link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

link to searchable text of slide shown above

GREENVILLE FIRST BANCSHARES, INC.

www.greenvillefirst.com

[LOGO]

Southeast - February 6-7, 2006

Forward-Looking Statements

During the course of this presentation, management may make projections and forward-looking statements regarding events or the future financial performance of Greenville First Bancshares, Inc. We wish to caution you that these forward-looking statements involve certain risks and uncertainties, including a variety of factors that may cause Greenville First's actual results to differ materially from the anticipated results expressed in these forward-looking statements. Investors are cautioned not to place undue reliance on these forward-looking statements and are advised to review the risk factors that may affect Greenville First's operating results in documents filed by Greenville First Bancshares, Inc. with the Securities and Exchange Commission, including the Form SB-2 Registration Statement, the Annual report on Form 10-KSB and other required filings. Greenville First assumes no duty to update the forward-looking statements made in this presentation.

[LOGO]

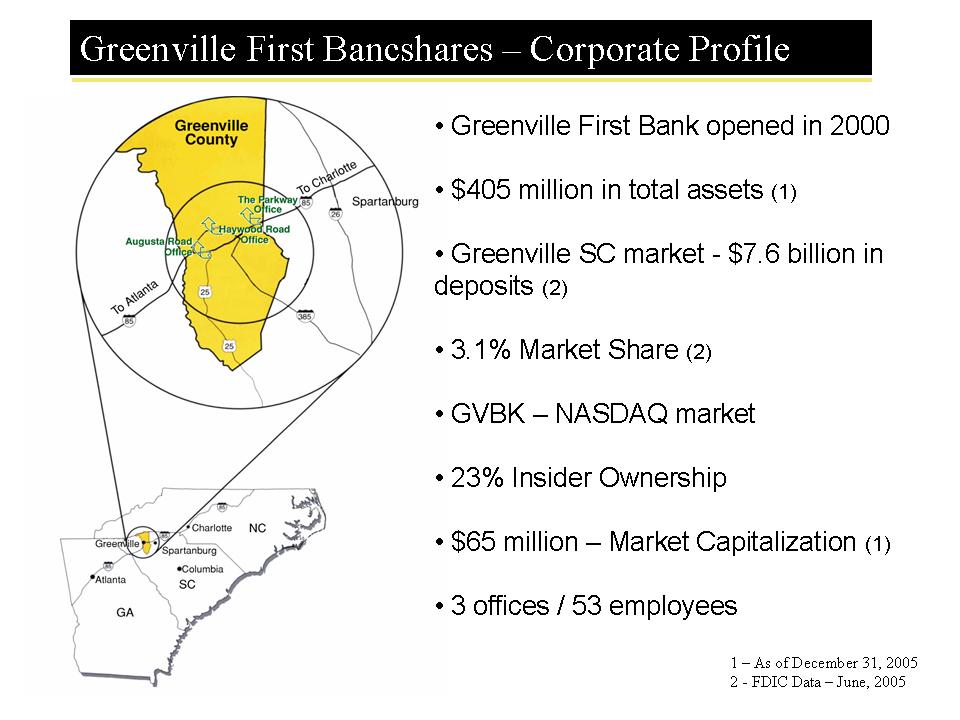

Greenville First Bancshares - Corporate Profile

[CHART]

Greenville First Bank opened in 2000

$405 million in total assets (1)

Greenville SC market - $7.6 billion in deposits (2)

3.1% Market Share (2)

GVBK - NASDAQ market

23% Insider Ownership

$65 million - Market Capitalization (1)

3 offices / 53 employees

1 - As of December 31, 2005

2 - FDIC Data - June, 2005

GVBK - Investment Profile

Growth Story

Performance Driven Leadership

Unique Client FIRST Model

Dynamic Greenville, SC Market

Performance / Momentum

[LOGO]

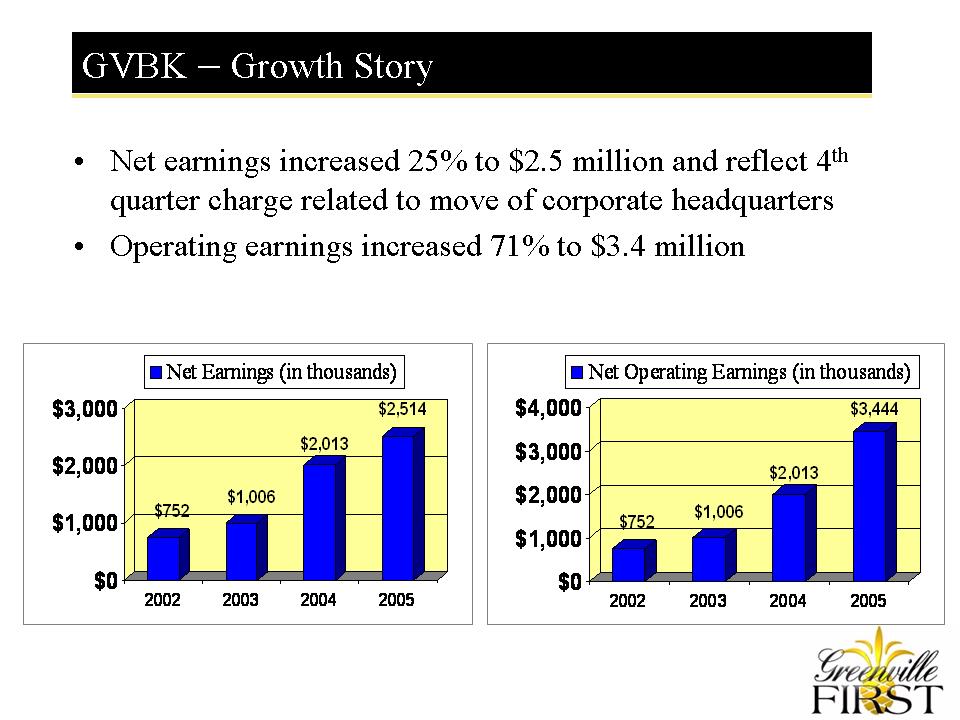

GVBK - Growth Story

Total Assets (in millions)

[CHART]

Loans (in millions)

[CHART]

[LOGO]

GVBK - Growth Story

Net Earnings (in thousands)

[CHART]

Net Operating Earnings (in thousands)

[CHART]

[LOGO]

GVBK - Performance Driven Leadership

Market Knowledge & Experience

Average executive team member has worked in the market for more than 20 years

Executive team brings experience from 7 separate banks

[LOGO]

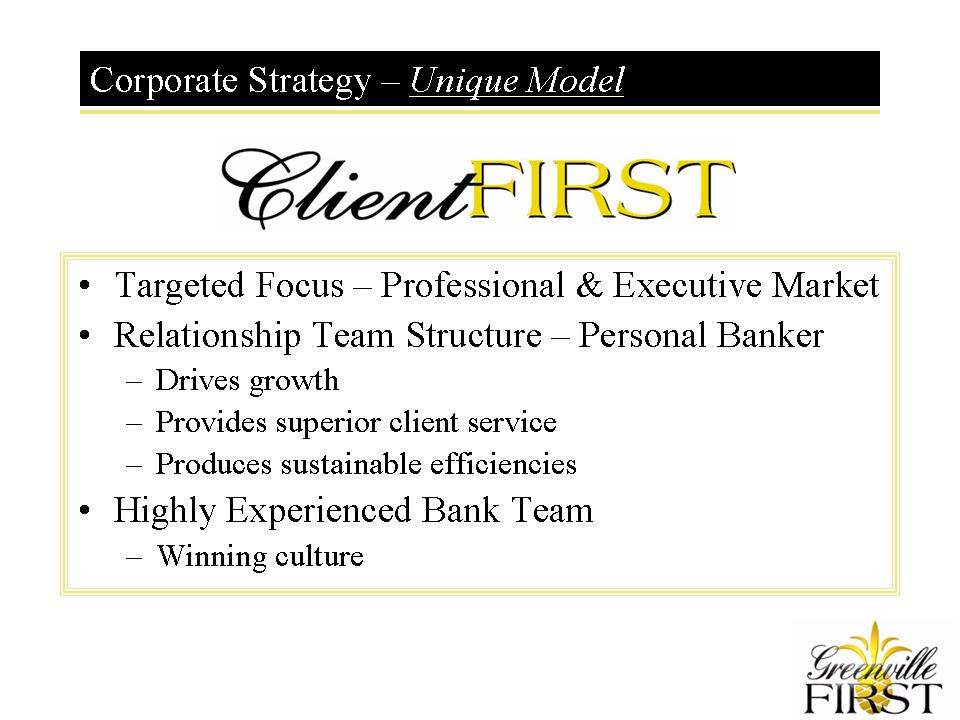

Corporate Strategy - Unique Model

Client FIRST

- Drives growth

- Provides superior client service

- Produces sustainable efficiencies

- Winning culture

[LOGO]

Dynamic Greenville Market

[CHART]

SC's most populous county

Largest deposit market in SC with over $7.6 billion in deposits

Deposit growth averaging 9% annually over the past five years

Diverse economy as market is home to over 240 international companies including BMW & Michelin

Source - FDIC 2005

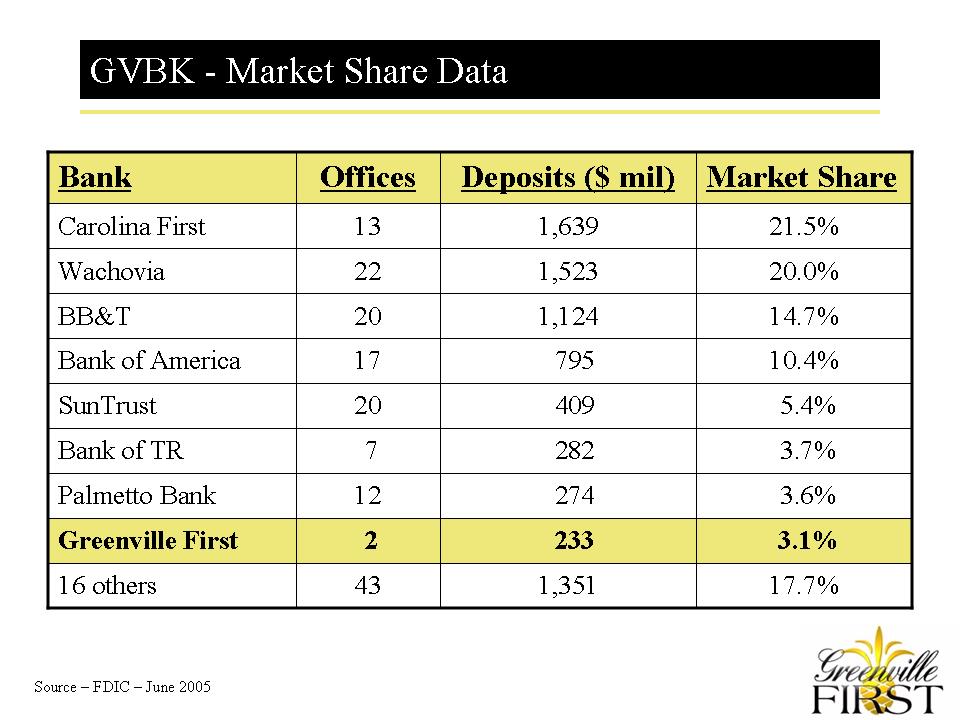

GVBK - Market Share Data

[CHART]

Source - FDIC - June 2005

[LOGO]

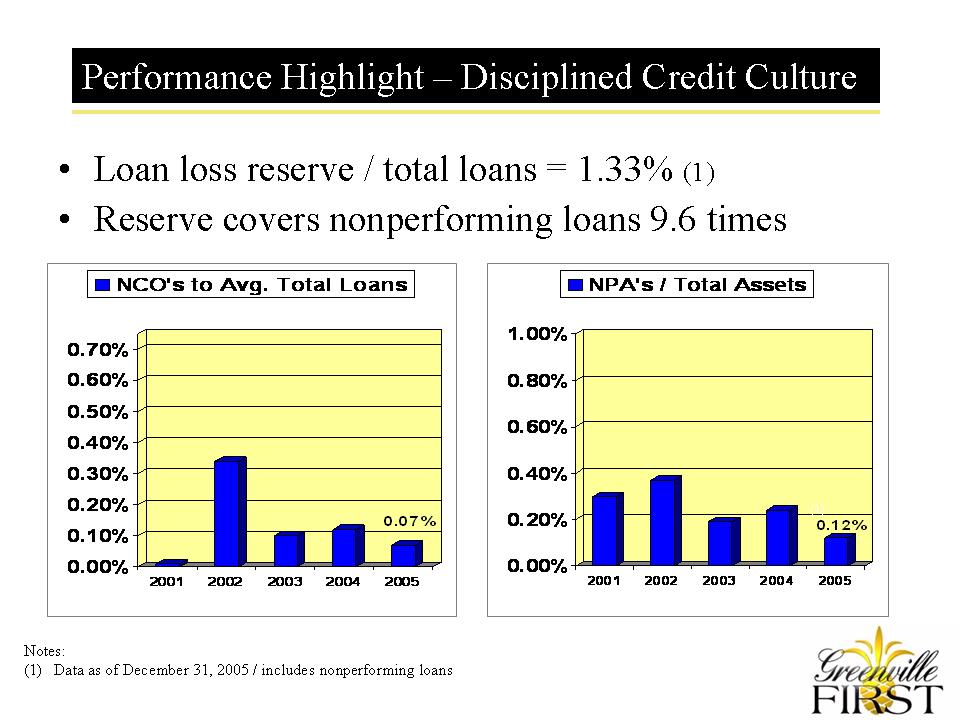

Performance Highlight - Disciplined Credit Culture

NCO's to Avg. Total Loans

[CHART]

NPA's /Total Assets

[CHART]

Notes:

(1) Data as of December 31, 2005 / includes nonperforming loans

[LOGO]

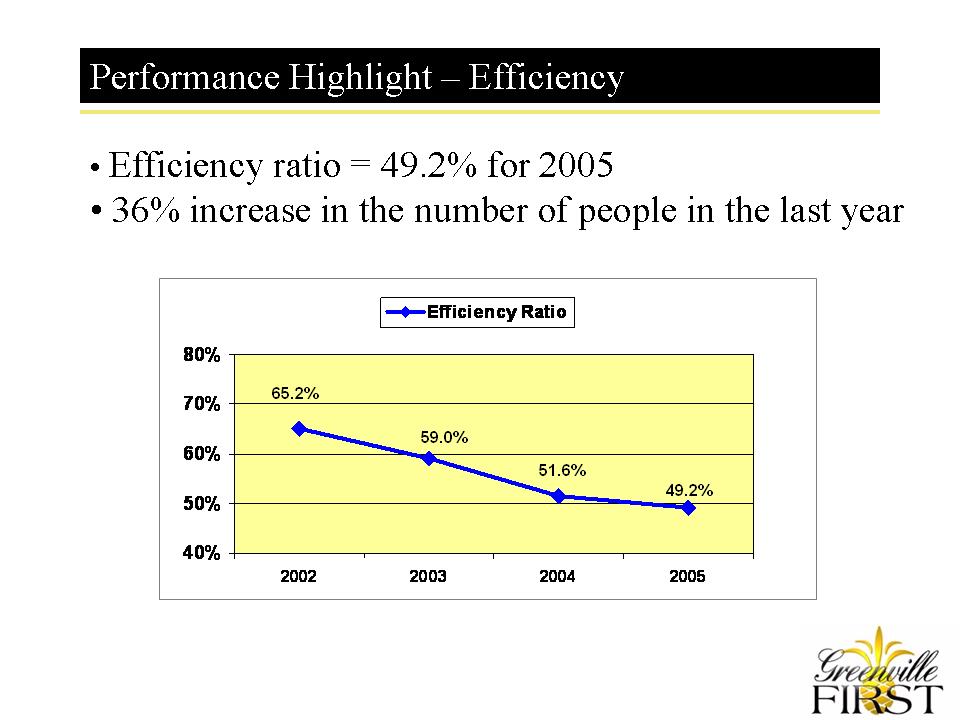

Performance Highlight - Efficiency

Efficiency Ratio

[CHART]

[LOGO]

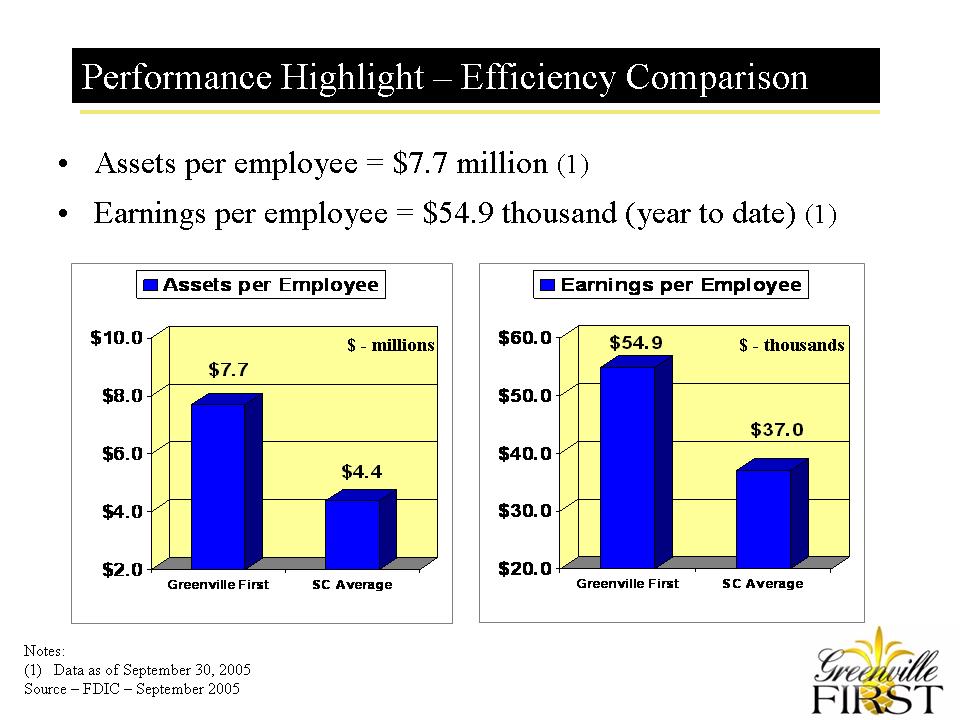

Performance Highlight - Efficiency Comparison

Assets per Employee

[CHART]

Earnings per Employee

[CHART]

Notes:

(1) Data as of September 30, 2005

Source - FDIC - September 2005

[LOGO]

GVBK - Momentum

- ROA & margin improvement

- Operating earnings increased 71%

- 36% increase in retail deposits

- 24% increase in transaction accounts

Return on Assets - operating earnings

[CHART]

Net Interest Margin

[CHART]

[LOGO]

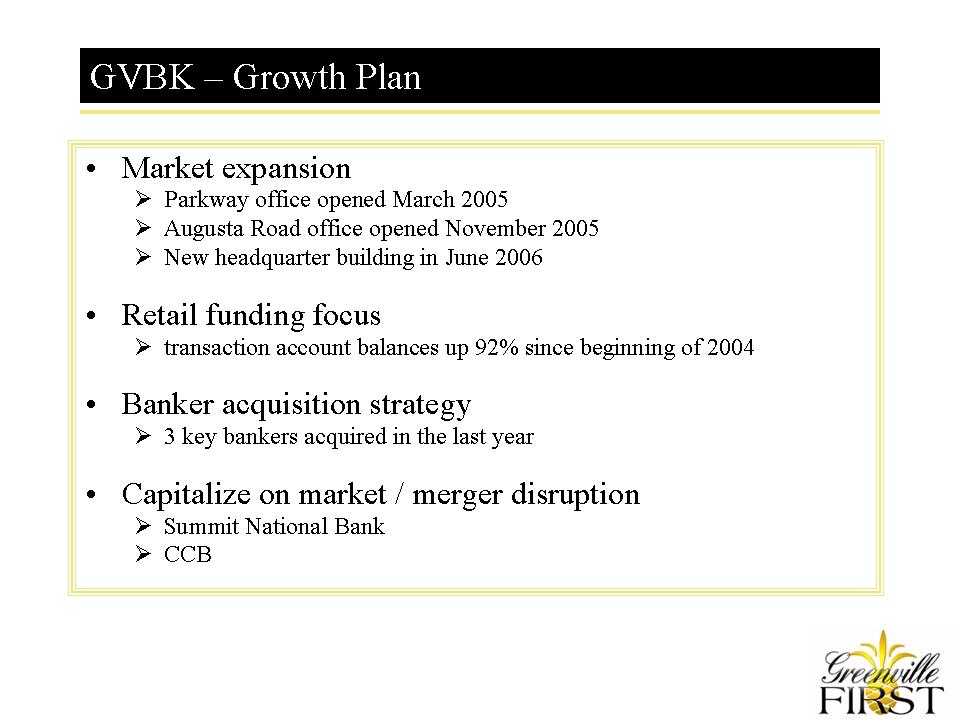

GVBK - Growth Plan

Market expansion

Parkway office opened March 2005

Augusta Road office opened November 2005

New headquarter building in June 2006

[LOGO]

GVBK - Summary

Experienced & Performance Driven Leadership

Unique Client FIRST Model

Attractive Greenville, SC Market

Growth Story

Solid Performance / Disciplined Credit Culture

Momentum

[LOGO]

Reconciliation of Non-GAAP Financial Measures

This presentation contains financial information determined by methods other than in accordance with Generally Accepted Accounting Principles ("GAAP"). Operating noninterest expense is used to compute the operating efficiency ratio.

Net income, (GAAP) $2,514

Non-operating items:

Impairment on real estate, net of income taxes 930

Operating earnings $3,444

Noninterest expense, (GAAP) $7,856

Non-operating items:

Impairment on real estate 1,500

Operating noninterest expense $6,356

[LOGO]