Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16 of

Securities Exchange Act of 1934

For the month of August 2015

SANTANDER UK PLC

(Translation of registrant’s name into English)

2 Triton Square, Regent’s

Place, London NW1 3AN, England

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

THE REGISTRANT HEREBY INCORPORATES ALL PARTS OF THIS REPORT ON FORM 6-K BY REFERENCE IN REGISTRATION STATEMENT NO. 333-190509 FILED BY THE REGISTRANT WITH THE SECURITIES AND EXCHANGE COMMISSION ON FORM F-3ASR UNDER THE SECURITIES ACT OF 1933.

Table of Contents

2015 Half Yearly Financial Report

Santander UK plc

PART OF THE SANTANDER GROUP

Table of Contents

| ||||||||||||

HY 2015 business and financial highlights

|

We are pleased to report strong results for the first half of 2015, with continued improvement in profitability and strong commercial momentum.

| |||||||||||

Net interest income |

Profit before tax |

Banking net interest margin (‘NIM’) | ||||||||||

| £1,783m | £929m | 1.86%(1) | ||||||||||

| Up 7% on the first half of 2014, driven by margin improvements and increased retail and corporate lending. | Up strongly on the first half of 2014, with continued growth in net interest income, and well-performing retail and corporate loan portfolios.

| Up 6 basis points on the first half of 2014, largely due to the lower cost of retail liabilities. | |||||||||

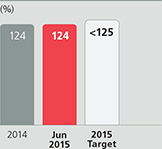

| Cost-to-income ratio | CET 1 capital ratio | Loan-to-deposit ratio | ||||||||||

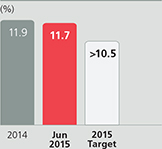

| 53% | 11.7% | 124% | ||||||||||

Improved from the first half of 2014, with administrative expenses tightly managed

| Strong capital position with an improved PRA end-point Tier 1 leverage ratio of 4.1%. | Unchanged from the end of 2014, with strong growth in Retail Banking assets and liabilities. | ||||||||||

| Gross mortgage lending | Lending to corporates | Retail customer satisfaction | ||||||||||

| £11.9bn | +11%year-on-year | 61.7% | ||||||||||

| We helped 15,800 first-time buyers and 2,800 Help to Buy customers purchase a home. | During the first half of 2015, we extended £4.5bn of new facilities to SMEs and mid-sized corporates, an increase of 15% on the first half of 2014. | Gap between Santander UK and the average of three highest performing peers closed1. Further improvement is at the heart of our plans. | ||||||||||

This Half Yearly Financial Report contains forward-looking statements that involve inherent risks and uncertainties. Actual results may differ materially from those contained in such forward-looking statements. See ‘Forward-looking Statements’ on page 138. For definitions of terms used in this Half Yearly Financial Report, see ‘Glossary’ on page 137.

Santander UK plc (the ‘Company’) and its subsidiaries (collectively ‘Santander UK’ or ‘Santander UK group’) operate primarily in the UK, and are part of the Banco Santander, S.A. group (comprising Banco Santander, S.A. and its subsidiaries, the ‘Banco Santander group’).

Santander UK plc is regulated by the UK Prudential Regulation Authority (‘PRA’) and the Financial Conduct Authority (‘FCA’), and certain other companies within the Santander UK group are regulated by the FCA.

1. Source: Customer satisfaction as measured by the Financial Research Survey (‘FRS’) run by GfK NOP (June 2015). See ‘Glossary’ on page 137.

| ||||||||||||

| (1) | Non-IFRS measure. See page 139. |

Table of Contents

| 1 |

Table of Contents

| Helping people and businesses prosper |

“I joined Santander UK as its Chair because I believe it is true in its intent to help people and businesses prosper and also has the potential to be transformative to the sector and the economy”

Baroness Shriti Vadera

Chair

12 August 2015

| (1) | CMA Retail Banking Market Investigation, |

updated issues statement, May 2015 |

Our purpose is to help people and businesses prosper as we build the Best Bank in the UK – a bank that is Simple, Personal and Fair.

Overview

The UK banking sector needs to continue its transformation to focus more on the genuine needs of households and small and medium business customers and to win their trust and that of regulators, policymakers, investors and the wider public. A better service to the domestic economy has to be the cornerstone of the sector’s ambition to remain a leading global financial centre.

Santander UK remains on course on its own journey, launched by Ana Botín during her time as CEO, to become a bank that is Simple, Personal and Fair and that wins the lasting loyalty of its customers, people, shareholders and communities. It has been a journey so far with some remarkably successful milestones. I was particularly pleased to see we won the Moneywise award for ‘Most Trusted Mainstream Bank’, as voted for by UK consumers.

But we know we have further to go. Nathan Bostock made it one of his three commitments to our shareholder in 2015 to develop a set of behaviours to underpin our values of Simple, Personal and Fair in the UK. Defining these behaviours, through the engagement of our people at roadshows across the country, has been an essential step towards embedding the culture we aspire to.

I joined Santander UK as its Chair because I believe it is true in its intent to help people and businesses prosper and also has the potential to be transformative to the sector and the economy. With its building society heritage, Santander UK has sustained its position as one of the significant mortgage providers in a highly competitive and commoditised market. In all other markets, spanning personal current accounts, credit cards and SMEs, we are a challenger bank.

In the SME market, we have grown our business steadily, but still only account for a small proportion of the SME lending market, while the Big Four UK banks together take over 85% of the outstanding volume of lending(1). But we also have a scale and the backing of our parent that give us geographic reach, brand recognition and resources – including a strong branch presence on the high street and a network of Corporate Business Centres across the UK. These help us to make a difference to significant segments of banking service provided to the population.

Santander UK has used its position as ‘scale challenger’ to launch innovative products that require substantial investment and the ability to reach a national market. These include the 1I2I3 Current Account, part of our 1I2I3 World proposition with more than four million customers, which has led to changes elsewhere in the sector as the incumbents seek to respond. Our scale challenger status has also enabled us to create Santander Breakthrough to support fast-growth SMEs. Our unique trade proposition leverages Banco Santander’s global network and is the only UK bank export scheme targeted specifically at SMEs. We will continue to aspire to be transformative as we embrace the pace of change in the digital world.

In February, Santander UK was announced as one of the UK’s best employers, placed in ‘The Sunday Times 25 Best Big Companies to Work For 2015’ awards, and in April we were named in ‘The Times Top 50 Employers for Women 2015’. Such milestones give us confidence that we are making progress against our own challenging goals.

Most Trusted Mainstream Bank

June 2015

25 Best Big Companies to Work For 2015

April 2015

| 2 | Santander UK plc |

Table of Contents

Chair’s review | Chief Executive Officer’s review | KPIs | Chief Financial Officer’s review |

Shriti Vadera sets out our position as a ‘scale challenger’ in the UK banking sector and gives an overview of changes to the Board

|

| See Our heritage and Santander UK today on pages 2 and 3 of the 2014 Annual Report | |

| See the Compass and our business model on pages 6 and 7 of the 2014 Annual Report | |

| See Governance report on page 145 of the 2014 Annual Report | |

| See Corporate Social Responsibility review on page 22 of the 2014 Annual Report | |

I would like to thank all of my colleagues for all they have done, and continue to do, to transform the business. Their dedication, commitment and loyalty underpins our success.

A priority for the coming years will be to ensure that Santander UK and our customers are well prepared for the very significant structural changes that will result from implementation of the Financial Services (Banking Reform) Act 2013. Our plans to establish a retail bank for our personal and small business customers and a corporate bank for our corporate and institutional customers and markets business will enable us to continue our growth in the UK, while also preparing us to conform with the new regulatory regime.

I do not underestimate the very significant challenges to our systems and our people of implementation on multiple simultaneous fronts – the scale of regulatory changes on our balance sheet and operations, the cultural changes that need embedding, and the digital transformation to be initiated in parallel to giving customers the choices they need as they themselves adapt to digital use. And all the while ensuring we are profitable, improve our cost-to-income ratio and win competitive market share as a challenger. I remain confident in the ability of Nathan and his team to manage this transformation risk effectively and well.

The Board

I would like to pay tribute to the Chairmanship of my predecessor Lord Burns and to personally thank him for the enormous support and advice he has provided me during and since the period of transition. His strategic leadership and courageous decisions over 14 years saw the creation of Santander UK and, with the rest of the Board and management, he steered it successfully through the financial crisis.

Terry and Ana leave behind a legacy of which we can all be proud, but importantly a bank that is well placed to look to the future under Nathan’s leadership.

To date, 2015 has been a year of considerable change on the Board. Chris Jones succeeded Rosemary Thorne as the Chair of Board Audit Committee with effect from 30 June 2015. Chris has significant experience in financial services since the mid-1980s after specialising in the audit of banks during his time as a Senior Audit Partner and leader of PwC’s EMEA Financial Services practice. Demonstrating our commitment to digital change, Genevieve Shore joined the Board as an Independent Non-Executive Director on 18 May 2015 and brings a wealth of digital experience gained through her extensive executive career at Pearson and Penguin, where she led and implemented innovative technology solutions. Scott Wheway has been appointed as a Senior Independent Director. Scott joined the Board in October 2013 and has extensive experience in retail and financial services.

We continue to review the composition, experience and skill set of the Board on an ongoing basis to ensure that we are well placed for future challenges.

I would like to thank two long-serving Directors for their commitment and dedication over many years. José María Carballo stepped down in March 2015 after 10 years, and Rosemary Thorne stepped down from her position as Independent Non-Executive Director and Chair of the Board Audit Committee on 30 June 2015 after nine years. I would also like to thank Stephen Jones, who steps down as Director and Chief Financial Officer at the end of October.

| 2015 Half Yearly Financial Report | 3 |

Table of Contents

Strategic report update | Helping people and businesses prosper |

Chief Executive

Officer’s review

“Our ongoing focus on operational and digital excellence has led to a much improved customer experience and will remain at the heart of our future plans”

Nathan Bostock

Chief Executive Officer

12 August 2015

Our strategic priorities

| 1 | Loyal and satisfied retail customers |

| 2 | ‘Bank of Choice’ for UK companies |

| 3 | Consistent profitability and a strong balance sheet |

We have delivered a strong set of results for the first half of the year, with good momentum in profitability. We have achieved our 2015 targets for 1I2I3 World and customer satisfaction ahead of schedule, and remained the first choice for UK retail customers switching their current account provider. We also grew lending to UK companies by £1.8bn in the past six months, maintaining positive momentum in an increasingly competitive market.

Economic and market backdrop

The UK economy continued to grow at a steady pace in early 2015, approaching the strongest performance for several years. Consumer spending growth in the first quarter of 2015 continued to be supported by solid gains in employment and further falls in unemployment. More recently, there has been a boost from the return of real earnings growth, due to low inflation and faster average wage increases.

Mortgage lending growth in the first half of 2015 continued the positive trend of the second half of 2014, underpinned by the positive economic fundamentals of record low mortgage rates, high consumer confidence, low unemployment and positive real earnings growth. Annual corporate borrowing growth remained subdued as companies continued to rely on other sources of finance.

The demands of high volumes of regulatory and competition reviews facing the UK banking sector continued in the first half of 2015. We remain actively engaged in formal policy consultation processes and in close dialogue with our regulators. We support proportionate developments in regulation which increase competition in the market and lead to better outcomes for our customers.

The most significant change facing the banking sector is the UK Government’s proposals for major banks to separate their wholesale and investment banking functions from their retail operations, as laid out in the Financial Services (Banking Reform) Act 2013.

Our customer-focused strategy, low risk approach and fewer legacy issues leave us well aligned to the reform agenda. We intend to establish a bank for retail and small business customers, as well as a separate bank dedicated to corporate and institutional customers and our markets business. As a scale challenger, we believe this approach will enable us to meet the distinct needs of the different segments of our retail, corporate and institutional customer base and comply with the Banking Reform Act by 1 January 2019, as required.

Improving how we do business and making our processes and systems even more simple, personal and fair is key to our continued success. We continue to invest in our digital and mobile platforms and have made a number of improvements to the service we offer this year. We have adopted the Apple Pay service to enable users to pay for goods and services using their phone and launched a new app, ‘Spendlytics’, which enables users to track, analyse and understand their debit and credit card spend in detail. In 2015, we are continuing to focus on digital developments, in particular security, new services, increased functionality across platforms and a single consolidated account view for each customer.

Loyal and satisfied retail customers

We have made significant improvements to our products and services in the past three years. We have now closed the gap between our retail customer satisfaction score and that of the average three highest performers among our peers.

Current account switchers(1)

1-in-4

We gained more customers than any other UK bank as part of the Current Account Switch Scheme (‘CASS’) since it launched in September 2013.

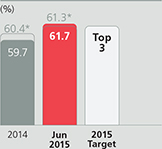

Retail customer satisfaction (‘FRS’)(2)

61.7%

Significantly improved customer satisfaction since June 2012.

| 4 | Santander UK plc |

Table of Contents

Chair’s review | Chief Executive Officer’s review | KPIs | Chief Financial Officer’s review |

Nathan Bostock reports on the backdrop to our business and performance in the first half of 2015

|

| See Top and Emerging Risks on pages 13 and 14 |

Further improvements are at the heart of our plans, as we aim to achieve the best outcomes for customers.

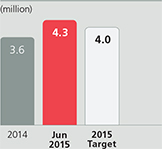

We now have 4.3 million 1I2I3 World customers, well above our 2015 target of four million, with an associated increase in our loyal customer base. Total banking and savings balances held by primary banking customers increased 14% to £80.4bn at 30 June 2015, enabling us to focus on lower cost, more loyal deposits.

Our 1I2I3 Current Account and much improved customer service make Santander UK the first choice for customers changing their bank. Over 500,000 customers have switched their current account to Santander UK since the introduction of the Current Account Switch Service in September 2013.

‘Bank of Choice’ for UK companies

We have made a substantial investment over the past three years to increase the business we do with SMEs and larger corporates. This investment is largely complete and we now have 68 regional Corporate Business Centres and 729 relationship managers around the UK to support local businesses. Our focus going forward is to build productivity across our platform with the broader product suite and with the extended footprint we have in place.

We continued to deliver an improvement in corporate customer satisfaction(3), as well as an improvement in our rating for overall relationship management quality compared with a year ago.

In the first half of 2015 we extended £4.5bn of new facilities to SMEs and mid-sized corporates, an increase of 15%, with total customer loans increasing to £25.7bn. Commercial bank account openings increased by 15% with acceleration in the usage of our corporate banking platform.

Consistent profitability and a strong balance sheet

Profit before tax increased to £929m in the first half of 2015, a strong result in a competitive environment. Net interest income was higher, driving an increase in the banking net interest margin(4) to 1.86%, up 6 basis points since June 2014.

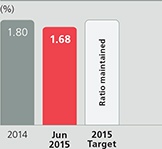

The ratio of non-performing loans to total customer loans improved to 1.68% from 1.80% at 31 December 2014, with retail and corporate loans both performing well in an improving credit environment.

The balance sheet remained strong, with a Common Equity Tier 1 capital ratio of 11.7% and an improved leverage ratio of 4.1%. In June 2015, we completed our first public issuance from Santander UK Group Holdings plc with the issuance of £750m of Additional Tier 1 securities, which was well received by the market.

Looking forward

We have done much to improve the customer experience and to begin embedding our cultural values while improving the customer experience with our new digital platforms. Making further improvements to customer satisfaction, maintaining control of costs and building our digital business remain key priorities for us.

Our current key performance indicators were set in 2012 and are measured against a target date of 2015. Our key performance indicators and targets will be updated at the Banco Santander Investor Day in late September 2015 when we will set out our new medium-term objectives.

The structural reforms of the UK banking sector will lead to significant change in the coming years; we will keep all stakeholders updated as we evolve our new operating models. I am confident that Santander UK offers a strong challenge and can continue to grow both its retail and corporate banking propositions profitably.

Sources: ‘Glossary’ on page 137 for definitions.

| (1) | Bacs, Current Account Switch Service statistics, June 2015 |

| (2) | Financial Research Survey, GfK NOP, June 2015 |

| (3) | Business Banking Survey, Charterhouse UK Q2 2015 |

| (4) | Non-IFRS measure. See page 139. |

| 2015 Half Yearly Financial Report | 5 |

Table of Contents

Strategic report update | Helping people and businesses prosper |

Performance against our KPIs | KPIs help us measure progress towards our 2015 targets. They were set in 2012 and aligned to our strategic priorities. |

1 | Loyal and satisfied

| Loyal customers As part of our transformation to a more customer-focused organisation, we seek to develop and build deeper customer relationships. We are on-track to deliver our 2015 target. | 1I2I3 World customers Our 1I2I3 World products are key to our strategy of building deeper customer relationships and delivering ongoing value to our customers. | |||

| Deepening our customers’ loyalty by meeting their changing needs |  |  | ||||

2 | ‘Bank of Choice’ for

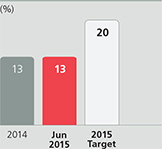

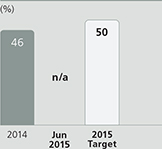

Growing our business with corporate customers, while expanding the range of products and services we offer to them | Corporate loans percentage of total customer loans A key element of our strategy is to diversify the business mix, in terms of income and customer base, and to provide a better strategic balance. We have consistently grown corporate lending since 2012, in what has been

|

a shrinking market. However, we will not compromise our prudent risk management and return objectives and do not expect to achieve our 2015 target - which was set with the prospect of an acquisition which we did not subsequently proceed with. | |||

3 | Consistent

Providing our shareholders with a sustainable return on their investment | Adjusted RoTE(1) We monitor return on tangible equity (‘RoTE’) to measure the overall profitability and sustainability of the business. We are unlikely to reach our 2015 target as we are holding more capital than we assumed when the target was set in 2012.

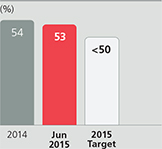

| Cost-to-income ratio We monitor this ratio to measure our operating efficiency. We are unlikely to reach our 2015 target given investment spend and regulatory compliance costs, which have been higher than anticipated when the target was set in 2012.

| |||

| (1) | Non-IFRS measure. See page 139. |

| 6 | Santander UK plc |

Table of Contents

Chair’s review | Chief Executive Officer’s review | KPIs | Chief Financial Officer’s review |

Nathan Bostock explains our KPI performance and the progress made against our strategic priorities

|

| ||

Retail customer satisfaction (‘FRS’)(1) We place a significant focus on improving the customer experience and putting the customer at the heart of what we do. See ‘Glossary’ on page 137.

*Avg. of 3 highest performing peers

| ||

| CET 1 capital ratio | Loan-to-deposit ratio (‘LDR’) | Non-performing loan (‘NPL’) ratio | Dividend payout ratio | |||

| We monitor the Common Equity Tier 1 (‘CET 1’) capital ratio to assess our capacity to grow while maintaining sufficient capital resources to meet regulatory requirements. | We monitor the LDR to assess our ability to fund customer lending with customer deposits, reducing our reliance on wholesale markets. | We monitor the NPL ratio as an important measure of risk in our business to ensure it remains consistent with our low-to-moderate risk appetite. | We monitor the dividend payout ratio to ensure we are able to grow the business while maintaining a sustainable return for our shareholder. | |||

|

|

|

| |||

| (1) | Financial Research Survey, GFK NOP, June 2015 |

| 2015 Half Yearly Financial Report | 7 |

Table of Contents

Strategic report update | Helping people and businesses prosper |

Officer’s review

“In June 2015, we successfully launched our first public issuance from Santander UK Group Holdings plc. This £750m Additional Tier 1 capital securities issuance was well-received by the market.”

Stephen Jones

Chief Financial Officer

12 August 2015

Profit before tax of £929m was up strongly in the first half of 2015, with continued growth in net interest income, underlying cost efficiency and robust credit quality.

Income statement highlights(A)

Profit after tax increased to £734m in the first half of 2015, with adjusted RoTE(1) improving to 12.8% (2014: 10.4%).

Net interest income was 7% higher, driven by improved margins and increased unsecured retail and corporate lending.

Non-interest income was 4% lower, reflecting lower net banking fee income in Retail Banking. This was partially offset by higher banking fee and international payments income in Commercial Banking as well as higher revenues from client derivative and cash sales activities in Corporate & Institutional Banking.

Operating expenses fell 2%, largely due to a number of specific gains, expenses and charges which increased operating expenses by £86m in the first half of 2014. Excluding this impact, operating expenses in the first half of 2015 increased due to investment in business growth, regulatory compliance project costs (including banking reform) and continued enhancements to our digital channels.

Operating impairment losses, provisions and charges were significantly lower, in part due to specific provisions with a net impact of £120m in the first half of 2014.

Excluding these provisions, impairment losses in the first half of 2015 were lower due to improved economic conditions, lower mortgage impairment losses as well as provision releases in Corporate & Institutional Banking and Corporate Centre following the disposal and restructuring of certain loans. Charges associated with our programme of branch de-duplication were also lower.

Customer balances(B)

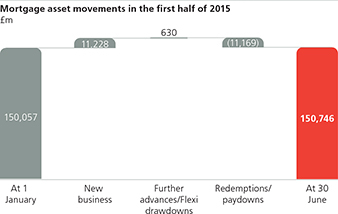

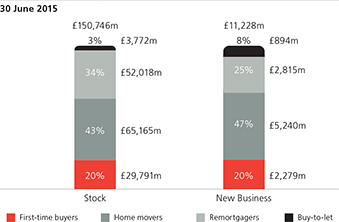

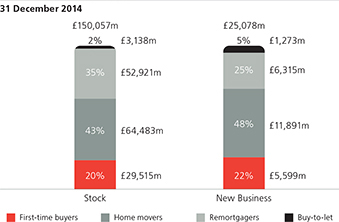

Customer assets grew £5.5bn to £196.2bn following the commencement of the PSA cooperation, which added a vehicle finance loan book of £2.5bn to the balance sheet in February 2015 (See Note 35 to the Condensed Consolidated Interim Financial Statements). In addition, during the first half of the year, corporate customer loans increased by £1.8bn to £25.7bn and mortgage balances increased by £0.6bn to £150.7bn. The growth in mortgage loans was driven by stronger approval volumes in the first and second quarters of the year, following lower volumes in late 2014. Mortgage gross lending in the first half of 2015 was £11.9bn and we also retained about 80% of maturing products onto new Santander UK mortgages. Customer deposits increased £4.7bn to £157.1bn at 30 June 2015, as we focused on retaining and originating accounts held by more loyal customers.

| (A) | Income statement highlights |

| 6 months ended | 30 June 2015 £m | 30 June 2014 £m | ||||||

Net interest income | 1,783 | 1,673 | ||||||

Non-interest income(2) | 500 | 519 | ||||||

Operating expenses(3) | (1,200 | ) | (1,223 | ) | ||||

Operating impairment losses, provisions and charges | (154 | ) | (424 | ) | ||||

Profit before tax | 929 | 545 | ||||||

Profit after tax | 734 | 438 | ||||||

| (1) | Non-IFRS measure. See page 139. |

| (2) | Non-interest income is comprised of Net fee and commission income and Net trading and other income. |

| (3) | Operating expenses equals Total operating expenses excluding impairment losses, provisions and charges. |

| 8 | Santander UK plc |

Table of Contents

Chair’s review | Chief Executive Officer’s review | KPIs | Chief Financial Officer’s review |

Stephen Jones outlines the financial results for the first half of 2015.

|

Retail Banking current account balances grew by £6.6bn to a total of £47.7bn, partially offset by lower savings balances. Commercial Banking deposits grew £1.3bn as we increased the utilisation of our expanded Corporate Banking capabilities to build upon our strong customer relationships.

The loan-to-deposit ratio of 124% was unchanged from December 2014. The positive impact of continued strong growth in retail current accounts was offset by the impact of the PSA cooperation.

Credit quality(C)

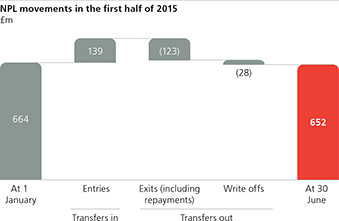

The Retail Banking non-performing loan ratio improved to 1.53% at 30 June 2015, as a result of lower mortgage non-performance and overall growth in retail assets. The residential mortgage non-performing loan ratio was 1.57%, reflecting good performance of the portfolio supported by low interest rates, rising house prices and falling unemployment. We are conscious that these conditions may not continue and our provisions reflect our conservative position on the UK economy and the housing market, notwithstanding current trends. The banking and consumer credit non-performing loan ratio decreased to 1.05%, mainly as a result of the commencement of the PSA cooperation.

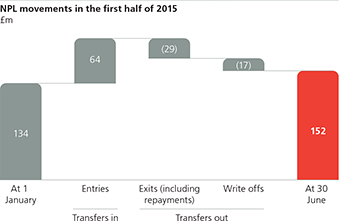

The Commercial Banking non-performing loan ratio decreased to 3.25% at 30 June 2015, with credit quality remaining strong. We continue to adhere to our prudent criteria as we grow lending.

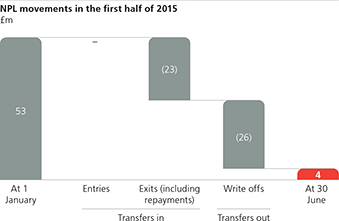

The Corporate & Institutional Banking non-performing loan ratio decreased to 0.07% at 30 June 2015, due to the disposal of a single loan of £49m as well as asset growth.

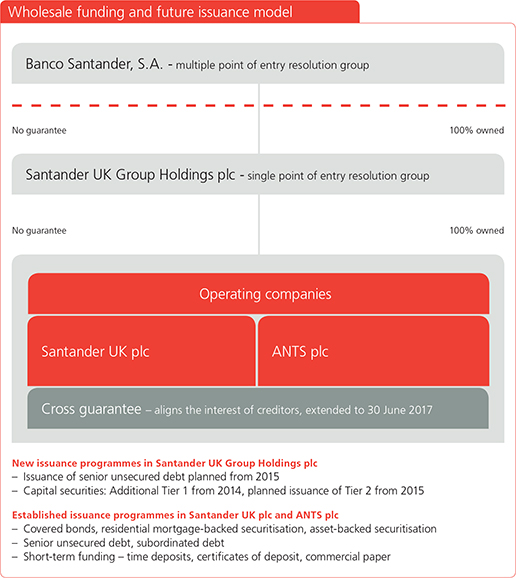

Issuance and debt buy-back

In June 2015, we successfully launched our first public issuance from Santander UK Group Holdings plc. This £750m Additional Tier 1 capital securities issuance was well-received by the market and was downstreamed to Santander UK plc in mirror form with a coupon of 7.375%.

At the same time, we also completed the partial buy-back of four capital instruments in order to improve our capital position, as under current capital regulations, these securities are impacted by both CRD IV Minority Interest and ‘grandfathering’ rules.

Capital and leverage(D)

Risk weighted assets were up £2.9bn to £85.2bn, broadly in line with asset growth and reflecting the commencement of the PSA cooperation.

(B) Customer balances

30 June 2015 £bn | 31 December 2014 £bn | |||||||

Total customer loans | 196.2 | 190.7 | ||||||

Total customer deposits | 157.1 | 152.4 | ||||||

Loan-to-deposit ratio | 124% | 124% | ||||||

(C) Credit quality

30 June 2015 % | 31 December 2014 % | |||||||

Retail Banking NPL ratio | 1.53 | 1.62 | ||||||

Commercial Banking NPL ratio | 3.25 | 3.56 | ||||||

Corporate & Institutional Banking NPL ratio | 0.07 | 1.01 | ||||||

Corporate Centre NPL ratio | 1.93 | 1.62 | ||||||

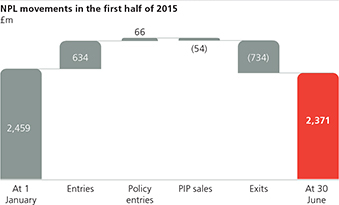

Total NPL ratio | 1.68 | 1.80 | ||||||

| 2015 Half Yearly Financial Report | 9 |

Table of Contents

Strategic report update | Helping people and businesses prosper |

Chief Financial

Officer’s review

continued

The CET 1 capital ratio was 11.7%, largely due to the increase in RWAs from the PSA cooperation. The PRA end-point Tier 1 leverage ratio was 4.1%, up from 3.8% at 31 December 2014, mainly due to the £750m Additional Tier 1 issuance.

Liquidity and funding(D)

The liquidity coverage ratio (‘LCR’)(2) eligible liquidity pool decreased £5.0bn, to £34.5bn at 30 June 2015, largely due to the phasing of short-term funding and of medium-term maturities. The decrease is expected to partially reverse in the second half of the year. Wholesale funding with a residual maturity of less than one year decreased £4.4bn, to £18.7bn, reflecting changes in the medium term funding maturity profile. The LCR(2) eligible liquidity pool significantly exceeded wholesale funding of less than one year, with a 184% coverage ratio.

Medium-term funding (‘MTF’) issuance of £8.0bn (sterling equivalent) in the first half of 2015 included £4.3bn of senior unsecured issuance and £750m of Additional Tier 1 securities outlined on the previous page. At 30 June 2015, we had total outstandings of £2.2bn under the Bank of England and HM Treasury’s Funding for Lending Scheme (‘FLS’), with no additional drawings made in 2015.

2015 outlook

We anticipate that the UK economy will continue to be supportive of our business. There is evidence of increasing liquidity in the lending market resulting in competitive pressures in many business lines, which may impact new asset margins. We also expect the implementation costs of regulatory reform to increase significantly in the months ahead as we evolve our new operating models to address ring fencing requirements.

The Banking NIM(2) for 2015 is expected to remain broadly unchanged from the 1.82% we reported for 2014, predicated on the Bank of England base rate not rising this year. Reduced stock margins and new lending margin pressures for mortgages, which started in the second half of 2014, are likely to be largely offset by improvement in liability margins.

We expect our net mortgage lending to grow in line with the market for the rest of the year, and the decline in SVR mortgage balances, which reduced by a net £3.9bn in the first half of 2015, to continue.

The bank Corporation Tax surcharge and changes to the Bank Levy announced in the UK Budget on 10 July 2015 will have a material impact on future earnings.

(D) Liquidity, funding, capital and leverage – CRD IV

30 June 2015 £bn | 31 December 2014 £bn | |||||||

LCR(2) eligible liquidity pool | 34.5 | 39.5 | ||||||

LCR(2) | 109% | 110% | ||||||

Risk Weighted Assets (‘RWAs’) | 85.2 | 82.3 | ||||||

CET 1 capital | 10.0 | 9.8 | ||||||

CET 1 capital ratio | 11.7% | 11.9% | ||||||

PRA end-point Tier 1 leverage ratio(1) | 4.1% | 3.8% | ||||||

(1) The leverage ratio defined by the PRA uses an exposure measure consistent with the Basel Committee’s January 2014 Leverage Ratio Framework.

(2) Non-IFRS measure. See page 139.

| 10 | Santander UK plc |

Table of Contents

Risk governance | Top and emerging risks | Credit risk | Market risk | Balance sheet management risk | Other important risks | Areas of focus and other items | ||||||

|

| 2015 Half Yearly Financial Report | 11 |

Table of Contents

This Risk review contains information that forms an integral part of the Condensed Consolidated Interim Financial Statements.

As a significant financial services provider, risk is at the core of Santander UK’s day-to-day activities. The understanding and control of risk on an enterprise-wide basis is critical for the effective management of the business. Santander UK aims to employ a prudent approach and advanced risk management techniques to facilitate the delivery of robust financial performance, and ultimately build sustainable value for all our stakeholders.

Santander UK aims to maintain a predictable medium-low risk profile, consistent with its business model, which is key to the successful achievement of our strategic objectives.

RISK FRAMEWORK

The Risk Framework in place at 30 June 2015 was based upon the following key components:

| – | Risk definition; |

| – | Risk culture, overriding principles and minimum standards; |

| – | Governance, roles and responsibilities; and |

| – | Internal control system. |

During the first half of 2015, there have been no significant changes to the Risk Framework or the risk governance arrangements as described in the ‘Risk governance’ section in the 2014 Annual Report.

Risk culture, overriding principles and minimum standards

Risk culture plays an important role in our aim to be the best bank for our people, customers, shareholders and communities. Having a strong unified culture is critical to success. Risk culture is embedded into all business units through the implementation of the Santander UK Risk Framework (including Risk Attestations) and a programme of initiatives aligned to our Risk Culture Statement.

During the first half of 2015 we continued our programme of initiatives to help strengthen and embed the risk management culture across Santander UK. Building on the progress made in Retail and Commercial Banking, we are extending our focus across other segments, including Corporate & Institutional Banking. The main aims of this programme are to:

| – | Help embed the Risk Framework through ensuring personal accountability for risk; |

| – | Reinforce the importance of identification, assessment, management, and reporting of all risks. This is achieved through communication, education and training at all levels; |

| – | Enhance and embed risk management across the whole employee life-cycle including recruitment, performance management, and reward; |

| – | Measure behavioural change through ‘speaking up’ campaigns and surveys; and |

| – | Improve the identification and management of risk in planning and change projects. |

Mandatory risk management training was undertaken throughout the period to promote the understanding of Santander UK’s values and risk culture.

| 12 | Santander UK plc |

Table of Contents

Risk governance | emerging risks | Credit risk | Market risk | Balance sheet management risk | Other important risks | Areas of focus and other items | ||||||

|

Top risks in H1 2015 | Strategic priority: | |||

| Loyal and satisfied retail customers | |||

| ‘Bank of Choice’ for UK companies | |||

| Consistent profitability and a strong balance sheet | |||

| Risk indicator | Risk features, impacts and developments in the first half of 2015 | Strategic priorities | ||||

Banking market |

| Banking market risk could lead to lower income or a loss of value from changes in interest rates. The current low rate environment remains a key concern. We monitor forecasted rates closely and keep our options under review. Net interest margin (‘NIM’) and economic value of equity (‘EVE’) sensitivities were relatively unchanged during the first half of 2015 as the growth in bank account liability volumes was largely offset by additional unhedged fixed rate assets.

|  | |||

Capital |

| Capital risk has the potential to disrupt our business model and stop the normal functions of Santander UK. Failure to meet the capital requirements of regulators could lead them to constrain dividend payments or to resolve Santander UK. The CET 1 capital ratio was 11.7% at 30 June 2015 and was impacted by the commencement of the PSA cooperation in our consumer finance business. The PRA end-point Tier 1 leverage ratio was 4.1%, up from 3.8% at 31 December 2014.

| | |||

Conduct |

| Conduct risk is a key factor in determining if we are meeting our aim to be the best bank for our customers. The remaining provision for PPI redress and related costs amounted to £73m. Monthly utilisation, including proactive customer contact, during the first half of 2015 decreased to £9m per month, against an average of £11m in 2014. Excluding proactive customer contact, the average redress costs during the first half of the year were £6m per month. The high proportion of invalid complaints also continued. Existing non-PPI related conduct provisions amounted to £159m.

|  | |||

Credit |

| Credit risk could reduce the value of our assets as well as increase write-offs and impairment loan loss allowances. The total NPL ratio of 1.68% at 30 June 2015 continued to improve, with retail and corporate loans performing well in an improving credit environment.

| | |||

Liquidity |

| Liquidity risk could affect our ability to meet our financial obligations as well as disrupt our day-to-day operations, business model or lead to the insolvency of Santander UK. Although credit ratings downgrade risk (and the associated impact this might have on the group’s liquidity position) in the medium term has reduced, longer-term risk remains due to the possibility that the Santander UK group’s senior debt issuance plan fall short of expectations over the next two years (whether this is due to eurozone concerns or other causes).

|  | |||

Operational |

| Operational risk could impact any aspect of our business or support processes associated with people, systems or external events which could prevent us from achieving our desired business objectives. The industry-wide threat from cyber- attacks continues to rise; criminal methods are increasing in sophistication, and use of mobile and internet-based products continues to grow. We are mitigating these risks through IT enhancement, and further development of our cyber-threat intelligence function.

| | |||

Pension |

| Pension risk arises to the extent that the assets of the defined benefit pension schemes do not fully match the timing and amount of the schemes’ liabilities and can impact our financial results and capital metrics. The current low interest rate environment remains a concern, as does the potential for assets to fall in value. These risks are monitored closely and strategies to manage their impact kept under review. The Scheme’s accounting position was broadly unchanged at £180m surplus at 30 June 2015 (31 December 2014: £156m surplus).

| | |||

See ‘Banking market risk’ on page 53.

See ‘Banking market risk’ on page 53.

See ‘Capital risk’ on page 64.

See ‘Capital risk’ on page 64.

| (1) | Non-IFRS measure. See page 139. |

| 2015 Half Yearly Financial Report | 13 |

Table of Contents

Risk review

Top and emerging risks

continued

Emerging and

future risks

| Timeframe | Risk description and mitigation | Strategic priorities | ||

1-3 years | The UK economy The financial performance of Santander UK is intrinsically linked to the UK economy. This is particularly so for those aspects that have greatest influence on our larger credit portfolios, such as the housing market and unemployment. In turn, the prospects for the UK are also dependent, to a degree, on the economies of other major trading areas, such as the eurozone.

If the UK economy continues to improve, interest rates are expected to rise, especially if inflation moves back towards the Bank of England’s target rate. In such a scenario, the behaviour of our customers and other market participants might change. This could include increased customer movement and more competitive product pricing.

If the UK economy doesn’t continue to recover as expected, or even experiences a downturn, Bank of England interest rates may remain at record low levels or even be reduced further. This could affect credit losses, net interest margins and pension risk.

We continue to monitor these risks regularly, and assess their potential impacts with scenario analysis. |  | ||

New and emerging regulation The aftermath of the financial crisis has seen the emergence of a significant volume of additional regulation in the UK, the US and other jurisdictions. In some cases, the impact on Santander UK has become clearer and more precisely quantified. In response to these new regulations, a number of significant change projects are already under way, including those relating to the Financial Services (Banking Reform) Act 2013. We regularly assess the potential impact of regulation to gauge its implications on our risk profile and financial resources, including capital. However, there also remains a significant body of emerging regulation where the impact and timing remain uncertain.

The first half of 2015 has also seen the advent of further market reviews which may affect our business. | | |||

IT and business change Santander UK continues to invest in new IT platforms and systems, to support its strategic growth plans. There are also a number of key business change initiatives under way, the successful delivery of which is crucial to meet regulatory demands and strategic aims. As with any significant change programmes of this nature, we continue to monitor and control the risks associated with the pace of change. | | |||

New competitors and technology Innovations in technology continued to develop at a rapid pace. We have also seen the advent of new financial services providers. These factors bring with them the potential for increased levels of competition in the medium term.

| | |||

More than 3 years | The UK and European political environments Following the May 2015 UK general election, the UK Government committed to renegotiating the terms of the UK’s membership of the European Union and subsequently holding a referendum.

The EU itself also continues to face uncertainty, especially as the economic and political environment develops, particularly in eurozone member states, including Greece. We continue to monitor the potential consequences for our business plan from any associated impacts.

| | ||

| 14 | Santander UK plc |

Table of Contents

Risk governance | Top and emerging risks | Credit risk | Market risk | Balance sheet management risk | Other important risks | Areas of focus and other items | ||||||

|

During the first half of 2015, there have been no significant changes to Santander UK’s credit risk management policies, as described in the ‘Credit risk management’ section in the 2014 Annual Report.

Maximum exposure and net exposure to credit risk

The tables below set out the main differences between the Santander UK group’s maximum exposure and net exposure to credit risk. They show the effects of collateral, netting, and risk transfer to mitigate the Santander UK group’s exposure. The tables present only those financial assets subject to credit risk.

For balance sheet assets, the maximum exposure to credit risk represents the carrying value after allowance for impairment. Off-balance sheet exposures comprise guarantees, formal standby facilities, credit lines and other commitments. For off-balance sheet guarantees, the maximum exposure is the maximum amount that Santander UK would have to pay if the guarantees were to be called upon. For formal standby facilities, credit lines and other commitments that are irrevocable over the life of the respective facilities, the maximum exposure is the full amount of the committed facilities.

| Maximum exposure | Collateral | |||||||||||||||||||||||||||||||||||

| Balance sheet asset | ||||||||||||||||||||||||||||||||||||

| Gross amounts | Loan loss allowance | Net amounts | Off-balance sheet | Cash(1) | Non-cash(1) | Netting(2) | Risk transfer(3) | Net exposure | ||||||||||||||||||||||||||||

30 June 2015 | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | |||||||||||||||||||||||||||

Cash and balances at central banks | 15.2 | — | 15.2 | — | — | — | — | — | 15.2 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Trading assets: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to banks | 7.1 | — | 7.1 | — | — | — | (1.7 | ) | — | 5.4 | ||||||||||||||||||||||||||

- Loans and advances to customers | 5.6 | — | 5.6 | — | — | (4.1 | ) | — | — | 1.5 | ||||||||||||||||||||||||||

- Debt securities | 5.9 | — | 5.9 | — | — | — | — | — | 5.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total trading assets | 18.6 | — | 18.6 | — | — | (4.1 | ) | (1.7 | ) | — | 12.8 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Financial assets designated at fair value: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to customers | 2.1 | — | 2.1 | 0.2 | — | (2.3 | ) | — | — | — | ||||||||||||||||||||||||||

- Debt securities | 0.6 | — | 0.6 | — | — | — | — | — | 0.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total financial assets designated at fair value | 2.7 | — | 2.7 | 0.2 | — | (2.3 | ) | — | — | 0.6 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Available-for-sale debt securities | 9.1 | — | 9.1 | — | — | — | — | — | 9.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Derivative financial instruments | 20.6 | — | 20.6 | — | (0.7 | ) | — | (17.0 | ) | — | 2.9 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to banks | 2.5 | — | 2.5 | 1.2 | — | (0.9 | ) | — | (0.1 | ) | 2.7 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to customers(4): | ||||||||||||||||||||||||||||||||||||

- Advances secured on residential property | 151.2 | (0.6 | ) | 150.6 | 6.7 | — | (157.2 | ) | — | — | 0.1 | |||||||||||||||||||||||||

- Corporate loans | 30.8 | (0.4 | ) | 30.4 | 15.1 | (0.1 | ) | (22.7 | ) | — | — | 22.7 | ||||||||||||||||||||||||

- Finance leases | 6.4 | (0.1 | ) | 6.3 | — | (0.1 | ) | (5.2 | ) | — | — | 1.0 | ||||||||||||||||||||||||

- Other secured advances | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

- Other unsecured advances | 6.7 | (0.2 | ) | 6.5 | 12.1 | — | — | — | — | 18.6 | ||||||||||||||||||||||||||

- Amounts due from fellow subsidiaries, associates and joint ventures | 1.1 | — | 1.1 | — | — | — | — | — | 1.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total loans and advances to customers | 196.2 | (1.3 | ) | 194.9 | 33.9 | (0.2 | ) | (185.1 | ) | — | — | 43.5 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and receivables securities(4) | 0.1 | — | 0.1 | — | — | — | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total | 265.0 | (1.3 | ) | 263.7 | 35.3 | (0.9 | ) | (192.4 | ) | (18.7 | ) | (0.1 | ) | 86.9 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| (1) | The forms of collateral which Santander UK takes to mitigate credit risk include: residential and commercial property; other physical assets, including motor vehicles; liquid securities, including those transferred under reverse repurchase agreements; cash, including that which is used to collateralise derivative transactions; and receivables. In terms of exposure, charges on residential property represent the majority of collateral taken. |

| (2) | Credit risk exposures can be reduced by applying netting and set-off. Santander UK uses this approach mainly for derivative and repurchase transactions with financial institutions. For derivatives transactions, Santander UK uses standard master netting agreements (e.g. ISDA). These agreements allow for netting of credit risk exposure to a counterparty resulting from a derivative transaction against Santander UK’s obligations to the counterparty in the event of default, to produce a lower net credit exposure. They may also reduce settlement exposure. |

| (3) | Certain financial instruments can be used to transfer credit risk from Santander UK to another counterparty. The main form of risk transfer employed by Santander UK is the use of credit default swaps, principally transacted with other banks. |

| (4) | Loans and advances to customers and loans and receivables securities include interest charged to the customer’s account and interest accrued but not yet charged to the account. |

| 2015 Half Yearly Financial Report | 15 |

Table of Contents

Risk review

Credit risk

| Maximum exposure | Collateral | |||||||||||||||||||||||||||||||||||

| Balance sheet asset | ||||||||||||||||||||||||||||||||||||

31 December 2014 | Gross amounts £bn | Loan loss allowance £bn | Net amounts £bn | Off-balance sheet £bn | Cash(1) £bn | Non-cash(1) £bn | Netting(2) £bn | Risk transfer(3) £bn | Net exposure £bn | |||||||||||||||||||||||||||

Cash and balances at central banks | 22.6 | — | 22.6 | — | — | — | — | — | 22.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Trading assets: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to banks | 5.9 | — | 5.9 | — | — | — | (0.8 | ) | — | 5.1 | ||||||||||||||||||||||||||

- Loans and advances to customers | 3.0 | — | 3.0 | — | — | (2.2 | ) | — | — | 0.8 | ||||||||||||||||||||||||||

- Debt securities | 8.0 | — | 8.0 | — | — | — | — | �� | — | 8.0 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total trading assets | 16.9 | — | 16.9 | — | — | (2.2 | ) | (0.8 | ) | — | 13.9 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Financial assets designated at fair value: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to customers | 2.3 | — | 2.3 | 0.2 | — | (2.4 | ) | — | — | 0.1 | ||||||||||||||||||||||||||

- Debt securities | 0.6 | — | 0.6 | — | — | — | — | — | 0.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total financial assets designated at fair value | 2.9 | — | 2.9 | 0.2 | — | (2.4 | ) | — | — | 0.7 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Available-for-sale debt securities | 8.9 | — | 8.9 | — | — | — | — | — | 8.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Derivative financial instruments | 23.0 | — | 23.0 | — | (1.3 | ) | — | (19.2 | ) | — | 2.5 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to banks | 2.1 | — | 2.1 | 1.7 | — | (0.3 | ) | — | (0.1 | ) | 3.4 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to customers(4): | ||||||||||||||||||||||||||||||||||||

- Advances secured on residential property | 150.5 | (0.6 | ) | 149.9 | 6.7 | — | (156.5 | ) | — | — | 0.1 | |||||||||||||||||||||||||

- Corporate loans | 29.9 | (0.6 | ) | 29.3 | 14.9 | (0.1 | ) | (20.1 | ) | — | — | 24.0 | ||||||||||||||||||||||||

- Finance leases | 2.7 | — | 2.7 | — | (0.1 | ) | (2.2 | ) | — | — | 0.4 | |||||||||||||||||||||||||

- Other secured advances | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

- Other unsecured advances | 6.2 | (0.2 | ) | 6.0 | 11.2 | — | — | — | — | 17.2 | ||||||||||||||||||||||||||

- Amounts due from fellow subsidiaries, associates and joint ventures | 0.8 | — | 0.8 | — | — | — | — | — | 0.8 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total loans and advances to customers | 190.1 | (1.4 | ) | 188.7 | 32.8 | (0.2 | ) | (178.8 | ) | — | — | 42.5 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and receivables securities(4) | 0.1 | — | 0.1 | — | — | — | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total | 266.6 | (1.4 | ) | 265.2 | 34.7 | (1.5 | ) | (183.7 | ) | (20.0 | ) | (0.1 | ) | 94.6 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| (1) | The forms of collateral which Santander UK takes to mitigate credit risk include: residential and commercial property; other physical assets, including motor vehicles; liquid securities, including those transferred under reverse repurchase agreements; cash, including that which is used to collateralise derivative transactions; and receivables. In terms of exposure, charges on residential property represent the majority of collateral taken. |

| (2) | Credit risk exposures can be reduced by applying netting and set-off. Santander UK uses this approach mainly for derivative and repurchase transactions with financial institutions. For derivatives transactions, Santander UK uses standard master netting agreements (e.g. ISDA). These agreements allow for netting of credit risk exposure to a counterparty resulting from a derivative transaction against Santander UK’s obligations to the counterparty in the event of default, to produce a lower net credit exposure. They may also reduce settlement exposure. |

| (3) | Certain financial instruments can be used to transfer credit risk from one counterparty to another. The main form of risk transfer employed by Santander UK is through the use of credit default swaps, principally transacted with banks. |

| (4) | Loans and advances to customers and loans and receivables securities include interest charged to the customer’s account and interest accrued but not yet charged to the account. |

Credit quality

Santander UK uses a single rating scale to provide a consistent approach for reporting default risk across all the credit risk portfolios. The scale is comprised of eight grades for non-defaulted exposures numbered from 9 (lowest risk) to 2 (highest risk). Each grade is defined by an upper and lower probability of default (‘PD’) value and is scaled so that the default risk increases by a factor of 10 for every 2 step reduction in the grade number. For example, risk grade 9 equates to an average PD of 0.01%, and risk grade 7 equates to an average PD of 0.1%. Defaulted exposures are assigned to grade 1 and a PD value of 100%. An approximation to the equivalent credit rating grade used by Standard and Poor’s Ratings Services (‘S&P’) is shown in the final column of the table.

| PD range | ||||||||||||||||

Santander UK risk grade | Mid % | Lower % | Upper % | S&P equivalent | ||||||||||||

9 | 0.010 | 0.000 | 0.021 | AAA to AA- | ||||||||||||

8 | 0.032 | 0.021 | 0.066 | A+ to A | ||||||||||||

7 | 0.100 | 0.066 | 0.208 | A- to BBB+ | ||||||||||||

6 | 0.316 | 0.208 | 0.658 | BBB to BBB- | ||||||||||||

5 | 1.000 | 0.658 | 2.081 | BB+ to BB- | ||||||||||||

4 | 3.162 | 2.081 | 6.581 | B+ to B | ||||||||||||

3 | 10.000 | 6.581 | 20.811 | B- to CCC | ||||||||||||

2 | 31.623 | 20.811 | 99.999 | CC TO C | ||||||||||||

1 Default | 100.000 | 100.000 | 100.000 | D | ||||||||||||

| 16 | Santander UK plc |

Table of Contents

Risk governance | Top and emerging risks | Credit risk | Market risk | Balance sheet management risk | Other important risks | Areas of focus and other items | ||||||

|

The tables below set out the distribution across the credit rating master scale for those financial assets subject to credit risk. For further detail and commentary on the credit rating profiles of key portfolios, see the Retail Banking (i.e. residential mortgages), Commercial Banking, Corporate & Institutional Banking and Corporate Centre sections.

| Santander UK rating guide | ||||||||||||||||||||||||||||||||||||

| 9 (AAA to AA-) | 8 (A+ to A) | 7 (A- to BBB+) | 6 (BBB to BBB-) | 5 (BB+ to BB-) | 4 (B+ to B) | 1 to 3 (B- to D) | Other(1) | Total | ||||||||||||||||||||||||||||

30 June 2015 | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | |||||||||||||||||||||||||||

Cash and balances at central banks | 14.1 | — | — | — | — | — | �� | — | 1.1 | 15.2 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Trading assets: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to banks | 0.2 | 2.4 | 4.4 | 0.1 | — | — | — | — | 7.1 | |||||||||||||||||||||||||||

- Loans and advances to customers | 0.7 | 4.6 | 0.3 | — | — | — | — | — | 5.6 | |||||||||||||||||||||||||||

- Debt securities | 2.0 | 2.9 | 0.5 | 0.5 | — | — | — | — | 5.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Trading assets | 2.9 | 9.9 | 5.2 | 0.6 | — | — | — | — | 18.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Financial assets designated at fair value | ||||||||||||||||||||||||||||||||||||

- Loans and advances to customers | 0.7 | 0.7 | 0.6 | — | — | — | — | 0.1 | 2.1 | |||||||||||||||||||||||||||

- Debt securities | — | 0.2 | 0.1 | 0.1 | — | — | — | 0.2 | 0.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Financial assets designated at fair value | 0.7 | 0.9 | 0.7 | 0.1 | — | — | — | 0.3 | 2.7 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Available-for-sale debt securities | 7.3 | 1.3 | 0.5 | — | — | — | — | — | 9.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Derivative financial instruments | 0.4 | 11.5 | 6.3 | 1.5 | 0.5 | — | — | 0.4 | 20.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to banks | 0.2 | 1.7 | 0.1 | 0.5 | — | — | — | — | 2.5 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to customers(2): | ||||||||||||||||||||||||||||||||||||

- Advances secured on residential property | 1.5 | 17.4 | 67.7 | 43.6 | 7.7 | 7.0 | 6.3 | — | 151.2 | |||||||||||||||||||||||||||

- Corporate loans | 2.8 | 3.4 | 3.0 | 8.3 | 7.3 | 3.7 | 0.9 | 1.4 | 30.8 | |||||||||||||||||||||||||||

- Finance leases | — | — | 0.4 | 1.2 | 2.0 | 1.7 | 0.9 | 0.2 | 6.4 | |||||||||||||||||||||||||||

- Other secured advances | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

- Other unsecured advances | — | — | 0.2 | 1.4 | 2.6 | 1.0 | 0.5 | 1.0 | 6.7 | |||||||||||||||||||||||||||

- Amounts due from fellow subsidiaries, associates & joint ventures | 1.1 | — | — | — | — | — | — | — | 1.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Loans and advances to customers | 5.4 | 20.8 | 71.3 | 54.5 | 19.6 | 13.4 | 8.6 | 2.6 | 196.2 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and receivables securities(2) | — | — | — | — | — | 0.1 | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| 31.0 | 46.1 | 84.1 | 57.2 | 20.1 | 13.5 | 8.6 | 4.4 | 265.0 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Loan loss allowance | (1.3 | ) | ||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Total | 263.7 | |||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Of which: | ||||||||||||||||||||||||||||||||||||

Neither past due nor impaired: | ||||||||||||||||||||||||||||||||||||

- Cash and balances at central banks | 14.1 | — | — | — | — | — | — | 1.1 | 15.2 | |||||||||||||||||||||||||||

- Trading assets | 2.9 | 9.9 | 5.2 | 0.6 | — | — | — | — | 18.6 | |||||||||||||||||||||||||||

- Financial assets designated at fair value | 0.7 | 0.9 | 0.7 | 0.1 | — | — | — | 0.3 | 2.7 | |||||||||||||||||||||||||||

- Available-for-sale debt securities | 7.3 | 1.3 | 0.5 | — | — | — | — | — | 9.1 | |||||||||||||||||||||||||||

- Derivative financial instruments | 0.4 | 11.5 | 6.3 | 1.5 | 0.5 | — | — | 0.4 | 20.6 | |||||||||||||||||||||||||||

- Loans and advances to banks | 0.2 | 1.7 | 0.1 | 0.5 | — | — | — | — | 2.5 | |||||||||||||||||||||||||||

- Loans and advances to customers | 5.4 | 20.8 | 71.3 | 54.5 | 19.5 | 13.3 | 3.8 | 2.6 | 191.2 | |||||||||||||||||||||||||||

- Loans and receivables securities | — | — | — | — | — | 0.1 | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total neither past due nor impaired | 31.0 | 46.1 | 84.1 | 57.2 | 20.0 | 13.4 | 3.8 | 4.4 | 260.0 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Past due but not impaired | — | — | — | — | 0.1 | — | 3.4 | — | 3.5 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Impaired(3) | — | — | — | — | — | 0.1 | 1.4 | — | 1.5 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| 31.0 | 46.1 | 84.1 | 57.2 | 20.1 | 13.5 | 8.6 | 4.4 | 265.0 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Loan loss allowance | (1.3 | ) | ||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Total | 263.7 | |||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

| (1) | Other items include cash in hand and smaller cases predominantly within the consumer finance and commercial mortgages portfolios which are subject to scorecards rather than rating models. |

| (2) | Loans and advances to customers and loans and receivables securities include interest charged to the customer’s account and interest accrued but not yet charged to the account. |

| (3) | Impaired loans consists of loans assessed for observed impairment loss allowances. |

| 2015 Half Yearly Financial Report | 17 |

Table of Contents

Risk review

Credit risk

continued

| Santander UK rating guide | ||||||||||||||||||||||||||||||||||||

| 9 (AAA to AA-) | 8 (A+ to A) | 7 (A- to BBB+) | 6 (BBB to BBB-) | 5 (BB+ to BB-) | 4 (B+ to B) | 1 to 3 (B- to D) | Other(1) | Total | ||||||||||||||||||||||||||||

31 December 2014 | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | £bn | |||||||||||||||||||||||||||

Cash and balances at central banks | 21.1 | — | — | — | — | — | — | 1.5 | 22.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Trading assets: | ||||||||||||||||||||||||||||||||||||

- Loans and advances to banks | 0.1 | 1.2 | 4.6 | — | — | — | — | — | 5.9 | |||||||||||||||||||||||||||

- Loans and advances to customers | — | 2.1 | 0.7 | 0.2 | — | — | — | — | 3.0 | |||||||||||||||||||||||||||

- Debt securities | 2.3 | 4.0 | 1.1 | 0.6 | — | — | — | — | 8.0 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Trading assets | 2.4 | 7.3 | 6.4 | 0.8 | — | — | — | — | 16.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Financial assets designated at fair value | ||||||||||||||||||||||||||||||||||||

- Loans and advances to customers | 0.4 | 0.8 | 1.0 | 0.1 | — | — | — | — | 2.3 | |||||||||||||||||||||||||||

- Debt securities | — | 0.2 | 0.1 | 0.1 | — | 0.2 | — | — | 0.6 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Financial assets designated at fair value | 0.4 | 1.0 | 1.1 | 0.2 | — | 0.2 | — | — | 2.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Available-for-sale debt securities | 8.9 | — | — | — | — | — | — | — | 8.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Derivative financial instruments | 0.4 | 10.8 | 9.7 | 1.4 | 0.4 | — | — | 0.3 | 23.0 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to banks | 0.3 | 1.4 | 0.3 | 0.1 | — | — | — | — | 2.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and advances to | ||||||||||||||||||||||||||||||||||||

- Advances secured on residential property | 2.3 | 16.1 | 65.2 | 44.2 | 8.1 | 7.7 | 6.9 | — | 150.5 | |||||||||||||||||||||||||||

- Corporate loans | 2.3 | 4.0 | 2.6 | 8.0 | 7.1 | 3.6 | 0.8 | 1.5 | 29.9 | |||||||||||||||||||||||||||

- Finance leases | — | — | 0.2 | 0.5 | 0.8 | 0.7 | 0.4 | 0.1 | 2.7 | |||||||||||||||||||||||||||

- Other secured advances | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

- Other unsecured advances | — | — | 0.2 | 1.0 | 2.5 | 1.0 | 0.5 | 1.0 | 6.2 | |||||||||||||||||||||||||||

- Amounts due from fellow subsidiaries, associates & joint ventures | 0.7 | — | — | — | 0.1 | — | — | — | 0.8 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total Loans and advances to customers | 5.3 | 20.1 | 68.2 | 53.7 | 18.6 | 13.0 | 8.6 | 2.6 | 190.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Loans and receivables securities(2) | — | — | 0.1 | — | — | — | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| 38.8 | 40.6 | 85.8 | 56.2 | 19.0 | 13.2 | 8.6 | 4.4 | 266.6 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Loan loss allowance | (1.4 | ) | ||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Total | 265.2 | |||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Of which: | ||||||||||||||||||||||||||||||||||||

Neither b past due nor impaired: | ||||||||||||||||||||||||||||||||||||

- Cash and balances at central banks | 21.1 | — | — | — | — | — | — | 1.5 | 22.6 | |||||||||||||||||||||||||||

- Trading assets | 2.4 | 7.3 | 6.4 | 0.8 | — | — | — | — | 16.9 | |||||||||||||||||||||||||||

- Financial assets designated at fair value | 0.4 | 1.0 | 1.1 | 0.2 | — | 0.2 | — | — | 2.9 | |||||||||||||||||||||||||||

- Available-for-sale debt securities | 8.9 | — | — | — | — | — | — | — | 8.9 | |||||||||||||||||||||||||||

- Derivative financial instruments | 0.4 | 10.8 | 9.7 | 1.4 | 0.4 | — | — | 0.3 | 23.0 | |||||||||||||||||||||||||||

- Loans and advances to banks | 0.3 | 1.4 | 0.3 | 0.1 | — | — | — | — | 2.1 | |||||||||||||||||||||||||||

- Loans and advances to customers | 5.3 | 20.1 | 68.2 | 53.6 | 18.4 | 12.8 | 3.5 | 2.5 | 184.4 | |||||||||||||||||||||||||||

- Loans and receivables securities | — | — | 0.1 | — | — | — | — | — | 0.1 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Total neither past due nor impaired | 38.8 | 40.6 | 85.8 | 56.1 | 18.8 | 13.0 | 3.5 | 4.3 | 260.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Past due but not impaired | — | — | — | — | 0.1 | — | 3.8 | — | 3.9 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Impaired(3) | — | — | — | 0.1 | 0.1 | 0.2 | 1.3 | 0.1 | 1.8 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| 38.8 | 40.6 | 85.8 | 56.2 | 19.0 | 13.2 | 8.6 | 4.4 | 266.6 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Loan loss allowance | (1.4 | ) | ||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

Total | 265.2 | |||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||

| (1) | Other items include cash in hand and smaller cases predominantly within the consumer finance and commercial mortgages portfolios which are subject to scorecards rather than rating models. |

| (2) | Loans and advances to customers and loans and receivables securities include interest charged to the customer’s account and interest accrued but not yet charged to the account. |

| (3) | Impaired loans consists of loans assessed for observed impairment loss allowances. |

| 18 | Santander UK plc |

Table of Contents

Risk governance | Top and emerging risks | Credit risk | Market risk | Balance sheet management risk | Other important risks | Areas of focus and other items | ||||||

|

Maturity analysis of loans and advances that are past due but not impaired

At 30 June 2015, loans and advances of £3.5bn (2014: £3.9bn) were past due but not impaired. Of these balances, £0.1bn (2014: £0.1bn) were due within one month, £1.1bn (2014: £1.2bn) were due after one month but within two months, £0.7bn (2014: £0.8bn) were due after two months but within three months, £0.8bn (2014: £1.0bn) were due after three months but within six months, and £0.8bn (2014: £0.8bn) were due after six months.

Concentrations of credit risk exposures