurance and investment contract liabilities and on macro hedging program | | | 17,092 | | | | (17,607 | ) | | | 1,825 | | | |

Total revenue | | $ | 54,522 | | | $ | 18,639 | | | $ | 29,110 | | | |

| (1) | Other revenue in 2013 includes a pre-tax gain of $479 million on the sale of our Taiwan insurance business. |

Premiums and Deposits

Premiums and deposits4 is an alternate measure of our top line growth, as it includes all new policyholder cash flows and, unlike total revenue, is not impacted by the volatility created by fair value accounting. Premiums and deposits for insurance products were $25.0 billion in 2014, down 1% on a constant currency basis compared with 2013. Premiums and deposits for wealth products were $73.0 billion in 2013, an increase of 9% on a constant currency basis over 2013.

Assets under Management

Assets under management4 as at December 31, 2014 were a record $691 billion, an increase of $92 billion, or 9% on a constant currency basis, compared with December 31, 2013. The increase was largely attributable to growth in our asset management business, favourable equity markets, and the fair value accounting impact of the reduction in interest rates on fixed income investments.

Assets under Management

| | | | | | | | | | | | | | |

As at December 31, (C$ millions) | | 2014 | | | 2013 | | | 2012 | | | |

General fund | | $ | 269,310 | | | $ | 232,709 | | | $ | 227,932 | | | |

Segregated funds net assets(1) | | | 256,532 | | | | 239,871 | | | | 209,197 | | | |

Mutual funds, institutional advisory accounts and other(1),(2) | | | 165,287 | | | | 126,353 | | | | 94,029 | | | |

Total assets under management | | $ | 691,129 | | | $ | 598,933 | | | $ | 531,158 | | | |

| (1) | Segregated funds net assets, mutual fund assets and other funds are not available to satisfy the liabilities of the Company’s general fund. |

| (2) | Other funds represent pension funds, pooled funds, endowment funds and other institutional funds managed by the Company on behalf of others. |

| 4 | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| | | | |

| 7 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

Capital

Total capital5 was $39.6 billion as at December 31, 2014 compared with $33.5 billion as at December 31, 2013, an increase of $6.1 billion. The increase included net income of $3.5 billion, currency impacts of $1.9 billion and net capital issued of $1.0 billion (excludes $1.0 billion redemption of senior debt of MFC as it is not included in the definition we use for capital), partially offset by cash dividends of $0.9 billion over the period.

The Minimum Continuing Capital and Surplus Requirements (“MCCSR”) ratio for The Manufacturers Life Insurance Company (“MLI”) was 248% at the end of 2014, consistent with the ratio at the end of 2013. MFC’s financial leverage ratio was 27.8% at December 31, 2014 compared with 31.0% at the end of 2013.

During 2014, we raised $1.8 billion of new financing and $1.8 billion matured or was redeemed, including $1.0 billion of senior debt.

We also issued $2.26 billion of subscription receipts that were exchanged for common shares after year end, as a result of the closing of the acquisition of the Canadian-based operations of Standard Life plc on January 30, 2015. On a pro-forma basis, had the transaction closed on December 31, 2014, the MCCSR ratio would be in the range of 235% to 240% and the financial leverage ratio would have been approximately 27.1%. The impact on the MCCSR ratio will be partially offset by the favourable impact of change in the MCCSR guidelines effective January 1, 2015.

Impact of Fair Value Accounting

Fair value accounting policies affect the measurement of both our assets and our liabilities. The difference between the reported amounts of our assets and liabilities determined as of the balance sheet date and the immediately preceding balance sheet date in accordance with the applicable mark-to-market accounting principles is reported as investment-related experience and the direct impact of equity markets and interest rates and variable annuity guarantees that are dynamically hedged, each of which impacts net income (see “Analysis of Net Income” above).

We reported $17.1 billion of net realized and unrealized gains in investment income in 2014. These amounts were driven by the mark-to-market impact of the decrease in interest rates on our bond and fixed income derivative holdings and the increase in equity markets on our equity futures in our macro and dynamic hedging program, as well as other items.

As outlined under “Critical Accounting and Actuarial Policies” below, net insurance contract liabilities under IFRS are determined using the Canadian Asset Liability Method (“CALM”), as required by the Canadian Institute of Actuaries. The measurement of policy liabilities includes the estimated value of future policyholder benefits and settlement obligations to be paid over the term remaining on in-force policies, including the costs of servicing the policies, reduced by the future expected policy revenues and future expected investment income on assets supporting the policies. Investment returns are projected using the current asset portfolios and projected reinvestment strategies. Experience gains and losses are reported when current period activity differs from what was assumed in the policy liabilities at the beginning of the period. We classify gains and losses by assumption type. For example, current period investing activities that increase (decrease) the future expected investment income on assets supporting the policies will result in an investment-related experience gain (loss).

Public Equity Risk and Interest Rate Risk

At December 31, 2014, the impact of a 10% decline in equity markets was estimated to be a charge of $480 million and the impact of a 50 basis point decline in interest rates on our earnings was estimated to be a charge of $100 million. See “Risk Management and Risk Factors” below.

Impact of Foreign Exchange Rates

We have operations in many markets worldwide, including Canada, the United States and various countries in Asia, and generate revenues and incur expenses in local currencies in these jurisdictions, which are translated to Canadian dollars. The bulk of our exposure to movements in foreign exchange rates is to the U.S. dollar.

Items impacting our Consolidated Statements of Income are translated to Canadian dollars using average exchange rates for the respective period. For items impacting our Consolidated Statements of Financial Position, period end rates are used for currency translation purpose. The following table provides the most relevant foreign exchange rates for 2014 and 2013.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Exchange rate | | Quarterly | | | | | Full Year |

| | 4Q14 | | | 3Q14 | | | 2Q14 | | | 1Q14 | | | 4Q13 | | | | | 2014 | | | 2013 | | | |

Average(1) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. dollar | | | 1.1356 | | | | 1.0890 | | | | 1.0905 | | | | 1.1031 | | | | 1.0494 | | | | | | 1.1046 | | | | 1.0298 | | | |

Japanese yen | | | 0.0099 | | | | 0.0105 | | | | 0.0107 | | | | 0.0107 | | | | 0.0105 | | | | | | 0.0105 | | | | 0.0106 | | | |

Hong Kong dollar | | | 0.1464 | | | | 0.1405 | | | | 0.1407 | | | | 0.1422 | | | | 0.1353 | | | | | | 0.1425 | | | | 0.1328 | | | |

Period end | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. dollar | | | 1.1601 | | | | 1.1208 | | | | 1.0676 | | | | 1.1053 | | | | 1.0636 | | | | | | 1.1601 | | | | 1.0636 | | | |

Japanese yen | | | 0.0097 | | | | 0.0102 | | | | 0.0105 | | | | 0.0107 | | | | 0.0101 | | | | | | 0.0097 | | | | 0.0101 | | | |

Hong Kong dollar | | | 0.1496 | | | | 0.1443 | | | | 0.1378 | | | | 0.1425 | | | | 0.1372 | | | | | | 0.1496 | | | | 0.1372 | | | |

| (1) | Average rates for the quarter are from Bank of Canada which are applied against Consolidated Statements of Income items for each period. Average rate for the full year is a 4 point average of the quarterly average rates. |

In general, our net income benefits from a weakening Canadian dollar and is adversely affected by a strengthening Canadian dollar as net income from the Company’s foreign operations are translated to Canadian dollars. However, in a period of losses, the weakening

| 5 | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 8 |

of the Canadian dollar has the effect of increasing the losses. The relative impact of foreign exchange in any given period is driven by the movement of currency rates as well as the proportion of earnings generated in our foreign operations.

Changes in foreign exchange rates, primarily due to the strengthening of the U.S. dollar compared to the Canadian dollar, increased core earnings by $129 million in 2014 compared with 2013. The impact of foreign currency on items excluded from core earnings is not relevant given the nature of these items.

Fourth Quarter Financial Highlights

| | | | | | | | | | | | | | |

For the quarters ended December 31, (C$ millions, except per share amounts) | | 2014 | | | 2013 | | | 2012 | | | |

Net income attributed to shareholders | | $ | 640 | | | $ | 1,297 | | | $ | 1,077 | | | |

Core earnings(1),(2)(see next page for reconciliation) | | $ | 713 | | | $ | 685 | | | $ | 554 | | | |

Diluted earnings per common share (C$) | | $ | 0.33 | | | $ | 0.68 | | | $ | 0.57 | | | |

Diluted core earnings per common share (C$)(2) | | $ | 0.36 | | | $ | 0.35 | | | $ | 0.28 | | | |

Return on common shareholders’ equity (annualized) | | | 8.1% | | | | 20.2% | | | | 19.2% | | | |

Sales(2) | | | | | | | | | | | | | | |

Insurance products(3) | | $ | 760 | | | $ | 617 | | | $ | 922 | | | |

Wealth products | | $ | 13,762 | | | $ | 12,241 | | | $ | 10,439 | | | |

Premiums and deposits(2) | | | | | | | | | | | | | | |

Insurance products | | $ | 6,649 | | | $ | 6,169 | | | $ | 6,629 | | | |

Wealth products | | $ | 18,863 | | | $ | 15,367 | | | $ | 17,499 | | | |

| (1) | Impact of currency movement on 4Q14 versus 4Q13 was $35 million. |

| (2) | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| (3) | Insurance sales have been adjusted to exclude Taiwan for all periods due to the sale of our Taiwan insurance business at the end of 2013. |

Manulife’s 4Q14 net income attributed to shareholderswas $640 million compared with $1,297 million in 4Q13. Net income attributed to shareholders is comprised of core earnings which amounted to $713 million in 4Q14 compared with $685 million in 4Q13, and items excluded from core earnings, which netted to a loss of $73 million in 4Q14 compared with a net gain of $612 million in 4Q13.

The $28 million increase in core earnings compared with 4Q13 was the result of higher fee income due to higher asset levels in our wealth management businesses, increases in new business volumes, lower expenses and the strengthening of the U.S. dollar, partially offset by policyholder experience losses in North America. On a divisional basis, Asia core earnings increased 19% compared with 4Q13, after adjusting for increased dynamic hedging costs (there is a corresponding decrease in macro hedging costs in the Corporate and Other segment), changes in currency rates and the sale of our Taiwan insurance business at the end of 2013. Canadian core earnings decreased 4% and U.S. core earnings decreased 15%, both divisions reported policyholder experience losses in 4Q14.

With respect to items excluded from 4Q14 core earnings, fair value losses related to impact of the sharp decline in oil prices on investments held in Canada and the U.S. were mostly offset by the favourable impact on the measurement of policy liabilities of changes in yield curves as investment-related experience losses were $353 million (of which gains of $50 million were included in core earnings and $403 million of losses were excluded from core earnings) and gains related to the direct impact of interest rates and equity markets were $377 million. Charges related to actuarial methods and assumptions and policy changes netted to $59 million and included a net gain of $65 million from the implementation of the Canadian Actuarial Standards Board’s revisions to the Actuarial Standards of Practice related to economic reinvestment assumptions. A gain from changes to fixed income reinvestment assumptions (an allowance for the use of credit spread assets for all durations, a change from deterministic to stochastically generated scenarios for most North American businesses, and changes to risk free interest rate scenarios) was partly offset by a new margin for adverse deviation for alternative long-duration assets and public equities.

Items excluded from core earnings in 4Q13 included strong investment-related experience and the one-time gains related to the sale of our Taiwan insurance business and to changes to investment objectives of separate accounts that support our U.S. variable annuity products.

Analysis of Net Income

The table below reconciles the 4Q14 net income attributed to shareholders of $640 million to core earnings of $713 million.

| | | | | | | | | | |

| (C$ millions, unaudited) | | 4Q 2014 | | | 4Q 2013 | | | |

Core earnings(1) | | | | | | | | | | |

Asia Division(2) | | $ | 260 | | | $ | 227 | | | |

Canadian Division(2) | | | 224 | | | | 233 | | | |

U.S. Division(2) | | | 338 | | | | 366 | | | |

Corporate and Other (excluding expected cost of macro hedges and core investment gains) | | | (112 | ) | | | (138 | ) | | |

Expected cost of macro hedges(2),(3) | | | (47 | ) | | | (53 | ) | | |

Investment-related experience in core earnings(4) | | | 50 | | | | 50 | | | |

Core earnings | | $ | 713 | | | $ | 685 | | | |

Investment-related experience in excess of amounts included in core earnings(4) | | | (403 | ) | | | 215 | | | |

Core earnings and investment-related experience in excess of amounts included in core earnings | | $ | 310 | | | $ | 900 | | | |

Other items to reconcile core earnings to net income attributed to shareholders: | | | | | | | | | | |

Gains (charges) on direct impact of equity markets and interest rates and variable annuity guarantee liabilities (see table below)(4),(5) | | | 377 | | | | (81 | ) | | |

Changes in actuarial methods and assumptions(6) | | | (59 | ) | | | (133 | ) | | |

Disposition of Taiwan insurance business | | | 12 | | | | 350 | | | |

Impact of in-force product changes and recapture of a reinsurance treaty(7) | | | – | | | | 261 | | | |

Net income attributed to shareholders | | $ | 640 | | | $ | 1,297 | | | |

| | | | |

| 9 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

| (1) | This is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| (2) | The decrease in expected cost of macro hedges cost in 4Q14 compared with 4Q13 was partially offset by an increase in dynamic hedging costs included in Asia, Canada and U.S. divisional core earnings. |

| (3) | The 4Q14 net loss from macro equity hedges was $107 million and consisted of a $47 million charge related to the estimated expected cost of the macro equity hedges relative to our long-term valuation assumptions and a charge of $60 million because actual markets outperformed our valuation assumptions (included in direct impact of equity markets and interest rates and variable annuity guarantee liabilities below). |

| (4) | As outlined under “Critical Accounting and Actuarial Policies” below, net insurance contract liabilities under IFRS for Canadian insurers are determined using CALM. Under CALM, the measurement of policy liabilities includes estimates regarding future expected investment income on assets supporting the policies. Experience gains and losses are reported when current period activity differs from what was assumed in the policy liabilities at the beginning of the period. These gains and losses can relate to both the investment returns earned in the period, as well as to the change in our policy liabilities driven by the impact of current period investing activities on future expected investment income assumptions. The direct impact of equity markets and interest rates is separately reported. The inclusion of up to $200 million per annum of favourable investment experience will be increasing to $400 million per annum commencing 1Q15. See “Performance and Non-GAAP Measures” below for more information. |

| (5) | The direct impact of equity markets and interest rates is relative to our policy liability valuation assumptions and includes changes to interest rate assumptions, including experience gains and losses on derivatives associated with our macro equity hedges. We also include gains and losses on derivative positions and the sale of AFS bonds in the Corporate and Other segment. See table below for components of this item. Until 3Q14 this also included a quarterly URR update. |

| (6) | The 4Q14 charge of $59 million is primarily attributable to method and modeling refinements, partially offset by a gain of $65 million due to the implementation of the Canadian Actuarial Standards Board’s revisions to the Canadian Actuarial Standards of Practice related to economic reinvestment assumptions. |

| (7) | The 4Q13 gain of $261 million included $193 million related to policyholder approved changes to the investment objectives of separate accounts that support our Variable Annuity products in the U.S. and $68 million related to a recapture of a reinsurance treaty in Asia. |

The gain (charge) related to the direct impact of equity markets and interest rates and variable annuity guarantee liabilities in the table above is attributable to:

| | | | | | | | | | |

| C$ millions, unaudited | | 4Q 2014 | | | 4Q 2013 | | | |

Direct impact of equity markets and variable annuity guarantee liabilities(1) | | $ | (142 | ) | | $ | 105 | | | |

Fixed income reinvestment rates assumed in the valuation of policy liabilities(2) | | | 533 | | | | (105 | ) | | |

Sale of AFS bonds and derivative positions in the Corporate and Other segment | | | (14 | ) | | | (55 | ) | | |

Charges due to lower fixed income URR assumptions used in the valuation of policy liabilities(3) | | | – | | | | (26 | ) | | |

Direct impact of equity markets and interest rates and variable annuity guarantee liabilities | | $ | 377 | | | $ | (81 | ) | | |

| (1) | In 4Q14, gross equity exposure losses of $881 million and gross equity hedging charges of $60 million from macro hedge experience were partially offset by gains of $799 million from dynamic hedging experience which resulted in a loss of $142 million. |

| (2) | The gain in 4Q14 for fixed income reinvestment assumptions was driven by the favourable impact on the measurement of policy liabilities of changes in yield curves primarily in the U.S. and Canada. |

| (3) | The periodic URR charges have ceased effective 4Q14 due to revisions to the Canadian Actuarial Standards of Practice related to economic reinvestment assumptions. |

Sales

Insurance sales were $760 million in 4Q14, an increase of 20% compared with 4Q13, with all divisions reporting strong growth. In Asia, we achieved record sales, with most territories growing at a double digit pace. In Canada, we had a strong fourth quarter in large case Group Benefits sales. In the U.S., we continued to build momentum in life insurance sales as product enhancements and targeted pricing changes implemented earlier in the year continued to make an impact.

Wealth saleswere $13.8 billion in 4Q14, an increase of 6% compared with 4Q13. New bank loan volumes (which we include in wealth sales) declined due to competitive rate pressures in a slowing residential mortgage market. Excluding new bank loan volumes, 4Q14 wealth sales increased 9% compared with the prior year. In Asia, wealth sales continued to demonstrate outstanding momentum, growing 64% from 4Q13, benefiting from new product launches, marketing campaigns and improved market sentiment. In Canada, group retirement sales increased compared with 4Q13 with strong sales of defined contribution plans. In the U.S., wealth sales were in line with the prior year, reflecting continued strong mutual fund sales.

Efficiency and Effectiveness Initiative

Our Efficiency and Effectiveness (“E&E”) initiative, announced November 2012, is aimed at leveraging our global scale and capabilities to achieve operational excellence throughout the organization. In 2013, we achieved pre-tax run rate savings6 of approximately $200 million. In 2014, we continued to make substantial progress and have now achieved pre-tax run rate savings in excess of $300 million related to operations, information services, procurement, workplace transformation, as well as organizational design. This has translated into approximately $200 million in net pre-tax savings, which enabled us to fund new initiatives to accelerate our long-term earnings growth. We remain on track to achieve $400 million in pre-tax E&E savings in 2016.7

Over the next four years, we also plan to invest a significant amount in projects in order to realize our strategic vision. The amount of that investment is subject to change as our strategy unfolds. In particular, we intend to ensure that projects are appropriately sequenced and prioritized given recent headwinds.

Acquisition of Canadian-based operations of Standard Life plc

On September 3, 2014, MLI entered into an agreement with Standard Life Oversea Holdings Limited, a subsidiary of Standard Life plc, and Standard Life plc to acquire the shares of Standard Life Financial Inc. and of Standard Life Investments Inc., collectively the Canadian-based operations of Standard Life plc.

On January 30, 2015, the Company completed its purchase of the Canadian-based operations of Standard Life plc for cash consideration of $4.0 billion. Upon closing, the Company’s outstanding subscription receipts were automatically exchanged on a one-for-one basis for 105,647,334 MFC common shares, with a stated value of approximately $2.2 billion. In addition, pursuant to the

| 6 | Pre-tax run rate savings represent cumulative annualized savings from the E&E initiative. |

| 7 | See “Caution regarding forward-looking statements” above. |

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 10 |

terms of the subscription receipts, a dividend equivalent payment of $0.155 per subscription receipt ($16.4 million in the aggregate) was also paid to holders of subscription receipts, which is an amount equal to the cash dividends declared on MFC common shares for which record dates have occurred during the period from September 15, 2014 to January 29, 2015.

The following table summarizes the unaudited assets and liabilities of the Canadian-based operations of Standard Life plc as at December 31, 2014.

| | | | |

| (C$ millions, unaudited) | | As at December 31, 2014 | |

Assets | | | | |

Invested assets | | $ | 18,670 | |

Other assets | | | 970 | |

Segregated funds’ net assets | | | 31,251 | |

Total assets | | $ | 50,891 | |

Liabilities | | | | |

Insurance and investment contract liabilities | | $ | 16,271 | |

Other liabilities | | | 771 | |

Subordinated debentures | | | 403 | |

Segregated funds’ net liabilities | | | 31,251 | |

Total liabilities assumed | | $ | 48,696 | |

Net assets | | $ | 2,195 | |

The difference between the purchase price and the determination of the final fair value of tangible net assets acquired as of January 30, 2015 represents goodwill and intangible assets. Due to the recent closing of the acquisition, the fair value determination and the initial purchase price accounting for the business combination have not been completed, and certain disclosures have not been provided. The final allocation of the purchase price as at January 30, 2015 will be determined after completing a comprehensive evaluation of the fair value of assets (including intangibles) and liabilities acquired at that date.

This transaction significantly builds the Company’s capability to serve customers in all of Canada, and elsewhere in the world, from Quebec. On a pro forma basis as of December 31, 2014 after giving effect to the transaction, the acquisition:

| n | | adds $20.9 billion in assets under administration8 in capital accumulation plans to our group retirement business in Canada, bringing our total group retirement assets under administration in capital accumulation plans in Canada to $46.1 billion; |

| n | | adds $6.5 billion in assets under management to our mutual funds business in Canada, bringing our total mutual fund assets under management8 in Canada to $39.6 billion; and, |

| n | | adds $0.7 billion in premiums and deposits to our Canadian group benefits business, bringing our total Canadian group benefits premiums and deposits in Canada to $7.8 billion. |

Transaction highlights9:

| n | | Excluding transition and integration costs, after the first year we expect the transaction to be accretive by approximately $0.03 to earnings per common share (“EPS”) per year over each of the next 3 years. It will also increase our earnings capacity beyond our 2016 core earnings objective of $4 billion. |

| n | | The transaction, and the financing, maintain our strong capital position and financial flexibility, and in no way inhibit our ability to pay dividends. In fact, it will enhance our ability to increase dividends in the future. |

| n | | We believe the transaction will improve core earnings, however the transition costs reported in core earnings will create a modest, temporary headwind on our core return on common shareholders’ equity (“Core ROE”) 2016 objective of 13%. |

| n | | Excluding transition and integration costs, the transaction is expected to be marginally accretive to EPS in the 1st year. |

| n | | The transaction increases earnings contributions from less capital intensive, fee-based businesses. |

| n | | Integration costs totaling $150 million post-tax are expected to be incurred in the first 3 years and we expect revenue synergies which will build over time. |

| n | | Annual cost savings of $100 million post-tax is expected to be largely achieved by the 3rd year. |

| n | | At the time of announcement, we indicated we were targeting an MCCSR ratio in the range of 235% to 240% at close. The pro forma ratio assuming we had closed on December 31, 2014 would have been in that range. |

| n | | We also indicated that we were targeting a financial leverage ratio of approximately 28% at close. The pro forma ratio assuming we had closed on December 31, 2014 would have been approximately 27.1%. |

| n | | We continue to target a 25% financial leverage ratio over the long-term. |

| 8 | This item is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| 9 | See “Caution regarding forward-looking statements” above and “Performance and Non-GAAP Measures” below. |

| | | | |

| 11 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

Performance by Division

Asia Division

Manulife has a demonstrated business expertise in Asia dating back more than 100 years. Since issuing our first Asian policy in Shanghai in 1897, we have pursued strong, sustained growth and remained a leading provider of financial protection and wealth management products. We are relentlessly focused on helping our customers prepare for their futures, and that focus drives our growth strategy and underpins our commitment to the region. We are diversified across Asia, including some of the world’s largest and fastest-growing economies, with operations in Hong Kong, Japan, Indonesia, the Philippines, Singapore, China, Taiwan, Vietnam, Malaysia, Thailand, Macau and Cambodia.

We offer a broad portfolio of products and services including life and health insurance, annuities, mutual funds and retirement solutions that cater to the needs of individuals and corporate customers through a multi-channel network, supported by a team of approximately 9,000 employees. We now have more than 57,800 contracted agents selling our products and have expanded our distribution capabilities to include more than 100 bank partnerships and more than 500 dealers, independent agents and brokers.

In 2014, Asia Division contributed 18% of the Company’s total premiums and deposits and, as at December 31, 2014, accounted for 13% of the Company’s assets under management.

Financial Performance

Asia Division reported net income attributed to shareholders of $1,247 million in 2014 compared with $2,519 million in 2013. Net income attributed to shareholders is made up of core earnings (consisting of items we believe reflect the underlying earnings capacity of the business), which amounted to $1,008 million in 2014 compared with $921 million in 2013, and items excluded from core earnings, which amounted to $239 million for 2014 compared with $1,598 million in 2013.

Expressed in U.S. dollars, the presentation currency of the division, net income attributed to shareholders was US$1,129 million in 2014 compared with US$2,451 million in 2013, core earnings was US$913 million in 2014 compared with US$893 million in 2013 and items excluded from core earnings were US$216 million in 2014 compared with US$1,558 million in 2013. The increase in core earnings was US$138 million after adjusting for the increased dynamic hedging costs (there is a corresponding decrease in macro hedging costs in the Corporate and Other segment), the impact of changes in currency rates and sale of our Taiwan insurance business at the end of 2013. This 16% increase was driven by higher new business volumes and margins, growth in our in-force business and favourable policyholder experience. The US$1,342 million decrease in items excluded from core earnings was due to the non-recurrence of large gains reported in 2013 related to the direct impact of equity markets and interest rates and variable annuity guarantee liabilities, the sale of our Taiwan insurance business and the recapture of a reinsurance treaty.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

For the years ended December 31, ($ millions) | | Canadian $ | | | | | US $ | |

| | 2014 | | | 2013 | | | 2012 | | | | | 2014 | | | 2013 | | | 2012 | |

Core earnings(1) | | $ | 1,008 | | | $ | 921 | | | $ | 963 | | | | | $ | 913 | | | $ | 893 | | | $ | 963 | |

Items to reconcile core earnings to net income attributed to shareholders: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Direct impact of equity markets and interest rates and variable annuity guarantee liabilities(2) | | | 173 | | | | 1,164 | | | | 911 | | | | | | 157 | | | | 1,142 | | | | 920 | |

Investment-related experience related to fixed income trading, market value increases in excess of expected alternative assets investment returns, asset mix changes and credit experience | | | 62 | | | | 16 | | | | 55 | | | | | | 56 | | | | 18 | | | | 56 | |

Favourable impact of enacted tax rate changes | | | 4 | | | | – | | | | 40 | | | | | | 3 | | | | – | | | | 40 | |

Disposition of Taiwan insurance business | | | – | | | | 350 | | | | – | | | | | | – | | | | 334 | | | | – | |

Impact of recapture of a reinsurance treaty | | | – | | | | 68 | | | | – | | | | | | – | | | | 64 | | | | – | |

Net income (loss) attributed to shareholders | | $ | 1,247 | | | $ | 2,519 | | | $ | 1,969 | | | | | | $ 1,129 | | | $ | 2,451 | | | $ | 1,979 | |

| (1) | Core earnings is a non-GAAP measure. See “Performance and Non-GAAP Measure” below. |

| (2) | The direct impact of equity markets and interest rates is relative to our policy liability valuation assumptions and includes changes to interest rate assumptions. The net gain of $173 million in 2014 (2013 – net gain of $1,164 million) consisted of a $47 million gain (2013 – $1,057 million gain) related to variable annuities that are not dynamically hedged, a $1 million gain (2013 – $60 million gain) on general fund equity investments supporting policy liabilities and on fee income and a $125 million gain (2013 – $75 million gain) related to fixed income reinvestment rates assumed in the valuation of policy liabilities and nil (2013 – $28 million loss) related to variable annuity guarantee liabilities that are dynamically hedged. The amount of variable annuity guaranteed value that was dynamically hedged at the end of 2014 was 51% (2013 – 49%). Our variable annuity guarantee dynamic hedging strategy is not designed to completely offset the sensitivity of policy liabilities to all risks associated with the guarantees embedded in these products. |

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 12 |

Sales

Asia Division’s 2014 insurance sales were a record US$1,278 million, an increase of 31%10 compared with 2013, driven by double digit sales growth in most of the territories in which we operate. Sales in Japan of US$589 million were 60% higher than the prior year driven by strong sales of corporate products and channel expansion. Hong Kong sales of US$293 million increased 15% from 2013, reflecting new product launches and successful sales campaigns. In Indonesia, sales of US$114 million grew 8% over the prior year as strong growth in bancassurance business was partially offset by lower agency sales. Asia Other sales (excluding Japan, Hong Kong and Indonesia) of US$282 million were 17% higher than in 2013 driven by successful product launches and improved agent productivity in China, the Philippines and Vietnam.

Asia Division’s 2014 wealth sales were a record US$8.0 billion, an increase of 2% compared with 2013. Japan sales of US$1.5 billion were 11% lower than the prior year due to lower mutual fund sales, reflecting a shift in investor product preferences in the second half of 2013; partly offset by higher sales from new product launches and expanded bank distribution. Hong Kong sales of US$1.2 billion increased 6% from 2013, driven by continued momentum in pension sales and successful sales campaigns. In Indonesia, sales of US$851 million grew 4% over the prior year as higher mutual fund sales, reflecting improved market sentiment since 2Q14, were partly offset by lower single premium unit-linked sales. Asia Other sales of US$4.4 billion were 5% higher than 2013 driven by higher mutual fund sales in Taiwan and Thailand and the contribution from the asset management company acquired at end of 2013 in Malaysia.

Sales

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For the years ended December 31, ($ millions) | | Canadian $ | | | | | US $ | | | |

| | | 2014 | | | | 2013 | | | | 2012 | | | | | | 2014 | | | | 2013 | | | | 2012 | | | |

Insurance products(1) | | $ | 1,412 | | | $ | 1,052 | | | $ | 1,370 | | | | | $ | 1,278 | | | $ | 1,020 | | | $ | 1,370 | | | |

Wealth products | | | 8,900 | | | | 8,536 | | | | 5,690 | | | | | | 8,045 | | | | 8,319 | | | | 5,698 | | | |

| (1) | All periods have been restated to exclude insurance product sales from Taiwan due to the sale of our Taiwan insurance business at the end of 2013. |

Revenue

Total revenue in 2014 of US$10.8 billion increased US$2.2 billion compared with 2013, primarily driven by the impact of fair value accounting (see “Financial Performance – Impact of Fair Value Accounting” above). Revenue before net realized and unrealized investment gains and losses decreased by US$0.3 billion primarily due to lower revenue from the non-recurrence of the one-time gain on the sale of our Taiwan insurance business in 2013 of US$454 million, partially offset by the increase in premium and fee income.

Revenue

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| For the years ended December 31, | | Canadian $ | | | | | US $ | | | |

| ($ millions) | | | 2014 | | | | 2013 | | | | 2012 | | | | | | 2014 | | | | 2013 | | | | 2012 | | | |

Net premium income | | $ | 7,275 | | | $ | 6,330 | | | $ | 7,045 | | | | | $ | 6,583 | | | $ | 6,148 | | | $ | 7,050 | | | |

Investment income | | | 1,271 | | | | 1,224 | | | | 1,104 | | | | | | 1,150 | | | | 1,187 | | | | 1,101 | | | |

Other revenue | | | 1,334 | | | | 1,963 | | | | 716 | | | | | | 1,208 | | | | 1,898 | | | | 715 | | | |

Revenue before net realized and unrealized investment gains (losses)(1) | | $ | 9,880 | | | $ | 9,517 | | | $ | 8,865 | | | | | $ | 8,941 | | | $ | 9,233 | | | $ | 8,866 | | | |

Net realized and unrealized investment gains (losses) | | | 2,078 | | | | (619 | ) | | | 1,090 | | | | | | 1,867 | | | | (593 | ) | | | 1,091 | | | |

Total revenue | | $ | 11,958 | | | $ | 8,898 | | | $ | 9,955 | | | | | $ | 10,808 | | | $ | 8,640 | | | $ | 9,957 | | | |

| (1) | See “Financial Performance – Impact of Fair Value Accounting” above. |

Premium and Deposits

Premiums and deposits for the full year 2014 of US$16.2 billion increased 5% on a constant currency basis compared with 2013. Of this, premiums and deposits for insurance products of US$6.4 billion increased 13% compared with 2013 (adjusted to exclude the Taiwan insurance business sold in 2013). Premiums and deposits for wealth products of US$9.8 billion increased by 3% compared with 2013. The increase was driven by sales from new single premium whole life products (classified as wealth sales due to their high investment component) and the favourable impact of expanded distribution in Japan, continued momentum in pension sales in Hong Kong and improved market sentiment in Indonesia, partially offset by lower single premium unit-linked sales in Indonesia and the non-recurrence of strong sales of the Strategic Income Fund in the first half of 2013 due to a shift in investor preference from bonds to equities.

Premiums and Deposits

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For the years ended December 31, ($ millions) | | Canadian $ | | | | | US $ | | | |

| | | 2014 | | | | 2013 | | | | 2012 | | | | | | 2014 | | | | 2013 | | | | 2012 | | | |

Insurance products | | $ | 7,066 | | | $ | 6,337 | | | $ | 6,650 | | | | | $ | 6,396 | | | $ | 6,154 | | | $ | 6,655 | | | |

Wealth products | | | 10,831 | | | | 10,167 | | | | 6,811 | | | | | | 9,789 | | | | 9,908 | | | | 6,822 | | | |

Total premiums and deposits | | $ | 17,897 | | | $ | 16,504 | | | $ | 13,461 | | | | | $ | 16,185 | | | $ | 16,062 | | | $ | 13,477 | | | |

| 10 | Growth (declines) in sales, premiums and deposits and assets under management are stated on a constant currency basis. Constant currency basis is a non-GAAP measure. See “Performance and Non-GAAP Measures” below. |

| | | | |

| 13 | | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | |

Assets under Management

Asia Division assets under management as at December 31, 2014 were US$75.1 billion, an increase of 10% on a constant currency basis compared with December 31, 2013, driven by net policyholder cash inflows of US$2.0 billion, combined with the impact of the decline in interest rates and higher equity markets, partially offset by a weaker yen compared with the U.S. dollar.

Assets under Management

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

As at December 31, ($ millions) | | Canadian $ | | | | | US $ | | | |

| | | 2014 | | | | 2013 | | | | 2012 | | | | | | 2014 | | | | 2013 | | | | 2012 | | | |

General fund | | $ | 41,991 | | | $ | 34,756 | | | $ | 36,608 | | | | | $ | 36,198 | | | $ | 32,680 | | | $ | 36,800 | | | |

Segregated funds | | | 22,925 | | | | 23,568 | | | | 24,647 | | | | | | 19,761 | | | | 22,160 | | | | 24,780 | | | |

Mutual and other funds | | | 22,167 | | | | 18,254 | | | | 16,480 | | | | | | 19,108 | | | | 17,164 | | | | 16,563 | | | |

Total assets under management | | $ | 87,083 | | | $ | 76,578 | | | $ | 77,735 | | | | | $ | 75,067 | | | $ | 72,004 | | | $ | 78,143 | | | |

Strategic Direction

Manulife Asia’s strategic ambition is to become a premier pan-Asian insurance and wealth management franchise that is well positioned to meet the evolving protection, savings and retirement needs of its customers. Our core strategy of providing customers with personalized financial solutions that enable them to confidently secure their own and their family’s financial future focuses on expanding our professional agency force and alternative distribution channel, building and expanding our portfolio of products in wealth and protection, building long-lasting customer relationships as well as investing in our brand across Asia. Our agency and bank distribution strategies will help us to reach the rapidly expanding middle class across Asia and by leveraging our insurance and asset management businesses, we will offer holistic retirement solutions from insurance, pensions and mutual funds to support the needs of the aging population. We will also accelerate the development of mobile and digital platforms and interactions to enhance our customers’ experience.

In 2014, we entered into several new strategic bancassurance agreements, including with RHB Bank in Singapore and Industrial and Commercial Bank of China in Macau. We also strengthened our strategic bancassurance alliance in the Philippines by renewing our 10-year distribution agreement with China Banking Corporation, which also increased its stake in our joint venture company, Manulife China Bank Life Assurance Corporation, to 40%. To support our customer centricity objectives, we improved our public websites to enhance customer experience and launched an electronic point of sale solution in a number of markets to improve the structure and efficiency of the financial advice and sales process.

In Hong Kong, in 2014, we were first-in-market with a multiple critical illness plan which provides customers with increased protection and we continued to build our retirement business with the launch of two new retirement products. In addition, through advancements in technology we enhanced customer experience, strengthened agency training and development, and promoted our brand in the retirement field.

In Japan, in 2014, we expanded corporate, retail and bancassurance distribution and enhanced customer experience by streamlining sales and back-office processes, and point-of-sales tools for new products.

In Indonesia, in 2014, we further developed our sharia business by signing a memorandum of understanding to form a new strategic bancassurance partnership with a local sharia bank and launched a series of new products and riders to cater to the growing protection and investment needs of the middle class. To further promote our brand awareness in the market, we launched a series of branding campaigns throughout the year including one that coincided with the important national festival, Eid al-Fitr, in July.

In the Other Asia territories, in 2014, we continued investing to expand and diversify our distribution channels and develop our wealth and asset management businesses. We also focused on improving product competitiveness, for example in Singapore where we improved insurance sales in the second half of the year by 162% compared with the first half of the year.

| | | | |

| | Manulife Financial Corporation 2014 Management’s Discussion and Analysis | | 14 |

Canadian Division

Serving one in five Canadians, our Canadian Division is one of the leading financial services organizations in Canada. We offer a broad portfolio of protection, estate planning, investment and banking solutions through a diversified independent distribution network, supported by a team of more than [8,600] employees.