UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-09687

ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: November 30, 2010

Date of reporting period: May 31, 2010

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

SEMI-ANNUAL REPORT

AllianceBernstein Core Opportunities Fund

(formerly Focused Growth & Income Fund)

Semi-Annual Report

Investment Products Offered

| | • | | Are Not Bank Guaranteed |

The investment return and principal value of an investment in the Fund will fluctuate as the prices of the individual securities in which it invests fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. You should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For a free copy of the Fund’s prospectus, which contains this and other information, visit our web site at www.alliancebernstein.com or call your financial advisor or AllianceBernstein® at (800) 227-4618. Please read the prospectus carefully before you invest.

You may obtain performance information current to the most recent month-end by visiting www.alliancebernstein.com.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AllianceBernstein’s web site at www.alliancebernstein.com, or go to the Securities and Exchange Commission’s (the “Commission”) web site at www.sec.gov, or call AllianceBernstein at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s web site at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. AllianceBernstein publishes full portfolio holdings for the Fund monthly at www.alliancebernstein.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AllianceBernstein family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the manager of the funds.

AllianceBernstein® and the AB Logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.

July 26, 2010

Semi-Annual Report

This report provides management’s discussion of fund performance for AllianceBernstein Core Opportunities Fund (the “Fund”) for the semi-annual reporting period ended May 31, 2010.

Investment Objective and Policies

The Fund’s investment objective is long-term growth of capital. The Fund invests primarily in the equity securities of US companies that AllianceBernstein L.P. (the “Adviser”) believes are undervalued. The Adviser believes that, over time, a company’s stock price will come to reflect its intrinsic economic value. The Fund may invest in companies of any size and in any industry. The Adviser anticipates that the Fund’s portfolio normally will include approximately 50-60 companies. The Fund may invest in securities of non-US issuers. The Fund may enter into derivatives transactions, such as options, futures, forwards and swap agreements.

Effective March 1, 2010, the Fund changed its name from AllianceBernstein Focused Growth & Income Fund to AllianceBernstein Core Opportunities Fund.

Investment Results

The table on page 4 provides performance data for the Fund as well as its benchmark, the S&P 500 Index, for the six- and 12-month periods ended May 31, 2010. On November 30, 2009, the Fund’s benchmark changed from the Russell 1000 Value Index to the S&P 500 Stock Index. The Fund’s Relative Value Investment Team (the

“Team”) believes that the S&P 500 Stock Index better suits the Fund’s investment process and relative value philosophy. Also included in the table are returns for the Fund’s previous benchmark as well as the peer group, as represented by the Lipper Multi-Cap Core Funds Average (the “Lipper Average”). Funds in the Lipper Average have generally similar investment objectives to the Fund, although some may have different investment policies and sales and management fees.

The Fund’s Class A shares without sales charges underperformed both benchmarks, and the Lipper Average for both the six- and 12-month periods ended May 31, 2010. For the semi-annual period, stock selection detracted from returns primarily in the industrial and energy sectors where the Team avoided firms valued well above its perception of value. Contributing to returns was stock selection in the telecommunication and information technology sectors, as well as an underweight versus the benchmark in the energy sector, and overweights in the industrial and information technology sectors.

For the 12-month period, performance was hurt by stock selection in the consumer discretionary, industrial and health care sectors. The Fund again benefited from holdings in the telecommunications and information technology sectors, as well as underweight positions in the energy and utilities sectors and overweights in the industrial and information technology sectors.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 1 |

Relative performance was particularly impacted by the recent, unprecedented performance of riskier stocks, which left the Fund’s conservative, high-quality strategy in a weakened light. The Fund’s emphasis on firms with attractive free cash flow yields and disciplined capital management led the Fund to outperform the benchmark when risk aversion was rising, but underperform in periods when risk aversion declined.

Market Review and Investment Strategy

Equity markets posted solid returns during the six-month period ended May 31, 2010. Markets fell in the beginning of 2010 on mixed economic news as well as growing concerns about Greece’s sovereign debt crisis and policies in various countries that investors feared could slow the economic recovery. Then a sharp rebound began in early February, amid signs of accelerating global economic growth and improving corporate earnings, large mergers and acquisitions, plus signals that European governments would support Greece.

The Fund’s relative-value investment process balances valuation with quality (fundamental business success) and momentum. This approach tends to work well over time, but not in all environments. However, this was not the case for the 12-month period ended May 31, 2010, when equities

rocketed back from crisis-driven lows on expectations of a recovery, and the most beaten-down stocks did best. The Fund’s philosophy makes the Team deeply reluctant to make investments in companies for which fundamental outcomes are variable and difficult to forecast.

Thus, the Team is sticking with its disciplines. The Team’s conviction in its current strategy is bolstered by research and experience showing that relative-value portfolios tend to outperform by wide margins after periods of strong deep-value leadership. The Fund currently has a modest tilt to cyclical sectors, with a large overweight in technology and more moderate overweights in industrial and consumer sectors, relative to the benchmark.

The Team only purchased companies with very cyclically sensitive earnings if research showed they have the balance-sheet strength to see them through the downturn. The Fund also retains a significant underweight in financials. The Fund’s largest active weights versus the benchmark are a diverse array of mostly high-quality and high-yielding investments. Of course, trading off valuation, quality and momentum can lead to buying lower-quality stocks, if their valuations are sufficiently low and the Team’s research gives it confidence that an investment would be prudent.

| | |

| 2 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

HISTORICAL PERFORMANCE

An Important Note About the Value of Historical Performance

The performance shown on the following pages represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting www.alliancebernstein.com. The investment return and principal value of an investment in the Portfolios will fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost.

Investors should consider the investment objectives, risks, charges and expenses of the Fund / Portfolio carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.alliancebernstein.com or contact your AllianceBernstein Investments representative. Please read the prospectus and/or summary prospectus carefully before investing.

All fees and expenses related to the operation of the Fund have been deducted. NAV returns do not reflect sales charges; if sales charges were reflected, the Fund’s quoted performance would be lower. SEC returns reflect the applicable sales charges for each share class: a 4.25% maximum front-end sales charge for Class A shares; the applicable contingent deferred sales charge for Class B shares (4% year 1, 3% year 2, 2% year 3, 1% year 4); a 1% 1 year contingent deferred sales charge for Class C shares. Returns for the different share classes will vary due to different expenses associated with each class. Performance assumes reinvestment of distributions and does not account for taxes.

Benchmark Disclosure

Neither the unmanaged Russell 1000 Value Index nor the unmanaged S&P 500 Stock Index reflects fees and expenses associated with the active management of a mutual fund portfolio. The Russell 1000 Value Index contains those securities in the Russell 1000 Index with a less-than-average growth orientation. The Russell 1000 Index is composed of 1000 of the largest capitalized companies that are traded in the United States. The S&P 500 Stock Index is comprised of 500 US companies and is a common measure of the performance of the overall US stock market. For the six-and 12-month periods ended May 31, 2010, the Lipper Multi-Cap Core Funds Average consisted of 844 and 821 funds, respectively. Funds in the Lipper Average have generally similar investment objectives to the Fund, although some may have different investment policies and sales and management fees. An investor cannot invest directly in an index or average, and their results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

The Fund can invest in foreign securities, which may magnify fluctuations due to changes in foreign exchange rates and the possibility of substantial volatility due to political and economic uncertainties in foreign countries. The Fund can invest in small-to mid-capitalization companies. These investments may be more volatile than investments in large-capitalization companies. The Fund may at times be concentrated in a particular sector or industry group and, therefore, may be subject to greater risk. While the Fund invests principally in common stocks and other equity securities, in order to achieve its investment objectives, the Fund may at times use certain types of investment derivatives, such as options, futures, forwards and swaps. These instruments involve risks different from, and in certain cases, greater than, the risks presented by more traditional investments. These risks are fully discussed in the Fund’s prospectus.

(Historical Performance continued on next page)

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 3 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| | | | | | | |

| | | | | | | |

THE FUND VS. ITS BENCHMARKS PERIODS ENDED MAY 31, 2010 | | Returns | | |

| | 6 Months | | | 12 Months | | |

AllianceBernstein Core Opportunities Fund* | | | | | | | |

Class A | | 0.31% | | | 14.24% | | |

| |

Class B** | | 0.22% | | | 14.05% | | |

| |

Class C | | 0.00% | | | 13.52% | | |

| |

Advisor Class† | | -7.25% | ‡ | | n/a | | |

| |

Class R† | | 0.21% | | | 14.12% | | |

| |

Class K† | | 0.41% | | | 14.45% | | |

| |

Class I† | | 0.62% | | | 14.92% | | |

| |

Previous Benchmark: Russell 1000 Value Index | | 2.32% | | | 22.98% | | |

| |

New Benchmark: S&P 500 Stock Index | | 0.40% | | | 20.99% | | |

| |

Lipper Multi-Cap Core Funds Average | | 2.08% | | | 21.01% | | |

| |

* Includes the impact of proceeds received and credited to the Fund resulting from class action settlements, which enhanced the Fund’s performance for the six- and 12-month periods ended May 31, 2010, by 0.43% and 0.65%, respectively. ** Effective January 31, 2009, Class B shares are no longer available for purchase to new investors. Please see Note A for additional information. † Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Funds. ‡ Inception Date: 3/31/10 Please keep in mind that high, double-digit returns are highly unusual and cannot be sustained. Investors should also be aware that these returns were primarily achieved during favorable market conditions. |

| | | | | | | |

See Historical Performance and Benchmark disclosures on previous page.

(Historical Performance continued on next page)

| | |

| 4 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| | | | | | |

| AVERAGE ANNUAL RETURNS AS OF MAY 31, 2010 | |

| | | NAV Returns | | | SEC Returns | |

| | | | | | |

| Class A Shares | | | | | | |

1 Year | | 14.24 | % | | 9.35 | % |

5 Years | | -0.95 | % | | -1.80 | % |

10 Years | | 2.42 | % | | 1.98 | % |

| | | | | | |

| Class B Shares | | | | | | |

1 Year | | 14.05 | % | | 10.05 | % |

5 Years | | -1.30 | % | | -1.30 | % |

10 Years(a) | | 1.92 | % | | 1.92 | % |

| | | | | | |

| Class C Shares | | | | | | |

1 Year | | 13.52 | % | | 12.52 | % |

5 Years | | -1.65 | % | | -1.65 | % |

10 Years | | 1.71 | % | | 1.71 | % |

| | | | | | |

| Advisor Class Shares | | | | | | |

Since Inception* | | -7.25 | % | | -7.25 | % |

| | | | | | |

| Class R Shares† | | | | | | |

1 Year | | 14.12 | % | | 14.12 | % |

5 Years | | -1.12 | % | | -1.12 | % |

Since Inception* | | 1.30 | % | | 1.30 | % |

| | | | | | |

| Class K Shares† | | | | | | |

1 Year | | 14.45 | % | | 14.45 | % |

5 Years | | -0.84 | % | | -0.84 | % |

Since Inception* | | -1.18 | % | | -1.18 | % |

| | | | | | |

| Class I Shares† | | | | | | |

1 Year | | 14.92 | % | | 14.92 | % |

5 Years | | -0.49 | % | | -0.49 | % |

Since Inception* | | -0.83 | % | | -0.83 | % |

The Fund’s prospectus fee table shows the Fund’s total annual operating expense ratios as 1.58%, 2.37%, 2.31%, 1.28%, 1.69%, 1.40% and 0.98% for Class A, Class B, Class C, Advisor Class, Class R, Class K and Class I, respectively, gross of any fee waivers or expense reimbursements. Contractual fee waivers and/or expense reimbursements limit the Fund’s annual operating expense ratios to 1.35%, 2.05%, 2.05%, 1.05%, 1.55%, 1.30% and 1.05% for Class A, Class B, Class C, Advisor Class, Class R, Class K and Class I, respectively. These waivers/reimbursements extend through the Fund’s current fiscal year and may be extended by the Adviser for additional one-year terms. Absent reimbursements or waivers, performance would have been lower.

| * | | Inception dates: 11/3/03 for Class R shares; 3/1/05 for Class K and Class I shares; 3/31/10 for Advisor Class shares. |

| (a) | | Assumes conversion of Class B shares into Class A shares after eight years. |

| † | | These share classes are offered at net asset value (NAV) to eligible investors and their SEC returns are the same as the NAV returns. Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Funds. The inception dates for these classes are listed above. |

See Historical Performance disclosures on page 3.

(Historical Performance continued on next page)

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 5 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| | | | | | | |

| SEC AVERAGE ANNUAL RETURNS (WITH ANY APPLICABLE SALES CHARGES) AS OF THE MOST RECENT CALENDAR QUARTER-END (JUNE 30, 2010) | |

| | | | | | | SEC Returns | |

| | | | | | | |

| Class A Shares | | | | | | | |

1 Year | | | | | | 1.90 | % |

5 Years | | | | | | -2.92 | % |

10 Years | | | | | | 1.74 | % |

| | | | | | | |

| Class B Shares | | | | | | | |

1 Year | | | | | | 2.28 | % |

5 Years | | | | | | -2.41 | % |

10 Years(a) | | | | | | 1.68 | % |

| | | | | | | |

| Class C Shares | | | | | | | |

1 Year | | | | | | 4.70 | % |

5 Years | | | | | | -2.77 | % |

10 Years | | | | | | 1.47 | % |

| | | | | | | |

| Advisor Class Shares | | | | | | | |

Since Inception* | | | | | | -10.21 | % |

| | | | | | | |

| Class R Shares† | | | | | | | |

1 Year | | | | | | 6.34 | % |

5 Years | | | | | | -2.23 | % |

Since Inception* | | | | | | 0.38 | % |

| | | | | | | |

| Class K Shares† | | | | | | | |

1 Year | | | | | | 6.63 | % |

5 Years | | | | | | -1.97 | % |

Since Inception* | | | | | | -2.27 | % |

| | | | | | | |

| Class I Shares† | | | | | | | |

1 Year | | | | | | 6.97 | % |

5 Years | | | | | | -1.62 | % |

Since Inception* | | | | | | -1.93 | % |

| * | | Inception dates: 11/3/03 for Class R shares; 3/1/05 for Class K and Class I shares, 3/31/10 for Advisor Class shares. |

| (a) | | Assumes conversion of Class B shares into Class A shares after eight years. |

| † | | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Funds. The inception dates for these classes are listed above. |

See Historical Performance disclosures on page 3.

| | |

| 6 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Historical Performance

FUND EXPENSES

(unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution (12b-l) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

December 1, 2009 | | Ending

Account Value

May 31, 2010 | | Expenses Paid

During Period* |

| | | Actual | | Hypothetical | | Actual | | Hypothetical** | | Actual | | Hypothetical |

| Class A | | $ | 1,000 | | $ | 1,000 | | $ | 1,003.10 | | $ | 1,017.60 | | $ | 7.34 | | $ | 7.39 |

| Class B | | $ | 1,000 | | $ | 1,000 | | $ | 1,002.19 | | $ | 1,016.11 | | $ | 8.84 | | $ | 8.90 |

| Class C | | $ | 1,000 | | $ | 1,000 | | $ | 1,000.00 | | $ | 1,014.01 | | $ | 10.92 | | $ | 11.00 |

| Advisor Class† | | $ | 1,000 | | $ | 1,000 | | $ | 927.48 | | $ | 1,019.70 | | $ | 1.69 | | $ | 5.29 |

| Class R | | $ | 1,000 | | $ | 1,000 | | $ | 1,002.09 | | $ | 1,016.65 | | $ | 8.29 | | $ | 8.35 |

| Class K | | $ | 1,000 | | $ | 1,000 | | $ | 1,004.13 | | $ | 1,018.15 | | $ | 6.80 | | $ | 6.84 |

| Class I | | $ | 1,000 | | $ | 1,000 | | $ | 1,006.18 | | $ | 1,019.95 | | $ | 5.00 | | $ | 5.04 |

| * | | Expenses are equal to the classes’ annualized expense ratios of 1.47%, 1.77%, 2.19%, 1.66%, 1.36% and 1.00%, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

| ** | | Assumes 5% return before expenses. |

| † | | For Advisor Class shares, expenses are equal to the class’s annualized expense ratio of 1.05%. The “Actual” and “Hypothetical” expenses paid are based on the period from March 31, 2010 (commencement of distribution) to May 31, 2010. Actual expenses are equal to the class’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 61/365 (to reflect the since inception period). Hypothetical expenses are equal to the class’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 7 |

Fund Expenses

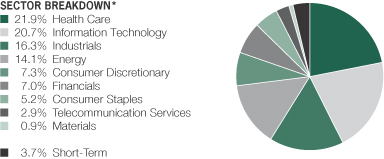

PORTFOLIO SUMMARY

May 31, 2010 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $105.6

TEN LARGEST HOLDINGS**

May 31, 2010 (unaudited)

| | | | | | |

| Company | | U.S. $ Value | | Percent of

Net Assets | |

Gilead Sciences, Inc. | | $ | 5,079,088 | | 4.8 | % |

BP PLC (Sponsored ADR) | | | 4,617,125 | | 4.4 | |

Amgen, Inc. | | | 4,147,578 | | 3.9 | |

Comcast Corp. – Class A | | | 3,068,064 | | 2.9 | |

Google, Inc. – Class A | | | 2,988,709 | | 2.8 | |

Vertex Pharmaceuticals, Inc. | | | 2,974,740 | | 2.8 | |

Qwest Communications International, Inc. | | | 2,969,560 | | 2.8 | |

Exxon Mobil Corp. | | | 2,932,310 | | 2.8 | |

Chevron Corp. | | | 2,917,865 | | 2.8 | |

Dover Corp. | | | 2,917,850 | | 2.8 | |

| | $ | 34,612,889 | | 32.8 | % |

| * | | All data are as of May 31, 2010. The Fund’s sector breakdown is expressed as a percentage of total investments and may vary over time. |

| ** | | Long-term investments. |

Please Note: The sector classifications presented herein are based on the Global Industry Classification Standard (GICS) which was developed by Morgan Stanley Capital International and Standard and Poor’s. The components are divided into sector, industry group, and industry sub-indices as classified by the GICS for each of the market capitalization indices in the Broad Market. These sector classifications are broadly defined. The “Portfolio of Investments” section of the report reflects more specific industry information and is consistent with the investment restrictions discussed in the Fund’s prospectus.

| | |

| 8 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Portfolio Summary and Ten Largest Holdings

PORTFOLIO OF INVESTMENTS

May 31, 2010 (unaudited)

| | | | | |

| Company | | Shares | | U.S. $ Value |

| |

| | | | | |

COMMON STOCKS – 94.4% | | | | | |

Health Care – 21.5% | | | | | |

Biotechnology – 13.4% | | | | | |

Amgen, Inc.(a) | | 80,100 | | $ | 4,147,578 |

Celgene Corp.(a) | | 37,100 | | | 1,957,396 |

Gilead Sciences, Inc.(a) | | 141,400 | | | 5,079,088 |

Vertex Pharmaceuticals, Inc.(a) | | 86,000 | | | 2,974,740 |

| | | | | |

| | | | | 14,158,802 |

| | | | | |

Health Care Providers & Services – 5.4% | | | | | |

AmerisourceBergen Corp. – Class A | | 30,600 | | | 957,168 |

Cardinal Health, Inc. | | 26,400 | | | 910,536 |

Medco Health Solutions, Inc.(a) | | 17,100 | | | 985,815 |

UnitedHealth Group, Inc. | | 98,930 | | | 2,875,895 |

| | | | | |

| | | | | 5,729,414 |

| | | | | |

Life Sciences Tools & Services – 0.9% | | | | | |

Thermo Fisher Scientific, Inc.(a) | | 17,400 | | | 905,844 |

| | | | | |

| | |

Pharmaceuticals – 1.8% | | | | | |

Forest Laboratories, Inc.(a) | | 74,000 | | | 1,915,120 |

| | | | | |

| | | | | 22,709,180 |

| | | | | |

Information Technology – 20.2% | | | | | |

Communications Equipment – 2.4% | | | | | |

Cisco Systems, Inc.(a) | | 74,300 | | | 1,720,788 |

F5 Networks, Inc.(a) | | 12,170 | | | 855,916 |

| | | | | |

| | | | | 2,576,704 |

| | | | | |

Computers & Peripherals – 7.5% | | | | | |

Apple, Inc.(a) | | 10,300 | | | 2,648,748 |

EMC Corp.(a) | | 106,500 | | | 1,983,030 |

Hewlett-Packard Co. | | 39,000 | | | 1,794,390 |

Teradata Corp.(a) | | 47,400 | �� | | 1,513,956 |

| | | | | |

| | | | | 7,940,124 |

| | | | | |

Electronic Equipment, Instruments & Components – 1.9% | | | | | |

Arrow Electronics, Inc.(a) | | 31,000 | | | 845,680 |

Avnet, Inc.(a) | | 38,600 | | | 1,108,592 |

| | | | | |

| | | | | 1,954,272 |

| | | | | |

Internet Software & Services – 2.8% | | | | | |

Google, Inc. – Class A(a) | | 6,160 | | | 2,988,709 |

| | | | | |

| | |

IT Services – 1.7% | | | | | |

Amdocs Ltd.(a) | | 33,000 | | | 940,500 |

SAIC, Inc.(a) | | 49,700 | | | 854,343 |

| | | | | |

| | | | | 1,794,843 |

| | | | | |

Semiconductors & Semiconductor Equipment – 1.6% | | | | | |

Texas Instruments, Inc. | | 69,800 | | | 1,704,516 |

| | | | | |

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 9 |

Portfolio of Investments

| | | | | |

| Company | | Shares | | U.S. $ Value |

| |

| | | | | |

Software – 2.3% | | | | | |

Oracle Corp. | | 45,600 | | $ | 1,029,192 |

Sybase, Inc.(a) | | 21,910 | | | 1,409,470 |

| | | | | |

| | | | | 2,438,662 |

| | | | | |

| | | | | 21,397,830 |

| | | | | |

Industrials – 16.0% | | | | | |

Aerospace & Defense – 3.6% | | | | | |

Honeywell International, Inc. | | 46,800 | | | 2,001,636 |

Raytheon Co. | | 35,300 | | | 1,850,073 |

| | | | | |

| | | | | 3,851,709 |

| | | | | |

Air Freight & Logistics – 2.7% | | | | | |

United Parcel Service, Inc. – Class B | | 45,000 | | | 2,824,200 |

| | | | | |

| | |

Construction & Engineering – 0.9% | | | | | |

URS Corp.(a) | | 20,330 | | | 906,312 |

| | | | | |

| | |

Electrical Equipment – 5.3% | | | | | |

AMETEK, Inc. | | 23,300 | | | 945,980 |

Emerson Electric Co. | | 42,800 | | | 1,987,632 |

Hubbell, Inc. – Class B | | 40,200 | | | 1,714,530 |

Thomas & Betts Corp.(a) | | 24,300 | | | 931,662 |

| | | | | |

| | | | | 5,579,804 |

| | | | | |

Machinery – 3.5% | | | | | |

Dover Corp. | | 65,000 | | | 2,917,850 |

Joy Global, Inc. | | 15,660 | | | 798,660 |

| | | | | |

| | | | | 3,716,510 |

| | | | | |

| | | | | 16,878,535 |

| | | | | |

Energy – 13.9% | | | | | |

Energy Equipment & Services – 4.0% | | | | | |

Helmerich & Payne, Inc. | | 47,600 | | | 1,793,568 |

Nabors Industries Ltd.(a) | | 91,300 | | | 1,737,439 |

Noble Corp.(a) | | 22,400 | | | 651,168 |

| | | | | |

| | | | | 4,182,175 |

| | | | | |

Oil, Gas & Consumable Fuels – 9.9% | | | | | |

BP PLC (Sponsored ADR) | | 107,500 | | | 4,617,125 |

Chevron Corp. | | 39,500 | | | 2,917,865 |

Exxon Mobil Corp. | | 48,500 | | | 2,932,310 |

| | | | | |

| | | | | 10,467,300 |

| | | | | |

| | | | | 14,649,475 |

| | | | | |

Consumer Discretionary – 7.2% | | | | | |

Auto Components – 1.8% | | | | | |

Johnson Controls, Inc. | | 66,700 | | | 1,902,951 |

| | | | | |

| | |

Media – 2.9% | | | | | |

Comcast Corp. – Class A | | 169,600 | | | 3,068,064 |

| | | | | |

| | |

| 10 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Portfolio of Investments

| | | | | |

| Company | | Shares | | U.S. $ Value |

| |

| | | | | |

Multiline Retail – 2.5% | | | | | |

Dollar Tree, Inc.(a) | | 13,400 | | $ | 838,706 |

Kohl’s Corp.(a) | | 34,700 | | | 1,761,025 |

| | | | | |

| | | | | 2,599,731 |

| | | | | |

| | | | | 7,570,746 |

| | | | | |

Financials – 6.8% | | | | | |

Capital Markets – 2.2% | | | | | |

BlackRock, Inc. – Class A | | 8,600 | | | 1,443,768 |

Franklin Resources, Inc. | | 8,500 | | | 833,765 |

| | | | | |

| | | | | 2,277,533 |

| | | | | |

Diversified Financial Services – 1.6% | | | | | |

JPMorgan Chase & Co. | | 43,900 | | | 1,737,562 |

| | | | | |

| | |

Insurance – 3.0% | | | | | |

Axis Capital Holdings Ltd. | | 70,800 | | | 2,152,320 |

Travelers Cos., Inc. (The) | | 21,100 | | | 1,043,817 |

| | | | | |

| | | | | 3,196,137 |

| | | | | |

| | | | | 7,211,232 |

| | | | | |

Consumer Staples – 5.1% | | | | | |

Food Products – 0.8% | | | | | |

Archer-Daniels-Midland Co. | | 32,800 | | | 828,856 |

| | | | | |

| | |

Tobacco – 4.3% | | | | | |

Lorillard, Inc. | | 38,990 | | | 2,787,395 |

Philip Morris International, Inc. | | 39,200 | | | 1,729,504 |

| | | | | |

| | | | | 4,516,899 |

| | | | | |

| | | | | 5,345,755 |

| | | | | |

Telecommunication Services – 2.8% | | | | | |

Diversified Telecommunication Services – 2.8% | | | | | |

Qwest Communications International, Inc. | | 566,710 | | | 2,969,560 |

| | | | | |

| | |

Materials – 0.9% | | | | | |

Chemicals – 0.9% | | | | | |

CF Industries Holdings, Inc. | | 14,000 | | | 960,260 |

| | | | | |

| | |

Total Common Stocks

(cost $97,223,150) | | | | | 99,692,573 |

| | | | | |

| | | | | |

SHORT-TERM INVESTMENTS – 3.6% | | | | | |

Investment Companies – 3.6% | | | | | |

AllianceBernstein Fixed-Income Shares, Inc. – Government STIF Portfolio, 0.18%(b)

(cost $3,847,167) | | 3,847,167 | | | 3,847,167 |

| | | | | |

| | |

Total Investments – 98.0%

(cost $101,070,317) | | | | | 103,539,740 |

Other assets less liabilities – 2.0% | | | | | 2,075,826 |

| | | | | |

| | |

Net Assets – 100.0% | | | | $ | 105,615,566 |

| | | | | |

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 11 |

Portfolio of Investments

| (a) | | Non-income producing security. |

| (b) | | Investment in affiliated money market mutual fund. The rate shown represents the 7-day yield as of period end. |

Glossary:

ADR – American Depository Receipt

See notes to financial statements.

| | |

| 12 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Portfolio of Investments

STATEMENT OF ASSETS & LIABILITIES

May 31, 2010 (unaudited)

| | | | |

| Assets | | | | |

Investments in securities, at value | | | | |

Unaffiliated issuers (cost $97,223,150) | | $ | 99,692,573 | |

Affiliated issuers (cost $3,847,167) | | | 3,847,167 | |

Receivable for investment securities sold | | | 4,274,474 | |

Receivable for capital stock sold | | | 371,090 | |

Dividends receivable | | | 287,860 | |

| | | | |

Total assets | | | 108,473,164 | |

| | | | |

| Liabilities | | | | |

Payable for investment securities purchased | | | 1,944,633 | |

Payable for capital stock redeemed | | | 724,405 | |

Distribution fee payable | | | 37,886 | |

Advisory fee payable | | | 28,354 | |

Transfer Agent fee payable | | | 20,717 | |

Administrative fee payable | | | 19,482 | |

Accrued expenses | | | 82,121 | |

| | | | |

Total liabilities | | | 2,857,598 | |

| | | | |

Net Assets | | $ | 105,615,566 | |

| | | | |

| Composition of Net Assets | | | | |

Capital stock, at par | | $ | 11,117 | |

Additional paid-in capital | | | 143,095,460 | |

Accumulated net investment loss | | | (146,298 | ) |

Accumulated net realized loss on investment transactions | | | (39,814,136 | ) |

Net unrealized appreciation on investments | | | 2,469,423 | |

| | | | |

| | $ | 105,615,566 | |

| | | | |

Net Asset Value Per Share—21 billion shares of capital stock authorized, $.001 par value

| | | | | | | | | |

| Class | | Net Assets | | Shares

Outstanding | | Net Asset

Value | |

| A | | $ | 69,105,890 | | 7,116,800 | | $ | 9.71 | * |

| | |

| B | | $ | 18,342,190 | | 2,001,060 | | $ | 9.17 | |

| | |

| C | | $ | 17,606,922 | | 1,941,779 | | $ | 9.07 | |

| | |

| Advisor | | $ | 9,272 | | 954 | | $ | 9.72 | |

| | |

| R | | $ | 209,158 | | 21,736 | | $ | 9.62 | |

| | |

| K | | $ | 335,695 | | 34,472 | | $ | 9.74 | |

| | |

| I | | $ | 6,439 | | 658.48 | | $ | 9.78 | |

| | |

| * | | The maximum offering price per share for Class A shares was $10.14 which reflects a sales charge of 4.25%. |

See notes to financial statements.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 13 |

Statement of Assets & Liabilities

STATEMENT OF OPERATIONS

Six Months Ended May 31, 2010 (unaudited)

| | | | | | | | |

| Investment Income | | | | | | | | |

Dividends | | | | | | | | |

Unaffiliated issuers | | $ | 811,701 | | | | | |

Affiliated issuers | | | 7,924 | | | $ | 819,625 | |

| | | | | | | | |

| Expenses | | | | | | | | |

Advisory fee (see Note B) | | | 322,012 | | | | | |

Distribution fee—Class A | | | 110,349 | | | | | |

Distribution fee—Class B | | | 114,043 | | | | | |

Distribution fee—Class C | | | 98,713 | | | | | |

Distribution fee—Class R | | | 1,458 | | | | | |

Distribution fee—Class K | | | 481 | | | | | |

Transfer agency—Class A | | | 119,711 | | | | | |

Transfer agency—Class B | | | 45,346 | | | | | |

Transfer agency—Class C | | | 34,409 | | | | | |

Transfer agency—Advisor Class | | | 5 | | | | | |

Transfer agency—Class R | | | 740 | | | | | |

Transfer agency—Class K | | | 368 | | | | | |

Transfer agency—Class I | | | 1 | | | | | |

Custodian | | | 50,559 | | | | | |

Registration fees | | | 49,996 | | | | | |

Administrative | | | 42,820 | | | | | |

Directors’ fees | | | 25,245 | | | | | |

Audit | | | 25,071 | | | | | |

Printing | | | 24,007 | | | | | |

Legal | | | 22,151 | | | | | |

Miscellaneous | | | 6,192 | | | | | |

| | | | | | | | |

Total expenses | | | 1,093,677 | | | | | |

Less: expenses waived by the Distributor (see Note C) | | | (68,426 | ) | | | | |

Less: expenses waived and reimbursed by the Adviser (see Note B) | | | (59,328 | ) | | | | |

| | | | | | | | |

Net expenses | | | | | | | 965,923 | |

| | | | | | | | |

Net investment loss | | | | | | | (146,298 | ) |

| | | | | | | | |

| Realized and Unrealized Gain (Loss) on Investment Transactions | | | | | | | | |

Net realized gain on investment transactions | | | | | | | 7,766,348 | |

Net change in unrealized appreciation/depreciation of investments | | | | | | | (6,775,035 | ) |

| | | | | | | | |

Net gain on investment transactions | | | | | | | 991,313 | |

| | | | | | | | |

Net Increase in Net Assets from Operations | | | | | | $ | 845,015 | |

| | | | | | | | |

See notes to financial statements.

| | |

| 14 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Statement of Operations

STATEMENT OF CHANGES IN NET ASSETS

| | | | | | | | |

| | | Six Months Ended

May 31, 2010

(unaudited) | | | Year Ended

November 30,

2009 | |

| Increase (Decrease) in Net Assets from Operations | | | | | | | | |

Net investment loss | | $ | (146,298 | ) | | $ | (86,944 | ) |

Net realized gain (loss) on investment transactions | | | 7,766,348 | | | | (10,820,800 | ) |

Net change in unrealized appreciation/depreciation of investments | | | (6,775,035 | ) | | | 38,601,094 | |

| | | | | | | | |

Net increase in net assets from operations | | | 845,015 | | | | 27,693,350 | |

| Dividends and Distributions to Shareholders from | | | | | | | | |

Net investment income | | | | | | | | |

Class A | | | – 0 | – | | | (297,156 | ) |

Class B | | | – 0 | – | | | (76,653 | ) |

Class R | | | – 0 | – | | | (3,773 | ) |

Class I | | | – 0 | – | | | (63 | ) |

Tax return of capital | | | | | | | | |

Class A | | | – 0 | – | | | (24,634 | ) |

Class B | | | – 0 | – | | | (6,355 | ) |

Class R | | | – 0 | – | | | (313 | ) |

Class I | | | – 0 | – | | | (5 | ) |

| Capital Stock Transactions | | | | | | | | |

Net decrease | | | (14,102,964 | ) | | | (28,012,275 | ) |

| Capital Contributions | | | | | | | | |

Proceeds from third party regulatory settlement (see Note E) | | | – 0 | – | | | 16,333 | |

| | | | | | | | |

Total decrease | | | (13,257,949 | ) | | | (711,544 | ) |

| Net Assets | | | | | | | | |

Beginning of period | | | 118,873,515 | | | | 119,585,059 | |

| | | | | | | | |

End of period (including accumulated net investment loss of ($146,298) and $0, respectively) | | $ | 105,615,566 | | | $ | 118,873,515 | |

| | | | | | | | |

See notes to financial statements.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 15 |

Statement of Changes in Net Assets

NOTES TO FINANCIAL STATEMENTS

May 31, 2010 (unaudited)

NOTE A

Significant Accounting Policies

AllianceBernstein Core Opportunities, Fund, Inc., (formerly, AllianceBernstein Focused Growth & Income Fund, Inc.) (the “Fund”), organized as a Maryland corporation on July 6, 1999, is registered under the Investment Company Act of 1940 as a diversified, open-end management investment company. The Fund offers Class A, Class B, Class C, Advisor Class, Class R, Class K and Class I shares. Advisor Class commenced distributions on March 31, 2010. Class A shares are sold with a front-end sales charge of up to 4.25% for purchases not exceeding $1,000,000. With respect to purchases of $1,000,000 or more, Class A shares redeemed within one year of purchase may be subject to a contingent deferred sales charge of 1%. Class B shares are currently sold with a contingent deferred sales charge which declines from 4% to zero depending on the period of time the shares are held. Effective January 31, 2009, sales of Class B shares of the Fund to new investors were suspended. Class B shares will only be issued (i) upon the exchange of Class B shares from another AllianceBernstein Fund, (ii) for purposes of dividend reinvestment, (iii) through the Fund’s Automatic Investment Program (the “Program”) for accounts that established the Program prior to January 31, 2009, and (iv) for purchases of additional shares by Class B shareholders as of January 31, 2009. The ability to establish a new Program for accounts containing Class B shares was suspended as of January 31, 2009. Class B shares will automatically convert to Class A shares eight years after the end of the calendar month of purchase. Class C shares are subject to a contingent deferred sales charge of 1% on redemptions made within the first year after purchase. Class R and Class K shares are sold without an initial or contingent deferred sales charge. Advisor Class and Class I shares are sold without an initial or contingent deferred sales charge and are not subject to ongoing distribution expenses. All seven classes of shares have identical voting, dividend, liquidation and other rights, except that the classes bear different distribution and transfer agency expenses. Each class has exclusive voting rights with respect to its distribution plan. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Fund.

1. Security Valuation

Portfolio securities are valued at their current market value determined on the basis of market quotations or, if market quotations are not readily available or are deemed unreliable, at “fair value” as determined in accordance with procedures established by and under the general supervision of the Fund’s Board of Directors.

| | |

| 16 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

In general, the market value of securities which are readily available and deemed reliable are determined as follows. Securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities exchange. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices on such day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed put or call options are valued at the last sale price. If there has been no sale on that day, such securities will be valued at the closing bid prices on that day; open futures contracts and options thereon are valued using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used; securities traded in the over-the-counter market (“OTC”) are valued at the mean of the current bid and asked prices as reported by the National Quotation Bureau or other comparable sources; U.S. government securities and other debt instruments having 60 days or less remaining until maturity are valued at amortized cost if their original maturity was 60 days or less; or by amortizing their fair value as of the 61st day prior to maturity if their original term to maturity exceeded 60 days; fixed-income securities, including mortgage backed and asset backed securities, may be valued on the basis of prices provided by a pricing service or at a price obtained from one or more of the major broker/dealers. In cases where broker/dealer quotes are obtained, AllianceBernstein L.P. (the “Adviser”) may establish procedures whereby changes in market yields or spreads are used to adjust, on a daily basis, a recently obtained quoted price on a security; and OTC and other derivatives are valued on the basis of a quoted bid price or spread from a major broker/dealer in such security. Investments in money market funds are valued at their net asset value each day.

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Fund may use fair value pricing for securities primarily traded in non-U.S. markets because most foreign markets close well before the Fund values its securities at 4:00 p.m., Eastern Time. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities. To account for this, the Fund may frequently value many of its foreign equity securities using fair value prices based on third party vendor modeling tools to the extent available.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 17 |

Notes to Financial Statements

2. Fair Value Measurements

In accordance with U.S. GAAP regarding fair value measurements, fair value is defined as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. The U.S. GAAP disclosure requirements establish a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions that market participants would use in pricing the asset or liability based on the best information available in the circumstances. Each investment is assigned a level based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| | • | | Level 1—quoted prices in active markets for identical investments |

| | • | | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| | • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The following table summarizes the valuation of the Fund’s investments by the above fair value hierarchy levels as of May 31, 2010:

| | | | | | | | | | | | |

Investments in

Securities | | Level 1 | | Level 2 | | Level 3 | | Total |

Common Stocks | | $ | 99,692,573 | | $ | — | | $ | — | | $ | 99,692,573 |

Short-Term Investments | | | 3,847,167 | | | — | | | — | | | 3,847,167 |

| | | | | | | | | | | | |

Total Investments in Securities | | | 103,539,740 | | | — | | | — | | | 103,539,740 |

Other Financial Instruments* | | | — | | | — | | | — | | | — |

| | | | | | | | | | | | |

Total | | $ | 103,539,740 | | $ | — | | $ | — | | $ | 103,539,740 |

| | | | | | | | | | | | |

| * | | Other financial instruments are derivative instruments, such as futures, forwards and swap contracts, which are valued at the unrealized appreciation/depreciation on the instrument. |

3. Currency Translation

Assets and liabilities denominated in foreign currencies and commitments under forward currency exchange contracts are translated into U.S. dollars at the mean of the quoted bid and asked prices of such currencies against the U.S. dollar. Purchases and sales of portfolio securities are translated into U.S. dollars at the rates of exchange prevailing when such securities were acquired or sold. Income and expenses are translated into U.S. dollars at rates of exchange prevailing when accrued.

| | |

| 18 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

Net realized gain or loss on foreign currency transactions represents foreign exchange gains and losses from sales and maturities of foreign fixed income investments, foreign currency exchange contracts, holding of foreign currencies, currency gains or losses realized between the trade and settlement dates on foreign investment transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains and losses from valuing foreign currency denominated assets and liabilities at period end exchange rates are reflected as a component of net unrealized appreciation or depreciation of investments and foreign currency denominated assets and liabilities.

4. Taxes

It is the Fund’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to shareholders. Therefore, no provisions for federal income or excise taxes are required. The Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income and/or capital gains earned or repatriated. Taxes are accrued and applied to net investment income, net realized gains and net unrealized appreciation/depreciation as such income and/or gains are earned.

In accordance with U.S. GAAP requirements regarding accounting for uncertainties in income taxes, management has analyzed the Fund’s tax positions taken on federal and state income tax returns for all open tax years (the current and the prior three tax years) and has concluded that no provision for income tax is required in the Fund’s financial statements.

5. Investment Income and Investment Transactions

Dividend income is recorded on the ex-dividend date or as soon as the Fund is informed of the dividend. Interest income is accrued daily. Investment transactions are accounted for on the date the securities are purchased or sold. Investment gains or losses are determined on the identified cost basis. The Fund amortizes premiums and accretes discounts as adjustments to interest income.

6. Class Allocations

All income earned and expenses incurred by the Fund are borne on a pro-rata basis by each outstanding class of shares, based on the proportionate interest in the Fund represented by the net assets of such class, except for class specific expenses which are allocated to the respective class. Realized and unrealized gains and losses are allocated among the various share classes based on respective net assets.

7. Dividends and Distributions

Dividends and distributions to shareholders, if any, are recorded on the ex-dividend date. Income dividends and capital gains distributions are

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 19 |

Notes to Financial Statements

determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. GAAP. To the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

NOTE B

Advisory Fee and Other Transactions with Affiliates

Under the terms of the investment advisory agreement, the Fund pays the Adviser an advisory fee at an annual rate of .55% of the first $2.5 billion, .45% of the next $2.5 billion and .40% in excess of $5 billion, of the Fund’s average daily net assets. The fee is accrued daily and paid monthly. As of March 1, 2010 the Adviser has agreed to waive its fees and bear certain expenses to the extent necessary to limit total operating expenses on an annual basis to 1.35%, 2.05%, 2.05%, 1.05%, 1.55%, 1.30% and 1.05% of the daily average net assets for the Class A, Class B, Class C, Advisor Class, Class R, Class K and Class I shares, respectively (the “Expense Caps”). This waiver extends through November 30, 2010 and then may be extended by the Adviser for additional one year terms. Prior to January 1, 2009, the Expense Caps were 2.50%, 3.20%, 3.20%, 2.70%, 2.45%, and 2.20% of the daily average net assets for the Class A, Class B, Class C, Class R, Class K and Class I shares, respectively. For the six months ended May 31, 2010, such reimbursement amounted to $59,328.

Pursuant to the investment advisory agreement, the Fund may reimburse the Adviser for certain legal and accounting services provided to the Fund by the Adviser. For the six months ended May 31, 2010, such fee amounted to $42,820.

The Fund compensates AllianceBernstein Investor Services, Inc. (“ABIS”), a wholly-owned subsidiary of the Adviser, under a Transfer Agency Agreement for providing personnel and facilities to perform transfer agency services for the Fund. ABIS may make payments to intermediaries that provide omnibus account services, sub-accounting services and/or networking services. Such compensation retained by ABIS amounted to $92,128 for the six months ended May 31, 2010.

AllianceBernstein Investments, Inc. (the “Distributor”), a wholly-owned subsidiary of the Adviser, serves as the distributor of the Fund’s shares. The Distributor has advised the Fund that it has retained front-end sales charges of $2,569 from the sale of Class A shares and received $2,154, $3,791 and $1,392 in contingent deferred sales charges imposed upon redemptions by shareholders of Class A, Class B and Class C shares, respectively, for the six months ended May 31, 2010.

The Fund may invest in the AllianceBernstein Fixed-Income Shares, Inc.—Government STIF Portfolio, an open-end management investment company

| | |

| 20 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

managed by the Adviser. The Government STIF Portfolio is offered as a cash management option to mutual funds and other institutional accounts of the Adviser, and is not available for direct purchase by members of the public. The Government STIF Portfolio pays no investment management fees but does bear its own expenses. A summary of the Fund’s transactions in shares of the Government STIF Portfolio for the six months ended May 31, 2010 is as follows:

| | | | | | | | | | | | |

Market Value

November 30, 2009

(000) | | Purchases

at Cost

(000) | | Sales

Proceeds

(000) | | Market Value

May 31, 2010

(000) | | Dividend

Income

(000) |

| $ 14,202 | | $ | 49,945 | | $ | 60,300 | | $ | 3,847 | | $ | 8 |

Brokerage commissions paid on investment transactions for the six months ended May 31, 2010 amounted to $85,779, of which $0 and $0, respectively, was paid to Sanford C. Bernstein & Co. LLC and Sanford C. Bernstein Limited, affiliates of the Adviser.

NOTE C

Distribution Services Agreement

The Fund has adopted a Distribution Services Agreement (the “Agreement”) pursuant to Rule 12b-1 under the Investment Company Act of 1940. Under the Agreement, the Fund pays distribution and servicing fees to the Distributor at an annual rate of up to .30% of the Fund’s average daily net assets attributable to Class A shares, 1% of the Fund’s average daily net assets attributable to both Class B and Class C shares, .50% of the Fund’s average daily net assets attributable to Class R shares and .25% of the Fund’s average daily net assets attributable to Class K shares. There are no distribution and servicing fees on the Advisor Class and Class I shares. For the period February 1, 2007 through October 31, 2007, with respect to Class B shares, payments to the distributor were voluntarily limited to .30% of the average daily net assets attributable to Class B shares. As of November 1, 2007, with respect to Class B shares, payments to the distributor are voluntarily being limited to .40% of the average daily net assets attributable to Class B shares. The fees are accrued daily and paid monthly. For the six months ended May 31, 2010, such waiver amounted to $68,426. The Agreement provides that the Distributor will use such payments in their entirety for distribution assistance and promotional activities. Since the commencement of the Fund’s operations, the Distributor has incurred expenses in excess of the distribution costs reimbursed by the Fund in the amounts of $89,536, $1,611,817, $153,861, and $29,533 for Class B, Class C, Class R and Class K shares, respectively. While such costs may be recovered from the Fund in future periods so long as the Agreement is in effect, the rate of the distribution and servicing fees payable under the Agreement may not be increased without a shareholder vote. In accordance with the Agreement, there is no provision for recovery of unreimbursed distribution costs incurred by the Distributor beyond the current fiscal year for Class A shares. The Agreement also provides that the Adviser may use its own resources to finance the distribution of the Fund’s shares.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 21 |

Notes to Financial Statements

NOTE D

Investment Transactions

Purchases and sales of investment securities (excluding short-term investments) for the six months ended May 31, 2010 were as follows:

| | | | | | | | |

| | | Purchases | | | Sales | |

Investment securities (excluding

U.S. government securities) | | $ | 73,301,139 | | | $ | 81,741,913 | |

U.S. government securities | | | – 0 | – | | | – 0 | – |

The cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes. Accordingly, gross unrealized appreciation and unrealized depreciation are as follows:

| | | | |

Gross unrealized appreciation | | $ | 7,915,131 | |

Gross unrealized depreciation | | | (5,445,708 | ) |

| | | | |

Net unrealized appreciation | | $ | 2,469,423 | |

| | | | |

1. Derivative Financial Instruments

The Fund may use derivatives to earn income and enhance returns, to hedge or adjust the risk profile of its portfolio, to replace more traditional direct investments, or to obtain exposure to otherwise inaccessible markets. The Fund may also use derivatives for non-hedging purposes as a means of making direct investment in foreign currencies, as described below under “Currency Transactions”.

The principal type of derivatives utilized by the Fund, as well as the methods in which they may be used are:

The Fund may buy or sell futures contracts for the purpose of hedging its portfolio against adverse effects of anticipated movements in the market. The Fund bears the market risk that arises from changes in the value of these instruments and the imperfect correlation between movements in the price of the futures contracts and movements in the price of the securities hedged or used for cover. The Fund may also purchase or sell futures contracts for foreign currencies or options thereon for non-hedging purposes as a means of making direct investment in foreign currencies, as described below under “Currency Transactions”.

At the time the Fund enters into a futures contract, the Fund deposits and maintains as collateral an initial margin with the broker, as required by the exchange on which the transaction is effected. Pursuant to the contract, the Fund agrees to receive from or pay to the broker an amount of cash equal to the daily fluctuation in the value of the contract. Such receipts or payments are known as variation margin and are recorded by the Fund as unrealized gains or losses. Risks may arise from the potential inability of a

| | |

| 22 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

counterparty to meet the terms of the contract. The credit/counterparty risk for exchange-traded futures contracts is generally less than privately negotiated futures contracts, since the clearinghouse, which is the issuer or counterparty to each exchange-traded future, provides a guarantee of performance. This guarantee is supported by a daily payment system (i.e., margin requirements). When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the time it was closed.

Use of long futures contracts subjects the Fund to risk of loss in excess of the amounts shown on the statement of assets and liabilities, up to the notional value of the futures contracts. Use of short futures contracts subjects the Fund to unlimited risk of loss. Under some circumstances, futures exchanges may establish daily limits on the amount that the price of a futures contract can vary from the previous day’s settlement price, which could effectively prevent liquidation of unfavorable positions.

The Fund did not engage in derivatives transactions for the six months ended May 31, 2010.

2. Currency Transactions

The Fund may invest in non-U.S. Dollar securities on a currency hedged or unhedged basis. The Fund may seek investment opportunities by taking long or short positions in currencies through the use of currency-related derivatives, including forward currency exchange contracts, futures and options on futures, swaps, and options. The Fund may enter into transactions for investment opportunities when it anticipates that a foreign currency will appreciate or depreciate in value but securities denominated in that currency are not held by the Fund and do not present attractive investment opportunities. Such transactions may also be used when the Adviser believes that it may be more efficient than a direct investment in a foreign currency-denominated security. The Fund may also conduct currency exchange contracts on a spot basis (i.e., for cash at the spot rate prevailing in the currency exchange market for buying or selling currencies).

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 23 |

Notes to Financial Statements

NOTE E

Capital Stock

Each class consists of 3,000,000,000 authorized shares. Transactions in capital shares for each class were as follows:

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | Shares | | | | | Amount | | | |

| | | Six Months Ended

May 31, 2010

(unaudited) | | | Year Ended

November 30,

2009 | | | | | Six Months Ended

May 31, 2010

(unaudited) | | | Year Ended

November 30,

2009 | | | |

| | | | | |

| Class A | | | | | | | | | | | | | | | | | | |

Shares sold | | 502,469 | | | 1,382,398 | | | | | $ | 5,134,734 | | | $ | 11,336,750 | | | |

| | | | |

Shares issued in reinvestment of dividends and distributions | | – 0 | – | | 36,827 | | | | | | – 0 | – | | | 284,306 | | | |

| | | | |

Shares converted from Class B | | 414,960 | | | 954,979 | | | | | | 4,181,301 | | | | 8,212,044 | | | |

| | | | |

Shares redeemed | | (1,240,697 | ) | | (3,096,344 | ) | | | | | (12,592,552 | ) | | | (26,735,521 | ) | | |

| | | | |

Net decrease | | (323,268 | ) | | (722,140 | ) | | | | $ | (3,276,517 | ) | | $ | (6,902,421 | ) | | |

| | | | |

| | | | | | | | | | | | | | | | | | |

| Class B | | | | | | | | | | | | | | | | | | |

Shares sold | | 36,525 | | | 128,540 | | | | | $ | 347,474 | | | $ | 984,412 | | | |

| | | | |

Shares issued in reinvestment of dividends and distributions | | – 0 | – | | 10,200 | | | | | | – 0 | – | | | 74,557 | | | |

| | | | |

Shares converted to Class A | | (439,271 | ) | | (1,009,328 | ) | | | | | (4,181,301 | ) | | | (8,212,044 | ) | | |

| | | | |

Shares redeemed | | (357,928 | ) | | (1,049,806 | ) | | | | | (3,418,926 | ) | | | (8,223,864 | ) | | |

| | | | |

Net decrease | | (760,674 | ) | | (1,920,394 | ) | | | | $ | (7,252,753 | ) | | $ | (15,376,939 | ) | | |

| | | | |

| | | | | | | | | | | | | | | | | | |

| Class C | | | | | | | | | | | | | | | | | | |

Shares sold | | 103,072 | | | 307,405 | | | | | $ | 982,137 | | | $ | 2,424,582 | | | |

| | | | |

Shares redeemed | | (390,729 | ) | | (976,250 | ) | | | | | (3,711,335 | ) | | | (7,605,833 | ) | | |

| | | | |

Net decrease | | (287,657 | ) | | (668,845 | ) | | | | $ | (2,729,198 | ) | | $ | (5,181,251 | ) | | |

| | | | |

| | | | | | | | | | | | | | | | | | |

| Advisor Class(a) | | | | | | | | | | | | | | | | | | |

Shares sold | | 954 | | | – 0 | – | | | | $ | 10,000 | | | $ | – 0 | – | | |

| | | | |

Net increase | | 954 | | | – 0 | – | | | | $ | 10,000 | | | $ | – 0 | – | | |

| | | | |

| | | | | | | | | | | | | | | | | | |

| Class R | | | | | | | | | | | | | | | | | | |

Shares sold | | 7,218 | | | 50,523 | | | | | $ | 73,240 | | | $ | 365,118 | | | |

| | | | |

Shares issued in reinvestment of dividends and distributions | | – 0 | – | | 533 | | | | | | – 0 | – | | | 4,086 | | | |

| | | | |

Shares redeemed | | (85,478 | ) | | (100,311 | ) | | | | | (873,869 | ) | | | (866,154 | ) | | |

| | | | |

Net decrease | | (78,260 | ) | | (49,255 | ) | | | | $ | (800,629 | ) | | $ | (496,950 | ) | | |

| | | | |

| | |

| 24 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | Shares | | | | | Amount | | | |

| | | Six Months Ended

May 31, 2010

(unaudited) | | | Year Ended

November 30,

2009 | | | | | Six Months Ended

May 31, 2010

(unaudited) | | | Year Ended

November 30,

2009 | | | |

| | | | | |

| Class K | | | | | | | | | | | | | | | | | | |

Shares sold | | 1,590 | | | 13,838 | | | | | $ | 16,352 | | | $ | 122,666 | | | |

| | | | |

Shares redeemed | | (6,896 | ) | | (19,843 | ) | | | | | (70,219 | ) | | | (177,381 | ) | | |

| | | | |

Net decrease | | (5,306 | ) | | (6,005 | ) | | | | $ | (53,867 | ) | | $ | (54,715 | ) | | |

| | | | |

| | | | | | | | | | | | | | | | | | |

| Class I | | | | | | | | | | | | | | | | | | |

Shares sold | | – 0 | – | | – 0 | –(b) | | | | $ | – 0 | – | | $ | 1 | | | |

| | | | |

Net increase | | – 0 | – | | – 0 | –(b) | | | | $ | – 0 | – | | $ | 1 | | | |

| | | | |

| (a) | | The Advisor Class commenced distributions on April 1, 2010. |

| (b) | | Amount is less than one share. |

For the year ended November 30, 2009, the Fund received $16,333 related to a third-party’s settlement of regulatory proceedings involving allegations of improper trading. This amount is presented in the Fund’s statement of changes in net assets. Neither the Fund nor its affiliates were involved in the proceedings or the calculation of the payment.

NOTE F

Risks Involved in Investing in the Fund

Foreign Securities Risk—Investing in securities of foreign companies or foreign governments involves special risks which include changes in foreign currency exchange rates and the possibility of future political and economic developments which could adversely affect the value of such securities. Moreover, securities of many foreign companies or foreign governments and their markets may be less liquid and their prices more volatile than those of comparable U.S. companies or of the U.S. government.

Currency Risk—This is the risk that changes in foreign currency exchange rates may negatively affect the value of the Fund’s investments or reduce the returns of the Fund. For example, the value of the Fund’s investments in foreign currency-denominated securities or currencies may decrease if the U.S. Dollar is strong (i.e., gaining value relative to other currencies) and other currencies are weak (i.e., losing value relative to the U.S. Dollar). Currency markets are generally not as regulated as securities markets. Independent of the Fund’s investments denominated in foreign currencies, the Fund’s positions in various foreign currencies may cause the Fund to experience investment losses due to the changes in exchange rates and interest rates.

Derivatives Risk—The Fund may invest in derivatives such as forwards, options, futures and swaps. These investments may be illiquid, difficult to price, and leveraged so that small changes may produce disproportionate losses for the Fund, and subject to counterparty risk to a greater degree than more traditional investments.

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 25 |

Notes to Financial Statements

Indemnification Risk—In the ordinary course of business, the Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these indemnification provisions and expects the risk of loss thereunder to be remote. As such, the Fund has not accrued any liability in connection with these indemnification provisions.

NOTE G

Joint Credit Facility

A number of open-end mutual funds managed by the Adviser, including the Fund, participate in a $140 million revolving credit facility (the “Facility”) intended to provide short-term financing, if necessary, subject to certain restrictions in connection with abnormal redemption activity. Commitment fees related to the Facility are paid by the participating funds and are included in miscellaneous expenses in the statement of operations. The Fund did not utilize the Facility during the six months ended May 31, 2010.

NOTE H

Distributions to Shareholders

The tax character of distributions to be paid for the year ending November 30, 2010 will be determined at the end of the current fiscal year. The tax character of distributions paid during the fiscal years ended November 30, 2009 and November 30, 2008 were as follows:

| | | | | | | | |

| | | 2009 | | | 2008 | |

Distributions paid from: | | | | | | | | |

Ordinary income | | $ | 377,645 | | | $ | 18,398,807 | |

Long-term capital gains | | | – 0 | – | | | 37,116,140 | |

| | | | | | | | |

Total taxable distributions | | | 377,645 | | | | 55,514,947 | |

Tax return of capital | | | 31,307 | | | | – 0 | – |

| | | | | | | | |

Total distributions paid | | $ | 408,952 | | | $ | 55,514,947 | |

| | | | | | | | |

As of November 30, 2009, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| | | | |

Accumulated capital and other losses | | $ | (45,949,152 | )(a) |

Unrealized appreciation/(depreciation) | | | 7,613,126 | (b) |

| | | | |

Total accumulated earnings/(deficit) | | $ | (38,336,026 | ) |

| | | | |

| (a) | | On November 30, 2009, the Fund had a net capital loss carryforward for federal income tax purposes of $45,949,152 of which $30,369,280 expires in the year 2016 and $15,579,872 expires in the year 2017. To the extent future capital gains are offset by capital loss carryforwards, such gains will not be distributed. |

| (b) | | The differences between book-basis and tax-basis unrealized appreciation/(depreciation) are attributable primarily to the tax deferral of losses on wash sales. |

| | |

| 26 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

NOTE I

Legal Proceedings

On October 2, 2003, a purported class action complaint entitled Hindo, et al. v. AllianceBernstein Growth & Income Fund, et al. (“Hindo Complaint”) was filed against the Adviser, Alliance Capital Management Holding L.P. (“Alliance Holding”), Alliance Capital Management Corporation, AXA Financial, Inc., the AllianceBernstein Funds, certain officers of the Adviser (“AllianceBernstein defendants”), and certain other unaffiliated defendants, as well as unnamed Doe defendants. The Hindo Complaint was filed in the United States District Court for the Southern District of New York by alleged shareholders of two of the AllianceBernstein Funds. The Hindo Complaint alleges that certain of the AllianceBernstein defendants failed to disclose that they improperly allowed certain hedge funds and other unidentified parties to engage in “late trading” and “market timing” of AllianceBernstein Fund securities, violating Sections 11 and 15 of the Securities Act, Sections 10(b) and 20(a) of the Exchange Act and Sections 206 and 215 of the Advisers Act. Plaintiffs seek an unspecified amount of compensatory damages and rescission of their contracts with the Adviser, including recovery of all fees paid to the Adviser pursuant to such contracts.

Following October 2, 2003, 43 additional lawsuits making factual allegations generally similar to those in the Hindo Complaint were filed in various federal and state courts against the Adviser and certain other defendants. On September 29, 2004, plaintiffs filed consolidated amended complaints with respect to four claim types: mutual fund shareholder claims; mutual fund derivative claims; derivative claims brought on behalf of Alliance Holding; and claims brought under ERISA by participants in the Profit Sharing Plan for Employees of the Adviser. All four complaints include substantially identical factual allegations, which appear to be based in large part on the Order of the SEC dated December 18, 2003 as amended and restated January 15, 2004 (“SEC Order”) and the New York State Attorney General Assurance of Discontinuance dated September 1, 2004 (“NYAG Order”).

On April 21, 2006, the Adviser and attorneys for the plaintiffs in the mutual fund shareholder claims, mutual fund derivative claims, and ERISA claims entered into a confidential memorandum of understanding containing their agreement to settle these claims. The agreement has been documented by a stipulation of settlement, which has been submitted for court approval. The settlement amount ($30 million), which the Adviser previously accrued and disclosed, has been disbursed. The derivative claims brought on behalf of Alliance Holding, in which plaintiffs seek an unspecified amount of damages, remain pending.

It is possible that these matters and/or other developments resulting from these matters could result in increased redemptions of the AllianceBernstein Mutual Funds’ shares or other adverse consequences to the AllianceBernstein Mutual Funds. This may require the AllianceBernstein Mutual Funds to sell investments

| | |

| ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND • | | 27 |

Notes to Financial Statements

held by those funds to provide for sufficient liquidity and could also have an adverse effect on the investment performance of the AllianceBernstein Mutual Funds. However, the Adviser believes that these matters are not likely to have a material adverse effect on its ability to perform advisory services relating to the AllianceBernstein Mutual Funds.

NOTE J

Subsequent Events

Management has evaluated subsequent events for possible recognition or disclosure in the financial statements through the date the financial statements are issued. Management has determined that there are no material events that would require disclosure in the Fund’s financial statements through this date.

| | |

| 28 | | • ALLIANCEBERNSTEIN CORE OPPORTUNITIES FUND |

Notes to Financial Statements

FINANCIAL HIGHLIGHTS

Selected Data For A Share Of Capital Stock Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | |

| | | Class A | |

| | | Six Months

Ended

May 31,

2010 (unaudited) | | | Year Ended November 30, | |

| | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| | | |

| | | | | | | | | | | | | | | | | | |