FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a - 16 or 15d - 16 of

the Securities Exchange Act of 1934

For the month of August 2020

Commission File Number: 001-14930

HSBC Holdings plc

42nd Floor, 8 Canada Square, London E14 5HQ, England

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F).

Form 20-F X Form 40-F ......

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ______

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ______

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934).

Yes....... No X

This Report on Form 6-K with respect to our interim results for the first half of 2020 is hereby incorporated by reference in the following HSBC Holdings plc registration statements: Registration Statements on Form F-3 (Nos. 333-92024, 333-135007, 333-158065, 333-180288, 333-202420, 333-223191) and Registration Statement on Form F-4 (No. 333-126531) and Registration Statements on Form S-8 (Nos. 333-103887, 333-104203, 333-109288, 333-113427, 333-127327, 333-143639, 333-145859, 333-155338, 333-162565, 333-170525, 333-176732, 333-183806, 333-197839, 333-220458).

Neither our website referred to herein, nor any of the information contained on our website, is incorporated by reference in the Form 6-K.

Contents

Overview

1a Cautionary statement regarding forward-looking statements

1b Certain defined terms

1 At a glance

2 Highlights

4 Group Chief Executive’s review

8 How we do business

10 Financial overview

14 Global businesses

21 Risk overview

Interim management report

25 Financial summary

32 Global businesses

40 Geographical regions

50 Reconciliations of return on equity and return on tangible equity

52 Risk

52 – Key developments in the first half of 2020

52 – Areas of special interest

56 – Credit risk

81 – Capital and liquidity risk

88 – Market risk

91 – Insurance manufacturing operations risk

Interim condensed financial statements

94 Interim condensed financial statements

100 Notes on the interim condensed financial statements

Additional information

123 Shareholder information

129 Abbreviations

A reminder

The currency we report in is US dollars.

Adjusted measures

We supplement our IFRS figures with alternative performance measures used by management internally. These measures are highlighted with the following symbol: <>

Further explanation may be found on page 12.

In this document we use the following abbreviations to refer to reporting periods:

1H20 First half of 2020 2Q20 Second quarter of 2020

2H19 Second half of 2019 1Q20 First quarter of 2020

1H19 First half of 2019 2Q19 Second quarter of 2019

1Q19 First quarter of 2019

For a full list of abbreviations see page 129.

None of the websites referred to in this Interim Report on Form 6-K for the half-year ended June 30, 2020 (the ‘Form 6-K’), including where a link is provided, nor any of the information contained on such websites is incorporated by reference in the Form 6-K.

Cover image: Connecting our customers through blockchain

For centuries, international trade has been reliant on paper documents – from letters of credit to bills of lading. Today, HSBC is leading the way towards paperless trade finance. We are working with our clients, financial institutions and fintech partners to pioneer digitisation of trade, which has made doing business simpler and faster, improving the working capital efficiency for our customers. Paperless trade is becoming a reality. We have used a blockchain-based letter of credit platform, built on R3 Corda blockchain technology, to complete digital trade transactions for shipments of iron ore from Australia to mainland China, and soybeans from Argentina to Malaysia. By investing in digital solutions such as blockchain technology, we can help to increase the velocity of trade globally.

Our global businesses

We serve customers through three global businesses. On pages 14 to 20 we provide an overview of our performance in the first half of 2020 for each of the global businesses, as well as our Corporate Centre.

In the second quarter, we simplified our organisational structure by combining Global Private Banking and Retail Banking and Wealth Management to form Wealth and Personal Banking. This followed realignments within our internal reporting and includes the reallocation of Balance Sheet Management, hyperinflation accounting in Argentina and HSBC Holdings net interest expense from Corporate Centre to the global businesses.

Wealth and Personal Banking (’WPB’)

We help millions of our customers look after their day-to-day finances and manage, protect and grow their wealth.

Commercial Banking (‘CMB’)

Our global reach and expertise help domestic and international businesses around the world unlock their potential.

Global Banking and Markets (’GBM’)

We provide a comprehensive range of financial services and products to corporates, governments and institutions.

| Cautionary statement regarding forward-looking statements |

This Form 6-K contains certain forward-looking statements with respect to HSBC’s: financial condition; results of operations and business, including the strategic priorities; 2020 financial, investment and capital targets; and ESG targets/commitments described herein.

Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘targets’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’ and ‘reasonably possible’, variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, information, data, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made. HSBC makes no commitment to revise or update any forward-looking statements to reflect events or circumstances occurring or existing after the date of any forward-looking statements.

Written and/or oral forward-looking statements may also be made in the periodic reports to the US Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These include, but are not limited to:

| • | changes in general economic conditions in the markets in which we operate, such as continuing or deepening recessions and fluctuations in employment and creditworthy customers beyond those factored into consensus forecasts (including, without limitation, as a result of the Covid-19 outbreak); the Covid-19 outbreak, which will have adverse impacts on our income due to lower lending and transaction volumes, lower wealth and insurance manufacturing revenue, and lower or negative interest rates in markets where we operate, as well as, more generally, the potential for material adverse impacts on our financial condition, results of operations, prospects, liquidity, capital position and |

credit ratings; deviations from the market and economic assumptions that form the basis for our ECL measurements (including, without limitation, as a result of the Covid-19 outbreak); potential changes in future dividend policy; changes in foreign exchange rates and interest rates, including the accounting impact resulting from financial reporting in respect of hyperinflationary economies; volatility in equity markets; lack of liquidity in wholesale funding or capital markets, which may affect our ability to meet our obligations under financing facilities or to fund new loans, investments and businesses; geopolitical tensions or diplomatic developments producing social instability or legal uncertainty, such as the unrest in Hong Kong, the existing US-China tensions and the emerging challenges in UK-China relations, which in turn may affect demand for our products and services and could result in (among other things) regulatory, reputational and market risks for HSBC; climate change, which may cause both idiosyncratic and systemic risks resulting in potential financial impacts; illiquidity and downward price pressure in national real estate markets; adverse changes in central banks’ policies with respect to the provision of liquidity support to financial markets; heightened market concerns over sovereign creditworthiness in over-indebted countries; adverse changes in the funding status of public or private defined benefit pensions; consumer perception as to the continuing availability of credit; exposure to counterparty risk, including third parties using us as a conduit for illegal activities without our knowledge; the expected discontinuation of certain key Ibors and the development of alternative risk-free benchmark rates, which may require us to enhance our capital position and/or position additional capital in specific subsidiaries; and price competition in the market segments we serve;

| • | changes in government policy and regulation, including the monetary, interest rate and other policies of central banks and other regulatory authorities in the principal markets in which we operate and the consequences thereof (including, without limitation, actions taken as a result of the Covid-19 outbreak); initiatives to change the size, scope of activities and interconnectedness of financial institutions in connection with the implementation of stricter regulation of financial institutions in key markets worldwide; revised capital and liquidity benchmarks, which could serve to deleverage bank balance sheets and lower returns available from the current business model and portfolio mix; imposition of levies or taxes designed to change business mix and risk appetite; the practices, pricing or responsibilities of financial institutions serving their consumer markets; expropriation, nationalisation, confiscation of assets and changes in legislation relating to foreign ownership; the UK’s exit from the EU, which may result in a prolonged period of uncertainty, unstable economic conditions and market volatility, including currency fluctuations; passage of the Hong Kong national security law and restrictions on telecommunications, as well as the US Hong Kong Autonomy Act, which have caused tensions between China, the US and the UK; general changes in government policy that may significantly influence investor decisions; the costs, effects and outcomes of regulatory reviews, actions or litigation, including any additional compliance requirements; and the effects of competition in the markets where we operate including increased competition from non-bank financial services companies; and |

| • | factors specific to HSBC, including our success in adequately identifying the risks we face, such as the incidence of loan losses or delinquency, and managing those risks (through account management, hedging and other techniques); our ability to achieve our targets, which may result in our failure to achieve any of the expected benefits of our strategic initiatives; model limitations or failure, including, without limitation, the impact that the consequences of the Covid-19 outbreak have had on the performance and usage of financial models, which may require us to hold additional capital, incur losses and/or use compensating controls, such as overlays and overrides, to address model limitations; changes to the judgements, estimates and assumptions we base our financial statements on; changes in our ability to meet the requirements of regulatory stress tests; a reduction in the credit rating assigned to us or any of our subsidiaries, which could increase the cost or decrease the availability of our funding and affect our liquidity position and net interest margin; changes to the reliability and security of our data management, data privacy, information and technology infrastructure, including threats from cyber-attacks, which may impact our ability to service clients and may result in financial loss, business disruption and/ or loss of customer services and data; changes in insurance customer behaviour and insurance claim rates; our dependence on loan payments and dividends from subsidiaries to meet our obligations; changes in accounting standards, which may have a material impact on the way we prepare our financial statements; changes in our ability to manage third-party, fraud and reputational risks inherent in our operations; employee misconduct, which may result in regulatory sanctions and/or reputational or financial harm; and changes in skill requirements, ways of working and talent shortages, which may affect our ability to recruit and retain senior management and diverse and skilled personnel. Effective risk management depends on, among other things, our ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses; and our success in addressing operational, legal and regulatory, and litigation challenges; and other risks and uncertainties we identify in ‘Top and emerging risks’ on pages 76 to 81 of the Annual Report and Accounts 2019. |

| 1a | HSBC Holdings plc |

| Certain defined terms |

Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’, the ‘Group’, ‘we’, ‘us’ and ‘our’ refer to HSBC Holdings together with its subsidiaries. Within this document the Hong Kong Special Administrative Region of the People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings ordinary shares and those preference shares and capital securities issued by HSBC Holdings classified as equity. The abbreviations ‘$m’, ‘$bn’ and ‘$tn’ represent millions, billions (thousands of millions) and trillions of US dollars, respectively.

| HSBC Holdings plc | 1b |

At a glance

Covid-19: The nature, scale and pervasiveness of the coronavirus pandemic dramatically impacted the global macroeconomic environment. The economic disruption caused by Covid-19, together with the worsened economic outlook, resulted in a material increase in expected credit losses and other credit impairment charges (‘ECL’), as well as a reduction in revenue due to lower transaction volumes and reduced client activity.

Read more on page 22.

Geopolitical risk: Levels of geopolitical risk increased in particular markets and are expected to have economic impacts for the Group. US-China relations continue to be under pressure, heightened by the passing of the Hong Kong national security law and the US Hong Kong Autonomy Act. The future relationship between the UK and the EU remains uncertain, while there are also emerging challenges in UK-China relations.

Read more on pages 22 and 23.

Market factors: Interest rates fell in the majority of our key markets and are expected to remain at lower levels for the foreseeable future, which will adversely impact our net interest income. In addition, heightened levels of uncertainty have led to a significant increase in market volatility globally. While this benefited some Global Markets businesses, it also led to large adverse mark-to-market movements in the first quarter of 2020, which reversed to some extent in the second quarter, notably in life insurance manufacturing.

Read more on pages 88 to 93.

Financial performance in 1H20:

Reported profit after tax

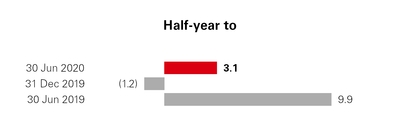

$3.1bn

(1H19: $9.9bn)

Return on average tangible equity (annualised) <>

3.8%

(1H19: 11.2%)

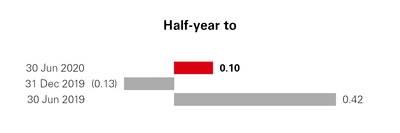

Basic earnings per share

$0.10

(1H19: $0.42)

Read more on page 10.

Supporting customers: We have remained operationally resilient throughout the Covid-19 outbreak and continued to keep our customers at the forefront of our operations. During 1H20, we introduced several measures and initiatives to support our customers and are also working with governments supporting national schemes, granting more than $27bn in payment holidays on loans, credit cards and mortgages for our personal lending customers around the world. For our wholesale lending customers, we have provided more than $52bn in lending to more than 172,000 customers.

Read more on page 9.

Business highlights: We helped our clients raise over $1.15tn in capital markets financing in 1H20, and we remained number one globally in sustainable finance bonds, according to Dealogic’s 1H20 rankings. In Hong Kong, we launched a fully remote, digital account opening solution for business customers, while in the UK, we launched HSBC Kinetic, our new app-only digital banking offering for small and medium-sized business customers. In WPB, we launched Pinnacle in mainland China, our new digital platform for wealth planning and insurance services.

Read more on pages 14 to 20.

Business update: We have restarted most areas of the transformation programme we announced in February 2020, having temporarily paused elements, and we have already made progress in other areas. In the US, we completed the consolidation of our branch network, impacting 80 branches, and we closed a further 31 branches in other locations as we seek to optimise our global footprint. In GBM, we have formed a risk-weighted assets (‘RWAs’) optimisation unit and delivered a gross reduction in RWAs of $21bn in 1H20.

Read more on page 4.

HSBC Holdings plc Interim Report 2020 | 1 |

Highlights

Performance in the first half of 2020 was heavily impacted by the Covid-19 outbreak, geopolitical risk and market factors. The outlook is highly uncertain and dependent on the path and speed of economic recovery.

Financial performance (vs 1H19)

| • | Reported profit after tax down 69% to $3.1bn and reported profit before tax down 65% to $4.3bn from higher ECL and lower revenue. Reported profit in 1H20 also included a $1.2bn impairment of software intangibles, mainly in Europe. |

| • | In Asia, we reported profit before tax of $7.4bn in 1H20, despite higher ECL, demonstrating the strength and continued resilience of our operations in the region and underlining the importance of Asia to the Group. Higher ECL charges materially impacted profitability in our markets across the rest of the world, notably in our operations throughout Europe. |

| • | Reported revenue down 9% to $26.7bn, reflecting the impact of interest rate reductions, as well as adverse market impacts in life insurance manufacturing and adverse valuation adjustments in GBM, notably in 1Q20. These factors more than offset higher revenue in Global Markets. |

| • | Net interest margin (‘NIM’) of 1.43% in 1H20, down 18 basis points (‘bps’) from 1H19. NIM in 2Q20 was 1.33%, down 21bps from 1Q20, primarily reflecting the initial impact of the reduction in interest rates due to the Covid-19 outbreak. |

| • | Reported ECL increased by $5.7bn to $6.9bn due to the impact of the Covid-19 outbreak and the forward economic outlook, and due to an increase in charges related to specific wholesale customers. ECL (annualised) as a percentage of average gross loans and advances to customers was 1.33% in 1H20, while allowance for ECL against loans and advances to customers increased from $8.7bn at 31 December 2019 to $13.2bn at 30 June 2020. |

| • | Reported operating expenses down 4%, despite a $1.2bn impairment of software intangibles. Adjusted operating expenses fell 5%, despite continued investment, due to lower performance-related pay and reduced discretionary costs. |

| • | In 1H20, lending decreased by $18bn on a reported basis. On a constant currency basis, lending increased by $12bn, reflecting corporate customers drawing on existing and new credit lines and re-depositing these to increase cash balances in 1Q20, which was partly offset by paydowns in 2Q20. Deposits grew by $93bn on a reported basis and $133bn on a constant currency basis, with growth in all global businesses, including through the depositing of loans from government-backed schemes. |

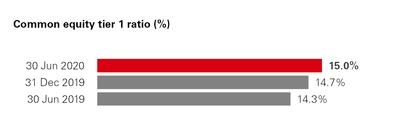

| • | Common equity tier 1 capital (‘CET1’) ratio of 15.0%, up 30bps from 4Q19, as higher CET1 capital, which included an increase from the cancellation of the 4Q19 dividend and the current suspension of dividends on ordinary shares, more than offset the impact of RWA growth. |

Financial performance (vs 2Q19)

| • | Reported profit after tax down 88% to $0.6bn and reported profit before tax down 82% to $1.1bn due to higher ECL and lower revenue, which included the non-recurrence of a 2Q19 dilution gain of $0.8bn. This was partly offset by a reduction in operating expenses, despite a $1.2bn impairment of software intangibles. |

Financial performance (vs 1Q20)

| • | Reported profit after tax down 75% to $0.6bn and reported profit before tax down 66% to $1.1bn, reflecting higher ECL, primarily in CMB, which reported a loss before tax in 2Q20. Lower revenue reflected the impact of interest rate reductions, with net interest margin falling by 21bps to 1.33%. This was partly offset by the partial reversal of the adverse market impacts in life insurance manufacturing and valuation adjustments in GBM recorded in 1Q20. Results in 2Q20 were also adversely impacted by a $1.2bn impairment of software intangibles. |

Outlook for 2020

| • | We continue to face a wide range of potential economic outcomes for the second half of 2020 and into 2021, partly dependent on the extent of any potential impacts from new waves of Covid-19, the path to the development of a possible vaccine and market and consumer confidence levels. Heightened geopolitical risk could also impact a number of our markets, including Hong Kong and the UK. |

| • | Applying a range of weightings to our ECL sensitivity analysis, as disclosed on pages 60 to 66, could result in an ECL charge in the range of $8bn to $13bn for 2020. This range, which continues to be subject to a high degree of uncertainty due to Covid-19 and geopolitical tensions, is higher than at 1Q20 given the deterioration in consensus economic forecasts and actual loss experience during 2Q20. |

| • | Lower global interest rates and reduced customer activity have put increasing pressure on revenue, and are expected to continue to do so. |

| • | We intend to accelerate our transformation programme and execute additional cost actions to help mitigate pressures on revenue and create capacity for further investments in technology. |

| • | We expect mid-to-high single-digit percentage growth in RWAs in 2020, primarily from credit rating migration movements, which is expected to have an adverse impact on our CET1 ratio. We will continue to aim to reduce RWAs in low-returning areas, and improve efficiency to allow resources to be further and faster allocated to areas of competitive advantage, higher returns and growth. |

| • | Given the current high degree of uncertainty, we are continuing to monitor closely the implications on our business plan and medium-term financial targets, while also undertaking a review of our future dividend policy. We intend to provide an update on our medium-term financial targets and dividend policy at our year-end results for 2020. |

| 2 | HSBC Holdings plc |

Key financial metrics

| Half-year to | ||||||

| Reported results | 30 Jun 2020 | 30 Jun 2019 | 31 Dec 2019 | |||

| Reported revenue ($m) | 26,745 | 29,372 | 26,726 | |||

| Reported profit before tax ($m) | 4,318 | 12,407 | 940 | |||

| Reported profit after tax ($m) | 3,125 | 9,937 | (1,229 | ) | ||

| Profit attributable to the ordinary shareholders of the parent company ($m) | 1,977 | 8,507 | (2,538 | ) | ||

| Cost efficiency ratio (%) | 61.8 | 58.4 | 94.3 | |||

| Basic earnings per share ($) | 0.10 | 0.42 | (0.13 | ) | ||

| Diluted earnings per share ($) | 0.10 | 0.42 | (0.13 | ) | ||

| Return on average ordinary shareholders’ equity (annualised) (%) | 2.4 | 10.4 | (3.0 | ) | ||

Net interest margin (%)1 | 1.43 | 1.61 | 1.58 | |||

Alternative performance measures <> | ||||||

| Adjusted revenue ($m) | 26,477 | 27,815 | 26,632 | |||

| Adjusted profit before tax ($m) | 5,635 | 12,273 | 9,660 | |||

| Adjusted cost efficiency ratio (%) | 56.4 | 56.6 | 61.8 | |||

| Annualised expected credit losses and other credit impairment charges (‘ECL’) as a % of average gross loans and advances to customers (%) | 1.33 | 0.22 | 0.30 | |||

Return on average tangible equity (annualised) (%)1,2 | 3.8 | 11.2 | 8.4 | |||

| At | ||||||

| Balance sheet | 30 Jun 2020 | 30 Jun 2019 | 31 Dec 2019 | |||

| Total assets ($m) | 2,922,798 | 2,751,273 | 2,715,152 | |||

| Net loans and advances to customers ($m) | 1,018,681 | 1,021,632 | 1,036,743 | |||

| Customer accounts ($m) | 1,532,380 | 1,380,124 | 1,439,115 | |||

Average interest-earning assets ($m)1 | 2,034,939 | 1,912,708 | 1,922,822 | |||

| Loans and advances to customers as % of customer accounts (%) | 66.5 | 74.0 | 72.0 | |||

| Total shareholders’ equity ($m) | 187,036 | 192,676 | 183,955 | |||

| Tangible ordinary shareholders’ equity ($m) | 147,879 | 145,441 | 144,144 | |||

Net asset value per ordinary share at period end ($)3,4 | 8.17 | 8.35 | 8.00 | |||

Tangible net asset value per ordinary share at period end ($)4 | 7.34 | 7.19 | 7.13 | |||

| Capital, leverage and liquidity | ||||||

Common equity tier 1 capital ratio (%)5 | 15.0 | 14.3 | 14.7 | |||

Risk-weighted assets ($m)5 | 854,552 | 885,971 | 843,395 | |||

Total capital ratio (%)5 | 20.7 | 20.1 | 20.4 | |||

Leverage ratio (%)5 | 5.3 | 5.4 | 5.3 | |||

| High-quality liquid assets (liquidity value) ($bn) | 654 | 533 | 601 | |||

| Liquidity coverage ratio (%) | 148 | 136 | 150 | |||

| Share count | ||||||

| Period end basic number of $0.50 ordinary shares outstanding (millions) | 20,162 | 20,221 | 20,206 | |||

| Period end basic number of $0.50 ordinary shares outstanding and dilutive potential ordinary shares (millions) | 20,198 | 20,286 | 20,280 | |||

| Average basic number of $0.50 ordinary shares outstanding (millions) | 20,162 | 20,124 | 20,191 | |||

Dividend per ordinary share (in respect of the period) ($)1 | — | 0.20 | 0.30 | |||

| 1 | For these metrics, half-year to 31 December 2019 is calculated on a full-year basis and not a 2H19 basis. |

| 2 | Annualised profit attributable to ordinary shareholders, excluding impairment of goodwill and other intangible assets and changes in present value of in-force insurance contracts (‘PVIF’) (net of tax), divided by average ordinary shareholders’ equity excluding goodwill, PVIF and other intangible assets (net of deferred tax). |

| 3 | The definition of net asset value per ordinary share is total shareholders’ equity less non-cumulative preference shares and capital securities, divided by the number of ordinary shares in issue excluding shares the company has purchased and are held in treasury. |

| 4 | Excludes impact of $0.10 per share dividend in 1Q19, following a June 2019 change in accounting practice on the recognition of interim dividends, from the date of declaration to the date of payment. |

| 5 | Unless otherwise stated, regulatory capital ratios and requirements are calculated in accordance with the transitional arrangements of the Capital Requirements Regulation in force in the EU at the time, including the regulatory transitional arrangements for IFRS 9 ‘Financial Instruments’ in article 473a. The capital ratios and requirements at 31 December 2019 and 30 June 2020 are reported in accordance with the revised Capital Requirements Regulation and Directive (‘CRR II’), as |

implemented, whereas the Capital Requirements Regulation and Directive (‘CRD IV’) applied at 30 June 2019. Leverage ratios are calculated using the end point definition of capital.

HSBC Holdings plc Interim Report 2020 | 3 |

Group Chief Executive’s review

We are helping our customers navigate their own path through uncertainty and acting with pace and decisiveness to adapt HSBC to an environment in which no business can afford to stand still.

The first six months of 2020 have been some of the most challenging in living memory. Due to the Covid-19 pandemic, much of the global economy slowed significantly and some sectors drew to a near total halt.

This meant two things for HSBC. First, that the financial performance of the bank inevitably suffered in line with the rest of the global economy. But second, that the real measure of our performance became our success in supporting our customers, colleagues and communities during the pandemic, and in laying the groundwork for the recovery to come.

Covid-19

In difficult times, HSBC’s job has always been to support our communities, provide stability and help build economic growth. I have been immensely proud of the way our people have delivered this purpose as the Covid-19 outbreak has unfolded.

Our approach has hinged on three themes – securing a continuous service for all who rely on us; providing a financial bridge for our personal and business customers beyond the crisis; and ensuring that HSBC retains the strength to help our customers thrive once restrictions begin to ease.

We maintained a high level of business continuity with 85% of colleagues equipped to work from home, all of our customer contact centres fully operational, and between 70% and 90% of our branches open for business in the first half. We enhanced our digital capabilities to serve more customers remotely, with faster access and improved security. We also engaged with our regulators to better enable customers to access a broad range of banking products and services from their homes, including through remote consultations and sales.

This underpinned our ability to get our customers the support they need. For our personal lending customers, we granted more than 700,000 payment holidays on loans, credit cards and mortgages, providing more than $27bn in customer relief in the first half of the year. For our wholesale lending customers, we provided more than $52bn of facilities to more than 172,000 customers globally over the same period, both through government schemes and our own relief initiatives.

As a global bank, HSBC played a vital role in keeping capital flowing for our clients, arranging more than $1.1tn of loan, debt and equity financing for our wholesale customers in the first six months of 2020. Global Banking and Markets made a direct contribution to the Covid-19 relief effort, helping to arrange more than $48bn of financing for our clients through social and Covid-19 relief bonds.

We also took an early decision not to apply for government support packages for employees across the countries in which we operate.

Throughout all of this, the well-being of our people has been our paramount concern. We have taken steps to enable our front-line colleagues to do their jobs safely and effectively. For all our colleagues, we have maintained a regular flow of communication and listened closely to their needs, providing the support and flexibility to help them manage their lives during the pandemic.

| 4 | HSBC Holdings plc |

“The real measure of our performance became our success in supporting our customers, colleagues and communities.“

This has been one of the most demanding periods that I can remember for all of our people across HSBC. Many have had to juggle personal and professional priorities, while adapting to new and unfamiliar ways of working. I have been humbled by the dedication and commitment that they have shown in incredibly tough circumstances, and thank them deeply for all they have done – and are doing – for our customers, communities and each other.

Transformation

On 18 February, we announced a substantial transformation programme to ensure that HSBC is fit for the future. We published plans to reshape underperforming businesses, simplify our complex organisation and reduce our costs.

We are moving forward with these plans wherever we can. We have already begun combining our wholesale back office operations, and brought our retail, wealth and private banking businesses together into a single global business – Wealth and Personal Banking. Our US business has reduced its branch footprint, and Global Banking and Markets has made good early progress in reducing its risk-weighted assets. The

lessons of the past six months are also being applied more broadly, particularly from parts of the business that have responded to a fast-moving situation with exceptional pace and agility.

The operational risks posed by the Covid-19 outbreak meant that we had to move more slowly in some areas than others. In March, I paused the redundancy programme intended to deliver the reduction in headcount we promised in February. It would have been wrong to proceed with job losses at a time of significant stress for our people and communities, and at a point when we needed to protect our capacity to serve our customers. Now, many countries have slowed the spread of the virus and are emerging from lockdown, and we have adapted to new ways of working. I therefore decided in June to lift the pause on redundancies, proceeding thoughtfully but purposefully, while taking local considerations into account.

Now that many governments have become better accustomed to managing the ebb and flow of the pandemic, we intend to accelerate implementation of the plans we announced in February. At the same time, our operating environment has changed significantly since the start of the year. We will also therefore look at what additional actions we need to take in light of the new economic environment to make HSBC a stronger and more sustainable business.

Financial performance

A good start to the year in January and February was overshadowed from March onwards by the Covid-19 outbreak and the impact of falling interest rates.

The sharp increase in expected credit losses that followed impacted all markets, but particularly those outside Asia. ECL grew further from the first to the second quarter as the economic outlook deteriorated, with increases in both stage 1 and 2 allowances. Stage 3 ECL were up overall but broadly stable during the first half, although the first quarter included a charge in Singapore unrelated to the Covid-19 crisis.

First half reported revenue was 9% lower than last year’s first half, due mainly to the effects of interest rate cuts made at the start of the year across our deposit franchises. By contrast, our Asia businesses showed good resilience and Global Markets grew revenue on the back of higher client activity.

HSBC Holdings plc Interim Report 2020 | 5 |

Response to Covid-19

Operational response

Our operations have stayed highly resilient:

Approximately

90%

of our branch network remained open for business globally, as at 30 June 2020.

Approximately

85%

of our employees are now equipped to work from home.

“We have taken steps to enable our front-line colleagues to do their jobs safely and effectively.”

We took further action on costs in response to the weaker revenue environment, reducing both performance-related pay and discretionary spending. Together with our ongoing cost-saving initiatives, this helped reduce reported operating expenses by 4%.

While these cost measures mitigated some of the adverse effects of the radically changed economic environment, reported first half profit before tax was 65% lower than the same period last year, and adjusted profit before tax fell by 54%.

Lending decreased by $18bn in the first half. Customers initially drew on new and existing credit lines in the first quarter in response to the Covid-19 outbreak, but began to pay these down in the second quarter as circumstances changed. Deposits rose by $93bn in the first half, as customers increased their cash reserves and reduced their spending during lockdown.

We continued to invest in the future of the business while managing costs down, spending $2.8bn on technology in the first six months of the year.

Our balance sheet remains robust with a CET1 ratio of 15.0% and strong liquidity and funding.

Facing the future

Our performance in the second half of the year will continue to be influenced by the path and economic impact of the Covid-19 outbreak. Geopolitical uncertainty could also weigh heavily on our clients, particularly those impacted by heightened US-China and UK-China tensions, and the future of UK-EU trade relations.

Amid the current uncertainty, we remain focused on the things we can control – helping our customers navigate their own path to a complex future, and acting with pace and decisiveness to adapt HSBC to an environment in which no business can afford to stand still.

HSBC has always helped our clients manage complexity. There have been many times in the last 155 years when geopolitics has altered the nature of trade, or disruptive forces have changed entire industries. On each occasion, HSBC has adapted and innovated to help our customers when they need us most, and we will do so again.

We start from a strong position. As the world’s leading trade bank1, we have the knowledge and network to help customers reorder their supply chains securely and sustainably. As the world’s number one bank for green, social and sustainable bonds2, we have the experience and expertise to help customers finance their transition to a cleaner, more resilient future. These are important strengths, but we have to keep investing to maintain them and to provide the agile, responsive and entrepreneurial service that our clients require.

Like our clients, HSBC has to operate in a difficult geopolitical environment. Current tensions between China and the US inevitably create challenging situations for an organisation with HSBC’s footprint. However, the need for a bank capable of bridging the economies of east and west is acute, and we are well placed to fulfil this role. We will face any political challenges that arise with a focus on the long-term needs of our customers and the best interests of our investors.

| 6 | HSBC Holdings plc |

Response to Covid-19

Customer response

We are participating in several Covid-19 relief programmes to deploy a range of support measures for our customers at pace.

We arranged more than

$48bn

of financing through social and Covid-19 relief bonds in 1H20.

We granted more than

700,000

payment holidays for personal lending customers in 1H20.

We provided more than

$52bn

of lending facilities for our wholesale customers in 1H20.

“HSBC has always helped our clients manage complexity.“

As we seek to accelerate our transformation in the second half of the year, I am mindful of the impact it will have for some of our people, particularly those leaving us. As necessary as these changes are, the human impact is a matter of deep personal regret to me. We will make sure that all those leaving HSBC as part of our transformation will be treated with fairness and consideration, and will receive support in finding new employment.

Finally, HSBC is a global bank serving customers from many different backgrounds. We therefore need to resemble the communities we serve. In May, we launched a new global ethnicity inclusion programme to better enable careers and career progression for colleagues from ethnic minorities, and in July, we made a series of commitments to address feedback from Black colleagues in particular. However, I want us to be

judged by our actions, not our words. We will therefore provide more information about the ethnicity of our workforce in our annual reporting in February, so that our stakeholders can hold us accountable.

Noel Quinn

Group Chief Executive

3 August 2020

1 Euromoney, Trade Finance Survey, January 2020

2 Dealogic, Sustainable Finance Bond league table, 1H20

HSBC Holdings plc Interim Report 2020 | 7 |

How we do business

We conduct our business intent on supporting the sustained success of our customers, people and other stakeholders.

Our approach

Our purpose is to connect customers to opportunities. To achieve our purpose, we need to build strong relationships with all of our stakeholders, including customers, employees and the communities in which we operate. This will help us deliver our strategy and operate our business in a way that is sustainable.

Our Covid-19 actions

Our ability to help our stakeholders is more important than ever during these challenging and unprecedented times. In the first half of 2020, we continued to promote and encourage good conduct through our people's behaviour and decision making to deliver fair outcomes for customers and preserve market integrity. This included our continuing focus on the needs of vulnerable customers in our product and process design.

We developed a number of digital enhancements to support the ongoing delivery of fair outcomes for our customers in different markets. This included the development of video conferencing guidance to ensure we continue to provide services and products to our customers securely when there is limited access to branches.

We have also played a lead role in issuing social and Covid-19 relief bonds to help raise funds for communities affected by Covid-19, and provided innovative supply chain solutions to help our business customers, as set out in the examples on this page.

On the following page, we have set out further ways that we have supported our stakeholders, including our communities, customers, employees, investors, regulators and governments, and suppliers.

Our approach to diversity

Our actions are focused on ensuring our people are valued, respected and supported to fulfil their potential and thrive. Our global ethnicity inclusion programme, which launched in May, is designed to improve the data and reporting of our people’s ethnic backgrounds. It will help us take specific actions to enable the careers and career progression of all our colleagues in a supportive and inclusive way.

We are listening to what our colleagues are telling us in response to the Black Lives Matter movement. We are implementing further plans to develop senior Black talent and help diversify the ethnicity profile of HSBC’s senior leadership through targeted development interventions. We aim to build a pipeline of future Black talent by strengthening our recruitment processes and partnering with a specialist search firm.

Further details on our plans and progress will be included in our Annual Report and Accounts 2020.

Social bonds fund Covid-19 response

We played a lead role in the issuance of the Bank of China Macau branch’s HK$4bn social bond, with proceeds earmarked to help small firms hit by the Covid-19 crisis. The funds will be used to provide loans to micro, small and medium-sized enterprises in Macau to help generate employment in industries that have struggled due to the sharp drop in tourism.

We helped to arrange $66bn-worth of social and Covid-19 relief bonds in the first half of 2020, with proceeds supporting responses to the pandemic and projects that aim to deliver a positive societal impact.

Easing supply chain strains with trade finance solutions

We are working closely with our customers and governments to help ensure that the flow of critical goods and documents continues during Covid-19 lockdown restrictions. We are helping governments secure personal protective equipment and other critical medical goods, for example, by using our automated utility for sanctions and anti-money laundering controls to navigate risk. We are also supporting clients to deliver critical medical items through fast-track credit approvals. We provided more than 50,000 repayment extensions to our trade finance customers in the first half of 2020, and are helping them to manage liquidity in their end-to-end supply chains.

| 8 | HSBC Holdings plc |

Supporting our stakeholders through Covid-19

The Covid-19 outbreak has created a great deal of uncertainty and disruption for the people, businesses and communities we serve around the world. It is affecting everyone in different ways, with markets at different stages of the crisis. We are tailoring our response to the different circumstances and situations in which our stakeholders find themselves.

| Our stakeholders | How we have engaged | |

| Customers | The Covid-19 outbreak has posed significant challenges for our customers worldwide. Our immediate priority is to do what we can to provide them with support and flexibility. This has included offering payment holidays and restructuring mortgage payments, as well as extending relief loans or temporary credit limit increases for borrowers. We are working across many markets to offer relief through market-wide and HSBC-led schemes. In the UK, we granted relief to our personal lending customers on 65,000 mortgage accounts and 153,000 personal loan and credit card accounts during the first half of the year. In Hong Kong, we initiated a simple digital and branch registration process to help customers gain access to government funds, following the launch of a government cash payout scheme. On the first day of the scheme, we received one million registrations. For our wholesale lending customers, we provided approximately $33bn of facilities through market-wide schemes and $19bn via HSBC-led schemes in the first half of the year, and helped them to navigate the current environment. For further details on our customer relief programmes, see page 70. We have taken steps to keep many of our branches open while protecting customers and employees. However, with customers doing more of their banking online, we have also deployed new technology to help enable them to engage with us in new ways, including video calls with personal and business relationship managers, and, in some markets, online capabilities for payment relief programmes. | |

| Employees | We moved quickly to protect our people. More than 230,000, or 85%, of our total workforce are now enabled to work from their homes if needed. We provided new and enhanced well-being support to employees during this challenging time. Our dedicated Covid-19 resources are accessible to everyone and include expert medical guidance, education on mental health awareness, training on how to lead remote teams, and advice on managing stress and working remotely. Our employee assistance programmes, which provide confidential counselling to employees, continue to provide clinical support. We have encouraged a culture of looking out for each other, and our employee networks have held regular support calls for those experiencing mental health challenges, and for those with caring responsibilities. Listening to employees is vital to ensure we provide the right support. More than 118,000 employees responded to our employee survey, helping us understand how Covid-19 is impacting them and their thoughts about the future. Overall, 89% of people said they were getting the information they needed and 86% reported they were getting the support they needed from their line manager. We continue to use this data and insight to shape our work. | |

| Communities | In the first half of the year, we committed more than $20m of donations for programmes and partners that support the medical response, relieve food insecurity and provide access to help for vulnerable people. | |

| Regulators and governments | We have engaged proactively with regulators and governments globally regarding the policy changes issued in response to Covid-19 to help our customers, to contribute to normalisation and recovery, and to manage the operational capacity at both banks and regulators. | |

| Suppliers | We made early payments to thousands of our suppliers during the first half of the year to support them through the pandemic. | |

| Investors | At this year’s Annual General Meeting (‘AGM’), it was unfortunately not possible for shareholders to attend due to the introduction of social distancing measures. Shareholders were instead encouraged to vote by proxy and submit questions in advance. After the AGM, responses to the most frequent questions across key themes were published on our website. HSBC, in line with all other large UK-based banks and at the direct request of the Group’s lead regulator (the UK Prudential Regulation Authority), cancelled the fourth interim dividend of 2019. We have also suspended dividend payments until the end of 2020. We profoundly regret the impact this will have on shareholders, their families and their businesses. The Board will review the position at the 2020 year-end results. | |

HSBC Holdings plc Interim Report 2020 | 9 |

Financial overview

In assessing the Group’s financial performance, management uses a range of financial measures that focus on the delivery of sustainable returns for our shareholders and maintaining our financial strength.

Executive summary

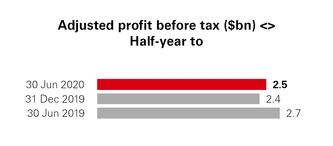

Performance in the first half of 2020 was heavily impacted by the Covid-19 outbreak, geopolitical risk and market factors. Reported profit before tax of $4.3bn fell by 65% compared with 1H19, while adjusted profit before tax of $5.6bn decreased by 54%, mainly from higher ECL and lower revenue. The annualised return on average tangible equity (‘RoTE’) for 1H20 was 3.8%, compared with 11.2% in 1H19.

Revenue declined compared with 1H19, reflecting the impact of interest rate reductions, as well as adverse market impacts in life insurance manufacturing in WPB and adverse valuation adjustments in GBM, notably in 1Q20. Notwithstanding these factors, certain parts of the Group have remained resilient, notably our Asian franchises including Hong Kong, while our Global Markets business delivered growth compared with 1H19. The increase in ECL and lower revenue were in part mitigated by lower operating expenses due to reductions in the performance-related pay accrual and lower discretionary expenditure. The 1H20 period also included a $1.2bn impairment of capitalised software related principally to businesses within HSBC Bank plc, our non-ring-fenced bank in Europe. This reflected underperformance and a deterioration in the future forecasts of these businesses, substantially relating to prior periods.

The outlook remains highly uncertain. We will continue to monitor closely the implications on our business plan, while also undertaking a review of our future dividend policy. We intend to provide an update on our medium-term financial targets and dividend policy at our year-end results for 2020.

Reported results

| Half-year to | Quarter ended | |||||||||||

| Reported results | 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Dec 2019 $m | 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Mar 2020 $m | ||||||

| Net operating income before change in expected credit losses and other credit impairment charges (‘revenue’) | 26,745 | 29,372 | 26,726 | 13,059 | 14,944 | 13,686 | ||||||

| ECL | (6,858 | ) | (1,140 | ) | (1,616 | ) | (3,832 | ) | (555 | ) | (3,026 | ) |

| Net operating income | 19,887 | 28,232 | 25,110 | 9,227 | 14,389 | 10,660 | ||||||

| Total operating expenses | (16,527 | ) | (17,149 | ) | (25,200 | ) | (8,675 | ) | (8,927 | ) | (7,852 | ) |

| Operating profit/(loss) | 3,360 | 11,083 | (90 | ) | 552 | 5,462 | 2,808 | |||||

| Share of profit in associates and joint ventures | 958 | 1,324 | 1,030 | 537 | 732 | 421 | ||||||

| Profit before tax | 4,318 | 12,407 | 940 | 1,089 | 6,194 | 3,229 | ||||||

| Tax expense | (1,193 | ) | (2,470 | ) | (2,169 | ) | (472 | ) | (1,167 | ) | (721 | ) |

| Profit/(loss) after tax | 3,125 | 9,937 | (1,229 | ) | 617 | 5,027 | 2,508 | |||||

Reported performance - 1H20 vs 1H19

Reported profit

Reported profit after tax of $3.1bn in 1H20 was $6.8bn or 69% lower than in 1H19.

Reported profit before tax of $4.3bn was $8.1bn or 65% lower than in 1H19, primarily due to a rise in reported ECL, reflecting the impact of the Covid-19 outbreak on the economic outlook. The reduction also reflected lower reported revenue, reflecting the impact of interest rate reductions, as well as adverse market impacts in life insurance manufacturing in WPB and adverse valuation adjustments in GBM, notably in 1Q20. Lower revenue also reflected the non-recurrence of an $828m dilution gain in 1H19 recognised on the completion of the merger of our associate The Saudi British Bank (‘SABB’) with Alawwal bank in Saudi Arabia. These reductions were in part mitigated by lower reported operating expenses as we reduced the performance-related pay accrual and lowered discretionary expenditure. The 1H20 period also included a $1.2bn impairment of capitalised software related principally to businesses within HSBC Bank plc. This reflected underperformance and a deterioration in the future forecasts of these businesses, substantially relating to prior periods. This impairment has been recognised as a significant item, with $1.0bn included within ‘impairment of goodwill and other intangibles’ and $0.2bn included within ‘restructuring and other related costs’.

Results in 1H20 included certain volatile items, which impacted revenue. These included adverse market impacts in life insurance manufacturing in WPB of $334m (1H19: $152m favourable), while GBM included an adverse movement in credit and funding valuation adjustments of $355m (1H19: $14m favourable) and losses in Principal Investments of $12m (1H19: $122m favourable). Results also included favourable movements on our long-term debt and associated swaps in Corporate Centre of $195m (1H19: $143m favourable). In 1H19, results included disposal gains in WPB and CMB of $157m.

| 10 | HSBC Holdings plc |

Our operations across Asia delivered resilient performances during 1H20, despite interest rate headwinds, adverse market impacts in life insurance manufacturing and a rise in ECL. In 1H20, reported profit before tax in Asia represented more than 170% of Group profits, underlining the importance of the region to the Group. Outside of Asia, the increase in ECL and interest rate reductions adversely affected the profitability of our operations, most notably across Europe, including HSBC UK plc, our ring-fenced bank in Europe, while HSBC Bank plc was also impacted by an impairment of software intangibles.

Reported revenue

Reported revenue of $26.7bn was $2.6bn or 9% lower than in 1H19, reflecting the impact of interest rate reductions across our global businesses, most notably in Retail Banking and Global Liquidity and Cash Management (‘GLCM’). In addition, the reduction reflected adverse market impacts in life insurance manufacturing in WPB and adverse valuation adjustments in GBM, both notably in the first quarter. These factors more than offset higher revenue in Global Markets as increased volatility resulted in higher client activity.

The reduction in reported revenue included net adverse movements in significant items of $0.6bn, primarily from the non-recurrence of a $0.8bn dilution gain in 1H19, as mentioned above.

Reported ECL

Reported ECL of $6.9bn were $5.7bn higher than in 1H19, with increases across all global businesses, mainly from charges relating to the global impact of the Covid-19 outbreak on the forward economic outlook. The increase also reflected higher charges related to specific wholesale exposures, including a significant charge related to a corporate exposure in Singapore in CMB.

The estimated impact of the Covid-19 outbreak was incorporated in the ECL through additional scenario analysis, which considered differing severity and duration assumptions relating to the global pandemic. These included probability-weighted shocks to annual GDP and consequential impacts on unemployment and other economic variables, with differing economic recovery assumptions.Given the severity of the macroeconomic projections, and the complexities of the government measures, which have never been modelled, additional judgemental adjustments have been made to our provisions.

For further details on the calculation of ECL, including the measurement uncertainties and significant judgements applied to such calculations, the impact of alternative/additional scenarios and post model-adjustments, see pages 60 to 66.

Reported operating expenses

Reported operating expenses of $16.5bn were $0.6bn or 4% lower than in 1H19 and included favourable foreign currency translation differences of $0.5bn and net adverse movements in significant items of $0.6bn, which included:

| • | a $1.0bn impairment of capitalised software related principally to businesses within HSBC Bank plc. This reflected underperformance and a deterioration in the future forecasts of these businesses, substantially relating to prior periods (for more information, see Note 11 on the interim condensed financial statements); and |

| • | higher restructuring and other related costs of $0.5bn, of which $116m related to severance and $0.2bn related to an impairment of software intangibles, compared with $0.3bn in 1H19. |

This was partly offset by:

| • | customer redress programme costs in respect of payment protection insurance (‘PPI’) of $0.1bn in 1H20, compared with $0.6bn in 1H19. |

The remaining reduction reflected lower performance-related pay and discretionary expenditure, while we continued to invest in technology.

Reported share of profit in associates and joint ventures

Reported share of profit in associates of $1.0bn fell $366m or 28%, primarily reflecting the impact of the Covid-19 outbreak and the lower interest rate environment on the share of profit we recognise from our associates.

Tax expense

The effective tax rate for 1H20 of 27.6% was higher than the 19.9% for 1H19, primarily reflecting the non-recognition of deferred tax on losses in the UK in 1H20. The effective tax rate for 1H19 was reduced by the non-taxable dilution gain arising on the merger of SABB with Alawwal bank in Saudi Arabia.

Reported 1H20 profit after tax ($bn)

$3.1bn

Basic earnings per share for 1H20 ($)

$0.10

Reported performance - 2Q20 vs 2Q19

Reported profit

Reported profit after tax of $0.6bn in 2Q20 was $4.4bn or 88% lower than in 2Q19.

Reported profit before tax of $1.1bn was $5.1bn or 82% lower. This decrease reflected a significant rise in reported ECL and lower reported revenue, primarily in our CMB business, which reported a loss before tax in 2Q20, as well as in WPB. These factors were partly offset by reported revenue growth in GBM, as well as a reduction in reported operating expenses.

The reduction in profit before tax included the impact of the non-recurrence of a 2Q19 dilution gain of $0.8bn in Saudi Arabia, and a $1.2bn impairment of software intangibles in Europe. However, results were favourably affected by lower charges in respect of PPI.

Reported revenue of $13.1bn was $1.9bn or 13% lower, which included the non-recurrence of the dilution gain mentioned above. The impact of interest rate reductions adversely affected deposit revenue in Retail Banking and GLCM, which resulted in lower revenue in both WPB and CMB. Wealth management revenue in WPB was broadly unchanged. This reflected the partial reversal in 2Q20 of the significant adverse movement in market impacts in life insurance manufacturing recorded in 1Q20, offset by the lower demand for investment products due to market uncertainty. The reductions in WPB and CMB were partly offset by higher revenue in our Global Markets business in GBM as increased market volatility resulted in higher client activity.

ECL increased by $3.3bn to $3.8bn, largely from charges relating to the ongoing global impact of the Covid-19 outbreak and the forward economic outlook, and from charges relating to a small number of wholesale exposures in 2Q20.

Reported operating expenses of $8.7bn were $0.3bn or 3% lower, reflecting a reduction in discretionary expenditure and lower performance-related pay, partly offset by the impact of a $1.2bn impairment of software intangibles.

Reported share of profit in associates and joint ventures fell by $0.2bn, primarily reflecting the impact of the Covid-19 outbreak and the lower interest rate environment on the share of profit we recognise from our associates.

Reported 2Q20 profit after tax ($bn)

$0.6bn

(2Q19: $5.0bn)

HSBC Holdings plc Interim Report 2020 | 11 |

Adjusted results

Our reported results are prepared in accordance with International Financial Reporting Standards (‘IFRSs’) as detailed in the financial statements on page 240 of the Annual Report and Accounts 2019.

We also present alternative performance measures. Adjusted performance is an alternative performance measure used to align internal and external reporting, identify and quantify items management believes to be significant, and provide insight into how management assesses period-on-period performance. Alternative performance measures are highlighted with the following symbol: <>

To derive adjusted performance, we adjust for:

- the period-on-period effects of foreign currency translation differences; and

- the effect of significant items that distort period-on-period comparisons, which are excluded in order to improve understanding of the underlying trends in the business.

The results of our global businesses are presented on an adjusted basis, which is consistent with how we manage and assess global business performance.

For reconciliations of our reported results to an adjusted basis, including lists of significant items, see page 33.

Adjusted results <> | Half-year to | 1H20 vs 1H19 | |||||||||

| 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Dec 2019 $m | $m | % | |||||||

| Revenue | 26,477 | 27,815 | 26,632 | (1,338 | ) | (5 | ) | ||||

| ECL | (6,858 | ) | (1,088 | ) | (1,554 | ) | (5,770 | ) | >(100) | ||

| Total operating expenses | (14,942 | ) | (15,739 | ) | (16,448 | ) | 797 | 5 | |||

| Operating profit | 4,677 | 10,988 | 8,630 | (6,311 | ) | (57 | ) | ||||

| Share of profit in associates and joint ventures | 958 | 1,285 | 1,030 | (327 | ) | (25 | ) | ||||

| Profit before tax | 5,635 | 12,273 | 9,660 | (6,638 | ) | (54 | ) | ||||

Adjusted performance - 1H20 vs 1H19

Adjusted profit before tax <>

Adjusted profit before tax of $5.6bn was $6.6bn or 54% lower than in 1H19, primarily from higher adjusted ECL and lower adjusted revenue. Adjusted ECL increased by $5.8bn, mainly from charges relating to the global impact of the Covid-19 outbreak on the forward economic outlook. Adjusted revenue decreased by $1.3bn, primarily from interest rate reductions across our deposit franchises, as well as the effects of a sharp fall in equity markets and widening of credit spreads towards the end of the first quarter of 2020, although there was a partial recovery in equity markets and a tightening of credit spreads during the second quarter. This was partly offset by higher revenue from Global Markets. Adjusted operating expenses decreased by $0.8bn as we lowered the performance-related pay accrual and reduced discretionary expenditure while continuing to invest in our businesses.

Reconciliation of reported to adjusted profit before tax

| Half-year to | ||||||

| 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Dec 2019 $m | ||||

| Reported profit before tax | 4,318 | 12,407 | 940 | |||

| Currency translation | (215 | ) | 9 | |||

| Significant items: | 1,317 | 81 | 8,711 | |||

| – costs of structural reform | — | 91 | 67 | |||

| – customer redress programmes | 24 | 610 | 834 | |||

| – disposals, acquisitions and investment in new businesses | 8 | (827 | ) | 59 | ||

| – fair value movements on financial instruments | (299 | ) | (50 | ) | (34 | ) |

| – impairment of goodwill and other intangibles | 1,025 | — | 7,349 | |||

| – restructuring and other related costs | 554 | 287 | 540 | |||

| – settlements and provisions in connection with legal and regulatory matters | 5 | (2 | ) | (59 | ) | |

| – currency translation on significant items | — | (28 | ) | (45 | ) | |

| Adjusted profit before tax | 5,635 | 12,273 | 9,660 | |||

| 12 | HSBC Holdings plc Interim Report 2020 |

Adjusted revenue <>

Adjusted revenue of $26.5bn was $1.3bn or 5% lower than in 1H19, reflecting falls in WPB (down $1.6bn) and CMB (down $0.6bn), partly offset by higher revenue in GBM (up $0.6bn) and Corporate Centre (up $0.3bn).

The reduction in adjusted revenue reflected lower interest rates in many of the key markets in which we operate. This had an adverse impact on revenue from Retail Banking within WPB, and from GLCM within CMB and GBM, although we continued to grow average balances across these businesses. In addition, lower revenue included adverse movements in market impacts of $482m in life insurance manufacturing within WPB, following a weakening of global equity prices and lower interest rates. It also included an adverse movement in credit and funding valuation adjustments (down $0.4bn) and losses in Principal Investments of $12m, compared with gains in 1H19 of $120m in GBM. In 1H19, adjusted revenue included disposal gains in WPB and CMB of $157m.

These reductions were partly offset by higher revenue in Global Markets as increased market volatility resulted in higher client activity. Revenue also rose in Corporate Centre, which included favourable fair value movements of $0.1bn relating to the economic hedging of interest rate and exchange rate risk on our long-term debt with associated swaps, notably in 1Q20.

Revenue relating to Balance Sheet Management (‘BSM’), Holdings net interest expense and Argentina hyperinflation was $0.4bn higher, primarily due to disposal gains in BSM. This revenue is allocated to our global businesses.

Adjusted ECL <>

Adjusted ECL, which removes the period-on-period effects of foreign currency translation differences, were $6.9bn, an increase of $5.8bn from 1H19. This increase occurred in WPB (up $1.7bn), CMB (up $3.0bn) and GBM (up $1.0bn) and mainly reflected charges related to the global impact of the Covid-19 outbreak and the forward economic outlook in all of our global businesses. In addition to these charges, ECL in 1H20 included a significant charge related to a corporate exposure in Singapore in CMB, and charges against a small number of corporate exposures in GBM.

Adjusted ECL (annualised) as a percentage of average gross loans and advances to customers was 1.33%, compared with 0.22% in 1H19.

Adjusted operating expenses <>

Adjusted operating expenses of $14.9bn were $0.8bn or 5% lower than in 1H19, as we continue to review and reprioritise costs and investments to help mitigate revenue headwinds. The decrease primarily reflected a $0.6bn reduction in the performance-related pay accrual and lower discretionary expenditure, including marketing (down $0.2bn) and travel costs (down $0.1bn). In addition, our cost-saving initiatives resulted in a reduction of $0.3bn. These decreases were partly offset by an increase of $0.2bn on investments in technology to enhance our digital capabilities and increase automation to improve how we serve our customers.

The number of employees expressed in full-time equivalent staff (‘FTE’) at 30 June 2020 was 232,764, a decrease of 2,587 compared with 31 December 2019. The number of contractors at 30 June 2020 was 6,221, a decrease of 1,190 from 31 December 2019.

Adjusted share of profit in associates and joint ventures<>

Adjusted share of profit from associates of $1.0bn was $0.3bn or 25% lower than in 1H19, primarily reflecting the impact of the Covid-19 outbreak and the lower interest rate environment on the share of profit we recognise from our associates.

Balance sheet and capital

$2,923bn

15.0%

Balance sheet strength

Total assets of $2.9tn were $208bn or 8% higher than at 31 December 2019 on a reported basis, and 11% higher on a constant currency basis. The increase in total assets included growth in cash balances and in financial investments, as well as from an increase in derivative assets, mainly reflecting gains on interest rate derivatives. The increase in derivative assets was consistent with the increase in derivative liabilities as the underlying risk is broadly matched. On a constant currency basis, loans and advances to customers grew by $12bn during 1H20.

Customer accounts of $1.5tn increased by $93bn, or $133bn on a constant currency basis, as corporate and personal customers consolidated their funds and redeployed them into cash, with growth in all global businesses. The growth reflected customers spending less during lockdown restrictions and the depositing of loans from government-backed schemes.

Distributable reserves

The distributable reserves of HSBC Holdings at 30 June 2020 were $33.1bn, compared with $31.7bn at 31 December 2019. The increase was primarily driven by profits generated during the year.

Capital position

We actively manage the Group’s capital position to support our business strategy and meet our regulatory requirements at all times, including under stress, while optimising our capital efficiency. To do this, we monitor our capital position using a number of measures. These include: our capital ratios, the impact on our capital ratios as a result of stress, and the degree of double leverage being run by HSBC Holdings. Double leverage is a constraint on managing our capital position, given the complexity of the Group’s subsidiary structure and the multiple regulatory regimes under which we operate. For further details, see page 81.

Our CET1 ratio at 30 June 2020 was 15.0%, up from 14.7% at 31 December 2019. This increase included the impact of the cancellation of the 4Q19 dividend and the current suspension of dividends on ordinary shares. These increases were partly offset by an increase in RWAs.

Liquidity position

We actively manage the Group’s liquidity and funding to support our business strategy and meet regulatory requirements at all times, including under stress. To do this, we monitor our position using a number of risk appetite measures, including the liquidity coverage ratio and the net stable funding ratio. At 30 June 2020, we held high-quality liquid assets of $654bn.

HSBC Holdings plc Interim Report 2020 | 13 |

Wealth and Personal Banking

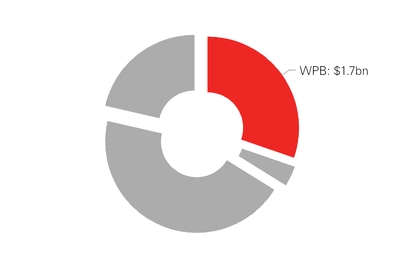

Contribution to Group 1H20 adjusted profit before tax<>

| % contribution to Group | |

| 30 | % |

WPB was formed in the second quarter by combining our Retail Banking and Wealth Management and Global Private Banking businesses. We supported our customers during the Covid-19 crisis through payment holidays, short-term credit facilities and access to cash. We continue to invest in digital capabilities to make it easier for customers to bank with us. Performance in 1H20 reflected a rise in adjusted ECL charges and a decline in adjusted revenue from the fall in global equity prices and lower interest rates.

We provide a full range of retail banking and wealth services to more than 39 million customers from personal banking to ultra high net worth individuals and their families.

We offer locally-tailored products and services across multiple channels for our customers’ everyday banking needs, as well as insurance, investment management and Private Wealth Solutions for those with more sophisticated requirements. Our global presence provides for customers with international needs.

| Adjusted results<> | Half-year to | 1H20 vs 1H19 | |||||||||

| 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Dec 2019 $m | $m | % | |||||||

| Net operating income | 11,251 | 12,861 | 12,492 | (1,610 | ) | (13 | ) | ||||

| ECL | (2,202 | ) | (527 | ) | (829 | ) | (1,675 | ) | >(100) | ||

| Operating expenses | (7,346 | ) | (7,551 | ) | (7,685 | ) | 205 | 3 | |||

| Share of profit in associates and JVs | (8 | ) | 41 | 11 | (49 | ) | >(100) | ||||

| Profit before tax | 1,695 | 4,824 | 3,989 | (3,129 | ) | (65 | ) | ||||

| RoTE excluding significant items and UK bank levy (annualised, YTD) (%) | 6.0 | 22.1 | 19.7 | ||||||||

| Management view of adjusted revenue <> | Half-year to | 1H20 vs 1H19 | |||||||||

| 30 Jun 2020 $m | 30 Jun 2019 $m | 31 Dec 2019 $m | $m | % | |||||||

| Retail Banking | 6,896 | 7,649 | 7,879 | (753 | ) | (10 | ) | ||||

| – net interest income | 6,301 | 6,810 | 7,067 | (509 | ) | (7 | ) | ||||

| – non-interest income | 595 | 839 | 812 | (244 | ) | (29 | ) | ||||

| Wealth Management | 3,606 | 4,506 | 4,056 | (900 | ) | (20 | ) | ||||

| – investment distribution | 1,602 | 1,696 | 1,554 | (94 | ) | (6 | ) | ||||

| – life insurance manufacturing | 587 | 1,371 | 1,078 | (784 | ) | (57 | ) | ||||

| – Global Private Banking | 921 | 925 | 927 | (4 | ) | — | |||||

| net interest income | 372 | 441 | 439 | (69 | ) | (16 | ) | ||||

| non-interest income | 549 | 484 | 488 | 65 | 13 | ||||||

| – asset management | 496 | 514 | 497 | (18 | ) | (4 | ) | ||||

Other1 | 262 | 404 | 366 | (142 | ) | (35 | ) | ||||

| Balance Sheet Management, Holdings interest expense and Argentina hyperinflation | 487 | 302 | 191 | 185 | 61 | ||||||

Net operating income2 | 11,251 | 12,861 | 12,492 | (1,610 | ) | (13 | ) | ||||

1 ‘Other’ mainly includes interest on capital and the distribution and manufacturing (where applicable) of non-wealth insurance products.

2 ‘Net operating income’ means net operating income before change in expected credit losses and other credit impairment charges (also referred to as ‘Revenue’).

| 14 | HSBC Holdings plc Interim Report 2020 |

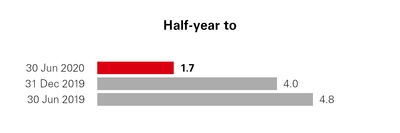

Financial performance

Adjusted profit before tax of $1.7bn in 1H20 was $3.1bn or 65% lower than in 1H19. This reflected an increase in adjusted ECL, as well as lower adjusted revenue. Lower revenue was driven by a reduction in life insurance manufacturing revenue largely from negative market impacts following a fall in equity markets in 1Q20, although these losses were partially reversed in 2Q20 as equity markets recovered. Retail Banking revenue was also lower from the reduction in interest rates.

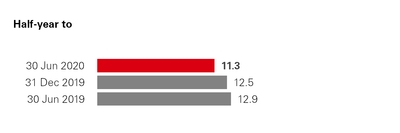

Adjusted revenue of $11.3bn was $1.6bn or 13% lower, and included the non-recurrence of 1H19 disposal gains in Argentina and Mexico of $133m.

In Retail Banking, revenue of $6.9bn was down $0.8bn or 10%.

| • | Net interest income was $0.5bn lower due to narrower margins, notably in the second quarter, as global interest rates fell as a result of the Covid-19 outbreak. This reduction was partly offset by deposit balance growth of $57bn or 9%, particularly in Hong Kong and the UK, and lending balance growth of $14bn or 4% compared with 1H19. |

| • | Non-interest income declined by $0.2bn from lower fee income earned on unsecured lending products. |

In Wealth Management, revenue of $3.6bn was down $0.9bn or 20%.

| • | Life insurance manufacturing revenue reduced by $0.8bn or 57%, primarily from an adverse movement in market impacts of $482m (an adverse movement of $334m in 1H20, compared with a favourable movement of $148m in 1H19). The value of new business written fell by $0.3bn or 37% as the reduction in volumes resulting from the Covid-19 outbreak was in part mitigated by actions to support remote engagement with customers, including digital enhancements to sales processes. |

| • | Investment distribution revenue was $0.1bn or 6% lower reflecting adverse market conditions in Hong Kong, which resulted in lower mutual fund sales, partly offset by higher brokerage fees from increased transaction volumes. |

| • | Global Private Banking revenue was stable, as higher investment revenue from increased market volatility and a rise in fees from advisory and discretionary mandates was broadly offset by the impact of lower interest rates on deposit revenue. |

Adjusted ECL of $2.2bn were $1.7bn higher than in 1H19, reflecting the global impact of the Covid-19 outbreak on the forward economic outlook of $1.2bn and from higher charges, notably in the UK, Asia and the US against unsecured lending driven by moderate credit deterioration.

Adjusted operating expenses of $7.3bn were $0.2bn or 3% lower, as a lower performance-related pay accrual and reduced discretionary expenditure more than offset the impact of inflation and our continued investment in digital and wealth initiatives.

Divisional highlights

$1.4tn

WPB wealth balances at 30 June 2020. This was a 3% year-on-year increase, and broadly unchanged from 31 December 2019.

$17bn

Growth in mortgage book in the UK (up 6%) and Hong Kong (up 5%) since 30 June 2019.

Adjusted profit before tax <>

($bn)

$1.7bn

Adjusted net operating income <>

($bn)

$11.3bn

HSBC Holdings plc Interim Report 2020 | 15 |

Commercial Banking

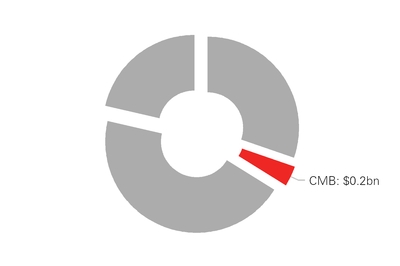

Contribution to Group 1H20 adjusted profit before tax<>

| % contribution to Group | |

| 3 | % |

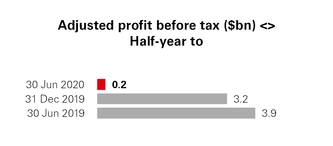

CMB continued to support our customers’ liquidity and working capital needs, growing lending and deposit balances, while our ongoing investment in technology has enabled us to support customers under exceptionally challenging conditions. Performance in 1H20 was adversely impacted by an increase in adjusted ECL charges and the fall in interest rates globally.

We support approximately 1.3 million business customers in 53 countries and territories, ranging from small enterprises focused primarily on their domestic markets to large companies operating globally.