UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

FORM 10-K

______________

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to__________

Commission file number 001-32518

——————

CYTOMEDIX, INC.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 23-3011702 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) |

416 Hungerford Drive, Suite 330

Rockville, MD 20850

(Address of Principal Executive Offices) (Zip Code)

(240) 499-2680

(Registrant’s Telephone Number, Including Area Code)

——————

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, par value $.0001

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ¨ | Accelerated Filer x | Non-Accelerated Filer ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock (Common stock) held by non-affiliates of the registrant as of the close of business on June 30, 2006 was approximately $84 million based on the closing sale price of the Common stock on the American Stock Exchange on that date. The registrant does not have any non-voting common equity.

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS

DURING THE PRECEDING FIVE YEARS

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ý No ¨

APPLICABLE ONLY TO CORPORATE REGISTRANTS

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. 28,998,248 shares of Common stock, par value $.0001, outstanding as of February 15, 2007.

DOCUMENTS INCORPORATED BY REFERENCE

None.

CYTOMEDIX, INC.

TABLE OF CONTENTS

Page | |||

PART I | |||

| Item 1. | Business | 1 | |

| Item 1A. | Risk Factors | 10 | |

| Item 1B. | Unresolved Staff Comments | 14 | |

| Item 2 | Properties | 14 | |

| Item 3. | Legal Proceedings | 14 | |

| Item 4. | Submission of Matters to a Vote of Security Holders | 14 | |

PART II | |||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 16 | |

| Item 6. | Selected Financial Data | 17 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 17 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 23 | |

| Item 8. | Financial Statements and Supplementary Data | 24 | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 52 | |

| Item 9A. | Controls and Procedures | 52 | |

| Item 9B. | Other Information | 54 | |

PART III | |||

| Item 10. | Directors, Executive Officers and Corporate Governance | 55 | |

| Item 11. | Executive Compensation | 57 | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 62 | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 63 | |

| Item 14. | Principal Accounting Fees and Services | 64 | |

PART IV | |||

| Item 15. | Exhibits and Financial Statement Schedules | 64 | |

Signatures | 65 | ||

Exhibit Index | 66 | ||

PART I

ITEM 1. BUSINESS

The terms "Cytomedix," and "Company," as used in this annual report, refer to Cytomedix, Inc.

You are cautioned that this Form 10-K contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. When the words "believes," "plans," "anticipates", "will likely result," "will continue," "projects," "expects," and similar expressions are used in this Form 10-K, they are intended to identify "forward-looking statements," and such statements are subject to certain risks and uncertainties which could cause actual results to differ materially from those projected. Furthermore, the Company’s plans, strategies, objectives, expectations and intentions are subject to change at any time at the discretion of management and the Board of Directors.

These forward-looking statements speak only as of the date this report is filed. The Company does not intend to update the forward-looking statements contained in this report, so as to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as may occur as part of its ongoing periodic reports filed with the SEC.

GENERAL DEVELOPMENT OF THE BUSINESS

Informatix Holdings, Inc. was incorporated in Delaware in 1998. In 1999, an unrelated Arkansas corporation, Autologous Wound Therapy, Inc. ("AWT"), merged with and into Informatix Holdings, Inc. and the name of the surviving corporation was changed to Autologous Wound Therapy, Inc. In 2000, AWT changed its name to Cytomedix, Inc. The principal offices are located in Rockville, Maryland.

In 2001, the Company filed bankruptcy under Chapter 11 of the United States Bankruptcy Code, after which Cytomedix was authorized to continue to conduct its business as debtor and debtor-in-possession. A new board of directors was elected which then appointed a new management team. New management immediately began formulating a plan of reorganization that would enable the Company to reorganize and emerge quickly from Chapter 11 in order to preserve its value as a going concern. The Company emerged from bankruptcy in 2002 under a Plan of Reorganization. At that time, all of the Company’s securities or other claims against or equity interest in the Company were canceled and of no further force or effect. Holders of certain claims or securities were entitled to receive new securities from Cytomedix in exchange for their claims or equity interests prior to bankruptcy. All known and allowed claims and equity interests have been satisfied and resolved as of the filing of this form 10-K.

FINANCIAL INFORMATION ABOUT SEGMENTS AND GEOGRAPHIC REGIONS

Cytomedix has only one operating segment and operates only in the United States. See Item 8, Financial Statements and Supplementary Data.

DESCRIPTION OF THE BUSINESS

Overview

Cytomedix is a biotechnology company that develops and licenses autologous cellular therapies (i.e., therapies using the patient’s own body products), including Cytomedix’s proprietary AutoloGel™ Process to produce a platelet rich plasma gel (“AutoloGel™”) for the treatment of wounds. To create AutoloGel™, the patient’s own platelets and plasma are separated through centrifugation and combined with several reagents. This process releases multiple growth factors from the platelets, creates a fibrin matrix scaffold, and forms a gel that is topically applied to a wound (under the direction of a physician). Upon topical application, the Company believes that AutoloGel™ initiates a reaction that closely mimics the body’s natural healing process.

Company-sponsored studies indicate increased healing for AutoloGelTM as compared to enhanced traditional treatments as well as competing treatments for the treatment of diabetic foot ulcers, the Company’s initial focus within its target market.

Multiple growth factor therapies have not been widely used in the traditional commercial setting because such therapies have generally not been available or widely known by clinicians. Until a few years ago, the autologous process of securing multiple growth factors from a patient’s blood products was, substantially, an exclusive treatment available through outpatient wound care centers affiliated with Curative Health Services (“Curative”). In January 2001, the Company purchased certain technology, assets and intellectual property rights associated with autologous multiple growth factor therapies from Curative and has since refined the product to a more marketable state.

1

Market

Cytomedix’s primary target market is the multi-billion dollar, chronic, non-healing wound market. Such wounds typically arise from one of three etiologies: diabetic foot ulcers, venous leg ulcers, and pressure ulcers. The following table lists the prevalence of these wound types:

Incidence of Chronic Wounds in the U.S.

(number of wounds in millions)

Source: Advanced Wound Management: Healing and Restoring Lives;

Advanced Medical Technology Association (AdvaMed), June 2006

U.S. | |||

| Diabetic Foot Ulcers | 1.5 | ||

| Venous Leg Ulcers | 2.5 | ||

| Pressure Ulcers | 2.0 | ||

| Totals | 6.0 |

The prevalence of chronic wounds in the U.S. is linked directly to increased aging demographics, vascular diseases, venous insufficiency, and excessive pressure and diabetic neuropathy. The prevalence of worldwide chronic wounds is estimated to be 18 million (6).

Diabetic Foot Ulcers

According to the American Diabetes Association (“ADA”)(1), there are approximately 20.8 million people with diabetes in the U.S., or 7% of the total population. It is estimated that 15-20% of these people with diabetes will develop a foot ulcer in their lifetime and that 14-24% of diabetic foot ulcers result in amputation.(2) Over 82,000 amputations per year have been documented.(3) Estimated amputation costs are between $20,000 and $60,000 per procedure (4), implying an aggregate cost of between $1.6 billion and $4.9 billion per year. The chances of a second amputation within 3-5 years may be as high as 50%, with a 5 year post-amputation mortality rate of 39-68%.(5)

Venous Stasis Leg Ulcers

Venous leg ulcers are the most frequently occurring type of chronic wound. The prevalence rises dramatically with age, increasing to 1% of the population over age 60. It is estimated that treatment costs total between $2.5 to $3.5 billion annually and a loss of 2 million workdays per year. (4)

Pressure Ulcers

Over 2.0 million pressure ulcers occur each year with an annual cost greater than $1.3 billion. One study indicates that nearly 15% of hospitalized patients age 65 or older developed a pressure ulcer during a 5-day or longer stay. Furthermore, up to one-fifth of all home health service visits involve care of a pressure ulcer, and more than one-third of people with spinal cord injuries develop pressure ulcers. (4)

References

(1) www.diabetes.org, 2006

(2) H.R 3203 Submitted to the House of Representatives, Sept 30, 2003

(3) National Diabetes Statistics, National Diabetes Information Clearinghouse, National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), NIH, 2004

(4) Advanced Wound Management: Healing and Restoring Lives; Advanced Medical Technology Association (AdvaMed); June 2006

(5) Reiber GE, Boyko EJ, Smith DG: Lower Extremity Foot Ulcers and Amputations in Diabetes. In Diabetes in America. 2nd ed., National Institutes of Health, NIDDK, NIH Pub No. 95-1468, 1995.

(6) Growth Factors: Indications, Products, and Markets; Kalorama Publications; October 2003

2

Strategy

The Company has developed a three-pronged strategy to leverage its intellectual property and capitalize on the market for its AutoloGel™:

| · | Obtain broad reimbursement from third-party payers |

| · | Enforce rights under the Company’s patents |

| · | Target the non-reimbursement sensitive market |

In order to increase the prospects for securing broad reimbursement as well as enhance the sales and marketing efforts, the Company completed a well-controlled, prospective clinical trial and submitted a 510(k) Premarket Notification to the FDA.

Clinical Trial and FDA Clearance

In 2005, the Company completed its prospective, randomized, blinded, controlled, multi-center clinical trial designed to prove the efficacy and safety of its AutoloGel™ System (see discussion in this section under “Government Approval”) for the treatment of non-healing diabetic foot ulcers. The audited results yielded 40 patients who met the trial protocol. Analysis of the size of wounds in the study shows that 35 out of the 40 patients (88%) had wounds that were less than or equal to 7 square centimeters in area and 2 cubic centimeters in volume. For these most common wound sizes in the study, the healing rate of the AutoloGel™ group was 81.3% and that for the control group was 42.1%. The difference of 39.2% between these groups is clearly statistically significant, with a p-value of 0.036. Within the full cohort of the 40 patients, 68.4% of the patients treated with AutoloGel™ achieved full wound closure versus 42.9% of those patients treated in the control group. The difference of 25.5% between the healing rate of the AutoloGel™ group versus the control group is approaching statistical significance with a p-value of 0.125. The Company believes that the healing rates of AutoloGel™ at 81.3% for the most common wound sizes in the study and 68.4% for all wound sizes appear to be better than any other wound care products cleared by the FDA and covered by Medicare reimbursement with which the Company is familiar, although this comparison is not as reliable as a head-to-head study. The control group patients were not on placebo; rather, they were treated using a saline gel cleared by the FDA for wound treatment. If the control group patients healed at the originally anticipated rate of 20-30% for standard treatments for diabetic foot ulcers, the difference between the healing rates in the AutoloGel™ group versus the control group would have been even more strongly statistically significant.

These data reflect the results following an independent audit of the data by a former FDA official responsible for Bio-Research Monitoring. During the audit, Cytomedix discovered that some patients originally included in the trial had not met the inclusion criteria or were not provided treatment according to the study protocol. This audit was conducted at the request of Cytomedix when preliminary data were inconsistent with independent and Company retrospective studies.

Based on the audited results of the trial, and other data compiled by the Company, in late January 2006 Cytomedix submitted a Premarket Notification (“510(k)”) to the FDA seeking clearance of its AutoloGel™ System for diabetic foot ulcers and other indications. While AutoloGel™ is regulated by FDA under the Medical Device Amendments of the Food, Drug and Cosmetic Act, the FDA Center for Biologics Evaluation and Research (“CBER”) has the jurisdiction for reviewing such products. FDA assigned CBER as the primary center that reviewed and approved the Investigational Device Exemption (“IDE”) under which this clinical trial was conducted. On October 13, 2006, the FDA denied Cytomedix’s claim that AutoloGel™ is substantially equivalent to predicate devices, as asserted in the 510(k), and delivered to Cytomedix a Non-Substantial Equivalence (“NSE”) determination letter.

Based on the information contained in the NSE determination letter and conversations with the FDA, the Company believes that the primary grounds for rejecting the claim of substantial equivalence concern the use of bovine thrombin which is used to activate the platelet rich plasma (“PRP”) in the AutoloGel™ System. Bovine thrombin is a clotting agent derived from cows that has been used extensively on humans in surgery and other medical applications to stop bleeding. It is also used along with platelet gel therapy products that have been cleared by FDA for use in surgery. However, CBER cites published articles that contend that bovine thrombin creates antibodies that may decrease a patient’s Factor V count (a clotting agent naturally found within blood) which could cause a bleeding tendency. The analysis and clinical interpretation of the data in Cytomedix’s submission to the FDA had concluded that the data from the clinical trial does not demonstrate this complication. No statistically or clinically significant differences were noted between the PRP gel and control from baseline to endpoint laboratory shifts in hematology, clotting factors, and Factor V tests. Additionally, no clinically important changes in clotting factors that would cause concern about the effect of the PRP gel or control on Factor V activity were found during an independent medical expert review of the medical records, including clinical lab test data and concomitant medications.

3

FDA also raised concerns relating to the clinical trial and the number of protocol violations which resulted in a lack of statistical significance in the results of the “intent-to-treat” patient cohort and the subset analysis that showed full statistical significance in the results for 88% of the wounds which represented the per protocol majority wound group within the trial. The Company believed that, during face-to-face meetings with the FDA and in subsequent formal responses to FDA questions, it had addressed these concerns to the FDA’s satisfaction, although they were still listed in the NSE letter from the FDA.

The Company disagrees with the decision as expressed in the NSE determination letter and, in response to an offer made by the FDA, appealed the decision via an informal review with officials in the Office of the Center Director for CBER. The written appeal was submitted to the FDA in late December 2006 and then a face-to-face meeting was held in late January 2007 between Cytomedix, its outside experts, and various FDA personnel involved in the review process. Cytomedix presented additional expert analysis of the safety data gathered during the clinical trial, in particular that data relating to the use of bovine thrombin. In addition, Cytomedix clarified the grounds on which it is seeking marketing clearance for AutoloGel and argued the appropriateness of a reversal of the FDA’s original decision. A decision from the FDA regarding the Company’s appeal is pending.

The Company currently sells commercially AutoloGel™ process components, the AutoloGel™ Component Kit and Process Centrifuge for use in wound care and autologous wound therapy performed under the physicians’ practice of medicine doctrine. This approach represents the practice currently prevalent in the platelet gel therapy industry, both in the treatment of chronic wounds as well as the use of platelet gel therapies in the operating room in fields such as orthopedic and cardiovascular surgery. However, without FDA clearance, the Company’s ability to make claims for the AutoloGel™ System regarding its use to treat or heal wounds is limited. The Company believes this is a significant barrier to broad clinical and market acceptance of the Company’s product. It is also possible that at some point the FDA may require companies to conduct clinical trials on all specific clinical therapies and uses for which their products can be used, whether or not they make a specific labeled claim to that effect. Further, it is also possible that FDA could require companies to stop marketing platelet gel therapies until FDA clearance or approval for specific wound healing claims is obtained.

Third-Party Reimbursement

The Company believes the full market potential of AutoloGel™ cannot be achieved without broad third-party reimbursement from Medicare and commercial insurers. The Company has initiated efforts to obtain Medicare reimbursement through the Center for Medicare and Medicaid Services (“CMS”). This process involves three tracks which can be pursued simultaneously:

| § | Coverage - Coverage requires a determination by CMS that AutoloGel™ is “reasonable and necessary.” A National Non-Coverage Decision, issued in 1992 and amended in 2003, broadly disallows Medicare coverage for Autologous Blood-Derived Products for Chronic Non-Healing Wounds. This decision currently applies to AutoloGel™. The primary basis cited for this non-coverage decision was a lack of specific evidence. The Company is planning to meet with CMS to discuss a reconsideration of that decision based on data from the controlled clinical trial and other recent evidence. |

| § | Coding - Coding involves identifying an existing code or codes which aptly describe the AutoloGel™ System, or applying for new coding or modification of the definitions of existing coding to properly describe the Company’s offering. The Company is evaluating the Healthcare Common Procedure Coding System (“HCPCS”) codes, obtained through CMS and Current Procedural Terminology (“CPT”) codes, obtained through the American Medical Association, to determine the optimal reimbursement pathway for AutoloGel™. |

| § | Payment - Payment involves the establishment of a fee schedule associated with the Company’s product vis a vis the applicable codes. |

The Company has had the results of its clinical trial published in a peer-reviewed journal. The article, entitled “A Prospective, Randomized, Controlled Trial of Autologous Platelet-Rich Plasma Gel for the Treatment of Diabetic Foot Ulcers,” was published, as the feature article in the June 2006 issue of Ostomy/Wound Management (“OWM”). OWM is the premiere journal for information on wound care and the related, overlapping fields of skin care, ostomy care, incontinence care, and nutrition, and is the only peer-reviewed, multidisciplinary publication specifically targeted to the advanced wound care practitioner. The Company believes that publication in peer-reviewed journals is generally regarded as a necessary precursor to a favorable reimbursement decision from CMS and also is an important step toward building broad clinical awareness and acceptance of AutoloGel™. The Company plans to present the results of its clinical trial and other recent evidence as support for its reimbursement pursuits with CMS. Additionally, Cytomedix requisitioned a pharmaco-economic study to evaluate the cost effectiveness of the AutoloGel™ System. Such studies are performed to present scientific, demographic and economic information to justify to CMS and other payor organizations that a particular product and therapy is clinically safe and effective and cost effective with respect to its alternatives. Preliminary results of the pharmaco-economic study suggest a favorable comparison of AutoloGel™ over competing treatments in both clinical and cost effectiveness. The final report should be available sometime in the first quarter of 2007 and would also be provided to CMS.

4

While not an official precondition for a reimbursement code, the Company believes that securing Food and Drug Administration (“FDA”) clearance of the AutoloGel™ System for specific clinical indications, such as for the treatment of non-healing diabetic foot ulcers, will be heavily weighed by CMS when making its decision. Should the Company’s appeal to the FDA ultimately prove unsuccessful, the Company would need to analyze the ultimate nature of the FDA’s determination and the potential impact on the efforts to secure CMS reimbursement for the AutoloGel™ System and components.

While commercial insurers are not required to follow CMS reimbursement decisions, the Company believes they generally weigh heavily the position taken by CMS. Therefore, the results of the Company’s efforts with CMS could likely influence the degree of success the Company achieves in securing reimbursement from other third-party payers such as commercial insurers.

Should the Company be successful in its efforts to obtain reimbursement, third-party payors, including CMS, would permit payment for the AutoloGel™ System for use in certain types of chronic wounds. If this is accomplished, AutoloGel™ could then be positioned as a reimbursed alternative treatment for the estimated 6.0 million chronic wounds that occur each year in the United States.

In general, to raise the scientific awareness of the use of AutoloGel™, posters and oral presentations of the clinical trial results have been presented at multiple scientific/medical meetings including: American Diabetes Association, American Podiatric Medical Association, and the Clinical Symposium on Advances in Skin and Wound Care.

Patents and Licensing

The Company has initiated a broad based patent and licensing strategy intended to (i) enforce the rights under the Company’s patents in order to ensure that Cytomedix shareholders derive economic benefit from the Company’s intellectual property, and (ii) assist the Company in establishing a dominant market position for the AutoloGel™ System within the market for autologous growth factor products used for the treatment of chronic wounds. In 2005 and 2006, the Company identified and successfully pursued numerous companies, both small and large, that market products similar to AutoloGel™, that the Company believed were infringing or inducing infringement of its intellectual property rights. Settlements have been achieved and licenses have been granted to these companies resulting in a royalty stream for Cytomedix.

The primary license agreements are listed below:

Licensee | Date of Agreement | Date of Expiration (4) | Initial Licensing Fee | On-going Royalty Percentage (2) | |||||||||

| DePuy Spine, Inc. (1) | 3/19/2001 | 11/24/2009 | $ | 750,000 | 6.5% | ||||||||

| 3/4/2005 | |||||||||||||

| Medtronic, Inc. | 5/1/2005 | 11/24/2009 | $ | 680,000 | 7.5% on disposables | ||||||||

| 1.5% on hardware | |||||||||||||

| Harvest Technologies, Inc. | 6/30/2005 | 11/24/2009 | $ | 500,000 | 7.5% on disposables | ||||||||

| 1.5% on hardware | |||||||||||||

| Perfusion Partners, Inc. | 6/26/2005 | 11/24/2009 | $ | 250,000 | (3) | 10.0% | |||||||

| COBE Cardiovascular, Inc. | 10/7/2005 | 11/24/2009 | $ | 45,000 | 7.5% on disposables | ||||||||

| 1.5% on hardware | |||||||||||||

| SafeBlood Technologies, Inc. | 10/12/2005 | 11/24/2009 | $ | 50,000 | (3) | 8.0% to 9.0% | |||||||

| Biomet Biologics, Inc. (5) | 5/19/2006 | 11/24/2009 | $ | 2,600,000 | none | ||||||||

| CellMedix, Inc. | 11/28/2006 | 11/24/2009 | $ | 30,000 | 9.5% | ||||||||

(1) Cytomedix has two license agreements with DePuy Spine, Inc.. The original license agreement was dated March 19, 2001, amended March 3, 2005, and provides for the use of applications under Cytomedix patents in the fields of diagnostic and therapeutic spinal, neurosurgery and orthopedic surgery. The second license agreement is dated March 4, 2005, and applies to all fields not covered in the original license agreement as amended.

(2) Certain minimum royalties may apply to certain agreements and other royalty percentages may apply to future products covered under selected license agreements.

(3) Some of these amounts are payable over a period of time as defined in executed notes payable to Cytomedix.

(4) These dates reflect the expiration of the license in the U.S., which coincides with the expiration of the Knighton Patent in the U.S. In some cases, the licensing agreements applicable to territories outside the U.S. extend to the expiration of the patents in the respective foreign countries.

5

(5) The Settlement and License Agreement with Biomet Biologics, Inc. (“Biomet”) called for a $2.6 million payout from Biomet to Cytomedix. This payout took the form of $1.4 million payable upon execution of the agreement and $100,000 payable at the end of each of 12 consecutive quarters beginning with the quarter ending September 2006. These payments are not tied to any performance commitments by Cytomedix and are not dependent on Biomet sales.

The Company’s ongoing patent enforcement strategy is being conducted on a full contingency basis by the law firms Fitch, Even, Tabin & Flannery and Robert F. Coleman and Associates, both based in Chicago, Illinois.

The Company expects to incur “Cost of royalties” (consisting of royalty expense and contingent legal fees) in the range of 30-50% of on-going royalty revenues relating to these and future settlements.

The Company intends to press forward aggressively in other instances of infringement with aggressive legal and business actions to defend its intellectual property and, where possible, arrive at equitable settlements with infringers.

Non-Reimbursement Sensitive Market

The Company is also working to penetrate the segment of the national market that is not sensitive to direct reimbursement for the Company’s product. This includes capitated environments such as long-term acute care facilities, health maintenance organizations, home health agencies, as well as government agencies, (e.g. the Veterans Administration).

The Company is addressing various parts of this market via distributors, independent sales representatives, and internal sales representatives.

Sales and Marketing

Given the Company’s status with respect to marketing clearance for its AutoloGel™ System, Cytomedix continues to maintain a limited sales and marketing infrastructure for the AutoloGel™ Component Kit and Process Centrifuge. The Company predominately distributes its products through a network of commission-based internal and independent sales representatives. At December 31, 2006, the Company was represented by three internal and one independent sales representative, servicing approximately a dozen states. The Company expects to expand this representation in 2007.

Suppliers

The Company outsources manufacturing for all the components of the AutoloGelTM process. While the Company utilizes single suppliers for several components of AutoloGelTM, such components are readily available on the open market and therefore the Company believes that no dependencies exist from its current sourcing practices. The one exception is a reagent, bovine thrombin, available exclusively through King Pharmaceuticals.

Competition

Wound care products can be categorized into 3 general areas: passive, interactive, and active.

| · | Passive products -- such as gauze and bandages, cover the wound to protect it. |

| · | Interactive products -- attempt to optimize the wound environment so it is more conducive for the body to enact the innate healing process. The wound care world recognizes that moist wound healing is more effective for cellular growth than dry wound healing, however excessive moisture can be detrimental to healing. In addition, wounds need to be free of infection, have adequate perfusion and tissue oxygenation, and reduced pressure. There are hundreds of wound dressings on the market, some provide a long-term moist wound environment, others absorb large amounts of exudates, and some provide topical antimicrobial agents. In addition, there are multiple devices that attempt to assist with creating the optimal wound environment. However, as a whole, none of them are positioned to actively direct cellular growth. |

| · | Active wound products -- directly stimulate cellular growth and migration in the wound area. Growth factor products, such as AutoloGel™, are a predominant product in this category. Science has documented that multiple growth factors cause cellular growth and migration to actively grow granulation tissue, capillaries, and epithelium. Tissue engineered grafts could also fall into this category because they contain live cells and secondarily, may have some growth factors in the tissue. |

Thus, when identifying competitors, each product can be categorized in the above breakdown. Passive products are not a competitor for AutoloGel™. While some of the interactive products can be competitors, others can be complimentary to AutoloGel™. The other active products could be categorized as the major competitors.

6

The major competitors are other platelet gel companies, many of whom have licensing agreements with Cytomedix. To date, these companies are selling platelet gel mostly into the surgical market for dental, plastic, orthopedic, and general surgery purposes but may also try to sell into the wound care market. When compared to the other platelet gel companies, Cytomedix’s AutoloGel™ System has the smallest, most portable centrifuge with the fastest spin time (1.5 minutes compared to 13-20 minutes). This makes it possible to use in a greater variety of health care settings, i.e. hospital, outpatient clinics, physicians offices, or long term care, long term acute care, and home health settings. In addition, it is a user-friendly system so multiple health care providers can process the gel, rather than specialty technicians. Competitors’ systems generally require a larger blood draw, more detailed processing steps, and a longer spin time. While competitors claim a larger growth factor and platelet count than at baseline, no studies exist that prove this is efficacious. To date, Cytomedix’s AutoloGel™ System is the only platelet gel system that has completed a prospective, randomized, controlled trial in humans. The Company believes this trial demonstrated both the safety and efficacy of the AutoloGel™ System.

Regranex, a prescription cream marketed by Ethicon, a division of Johnson & Johnson, Inc. ("J&J"), contains a single recombinant growth factor. Having been introduced after lengthy clinical trials several years ago, its revenues, based on the Company’s best estimate, have grown significantly. Cytomedix perceives the single growth factor Regranex as a less effective method of healing chronic wounds in comparison with autologous multiple growth factors. While Cytomedix acknowledges the success of the Regranex product in the marketplace, an excellent opportunity exists to capture market share from this product once reimbursement is available for AutoloGel™. A recent CMS (Medicare) decision disallowed coverage for Regranex because it is self-administered.

The tissue-engineered products have changed extensively lately. Smith and Nephew, the manufacturer of Dermagraft, has taken the product off the market recently and has subsequently sold the technology to Advanced BioHealing. Ortec International, Inc.is continuing to conduct clinical trials on its product Orcel. Apligraf, manufactured by Organogenesis, is the only tissue engineered product on the market at this time.

The major competitor in the interactive area is a device called Vacuum Assisted Closure (“V.A.C.”) system produced by Kinetic Concepts, Inc. (“KCI”). During the year ended December 31, 2005, KCI worldwide revenues due to V.A.C. sales and rentals were reported as $908 million. Several of the sites that have used the V.A.C. system have now tried AutoloGel™. It has been reported to the Company by several of these sites that AutoloGel™ was very competitive with the V.A.C. and may even be better in both clinical and cost effectiveness. This, however, was based on individual case reports and experience of physicians rather than any rigorous comparative studies. Yet the V.A.C's established position is substantially CMS reimbursed, which provides for a substantial current economic competitive advantage.

Intellectual Property Rights

Cytomedix regards its patents, trademarks, trade secrets, and other intellectual property (collectively, the “Intellectual Property Assets”) as critical to its success. Cytomedix relies on a combination of patents, trademarks, and trade secret and copyright laws, as well as confidentiality procedures, contractual provisions, and other similar measures, to establish and protect its Intellectual Property Assets. Cytomedix has in the past several years filed numerous patent applications worldwide seeking protection of its technologies. Cytomedix owns eight U.S. patents (including U.S. Patent No. 5,165,938 (the “Knighton Patent”) and U.S. Patent No. 6,303,112 (the “Worden Patent”)), various corresponding foreign patents, and various trademarks. Cytomedix has received, filed, or is in the process of filing trademarks for the names “Cytomedix,” “AutoloGel”, and a few variants thereof. In addition, Cytomedix has numerous pending trademark applications and foreign patent applications involving enriched platelet wound healant, platelet derived wound healant, angiogenic peptides, and anti-inflammatory peptides.

To prevent disclosure of its trade secrets, Cytomedix restricts access to its proprietary information. All of its employees, consultants, and other persons with access to Cytomedix's proprietary information execute confidentiality agreements with Cytomedix. Cytomedix has also pursued litigation against those persons believed to be infringing on the Company's Intellectual Property Assets seeking both damages and injunctive relief.

Despite these efforts, Cytomedix may not be able to prevent misappropriation of its technology or deter others from developing similar technology in the future. Furthermore, policing the unauthorized use of its Intellectual Property Assets is difficult. Litigation necessary to enforce Cytomedix's Intellectual Property Assets could result in substantial costs and diversion of resources.

The Company is party to certain royalty agreements relating to its intellectual property under which it pays certain fees. See Note 5 to the Financial Statements.

7

Government Regulation

Devices that the Company manufactures and distributes are subject to regulations by the Food and Drug Administration, including record-keeping requirements, good manufacturing practices and mandatory reporting of certain adverse experiences resulting from use of the devices, and certain state agencies. Labeling and promotional activities are also subject to regulation by the FDA and the Federal Trade Commission, in certain circumstances. Current FDA enforcement policy prohibits the marketing of approved medical devices for unapproved uses and the agency scrutinizes the labeling and advertising of medical devices to ensure that unapproved uses are not promoted.

Before a new medical device can be introduced to the market, the manufacturer must generally obtain FDA clearance or approval. In the United States, medical devices are classified into one of three classes - Class I, II or III. The controls applied by the FDA to the different classifications are those believed by the FDA to be necessary to provide reasonable assurance that the device is safe and effective. Class I devices are non-critical products that FDA believes can be adequately regulated by “general controls” that include provisions relating to labeling, manufacturer registration, defect notification, records and reports, and good manufacturing practices (“GMP”) based on the FDA’s Quality Systems Regulations. Most Class I devices are exempt from pre-market notification and some are also exempt from GMP requirements. Class II devices are products for which the general controls of Class I devices, by themselves, are not sufficient to assure safety and effectiveness and, therefore, require special controls. Additional special controls for Class II devices include performance standards, post-market surveillance patient registries, and the use of FDA guidelines. Standards may include both design and performance requirements. Class III devices have the most restrictive controls and require pre-market approval by the FDA. Generally, Class III devices are limited to life-sustaining, life-supporting or implantable devices. The FDA inspects medical device manufacturers and has a broad authority to order recalls of medical devices, to seize non-complying medical devices, and to criminally prosecute violators.

Section 510(k) of the Federal Food, Drug and Cosmetic Act requires individuals or companies manufacturing most medical devices intended for human use to file a notice with the FDA at least ninety days before intending to introduce the device into the market. This notice, commonly referred to as a 510(k), must identify the type of classified device into which the product falls, the class of that type, and a specific product already being marketed or cleared by FDA and to which the product is “substantially equivalent.” In some instances, the 510(k) must include data from human clinical studies in order to establish “substantial equivalence.” The FDA must agree with the claim of “substantial equivalence” before the device can be marketed. The statutory time frame for clearance of a 510(k) is 90 days, though it often takes longer.

If a product is Class III and does not qualify for the 510(k) process, then the FDA must approve a pre-market approval (“PMA”) application before marketing can begin. PMA applications must demonstrate, among other factors, that the device in question is safe and effective. Obtaining a PMA application approval can sometimes take several years, depending upon the complexity of the issues involved with the device. The statutory time frame for the review of a PMA by the FDA is 180 days and many devices are reviewed and approved within that time frame or within a few months afterward. Marketing approval based on a PMA is generally a longer process than the 510(k) clearance process that is typically obtained in comparatively less time.

Government Approval

Cytomedix has sought to ensure compliance with the FDA regulations and policies for medical devices and, specifically, platelet gel therapies.

The Company currently markets the AutoloGel™ Process Centrifuge,the AutoloGel™ Component Kit, and certain commercially available reagents (i.e. calcium chloride, ascorbic acid, and bovine thrombin). Each component is a legally-marketed product that either has been cleared by FDA for marketing or is exempt from pre-market notification and clearance. The AutoloGel™ Centrifuge, when used with the AutoloGel™ Component Kit and certain reagents, form the basis for the AutoloGel process and are used for wound care and for treating chronic wound, including diabetic ulcers, at the physician’s discretion. The Federal Food, Drug and Cosmetic Act does not authorize the FDA to limit or interfere with the “physician's practice of medicine” and use of legally-marketed devices for any condition or disease within a legitimate doctor-patient relationship as long as no specific claims are made for the product.

In 2003, the Company conceptualized marketing an AutoloGel™ System, consisting of a centrifuge, a component kit, and reagents, for specific indications such as diabetic, pressure, and venous ulcers.

During 2003, the Company made a business decision to undertake a prospective, randomized, blinded, controlled trial for the AutoloGel™ System. The objective of the trial was to demonstrate safety and efficacy of the AutoloGel™ System for treating diabetic foot ulcers to the scientific and reimbursement community, as well as to the FDA in order to obtain the agency’s marketing clearance of the AutoloGel™ System. In making this decision, the Company subjected itself to increased FDA oversight and its regulations governing the investigational use of medical devices, codified at 21 C.F.R. Part 812. To this end, the Company submitted an “Investigational Device Exemption” (“IDE”) application to the FDA under these rules and obtained approval on March 5, 2004, thus allowing the Company to begin its clinical trial.

8

Once the study was completed and clinical results analyzed, the Company submitted a 510(k) requesting FDA’s clearance of the AutoloGel™ System in January 2006, as discussed above, under the caption Clinical Trial and FDA Clearance.

Fraud and Abuse Laws

The Company may also be indirectly subject to federal and state physician self referral laws. Federal physician self-referral legislation (commonly known as the “Stark Law”) prohibits, subject to certain exceptions, physician referrals of Medicare and Medicaid patients to an entity providing certain “designated health services” if the physician or an immediate family member has any financial relationship with the entity. A person who engages in a scheme to circumvent the Stark Law's referral prohibition may be fined up to $100,000 for each such arrangement or scheme. The penalties for violating the Stark Law also include civil monetary penalties of up to $15,000 per referral and possible exclusion from federal health care programs such as Medicare and Medicaid. The Stark Law also prohibits the entity receiving the referral from billing any good or service furnished pursuant to an unlawful referral, and any person collecting any amounts in connection with an unlawful referral is obligated to refund such amounts. Various states have corollary laws to the Stark Law, including laws that require physicians to disclose any financial interest they may have with a health care provider to their patients when referring patients to that provider. Both the scope and exception for such laws vary from state to state.

The Company may also be subject to federal and state anti-kickback laws. Section 1128B (b) of the Social Security Act, commonly referred to as the Anti-Kickback Law, prohibits persons from knowingly and willfully soliciting, receiving, offering or providing remuneration, directly or indirectly, to induce either the referral of an individual, or the furnishing, recommending, or arranging for a good or service, for which payment may be made under a federal health care program such as Medicare and Medicaid. The Anti-Kickback Law is broad, and it prohibits many arrangements and practices that are otherwise lawful in businesses outside of the health care industry. The U.S. Department of Health and Human Services (“DHHS”) has issued regulations, commonly known as safe harbors that set forth certain provisions which, if fully met, will assure health care providers and other parties that they will not be prosecuted under the federal Anti-Kickback Law. Although full compliance with these provisions ensures against prosecution under the Anti-Kickback Law, the failure of a transaction or arrangement to fit within a specific safe harbor does not necessarily mean that the transaction or arrangement is illegal or that prosecution under the federal Anti-Kickback Law will be pursued. The penalties for violating the Anti-Kickback Law include imprisonment for up to five years, fines of up to $250,000 per violation for individuals and up to $500,000 per violation for companies and possible exclusion from federal health care programs. Many states have adopted laws similar to the federal Anti-Kickback Law, and some of these state prohibitions apply to patients for health care services reimbursed by any source, not only federal health care programs such as Medicare and Medicaid.

In addition, there are two other health care fraud laws to which the Company may be subject, one which prohibits knowingly and willfully executing or attempting to execute a scheme or artifice to defraud any health care benefit program, including private payers (“fraud on a health benefit plan”) and one which prohibits knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false, fictitious or fraudulent statement or representation in connection with the delivery of or payment for health care benefits, items or services. These laws apply to any health benefit plan, not just Medicare and Medicaid.

The Company may also be subject to other laws which prohibit submitting claims for payment or causing such claims to be submitted that are false. Violation of these false claims statutes may lead to civil money penalties, criminal fines and imprisonment, and/or exclusion from participation in Medicare, Medicaid and other federally funded state health programs. These statutes include the federal False Claims Act, which prohibits the knowing filing of a false claim (or causing the submission of a false claim) or the knowing use of false statements to obtain payment from the U.S. federal government. When an entity is determined to have violated the False Claims Act, it must pay three times the actual damages sustained by the government, plus mandatory civil penalties of between $5,500 and $11,000 for each separate false claim. Suits filed under the False Claims Act can be brought by an individual on behalf of the government (a “qui tam action”). Such individuals (known as “qui tam relators”) may share in the amounts paid by the entity to the government in fines or settlement. In addition certain states have enacted laws modeled after the False Claims Act. “Qui tam” actions have increased significantly in recent years causing greater numbers of health care companies to have to defend false claim actions, pay fines or be excluded from the Medicare, Medicaid or other federal or state health care programs as a result of an investigation arising out of such action.

Several states also have referral, fee splitting and other similar laws that may restrict the payment or receipt of remuneration in connection with the purchase or rental of medical equipment and supplies. State laws vary in scope and have been infrequently interpreted by courts and regulatory agencies, but may apply to all health care products and services, regardless of whether Medicaid or Medicare funds are involved.

9

Research and Development

The Company is currently focusing its limited resources on broadly commercializing AutoloGelTM. It therefore expends only very minor amounts on research and development activities (“R&D”). The Company currently focuses its R&D activities on the improvement of its current product offering, but, in the future, intends to develop the technology underlying its broader patent portfolio.

Employees

At December 31, 2006, the Company had twelve full-time employees. These include three executive officers, Dr. Kshitij Mohan as Chief Executive Officer, Mr. Andrew S. Maslan as Chief Financial Officer and Ms. Carelyn P. Fylling as Vice President of Professional Services. The remaining personnel consist of sales and marketing, clinical, accounting, and regulatory professionals.

AVAILABLE INFORMATION

Cytomedix files periodic reports and all amendments thereto pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934. These reports are available, free of charge, through the Company’s website at www.cytomedix.com.

ITEM 1A. RISK FACTORS

Cytomedix cautions the readers not to place undue reliance on any forward-looking statements, which are based on certain assumptions and expectations that may or may not be valid or actually occur. The risk factors that follow may cause actual results to differ materially from those expressed or implied by any forward-looking statement. The risks described below are not to be deemed an exhaustive list of all potential risks.

The FDA Denied the Company’s Claims in its 510(k) Pre-Market Notification and the Company’s Appeal May Not Be Successful

The FDA denied the Company’s claims in its 510(k). The Company has appealed this decision and currently awaits a final ruling from the FDA. There is no assurance that the Company’s efforts to have the original decision reversed or amended to the Company’s satisfaction will be successful. A lack of FDA clearance may make it more difficult to obtain reimbursement codes and/or adversely affect the Company’s ability to implement a significant portion of its business plan. Specifically, the Company may be unable to obtain a significant share of the chronic wound care market. Even with FDA clearance, the Company can provide no assurance that it will be able to obtain Medicare or other third party reimbursement.

The Company Has Limited Sources of Working Capital

Because the Company was in bankruptcy in 2002, the Company will not be able to obtain debt financing. All working capital required to implement the Company’s business plan will be provided by funds obtained through offerings of its equity securities, and revenues generated by the Company. No assurance can be given that the Company will have revenues sufficient to support and sustain its operations through 2007.

If the Company does not have sufficient working capital and is unable to generate revenues or raise additional funds, the following may occur: delaying the completion of the Company’s current business plan or significantly reducing the scope of the business plan; delaying some of its development and clinical or marketing testing; delaying its plans to pursue government regulatory and reimbursement approval and/or clearance for its wound treatment technologies; postponing the hiring of new personnel; or, in an extreme situation, ceasing operations.

The Company Has a History of Losses

The Company has a history of losses, is not currently profitable, and expects to incur substantial losses and negative operating cash flows for the foreseeable future. The Company may never achieve or maintain profitability. The Company will need to generate significant revenues to achieve and maintain profitability. The Company cannot guarantee that it will be able to generate these revenues, and it may never achieve profitability.

10

The Company Has a Short Operating History and Limited Operating Experience

The Company must be evaluated in light of the uncertainties and complexities affecting an early stage biotechnology company. The Company has only recently begun to implement its current business plan. Thus, the Company has a very limited operating history. Continued operating losses, together with the risks associated with the Company’s ability to gain new customers for its product offerings may have a material adverse effect on the Company’s liquidity. The Company may also be forced to respond to unforeseen difficulties, such as decreasing demand for its products and services, regulatory requirements and unanticipated market pressures.

Since emerging from bankruptcy and continuing through today, the Company is developing a business model that includes protecting its patent position, addressing its third-party reimbursement issues, and developing a sales and marketing program. There can be no assurance that its business model in its current form can accomplish the Company’s stated goals.

The Company’s Intellectual Property Assets Are Critical to Its Success

The Company regards its patents, trademarks, trade secrets, and other intellectual property assets as critical to its success. The Company relies on a combination of patents, trademarks, and trade secret and copyright laws, as well as confidentiality procedures, contractual provisions, and other similar measures, to establish and protect its intellectual property. The Company attempts to prevent disclosure of its trade secrets by restricting access to sensitive information and requiring employees, consultants, and other persons with access to the Company’s sensitive information to sign confidentiality agreements. Despite these efforts, the Company may not be able to prevent misappropriation of its technology or deter others from developing similar technology in the future. Furthermore, policing the unauthorized use of its intellectual property assets is difficult and expensive. Litigation has been necessary in the past and may likely be necessary in the future in order to protect the Company’s intellectual property assets. Litigation could result in substantial costs and diversion of resources. The Company cannot guarantee that it will be successful in any litigation matter relating to its intellectual property assets. Continuing litigation or other challenges could result in one or more of its patents being declared invalid. In such a case, any royalty revenues from the affected patents would be adversely affected although the Company may still be able to continue to develop and market its products.

The Company’s patent covering the specific gel formulation that is applied as part of the AutoloGel™ System (the “Worden Patent”) expires no earlier than February 2019. The Company’s U.S. Knighton Patent (which is the subject of license agreements between the Company and Medtronic, Inc., DePuy Spine, Inc., Biomet Biologics, Inc., COBE Cardiovascular, Inc., and Harvest Technologies Corporation, among others) expires in November 2009. The Company is pursuing a strategy to obtain FDA clearance and CMS reimbursement, but there can be no assurance that the Company will be able to establish such a significantly increased share of the wound care market prior to the expiration of the U.S. Knighton Patent in 2009, after which the Company may be more vulnerable to competitive factors because third parties will not then need a license from the Company to perform the methods claimed in the Knighton Patent.

The AutoloGel™ Components are Subject to Governmental Regulation

The Company’s success is also impacted by factors outside of the Company’s control. The Company’s current therapies may be subject to extensive regulation by numerous governmental authorities in the United States, both federal and state, and in foreign countries by various regulatory agencies.

Specifically, the Company’s devices are subject to regulation by the FDA and state regulatory agencies. The FDA regulates drugs, medical devices and biologics that move in interstate commerce and requires that such products receive pre-marketing approval based on evidence of safety and efficacy. The regulations of government health ministries in foreign countries are analogous to those of the FDA in both application and scope. In addition, any change in current regulatory interpretations by, or positions of, state regulatory officials where the AutoloGel™ process is practiced could materially and adversely affect the Company’s ability to sell products in those states.

The FDA could require the Company to stop selling the components used to prepare AutoloGel™ until it obtains clearance or approval of a specific wound healing claim. While the Company believes that all of said components are legally marketed, the FDA could take the position that the Company cannot market the AutoloGel™ Component Kit or Process Centrifuge for wound healing until the Company has a specific approval or clearance to do so from the FDA.

Further, as the Company expands and offers additional products in the United States and in foreign countries, approval from the FDA and comparable foreign regulatory authorities prior to introduction of any such products into the market may be required. The Company has no assurance that it will be able to obtain all necessary approvals from the FDA or comparable regulatory authorities in foreign countries for these products. Failure to obtain the required approvals would have a material adverse impact on the Company’s business and financial condition.

11

Compliance with FDA and other governmental requirements imposes significant costs and expenses. Further, the Company’s failure to comply with these requirements could result in sanctions, limitations on promotional or other business activities, or other adverse effects on the Company’s business. Further, recent efforts to control healthcare costs could negatively effect demand for the Company’s products and services.

The Company Could Be Adversely Affected if Customers Cannot Obtain Reimbursement

The AutoloGel™ Component Kit and Process Centrifuge are marketed to healthcare providers. Some of these providers, in turn, seek reimbursement from third-party payers such as Medicare, Medicaid, and other private insurers. Many foreign countries also have comprehensive government managed healthcare programs that provide reimbursement for healthcare products. Under such healthcare systems, reimbursement is often a determining factor in predicting a product’s success, with some physicians and patients strongly favoring only those products for which they will be reimbursed.

In order to achieve a viable reimbursement pathway for the AutoloGel™ process components, the Company has conducted a prospective, randomized, blinded, controlled, multi-site clinical trial as approved by the FDA to provide the necessary data as required by CMS, formerly known as the Healthcare Financing Agency. In addition, the 2003 CMS non-coverage decision for “Autologous Blood-Derived Products for the Treatment of Chronic Wounds”, which builds on the 1992 HCFA ruling may have to be dismissed or a carve-out would need to be created in order to make national coverage by Medicare possible. The Company cannot assure that its efforts in this area will be successful and therefore, a significant obstacle to broad third-party reimbursement may remain. Further, even if the Non-Coverage Decision is reversed, the Company cannot guarantee that third-party payers will elect to reimburse treatments using the Company’s products or processes or, if such reimbursement is approved, that the level of reimbursement granted will be sufficient to cover the cost of the product or process to the physician or to the patient.

Healthcare providers’ inability to obtain third-party reimbursement for the treatment could have an adverse effect on the Company’s success.

Royalty Revenues Are Unpredictable

While the Company currently has several primary licensing agreements that are expected to generate on-going royalty revenues, the Company cannot currently reasonably predict the magnitude of those revenues. Because Cytomedix’s licensing activities are recent, it is premature to predict the resulting royalty streams from these licensing agreements. Furthermore, royalty streams from these agreements are entirely dependent on the sales of its licensees and are therefore outside the control of Cytomedix. Past levels of royalty revenues from these agreements are not necessarily an indication of future activity.

The Success of the AutoloGel™ System Is Dependent on Acceptance by the Medical Community

The commercial success of the Company’s products and processes will depend upon the medical community and patients accepting the therapies as safe and effective. If the medical community and patients do not ultimately accept the therapies as safe and effective, the Company’s ability to sell the products and processes will be materially and adversely affected. While acceptance by the medical community may be fostered by broad evaluation via peer-reviewed literature, the Company may not have the resources to facilitate sufficient publication.

The Company May Be Unable to Attract and Retain Key Personnel

The future success of the Company depends on the ability to attract, retain and motivate highly skilled management, including sales representatives. The Company has retained a team of highly qualified officers and consultants, but the Company cannot provide assurance that it will be able to successfully integrate these officers and consultants into its operations, retain all of them, or be successful in recruiting additional personnel as needed. The Company’s inability to do so will materially and adversely affect the business prospects, operating results and financial condition.

The Company’s ability to maintain and provide additional services to its existing customers depends upon its ability to hire and retain business development and scientific and technical personnel with the skills necessary to keep pace with continuing changes in cellular therapy technologies. Competition for such personnel is intense; the Company competes with pharmaceutical, biotechnology and healthcare companies. The Company’s inability to hire additional qualified personnel may lead to higher recruiting, relocation and compensation costs for such personnel. These increased costs may reduce the Company’s profit margins or make hiring new personnel impractical.

12

Legislative and Administrative Action May Have an Adverse Effect on the Company

Political, economic and regulatory influences are subjecting the health care industry in the United States to fundamental change. The Company cannot predict what other legislation relating to its business or to the health care industry may be enacted, including legislation relating to third-party reimbursement, or what effect such legislation may have on the Company’s business, prospects, operating results and financial condition. The Company expects federal and state legislators to continue to review and assess alternative health care delivery and payment systems and possibly adopt legislation affecting fundamental changes in the health care delivery system. Such laws may contain provisions that may change the operating environment for its targeted customers including hospitals and managed care organizations.

Health care industry participants may react to such legislation by curtailing or deferring expenditures and initiatives, including those relating to the Company’s products. Future legislation could result in modifications to the existing public and private health care insurance systems that would have a material adverse effect on the reimbursement policies discussed above.

The Company Could Be Affected by Malpractice Claims

Providing medical care entails an inherent risk of professional malpractice and other claims. The Company does not control or direct the practice of medicine by physicians or health care providers who use the products and does not assume responsibility for compliance with regulatory and other requirements directly applicable to physicians. The Company cannot guarantee that claims, suits or complaints relating to the use of the AutoloGel™ components and treatment administered by physicians will not be asserted against the Company in the future.

The production, marketing and sale, and use of the AutoloGel™ Component Kit and Process Centrifuge entail risks that product liability claims will be asserted against the Company. These risks cannot be eliminated, and the Company could be held liable for any damages that result from adverse reactions or infectious disease transmission. Such liability could materially and adversely affect the Company’s business, prospects, operating results and financial condition.

The Company currently maintains professional and product liability insurance coverage, but the Company cannot give assurance that the coverage limits of this insurance would be adequate to protect against all potential claims. The Company cannot guarantee that it will be able to obtain or maintain professional and product liability insurance in the future on acceptable terms or with adequate coverage against potential liabilities.

AutoloGel™ Has Existing Competition in the Marketplace

In the market for biotechnology products, the Company faces competition from pharmaceutical companies, biopharmaceutical companies and other competitors. Other companies have developed or are developing products that may be in direct competition with the AutoloGel™ process. Biotechnology development projects are characterized by intense competition. Thus, the Company cannot assure any investor that it will be the first to the market with any newly developed products or that it will successfully be able to market these products. If the Company is not able to participate and compete in the cellular therapy market, the Company’s financial condition will be materially and adversely affected. The Company cannot guarantee that it will be able to compete effectively against such companies in the future. Many of these companies have substantially greater capital resources, larger marketing staffs and more experience in commercializing products. Recently developed technologies, or technologies that may be developed in the future, may be the basis for developments that will compete with the Company’s products.

Risks Related to the Company’s Common Stock

The average daily trading volume in Cytomedix Common stock is relatively low. As long as this condition continues, it could be difficult or impossible to sell a significant number of shares of Common stock at any particular time at the market prices prevailing immediately before such shares are offered. In addition, sales of substantial amounts of Common stock could lower the prevailing market price of the Company’s Common stock. This would limit or perhaps prevent the Company’s ability to raise capital through the sale of securities. Additionally, the Company has significant numbers of outstanding warrants and options that, if exercised and sold, could put additional downward pressure on the Common stock price.

The Company is Subject to Anti-Takeover Provisions and Laws.

Provisions in Cytomedix’s Restated Certificate of Incorporation and Restated Bylaws and applicable provisions of the Delaware General Corporation Law may make it more difficult for a third party to acquire control of the Company without the approval of the board of directors. These provisions may make it more difficult or expensive for a third party to acquire a majority of the Company’s outstanding voting Common stock or delay, prevent or deter a merger, acquisition, tender offer or proxy contest, which may negatively affect the Common stock price.

13

Purchases of the Company’s Common Stock Are Subject to the SEC's Penny Stock Rules.

Generally, any non-NASDAQ equity security that has a market price of less than $5.00 per share is defined as a Penny Stock. Penny Stocks are subject to special rules and regulations under the Securities Exchange Act of 1934. These rules require additional disclosure by broker-dealers in connection with any trades involving Penny Stock. Cytomedix Common stock is currently defined as a Penny Stock, and the Company is uncertain if the market price of its common stock will ever be above $5.00 per share. As a result of its characterization as a Penny Stock, the market liquidity for the Company’s Common stock may be adversely affected by the Penny Stock rules and regulations. This could restrict an investor's ability to sell the common stock in a secondary market. The rules governing Penny Stock require the delivery, prior to any Penny Stock transaction, of a disclosure schedule explaining the Penny Stock market and the risks associated therewith, and impose various sales practice requirements on broker-dealers who sell Penny Stocks to persons other than established customers and accredited investors (generally defined as an investor with a net worth in excess of $1,000,000 or annual income exceeding $200,000, $300,000 together with a spouse). For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and have received the purchaser's written consent to the transaction prior to sale. The broker-dealer also must disclose the commissions payable to the broker-dealer, current bid and offer quotations for the Penny Stock and, if the broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer's presumed control over the market. Such information must be provided to the customer orally or in writing prior to effecting the transaction and in writing before or with the customer confirmation. Monthly statements must be sent disclosing recent price information for the Penny Stock held in the account and information on the limited market in Penny Stock. The additional burdens imposed on broker-dealers may discourage them from effecting transactions in the Company’s Common stock, which could severely limit the liquidity of the Common stock and the ability of shareholders to sell the Common stock in the secondary market.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The Company does not own any real property and does not intend to invest in any real property.

The Company’s principal executive offices are located in Rockville, Maryland. Cytomedix occupies facilities consisting of 3,100 square feet under an operating lease expiring July 31, 2008, subject to an early termination option available to Cytomedix. See Note 16 to the Financial Statements.

ITEM 3. LEGAL PROCEEDINGS

At present, the Company is not engaged in or the subject of any legal proceedings.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

The Company held its annual meeting of shareholders on November 3, 2006, at the Company’s offices in Rockville, Maryland. At the meeting, the shareholders re-elected James S. Benson, David P. Crews, Arun K. Deva, David F. Drohan, Mark T. McLoughlin, and Kshitij Mohan as Directors to hold office until the next annual meeting of shareholders and until their successors are duly elected. A summary of votes cast follows below:

14

NOMINEE | VOTES FOR | VOTES WITHHELD | ABSTENTIONS* | |||||||

| James S. Benson | 21,816,240 | 196,940 | — | |||||||

| David P. Crews | 21,815,308 | 197,872 | — | |||||||

| Arun K. Deva | 21,810,640 | 202,540 | — | |||||||

| David F. Drohan | 21,815,308 | 197,872 | — | |||||||

| Mark T. McLoughlin | 21,816,240 | 196,940 | — | |||||||

| Dr. Kshitj Mohan | 21,794,443 | 218,737 | — |

* Pursuant to the terms of the Proxy Statement, proxies received were voted, unless authority was withheld, in favor of the election of the six nominees.

Shareholders also voted to ratify the appointment of L J Soldinger Associates, LLC as the Company’s independent registered accountant for the fiscal year ending December 31, 2006 with 21,969,431 votes for, 24,235 votes against, and 19,514 abstentions.

Shareholders also voted to ratify an amendment to the Long-Term Incentive Plan making Awards available representing up to 5,000,000 shares of Common stock with 6,056,251 votes for, 2,401,658 votes against, and 86,838 abstentions.

Further information regarding the meeting and the proposals submitted to a vote of the shareholders may be found in the Company’s definitive proxy statement filed with the Securities and Exchange Commission on September 22, 2006.

15

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITES

Since June 2005, the Company’s Common stock has been listed on the American Stock Exchange under the symbol GTF. Prior to this listing the Company’s Common stock was traded in the Over-the-Counter (“OTC”) market and quoted on the OTC bulletin board under the symbol CYME. Set forth below are the high and low closing sale prices for the Common stock for each quarter since the quarter beginning January 1, 2004, as reported by NASDAQ and AMEX as appropriate. The prices prior to June 30, 2005 are over-the-counter market quotations and reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.

Quarter ended | High | Low | |||||

| December 31, 2006 | $ | 2.76 | $ | 0.91 | |||

| September 30, 2006 | $ | 3.34 | $ | 2.60 | |||

| June 30, 2006 | $ | 3.20 | $ | 2.25 | |||

| March 31, 2006 | $ | 2.90 | $ | 2.23 | |||

| December 31, 2005 | $ | 3.36 | $ | 2.01 | |||

| September 30, 2005 | $ | 6.85 | $ | 1.68 | |||

| June 30, 2005 | $ | 5.07 | $ | 3.12 | |||

| March 31, 2005 | $ | 3.50 | $ | 2.35 | |||

There were approximately 658 shareholders of record of Common stock as of February 15, 2007.

Cytomedix did not pay dividends to holders of Common stock in 2006 or 2005. The Company is prohibited from declaring dividends on Common stock if any dividends are due on shares of Series A, B, or C Convertible Preferred stock. If there are no unpaid dividends on shares of Series A, B, or C Convertible Preferred stock, any decision to pay cash dividends on Common stock will depend on the Company’s ability to generate earnings, need for capital, and overall financial condition, and other factors the Board deems relevant. Cytomedix does not anticipate paying cash dividends on Common stock in the foreseeable future, but instead will retain any earnings for reinvestment in the business.

RECENT SALES OF UNREGISTERED SECURITIES

The Company issued 1,062,500 shares of Common stock during the fourth quarter of 2006. The following table lists the sources of and the proceeds from those issuances:

Source | # of Shares | Total Exercise Price | ||||||

| Exercise of unit offering warrants | 287,500 | $ | 431,250 | |||||

| Exercise of other warrants (1) | 775,000 | $ | 775,000 | |||||

| Totals | 1,062,500 | $ | 1,206,250 | |||||

| (1) | These warrants reflect consultant warrants held by one party. Upon exercise, the Company accepted $75,000 in cash and a Negotiable Term Promissory Note and related Security Agreement (the “Note”). The Note, which was amended in February 2007, provides for the remaining exercise proceeds to be delivered to the Company in installment payments ending on April 30, 2007. The Note bears interest on the outstanding balance at 6% per year. As of February 15, 2007, the maker of the Note was current in making all required principal and interest payments and the principal balance remaining was $426,250. |

The Company has used the cash proceeds from these issuances for general corporate purposes. All shares were issued in private offerings exempt from registration pursuant to Section 4(2) of the Securities Act.

See Note 11 to the Financial Statements for further information on the Company’s capital structure.

16

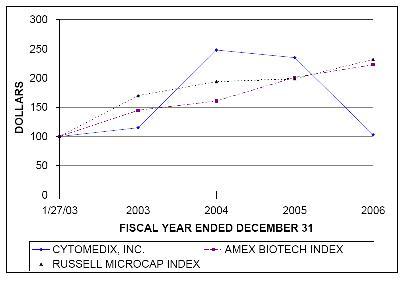

PERFORMANCE GRAPH