UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of report (Date of earliest event reported): August 3, 2009 (July 31, 2009)

JAG Media Holdings, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 000-28761 | 88-0380546 |

| | | |

(State or other jurisdiction of incorporation) | (Commission File Number) | (I.R.S. Employer Identification) |

6295 Northam Drive, Unit 8, Mississauga, Ontario, L4V 1W8

(Address of Principal Executive Offices)(Zip Code)

Registrant’s telephone number, including area code: 905.673.8501

6865 SW 18th Street, Suite B13

Boca Raton, Florida 33433

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

TABLE OF CONTENTS

Item 2.01 Completion of Acquisition or Disposition of Assets | 4 |

| | |

Item 3.02 Unregistered Sale of Equity Securities | 40 |

| | |

Item 5.01 Changes in Control of Registrant | 41 |

| | |

Item 5.02 Departure of Directors or Principal Officers; Election of Directors; Appointment Of Principal Officers | 41 |

| | |

Item 5.03 Amendment to Articles of Incorporation; Change in Fiscal Year End | 46 |

| | |

Item 9.01 Exhibits | 47 |

| | |

| 48 |

| |

EX-99.1: Press Release dated July 31, 2009 | 1 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains forward-looking statements, which reflect our views with respect to future events and financial performance. These forward-looking statements are subject to certain uncertainties and other factors that could cause actual results to differ materially from such statements. These forward-looking statements are identified by, among other things, the words “anticipates”, “believes”, “estimates”, “expects”, “plans”, “projects”, “targets” and similar expressions. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statement was made. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Important factors that may cause actual results to differ from those projected include the risk factors specified below.

USE OF DEFINED TERMS

Except as otherwise indicated by the context, references in this report to:

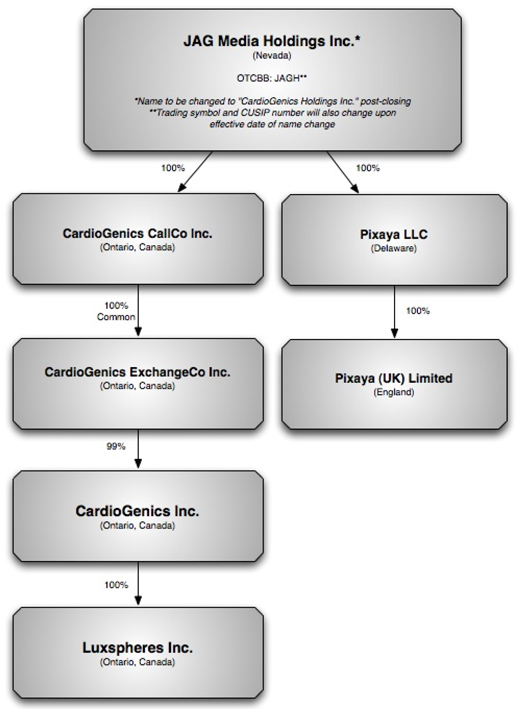

| . | “JAG Media,” “JAG,” “the Company,” “we,” “us,” or “our,” refers to the combined business of JAG Media Holdings, Inc., and its direct and indirect subsidiaries, CardioGenics CallCo Inc., CardioGenics ExchangeCo Inc., CardioGenics Inc., Pixaya LLC and Pixaya (UK) Limited; |

| . | “JAG Media” or “JAG” refers to JAG Media Holdings, Inc., a Nevada corporation; |

| . | “CallCo” refers to CardioGenics CallCo Inc., an Ontario, Canada corporation and our direct, wholly owned subsidiary, and/or its direct and indirect subsidiaries, as the case may be; |

| . | “ExchangeCo” refers to CardioGenics ExchangeCo Inc., an Ontario, Canada corporation and our indirect subsidiary and subsidiary of CallCo; |

| . | “CardioGenics” refers to CardioGenics Inc., an Ontario, Canada corporation and our indirect subsidiary and subsidiary of ExchangeCo; |

| . | “Pixaya” refers to Pixaya LLC, a Delaware limited liability company and our direct, wholly-owned subsidiary, and/or its wholly-owned subsidiary, Pixaya (UK) Limited, as the case may be; |

| . | “Share Purchase Agreement” refers to that certain share purchase agreement dated May 22, 2009 among JAG Media, ExchangeCo, CardioGenics and Yahia Gawad, the principal stockholder of CardioGenics, pursuant to which ExchangeCo agreed to acquire all of the outstanding CardioGenics common shares (other than 173,869 common shares owned by two (2) minority stockholders of CardioGenics); |

| . | “Trust Agreement” refers to that certain Voting and Exchange Trust Agreement dated July 6, 2009 among JAG Media, Exchangeco, and WeirFoulds LLP, as trustee, pursuant to which the parties make provision and establish procedures whereby, among other matters (a) voting rights in JAG Media shall be exercisable by the holders from time-to-time of the “Exchangeable Shares” (other than JAG Media and its subsidiaries) and (b) the holders of the Exchangeable Shares shall have the right to require JAG Media, ExchangeCo or another subsidiary to-be-created at the option of JAG Media to purchase the Exchangeable Shares from the holders, all in accordance with the terms of the Trust Agreement. |

| . | “Support Agreement” refers to that certain Support Agreement dated July 6, 2009 between JAG Media and ExchangeCo pursuant to which JAG Media is required to take various actions in connection with the Exchangeable Shares to insure that ExchangeCo is able to meet its obligations with respect to the holders and the Exchangeable Shares. |

| . | “Share Consideration” refers to the 422,183,610 JAG Common Shares issued to the CardioGenics stockholders at the closing of the acquisition of CardioGenics by ExchangeCo in consideration for the surrender to ExchangeCo of their CardioGenics Common Shares (a portion of which was issued indirectly in the form of Exchangeable Shares at the election of certain CardioGenics stockholders). |

| . | “JAG Common Shares” refers to the common stock of JAG Media, par value $0.00001. |

| . | “Series1 Preferred Shares“ refers to the Series 1 Preferred Stock of JAG Media, par value $0.0001. |

| . | “Exchangeable Shares” refers to the Exchangeable Shares of ExchangeCo, which are exchangeable into JAG Common Shares in accordance with the terms of the Trust Agreement and the rights and preferences of the Exchangeable Shares. |

| . | “CardioGenics Common Shares” refers to the common stock of CardioGenics. |

| . | “U.S. dollar,” “$” and “US$” refer to the legal currency of the United States; |

| . | “Securities Act” refers to the Securities Act of 1933, as amended; and |

| . | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

Item 2.01 - Completion of Acquisition or Disposition of Assets

OUR ACQUISITION OF CARDIOGENICS

On July 31, 2009 we completed the acquisition of CardioGenics by ExchangeCo, our Ontario, Canada subsidiary, pursuant to the terms of the Share Purchase Agreement. CardioGenics is considered the acquirer in the transaction for accounting and financial reporting purposes.

In connection with the acquisition, ExchangeCo acquired all of the outstanding CardioGenics Common Shares, excluding 173,869 CardioGenics Common Shares in the aggregate owned by two (2) minority stockholders of CardioGenics (the “Dissenting Stockholders”). Pursuant to the terms of the Share Purchase Agreement and in consideration for the surrender of their CardioGenics Common Shares, the CardioGenics stockholders had the option to receive at the closing their pro-rata allocation of the Share Consideration in the form of (a) JAG Common Shares or (b) Exchangeable Shares. Those CardioGenics stockholders who elected to receive directly JAG Common Shares were issued, in the aggregate, 145,528,195 JAG Common Shares at the closing and those CardioGenics stockholders who elected to receive Exchangeable Shares were issued 16 Exchangeable Shares at the closing, which are exchangeable at any time into 276,655,415 JAG Common Shares, in the aggregate. The Share Consideration issued at the closing provides the CardioGenics stockholders with direct and indirect ownership of approximately 85% of JAG Media’s outstanding common stock, on a fully diluted basis.

Immediately prior to the closing, all CardioGenics debenture holders converted their debentures into CardioGenics Common Shares in accordance with the terms of their respective debentures, as required by the terms of the Share Purchase Agreement. Accordingly, such former debenture holders became CardioGenics stockholders for purposes of the acquisition and received their pro-rata allotment of the Share Consideration in the form of JAG Common Shares and/or Exchangeable Shares at the closing in consideration for the surrender of the CardioGenics Common Shares they received upon conversion of their debentures.

Also prior to the closing, CardioGenics closed on an equity investment round of financing totaling $2,715,000. These equity investors in CardioGenics became CardioGenics stockholders for purposes of the acquisition and received their pro-rata allotment of the Share Consideration in the form of JAG Common Shares.

On March 12, 2009 we entered into a Standby Equity Distribution Agreement with YA Global Master SPV Ltd. (“YA Ltd ”) (the “ SEDA ”) pursuant to which YA Ltd agreed to purchase up to $5,000,000 of our common stock (the “ Commitment Amount ”) over the course of the thirty-six (36) months following the date the registration statement for the shares to be issued pursuant to the SEDA is first declared effective (the “ Commitment Period ”). We will have the right, but not the obligation, to sell common stock to YA Ltd during the Commitment Period. Concurrent with the execution of the SEDA, we also entered into a Registration Rights Agreement with YA Ltd pursuant to which we agreed to register the shares of our common stock to be issued in connection with the SEDA. We intend to file such registration statement after the closing, in accordance with the terms of the Registration Rights Agreement

A more detailed summary of the terms of the SEDA and the Registration Rights Agreement, along with copies of both agreements, are contained in a Current Report on Form 8-K filed on March 12, 2009.

All JAG Common Shares received by CardioGenics stockholders in exchange for their CardioGenics Common Shares shall not be registered for resale and, therefore, shall remain subject to the rights and restrictions of Rule 144. All Exchangeable Shares received by CardioGenics stockholders in exchange for their CardioGenics Common Shares (and any JAG Common Shares into which such Exchangeable Shares may be exchanged) shall not be registered for resale prior to six (6) months following the closing and, therefore shall remain subject to the rights and restrictions of Rule 144 prior to any such registration.

Also at the closing, all holders of CardioGenics warrants entitling the holders to purchase CardioGenics Common Shares at various prices exchanged their CardioGenics warrants for warrants to purchase, in the aggregate, 36,148,896 JAG Common Shares at exercise prices of $0.047 per share, in accordance with the terms of the Share Purchase Agreement and the respective warrants. The terms of these newly issued warrants did not include any registration rights for the warrant holders. CardioGenics had no options to acquire CardioGenics Common Shares outstanding as of the closing.

At the closing, our current directors resigned as directors of JAG Media and its subsidiaries after appointing their successors and our current officers also resigned as officers and executives of JAG Media and its subsidiaries. After their resignation and the closing, our former directors entered into consulting agreements with the Company pursuant to which they will render various services to assist us in connection with certain transition matters. A more detailed discussion of this change in control is contained in Item 5.01 of this report.

Immediately following the closing, a majority of our stockholders approved, by written consent, an amendment to our articles of incorporation, which provided for (a) a change in our corporate name from “JAG Media Holdings, Inc.“ to “CardioGenics Holdings Inc.” and (b) an increase in the number of our authorized JAG Common Shares from 500,000,000 to 650,000,000. A more detailed discussion of the amendment to our articles of incorporation is contained in Item 5.03 of this report.

OUR CORPORATE HISTORY

Background of JAG Media

We have been providing financial information to the investment community since 1989. In May 1999, we began offering our services on a subscription fee basis to the general public for the first time through our website at jagnotes.com. Through our website and our traditional fax-based service, we offer timely financial data, reports and commentary.

Our online services currently consist of a subscription-based service that offers two specific products, the JAGNotes (Upgrade/Downgrade) Report and the Rumor Room, providing timely market reports, including breaking news and potentially market moving information. We currently derive revenues primarily from the sale of subscriptions.

From 1989 to 1992, we operated as an unincorporated business entity. In 1992, we incorporated in the State of New Jersey as New Jag, Inc. On December 14, 1993, JagNotes, Inc. merged with and into New Jag Inc., and we changed our name to JagNotes, Inc. We operated as JagNotes, Inc. until March 1999 when we were acquired by Professional Perceptions, Inc., a Nevada corporation, which subsequently changed our name to JagNotes.com Inc.

Until 1999, we targeted only a limited audience of financial professionals and did not engage in organized sales and marketing efforts. In 1999, we decided to change focus by expanding onto the Internet and targeting retail subscribers with the hope of expanding our subscriber base and business.

We undertook a corporate reorganization in January 2002 in order to distinguish and better manage separate areas of business. On January 4, 2002, we formed JAG Media LLC, a Delaware limited liability company and wholly owned subsidiary. The assets and liabilities of our current fax and Internet subscription business were transferred to JAG Media LLC. In order to better reflect the overall business in which we expected to engage and the corporate structure we intended to use to conduct that business, we changed our name from JagNotes.com Inc. to JAG Media Holdings, Inc. effective April 8, 2002.

On November 24, 2004, through one of our subsidiaries, Pixaya (UK) Limited (“Pixaya”), we purchased certain development stage software products and related assets in the United Kingdom from TComm Limited, a company organized in the United Kingdom. We subsequently changed the name of our subsidiary, JAG Media LLC, to Pixaya LLC in order to better reflect its role as owner of Pixaya and primary provider of support for our Pixaya products in the United States. Due to cash constraints, we ceased financing development and marketing by Pixaya of our SurvayaCam product, a mobile surveillance system which streams live video in real time from the point of use back to a control center and, if desired, to other locations. To date, we have only made minimal sales of SurvayaCam as part of our prior marketing and distribution efforts.

In light of the difficulties we encountered in growing our JAG Notes subscription business and Pixaya business, we began seeking merger and acquisition candidates, in related and unrelated lines of businesses, to augment our current business. On July 31, 2009, we completed the acquisition of CardioGenics, a developer of products targeting the immunoassay segment of the point-of-care in vitro diagnostic (“IVD”) testing market, based in Ontario, Canada. See “—Our Acquisition of CardioGenics.”

Background of CardioGenics

CardioGenics was founded in Toronto, Canada in 1997 by Dr. Yahia Gawad to develop technology and products targeting the immunoassay segment of the IVD testing market. These include:

| | § | The QL Care Analyzer (“QLCA”), a state-of-the-art proprietary point of care (“POC”) immunoanalyzer; |

| | § | A series of immunoassay tests to detect cardiac markers (the “Cardiovascular Tests”); and |

| | § | Paramagnetic beads developed through our proprietary method, which improves their light collection (“Beads”). |

OUR BUSINESS

Overview

Following our acquisition of CardioGenics, our primary business now focuses on developing products and components for the IVD testing market. We operate in that market through our Ontario, Canada subsidiary, CardioGenics. An overview of our current corporate structure is set forth in the diagram below

QL Care Analyzer

The QLCA represents a shift in the design POC analyzers. The QLCA is small, portable, stand-alone and completely automated point-of-care immunoanalyzer. The QLCA has successfully miniaturized lab test technology, and combined it with a simplified mechanical design and proprietary triggering mechanism.

The QLCA uses a proprietary self-metering cartridge to perform immunoassay tests at the POC. Each cartridge is pre-loaded with our beads, which have been coated with specific bioluminescent proteins linked to the target marker. A drop of whole blood added to the Cartridge creates the chemiluminescent reaction needed to deliver sensitive and accurate test results. Operation of the QLCA does not require specialized training and testing can be completed in 15 minutes.

POC immunoassay analyzers are not new, however, none of the commercial analyzers can replicate the sensitivity and accuracy of a test done in a medical lab. The QLCA delivers the required laboratory sensitivity and accuracy. The QLCA employs chemical light generation or “chemiluminescence“ (“CL“), the same technology used in the medical labs. The QLCA uses a patented automated electronic process to trigger CL, which enhances light collection, speeds up marker binding and increases sensitivity.

We have rigorously tested the QLCA protocols and have compared our test results against medical laboratory test data. Based on these internal test results, we have consistently met or exceeded the sensitivity standards of medical laboratory immunoassay equipment.

Cardiovascular Tests

To support the use of the QLCA, we have developed four immunoassay tests designed to identify cardiac markers in the blood at the time of a heart attack.

| | |

| Troponin I (TnI) | | § TnI testing is the current routine testing for a heart attack. § TnI is a heart muscle protein, released in the bloodstream shortly after a heart attack (myocardial infarction or MI). § Current laboratory analyzers cannot detect TnI before 4-6 hours after the onset of symptoms, when TnI concentration in the blood reaches its detection threshold. § Our test will take only 15 minutes to deliver quantitative results, allowing physicians to obtain much more rapid results and therefore accelerate patient triage. |

| Plasminogen Activator Inhibitor Type-1 (PAI-1) | | § This test will help to optimize the performance of a heart drug (“tPA” or tissue Plasminogen Activator), a clot buster used as the first line of therapy for MI patients. § This proprietary whole blood test will quantify PAI-1 levels within 15 minutes. |

| | |

| | | § Forty percent of patients do not respond to tPA, a fact recognized only after the “golden hour” (the time period in which permanent heart damage can be prevented) has passed. |

| | | |

| Heart Failure Risk Stratification (HFRS) | | § We have discovered a family of related proteins that are released into the bloodstream during heart failure. § We are developing a proprietary test, the Heart Failure Risk Stratification or HFRS test to stratify the risk of death in patients with heart failure, thus permitting the initiation of appropriate therapy at an early stage. |

| Heart Failure Genomics Risk (HFGR) | | § We are developing a proprietary HFGR test that predicts the response of heart failure patients to routinely administered drugs. § The need to measure the precise response to these drugs in a timely manner would minimize the trial and error methods now used by doctors to optimize drugs best suited to each patient. |

These tests are designed to be administered sequentially in the diagnostic process and management of patients with heart disease. The full scope of our core technology, as well as the know-how we have developed respecting aspects of chemical entrapment in bioassays, are covered under our patent applications.

Upon receipt of FDA approval, we intend to market the QLCA and the Cardiovascular Tests through a major IVD distributor. We have initiated discussions with a number of the Tier 1 IVD companies, and we anticipate that we will select a partner before we receive FDA approval. In accordance with industry practice, we intend to enter into a license agreement with our distribution partner for the manufacture and distribution of our products.

Paramagnetic Beads

Medical laboratories widely use paramagnetic particles as a solid surface in heterogeneous immunoassay tests utilizing the process of phase separation done by eletromagnetical field. Such tests involve the measurement of light generated on the surface area of paramagnetic beads coated with bio-organic material.

Our Beads represent a significant product advance. Most paramagnetic beads are made of iron oxide, and all are traditionally black or brown. We have developed a proprietary process that coats the beads with a layer of silver, making them white, and more sensitive to light. Our production process is also significantly less expensive than those used by our competitors. We have internally tested our Beads against all commercially available beads, and have found our silver-coated Beads to be five times more sensitive than traditional black or brown magnetic particles.

While the CardioGenics business described above is now our primary business, we intend, for the time being, to continue to operate our pre-closing JAG Notes subscription business.

OUR INDUSTRY

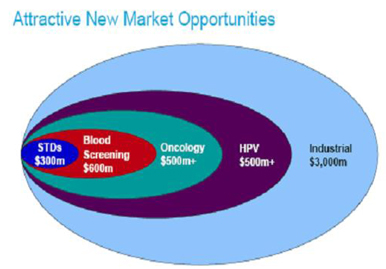

IVD Market

In vitro diagnostics (IVD) refers to testing that aim for the identification of diseases states outside the body, using samples such as body fluids (blood, urine) and tissues (biopsies and tissue sections). The IVD is a well established market, offering essential products (tests, components and machinery) used by physicians and clinical chemistry personnel to assess disease conditions. The world market for IVD is estimated at $42 billion in 2007 and is expected to grow 6% annually to $56.3 billion by 20121. North America, Europe, Japan and Western Europe currently make up 81% of the total IVD market, and this is expected to decrease to 76% by 2012 as China and India become more significant players in the IVD market. Sales of IVD products in emerging economies in Latin America and Eastern Europe are expected to grow from 4% of the market in 2007 to 5% in 2012. Overall, sales growth of IVD products in emerging markets will account for 10-20% annual growth in the IVD market, while the developed world will see annual growth of 3-6%.2

The following table summarizes the market size and projections of the IVD market and the sub-sectors where our products will compete:

| Product | | 2007 | | | 2008 | | | 2009 | | | 2010 | | | 2011 | |

| IVD (billions) | | | 42.1 | | | | 44.5 | | | | 47.1 | | | | 49.1 | | | | 52.9 | |

| Immunoassay Testing (millions) | | | 4.185 | | | | 4.435 | | | | 4.695 | | | | 4.975 | | | | 5.260 | |

| POC Testing (millions) | | | 1.625 | | | | 1.715 | | | | 1.815 | | | | 1.910 | | | | 2.02 | |

| Cardiac Marker Tests (millions) | | | 425 | | | | 471.75 | | | | 523.64 | | | | 581.24 | | | | 645.17 | |

Source: Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008

In 2007 16 top tier IVD companies occupied 78% of the global market ($32,000,000,000). Since 2005, there has been a trend toward consolidation at all levels of the IVD market. In 2007, three top tier companies, DPC, Dade Behring and Bayer Diagnostics, merged to become Siemens Medical Diagnostics.

1 This includes all laboratory, hospital-based products and OTC products, according to Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008

2 Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008, p3

Immunoassay Market

The 2007 world market for all immunoassays excluding infectious diseases is estimated at $4, 185 million3, and by 2012 the market is projected to grow by 6% annually to reach $5,605 million worldwide. Immunoassays sales for cardiac markers were 785 million in 2007, or 12% of market, and this is expected to increase to 1,050 million (12%) by 20124. The following Table illustrates the relationships between the top IVD companies and sales of IVD products.

Revenue History of Leading Immunoassay Vendors, $ million 2005-20075

| | | 2007 | | | 2006 | | | 2005 | |

| Abbott Diagnostics | | | 2,100 | | | | 1,900 | | | | 1,800 | |

| Siemans/Dade Behring | | | 825 | | | | 785 | | | | 750 | |

| Siemens/Bayer | | | 750 | | | | 714 | | | | 680 | |

| Beckman Coulter | | | 596 | | | | 484 | | | | 402 | |

| Siemens/DPC | | | 595 | | | | 517 | | | | 473 | |

| Roche | | | 575 | | | | 509 | | | | 450 | |

| bioMérieux | | | 363 | | | | 362 | | | | 353 | |

| Fujirebio | | | 299 | | | | 277 | | | | 279 | |

| Ortho | | | 200 | | | | 190 | | | | 160 | |

| TOTAL | | $ | 6,303 | | | $ | 5,738 | | | $ | 5,347 | |

Immunoassay testing segment of the IVD market is characterized by:

· Expanding opportunities after completion of the human genome project.

· Demand for automated and sensitive POC immunoanalyzers.

· Search for an ideal POC platform.

· Increased mergers and acquisition among top tier IVD companies to achieve more complete product lines

· Greater cooperation between test developers and top tier IVD companies.

Over the next 5-10 years, the immunoassay business will see:

| | · | The continued automation of routine immunoassays – thyroid, anemia, fertility, therapeutic drug monitoring and drugs of abuse; and |

| | · | More new assays and test categories for disease risk evaluation.6 |

3 $6.685 including infectious diseases

4 Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008, p401

5 Estimated. Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008, p402

6 Kalorama Information, The Worldwide Market for In Vitro Diagnostics Tests, 6th Edition, June 2008, p20

Point-Of-Care (POC) Testing Market

Point Of Care (POC) testing refers to a laboratory assay that can be performed outside of a centralized facility, with results available within minutes. POC testing is divided into personal use tests, such as pregnancy tests, and professional use tests, that are administered in a physicians office or hospital emergency ward. Our tests will compete in the professional use testing market sector.

The market for professional7 POC immunoassays is estimated at $1.625 million in 2007 and with the 14% projected growth, this market will reach $2.770 million in 2012. It is anticipated that most of the growth will come from increased use of cardiac markers and new assays for cancer markers and diabetes/cardiac disease markers. The market for professional POC tests for cardiac markers is estimated at $425 million in 2007 (11%) and this is expected to increase to $850 million (15%) by 2012.7

There is a wide perception that POC are more expensive than lab-based tests and that patient test results are lost to the historical record. There is also the perception that once the patient leaves the acute care area, the baseline POC tests done in that unit are of little value because the POC testing results do not correlate with lab-based systems.

Two critical characteristics are necessary for potential POC test products to become more prevalent; POC testing results must correlate with lab results and the POC devices must be more consistent and robust in delivering those results.

The impact of POC testing on improving patients’ care is clear and has been well documented. Further, the impact of POC testing on saving healthcare resources was also demonstrated by numerous agencies and institutions.

Cardiovascular Disease Testing Market

Cardiac markers are proteins released from heart muscle when it is damaged as a result of a heart attack (myocardial infarction), when the blood supply to part of the heart is interrupted. Physicians use cardiac markers in two ways – to diagnose a cardiac event in a hospital emergency room or within the hospital or to evaluate a risk of a cardiovascular event occurring. The routine markers of myocardial infarction – CK-MB, troponin and myoglobin and recently BNP are used in the acute care and tests such as cholesterol are used to evaluate risk.

The world market for cardiac markers is estimated at $740 million in 2007, with projected annual growth of 5%, will reach $1,050 million in 2012.

Until recently, Troponin and CK-MB were the lead cardiac markers. Brain Natriuetic Pepetide (BNP) was recently introduced to differentiate between a myocardial infarction and heart failure. A number of companies are focused on developing new cardiac markers.

7 Administered in a professional setting, i.e. not home tests.

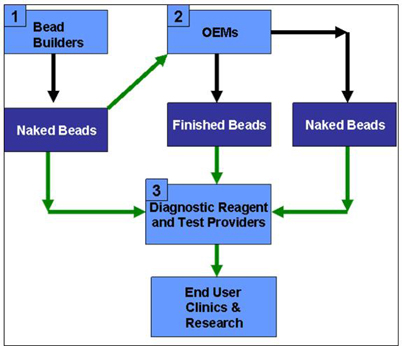

Magnetic Particles Market

Magnetic particles, or beads, are widely used as the solid phase for binding tests for automating and simplifying the methods for isolation and detection of biomolecules in both research and routine clinical laboratories. Eight of the top 10 IVD companies employ magnetic particles in their fully automated analyzers.

An independent 2006 market research report, prepared for CardioGenics by Adventus Research Inc. (the “Adventus Report”) and sponsored by the National Research Council of Canada (NRC), estimated the market for magnetic beads for immunoassays and molecular diagnostics to be approximately $900 million (between $833 million and $1.3 billion). The report of market size did not include magnetic beads produced in-house by some of the IVD test manufacturers or beads produced for research applications. The Adventus Report was conducted using several methods, including interviews with leading particle-manufacturers and the end-users, published industry reports and data from leading IVD manufacturers.

As stated in the Adventus Report, according to Dynal, a leading magnetic beads manufacturer, the largest part of its Molecular Systems’ business is OEM sales of magnetic beads to IVD companies. Dynal stated that “the IVD market is very large, and still growing. However, the magnetic bead-based part of this market is growing at an even higher rate per year”.8 According to Dynal, immunoassays make up more than USD 4 billion of the IVD market, and magnetic beads are now the gold standard for immunoassay testing, as opposed to older technologies such as microtitre plate based tests. Nucleic acid testing makes up a smaller portion of the IVD, USD 2 billion, but is fast growing. Magnetic beads are also the most common solid phase employed in this market.

8 Adventus Report

Furthermore, according to Dynal, as stated in the Adventus Report, end-user business rather than OEM business (referred to as functionalized and naked beads markets respectively) goes to research and routine laboratories within Genomics, Expression Profiling and Proteomics. The market size for Genomics, including DNA and RNA extraction and purification products was USD 300 million in 2001 while the market size of Pharmacogenomics was estimated to be USD 2.3 billion in 2001.

As stated in the Adventus Report, according to Gen-Probe, which is a leading DNA clinical testing company, other markets that are employing magnetic beads as a solid phase are growing also. Further, magnetic particles are used for Separation of Microorganisms in Food and Water Testing and also for HLA testing for organ transplantation.

Source: Gen-Probe presentation- May 2006

Regulation

Our QL Analyzer, Cartridge and Tests are classified as medical devices. Our beads are reagents of medical testing equipments. Accordingly, they are subject to a number of regulations in the jurisdictions where our products will be sold.

United States

The testing, production and sale of IVD products are subject to regulation by numerous state and federal government authorities, principally the FDA.

Pursuant to the U.S. Federal Food, Drug and Cosmetic Act (“FD&C Act”), the FDA regulates the preclinical and clinical testing, manufacture, labeling, distribution and promotion of medical devices.

Medical devices are classified into three categories, Class I, Class II or Class III. The classification of a device is based on the level of control necessary to assure the safety and effectiveness of the device. Generally, the complexity of the submission and the approval times are based on the regulatory class of the device. Device classification depends on the intended use and also the indications for use of the device. Classification is also based on the risk the device poses to the patient and/or the user. Class I devices include devices with the lowest risk, and Class III devices are those with the greatest risk. Class I devices are subject to general control, Class II devices are subject to general controls and special controls, and Class III devices are subject to general controls and must receive a Premarket Assessment or PMA by the FDA.

Before some Class I and most Class II devices can be introduced in the market, either the manufacturer or distributor of the device is required to follow the pre-market notification process described in section 510(k) of the FD&C Act. A 510(k) is a pre-marketing submission made to the FDA to demonstrate that the device to be marketed is as safe and effective, and is substantially equivalent to a legally marketed device. Applicants must compare their 510(k) device to one or more similar devices currently on the US market and support their claims for substantial equivalency. The FDA requires a rigorous demonstration of substantial equivalency. It generally takes three to six months from submission to obtain 510(k) clearance. If any device cleared through 510(k) is modified or enhanced, or if there is a change of use of the device, a new amended 510(k) application must be submitted. According to FDA regulations and our management team’s prior experiences with submissions of similar products, our QLCA and launch product (TnI) will be classified as a Class II device and will be subjected to the 510(K) process. Further, a second test product of ours (HFRS) will also be subjected to the same 510(K) process. As for both tests, predicate devices are commercially available. For other test products, depending on the claims and with a prior agreement with the FDA, the submissions would be either a PMA or 510(K). We have not yet approached the FDA for that purpose.

Canada

Health Canada sets out the requirements governing the sale, importation and advertisement of medical devices. These regulations are intended to ensure that medical devices distributed in Canada are both safe and effective. We are also required to comply with certain procedures for the disposal of waste products under the Canadian Code of Practice for the Management of Biological Waste (the “Code”). We believe we are currently in compliance with all required Code provisions.

Europe

Our products will be subject to registration under the EU Medical Device Directives for in-vitro diagnostic products.

Other countries

Our products will be subject to the regulations of any country where they are sold, and we will make the necessary applications for approval on a country-by-country basis.

OUR TECHNOLOGY AND PRODUCTS

Core Technology

To date, CardioGenics’ developmental efforts have resulted in a novel and patent-protected method for controlling the delivery of compounds to a chemical reaction. CardioGenics deployed this core technology in a POC platform and approached the development of its technology with the direct objective of addressing the limitations of current “State-of-the-Art” commercial technologies, in order to commercialize clinically-needed test products. To demonstrate its benefits, CardioGenics applied its technology to CL, the most promising and the most challenging detection method commercially available.

CardioGenics’ proprietary triggering method facilitates the development of highly sensitive testing platforms that employ complicated reactions, but with a very simple mechanical design. With CardioGenics’ technology, all necessary reaction compounds are pre-deposited in the reaction chamber of a single-use disposable cartridge without fear of premature reaction triggering, thus eliminating the need for a complex mechanical design. Relying on mechanical or physical means for compound delivery increases the likelihood of test failure. Also, moving mechanical components in and out of the measuring filed to deliver the trigger compound interferes with the collection of emitted light, when applied to luminescent reactions. The following outlines the major advantages of CardioGenics’ core technology over the current leading CL technologies:

| | · | Versatile – applicable to all five families of CL compounds |

| | · | High efficiency light collection (solution-phase light emission) – the technology can be used by both small POC test machines and large laboratory analyzers; |

| | · | No restriction to a specific solid phase- ELISA plates, latex and paramagnetic particles, etc., all could be used as the solid phase; and |

| | · | No moving parts for trigger– no pipette injectors and no tanks are required to trigger the light generation. |

The QLCA

CardioGenics harnessed its proprietary technology by developing the QLCA, a small, automated, robust and proprietary POC testing device. The QLCA employs chemical light generation or chemiluminescence, as the detection means.

This compact analyzer meets all POC testing requirements and is able to deliver accurate results of complex testing procedures at the patient’s bedside in a cost-effective manner. The OLCA is fully portable (8”X9”X5”), weighing about seven pounds - and has dual power with a 7-8 hour rechargeable battery life. It has the ability to internally store over 5,000 patient test results, integrate with networks for data transfer and print results using its integral printer.

CardioGenics is in the process of adapting test products for the POC disposable and single-use cartridge-format. Detailed manufacturing specifications and costing have been created and manufacturers have been sourced and are ready to commence production. The main features of the OLCA are:

| | · | It is designed for use by operators without specific laboratory training, following the current trend of POC testing; |

| | · | It employs disposable test cartridges which have been developed by CardioGenics for this Platform; |

| | · | The cartridge and machine design facilitates “walk-away testing”. Other than the addition of the patient’s whole blood sample, the pre-packaged test cartridges require no preparation by the user and are expected to have a minimum shelf life of 12 months; and, |

| | · | Adapting new tests entails only changing the biological reagents without changing either cartridge design or the QLCA. |

By providing these benefits, the Company believes the OLCA and test cartridges have addressed the key needs of the IVD immunodiagnostic testing market described in the “Our Industry“ section of this report; namely (a) reduced turn-around-time; (b) higher quality test results; and (c) both achieved with less cost. These benefits, in patient management and healthcare cost savings, lead us to believe that the POC Platform has the potential to become the small analyzer of choice in the global market.

For human testing, the QLCA can be deployed in any location where fast turn-around-time, combined with lab quality results, will add significant value. It will also supplement and complement the use of larger lab-based testing machines in hospitals and large central labs. Quantitative testing at the bedside for various disease markers would be a natural addition to taking and monitoring vital signs in situations where complete and timely patient information is desired. Laboratories will also benefit by having the QLCA available for off-hours or emergency response.

The Cardiovascular Tests

Although the QLCA can be used for numerous immunodiagnostic tests, of which there are approximately 200 in existence today, we have chosen the Cardiovascular Disease (CVD) sector as its point of entry to the immunodiagnostics market. We currently have under development the following four CVD test products.

TROPONIN I (TNI)

The first test product we will commercialize is a Troponin I (TnI) test. TnI, a protein of the heart muscle, is released into the blood shortly after the heart is injured during a heart attack. Testing for this protein represents the current standard and the latest advance in the management of patients with suspected heart attacks. On average, current laboratory tests detect TnI in blood four to six hours after the onset of symptoms. It can then take as many as several hours for the physician to obtain the results.

As EKG testing is not very sensitive for diagnosing a heart attack and clinical decisions to admit patients presenting to the ER with chest pain are made before blood testing results are obtained, only a small portion of patients admitted to hospitals are eventually diagnosed as actually having had a heart attack. As a result, approximately $4 billion of unnecessary costs are incurred each year in emergency rooms and coronary units on patients who are erroneously triaged for heart attacks34. Further, an estimated 5% to 13% of the 8 million patients in the U.S. who go to the ER with chest pain are inappropriately discharged and 10-26% of those discharged subsequently die.

We believe that the increased sensitivity of QLCA will enable its TnI test to offer significant advantages over present commercial TnI tests, with both greater sensitivity and accuracy in results that are delivered in a timely manner. CardioGenics designed its TnI test to deliver sensitive, accurate and quantitative results that can assist physicians in the triage of patients with chest pain by enabling them to provide such patients proper medical care almost immediately. This is the most critical point of decision-making in treating a patient with a heart attack and, with the help of our QLCA and TnI test, can translate into saving both lives and healthcare costs. We intend to submit this test to the FDA within 48 weeks from closing and have it commercially approved after approximately 16 weeks after submission to the FDA.

PLASMINOGEN ACTIVATOR INHIBITOR TYPE-1 (PAI-1)

Tissue Plasminogen Activator (commonly referred to as “tPA” or the “clot buster”) is currently the first line of therapy for patients with Myocardial Infarction (MI). tPA not only removes the blockage in blood vessels but also minimizes the risks of subsequent heart failure. Although tPA should be administered as soon as possible following the onset of the MI (in order to realize its well documented benefits), approximately 40% of patients with MI do not respond to tPA. Further, administering a single dose of tPA (at a cost of over $2,000 per dose) to patients who ultimately receive no benefit, exposes them to an unnecessary risk of developing a stroke, a frequent side effect of tPA administration. A patient’s poor response to tPA is usually recognized only after the “golden hour” - - the time in which permanent heart damage can be prevented - has passed. Only then is alternate therapy initiated.

While inhibition of tPA by PAI-1, a naturally occurring inhibitor of tPA, is well known, currently, no clinically marketed test for measuring PAI-1 levels is available, precluding a quick and accurate quantification of functional PAI-1.

CardioGenics has conducted extensive research on the various methods of measuring the functionally-relevant form of PAI-1 in blood. Based upon this research, CardioGenics is developing a patent-protected whole blood test to measure the level of active PAI-1 and overcome the shortfalls of other testing methods. This test will rapidly (less than 15 minutes) quantify functional PAI-1 blood levels at the patient’s bedside.

We are planning to submit our PAI-1 test to the FDA within 24 months from closing and anticipate generating revenues from its commercialization shortly after.

PAI-1 testing results will be utilized to optimize the performance of tPA and allow timely initiation of alternate therapy, in cases where tPA would be ineffective. We also anticipate the use of this new test product to monitor the performance of other cardiovascular medications that impact tPA level and are used to treat patients with coronary artery diseases. Using the QLCA, we believe our PAI-1 test will meet an unfulfilled critical need and will be a significant advancement in CVD testing.

HEART FAILURE RISK STRATIFICATION (HFRS)

CardioGenics has discovered a family of related proteins that are released into the bloodstream during heart failure. We believe that the quantification of these proteins would be invaluable to stratify the risk of death in patients with heart failure, thus permitting the initiation of appropriate therapy at an early stage.

Progressing through four stages of severity, heart failure is stratified as “Stage 1” where the patient is asymptomatic with a 5% chance of dying within 12 months to “Stage 4” where the patient has difficulty with almost any exertion or effort and has a 50% chance of dying within a year. This wide variance in death rates necessitates specific management through each phase of heart failure.

Currently, treatment of heart failure is optimized according to risk stratification protocols based on the doctor’s experience and echocardiogram, (a measure of the heart’s pumping efficiency). Echocardiograms do not reliably stratify the risk and thus the search for alternatives is very active.

Biochemical markers provide more reliable results and several candidate proteins are under evaluation and development. The FDA recently granted approvals for two different test products for this purpose on various platforms. Subsequently, these tests were introduced to the Heart Failure Clinics and the value of quantitative stratification of risk was realized through their utilization.

CardioGenics’ HFRS test does not employ the current commercial markers. Further, we believe that our HFRS test product will be of relevant clinical value to all patients with heart failure (systolic and diastolic failure).

CardioGenics is planning to submit its HFRS test to the FDA within approximately 36 months after the closing, and anticipates that it will begin generating revenues from its commercialization approximately 6 months after FDA approval.

HEART FAILURE GENOMICS RISK (HFGR)

This test is a nucleic acid-based test capable of providing information that predicts the response of heart failure patients to routinely used drugs (such as beta blockers or ACE inhibitors). The need to measure the precise response to these drugs, in a timely manner, would minimize the trial and error method now used by doctors to optimize drugs best suited to each patient. This product will permit the physician to select the drugs most likely to benefit the patient, permitting patient-tailored therapy, thus improving the outcome.

As the development and progression of heart failure is directly related to the patient’s individual genetic responses, patients react differently to administered drugs, with significant benefits provided only to some. Recognizing this, pharmaceutical companies are trying to match each patient’s requirements. However, there remains a need to measure the precise response to these drugs in a timely manner, using biochemical markers.

CardioGenics is planning to submit its HFGR test to the FDA within approximately 42 months after the closing, and anticipates that it will begin generating revenues from its commercialization approximately 6 months after FDA approval.

CardioGenics anticipates the formation of alliances or partnerships with one or more therapeutic drug companies for this test product, as this POC test product should be attractive to drug companies looking to improve the performance of specific drugs.

THE BEADS

CardioGenics has exclusive access to proprietary magnetic beads with improved testing sensitivity. The Beads are light colored and are optimized for collecting light signals in binding tests. The light colored magnetic beads are covered with a thin layer of silver and are available in various sizes from 1 to 50 micron. Also, the Beads are covered with a functionalized polymer shell for chemical derivitization. The polymer shell is hydrophilic to minimize non-specific binding.

The Beads are plated with silver and then coated with a polymer encapsulation. We use a multilayer coating process with the polymer to create stability in our beads. In addition, we use a simplified process to manufacture these beads. Our beads are available in various sizes (1 to 50 micron). The Beads are manufactured by a 2-step proprietary process as follows:

Color conversion

A proprietary color conversion process was developed and adapted for magnetic beads of various sizes. Through a proprietary electroless silver plating process, black magnetic beads are converted to silver-colored beads. The thickness of the silver layer is controlled and optimized in order to control the surface reflectivity while not impeding the beads magnetic movement. This process was then optimized to magnetic beads of various sizes. Since the surface area of various size beads will be different, the constituents and speed of adding the components to the silver reduction bath need to be adapted accordingly. Furthermore, the large surface area of the beads results in a large catalytic surface that could spoil the plating bath and result in premature homogeneous silver precipitation in the bath.

Polymer coating

We have also developed a proprietary multilayer polymer encapsulation process of the silver plated magnetic beads. The process of polymer encapsulation combines electrostatic surface bonding, covalent polymer linking, as well as monomer assembly. A minimum of three polymer layers was assembled and cross-linked to control the layer thinness, brightness, stability and surface functional groups.

During a 24-month development process, supported by government grants (4 in total), we have acquired a large amount of data and expertise on beads stability. The end results of our internal testing have confirmed the quality of the developed Beads and their value in increasing test sensitivity.

Competitive advantage

Several companies commercialize magnetic particles manufactured by polymer encapsulation processes or by paramagnetic pigment insertion in latex. These commercial manufacturing processes are labor intensive, expensive and require sophisticated and specialized equipments. Due to the manufacturing costs, commercial beads range in prices from $900 – 1500 per gram of solids.

CardioGenics magnetic beads are light in color and were developed specifically for light collection measurements. Due to the minimized adsorption of generated light, the collected signal is several folds improved in comparison to black beads coated with the same polymer using the same procedure.

CardioGenics’ magnetic beads were tested along side commercial magnetic beads from various suppliers. Without correcting for size variances (surface area) or density of the functional surface groups, CardioGenics’ beads consistently showed improved signal. In comparison to commercial magnetic beads from the top 4 suppliers, CardioGenics’ beads showed at least a 4-fold improvement in the collected light signal. We presented this data in 2008 to an international conference. CardioGenics’ magnetic beads are offered in sizes and functional groups similar to other magnetic beads commercialized for biotechnology applications.

CardioGenics entered into a supply, development and distribution contract with Merck Chimie of France (“Merck”) dated January 19, 2009, as amended, pursuant to which Merck will further develop the beads and distribute and market the final developed product on an exclusive worldwide basis in accordance with the terms of such agreement. The agreement is a 10-year renewable agreement, with Merck receiving 70% of the profits generated from gross sales of the beads and CardioGenics receiving 30% of the proceeds generated from such sales. Merck will be responsible for all marketing costs. Merck anticipates that the final developed version of the beads will be commercially available during the last quarter of 2009.

LEGAL PROCEEDINGS

On April 22, 2009 CardioGenics was served with a statement of claim from a prior contractor claiming compensation for wrongful dismissal and ancillary causes of action including payment of monies in realization of his investment in CardioGenics, with an aggregate claim of $514,000. The Company considers all the claims to be without any merit, has already delivered a statement of defence and intends to vigorously defend the action. If the matter eventually proceeds to trial, the Company does not expect to be found liable on any ground or for any cause of action.

On June 22nd, CardioGenics received a letter from Flow Capital Advisors with regards to a Non-Circumvention Agreement dated July 16th, 2004 and a Finder's Fee Agreement dated December 13, 2004 with Flow Capital Advisors. The letter states that CardioGenics has breached these agreements insofar as the transaction between CardioGenics and JAG Media is concerned and advising that Flow Capital is entitled to payment of 8% of the transaction value in accordance with the terms of the Finder's Fee Agreement. CardioGenics' lawyers have written to Flow Capital denying any contractual breach and explaining why Flow Capital’s claims are without merit.

RISK FACTORS

In addition to the other information in this report, the following risk factors should be considered before deciding to invest in any of our securities. Additional risks and uncertainties not presently known to us, or risks we currently consider immaterial, could also affect our actual results. Our business, financial condition, results of operations, or prospects could be materially adversely affected by any of these risks.

Risks Related to Our CardioGenics Business and Industry

The global financial crisis has had, and may continue to have, an impact on our business and financial condition.

The ongoing global financial crisis may limit our ability to access the capital markets at a time when we would like, or need, to raise capital, which could have an impact on our ability to react to changing economic and business conditions. Accordingly, if the global financial crisis and current economic downturn continue or worsen, our business, results of operations and financial condition could be materially and adversely affected.

The requirements of being a public company may strain our resources and distract our management

As a public company, we are subject to the reporting requirements of the Exchange Act and the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”). These requirements place a strain on our systems and resources. The Exchange Act requires that we file annual, quarterly and current reports with respect to our business and financial condition. The Sarbanes-Oxley Act requires that we maintain effective disclosure controls and procedures and internal controls for financial reporting. We are required to document and test our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act, which requires annual management assessments of the effectiveness of our internal controls over financial reporting and in the future will require a report by our independent registered public accountants addressing these assessments. During the course of our testing, we may identify deficiencies which we may not be able to remediate in time to meet the deadlines imposed by the Sarbanes-Oxley Act. If we fail to achieve and maintain the adequacy of our internal controls, as such standards are modified, supplemented or amended from time to time, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with the Sarbanes-Oxley Act.

In order to maintain and improve the effectiveness of our disclosure controls and procedures and internal control over financial reporting, significant resources and management oversight will be required. This may divert management’s attention from other business concerns, which could have a material adverse effect on our business, financial condition, results of operations and cash flows. In addition, we may need to hire additional accounting and financial staff with appropriate public company experience and technical accounting knowledge, and we cannot assure you that we will be able to do so in a timely fashion.

We have not earned any revenues in our CardioGenics business unit since its incorporation and only have a limited operating history in its current business, which raise doubt about our ability to continue as a going concern.

Our CardioGenics business unit has a limited operating history in its current business and must be considered in the development stage. It has not generated any revenues since its inception and we will, in all likelihood, continue to incur operating expenses without significant revenues until we complete development of our Cardiovascular Tests and commercialize our QLCA and the Cardiovascular Tests. The primary source of funds for our CardioGenics business unit has been the sale of common stock. We cannot assure that we will be able to generate any significant revenues or income. These circumstances make us dependent on additional financial support until profitability is achieved. There is no assurance that we will ever be profitable and we have not yet achieved profitable operations. These factors raise substantial doubt that we will be able to continue as a going concern.

We need to raise additional financing to support the research and development of our CardioGenics business but we cannot be sure that we will be able to obtain additional financing on terms favorable to us when needed. If we are unable to obtain additional financing to meet our needs, our operations may be adversely affected or terminated.

Our ability to develop new test products for our QLCA is dependent upon our ability to raise significant additional financing when needed. If we are unable to obtain such financing, we will not be able to fully develop and commercialize our platform and technology. Our future capital requirements will depend upon many factors, including:

| | • | continued scientific progress in our research and development programs; |

| | • | costs and timing of conducting clinical trials and seeking regulatory approvals and patent prosecutions; |

| | • | competing technological and market developments; |

| | • | our ability to establish additional collaborative relationships; and |

| | • | the effect of commercialization activities and facility expansions if and as required. |

We have limited financial resources and to date, no cash flow from the operations of our CardioGenics business unit and we are dependent for funds on our ability to sell our common stock, primarily on a private placement basis. There can be no assurance that we will be able to obtain financing on that basis in light of factors such as the market demand for our securities, the state of financial markets generally and other relevant factors. Any sale of our common stock in the future will result in dilution to existing stockholders. Furthermore, there is no assurance that we will not incur debt in the future, that we will have sufficient funds to repay any future indebtedness or that we will not default on our future debts, jeopardizing our business viability. Finally, we may not be able to borrow or raise additional capital in the future to meet our needs or to otherwise provide the capital necessary to continue the development of our technology, which might result in the loss of some or all of your investment in our common stock.

We may acquire other businesses, license rights to technologies or products, form alliances, or dispose of or spin-off businesses, which could cause us to incur significant expenses and could negatively affect profitability.

We may pursue acquisitions, technology licensing arrangements, and strategic alliances, or dispose of or spin-off some of our businesses, as part of our business strategy. We may not complete these transactions in a timely manner, on a cost-effective basis, or at all, and may not realize the expected benefits. If we are successful in making an acquisition, the products and technologies that are acquired may not be successful or may require significantly greater resources and investments than originally anticipated. We may not be able to integrate acquisitions successfully into our existing business and could incur or assume significant debt and unknown or contingent liabilities. We could also experience negative effects on our reported results of operations from acquisition or disposition-related charges, amortization of expenses related to intangibles and charges for impairment of long-term assets.

The expiration or loss of patent protection and licenses may affect our future revenues and operating income.

Much of our business relies on patent and trademark and other intellectual property protection. Although most of the challenges to our intellectual property would likely come from other businesses, governments may also challenge intellectual property protections. To the extent our intellectual property is successfully challenged, invalidated, or circumvented or to the extent it does not allow us to compete effectively, our business will suffer. To the extent that countries do not enforce our intellectual property rights or to the extent that countries require compulsory licensing of our intellectual property, our future revenues and operating income will be reduced. Our principal patents and trademarks are described in greater detail in the sections captioned, "Patents, Trademarks, and Licenses."

Competitors' intellectual property may prevent us from selling our products or have a material adverse effect on our future profitability and financial condition.

Competitors may claim that one or more of our products infringe upon their intellectual property. Resolving an intellectual property infringement claim can be costly and time consuming and may require us to enter into license agreements. We cannot guarantee that we would be able to obtain license agreements on commercially reasonable terms. A successful claim of patent or other intellectual property infringement could subject us to significant damages or an injunction preventing the manufacture, sale or use of our affected products. Any of these events could have a material adverse effect on our profitability and financial condition.

We may not be able to adequately protect our intellectual property

We believe the patents, trade secrets and other intellectual property we use are important to our business, and any unauthorized use of such intellectual property by third parties may adversely affect our business and reputation. We rely on the intellectual property laws and contractual arrangements with our employees, business partners and others to protect such intellectual property rights. Filing, prosecuting, defending and enforcing patents on all of our technologies and products throughout the world would be prohibitively expensive. Competitors may, without our authorization, use our intellectual property to develop their own competing technologies and products in jurisdictions where we have not obtained patent protection. These technologies and products may not be covered by any of our patent claims or other intellectual property rights. Furthermore, the validity, enforceability and scope of protection of intellectual property in some countries where we may conduct business is uncertain and still evolving, and these laws may not protect intellectual property rights to the same extent as the laws of the United States.

Many companies have encountered significant problems in protecting and defending their intellectual property rights in foreign jurisdictions. Many countries, including certain countries in Europe, have compulsory licensing laws under which a patent owner may be compelled to grant licenses to third parties (for example, the patent owner has failed to “work” the invention in that country or the third party has patented improvements). In addition, many countries limit the enforceability of patents against government agencies or government contractors. In these countries, the patent owner may have limited remedies, which could materially diminish the value of the patent. Moreover, litigation involving patent or other intellectual property matters in the United States or in foreign countries may be necessary in the future to enforce our intellectual property rights, which could result in substantial costs and diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations.

We are subject to numerous governmental regulations and it can be costly to comply with these regulations and to develop compliant products and processes.

Our products are subject to regulation by the U.S. Food and Drug Administration (“FDA”), and numerous international, federal, and state authorities. The process of obtaining regulatory approvals to market a medical device can be costly and time-consuming, and approvals might not be granted for future products, or additional uses of existing products, on a timely basis, if at all. Delays in the receipt of, or failure to obtain approvals for, future products, or additional uses of existing products, could result in delayed realization of product revenues, reduction in revenues, and in substantial additional costs. In particular, in the United States our products are regulated under the 1976 Medical Device Amendments to the Food, Drug and Cosmetic Act, which is administered by the FDA. We believe that the FDA will classify our products as “Class II” devices, thus requiring us to submit to the FDA a pre-market notification form or 510(k). The FDA uses the 510(k) to substantiate product claims that are made by medical device manufacturers prior to marketing. In our 510(k) notification, we must, among other things, establish that the product we plan to market is “substantially equivalent” to (1) a product that was on the market prior to the adoption of the 1976 Medical Device Amendment or (2) a product that the FDA has previously cleared.

The FDA review process of a 510(k) notification can last anywhere from three to six months, and the FDA must issue a written order finding “substantial equivalence” before a company can market a medical device. We are currently developing a group of cardiovascular tests that we will have to clear with the FDA through the 510(k) notification procedures. These test products are crucial for our success and if we do not receive 510(k) clearance for a particular product, we will not be able to market these products in the United States, which will have a material adverse effect on our revenues, profitability and financial condition.

In addition, no assurance can be given that we will remain in compliance with applicable FDA and other regulatory requirements once clearance or approval has been obtained for a product. We must incur expense and spend time and effort to ensure compliance with these complex regulations. Possible regulatory actions could include warning letters, fines, damages, injunctions, civil penalties, recalls, seizures of our products and criminal prosecution. These actions could result in, among other things, substantial modifications to our business practices and operations; refunds, recalls, or seizures of our products; a total or partial shutdown of production while we or our suppliers remedy the alleged violation; the inability to obtain future pre-market clearances or approvals; and withdrawals or suspensions of current products from the market. Any of these events could disrupt our business and have a material adverse effect on our revenues, profitability and financial condition.

Changes in third-party payor reimbursement regulations can negatively affect our business.

By regulating the maximum amount of reimbursement they will provide for blood testing services, third-party payors, such as HMOs, pay-per-service insurance plans, Medicare and Medicaid, can indirectly affect the pricing or the relative attractiveness of our diagnostic products. For example, the Centers for Medicare and Medicaid Services set the level of reimbursement of fees for blood testing services for Medicare beneficiaries. If third-party payors decrease the reimbursement amounts for blood testing services, it may decrease the amount that physicians and hospitals are able to charge patients for such services. Consequently, we would either need to charge less for our products or incur a reduction in our profit margins. If the government and third-party payors do not provide for adequate coverage and reimbursement levels to allow health care providers to use our products, the demand for our products will decrease.

Laws and regulations affecting government benefit programs could impose new obligations on us, require us to change our business practices, and restrict our operations in the future.

Our industry is also subject to various federal, state, and international laws and regulations pertaining to government benefit program reimbursement, price reporting and regulation, and health care fraud and abuse, including anti-kickback and false claims laws, the Medicaid Rebate Statute, the Veterans Health Care Act, and individual state laws relating to pricing and sales and marketing practices. Violations of these laws may be punishable by criminal and/or civil sanctions, including, in some instances, substantial fines, imprisonment, and exclusion from participation in federal and state health care programs, including Medicare, Medicaid, and Veterans Administration health programs. These laws and regulations are broad in scope and they are subject to evolving interpretations, which could require us to incur substantial costs associated with compliance or to alter one or more of our sales or marketing practices. In addition, violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse effect on our revenues, profitability, and financial condition.

Our research and development efforts may not succeed in developing commercially successful products and technologies, which may cause our revenue and profitability to decline.

To remain competitive, we must continue to launch new products and technologies. To accomplish this, we must commit substantial efforts, funds, and other resources to research and development. A high rate of failure is inherent in the research and development of new products and technologies. We must make ongoing substantial expenditures without any assurance that its efforts will be commercially successful. Failure can occur at any point in the process, including after significant funds have been invested.

Promising new product candidates may fail to reach the market or may only have limited commercial success because of efficacy or safety concerns, failure to achieve positive clinical outcomes, inability to obtain necessary regulatory approvals, limited scope of approved uses, excessive costs to manufacture, the failure to establish or maintain intellectual property rights, or infringement of the intellectual property rights of others. Even if we successfully develop new products or enhancements or new generations of our existing products, they may be quickly rendered obsolete by changing customer preferences, changing industry standards, or competitors' innovations. Innovations may not be accepted quickly in the marketplace because of, among other things, entrenched patterns of clinical practice or uncertainty over third-party reimbursement. We cannot state with certainty when or whether any of our products under development will be launched or whether any products will be commercially successful. Failure to launch successful new products or new uses for existing products may cause our products to become obsolete, causing our revenues and operating results to suffer.

New products and technological advances by our competitors may negatively affect our results of operations.

Our products face intense competition from our competitors' products. Competitors' products may be safer, more effective, more effectively marketed or sold, or have lower prices or superior performance features than our products. We cannot predict with certainty the timing or impact of the introduction of competitors' products.

We depend on key members of our management and scientific staff and, if we fail to retain and recruit qualified individuals, our ability to execute our business strategy and generate sales would be harmed.

We are highly dependent on the principal members of our management and scientific staff. The loss of any of these key personnel, including in particular Dr. Yahia Gawad, our Chief Executive Officer, might impede the achievement of our business objectives. We may not be able to continue to attract and retain skilled and experienced scientific, marketing and manufacturing personnel on acceptable terms in the future because numerous medical products and other high technology companies compete for the services of these qualified individuals. We currently do not maintain key man life insurance on any of our employees.

The manufacture of many of our products is a highly exacting and complex process, and if we or one of our suppliers encounter problems manufacturing products, our business could suffer.

The manufacture of many of our products is a highly exacting and complex process, due in part to strict regulatory requirements. Problems may arise during manufacturing for a variety of reasons, including equipment malfunction, failure to follow specific protocols and procedures, problems with raw materials, natural disasters, and environmental factors. In addition, we may use single suppliers for certain products and materials. If problems arise during the production of a batch of product, that batch of product may have to be discarded. This could, among other things, lead to increased costs, lost revenue, damage to customer relations, time and expense spent investigating the cause and, depending on the cause, similar losses with respect to other batches or products. If problems are not discovered before the product is released to the market, recall and product liability costs may also be incurred. To the extent we or one of our suppliers experience significant manufacturing problems, this could have a material adverse effect on our revenues and profitability.

Significant safety issues could arise for our products, which could have a material adverse effect on our revenues and financial condition.

All medical devices receive regulatory approval based on data obtained in controlled testing environments of limited duration. Following regulatory approval, these products will be used over longer periods of time with many patients. If new safety issues arise, we may be required to change the conditions of use for a product. For example, we may be required to provide additional warnings on a product's label or narrow its approved use, either of which could reduce the product's market acceptance. If serious safety issues with one of our products arise, sales of the product could be halted by us or by regulatory authorities. Safety issues affecting suppliers' or competitors' products also may reduce the market acceptance of our products.

In addition, in the ordinary course of business, we may be the subject of product liability claims and lawsuits alleging that our products or the products of other companies that we promote, or may be incorporated in our products, have resulted or could result in an unsafe condition for or injury to patients. Product liability claims and lawsuits and safety alerts or product recalls, regardless of their ultimate outcome, may have a material adverse effect on our business, reputation and financial condition, as well as on our ability to attract and retain customers. Product liability losses are self-insured.

The international nature of our business subjects us to additional business risks that may cause our revenue and profitability to decline.

Since we intend to market our products internationally, our business will be subject to risks associated with doing business internationally. The risks associated with any such operations outside the United States include:

| • | changes in foreign medical reimbursement policies and programs; |

| • | multiple foreign regulatory requirements that are subject to change and that could restrict our ability to manufacture, market, and sell our products; |

| • | differing local product preferences and product requirements; |

| • | trade protection measures and import or export licensing requirements; |

| • | difficulty in establishing, staffing, and managing foreign operations; |

| • | differing labor regulations; |

| • | potentially negative consequences from changes in or interpretations of tax laws; |

| • | political and economic instability; |

| • | inflation, recession and fluctuations in foreign currency exchange and interest rates; and |

| • | compulsory licensing or diminished protection of intellectual property. |