Filed by New Focus, Inc. Pursuant to Rule 425

Under the Securities Act of 1933

And Deemed Filed Pursuant to Rule 14a-6

Under the Securities Exchange Act of 1934

Subject Company: New Focus, Inc.

Commission File No.: 000-29811

This filing relates to a proposed merger (the “Merger”) between Bookham Technology plc (“Bookham”) and New Focus, Inc. (“New Focus”) pursuant to the terms of an Agreement and Plan of Merger, dated as of September 21, 2003, by and among Bookham, Budapest Acquisition Corp. and New Focus. On October 29, 2003, New Focus posted the following slide presentation regarding the Merger on its website.

US Presentation

October 2003

Disclaimer

Information regarding Bookham in this presentation has been provided by Bookham. Any

remarks in this presentation about future expectations, plans and prospects for Bookham

constitute forward-looking statements for purposes of the safe harbor provisions under The

Private Securities Litigation Reform Act of 1995. Actual results may differ materially from

those indicated by these forward-looking statements as a result of various important

factors, including those discussed in the proxy statement / prospectus on Form F-4 filed by

Bookham, Bookham’s Annual Report on Form 20-F for the year ended December 31,

2002, as amended, and New Focus’s Annual Report on Form 10-K, as amended, each of

which is on file with the Securities and Exchange Commission. Forward-looking

statements represent Bookham’s or New Focus’s, as the case may be, estimates as of the

date made, and should not be relied upon as representing Bookham’s or New Focus’s, as

the case may be, estimates as of any subsequent date. While Bookham or New Focus

may elect to update forward-looking statements in the future, each disclaims any obligation

to do so. Certain information contained herein includes non-GAAP financial measures.

For information regarding the Bookham’s results on a US and UK GAAP basis and a

reconciliation of the non-GAAP measures included herein with such results, see the tables

included at the end of this presentation.

Agenda

Recent highlights

Bookham overview

New Focus overview

Financials

Summary

All US dollar numbers have been translated at £1 = $1.61 for the convenience of the reader

Recent highlights

Revenues $37.1 million, up 10% from Q2

Strong quarter-on-quarter improvement in performance

14% improvement in gross margin, near breakeven

11% reduction in operating expenses (excluding exceptionals)

25% reduction in operating loss

Cost reduction initiatives completed

Ottawa fab closed ahead of schedule and products transferred to Caswell

ASOC silicon wafer fab facility in Milton, UK, closed

Reallocation of R&D spending and restructuring to reduce manufacturing

overheads

Additional G&A overhead reductions completed

Two strategic acquisitions announced

New Focus

Ignis Optics…..closed October 7 2003

Stage set for:

Lower cost structure

Expanding revenue opportunities

Bookham overview

Key facts

Founded in 1988

1998: First commercial products (transceivers)

1998: Intel and Cisco invest in Bookham

April 2000: Traded on NASDAQ and London Stock Exchange (LSE)

Feb 2002: Acquired Marconi’s optical component business

Fab and actives; Became a player in tunable lasers and modulators

November 2002: Acquired Nortel Networks Optical Components

Acquired one of largest product lines in the industry

December 2002: Gained number 2 position worldwide in telecom optical

components

July 2003: Acquired Cierra Photonics (thin film filters)

August 2003: Completed consolidation of former Nortel facilities

September 2003: proposed acquisition of New Focus and acquired Ignis

Optics (TxRx)

Current Bookham positioning

No. 2 in telecom optical components

Most comprehensive, end-to-end product portfolio of active

components and amplifiers

Strong, Blue Chip customer base

Strategic relationship (supply and R&D agreements) with

Nortel, the No. 1 optical systems vendor

Emerging, non-telecom optical business leveraging existing

Bookham technologies

Efficient, integrated manufacturing capability

Proven ability to acquire and consolidate (Nortel, Marconi,

Cierra) – additional value enhancing opportunities available

Strong competitive positioning vs. its competitors

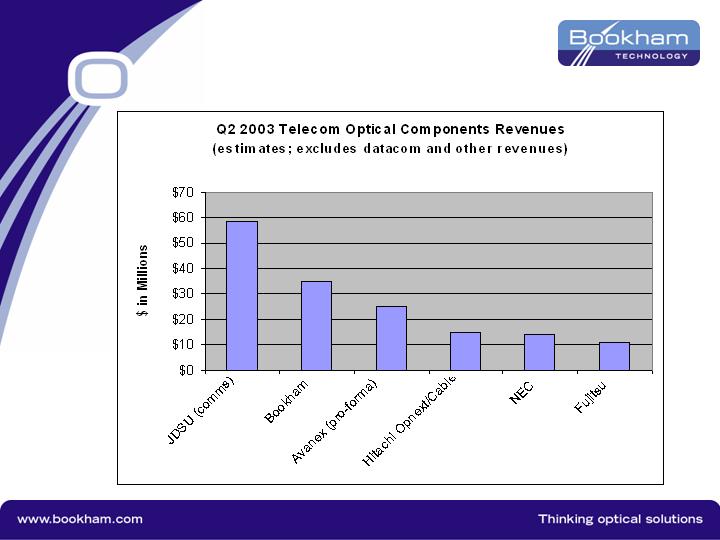

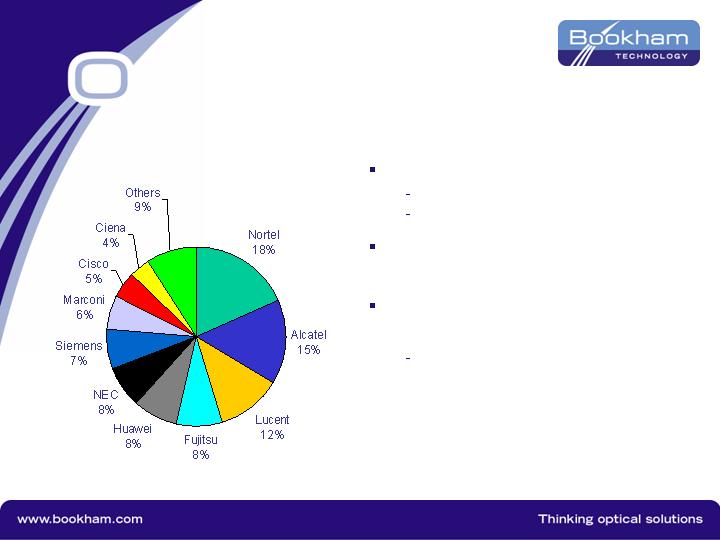

Number 2 in telecom optical components

Optical networking market

shares (sales Q2 2003)

Strong Blue Chip customer base

Source: Dell’Oro Sept 2003 & company estimate

Key customer penetration

Nortel

Marconi

Supply agreements – guaranteed

revenues

Expanding position with other Tier 1

customers (e.g. Huawei)

12% Q-on-Q revenue growth of other

customers

Strategic relationship with Nortel

and Marconi (supply contracts)

No. 1 market share in optical

systems

3 year supply agreement

Minimum commitment

85% to 65% TxRx

65% to 50% amplifiers

Other product areas: preferred

customer status

$20 million per quarter first 6

quarters

Part of acquisition Nov 02

Significant progress with new

design-wins

Leading market share within

European countries

$45 million take or pay supply

contract as part of Feb 02

acquisition

$12 million commitment remaining

at 28 September 03

Strategy: going forward

Leverage position of market leadership to gain share in

telecom

Secure revenue base (supply agreements)

Sell ex-NNOC products to all other customers

Forward-integrate into subsystems (create barriers to entry)

Use technology depth to deliver differentiation in cost, space and power

consumption

Exploit consolidation opportunities to gain added scale

Develop non-telecom business

Continue growth of MMICs

Expand into related opportunities in industrial, military and aerospace

Expand into datacom

New Focus would add non-telco revenues

Implement competitive cost structure

Deliver on restructuring targets

Realize scale benefits (R&D, manufacturing)

Continuing cost-reduction

Non-Telco markets & products

Strategy is to deliver existing technology customised to alternative

markets that value it – spreading fixed manufacturing costs and R&D

know-how

Leverages increased revenue and cash from existing facilities with

minimal incremental investment

Key targets:

MMICs > military and aerospace – a current business (25 year heritage)

High power GaAs lasers > industrial – Q1 2004 start

Datacom where crossover with Telecom

TX/RX > military customers

High profit-margin business

Transaction with New Focus would accelerate development of non

telecom optical business and reduce dependency on major telecom

customers

Non-telecom revenues in 2004 expected to be over 30% of total Bookham revenues

Kanata, Canada

R&D

Milton, UK

HQ

Paignton, UK

Main A&T

facility

240k sq ft

92k sq ft clean

room

Established

1970s

Zurich, Switzerland

980 Pump Laser Chip

Caswell, UK

Main GaAs

and InP fab

180k sq ft

37k sq ft clean

room

Established

1940s

Bookham facilities

Santa Rosa, US

TFF

San Jose, US

XFP/SFP

New Focus overview

Proposed acquisition of New Focus

by Bookham - transaction highlights

All-share acquisition of New Focus by Bookham

Bookham would acquire New Focus for $191 million (£118 million) in stock

84 million shares, including assumed exercise of options (fixed 1.2015 exchange ratio)

Cash distribution of approximately $140 million (£86 million) million to New Focus

stockholders

27.4% pro forma ownership for current stockholders of New Focus

Acquisition would give Bookham:

$25 million per year non-telecom optical components/RF business

New Focus business which is progressing towards breakeven with improving margins

and revenue growth prospects

$105 million (£65 million) of cash on closing balance sheet

Low-cost China manufacturing facility

Transaction expected to accelerate development of non-telecom optical

business and reduce dependency on major telecom customers

Non-telecom revenues in 2004 expected to be approximately 30% of total Bookham

revenues

Estimated closing date late 2003 or early 2004

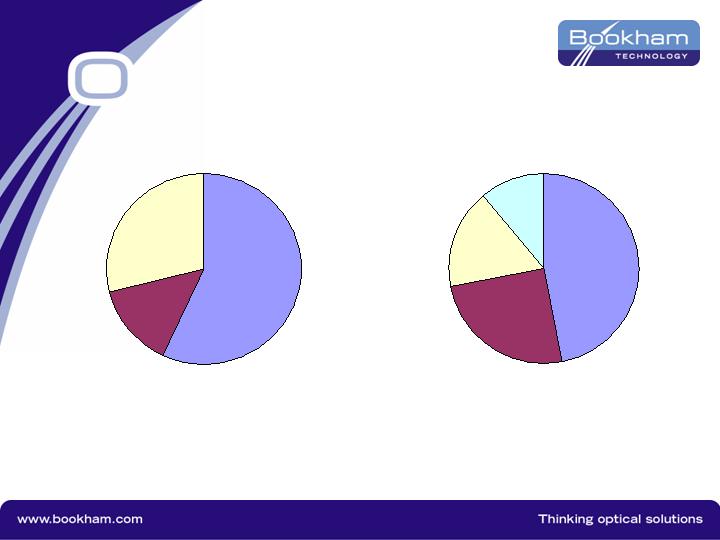

Expands customer base

Nortel

57%

Marconi

14%

Others

including Huawei

29%

Bookham

Bookham Pro forma

Nortel

47%

Marconi

11%

Others

25%

New Focus

Customers

17%

Q3 2003

including Huawei

Diversified Blue Chip customers

Several

Tier-1 defense

contractors

Other major semiconductor

capital equipment OEMs

New Focus facilities

Location: San Jose, CA

Size: 60k sq ft

Location: Shenzhen, China

Size: 247k sq ft

San Jose

Technical/business presence – important

asset for Bookham’s planned expansion

strategy

Two facilities: room for either expansion

or cost-reduction

China

State-of-the-art facility in Shenzhen Free

Trade Zone, close to Huawei and with

prime location overlooking Hong-Kong

(currently empty)

Financials

Management believes that the presentation of the information in the following slides

is useful to investors because such information excludes exceptional items associated

with the company’s past acquisitions and restructuring activity and gives investors

insight into the profitability of the company’s operating business. Management

believes that presenting financial measures exclusive of exceptional items helps

identify trends in the company’s business and the company uses these measures to

establish budgets and operational goals, to manage the business and evaluate the

performance of the company.

Financial highlights – Q3 2003

Revenues $37.1 million, up 10% on Q2 2003

Nortel Networks and Marconi Communications represented 57%

and 14% of revenues respectively, with Huawei as third largest

customer

Charges of $23.6 million, fab closure Ottawa and Milton

Net loss of $22.7 million (excluding charges) compared with $25.5

million in Q2 2003 (11% improvement)

Cash burn of $36.9 million (operating basis improved Q2 – Q3)

Summary P&L account

US GAAP ($ million)

Revenue growth was

across products and

customers

Gross loss improved by

reductions in

manufacturing overhead

Gross margin improved

(14 points on Q2)

Opex down 11%

from Q2

Net loss excluding

charges down 11%

* Excluding charges

Q4 02

Q1 03

Q2 03

Q3 03

Net revenues

$23.0

$33.9

$33.9

$37.1

Gross (loss) profit*

(9.1)

(8.0)

(5.0)

(0.5)

Gross margin %

(40%)

(24%)

(15%)

(1.5%)

OPEX*

(23.4)

(26.2)

(23.7)

(21.2)

Operating Loss*

(32.5)

(34.2)

(28.7)

(21.7)

Other income

(expense)

0.6

(0.5)

3.2

(1.0)

Charges

(49.7)

(4.9)

(3.0)

(23.6)

Net Loss

(excluding charges)

(31.9)

(34.7)

(25.5)

(22.7)

Net Loss

(with charges)

$(81.6)

$(39.6)

$(28.5)

$(46.3)

Balance sheet: solid financial position

US GAAP ($ million)

Debtors (A/R)

improving: 113 Dec;

65 September

Inventory generates

$4.6 million cash in

Q3

Capital spending

$3.8 million in Q3

($7.1 million in Q2)

Note: Year end reclassification on NNOC purchase price to inventory

from intangibles and fixed assets

Jun 03

Sept 03

Cash

$114.1

$77.2

Accounts receivables

23.8

26.6

Inventory

26.8

22.2

Net current assets

$122.2

$80.0

Long term liabilities

(54.4)

(54.9)

Net assets

$180.7

$138.2

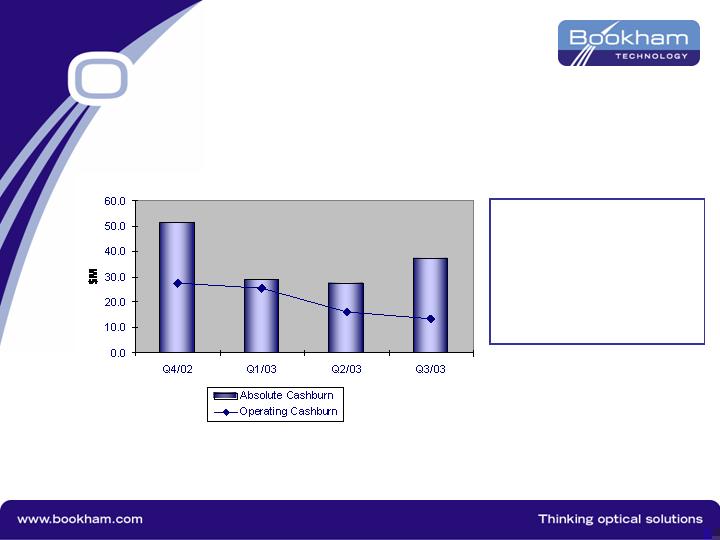

Continue to drive operating efficiencies $ million

Underlying operating cashburn

Operating cashburn defined as EDITDA, excluding exceptional charges + inventory benefit

Operating Cashburn

Q1/03

$25.5

Q2/03

$16.1

Q3/03

$13.3

-

16%

Ohd Red'n (Q1/03 Vs Q2/03)

-

24%

Ohd Red'n (Q1/03 Vs Q3/03)

- Continued Inventory sales

Financial impact

Pro-forma income statement (in $US million)

1.

Excludes charges which generally have included restructuring costs

2.

Represents earnings before interest, taxes, depreciation and amortisation and excluding charges

N.B Translated solely for the convenience of the reader at the rate of $1.61 = £1

Anticipated next steps

Announced restructurings

Bookham

- Ottawa fab closure

- Other Bookham cost

reductions

New Focus

- Q3 staff reductions

Anticipated synergies of

G&A consolidation of New

Focus

Anticipated growth

through market share

gains and expansion of

non-telecom revenues

Q3 2003

Bookham

New Focus

Combined

Revenue

$37.1

$7.7

$44.8

Cost of Sales

(1)

37.6

5.0

42.6

Gross Profit (Loss)

(1)

(0.5)

2.7

2.2

R&D

(1)

11.5

1.9

13.4

SG&A

(1)

9.7

4.1

13.8

Operating Income (Loss)

(1)

($21.7)

($3.3)

($25.0)

Operating Cash Flow

(2)

(17.9)

(2.5)

(20.4)

Financial impact

Summary balance sheet (in $US million)

(1) New Focus cash figure is post distribution of $140m (and potential proceeds from New Focus option

exercises) but excludes deal costs estimated at $12.1 m.

N.B. Translated solely for the convenience of the reader at the rate of $1.61 = £1

Pro-forma 28 September 2003

Bookham

New Focus (1)

Combined

Cash & short term investments

$77.2

$109.7

$186.9

Accounts Receivable

26.6

3.2

29.8

Inventory

22.2

3.3

25.5

Net Current Assets

80.0

106.1

186.1

Long-Term Liabilities

(54.9)

(11.3)

(66.2)

Net Assets

138.2

117.2

255.4

Outlook

Q4 03 revenue projection: $38 million to $41 million

up 3% to 10%

Gross margin improvement 5 to 10 percentage points

Exceptionals projection: $3 million to $5 million

(credits from asset sales coupled with R&D tax credit recognition)

Q4 03 cash burn projection including exceptionals under

$15 million

New Focus acquisition timing expected late 2003 or early

2004. Cash costs and charges not considered in outlook

for Q4

Summary

Strong market position: #2 in telecom, which would be

balanced outside of telecom

Strong and expanding telecom customer base

(NT/MONI/Huawei), which would be significantly de-risked

Strong revenue base (supply agreements)

Strong product line-up

Strong manufacturing base; proposed transaction would add

low-cost manufacturing site

Operational execution

Deep management expertise

Strong financial position

Record of consolidation and successful integration

Additional Information And Where To Find It

On October 22, 2003, Bookham Technology, Inc. filed a Registration Statement on Form F-4 with the

Securities and Exchange Commission in connection with the merger transaction involving Bookham

Technology and New Focus and this Registration Statement on Form F-4 contains a joint proxy

statement/prospectus that Bookham Technology and New Focus, Inc. filed in connection with the

merger transaction. Investors and security holders are urged to read this filing because it contains

important information about the merger. Investors and security holders may obtain free copies of these

documents and other documents filed with the Securities and Exchange Commission at the Securities

and Exchange Commission’s web site at www.sec.gov. In addition, investors and security holders may

obtain free copies of the documents filed with the Securities and Exchange Commission by Bookham

Technology by contacting Bookham Technology Investor Relations at + 44 (0) 1235 837000. Investors

and security holders may obtain free copies of the documents filed with the Securities and Exchange

Commission by New Focus, Inc. by contacting New Focus Investor Relations at (408) 919 5384.

Bookham Technology and its directors and executive officers may be deemed to be participants in the

solicitation of proxies from the stockholders of New Focus in connection with the merger. Information

regarding the special interests of these directors and executive officers in the merger will be included in

the proxy statement/prospectus of Bookham Technology and New Focus described above. Additional

information regarding the directors and executive officers of Bookham Technology is also included in

Bookham Technology’s Annual Report on Form 20-F, which was initially filed with the Securities and

Exchange Commission on March 19, 2003, as amended by the Annual Report on Form 20-F/A filed with

the Securities and Exchange Commission on September 10, 2003 and October 22, 2003. This

document is available free of charge at the Securities and Exchange Commission’s web site at

www.sec.gov and from Bookham Technology by contacting Bookham Technology Investor Relations at

+ 44 (0) 1235 837000.

New Focus and its directors and executive officers also may be deemed to be participants in the

solicitation of proxies from the stockholders of New Focus in connection with the merger. Information

regarding the special interests of these directors and executive officers in the reorganization transaction

described herein is included in the proxy statement/prospectus of Bookham Technology and New Focus

described above. Additional information regarding these directors and executive officers is also included

in New Focus’s proxy statement for its 2003 Annual Meeting of Stockholders, which was filed with the

Securities and Exchange Commission on or about April 11, 2003. This document is available free of

charge at the Securities and Exchange Commission’s web site at www.sec.gov and from New Focus by

contacting New Focus Investor Relations at (408) 919 5384.