| Filed by Bookham Technology plc |

| pursuant to Rule 425 under the Securities Act of 1933 |

| Subject Company: New Focus, Inc. |

| Commission File No.: 333-109904 |

This filing relates to a proposed merger between Bookham Technology plc (“Bookham”) and New Focus, Inc. (“New Focus”) pursuant to the terms of an Agreement and Plan of Merger, dated as of September 21, 2003, by and among Bookham, Budapest Acquisition Corp. and New Focus.

On February 10, 2004, Bookham posted the following slide presentation to its website.

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

[LOGO]

Fourth Quarter and Full Year

2003 Results Announcement

February 2004 - UK

|

| Thinking optical solutions |

1

Disclaimer

Any remarks that we may make about future expectations, plans and prospects for Bookham constitute forward-looking statements for purposes of the safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those indicated by these forward- looking statements as a result of various important factors, including those discussed in our Annual Report on Form 20-F for the year ended December 31, 2002, as amended, which is on file with the Securities and Exchange Commission (SEC) and Registration Statement of Form F-4, which is also on file with the SEC. Forward-looking statements represent Bookham’s estimates as of the date made, and should not be relied upon as representing Bookham’s estimates as of any subsequent date. While Bookham may elect to update forward-looking statements in the future, it disclaims any obligation to do so.

www.bookham.com

2

Agenda

• Recent highlights

• Markets, customers and products

• Operations

• Financials

• Summary

3

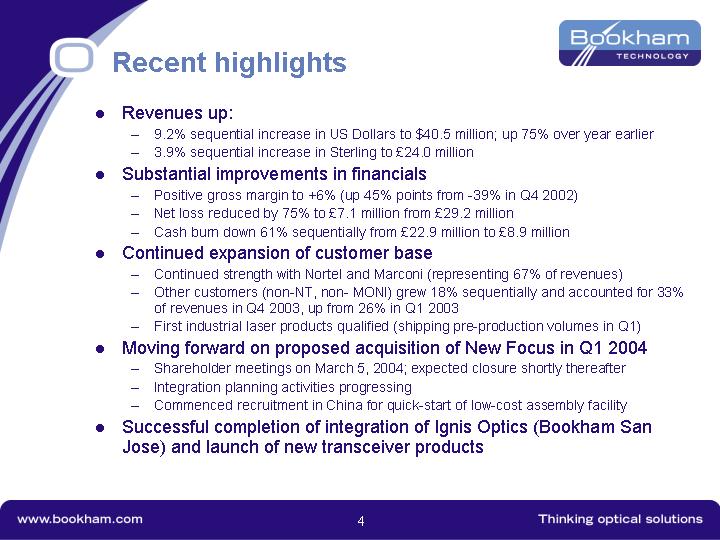

Recent highlights

• Revenues up:

• 9.2% sequential increase in US Dollars to $40. 5 million; up 75% over year earlier

• 3.9% sequential increase in Sterling to £24.0 million

• Substantial improvements in financials

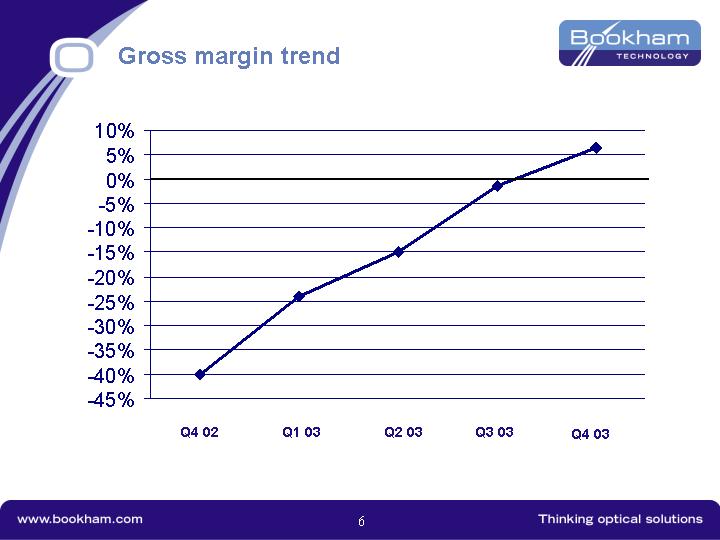

• Positive gross margin to +6% (up 45% points from -39% in Q4 2002)

• Net loss reduced by 75% to £7.1 million from £29. 2 million

• Cash burn down 61% sequentially from £22. 9 million to £8. 9 million

• Continued expansion of customer base

• Continued strength with Nortel and Marconi (representing 67% of revenues)

• Other customers (non-NT, non-MONI) grew 18% sequentially and accounted for 33% of revenues in Q4 2003, up from 26% in Q1 2003

• First industrial laser products qualified (shipping pre-production volumes in Q1)

• Moving forward on proposed acquisition of New Focus in Q1 2004

• Shareholder meetings on March 5, 2004; expected closure shortly thereafter

• Integration planning activities progressing

• Commenced recruitment in China for quick-start of low-cost assembly facility

• Successful completion of integration of Ignis Optics (Bookham San Jose) and launch of new transceiver products

4

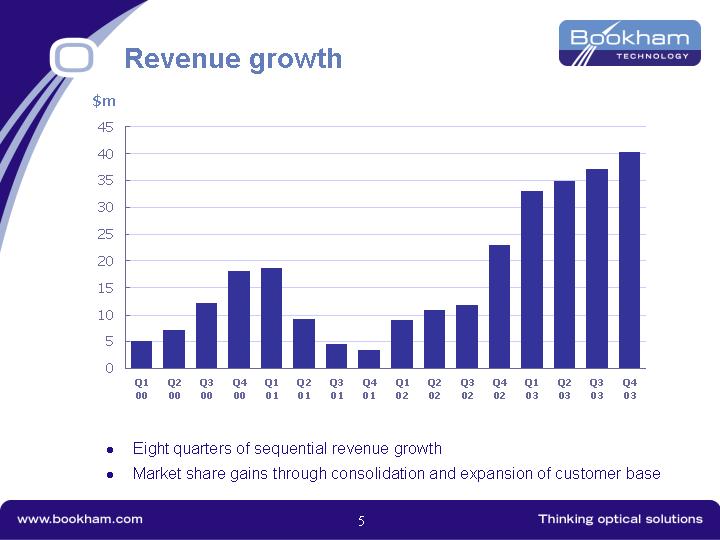

Revenue growth

[CHART]

• Eight quarters of sequential revenue growth

• Market share gains through consolidation and expansion of customer base

5

Gross margin trend

[CHART]

6

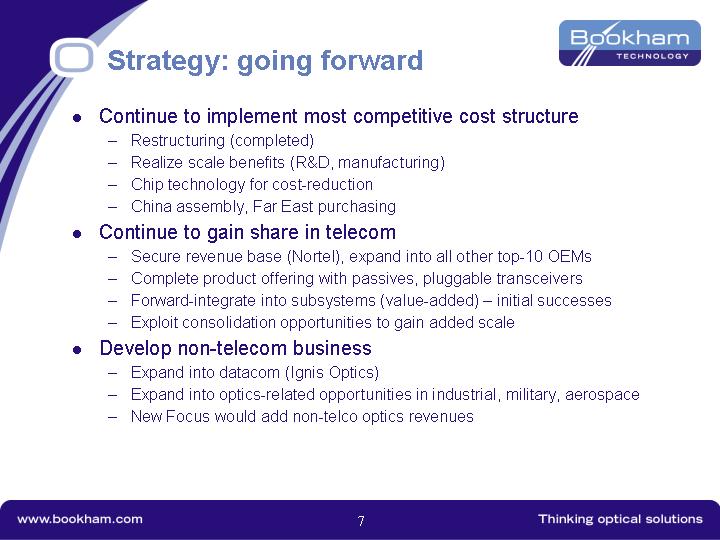

Strategy: going forward

• Continue to implement most competitive cost structure

• Restructuring (completed)

• Realize scale benefits (R&D, manufacturing)

• Chip technology for cost-reduction

• China assembly, Far East purchasing

• Continue to gain share in telecom

• Secure revenue base (Nortel), expand into all other top-10 OEMs

• Complete product offering with passives, pluggable transceivers

• Forward-integrate into subsystems (value-added) – initial successes

• Exploit consolidation opportunities to gain added scale

• Develop non-telecom business

• Expand into datacom(Ignis Optics)

• Expand into optics-related opportunities in industrial, military, aerospace

• New Focus would add non-telco optics revenues

7

Markets, Customers and Products

8

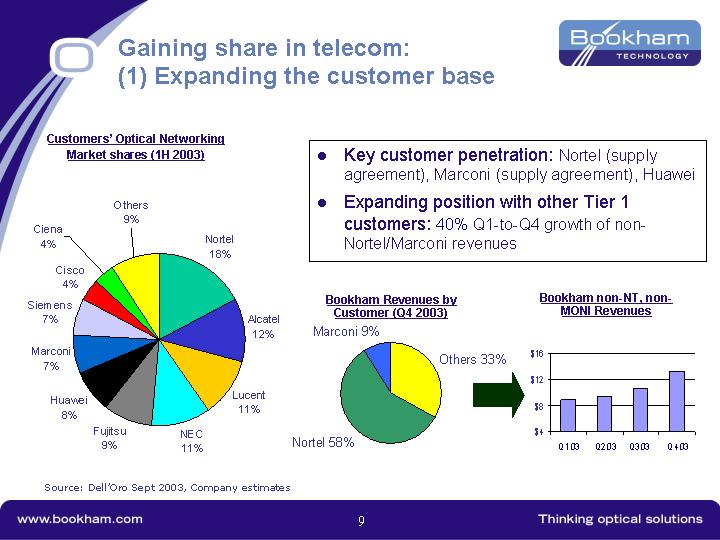

Gaining share in telecom:

(1) Expanding the customer base

Customers’ Optical Networking |

|

Market shares (1H 2003) |

|

|

|

[CHART] |

|

|

|

Source: Dell’Oro Sept 2003, Company estimates

• Key customer penetration: Nortel (supply agreement), Marconi (supply agreement), Huawei

• Expanding position with other Tier 1 customers: 40% Q1-to-Q4 growth of non-Nortel/Marconi revenues

Bookham Revenues by |

|

Customer (Q4 2003) |

|

|

|

[CHART] |

|

|

|

Bookham non-NT, non-MONI Revenues |

|

|

|

[CHART] |

|

9

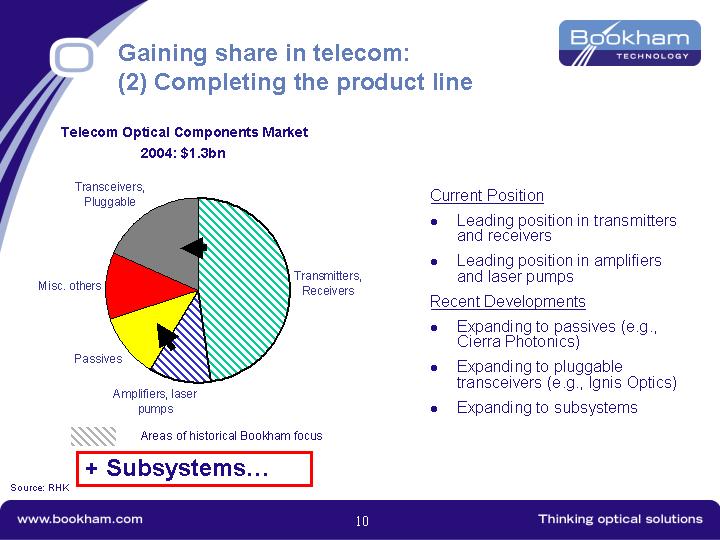

Gaining share in telecom:

(2) Completing the product line

Telecom Optical Components Market |

|

2004: $1.3bn |

|

|

|

[CHART] |

|

+ Subsystems…

Source: RHK

Current Position

• Leading position in transmitters and receivers

• Leading position in amplifiers and laser pumps

Recent Developments

• Expanding to passives (e.g., Cierra Photonics)

• Expanding to pluggable transceivers (e.g., Ignis Optics)

• Expanding to subsystems

10

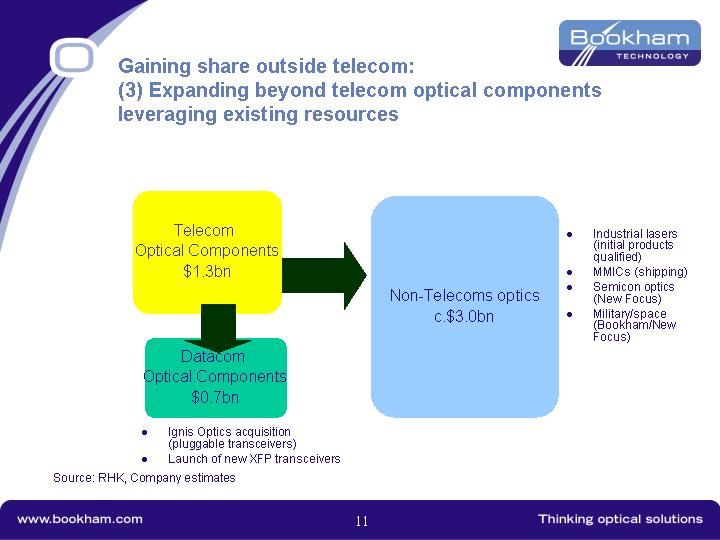

Gaining share outside telecom:

(3) Expanding beyond telecom optical components leveraging existing resources

Telecom Optical Components $1.3bn

Non-Telecoms optics c.$3.0bn

• Industrial lasers (initial products qualified)

• MMICs (shipping)

• Semicon optics (New Focus)

• Military/space (Bookham/New Focus)

Datacom Optical Components $0.7bn

• Ignis Optics acquisition (pluggable transceivers)

• Launch of new XFP transceivers

Source: RHK, Company estimates

11

Operations

12

Completed post-acquisition restructuring Bookham facilities:

Caswell, UK

Main GaAs and InP fab

180k sq ft 37k sq ft clean room

Established 1940s

Fully owned

1 MAIN CHIP FAB

[GRAPHIC]

1 MAIN ASSEMBLY PLANT

[GRAPHIC]

Paignton, UK

Main A&T facility

240k sq ft 92k sq ft clean room

Established 1970s

Fully owned

Milton, UK |

|

HQ |

|

|

|

[GRAPHIC] |

|

|

|

Zurich, Switzerland |

|

980 Pump Laser Chip |

|

|

|

[GRAPHIC] |

|

|

|

Santa Rosa, US |

|

Thin Film Filters |

|

|

|

[GRAPHIC] |

|

|

|

Kanata, Canada |

|

R&D |

|

|

|

[GRAPHIC] |

|

|

|

San Jose, US |

|

XFP/SFP Transceivers |

|

|

|

[GRAPHIC] |

|

13

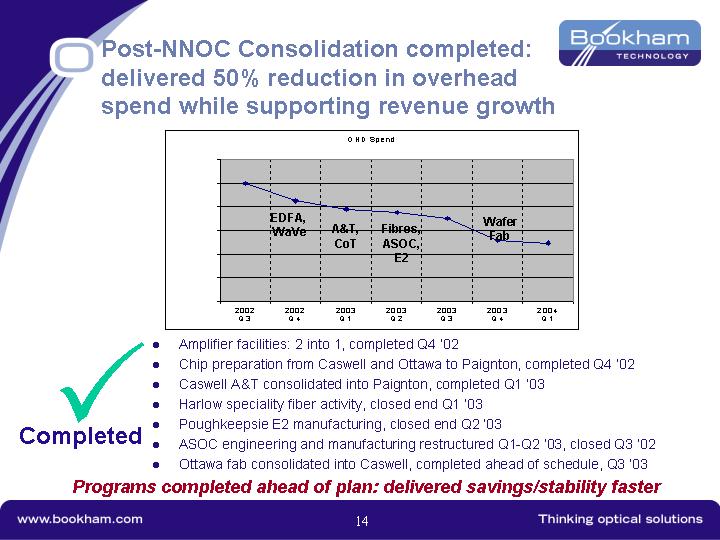

Post-NNOC Consolidation completed:

delivered 50% reduction in overhead spend while supporting revenue growth

[CHART]

Completed

• Amplifier facilities: 2 into 1, completed Q4 ‘02

• Chip preparation from Caswell and Ottawa to Paignton, completed Q4 ‘02

• Caswell A&T consolidated into Paignton, completed Q1 ‘03

• Harlow speciality fiber activity, closed end Q1 ‘03

• Poughkeepsie E2 manufacturing, closed end Q2 ‘03

• ASOC engineering and manufacturing restructured Q1-Q2 ‘03, closed Q3 ‘02

• Ottawa fab consolidated into Caswell, completed ahead of schedule, Q3 ‘03

Programs completed ahead of plan: delivered savings/stability faster

14

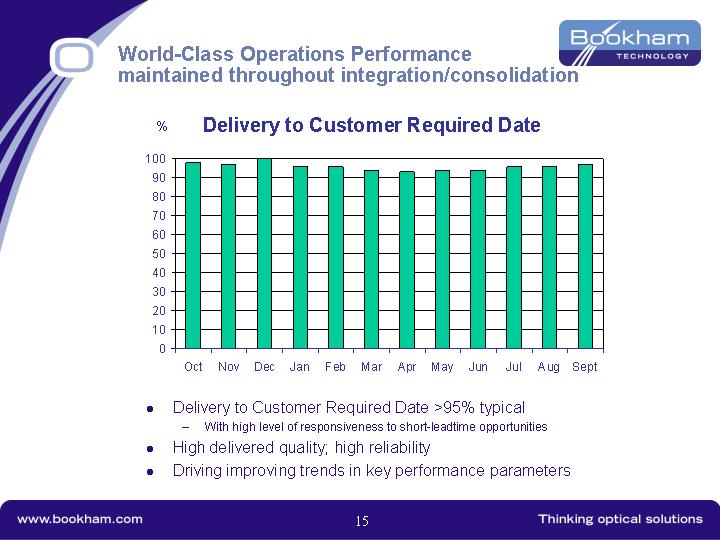

World-Class Operations Performance maintained throughout integration/consolidation

Delivery to Customer Required Date

[CHART]

• Delivery to Customer Required Date >95% typical

• With high level of responsiveness to short-leadtime opportunities

• High delivered quality; high reliability

• Driving improving trends in key performance parameters

15

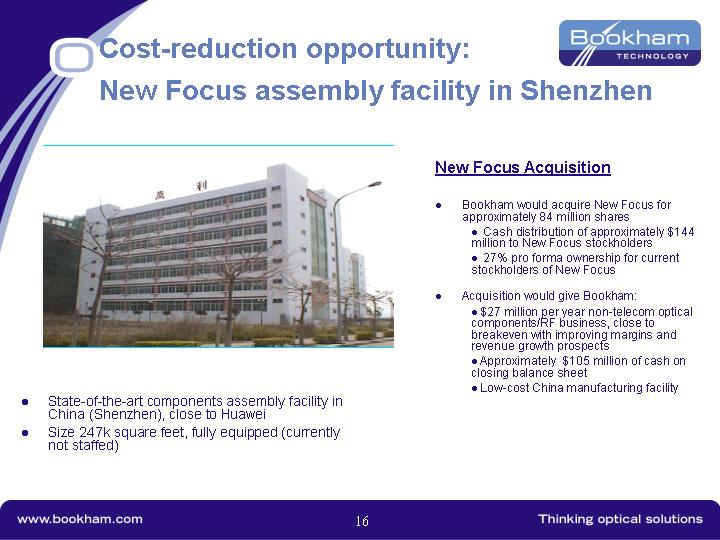

Cost-reduction opportunity:

New Focus assembly facility in Shenzhen

[GRAPHIC]

• State-of-the-art components assembly facility in China (Shenzhen), close to Huawei

• Size 247k square feet, fully equipped (currently not staffed)

New Focus Acquisition

• Bookham would acquire New Focus for approximately 84 million shares

• Cash distribution of approximately $144 million to New Focus stockholders

• 27% pro forma ownership for current stockholders of New Focus

• Acquisition would give Bookham:

• $27 million per year non-telecom optical components/RF business, close to breakeven with improving margins and revenue growth prospects

• Approximately $105 million of cash on closing balance sheet

• Low-cost China manufacturing facility

16

Financials

17

Financial highlights — Q4 2003

• Revenues £24.0 million ($40.5 million)

• up 9.2% in US Dollars; 3.9% in Sterling

• Nortel Networks and Marconi Communications represented 58% and 9% of revenues respectively

• Other customers up to 33% of revenues

• Gross margin up to +6% (UK GAAP), despite FX drop

• Net loss of £7.1 million (including exceptionals) compared with £29.2 million in Q3 2003 (75% improvement)

• Cash burn of £8.9 million (down from £22.9 million in Q3 03)

18

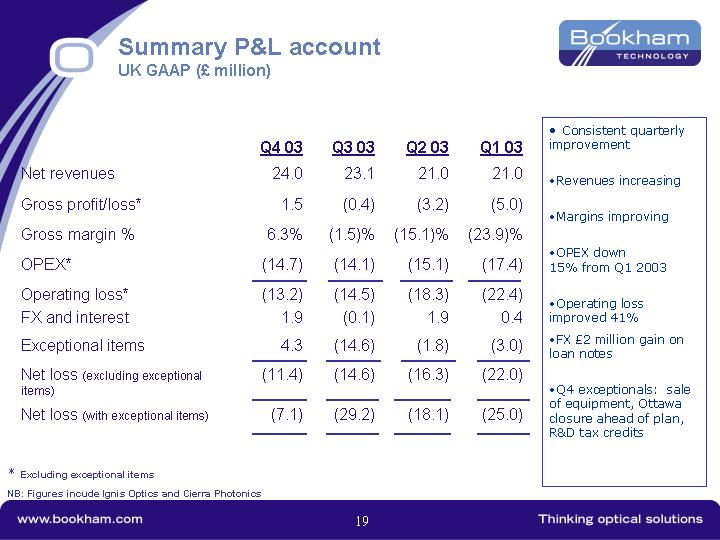

Summary P&L account

UK GAAP (£ million)

|

| Q4 03 |

| Q3 03 |

| Q2 03 |

| Q1 03 |

|

Net revenues |

| 24.0 |

| 23.1 |

| 21.0 |

| 21.0 |

|

Gross profit/loss* |

| 1.5 |

| (0.4 | ) | (3.2 | ) | (5.0 | ) |

Gross margin % |

| 6.3 | % | (1.5 | )% | (15.1 | )% | (23.9 | )% |

OPEX* |

| (14.7 | ) | (14.1 | ) | (15.1 | ) | (17.4 | ) |

Operating loss* |

| (13.2 | ) | (14.5 | ) | (18.3 | ) | (22.4 | ) |

FX and interest |

| 1.9 |

| (0.1 | ) | 1.9 |

| 0.4 |

|

Exceptional items |

| 4.3 |

| (14.6 | ) | (1.8 | ) | (3.0 | ) |

Net loss (excluding exceptional |

| (11.4 | ) | (14.6 | ) | (16.3 | ) | (22.0 | ) |

|

|

|

|

|

|

|

|

|

|

Net loss (with exceptional items) |

| (7.1 | ) | (29.2 | ) | (18.1 | ) | (25.0 | ) |

* Excluding exceptional items

NB: Figures incude Ignis Optics and Cierra Photonics

• Consistent quarterly improvement

• Revenues increasing

• Margins improving

• OPEX down 15% from Q1 2003

• Operating loss improved 41%

• FX £2 million gain on loan notes

• Q4 exceptionals: sale of equipment, Ottawa closure ahead of plan, R&D tax credits

19

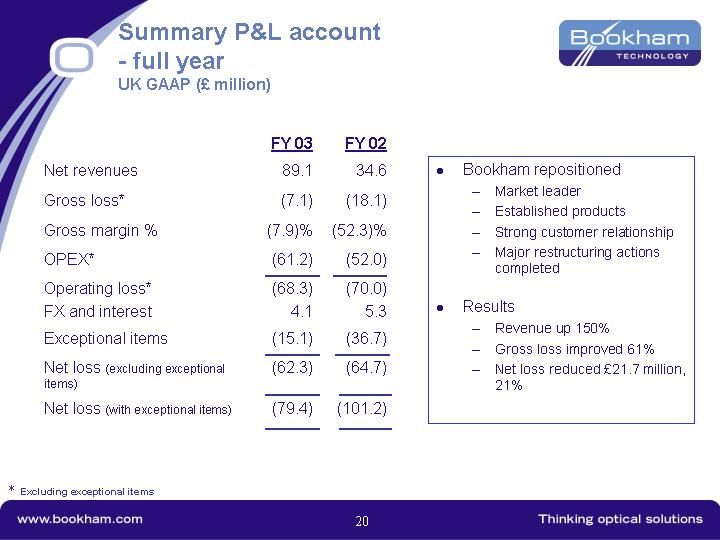

Summary P&L account - full year

UK GAAP (£ million)

|

| FY 03 |

| FY 02 |

|

Net revenues |

| 89.1 |

| 34.6 |

|

Gross loss* |

| (7.1 | ) | (18.1 | ) |

Gross margin % |

| (7.9 | )% | (52.3 | )% |

OPEX* |

| (61.2 | ) | (52.0 | ) |

Operating loss* |

| (68.3 | ) | (70.0 | ) |

FX and interest |

| 4.1 |

| 5.3 |

|

Exceptional items |

| (15.1 | ) | (36.7 | ) |

Net loss (excluding exceptional |

| (62.3 | ) | (64.7 | ) |

|

|

|

|

|

|

Net loss (with exceptional items) |

| (79.4 | ) | (101.2 | ) |

* Excluding exceptional items

• Bookham repositioned

• Market leader

• Established products

• Strong customer relationship

• Major restructuring actions completed

• Results

• Revenue up 150%

• Gross loss improved 61%

• Net loss reduced £21.7 million, 21%

20

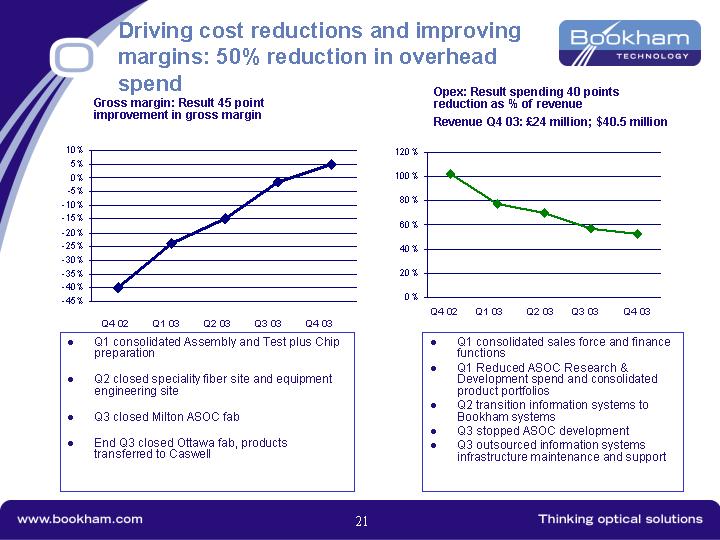

Driving cost reductions and improving margins: 50% reduction in overhead spend

Gross margin: Result 45 point improvement in gross margin

[CHART]

• Q1 consolidated Assembly and Test plus Chip preparation

• Q2 closed speciality fiber site and equipment engineering site

• Q3 closed Milton ASOC fab

• End Q3 closed Ottawa fab, products transferred to Caswell

Opex: Result spending 40 points reduction as % of revenue

Revenue Q4 03: £24 million; $40.5 million

[CHART]

• Q1 consolidated sales force and finance functions

• Q1 Reduced ASOC Research & Development spend and consolidated product portfolios

• Q2 transition information systems to Bookham systems

• Q3 stopped ASOC development

• Q3 outsourced information systems infrastructure maintenance and support

21

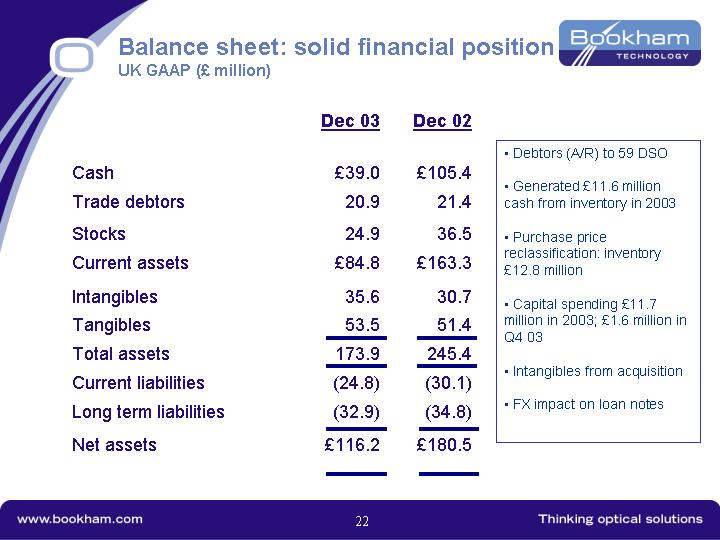

Balance sheet: solid financial position

UK GAAP (£ million)

|

| Dec 03 |

| Dec 02 |

| ||

|

|

|

|

|

| ||

Cash |

| £ | 39.0 |

| £ | 105.4 |

|

Trade debtors |

| 20.9 |

| 21.4 |

| ||

Stocks |

| 24.9 |

| 36.5 |

| ||

Current assets |

| £ | 84.8 |

| £ | 163.3 |

|

Intangibles |

| 35.6 |

| 30.7 |

| ||

Tangibles |

| 53.5 |

| 51.4 |

| ||

Total assets |

| 173.9 |

| 245.4 |

| ||

Current liabilities |

| (24.8 | ) | (30.1 | ) | ||

Long term liabilities |

| (32.9 | ) | (34.8 | ) | ||

Net assets |

| £ | 116.2 |

| £ | 180.5 |

|

• Debtors (A/R) to 59 DSO

• Generated £11.6 million cash from inventory in 2003

• Purchase price reclassification: inventory £12.8 million

• Capital spending £11.7 million in 2003; £1.6 million in Q4 03

• Intangibles from acquisition

• FX impact on loan notes

22

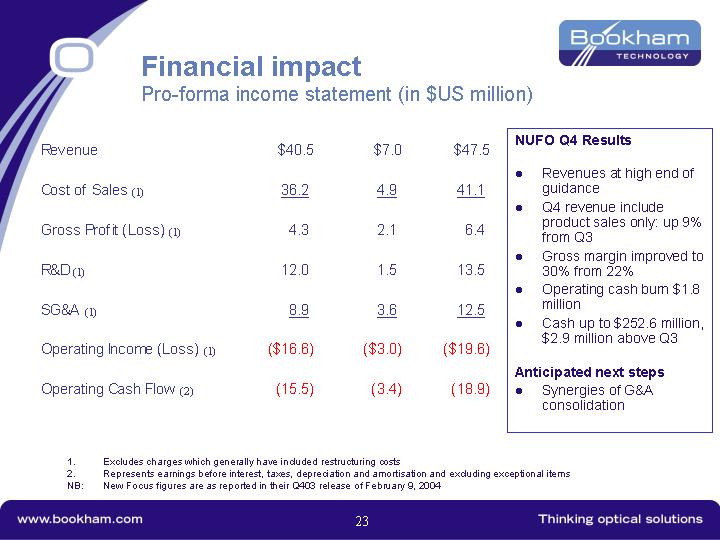

Financial impact

Pro-forma income statement (in $US million)

Q4 2003 |

| Bookham |

| New Focus |

| Combined |

| |||

Revenue |

| $ | 40.5 |

| $ | 7.0 |

| $ | 47.5 |

|

|

|

|

|

|

|

|

| |||

Cost of Sales (1) |

| 36.2 |

| 4.9 |

| 41.1 |

| |||

|

|

|

|

|

|

|

| |||

Gross Profit (Loss) (1) |

| 4.3 |

| 2.1 |

| 6.4 |

| |||

|

|

|

|

|

|

|

| |||

R&D (1) |

| 12.0 |

| 1.5 |

| 13.5 |

| |||

|

|

|

|

|

|

|

| |||

SG&A (1) |

| 8.9 |

| 3.6 |

| 12.5 |

| |||

|

|

|

|

|

|

|

| |||

Operating Income (Loss) (1) |

| $ | (16.6 | ) | $ | (3.0 | ) | $ | (19.6 | ) |

|

|

|

|

|

|

|

| |||

Operating Cash Flow (2) |

| (15.5 | ) | (3.4 | ) | (18.9 | ) | |||

(1). Excludes charges which generally have included restructuring costs

(2). Represents earnings before interest, taxes, depreciation and amortisation and excluding exceptional items

NB: New Focus figures are as reported in their Q403 release of February 9, 2004

NUFO Q4 Results

• Revenues at high end of guidance

• Q4 revenue include product sales only: up 9% from Q3

• Gross margin improved to 30% from 22%

• Operating cash burn $1.8 million

• Cash up to $252.6 million, $2.9 million above Q3

Anticipated next steps

• Synergies of G&A consolidation

23

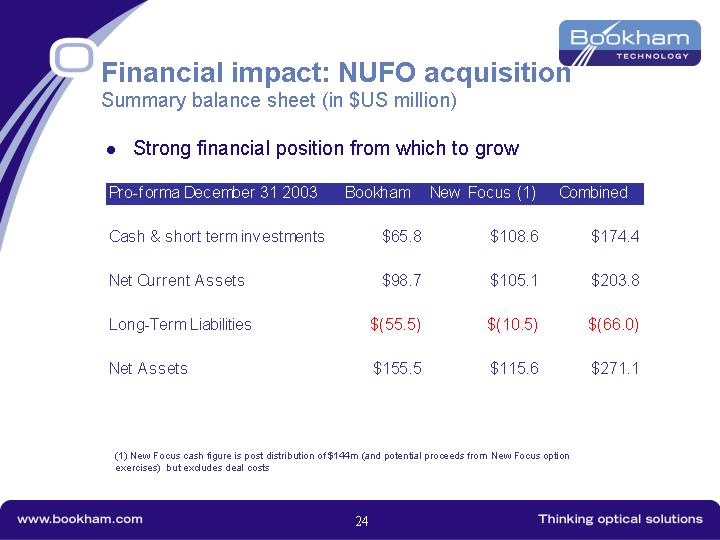

Financial impact: NUFO acquisition

Summary balance sheet (in $US million)

• Strong financial position from which to grow

Pro-forma December 31 2003 |

| Bookham |

| New Focus (1) |

| Combined |

| |||

|

|

|

|

|

|

|

| |||

Cash & short term investments |

| $ | 65.8 |

| $ | 108.6 |

| $ | 174.4 |

|

|

|

|

|

|

|

|

| |||

Net Current Assets |

| $ | 98.7 |

| $ | 105.1 |

| $ | 203.8 |

|

|

|

|

|

|

|

|

| |||

Long-Term Liabilities |

| $ | (55.5 | ) | $ | (10.5 | ) | $ | (66.0 | ) |

|

|

|

|

|

|

|

| |||

Net Assets |

| $ | 155.5 |

| $ | 115.6 |

| $ | 271.1 |

|

(1) New Focus cash figure is post distribution of $144m (and potential proceeds from New Focus option exercises) but excludes deal costs

24

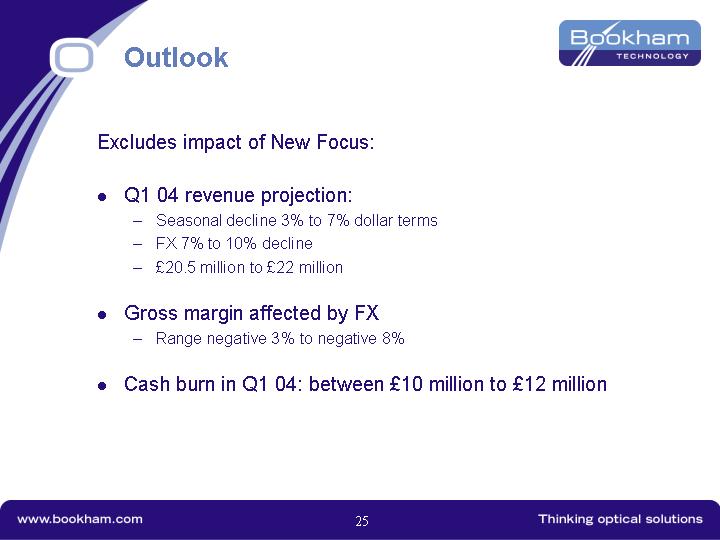

Outlook

Excludes impact of New Focus:

• Q1 04 revenue projection:

• Seasonal decline 3% to 7% dollar terms

• FX 7% to 10% decline

• £20.5 million to £22 million

• Gross margin affected by FX

• Range negative 3% to negative 8%

• Cash burn in Q1 04: between £10 million to £12 million

25

Summary

26

Summary

• Strong market position: #2 worldwide in telecom optical components

• Growing revenues

• Hugely improved financials

• Strong telecom customer base and product line-up, steadily expanding (new customers, new products)

• Attacking non-telecom markets for added profits leveraging current assets and know-how

• Strong cost-effective manufacturing base, exceptional operational execution

• Deep management expertise

• Proposed New Focus acquisition to be voted on March 5, 2004, should add additional non-telecom revenues, significant cash and low-cost assembly site in China

• Track record of consolidation and successful integration

27

[LOGO]

Thinking optical solutions

28

Appendix

29

Key facts

• Founded in 1988

• 1998: First commercial products (transceivers)

• 1998: Intel and Cisco invest in Bookham

• April 2000: IPO, started trading on NASDAQ and London Stock Exchange

(market downturn: developed new strategy)

• Feb 2002: acquired Marconi’s optical component business

• November 2002: Acquired Nortel Networks Optical Components (NNOC)

• One of largest and most widely deployed product lines in the industry

• Leaders in Tx and Rx, and in amplification/pumps

• July 2003: acquired Cierra Photonics (thin film filters)

• August 2003: Completed integration of former Nortel facilities

• September 2003: announced acquisition of New Focus

• October 2003: acquired Ignis Optics (XFP/SFP transceivers)

Now number 2 position worldwide in telecom optical components

30

Current Bookham positioning

• No. 2 worldwide in telecom optical components

• Eight quarters of sequential revenue growth

• Comprehensive, end-to-end product portfolio of active components and amplifiers, now broadening to remaining telecom market segments (passives, transceivers)

• Strong and expanding customer base

• Strategic relationship with Nortel (supply and R&D agreements), the No. 1 optical systems vendor

• Marconi and Huawei significant current customers

• Expanding to other tier-1 OEMs

• Emerging non-telecom optical business leveraging existing Bookham technologies

• Proven ability to acquire and consolidate companies (Marconi-Nortel-Cierra-Ignis)

• Efficient, very strong integrated manufacturing capability

• Facilities consolidation completed

• Caswell fab upgraded and ramping up Ottawa designs: leading-edge 3” InP and 6” GaAs

• Rapidly improving financials

• Proposed acquisition of New Focus brings:

• Additional market segments

• Low cost China assembly facility

• Significant additional cash on balance sheet

31

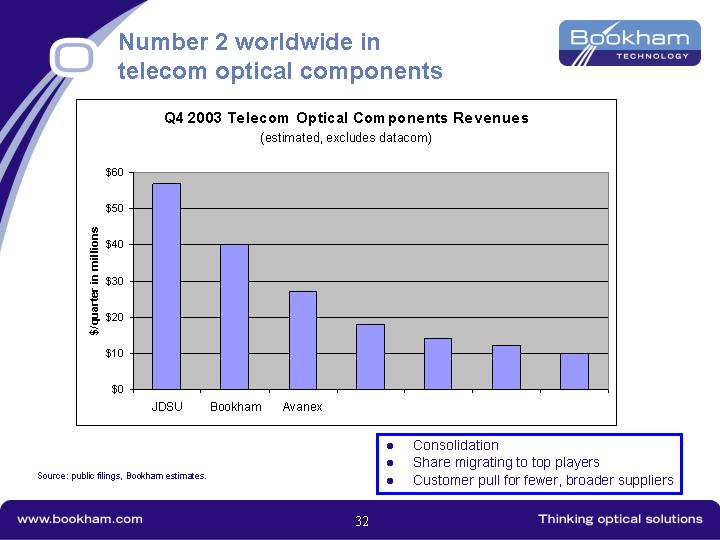

Number 2 worldwide in telecom optical components

[CHART]

Source: public filings, Bookham estimates.

• Consolidation

• Share migrating to top players

• Customer pull for fewer, broader suppliers

32

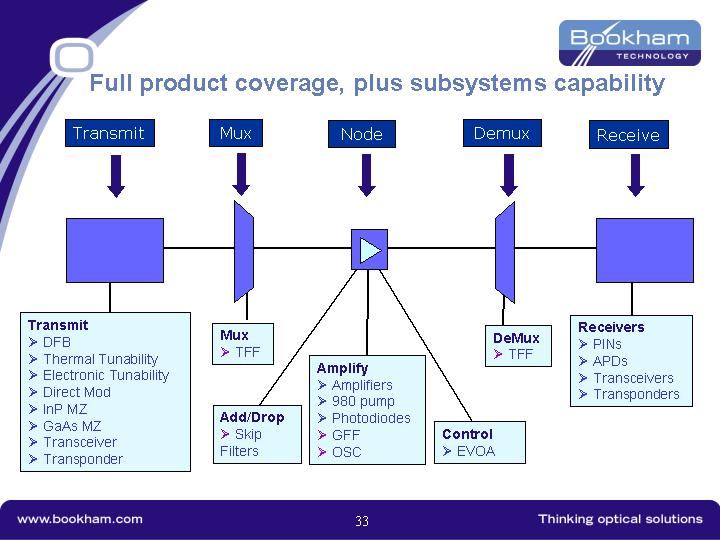

Full product coverage, plus subsystems capability

[CHART]

Transmit

• DFB

• Thermal Tunability

• Electronic Tunability

• Direct Mod

• InP MZ

• GaAs MZ

• Transceiver

• Transponder

Mux

• TFF

Add/Drop

• Skip Filters

Amplify

• Amplifiers

• 980 pump

• Photodiodes

• GFF

• OSC

Control

• EVOA

DeMux

• TFF

Receivers

• PINs

• APDs

• Transceivers

• Transponders

33

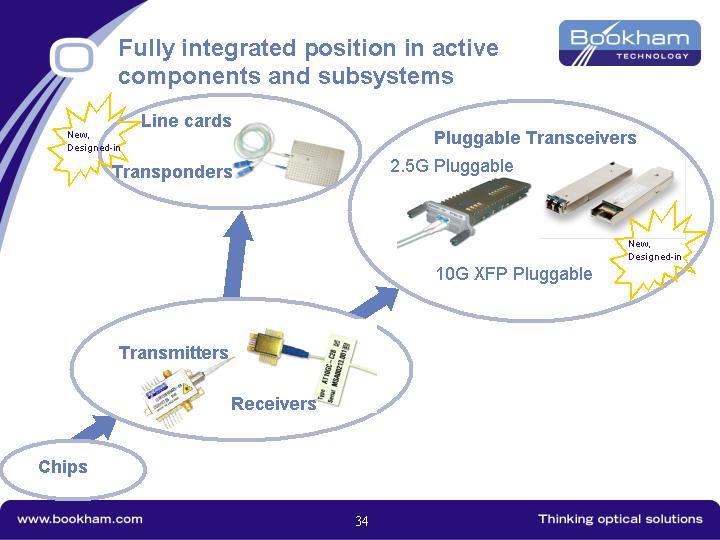

Fully integrated position in active components and subsystems

[GRAPHIC]

34

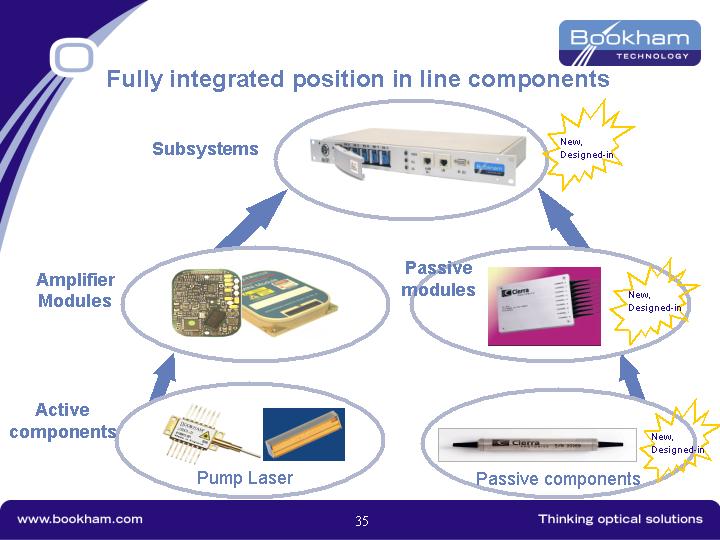

Fully integrated position in line components

[GRAPHIC]

35

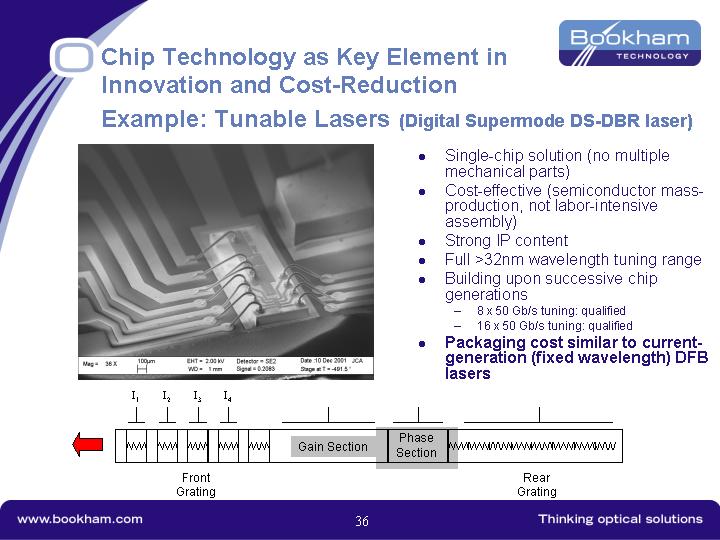

Chip Technology as Key Element in Innovation and Cost-Reduction

Example: Tunable Lasers (Digital Supermode DS-DBR laser)

[GRAPHIC]

• Single-chip solution (no multiple mechanical parts)

• Cost-effective (semiconductor mass-production, not labor-intensive assembly)

• Strong IP content

• Full >32nm wavelength tuning range

• Building upon successive chip generations

• 8 x 50 Gb/s tuning: qualified

• 16 x 50 Gb/s tuning: qualified

• Packaging cost similar to current-generation (fixed wavelength) DFB lasers

[GRAPHIC]

36

IMPORTANT ADDITIONAL INFORMATION FILED WITH THE SECURITIES AND EXCHANGE COMMISSION

Bookham has filed with the SEC a Registration Statement on Form F-4 in connection with the transaction and Bookham and New Focus have filed with the SEC and mailed to the stockholders of New Focus, a Proxy Statement/Prospectus in connection with the transaction. The Registration Statement and the Proxy Statement/Prospectus contain important information about Bookham, New Focus, the transaction and related matters. Investors and security holders are urged to read the Registration Statement and the Proxy Statement/Prospectus carefully.

Investors and security holders are able to obtain free copies of the Registration Statement and the Proxy Statement/Prospectus and other documents filed with the SEC by Bookham and New Focus through the web site maintained by the SEC at http://www.sec.gov.

In addition, investors and security holders are able to obtain free copies of the Registration Statement and the Proxy Statement/Prospectus from Bookham by contacting Investor Relations on +44 (0) 1235 837000 or from New Focus by contacting the Investor Relations Department at +1 408 919 2736.

Bookham and New Focus, and their respective directors and executive officers, may be deemed to be participants in the solicitation of proxies in respect of the transactions contemplated by the merger agreement. Information regarding Bookham’s directors and executive officers is contained in Bookham’s Annual Report on Form 20-F for the year ended December 31, 2002, as amended, which is filed with the SEC. As of September 1, 2003, Bookham’s directors and executive officers beneficially owned approximately 33,806,421 shares (including shares underlying options exercisable within 60 days), or 15.92%, of Bookham’s ordinary shares. Information regarding New Focus’s directors and executive officers is contained in New Focus’s Annual Report on Form 10-K for the year ended December 29, 2002 and its proxy statement dated April 15, 2003, which are filed with the SEC. As of April 15, 2003, New Focus’s directors and executive officers beneficially owned approximately 3,317,696 shares (including shares underlying options exercisable within 60 days), or 5.2%, of New Focus’s common stock. A more complete description is available in the Registration Statement and the Proxy Statement/Prospectus.

Statements in this document regarding the proposed transaction between Bookham and New Focus, the expected timetable for completing the transaction, future financial and operating results, benefits and synergies of the transaction, future opportunities for the combined company and any other statements about Bookham or New Focus managements’ future expectations, beliefs, goals, plans or prospects constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Any statements that are not statements of historical fact (including statements containing the words “believes,” “plans,” “anticipates,” “expects,” “estimates” and similar expressions) should also be considered to be forward-looking statements. There are a number of important factors that could cause actual results or events to differ materially from those indicated by such forward-looking statements, including: the ability to consummate the transaction, the ability of Bookham to successfully integrate New Focus’s operations and employees, the ability to realize anticipated synergies and cost savings; recover

37

of industry demand, the need to manage manufacturing capacity, production equipment and personnel to anticipated levels of demand for products, possible disruption in New Focus’s commercial activities caused by terrorist activities or armed conflicts, the related impact on margins, reductions in demand for optical components, expansion of our business operations, quarterly variations in results, currency exchange rate fluctuations, manufacturing capacity yields and inventory, intellectual property issues and the other factors described in Bookham’s annual report on Form 20-F for the year ended December 31, 2002, as amended, and New Focus’s annual report on Form 10-K for the year ended December 29, 2002 and New Focus’s most recent quarterly report filed with the SEC. Bookham and New Focus disclaim any intention or obligation to update any forward-looking statements as a result of developments occurring after the date of this document.

38